private equity case study february 26, 2006 - franchise · private equity case study. february 26,...

TRANSCRIPT

1

Private Equity Case Study

February 26, 2006

2

Today

Steve CarleyPresident & CEO3333 Michelson DriveSuite 550Irvine, CA 92612949-399-2000www.elpolloloco.com

Glenn KaufmanManaging Director666 Third Ave., 29th FloorNew York, NY 10017212-476-8000www.american-securities.com

3

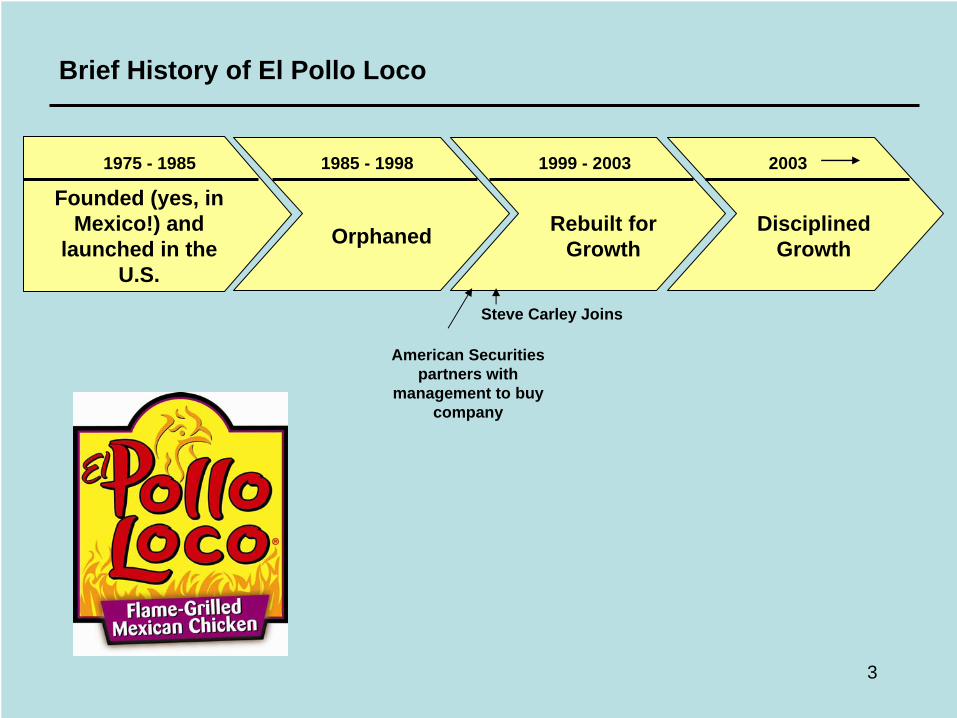

Brief History of El Pollo Loco

1975 - 1985 1985 - 1998 1999 - 2003 2003

Founded (yes, in Mexico!) and

launched in the U.S.

Orphaned Rebuilt for Growth

Disciplined Growth

American Securities partners with

management to buy company

Steve Carley Joins

4

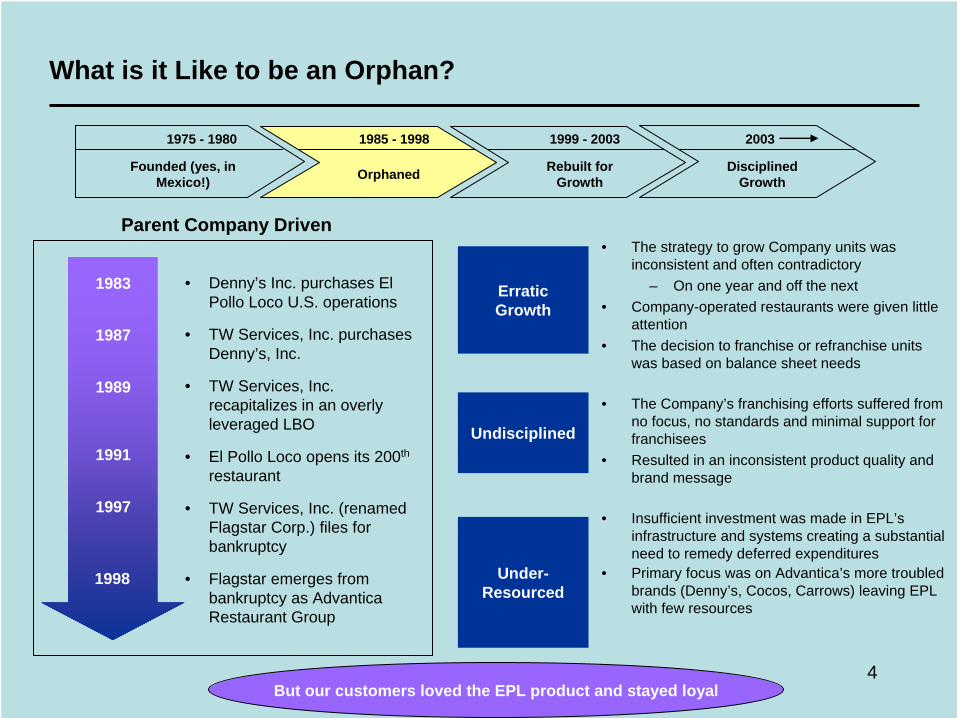

What is it Like to be an Orphan?

• Denny’s Inc. purchases El Pollo Loco U.S. operations

• TW Services, Inc. purchases Denny’s, Inc.

• TW Services, Inc. recapitalizes in an overly leveraged LBO

• El Pollo Loco opens its 200th

restaurant

• TW Services, Inc. (renamed Flagstar Corp.) files for bankruptcy

• Flagstar emerges from bankruptcy as Advantica Restaurant Group

1983

1987

1997

1998

1989

1991

Parent Company Driven

1975 - 1980 1985 - 1998 1999 - 2003 2003

Founded (yes, in Mexico!) Orphaned Rebuilt for

GrowthDisciplined

Growth

• The strategy to grow Company units was inconsistent and often contradictory

– On one year and off the next• Company-operated restaurants were given little

attention • The decision to franchise or refranchise units

was based on balance sheet needs

• The Company’s franchising efforts suffered from no focus, no standards and minimal support for franchisees

• Resulted in an inconsistent product quality and brand message

• Insufficient investment was made in EPL’s infrastructure and systems creating a substantial need to remedy deferred expenditures

• Primary focus was on Advantica’s more troubled brands (Denny’s, Cocos, Carrows) leaving EPL with few resources

ErraticGrowth

Undisciplined

Under- Resourced

But our customers loved the EPL product and stayed loyal

5

The Ownership Transition

• American Securities Capital Partners and management bought from Advantica

• Committed to fixing the problems and making the investments required to rebuild/correct the past deferred investment and to sustain an ongoing growth program

• Reduced leverage!!

What Happened

1975 - 1980 1985 - 1998 1999 - 2003 2003

Founded (yes, in Mexico!) Orphaned Rebuilt for

GrowthDisciplined

Growth

• Stopped aggressive growth

• Stopped aggressive franchising

– No new franchise development agreements

– Shrunk franchise base from 71 to 54

What We Stopped

6

Rebuilding the Foundation for Growth – Investing Into the Company

American Securities and management committed to a substantial capital plan toward the chain’s long term success

• Restaurants– Remodeled and refocused on deferred maintenance– Redesigned and re-imaged units to be consistent with the brand– Re-engineered the buildings for efficiency of cost and function– Ultimately developed “next generation” restaurant, changing the

operational aspects of the business• Information technology

– Installed new back office systems designed for this type of business– Upgraded each unit in POS and communication– Laid foundation for continued IT improvement

• People– Deepened the group of world class executives/managers– Substantially invested in new HR/training/leadership department– Added area leaders to tighten span of control

7

Rebuilding the Foundation for Growth – Strategic Repositioning

• Based on a developed vision, over the last five years, EPL has strategically positioned itself between the traditional chicken/Mexican QSR and fast-casual Mexican market segments

Higher

Con

veni

ence

an

dVa

lue

Lower

Lower HigherMenu and DiningExperience Quality

QSR ($128bn)

Fast-Casual ($7bn)

8

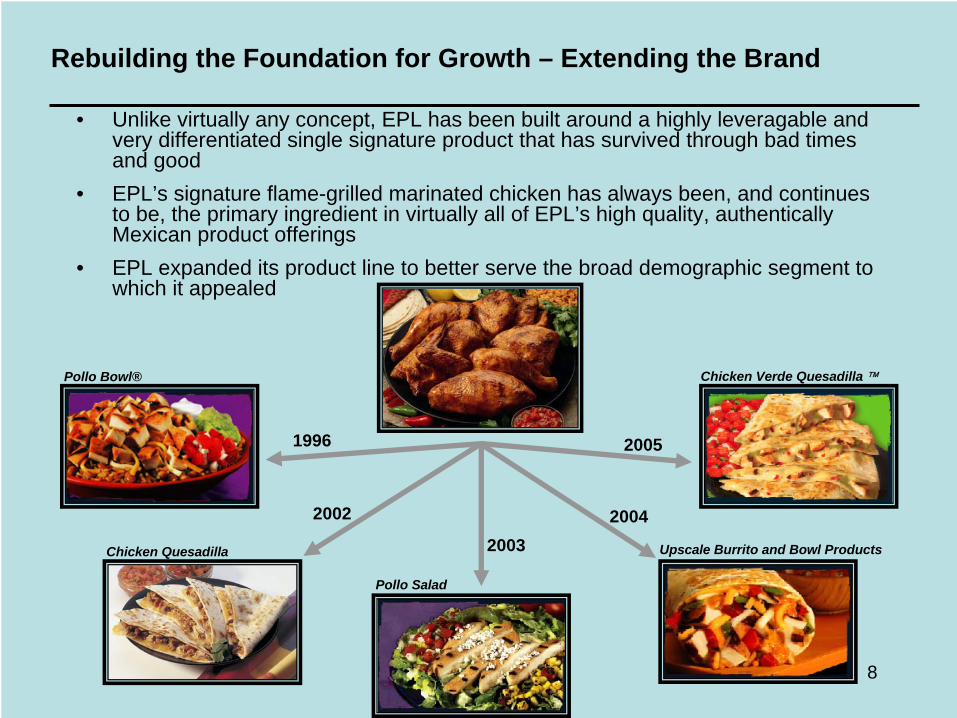

Rebuilding the Foundation for Growth – Extending the Brand

• Unlike virtually any concept, EPL has been built around a highly leveragable and very differentiated single signature product that has survived through bad times and good

• EPL’s signature flame-grilled marinated chicken has always been, and continues to be, the primary ingredient in virtually all of EPL’s high quality, authentically Mexican product offerings

• EPL expanded its product line to better serve the broad demographic segment to which it appealed

1996

2002 2004

2005

Pollo Bowl®

2003

Pollo Salad

Upscale Burrito and Bowl Products

Chicken Verde Quesadilla ™

Chicken Quesadilla

9

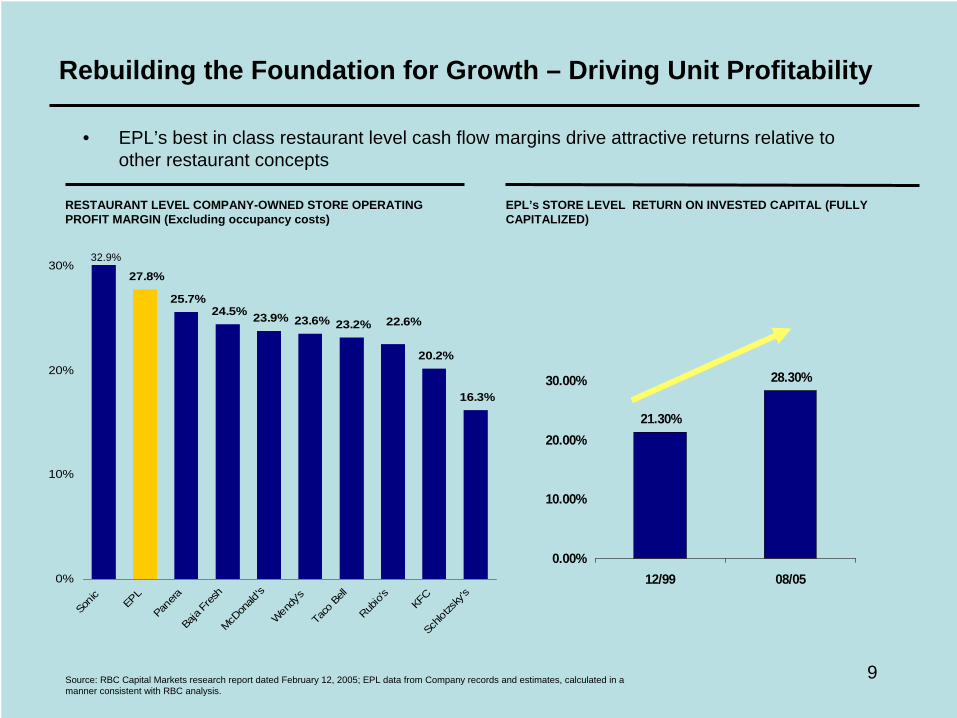

25.7%24.5% 23.9% 23.6% 23.2%

20.2%

16.3%

27.8%

22.6%

0%

10%

20%

30%

Sonic EP

L

Pane

raBa

ja Fr

esh

McDon

ald's

Wendy

'sTa

co Be

ll

Rubio'

s

KFC

Schlo

tzsky

's

• EPL’s best in class restaurant level cash flow margins drive attractive returns relative to other restaurant concepts

Rebuilding the Foundation for Growth – Driving Unit Profitability

Source: RBC Capital Markets research report dated February 12, 2005; EPL data from Company records and estimates, calculated in a manner consistent with RBC analysis.

RESTAURANT LEVEL COMPANY-OWNED STORE OPERATING PROFIT MARGIN (Excluding occupancy costs)

EPL’s STORE LEVEL RETURN ON INVESTED CAPITAL (FULLY CAPITALIZED)

21.30%

28.30%

0.00%

10.00%

20.00%

30.00%

12/99 08/05

32.9%

10

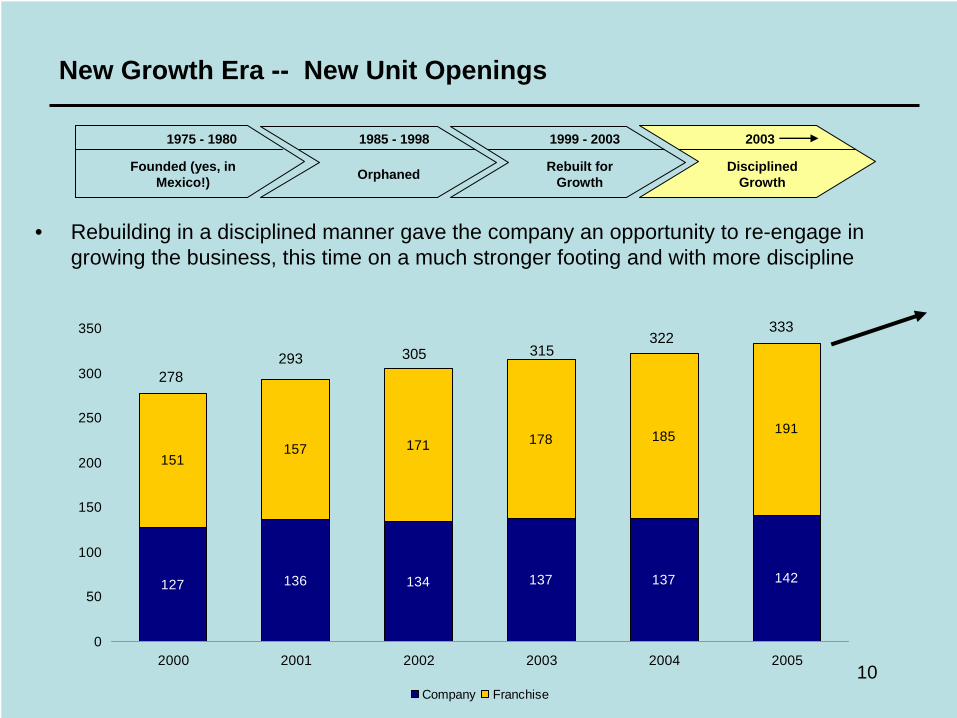

New Growth Era -- New Unit Openings

127 136 134 137 137 142

157 171 178 185 191

151

0

50

100

150

200

250

300

350

2000 2001 2002 2003 2004 2005

Company Franchise

278293 305 315

322333

1975 - 1980 1985 - 1998 1999 - 2003 2003

Founded (yes, in Mexico!) Orphaned Rebuilt for

GrowthDisciplined

Growth

• Rebuilding in a disciplined manner gave the company an opportunity to re-engage in growing the business, this time on a much stronger footing and with more discipline

11

New Growth Era – The Future of EPL

• 7-10 new each year in existing markets

• Total of 143

New Company

Stores

Aggressive Franchise

Growth

• Total of 192

12

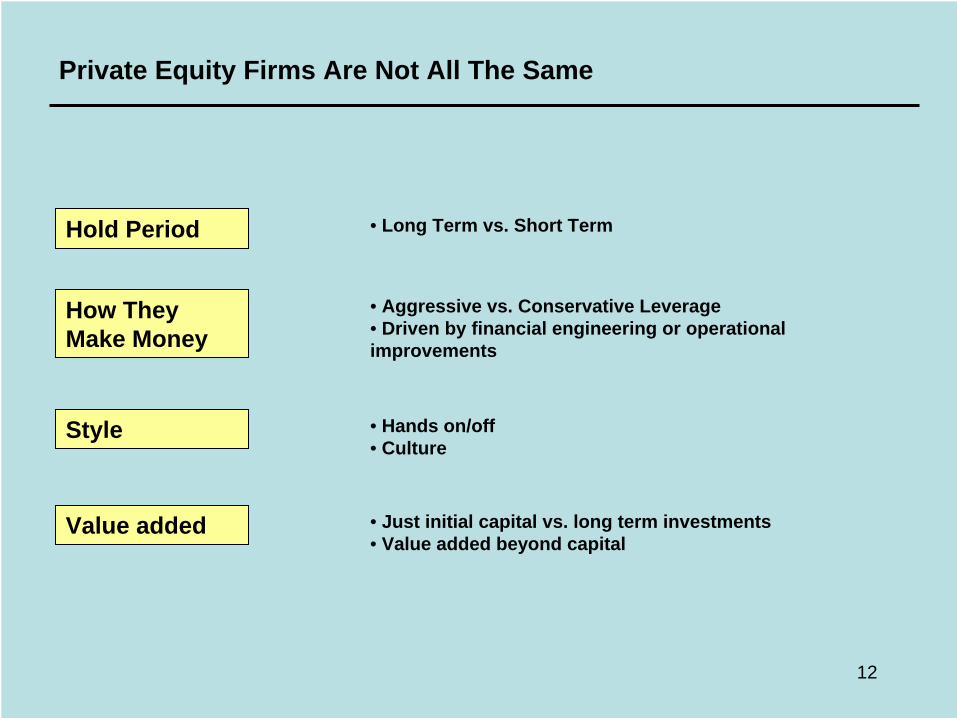

Private Equity Firms Are Not All The Same

Hold Period • Long Term vs. Short Term

How They Make Money

• Aggressive vs. Conservative Leverage• Driven by financial engineering or operational improvements

Style • Hands on/off• Culture

Value added • Just initial capital vs. long term investments• Value added beyond capital

13

My Thoughts on Choosing a Private Equity Partner

• Hello “Controlling Equity Partner”– Internalize intellectually and emotionally

• Establish Broad Strategic Alignment– Confirm CEO and management team’s participation vis a vis a private

equity partner• Leverage Formal and “Back-Channel” References Personally

– Probe any areas of concern• Discuss “Freedom of Action” Guidelines/Approval Authority in

Advance• Understand Formal and Informal Communication Expectations

and Roles• Actively Explore “Rules of Engagement” for CEO/Direct Reports

and Private Equity Members• Discuss “Disaster Scenario” Definitions and Implications on

Management Team Up Front

14

Steve CarleyPresident & CEO3333 Michelson DriveSuite 550Irvine, CA 92612949-399-2000www.elpolloloco.com

Today

Glenn KaufmanManaging Director666 Third Ave., 29th FloorNew York, NY 10017212-476-8000www.american-securities.com

15

American Securities Capital Partners: Overview

• Founded by William Rosenwald to manage his share of the Sears, Roebuck fortune

• Designed around the visions and needs of the wealthy individuals and families – long term, wealth preservation and desire to support the building of great enterprises

• 12 year history of top quartile returns, with no bad investments

• Currently managing $1.6 billion in capital

• Focused on companies between $50- 500 million in revenue

• Experienced investment professionals in both franchisor and franchisee settings

Background Our Philosophy

• Great Companies: Find good or great companies with strong position/ differentiation

• Invest with management: Always invest with management under the same terms – align incentives - we all win or we all lose

• Focus on upside to management: Increase management potential by granting meaningful options across the management team

• Low leverage: If we use leverage – keep it low, to allow companies to focus on business not balance sheet

• Add value: Act as a thought partner and add value in finance, strategy, growth, operations – but never interfere with management role

16

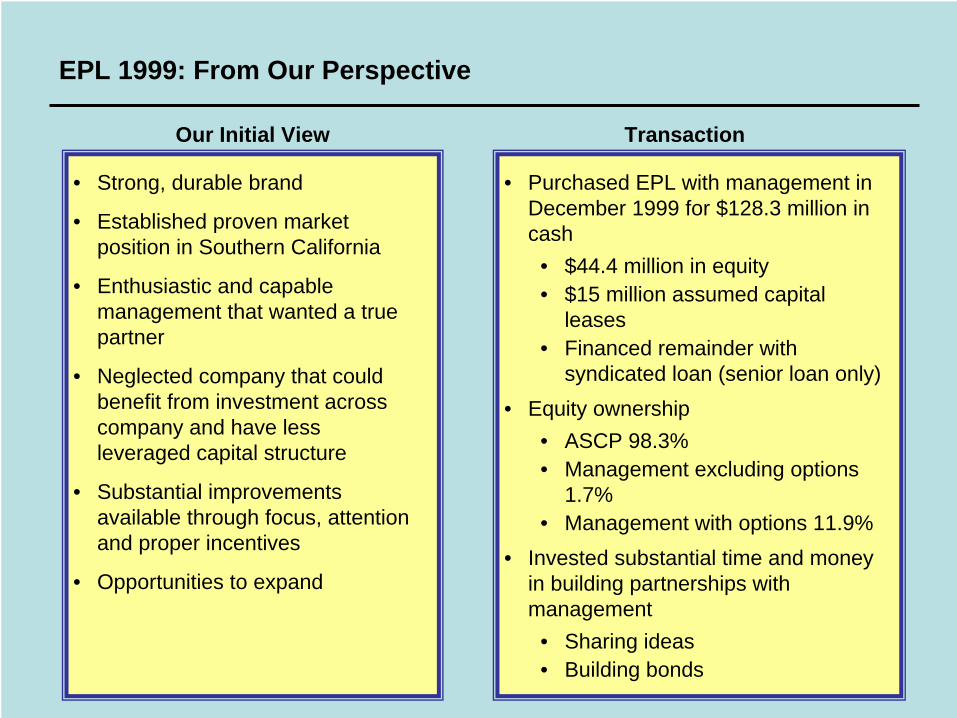

EPL 1999: From Our Perspective

• Strong, durable brand

• Established proven market position in Southern California

• Enthusiastic and capable management that wanted a true partner

• Neglected company that could benefit from investment across company and have less leveraged capital structure

• Substantial improvements available through focus, attention and proper incentives

• Opportunities to expand

Our Initial View Transaction

• Purchased EPL with management in December 1999 for $128.3 million in cash

• $44.4 million in equity• $15 million assumed capital

leases• Financed remainder with

syndicated loan (senior loan only)• Equity ownership

• ASCP 98.3%• Management excluding options

1.7%• Management with options 11.9%

• Invested substantial time and money in building partnerships with management

• Sharing ideas• Building bonds

17

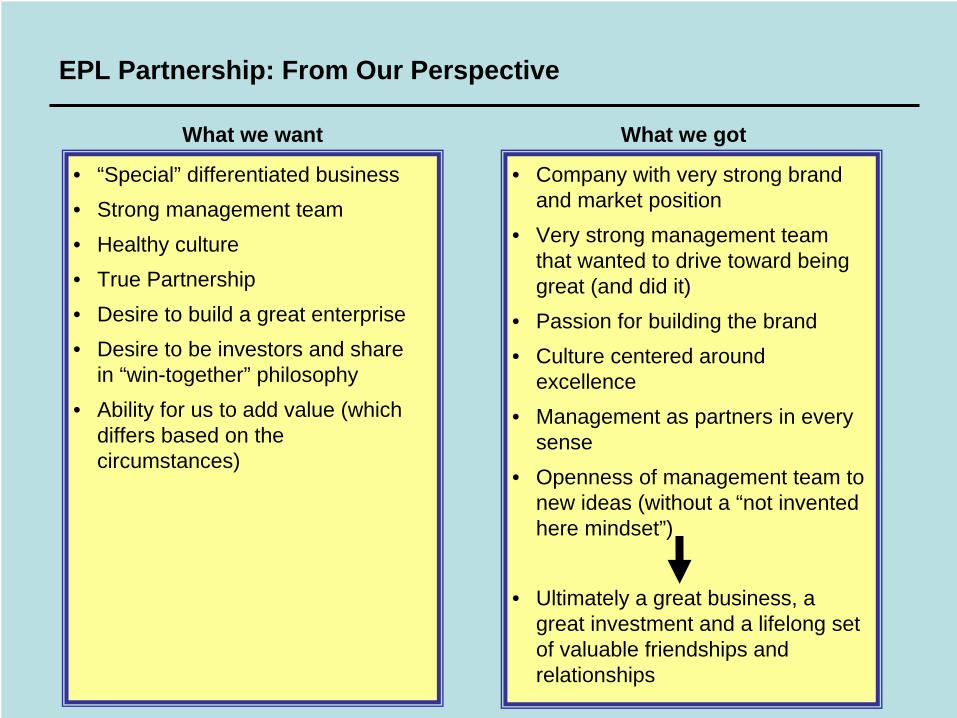

EPL Partnership: From Our Perspective

• “Special” differentiated business• Strong management team• Healthy culture• True Partnership• Desire to build a great enterprise• Desire to be investors and share

in “win-together” philosophy• Ability for us to add value (which

differs based on the circumstances)

What we want What we got

• Company with very strong brand and market position

• Very strong management team that wanted to drive toward being great (and did it)

• Passion for building the brand• Culture centered around

excellence• Management as partners in every

sense• Openness of management team to

new ideas (without a “not invented here mindset”)

• Ultimately a great business, a great investment and a lifelong set of valuable friendships and relationships

18