preliminary results - hays – recruiting experts …/media/files/h/hays/results... · ·...

TRANSCRIPT

PRELIMINARY RESULTSYear ended 30 June 2017

CAUTIONARY STATEMENT

This presentation contains certain statements that are neither reported financial results nor other historical information. The informationcontained in this presentation is not audited, is for personal use and informational purposes only and is not intended for distribution to, or useby, any person or entity in any jurisdiction in any country where such distribution or use would be contrary to law or regulation, or which wouldsubject any member of the Hays Group to any registration requirement. No representation or warranty, express or implied, is or will be madein relation to the accuracy, fairness or completeness of the information or opinions made in this presentation.

Statements in this presentation reflect the knowledge and information available at the time of its preparation. Certain statements included orincorporated by reference within this presentation may constitute “forward-looking statements” in respect of the Group’s operations,performance, prospects and/or financial condition. By their nature, forward-looking statements involve a number of risks, uncertainties andassumptions and actual results or events may differ materially from those expressed or implied by those statements. Accordingly, noassurance can be given that any particular expectation will be met and reliance should not be placed on any forward-looking statement.Additionally, forward-looking statements regarding past trends or activities should not be taken as a representation that such trends oractivities will continue in the future. No responsibility or obligation is accepted to update or revise any forward-looking statement resulting fromnew information, future events or otherwise. Nothing in this presentation should be construed as a profit forecast.

This presentation does not constitute or form part of any offer or invitation to sell, or any solicitation of any offer to purchase any shares in theCompany, nor shall it or any part of it or the fact of its distribution form the basis of, or be relied on in connection with, any contract orcommitment or investment decision relating thereto, nor does it constitute a recommendation regarding the shares of the Company or anyinvitation or inducement to engage in investment activity under section 21 of the Financial Services and Markets Act 2000. Past performancecannot be relied upon as a guide to future performance. Liability arising from anything in this presentation shall be governed by English Law,and neither the Company nor any of its affiliates, advisors or representatives shall have any liability whatsoever (in negligence or otherwise)for any loss howsoever arising from any use of this presentation or its contents or otherwise arising in connection with this presentation.Nothing in this presentation shall exclude any liability under applicable laws that cannot be excluded in accordance with such laws.

2

AGENDA

OPERATING REVIEW ALISTAIR COX, CHIEF EXECUTIVE

FINANCIAL REVIEW PAUL VENABLES, FINANCE DIRECTOR

CURRENT TRADING PAUL VENABLES, FINANCE DIRECTOR

STRATEGY UPDATE ALISTAIR COX, CHIEF EXECUTIVE

APPENDICES

1

2

3

4

5

3

1. OPERATING REVIEWALISTAIR COXCHIEF EXECUTIVE

2017 HAS BEEN A MILESTONE YEAR WITH RECORD INTERNAT IONAL FINANCIAL PERFORMANCE & FIRST SPECIAL DIVIDEND

Sector-leading financial efficiency

Maximising financial performance

Further building diversification

� Profits above £200m for the first time since 2008, at £211.5m� All time record levels of International net fees an d profits� France the first of our Future Material Profit Driv ers to deliver over £10m

� Maintained sector leading 22% Conversion Rate*� Built our strongest balance sheet: closing net cash of £112m � Propose increase to full-year core dividend of 11% to 3.22p/share or £46.7m � Propose payment of our first special dividend of 4. 25p/share or £61.6m

Our focus remains on… We have delivered…

* Conversion Rate is the conversion of net fees into operating profit.

� 75% of net fees and 80% of operating profit generat ed outside of UK� Temp & Contracting now c.60% of Group net fees� Non-UK consultant headcount up 16% (Germany +24%; A ustralia +15%)

5

Net Fees £230.9m +9%

Op Profit £69.3m +10%

Conversion rate 30.0% 150bp

Consultants** 1,336 10%

ACCELERATION OF GROWTH IN AUSTRALIA; ASIA MIXED BUT STABLE OVERALL

Australia & NZ (net fees: £180.7m; operating profit : £62.8m)� Further strong net fee growth +11%*, with Temp (66% of net

fees) +13%* and Perm +8%� Broad-based growth across all Australian states and most

specialisms. Net fees in New Zealand down 4%*� Standout performances from Australia IT +23%* and C&P

+13%*, with public sector +11%* and private sector +14%*� Rapid investment in headcount to support growth, up 12%

Asia (net fees: £50.2m; operating profit: £6.5m)� Subdued, but overall stable with net fees flat*� Strong growth in China and Hong Kong, both up 15%*� Japan (7)%* and Singapore (24)%* in part due to tough

trading conditions in banking-focused markets� Targeted investment in consultant headcount, up 7% overall

Headline APAC net fees

LFL* growth Year to 30 June 2017

* LFL (‘like-for-like’) growth represents organic growth at constant currency. Conversion rate represents percentage movement versus prior year. ** Consultant numbers represent closing numbers, and percentage changes are 30 June 2017 closing number versus 30 June 2016 closing number.

APAC

1011

£146m£210m

£242mFY 17£176mFY 16

FY 15 £179m

45%Perm

55%Temp

24%of netfees

6

£231m

Germany (net fees: £230.3m)� Record net fees and operating profits. Net fee growth of 14%*,

operating profit up 9%* to £80.5m

� Strong 13%* growth in Temp/Contracting, driven by IT (+15%*) and Engineering (+14%*). Excellent 27%* growth in Perm

� Within other specialisms, A&F +14%*, Life Sciences +23%*� Further aggressive headcount investment, up 24% y-o-y to

over 1,500 consultants

Rest of the division (net fees: £240.5m)

� Strong broad-based growth driven by Continental Europe, where 11 countries grew by over 10%*

� Further operating profit improvement, including 34%* operating profit increase in France to over £10m

� Americas solid, including US +7%* and Canada +5%*

RECORD PERFORMANCE IN GERMANY, STRONG BROAD-BASED GROWTH IN REST OF THE DIVISION

Headline CE&RoW net fees

* LFL (‘like-for-like’) growth represents organic growth at constant currency. Conversion rate represents percentage movement versus prior year. ** Consultant numbers represent closing numbers, and percentage changes are 30 June 2017 closing number versus 30 June 2016 closing number.

CE&RoW

1011

£168m£220m

£267mH1 13 £140m£134m£133mFY 15

FY 16FY 17

£314m£363m

LFL* growth Year to 30 June 2017

38%Perm

62%Temp

49%of netfees

Net Fees £470.8m +12%

Op Profit £100.7m +7%

Conversion rate 21.4% (30)bp

Consultants** 3,600 19%

7

£471m

Net Fees £252.9m (7%)

Op Profit £41.5m (21%)

Conversion rate 16.4% (280)bp

Consultants** 1,948 (4%)

TOUGH BUT SEQUENTIALLY STABLE; EXITING THE YEARWITH MODEST SIGNS OF IMPROVEMENT IN PRIVATE SECTOR

Headline UK&I net fees

* LFL (‘like-for-like’) growth represents organic growth at constant currency. Conversion rate represents percentage movement versus prior year. ** Consultant numbers represent closing numbers, and percentage changes are 30 June 2017 closing number versus 30 June 2016 closing number.

UK & IRELAND

1011

12

£244m£242m

£225m

Net fees down 7%* in challenging trading conditions

� Temp net fees down 8%*, Perm down 6%*

� UK regional business more resilient than London. Scotland & NI (1)%, South West & Wales (4)%. Ireland +14%*

� Early action in FY16 to reduce costs; headcount down a further 4% in FY17 to best defend financial performance

Private sector net fees down 5%*: 74% of UK&I net f ees

� Post-Referendum step-down in Perm, quickly stabilised and exited the year with modest underlying growth

� Overall for the year: A&F (3)%*, C&P (3)%*, IT (12)%*

Public sector net fees down 13%*: 26% of UK&I net f ees

� Tough market conditions throughout the year

� Education (12)%*, C&P (10)%*, IT (21)%*

FY 17 £253m£272m£272m

FY 16FY 15

LFL* growth Year to 30 June 2017

44%Perm

56%Temp

27%of net fees

8

2018 ASPIRATIONS: WE REMAIN ON TRACK AFTER 4 YEARS

Other Countries (£m) Operating Profit*

25 35 45

ASSUMED 5YR NET FEE CAGR: +8% to +12%

* Nothing in this presentation should be construed as a profit forecast. There is no certainty over timing or probability of achieving these objectives and they are dependent on a variety of assumptions and factors both Hays specific and otherwise. The 2018 Operating Profit ranges are after Group central cost allocation but before allocation of CERoW & Asia Pac divisional overheads (assumed to be £15m per annum) and assume constant rates of exchange as of 30 September 2013. All reported profit numbers are shown on a headline basis.

FY18 ORIGINAL FX

FY 2013

FY 2017 41

Australia & NZ (£m) Operating Profit*

ASSUMED 5YR NET FEE CAGR: +1% to +5%

FY 2013

FY 2017 6364

FY18 ORIGINAL FX 60 70 80

UK & Ireland (£m) Operating Profit*

45 60 75

ASSUMED 5YR NET FEE CAGR: +5% to +9%

FY 2013

FY18 OBJECTIVE

FY 2017 42

Germany (£m) Operating Profit*

ASSUMED 5YR NET FEE CAGR: +7% to +12%

FY 2013

FY 2017FY18 ORIGINAL FX

8158

85 100 115

6

12

9

2. FINANCIAL REVIEWPAUL VENABLESGROUP FINANCE DIRECTOR

GOOD OVERALL GROUP FINANCIAL PERFORMANCENet fees Operating profit**

£125.5m

£140.3m£724.9m

£719.0m

Basic earnings per share

5.14p

6.13p

8.48p

9.66p

7.44p

Net fees £954.6m

6% increase*

EPS9.66p

14% increase

Operating profit £211.5m

1% increase*

* LFL (‘like-for-like’) growth is organic growth at constant currency.** Continuing operations only.

£164.1m

£181.0m

FY 13

FY 14

FY 15

FY 16 £810.3m

£764.2m

11

FY 13

FY 14

FY 15

FY 16

FY 14

FY 15

FY 16

FY 17

FY 13

PROPOSED INCREASE IN FULL-YEAR CORE DIVIDEND OF 11% TO 3.22p, WITH 3.0X COVER, AND FIRST SPECIAL DIVIDEND OF 4.25p

FY 17 £954.6m FY 17 £211.5m

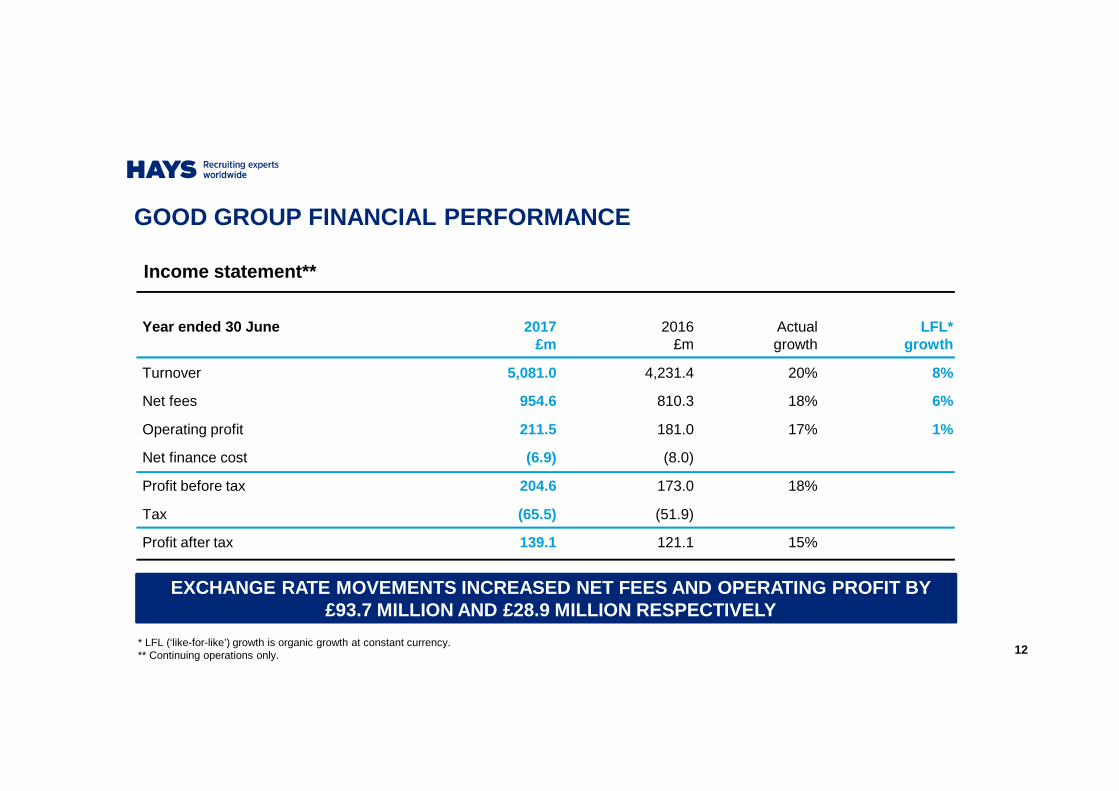

GOOD GROUP FINANCIAL PERFORMANCE

Income statement**

Year ended 30 June 2017£m

2016£m

Actual growth

LFL* growth

Turnover 5,081.0 4,231.4 20% 8%

Net fees 954.6 810.3 18% 6%

Operating profit 211.5 181.0 17% 1%

Net finance cost (6.9) (8.0)

Profit before tax 204.6 173.0 18%

Tax (65.5) (51.9)

Profit after tax 139.1 121.1 15%

* LFL (‘like-for-like’) growth is organic growth at constant currency. ** Continuing operations only.

EXCHANGE RATE MOVEMENTS INCREASED NET FEES AND OPER ATING PROFIT BY £93.7 MILLION AND £28.9 MILLION RESPECTIVELY

12

£181.0m

£28.9m£6.1m £(11.1)m

UK&IAPAC CEROWFY16EBIT

£6.6m

OPERATING PROFIT OVER £200M FOR THE FIRST TIME SINCE 2008:DRIVEN BY EXCHANGE RATE GAINS AND INTERNATIONAL PRO FIT GROWTH

FY17EBIT

£211.5m

INTERNATIONAL PROFIT GROWTH

13

£’m

150

250

FX IMPACT

INTERNATIONAL PROFIT GROWTH MORE THAN OFFSETS UK DE CLINE

Net Fees £470.8m 12%*

Op Profit £100.7m 7%*

� Record performance in Germany with net fees up 14%* to £230.3m

� Rest of division grew 11%*, with 8 countries growing by over 20%*, and delivered 5%* increase in trading profit

STRONG GROWTH IN INTERNATIONAL BUSINESS OFFSETS UK DECLINE

Asia Pacific

Performance by region

Continental Europe & RoW

24%of netfees

49% of netfees

Net Fees £230.9m 9%*

Op Profit £69.3m 10%*

� 11%* growth in Australia & NZ led by strong temp/contracting up 13%*; operating profit up 14%*

� Asia subdued, with flat* net fees and operating profit (18)%* as banking markets remained tough

United Kingdom & Ireland

27% of netfees

Net Fees £252.9m (7)%*

Op Profit £41.5m (21)%*

� Trading conditions tough but sequentially stable since Nov. ’16. Net fees (7)%*, primarily in H1, and operating profit (21)%*

� Exited the year with modest underlying growth in private sector

14* LFL (‘like-for-like’) growth is organic growth at constant currency.

GOOD GROWTH IN TEMP FEES, SOLID IN PERM

Permanent placement business

£393.9m(41% of net fees)

Temporary placement business

£560.7m(59% of net fees)

* Growth rates and margin change are for the year ended 30 June 2017 versus year ended 30 June 2016, on a like-for-like basis which is organic growth at constant currency.

Review of Group Permanent and Temporary Businesses*

** The underlying Temp gross margin is calculated as Temp net fees divided by Temp gross revenue and relates solely to Temp placements in which Hays generates net fees and specifically excludes transactions in which Hays acts as agent on behalf of workers supplied by third party agencies and arrangements where the Company provides major payrolling services.

49% Temp52% Temp

Split of net fees

FY 16FY 15

58% Temp

58% Temp

FY 17

� 8% volume increase driven primarily by Germany and Australia

� Mix/hours worked increased 1%

� Underlying Temp margin** down 30bps, primarily due to mix and a reduction in Temp margin in our Australia and UK markets

� Volumes increased by 4% as strong increases in CE&RoW offset decreases in the UK&I

� Average Perm fee broadly flat

7% net fee growth

8% volume increase

1% increase in mix/hours

(30) bps underlying margin decrease**

4% net fee growth

4% volume increase

0% average Perm fee increase

15

59% Temp

THE AUSTRALIAN DOLLAR AND EURO REMAIN SIGNIFICANT F X TRANSLATION SENSITIVITIES FOR THE GROUP

Year ended 30 June 2017 Average Closing

Australian $ 1.6836 1.6952

Euro € 1.1642 1.1406

Impact of a one cent change per annum Net fees Op pr ofit

Australian $ +/- £1.0m +/- £0.4m

Euro € +/- £3.2m +/- £1.1m

Key FX rates and sensitivities

� FX rates at 29 August 2017: £1 / AUD1.6327; £1 / €1.0764

� Retranslating the Group’s full year operating profit at current exchange rates would increase the actual result by c.£12m from £211.5m to c.£223m

16

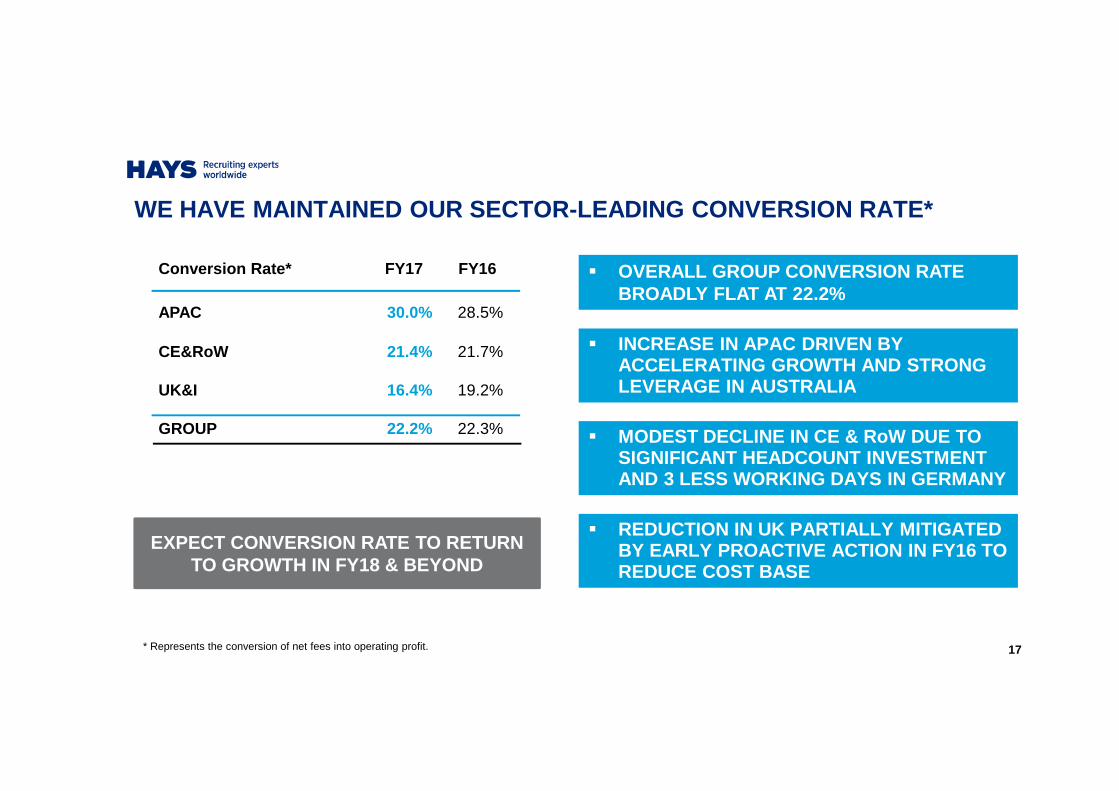

WE HAVE MAINTAINED OUR SECTOR-LEADING CONVERSION RA TE*

1717

EXPECT CONVERSION RATE TO RETURN TO GROWTH IN FY18 & BEYOND

Conversion Rate* FY17 FY16

APAC 30.0% 28.5%

CE&RoW 21.4% 21.7%

UK&I 16.4% 19.2%

GROUP 22.2% 22.3%

* Represents the conversion of net fees into operating profit.

� OVERALL GROUP CONVERSION RATE BROADLY FLAT AT 22.2%

� INCREASE IN APAC DRIVEN BY ACCELERATING GROWTH AND STRONG LEVERAGE IN AUSTRALIA

� MODEST DECLINE IN CE & RoW DUE TO SIGNIFICANT HEADCOUNT INVESTMENT AND 3 LESS WORKING DAYS IN GERMANY

� REDUCTION IN UK PARTIALLY MITIGATED BY EARLY PROACTIVE ACTION IN FY16 TO REDUCE COST BASE

� We expect the net finance charge for the year ending 30 June 2018 to be c.£5 million

18

Taxation

Underlying effective tax rate 32.0% 30.0%

INCREASE IN ‘ETR’ TO 32.0% DRIVEN BY HIGHER INTERNA TIONAL PROFITS VERSUS LOWER UK PROFITS Finance charge and taxation

Year ended 30 June 2017£m

2016£m

Finance charge

Net interest charge on debt (2.1) (2.9)

Interest unwind of discount on Acquisition Liability (non-cash) (1.1) (0.9)

IAS 19 pension charge (non-cash) (2.4) (3.9)

PPF levy (0.5) (0.3)

Other interest payable (0.8) -

Net finance charge (6.9) (8.0)

� Higher profitability in Germany and Australia increases the Group effective tax rate to 32.0%.

� ETR for FY18 will be driven by the mix of profits. We currently expect the rate to be 31.5%.

14% INCREASE IN EARNINGS PER SHARE

Basic earnings per share (EPS)

* Number of shares used for basic EPS calculation purposes excludes shares held in Treasury.

Year ended 30 June 2017 2016 Change

Basic earnings £139.1m £121.1m 15%

Weighted average number of shares* 1,440.7m 1,428.4m

Basic earnings per share 9.66p 8.48p 14%

Memo

Shares in issue* at 30 June 2017 and 29 August 2017 1,443m

Basic EPS

1110

125.19p**

3.25p**H1 12 7.72pH2 12H1 13

5.19p5.47pFY 17 9.66p

7.44p8.48pFY 16

FY 15

19

STRONG UNDERLYING CASH PERFORMANCE

£211.5m

£33.7m

£(28.2)m

£(68.2)m £(1.9)m

£146.9m

Operating profit to free cash flow conversion Uses of cash flow

Operating profit

Non-cash items

Working capital

Taxpaid

Interestpaid

Free cash flow

Operating cash flow £217.0m (FY16: £159.3m)

Cash from operations

H1 13 £162.2m

Capex guidance for FY18 is c. £20m and depreciation & amortisation guidance is c. £19mUS$18.5m payment in FY18 for remaining 20% equity i n Veredus Corp.

£78.1m £97.3m£159.3mFY 16

FY 17

FY 15 £189.8m

£217.0m

Increased net cash £74.8m

Capex £21.4m

Pensions £14.8m

20

Dividend £42.6m

Other £(6.7)m

£m30 June

201730 June

2016

Goodwill & intangibles 241.9 242.0

Property, plant & equipment 24.0 19.8

Net deferred tax 23.3 23.9

Net working capital* 231.7 190.6

Derivative financial instruments - 6.6

Tax liabilities (23.5) (27.1)

Retirement benefit obligations (0.2) (14.3)

Acquisition Liabilities (13.6) (11.2)

Other provisions & liabilities (8.8) (9.3)

474.8 421.0

Net cash/(debt) 111.6 36.8

Net assets 586.4 457.8

STRONGEST BALANCE SHEET

Balance sheet analysis

* Movement in net working capital in the balance sheet is calculated at closing exchange rates. For cash flow purposes, the movement in working capital is calculated at average exchange rates.

� Good underlying working capital management with debtor days at 39 (FY16: 37 days)

� Increase primarily due to expansion of Temp/Contracting business in Germany and Australia

NET WORKING CAPITAL

� Decrease primarily due to an increase in asset values together with company contributions offset by a change in financial assumptions (decrease in discount rate and increase in inflation rate).

RETIREMENT BENEFITS

21

22

FURTHER MATERIAL INCREASE IN CASH POSITION

** Covenant ratios are shown on a pro-forma basis for 12 months ended 30 June 2017.

Closing net cash/(net debt) £m

Free cash flow*

H1 13 £111.8m

£52.7m£62.2m

* Free cash flow is defined as cash flow before dividends, additional pension contributions, capital expenditure, acquisitions and exceptional items.

FY 17 £146.9m

FY 15FY 16 £114.0m

£141.0m

Jun 15Jun 12 Jun 17Jun 13 Jun 14

(132.9)

36.8

(30.7)

(105.2)

NET DEBT ELIMINATED IN FY16� FY17 ended with net cash of £111.6m

£210M BANK FACILITY IN PLACE� expires April 2020

EBITDA / INTEREST RATIO: 65X**� debt covenant: > 4.0

NET DEBT / EBITDA RATIO: N/A� debt covenant: < 2.5

(62.7)

22

Jun 16

111.6

TOTAL DIVIDEND PAYOUT OF £108.3M FOLLOWING FIRST SP ECIAL DIVIDEND OF £61.6M

� Target core dividend cover of 2.0x to 3.0x Group EP S� Increase of 11% in full year core dividend to 3.22p per share� Cash cost of proposed FY17 core dividend £46.7m, co ver of 3.0x

EXCESS CASH RETURNS POLICY

FREE CASH FLOW PRIORITIES

CORE DIVIDEND POLICY

� Maintain a net cash position of c.£50m� Assuming a positive outlook, any free cash flow gen erated over

and above this position will be distributed to shar eholders via special dividends, or other appropriate methods, an nually

� First special dividend of 4.25p per share, in line with policy

� Fund Group investment and development� Maintain a strong balance sheet� Deliver a core dividend which is sustainable, progr essive and

appropriate

23

The final dividend and special dividend will be pai d, subject to shareholder approval, on 17 November 2017 to shareholders on the register on 6 October 2017

24* LFL (‘like-for-like’) growth is organic growth at constant currency.

FINANCIAL SUMMARY

RECORD LEVELS OF INTERNATIONAL PROFIT

� Strong 10%* profit growth in APAC driven by excellent profit growth in Australia � 7%* profit growth in CE&RoW, as we continued to invest to drive further growth; decline

in UK profit partially mitigated by early cost base adjustments� Maintained sector-leading conversion rate of 22.2%

STRONG UNDERLYING CASH PERFORMANCE; FIRST SPECIAL D IVIDEND� 103% conversion of operating profit to operating cash flow� Year-end net cash position of £111.6m� Core dividend increased by 11% to 3.22p, first special dividend of £61.6m

GOOD, BROAD-BASED NET FEE GROWTH

� Strong 12%* growth in CE&RoW, record net fee performance in Germany, up 14%* � Australia growth accelerated to 13%*; UK (7)% but broadly stable since November ‘16

24

3. CURRENT TRADINGPAUL VENABLESGROUP FINANCE DIRECTOR

SUPPORTIVE CONDITIONS IN VAST MAJORITY OF INTERNATI ONAL MARKETS; UK REMAINS STABLE

Current trading conditions by region

APAC

UK&I

CE & RoW

� Conditions remain subdued, but broadly sequentially stable� Continuation of early signs of modest improvement in privat e sector markets� Public sector remains tough

� Strong activity levels in Australia across all stat es and most specialisms� Growth in Asia is good

� Growth remains strong overall, despite tough compar ators� Strong growth in Germany and across the rest of Eur ope� More mixed conditions in the Americas

26In FY18 our Germany business will have 3 fewer working days compared to FY17, all of which relate to H1. We estimate that this will have a negative impact on profit of c.£4 million.

4. STRATEGY UPDATEALISTAIR COXCHIEF EXECUTIVE

28

WE HAVE CLEAR, WELL ESTABLISHED STRATEGIC PRIORITIE S TO DELIVER OUR LONG-TERM AIMS

GENERATE, REINVEST & DISTRIBUTE

MEANINGFUL CASH RETURNS

BUILD CRITICAL MASS & DIVERSITY

ACROSS OUR GLOBAL PLATFORM

MATERIALLY INCREASE &

DIVERSIFY GROUP PROFITS

INVEST IN PEOPLE, TECHNOLOGY,

COLLABORATIONS & INNOVATION

29

INVESTOR DAY 2017: 9 NOVEMBER, LONDON 12:00pm – 6:00 pm

AT OUR INVESTOR DAY, WE WILL DEMONSTRATE OUR KEY AR EAS OF FOCUS & DETAIL OUR ASPIRATIONS FOR OUR FUTURE POTEN TIAL

We will specifically detail:• Our aspiration to deliver further material increase s in earnings over the next 5 years• Our strategies and areas of focus to deliver those aspirations• The potential cash generation implications of deliv ering on those aspirations

We will clearly demonstrate:• The key success factors that we focus on to drive o ur business • How we are responding to the evolving needs of clie nts and candidates• How we are utilising data, technology and innovatio n to preserve and enhance our

core business• The detail of where our future growth will be deliv ered, including doubling our

German profits over 5 years

Attendees will have the opportunity to:• Meet and interact with over 20 senior Hays operator s from around the world• See demos of a range of the tools and systems we ha ve in place in our business

5. QUESTIONS & ANSWERS

6. APPENDICES

32

1.0FY 2017 RESULTS SUPPORTING INFORMATION

Year ended 30 June 2017£m

2016£m

LFL growth*

Germany 80.5 63.2 9%

Rest of CE&RoW (23 countries) 35.6 28.3 5%

CE&RoW Central Costs (15.4) (12.8) 15%

CE&RoW Operating Profit 100.7 78.7 7%

FURTHER PROGRESS IN CE&RoW (EX-GERMANY) PROFITABILI TY

* LFL (‘like-for-like’) growth represents organic growth at constant currency.

Operating profit split in Continental Europe & RoW – HEADLINE

� Germany delivered operating profit LFL growth of 9%* despite significant investment in headcount and the negative impact of three less working days in the year. Excellent conversion rate of 35%

� A good performance elsewhere in CE&RoW where market conditions were strong and we invested in headcount while controlling our cost base

33

LIKE-FOR-LIKE SUMMARY

* LFL (‘like-for-like’) growth is organic growth at constant currency.

Year ended 30 June 2016£m

FX impact£m

Organic£m

2017£m

LFL* growth

Net fees

Asia Pacific 176.1 36.5 18.3 230.9 9%

Continental Europe & RoW 362.5 56.1 52.2 470.8 12%

United Kingdom & Ireland 271.7 1.1 (19.9) 252.9 (7%)

810.3 93.7 50.6 954.6 6%

Operating profit

Asia Pacific 50.2 13.0 6.1 69.3 10%

Continental Europe & RoW 78.7 15.4 6.6 100.7 7%

United Kingdom & Ireland 52.1 0.5 (11.1) 41.5 (21%)

181.0 28.9 1.6 211.5 1%

34

H2 FY17 v H1 FY17: ANALYSIS BY DIVISION

* LFL (‘like-for-like’) growth is organic growth at constant currency.Note: H1 17 is the period from 1 July 2016 to 31 December 2016. H2 17 is the period from 1 January 2017 to 30 June 2017.

Net fee growth (LFL*) versus same period last year

Q1 17 Q2 17 H1 17 Q3 17 Q4 17 H2 17 FY 17

Asia Pacific 5% 7% 6% 12% 11% 11% 9%

Continental Europe & RoW 13% 8% 10% 18% 11% 15% 12%

United Kingdom & Ireland (10%) (10%) (10%) (4)% (5)% (4)% (7%)

Operating profit growth (LFL*)versus same period last year

Asia Pacific 12% 8% 10%

Continental Europe & RoW 6% 8% 7%

United Kingdom & Ireland (29%) (14)% (21%)

Conversion rate (%)*operating profit as % of net fees

Asia Pacific 29.8% 30.2% 30.0%

Continental Europe & RoW 21.4% 21.4% 21.4%

United Kingdom & Ireland 14.4% 18.4% 16.4%

35

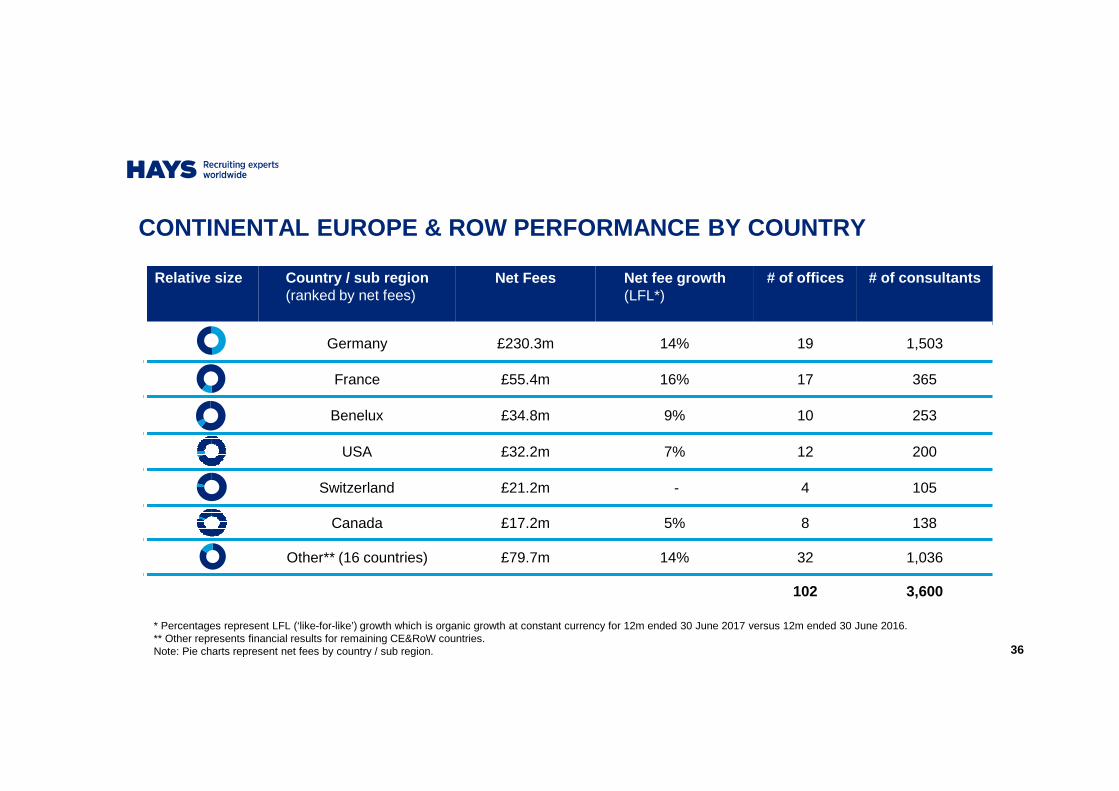

Relative size Country / sub region(ranked by net fees)

Net Fees Net fee growth(LFL*)

# of offices # of consultants

Germany £230.3m 14% 19 1,503

France £55.4m 16% 17 365

Benelux £34.8m 9% 10 253

USA £32.2m 7% 12 200

Switzerland £21.2m - 4 105

Canada £17.2m 5% 8 138

Other** (16 countries) £79.7m 14% 32 1,036

102 3,600

CONTINENTAL EUROPE & ROW PERFORMANCE BY COUNTRY

* Percentages represent LFL (‘like-for-like’) growth which is organic growth at constant currency for 12m ended 30 June 2017 versus 12m ended 30 June 2016. ** Other represents financial results for remaining CE&RoW countries.Note: Pie charts represent net fees by country / sub region. 36

CONSULTANT HEADCOUNT

Change in headcount As at June2017

As at Dec

2016

Changesince

Dec 2016

As at June2016

Changesince

June 2016

Asia Pacific 1,336 1,270 5% 1,210 10%

Continental Europe & RoW 3,600 3,358 7% 3,034 19%

United Kingdom & Ireland 1,948 1,978 (2%) 2,024 (4%)

Group 6,884 6,606 4% 6,268 10%

37

OFFICE NETWORK

* Offices opened is shown net of closed and merged offices.

Number of offices 30 June 2016

Opened/(Closed)*

30 June 2017

Asia Pacific 49 1 50

Continental Europe & RoW 103 (1) 102

United Kingdom & Ireland 100 (2) 98

Total 252 (2) 250

38

TRADING DAYS

Number of trading days* H1 H2 Year H1 H2 Year

Year ended 30 June 2016 129 125 254 131 123 254

Year ended 30 June 2017 128 125 253 128 123 251

Year ending 30 June 2018 127 125 252 125 123 248

* UK and Germany only. 39

UK Germany

THE SCALE AND SCOPE OF OUR BUSINESS IS UNIQUE

LINKEDIN FOLLOWERS

HITS ON HAYS WEBSITES 1.8 million27 million

CV’S RECEIVEDINTERVIEWS PER MONTH7 million 45,000

PERM PLACEMENTS70,000TEMP ASSIGNMENTS240,000

WORLDWIDE IN FY17 WE FILLED OVER 1,000 JOBS EVERY W ORKING DAY

FY17 STATISTICS

40

41

2.0THE HAYS BUSINESS MODEL & STRATEGY FOR GROWTH

HAYS IS A LEADING GLOBAL EXPERT IN QUALIFIED, PROFE SSIONAL AND SKILLED RECRUITMENT

GENERALIST RECRUITMENT (mostly blue collar)

EXECUTIVE SEARCH (head hunting)

PROFESSIONAL RECRUITMENT (mostly white collar)

� Contingent fee model� Focus on high-skilled roles� Clear structural growth markets

42

A PROVEN TRACK RECORD OF ORGANIC GROWTH

New country & specialism entries

33 COUNTRIES 20 SPECIALISMS

Pre 1990

Early 1990s

Late 1990s

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Brazil

China, HK

Organic Acquisition

A&F C&P

FranceCzech Re.

Netherlands

Portugal

Canada

Belgium

Germany Switzerland

Spain

Austria

Sweden Poland

Australia

N.Zealand

Singapore

Italy UAELuxembourg

UK

Key:

Legal

Banking Fin Services

EducationContact Ce.

Engineering

HR

Sales & Ma.

Executive

Retail

Healthcare

Purchasing

IT

Japan Life Sciences

Energy O&G

Hungary Denmark

Ireland

India Russia

Mining

Mexico USA

Colombia

Chile Malaysia

Office Pros

Telecoms

43

Top 3 position Top 5 positionMarket Leader Other

OUR WORLDWIDE PLATFORM PROVIDES A PIPELINE OF FUTUR E GROWTH OPPORTUNITIES & LEADERSHIP IN ALL CORE MARKETS

Australia (#1)BelgiumBrazilFranceGermany (#1)Hong KongHungaryIreland (#1)ItalyJapan (#1)

MalaysiaNew Zealand (#1)Poland (#1)Portugal (#1)RussiaSingaporeSpainSwedenSwitzerlandUK (#1)

AustriaCanadaChileChinaColombiaCzech Rep

DenmarkLuxembourgMexicoNetherlandsUAE

Hays market positioning*

TOP 3

TOP 5

* Market position is based on Hays estimates. List of countries only includes those with top 5 market positions and excludes newly opened countries.

The largest international specialist recruitment bu siness in the world

44

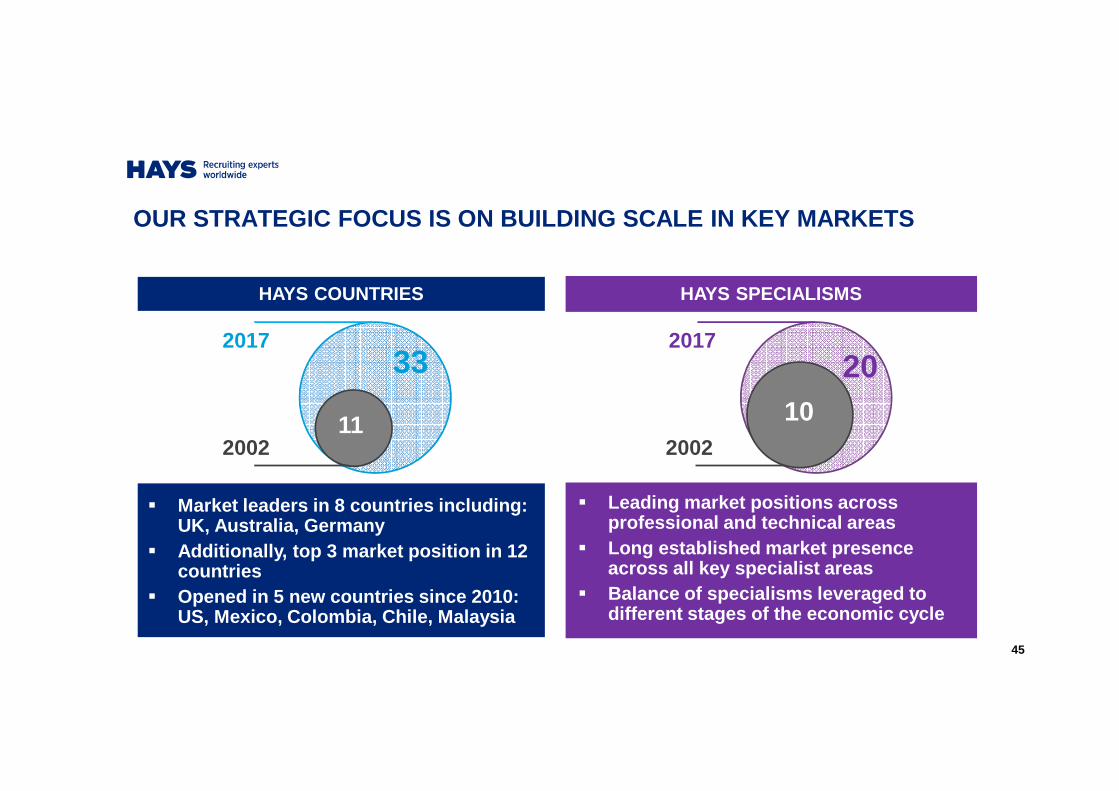

OUR STRATEGIC FOCUS IS ON BUILDING SCALE IN KEY MAR KETS

� Market leaders in 8 countries including: UK, Australia, Germany

� Additionally, top 3 market position in 12 countries

� Opened in 5 new countries since 2010: US, Mexico, Colombia, Chile, Malaysia

� Leading market positions across professional and technical areas

� Long established market presence across all key specialist areas

� Balance of specialisms leveraged to different stages of the economic cycle

HAYS COUNTRIES HAYS SPECIALISMS

33

2002

2017

11

20

2002

2017

10

45

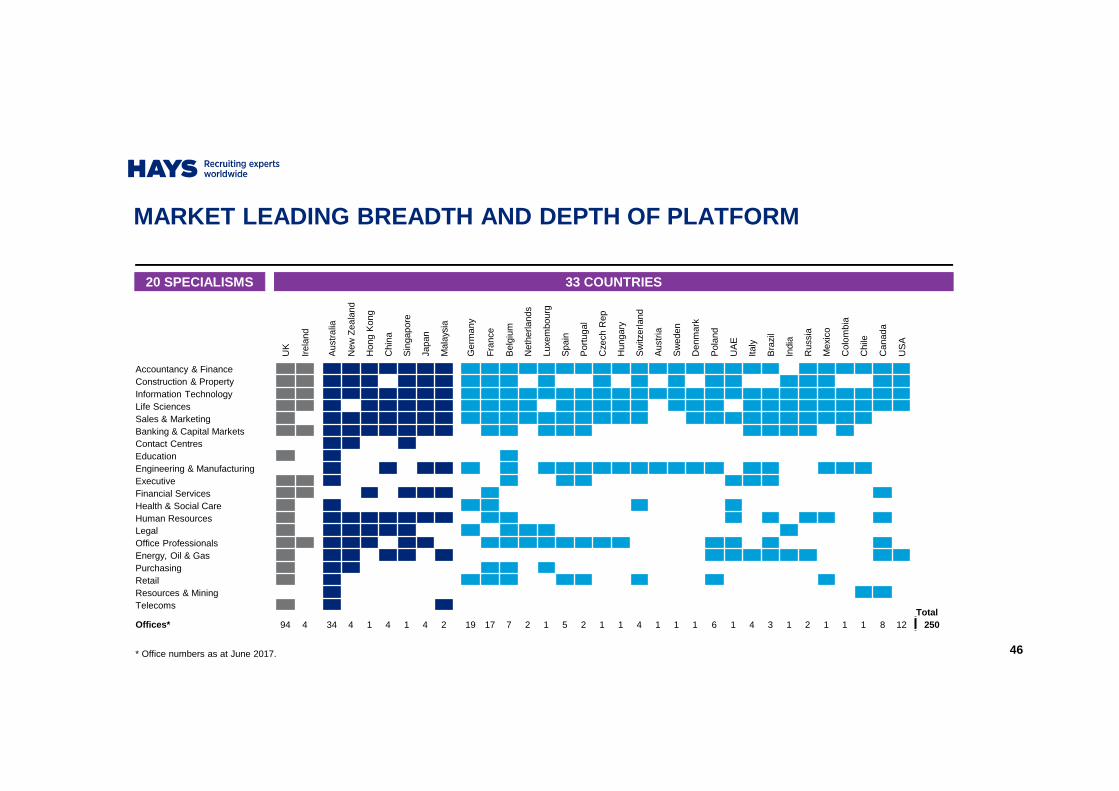

MARKET LEADING BREADTH AND DEPTH OF PLATFORMDivisional operating review

UK

Irel

and

Aus

tral

ia

New

Zea

land

Hon

g K

ong

Chi

na

Sin

gapo

re

Japa

n

Mal

aysi

a

Ger

man

y

Fra

nce

Bel

gium

Net

herla

nds

Luxe

mbo

urg

Spa

in

Por

tuga

l

Cze

ch R

ep

Hun

gary

Sw

itzer

land

Aus

tria

Sw

eden

Den

mar

k

Pol

and

UA

E

Italy

Bra

zil

Indi

a

Rus

sia

Mex

ico

Col

ombi

a

Chi

le

Can

ada

US

A

Accountancy & FinanceConstruction & PropertyInformation TechnologyLife SciencesSales & MarketingBanking & Capital MarketsContact CentresEducationEngineering & ManufacturingExecutiveFinancial ServicesHealth & Social CareHuman ResourcesLegalOffice ProfessionalsEnergy, Oil & GasPurchasingRetailResources & MiningTelecoms

TotalOffices* 94 4 34 4 1 4 1 4 2 19 17 7 2 1 5 2 1 1 4 1 1 1 6 1 4 3 1 2 1 1 1 8 12 250

33 COUNTRIES20 SPECIALISMS

* Office numbers as at June 2017. 46

… and leverages the Group to economic improvement

THE STRENGTH OF OUR MODEL IS KEY TO DELIVERING FOR CLIENTS AND DRIVING FINANCIAL PERFORMANCE THROUGH THE CYCLE

… a resilient financial performance in tougher economic times…

…delivers the best solutions for clients & candidates…

… the best people, sector leading technologyand a world class brand…

Unrivalled scale, balance and diversity…

47

� Exposure to structural growth and more mature areas

� Long-established across technical, white-collar spe cialisms

� Unmatched breadth and scale of operations globally

� Global connectedness of operations is key

� 33 countries around the world, up from 11 in 2002

� Rapid start-up phase now largely completed

� 20 specialist areas across professional / technical skills

� Focus on building scale in key specialisms in core markets

� Temporary / Contracting / Permanent

� Rolling out IT Contractor model to selected markets

THERE ARE 5 PILLARS WHICH UNDERPIN THE STRENGTH OF OUR BUSINESS MODEL

1. BALANCE

2. SCALE

3. GEOGRAPHIC DIVERSIFICATION

4. SECTORAL DIVERSIFICATION

5. CONTRACT FORM DIVERSIFICATION

BALANCE, SCALE AND DIVERSIFICATION ARE WHAT SETS TH E HAYS BUSINESS MODEL APART AND DRIVES OUTPERFORMANCE

48

LEVERAGING OUR BEST-IN-CLASS TECHNOLOGY PLATFORM AN D BRAND

OPERATIONAL EFFECTIVENESS

BEST CUSTOMER SERVICE

DIGITALLY-ENABLED CONSULTANTS

1

2

3

OP

ER

ATIO

NA

L E

FF

EC

TIV

EN

ES

S

THE BEST CANDIDATES TO CLIENTS, FASTER THAN ANYONE ELSE

CROSS SYSTEM AWARENESS

SEARCH CAPABILITIES

GLOBAL DIGITAL PLATFORM

OPERATIONAL INTELLIGENCE

MANAGEMENT INFORMATION

AUTOMATED ATS VMS INTERFACES

DIGITAL CV PARSING

AUTOMATIC JOB BOARD

POSTINGS

Global Database

Internally integrated & externally connected

Delivering outcomes to drive growth

49

A BALANCED PORTFOLIO

Net Fees by type*

* Indicative purposes only based on information for the 12 months ended June 2017.

** Major specialisms within Other include: Banking Related (7%), Life Sciences (5%), Sales & Marketing (4%) and Education (3%).

Spot~75%

Recruitment contracts

~25%

Public sector15%

Private sector85%

Top 40~15%

30,000 customers

~85%

Other**33%

Accountancy & Finance

15%

Construction & Property

15%

IT21%

Temp59%

Perm41%

APAC24%

CE&RoW49%

UK&I27%

Office Sup. 7%

Engineering 9%

50

HK, Singapore (2%)

* Market penetration represents the percentage of skilled and professional recruitment that is outsourced, based on Hays’ management estimates.

Net fees by market maturity* (percentages in table show % of Group net fees in FY17)

ESTABLISHED:>70% penetration30% of Group net fees(6)% LFL net fee growth

DEVELOPING:>30-70% penetration

28% of Group net fees+12% LFL net fee growth

EMBRYONIC: <10% penetration5% of Group net fees+8% LFL net fee growth

EMERGING:10-30% penetration37% of Group net fees

+12% LFL net fee growth

UK & Ireland (27%)

Australia & NZ (19%) France, Netherlands,

Canada (9%)

Japan, China, Malaysia (3%)

Latin America, Russia, India (2%)

Germany (24%)

Other CE&RoW (11%)

BALANCED BUSINESS MODEL: WELL DIVERSIFIED IN STRUCTURAL AND CYCLICAL MARKETS

USA (3%)

51

39%

51%

10%

Net fees FY17

£954.6m

Information TechnologyEngineering

Sales & Marketing

Candidate shortagesClients investing

Continued investmentDrive growth

STRONG: GROWTH >10%* TOUGH: DECLINE <0%*

BankingUK Education

Oil & Gas

Short term challengesLong term opportunity

Defend market position Reduce costs

SOLID / GOOD:GROWTH 0-10%*

Accountancy& FinanceConstruction

& PropertyLife Sciences

Mixed conditions but opportunities

available

Selective investmentMaintain position

* Represents LFL (‘like-for-like’) growth rates in the 12 months to 30 June 2017. Listed specialisms are examples only and are not exhaustive.

BALANCED BUSINESS MODEL: SECTOR DIVERSITY EXPOSES U S TO GROWTH OPPORTUNITIES AND PROTECTS OUR BUSINESS

52

Asia

Hays FY17 Net Fees by geography

0% 100%Group net fees

Temp Perm

Rest of CE&RoW UK & Ireland Australia & New Zealand Germany

86%

61%44% 34%

13%

87%

66%56%

39%

14%

BALANCED BUSINESS MODEL: SECTOR-LEADING EXPOSURE TO KEY TEMP/CONTRACTOR MARKETS, PERM-GEARED IN HIGH GROWTH AREAS

53

54

3.0DIVISIONAL PROFILES

#1 market position*

Net fees by specialism

Perm : Temp

Private : Public sector

Net fees by countryNet fees: £230.9m

Operating profit: £69.3m

Conversion rate: 30.0%

Countries: 7

Consultants: 1,336

Offices: 50

Note: Private:Public sector and Temp:Perm split is based on net fees for 12 months ended 30 June 2017.* Market position is based on Hays estimates.

Diverse sector exposure Asia structural opportunity

Net fees by specialism Net fees by country

ASIA PACIFIC REPRESENTS 24% OF GROUP NET FEES WITH AUSTRALIA REPRESENTING 72% OF DIVISIONAL NET FEES

45%%

55%

74% 26%

22%

13%

12%10%

10%

6%4%

23%

Const. & Property Account. & FinanceIT Office SupportBanking Sales & MarketingHR Other

72%

8%

6%5%

Australia JapanNew Zealand ChinaHong Kong (4%) Singapore (3%)Malaysia (2%)

55

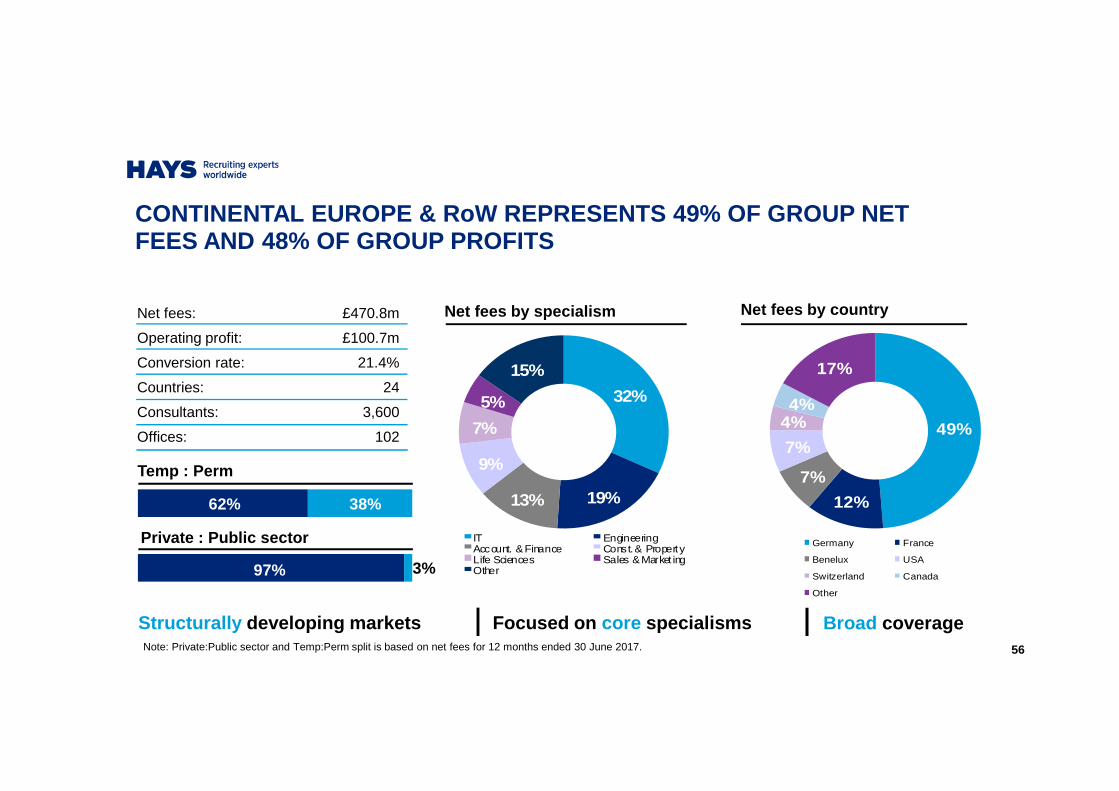

Net fees: £470.8m

Operating profit: £100.7m

Conversion rate: 21.4%

Countries: 24

Consultants: 3,600

Offices: 102

Note: Private:Public sector and Temp:Perm split is based on net fees for 12 months ended 30 June 2017.

Structurally developing markets Focused on core specialisms Broad coverage

CONTINENTAL EUROPE & RoW REPRESENTS 49% OF GROUP NE T FEES AND 48% OF GROUP PROFITS

Temp : Perm

Private : Public sector

62% 38%

Net fees by specialism Net fees by countryNet fees by specialism Net fees by country

97% 3%

32%

19%13%

9%

7%

5%

15%

IT EngineeringAccount. & Finance Const. & PropertyLife Sciences Sales & Market ingOther

49%

12%

7%

7%

4%4%

17%

Germany France

Benelux USA

Switzerland Canada

Other

56

Net fees by specialism Net fees by regionNet fees: £252.9m

Operating profit: £41.5m

Conversion rate: 16.4%

Consultants: 1,948

Offices: 98

Note: Private:Public sector and Temp:Perm split is based on net fees for 12 months ended 30 June 2017.* Market position is based on Hays estimates.

#1 market position* Diverse sector exposure Nationwide coverage

UK & IRELAND REPRESENTS 27% OF GROUP NET FEES

Temp : Perm

Private : Public sector

56% 44%

74% 26%

22%

20%

11%10%

9%

8%

20%

Account. & Finance Const. & PropertyOffice Support EducationIT Banking & Fin. Serv.Other

34%

27%

17%

10%

8% 4%

London North & ScotlandMidlands & E.Anglia Home CountiesSouth West & Wales Ireland

57

PROFILE OF HAYS AUSTRALIA & NEW ZEALAND

TEMP 66% PERM 34%

19% GROUP NET FEES

911 CONSULTANTS

38 OFFICES

Net fees by specialism Net fees by region

Construction & Property

Acc. & Finance

Office Support IT Other

27% 14% 12% 10% 7% 26%

£181m £63m 35%

NSW Victoria WA

Q’la

nd Other

30% 23% 11% 9% 9% 18%

ACT

Note: All data is presented as of 30 June 2017. * Includes Oil & Gas and Energy.

NET FEES EBIT CONV. RATE

Year ended 30 June 2017

58

Ban

king

Res

&

Min

ing*

4%

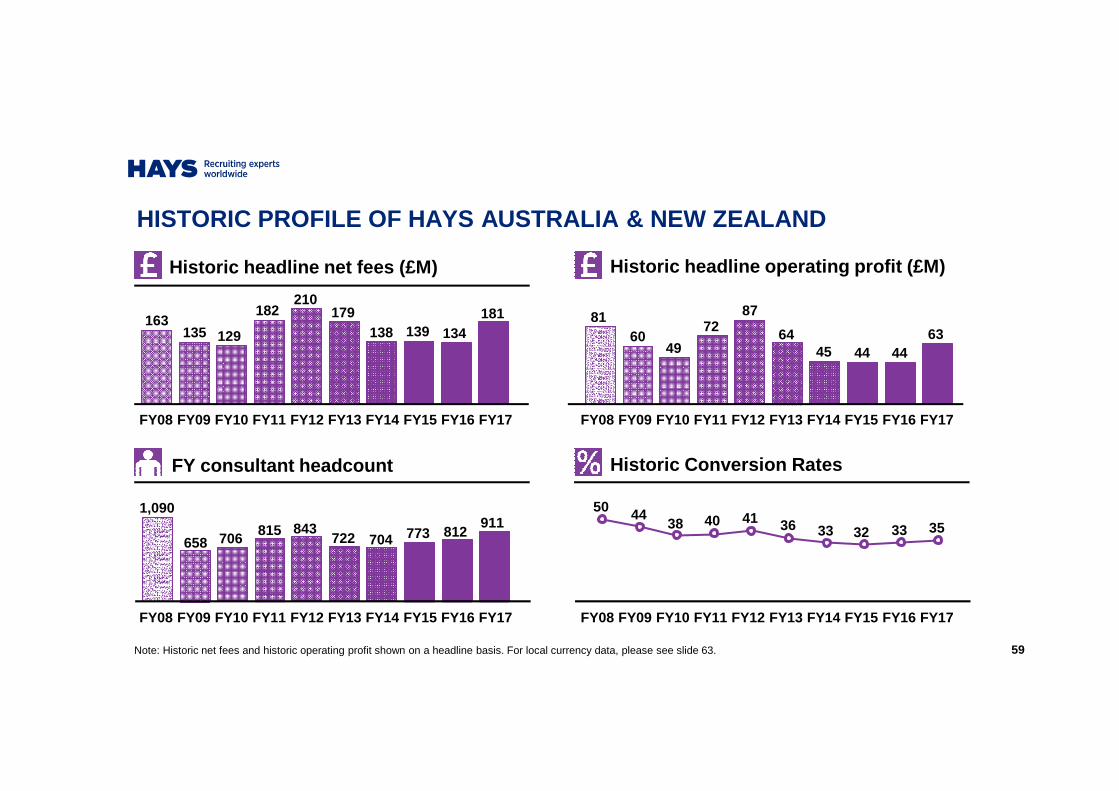

HISTORIC PROFILE OF HAYS AUSTRALIA & NEW ZEALAND

134139138179

210182

129

FY16FY15FY14FY13FY12FY11FY08

FY consultant headcount Historic Conversion Rates

Historic headline net fees (£M) Historic headline operating profit (£M)

Note: Historic net fees and historic operating profit shown on a headline basis. For local currency data, please see slide 63. 59

181

FY17FY09 FY10

135163

44444564

8772

49

FY16FY15FY14FY13FY12FY11FY08

63

FY17FY09 FY10

6081

812773704722815706

FY16FY15FY14FY13FY12FY11FY08

911

FY17FY09 FY10

658

1,090

333233364038

FY16FY15FY14FY13FY12FY11FY08

35

FY17FY09 FY10

4450

84341

PROFILE OF HAYS GERMANY

TEMP 87% PERM 13%

24% GROUP NET FEES

1,503 CONSULTANTS

19 OFFICES

Net fees by specialism Net fees by contract type

Note: All data is presented as of 30 June 2017.

IT Engineering

42% 30% 11%

Contracting Temp Perm

62% 25% 13%

£230m £81m 35%NET FEES EBIT CONV. RATE

Year ended 30 June 2017

60

Other Acc. & Finance

17%

HISTORIC PROFILE OF HAYS GERMANY

FY consultant headcount Historic Conversion Rates

Historic headline net fees (£M) Historic headline operating profit (£M)

Note: Historic net fees and historic operating profit shown on a headline basis. For local currency data, please see slide 63. 61

175158164150106

80

FY16FY15FY14FY13FY12FY11FY08

230

FY17FY09 FY10

8863

136

1,2131,088944940

670479

FY16FY15FY14FY13FY12FY11FY08

1,503

FY17FY09 FY10

463452786

636062585238

26

FY16FY15FY14FY13FY12FY11FY08

81

FY17FY09 FY10

3624

363838383633

FY16FY15FY14FY13FY12FY11FY08

35

FY17FY09 FY10

4138 38

HISTORIC PROFILE OF HAYS UK & IRELAND

FY consultant headcount Historic Conversion Rates

Historic headline net fees (£M) Historic headline operating profit (£M)££

Note: Historic net fees and historic operating profit shown on a headline basis. 62

272272246222225242244

FY16FY15FY14FY13FY12FY11FY08

253

FY17FY09 FY10

331

453

2,0242,2032,1571,9292,1582,272

FY16FY15FY14FY13FY12FY11FY08

1,948

FY17FY09 FY10

2,315

3,128

1,934

524626

6(7)411

FY16FY15FY14FY13FY12FY11FY08

42

FY17FY09 FY10

64

137

191711

315

FY16FY15FY14FY13FY12FY11FY08

16

FY17FY09 FY10

1930

(3)

LOCAL CURRENCY – HAYS NET FEES AND OPERATING PROFIT Australia & New ZealandHistoric net fees (AUDm)

Australia & New ZealandHistoric operating profit (AUDm)

GermanyHistoric net fees (EURm)

GermanyHistoric operating profit (EURm)

63

273263245274323293

232

FY16FY15FY14FY13FY12FY11FY08

305

FY17FY09 FY10

293365

90838098

134116

88

FY16FY15FY14FY13FY12FY11FY08

106

FY17FY09 FY10

130

182

234208197182

12491

FY16FY15FY14FY13FY12FY11FY08

268

FY17FY09 FY10

10386

161

85797470

4430

FY16FY15FY14FY13FY12FY11FY08

94

FY17FY09 FY10

4233

62

FURTHER INFORMATION

HEAD OF INVESTOR RELATIONS DAVID [email protected]+44 207 391 6613

For more information about the Group: haysplc.com/investors or @haysplcIR