overview of real estate market in sri...

TRANSCRIPT

Savlanka’s newest property market research report examines the real estate landscape in Sri Lanka, with a focus on the hotel and leisure sector. Savlanka’s close relationship with Savills (the famous global real estate service provider) combined with its local expertise enables deep, accurate insights into the Sri Lankan property market.

In this report, Savlanka presents �ndings on the growth and development of the real estate market in Sri Lanka, highlighting key trends in the hotel and leisure sector and forecasting future demand and supply patterns. The report’s assessment of the market clearly shows the promising opportunities for tourism investment in Sri Lanka at the present time. The data and the analysis demonstrate that the time is ripe for investors to enter the market and take advantage of the skyrocketing growth in demand. Savlanka forecasts massive growth in the leisure property sector in Sri Lanka over the next few years, particularly in coastal areas - including hotels, resorts, and leisure facilities such as golf courses.

Download the entire market research report from the Savlanka website now! Get a bird’s eye view of the hotel and leisure segment of the real estate market in Sri Lanka and familiarise yourself with key property trends, growth statistics, demand and supply patterns and data-backed forecasts for the market.

OVERVIEW OF REAL ESTATE MARKET IN SRI LANKA Hotel and Leisure Sector November 2012

www.savlanka.com

www.savlanka.comwww.savlanka.com

WHY invest in Sri Lanka

Sri Lanka continues to experience strong economic growth, driven by large-scale reconstruction and development projects following the end of the 26-year con�ict with the LTTE. Economic activity rebounded strongly with an IMF agreement, resulting in two straight years of high growth in 2010 and 2011. Per capita income is among the highest in the region.

Total foreign ownership

permitted across almost all areas of economy

Strategic location next to Indian

sub-continent and proximity to Southeast Asia and

Middle East

No restrictions on repatriation of

earnings, fees and capital

Safety of foreign investment

guaranteed by the constitution

Tax Holidays to promote private

foreign investments

Ranked 5th in �nancial attractivness

ahead of India, China,Central and East Europe

Among the 10 fastest

growing economies in the next 40 years

projected by Citi Bank

The 2nd fastest growing economy in South East Asia

in 2011

GDP growth 8%Two succesive years

2010 - 2011

Area: 65,610 sq km

Coastline: 1,340 km

Climate: Tropical monsoon

Population: 21,481,334

Median age: 30.8 years

Literacy: 90.7%

Government: Republic

Capital: Colombo

Ranked as the most liberalized

economy in South Asia

www.savlanka.com

INTRODUCTION

Sri Lanka is at the crossroads of a sea-change, jumping from tradition to modernity, from a conservative outlook to a bold con�dence in the future. The de�nitive end to the war has brought with it the economic bene�ts of peace. Sri Lanka was the second-fastest growing economy in emerging Asia during 2011 – second only to China. The government is investing heavily in infrastructure and harnessing the country’s key strengths like high literacy and its strategic position along shipping routes. This is creating nationwide bene�ts like foreign investment and tourism revenue.

In the Global Competitive Index of 2011-2012 Sri Lanka is ranked 52nd out of a total sample of 142 countries advancing 10 places within the year. Also in 2010, Sri Lanka ranked 62nd after moving up 27 places.

The World Bank’s Ease of Doing Business Review 2012 ranked Sri Lanka 89th globally. The country rose 9 places in only a year, making it one of the fastest-improving countries in the world. It comes 32 places higher than the regional average, 43 places higher than India and it fared better than all of the BRICs. In the “protecting investors” sub-category, Sri Lanka is ranked as high as 46th.

In this ebullient environment, the real estate market is growing fast. Improved communication and connectivity are making an array of spectacular locations accessible. From amazing beaches, coral reefs and wildlife parks, to historical sites and bustling cities. Sri Lanka holds a diversity that will keep international tourists coming in ever-increasing numbers for years.

Global hospitality players are set to capitalise on this enormous potential: existing hotels like Hilton and Taj are upgrading their products to international luxury standards, while Shangri-La, Hyatt and the Starwood Group have also entered the market. Despite this, accommodation will continue to be in short supply, creating an opportunity to build new hotels.

The residential and rental market for high-end condominiums looks very positive. There is a surge in demand from foreigners as well as expatriates. Compared with neighbours, property prices in Sri Lanka are still low, making it even more attractive.

With a new airport and seaport soon to be operational in Hambantota, Sri Lanka is poised to become a major shipping hub. With only a few purpose-built o�ce buildings in the entire country, the �eld is wide open for developers and investors to create quality commercial spaces.

In the words of Ruchir Sharma, head of emerging markets at Morgan Stanley; “Sri Lanka’s time has come… it is no longer a land in waiting”.

1

Area: 65,610 sq km

Coastline: 1,340 km

Climate: Tropical monsoon

Population: 21,481,334

Median age: 30.8 years

Literacy: 90.7%

Government: Republic

Capital: Colombo

www.savlanka.com

LEISURE SECTOR: TURN-AROUND IN FORTUNES

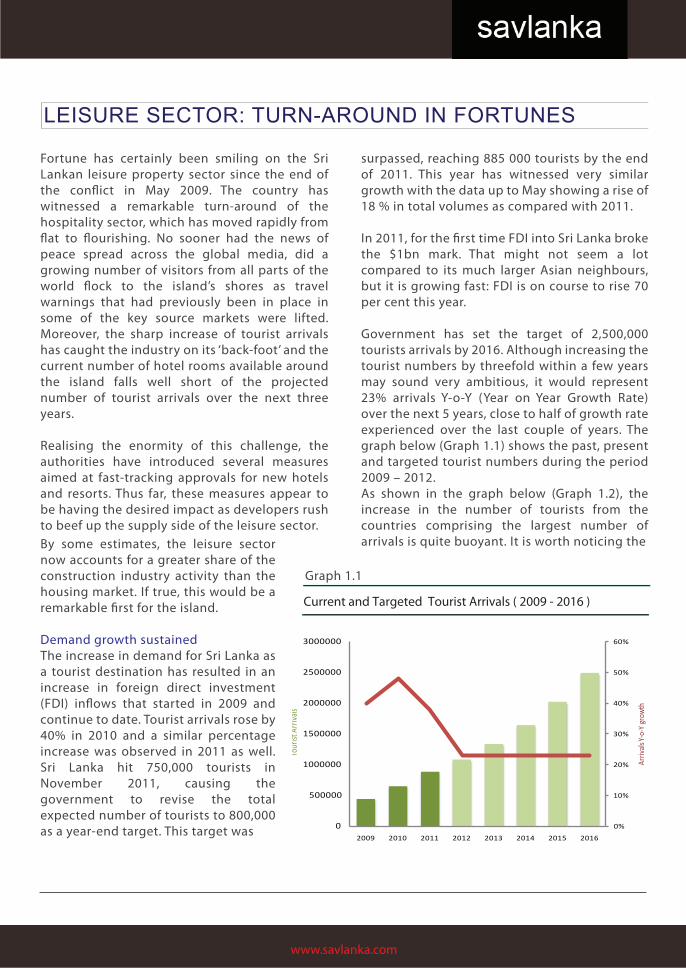

Fortune has certainly been smiling on the Sri Lankan leisure property sector since the end of the con�ict in May 2009. The country has witnessed a remarkable turn-around of the hospitality sector, which has moved rapidly from �at to �ourishing. No sooner had the news of peace spread across the global media, did a growing number of visitors from all parts of the world �ock to the island’s shores as travel warnings that had previously been in place in some of the key source markets were lifted. Moreover, the sharp increase of tourist arrivals has caught the industry on its ‘back-foot’ and the current number of hotel rooms available around the island falls well short of the projected number of tourist arrivals over the next three years. Realising the enormity of this challenge, the authorities have introduced several measures aimed at fast-tracking approvals for new hotels and resorts. Thus far, these measures appear to be having the desired impact as developers rush to beef up the supply side of the leisure sector. By some estimates, the leisure sector now accounts for a greater share of the construction industry activity than the housing market. If true, this would be a remarkable �rst for the island.

Demand growth sustainedThe increase in demand for Sri Lanka as a tourist destination has resulted in an increase in foreign direct investment (FDI) in�ows that started in 2009 and continue to date. Tourist arrivals rose by 40% in 2010 and a similar percentage increase was observed in 2011 as well. Sri Lanka hit 750,000 tourists in November 2011, causing the government to revise the total expected number of tourists to 800,000 as a year-end target. This target was

Current and Targeted Tourist Arrivals ( 2009 - 2016 )

2

0%

10%

20%

30%

40%

50%

60%

0

500000

1000000

1500000

2000000

2500000

3000000

2009 2010 2011 2012 2013 2014 2015 2016

Arriv

als Y-

o-Y

grow

th

Tour

ist A

rriva

ls

surpassed, reaching 885 000 tourists by the end of 2011. This year has witnessed very similar growth with the data up to May showing a rise of 18 % in total volumes as compared with 2011.

In 2011, for the �rst time FDI into Sri Lanka broke the $1bn mark. That might not seem a lot compared to its much larger Asian neighbours, but it is growing fast: FDI is on course to rise 70 per cent this year.

Government has set the target of 2,500,000 tourists arrivals by 2016. Although increasing the tourist numbers by threefold within a few years may sound very ambitious, it would represent 23% arrivals Y-o-Y (Year on Year Growth Rate) over the next 5 years, close to half of growth rate experienced over the last couple of years. The graph below (Graph 1.1) shows the past, present and targeted tourist numbers during the period 2009 – 2012.As shown in the graph below (Graph 1.2), the increase in the number of tourists from the countries comprising the largest number of arrivals is quite buoyant. It is worth noticing the

Graph 1.1

www.savlanka.com

sharp increase of visitors from India. India’s potential to become a source market for Sri Lanka is evident, yet, Sri Lankan capture of Indian outbound market (currently at about 13 m tourists) is only 1.4%. If this is to increase to 4%, the number of tourist arrivals from India will exceed half a million. These �gures should not be hard to achieve, bearing in mind India’s size, proximity and cultural a�nity.

Supply-side scramble Currently, the total number of hotel, guest house and villa rooms across the island can be estimated at around 22,000, though it is thought to be closer to 15,000. Due to the sharp increase in tourist numbers in the last few years the average occupancy rates reached over 75%. Table 1.1 shows the number of rooms by category and the occupancy rates.

In order to reach the government’s target of 2.5 million guests by 2016, the total number of rooms to accommodate the number is calculated to be over 50,000 (see table 1.2 ). This will �ll the capacity gap of 29,000 that Sri Lanka will experience, especially during peak tourist seasons.

Table 1.1Hotel grade No. of rooms % of total Ocup. rates 2011 Ocup. rates 2010 Increase Y-o-Y5 star 3202 22% 78.7% 76.8% 1.9%4 star 1775 12.2% 78.1% 74.7% 3.4%3 star 1164 8% 74.6% 68.1% 6.5%2 star 2008 13.8% 76.8% 67.7% 9.1%1 star 1164 8% 77.9% 66.5% 11.4%Total 14653 77.1% 70.2% 6.9%

Unclassified 6141 76.8% 67.7% 9.1%

Others 1000 est.

Total No. rooms 21794 Total No. of Establishmants 906

0 50000 100000 150000 200000

IndiaU.K

GermanyFrance

AustrailiaNetherlands

MaldivesRussiaU.S.A

Tourist Arrivals by Country of Residence

Total Arrivals 2011

Total Arrivals 2010

Total Arrivals 2009

Graph 1.2

www.savlanka.com

Up until January 2012 the Tourist Board received 189 project proposals. From the projects that were approved, 33 projects are going through the environmental assessment process and the rest have already started moving. The total number of rooms for which approval has been granted stands at 7,900.

Colombo, Galle, Kalutara, Trincomalee and Puttalam are the top �ve cities that are set for leisure sector expansion in terms of room numbers. The arrangement of rooms across the

island today focuses on these major cities and tourist destination points. However, by 2016, although the major concentration of hotel rooms will still be in the Western and Southern provinces, a signi�cant shift will take place with regards to the spread of hotel room development across the island. Areas North of Colombo on the West coast will see their hotel rooms expand from just over 2,000 rooms currently, to over 7,000 rooms from 2016 to 2020. In addition, the Central province, which is known for its tea estates, hill country and Sri Lanka’s Cultural Triangle, will experience a rejuvenation of hotel room volumes, with concentrations in the city of Kandy. Towns like Habarana, Anuradhapura and Polonnaruwa are also set to witness a similar boost in capacity. Graph 1.3 shows regional distribution of graded rooms; existing and in the pipeline.

Despite all the activities taking place in the sector, building nearly 30,000 rooms within �ve years is a colossal task. For most of the new room applications being processed, construction is unlikely to have started. Also considering time needed to complete a hotel project, the average yearly supply of new rooms on the market will struggle to reach 6,000 – the number of rooms required to accommodate 2.5 million guests by

Table 1.2

CALCULATION FOR NUMBER OF ROOMS TO BUILT

T = number of Tourist arrivals 2500000P = Percentage staying in hotels 0.95N= Average No. of guests per room 1.7O= Average hotel occupancy 0.75S= Number of days in business 365L= Average nights of stay 10

R=Number of rooms required

R= T x P x L \ S x N x O = 51034

Existing number of rooms 21794

Number of rooms to built by 2016 29240

5800

5100

200

36003800

9001200 1100

West Coast South Coast East Coast Other Areas

Existing room capacity

Pipeline room capacity

Regional distribution of graded roomsGraph 1.3

Area: 65,610 sq km

Coastline: 1,340 km

Climate: Tropical monsoon

Population: 21,481,334

Median age: 30.8 years

Literacy: 90.7%

Government: Republic

Capital: Colombo

www.savlanka.com

2016. Graph 1.4 maps out a potential supply gap that will appear if the average yearly in�ow of new rooms is 4,000 (an optimistic �gure of new rooms coming to the market considering current activities). The estimated gap of 9,000 rooms at the end of 2016 could only be �lled by a surge of new foreign investment in the Hotel and Leisure sector.

Incentives for investors The beach-front properties market across the island is booming and the land prices are moving quickly on an upward trend. Sri Lanka has recently atracted a new number of international hotel chains including Shangri-La, Sheraton, Ra�es, Hyatt Regency, Doubletre, etc. In Colombo city, the sale of land to Shangri-La hotel chain in 2011 for US$125 million registered the single largest contribution to foreign direct investment in 2011.

Shangri-La also purchased a property in Hambantota for a smaller 300-room villa , compared to the 500 rooms for its Colombo property. The US-based Sheraton hotel group has also con�rmed a US$300 million dollar investment into the country. Domestic property developers and construction �rms have also moved into the leisure sector, investing in Colombo city hotels, shopping districts designed speci�cally for tourists and boutique hotels across the island. Table 1.3 lists projects in the pipeline that are developed and / or operated by international brands.

5

Graph 1.4

New rooms supply and forecast gap by 2016

0

500000

1000000

1500000

2000000

2500000

3000000

0

10000

20000

30000

40000

50000

60000

2010 2011 2012 2013 2014 2015 2016G

uest

s ar

rival

s

Num

ber o

f roo

ms

Estimated Supply Gap

Projected tourist numbers Number of rooms required Estimated supply

Area: 65,610 sq km

Coastline: 1,340 km

Climate: Tropical monsoon

Population: 21,481,334

Median age: 30.8 years

Literacy: 90.7%

Government: Republic

Capital: Colombo

www.savlanka.com

DISCLAIMER: In accordance with our normal practice, we would state that this document and information it contains is for general informative purposes only and does not constitute a formal valuation, appraisal or recommendation. It is only for the use of the persons to whom it is addressed and no responsibility can be accepted to any third party for the whole or any part of its contents. It may not be published, reproduced or quoted in part or in whole, nor may it be used as a basis for any contract, prospectus, agreement or other document without prior consent, which will not be unreasonably withheld.

Whilst every e�ort has been made to ensure that the data contained in it is correct, no responsibility can be taken for omissions or erroneous data provided by a third party or due to information being unavailable or inaccessible during the research period. The estimates and conclusions contained in this report have been conscientiously prepared in the light of our experience in the property market and information that we were able to collect, but their accuracy is in no way guaranteed.

Outlook – sustained momentumIn the current climate of increasing tourist arrivals and the government drive to increase the number of hotels and rooms, we can note that the leisure sector is actually the driving force behind the boom in the construction sector of the island. Both policy makers and the business community have realised that any severe shortage in room availability will result in a price hike that will ultimately damage Sri Lanka’s chances of regaining its former glory as one of Asia’s leading lights.

The newly set-up ‘One Stop Shop’ at the Tourist Board has an extended mandate to fast-track investments over US$5 million in the leisure sector and dozens of investors have got their project approvals each month. Moreover, such measures, packaged with tax-holidays and unrestricted pro�t repatriation, serve to send a clear message to international investors than Sri Lanka means to do business and o�ers a competitive proposition.

Table 1.3

Developer / Operator Location Number of Keys Value in $ mil Completion yearITC- Sheraton Colombo 650 425 2015Shangri-Laa Hambatota 300 45 2014Shangri-Laa Colombo 600 500 2015Minor Hotel Group Bentota 75 50 2012Minor Hotel Group Kalutara 105 2012Marriott International Waligama 200 2014Six Senses Ahungalla 54 20 2013

www.savlanka.com

ABOUT US

We provide international quality real estate services to the Sri Lankan real estate industry. Underpinning this is our powerful entrepreneurial value-embracing ethos. Our objective is to develop long-term client relationships by providing professional

services and adding value through our local knowledge, global reach and brand strength.

Market research and valuations

Feasibility, viability and other studies

Marketing and sales

Development, project and design management

Facilitating development process

Professional and advisory services

Finance and investment structuring

Facility management

Savlanka is Sri Lanka's �rst real estate consultancy o�ce providing international standard service, with global reach through Savills network of o�ces. It was founded by a group of real estate professionals who collectively have extensive knowledge of the International and Sri Lankan property markets and have a wide range of experience across all sectors of the real estate industry.

Internationally the founders of Savlanka undertook investments, design, project and development management, and construction of luxury residential units ranging from £1M to £35M in London's prime areas of Belgravia, Mayfair, Knightsbridge and Chelsea. In Europe they managed prime residential, commercial, hotel and resort developments ranging in value from €100M to €300M on behalf of international investors and developers such as Merrill Lynch, Investment Dar, Latsis Group of Companies, etc. They have strong working relationships with some of the World’s leading architects, engineers and consultants such as Zaha Hadid Architects, WATG, YOO, ARUP, AECOM, G&T, HVS and many others.

In Sri Lanka they act on behalf of institutional investors and developers, both local and international. They have successfully worked on some of the largest transactions in post war Sri Lanka and have the most extensive database of private and institutional investors. Their in depth understanding of what constitutes an informal market, strong working relationships with leading consultants, professionals and relevant government authorities and their understanding of the regulatory framework, is key to insuring the success of projects.

Savlanka is uniquely placed on the Sri Lankan real estate market o�ering a wide range of bespoke services utilising its local knowledge and expertise, international experience and global reach.

Savills was established in the UK in 1855, and has grown to have over 23,000 employees across a network of more than 200 international o�ces and associates throughout the Americas, the UK, continental Europe, Asia Paci�c, Africa and the Middle East. Savills is one of the largest real-estate service providers in the World and it is listed on the London Stock Exchange.

Savills o�ers a broad range of specialist advisory, management and transactional services to clients all over the world including governments, corporations and individual clients.

CONTACT US

Savlanka (Pvt) Ltd.304 Union Place

Colombo 3. Sri Lanka

Tel: +94 11 745 745 0Fax: + 94 11 745 745 1

E-mail: [email protected]

www.savlanka.com