potential impact of consumer behaviour and fossil fuelled

TRANSCRIPT

Potential Impact of Consumer Behaviour and Fossil Fuelled

Hydrogen Generation on National y gEnergy Policy of New Zealand

Jonathan Leaver MS(Stanford) PhD (Auckland)

Dept of Civil Engineering, Unitec NZp g g,

Luke Leaver BE(Hons) MS(Stanford)Asia Pacific Energy Research Centre

AcknowledgementsResearchers• Kenneth Gillingham, AB (Dartmouth), MS (Stanford), MA (Auckland)

• Andrew Baglino BS(Hons)(Stanford)d e ag o S( o s)(S a o d)

Adviser and Dedication• Dr Paul Kruger (Stanford) (deceased)

Project PartnersProject Partners• Dr Tony Clemens (deceased) – CRL Energy

• Alister Gardner - Industrial Research Ltd

Outline

U.S. U.S. –– N.Z. National Energy ProfilesN.Z. National Energy ProfilesUniSyDUniSyD ModelModelScenario ResultsScenario Resultsa o ua o uConclusionsConclusions

Part 1: U.S. and N.Z. National Profiles

USA

N Z l dNew Zealand

Source: http://en.wikipedia.org/

U.S. – N.Z. Economy 2009

52.9

46.4

US New Zealand

33.529.3

27.4

9.36.2

15.8

-1.6 -2.6

% Econ.Growth % Unemployment % Public debt/GDP

GDP/Cap (US$1000)

Pop density (ca/sq. km)

Source: CIA – The World Factbook

Selected Resource Potential40

p-20

10)

U.S. New Zealand

119

30

tion

(MW

h/ca

20

dded

Gen

erat

US - 2010 = 13.8

10

Pot

entia

l Ad NZ - 2010 = 10.2

0Coal* Wind CSP* Nuclear Geothermal Hydro Solar hot

water

Note: *Coal based on 100 years of generation. CSP=concentrated solar power.Sources: NZ: MED EHMS 2005, MED Energy Outlook 2009

U.S.: MIT Update of MIT Future of Nuclear Power 2009, NREL Estimates of Wind Resource Potential 2010, The Future of Geothermal Energy MIT/DOE 2006, NREL Potential of Solar Water Heating NREL/TP-640-41157 2007, U.S. Hydropower Resources INEEL/EXT-03-00662, BP Statistical Review of World Energy.

Part 2: UNISYD Model

Models NZ’s Energy-Economic System• Detailed technological specificity and resource • Detailed technological specificity and resource

modelling– 1100 primary variables, 7000 lines of code

• Simulates in biweekly time steps• Simulates in biweekly time steps.• 13 NZ regions

Primary SectorsPrimary Sectors• Electricity Market • Hydrogen Market• Lignocellulose market• Vehicle Fleet Market

Modelled Regions

© Unitec New Zealand8

UniSyD Model

Petrol Fleet

H2KM/ Y

PetrolKM/ Y

H2 FleetElectric Fleet

Electricity KM/Y

Structure PetrolKM/ L

and $/ KMH2

DemandPetrol

Demand Transport

VehicleSales

H2KM/ KG

and $/ K M

GDPPop

Electricity KM/J and $/KM

Pop

Electricity Demand

Electricity

Carbon Emissions

GDPPop

Electrolyzers

Electricity Generation

Electricity

ElectricityMarket

HydrogenMarket

St

Coal Gasifiers

and Cogenerators

PetroleumExtraction and

Imports

Natural GasExtraction

and Imports

CoalMining

Steam Methane

Reformers

BiomassGasification

HydrogenF il

FossilResources

LEGEND

SupplyDemand

Price Signal

Fossil

Fuel

Prices

BioFuels not included

Electricity Market - Overview

• DemandExogenous demand growth– Exogenous demand growth

– Dynamic interaction with price signals• Supply: generation options (+sequestration option)

– Coal– Natural gas– Hydro– Geothermal– e-/H2 Cogeneration– Biomass

S l PV– Solar PV– Wind– Solar Thermal

Combined Heat and Power

Huntly. Source: Genesis Energy

– Combined Heat and Power– Microgeneration

Electricity Generation

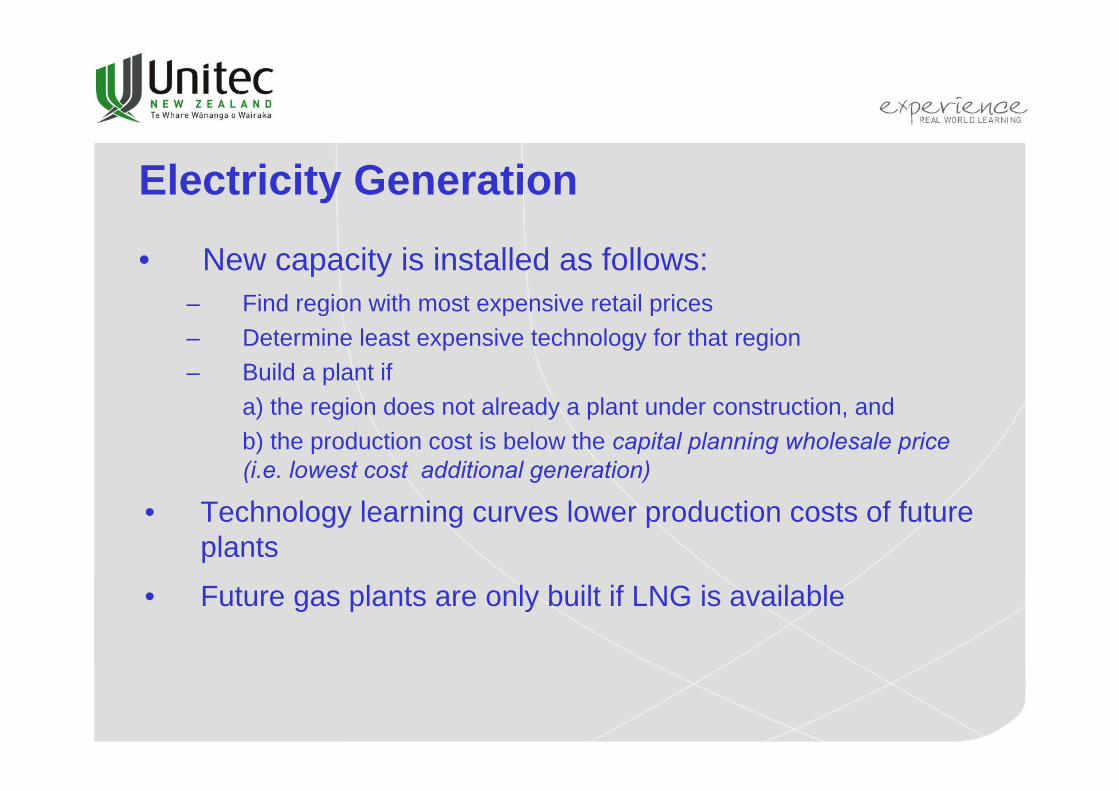

• New capacity is installed as follows:– Find region with most expensive retail prices– Find region with most expensive retail prices– Determine least expensive technology for that region– Build a plant if

a) the region does not already a plant under construction, and b) the production cost is below the capital planning wholesale price (i.e. lowest cost additional generation)

• Technology learning curves lower production costs of future plants

• Future gas plants are only built if LNG is available

Hydrogen Market Overview

• There are 4 centralised plant types, each with 5 sizes:– Biomass gasification– Biomass gasification.– Coal gasification.– Coal co-generation of hydrogen and electricity using a solid oxide fuel

ll t i l d t i CO2cell topping cycle and sequestering CO2.– Large steam methane reforming.

• Delivery is via liquid hydrogen tankersDelivery is via liquid hydrogen tankers– considered to be the most economic for New Zealand

• Forecourt generation includes SSMR and electrolysisForecourt generation includes SSMR and electrolysis– steam methane reforming is unavailable in the South Island, where there

is no reticulated gas.– forecourt generators are must-use, or base load.

Lignocellulose (Forest) Market - Overview

• Bio-ethanol from forests and biodiesel from rape seed crop

• New biomass development cannot exceed the regional supply limit.

• Marginal pricing system with H2 from biogasification, bioethanol and biomass electricity generation competing for the same fuel.

Vehicle Choice: Logit A – 1st Option

• Logit choice model used for market share, S, of vehicle type, i:yp ,

1 1 11

exp( )exp( )i i i

pSp

β γβ γ

−=

−∑

p is the annual cost

i∑

Β is the price elasticityγ the intrinsic preference parameter

Vehicle Choice: Logit B – 2nd Option

• The market share, S, is function of:F l t k f ICEV• Fuel cost per km from ICEV

• Purchase price from ICEV

• Driving range (km)Driving range (km)

• Convenient medium range destinations requiring no advanced planning.

• Proportion of long range destinations that can be reached.

• Reluctance to drive ICEVs.

Note: CMDD and PLDD utility factors for EVs are sigmoid functions of the % of fleet penetration

Vehicle Fleets

Vehicle Type Modelled Profile

ICEVs, H2ICEVs, BICEVs, HEV PHEV BEV

Imported Used North Island

Light South IslandHEVs, PHEVs, BEVs, FCVs,

New North Island

South Island

Heavy North IslandHeavy North Island

South Island

Vehicle Fuel EconomyFuel Economy (km/kWh)

Vehicle Type Imported Light New Light Heavy

ICEV/HICEVLow Bound 1.24 1.21 0.40ICEV/HICEVHigh Bound 2.17 2.17 0.62

HFCVLow Bound 3.09 3.09 0.89Hi h B dHigh Bound 3.36 3.36 0.97

BEV(320 km range)

Low Bound 4.50 4.50 1.35

High Bound 5 10 5 10 1 52( g ) High Bound 5.10 5.10 1.52

Light Vehicle: Specific Fuel Cost

Fuel Cost0.30

$/km

)

Fuel CostBioEthanolH2ICEVPetrolFCVEV

0 10

0.20

Cos

t (U

S$ EV

0 00

0.10

Fuel

0.002010 2020 2030 2040 2050

Year

18

Vehicle Cost and Payback

24

32k

(yea

rs)

Logit A - No weighting

Low bound

High bound24

32

(yea

rs)

Logit B - Consumer weighted

Low bound

High bound

8

16

Sim

ple

Pay

back

8

16

Sim

ple

Pay

back

0Turbo Diesel HEV PHEV-48

kmHFCV PHEV-96

kmBEV

24000Low bound

24000Low bound

0Turbo Diesel HEV PHEV-48

kmHFCV PHEV-96

kmBEV

12000

18000

vehi

cle

cost

(US

$) High bound

12000

18000

ehic

le c

ost (

US

$) High bound

0

6000

Turbo Diesel HEV PHEV-48 km

HFCV PHEV-96 km

BEV

Ext

ra v

0

6000

Turbo Diesel HEV PHEV-48 km

HFCV PHEV-96 km

BEV

Ext

ra v

e

19

Gasoline US$1.00/litre (US$3.80/gal); electricity US$0.05/kWh; H2 US$3.50/kg; 20,000 km per year, BEV (320 km range).Data from: Matthew A. Kromer and John B. Heywood May 2007 “Electric Powertrains: Opportunities and Challenges in the U.S. Light-Duty Vehicle Fleet “, MIT Report LFEE 2007-02 RP

km km km km

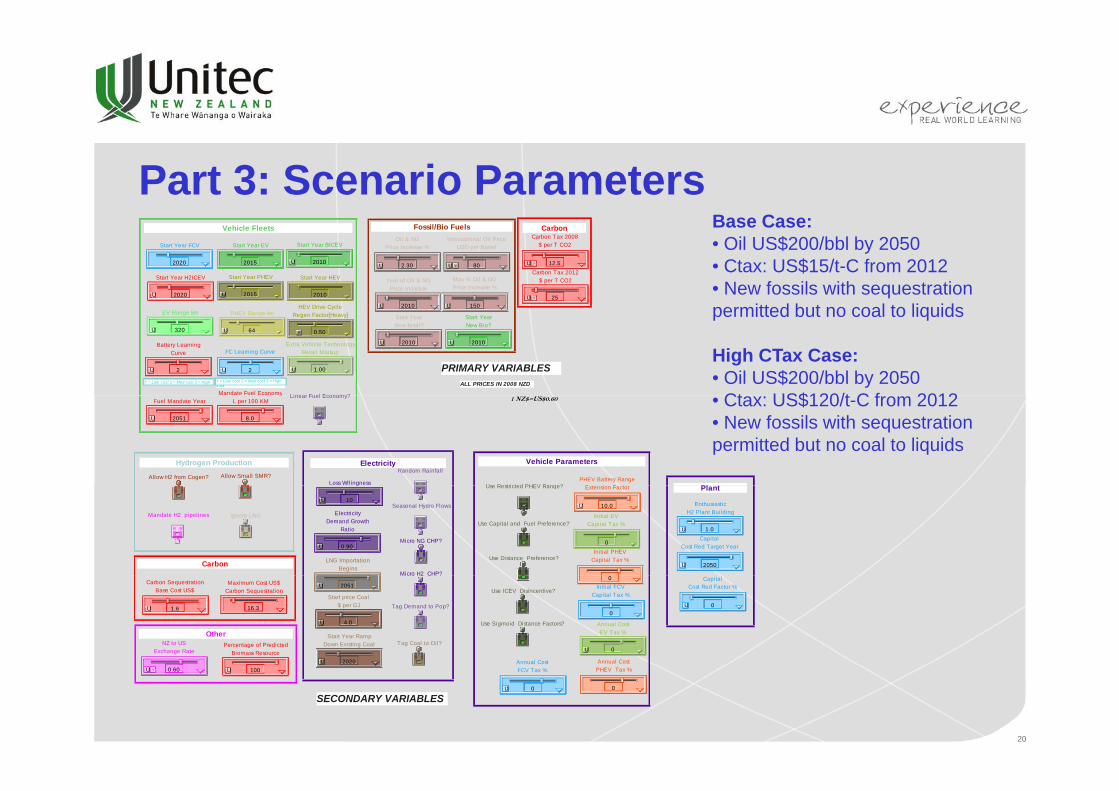

Part 3: Scenario ParametersB CBase Case:• Oil US$200/bbl by 2050• Ctax: US$15/t-C from 2012• New fossils with sequestration

itt d b t l t li id

2.30U

Oil & NG Price Increase %

2020U

Start Year H2ICEV

2015U

Start Year PHEV

2015

Start Year EV

80?U

International Oil PriceUSD per Barrel

12.5?U

Carbon Tax 2008$ per T CO2

25?U

Carbon Tax 2012$ per T CO2

2020

Start Year FCV

2010

Start Year HEV

150U

Max % Oil & NG Price Increase %

2010U

Year of Oil & NG Price Increase

2010U

Start Year BICEV

HEV Drive Cycle

Vehicle Fleets CarbonFossil/Bio Fuels

permitted but no coal to liquids

High CTax Case:• Oil US$200/bbl by 2050

Ct US$120/t C f 2012

2U

Battery Learning Curve

2U

FC Learning Curve2010U

Start Year New fossil?

1.00U

Extra Vehicle TechnologyRetai l Markup

150U2010U

320U

EV Range km

Mandate Fuel Economy

2010U

Start Year New Bio?

64U

PHEV Range km

Linear Fuel Economy?

0.50?

HEV Drive Cycle Regen Factor[Heavy]

ALL PRICES IN 2008 NZD1 = Low cost 2 = Med cost 3 = High 1 = Low cost 2 = Med cost 3 = High cost

PRIMARY VARIABLES

1 NZ$=US$0.60 • Ctax: US$120/t-C from 2012• New fossils with sequestration permitted but no coal to liquids

Allow H2 from Cogen? Allow Small SMR? PHEV Battery Range E t i F t

8.0

yL per 100 KM

Random Rainfall

Loss Wll ingness

2051U

Fuel Mandate YearLinear Fuel Economy?

Use Restricted PHEV Range?

Vehicle ParametersElectricity

Pl t

Hydrogen Production

Ignore LNG

LNG ImportationBegins

Micro NG CHP?

Seasonal Hydro Flows

Micro H2 CHP?

Use Distance Preference?

0

Initial EVCapital Tax %

Mandate H2 pipelines

Initial PHEVCapital Tax %

10.0U

Extension Factor

2050U

Capital Cost Red Target Year

Use Capital and Fuel Preference?

10U

g Use Restricted PHEV Range?

0.90U

ElectricityDemand Growth

Ratio 1.0U

EnthusiasticH2 Plant Building

Carbon

Plant

16.3

Maximum Cost US$Carbon Sequestration

NZ to USExchange Rate

2051U

4.0U

Start price Coal$ per GJ

0

Initial FCVCapital Tax %

Micro H2 CHP?

Use ICEV Disincentive?

0

Tag Coal to Oil?

2020U

Start Year Ramp Down Existing CoalPercentage of Predicted

Biomass Resource

0U

Capital Cost Red Factor %

Use Sigmoid Distance Factors?

Annual Cost

0U

Annual Cost EV Tax %

Annual Cost

Tag Demand to Pop?1.6U

Carbon SequestrationBase Cost US$

Other

20

0.60?U 100U

0U

FCV Tax %

0

PHEV Tax %

SECONDARY VARIABLES

Electricity and Vehicle Fleet Profiles

Low CtaxLogit A

0.30

0.40

S$/k

Wh)

National Wholesale Electricity Price

300

400

atio

n (P

J)

National ElectricityHydroDG CogenCoalGeothermalBioNatural Gas

4000

6000

(100

0s)

Vehicle Fleet Nos

Light BICEVLight FCVLight EVLogit A

0.00

0.10

0.20

2010 2020 2030 2040 2050Who

lesa

le P

rice

(US

Year

0

100

200

2010 2020 2030 2040 2050Elec

trici

ty G

ener

a

Year

Natural GasH2 CogenSolar ThermalWindBioEth CogenGovt-DieselElectricity Demand

0

2000

2010 2020 2030 2040 2050

Vehi

cle

No.

(

Year

Light PHEVLight HEVLight Petrol

Low CtaxLogit B

0 10

0.20

0.30

0.40

Pric

e (U

S$/

kWh)

National Wholesale Electricity Price

100

200

300

400

y G

ener

atio

n (P

J)

National ElectricityHydroDG CogenCoalGeothermalBioNatural GasH2 CogenSolar ThermalWindBioEth Cogen

2000

4000

6000

cle

No.

(100

0s)

Vehicle Fleet Nos

Light BICEVLight FCVLight EVLight PHEVLight HEVLi ht P t l

0.00

0.10

2010 2020 2030 2040 2050Who

lesa

le P

Year

0

100

2010 2020 2030 2040 2050Elec

trici

ty

Year

BioEth CogenGovt-DieselElectricity Demand

0.40National Wholesale Electricity Price

400

)

National ElectricityHydroDG Cogen

02010 2020 2030 2040 2050

Vehi

Year

Light Petrol

6000Vehicle Fleet Nos

Light BICEV

High CtaxLogit A

0.00

0.10

0.20

0.30

hole

sale

Pric

e (U

S$/k

Wh)

0

100

200

300

Elec

trici

ty G

ener

atio

n (P

J)

gCoalGeothermalBioNatural GasH2 CogenSolar ThermalWindBioEth CogenGovt-DieselElectricity Demand

0

2000

4000

Vehi

cle

No.

(100

0s) Light BICEV

Light FCVLight EVLight PHEVLight HEVLight Petrol

21

2010 2020 2030 2040 2050Wh

Year2010 2020 2030 2040 2050E

Year2010 2020 2030 2040 2050

Year

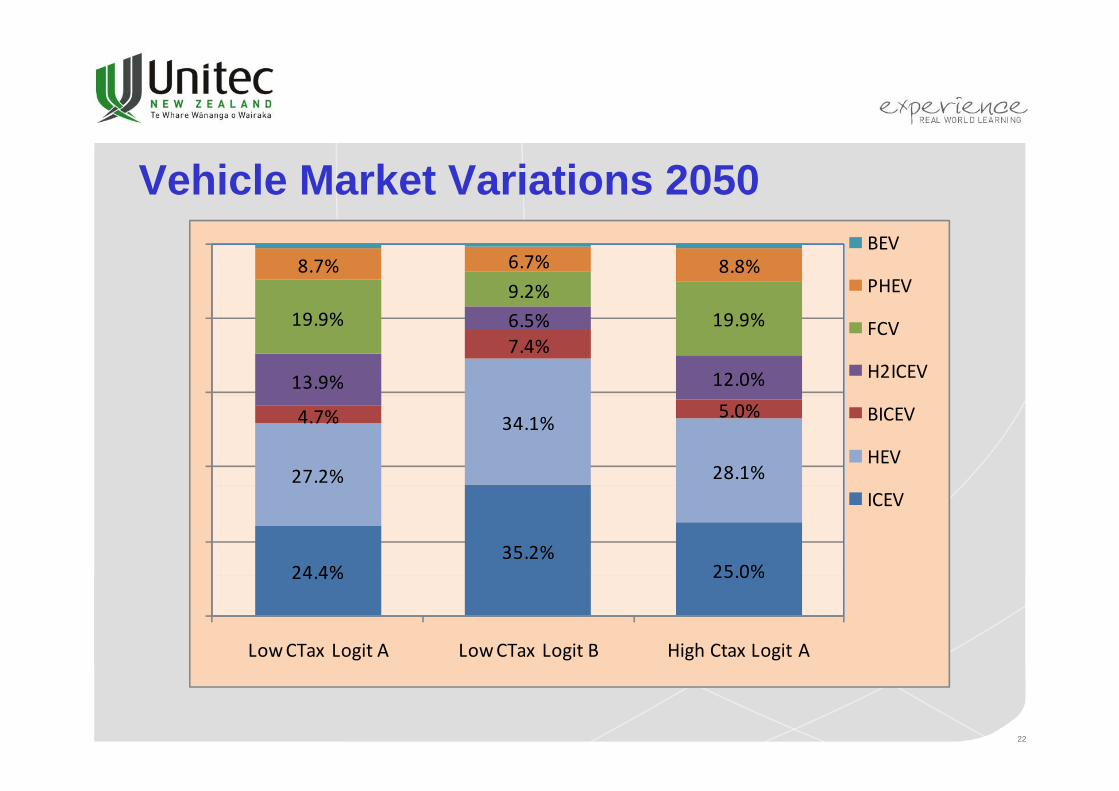

Vehicle Market Variations 2050

9.2%8.7% 6.7% 8.8%

BEV

PHEV

7.4%

13.9%

6.5%

12.0%

19.9% 19.9% FCV

H2ICEV

27.2%

34.1%

28.1%

4.7% 5.0% BICEV

HEV

24 4%35.2%

25 0%

ICEV

24.4% 25.0%

Low CTax Logit A Low CTax Logit B High Ctax Logit A

22

Greenhouse Gas Emissions

Low CtaxLogit A 20

30

40

sions

(Mt)

GHG EmissionsSequesteredEmitted due to Seq ConstraintEmitted 15

20

e (U

S$/k

g)

National Wholesale Hydrogen Price

South Island

North Island600

800

atio

n (k

t)

National Hydrogen

Large SMRCogenBioGasificationCoal GasificationSmall SMRLogit A

0

10

20

2010 2020 2030 2040 2050

CO

2 E

mis

s

Year

0

5

10

2010 2020 2030 2040 2050

Who

lesa

le P

rice

Year

0

200

400

2010 2020 2030 2040 2050

H2

Gen

era

Year

Small SMRElectrolysis

Low CtaxLogit B 20

30

40

2 Em

issio

ns (M

t)

GHG EmissionsSequesteredEmitted due to Seq ConstraintEmitted

10

15

20

e P

rice

(US

$/kg

)

National Wholesale Hydrogen Price

South Island

North Island

400

600

800

Gen

erat

ion

(kt)

National Hydrogen

Large SMRCogenBioGasificationCoal GasificationSmall SMRElectrolysis

40GHG Emissions

S d

0

10

2010 2020 2030 2040 2050

CO

2

Year

20National Wholesale Hydrogen Price

800National Hydrogen

L SMR

0

5

2010 2020 2030 2040 2050

Who

lesa

le

Year

0

200

2010 2020 2030 2040 2050

H2

G

Year

High CtaxLogit A

10

20

30

CO

2 E

miss

ions

(Mt)

SequesteredEmitted due to Seq ConstraintEmitted

5

10

15

0

esal

e H

2 Pr

ice

(US

$/kg

)

South IslandNorth Island

200

400

600

800

H2

Gen

erat

ion

(kt)

Large SMRCogenBioGasificationCoal GasificationSmall SMRElectrolysis

23

02010 2020 2030 2040 2050

Year

02010 2020 2030 2040 2050W

hole

Year

02010 2020 2030 2040 2050

Year

Conclusions• In the base case scenario using the Logit B consumer weightings of

capital and fuel costs results in a 34% increase in CVs (ICEVs, HEVs) in 2050HEVs) in 2050.

• Increasing the carbon tax in the Logit A case from US$15/t-CO2-eq to US$120/t-CO2-eq results in:2 eq

– Reduction of CVs from 69% to 52% by 2050.– A 27% increase in GHG emissions from 2010 levels due to lack of sequestration

capacity.

• To counter consumer resistance to the purchase of higher priced electric drive vehicles it is advisable to capitalise fuel savings with a fuel tax and subsidise the capital cost.

• A cap and trade policy may be necessary to keep GHG emissions at or below 2010 levels due to the production of hydrogen from advanced technology plants producing hydrogen by coaladvanced technology plants producing hydrogen by coal gasification.

Questions? Pohutu Geyser, Rotorua Akaroa, South Island

Kereru (Native Wood Pigeon)

Lake Pukaki & Mt Aoraki (Cook) 3,754 metres, 12,316 ft

Omaha Beach, North Auckland

25