private equity – top tax issues for fundraising and deal ... equity – top tax issues for...

TRANSCRIPT

Private Equity – top tax issues for fundraising and deal structuring in Asian markets2016 KPMG Asia Pacific Tax Summit

JW Marriott Hotel, China Central Place, Beijing9-12 May 2016

KPMG Asia Pacific Tax Centre

2©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

AgendaFund raising developments and trends in Asia

• recent PE fund raising activity• PE fund structures in Asia• incentives and concessions• LP demands and corporate governance• tax authority challenges and contentious issues

Investment structuring issues of Asian PE funds• investment structures into key markets• China specific structuring developments• indirect disposal developments• best practice on substance• changing tax authority developments• use of SPVs in low tax countries• consolidating investment platforms

Fundraising trends in AsiaDarren BowdernKPMG in Hong Kong

John GuKPMG in China

Chee Wee TanKPMG in Singapore

Malcolm PrebbleKPMG in Hong Kong

Ryan DavisKPMG in the US

4©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Fundraising – Asian PE market• Significant build up of capital for pooled investments over

the last few years• Increase allocation by institutional investors in PE• The rise of large successful Asian funds• Baring Private Equity, Hony, PAG, CDH, Gaw…• Also, the rise of Chinese domestics funds• Asian funds focusing on opportunities in Asia and global• Buoyant and competitive market, with a debt fuelled M&A

binge over the last few years• Impact of the slowdown in China, credit constraints, rising

interest rates, devaluation in local emerging currencies• Valuations creating more buying opportunities• Governments in Asia promoting asset management –

Hong Kong and Singapore, others?

5©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Fundraising trends – Asia Pacific snapshot

• Significant fund raising activity in Asia

• Asia fundraising for 2014/15 $85.7 billion

• KKR - $6bn,Affinity Asia - $3.8bn,CVC Capital Partners - $3.5bn,Baring Private Equity $4bn, PAG II $3.6bn, RRJ $3bn, ACA $3bn

Source: AVCJ Private Equity

0

100

200

300

400

500

600

700

0100002000030000400005000060000700008000090000

100000

2011 2012 2013 2014 2015

No

of fu

nds

US

$ m

illion

Fundraising in Asia Pacific

Amount (US$m) No of funds

6©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Fundraising – in China• Focus on domestic fund raising

• RMB fundraising is increasing post a 2013 dip; noticeably, the number of funds is relatively constant which means that fewer funds are raising more $

Source: AVCJ Private Equity

0

100

200

300

400

0

10000

20000

30000

40000

50000

60000

70000

2011 2012 2013 2014 2015

Fund

s

US

$milli

on

Fundraising in China

Amount (US$m) No of funds

0%

20%

40%

60%

80%

100%

2011 2012 2013 2014 2015Fund

rais

ing

volu

me

China compared to broader Asia

RMB USD Other Asia

0%10%20%30%40%50%60%70%80%90%

100%

2011 2012 2013 2014 2015

No

of fu

nds

RMB USD Other Asia

7©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Fundraising – in Singapore• At end 2014, total assets managed by

Singapore based asset managers grew by 30% to approx. US$1.78 trillion (of which US$70.3 billion are managed by VC and PE firms), compared to US$1.43 trillion as at end 2013.

• More than 80% of total AUM was sourced from outside Singapore, demonstrating Singapore’s primary role in serving regional and international investors

• The Asia Pacific region continued to be the key investment destination for Singapore-based asset managers, and accounted for 68% of total AUM in 2014, which is on par with 2013. This reflects strong investor interest in the region.

Equity50%

Bonds21%

Alternatives15%

CIS10%

Cash / Money Mkts4%

Investment of funds: By asset class

Asia Pacific68%

Europe13%

North America

11%

Others8%

Investors: By region

Source: AVCJ Private Equity

8©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

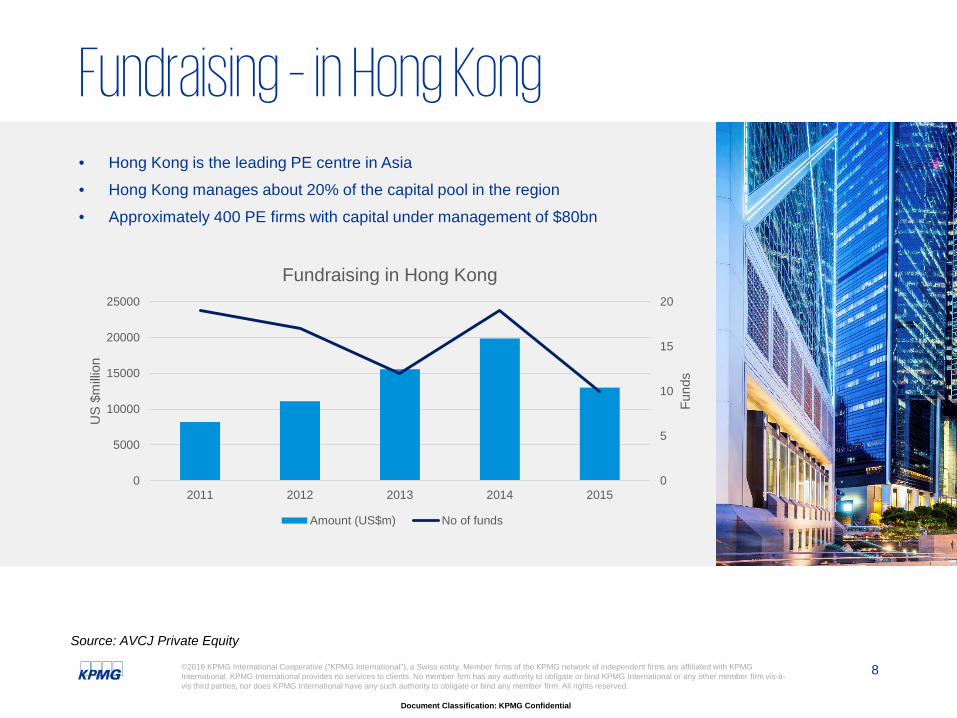

Fundraising – in Hong Kong• Hong Kong is the leading PE centre in Asia

• Hong Kong manages about 20% of the capital pool in the region

• Approximately 400 PE firms with capital under management of $80bn

Source: AVCJ Private Equity

0

5

10

15

20

0

5000

10000

15000

20000

25000

2011 2012 2013 2014 2015

Fund

s

US

$milli

on

Fundraising in Hong Kong

Amount (US$m) No of funds

Singapore and Hong Kong based fund structures

10©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Private Equity Funds Exemption Hong Kong Hong Kong as a PE Hub• Onshore / Offshore structures

• Cayman Funds dominate

• Hong Kong is an established asset management centre and generally the preferred location for Private Equity funds setting up operations in Asia

• Specific tax exemption for PE funds

• But, onerous operating protocols for PE funds in Hong Kong in order for the PE funds to be exempt if exemption doesn’t apply

• Aggressive IRD activities on taxation of management fees and carry

• New domestic fund regime

Fund Manager Parent

(Cayman Islands)

Fund Manager(Cayman Islands)

General Partner(Cayman Islands)

Grandpix subsidiariesGrandpix

subsidiariesOffshore SPVs

Fund (Cayman Islands)

Grandpix subsidiariesGrandpix

subsidiariesInvestment SPVs

(Hong Kong)

Investment Advisor

(Hong Kong)

Investment Committee

LPs

OffshoreHong Kong

Management fee

Advisory fee

Investment Professionals

Offshore target

Carry Vehicle

Source: KPMG International, 2016

11©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Private Equity Funds Exemption Hong Kong PE funds exemption

• Exemption for offshore PE funds apply to non-resident funds

• Apply to non-resident funds (consultation also on a new Hong Kong domiciled regime)

• Exemption of Hong Kong SPVs that are intermediate holding companies

• Funds may need to be regulated by the SFC to qualify as exempt

Key Benefits

• Relaxation of the operating protocols for PE funds in Hong Kong

• Substance considerations

• Board meetings in Hong Kong

• Investment decisions in Hong Kong

Key Tax Considerations

• Transfer pricing considerations

• Investments in Real Estate / Hong Kong investments

• Regulation of the manager in Hong Kong

• Permanent establishment risks

Fund Manager Parent

(Cayman Islands)

General Partner(Cayman Islands)

Grandpix subsidiariesGrandpix

subsidiariesOffshore SPVs

Fund (Cayman Islands)

Grandpix subsidiariesGrandpix

subsidiariesInvestment SPVs

(Hong Kong)

LPs

OffshoreHong Kong

Management fee

Offshore target

Exempt

Exempt

Carry Vehicle

Source: KPMG International, 2016

12©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Funds Exemption Singapore

Singapore – a favourable jurisdiction for Funds and Fund Management• Good geographical location – next door to some of

Asia’s highest potential markets (i.e. ASEAN)• Developed infrastructure facilitates relocation of

employees• Extensive tax treaty network – over 80

comprehensive tax treaties, and counting• Generally not regarded as a tax haven jurisdiction• Favourable tax incentives for Funds and Fund

Managers• Substance-based incentives given increasing need

to prove substance at the Fund level• Progressive and forward looking tax authorities

13©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Funds Exemption Singapore Broad-based Fund Tax Exemption Schemes• Caters for a wide range of fund types, including private equity funds• Fund Tax exemption schemes:

- Qualifying Offshore Funds- Qualifying Resident Funds- Enhanced-Tier Funds

Key Benefits• Income tax exemption on specified income derived from designated

investments• Specified income covers all income and gains in respect of designated

investments, unless they fall within an exclusion list• Designated investments include most types of investments like stocks,

shares, securities, derivatives etc. Immovable property in Singapore is excluded.

Key Conditions• Minimum annual expenditure (for Enhanced-Tier and Resident Funds)• Minimum funding size (for Enhanced-Tier Funds)• Restriction on shareholdings by Singapore investors (for Offshore and

Resident Funds)• Requirement to be managed by a Singapore fund management

company which holds the relevant regulatory licence or is exempted from holding such licence

14©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Offshore fund exemption scheme –Singapore vs Hong Kong

Issue

Singapore

Hong KongOffshore

fund exemptionEnhanced-Tierfund exemption

Fund vehicle • Individuals, companies and trusts (partnerships will be looked through)

• Companies, trusts and limited partnership

• Individuals, corporations, partnerships, trustees of trust• SPVs

Exempted income

• “Specified income” from “designated investments”• Exclude investments in Singapore immovable properties or unlisted

companies holding /trading of Singapore immovable properties (other than a property developer)

• Profits derived from “specified transactions” or transactions incidental (not exceeding 5% of total trading receipts) to the carrying out of the specified transactions;

• Specified transactions now include investments in private companies outside Hong Kong which do not hold Hong Kong properties or carry out business in Hong Kong)

Necessity for local fund manager/financial institution

• Managed by a Singapore resident fund manager • Specified transactions carried out through or arranged by a “specified person” covering corporations licensed or authorised financial institution registered under the SFO

• Qualifying funds

Residency of investors

• Less than 100% held by resident/PE in Singapore;

• Not more than 30% (50% if more than 10 investors) of the value of the fund held by a Singapore corporate investor alone or jointly with his associates

• No restriction on Singapore investors • Not more than 30% of the tax-exempt offshore fund held

by a resident person alone or jointly with his associates (or any percentage if the offshore fund is the resident person’s associate)

Others

• No approval from the Monetary Authority of Singapore required

• Subject to approval by the Monetary Authority of Singapore

• Subject to economic and professional conditions

• Hong Kong incorporated SPVs owned by exempt funds

15©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Singapore Platform for international funds investing in IndiaStructure

• CayCo acts as an aggregation vehicle to pool capital contributed by the Funds.

• The Indian Target shares are acquired through a chain of Singapore entities that are disregarded for US federal tax purposes.

• The Singapore entities must satisfy certain conditions to qualify for one of the Fund tax exemption Scheme.

Key Tax Considerations

Singapore

• Approved fund vehicles (subject to meeting the conditions) may enjoy tax exemption for specified income from designated investments

• Broadly, the conditions include minimum annual expenditure, minimum funding size, restriction on shareholdings by Singapore investors, and requirement to be managed by a Singapore fund management company. The Singapore fund manager must hold a capital markets services licence for the regulated activity of fund management or is exempted from holding such licence.

• Gains on exit from investment in Indian Target should qualify as specified income from designated investments and enjoy tax exemption under the Fund Tax Exemption Scheme

Funds

Indian Target

SingInv.Co

Singapore Manager Management

Agreement

Corporation for U.S. tax purposes

Partnership for U.S. tax purposes

Disregarded entity forU.S. tax purposes

CayCo

Sing Manager

Source: KPMG International, 2016

Sing Hold Co

16©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Singapore Platform for international funds investing in India (cont)Key Tax Considerations (cont)

India

• Capital gains on exit should generally not be taxable in India, to the extent that the Singapore-India tax treaty applies (but, consider indirect transfer tax)

U.S.

• Dry income considerations (e.g., CFC vs. PFIC)

- Indian Target: consider the activities performed by the Target.

• UBTI potentially arising from third-party acquisition indebtedness

• Capitalization (debt vs. equity)

• Exit (full vs. partial)

Sing Hold Co

Funds

Indian Target

SingInv.Co

Management Agreement

Corporation for U.S. tax purposes

Partnership for U.S. tax purposes

Disregarded entity forU.S. tax purposes

CayCo

Sing Manager

Source: KPMG International, 2016

Investment trendsDarren BowdernKPMG in Hong Kong

John GuKPMG in ChinaBrendon LamersKPMG in AustraliaUmang DaiyaKPMG in SingaporeRobin Walduck KPMG in the UKRyan DavisKPMG in the US

Australia

Brendon Lamers

19©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Australia – landscape changes

• High profile liquidation of a PE IPO – Dick Smith

• Australian government BEPS response

• Withholding tax imposed on sale of direct and indirect real property transactions

• Government announcements (3 May 2016 Government Budget)

‒ New CIV regime

‒ Diverted profits tax

‒ Company tax cuts

• New foreign investment review board protocols

• Official Cash Rate at record lows (1.75%)

20©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Australian Government response to BEPS Final Report

Australia

Support with domestic change

(2) Hybrids: Implementation report

(13) CbC: Legislation in Parliament

(8-10) Transfer pricing: Used for guidance

Support with international process

(6) Treaties: Support both LOB & PPT

(14) Dispute: Support binding arbitration

Considering

(12) Disclosure: Cost-benefit analysis

Govt. says already meet standard

(3) CFCs: Rules stricter than OECD

(5) Harmful practices: Already exchange

Treasurer press release “ducks issue”

(4) Interest: Current law meet proposals?

(7) PE: Proposal already followed?

21©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

FIRB – tax conditions • The Australian Treasury has announced new draft guidelines for foreign

investment applications considered by the Foreign Investment Review Board (FIRB).

• Future foreign investment approvals will require that applicants comply with a number of tax conditions, including that applicants and their associates in respect of an investment comply with Australian tax laws.

• Traditionally, FIRB applications have said very little about tax. The new conditions mean that foreign investors into Australia will need to consider carefully, with tax and legal advisors, what tax disclosures are made to FIRB. This change is very signifcant and adds to process and implementation risks.

• It will also be necessary to engage fully with the Australian Tax Office throughout the FIRB application process, particularly in relation to large transactions.

• The tax conditions imposed may be ongoing obligations, such as the requirement to provide annual reporting of compliance with tax conditions.

22©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

PE investors

Australia – Exit considerations

TPG Myer and ATO's reactionTPG’s divestment of Myer group• IPO to retail and institutional investors on the ASX

• ATO viewed the interposition of treaty resident holding companies as a scheme to avoid tax

ATO’s reaction• To counteract perceived abuse in this structure, the ATO

issued a number of tax determinations (TDs) discussed further below.

• The ATO’s view is that gains realised on the disposal of Australian portfolio companies by foreign private equity funds are generally both income in nature and Australian sourced and are therefore subject to Australian tax.

• The relevant DTA should allocate taxing rights to the off shore treaty entity, subject to the application of Australia’s GAAR.

• ATO now has a dedicated team actively pursuing foreign private equity exits. ATO tracks approvals given by foreign investment review board (FIRB) and media

ATO’s reaction• Ongoing activity evidenced in the Resource Capital Fund

cases. ATO using valuation arguments to asset taxing rights via the real property rules/DTA provisions

Sale

LuxCo

DutchCo

Cayman Islands

LP

Australian HoldCo Australian HoldCo

Source: KPMG International, 2016

Germany

Holger Lampe

24©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Germany – typical investment structure (1/2)Key Tax Benefits• Debt push down through tax group to

offset interest expenses with operating profits

• Tax efficient cash repatriation through shareholder loans

• Potentially, 0% withholding tax on dividends to EU HoldCo

• Exit gain not subject to German tax

Key Tax Considerations

• Jurisdiction of EU HoldCo

• Substance of EU HoldCo

• Legal form of BidCo (GmbH vs. KG)

• Tax residency of BidCo

• Timing and formal requirements to set up a tax group

• Availability of tax loss carry forwards and interest carry forwards of Target post-closing

Fund

EU HoldCo

OffshoreEU

Management Participation

BidCo(Germany)

Germany

Target(Germany)

Tax group

Bank financing

Shareholder loan

Source: KPMG International, 2016

25©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Germany – typical investment structure (2/2)Key Tax Considerations (cont’d)

• Limitation on interest deductibility due to earning stripping rules

• Expected implications from BEPS action plan

• Real Estate Transfer Tax (3.5%-6.5%)

• Management Participation Programs under intensive scrutiny by German tax authorities

• VAT status of BidCo

• Transaction costs

• Management fees

Fund

EU HoldCo

OffshoreEU

Management Participation

BidCo(Germany)

Germany

Target(Germany)

Tax group

Bank financing

Shareholder loan

Source: KPMG International, 2016

India

Vikram Doshi

27©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Fund Raising Parameters

• Currency fluctuation risk• Political environment• Bilateral Investment Promotion and

Protection Agreements (BIPA)• Major tax breakthroughs such as

lowering of corporate tax rates

• E-Commerce sector (100% under automatic) - allowing e-commerce for manufacturing entities as well as for single brand retail trading entities;

• Relaxation of conditions for FDI in real estate sector

• Banking – Private Sector (up to 74% under automatic route)

• Defense (up to 49% under automatic route);

• Insurance (up to 49% under automatic route):

• 100% FDI in LLPs;

• Start Up India• Digital India• Smart City Mission• AMRUT mission (for urban

transformation)

• GAAR• POEM• Treaty• Indirect transfer• GST• BEPS• NJA

Make in India

Boosting FDI

Ease of doing business

Others

Tax uncertainties

• Higher Domestic and Foreign participation

• 100 million jobs to be created by 2022 in manufacturing

• Manufacturing sector’s contribution expected to be at 25 percent 2024

28©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

11.5 10.7 11.2 12.6

21.1

756836 863

934

1378

0

200

400

600

800

1000

1200

1400

1600

0

5

10

15

20

25

2011 2012 2013 2014 2015

Value in USD billion Volume

PE/VC Investments in IndiaPE/VC Investments in India

Source: “2016, Annual Deal Report“, VCCEdge

29©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Top sectors attracting PE investments

Source: “2016, Annual Deal Report“, VCCEdge

4,847

4,705

3,736

3,454

1,790

Consumer Discretionary

Information Technology

Financials

Industrials

Utilities

Value in USD billion

720

300

112

88

74

Information Technology

Consumer Discretionary

Industrials

Financials

Health care

Number of deals

30©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

PE/VC funds raised in India

Source: “2016, Annual Deal Report“, VCCEdge

5.6

3.5 3.43.9

5.1

48

54

43 44

39

0

10

20

30

40

50

60

0

1

2

3

4

5

6

2011 2012 2013 2014 2015

Amount raised in USD billion Volume

31©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

PE/VC exits in India

3.2

6.05.4

4.85.5

201

235 243

270252

0

50

100

150

200

250

300

0

1

2

3

4

5

6

7

2011 2012 2013 2014 2015

Value in USD billion Volume

Source: “2016, Annual Deal Report“, VCCEdge

32©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Top 10 PE deals in India in 2015Date Target Buyer / Lender Deal Value ($ mn) Sub Industry

22-Jan-15 Senvion SE Centerbridge Partners LP 1,158 Heavy Electrical Equipment

28-Jul-15 Flipkart Pvt. Ltd. Steadview Capital Master Fund Ltd., Tiger Global Management LLC 700 Internet Retail

13-Oct-15 Welspun Renewables Energy Pvt. Ltd. GE Energy Financial Services 570 Electric Utilities

18-Aug-15 Jasper Infotech Pvt. Ltd.SoftBank Corp., Hon Hai Precision Industry Co. Ltd., Alibaba Group Holding Ltd., BlackRock, Inc., Myriad Asset Management Ltd., PI Opportunities Fund II, Temasek Holdings Advisors India Pvt. Ltd.

500 Internet Retail

12-Aug-15 ANI Technologies Pvt. Ltd.

Tiger Global Management LLC, Steadview Capital Master Fund Ltd., SoftBank Corp., ABG Capital, Falcon Edge Capital LP, Sarin Family India LLC, Baillie Gifford and Company, Didi Kuaidi, DST Global, Arun Sarin

500 Internet Software & Services

22-Jun-15 Magna Energy Ltd. Carlyle International Energy Partners LP 500 Oil & Gas Exploration & Production

18-Jun-15 Atria Convergence Technologies Pvt. Ltd.

India Value Fund Advisors Pvt. Ltd., TA Associates Advisory Pvt. Ltd. 500 Broadcasting

19-Mar-15 ANI Technologies Pvt. Ltd.

Tiger Global Management LLC, Steadview Capital Master Fund Ltd., Accel India III LP, DST Global, ABG Capital, Falcon Edge Capital LP, GIC Pte. Ltd., SoftBank Corp., RNT Associates Pvt. Ltd., Ratan Naval Tata

402 Internet Software & Services

7-May-15 Shriram City Union Finance Ltd. Apax Partners LLP 385 Consumer Finance

16-Sep-15 Intelenet Global Services Pvt. Ltd. Blackstone Advisors India Pvt. Ltd. 384 Data Processing &

Outsourced Services

Source: “2016, Annual Deal Report“, VCCEdge

United Kingdom

Robin Walduck

34©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Case study: current structureInvestment management teams in Singapore and UK

Limited investment management activity in Luxembourg

Current structure no longer viable in a post-BEPS environment

Options available:1. Relocate investment management

activity to Luxembourg2. Restructure corporate holding

structure to align with operating structure

Fund(Singapore)

Holding Co(Luxembourg)

Investment management

teams (UK and Singapore)

Multiple Global Investments

PEReal

EstateInfra-

structureGeneral market trading

Debt funding

Source: KPMG International, 2016

35©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Case study: proposed structureRestructure corporate holding structure to align with operating structure

Benefits (UK):• Substantial Shareholding Exemption• Distribution exemption• Extensive treaty network• Quoted Eurobond exemption• REIT regime• Sovereign immunity status

Points for consideration:• Exit route from Luxembourg

(sale/migration)• Optimum holding structure for non-

UK real estate

Fund(Singapore)

Holding Co(Singapore)

Multiple Global Investments

PE

<10%

Real Estate (excl. UK)

Infra-structure (<10%)

General market trading

Debt funding

Holding Co(UK)

Multiple Global Investments

PE

>10%

UK Real Estate

Infra-structure (>10%)

Debt funding

Source: KPMG International, 2016

36©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Key points driving changeImpact of BEPS Action items

• Action 6 – Treaty Abuse• Action 4 – Interest Deductibility – UK already consulting• Action 2 – Hybrid Mismatches – draft legislation effective 1

January 2017• Substance

Luxembourg popular, but dynamic changing?• Luxembourg

‒ Cost, execution process, adviser fees‒ Ruling process, treaty network, funding models (PECs, etc.)

• UK‒ Management of substance‒ Consulting on SSE rules‒ Inward investment success - positive FDI, large increases

in value and volume

37©2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Document Classification: KPMG Confidential

Contacts …..Brendon Lamers KPMG in Australia +61 7 3434 9148 [email protected]

John Gu KPMG in China +86 10 8508 7095 [email protected]

Holger Lampe KPMG in Germany +49 211 475 7628 [email protected]

Darren Bowdern KPMG in Hong Kong +852 2826 7166 [email protected]

Malcolm Prebble KPMG in Hong Kong +852 2685 7472 [email protected]

Vikram Doshi KPMG in India +91 40 3046 5100 [email protected]

Chee Wei Tan KPMG in Singapore +65 6213 2470 [email protected]

Umang Daiya KPMG in Singapore +65 6213 2957 [email protected]

Robin Walduck KPMG in the UK +44(0)20 7311 1816 [email protected]

Ryan Davis KPMG in the US +1 212 872 6536 [email protected]

kpmg.com/socialmedia kpmg.com/app

© 2016 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

The KPMG name, logo are registered trademarks or trademarks of KPMG International.