payback period time value of money ad internal rate ofreturn

TRANSCRIPT

Payback Period,Time Value of

Money &Internal Rate of

ReturnPresented By:SUBHASH ROHIT

Payback Period

Def i ni t i on:The Payback

peri od i s t he amount of t i me t hat i t t ake t o recover your cos t s i n a proj ect .

FORMULA: Payback Period Even Or Uneven

Even:Payback Per iod = I nit ial I nvest ment / Annual Cash f lows

Uneven:Paybeck Per iod=A+(B/ C)

Wher e; A=The Last per iod wit h a negat ive cumulat ive cash f low

B=The absolut e value of cumulat ive cash f low at t he end of t he per iod A;

C=The t ot al cash f low dur ing t he per iod af t er A

ExampleEven Cash Flow:Company C is planning to undertake a project requiring initial

investment of $105 million. The project is expected to generate $25 million per year for 7 years. Calculate the payback period of the project.

Cont. .Payback Per iod = I nit ial I nvest ment / Annual Cash f lows

=$105/ $25 =4.2 year

Cont. .Uneven Cash Flows.Company C is planning to undertake another project requiring initial

investment of $50 million and is expected to generate $10 million in Year 1, $13 million in Year 2, $16 million in year 3, $19 million in Year 4 and $22 million in Year 5. Calculate the payback value of the project.

Cont. .

Payback Per iod= 3 + (| -$11M| ÷ $19M)= 3 + ($11M ÷ $19M)≈ 3 + 0.58≈ 3.58 year s

(cash flows in millions) Year Cash Flow

CumulativeCash Flow

0 50 -50

1 10 -40

2 13 -27

3 16 -11

4 19 8

5 22 30

Payback Period RuleThe Decision Rule: t he act ual

payback is compar ed wit h a pr edet er mined pay back, t hat is, t he pay back set by t he management in t er ms of t he maximum per iod dur ing which t he invest ment must r ecover ed.

I f t he pay back per iod is less t han t he pr edet er mined payback, t hen t he pr oj ect would be Accept ed; if not , it would be r ej ect ed

Advantage of Payback Period

I t is ver y simple. I t is easy t o under st and and apply

I t is cost ef f ect iveThe payback per iod measur es

t he dir ect r elat ionship bet ween annual cash inf lows f r om Pr oposal and t he net invest ment r equir ed

Disadvantage Of Payback Period

The pay back per iod ent ir ely ignor es t he cash inf lows t hat occur af t er t he pay back per iod

The pay back per iod also ignor es salvage value and t ot al economic lif e of t he pr oj ect

I t ignor es t he t ime value of money

Drawbacks of Payback Period

Does not consider all of t he pr oj ect ’s case f lows.

This pr oj ect is clear ly pr of it able, but we would accept it based on a 4 year payback cr it er ion!

Time Value Of MoneyThe concept moder n f inance

and management .We say t hat money has a t ime

value because t hat money can be invest ed wit h t he expect at ion of ear ning a posit ive r at e of r et ur n

I n ot her wor ds, “a r upee r eceived t oday is wor t h mor e t han a r upee t o be r eceived t omor r ow”

Calculations based on the time value of money

Present Value - An amount of money t oday, or t he cur r ent value of a f ut ur e cash f low

Future Value - An amount of money at some f ut ur e t ime per iod

‘n’ is t he number of per iods ‘r ’ is t he r at e at which t he

amount will be compounded each per iod

Cont…PV(A) t he value of t he annuit y

at t ime = 0 FV(A) t he value of t he annuit y

at t ime = n ‘A’ t he value of t he individual

payment s in each compounding per iod

‘n’ is t he number of per iods ‘r ’ is t he r at e at which t he

amount will be compounded each per iod

FormulasPresent value of a future sum

/ Future value of a present sum.

Example Consider 2 sit uat ions

Opt ion A: You r eceive Rs. 10,000 t oday.

Opt ion B: You r eceive Rs. 10,000 in 3 year s t ime

Assume no inf lat ion Assume int er est r at e 10%

(Compound I nt er est ) Assume no change in any ot her

f inancial sit uat ion

Future Value Calculation

Consider Opt ion B Let ’s calculat e t he f ut ur e value

of Rs. 10,000 r eceived at t he pr esent t ime.

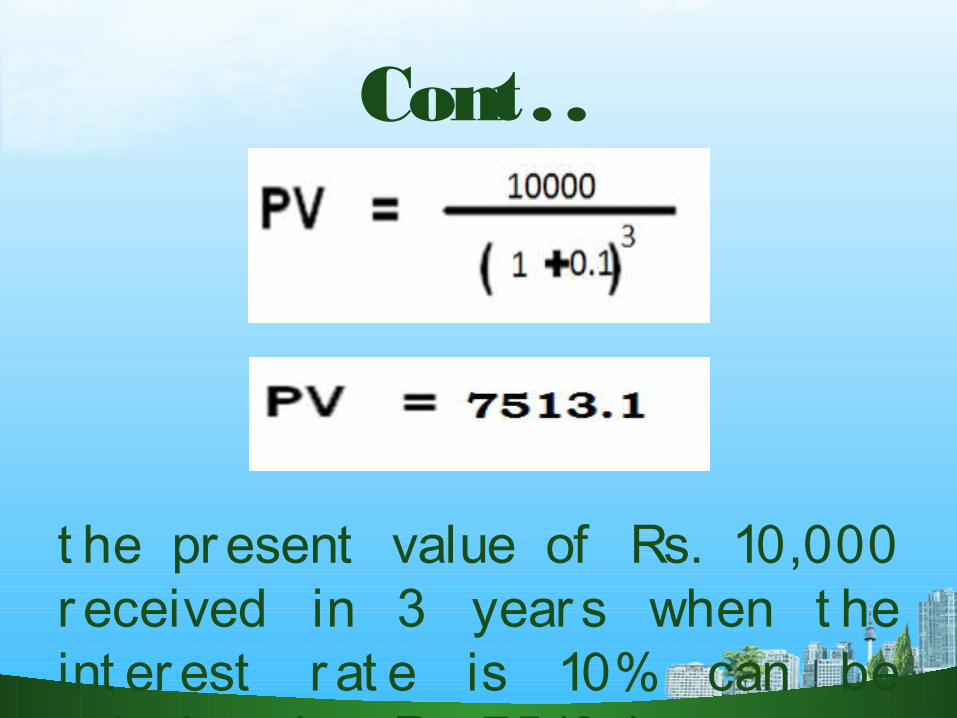

Cont. .

Present Value Calculation

Similar ly using t he equat ion as

Cont. .

t he pr esent value of Rs. 10,000 r eceived in 3 year s when t he int er est r at e is 10% can be calculat ed as Rs. 7513.1

Cont. .

(Internal Rate of Return) IRRThe I RR should be applied only

f or ver y simple invest ment s. I nt er nal r at e of r et ur n (I RR) is

t he discount r at e at which t he net pr esent value of an invest ment becomes zer o. I n ot her wor ds, I RR is t he discount r at e which equat es t he pr esent value of t he f ut ur e cash f lows of an invest ment wit h t he init ial invest ment .

Cont…Decision Rule

St and-alone Pr oj ect s I f I RR > cost of capit al

(k) ⇒ accept I f I RR < cost of capit al

(k) ⇒ r ej ect

IIR Calculation Formula

Cont..

Find the IRR of an investment having initial cash outflow of $213,000. The cash inflows during the first, second, third and fourth years are expected to be $65,200, $96,000, $73,100 and $55,400 respectively.

Assume that r is 10%.

NPV at 10% discount r at e =

$18,372Since NPV is gr eat er t han zer o we have t o incr ease discount r at e, t husNPV at 13% discount r at e = $4,521But it is st ill gr eat er t han zer o we have t o f ur t her incr ease t he discount r at e, t husNPV at 14% discount r at e = $204NPV at 15% discount r at e = ($3,975)Since NPV is f air ly close t o zer o at 14% value of r , t her ef or eI RR ≈ 14%

Cont…

Fir st , imagine a sit uat ion in which you invest $1 million t oday and t hen r eceive $500,000 per year f or t he next 4 year s. That invest ment gives an I RR of 35%, which would be pr et t y good by t oday’s st andar ds. Now let ’s change some of t he key var iables.

I f inst ead you had t o invest only

$500,000 up f r ont f or t he same amount of r et ur n, t he I RR impr oves t o 93%.For t hose of you unf amiliar wit h t he t er minology, a pr oj ect wit h an I RR of 93% is bot h r ar e and ver y desir able t o pur sue. The r educt ion in t he up-f r ont invest ment caused t he r et ur n t o skyr ocket .

Now let ’s go back t o t he init ial $1 million invest ment and make t he r et ur n only $350,000 f or 4 year s. This manipulat ion causes t he I RR t o dr op t o only 15% f r om t he pr evious value of 35%.

CONCLUSIONAny t ime you ar e evaluat ing an

invest ment over t ime, use t ime-value-of -money.

I n f inancial modelling, allow f or bot h t ime-value-of money calculat ions as well as uncer t aint y t o impr ove your pr oj ect ions and t he decisions on which t hey ar e based.

Thank

You…!