pesticide industry

TRANSCRIPT

PESTICIDEINDUSTRY

Presented by:Abhishek Mall

Flow of Presentation.

• Introduction• Global Market Overview• Indian Market Overview• Bio pesticide• Supply Chain• Challenges• Regulation

Introduction•PEST: A pest may be insect, rodent, nematode, fungus, or weed.•Pesticides or crop protection products, also known as agro–chemicals are products that preserve crops from pests, diseases and weeds.•Agrochemicals are substances manufactured through chemical or biochemical processes containing the active ingredient, in a definite concentration along with other materials which improve its performance and increase safety. Losses caused by different pests (%) •25% to 40% of world crop output is

lost due to the attack of pests, weeds and diseases.•For each acre of land there are 50 to 300 million buried weeds•A crop and plant have to compete with 30,000 species of weeds, 3,000 species of nematodes and 100,000 species of plant eating insects.

Cont...

• The industry is estimated to reduce overall potential pre-harvest wheat loss of 50% to an actual loss of 29%.

• Some 20% of the entire world's agricultural production would be lost to post-harvest pest attacks if it were not for crop protection chemicals.

• To minimize these losses and to enhance yields it is essential to use crop protection chemicals.

• There are broadly 5 categories of crop protection products:• Insecticides• Herbicides• Fungicides• Bio-pesticides• Others (Nematicides, Rodenticides etc.)

Global Market Overview• Expected to grow at a CAGR of

5.4% p.a• The Global market size of the

industry is around 48Bn USD.• The size is expected to reach

71.3Bn USD by the year 2018.

•Europe has the largest share in the agrochemical market followed by Asia, Latin America and North America. •the crop protection chemicals market has reached its saturation in developed regions such as North America and Western EuropeConsumption: Continent wise

Cont...

• .• Insecticides are more prevalent in Asian countries. This is due to higher

growth of cotton, cereal, fruits and vegetables in these regions which have higher incidence of insect attacks.

• Germany($3.6Bn), France($3.5Bn), US($3.3Bn), China($2.8Bn) and Belgium($2.1Bn) are the largest exporters of crop protection products.

• Brazil($2.2Bn), Canada($1.2Bn), United Kingdom($0.9Bn), Italy($0.9Bn) and Spain($0.8Bn) are the major importers.

•Herbicides are the most widely used agrochemical products globally(44%), followed by fungicides(27%) and insecticides(22%).•major markets for herbicides are North America and Europe due to the favorable climatic conditions in these regions

Product categorization of pesticide Industry

Cont…Top molecules in top 3 Product categories of pesticide are:

Distribution of global crop protection market - Crop wise

•Globally, fruits and vegetables and cereals account for the largest share of the crop protection industry.

•Share of Fruits and vegetables is largest(26%) followed by Cereals(18%) and Maize(13%)

Global Industry Challenges• Evolution of biotechnology: Development of genetically modified

crops in recent years, especially for pest resistance would result in relatively lesser need for traditional crop protection chemicals.

• Regulations: Stringent environmental regulations across all countries increase the cost of developing new products. These regulations are primarily affecting the older products while at the same time resulting in delay in introduction of new products.

• Acquisitions : Larger companies are acquiring/ entering into strategic alliances with smaller companies to increase their market reach. This poses a threat to local companies who are forced to reduce pricesin order to compete, thereby leading to lower margins.

Indian market overview• India is the fourth largest producer of crop protection chemicals

globally, after United States, Japan & China.• The Indian pesticide industry is estimated to be USD 4.1 billion. • Expected to grow at a CAGR of 12% to reach USD 7.1 billion by

FY18. • The exports currently constitute almost 50% of the Indian crop

protection industry. • Expected to grow at a CAGR of 16% to reach USD 4.2 billion by FY18• There were about 125 technical grade manufacturers, including

about 10 multinationals, more than 800 formulators and over 1,45,000 distributors in India in FY12.

• More than60 technical grade pesticides are being manufactured indigenously.

Cont…• The Indian crop protection industry is dominated by the generic

products with more than 80% of the non- patented molecules.

•Top ten companies control almost 75-80% of the market share. The market share of large players depends primarily on product portfolio and introduction of new molecules.

Per capita consumption of pesticides (Kg/ ha) •The per capita consumption of crop protection products in India is amongst the lowest in the world.•This is creating tremendous opportunity for the growth of crop protection industry in India.

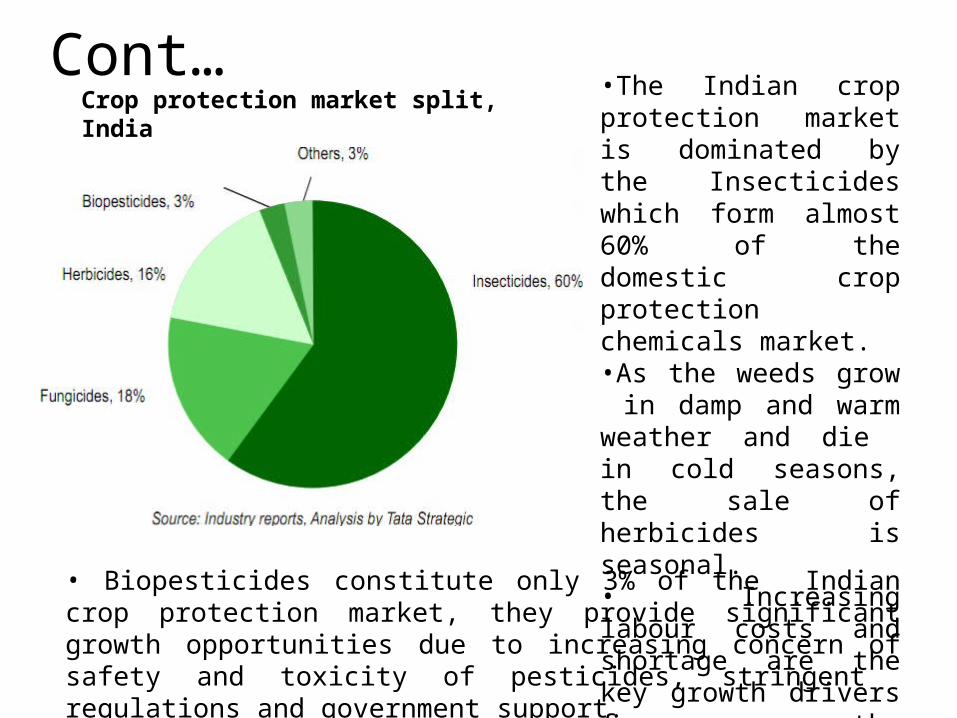

Cont…•The Indian crop protection market is dominated by the Insecticides which form almost 60% of the domestic crop protection chemicals market.•As the weeds grow in damp and warm weather and die in cold seasons, the sale of herbicides is seasonal.• Increasing labour costs and shortage are the key growth drivers for the herbicides.

Crop protection market split, India

• Biopesticides constitute only 3% of the Indian crop protection market, they provide significant growth opportunities due to increasing concern of safety and toxicity of pesticides, stringent regulations and government support.

Cont…

Top molecules in Product categories of pesticide are:

• The major applications are found in rice and cotton crops.•Fungicides and Herbicides are the largest growing segments accounting for 18% and 16% respectively of the total crop protection chemicals market.• Rice and wheat crops are the major application areas of herbicides. • The fungicides find applications in fruits, vegetables and rise and their increasing usage is due to shift in agriculture from cash crops to fruits and vegetables and government support for exports.

•Andhra Pradesh, Maharashtra and Punjab are the top three states contributing to 50% of the pesticide consumption in India. •Andhra Pradesh is the leading consumer with 24% share.

•The top seven states together account for more than 70% of the crop protection chemicals usage in India.

Bio pesticide• Biological origin i.e., viruses, bacteria, pheromones, plant or

animal compounds.• highly specific, affecting only the targeted pest or closely related

pests and do not harm humans or beneficial organisms.• The global market for biopesticides was valued at USD 1.5Bn in

FY13.• expected to grow at a CAGR of 15.5% to reach USD 3.2 Bn by FY18.• Asia and Europe are the fastest growing markets and are expected

to grow at CAGR of 14.2% and 16% respectively.• The Indian market currently stands at USD 0.16 billion and is

expected to grow to USD 0.35 billion by 2018.• Neem based pesticides, Bacillus thuringiensis, Nuclear

Polyhedrosis Virus and Trichoderma are some of the major biopesticides produced and used in India.

Factors affecting growth of Bio Pesticides • Positive:

Increasing demand for residue free crop protection products. Growth in organic food market. Easy registrations compared to conventional pesticides. Increasing concern about safety and toxicity of traditional pesticides.

• Negative:• Low reliability because of low stability.• Target specificity.• Slow in action compared to synthetics.• Shorter shelf life.• Erratic availability in the market.• Already established and strong market of

chemical pesticides.

$$

Key Players (India)Company Name Head office (India) Head office

(International)Sales (2013-14)

(in crore)

BASF india Mumbai Germany 4430Dupont Haryana USA 4200

Bayer crop Science Ltd. Mumbai Germany 3283Dow Agroscience ltd Mumbai USA 1980

PI industries ltd. Haryana India 1595Rallis India ltd. Mumbai India 1531

Excel Crop Care Ltd. Haryana India 965Meghmani organic Ltd. Ahmedabad India 893

Insecticide India Ltd. New Delhi India 864Dhanuka Agritec Ltd. New Delhi India 738

KEY GROWTH DRIVERS:

• Increasing demand for food grains• Limited farmland availability• Low Productivity• Growth of horticulture and floriculture• Increasing exports• Patent expiry

CHALLENGES• Support for Integrated Pest Management

(IPM) and rising demand for organic farming.• Threat from Genetically Modified (GM) seeds.• Low focus on R&D by domestic manufacturers

due to high costs.• Lack of education and awareness among

farmers.• Spurious products• Longer period for registration of innovative

products.

REGULATIONS• In India, the Ministry of Agriculture regulates the manufacture, sale, import,

export and use of pesticides through the 'Insecticides Act, 1968'. • Central Insecticides Board (CIB) constituted under Section 4 of the Act advises

Central and State Governments on technical matters. The Registration Committee (RC) constituted under Section 5 of the Act approves the use of pesticides and new formulations to tackle the pest problem in Various crops.

• The monitoring of pesticides residue levels in food comes under the purview of Union Ministry of Health and Family Welfare.

• The Registration Committee (RC) constituted under Section 5 of the Act approves the use of pesticides and new formulations to tackle the pest problem in various crops.

• The Environment Act 1986• BIS Act• Air act 1981• Water Act 1974• Hazardous waste Act 1989

Cntd…

Some of the challenges posed by the regulations for the industry are as below:

• A long period of ~3 years is required for approval of pesticides due to requirement of data on parameters of Chemistry, Toxicology, Metabolism, Persistence, Efficacy, and Patents& Trade Marks. The cost of data generation is ~2 Cr, leading to loss of business opportunity for the companies in terms of both cost and time.

• Due to lack of inspection staff, inspection of pesticidesis generally done for top 20 to 25 MNCs or large Indian companies, which usually follow the procedures and meet the norms. However, this leaves many small companies and importers products to remain uninspected.

Thank You