cru mineral commodity outlook 2020 vision trench.pdfcommodity price ‘climate change’: zinc to...

TRANSCRIPT

CRU Mineral Commodity Outlook – 2020 Vision

Dr Allan Trench

What is driving commodity prices?

• ...that depends on which commodity you are looking at

• Each has it’s own dynamics

• CRU looks at the fundamentals: Supply of raw materials, production capacity, industry demand, stocks & the market balance, costs of production & investment capital and financial market influence, as well as prices

• Each commodity has a story & individual fundamentals

• China’s growth in consumption is common to all and this has been a factor in driving prices higher

3

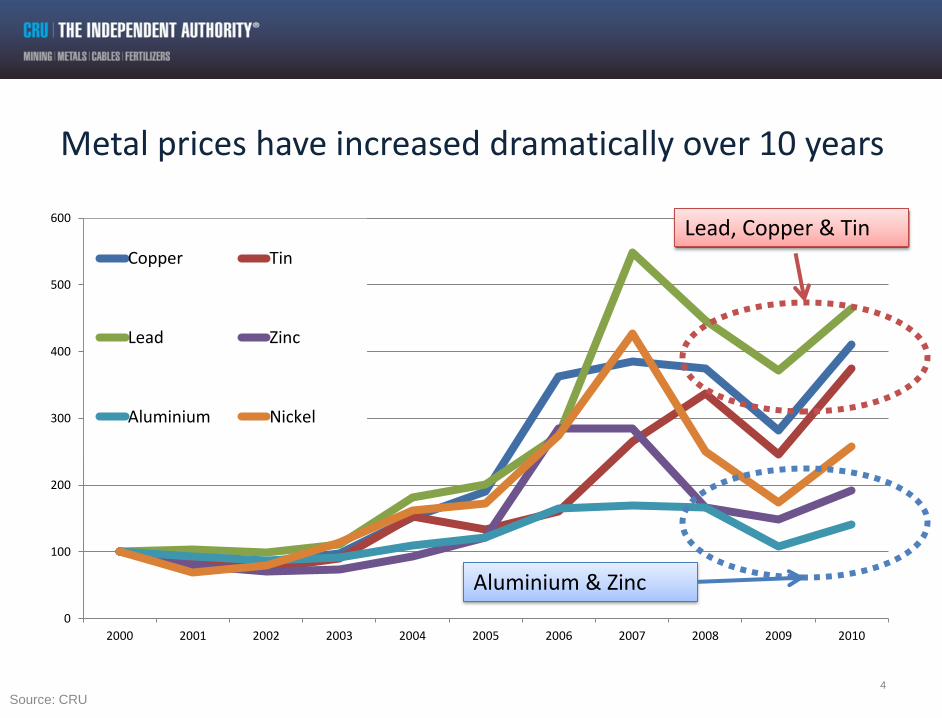

Metal prices have increased dramatically over 10 years

4

0

100

200

300

400

500

600

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Copper Tin

Lead Zinc

Aluminium Nickel

Lead, Copper & Tin

Aluminium & Zinc

Source: CRU

Here’s on reason why: China has accounted for more than 100% of global metals demand growth this millennium

0%

20%

40%

60%

80%

100%

120%

140%

160%

Copper Nickel Lead Zinc Steel Aluminium

Chinese metals consumption growth as a proportion of global metals consumption growth 2000-2010

Data: CRU Analysis

Average growth as proportion

of total global growth =118%

China’s share of metal consumption

At the turn of the last millennium China accounted for around10% metal consumption

Today China’s share of world consumption is over 40%

The industry size and structure has changed in the last decade; and continues to be shaped by China’s growth

There are industry constraints to be managed...

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Copper World Ex-China Lead World Ex-China Zinc World Ex-China

Nickel World Ex-China Aluminium World Ex-China Copper China

Lead China Zinc China Nickel China

Aluminium ChinaSource: CRU

• Looking at consumption growth of industrial metals China is driving demand growth

• The World Ex-China is cyclical but stable

China’s development has compensated for lower metal growth elsewhere

Source: CRU

Metal Consumption

Copper Zinc Lead Aluminium Tin Nickel

yoy 10/09 8.5% 15.8% 7.9% 19.5% 15.0% 15.9%

yoy 11/10 3.5% 4.4% 5.3% 8.8% 5.8%

CAGR 00-10 2.1% 2.9% 3.6% 5.1% 2.4% 2.7%

CAGR 10-15 4.7% 5.0% 4.5% 7.6% 5.7%

8

China is reliant on imports across a range of major commodities

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Aluminium Alumina Bauxite Fe Ore Copper Nickel

Net imports/Demand

Source: CRU

But importantly China is self-sufficient in Aluminium & Steel

9

0

50

100

150

200

250

300

350

400

450

0

100

200

300

400

500

600

700

800

0

50

100

150

200

250

300

350

400

0

100

200

300

400

500

600

700

800

900

1000

0

100

200

300

400

500

600

700

800

0

100

200

300

400

500

600

700

800

900

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Copper Lead Zinc

Nickel Aluminium Steel

Indexed Price Production Consumption Source: CRU

Business costs & 2010 average metal price ...at these prices just about every miner is making money

10

-500

500

1500

2500

3500

4500

5500

6500

7500

0 5000 10000 15000 0

5000

10000

15000

20000

25000

0 200 400 600 800 1000 1200

0

500

1000

1500

2000

2500

3000

0 500 1000 1500 2000 2500

0

500

1000

1500

2000

2500

0 1000 2000 3000 4000 5000 6000

Zinc US$/t

0

500

1000

1500

2000

2500

3000

0 10000 20000 30000 40000 50000

0

50

100

150

200

250

300

350

400

0 20000 40000 60000 80000 100000

Alumina US$/t

Copper US$/t Nickel US$/t Aluminium US$/t

Lead US$/t

Business costs $/t 2005 v 2010 Changes in the shape of the cost curve over time reflect changes in industry structure

11

0

500

1000

1500

2000

2500

3000

0 10000 20000 30000 40000

0

5000

10000

15000

20000

25000

0 200 400 600 800 1000

0

1000

2000

3000

4000

5000

6000

7000

0 2000 4000 6000 8000 10000 12000 140000

500

1000

1500

2000

2500

3000

0 500 1000 1500 2000

Costs $/t 2005 Costs $/t 2010 Linear Costs

Aluminium US$/t

Copper US$/t

Nickel US$/t

Lead US$/t

Supply-side Challenges to buoy Long-Term prices

• Influences vary from commodity to commodity

• Mining houses can’t do ‘everything’ simultaneously – adding to the challenge

• Room for smaller scale commodity-specific producers to add to contestable supply - Examples

– Copper

– Nickel

– Iron Ore

– Coking Coal

– Zinc

12

8

12

16

20

24

28

32

2000 2003 2006 2009 2012 2015 2018 2021 2024 2027 2030 2033

We need more mines to meet consumption growth...

Copper Example

13

Probable projects Possible projects

World copper mine production, 2000-2035

Existing mines

Firm projects

New

technology

Incremental

Discoveries

Prospects

Extra potential

supply requirement

= 13.1Mt

Production needed

2.67% per year

(2010 -2035)

(Mt co

nta

ine

d C

u in

co

nce

ntr

ate

s a

nd

SX

EW

ca

tho

de)

Source: CRU

Escondida Collahuasi

Los Pelambres

0

200

400

600

800

1000

1200

1988 1992 1996 2000 2004 2008 2012 2016 2020

Oyu Tolgoi

Tenke Fungurume

Toromocho

Mining start-up

gap of approx

10 years

Pro

du

ctio

n (

„00

0 t c

on

tain

ed

Cu

)

Significant volumes from

relatively “new” locations:

Mongolia, Pakistan, Alaska

After Escondida,

insufficient influx of

new supply

Source: CRU

Expected Year of production start-up

Miners are responding but it takes time ...on average it take 10 years to bring a project on stream

14

Mainly small-sized sulphide mines

starting up over this 10-year period

Pro

du

ctio

n (

„00

0 t c

on

tain

ed

Ni)

Many large-sized

projects scheduled to

start-up at the same

time

Two medium sized

operations start-up

Expected year of production start-up

Threat of several large-scale nickel projects...

15

New conventional* nickel operations and their start-up dates, ‘000

tonnes, 1995-2015

*Excluding mines in the Philippines and Indonesia that supply the Chinese nickel pig iron sector.

Voisey’s Bay

Raglan

Murrin Murrin

Talvivaara

Koniambo

VNC

Onca-

Puma

Barro

Alto

Data: CRU Analysis

Ravensthorpe

Ambatovy

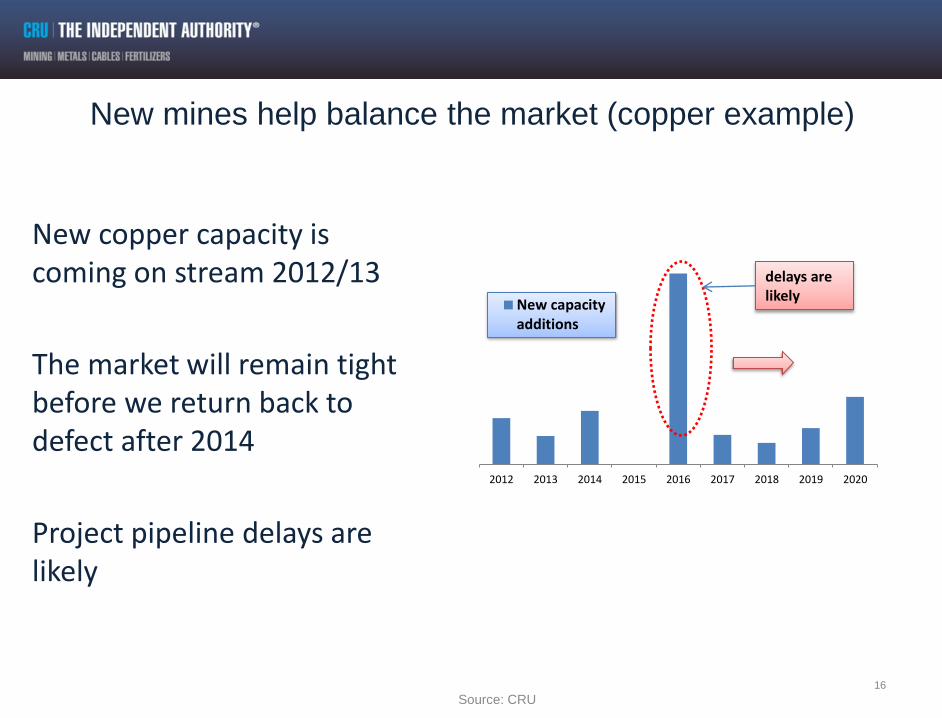

New copper capacity is coming on stream 2012/13

The market will remain tight before we return back to defect after 2014

Project pipeline delays are likely

16

2012 2013 2014 2015 2016 2017 2018 2019 2020

New capacityadditions

delays are likely

Source: CRU

New mines help balance the market (copper example)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2004 2005 2006 2007 2008 2009 2010 2011

Cu Mining, Refining and Smelting…

CRU estimates real

development cost inflation of

13% pa over this time period

US

$/t

on

ne

(2

011

$)

Copper development costs have increased

substantially...

17 Source: CRU

Projects compete for capital

18

Source: BHP Billiton Half Year Results Presentation – 16th Feb 2011

Iron Ore – A great business to be in........ Global business cost curve for iron ore fines, (UScents/dmtu)

...demand firmly at the high end of a steep cost curve –

providing strong pricing support & strong margins

Data: CRU iron ore cost model

cents/

dmtu

M tonnes

Iron ore Demand: The original China story – and still running Iron ore steel construction, transport, infrastructure....

-

500

1,000

1,500

2,000

2,500

Mill

ion

to

nn

es

Rest of World China

Chinese percentage of global steel production rising

Data: CRU Analysis

2

1

With China tracking towards more than 1 billion tonnes steel demand by 2020

0 100 200 300 400 500 600 700 800 900 1000 1100

GuizhouGansu

YunnanTibet

NingxiaQinghaiXinjiangHainanShanxiAnhui

GuangxiJiangxi

SichuanShaanxi

HunanChongqing

HubeiHebei

Inner MongoliaHeilongjiang

JilinFujian

LiaoningShandong

Inner MongoliaGuangdong

ZhejiangJiangsuBeijingTianjin

Shanghai

Per capita crude steel equivalent consumption kg/head

Regional

Kg/head 2009

610

341

258

Coastal

Central

Western

National average

2009 = 450kg/head

Source: CRU China

1000

700

600

Coastal

Central

Western

Regional

Kg/head 2020 National average

2020 = 794kg/head

39% POPULATION

39% POPULATION

22% POPULATION

But is future steel demand-growth simply about Asia? % of global growth in crude steel production 2007-2021

-20%

0%

20%

40%

60%

80%

100%

WesternEurope

Other Europe& CIS

North America South America Africa Asia Oceania

YES!

>95%

Data: CRU Analysis

0

200

400

600

800

1,000

1,200

0 5 10 15 20 25 30 35 40 45 50

Longer term, continued and rapid industrialisation expected in

China, India and other developing nations

23

X-axis: 2010 GDP/capita, US$’000(1), Y-axis: 2010 Apparent finished steel

consumption/capita, kg

Bubble area proportional to 2010 apparent finished steel consumption

Data: International Monetary Fund, CRU Analysis Note: (1) – current prices

China

Russia

Brazil

India

South Korea

Taiwan

Turkey

Saudi Arabia Spain

Japan Italy

Germany Canada

USA UK

France

Russia

Continued recovery in developed markets and further growth in emerging economies will see steel demand rise steadily

Data: CRU Analysis, OE Note: f forecast

0

200

400

600

800

1000

1200

1400

1600

1800

2000

-10%

-5%

0%

5%

10%

15%

20%

2004 2005 2006 2007 2008 2009 2010 2011f 2012f 2013f 2014f 2015f

Consumption Global China

India USA Germany

LHS: Industrial production by country, year-on-year change, %

RHS: Global finished steel consumption, m tonnes

Coking Coal - Chinese import potential is great, though Mongolia will

help fill the gap

-70

-60

-50

-40

-30

-20

-10

0

10

20

2003

2004

20

05

20

06

20

07

20

08

20

09

2010

2011

2012

2013

2014

2015

m t

on

ne

s

Imports from Mongolia Seaborne Imports Exports Net exports

25

Data: CRU Analysis, GTIS

Net imports/exports of metallurgical coal, China, 2003-2015

26

Steel mills have been aggressive in acquiring captive

coal supply, and this should continue

USA

Essar Trinity Coal 2010

JSW Steel WV ops 2010

Metinvest United Coal 2009

Mechel Bluestone Coal 2009

Severstal PBS Coals 2008

ArcelorMittal Mid-Vol Coal 2008

Mozambique

Nippon Revuboe 2010

POSCO Revuboe 2010

WISCO Zambeze 2010

CSN Benga, etc. 2009

ArcelorMittal CoAL (S Afr.) 2008

Tata Steel Benga 2007

Australia

Nippon Foxleigh 2010

POSCO Sutton Forest 2010

Xinyang Maryborough 2010

Jindal Rockalds Richfield jv 2010

Baosteel Aquila 2009

JFE Steel Byerwen 2009

ArcelorMitta

l Macarthur 2008

POSCO Cockatoo, Macarthur 2008

Bhushan

Steel Bowen Energy 2007

Russia

MMK Belon 2009

ArcelorMittal Kuzbass mines 2008

Mongolia

ArcelorMittal?

POSCO? Tavan Tolgoi ?

Data: CRU Analysis, TEX Report

Recent upstream integration movements from steel mills

27

But there are no perfect solutions for coking coal supply,

and the market will be dependent on higher-risk areas

Western Canada

High cost to develop, run

coal operations Appalachia

Dwindling base of quality

reserves, high operating

costs, decreasing yields,

increased regulation

Mozambique

Good reserves and

mining conditions, but

limited infrastructure, and

high ash

Central Queensland

Costs rising, fewer development

opportunities though substantial reserve

base remains

Indonesia

Limited current production.

Development of hard coal

deposits has proven difficult

logistically

Mongolia

Political risks, no infrastructure,

and limited seaborne export

options

Siberia (Elga deposit)

Infrastructure lacking, transport

costly, and export capacity

uncertain

Primary seaborne supply sources

Other important suppliers

Prospective major projects

Poland, E. Europe

Deep reserves, poor

geology, increased

local demand.

Western Ukraine

Size and quality of

deposits largely

unknown

Russia (Kuzbass)

Quality questionable. Will

continue to struggle with transport

limitations, and focus on domestic

market

“Torrid”

“Frigid”

“Warm Temperate”

* Relative forecast average 2015 prices versus June 1st 2011 e as a base level

Commodity Price ‘Climate Change’: Zinc to lead Global Warming

in Prices – Even ‘cooling’ commodities will be highly profitable

CRU Commodity Price Climatic Zones – What’s hot to 2015?

“Cool Temperate”

Zinc (2015, not before)

Uranium, Tin, Nickel, Molybdenum,

Alumina, Lead, Copper, Aluminium,

Manganese, Cobalt, Vanadium

Platinum, Iron Ore, Palladium, Gold

Phosphate Rock, Coking Coal, Met

Coke, Ammonia, Urea, Silver, Sulphur,

Sulphuric Acid

Thank you

29

Dr Allan Trench – Associate Consultant, CRU Strategies [email protected] Philip Sewell – Business Development Manager, Australasia [email protected] With Thanks to Peter Ghilchik CRU International Ltd 31 Mount Pleasant, London WC1X 0AD Phone: +44 20 7903 2208 [email protected] http://www.crugroup.com