permian basin primer target energy limited

TRANSCRIPT

PERMIAN BASIN PRIMER TARGET ENERGY LIMITED MAY 2013

DISCLAIMER AND FORWARD-LOOKING STATEMENTS

2

This Presentation is provided on the basis that none of the Company nor its respective officers, shareholders, related bodies corporate, partners, affiliates, employees, representatives and advisers make any representation or warranty (express or implied) as to the accuracy, reliability, relevance or completeness of the material contained in the Presentation and nothing contained in the Presentation is, or may be relied upon as, a promise, representation or warranty, whether as to the past or the future. The Company hereby excludes all warranties that can be excluded by law. All persons should consider seeking appropriate professional advice in reviewing the Presentation and all other information with respect to the Company and evaluating the business, financial performance and operations of the Company. Neither the provision of the Presentation nor any information contained in the Presentation or subsequently communicated to any person in connection with the Presentation is, or should be taken as, constituting the giving of investment advice to any person.

Certain statements in this presentation contain ‘forward-looking statements’ including, without limitation to: expectations, beliefs, plans and objectives regarding production and exploration activities. Any matters that are not historical facts are forward-looking and accordingly, involve estimates, assumptions, risks and uncertainties and other factors discussed in our most recently lodged Annual Report our website, http://www.targetenergy.com.au, and in our other public documents and press releases. These forward-looking statements are based on Target Energy Limited’s (“Target”) current expectations, estimates and projections about the company, its industry, its management’s beliefs and certain assumptions made by management. No assurance can be given that such expectations, estimates or projections will prove to have been correct. A number of factors could cause actual results to differ materially from the projections, anticipated results or other expectations expressed in this presentation, including, Target’s ability to meet its production targets, successfully manage its capital expenditures and to complete, test and produce the wells and prospects identified in this presentation; to successfully plan, secure necessary government approvals, finance and to achieve its production and budget expectations on its projects.

Whenever possible, these ‘forward-looking statements’ are identified by words such as “expects,” “believes,” “anticipates,” “projects,” and similar phrases. Because such statements involve risks and uncertainties, Target’s actual results and performance may differ materially from the results expressed or implied by such forward-looking statements. Given these risks and uncertainties, you are cautioned not to place undue reliance on such forward-looking statements, which speak only as of the date hereof. Unless legally required, we assume no duty to update these statements as of any future date. However, you should review carefully reports and documents that Target lodges periodically with the Australian Securities Exchange. NOTE: In accordance with ASX Listing Rules, any hydrocarbon reserves and/or drilling update information in this report has been reviewed and signed off by Mr Laurence Roe, B Sc, Managing Director of Target Energy, who is a member of the Society of Exploration Geophysicists and has over 30 years experience in the sector. He consents to that information in the form and context in which it appears.

WHERE IS THE PERMIAN BASIN?

3

The West Texas Permian Basin is the largest hydrocarbon basin in the US, covering 52 counties and over 75,000 square miles.

Map of US Lower 48 States

Midland Basin (TEX)

Delaware Basin

Val Verde Basin

Permian Basin

Regional Map of Permian Basin 1

Source: Apache Energy Corporation

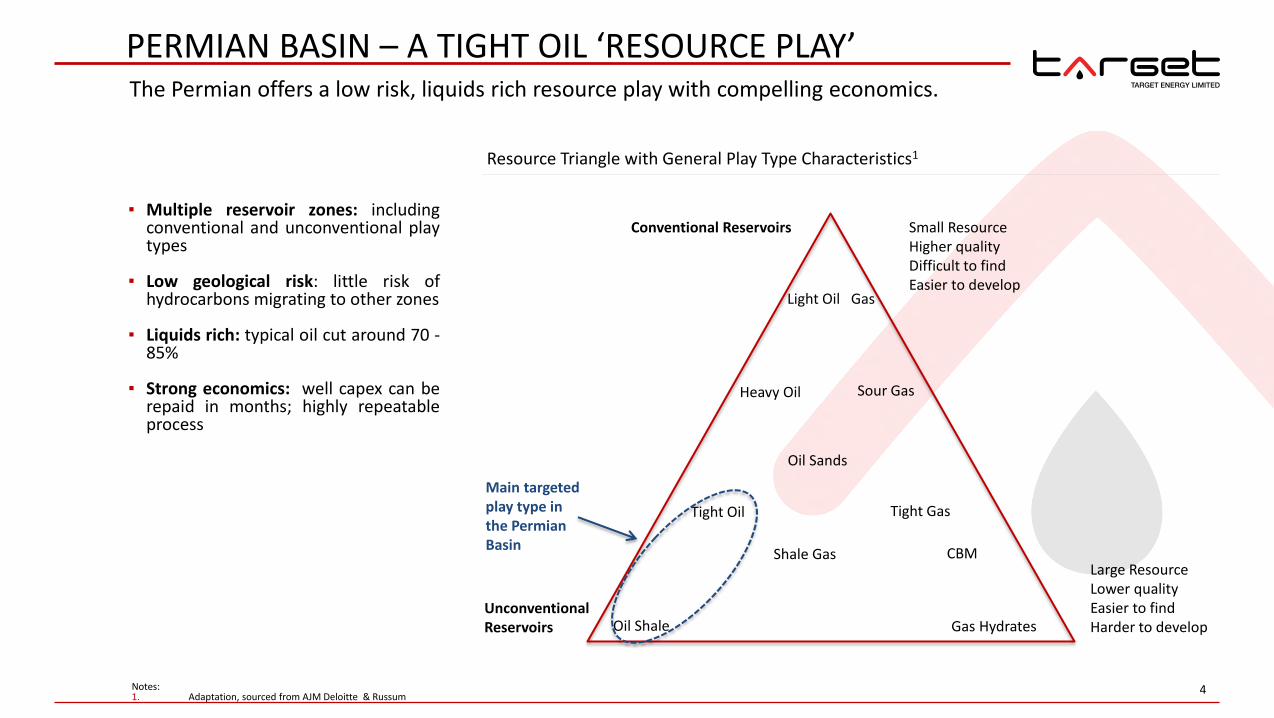

PERMIAN BASIN – A TIGHT OIL ‘RESOURCE PLAY’

4

The Permian offers a low risk, liquids rich resource play with compelling economics.

▪ Multiple reservoir zones: including conventional and unconventional play types

▪ Low geological risk: little risk of hydrocarbons migrating to other zones

▪ Liquids rich: typical oil cut around 70 - 85%

▪ Strong economics: well capex can be repaid in months; highly repeatable process

Conventional Reservoirs

Unconventional Reservoirs

Heavy Oil Sour Gas

Oil Sands

Tight Oil Tight Gas

Oil Shale

Shale Gas

Gas Hydrates

CBM

Resource Triangle with General Play Type Characteristics1

Main targeted play type in the Permian Basin

Small Resource Higher quality Difficult to find Easier to develop

Large Resource Lower quality Easier to find Harder to develop

Light Oil Gas

Notes: 1. Adaptation, sourced from AJM Deloitte & Russum

PERMIAN BASIN – ACTIVITY AND SUCCESS

5

Permian Basin oil production started in the 1920s, today the basin produces more than double Australia’s annual oil output.1

▪ Historic production: 29 billion barrels of oil and 75 trillion cubic feet of gas

▪ Current daily production: 1.3 million barrels of oil and 4 billion cubic feet of gas2

▪ Relative production: Permian Basin oil production is more than double Australia’s oil production and the gap is expected to widen1

▪ Production growth: oil production is expected to grow to 1.8

million barrels per day (1.8 mmbopd) by 20163

▪ Gas quality: gas produced is often liquids rich, attracting substantial premiums to the US ‘dry gas’ (methane) price

▪ Reserve growth: 29% of estimated US oil reserve growth in the US is expected to come from the Permian Basin 4

▪ Current activity: 397 drilling rigs are operating in the

Permian Basin, compared to Australia’s total rig count of 21 rigs6

Average Daily Oil Production - Australia vs. US Permian Basin1

Notes: 1. US EIA, HPDI, LLC, BP and APPEA - figures relate to 2011 production. 2. Bentek, University of Texas estimates 3. Bentek estimates 4. Hart Energy 5. North American Shale Quarterly 6. Baker Hughes rig count

0

200

400

600

800

1,000

1,200

2008 2009 2010 2011

mb

op

d

Australia Permian Basin

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

mb

oep

d

Oil and Condensate Natural Gas Liquids Gas

Permian Basin Tight Oil and Shale Oil Production Forecast5

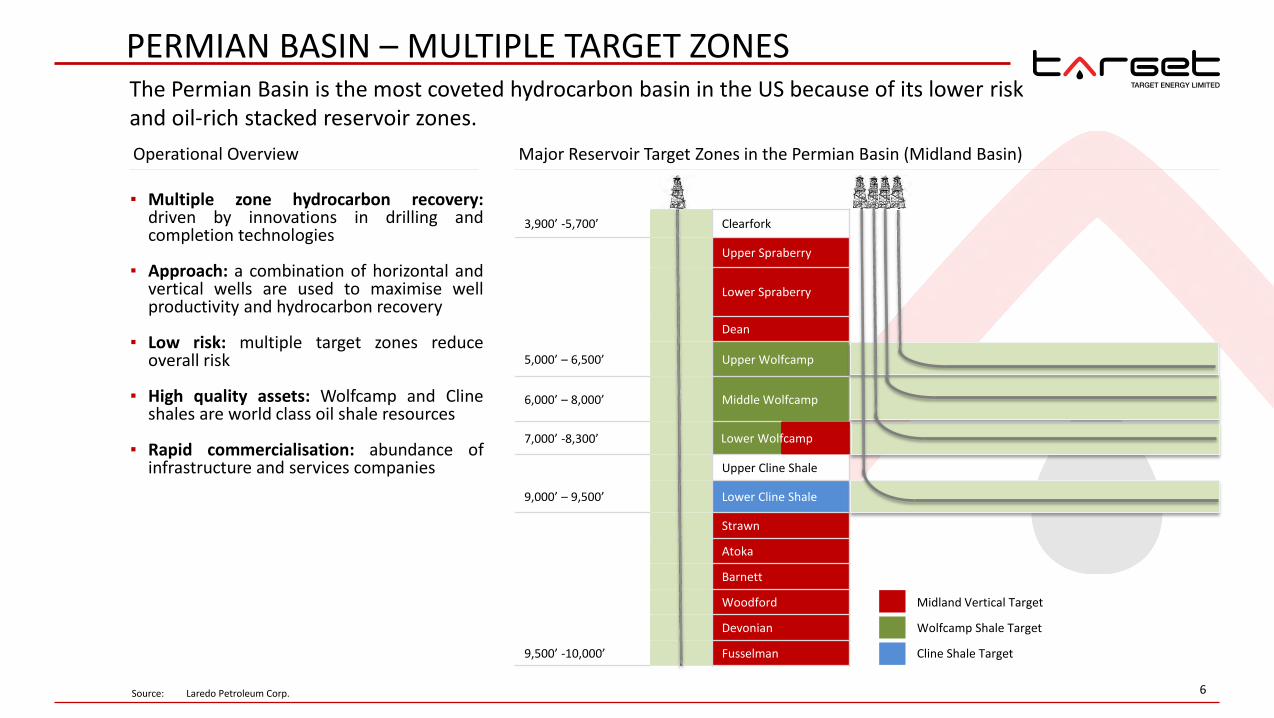

PERMIAN BASIN – MULTIPLE TARGET ZONES

6

The Permian Basin is the most coveted hydrocarbon basin in the US because of its lower risk and oil-rich stacked reservoir zones.

3,900’ -5,700’ Clearfork

Upper Spraberry

Lower Spraberry

Dean

5,000’ – 6,500’ Upper Wolfcamp

6,000’ – 8,000’ Middle Wolfcamp

7,000’ -8,300’

Upper Cline Shale

9,000’ – 9,500’ Lower Cline Shale

Strawn

Atoka

Barnett

Woodford

Devonian

9,500’ -10,000’ Fusselman

Lower Wolfcamp

Midland Vertical Target

Wolfcamp Shale Target

Cline Shale Target

Major Reservoir Target Zones in the Permian Basin (Midland Basin)

▪ Multiple zone hydrocarbon recovery: driven by innovations in drilling and completion technologies

▪ Approach: a combination of horizontal and

vertical wells are used to maximise well productivity and hydrocarbon recovery

▪ Low risk: multiple target zones reduce overall risk

▪ High quality assets: Wolfcamp and Cline shales are world class oil shale resources

▪ Rapid commercialisation: abundance of

infrastructure and services companies

Operational Overview

Source: Laredo Petroleum Corp.

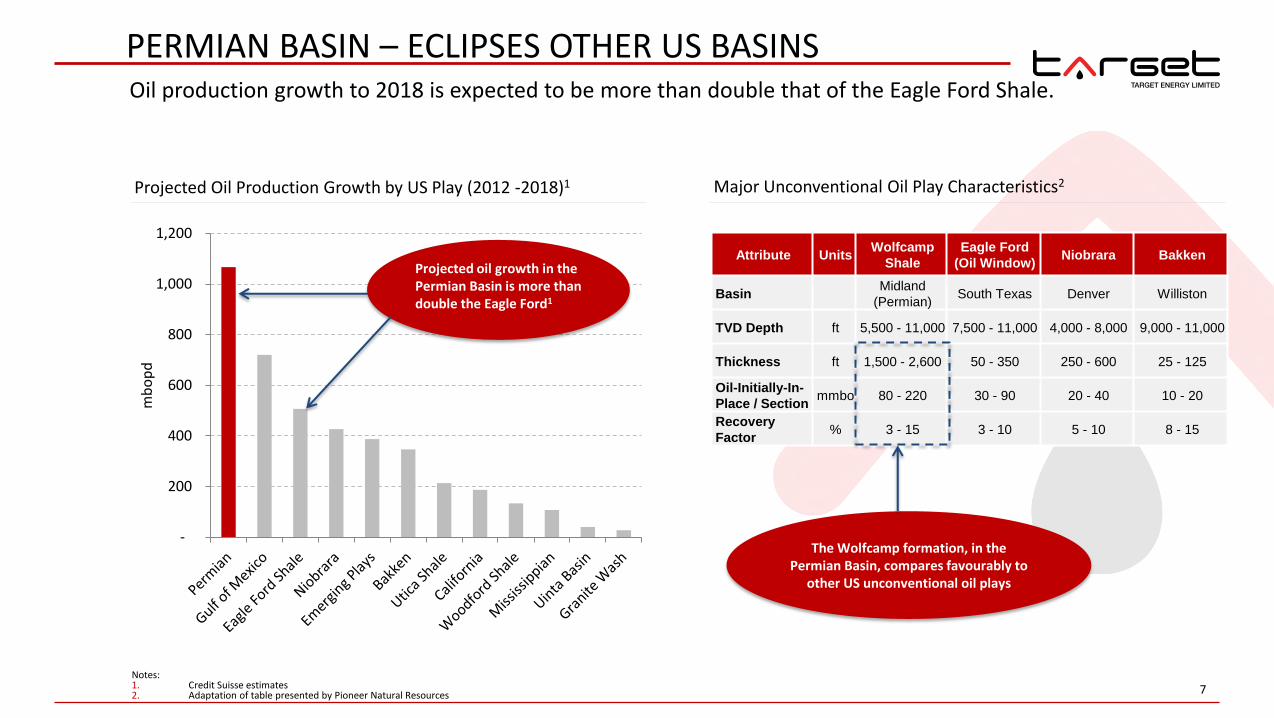

PERMIAN BASIN – ECLIPSES OTHER US BASINS

7 Notes: 1. Credit Suisse estimates 2. Adaptation of table presented by Pioneer Natural Resources

Oil production growth to 2018 is expected to be more than double that of the Eagle Ford Shale.

-

200

400

600

800

1,000

1,200

mb

op

d

Projected oil growth in the Permian Basin is more than double the Eagle Ford1

Projected Oil Production Growth by US Play (2012 -2018)1

Attribute Units Wolfcamp

Shale

Eagle Ford

(Oil Window) Niobrara Bakken

Basin Midland

(Permian) South Texas Denver Williston

TVD Depth ft 5,500 - 11,000 7,500 - 11,000 4,000 - 8,000 9,000 - 11,000

Thickness ft 1,500 - 2,600 50 - 350 250 - 600 25 - 125

Oil-Initially-In-

Place / Section mmbo 80 - 220 30 - 90 20 - 40 10 - 20

Recovery

Factor % 3 - 15 3 - 10 5 - 10 8 - 15

Major Unconventional Oil Play Characteristics2

The Wolfcamp formation, in the Permian Basin, compares favourably to

other US unconventional oil plays

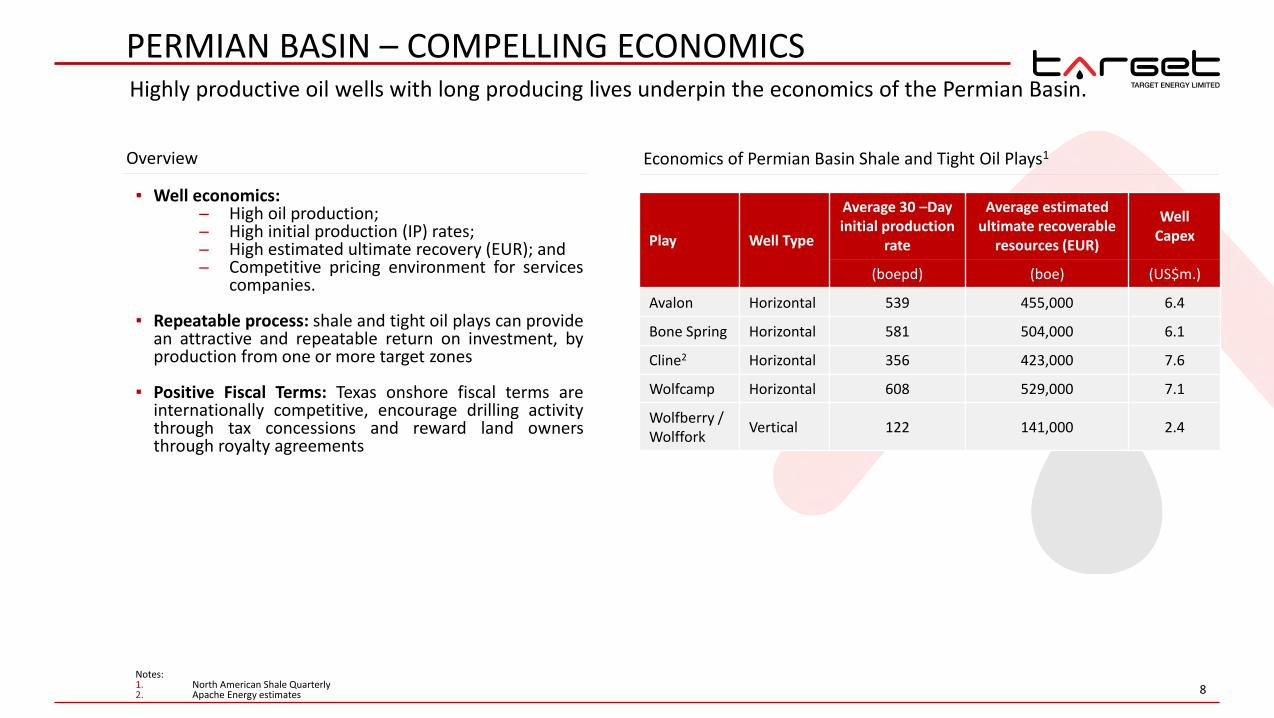

PERMIAN BASIN – COMPELLING ECONOMICS

8

Highly productive oil wells with long producing lives underpin the economics of the Permian Basin.

▪ Well economics: ─ High oil production; ─ High initial production (IP) rates; ─ High estimated ultimate recovery (EUR); and ─ Competitive pricing environment for services

companies.

▪ Repeatable process: shale and tight oil plays can provide an attractive and repeatable return on investment, by production from one or more target zones

▪ Positive Fiscal Terms: Texas onshore fiscal terms are internationally competitive, encourage drilling activity through tax concessions and reward land owners through royalty agreements

Play Well Type

Average 30 –Day initial production

rate

Average estimated ultimate recoverable

resources (EUR)

Well Capex

(boepd) (boe) (US$m.)

Avalon Horizontal 539 455,000 6.4

Bone Spring Horizontal 581 504,000 6.1

Cline2 Horizontal 356 423,000 7.6

Wolfcamp Horizontal 608 529,000 7.1

Wolfberry / Wolffork

Vertical 122 141,000 2.4

Economics of Permian Basin Shale and Tight Oil Plays1

Notes: 1. North American Shale Quarterly 2. Apache Energy estimates

Overview

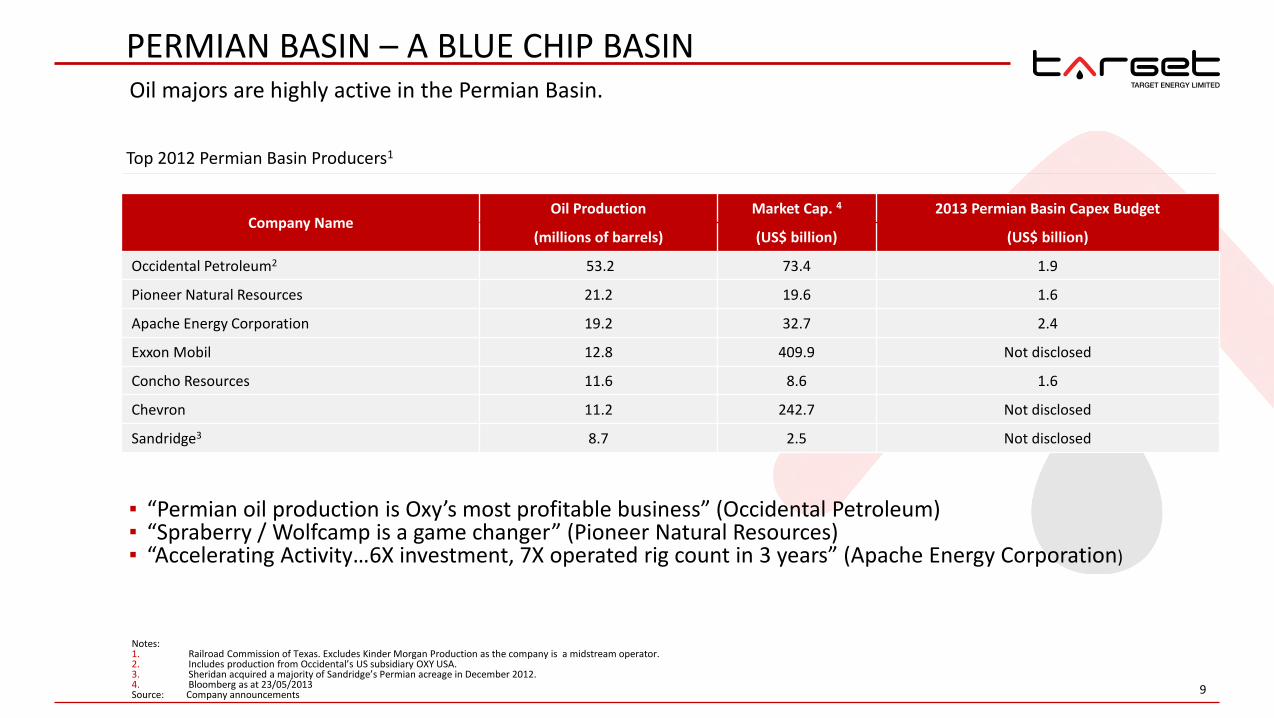

PERMIAN BASIN – A BLUE CHIP BASIN

9

Oil majors are highly active in the Permian Basin.

Notes: 1. Railroad Commission of Texas. Excludes Kinder Morgan Production as the company is a midstream operator. 2. Includes production from Occidental’s US subsidiary OXY USA. 3. Sheridan acquired a majority of Sandridge’s Permian acreage in December 2012. 4. Bloomberg as at 23/05/2013 Source: Company announcements

Company Name Oil Production Market Cap. 4 2013 Permian Basin Capex Budget

(millions of barrels) (US$ billion) (US$ billion)

Occidental Petroleum2 53.2 73.4 1.9

Pioneer Natural Resources 21.2 19.6 1.6

Apache Energy Corporation 19.2 32.7 2.4

Exxon Mobil 12.8 409.9 Not disclosed

Concho Resources 11.6 8.6 1.6

Chevron 11.2 242.7 Not disclosed

Sandridge3 8.7 2.5 Not disclosed

Top 2012 Permian Basin Producers1

▪ “Permian oil production is Oxy’s most profitable business” (Occidental Petroleum) ▪ “Spraberry / Wolfcamp is a game changer” (Pioneer Natural Resources) ▪ “Accelerating Activity…6X investment, 7X operated rig count in 3 years” (Apache Energy Corporation)

TARGET’S POSITION IN THE PERMIAN BASIN

10

Target is a Permian Basin focused company and is committed to building upon a high quality portfolio.

Gross Acres 3,492

Net Acres 2,095

Working Interest

60%

Net Production

320 boepd 1

Reserves Expected H2 2013

Planned 2013 Work Program

4 low-risk step out wells commencing August 2013

Ongoing petrophysical analysis

Comments Fairway Project is in the heart of the Midland Basin

Oil majors in adjacent acreage

Target’s relationships with the Midland community has afforded the company multiple bolt-on acreage opportunities

Notes: 1. Pre royalty interest to land owners

Howard Glasscock Field (1925)

1 mile

1.6 km

Howard County Glasscock County

Target acreage Target acquiring acreage Post 2009 Producer Proposed well location

Map of Target’s Fairway Project in the Midland Basin

BOA 12 #1

Darwin #1 & #2

Sydney #1

PERMIAN VALUATIONS - TRANSACTION COMPARABLES

11

The Permian M&A market is robust with valuations increasing for both producing and non-producing acreage as a result of drilling success and extensive basin activity.

-

50,000

100,000

150,000

200,000

250,000

US$

Transaction Enterprise Value (EV) / barrel of oil equivalent per day (boepd) 1

▪ Permian Basin valuations are rising generally but particularly in the Midland Basin with greater horizontal activity in the Wolfcamp and Cline shales

▪ The value of mergers and acquisitions (M&A) in the

Permian Basin in 2012 surpassed all other onshore basins.

▪ Permian Basin M&A outlook is strong as resource plays continue to be de-risked through extensive drilling

Median US$ 110,708 / boepd

Central Basin Platform Midland Basin

25%

14%

10% 10%

9%

7%

25%

Permian Basin Mid -Continent Bakken Gulf Coast Eagle Ford Utica Other

2012 US Onshore Mergers & Acquisitions 1

Notes: 1. RBC Richardson Barr. US onshore M&A includes transactions over US$100m. 2. Gulf Coast relates to Arkansas, Louisiana and other Texas plays. 3. Transaction values often include a premium for control.

2

Overview

DEFINED TERMS

12

DEFINED TERMS “$” or “US$” means United States (US) dollars, unless otherwise stated. “B” or “b” prefix means billion “bbl/s” means barrel/ s “bopd” or “boepd” means barrels of oil per day and barrels of oil equivalent per day, respectively “boe” means barrels of oil equivalent. Target reports boe using a gas to oil conversion based on equivalent thermal energy , i.e. 6000 cubic feet of gas = 1 barrel of oil “M” or “m” prefix means thousand “mcfgpd” means thousand cubic feet of gas per day “MM” or “mm” prefix means million “NGL” means natural gas liquids. “NRI” means net revenue interest (after deduction of royalties) “pd” or “/d” suffix means per day “PV10” or “NPV10” means, unless otherwise stated, the net present value of future net revenue, after deductions for operating and capital expenses, production

taxes and ad valorem taxes, but before corporate income tax and corporate overheads, using a real, pre-tax discount rate of 10%. “scf” means standard cubic feet “WI” means working interest within leases

13

TARGET ENERGY LIMITED AUSTRALIA 6 RICHARDSON STREET, SUITE 5 WEST PERTH, WA 6005 T: +61 8 9476 9000 | F: +61 8 9476 9099 USA 1900 ST JAMES PLACE, SUITE 425 HOUSTON, TEXAS 77056 T:+1 713 275 9800 | F: +1 713 275 0999