pittsburg unified school district budget workshop february ... · pittsburg unified school district...

TRANSCRIPT

PITTSBURG UNIFIED SCHOOL DISTRICTBUDGET WORKSHOP

February 12th, 2018

PRESENTED BY: ENRIQUE E. PALACIOS, DEPUTY SUPERINTENDENT

INTRODUCTION

• ANNUAL BUDGET CALENDAR• PURPOSE OF FUNDS• ACCOUNTS STRUCTURE• BUDGET STRUCTURE• MULTI YEAR BUDGET

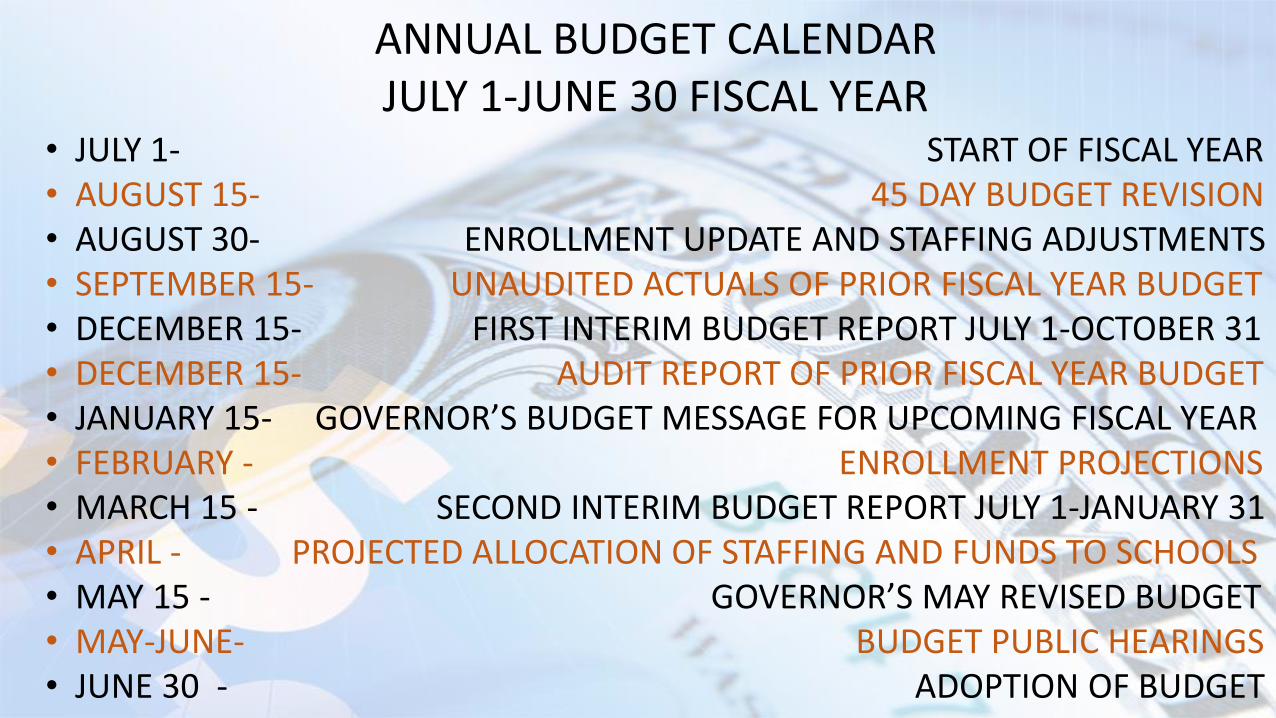

ANNUAL BUDGET CALENDARJULY 1-JUNE 30 FISCAL YEAR

• JULY 1- START OF FISCAL YEAR• AUGUST 15- 45 DAY BUDGET REVISION• AUGUST 30- ENROLLMENT UPDATE AND STAFFING ADJUSTMENTS• SEPTEMBER 15- UNAUDITED ACTUALS OF PRIOR FISCAL YEAR BUDGET• DECEMBER 15- FIRST INTERIM BUDGET REPORT JULY 1-OCTOBER 31• DECEMBER 15- AUDIT REPORT OF PRIOR FISCAL YEAR BUDGET• JANUARY 15- GOVERNOR’S BUDGET MESSAGE FOR UPCOMING FISCAL YEAR• FEBRUARY - ENROLLMENT PROJECTIONS • MARCH 15 - SECOND INTERIM BUDGET REPORT JULY 1-JANUARY 31• APRIL - PROJECTED ALLOCATION OF STAFFING AND FUNDS TO SCHOOLS• MAY 15 - GOVERNOR’S MAY REVISED BUDGET• MAY-JUNE- BUDGET PUBLIC HEARINGS• JUNE 30 - ADOPTION OF BUDGET

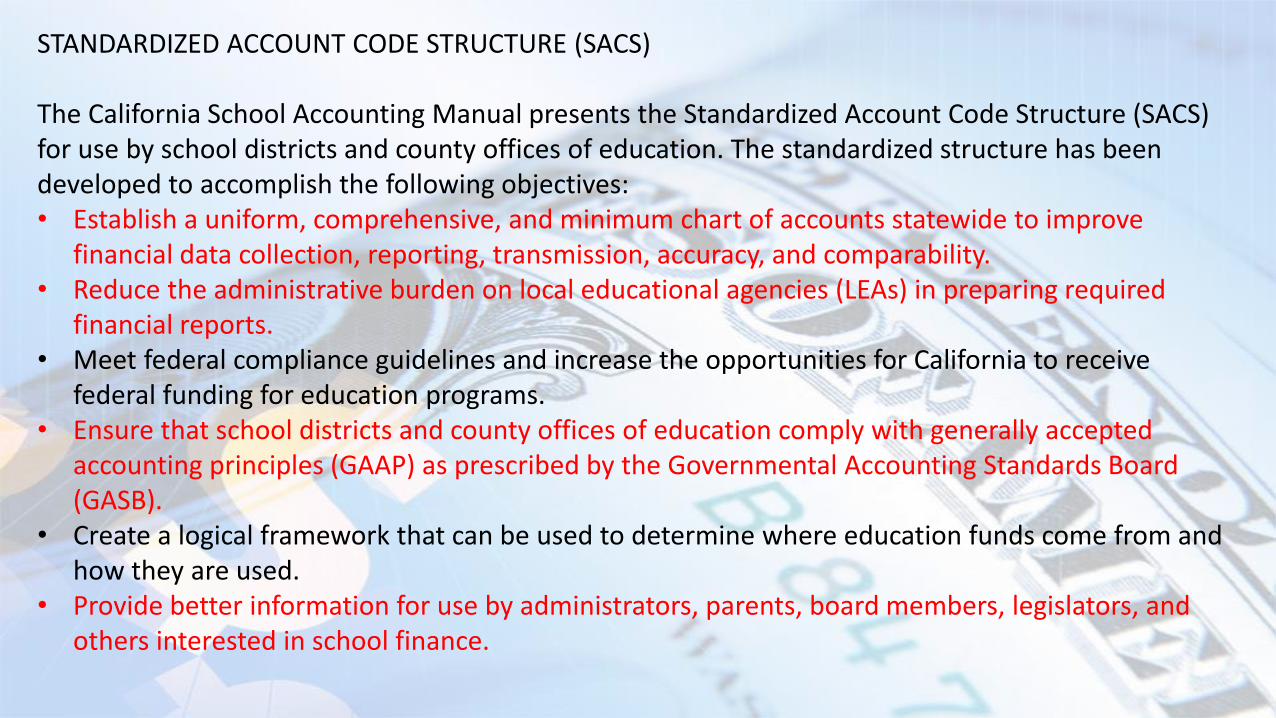

STANDARDIZED ACCOUNT CODE STRUCTURE (SACS)

The California School Accounting Manual presents the Standardized Account Code Structure (SACS) for use by school districts and county offices of education. The standardized structure has been developed to accomplish the following objectives: • Establish a uniform, comprehensive, and minimum chart of accounts statewide to improve

financial data collection, reporting, transmission, accuracy, and comparability.• Reduce the administrative burden on local educational agencies (LEAs) in preparing required

financial reports.• Meet federal compliance guidelines and increase the opportunities for California to receive

federal funding for education programs.• Ensure that school districts and county offices of education comply with generally accepted

accounting principles (GAAP) as prescribed by the Governmental Accounting Standards Board (GASB).

• Create a logical framework that can be used to determine where education funds come from and how they are used.

• Provide better information for use by administrators, parents, board members, legislators, and others interested in school finance.

FUNDS IN A SCHOOL DISTRICT BUDGET

CHILD DEVELOPMENT

12

CHILD NUTRITION

13

DEFERRED MAINTENANCE

14

SPECIAL RESERVES

17

STATE SCHOOL FACILITIES

35

ADULT ED11

CAPITAL BUILDING

BOND 21

GENERAL FUND

01

CAPITAL BUILDING RESERVES

40

BOND INTEREST & REDEMPTION

51

FOUNDATION TRUST

73

WARRANT PASS THROUGH

76

STUDENT BODY

95

Postemployment Benefits

20

CAPITAL FACIILITIES

25

GENERAL FUND

01

General Fund. This is the chief operating fund for all LEAs. It is

used to account for the ordinary operations of an LEA. All

transactions except those accounted for in another fund are accounted

for in this fund.

Restricted programs or activities within the general fund must be

identified and reported separately from unrestricted programs or

activities. This is done by using codes in the resource field that

identify whether the resources used are restricted or unrestricted.

GENERAL FUND

01LCFF BASE

& OTHER STATE

FUNDS

REGULAR ED CLASSROOM

TEACHERSCLERICAL STAFF

CUSTODIANSSITE

ADMINISTRATORSUTILITIESSUPPLIES

EQUIPMENTBOOKS

LCAP

SUPPLEMENTAL &

CONCENTRATIONFUNDS

SPECIAL EDTITLE 1 & 3RESTRICTED

MAINTENANCETRANSPORTATION

ASESPARCEL TAX

GRANTS

UNRESTRICTED RESTRICTED

ADULT ED11

Adult Education Fund. This fund is used to account separately for

federal, state, and local revenues that are restricted or committed for

adult education programs. Money in this fund shall be expended for

adult education purposes only. Except for moneys received

pursuant to the Local Control Funding Formula, moneys received for

programs other than adult education shall not be expended for adult

education.

CHILDDEVELOPMENT

12

Child Development Fund. This fund is used to account

separately for federal, state, and local revenues to operate child

development programs such as Pre-K.

CHILD NUTRITION

13

Child Nutrition Fund. This fund is used to account separately for

federal, state, and local resources to operate the food service

program.

DEFERRED MAINTENANCE

14

Deferred Maintenance Fund. This fund is used to account

separately for revenues that are restricted or committed for

deferred maintenance purposes in school facilities.

SPECIAL RESERVES

17

Special Reserve Fund for Other Than Capital Outlay

Projects. This fund is used primarily to provide for the

accumulation of general fund moneys for general operating

purposes other than for capital outlay. Amounts from this special

reserve fund must first be transferred into the general fund or

other appropriate fund before expenditures may be made.

POSTEMPLOYMENT BENEFITS

20

Postemployment Benefits Fund. This fund may be used to account

for amounts the LEA has earmarked for the future cost of

postemployment benefits but has not contributed irrevocably to a

separate trust for the postemployment benefit plan. Amounts

accumulated in this fund must be transferred back to the general

fund for expenditure

CAPITAL BUIDLING BOND

21

Capital Building Bond Fund. This fund exists primarily to

account separately for proceeds from the sale of bonds and may not

be used for any purposes other than those for which the bonds were

issued. Other authorized revenues to the Building Fund (Fund 21)

are proceeds from the sale or lease-with-option-to-purchase of real

property and revenue from rentals and leases of real property

specifically authorized for deposit into the fund by the governing

board.

CAPITAL FACIILITIES

25

Capital Facilities Fund. This fund is used primarily to account

separately for moneys received from fees levied on development

projects as a condition of approval. The authority for these levies

may also be county or city ordinances or private agreements

between the LEA and the developer. Interest earned in the Capital

Facilities Fund (Fund 25) is restricted to that fund.

STATE SCHOOL FACILITIES

35

State School Facilities Fund. This fund is established to receive

apportionments from the 1998 State School Facilities Fund

(Proposition 1A), the 2002 State School Facilities Fund (Proposition

47), the 2004 State School Facilities Fund (Proposition 55), or the

2006 State School Facilities Fund (Proposition 1D). The fund is used

primarily to account for new school facility construction,

modernization projects, and facility hardship grants, as provided in

the Leroy F. Greene School Facilities Act of 1998.

CAPITAL BUILDING RESERVES

40Capital Building Reserves. This fund exists primarily to provide

for the accumulation of general fund moneys for capital outlay

purposes. This fund may also be used to account for any other

revenues specifically for capital projects that are not restricted to

fund 21, 25, 30, 35, or 49. Other authorized resources that may be

deposited to the Special Reserve Fund for Capital Outlay Projects

(Fund 40) are proceeds from the sale or lease-with-option-to-

purchase of real property and rentals and leases of real property

specifically authorized for deposit to the fund by the governing

board.

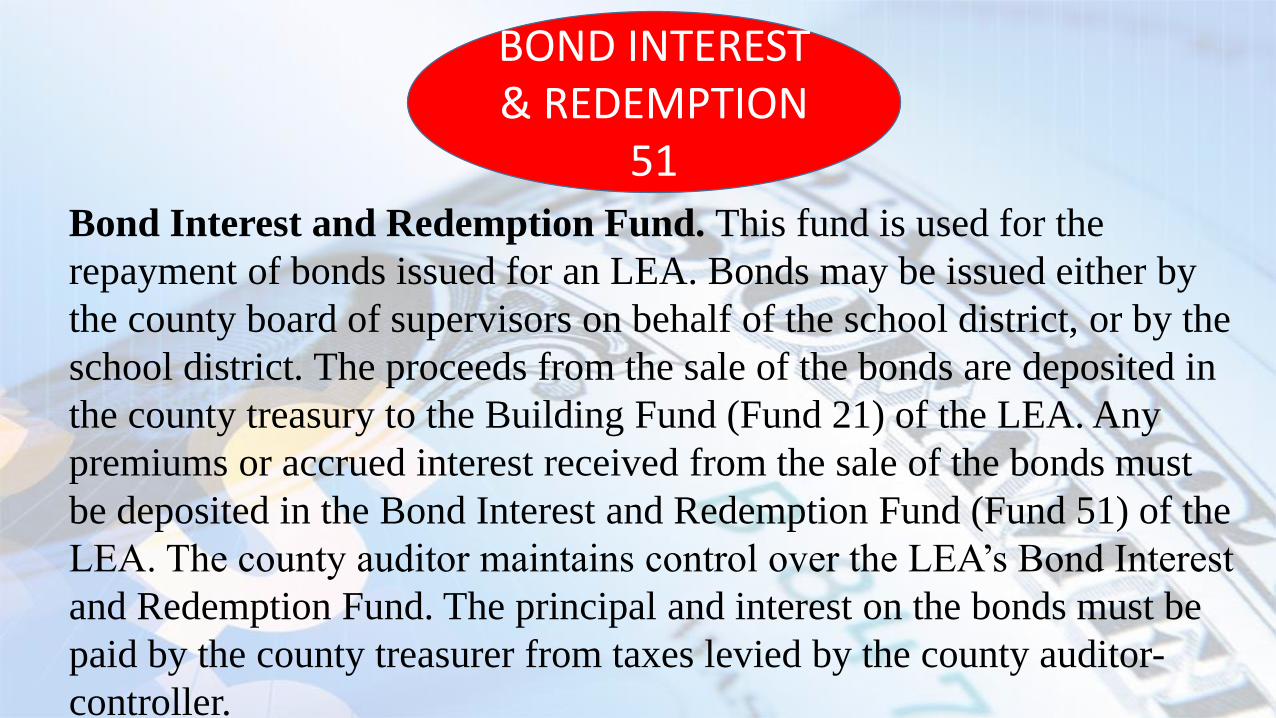

BOND INTEREST & REDEMPTION

51

Bond Interest and Redemption Fund. This fund is used for the

repayment of bonds issued for an LEA. Bonds may be issued either by

the county board of supervisors on behalf of the school district, or by the

school district. The proceeds from the sale of the bonds are deposited in

the county treasury to the Building Fund (Fund 21) of the LEA. Any

premiums or accrued interest received from the sale of the bonds must

be deposited in the Bond Interest and Redemption Fund (Fund 51) of the

LEA. The county auditor maintains control over the LEA’s Bond Interest

and Redemption Fund. The principal and interest on the bonds must be

paid by the county treasurer from taxes levied by the county auditor-

controller.

FOUNDATION TRUST

73

Foundation Trust Fund. This fund is used to account separately for

gifts or bequests that benefit individuals, private organizations, or

other governments and under which neither principal nor income

may be used for purposes that support the LEA’s own programs.

This fund should be used when there is a formal trust agreement

with the donor. Donations not covered by a formal trust agreement

should be accounted for in the general fund. Amounts in the

Foundation Private-Purpose Trust Fund shall be expended only for

the specific purposes of the gift or bequest.

WARRANT PASS THROUGH

76

Warrant/Pass-Through Fund. (Reporting of this fund to CDE is

not required; however, it must be included in the audited financial

statements to meet GAAP reporting requirements.) This fund exists

primarily to account separately for amounts collected from

employees for federal taxes, state taxes, transfers to credit unions,

and other contributions. It is also used to account for those receipts

for transfer to agencies for which the LEA is acting simply as a “cash

conduit.”

STUDENT BODY

95

Student Body Fund. (Reporting of this fund to CDE is not required;

however, it must be included in the audited financial statements to

meet GAAP reporting requirements.) In the financial reports of the

LEA, Fund 95 is an agency fund and, therefore, consists only of accounts such as Cash and balancing liability accounts, such as Dues to Student Groups. The student body itself maintains its own general fund, which accounts for the transactions of that entity in raising and expending money to promote the general welfare, morale, and educational experiences of the student body.

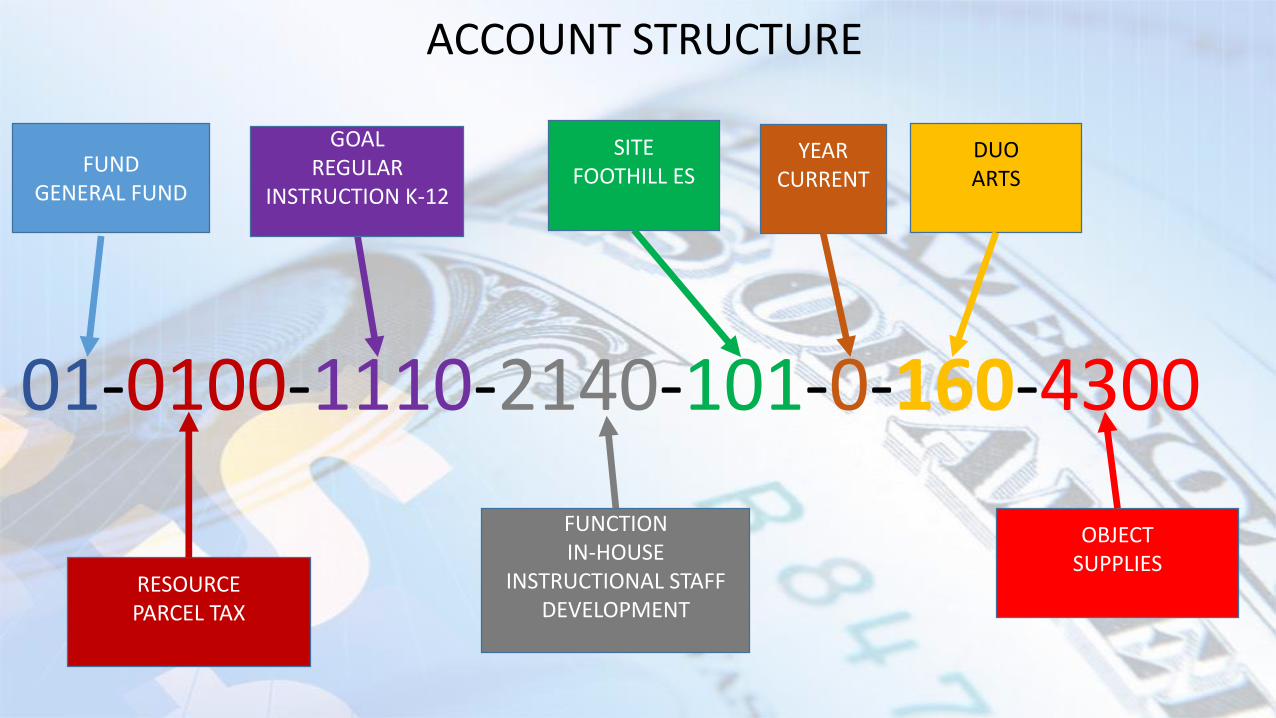

ACCOUNTS STRUCTURE

FUND 13

OBJECT 4700

RESOURCE 5310

GOAL 8500

FUNCTION 4700

01-0100-1110-2140-101-0-160-4300

Fund: A fund identifies specific activities or defines certain objectives in accordance with California Department of Education. Most activity in school districts occurs in Fund 01.

General Fund, Adult Ed Fund, Child Development Fund,…

01-0100-1110-2140-101-0-160-4300

Resource: The resource code is used to classify revenue and expenditures that have special accounting or reporting requirements or that are legally restricted.

Tittle 1, Special Ed, LCAP, Restricted Maintenance...

01-0100-1110-2140-101-0-160-4300

Goal: The goal identifies the instructional goals and objectives. It groups costs by population, setting, and/or educational mode. Examples include regular education K-12, continuation schools, migrant education, and special education.

Regular Education K-12 , Custodial, Mathematics, Robotics…

01-0100-1110-2140-101-0-160-4300

Function: The function identifies activities or services performed to support or accomplish one or more goals or objectives. Examples include instruction, school administration, and transportation.

Parent Participation, School Administration, Fiscal Services…

01-0100-1110-2140-101-0-160-4300

Site: The site code designates a specific, physical school structure or group of structures that form a campus under a principal’s responsibility.

Foothill ES, Hillview JHS, PHS, Education Services…

01-0100-1110-2140-101-0-160-4300

Year: Identifies the reporting year for a project that has more than one reporting year during the Local Education Agency’s fiscal year. If a project’s reporting year is the same throughout the LEA’s fiscal year, the Project Year code is 0.

01-0100-1110-2140-101-0-160-4300

DUO (District Use Only): Identifies activities or projects that are only perform in a particular district and no other.

Marina Vista Solar, Early Back Program, Parent Involvement...

01-0100-1110-2140-101-0-160-4300

Object: The object code classifies expenditures by type of commodity or service (e.g. – certificated salaries, benefits, instructional supplies, travel & conference) and revenue by source. (LCFF, federal, other state, other local)

Certificated Salaries, Supplies, Professional Services…

01-0100-1110-2140-101-0-160-4300

ACCOUNT STRUCTURE

FUNDGENERAL FUND

RESOURCEPARCEL TAX

YEARCURRENT

GOALREGULAR

INSTRUCTION K-12

FUNCTIONIN-HOUSE

INSTRUCTIONAL STAFF DEVELOPMENT

OBJECTSUPPLIES

DUOARTS

SITEFOOTHILL ES

SACS STRING: 01-9500-1110-2100-487-0-713-5800

GENERAL FUND

LCAP

INSTRUCTIONAL SERVICES

SUPERVISION OF INSTRUCTION

EDUCATION SERVICES

PROJECT YEAR

LCAP GOAL #3-CENTRALIZED

PROFESSIONAL CONSULTANT SERVICES

BUDGET STRUCTURE

2017-18 FIRST INTERIM MYP

UNRESTRICTED GENERAL FUND

OBJECT CODES 2017-18

REVENUES

LCFF/RL Sources 8010-8099 110,974,420

Federal Revenues 8100-8299 -

Other State Revenues 8300-8599 3,623,432

Other Local Revenues 8600-8799 1,865,745

Other Financing Sources

Transfers In 8900-8929 -

Other Sources 8930-8979 -

Contributions 8980-8999 (39,427,950)

TOTAL REVENUES 77,035,647

REVENUES

2017-18 FIRST INTERIM MYP UNRESTRICTED GENERAL FUND

OBJECT CODES 2017-18EXPENDITURES

Certificated Salaries 1000-1999 39,581,211 Classified Salaries 2000-2999 10,034,956 Benefits 3000-3999 18,860,352 Materials/Supplies 4000-4999 4,973,956 Other Services 5000-5999 7,490,703 Capital Outlay 6000-6999 70,067 Other Outgo 7100-7299,7400-7499 21,000 Other Outgo 7300-7399 (505,334)Other Financing Uses

Transfers Out 7600-7629 355,221 Other uses 7630-7699 -

Other Adjustments -TOTAL EXPENDITURES 80,882,133

Net Increase(Decrease) in Fund Balance (3,846,486)

EXPENDITURES

2017-18 FIRST INTERIM MYP UNRESTRICTED GENERAL FUND

OBJECT CODES 2017-18FUND BALANCE Net Beginning Fund Balance 12,520,474 Ending Fund Balance 8,673,989

Components of Ending Fund Balance Non-spendable 25,000

Restricted Committed Stabilization Arrangements -

Other Commitments -Assigned 1,622,145 Unassigned/Unappropriated

Reserves for Economic Uncertainties 4,340,534 Unassigned/Unappropriated 2,686,309

Total Components of Ending Fund Balance 8,673,989

FUND BALANCE

MYP

$5,926 $6,164 $6,359 $6,602 $6,885

$1,939$2,091

$2,268$2,885

$3,455$443

$464$489

$568

$637

$8,308$8,719

$9,116

$10,056

$10,977

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

0%-20% 20%-40% 40%-60% 60%-80% 80%-100%

Am

ou

nt

Pe

r A

DA

2018-19 Proposed

LCFF Increase(2013-14 through2017-18)

2012-13 Base

UPP Range

TRANSITIONING TO FULL FUNDING OF LCFF ENTITLEMENTS

Base Growth

Base Growth

Base GrowthBase Growth

SC Growth

SC Growth

SC Growth

SC Growth

STRS Increase STRS Increase STRS Increase

STRS Increase

PERS Increase PERS Increase PERS Increase

PERS Increase

Step & Column Step & Column Step & Column

Step & Column

Special Education

Contribution?

Special Education

Contribution?

Special Education

Contribution?

Special Education

Contribution?$235

$430

$549

$435

$236

$441

$281

$367

$-

$100

$200

$300

$400

$500

$600

LCFF GrowthRevenues

Expenditures LCFF GrowthRevenues

Expenditures LCFF GrowthRevenues

Expenditures LCFF GrowthRevenues

Expenditures

2017-18 2018-19 2019-20 2020-21

PER-ADA REVENUES GROWTH IN REVENUES AND EXPENDITURES

• SB 3 (Chapter 4/2016), which was signed by the Governor in April 2016, gradually increases California’s minimum wage and provides clarity on exempt employees

• The Governor can pause progress annually

Minimum WageEffective Date:> 25 Employees

Effective Date:≤ 25 Employees

$10.50/hour January 1, 2017 January 1, 2018

$11.00/hour January 1, 2018 January 1, 2019

$12.00/hour January 1, 2019 January 1, 2020

$13.00/hour January 1, 2020 January 1, 2021

$14.00/hour January 1, 2021 January 1, 2022

$15.00/hour January 1, 2022 January 1, 2023

MINIMUM WAGE

CalPERS Rate IncreasesActual Projected

2017-18

2018-19 2019-20 2020-21 2021-22 2022-23

15.531% 18.1% 20.8% 23.8% 25.2% 26.1%

CalSTRS Rate IncreasesYear Employer

Pre-PEPRAEmployees

Post-PEPRA Employees

2017-18 14.43% 10.25% 9.205%

2018-19 16.28% 10.25% 9.205%

2019-20 18.13% 10.25% 9.205%

2020-21 19.10% 10.25% 9.205%

CHANGES TO: 2017-18 2018-19 2019-20 TOTAL

Supplemental & Concentration Grant Funding

$ 147,199 $ 1,707,442 $ 1,091,004 $ 2,945,645

Base Funding$ (32,346) $ 584,158 $ 1,150,764 $ 1,702,576

TOTAL $ 114,853 $ 2,291,600 $ 2,241,768 $ 4,648,221

IMPACT OF THE GOVERNOR’S JANUARY BUDGET PROPOSAL ON

PUSD’S MYP

QUESTIONS?