payment improvements in the u.s. june 2015. should free market determination select the best...

TRANSCRIPT

Payment Improvements in the U.S.

Jun

e 20

15

2

• Should Free Market Determination Select the Best Option(s) for Electronic Business Payments?

– Fed estimates that only 27% of checks will move to the new online real-time credit push system by 2025

– Should the market support improvements for the other 73% of check payments?

– How far is the UK ahead of the US?

– How can free market determination be supported?

Questions

3

• No Universally Acceptable Alternative to Checks for Business Payments

– Phoenix-Hecht (2014) reported 65% of business payments made by check (small businesses not included)• Credit push alternatives have been available for decades• Fed, private sector and NACHA have heavily supported moving

business payments to ACH credits

– Alternatives to paper checks are:• Today - Fedwire or ACH credit• Future – Online, realtime credit push payments

– Years and billions of dollars away– Fed estimate is that only 27% of all checks will make transition in 10 years– Is there sufficient difference in this credit push option to overcome business

inertia? – What about the other 73% of checks – why not improve them?

Business Payments

4

• According to Phoenix-Hecht (2014)– Businesses prefer check payments by a ratio of

more than 3 to 1 over all other payment types

• In Both the U.S. and Canada– Businesses report that check systems work and

are not problems

• According to the Federal Reserve Payments Studies– The percentage of total check payments that are

business payments continues to rise

Business Payments

5

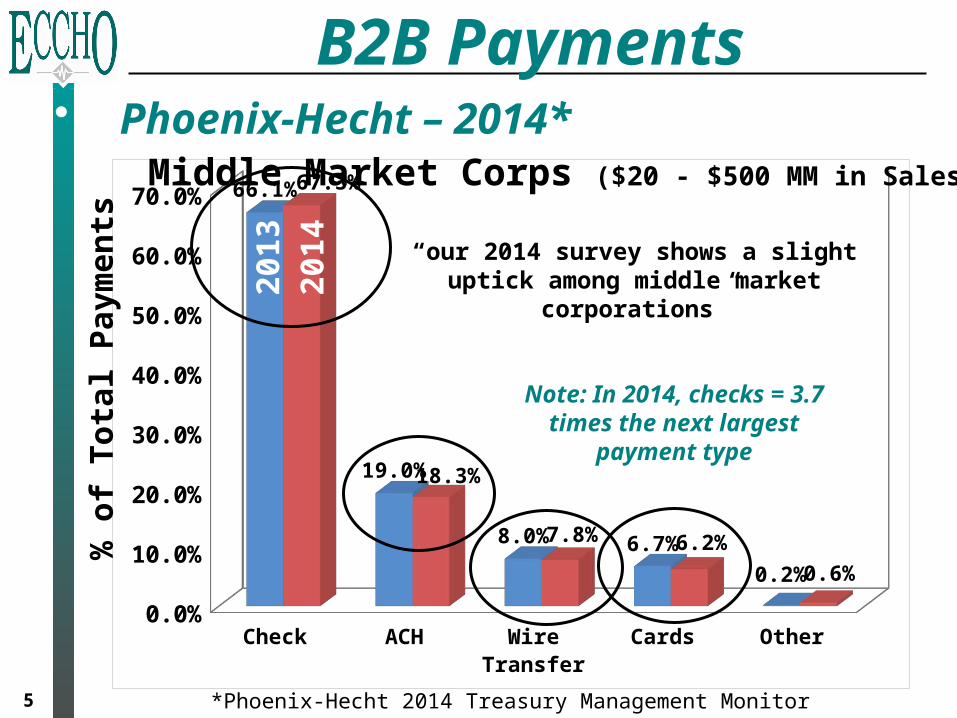

• Phoenix-Hecht – 2014*

B2B Payments

Check ACH Wire Transfer Cards Other0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0% 66.1%

19.0%

8.0% 6.7%

0.2%

67.3%

18.3%

7.8% 6.2%

0.6%

2013

2014 “our 2014 survey shows a slight uptick

among middle market corporations”

Middle Market Corps ($20 - $500 MM in Sales)

Note: In 2014, checks = 3.7 times the next largest

payment type

% o

f To

tal

Pay

men

ts

*Phoenix-Hecht 2014 Treasury Management Monitor

6

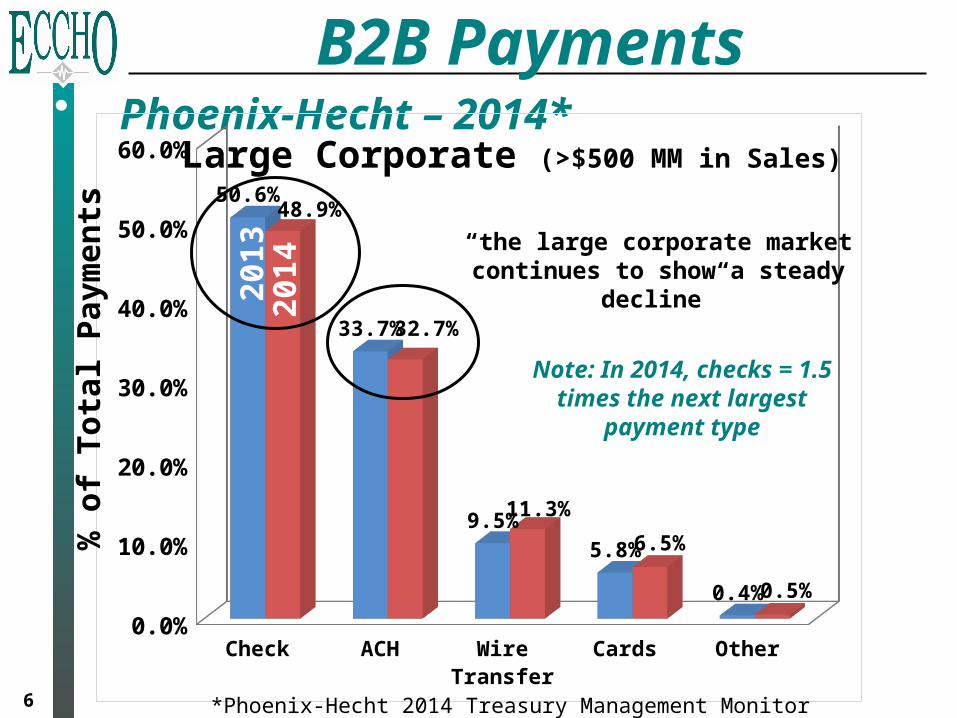

• Phoenix-Hecht – 2014* B2B Payments

2013

2014

Check ACH Wire Transfer Cards Other0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

50.6%

33.7%

9.5%5.8%

0.4%

48.9%

32.7%

11.3%

6.5%

0.5%

Large Corporate (>$500 MM in Sales)

2013

2014

“the large corporate market continues to show a steady decline”

Note: In 2014, checks = 1.5 times the next largest

payment type

% o

f To

tal

Pay

men

ts

*Phoenix-Hecht 2014 Treasury Management Monitor

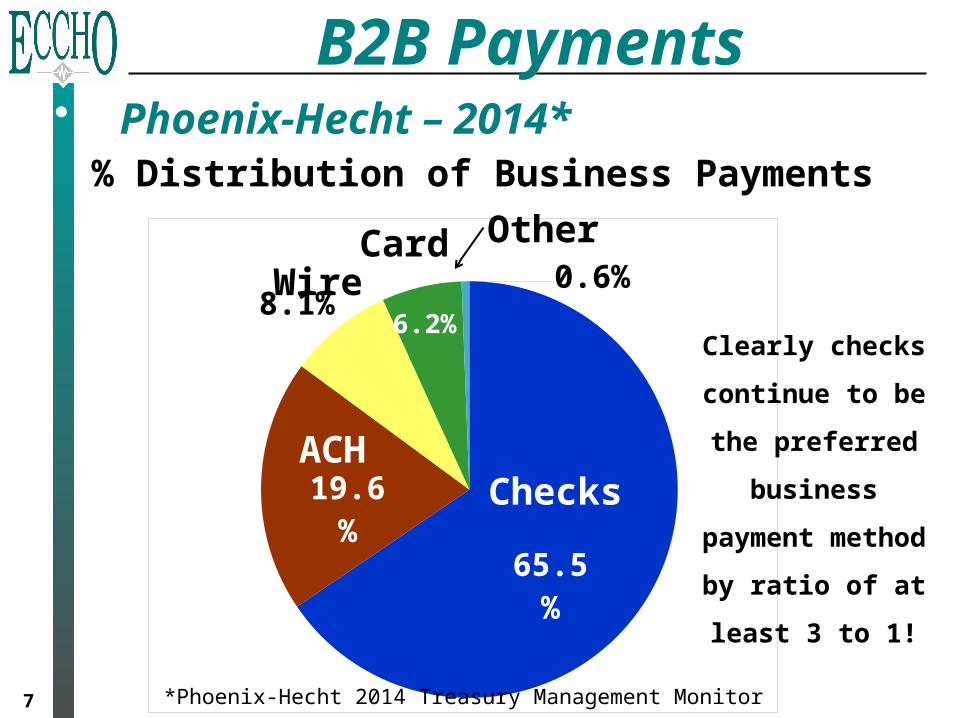

• Phoenix-Hecht – 2014*

B2B Payments

7

ChecksACH

65.5%

19.6%

8.1%6.2%

0.6%WireCard Other

% Distribution of Business Payments

Clearly checks

continue to be the

preferred

business payment

method by ratio of

at least 3 to 1!

ChecksACH

*Phoenix-Hecht 2014 Treasury Management Monitor

8

• Fed Payment Studies*

B2B Payments

B2B as Percentage of Checks Written

Clearly shows

the persistence

of business

checks

2001 2006 2009 20120%

5%

10%

15%

20%

25%

30%

35%

15%

25%27%

32%

*The 2013 Federal Reserve Payments Study

9

• Business Investment Options Are:– Spend money on administration/overhead or– Spend money where its make money

• On its goods and services

• To Spend on Administration/Overhead, Businesses Need:– To fix an existing or imminent problem that

prevents normal, ongoing business, or– An ROI that is greater than generated from their

normal business activities• Especially true for publically held corporations

• Payments are an Overhead Costs for Businesses

Investments in Payments

10

• Applying the UK Experience to U.S.– After 6 ½ years, single item, immediate Faster

Payments total 4% of total non-cash payments• Linearly extrapolated over 10 years yields 6.1%

– Between May 2008 and December 2014:• Non-cash payments in UK grew by 416 million payments

per month• Single item, immediate (SI) Faster Payments grew by 58

million per month– Market demand for non-cash payments grew 7.2 times

faster than demand for SI Faster Payments

– At same adoption rate, U.S. should continue to enhance all of its non-cash payment systems• Assumes 90% will not transition in first 10 years, and• 73% of checks will not transition in first 10 years

UK Experience

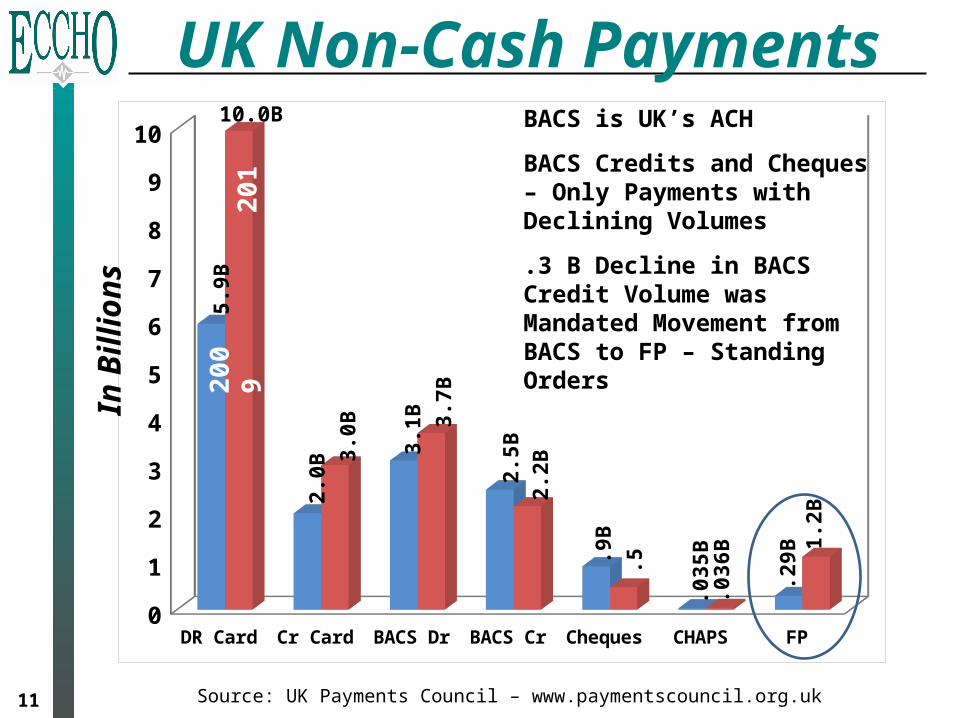

11 Source: UK Payments Council – www.paymentscouncil.org.uk

DR Card Cr Card BACS Dr BACS Cr Cheques CHAPS FP0

1

2

3

4

5

6

7

8

9

10In

Bil

lio

ns

200

92

014

BACS is UK’s ACH

BACS Credits and Cheques – Only Payments with Declining Volumes

.3 B Decline in BACS Credit Volume was Mandated Movement from BACS to FP – Standing Orders

UK Non-Cash Payments

5.9B

10.0B

2.0B

3.1B

2.5B

.9B

.035

B

.29B

3.0B

3.7B

2.2B

.5

.036

B 1.2B

12

May 2008 Dec 20140

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,05

6,57

6*

1,47

3,01

2*

All

Fas

ter

Pay

men

ts

Sin

gle

Ite

m I

mm

edia

te F

P

101,

885

58,5

04

Growth in Volumes 6.5 Years After FP Implementation:

Total Payments - 416.4 millionFaster Payments - 101.6 millionSI Payments - 58.2 million

Dec 2014 - SI Payments only 4.0% of Total Non-Cash Payments

Market demand for non-cash payments grew 7.2 times faster than demand for SI payments

*Source: UK Payments Council – www.paymentscouncil.org.uk

*Total Non-Cash Payments (w/o credit cards)

UK Faster Payments

Implementation Success

13

In T

ho

usa

nd

s /

Mo

nth

Volume Trends - 1st 80 Months

1 5 9 13 17 21 25 29 33 37 41 45 49 53 57 61 65 69 73 770

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1 5 9 13 17 21 25 29 33 37 41 45 49 53 57 61 65 69 73 770

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

Months

Months

UK’s Faster Payments

U.S. Image Exchange

So

urc

es:

UK

Pay

men

ts C

ou

nci

l & C

hec

kIm

ageC

entr

al

1.3B

.1B

May 2008 Dec 20140

200,000

400,000

600,000

800,000

1,000,000

1,200,000

14

Growth in Volumes 6.5 Years After FP Implementation:

Total Debits - 361,096Total Credits - 45,922

Demand for debit pull payments grew 7.8X faster than demand for credit push payments since introduction of Faster Payments

*Sources: UK Payments Council & UK Cards Association

*Total Debits vs Total Credits (w debit cards)

UK Payments Trend#

of

Pay

men

ts /

Mo

nth

Deb

it P

ull

s

Cre

dit

Pu

sh

Deb

it P

ull

s

Cre

dit

Pu

sh

15

UK Payments Trend#

of

Pay

men

ts /

Mo

nth

May '0

8

Sept '08

Jan '09

May '0

9

Sept '09

Jan '10

May '1

0

Sept '10

Jan '11

May '1

1

Sept '11

Jan '12

May '1

2

Sept '12

Jan '13

May '1

3

Sept '13

Jan '14

May '1

4

Sept '14

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000*Total Debits vs Total Credits (w debit cards)

Credit Push

Debit Pull

% Total Payments

May '08 Dec '14Debits 76.6% 97.5%Credits 33.4% 2.5%

*Sources: UK Payments Council & UK Cards Association

% Change/Yr:

Debits – 6.8%Credits – 2.8%

16

• Credit Push Options Have Been Available for >30 Years in the US– But all have failed the market adoption test

• Payment examples: ACH credits and Fedwire• Remittance standard: Electronic Data Interchange (EDI)

– Is there sufficient financial incentive in 2015 for businesses to invest in modified versions of credit push payments?

Credit Push in the US

17

• According to the Federal Reserve’s Summary of Its Electronic Payment Order (EPOs) Forum– “EPOs are a viable payment method for both small

and large businesses because of the speed in clearing and settling them, the finality of payment, their low cost, their ubiquity and their familiarity.”

• EPOs address many desired outcomes of the Payments Improvement initiative!

Is There a US Alternative?

• Minimal New Investment (+ROI image)• Minimal Changes in Processes• Reduced Expenses• Quick Implementation

EPO ScenarioC

HE

CK

WR

ITE

R

DE

PO

SIT

OR

CH

EC

K W

RIT

ER

PAYING BANK

INTERMEDIARY BANK

COLLECTING BANK (BOFD)

ImageImage Image

DepositRemittanceData

EPOStatement

Image

RDC

19

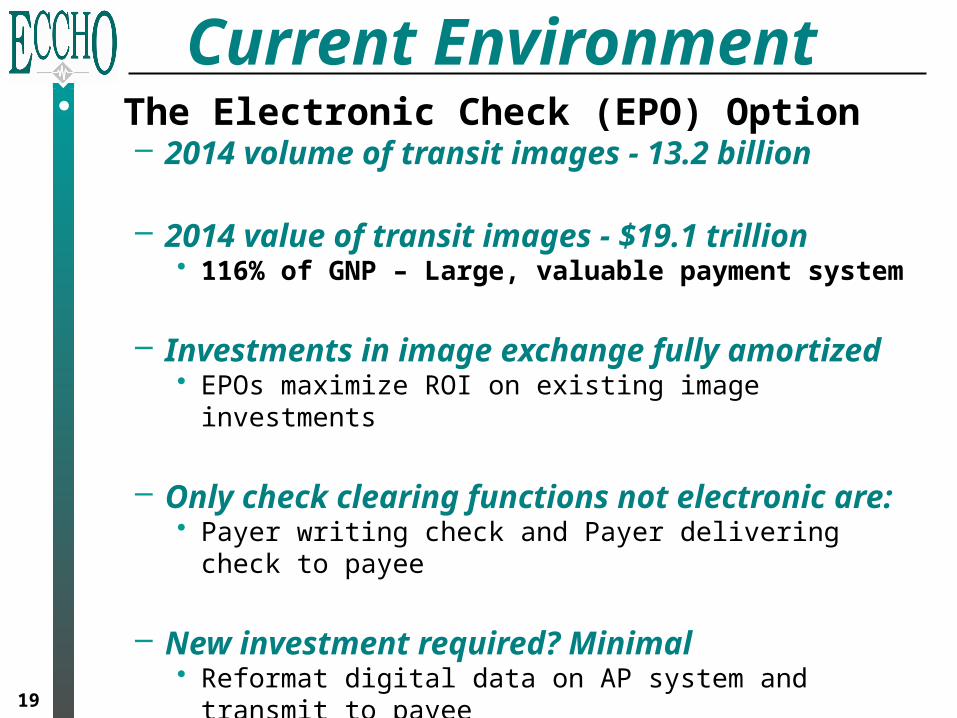

• The Electronic Check (EPO) Option– 2014 volume of transit images - 13.2 billion

– 2014 value of transit images - $19.1 trillion• 116% of GNP – Large, valuable payment system

– Investments in image exchange fully amortized• EPOs maximize ROI on existing image investments

– Only check clearing functions not electronic are:• Payer writing check and Payer delivering check to payee

– New investment required? Minimal• Reformat digital data on AP system and transmit to payee• Interface EPO with RDC application

Current Environment

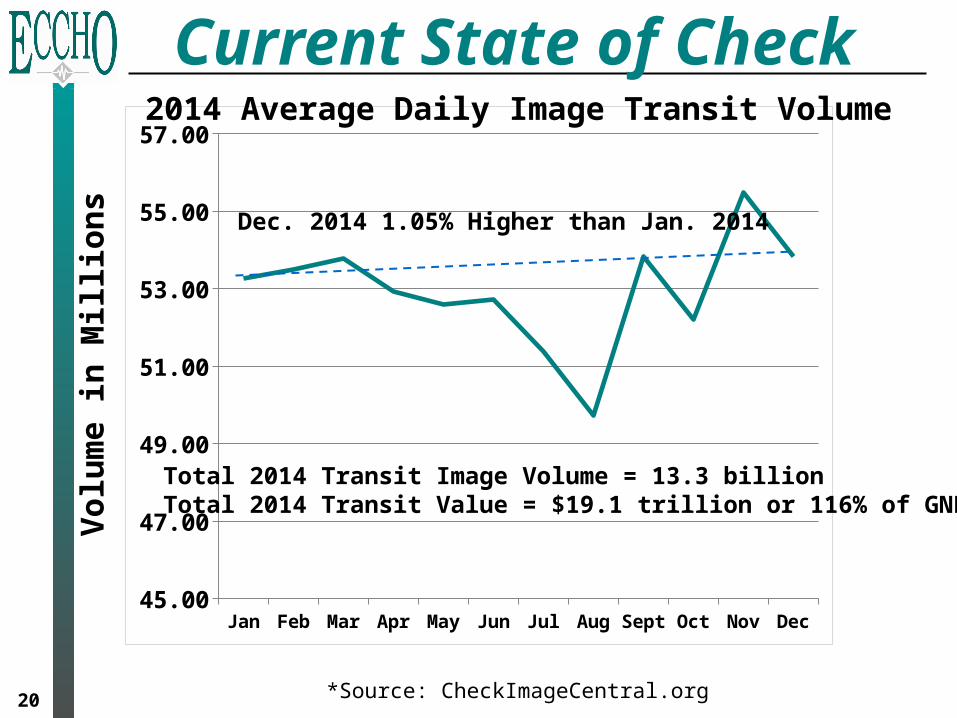

20

Jan Feb Mar Apr May Jun Jul Aug Sept Oct Nov Dec45.00

47.00

49.00

51.00

53.00

55.00

57.00

Current State of CheckV

olu

me

in M

illi

on

s

*Source: CheckImageCentral.org

2014 Average Daily Image Transit Volume

Dec. 2014 1.05% Higher than Jan. 2014

Total 2014 Transit Image Volume = 13.3 billionTotal 2014 Transit Value = $19.1 trillion or 116% of GNP

21

• EPO Societal Value?

– Cost savings similar to other electronic payments, but• Without significant new investment, and

– Enhanced value from short implementation

• EPOs Accelerate the Clearing of Checks

– With image, most checks clear same day as deposited• Some banks report more than 80% clear same day

– With EPOs, more checks can clear same day as written (originated)• Improves end user experience!

Value / Speed

22

• According the Federal Reserve

– The transaction and dollar amounts of fraud is less in check than in ACH or cards

– The rate of return of unpaid checks declined by 40% between 2009 and 2012

• According to the American Banker Association

– Check fraud down 37% from 2008 to 2012– Checks were ranked lowest among eleven

payment options in terms of future threats• Online Banking and ACH were ranked highest

Risks?

Unpaid Check Returns*V

olu

mes

in M

illio

n /

Yea

r

2003 2006 2009 20120

20

40

60

80

100

120

140

160

180

200 186.9

153

126.8

64

2003 2006 2009 20120.00%

0.05%

0.10%

0.15%

0.20%

0.25%

0.30%

0.35%

0.40%

0.45%

0.50%# Unpaid Cks Returned Return Rates

• Since 2003– Returns declined 66% (50% since 2009)

*Source: Federal Reserve’s 2013 Payments Study

.5%

.3%

23

Check Fraud Trend*

*Source: 2013 ABA Deposit Account Fraud Survey Report

1997 1999 2001 2003 2006 2008 2010 2012$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

$s in

Mill

ion

/ Y

ear 37% Decline

in 5 years

2012 – Lowest amount since 1997

$648

$1,024

24

• Check has Least Volume and Smallest $ Amount in Fraudulent Payments!

Distribution of Fraud*

*Source: Federal Reserve’s 2013 Payments Study

Number of Transactions Value of Transactions

Cards92%

Cards65%

ACH 5%

ACH 19%Check 3%

Check 16%

25

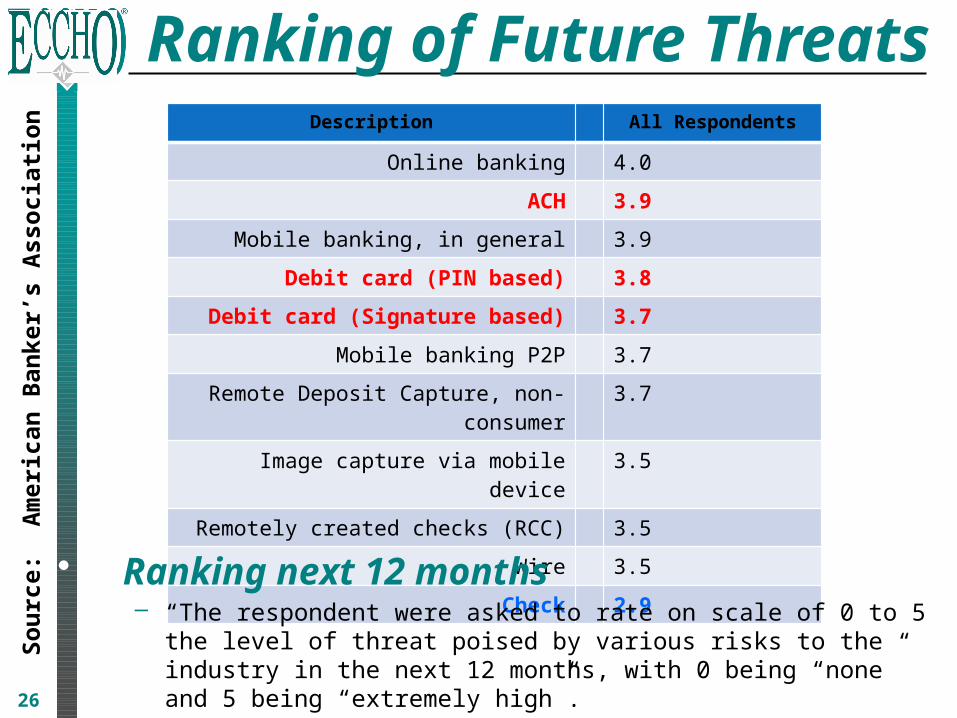

Ranking of Future Threats

26

Description All Respondents

Online banking 4.0

ACH 3.9

Mobile banking, in general 3.9

Debit card (PIN based) 3.8

Debit card (Signature based) 3.7

Mobile banking P2P 3.7

Remote Deposit Capture, non-consumer 3.7

Image capture via mobile device 3.5

Remotely created checks (RCC) 3.5

Wire 3.5

Check 2.9

• Ranking next 12 months– “The respondent were asked to rate on scale of 0 to 5 the level of threat

poised by various risks to the industry in the next 12 months, with 0 being “none” and 5 being “extremely high”.

So

urc

e: A

mer

ican

Ban

ker’

s A

sso

ciat

ion

27

• Enhance the Payment Type Preferred 3 to 1 by Businesses

– Maximize achievement of Payments Improvement initiative by building on most successful payment transition in history

• Achieve business savings associated with paper medium• Accelerate clearing to same day as written

– Maximize ROI on existing investments & minimize required new investments

– Minimize disruption to businesses and their payments and remittance processing• Avoids converting debit payments to credits

– Minimize uncertainty of business acceptance

Maximize Returns

28

• The Problem

– What was bad about paper checks was the medium

• Electronic images eliminated the physical medium for banks and the Fed

• Opportunity

– Eliminate the physical medium for businesses and create significant, new societal value

Problem Eliminated?

29

• Express Your Support

– If you support continued improvements to the check system contact ECCHO and let us know and contact your Federal Reserve Representative and let him/her know

– If you support letting the market determine the best option for business payments contact your Federal Reserve Representative and let him/her know

– If you support creating significant, new societal value for businesses through improvements in business payments, ECCHO and the Federal Reserve need to know

What to Do Now?

David Walker, [email protected]

214.273.3201

Thank You!

Electronic Check Clearing House Organizationwww.eccho.org