private credit & niche secondaries market update

TRANSCRIPT

1

Private Credit & Niche Secondaries Market UpdateMay 2021

Disclaimer:Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases has not been updated through the date of thedistribution of this presentation. While such sources are believed to be reliable for the purposes used herein, Dorchester does not assume any responsibility for the accuracy or completeness of suchinformation. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to theaccuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Dorchesterconsiders to be reasonable. This document does not constitute advice or a recommendation or offer to sell or a solicitation to deal in any security or financial product. It is provided for informationpurposes only.

2

Rob Johnson, CFADorchester Capital Advisors

Jason Gabrielli, CFADorchester Capital Advisors

Sophie GioanniLinchpin IFM Ltd

PRIVATE CREDIT & NICHE SECONDARIESHosted by Linchpin IFM Ltd and Dorchester Capital Advisors

3

D O RC H E S T E R C A P I TA L - OV E RV I E WWith over $1.1 billion of assets under management as of May 2021, Dorchester invests between $1 to $50 million1 in any single fund or asset, and up to $200 million1 in

diversified portfolios of funds or assets, among the following categories:

AN INTEGRATEDAPPROACH TO ALTERNATIVEINVESTMENTS

¹ Through Overflow Funds, Dorchester periodically invests in transactions in excess of $50 million for single assets or $200 million for diversified portfolios

S E C O N D A R I E S& G P S O L U T I O N S

Secondary LP investments and fund restructuring solutions in Hedge, Private Credit, Private Equity,

Tail-end, Co-investments, and other Alternative Investment Funds

O P P O R T U N I S T I CD I R E C T

I N V E S T M E N T SOpportunistic Direct Investments in Credit, and

Credit-like Special Situations

D I R E C TL E N D I N GBespoke financing solutions for Funds, General Partners, Limited Partners, and Corporates

P R I M A R YI N V E S T M E N T SPrimary investments in Hedge, Private Credit, and Private Equity Funds, including SMAs, Co-investments, Syndications and other Alternative Investment Funds

4

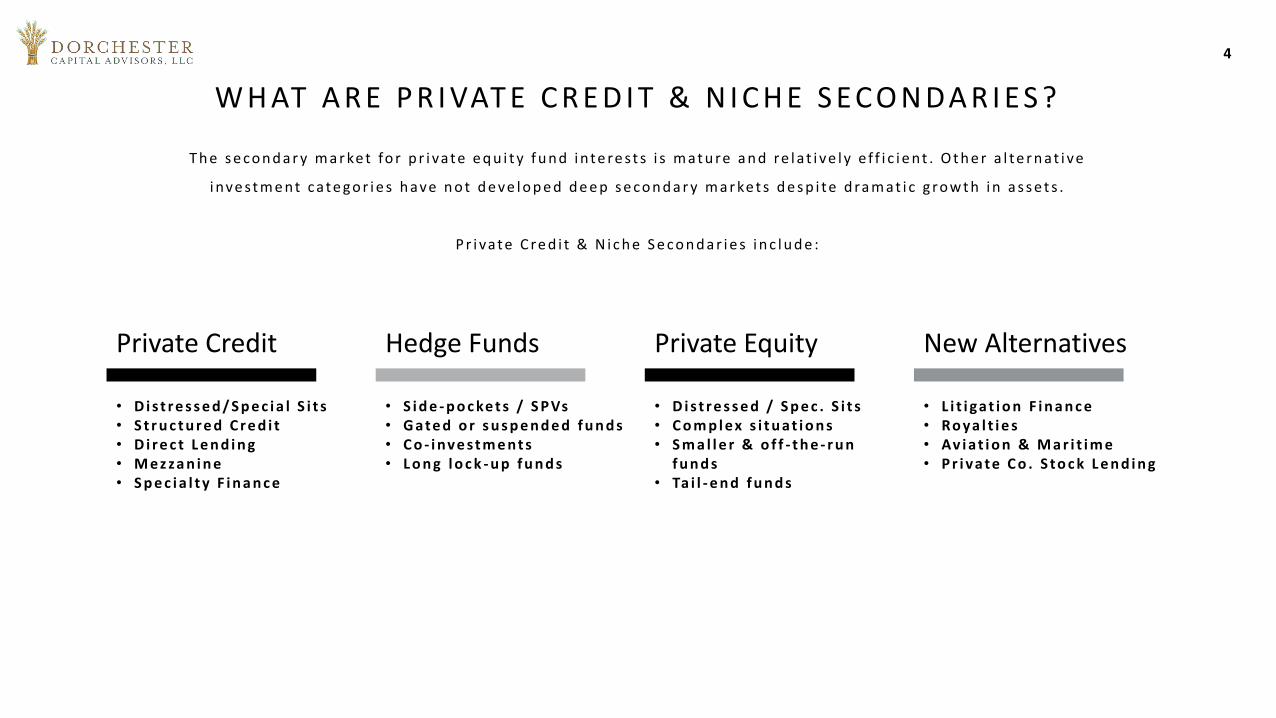

• D i s t r e s s e d / S p e c i a l S i t s• S t r u c t u r e d C r e d i t• D i re c t L e n d i n g• M e z za n i n e• S p e c i a l t y F i n a n c e

Private Credit

• S i d e - p o c ke t s / S P Vs• G a te d o r s u s p e n d e d f u n d s• C o - i nv e s t m e nt s• L o n g l o c k - u p f u n d s

Hedge Funds

• D i s t r e s s e d / S p e c . S i t s• C o m p l ex s i t u a t i o n s• S m a l l e r & o f f - t h e - r u n

f u n d s• Ta i l - e n d f u n d s

Private Equity

• L i t i ga t i o n F i n a n c e• Ro ya l t i e s• Av i a t i o n & M a r i t i m e• P r i va te C o . S to c k L e n d i n g

New Alternatives

W H AT A R E P R I VAT E C R E D I T & N I C H E S ECO N DA R I E S ?

T h e s e c o n d a r y m a r ke t fo r p r i va te e q u i t y f u n d i n te re st s i s m a t u re a n d re l a t i ve l y e f f i c i e nt . O t h e r a l te r n a t i ve

i nve st m e n t c a t e g o r i e s h ave n o t d e ve l o p e d d e e p s e c o n d a r y m a r ke t s d e s p i t e d ra m a t i c g ro w t h i n a s s e t s .

P r i va t e C re d i t & N i c h e S e c o n d a r i e s i n c l u d e :

5

I N V E S TO RS E XC H A N G E L I Q U I D I T Y F O R Y I E L D

I nve st o rs s e a rc h i n g fo r h i g h e r y i e l d s a re g rav i ta t i n g t o w a rd s l o n ge r d u ra t i o n , l e s s l i q u i d a l t e r n a t i ve s w i t h p o t e n t i a l l y g re a t e r r i s k l i ke

P r i va t e Eq u i t y a n d P r i va t e C re d i t , w h i c h c a n a l s o u s e l e ve ra ge t o e n h a n c e re t u r n s a n d w h o s e re s u l t s m ay n o t b e k n o w n fo r s o m e t i m e

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000Private Markets AUM ($ billions)Natural Resources

Private Debt

Infrastructure

Real Estate

Private Equity

Source: Preqin

6

Organizational priorities, CIOs, board members, Investment Policy

Statements, fundamental views on the markets, return expectations, and

GP & consultant relationships may change over time, necessitating re-

evaluation of portfolio holdings, especially small and unintended assets.

Investors are increasingly turning to the secondary market as a portfolio

management tool to respond to changes.

The secondary market for private equity investors is mature but has only

recently developed for private credit and niche alternatives.

As noted on chart on the right, more and more CIOs are reaching their

expected tenure leading to future CIO staff (and subsequent portfolio)

turnover 0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

5

10

15

20

25

30

35

5 10 15 20 More

% o

f To

p 1

00

CIO

s

Nu

mb

er o

f C

IOs

CIO Tenure in Years

Top 100 Asset Managers

Length of CIO Tenure

Source: AI-CIO Magazine

“ W H E N T H E FA C T S C H A N G E , I C H A N G E M Y M I N D ”-John Maynard Keynes

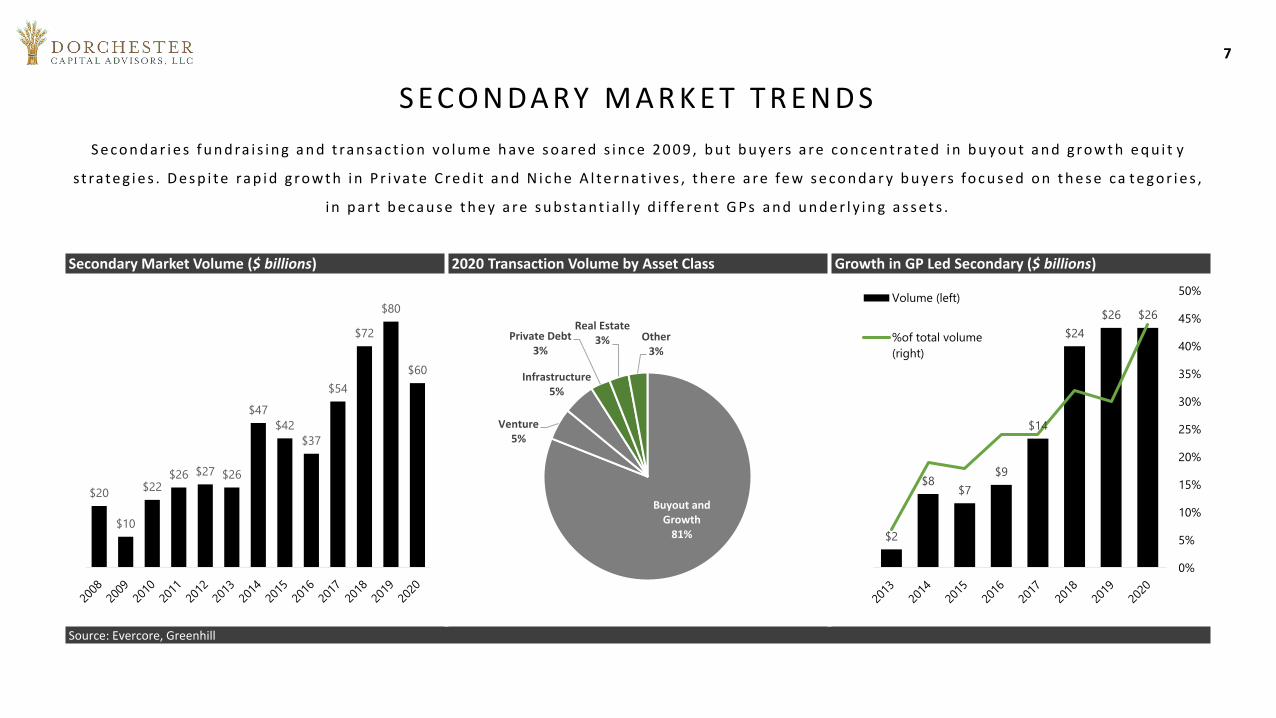

7

Secondary Market Volume ($ billions) 2020 Transaction Volume by Asset Class Growth in GP Led Secondary ($ billions)

Source: Evercore, Greenhill

S ECO N DA RY M A R K E T T R E N D S

S e c o n d a r i e s f u n d ra i s i n g a n d t ra n s a c t i o n vo l u m e h ave s o a re d s i n c e 2 0 0 9 , b u t b u y e rs a re c o n c e n t ra t e d i n b u y o u t a n d g ro w t h e q u i t y

s t ra t e g i e s . D e s p i t e ra p i d g ro w t h i n P r i va t e C re d i t a n d N i c h e A l t e r n a t i ve s , t h e re a re fe w s e c o n d a r y b u ye rs fo c u s e d o n t h e s e c a t e g o r i e s ,

i n p a r t b e c a u s e t h e y a re s u b st a n t i a l l y d i f fe re nt G Ps a n d u n d e r l y i n g a s s e t s .

$20

$10

$22$26 $27 $26

$47

$42

$37

$54

$72

$80

$60

$2

$8$7

$9

$14

$24

$26 $26

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%Volume (left)

%of total volume

(right)

Buyout and Growth

81%

Venture5%

Infrastructure5%

Private Debt3%

Real Estate3% Other

3%

8

D RY P O W D E R I S CO N C E N T R AT E D I N P R I VAT E EQ U I T Y S ECO N DA R I E S

Secondary Market Dry Powder (12/31/20, $b) Secondary Market Dry Powder – Split by Asset Class Secondary Market Fundraising – Split by Asset Class

Source: Evercore

E i g h t m e ga - f u n d s a c c o u n t fo r 5 0 % o f t h e d r y p o w d e r o f s e c o n d a r y b u ye rs , w h i c h d r i ve s t h e m a r ke t ’s fo c u s o n l a rge p o r t fo l i o a n d G P

l e d t ra n s a c t i o n s i n p r i va t e e q u i t y. M o st s e c o n d a r y f u n d s ’ c u r re n t a n d p l a n n e d d e p l o y m e n t s a re c o n c e n t ra t e d i n h i g h l y t ra n s p a r e nt

L B O a n d g ro w t h e q u i t y f u n d s ( 8 6 % o f vo l u m e ) . S m a l l e r, m o re o f f - t h e - r u n , a n d l e s s t ra n s p a re nt s t ra t e g i e s o r m a n a ge rs a re e s c h e w e d

b y l a rge r p l ay e rs .

Top 8

Buyers,

50%

Top 19

Buyers,

25%

Top 34

Buyers, 15%

10%

$113 billion

Broader PE

76%

Infrastructure

8%

Real Estate

2%

Preferred

Equity

9%

Other

5%

Broader PE

86%

Infrastructure

6%

Real Estate

4%

Preferred

Equity

3%

Other

1%

Top 19 buyers are 75% of dry

powder for secondaries

9

UNIQUE UNDERWRITING CHALLENGESU n d e r w r i t i n g p r i va t e c re d i t a n d n i c h e s e c o n d a r i e s t a ke s u n c o m m o n ex p e r t i s e .

R E L AT I O N S H I P S

Effective buyers have

existing relationships with

general partners in private

credit and other strategies.

By mandate and experience,

most PE secondary funds

lack this network.

F U N DA M E N TA L S

Credit and Niche

Secondaries require

fundamental, bottom-up

analysis and the ability to

solve for complex situations.

T R A N S PA R E N C Y

Credit and Niche Secondaries

frequently lack transparency PE

secondary buyers are

accustomed to having.

Effective buyers can overcome

this through pre-existing GP

relationships and knowledge.

C O M P L E X I T Y

Niche Secondaries

sometimes involve complex

issues, such as esoteric

investment strategies,

structures, legal issues, or

counterparty considerations.

M A N DAT E

Many secondary buyers

cannot buy Credit and Niche

Secondaries due to

restrictive mandates or

Investment Policy

Statements.

10

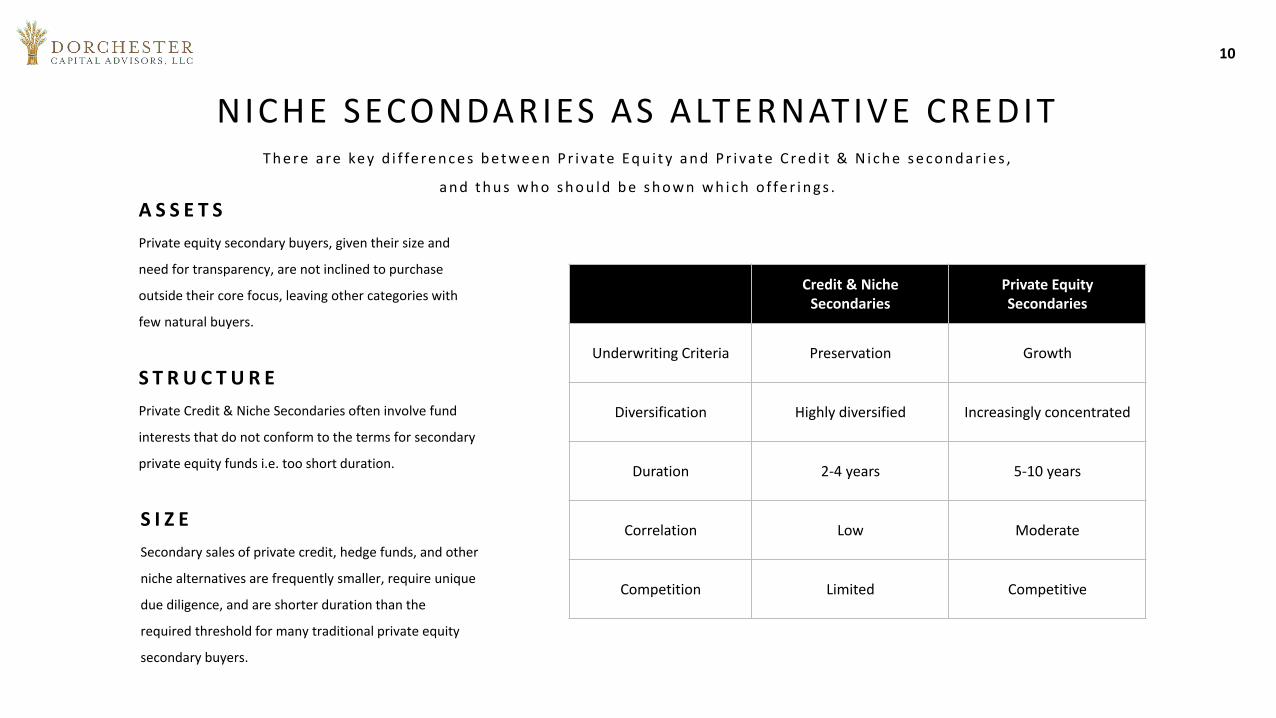

NICHE SECONDARIES AS ALTERNATIVE CREDIT

Credit & NicheSecondaries

Private EquitySecondaries

Underwriting Criteria Preservation Growth

Diversification Highly diversified Increasingly concentrated

Duration 2-4 years 5-10 years

Correlation Low Moderate

Competition Limited Competitive

T h e re a re ke y d i f fe re n c e s b e t w e e n P r i va t e Eq u i t y a n d P r i va t e C re d i t & N i c h e s e c o n d a r i e s ,

a n d t h u s w h o s h o u l d b e s h o w n w h i c h o f fe r i n g s .

Private equity secondary buyers, given their size and

need for transparency, are not inclined to purchase

outside their core focus, leaving other categories with

few natural buyers.

A S S E T S

Private Credit & Niche Secondaries often involve fund

interests that do not conform to the terms for secondary

private equity funds i.e. too short duration.

S T R U C T U R E

Secondary sales of private credit, hedge funds, and other

niche alternatives are frequently smaller, require unique

due diligence, and are shorter duration than the

required threshold for many traditional private equity

secondary buyers.

S I Z E

11

A private pension sought liquidity on a $200+ million portfolio consisting of more than 25 fund interests, $25 million of which were credit strategies. Outperformance in the

seller’s broader private equity portfolio provided “cushion” to accept a discount, especially with a timely sale by quarter-end.

Distressed Debt 156%

Mezzanine 117%

Distressed Debt 212%

Distressed Debt 312%

Distressed Debt 42%

Mezzanine 21%

CASE STUDY: PROJECT S ILVER

$25m subset of $200m+ portfolio

Dorchester overcame limited transparency

through its pre-existing relationship with 4 of

the 5 credit and niche GPs in the portfolio, and

independent knowledge of major underlying

positions.

T R A N S P A R E N C Y

Dorchester is one of only two approved

buyers of the largest position, Distressed

Debt 1, thereby reducing execution risk

for the seller1.

A P P R O V E D B U Y E R

Dorchester developed a constructive view and

identified overlooked sources of value due to

knowledge of the managers, underlying

positions, and fundamental credit underwriting

expertise.

C R E D I T E X P E R T I S E

Dorchester bid jointly with traditional PE

secondary buyers, who did not have the

due diligence expertise to buy the niche

and credit assets. Dorchester’s specialist

nature resulted in better overall pricing

and execution.

H O L I S T I C S O L U T I O N

Dorchester’s Advantage

Transaction Summary

1. Private Credit and Hedge Funds do not typically want to devote time to provide necessary transparency for secondary transfers, so they limit sales to pre-approved buyers

Please see Disclaimer on the cover page of this presentation

12

Dorchester is happy to work with prospective sellers on how best to position their portfolios

for a secondary market process. Dorchester provides liquidity solutions to Limited and

General Partners of Private Credit, Hedge Funds, Private Equity, and other Alternative

Investment Funds. Dorchester is willing to work with opaque, illiquid, overlooked,

complicated, or time constrained situations.

Whether buying illiquid LP Interests or restructuring an entire fund, Dorchester is a trusted

partner that can craft solutions to meet your specific needs and overcome constraints to

achieve your desired outcomes.

Please contact Sophie Gioanni, Rob Johnson, or Jason Gabrielli for additional information.

Addit ional Information

Robert Johnson

t: +1 (310) 402-5081

m: +1 (773) 358-0861

Jason Gabrielli

t: +1 (310) 402-5084

m: +1 (213) 422-7524

Dorchester Capital Advisors LLC | 11111 Santa Monica Blvd, Suite 1250, Los Angeles CA | www.dorchestercapital.com

Sophie Gioanni

t: +44 203 637 6341

m: +44 7923 246 376