presentation of swedbank's year-end report 2012

DESCRIPTION

Swedbank presents its Year-End results for 2012.TRANSCRIPT

Swedbank’s year-end 2012 results Michael Wolf, CEO Göran Bronner, CFO Håkan Berg, CRO

Stable development

2

Retail

SEKm Q2 Q3 Q4 Q/Q

Net interest income 3 404 3 447 3 407 -40

Net commissions 1 248 1 269 1 320 +51

Total income 5 138 5 209 5 107 -102

Total expenses 2 345 2 357 2 432 +75

Profit before

impairments 2 793 2 852 2 675 -177

Credit impairments 100 69 102 +33

• Deposit margins pressure

• Repricing lending

• Increased sales of funds

support commissions

• Solid asset quality ROE, % 24.6 24.4 26.2

C/I ratio 0.46 0.45 0.48

Improved profitability

• Continued growth in Large

Corporates NII

• High activity debt capital

markets and corporate

finance (Norway)

• Equities continue to be slow

• Credit impairment – one large

exposure

3

Large Corporates & Institutions

SEKm Q2 Q3 Q4 Q/Q

Net interest income 825 852 824 -28

- of which LC/FI* 666 689 729 +40

Net commissions 346 379 443 +64

Net gains and

losses 316 341 412 +71

Total income 1 499 1 581 1 703 +122

Expenses excl.

variable staff costs 602 638 612 -26

Variable staff costs 118 66 71 +5

Profit before

Impairments 779 877 1 020 +143

Credit impairments 54 -35 152 +187

* Large Corporates/Financial Institutions

ROE, % 9.8 14.2 17.5

C/I 0.48 0.45 0.40

Slow banking environment

• Lower Euribor affected NII

• Small lending growth in EUR

• One-off in Lithuania SEK -35m

affecting commissions

• Seasonally higher expenses

• Recoveries continued

• Further efficiency focus needed

4

Baltic Banking

SEKm Q2 Q3 Q4 Q/Q

Net interest income 870 755 761 +6

Net commissions 378 360 351 -9

Total income 1 430 1 273 1 275 +2

Total expenses 588 553 631 +78

Profit before

impairments 842 720 644 -76

Credit impairments -204 -18 -329 -311

ROE, % 14.8 11.0 13.7

C/I 0.41 0.43 0.49

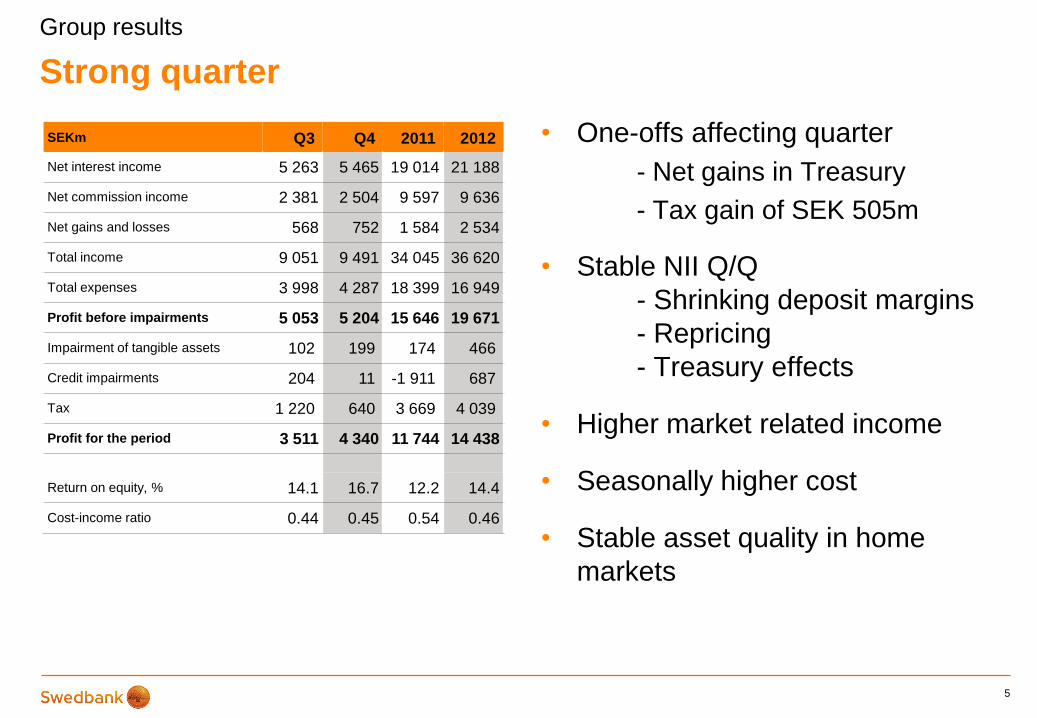

• One-offs affecting quarter

- Net gains in Treasury

- Tax gain of SEK 505m

• Stable NII Q/Q

- Shrinking deposit margins

- Repricing

- Treasury effects

• Higher market related income

• Seasonally higher cost

• Stable asset quality in home

markets

Strong quarter

5

Group results

SEKm Q3 Q4 2011 2012

Net interest income 5 263 5 465 19 014 21 188

Net commission income 2 381 2 504 9 597 9 636

Net gains and losses 568 752 1 584 2 534

Total income 9 051 9 491 34 045 36 620

Total expenses 3 998 4 287 18 399 16 949

Profit before impairments 5 053 5 204 15 646 19 671

Impairment of tangible assets 102 199 174 466

Credit impairments 204 11 -1 911 687

Tax 1 220 640 3 669 4 039

Profit for the period 3 511 4 340 11 744 14 438

Return on equity, % 14.1 16.7 12.2 14.4

Cost-income ratio 0.44 0.45 0.54 0.46

Expenses 2012

Expenses 2013

Focus on customer and efficiency

6

Focus 2013

Customer

service IT

investments

Ektornet Russia &

Ukraine Other

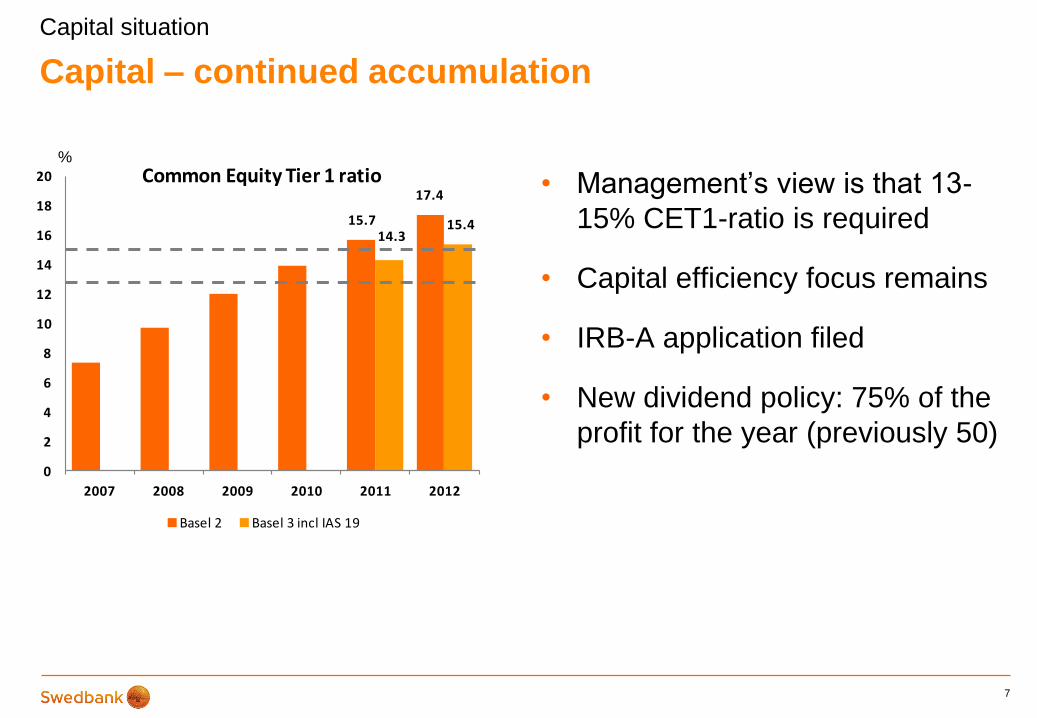

15.7

17.4

14.315.4

0

2

4

6

8

10

12

14

16

18

20

2007 2008 2009 2010 2011 2012

Common Equity Tier 1 ratio

Basel 2 Basel 3 incl IAS 19

Capital – continued accumulation

7

Capital situation

• Management’s view is that 13-

15% CET1-ratio is required

• Capital efficiency focus remains

• IRB-A application filed

• New dividend policy: 75% of the

profit for the year (previously 50)

%

Stable asset quality

8

Risk highlights

• Continued high credit quality in

Sweden

• Net recoveries Baltic Banking

• Exit costs Ukraine continue

Credit impairments

(SEKm) Q3 Q4 2012

Retail 69 102 295

LC&I -35 152 185

Baltic Banking -18 -329 -685

Estonia 2 -242 -343

Latvia 8 86 -124

Lithuania -28 -173 -218

Group Functions &

Other 188 86 892

Russia 28 -30 -43

Ukraine 140 117 915

Other 20 -1 20

Swedbank Group 204 11 687

31.7

14.0

0

5

10

15

20

25

30

35

Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12

SEK bnImpaired loans

0

5 000 000

10 000 000

15 000 000

20 000 000

25 000 000

Jan 2010 Jan 2011 Jan 2012Internetbank Mobilebank Telephonebank Branches

High ambition to make it easy for our customers

9

Digital channels

+150% Y/Y

Mobile Bank Sweden: log-ins per month Customer contacts by channel 2012

68% (83%)

5%

(7%)

26% (9%)

2%

Dec 2012

Q&A

Appendix

11

Improved profitability

12

Large Corporates & Institutions

SEKm Q4 11* Q1 12 Q2 12 Q3 12 Q4 12

Net interest income 845 887 825 852 824

of which LC & FI** 563 652 666 689 729

of which Markets 282 235 159 163 95

Commission income 269 434 346 379 443

of which LC & FI* * 261 278 278 311 290

of which Markets 6 156 68 68 153

Total income LC&I 1 328 1 980 1 499 1 581 1 703

of which LC & FI** 832 946 947 1 008 1 030

of which Markets 496 1 034 552 573 673

Total expenses, excl

variable pay 818 607 602 638 612

Variable staff costs 13 106 118 66 71

Profit before

impairments 497 1 267 779 877 1 020

of which LC & FI** 574 735 740 757 792

of which Markets -77 532 39 120 228

Total impairments 21 14 58 -35 152

C/I ratio 0.63 0.36 0.48 0.45 0.40

* Excluding Lehman one-off ,**Large corporates and Financial institutions

Strong execution on costs 2012

• Staff costs -847m and consultancy costs -241m year on year

13

Cost performance

Cost trend (SEKm) FY 2011 FY 2012 YTD

Total expenses 18 399 16 949 -1 450

Variable staff costs -395 -738

Compensation to savings banks -530 -622

Restructuring cost -430 -2

FX effects -87

Underlying cost 16 957 15 587 -1 370

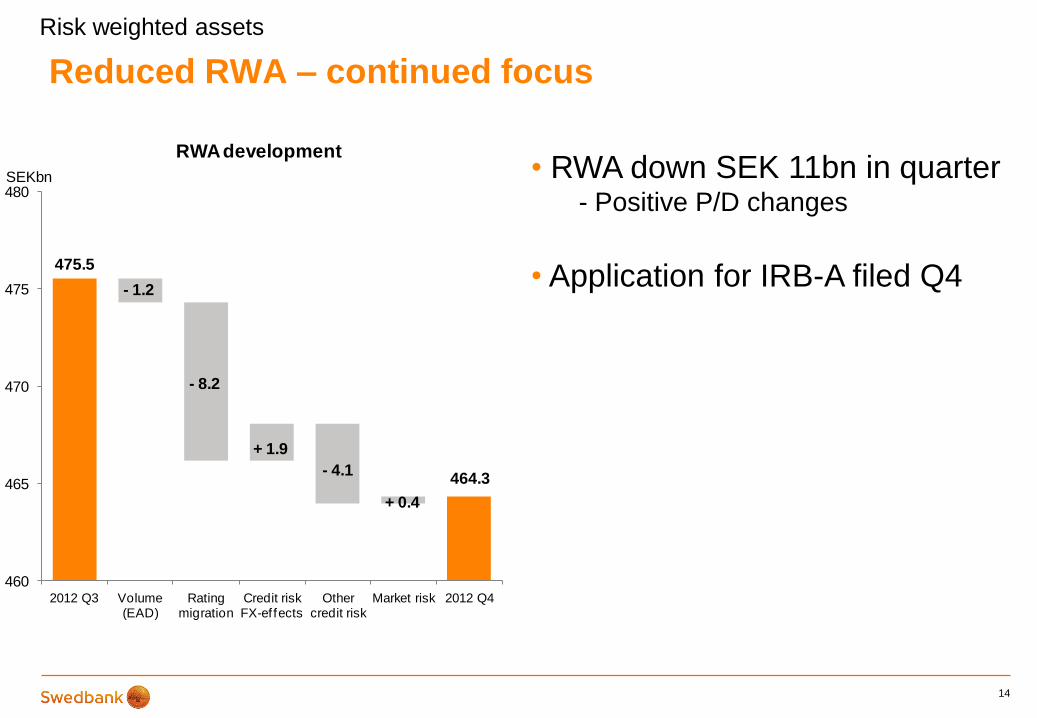

Reduced RWA – continued focus

14

Risk weighted assets

• RWA down SEK 11bn in quarter - Positive P/D changes

• Application for IRB-A filed Q4

464.3

- 1.2

- 8.2

+ 1.9

- 4.1

+ 0.4

475.5

460

465

470

475

480

2012 Q3 Volume (EAD)

Rating migration

Credit risk FX-ef fects

Other credit risk

Market risk 2012 Q4

SEKbn

RWA development

0

200

400

600

800

1 000

1 200

1 400

Q4 2012

0

200

400

600

800

1 000

1 200

1 400

Q4 2012

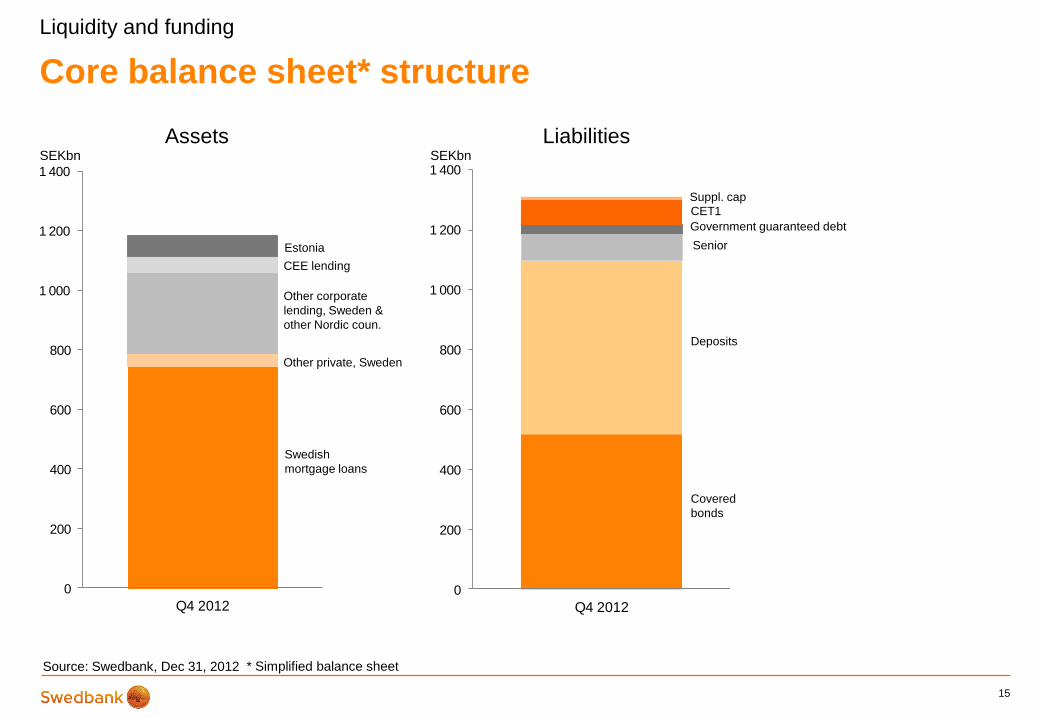

Core balance sheet* structure

15

Liquidity and funding

CEE lending

Estonia

Other corporate

lending, Sweden &

other Nordic coun.

Other private, Sweden

Swedish

mortgage loans

Senior

Covered

bonds

Deposits

CET1

Suppl. cap

Government guaranteed debt

Source: Swedbank, Dec 31, 2012

Assets Liabilities SEKbn SEKbn

* Simplified balance sheet

0

20

40

60

80

100

120

Covered bonds Senior unsecured

Lower funding needs

• LCR139% (Swedish FSA definition FFFS 2012:6)

• NSFR 91%

• Expanded investor base

16

Liquidity and funding

Term funding issuance – completed and planned

SEKbn

0

5 000

10 000

15 000

20 000

25 000

30 000

Domestic CB

Euro CB USD CB (144A)

Other CB Senior unsecured

Q1 12

Q2 12

Q3 12

Q4 12

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

Domestic CP

ECP/CD USCP Yankee CD French CD Finnish CD

Q1 12

Q2 12

Q3 12

Q4 12

Conservative funding plan

17

Long-term debt issued

• Issued SEK 142bn of term-funding FY 2012, maturities of SEK 86bn

• Term funding plan in 2013 of SEK 120bn, maturities of SEK 86bn

Liquidity and funding

Outstanding short-term debt SEKm SEKm

Source: Swedbank, Dec 31, 2012, nominal amounts

0

50

100

150

200

2013 2014 2015 2016 2017 2018-

Government guaranteed debt

Senior unsecured debt

Covered bonds

18

Long-term funding maturity profile

• FY 2013 maturities amount to nominal SEK 86bn

18

Long-term funding maturity profile

Source: Swedbank Dec 31, 2012

Liquidity and funding

SEKbn

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

0% -5% -10% -15% -20% -25% -30% -35% -40% -45% -50%

OC, Q412

0

20

40

60

2013 2014 2015 2016 2017 2018-

Senior unsecured debt

Senior unsecured debt strategy

19

Source: Swedbank, Dec 31, 2012, nominal amounts

• Limited need given Swedbank’s balance sheet structure

• Secure OC

• Fund liquidity reserves

Senior unsecured debt maturity profile

SEKbn

Over-

colla

tera

lisation

House price drop

House price sensitivity of the cover pool

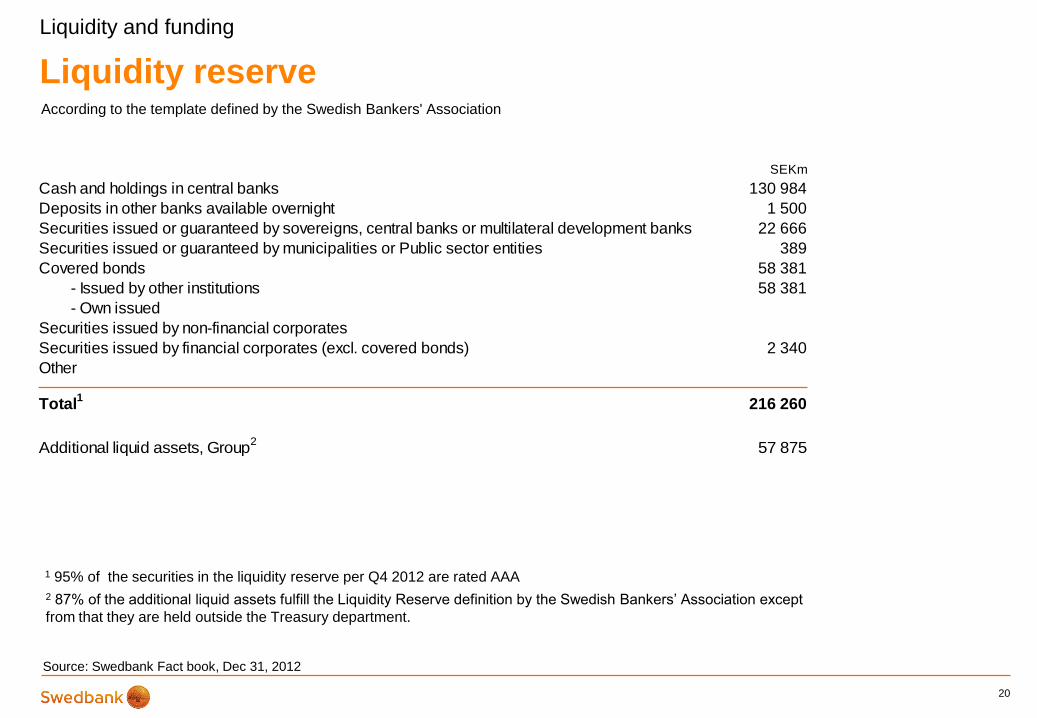

Liquidity and funding

SEKm

Cash and holdings in central banks 130 984

Deposits in other banks available overnight 1 500

Securities issued or guaranteed by sovereigns, central banks or multilateral development banks 22 666

Securities issued or guaranteed by municipalities or Public sector entities 389

Covered bonds 58 381

- Issued by other institutions 58 381

- Own issued

Securities issued by non-financial corporates

Securities issued by financial corporates (excl. covered bonds) 2 340

Other

Total1

216 260

Liquidity reserve

20

1 95% of the securities in the liquidity reserve per Q4 2012 are rated AAA

According to the template defined by the Swedish Bankers' Association

2 87% of the additional liquid assets fulfill the Liquidity Reserve definition by the Swedish Bankers’ Association except

from that they are held outside the Treasury department.

Liquidity and funding

Source: Swedbank Fact book, Dec 31, 2012

Additional liquid assets, Group2

57 875

Prolonged survival horizon*

21

Liquidity and funding

0

50

100

150

200

250

300

0 20 40 60 80 100 120 140 160 180 200 220 240 260 280 300 320 340 360Days forward

365

SEKbn

Source: Swedbank Dec 31, 2012

* For definition see Swedbank factbook

0

50

100

150

200

250

300

350

400

Next 12-month term funding maturities

CP / CDs and net interbank funding,

SEKm

0

50

100

150

200

250

300

350

400

Additional pledgeable and/or liquid assets

Liquidity reserve, securities

Liquidity reserve, central bank deposits,

SEKm

Conservative liquidity levels

• Short-term funding mainly a tool for cash management

• More than 12 months pre-funded

22

SEKbn

Source: Swedbank Dec 31, 2012

Liquidity and funding

1 As defined by the Swedish Bankers’ Association

1

1

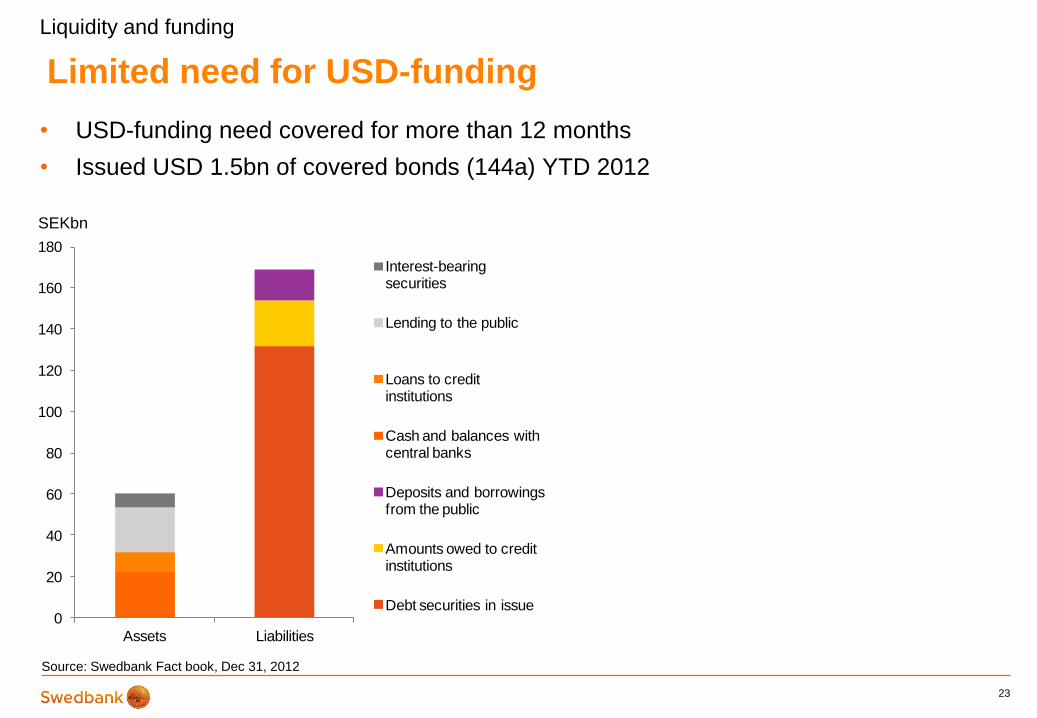

Limited need for USD-funding

23

SEKbn

• USD-funding need covered for more than 12 months

• Issued USD 1.5bn of covered bonds (144a) YTD 2012

Source: Swedbank Fact book, Dec 31, 2012

Liquidity and funding

0

20

40

60

80

100

120

140

160

180

Assets Liabilities

Interest-bearing securities

Lending to the public

Loans to credit institutions

Cash and balances with central banks

Deposits and borrowings from the public

Amounts owed to credit institutions

Debt securities in issue

0

20

40

2013 2014

JPY

CHF

USD

SEK

EUR

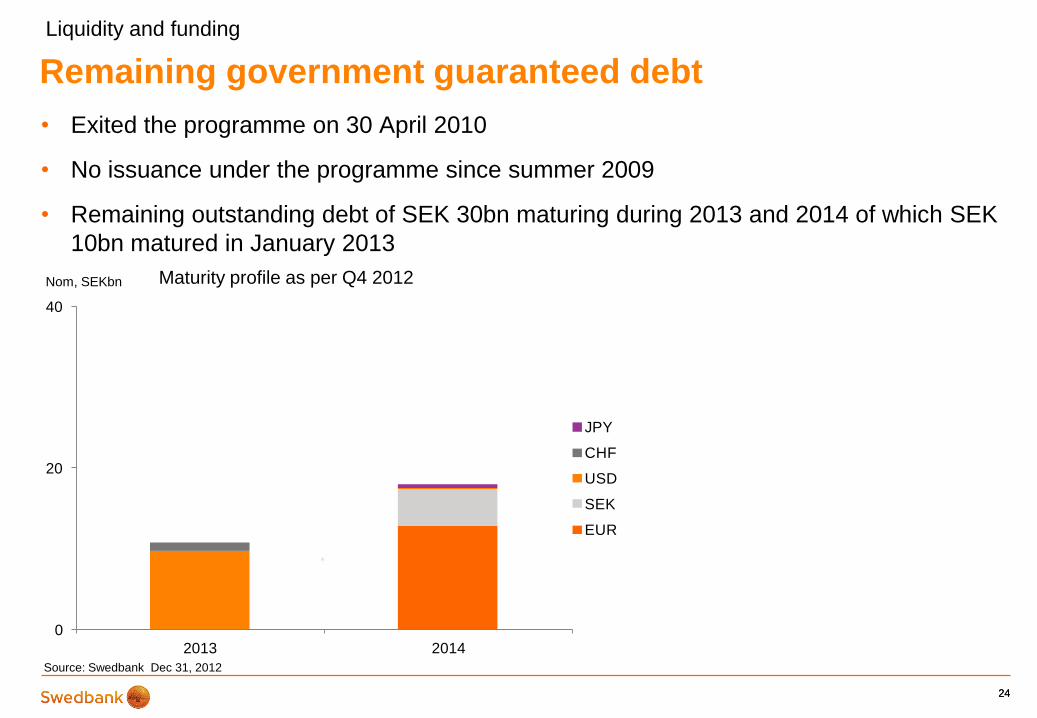

24

Remaining government guaranteed debt

• Exited the programme on 30 April 2010

• No issuance under the programme since summer 2009

• Remaining outstanding debt of SEK 30bn maturing during 2013 and 2014 of which SEK

10bn matured in January 2013

24

Maturity profile as per Q4 2012

Source: Swedbank Dec 31, 2012

Liquidity and funding

Nom, SEKbn

Asset encumbrance

25

Liquidity and funding

Source: Swedbank Facts Q4 2012

Distribution by type of liability and asset

SEKm

Government

debt

instruments

Central banks

and

supranational

debt

instruments

Covered

bonds

Debt

instruments

issued by

credit

institutions

Securities

issued by

corporate and

other issuers ABS

Mortgage

loans Cash Total

Central bank funding

Intraday settlement collateral 1) 2 12 369 12 371

Repurchase agreements 2) 12 992 13 496 26 488

Derivative collateral 3) 162 862 14 120 15 144

Covered bonds 4) 516 749 516 749

Accrued interest of assets in

the cover pool 2 330 2 330

Other 5) 366 366

Total 13 156 26 727 519 079 14 486 573 448

Financial assets pledged for insurance policy holders 103 083

Additional assets available for secured funding 6)

SEKm

Government

debt

instruments

Central banks

and

supranational

debt

instruments

Covered

bonds

Debt

instruments

issued by

credit

institutions

Securities

issued by

corporate and

other issuers ABS

Mortgage

loans Cash Total

Securities 7, 8) 26 883 3 265 84 045 11 393 8 203 1 059 134 848

Cover pool over

collateralisation incl. accr.

interest 4) 181 828 181 828

Cover pool eligible assets 9) 11 608 11 608

Total 26 883 3 265 84 045 11 393 8 203 1 059 193 436 328 284

1) Pledged securities on balance sheet.

2) Repoed securities on balance sheet.

3) Collateral posted under CSA agreements, gross (3-year, SEKm, High: 21 572,

Low : 10 945, Average: 13 644).

4) Nominal amount excluding accrued interest.

5) Collateral pledged in securities lending activities and w ith exchanges

6) Assets not currently encumbered.

7) Reversed repos are included.

8) All type of securities, including securities non pledgeable at central banks, of

w hich 82% are rated AAA, 2% are rated below A- and 8% are not rated.

9) Type of loans; Residential 84.4%, Forestry & Agriculture 15.3%, Commercial

0.3%.

Swedish mortgage market

• No securitization (on balance sheet), no sub-prime market, no 3rd party origination, no buy-to-let

market

• 70% home ownership1

• Rental market is regulated

• Transparent credit information (credit information agency, www.uc.se)

– Publicly available information regarding income, debt, payment track record etc

• Consumer credit legislation requires affordability calculations including stress test of higher interest

rate

• Very limited debt forgiveness possibilities (full recourse)

• Strong social security and generous unemployment benefit system

26

Swedish housing and mortgage market

1 Source: Boverket, 2011

Real estate prices – Sweden 12 months development

27

Swedish housing and mortgage market

Single-family homes1 Tenant-owner rights2 Combined3

12M Δ

12M Δ

12M Δ

Jan/12 -4% -2% -4%

Feb/12 -4% -1% -3%

Mar/12 -4% 1% -3%

Apr/12 -2% 2% -1%

May/12 -2% 3% -1%

Jun/12 -1% 4% 0%

Jul/12 0% 4% 1%

Aug/12 2% 4% 3%

Sep/12 2% 5% 3%

Oct/12 1% 6% 3%

Nov/12 3% 7% 4%

Dec/12 4% 7% 6%

Source: Valuegard www.valuegard.se (Based on data from Mäklarstatistik), 1 HOXHOUSESWE, 2 HOXFLATSWE, 3 HOXSWE

28

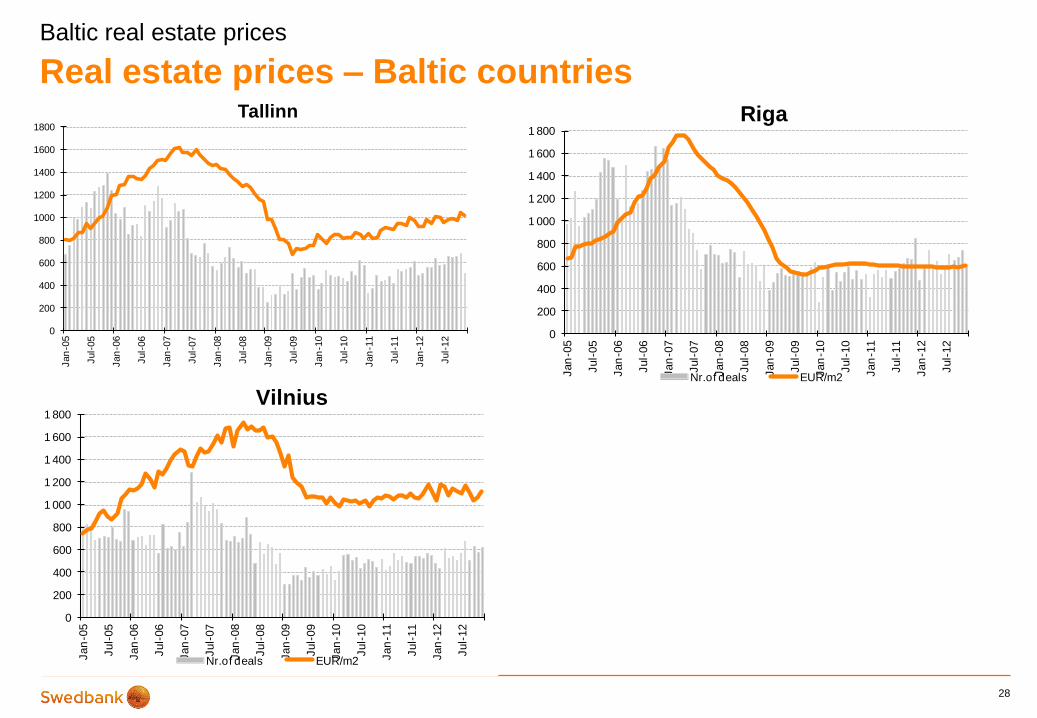

Real estate prices – Baltic countries

Source: Swedbank, Estonian Land Board Source: Swedbank

Baltic real estate prices

0

200

400

600

800

1000

1200

1400

1600

1800

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Tallinn

Nr.of deals EUR/m2

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Riga

Nr.of deals EUR/m2

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Vilnius

Nr.of deals EUR/m2

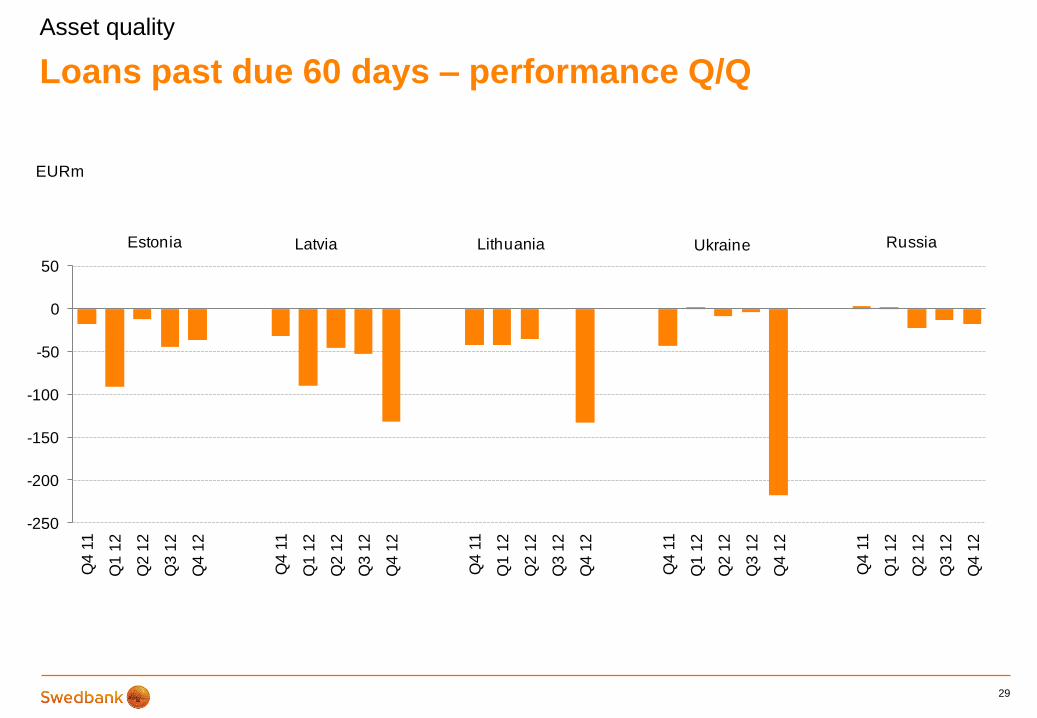

Loans past due 60 days – performance Q/Q

29

Asset quality

-250

-200

-150

-100

-50

0

50

Q4

11

Q1

12

Q2

12

Q3

12

Q4

12

Q4

11

Q1

12

Q2

12

Q3

12

Q4

12

Q4

11

Q1

12

Q2

12

Q3

12

Q4

12

Q4

11

Q1

12

Q2

12

Q3

12

Q4

12

Q4

11

Q1

12

Q2

12

Q3

12

Q4

12

EURm

Estonia Latvia Lithuania RussiaUkraine

Provisions – well provided for

30

Asset quality

Provision ratios, % Q4 12

Retail 75

LC&I 166

Baltic Banking 52

Russia 64

Ukraine 78

Group 62

12 82111 915

10 9519 934

7 077

2 4352 478

2 0401 774

1 545

61.5%65.0% 63.7% 65.2%

61.9%

0

5 000

10 000

15 000

20 000

25 000

Q4 11 Q1 12 Q2 12 Q3 12 Q4 12

SEKm

Individual provisions Portfolio provisions Provision ratio

Corporate Retail portfolio will drive capital efficiency

31

Credit portfolio – Retail

Segments excl. Swedbank

Mortgage and Swedbank Finance

Volume

(SEKbn)

Secured

(%)

Agriculture 6.0 82

Manufacturing 11.3 70

Public sector and utilities 4.7 86

Construction 4.4 85

Retail 8.8 89

Transportation 2.0 78

Shipping 0.1 95

Hotels and restaurants 3.0 90

Information & communication 0.9 49

Finance and insurance 3.3 79

Property management 54.9 96

Professional service 6.7 59

Other 6.4 61

Total 113 86

Total portfolio SEK 231bn

94

24

113

Swedbank Mortgage AB

Leasing (Swedbank

Finance AB)

Other

14

6

4

24 24 26

25 24

0

10

20

30

Q4-11 Q1-12 Q2-12 Q3-12 Q4-12

SEKbn Shipping and Offshore

Offshore Tanker Other

32

Credit portfolio – Large Corporates & Institutions

• Lending exposure to shipping and offshore sector of

SEK 24.2bn plus unutilised commitments of SEK

7.9bn

– Portfolio duration 4-5y

– Average fleet age 7y

– Strong employment profiles

0.4% -3.6%

Shipping and offshore

0 5 10 15 20 25

SEK

EUR

USD

NOK

JPY

Shipping and Offshore Portfolio by Currency

Q4-12

Q3-12

0.5

7.0

1.9

3.6

1.2

1.9

0.2

2.4

0.7

1.2

0.7

1.0

1.7

0 2 4 6 8

Cruise

Drilling & exploration

Oil service

Supply

Accommodation

Floating production

Chemical

Product

Crude oil

Gas (LNG/LPG)

Dry bulk

Container

RORO

Shipping and Offshore Portfolio by Subsegment

Q4-12

Q3-12

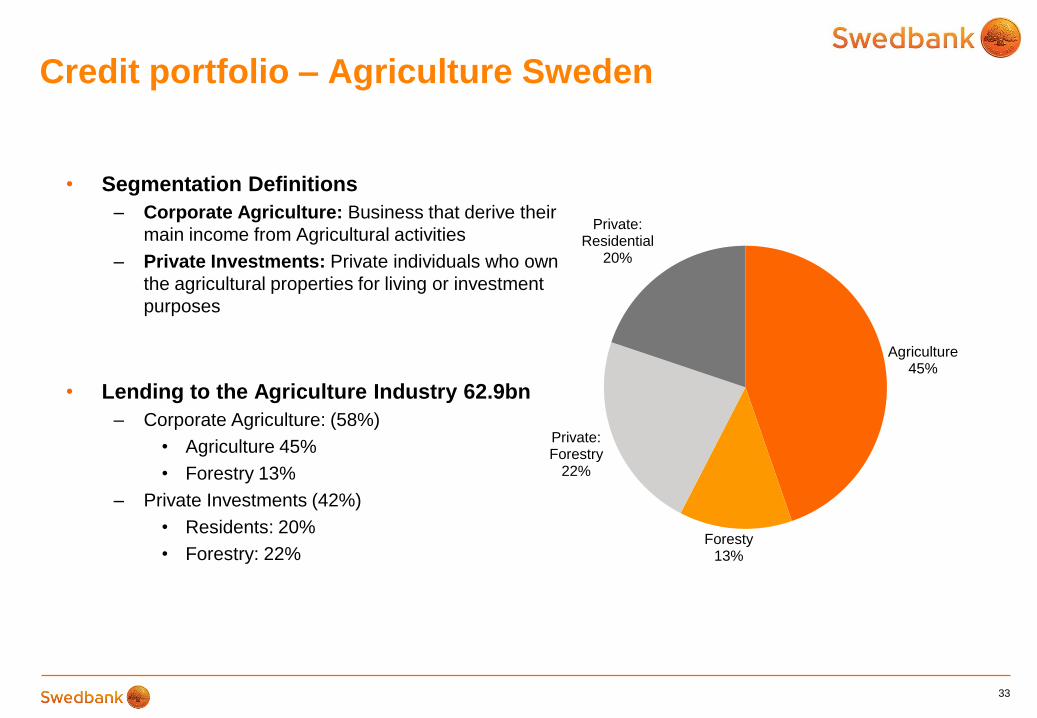

Credit portfolio – Agriculture Sweden

33

• Segmentation Definitions

– Corporate Agriculture: Business that derive their

main income from Agricultural activities

– Private Investments: Private individuals who own

the agricultural properties for living or investment

purposes

• Lending to the Agriculture Industry 62.9bn

– Corporate Agriculture: (58%)

• Agriculture 45%

• Forestry 13%

– Private Investments (42%)

• Residents: 20%

• Forestry: 22%

Agriculture 45%

Foresty 13%

Private: Forestry

22%

Private: Residential

20%

2012 ICAAP Scenario

– Deep recession without recovery

34

• Europe enters into deep

recession

• Limited possibilities for fiscal

stimulus

• European bank runs

• Credit contraction

• Closed funding markets

Triggers Outcome

• Sharp GDP drop with no

recovery (10-15% from 2011

level)

• Severe drop in house prices

(25-37% from 2011 level)

• Depreciated EUR and

appreciated SEK

• Devaluation in Latvia and

Lithuania

ICAAP

High capitalisation even in extremely stressed scenario

• Revenue decrease 31 percent

• Credit impairments SEK 64bn over 5 year

• Scenario effects on Core Tier 1 ratio -165bp

• Well above 12% Core Tier 1 ratio at low point even in extremely

stressed scenario in new regulatory environment

35

ICAAP

55

65

75

85

95

105

2011 2012 2013 2014 2015 2016

Sweden Estonia Latvia Lithuania

2012 ICAAP dcenario

– Deep recession without recovery

36

ICAAP

80

85

90

95

100

105

2011 2012 2013 2014 2015 2016

Sweden Estonia Latvia Lithuania

GDP - Index Real Estate prices - index

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

2011 2012 2013 2014 2015 2016

Euribor Stibor

Interest rates – 3m

0

2

4

6

8

10

12

14

2011 2012 2013 2014 2015 2016

USD/SEK EUR/SEK GBP/SEK

FX scenario

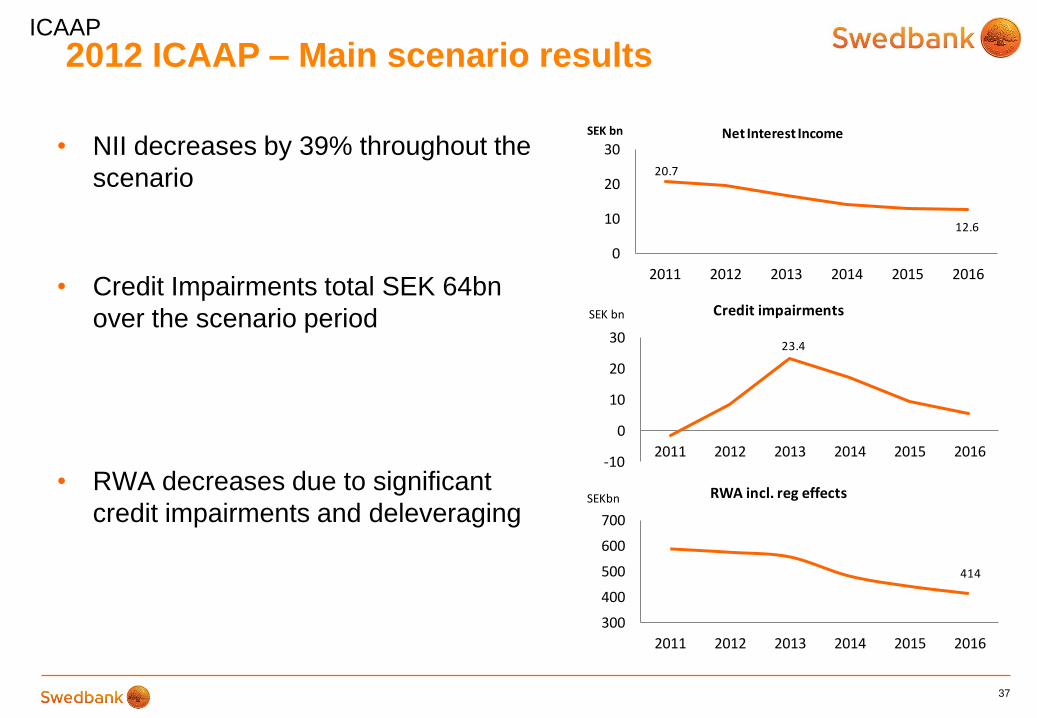

2012 ICAAP – Main scenario results

37

ICAAP

• NII decreases by 39% throughout the

scenario

• Credit Impairments total SEK 64bn

over the scenario period

• RWA decreases due to significant

credit impairments and deleveraging

20.7

12.6

0

10

20

30

2011 2012 2013 2014 2015 2016

SEK bn Net Interest Income

23.4

-10

0

10

20

30

2011 2012 2013 2014 2015 2016

SEK bn Credit impairments

414

300

400

500

600

700

2011 2012 2013 2014 2015 2016

SEKbn RWA incl. reg effects

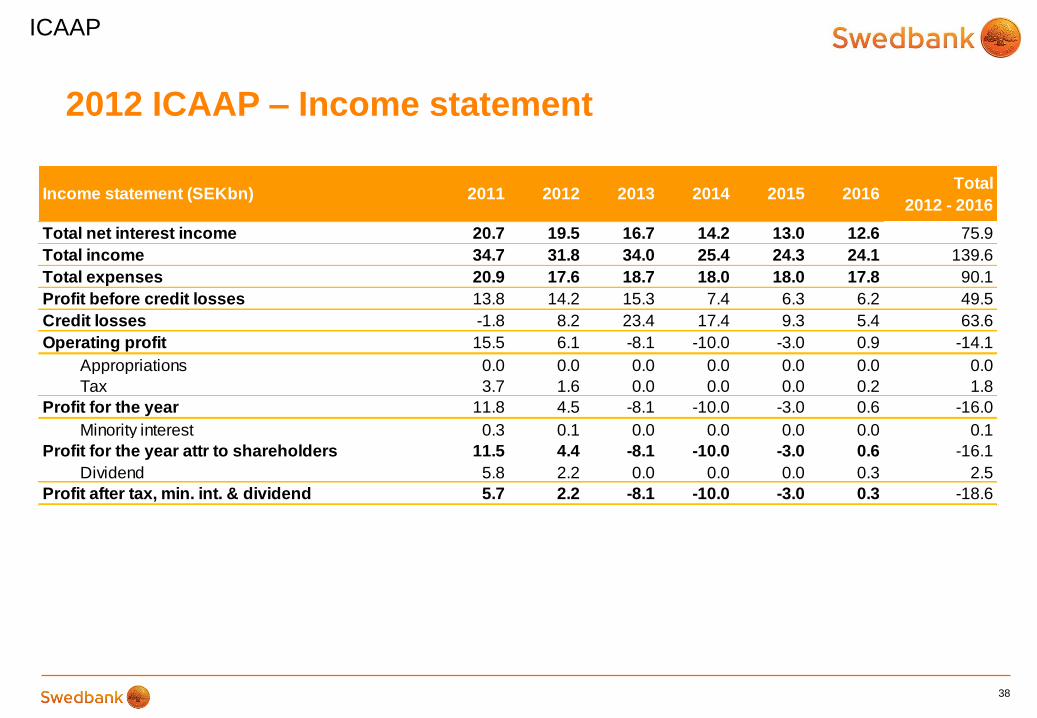

2012 ICAAP – Income statement

38

ICAAP

Income statement (SEKbn) 2011 2012 2013 2014 2015 2016Total

2012 - 2016

Total net interest income 20.7 19.5 16.7 14.2 13.0 12.6 75.9

Total income 34.7 31.8 34.0 25.4 24.3 24.1 139.6

Total expenses 20.9 17.6 18.7 18.0 18.0 17.8 90.1

Profit before credit losses 13.8 14.2 15.3 7.4 6.3 6.2 49.5

Credit losses -1.8 8.2 23.4 17.4 9.3 5.4 63.6

Operating profit 15.5 6.1 -8.1 -10.0 -3.0 0.9 -14.1

Appropriations 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Tax 3.7 1.6 0.0 0.0 0.0 0.2 1.8

Profit for the year 11.8 4.5 -8.1 -10.0 -3.0 0.6 -16.0

Minority interest 0.3 0.1 0.0 0.0 0.0 0.0 0.1

Profit for the year attr to shareholders 11.5 4.4 -8.1 -10.0 -3.0 0.6 -16.1

Dividend 5.8 2.2 0.0 0.0 0.0 0.3 2.5

Profit after tax, min. int. & dividend 5.7 2.2 -8.1 -10.0 -3.0 0.3 -18.6

2012 ICAAP – Credit impairments

39

The accumulated losses constitute SEK 63.6bn.

Credit impairments in LC&I and Retail constitute 74% of total accumulated credit impairments

ICAAP

Credit impairments (%)EAD 2011

(SEKbn) 2012 2013 2014 2015 2016Acc. loss ratio

2012 - 2016

Total 1,384.4 0.6 1.8 1.5 0.9 0.5 4.6

of which LC & I 309.8 0.5 2.3 2.0 0.8 0.6 5.4

Retail 950.8 0.3 1.2 1.0 0.7 0.3 3.2

Estonia 52.5 1.2 2.5 2.2 1.8 1.7 6.6

Latvia 30.6 2.7 6.1 5.6 4.4 4.6 15.0

Lithuania 31.1 2.4 4.1 3.0 2.4 2.2 9.5

Russia & Ukraine 9.6 5.2 20.9 10.5 3.7 1.6 41.9

Credit impairments LC & I and Retail

(%)

EAD 2011

(SEKbn) 2012 2013 2014 2015 2016Acc. loss ratio

2012 - 2016

Agriculture, forestry and fishing 25.8 0.5 1.4 1.3 1.0 0.2 3.7

Manufacturing 39.3 1.0 2.6 2.5 1.2 0.5 6.7

Public sector and utilities 11.6 0.6 1.8 2.1 1.3 0.4 5.3

Construction 15.1 1.2 3.4 3.4 1.9 0.4 8.5

Retail 22.8 1.3 4.6 5.4 4.0 2.4 14.0

Transportation 8.6 2.1 8.2 5.7 3.4 1.2 16.1

Shipping 31.2 0.4 8.5 6.2 0.6 0.5 14.4

Hotels and restaurants 3.8 2.7 6.3 6.3 3.7 0.7 15.0

Information and communication 5.0 0.6 1.7 1.9 1.0 0.5 4.9

Finance and insurance 20.4 0.3 0.8 1.2 0.6 0.3 2.8

Property management 125.1 0.9 3.9 3.8 2.0 1.0 9.6

Cooperative housing associations 75.4 0.3 1.1 1.2 0.5 0.1 2.8

Other corporate lending 75.5 0.9 1.4 1.2 0.7 0.3 3.9

Professional services 14.9 1.0 2.7 3.2 2.1 0.7 8.0

Bank 128.2 0.5 1.3 1.1 0.9 0.8 3.9

Private 657.8 0.1 0.4 0.3 0.3 0.2 1.2

Total 1,260.5 0.4 1.5 1.3 0.7 0.4 3.7

RWA & Capital (SEKbn) 2011 2012 2013 2014 2015 2016

RWA 492.3 489.5 504.1 433.9 395.2 365.0

RWA inc 15% mortgage riskweight * 565.3 552.2 557.1 482.4 442.6 414.4

RWA inc regulatory effects ** 588.1 575.0 557.1 482.4 442.6 414.4

Core Tier 1 77.3 79.7 62.1 52.4 49.5 49.8

Core Tier 1 inc regulatory effects ** 73.6 76.0 62.1 52.4 49.5 49.8

Total Capital base 93.2 88.3 70.9 61.5 57.2 55.2

Capital assessment (%) 2011 2012 2013 2014 2015 2016

Core Tier 1 ratio 15.7 16.3 12.3 12.1 12.5 13.6

Core Tier 1 ratio inc 15% mortgage riskweight * 13.7 14.4 11.1 10.9 11.2 12.0

Core Tier 1 ratio inc. regulatory effects ** 12.5 13.2 11.1 10.9 11.2 12.0

Total capital ratio inc. 15% mortgage riskweight * 16.5 16.0 12.7 12.7 12.9 13.3

2012 ICAAP Main adverse scenario results

Capital assessment

40

* The effect of a 15% average riskweight on the Swedish Mortgage portfolio

** Includes assessed effects of Basel 3, IAS 19 and changed mortgage risk-weights

ICAAP

The Riksbank's Financial Stability Report 2012:2

41

• Swedbank has the overall strongest capitalisation among

Swedish peers

• Swedbank has the strongest liquidity metrics among Swedish

peers,

• Swedbank is the most reciliant bank in a stressed scenario, only

Swedbank makes a profit every year of the stress

• Swedbank is the transparency leader

All subsequent slides are taken from the

Riksbank’s Financial Stability Report 2012:2

Core Tier 1 capital ratios according to Basel III Percent

0

2

4

6

8

10

12

14

16

18

Handels-banken

Nordea SEB Swedbank

March 2012 June 2012 September 2012

Sources: Bank reports and the Riksbank Chart 1:13

Adjusted Leverage ratio

December 2011, per cent

0 2 4 6 8 10 12

Handelsbanken

Deutsche Bank

Nordea

Danske Bank

Commerzbank

Credit Suisse

DNB

SEB

Swedbank

Raiffeisen

Lloyds

Société Générale

Credit Agricole

UniCredit

BNP Paribas

Barclays

BBVA

Erste Group Bank

St. Chartered

RBS

HSBC

Intesa Sanpaolo

UBS

Sources: Liquidatum and the Riksbank Chart 4:10

Level of loan losses in the main scenario, percent

0.00

0.05

0.10

0.15

0.20

0.25

0.30

Handels-

banken

Nordea SEB Swedbank Totalt

2013 2014 2015

Source: The Riksbank Chart 5:3

CET 1 capital ratio according to Basel III, initially

and in the Riksbank’s stress test Percent

0

2

4

6

8

10

12

14

16

18

12

Q3

13 14 15 12

Q3

13 14 15 12

Q3

13 14 15 12

Q3

13 14 15

Handelsbanken Nordea SEB Swedbank

Sources: Bank reports and the Riksbank Chart 5:9

P&L in the Riksbank stress test

The Riksbank’s short-term liquidity measure Survival period, number of days

0

20

40

60

80

100

120

Handels-banken

Nordea SEB Swedbank

September 2011 December 2011 March 2012 June 2012 September 2012

Sources: Liquidatum and the Riksbank Chart 5:12

The Riksbank’s structural liquidity measure Stable funding in relation to illiquid assets, per cent

0

20

40

60

80

100

120

Handels-banken

Nordea SEB Swedbank

September 2011 December 2011 March 2012 June 2012 September 2012

Sources: Liquidatum and the Riksbank Chart 5:14

The Riksbank's short-term and structural liquidity

measure (European Banks) June 2012

Nordea

SEB

Handelsbanken

Swedbank

0

20

40

60

80

100

120

140

160

180

70 80 90 100 110 120

Sh

ort

-term

liq

uid

ity m

easu

re (

days)

Structural liquidity measure (per cent)

Sources: Liquidatum and the Riksbank Chart 5:17

Transparency, liquidity risk

50

0

1

2

3

4

5

6

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

%

Gross margin Swedbank's funding cost Stibor 3 months Swedish Riksbanks reporate

51

The gross margin should cover:

Cost of liquidity ~0.2%

Administrative costs ~0.3%

Credit impairments ~ 0.03%

Tax (22 % on profit before tax)

Net margin

Mortgage loans, gross margin (3 months)