peru - iuj

TRANSCRIPT

COUNTRY PROFILE

PeruOur quarterly Country Report on Peru analyses currenttrends. This annual Country Profile provides backgroundpolitical and economic information.

1997-98The Economist Intelligence Unit15 Regent Street, London SW1Y 4LRUnited Kingdom

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The EIU delivers its information in four ways: through subscription products ranging from newslettersto annual reference works; through specific research reports, whether for general release or for particularclients; through electronic publishing; and by organising conferences and roundtables. The firm is amember of The Economist Group.

London New York Hong KongThe Economist Intelligence Unit The Economist Intelligence Unit The Economist Intelligence Unit15 Regent Street The Economist Building 25/F, Dah Sing Financial CentreLondon 111 West 57th Street 108 Gloucester RoadSW1Y 4LR New York Wanchai United Kingdom NY 10019, US Hong KongTel: (44.171) 830 1000 Tel: (1.212) 554 0600 Tel: (852) 2802 7288Fax: (44.171) 499 9767 Fax: (1.212) 586 1181/2 Fax: (852) 2802 7638e-mail: [email protected] e-mail: [email protected] e-mail: [email protected]

Website: http://www.eiu.com

Electronic deliveryEIU ElectronicNew York: Lou Celi or Lisa Hennessey Tel: (1.212) 554 0600 Fax: (1.212) 586 0248London: Moya Veitch Tel: (44.171) 830 1007 Fax: (44.171) 830 1023

This publication is available on the following electronic and other media:

Online databases CD-ROM Microfilm

FT Profile (UK) Knight-Ridder Information World Microfilms Publications (UK)Tel: (44.171) 825 8000 Inc (US) Tel: (44.171) 266 2202

DIALOG (US) SilverPlatter (US) University Microfilms Inc (US)Tel: (1.415) 254 7000 Tel: (1.800) 521 0600

LEXIS-NEXIS (US)Tel: (1.800) 227 4908

M.A.I.D/Profound (UK)Tel: (44.171) 930 6900

Copyright© 1998 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author’s and the publisher’s ability. However,the EIU does not accept responsibility for any loss arising from reliance on it.

Symbols for tables“n/a” means not available; “–” means not applicable

Printed and distributed by Redhouse Press Ltd, Unit 151, Dartford Trade Park, Dartford, Kent DA1 1QB, UK

ISSN 0269-5944

January 31st 1998 Contents

2 Basic data

3 Political background3 Historical background5 Constitution and institutions7 Political forces9 International relations and defence

10 The economy10 Economic structure12 Economic policy16 Economic performance18 Regional trends

19 Resources19 Population20 Education21 Health22 Natural resources and the environment

23 Economic infrastructure23 Transport and communications25 Energy provision27 Financial services28 Other services

29 Production29 Manufacturing32 Mining34 Agriculture, forestry and fishing

36 The external sector36 Merchandise trade38 Invisibles and the current account38 Capital flows and foreign debt40 Foreign reserves and the exchange rate

42 Appendices42 Regional trading associations43 Sources of information44 Reference tables

1

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

Peru

Basic data

Land area 1,285,216 sq km

Population 23.95m (1996 estimate)

Main towns Population in ’000, 1993 census

Lima 5,708 Piura 278Callao 640 Iquitos 275Arequipa 619 Chimbote 269Trujillo 509 Huancayo 258Chiclayo 412 Cuzco 256

Climate Varies considerably by region and altitude. In general temperate on the coast,tropical in jungles, cool in highlands. The western side of the highlands has adry climate, but on the eastern and northern sides there is heavy rainfallbetween October and April

Weather in Lima (altitude120 metres)

Hottest month, February, 19-28°C (average daily minimum and maximum);coldest month, August, 13-19°C; driest months, February, March, 1 mm aver-age monthly rainfall; wettest month, August, 8 mm average monthly rainfall

Language Spanish is the principal language and the lingua franca for the large numbersof Quechua and Aymara speakers. Quechua and Aymara also have officialstatus

Measures Metric system; also old Spanish measures, particularly in rural areas

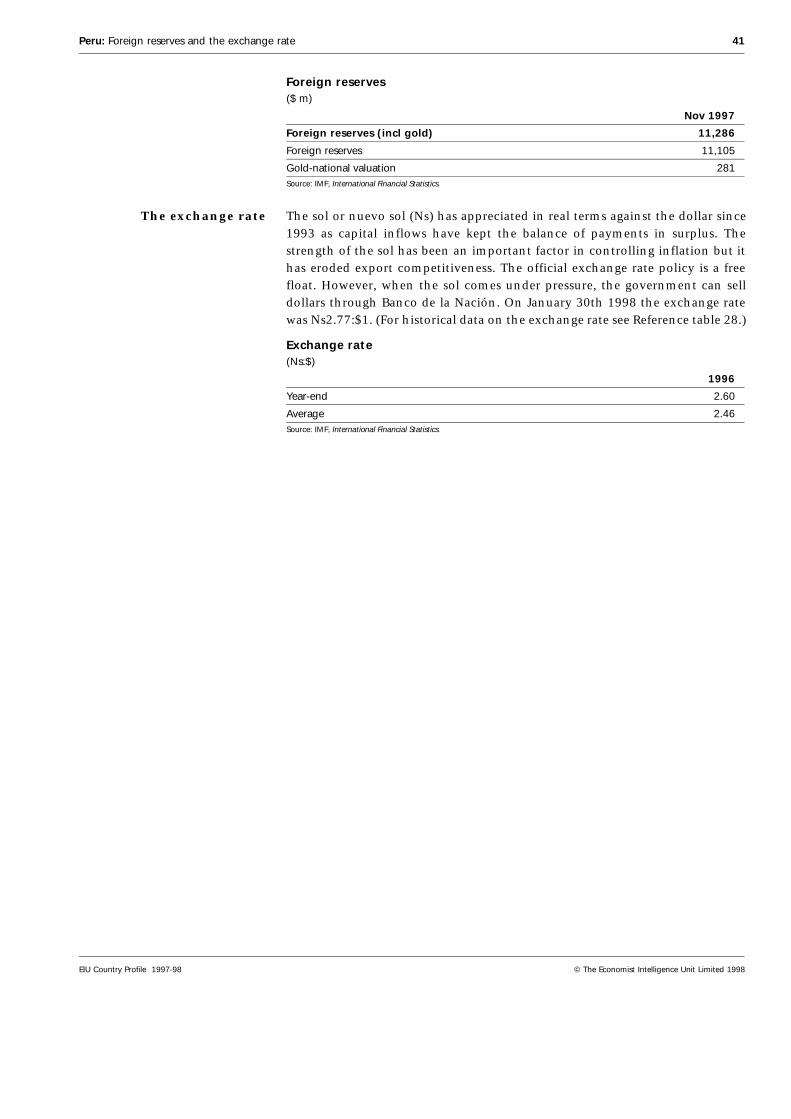

Currency Nuevo sol. Average exchange rate 1997, Ns2.67:$1; exchange rate on January30th 1998, Ns2.77: $1

Time 5 hours behind GMT

Public holidays January 1st; Easter (Maundy Thursday half day and Good Friday all day); May1st (Labour Day); June 29th (Saint Peter and Saint Paul); July 28th-29th (Inde-pendence Day); August 30th (Santa Rosa de Lima); October 8th (Battle ofArigamos); November 1st (All Saints Day); December 8th (Immaculate Concep-tion); December 25th (Christmas Day)

2 Peru: Basic data

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

Political background

Historical background

Peru is the birthplace of the Inca empire, one of the most important centres ofpre-Hispanic civilisation in the Americas. From Cuzco, their base in the high,southern Peruvian Andes, the Incas dominated the other tribes of the Andes aswell as the length of the Pacific coast from what is today southern Colombia tocentral Chile. An elaborate system of roads, garrisons and colonial settlementsallowed them to keep tight control of their large empire for more than acentury. Some of the Inca heritage survives in the Peruvian Andes today, in thesystem of communally owned lands, irrigation systems and shared communitylabour. The maize and potatoes first cultivated by the Incas have spread tobecome staple crops throughout the world.

Drawn by well-founded rumours of great wealth, the first Spanish conquerorsarrived in Peru in 1532. Led by Francisco Pizarro, they overcame the forces ofthe Inca Atahualpa: the rest of the empire swiftly fell to the conquistadores. Thenew capital, Lima, was founded in 1535 and the vice-royalty of Peru wasformally established in 1544. After the final defeat of the Incas in 1572, Spanishauthority went almost unchallenged for two centuries. Towards the end of the18th century, however, the ferment of new ideas and revolution in Europefuelled a desire for independence among landowners and criollos (descendantsof European settlers). Peru declared its independence from Spain on July 28th1821 (celebrated ever since as the national Independence Day holiday). A waveof military infighting ensued, punctuated by brief periods of relative politicalstability. The latter part of the 19th century was marked by the War of thePacific (1879-83), in which both Peru and Bolivia suffered ignominious de-feat—and the loss of important areas of territory—at the hands of Chile. Mu-tual suspicion still lingers today.

Peruvian 19th- and 20th-century history has been characterised by a successionof civilian caudillos, military strongmen and dictators of various persuasions.The election of one of the century’s more democratic leaders, Fernando Be-launde Terry, briefly looked to be a turning-point but he was overthrown by acoup in 1968: the left-wing, nationalist military, led by General Juan VelascoAlvarado, were convinced they could reform Peru faster and better than thecivilians. The first phase of military rule (1968-75) resulted in land reform,increased national control of natural resources and industrial partnership. Butspending and foreign borrowing spiralled out of control, ending in a bloodlesscoup in August 1975 which put General Morales Bermúdez in as president.

Democracy returned in 1980, when Mr Belaunde was elected for a secondperiod. Despite attempts at reform and liberalisation, world recession, the for-eign debt crisis and climatic disaster marred his presidency. Mr Belaunde’sparty, the centre-right Acción Popular (AP), lost support and, in the 1985general election, the left-of-centre Alianza Popular Revolucionaria Americana(APRA) was swept to office. A 36-year-old lawyer, Alan García Pérez, becamepresident amid popular euphoria and high expectations of change.

Peru: Historical background 3

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

From the outset, Mr García was a controversial figure. Radically unorthodoxeconomic policies initially generated high GDP growth rates and a sharp in-crease in purchasing power for the poor. But his popularity was short-lived.Economic mismanagement led to hyperinflation. Violent strikes affected al-most all economic activity. In mid-1987 an ill-judged move to nationalise thebanking system provoked strong protest and rallied opposition. By the elec-tions of 1990 Mr García and the APRA were discredited at home and abroadand the country was on the verge of economic collapse.

Against this depressing backdrop emerged a political unknown. Overcomingall the odds, Alberto Fujimori, the son of modest Japanese immigrants, whohad risen to become rector of Lima’s agrarian university, defeated both theAPRA party machine and Mario Vargas Llosa, the well-known novelist whoheaded a right-wing coalition. A pragmatist without party or programme,Mr Fujimori ran under the banner of hard work, honesty and technology, amessage which struck a chord among the voters. Once elected, he continued toprefer concrete achievements to ideology, improvising policy according tocircumstance.

Important recent events

July 1990: Alberto Fujimori, agricultural engineer and former university rector, takesoffice as president.August 1990: The government announces a series of drastic stabilisation measures;subsidies and price controls are removed and prices of many staples rise by 500%overnight.February 1991: The economy minister, Carlos Boloña, announces a sweepingprogramme of structural reforms, liberalisation and deregulation.April 1992: Faced with congressional opposition to proposals to give the securityforces greater powers in the fight against terrorism, Mr Fujimori closes Congress andsuspends the judiciary.April-August 1992: The Maoist guerrilla group, Sendero Luminoso, steps upbombings in Lima, killing dozens of civilians and severely damaging economicactivity. September 1992: Sendero Luminoso’s founder-leader, Abimael Guzmán, iscaptured in a surprise counter-terrorist police operation in Lima.November 1992: A planned coup by a group of serving and retired military officersis foiled. Elections are held for a new constituent assembly and Mr Fujimori’s Cambio90/Nueva Mayoría coalition wins an overall majority.December 1992: The new constitution is put to a national referendum andnarrowly approved. In a major departure from tradition, immediate presidentialre-election is permitted.April 1995: Mr Fujimori is re-elected outright, obtaining 64% of the valid votes inthe first round.April 1996: Mr Fujimori dismisses half of the 14-member cabinet, replacing themwith technocrats and entrepreneurs.December 1996-April 1997: Guerrillas hold hostages in the Japaneseambassador’s residence in Lima.February 1998: The Supreme Court upholds a 1996 law which interpreted theconstitution to allow Mr Fujimori to stand for president again in 2000.

4 Peru: Historical background

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

His rule has been characterised by a hybrid of democratic and autocratic ele-ments with a broad respect for press freedom. Under Mr Fujimori’s leadership,the traditional party system has given way to independent politicians. Mr Fuji-mori, who has shown no inclination to turn his own political movement into agenuine party, has been able to exploit the discredit into which the older partieshad fallen to enhance the authority of the executive branch.

Mr Fujimori’s style of governing owes something to the traditional LatinAmerican caudillo figure. His popular touch, which included frequent travel tothe remotest regions to supervise road repairs and school construction or tohand out advice to peasant farmers, gave him consistently high popularityratings, of more than 70%, until 1996. His 1992 self-coup (autogolpe), when heclosed down Congress and suspended the judiciary, was approved by the vastmajority of the population. A new constitution was enacted in 1993, andsubsequent laws have reduced the power of the legislature and reinforcedcentralism. In April 1995 Mr Fujimori was overwhelmingly re-elected as pres-ident for a second term. In the new, single-chamber Congress the governmentalliance, Cambio 90/Nueva Mayoría, holds 69 of the 120 seats.

An economic recession in 1996 severely damaged Mr Fujimori’s popularity,and since then disputes over the constitution have prompted harsh criticismfrom the news media. Although he is still credited with controlling inflationand combating terrorism, there has been growing dissatisfaction with per-ceived abuses of power by Mr Fujimori’s government.

Constitution and institutions

Peru’s current constitution, promulgated in 1993, is the fifth this century. Likemost of its predecessors, it is a pragmatic creation designed to bring the formallegal framework into line with the “new realities”. This time, the constitutionalinitiative responded to pressure from the international community, notablythe Organisation of American States (OAS), for a return to democratic rulefollowing Mr Fujimori’s April 1992 autogolpe.

The constitution was drafted by the 80-member constituent assembly,Congreso Constituyente Democrático (CCD, or Congress), elected in November1992. The main opposition parties boycotted that election, with the result thatMr Fujimori’s makeshift Cambio 90/Nueva Mayoría coalition obtained anoverall majority in the CCD. Several controversial changes, often promoted bythe president’s inner circle of advisers, were given unobstructed passagethrough the committees and plenary sessions. When put to the people forratification in what became seen as a plebiscite, the new constitution wasapproved by the tiniest of margins.

The 1993 constitution replaced the 1979 version which was seen as too statistfor Peru’s newly liberalised economy. The updated version enshrines free-market economic principles and reduces the role of the state. It also eliminatesmany congressional checks on the president, thereby enhancing the alreadysubstantial powers of the executive, and permits a president to stand for twoconsecutive terms. In theory the independence of the judiciary is strengthened

Peru: Constitution and institutions 5

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

by the new constitution. However, in practice the government often interfereswith the judiciary when rulings are not to its liking.

Congress now consists of 120 members, elected on a national basis every fiveyears through a system of lists prepared by the parties. Voters can overturn theparties’ choices of candidates by casting a preferential vote. However, thisoption is highly complex and well beyond the capabilities of less educatedvoters. The proliferation of small parties and supposedly independent move-ments has made recent ballot papers long and complicated: this tends to favourthe few better-known political movements.

Distribution of seats in Congress, Jan 1998

Cambio 90/Nueva Mayoría 69

Unión Por el Perú 12

Partido Aprista Peruano 8

Acción Popular-Code 7

Frente Independiente Moralizador 6

Movimiento Renovación 6

Others 12

Total 120Source: Local sources.

Internal war and economic chaos in the latter half of the 1980s weakened civilsociety and its institutions. This was especially true of political parties, thejudiciary, labour unions and peasant organisations. Congress is under the firmcontrol of the government: 52% of the valid votes cast in April 1995 gave 67 ofthe 120 seats to the government alliance, which comprises two movements ofso-called independents, Cambio 90, Mr Fujimori’s original movement, andNueva Mayoría, created to run in the November 1992 constituent assemblyelection. The opposition is led by Unión Por el Perú (UPP), a self-styled inde-pendent movement created to promote the 1995 presidential candidacy of theformer UN secretary-general, Javier Pérez de Cuéllar. UPP won 17 seats in theApril election. The remainder are divided among smaller, disparate groups,which include the once dominant traditional parties like APRA, Acción Popu-lar, Partido Popular Cristiano and others. Since the election, a number ofdefections has altered the distribution of congressional seats, but the govern-ments majority remains safe.

Ministries Formally, the Peruvian cabinet comprises 12 ministries under a premier who isknown as the president of the Council of Ministers. The economy minister istraditionally the most important, because he controls the purse- strings of allthe other ministries. There are few figures of weight in Mr Fujimori’s cabinet,however: his centralised style of government means that major decisions aremade in a small, closed circle of advisers and family members. Althoughcabinet meetings were rarely held, they have become more frequent sinceAlberto Pandolfi became prime minister in April 1996. Mr Fujimori channelsspending on social programmes and infrastructure through the presidencyministry, which is now second only to the economy and finance ministry inresources managed.

6 Peru: Constitution and institutions

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

Key political figures

Jorge Camet: He replaced the prominent Carlos Boloña as economy and financeminister in early 1993. Mr Camet has close links with the business community andhas presided over Peru’s private business lobby, Confiep. Under his stewardship,Peru in 1996 obtained a 20-year debt restructuring accord with the Paris Club and aBrady agreement with Peru’s commercial creditors. Carlos Torres y Torres Lara: A former labour minister and prime minister,Mr Torres y Torres Lara is one of Mr Fujimori’s oldest allies. He is vice-president ofCongress and helped draft the 1993 constitution. A lawyer, he is an adept defenderof controversial government actions and has often taken on the role of the unofficialspokesman of the governing alliance. He assumed a high profile in 1996 indefending Congress’s decision to pass a law opening the way for the president tostand for a third term.Martha Chávez: One of Mr Fujimori’s most vociferous and uncritical supporters,she obtained the highest number of preferential votes in the 1995 election andbecame the first woman to preside over Congress. Since then she has maintained ahigh profile as head of several legislative commissions, including one investigatingphone-tapping against opposition politicians and journalists.Vladimiro Montesinos: A lawyer and former army captain who was accused ofspying, Mr Montesinos is a shadowy but extremely influential, and feared, figure. Heis the effective, although not the titular, head of the Servicio de Inteligencia Nacional(SIN, the national intelligence service). He acts as liaison between Mr Fujimori andthe armed forces and is said to be the determining voice in senior militaryappointments. He has been credited by Mr Fujimori with much of the planning ofthe successful April 1997 raid on the Japanese ambassador’s residence (seeSubversion). Alberto Andrade: A lawyer and successful businessman, he has emerged asMr Fujimori’s main rival for the presidency in 2000. A liberal in economic matters, hewas associated for many years with the Partido Popular Cristiano (PPC). As aneffective mayor of Miraflores, he received 93.5% of the votes when he was re-electedin 1993. He then went on to be elected mayor of Lima. In 1995 he launched anindependent political movement, Somos Lima (We are Lima). In mid-1997 heannounced plans to establish a national party, Somos Perú. Although he hasdeclared his candidacy for a second term as the mayor of Lima in 1998, he has notruled out standing for the presidency in 2000.

Political forces

The political landscape of Peru in the mid-1990s is in stark contrast to thepicture a decade earlier. The election of Mr Fujimori, an outsider with no linksto the traditional political classes, transformed the country’s power structure.Subsequent elections have confirmed the decline in the influence of the trad-itional parties and the emergence of new actors on the political scene.

The armed forces In the absence of an organised party, Mr Fujimori’s only genuine power base isthe armed forces. From the earliest days of his first government, Mr Fujimorisought a close alliance with the military, primarily with its key branch, the

Peru: Political forces 7

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

army. By constitutional mandate, the president is commander-in-chief ofthe armed forces. Mr Fujimori used this position to hand-pick officers for keypositions, ending the traditional system of promotion by seniority. On six con-secutive occasions General Nicolás de Bari Hermoza has been reappointed aspresident of the joint chiefs-of-staff and the army’s strongman. In late 1997,however, Mr Fujimori suggested that Mr Hermosa’s position was under review.The influence of the army over civil society has steadily increased: in the exten-sive regions of the country which remain under emergency rule, army com-manders are simultaneously the highest political authorities and have control ofthe local police forces. In addition, the army has decisive influence in develop-ment projects in urban shanty towns and impoverished rural communities: itbuilds roads and irrigation systems, lends agricultural machinery to peasantfarmers and distributes food and medicines on behalf of other state agencies.

Subversion

1980: A Maoist guerrilla group, Sendero Luminoso (Shining Path), emerged. Basedin the impoverished Andean department of Ayacucho, Sendero Luminoso used acombination of terror tactics and political ideology to dominate many peasantcommunities in remote areas where there was little state presence. It spread in themid-1980s to the central Andes and the Huallaga valley, heartland of the illegal cocatrade.1984: A second guerrilla group, Movimiento Revolucionario Tupac Amaru (MRTA),started operating. Pro-Cuban, it was more in the traditional mould of Latin Americanguerrilla movements, using kidnap and ransom demands to try to achieve its aims.1984: The army took over full responsibility for counter-insurgency operations.Many areas of the country were put under state of emergency laws, with consequentrestrictions of civil liberties. Widespread violations of human rights ensued.April 1992: Following Mr Fujimori’s shutdown of Congress, Sendero Luminosoextended its armed struggle to the capital. Bombings became increasingly frequent.By this time, over 25,000 Peruvians had died in guerrilla-related violence andmaterial damage had cost an estimated $22bn, almost as much as the country’sentire foreign debt.June 1992: MRTA’s leader, Victor Polay, was captured in Lima; the subsequentdisintegration of his movement was rapid.September 1992: A combination of painstaking police work and an element ofluck led to the capture of Sendero’s ideological leader, Abimael Guzmán.Mr Guzmán’s capture and subsequent renouncing of the armed struggle were aturning-point. Arrests of other high-ranking members followed. A “repentance law”encouraged guerrillas to give themselves up in return for lenient treatment: theinformation they provided to military authorities led to yet more arrests.December 1996: Fourteen MRTA guerrillas, led by Nestor Cerpa Cartolini,assaulted the residence of the Japanese ambassador in Lima. They initially took morethan 600 hostages, including high-level government officials, foreign diplomats,businessmen and other influential personalities, but released all but 72. April 1997: After peace talks flagged, Mr Fujimori ordered some 150 commandosto storm the residence, in a well-planned operation. Seventy-one hostages werefreed. One hostage, two commandos and all 14 guerrillas were killed in the raid.

8 Peru: Political forces

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

The highest-ranking military officers share a common set of values with thepresident and agree with his view of the political system. (Dissident officershave, over the years, been “invited” to retire early.) In essence, the president seesthe need for a strong hand to tame the corrupt and inefficient political parties.Unlike its counterparts in much of Latin America, the Peruvian army sees itselfmore as a pressure group than a political participant. Low salary levels remain asource of dissatisfaction and some army officers resent Mr Fujimori’s interven-tion in military appointments. Nevertheless, malcontents are in a minority andthe prospects of a successful military coup are slight.

The Catholic Church The Catholic Church, which has sporadically criticised Mr Fujimori’s tougheconomic policies, retains the allegiance and affection of the majority of Peruvians.Its practical influence, however, is slight. In addition, in many parts of Peru’shinterland, the traditional influence of the Catholic Church is being under-mined by a host of evangelical movements. During 1995 Mr Fujimori came intodirect confrontation with senior churchmen about family planning: opinionpolls showed that Peruvians overwhelmingly sided with the president and hiscommitment to make free contraception (including sterilisations) available toall Peruvians. The Church has been forced to beat a strategic retreat.

Unions Labour unions, which were inordinately powerful a decade ago, are todayweakened, perhaps irrevocably. In the new political and economic climate theunions are often seen as irrelevant or are associated with the economic collapseof the late 1980s. The number of strikes has decreased sharply. Union leadershave proved incapable of capitalising on the thousands of jobs lost throughprivatisations to arouse popular sympathy. The mass demonstrations that wereonce a feature of street life in central Lima are now only occasionally seen.

International relations and defence

Mr Fujimori’s foreign policy is trade-driven and pragmatic. He has used hisown contacts and Peru’s geographical position to build links with the countriesof the Pacific Basin. At the same time, he has moved to strengthen bilateraltrade links with neighbouring countries. He has made goodwill visits to allPeru’s neighbours during his presidency. Relations with Bolivia have gone fromstrength to strength since the 1992 Ilo Agreement which grants land-lockedBolivia access to the Pacific Ocean for the first time since the War of the Pacific(1879-83). (Peru and Bolivia both lost land to Chile in the war.) In return, Peruhas access to the Atlantic via Bolivia’s river port, Puerto Suárez. Relations withChile remain cool more than a century after the war. Several matters are stillpending from a peace treaty signed in 1929. An agreement, known as the LimaConvention, was reached by the two governments in 1993 but was not ratifiedby the Peruvian Congress. In January 1996 the Peruvian government submittednew proposals to Chile, omitting mention of the Lima Convention. Progresstowards a final solution will remain slow.

Peru: International relations and defence 9

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

The relationship with Ecuador is Peru’s greatest problem. In late January 1995 anot uncommon skirmish between border patrols escalated into serious hostili-ties along a stretch of uninhabited, undemarcated jungle border. After a monthof fighting which left several dozen dead on each side, peace negotiations beganunder the auspices of Argentina, Brazil, Chile and the US. These were the fourguarantor countries of the Rio Protocol, a 1942 peace treaty signed by Peru andEcuador after an outbreak of hostilities in 1941. The establishment of a demili-tarised zone was a first step towards resolution of this long-standing conflict, inwhich nationalistic passions are readily aroused. In October 1996, Ecuador andPeru signed the Acuerdo de Santiago (Santiago Accord) under which they agreedto hold negotiations on the so-called “existing impasses” between the two na-tions within the framework of the Rio Protocol. The most contentious issues areEcuador’s refusal to accept the territorial division established by the Rio Protocoland its demand for a sovereign outlet to the Amazon. In November 1997 the twosides signed a four-point accord to discuss Ecuador’s non-sovereign navigationof the Amazon as well as border demarcation.

Because of a reduction in violations of human rights and the re-establishmentof democracy, relations with the US have improved. However, cultivation ofthe coca leaf and its processing into cocaine is a source of periodic tension.Every year, in a process called certification, the US government assesses theefforts made by drug-producing countries to combat the drug trade. In 1995the US was critical of Peru, only grudgingly renewing its certification for USassistance, and only in the interests of national security. In 1996 and 1997,however, the US State Department granted certification with more enthusiasm,congratulating Peru on its full co-operation over efforts to eradicate the drugstrade. However, there are still some deep-rooted suspicions about drugs-relatedcorruption inside the military.

The economy

Economic structure

Peru has a dual economy. There is a relatively modern sector on the coastalplains and a subsistence sector in the mountains of the interior, which is cut offby poor transport and communications. Economic power has traditionallybeen in the hands of an elite of European descent. Services account for 45% ofGDP, industry (including mining) for about 33% and agriculture for 13% (seeReference table 7). Mining is important for the balance of payments, providingalmost half of Peru’s export earnings. Industry is fairly diversified, with food,fishmeal, metals, steel, textiles and petroleum refining the largest sectors.Agriculture provides employment to over 30% of the workforce. The 1993census gave a labour force of 12.9m and an economically active population of7.1m, of whom 5m were men.

10 Peru: Economic structure

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

Main economic indicators

1996

Nominal GDP (Ns m) 149,481

GDP growth (%) 2.6

Consumer price inflation (av; %) 11.5

Exports fob ($ m) 5,897

Imports fob ($ m) 7,897

Current-account balance ($ m) –3,607

Exchange rate (av; Ns:$) 2.45

International reserves ($ m) 10,776.1Source: Banco Central de Reserva, Nota Semanal.

Peru is still largely a land of impoverished peasant farmers and underemployedshanty-town dwellers. According to the 1993 census, of the 7.1m economicallyactive population aged 14 and over, 20% were unskilled and 19% skilled agri-cultural workers. Of the total workforce, 10% described themselves as profes-sionals, 5% as technicians and 6% as office managers and workers. Only 13%of the non-agricultural workforce was qualified. Urban underemployment isnow classified as “visible” (those who work less than 35 hours but are willingto work more) and “invisible” (those who work more than 35 hours but earnless than needed to acquire the minimum consumer basket). In 1996 the ratesof underemployment were 17.9% and 24.7%, according to the two measuresrespectively. Income distribution is extremely unequal: the poorest 20% re-ceive under 5% of national income.

Unemployment and underemployment in Metropolitan Lima(%)

1995 1996

Unemploymenta 8.4 7.9 Male 6.7 7.2 Female 11.7 9.1

Underemployment 42.2 42.6 Visible 15.6 17.9 Invisible 26.8 24.7

a As % of labour force aged 14 years and above.

Source: Banco Central de Reserva, Memoria 1996.

According to official statistics, the service sector employs 50% of the eco-nomically active population in Lima. This conceals a harsh reality: the major-ity included in this figure eke out a precarious existence, selling low-valueobjects in the informal economy. The adjustment programme applied since1990 has sharply reduced formal employment. Drastic reductions in the statebureaucracy and rationalisation of state-owned companies as they were priva-tised has meant the loss of hundreds of thousands of jobs. In 1997 someimprovement was reported, with a 2.6% increase in employment in companieswith more than 100 workers.

Since colonial times and throughout the 19th and 20th centuries, Peru’s wealthhas been highly dependent on the extraction of natural resources. Mining hastraditionally been the backbone of export earnings. Despite a fall in the

Peru: Economic structure 11

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

percentage of total exports represented by minerals in the 1990s, mining stillaccounted in 1996 for 45% of total export earnings (see Reference table 18). Thisfigure is likely to rise in the late 1990s as new investments come on stream. In1994 Peru became the world’s second fishing nation after China, with a totalcatch of 11.6m tonnes. Fishing (largely for processing into fishmeal) earned$1,121m in export revenue in 1996, 19% of the total. In years like 1995 wheninternational mineral and commodity prices are high, around three-quarters ofPeruvian foreign-exchange earnings come from exports of minerals, fishmeal,oil and traditional semi-processed agricultural products such as cotton, coffee orsugar. This dependence upon exports of primary products leaves the economyvulnerable to shocks from volatile commodity prices.

Comparative economic indicators, 1996

Peru Bolivia Brazil Chile Paraguay

GDP ($ bn) 40.8 7.7 748.6 71.9 9.5

GDP per head ($) 2,539 1,015 4,745 4,988 1,925

Consumer price inflation (%) 11.5 12.4 16.5 7.4 9.8

Current-account balance ($ bn) –3.6 –403 –24.3 –2.8 –0.7 % of GDP –5.9 –5.2 –3.3 –3.9 –7.4

Exports of goods ($ bn) 5.9 1.1 47.7 15.5 2.7

Imports of goods ($ bn) 7.9 1.4 53.3 16.5 4.1

Trade balance fob (% of GDP) –3.3 –4.0 –0.7 –1.4 –14.7

External debt ($ bn) 31.0 5.3 172.4 27.3 2.2

Debt-service ratio, paid (%) 20.9 25.3 56.2 25.6 6.1Source: EIU.

Economic policy

After various economic experiments from the mid-20th century—the laisser-faire approach of the 1950s switching to import substitution and increasedgovernment spending in the 1960s—the economy turned inward during thenationalistic left-wing military government of General Juan Velasco Alvarado(1968-75). During this period the government nationalised most large foreigncorporations, creating huge state companies. Radical agrarian reform eliminatedthe large haciendas (estates) and replaced them with agricultural co-operatives,most of which have now disappeared.

The decade of democracy which followed the long period of military rule failedto bring prosperity to the bulk of the population. Indeed, by 1990 the eco-nomic policies of two consecutive democratically elected governments seemedto have brought the country to its knees. The hesitant liberalisation of theBelaunde regime (1980-85) collapsed with the advent of the debt crisis as Perudeclared a moratorium on servicing its foreign debt. GDP fell, inflation acceler-ated and the government retreated into protectionism. In 1985 the incomingpresident, Alan García, devalued the currency, raised wages and subsidisedfoodstuffs, restricted debt servicing, and banned many imports in an attemptto provoke demand-led growth. A boom in 1986-87 proved short-lived. Theeconomy contracted sharply in 1988-90, and by the time Alberto Fujimori tookpower in 1990, inflation was running at around 40% per month.

12 Peru: Economic policy

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

Mr Fujimori’s election in 1990 marked an immediate and radical change inpolicy direction. Although he had campaigned on the pledge of adjustmentwithout shock measures, it was clear that drastic measures were necessary totackle hyperinflation. On taking power, he eliminated price controls and statesubsidies. The immediate effect was for prices to spiral further. But a fewmonths later the drastic stabilisation policies began to show results and infla-tion subsided (see Reference table 18). A sweeping programme of economicliberalisation and structural reform was launched in February 1991 under adynamic economy minister, Carlos Boloña.

Key economic policy changes since 1990

● Trade liberalisation. Import duties were slashed and a simplified two-tier systemintroduced. Over 90% of all imports now pay 12% duty; the remainder pay 20%.● Unification and liberalisation of the exchange rate and abolition of all restrictionson capital flows. ● Thorough overhaul of the fiscal accounts. Expenditure was reduced through theabolition of subsidies, followed by privatisation of state-owned companies. The taxauthority, Sunat, was reorganised and tax collections were raised from less than 5%of GDP in 1990 to around 14% in 1996.● From 1993 the Banco Central de Reserva (the Central Bank) began to operate aninformal currency board under which sols in circulation have to be fully backed byforeign reserves. ● Gradual restoration of relations with the international financial communityfollowing a monitoring agreement and the granting of an extended fund facility bythe IMF in 1993.● Reform of the financial system, with new laws encouraging the development ofthe commercial banking sector and abolishing the state-owned, subsidiseddevelopment banks for agriculture, mining and other sectors.● Creation of a system of private pension funds, with voluntary affiliation.● Reform of the labour market, including greater freedom to hire and fire.● Legislation providing equal treatment and guarantees to foreign investors.

Fiscal policy Since 1990 the fiscal accounts have been transformed by the radical restructur-ing of the public sector (see Reference tables 1 and 2 for data on budget andpublic-sector finances). Spending on salaries has fallen sharply in real terms asthe state sector has been cut, while proceeds from privatisation and greater taxcompliance have increased revenue. In 1994 the public sector showed a finan-cial surplus (including interest payments) equivalent to 2.1% of GDP, com-pared with a deficit of 7.5% of GDP in 1990. Fiscal discipline was relaxed as thegovernment increased public spending sharply in the run-up to the generalelection of April 1995. The government trimmed spending after the election.Even so, the public-sector accounts (including interest payments) showed adeficit of 1.2% of GDP in 1995, compared with a surplus of 2% of GDP for1994. Spending cutbacks were necessary not only to ensure continued fiscalsoundness, but also to cool an overheating economy. In 1996 both current andcapital spending fell in real terms, restoring a surplus of 2.4% of GDP.

Mr Fujimori committed himself in his second term to increasing spending onsocial programmes to alleviate poverty. His scope for doing this depends upon

Peru: Economic policy 13

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

further gains in tax collection. Privatisation receipts, an important source offunding for social spending, will diminish. In addition, from 1997 onwards thegovernment’s foreign debt-service payments to commercial creditors (followingthe implementation of the Brady-style debt restructuring in mid-1996) and tobilateral Paris Club creditors has increased sharply.

Central government operationsa

(% of GDP)

Jan-Sep1995 1996 1997

Current-budget balance 0.4 1.5 3.0 Income 13.6 14.2 14.2 Expenditure 13.2 12.7 11.2 Interest 3.0 2.2 1.5 Other 10.2 10.5 9.7

Capital-budget balance –2.0 0.7 –2.2 Income 1.6 3.9 0.5 Expenditure 3.6 3.2 2.7

Overall balance –1.6 1.8 0.8

a Preliminary.

Source: Banco Central de Reserva, Nota Semanal.

Non-financial public-sector operations(% of GDP)

Jan-Sep1995 1996 1997

Current-budget balance excl interest 5.3 5.8 7.0 Interest 3.2 2.3 1.6

Current-budget balance 2.1 3.4 5.4

Capital-budget balance –3.4 –1.1 –3.6 Income 1.6 3.7 0.5 Expenditure 5.0 4.8 4.1

Overall balance –1.3 2.4 1.8Source: Banco Central de Reserva, Nota Semanal.

Tax reform The tax authority, Sunat, has been completely overhauled and is now an effi-cient and independent institution. From the dismal levels of revenue in 1989,when tax collected fell to below the equivalent of 7% of GDP, better systemsand a programme combining taxpayer education, penalties for evaders andpayment of arrears by instalments for industrial companies have boosted taxrevenue to about 12% of GDP in 1996, up from 11.5% in 1995. Sunat aims inthe medium term to raise tax revenue to between 20% and 22% of GDP.

Monetary policy In 1993 following a monitoring agreement with the IMF, the government intro-duced an informal currency board system whereby domestic currency has to befully backed by foreign reserves. High capital inflows caused foreign reserves torise sharply in 1993-94 (see Reference table 27). The Banco Central de Reserva(the Central Bank) allowed the accumulation of foreign reserves to expand themonetary base, with little recourse to sterilisation. It judged—correctly—thatthe expansion in the monetary base and other monetary aggregates was war-ranted by economic growth and remonetisation of the economy following the

14 Peru: Economic policy

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

hyperinflation of the late 1980s and early 1990s. As a result, rapid monetarygrowth did not fuel inflationary pressures. In 1995-96 the Central Bank tight-ened monetary policy to cool aggregate demand. (For data on money supply seeReference table 3.)

Foreign investment A cornerstone of Mr Fujimori’s economic policy has been that, in the absenceof adequate levels of internal savings, growth must be led by foreign invest-ment. To that end, the government has passed a series of laws encouragingprivate investment and imposing specific codes for the various productivesectors. Even the ownership of land, a politically sensitive issue, has beenliberalised and opened up to private investment, with foreigners as free toinvest as Peruvian nationals. Investment guarantees have been signed with anumber of international agencies.

Privatisation The principal stimulus to foreign investment has been the privatisation pro-gramme. After a hesitant start in 1991 and delays in the wake of the April 1992autogolpe, the disposal of state-owned companies got under way in earnest inlate 1992 with the sale of the iron producer, Hierroperú, and, at the start of1993, the national airline, Aeroperú. Since then, the process has been uninter-rupted and largely successful. The government’s sale in 1994 of stakes in thetwo telecommunications companies, Entel and Compañía Peruana deTeléfonos (CPT), attracted $1.3bn in cash and $700m in investment commit-ments from the Spanish telecommunications company, Telefónica. The privat-isation commission, Comisión de Privatización (Copri), is recognised to haveacted with efficiency and transparency.

At the end of 1997 almost all sales had been completed in telecommunications,banking, tourism and light industry, and about four-fifths in mining and met-als, basic industry, transport and cement. The major outstanding sales were theremaining units of Centromín, the huge state mining and refining company,two Petroperú refineries and the electricity generating units of Electoperú.Plans for the privatisation of Lima’s water utility, Sedapal, have been aban-doned, and the state has promised to invest $2.5bn by 2000.

In most privatisations, company workers are given the opportunity to buy upto 10% of the shares, in many cases in exchange for their rights to severancepay. The state retains a percentage in several important companies, notably thetelecommunications company now operated by Telefónica and in certain elec-tricity generators and distributors. Some 400,000 investors have acquiredshares through the so-called citizens’ participation programme since it beganin 1994, bringing a wider and more diversified pattern of share ownership.

Private pension funds Parallel to the privatisation programme and following the example ofneighbouring Chile, Peru has created a system of private pension funds (admin-istradoras de fondos de pensiones, AFPs). The purpose was twofold: to reorganisethe chaotic state social security system; and to offer a decent retirement pen-sion to members of the funds, while simultaneously encouraging domesticsavings and the creation of a local capital market.

Peru: Economic policy 15

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

Economic performance

Since liberalisation commenced in 1991, the Peruvian economy has been in aperiod of profound transition. Capital inflows have fuelled a strong economicrecovery (see Reference tables 5 and 6). However, the rapid economic growth of1993-95 is in large part attributable to a low base following the dramaticdecline of the late 1980s: GDP slumped by 22% between 1988 and 1992. GDPper head in 1996 was still only 4% above its 1987 level in real terms.

Gross domestic product(% real change, year on year)

Average 1992-95 1996a Jan-Sep 1997

Private consumption 5.8 1.4 4.0

Government consumption 7.0 1.6 –0.6

Gross fixed investment 15.3 –3.2 13.4

Exports of goods & services 6.9 11.4 16.3

Imports of goods & services 16.9 0.6 12.2

GDP 6.3 15.0 7.6

a These figures, from Nota Semanal January 23rd 1998, differ from the preliminary figures in theBanco Central de Reserva annual publication, Memoria 1996, given in Reference table 7. TheMemoria 1996 was published in mid-1997.

Source: Banco Central de Reserva, Nota Semanal.

The economic recovery was investment-led. A surge in private and publicinvestment raised the investment to GDP ratio from 21% in 1990 to 28% in1994. In 1994 growing confidence in the economy and a strong sol stimulateda consumer boom. Despite high interest rates, purchases of consumer durableson instalment plans boomed. Many of these consumer goods are imported.High import tariffs starved consumers of imported goods and luxuries for dec-ades. Once import tariffs were lifted, pent-up demand overflowed, contributingto the deterioration in the trade balance.

The benefits of opening up the economy have so far been confined to themiddle and upper classes, a small sector of the population. They have notreached either the hinterland or the shanty towns around the major citieswhere the bulk of the population live. Growth, while impressive, is unbal-anced. Peru has always been a country of extreme inequalities in terms ofincome distribution. The recent reforms have aggravated this structural imbal-ance.

Control of inflation was widely cited by voters as the principal reason for theircontinuing support for and re-election of Mr Fujimori in 1995. Nominal wagesoutstripped inflation in 1991, but the effect of hyperinflation and recessionkept real wages and salaries depressed in the first years of Mr Fujimori’s govern-ment. As growth has recovered, and inflation has remained low, real wagegrowth has been erratic. Central Bank figures show that after a strong increasein 1994, real wages had slipped back to their 1992 level by 1996. In 1993, theminimum wage level fell to under 60% of its August 1990 level. It recoveredslightly, to 82% of the 1990 level, by 1996, and then received a strong boost in1997, when it was adjusted upwards by 75% in real terms, restoring it to 40%above the 1990 level. (For prices and earnings, see Reference table 8.)

16 Peru: Economic performance

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

Price stabilisation and the dismantling of the two guerrilla groups, SenderoLuminoso (Shining Path) and Movimiento Revolucionario Tupac Amaru(MRTA), paved the way for strong GDP growth in 1993-95. The economy grewby 6.4% in 1993 and by 13.1% in 1994, easily the highest rate in the region.The economy did well again in 1995, growing by 7.2%. However, concernabout the widening current-account deficit caused the government to tighteneconomic policy in 1995 and growth fell to 2.6% in 1996, before recovering toaround 7% in 1997.

Agriculture Agricultural output contracted sharply in 1990-92. Guerrilla activity forcedfarmers off the land; liberalisation increased competition from imports; andcredit dried up following the closure of the state-owned bank, Banco Agrario.In addition to this, freak weather in 1992 decimated crops in the highlands andthe coastal plain. Output has recovered since then. Overall agricultural growthhas averaged 9% between 1993 and 1996. Output of export-oriented crops,such as cotton, sugar cane and asparagus, has been boosted as new investmentprojects have come on stream. Staple foods, such as potatoes, yucca and plan-tains, have also shown strong growth over the period (see Reference table 15).Harvests in 1997 were affected in the second half of the year by the El Niñoclimatic phenomenon. Crop production for the year to November 1997 wasonly 3.1% above the level for the same period in 1996.

Gross domestic product by sector(% real change, year on year)a

Average 1992-96 1996 Jan-Nov 1997

Agriculture & livestock 5.2 5.8 4.2

Fisheries 5.6 5.1 1.3

Mining 3.2 2.8 5.5

Manufacturing 5.1 2.7 7.5

Construction 13.2 –4.6 21.9

Services 4.6 3.6 6.5

GDP 5.5 7.2 7.6

a Preliminary.

Source: Banco Central de Reserva, Nota Semanal.

Construction Exceptionally high growth in construction in 1993-94 was a direct result ofhigh public spending on the rehabilitation of physical infrastructure, primarilyasphalting and rebuilding roads and bridges neglected for the previous decade.Construction activity grew by 34.5% in 1994 and by another 17.5% in 1995.Growth came to an end in 1996, as activity declined by 4.6% due to the sharpreduction of spending on infrastructure. However, the industry bounced backin 1997, stimulated by a surge in private sector investment. Construction out-put in January-November 1997, was 21.9% above its level in the same period of1996. (For construction data, see Reference table 17.)

Fishing Substantial investment in new plant has helped to increase the capacity of thefisheries sector by 50% in the 1990s. However, climatic variations have a strongimpact on annual catches. After growing by 21% in 1993 and 28.9% in 1994,the sector contracted by 19.1% in 1995 as a result of a fishing ban to replenish

Peru: Economic performance 17

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

stocks and less favourable maritime conditions. After the modest recovery of5.1% registered in 1996, the El Niño currents affected the catch in 1997, so thatin January-November production was only 1.3% higher than the same periodin 1996. El Niño’s effects are expected to continue into 1998. (For fishingproduction data, see Reference table 16.)

Mining The mining sector, which accounted for 11% of GDP and around 40% of exportearnings in 1994, grew by an annual average of around 5% in 1993-96. Gold hasbeen the fastest-growing subsector, owing to the success of the Yanacocha mineoperated by Newmont of the US. Iron output expanded strongly in 1993 and1994 after Hierroperú was sold to Shougang of China, but contracted in 1995, asa result of a prolonged strike and marketing problems experienced by ShougangHierro. Production of copper, the largest export earner, contracted in 1994 butrose by 11.3% in 1995 and a further 20% in 1996 as a result of heavy investment.Investment will drive strong increases in output of most minerals towards theyear 2000. (For minerals production data see Reference table 14.)

Manufacturing The manufacturing sector contracted sharply during the economic collapse of1989-90. Following a slight upturn in 1991 manufacturing output stagnated in1992-93, hit by depressed domestic demand and cheaper imports as tariff pro-tection was lifted. A recovery in consumer spending and a 40% rise in fishmealvolumes drove a 17% expansion in overall manufacturing output in 1994.However, production remains depressed. After moderate growth in 1995 and1996 (by 4.2% and 2.7% respectively), production is reported to have risen by7.5% in the first 11 months of 1997. But still, in November 1997, the manufac-turing sector was estimated to be operating at just 70% of installed capacity.Although this figure probably overestimates the current capacity of the manu-facturing sector, it shows that the sector has not recovered its former level ofactivity. (For manufacturing production data see Reference table 13.)

Regional trends

Regional imbalances in Peru are both historic and profound. The greater thedistance from the capital, Lima, and from a handful of other developed urbancentres, the more the economic and social indicators deteriorate. An attemptby the government of Alan García (1985-90) to devolve power to a dozenartificially created regions was swiftly halted by the incoming Fujimori admin-istration. Mr Fujimori’s style of government is to concentrate political power invery few hands.

Nevertheless, the new government has created a number of instruments whichassist in promoting economic development in the long-neglected provinces.The Fondo Nacional de Compensación y Desarrollo Social (Foncodes), set up in1991, is a channel for financing small infrastructure projects such as drinkingwater and sewerage systems and repairs to local roads and bridges. As well asimproving living standards, it provides temporary employment and remunera-tion in cash and kind for some of Peru’s poorest. The fund is used for politicalpurposes, serving as a permanent reminder to inhabitants of remote rural areasthat the presidency is working for them.

18 Peru: Regional trends

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

Another specially created state agency, Instituto Nacional de InfraestructuraEducativa y de Salud (Infes), is building new schools throughout the country.The need was great: in 1990, 80% of existing educational establishments hadno water, electricity or sewerage. Since then the government has pushedthrough promising if controversial legislation contained in Legislative Decree776. Opposed by the larger and more powerful town halls, the law redistributesresources from the richer to the poorer communities according to demo-graphic, territorial and social criteria. Financing comes from a special 2-per-centage-point allocation of the 18% value-added tax (VAT) collected atnational level. Funds are administered by the smallest local government units,known as districts.

Resources

Population

The 1993 census Peru’s 1993 census gave a mid-year population of 22,639,000 inhabitants (in-cluding an estimated 532,000 not contacted by census officials and anotherestimated 60,000 jungle-dwelling Indians). Of the total, 37% of all inhabitantswere under the age of 15 years. Population growth in 1990-95 averaged 1.78%per year. The National Statistics Institute estimates the 1996 population at23.95m. The overall population growth rate is expected to remain steady forthe next few years, giving a total projected population of 25.66m by the year2000. Life expectancy at birth is 71.1 years for women and 66.2 years for men.Improvements in health care have reduced the infant mortality rate from 109per 1,000 in 1972 to 48 by the end of 1996. (For population data see Referencetable 9.)

Internal migration Millions of Peruvians have migrated from the Andean highlands to the coastalcities over the past three decades in search of better standards of living, and thehealth-care and educational facilities usually lacking in the inaccessible hinter-land. From 1983, when the Sendero Luminoso (Shining Path) guerrilla move-ment became a serious threat to isolated rural communities and army reprisalswere stepped up, the number of migrants was swelled by hundreds of thou-sands of refugees from violence. The Geneva-based International Office forMigration (IOM) estimates that in the ten years from 1983 some 600,000Peruvians were forced to abandon their homes in the countryside for safety inthe provincial towns and the capital city. The 1993 census showed that 70% ofthe population lived in urban areas, up from 65% in the previous 1981 census.The trend towards urbanisation is expected to continue, although at a reducedrate since more peaceful conditions in the countryside have stemmed the flowof migrants and thousands of farming families have returned to their lands.Government funding of small infrastructure projects, as well as improvementsin highway infrastructure and communications in general, have also made theovercrowded shanty towns less attractive to potential migrants.

The proportion of the population living in poverty—defined as those living on$65 a month or less—dropped from 54% in 1990 to 50% in 1994. By mid-1995

Peru: Population 19

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

the number living in poverty (that is, unable to cover basic food, clothing,housing and transport requirements) remained around 11.5m. Of these, 4.7m,one-fifth of all Peruvians, were unable to meet basic nutritional needs. Strongereconomic growth and the targeting of the very poorest by the government’ssocial development projects is only gradually bringing reductions in povertylevels.

The indigenous population Peru has several large groups of Indians among its population. Quechua andAymara Indians have been integrated into society since the time of the Spanishconquest, but some tribes living in the remote Amazon basin have never yethad contact with the outside world. Most numerous of Peru’s non-integratedIndians are the Ashaninkas, who are to be found in greatest concentration inthe central jungle region east of Satipo. There are estimated to be between80,000 and 100,000 Ashaninkas, many of them living traditionally in smallextended family groups under a chief, dedicated to hunting, fishing and, to alesser extent, agriculture.

In the late 1980s and early 1990s, the Ashaninkas were a target for SenderoLuminoso. Subjected to blandishments, promises of land and weapons, or elseforcibly recruited, several thousand Ashaninkas are thought to have left theirlands to fight and act as guides for Sendero Luminoso. Ashaninka leaders claimthat some 3,500 men, women and children died between 1988 and 1995, andthat 50 communities have been abandoned.

Education

Public education standards are among the poorest in Latin America. This isespecially true of the rural areas where terrorism and a lack of discipline amongpoorly paid teachers have cut teaching hours drastically. As the Peruvian eco-nomy has been opened up and companies have been forced to compete in theinternational marketplace, the failings of the education system have beenthrown into stark relief.

Mr Fujimori has made improving education a priority for his second term.During his 1995 re-election campaign, he promised to build schools at the rateof three per day. However, teachers’ wages remain very low, school textbooksare almost non-existent and the education ministry has a reputation for ineffi-ciency. Overall, the state spends less than $100 per schoolchild per year.

Schools Although primary education is theoretically free, compulsory and available toall, the 1993 census showed that 12.7% of all children aged between 6 and 11,mainly in rural areas, do not attend school. In many remote regions, the localschool may offer tuition only to the first two school year grades. Drop-out ratesare as high as 40%. Few students go on to secondary education: while 4.2mwere enrolled at the primary level in 1995, only 1.8m were enrolled at thesecondary level. Illiteracy figures underline the problem: 1.78m Peruvians, or7.8% of the total population, were illiterate according to the 1993 census, andof the total 1.3m were women. In rural areas, the overall illiteracy rate was29.8%, compared with 6.7% in urban areas.

20 Peru: Education

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

Higher education There are around 50 universities in Peru, one-third of them in Lima. In 1995a total of 714,000 students were registered in universities or other higher educ-ation establishments. Technical education is woefully lacking. Quality trainingin practical skills at tertiary level is chiefly available through two institutions.They are: the Servicio Nacional de Adiestramiento en Trabajo Industrial (Senati),born out of a private-sector, entrepreneurial initiative, which operates nation-wide, providing full apprenticeships as well as short and sandwich courses; andthe Instituto Superior Tecnológico (Tecsup), a privately funded technologicalinstitute which caters for 1,000 full-time students in Lima and Arequipa.

Health

Statistics indicate that there have been some advances in healthcare in the pastfew decades. Life expectancy at birth, for example, rose from 47 years in 1960to 60 in 1985, 65 years in 1993 and 68 years in 1996, while infant mortalitydeclined from 109 per 1,000 in 1972 to 82 in 1981 and 48 in 1996. The severeeconomic recession of the late 1980s and the post-stabilisation recession of theearly 1990s, however, saw a decline in health-service funding and a sharp risein illnesses such as tuberculosis. The cholera epidemic which broke out in early1992 and spread rapidly throughout Peru was proof of poor overall levels ofnutrition and hygiene. Child malnutrition, measured by height and weightstatistics, remains a serious problem, especially in the remoter rural districts.According to the economy ministry, the rate of child malnutrition was reducedfrom 35% in 1993 to 26% in 1996. Regional variations in infant mortality arevery pronounced. Vaccination programmes ensure that nearly all children areprotected against polio, diphtheria, measles, tetanus and tuberculosis.

Healthcare for most of the population is provided by the health ministry andthe social security system. The latter has undergone a number of recent reforms.Through more than 300 hospitals, clinics and health centres around thecountry, it provides health services to 6.5m Peruvians, 2.5m of them are em-ployees on official company payrolls, the remainder their spouses and depend-ent children. Until the middle of 1995, employers paid the equivalent of 6% andemployees 3% of their salaries; now, the entire contribution is paid by theemployer while the employee is responsible for paying into either the statepension plan (now managed by a separate entity, Oficina de NormalizaciónPrevisional, ONP) or a private pension fund (administradora de fondos depensiones, AFP).

The three branches of the Peruvian armed forces and the Policía Nacionalprovide health services for their personnel and family members. Military andpolice hospitals are usually far superior to their counterparts in the publicsector. Some universities, municipalities and professional associations alsohave their own hospitals and health centres. In Lima and some other majorcities, the number of private clinics has grown rapidly since 1990. Privatehealth insurance schemes, a recent development, are proving attractive to thebetter-off.

Those who are not affiliated to the state national insurance scheme or otherproviders and have no private health insurance are entitled to free health-care

Peru: Health 21

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

provided by the ministry of health. Technically, this is free; in fact, most publichospitals are so underfunded that patients must buy their own medicines andbandages and rely on relatives for food.

Natural resources and the environment

Geography With an area of 1,285,216 sq km, Peru is the fourth largest country in LatinAmerica after Brazil, Argentina and Mexico. Topographically, Peru is dividedinto three regions: the coastal plain, the Andean highlands and the jungle. Thenarrow, arid coastal region bounded by the Pacific Ocean to the west and theAndean foothills to the east is the most densely populated region. Some 60rivers flow down from the Andes to the Pacific: their valleys are intensivelyfarmed. To the east are the valleys and high plains of the Andes: these were thepopulation centres of the great pre-Hispanic cultures and continue to be hometo around one-third of the population. Further east are the mountain slopes,lowlands and tropical rainforest of the selva or jungle, which comprises aboutthree-fifths of the national territory but is sparsely settled and has little agricul-ture or other development. Throughout history the rugged nature of the terrainhas been a serious obstacle to any attempt to integrate the country.

Climate The coastal climate is dominated by the cold current known as the Humboldt,which flows from the Antarctic along the Chilean and Peruvian coasts. Averagetemperatures here range between 18°C and 23°C. There is almost never anyrainfall, but dense cloud cover and fine mist are common between June andOctober. In the Andes, there are extremes of temperature between day andnight: in some highland areas it may drop from 34°C to below freezing in a fewhours. The rainy season in the Andes is from November to April. In the tropicalforest, a hot and humid tropical climate prevails: there are more than 200 daysof rain per year and average annual rainfall is over 250 cm.

Land use Peru is among the most ecologically diverse countries in the world. Soil use ishighly differentiated depending on the region. In parts of the coastal andAndean regions there are sophisticated irrigation works, some dating back tothe Inca period; in many steep Andean valleys Inca terraces are still in daily usefor agriculture. The tropical forests appear fertile, but the soils are fragile andintensive agriculture is difficult to sustain. The highlands have suffered severedeforestation, mostly because of small-scale wood-cutting. So far at least therehas been little mass exploitation of the timber resources of the Amazon rainforest.

Resources Peru has a wealth of largely unexploited mineral deposits, particularly copper,gold and zinc. Oil has been found in the Amazon and other eastern river basins,as well as offshore in the north. Huge natural gas deposits exist in the centraland southern selva, although exploitation has barely begun. The Peruvianstretch of the Pacific Ocean is one of the world’s richest fishing grounds. Abun-dant, fast-flowing rivers mean that potential for hydroelectric power generationis huge.

22 Peru: Natural resources and the environment

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

The environment Only in recent years have businesses and government started to concern them-selves with the environment. Legislation on environmental standards is beingimplemented, albeit slowly, in the mining and fishing sectors. However, partsof the Pacific coast still suffer from massive dumping of waste by fishmealplants, while mines dump tailings into nearby rivers. A Consejo Nacional delAmbiente (CONAM, national council for the environment) has been set upand every productive sector has its own particular regulations. Areas of respon-sibility are ill-defined and control mechanisms weak.

Economic infrastructure

When Alberto Fujimori took office as president in July 1990, Peru’s physicalinfrastructure was in an appalling state. There had been little new investmentfor a decade. Dwindling central government income in the late 1980s—as theeconomy contracted and tax revenue was eroded by hyperinflation—had beeninsufficient even for basic repair and maintenance. Terrorists regularly blew uproads, bridges and power installations. Telephone provision was among thelowest in the continent. Since then there has been a marked improvement. Aroadbuilding programme is under way, while new private investment is trans-forming airport facilities and telecommunications. Privatisation is expected toattract new investment for ports and railways.

Transport and communications

Roads The earliest loans granted by the multilateral organisations, once Peru hadregained its status of eligibility in late 1992, were for improvements to infra-structure. A first $400m credit from the Inter-American Development Bank(IDB), provided for the repair and resurfacing of the two main highways—thePan-American which runs the full 2,800-km length of the coast, and the centralhighway linking Lima to its agricultural and mining hinterland. In addition, aprogramme for the asphalting of some 10,000 km of roads to link the capitals ofall departments and provinces, at a total cost of $1bn, is under way. Another$400m is being spent on the repair of rural roads and the paving of 220 km ofstreets in run-down Andean towns. (For transport statistics see Reference table 10.)

Ports Peru has 21 ports, 11 of which are controlled by Empresa Nacional de Puertos(Enapu, the state ports authority). Deregulation has made them cheaper andmore efficient. Operating contracts for the state ports will be put out to tenderfrom 1998 onwards. Callao, Lima’s port, is by far the largest and most impor-tant at present, but Ilo in the south has a bright future. The 1992 free-tradeaccord with landlocked Bolivia made Ilo a free-trade and industrial zone which,it is hoped, will eventually handle a large percentage of Bolivian exports andimports. Ilo will also gain in importance as mining projects in the hinterlandcome on stream. However, so far little has been done to improve the port’sbasic infrastructure. A port modernisation programme is under way with thehelp of a $166m loan from Japan.

Peru: Transport and communications 23

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

Air Air transport is extremely important because of the country’s difficult terrain,and deregulation has encouraged a number of smaller operators to start upregular services to towns in the Andes and jungle inaccessible by road. Sched-uled services to major provincial cities have sharply increased in number andcompetition has resulted in improved time-keeping. There are over 50 airportsin Peru, the busiest being Lima’s Jorge Chávez, and Cuzco, Tacna, Arequipa andIquitos, all of which are classified as international. Airport services in Lima havebeen largely privatised and facilities much improved. Provincial airport servicesare to go in the same direction. The two main international airlines are Faucettand Aeroperú, both of which are privately owned. Other important domesticoperators are Americana, Expreso Aéreo, Aero Continente and Aero Cóndor.

Railways The Peruvian railway system, largely built by the British, is in a state of poorrepair. Commercially, the most important stretch of track runs eastward fromLima and transports large quantities of minerals from the mines in and aroundCerro de Pasco and La Oroya, the traditional mining heartland. EmpresaNacional de Ferrocarriles (Enafer, the railway company), state-owned and poorlyadministered, is scheduled to be handed over for concession to the private sectorbefore the year 2000. First to be transferred to the private sector is likely to theshort and profitable tourist train from Cuzco to Machu Picchu. The only stretchwhich is likely to remain in state hands is the line from Huancayo to Huancavelica,the only viable means of transport in the zone and heavily used by impover-ished peasant farmers. The transport and communications ministry views it as asocial service which would not survive unsubsidised.

Telecommunications At the beginning of 1994 Peru had almost the lowest level of telephone pene-tration in Latin America: under three lines per hundred inhabitants. In Febru-ary 1994, the government auctioned a 35% controlling shareholding in thetwo national telecommunications companies: the long-distance national andinternational state monopoly, Entel, and the telephone company for Lima,Compañía Peruana de Teléfonos (CPT). It was acquired by Telefónica Interna-cional (TISA), a subsidiary of Spain’s Telefónica, for over $2bn in what is to datePeru’s largest privatisation. Progress in telecommunications service has beendramatic since then. Telefónica del Perú will be expanding its services as fast asit can to take full advantage of its temporary monopoly, which expires inmid-1999. Telefónica’s strategic plan is to install 2.5m fixed lines by 2000 toachieve a density of 10%. The goal for the number of cellular customers is800,000 by that year. Plans also include the digitalisation of most lines by thetime Telefónica’s monopoly ends. Investment from 1998 to 2000 will total$1.5bn, bringing total investment since privatisation to some $7.5bn.

In December 1996 US-owned Bell South acquired 60% of the shares in thecellular telephone and cable television firm, Tele 2000, for $60m. In late 1996the telecommunications supervisory board, Ospital, ordered Telefónica to pro-vide cellular roaming rights in the provinces. The purchase will enable BellSouth to compete with Telefónica by the time the monopoly ends in 1999.

24 Peru: Transport and communications

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

Energy provision

Oil Peru is believed to have large, untapped energy potential in both gas and petro-leum. Oil output had risen in the late 1970s to peak at 71.4m barrels (204,000barrels/day, b/d) in 1980, but owing to decades of little investment by the stateand a lack of exploration by private companies, output had slumped to around118,500 b/d by 1997. Some 90% of output came from four companies: OccidentalPetroleum, Petrotech, Pluspetrol and Pérez Companc. Production is expected todecline further in 1998. Because of falling output and rising demand Peru is nolonger self-sufficient in oil. It still exports heavy crude (1996 exports earned$310m) but since 1987 has imported rising quantities of light crude. It has runan oil trade deficit since 1992.

Underinvestment in the oil industry was exacerbated by disputes in the late1980s between the government of Alan García and three foreign producers.Although Mr Fujimori made peace with foreign investors (which includedagreeing to pay $185m in compensation to the American Insurance Group forthe expropriation of oilfields originally operated by Belco of the US), newinvestment was slow to materialise at first. However, late in 1995 ChevronOverseas Petroleum, a subsidiary of the large US oil company, signed a majorexploration contract with Perupetro, the state contracting and promotion en-tity. Chevron made an aggressive bid for Block 52 in the Ucayali basin, border-ing the Camisea gas fields held by Shell. The 45% royalties offered by Chevronon future production were unprecedented in Peru and around double thenormal figure offered. Some 20 exploration and drilling contracts were signedin 1996.

The privatisation of the state oil company, Petroperú, was postponed because ofpolitical sensitivities in the run-up to the April 1995 general election, but beganin 1996. A consortium led by Spain’s state-owned firm, Repsol, acquired 60% ofthe shares in Petroperú’s La Pampilla refinery in June 1996, with a bid of $181m.Petroperú’s licensing agreement for Blocks 8 and 8X was transferred to a consor-tium led by Pluspetrol of Argentina, which bid $142m. Pérez Companc ofArgentina won the bidding for Block X on the northern coast, with an offer of£202m. Locally owned Grana y Montero and US-based Williams won the bid-ding in late 1997 for 30-year contracts to operate 15 oil storage terminals.

Gas After Shell’s 1987 discovery of the huge Camisea natural gas fields in thesouth-eastern jungle of Cuzco department, exploration companies widenedtheir interest in Peru’s hydrocarbon potential. The Camisea fields contain gasand condensates equivalent to 2.4bn barrels of oil, nearly seven times today’sproven reserves. A consortium of Shell (57.5%) and Mobil (42.5%) signed acontract with the Peruvian government in May 1996 to develop the deposits. Ifthe project is completed as scheduled, it will be the largest-ever private-sectorinvestment in Peru, involving about $2.8bn. In the first phase, four appraisalwells will be drilled, seismic and geological studies will be reworked and anenvironmental impact study will be prepared. The second phase—the con-struction of the trans-Andean pipeline, which would cost about $800m—willgo ahead only if sufficient demand for Camisea’s dry gas can be assured.

Peru: Energy provision 25

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1998

Electricity generation Despite the encouraging medium-term outlook for large discoveries of oil andgas, and the excellent prospects for Camisea, Peru is on the verge of an energycrisis in the short term. The present installed capacity is 4,420 mw, and some80% of output is hydroelectrically generated (see Reference table 11). Thismeans power supply is highly vulnerable to drought. When the warm Pacificcurrent known as El Niño made one of its periodic appearances in 1992, energysupply to industry was reduced by 30%. Official estimates are that capacitymust expand in the short term by 40% and thereafter by between 8.5% and10% per year to meet higher demand from mining and industry and to extendelectricity coverage to the 42% of the population still without power.