private equity, lbo & venture february 14 private equity ... · the 31st annual federal...

TRANSCRIPT

The 31st Annual Federal Securities Institute

Private Equity, LBO & Venture Capital Panel

February 14th & 15th, 2013 Private Equity Market Overview Andrew J. Stull Houlihan Lokey

Private Equity Market Trends

Current Observations

Private equity transaction volume in 2012 was lower than what was expected

Remains a very favorable market for sellers

Debt capital markets “could not be stronger”

Transaction multiples are approaching or exceeding pre-crisis peak levels in the middle market

Private equity exit activity has increased for a third straight year

Despite increase in private equity exits the average holding period remains at an all time high - 5.4 years

Competition for deals among private equity firms remains very intense

Middle market has become very efficient

Firms have become highly specialized in terms of industry focus and transaction type

Firms are being more creative on transaction origination in order to gain an edge

Secondary buyouts has become more common and accepted

More sales to private equity buyers than corporates for the first time in 2012

Fundraising by private equity firms continues to be a difficult process

The 31st Annual Federal Securities

Institute Panel

1

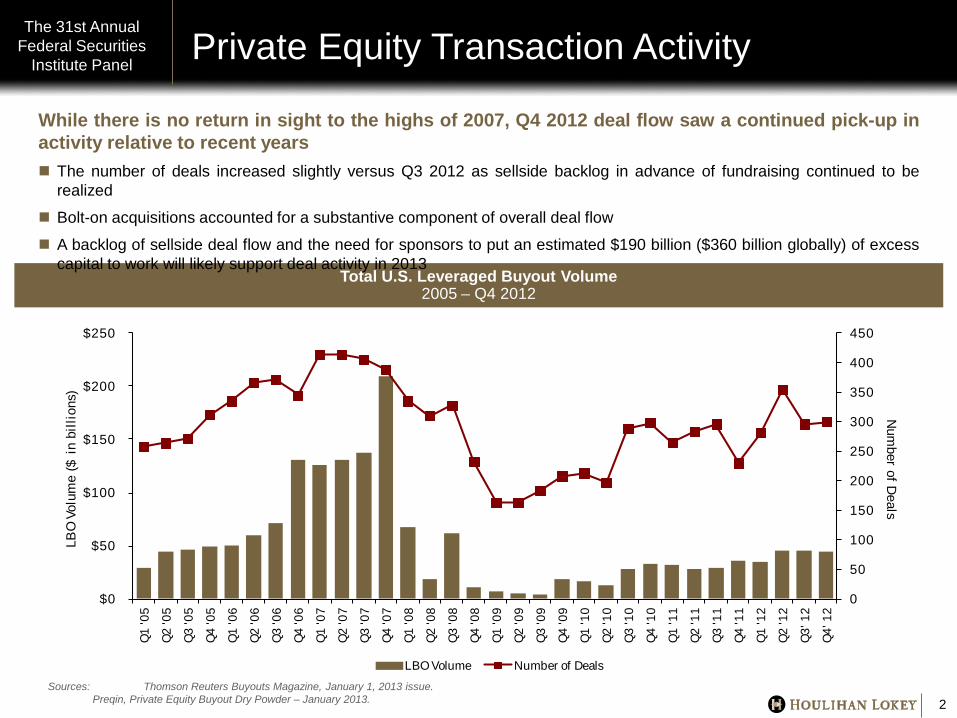

Private Equity Transaction Activity The 31st Annual

Federal Securities Institute Panel

2

Total U.S. Leveraged Buyout Volume 2005 – Q4 2012

While there is no return in sight to the highs of 2007, Q4 2012 deal flow saw a continued pick-up in activity relative to recent years The number of deals increased slightly versus Q3 2012 as sellside backlog in advance of fundraising continued to be

realized

Bolt-on acquisitions accounted for a substantive component of overall deal flow

A backlog of sellside deal flow and the need for sponsors to put an estimated $190 billion ($360 billion globally) of excess capital to work will likely support deal activity in 2013

0

50

100

150

200

250

300

350

400

450

$0

$50

$100

$150

$200

$250

Q1

'05

Q2

'05

Q3

'05

Q4

'05

Q1

'06

Q2

'06

Q3

'06

Q4

'06

Q1

'07

Q2

'07

Q3

'07

Q4

'07

Q1

'08

Q2

'08

Q3

'08

Q4

'08

Q1

'09

Q2

'09

Q3

'09

Q4

'09

Q1

'10

Q2

'10

Q3

'10

Q4

'10

Q1

'11

Q2

'11

Q3

'11

Q4

'11

Q1

'12

Q2

'12

Q3'

12

Q4'

12

Num

ber of Deals

LBO

Vol

ume

($ i

n bi

llion

s)

LBO Volume Number of DealsSources: Thomson Reuters Buyouts Magazine, January 1, 2013 issue. Preqin, Private Equity Buyout Dry Powder – January 2013.

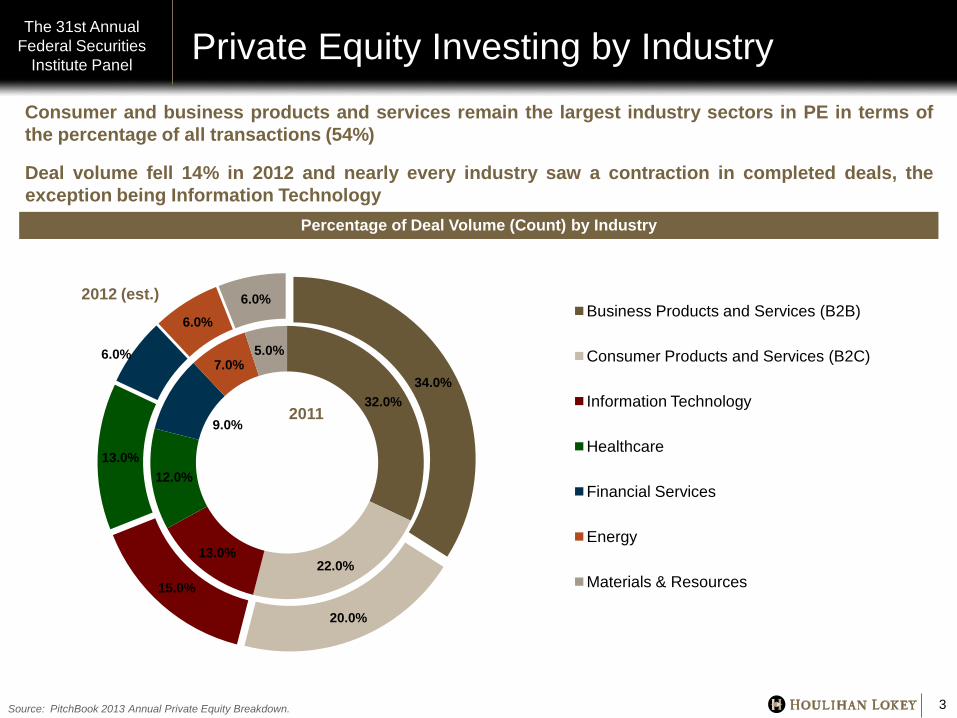

Private Equity Investing by Industry Consumer and business products and services remain the largest industry sectors in PE in terms of the percentage of all transactions (54%)

Deal volume fell 14% in 2012 and nearly every industry saw a contraction in completed deals, the exception being Information Technology

The 31st Annual Federal Securities

Institute Panel

3 Source: PitchBook 2013 Annual Private Equity Breakdown.

Percentage of Deal Volume (Count) by Industry

2012 (est.)

32.0%

22.0% 13.0%

12.0%

9.0%

7.0% 5.0%

34.0%

20.0%

15.0%

13.0%

6.0%

6.0% 6.0%

Business Products and Services (B2B)

Consumer Products and Services (B2C)

Information Technology

Healthcare

Financial Services

Energy

Materials & Resources

2011

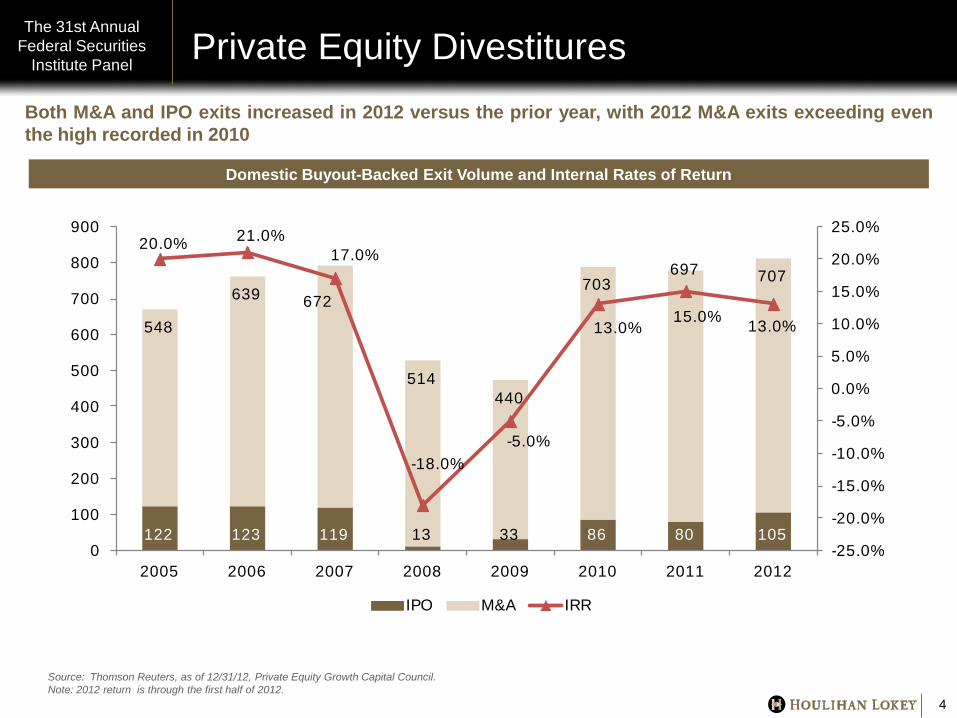

Private Equity Divestitures The 31st Annual

Federal Securities Institute Panel

4

Both M&A and IPO exits increased in 2012 versus the prior year, with 2012 M&A exits exceeding even the high recorded in 2010

Domestic Buyout-Backed Exit Volume and Internal Rates of Return

Source: Thomson Reuters, as of 12/31/12, Private Equity Growth Capital Council. Note: 2012 return is through the first half of 2012.

122 123 119 13 33 86 80 105

548

639 672

514440

703697 707

20.0% 21.0%17.0%

-18.0%-5.0%

13.0%15.0% 13.0%

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

0

100

200

300

400

500

600

700

800

900

2005 2006 2007 2008 2009 2010 2011 2012

IPO M&A IRR

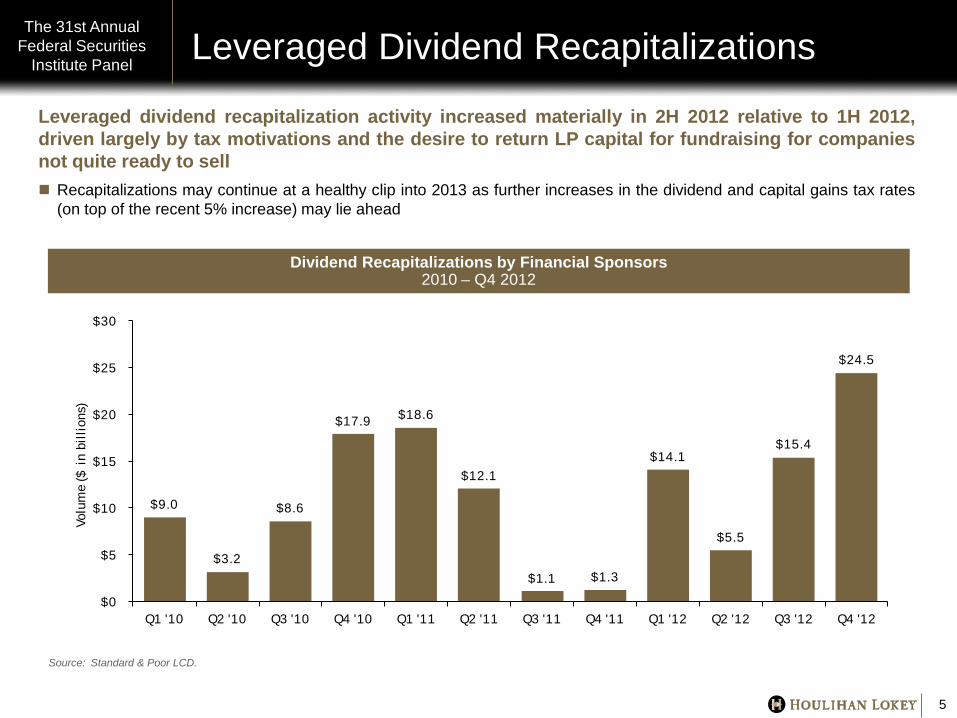

Leveraged Dividend Recapitalizations The 31st Annual

Federal Securities Institute Panel

5

Dividend Recapitalizations by Financial Sponsors 2010 – Q4 2012

Source: Standard & Poor LCD.

Leveraged dividend recapitalization activity increased materially in 2H 2012 relative to 1H 2012, driven largely by tax motivations and the desire to return LP capital for fundraising for companies not quite ready to sell Recapitalizations may continue at a healthy clip into 2013 as further increases in the dividend and capital gains tax rates

(on top of the recent 5% increase) may lie ahead

$9.0

$3.2

$8.6

$17.9 $18.6

$12.1

$1.1 $1.3

$14.1

$5.5

$15.4

$24.5

$0

$5

$10

$15

$20

$25

$30

Q1 '10 Q2 '10 Q3 '10 Q4 '10 Q1 '11 Q2 '11 Q3 '11 Q4 '11 Q1 '12 Q2 '12 Q3 '12 Q4 '12

Volu

me

($ i

n bi

llion

s)

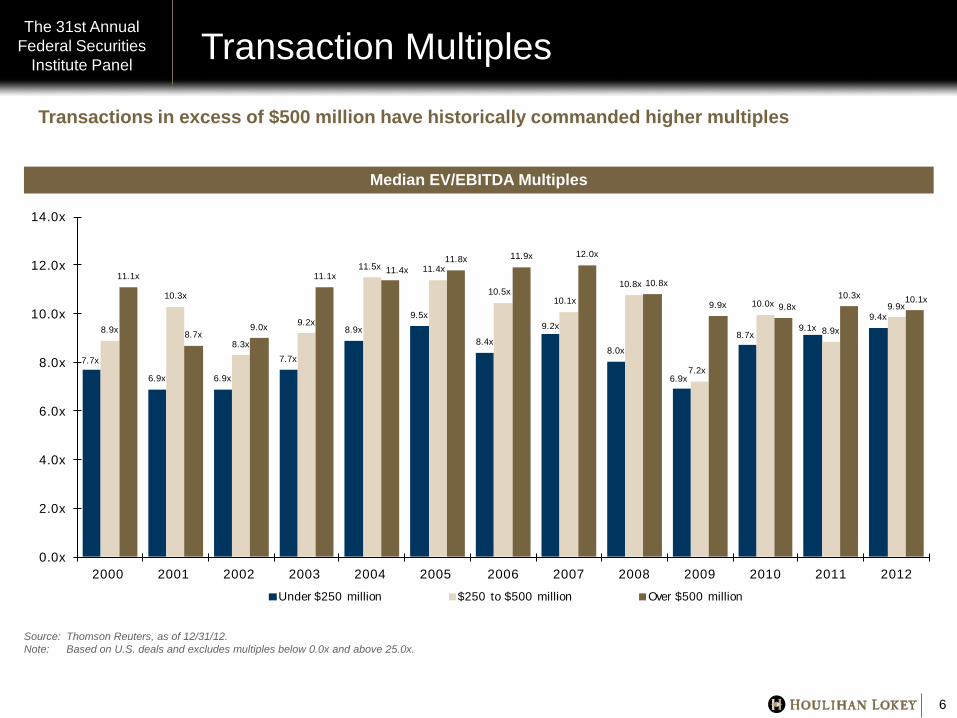

Transaction Multiples

6

Median EV/EBITDA Multiples

Source: Thomson Reuters, as of 12/31/12. Note: Based on U.S. deals and excludes multiples below 0.0x and above 25.0x.

Transactions in excess of $500 million have historically commanded higher multiples

7.7x

6.9x 6.9x

7.7x

8.9x9.5x

8.4x

9.2x

8.0x

6.9x

8.7x9.1x

9.4x8.9x

10.3x

8.3x

9.2x

11.5x 11.4x

10.5x10.1x

10.8x

7.2x

10.0x

8.9x

9.9x

11.1x

8.7x9.0x

11.1x11.4x

11.8x 11.9x 12.0x

10.8x

9.9x 9.8x10.3x 10.1x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Under $250 million $250 to $500 million Over $500 million

The 31st Annual Federal Securities

Institute Panel

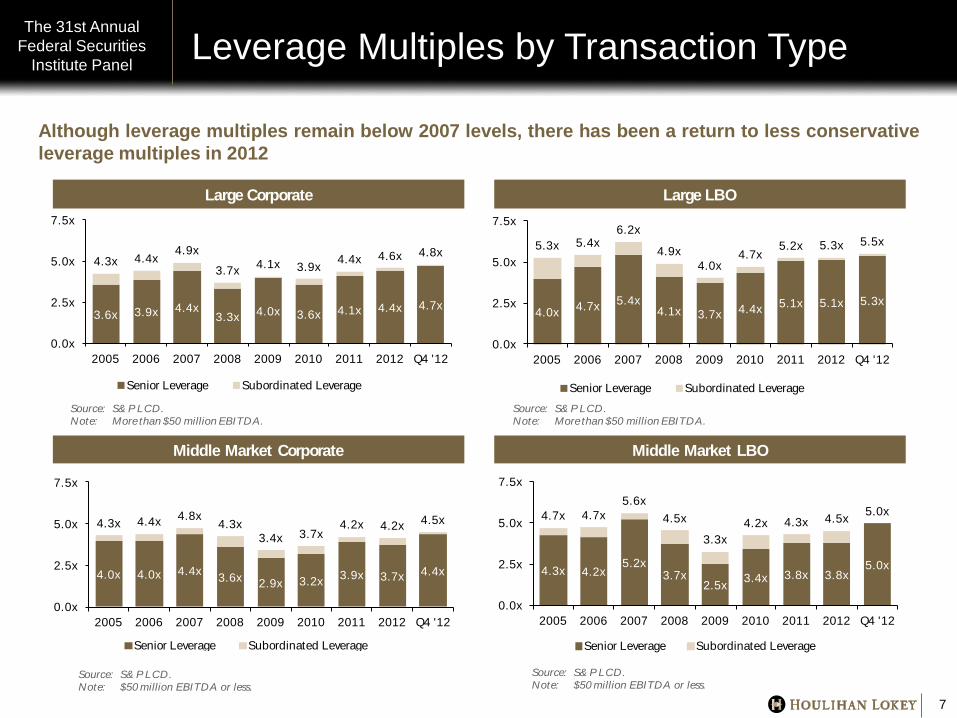

Leverage Multiples by Transaction Type The 31st Annual

Federal Securities Institute Panel

7

Although leverage multiples remain below 2007 levels, there has been a return to less conservative leverage multiples in 2012

Large Corporate Large LBO

Middle Market Corporate Middle Market LBO

3.6x 3.9x 4.4x3.3x 4.0x 3.6x 4.1x 4.4x 4.7x

4.3x 4.4x4.9x

3.7x 4.1x 3.9x 4.4x 4.6x 4.8x

0.0x

2.5x

5.0x

7.5x

2005 2006 2007 2008 2009 2010 2011 2012 Q4 '12

Senior Leverage Subordinated Leverage

Source: S& P LCD.Note: More than $50 million EBITDA.

4.0x 4.7x 5.4x4.1x 3.7x 4.4x 5.1x 5.1x 5.3x

5.3x 5.4x6.2x

4.9x4.0x

4.7x5.2x 5.3x 5.5x

0.0x

2.5x

5.0x

7.5x

2005 2006 2007 2008 2009 2010 2011 2012 Q4 '12

Senior Leverage Subordinated Leverage

Source: S& P LCD.Note: More than $50 million EBITDA.

4.0x 4.0x 4.4x 3.6x 2.9x 3.2x 3.9x 3.7x 4.4x

4.3x 4.4x 4.8x4.3x

3.4x 3.7x4.2x 4.2x 4.5x

0.0x

2.5x

5.0x

7.5x

2005 2006 2007 2008 2009 2010 2011 2012 Q4 '12

Senior Leverage Subordinated Leverage

Source: S& P LCD.Note: $50 million EBITDA or less.

4.3x 4.2x5.2x

3.7x2.5x 3.4x 3.8x 3.8x

5.0x

4.7x 4.7x5.6x

4.5x

3.3x4.2x 4.3x 4.5x 5.0x

0.0x

2.5x

5.0x

7.5x

2005 2006 2007 2008 2009 2010 2011 2012 Q4 '12

Senior Leverage Subordinated Leverage

Source: S& P LCD.Note: $50 million EBITDA or less.

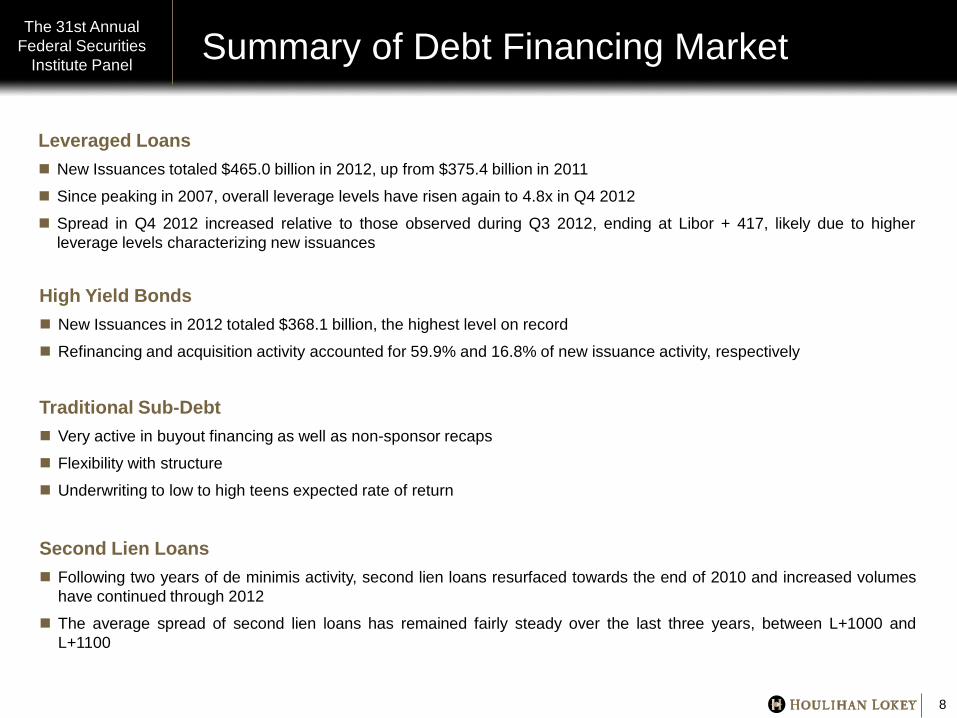

Summary of Debt Financing Market The 31st Annual

Federal Securities Institute Panel

8

Leveraged Loans New Issuances totaled $465.0 billion in 2012, up from $375.4 billion in 2011

Since peaking in 2007, overall leverage levels have risen again to 4.8x in Q4 2012

Spread in Q4 2012 increased relative to those observed during Q3 2012, ending at Libor + 417, likely due to higher leverage levels characterizing new issuances

High Yield Bonds New Issuances in 2012 totaled $368.1 billion, the highest level on record

Refinancing and acquisition activity accounted for 59.9% and 16.8% of new issuance activity, respectively

Second Lien Loans Following two years of de minimis activity, second lien loans resurfaced towards the end of 2010 and increased volumes

have continued through 2012

The average spread of second lien loans has remained fairly steady over the last three years, between L+1000 and L+1100

Traditional Sub-Debt Very active in buyout financing as well as non-sponsor recaps

Flexibility with structure

Underwriting to low to high teens expected rate of return

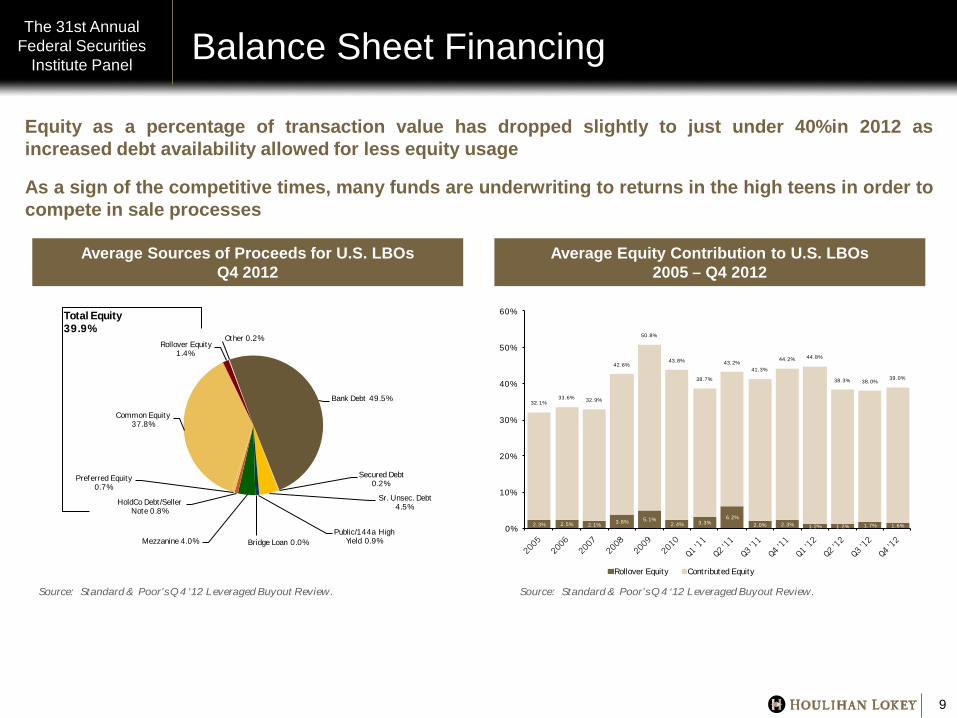

Balance Sheet Financing The 31st Annual

Federal Securities Institute Panel

9

Equity as a percentage of transaction value has dropped slightly to just under 40%in 2012 as increased debt availability allowed for less equity usage

As a sign of the competitive times, many funds are underwriting to returns in the high teens in order to compete in sale processes

Average Sources of Proceeds for U.S. LBOs Q4 2012

Average Equity Contribution to U.S. LBOs 2005 – Q4 2012

Bank Debt 49.5%

Secured Debt 0.2%

Sr. Unsec. Debt 4.5%

Public/144a High Yield 0.9%Bridge Loan 0.0%Mezzanine 4.0%

HoldCo Debt/Seller Note 0.8%

Preferred Equity 0.7%

Common Equity 37.8%

Rollover Equity 1.4%

Other 0.2%

Total Equity39.9%

Source: Standard & Poor’s Q4 ‘12 Leveraged Buyout Review.

2.3% 2.5% 2.1% 3.8% 5.1%2.4% 3.3%

6.2%2.0% 2.3% 1.2% 1.2% 1.7% 1.6%

32.1%33.6% 32.9%

42.6%

50.8%

43.8%

38.7%

43.2%41.3%

44.2% 44.8%

38.3% 38.0%39.0%

0%

10%

20%

30%

40%

50%

60%

Rollover Equity Contributed Equity

Source: Standard & Poor’s Q4 ‘12 Leveraged Buyout Review.

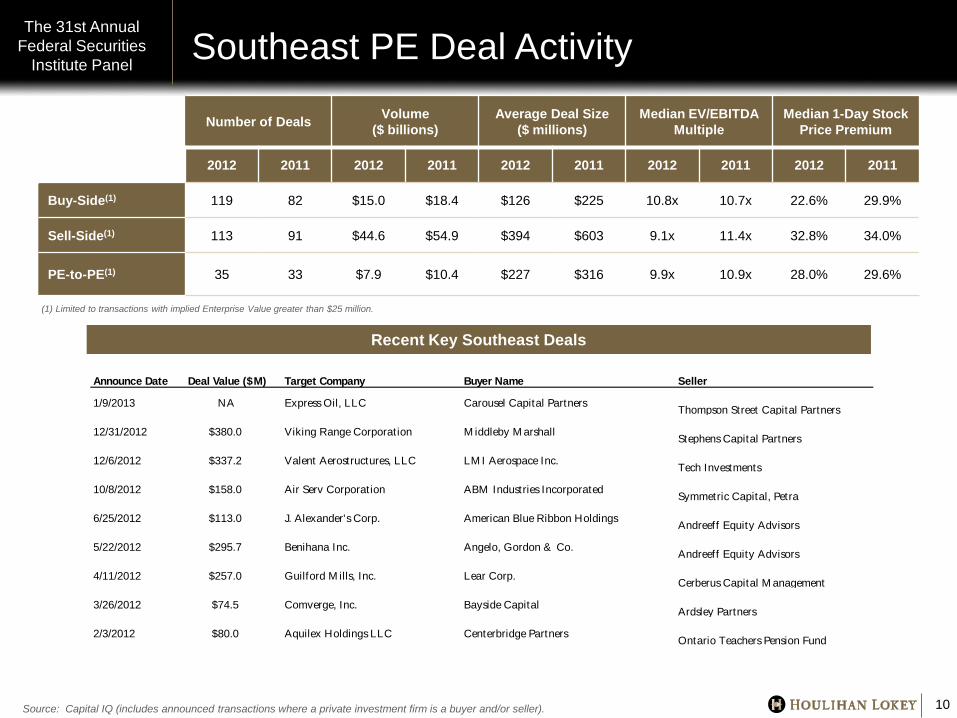

Southeast PE Deal Activity The 31st Annual

Federal Securities Institute Panel

10

Number of Deals Volume ($ billions)

Average Deal Size ($ millions)

Median EV/EBITDA Multiple

Median 1-Day Stock Price Premium

2012 2011 2012 2011 2012 2011 2012 2011 2012 2011

Buy-Side(1) 119 82 $15.0 $18.4 $126 $225 10.8x 10.7x 22.6% 29.9%

Sell-Side(1) 113 91 $44.6 $54.9 $394 $603 9.1x 11.4x 32.8% 34.0%

PE-to-PE(1) 35 33 $7.9 $10.4 $227 $316 9.9x 10.9x 28.0% 29.6%

Recent Key Southeast Deals

(1) Limited to transactions with implied Enterprise Value greater than $25 million.

Source: Capital IQ (includes announced transactions where a private investment firm is a buyer and/or seller).

Announce Date Deal Value ($M) Target Company Buyer Name Seller

1/9/2013 NA Express Oil, LLC Carousel Capital Partners Thompson Street Capital Partners

12/31/2012 $380.0 Viking Range Corporation M iddleby M arshall Stephens Capital Partners

12/6/2012 $337.2 Valent Aerostructures, LLC LM I Aerospace Inc. Tech Investments

10/8/2012 $158.0 Air Serv Corporation ABM Industries Incorporated Symmetric Capital, Petra

6/25/2012 $113.0 J. Alexander's Corp. American Blue Ribbon Holdings Andreeff Equity Advisors

5/22/2012 $295.7 Benihana Inc. Angelo, Gordon & Co. Andreeff Equity Advisors

4/11/2012 $257.0 Guilford M ills, Inc. Lear Corp. Cerberus Capital M anagement

3/26/2012 $74.5 Comverge, Inc. Bayside Capital Ardsley Partners

2/3/2012 $80.0 Aquilex Holdings LLC Centerbridge Partners Ontario Teachers Pension Fund

Venture Capital Overview The 31st Annual

Federal Securities Institute Panel

11

Source: The Wall Street Journal

Investment in U.S. venture backed companies was $6.9 billion across 820 deals in 3Q 2012, down from $10.1 billion and 906 deals in the prior year period.

High profile IPOs in 2012 that disappointed (i.e. Groupon, Facebook, Zynga) caused a tail off in venture investing in 2H 2012

Areas that continue to attract venture investing include: mobile, infrastructure, enterprise software and niche social media

Venture investing model has changed from a shorter investment horizon, IPO-driven exit to a longer term hold period and an M&A driven exit

Distressed M&A Observations The 31st Annual

Federal Securities Institute Panel

12

Source: Schulte Roth & Zabel LLP Distressed Investing M&A report, Thomson Reuters.

Payment default rates on leveraged loans reached a post-2007 low of 2.2% in Q4 2012

2007 default rate was 0.6%, the previous low

2009 default rate was 10.7%, a 20-year high

Globally, the ongoing eurozone crisis and macroeconomic concerns in emerging markets are likely to create a number of distressed opportunities in the coming year

Eurozone banks remain undercapitalized

Less accommodative capital markets

The Energy sector is expected to be active for distressed mergers & acquisitions, partly due to low U.S. natural gas prices and regulatory shifts negatively affecting several sectors such as:

Coal Producers

Alternative Energy

Utilities

Other sectors seeing levels of distress:

“Old” Media Companies

Conventional Retail

Transportation

Outlook for 2013 – Key Questions

Will PE deal volume and valuation increase in 2013?

Will the debt market stay highly accommodative?

Will the Dell take private transaction kick off a new buyout wave?

What are some of the tactics and strategies private equity firms will deploy on the buyside in the face of highly competitive processes?

What trends do we expect for transaction terms in middle market deals?

What is the outlook for distressed deals?

Any interesting trends in private equity on the sellside?

The 31st Annual Federal Securities

Institute Panel

13