preparing goverment wide financial statements

TRANSCRIPT

Statement of Activities

Statement of Net Position

June 2015

Statement of Activities

Statement of Net Position

June 2015

GOVERNMENT WIDEFINANCIAL STATEMENTS

Accrual

ERMA

GOVERNMENT WIDEFINANCIAL STATEMENTS

Accrual

ERMA Government wide financialstatements are prepared on

the economic resourcesmeasurement focus and the

accrual basis ofaccounting.

RECONCILE

RECONCILEReconciliations are required to show how yougot from the governmental statements to thegovernment wide statements. • You need one reconciliation that shows howyou got from fund balance to net position(equivalent of a balance sheet reconciliation).• You need another reconciliation to go fromthe change in fund balance to change in netposition (equivalent of an income statementreconciliation).

GOVERNMENTAL

GOVERNMENT-WIDE

FIXED ASSETSL/T DEBTDEFERRED REVACCRUALSINTERFUNDTRANSFERS

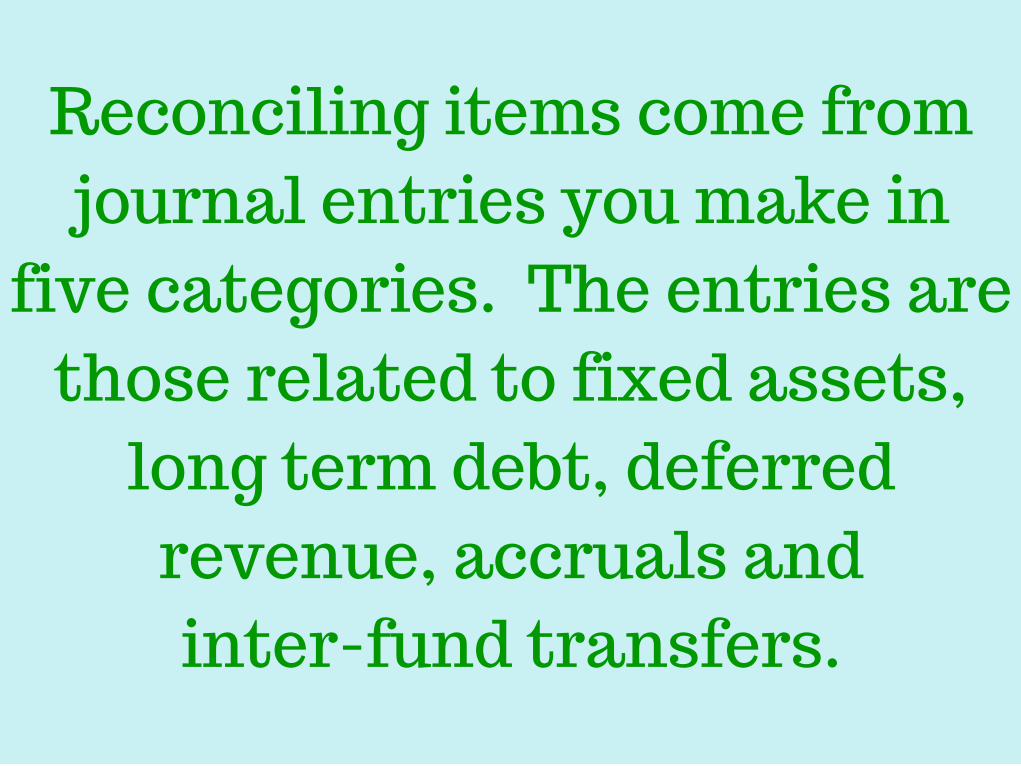

Reconciling items come fromjournal entries you make in

five categories. The entries arethose related to fixed assets,

long term debt, deferredrevenue, accruals andinter-fund transfers.

FIXED ASSETSBEGINNINGEXPENDITURESSALESDEPRECIATION

FIXED ASSETSBEGINNINGEXPENDITURESSALESDEPRECIATION

There are four things to do with fixedassets. Remember that governmentalfunds do not record fixed assets. Therefore, you have to:1. Record the beginning of year balances2. Zero the governmental fundexpenditures account and move thebalance to fixed assets3. Properly reflect the gain or loss on salesof fixed assets4. Record depreciation

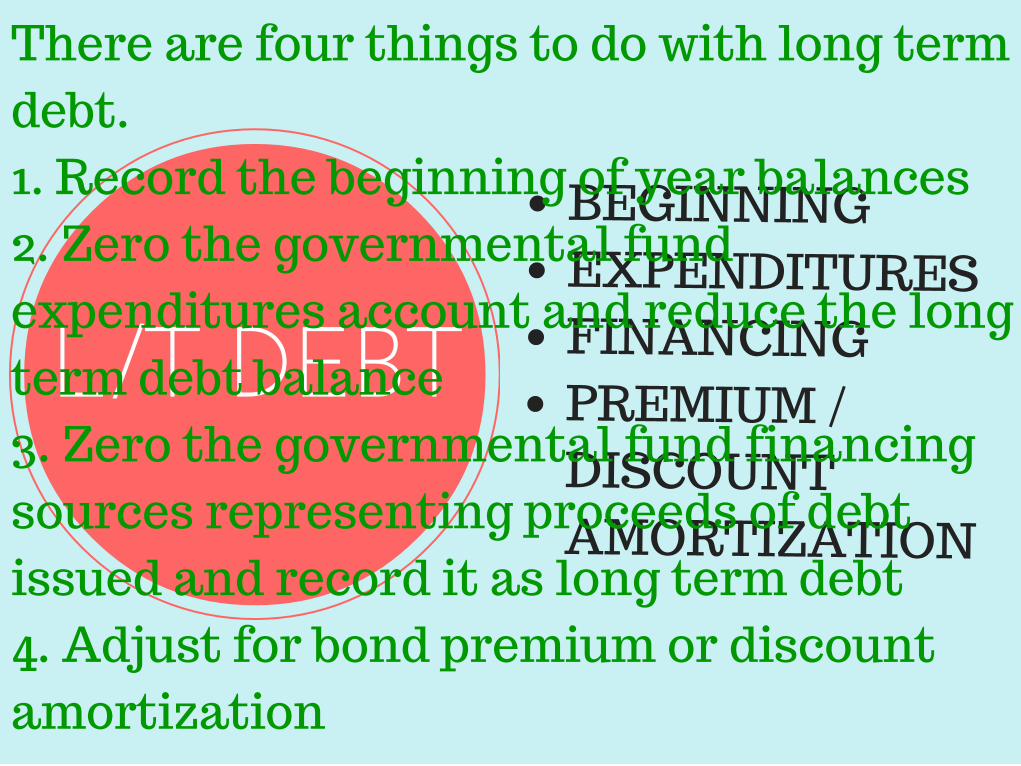

L/T DEBT

BEGINNINGEXPENDITURESFINANCINGPREMIUM /DISCOUNTAMORTIZATION

L/T DEBT

BEGINNINGEXPENDITURESFINANCINGPREMIUM /DISCOUNTAMORTIZATION

There are four things to do with long termdebt. 1. Record the beginning of year balances2. Zero the governmental fundexpenditures account and reduce the longterm debt balance3. Zero the governmental fund financingsources representing proceeds of debtissued and record it as long term debt4. Adjust for bond premium or discountamortization

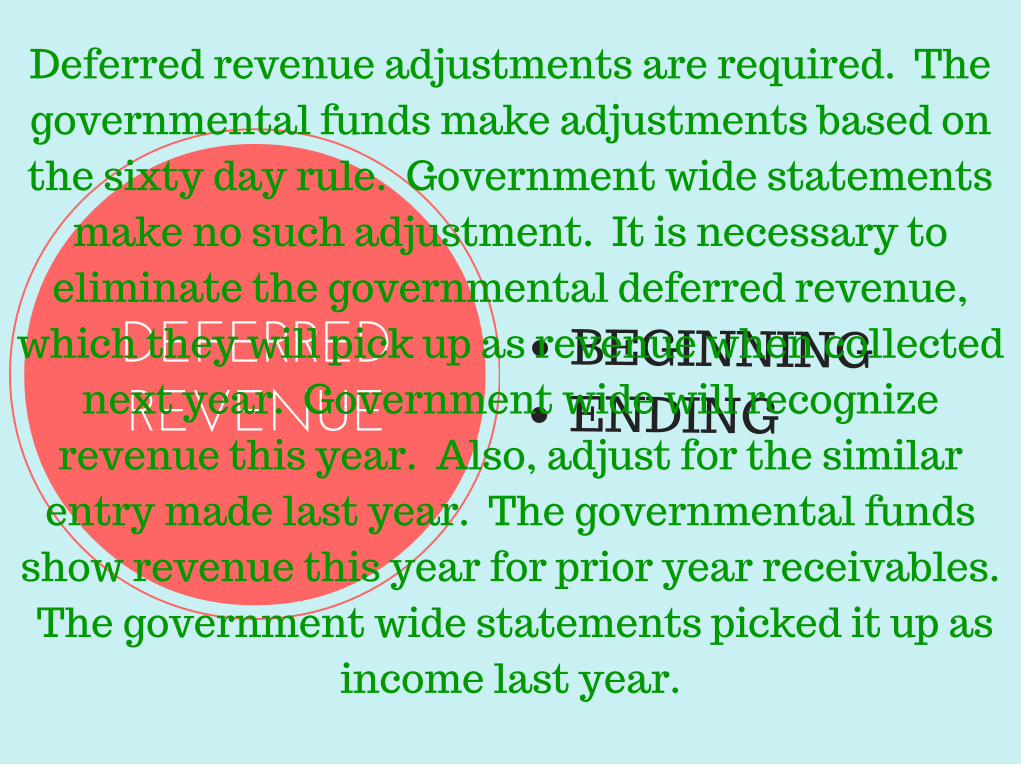

DEFERREDREVENUE

BEGINNINGENDING

DEFERREDREVENUE

BEGINNINGENDING

Deferred revenue adjustments are required. Thegovernmental funds make adjustments based onthe sixty day rule. Government wide statements

make no such adjustment. It is necessary toeliminate the governmental deferred revenue,

which they will pick up as revenue when collectednext year. Government wide will recognize

revenue this year. Also, adjust for the similarentry made last year. The governmental funds

show revenue this year for prior year receivables. The government wide statements picked it up as

income last year.

ACCRUALS BEGINNINGENDING

ACCRUALS BEGINNINGENDING

Similar entries areneeded for accrualsand other liabilities

such as long termpension obligations.

TRANSFERS ELIMINATEINTERGOV'T

TRANSFERS ELIMINATEINTERGOV'T

Eliminate the inter-governmentaltransfers. The statement ofactivity shows transfers betweenprimary government and businesstype activities but not those thattake place between funds withinthe primary government or withinthe business type activities.

INTERNAL SERVICE

FUNDS

FIRST

YEAR END STATEMENTOF NET POSITION

Add the year end statement of net position to the governmental funds balance sheet.

SECOND

REMOVE OPERATINGINCOME

Back the net operations of the internal service fund out of the balance sheet.

INCREASEINVESTMENT INCOME

ANDDECREASE

GOVERNMENT EXPENSES

INCREASEINVESTMENT INCOME

ANDDECREASE

GOVERNMENT EXPENSES

Operating income or loss results from transactionswith two types of customers – those that are

internal, or part of the government and those thatare external, or outside of the government. Anyprofit (or loss) from transactions with internal

customers should be subtracted from (or added to)the expense already recognized in the

governmental fund statements. Any profit or lossfrom transactions with outside customers should

be shown as income or loss on the statement ofactivities since those transactions representincreases or decreases in government assets.

THIRD

REMOVE TRANSFERS

Finally, the effects of any transfers between the governmental funds and the ISF during the current yearmust be removed from net position.