population - · pdf filename burlington northern santa fe, ... no. of international courier...

TRANSCRIPT

Clark County Demographic Profile 2015

Sources: State of Washington Office of Financial Management, Washington Employment Security Department, and US Census Bureau (2015)

POPULATION

POPULATION BY CITY

Population

Projections 1990 2000 2010 2014 2020 2030 2040

Clark County Total 238,053 345,238 425,363 442,800 509,876 567,982 585,137

Battle Ground 3,758 9,296 17,571 18,680

Camas 6,442 12,534 19,355 20,880

La Center 483 1,654 2,800 3,050

Ridgefield 1,332 2,147 4,763 6,035

Vancouver 46,380 143,560 161,791 167,400

Washougal 4,764 8,595 14,095 14,910

Yacolt 600 1,055 1,566 1,620

POPULATION BY CITY 2014

POPULATION BY AGE Age Group 1990 2000 2010 2014

Under – 20 74,472 108,037 123,429 120,996

20 – 34 53,569 68,789 79,268 82,835

35 – 54 66,752 107,377 121,580 121,245

55 – 74 32,766 45,362 80,458 94,548

75 & Older 10,194 15,673 20,628 23,175

18,680

20,880 3,050

6,035

167,400

14,910 1,620 Battle Ground

Camas

La Center

Ridgefield

Vancouver

Washougal

Yacolt

Clark County Demographic Profile 2015

Sources: State of Washington Office of Financial Management, Washington Employment Security Department, and US Census Bureau (2015)

POPULATION DISTRIBUTION

Distribution by Age Group 1990 2000 2010 2013 Under – 20 31% 31% 29% 28%

20 – 34 23% 20% 19% 19%

35 – 54 28% 31% 29% 28%

55 – 74 14% 13% 18% 20%

75- Older 4% 5% 5% 5%

Median Age 33.47 34.20 36.70 37.30

POPULATION DIVERSITY Total Population by Race

2000 Census 2010 Census

Total % of Total Total % of Total

Total Population 345,238 100% 425,363 100%

White 306,648 88.8% 363,397 85.4%

Black/African American 5,813 1.7% 8,426 1.9%

American Indian/Alaska Native 2,910 0.8% 3,624 0.9%

Asian and Pacific Islander 12,369 3.6% 20,212 4.8%

Two or More Races 10,641 3.1% 17,219 4.0%

Some Other Race alone 6,857 2.0% 12,485 3.0%

Hispanic Origin (of any race) 18,248 4.7% 32,166 7.6%

CLARK COUNTY HOUSEHOLDS

HOUSEHOLD SUMMARY Households 1990 2000 2010 2013

Total Households 92,849 127,290 155,533 170,752

Median Household Income $31,800 $51,232 $54,924 $58,225

Household Income Distribution

Under - $35,000 48,942 42,171 43,860 48,832

$35,001 - $50,000 18,659 23,938 23,952 22,965

$50,001 - $75,000 14,530 30,448 35,773 32,148

$75,001 - Above 6,440 30,733 59,103 59,910

Clark County Demographic Profile 2015

Sources: State of Washington Office of Financial Management, Washington Employment Security Department, and US Census Bureau (2015)

MIGRATION

MIGRATION

Clark County Net Migration 2000-2005 2006-2010 2011-Present

34,817 15,571 7,696

EDUCATIONAL ATTAINMENT

WORKFORCE EDUCATIONAL ATTAINMENT

Highest Level Completed Percentage

2000 2010 2013 Under – 12 Years 12.3% 9.2% 8.2%

K – 12 Only 27% 26.6% 26.7% Some College 30.4% 28.6% 27.0% Associate Degree 8.3% 9.9% 11.2%

High School Degree or Higher Not Available 91.1% 91.8% College Graduates 14.5% 16.8% 17.5%

Graduate + 7.5% 8.9% 9.4% Bachelor’s Degree or Higher Not Available 24.6% 26.9%

8%

26%

26.9%

26%

Clark County Labor Force Characteristics 2015

Sources: US Census Bureau “On The Map”, Washington Employment Security Department, and US Census Bureau (2015)

LABOR FORCE CHARACTERISTICS

CIVILIAN LABOR FORCE

2010

2011

2012

2013

2014 2015

Civilian Labor Force 217,620 214,130 208,930 209,130 209,280 212,940

Unemployment Rate 4.0% 12.4% 9.9% 11.6% 8.9% 7.8%

EMPLOYMENT BY INDUSTRY Non-Agricultural Employment Reported

by Place of Work Total Number Employed % of Total Employed

Persons 2005 2010 2015 2005 2011 2015

Construction, Mining, and Logging 12,500 8,100 9,900 9.70% 6.30% 5.92%

Manufacturing 13,800 11,500 13,300 10.71% 8.99% 7.96%

Wholesale Trade 5,200 5,400 6,400 4.03% 4.22% 3.83%

Retail Trade 15,000 15,700 17,000 11.64% 12.28% 10.18%

Transportation, Warehousing, and Utilities 3,700 4,100 3,800 2.87% 3.20% 2.23%

Information 2,900 2,600 3,100 2.25% 2.03% 1.86%

Finance and Insurance 4,000 3,600 4,900 3.10% 2.80% 2.93%

Real Estate, Rental & Leasing 2,700 2,200 2,300 2.09% 1.72% 1.38%

Professional, Scientific, and Technical Services 6,400 8,300 8,100 4.97% 6.49% 4.85%

Administrative Support and Waste Management 6,800 6,400 7,100 5.28% 5.00% 4.25%

Education Services 1,100 1,300 25,200 0.85% 1.02% 15.09%

Health Care and Social Assistance 15,000 18,100 23,400 11.64% 14.16% 14.01%

Arts, Entertainment and Recreation 2,300 2,000 2,000 1.78% 1.56% 1.20%

Accommodation and Food Services 9,800 9,800 11,000 7.60% 7.67% 6.59%

Other Services 4,300 4,800 5,500 3.34% 3.75% 3.29%

Government 22,500 23,900 24,000 17.49% 18.70% 14.37%

Total 128,900 127,800 167,000 99.31% 99.89% 99.94%

Clark County Labor Force Characteristics 2015

Sources: US Census Bureau “On The Map”, Washington Employment Security Department, and US Census Bureau (2015)

OUTFLOW JOB COUNTS IN CLARK COUNTY

2002 2005 2010 Count Share Count Share Count Share

Employed Clark County Residents Working Outside of Clark County

66,142

45%

76,832

47%

80,823

49%

Commute Distance Count Share Count Share Count Share Less than 10 mile 70,110 69% 74,899 67% 72,822 61%

10-24 miles 19,762 20% 22,053 20% 23,166 19%

25-50 miles 3,107 3% 3,533 3% 4,731 4%

Greater than 50 miles 8,141 8% 10,710 10% 19,136 16%

Median (Miles) 24.7 25.0 26.8 LABOR FORCE

Labor Participation Rate 2000 Percentage (%)

2005 Percentage (%)

2010 Percentage (%)

Male 55% 40% 47%

Female 45% 60% 53%

Total 100% 100% 100%

Education and Labor Force 2000

Enrollment 2005

Enrollment 2011

Enrollment

High School (Public and Private)

19,901

23,322

26,416

Four Year University (Full-Time)

22,974

21,999

22,017

ANNUAL WAGES BY INDUSTRY, 2014 Mean Wage Entry Level Wage Experienced Wage

All Occupations $48,109 $23,400 $60,464

Management Occupations $111,364 $62,462 $135,815

Financial Specialist $71,198 $43,434 $85,079

Computer Software Engineer $95,071 $66,890 $109,962

Electronics Engineer $103,997

$75,703 $118,145

Machinist $41,371 $28,430 $47,840

Production Workers $27,497 $21,953 $30,296

Office/Administrative Workers $35,663 $25,967 $40,510

Healthcare Support Occupations $34,183 $23,660 $39,444

Clark County Infrastructure Profile 2015

Compiled by CREDC, 2015

TRANSPORTATION AND INFRASTRUCTURE

DISTANCE TO NEAREST METRO AREAS

City Miles Portland – City Center 10

Seattle, WA 179

Vancouver, B.C., Canada 309

Spokane, WA 343

Boise, ID 432

San Francisco, CA 699

RAIL

Railroads (by Rail Carrier) Name Burlington Northern Santa Fe, Union Pacific RR, Canadian Pacific RR

Main or Branch Line Burlington Northern Santa Fe - Main Line

Shortline or National National

Nearest Switching Yard Port of Vancouver, USA

PORTS

WATER PORTS Port of Vancouver, USA Nearest Port Port of Vancouver USA

River, Lake, or Ocean Columbia River

Channel Depth 40 feet at mean low water

Turning Basin Yes

Barging Facilities Yes

General Cargo Facilities Yes

Containerized Facilities Yes

Storage Facilities Yes

Highways Serving Port Interstate 5, Interstate 84, Interstate 205, and State Route 14

Railways Serving Port

Burlington Northern Santa Fe, Union Pacific, Canadian Nation and Canadian Pacific

No. of Freight Forwarders Serving Area 39

No. of Import/Export Brokers Serving Area

6

No. of International Courier Firms Serving Area

6

Clark County Infrastructure Profile 2015

Compiled by CREDC, 2015

AIRPORT Portland International Airport Name Portland International Airport (PDX)

Hub Status Alaska Airlines (Horizon Airlines) and SeaPort Airlines

Distance from Community (in miles) 10

Hours of Operation 24 hours

Number of Runways 3

Runway Lengths 6,000 ft, 9,825 ft, and 11,000 ft Scheduled Passenger Carriers Serving PDX Air Canada, Alaska Airlines, American Airlines, Condor, Delta, Frontier, Hawaiian

Airlines, Icelandair, jetBlue, SeaPort Airlines, Southwest, Spirit Airlines, United, US Airways, Virgin America, and Volaris

Scheduled Air Cargo Carriers Serving PDX

Air Canada, Alaska Airlines, AmericanAirlines, Ameriflight, DHL, Empire Airlines, FedEx, Frontier, Hawaiian Airlines, United, UPS, US Airways, Western Air Express

Total No. of Non-stop Destinations 58

Carriers to Largest Non-Stop Metro Areas Served

Domestic:

New York City (JFK, EWR) Delta, jetBlue, United

Los Angeles Basin (LAX, BUR, SBA) Alaska Airlines, Delta, Southwest

Chicago (ORD, MDW) Alaska Airlines, American Airlines, Spirit, United, Southwest

Dallas-Fort Worth Alaska Airlines, American Airlines, Spirit, Southwest

Houston (HOU, IAH) Southwest, United

Philadelphia US Airways

Washington, DC (DCA, IAD) Alaska Airlines, United

Atlanta Alaska Airlines, Delta

Boston Alaska Airlines, jetBlue

Phoenix Alaska Airlines, Southwest, US Airways

San Francisco Bay Area (SFO, OAK, SJC) Alaska Airlines, United, Virgin America

Seattle Alaska Airlines, Delta, United

International:

Tokyo, Japan Delta

Amsterdam, Netherlands Delta

Calgary, Alberta, Canada Air Canada

Vancouver, B.C., Canada Air Canada, Alaska Airlines

Frankfurt, Germany (Seasonal) Condor

Reykjavik, Iceland (Seasonal) Icelandair

No. of days closed due to inclement weather in last 3 years

zero

Clark County Infrastructure Profile 2015

Compiled by CREDC, 2015

Foreign Trade Zones in Area

Designation N/A

Number None

Site/Location N/A

NO. of Acres N/A

Operator N/A Custom Port of Entry in the Area Name Portland Service Port

Site/Location 8337 NE Alderwood Road #200 Portland, OR 97220 Warehouses No. of Bonded Warehouses in the Area 7 No. of Public Warehouses in the Area 31

POSTAL SERVICES Overnight Express Service Availability Federal Express

Latest Pick-Up Time 4:00 PM

First Overnight Delivery Time 8:00 AM

Standard Overnight Delivery Time 3:00 PM

Saturday/Sunday Delivery Available

Zone Classification Standard

UPS

Latest Pick-Up Time 6:00 PM

First Overnight Delivery Time 8:00 AM

Standard Overnight Delivery Time 3:00 PM

Saturday/Sunday Delivery Available

Zone Classification Standard

United States Postal Service

Nearest General Mail Vancouver, WA

Latest Pick-Up Time 8:30 PM

Earliest Delivery Next Day

Saturday/Sunday Delivery Available

Nearest Bulk Mail Facility Vancouver, WA

State and Local Tax Incentives 2015

For information on all Washington State tax incentives please visit: http://www.dor.wa.gov/Content/FindTaxesAndRates/TaxIncentives/IncentivePrograms.aspx

INCENTIVES BY INDUSTRY

AEROSPACE INCENTIVE DESCRIPTION B&O Tax Credit Who: Businesses who develop, design, and engineer commercial airplanes or component

parts of commercial airplanes. What: Provides a B&O tax credit for expenditures for aerospace preproduction development. The B&O tax credit is equal to 1.5% of qualified preproduction development expenditures.

Reduced B&O Tax Rate Who: Manufacturers and processors for hire of commercial airplanes or component parts of commercial airplanes, non-manufacturers engaged in the business of aerospace product development, certificated FAR repair stations making retail sales, and aerospace tooling manufacturers. What: Qualifying businesses receive a reduced B&O tax rate (the new rate is .002904 – a reduction of 40%)

B&O Tax Credit Who: Businesses that manufacture commercial airplanes or component parts of commercial airplanes. What: B&O tax credit equal to the property taxes paid on new buildings, the land upon which the new buildings are located; and property taxes attributable to the renovation or expansion of buildings used exclusively in the manufacturing of commercial airplanes or component parts of commercial airplanes.

Reduced B&O Rate Who: Persons certified by the FAA to perform repair and maintenance on commercial airplanes under FAR Part 145. What: Lower B&O tax rate for persons performing repair and maintenance on commercial airplanes.

Sales & Use Tax Exemption Who: Persons who develop, design, and engineer, but do not manufacture, commercial airplanes or component parts of commercial airplanes. What: Sales and use tax exemption for purchases of computer hardware, software and peripherals, and charges for labor and services related to the installation of such equipment.

HIGH-TECHNOLOGY INCENTIVE DESCRIPTION B&O Credit Who: Advanced computing, advanced materials, biotechnology, electronic device

technology, environmental technology. What: An annual credit of up to $2 million for high technology businesses that perform R&D in specific high technology categories.

Sales & Use Tax Deferral Who: Advanced computing, advanced materials, biotechnology, electronic device technology, environmental technology. What: Defers or waives sales and use tax associated with construction, expansion, or renovation of qualified buildings and acquisition of qualified machinery and equipment in research and development and pilot scale manufacturing in the above fields.

Sales & Use Tax Deferral/Waiver

Who: Biotechnology & Medical Device Manufacturers What: Defers or waives sales and use tax on machinery and equipment, construction costs for new or expanded facility.

State and Local Tax Incentives 2015

For information on all Washington State tax incentives please visit: http://www.dor.wa.gov/Content/FindTaxesAndRates/TaxIncentives/IncentivePrograms.aspx

INTERNATIONAL BUSINESSES

INCENTIVE DESCRIPTION B&O Tax Credit Who: Firms engaged in international services

What: May receive a tax credit of $3,000 per year for every new employment position, for up to five years. Firms must be located in one of the eight International Service Districts in Vancouver, WA, to qualify.

WAREHOUSES

INCENTIVE DESCRIPTION Sales Tax Remittance Who: Wholesalers, retail distribution centers, third-party warehousers, and cold storage

warehousers What: A remittance of 100% of state sales tax (6.5%) paid on construction of qualifying structures and a 50% remittance for state sales tax paid on qualifying equipment.

SOFTWARE

INCENTIVE DESCRIPTION Property Tax Exemption Who: Software companies

What: Software designed for a specific need for a single person or group of persons is exempt from property tax. Included in the definition is modification of canned computer software.

MANUFACTURING INCENTIVES

GENERAL MANUFACTURING

INCENTIVE DESCRIPTION Sales & Use Tax Exemption Who: Manufacturers, processors for hire, manufacturers who perform R&D. What:

Exempts sales and use tax on machinery and equipment used directly in manufacturing or research operations. Includes installation, maintenance, and repairs in most cases.

FOOD PROCESSING/MANUFACTURING INCENTIVE DESCRIPTION B&O Tax Exemption Who: Manufacturers and processors of fresh fruit & vegetables, dairy products, and

seafood products. What: B&O tax exemption for goods destined for outside Washington. Defers or waives sales and use tax on machinery and equipment, construction costs for new or expanded facility. Expands the warehouse remittance program to include cold storage warehouses or fresh fruit & vegetables, dairy products, and seafood products.

State and Local Tax Incentives 2015

For information on all Washington State tax incentives please visit: http://www.dor.wa.gov/Content/FindTaxesAndRates/TaxIncentives/IncentivePrograms.aspx

SEMICONDUCTOR MATERIALS MANUFACTURING

INCENTIVE DESCRIPTION

Reduced B&O Tax Rate

Who: Manufacturers or processors for hire of semiconductor materials What: Lower B&O tax rate for manufacturers or processors of semiconductor materials, including silicon crystals, silicon ingots, raw polished semiconductor wafers, and compound semiconductor wafers.

Sales & Use Tax Exemption

Who: Manufacturers or processors for hire of semiconductor materials What: Sales and Use tax exemption on the purchase of gasses and chemicals used in the manufacturing of semiconductor materials, including silicon crystals, silicon ingots, raw polished semiconductor wafers, compound semiconductor wafers, silicon solar wafers, silicon solar cells, thin film solar devices, and compound semiconductor solar wafers.

TIMBER MANUFACTURING

INCENTIVE DESCRIPTION Timber & Wood Products Industry Incentive

Who: Extractors & Manufacturers of timber and wood products What: Provides a two-step reduction in the tax rate for extracting and wholesaling of timber and manufacturing of timber or wood products. Partially offsetting these rate reductions is a new surcharge tax rate that takes effect July 1, 2007.

ALUMINUM SMELTING/MANUFACTURING

INCENTIVE DESCRIPTION

Reduced B&O Tax Rate Who: Aluminum smelters and processors for hire who manufacture aluminum. What: A reduced B&O tax rate is offered to manufacturers of aluminum.

B&O Tax Credit

Who: Aluminum smelters and processors for hire who manufacture aluminum. What: A B&O tax credit is offered for the state portion of sales tax paid on materials, equipment, labor, and services used in aluminum smelter.

B&O Tax Credit Who: Aluminum smelters who manufacture aluminum. What: A B&O tax credit is offered for property tax paid by the aluminum smelter.

Use Tax Exemption

Who: Aluminum smelters who manufacture aluminum. What: A use tax exemption is offered for the use of natural or manufactured gas by an aluminum smelter.

ENERGY INCENTIVES

BIOFUEL AND RENEWABLE ENERGY/GREEN INCENTIVES INCENTIVE DESCRIPTION Reduced B&O Tax rate Who: Manufacturers, processors for hire, or wholesalers of solar energy systems using

photovoltaic modules or silicon components of these systems. What: The B&O rate is lowered from 0.484 percent to 0.2904 percent

Sales & Use Tax Exemption Who: Individuals, businesses, and local government entities that generate electricity using fuel cell, wind, landfill gas, or solar energy. What: Sales and use tax exemption on purchase or lease of machinery and equipment used directly in generating electricity using fuel cells, wind, landfill gas, or solar energy as the principal source of power.

Sales & Use Tax Exemption Who: Individuals & businesses What: Sales and use tax exemption on purchases of OG-300 rated solar water heating systems, OG-100 rated solar water heating collectors, solar heat exchangers, or differential solar controllers; charges for repair and replacement parts for such equipment; charges for labor and services for installing, repairing, cleaning, altering, or improving such equipment.

State and Local Tax Incentives 2015

For information on all Washington State tax incentives please visit: http://www.dor.wa.gov/Content/FindTaxesAndRates/TaxIncentives/IncentivePrograms.aspx

BIOFUEL AND RENEWABLE ENERGY/GREEN INCENTIVES, CONT. Cost Recovery Program Who: Individuals, businesses, and local government entities that are not in the light and

power business or gas distribution business. Light and power company may take public utility tax credit for amounts paid to participants. Participants must generate electricity on their own property with an anaerobic digester or a wind or solar energy system and apply to their light and power company for a cost recovery incentive payment. What: Cost recovery on investment (up to $2,000)

B&O Tax Credit Who: Businesses with a gross income of less than $750,000 in the previous year. What: A B&O tax credit equal to 8.8% of the purchase price on the purchase of qualifying energy efficient equipment.

Sales & Use Tax Exemption Who: Community Trade and Economic Development (CTED) weatherization program contractors. What: A sales and use tax exemption on purchase of tangible personal property that becomes a component part of a qualifying residence under the weatherization program administered by CTED. Examples of qualifying weatherization materials include, but are not limited to the following: insulation and sealants, parts for air infiltration, heating and cooling equipment, and supplies used to seal and repair ducts.

Sales & Use Tax Exemption Who: Any person that is not engaged in selling biodiesel fuel at wholesale or retail. What: Sales and use tax exemption on the purchase of waste vegetable oil to produce biodiesel fuel. Waste vegetable oil is used cooking oil gathered from restaurants or commercial food processors.

Reduced B&O Tax Rate Who: Manufacturers of alcohol fuel, biodiesel fuel, biodiesel feedstock, or wood biomass fuel. What: The tax rate for manufacturers of biodiesel fuel, biodiesel feedstock, alcohol fuel, and wood biomass fuel has been reduced from 0.484% to 0.138%.

Property/Leasehold Tax Exemption

Who: Manufacturers of alcohol fuel, biodiesel fuel, biodiesel feedstock, or wood biomass fuel. What: Qualifying real and personal property that is operational and used primarily for manufacturing alcohol, biodiesel or wood biomass fuels is exempt or partially exempt from property tax and leasehold excise tax.

B&O Tax Deduction Who: Retail sellers and distributors of biodiesel fuel, alcohol fuel, and wood biomass fuel. What: Income received from the distribution or retail sale of biodiesel fuel, wood biomass fuel, or E85 motor fuel may be deducted from gross income reported for B&O tax. Only income attributable to the pure biofuel portion of biodiesel fuel, wood biomass fuel, or E85 motor fuel sold may be deducted. This amount is computed based on the percentage of the product by volume that is the pure biofuel portion of biodiesel, wood biomass, or E85 motor fuel multiplied by the price of the product by volume. For example, if a fuel blend is 50% pure biodiesel and 50% diesel fuel and sells for $1.50 per gallon, the vendor may deduct $0.75 from gross income for each gallon sold.

Sales & Use Tax Exemption Who: Retail sellers of biodiesel fuel, alcohol fuel, and wood biomass fuel. What: The purchase of machinery and equipment and the construction of facilities used directly for the retail sale of biodiesel fuel blend, E85 motor fuel, and wood biomass fuel blend are exempt from retail sales tax and use tax. The purchase of fuel delivery vehicles and labor and service charges related to such vehicles are exempt from retail sales tax and use tax provided 75% of the fuel distributed by them is biodiesel fuel blend, E85 motor fuel, and wood biomass fuel blend.

State and Local Tax Incentives 2015

For information on all Washington State tax incentives please visit: http://www.dor.wa.gov/Content/FindTaxesAndRates/TaxIncentives/IncentivePrograms.aspx

GENERAL INCENTIVES

MISCELLANEOUS INCENTIVES

INCENTIVE DESCRIPTION Federal Tax Credit What: Businesses that hire from targeted groups of job seekers are eligible for a tax

incentive against their federal corporate income tax. $2,400 credit per employee that is hired from one of the five targeted groups; $4,800 credit per disabled veteran; $1,200 credit per summer youth (16-17 years old) who lives in a Renewal Community; $9,000 credit over two years for previous long-term welfare recipients.

B&O Tax Credit Who: Any Washington employer What: Establishes a new program for customized employment training through the community and technical colleges. Participating employers may claim a B&O tax credit for half of the amount repaid for the cost of employee training.

B&O Tax Credit

Who: Any Business in Washington What: Provides a B&O tax credit for businesses that make cash contributions to the Motion Picture Competitiveness Program and file their taxes electronically.

B&O Tax Credit

Who: Any Washington employer or property manager What: Employers and property managers who provide commute trip reduction incentives to or on behalf of their employees may qualify for a B&O Tax/Public Utility tax credit.

B&O Tax Credit

Who: Any Washington business What: Employers who contribute to an approved revitalization program or Main Street Trust Fund may qualify for a B&O Tax/Public Utility tax credit.

LOCAL INCENTIVES INCENTIVE DESCRIPTION B&O Tax Abrogation Who: Any Clark County business

What: The cities of Clark County do not impose a local B&O tax

Development Fee Waiver Who: Any Clark County business What: Clark County will waive 100 percent of fees for development proposals that create a minimum of 10 full-time jobs and are located in industrial, mixed-use, business park, or office campus zoning districts.

Development Fee Waiver Who: Any Clark County business What: Clark County will waive 50 percent of fees for commercial development proposals that create a minimum of 10 full-time jobs.

Traffic Impact Fee Reduction/Waiver

Who: Any Clark County business What: Clark County will waive or reduce traffic impact fees for development proposals that create a minimum of 10 full-time jobs and are located in industrial, mixed-use, business park, or office campus zoning districts.

Flexible Payment Options Who: Any Clark County business What: Clark County offers the option for developers to pay traffic impact fees in installments and extend deadlines for project completion.

State and Local Government 2015

Compiled by CREDC Research Analyst, 2013

GOVERNMENT STRUCTURE

CITY GOVERNMENT

Vancouver, Washington Form (Structure) City Council

Number of Elected Officials 7

Mayor Timothy D. Leavitt

Length of Term 4

Next Election Date 2017

City Manager Eric Holmes

COUNTY GOVERNMENT

Clark County, Washington Form (Structure) Board of County Councilors

Number of Elected Officials 9

County Councilors Tom Mielke, Jeanne E. Stewart, and David Madore

Length of Term 4

Next Election Date 2015

County Manager Mark McCauley

STATE GOVERNMENT

Washington State Form (Structure) Bicameral

Number of Elected Officials 9

Upper House 4

Total Statewide Upper 49

Lower House 8

Total Statewide Lower 98

Governor Name Jay Inslee

Length of Term 4

Current Term Expiration 2017

Allowed to Run for Another Term Yes

Washington Government Representation State Senate

14th District Curtis King (R)

17th District Don Benton (R)

18th District Ann Rivers (R)

49th District Annette Cleveland (D)

STATE GOVERNMENT, CONT.

State and Local Government 2015

Compiled by CREDC Research Analyst, 2013

State House of Representatives

14th District

Norm Johnson (R)

Gina McCabe (R)

17th District

Lynda Wilson (R)

Paul Harris (R)

18th District

Brandon Vick (R)

Liz Pike (R)

49th District

Sharon Wylie (D)

Jim Moeller (D)

FEDERAL GOVERNMENT REPRESENTATION US Congressmen Serving the Area (District 3) Name Jaime Herrera Beutler

Term Length 2

Current Term Expiration 2015

US Senators Serving the Area Name Patty Murray

Term Length 6

Current Tern Expiration 2017

Name Maria Cantwell

Term Length 6

Current Term Expiration 2019

Clark County Higher Education 2015

Compiled by CREDC Research Analyst, 2015

HIGHER EDUCATION

FOUR YEAR INSTITUTIONS

Institution

Location

Funding

2015 Fall Enrollment

Highest Level Degree Offered

Total Full- Time

Under- Graduate

Graduate

Charter College

Vancouver

Private

Not Available

N/A

B.S.

Washington State University Vancouver

Vancouver

Public

3,264

Ph.D.

TWO YEAR INSTITUTIONS

Institution

Location

Funding 2014 Fall Enrollment Highest Level

Degree Offered Total Full-Time

Clark College

Vancouver

Public

13,881

48%

A.A., A.F.A

VOCATIONAL AND CERTIFICATE PROGRAMS Institution

Location

Funding

Highest Level Degree Offered

Everest College

Vancouver

Private Certificate

International Air and Hospitality Academy

Vancouver

Private

Certificate

Manning Academy of Cosmetology, Inc.

Vancouver

Private

Certificate

Northwest Renewable Energy Institute

Vancouver

Private

Certificate

Northwest Culinary Institute

Vancouver

Private

Certificate

Vancouver School of Beauty

Vancouver

Private

Certificate

TOTAL ENROLLMENT

Clark County, WA Enrollment

2000 2010 2013 Four Year University (Full-Time) 22,974 26,218 25,468

Compiled by CREDC Research Analyst, 2015

Clark County Environmental Services 2015

ENVIRONMENTAL SERVICES

PERMITS

Permit Type Average Permit Time (From Date of Completed Routine Application)

Air 60-90 days

Water 60-90 days

Hazardous Waste 60-90 days

Washington does not have a "One Stop" Permit Assistance Center

WASTE DISPOSAL

Nearest Licensed Hazardous Waste Disposal Site Burlington Environmental Site (Washougal, WA)

No. of Licensed Hazardous Waste Haulers Serving the Area 6-11

Landfill Location Finley Buttes Regional Landfill (Boardman, OR)

ENVIRONMENTAL SERVICES Agency Contact Information

Air Quality

Southwest Clean Air Agency

11815 NE 99th St. Suite 1294

Vancouver, WA 97682

P. 360-574-3058

F. 360-576-0925

Toll Free. 800-633-0709

Water Quality

City of Vancouver

Operations and Maintenance

4711 Fourth Plain Blvd.

Vancouver, WA 98661

P. 360-696-8177

F. 360-696-8002

Environmental Business Assistance

Clark County

1101 Broadway Suite 120

Vancouver, WA 98660

P. 360-694-2588 x. 1074

Compiled by CREDC Research Analyst, 2015

Clark County Utilities 2015

UTILITY RATES

WATER CITY OF VANCOUVER – WATER RATES (Effective January 1, 2015)

Within City Limits Outside City Limits Base Charge

6" Meter $221.99 $332.99 8" Meter $354.08 $531.12 10" Meter $530.10 $795.15

Usage Charge

Commercial $1.47 per CCF $2.22 per CCF Industrial $1.47 per CCF $2.22 per CCF

WASTEWATER CITY OF VANCOUVER – WASTEWATER RATES (Effective January 1, 2015)

Within City Limits Outside City Limits Usage Charge

Commercial $5.26 per CCF $7.89 per CCF

Industrial $5.45 per CCF* $5.66 per CCF** Electronics $4.01 per CCF $4.16 per CCF

Electronics Customer Class - Effective January 1, 2015 - December 31, 2015: *For monthly average flows above 2.88 million gallons per day, the rate shall be $3.21 per CCF. **For monthly average flows above 2.88 million gallons per day, the rate shall be $3.33 per CCF.

Industrial User is defined as an industrial user of the public sewer system who: a) Has a discharge flow of ten thousand gallons or more per average work day; or b) Has a concentration of biochemical oxygen demand (BOD) and suspended solids (SS) in excess of two hundred milligrams per liter per average work day; or c) Has a discharge containing cadmium, chromium, copper, lead, zinc, silver, or similar toxic substances; or d) Is found by the city, State Department, or Ecology, or U.S. Environmental Protection Agency to have a significant impact on the wastewater treatment system.

Electronics User is defined as an industrial user of the public sewer system who: a) Has a discharge flow of five hundred thousand gallons or more per average work day; and b) Has a concentration of biochemical oxygen demand (BOD) and suspended solids (SS) less than two hundred milligrams per liter per average work day.

Compiled by CREDC Research Analyst, 2015

Clark County Utilities 2015

ELECTRICITY CLARK PUBLIC UTILITIES – ELECTRIC RATES (Effective January 1, 2013)

Commercial First Tier Schedule 34 Basic Charge $25.00

Energy Charge 7.70 cents per kWh

Commercial Second Tier Schedule 34 Basic Charge $58.00

Energy Charge

Sept-Mar 4.91 cents per kWh Apr-Aug 4.38 cents per kWh

Demand Charge

Primary Point-of-Delivery $6.77 per kWh Secondary Point-of-Delivery $5.94 per kWh

Off-Peak Demand: By special contract with the utility, off-peak demand is available for customers with demands in excess of 30 kW. Service will be available at a discount rate during the off-peak period, which includes all hours except the hours Monday through Saturday between 7 a.m. to 10 p.m. The off-peak demand rates are 60 cents per kW of demand for each kW the off-peak demand exceeds other recorded monthly demands. The energy rate as listed in the Monthly Rate section applies to all hours.

Adjustment of Demand for Power Factor: Demands will be adjusted to correct for average power factors lower than 95%. Such adjustments will be made by increasing the measured demand 1% for each 1% of major fraction thereof by which the average power factor is less than 95% lagging.

CLARK PUBLIC UTILITIES – ELECTRIC RATES (Effective November 1, 2011)

Industrial* Schedule 85 Basic Charge $200.00

Energy Charge

Sep-Mar 4.91 cents per kWh

Apr-Aug 4.38 cents per kWh

Demand Charge

Primary Point-of-Delivery $5.94 per kWh

Secondary Point-of-Delivery $6.77 per kWh

Transmission Point-of-Delivery $4.60 per kWh *To lighting, heating and power service for customers having measured minimum demands of not less than 1500 kilowatts.

Off-Peak Demand: By special contract with the utility, off-peak demand is available for customers with demands in excess of 1500 KW. Service will be available at a discount rate during the off-peak period, which includes all hours except the hours Monday through Saturday between 7:00 a.m. and 10:00 p.m. The off-peak demand rates are 60¢ per KW of demand for each KW the off—peak demand exceeds other recorded monthly demands. The energy rate as listed in the Monthly Rate section applies to all hours.

Adjustment of Demand for Power: Demands will be adjusted to correct for average power factors lower than 95%. Such adjustments will be made by increasing the measured demand l% for each l% or major fraction thereof by which the average power factor is less than 95% lagging.

Compiled by CREDC Research Analyst, 2015

Clark County Utilities 2015

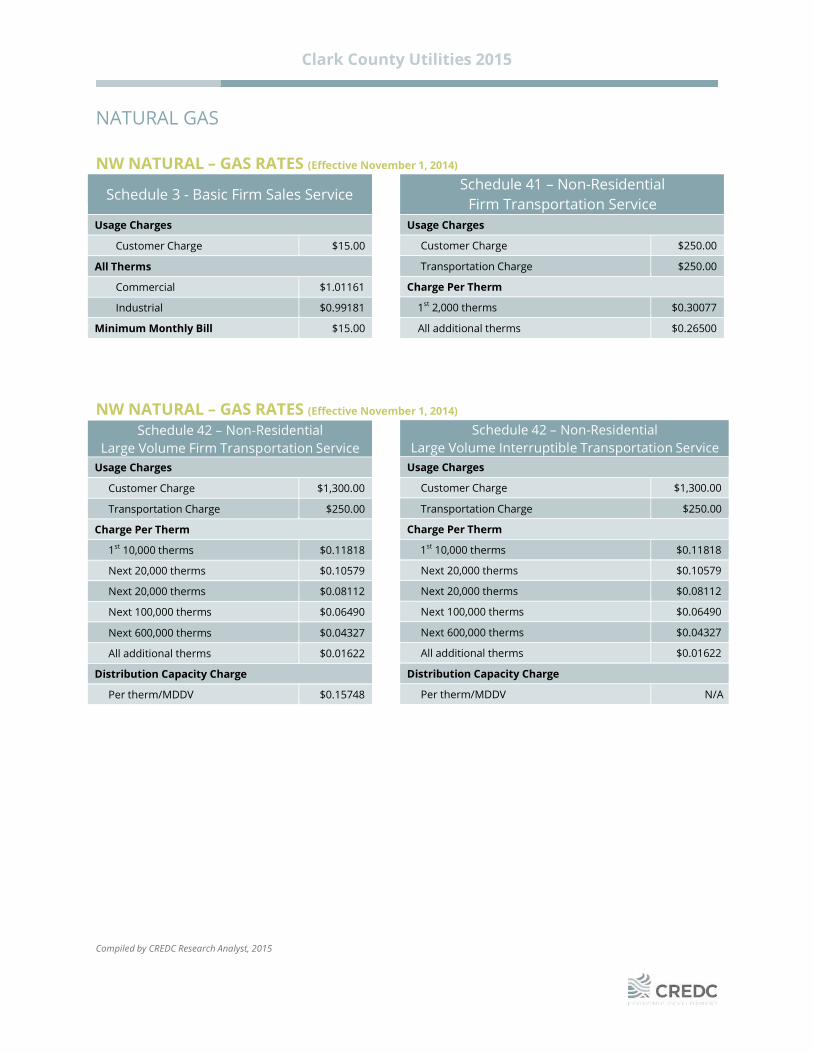

Schedule 41 – Non-Residential Firm Transportation Service

Usage Charges

Customer Charge $250.00

Transportation Charge $250.00

Charge Per Therm

1st 2,000 therms $0.30077

All additional therms $0.26500

Schedule 42 – Non-Residential Large Volume Interruptible Transportation Service

Usage Charges

Customer Charge $1,300.00

Transportation Charge $250.00

Charge Per Therm

1st 10,000 therms $0.11818

Next 20,000 therms $0.10579

Next 20,000 therms $0.08112

Next 100,000 therms $0.06490

Next 600,000 therms $0.04327

All additional therms $0.01622

Distribution Capacity Charge

Per therm/MDDV N/A

NATURAL GAS NW NATURAL – GAS RATES (Effective November 1, 2014)

NW NATURAL – GAS RATES (Effective November 1, 2014)

Schedule 3 - Basic Firm Sales Service

Usage Charges

Customer Charge $15.00

All Therms

Commercial $1.01161

Industrial $0.99181

Minimum Monthly Bill $15.00

Schedule 42 – Non-Residential Large Volume Firm Transportation Service

Usage Charges

Customer Charge $1,300.00

Transportation Charge $250.00

Charge Per Therm

1st 10,000 therms $0.11818

Next 20,000 therms $0.10579

Next 20,000 therms $0.08112

Next 100,000 therms $0.06490

Next 600,000 therms $0.04327

All additional therms $0.01622

Distribution Capacity Charge

Per therm/MDDV $0.15748

Compiled by CREDC Research Analyst, 2015

Clark County Utilities 2015

Schedule 41 - Non-Residential Interruptible Sales Service

Customer Charge

Commercial $250.00

Industrial $250.00

Volumetric Charges

Commercial

1st 2,000 therms $0.78165

All additional therms $0.74363

Industrial

1st 2,000 therms $0.76749

All additional therms $0.73166

Pipeline Capacity Charges

Commercial

Firm (per therm) $0.04372

Industrial

Firm (per therm) $0.04903

Minimum Monthly Bill: Customer charge, plus Volumetric charges, plus applicable Pipeline Capacity Charges

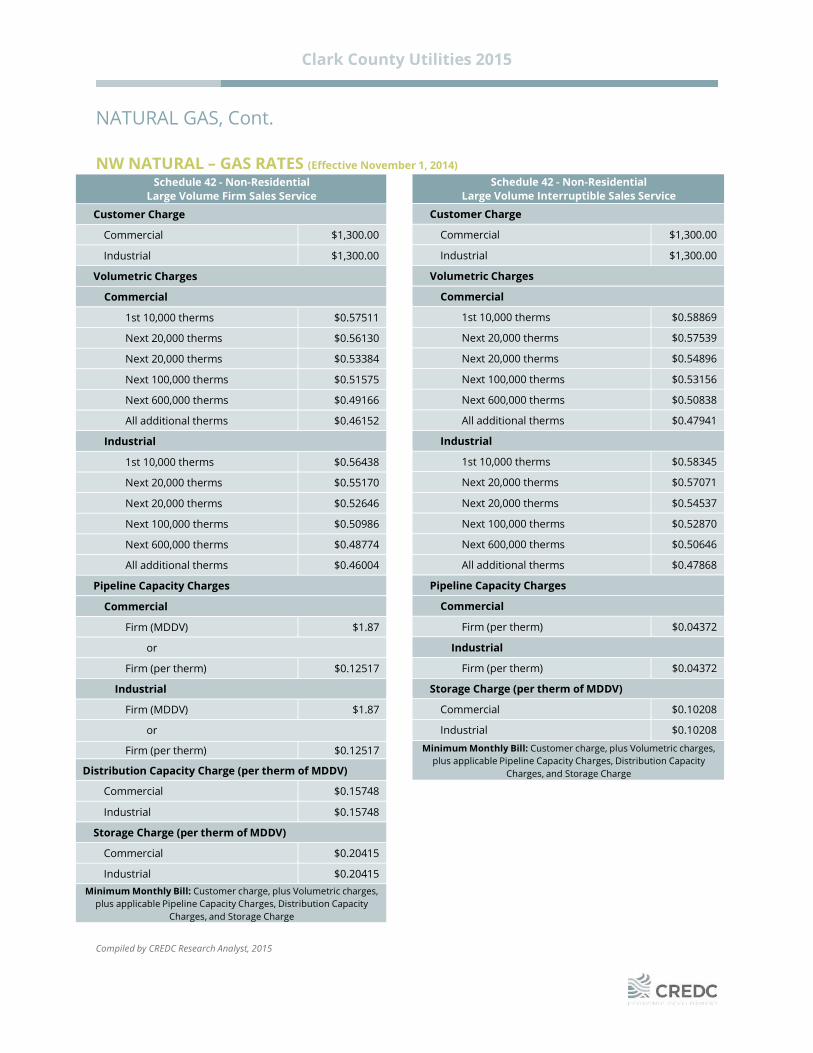

NATURAL GAS, Cont. NW NATURAL – GAS RATES (Effective November 1, 2014)

Schedule 41 - Non-Residential Firm Sales Service

Customer Charge

Commercial $250.00

Industrial $250.00

Volumetric Charges

Commercial

1st 2,000 therms $0.76423

All additional therms $0.72611

Industrial

1st 2,000 therms $0.74924

All additional therms $0.71289

Pipeline Capacity Charges

Commercial

Firm (MDDV) $1.87

or

Firm (per therm) $0.12517

Industrial

Firm (MDDV) $1.87

or

Firm (per therm) $0.12517 Minimum Monthly Bill: Customer charge, plus Volumetric

charges, plus applicable Pipeline Capacity Charges

Compiled by CREDC Research Analyst, 2015

Clark County Utilities 2015

Schedule 42 - Non-Residential Large Volume Interruptible Sales Service

Customer Charge

Commercial $1,300.00

Industrial $1,300.00

Volumetric Charges

Commercial

1st 10,000 therms $0.58869

Next 20,000 therms $0.57539

Next 20,000 therms $0.54896

Next 100,000 therms $0.53156

Next 600,000 therms $0.50838

All additional therms $0.47941

Industrial

1st 10,000 therms $0.58345

Next 20,000 therms $0.57071

Next 20,000 therms $0.54537

Next 100,000 therms $0.52870

Next 600,000 therms $0.50646

All additional therms $0.47868

Pipeline Capacity Charges

Commercial

Firm (per therm) $0.04372

Industrial

Firm (per therm) $0.04372

Storage Charge (per therm of MDDV)

Commercial $0.10208

Industrial $0.10208

Minimum Monthly Bill: Customer charge, plus Volumetric charges, plus applicable Pipeline Capacity Charges, Distribution Capacity

Charges, and Storage Charge

NATURAL GAS, Cont.

NW NATURAL – GAS RATES (Effective November 1, 2014)

Schedule 42 - Non-Residential Large Volume Firm Sales Service

Customer Charge

Commercial $1,300.00

Industrial $1,300.00

Volumetric Charges

Commercial

1st 10,000 therms $0.57511

Next 20,000 therms $0.56130

Next 20,000 therms $0.53384

Next 100,000 therms $0.51575

Next 600,000 therms $0.49166

All additional therms $0.46152

Industrial

1st 10,000 therms $0.56438

Next 20,000 therms $0.55170

Next 20,000 therms $0.52646

Next 100,000 therms $0.50986

Next 600,000 therms $0.48774

All additional therms $0.46004

Pipeline Capacity Charges

Commercial

Firm (MDDV) $1.87

or

Firm (per therm) $0.12517

Industrial

Firm (MDDV) $1.87

or

Firm (per therm) $0.12517

Distribution Capacity Charge (per therm of MDDV)

Commercial $0.15748

Industrial $0.15748

Storage Charge (per therm of MDDV)

Commercial $0.20415

Industrial $0.20415 Minimum Monthly Bill: Customer charge, plus Volumetric charges,

plus applicable Pipeline Capacity Charges, Distribution Capacity Charges, and Storage Charge

PORTLAND – VANCOUVER TAX COMPARISON 2015

Compiled by CREDC, January 2015

Tax Clark County, Washington Multnomah County, Oregon Washington County, Oregon Clackamas County, Oregon

Corporate Income (Excise) Tax

None

6.6% for taxable income of $10 million or less, and 7.6% for taxable income

greater than $10 million

6.6% for taxable income of $10 million or less, and 7.6% for taxable income

greater than $10 million

6.6% for taxable income of $10 million or less, and 7.6% for taxable income

greater than $10 million

Corporate Alternative Minimum Tax None

Tax is calculated on Oregon sales and ranges from $150-$100,000

Tax is calculated on Oregon sales and ranges from $150-$100,000

Tax is calculated on Oregon sales and ranges from $150-$100,000

B&O Tax Manufacturing and Wholesaling

0.484%; Retailing 0.471%; Services 1.5% on gross receipts

None

None

None

Personal Income Tax None Up to 9.9% of taxable income; ranges

from 5.00%-9.90% Up to 9.9% of taxable income; ranges

from 5.00%-9.90% Up to 9.9% of taxable income; ranges

from 5.00%-9.90%

Business License Fee $125 + $50 per FTE (for up to 400),

annually (City of Vancouver)

2.2% of net business income, $100 minimum, annually

(City of Portland)

$50 for 0-4 employees and $8.50 per additional employee, annually

(City of Beaverton)

$55-$240 annually, depending on number of employees (City of Tualatin)

Sales Tax (State and Local Combined) 8.40% None None None

Transit District Tax None 0.7237% flat rate payroll tax 0.7237% flat rate payroll tax 0.7237% flat rate payroll tax

Unemployment Insurance Tax

Average 2.07% on the first $42,100 in wages; Rates range from 0.14%-5.82%

Average rate of 2.53% on the first $35,700 in wages; Rates range from

1.8%-5.4%

Average rate of 2.53% on the first $35,700 in wages; Rates range from

1.8%-5.4%

Average rate of 2.53% on the first $35,700 in wages; Rates range from

1.8%-5.4%

Industrial Insurance

(WA)

Workers’ Compensation (OR)

Industrial Insurance Average Rate, per hour worked $0.7133. Sample Rates by Industry: Misc. Manufacturing: $0.7907 Transportation & Warehousing: $1.9997 Misc. Professional Services: $0.1893

Broken down into three taxes: 1) Pure Premium averages $1.27 per $100 of payroll 2) 6.2% Premium Assessment fee of the annual total premium for insured employers, 6.4% for self-insured employers, 7.2% for self-insured employer groups 3) Workers Benefit Fund, paid to the state at 3.3 cents per worker hour worked

Broken down into three taxes: 1) Pure Premium averages $1.27 per $100 of payroll 2) 6.2% Premium Assessment fee of the annual total premium for insured employers, 6.4% for self-insured employers, 7.2% for self-insured employer groups 3) Workers Benefit Fund, paid to the state at 3.3 cents per worker hour worked

Broken down into three taxes: 1) Pure Premium averages $1.27 per $100 of payroll 2) 6.2% Premium Assessment fee of the annual total premium for insured employers, 6.4% for self-insured employers, 7.2% for self-insured employer groups 3) Workers Benefit Fund, paid to the state at 3.3 cents per worker hour worked

Average rate per $100 of payroll: $2.70 Average rate per $100 of payroll: $1.55 Average rate per $100 of payroll: $1.55 Average rate per $100 of payroll: $1.55