part ii - micro business publications - business games and

TRANSCRIPT

Part IIManagement Accounting Decision-Making Tools

Chapter 7 • Cost-Volume-Profit Analysis

Chapter 8 • Comprehensive Business Budgeting

Chapter 9 • Incremental Analysis and Decision-making Costs

Chapter 10 • Incremental Analysis and Cost-Volume-profit Analysis: Special Applications

Chapter 11 • Economic Order Quantity Models

Chapter 12 • Capital Budgeting Decisions Tools

Chapter 13 • Pricing Decision Analysis

Management Accounting | 113

Cost-Volume-Profit Analysis

The success of a business as measured in terms of profit depends upon adequate sales; that is; the volume of sales must be sufficient to cover all costs and allow a satisfactory margin for net income. When the proportion of fixed costs in a business becomes large in relation to total costs, then volume becomes an extremely important factor in achieving profitability. For example, a business with only variable costs would be able to report net income at any level of sales as long as price exceeds the variable cost rate. However, a business with only fixed costs cannot show a profit until the contribution from sales is equal to the amount of fixed expenses. Therefore, a minimum level of sales is absolutely essential in a business that incurs fixed expenses.

Because changes in volume can have a profound impact on the profits of a business, cost-volume-profit analysis has been developed as a management tool to enable analysis of the following variables:

1. Price2. Quantity3. Variable costs4. Fixed costs

The focal point of cost-volume-profit analysis is on the effect that changes in volume have on fixed and variable costs. Volume may be regarded as either units sold or the dollar amount of sales. Typically, the theory of cost-volume-profit analysis is explained in terms of units. However, using units as the measure of volume for computing break even point or target income point requires that the business sell

114 | CHAPTER SEVEN • Cost-Volume-Profit Analysis

only a single product. Since all businesses from a practical viewpoint sell multiple products, the real world use of cost-volume-profit analysis requires that volume be measured in terms of sales dollars.

Cost-volume-profit analysis may be used as (1) a tool for profit planning and decision-making and (2) as a tool for evaluating the profitability of proposed business ventures. In this chapter, the discussion of profit analysis shall be limited to its use as a current period profit and decision-making tool.

Nature of Cost-Volume-Profit AnalysisIn chapter 5, the subject of cost behavior was discussed. The point was made that

the costs of a business could be classified as either fixed or variable. Mathematically, it was stated:

TC = V(Q) + F (1)TC - total costsV - variable cost rateQ - quantity

Revenue or sales may be defined as:S = P(Q) (2)

S - salesP - price

Income may be defined as:I = R - E (3)

R - revenueE - expenseI - income

When equations (1) and (2) are substituted into equation (3), equation (3) becomesI = P(Q) - V(Q) - F (4)

Equation (4) is recognized in this chapter as the foundation of cost-volume-profit analysis. Quantity (Q) is generally treated as the independent variable; that is, income is regarded as a function of quantity (Q). The variable cost rate (V) and fixed expenses (F) are assumed to be constants. However, for certain analytical purposes, the values of V and F may be assigned different values in order to determine the effect of the changes in these values on net income.

Equation 4, it should be noted, may be used as a tool of analysis only for a single product business. For firms that have more than one product, another equation which emphasizes sales as volume in dollars must be used:

I = S - v(S) - F (5)S - sales in dollarsv - variable cost percentage

In a multiple product business, it is necessary to express variable cost as a percentage of sales. This percentage will be discussed in detail in a later section of this chapter.

Management Accounting | 115

Cost-volume-profit Analysis for a Single Product BusinessFrequently, it is necessary to ask the question: how many units must be sold in

order to attain a given level of net income? Equation (4) may be used to answer this question; however, in order to do so it is necessary to solve for quantity, Q.

I = Q(P - V) - F

I + F = Q(P - V )

I + FQ = ––––– (6) P - V

Equation (6) may be used to determine the quantity of sales required to attain any desired level of income. For example, assume that the Acme Company’s selling price is $10 and its variable cost rate is $8. Also, assume that it has fixed expenses of $5,000. Suppose that management desires to earn $8,000 for the period. How many units must the company sell in order to attain the desired net income?

Answer: This question may be answered simply by substituting these given rev-enue and cost values into equation 6:

I + F $8,000 + $5,000 $13,000Q = –––– = ––––––––––––– = ––––––– = 6,500 units P - V $10 - $8 2

Therefore, the Acme Company must sell 6,500 units to earn $8,000. The validity of this answer can be demonstrated as follows:

Sales (6,500 x $10) $65,000Expenses: Variable (6,500 x $8) $52,000 Fixed 5,000

_______ Total expenses $57,000

_______ Net income $ 8,000 ––––––– –––––––

In management accounting literature, considerable emphasis is given to the concept of a break even point. While it is an interesting academic exercise to compute break even point, it should be stressed that a company does not set a goal to break even. The primary object of management in using cost-volume-profit analysis is to determine target income point and not break even point.

Nevertheless, assuming for some reason that it is considered desirable to know the break even point of a business, the break even point is calculated exactly in the same way as target income point. Equation (6) may be used to compute break even point. Break even point is simply the quantity of sales that achieves zero net income. It is that level of sales where total sales equals total expenses.

Using the same data from the example above, break even point may be computed as follows:

116 | CHAPTER SEVEN • Cost-Volume-Profit Analysis

I + F 0 + 5,000 5,000Q = ––––– = –––––––– = ––––– = 2,500 unitsP - V 10 - 8 2

The correctness of this answer may be demonstrated as follows:Sales (2,500 x $10) $25,000Expenses:

Variable (8 x 2,500) $20,000Fixed 5,000

–––––– 25,000 –––––––Net income $ 0 ––––––– –––––––

Cost-volume-profit Analysis for a Multiple Product BusinessA company with more than one product cannot use equations (4) or (6) as illustrated

and discussed above. It is not possible to logically add different quantities of product. The saying that “you can’t add apples and oranges” applies here. However, it is possible to meaningfully add the dollar value of oranges to the dollar value of apples. In a multiple product business, it is necessary to use the dollar value of sales as the measure of volume.

Equation 5, as previously indicated, is the basis of cost-volume-profit analysis for a multiple product business.

I = S - v(S) - FS - sales in dollarsv - variable cost percentage

The expression v(S) represents total variable expenses. It may be calculated by simply dividing total variable expenses or cost by total sales:

TVEv = –––– (7) S

Where:v - variable cost percentageTVE - total variable expensesS - sales ($)

The variable, v, requires an explanation. As used in the above equation, it is the variable cost percentage; that is, it represents the percentage that total variable cost bears to total sales. The variable cost percentage is assumed to be constant at all levels of activity. For example, assume that v = 70%. Total variable costs would vary with sales as illustrated:

Q v TVC ––––––– – –––––––

$ 10,000 .7 $ 7,000$100,000 .7 $ 70,000$200,000 .7 $140,000$400,000 .7 $280,000

Management Accounting | 117

In order for the variable cost percentage to hold constant in a multiple product business, it is necessary for the sales mix ratio to remain the same. The sales mix ratio is discussed later in this chapter.

As in the case of a single product firm, it is desirable to ask the question: how many units must be sold in order to attain a desired income level? Equation 5 may be used to answer this question; however, it is first necessary to solve for S (sales) as follows:

I = S - v(S) - F S(1 - v) - F = IS(1 - v) = I + F I + FS = –––––– (8) 1 - v

This equation may be used to compute the dollar level of sales required to attain a desired level of income. For example, assume that the Barton Company’s variable cost percentage is 80% and its fixed cost is $10,000. Furthermore, assume that management has set a profit goal of $50,000. What must the dollar volume of sales be in order to attain the $50,000 income objective?Answer:

I + F 50,000 + 10,000 60,000S = –––––– = –––––––––––––– = –––––– = $300,000 1 - v 1 - .8 .2

The correctness of this answer can be demonstrated as follows:

Sales $300,000Expenses:

Variable ($300,000 x .8) $240,000Fixed 10,000

250,000 ––––––– –––––––

Net income $ 50,000 ––––––– –––––––

The Contribution Margin ConceptThe study and use of cost-volume-profit analysis requires understanding the

concept of contribution margin. The study of this unique concept contributes greatly to an understanding of the importance of changes in volume. In an aggregate sense, contribution margin is simply total sales less total variable costs. From a decision-making tool perspective, it is also necessary to understand the concept mathematically. Variation of this concept include:

Single product business:Total contribution margin - P(Q) - V(Q) or Q(P - V)Contribution margin rate (per unit of product) - ( P - V)

Multiple product businessTotal contribution margin - S - v(S) or S(1 - v)Contribution margin percentage - ( 1 - v)

118 | CHAPTER SEVEN • Cost-Volume-Profit Analysis

The contribution margin rate (per unit) and the contribution margin percentage are often called the contribution margin ratio. A ratio may be expressed on a unit basis or a percentage basis.

The concept of contribution margin provides a rather unique way of interpreting the activity of a business. At the start of the operating period, a business with fixed expenses would show a loss. At zero sales, the loss would be equal to total fixed expenses. As each unit of product is sold, the loss is gradually reduced by the contribution margin of each unit sold. No profit can be reported until total contribution equals total fixed expenses. After break even point, each unit sold contributes to net income an amount equal to the contribution margin per unit of product.Total Contribution Margin - As previously defined, total contribution margin is total sales less total variable costs. Mathematically, in terms of the profit equation for a single product business, total contribution margin is equal to P(Q) - V(Q). It is important to understand that the term “contribution” means a contribution first to fixed expenses. As previously mentioned, there can be no profit in a business until total contribution equals total fixed expenses. When this occurs, the business has reached break even point. Break even point is that quantity of sales that causes total contribution margin to be exactly equal to total fixed expenses.Contribution Margin Per Unit of Product - The use of cost-volume-profit analysis as a decision-making tool also requires understanding of the concept of contribution margin per unit of product. The contribution margin rate is simply price less the variable cost rate. Mathematically, the contribution margin rate is P - V.

The use of the contribution margin rate is obvious in equation 6: I + FQ = ––––––– P - V

The denominator in this equation, P - V, is the contribution margin rate and, I + F, is the total contribution desired. An important question is: how much contribution is required in any business? The answer is that the contribution required must be enough to pay fixed expenses and then be sufficient to allow the firm to attain the desired level of income. Consequently, I + F, represents the total required contribution.Illustration

The Acme Company’s accountant provided the following cost-volume-profit data:

P - $10.00V - $8.00F - $5,000I - $25,000

The company’s contribution margin rate is $2 ($10 - $8). Each sale contributes $2. If the company sells 1,000 units, then the total contribution would be $2,000. The company obviously needs an additional $3,000 of contribution to reach break even point. When sales reach 2,500 the total contribution is $5,000 which is equal to fixed expenses. Break even point has been reached. Each additional units sold after break

Management Accounting | 119

even point contributes $2 to income. If 2,600 units are sold, net income would be $200 ($2 x 100).Contribution Margin Percentage - In a multiple product firm, it is necessary to talk in terms of contribution as a percentage. Mathematically, the contribution margin percentage rate is 1 - v. The contribution margin percentage requires that the variable cost percentage be first computed. If the variable cost percentage is 70%, then the contribution margin percentage would be 30% (1 - .70). The importance of the contribution margin percentage is apparent from examining equation 8:

I + FS = ––––––– 1 - v

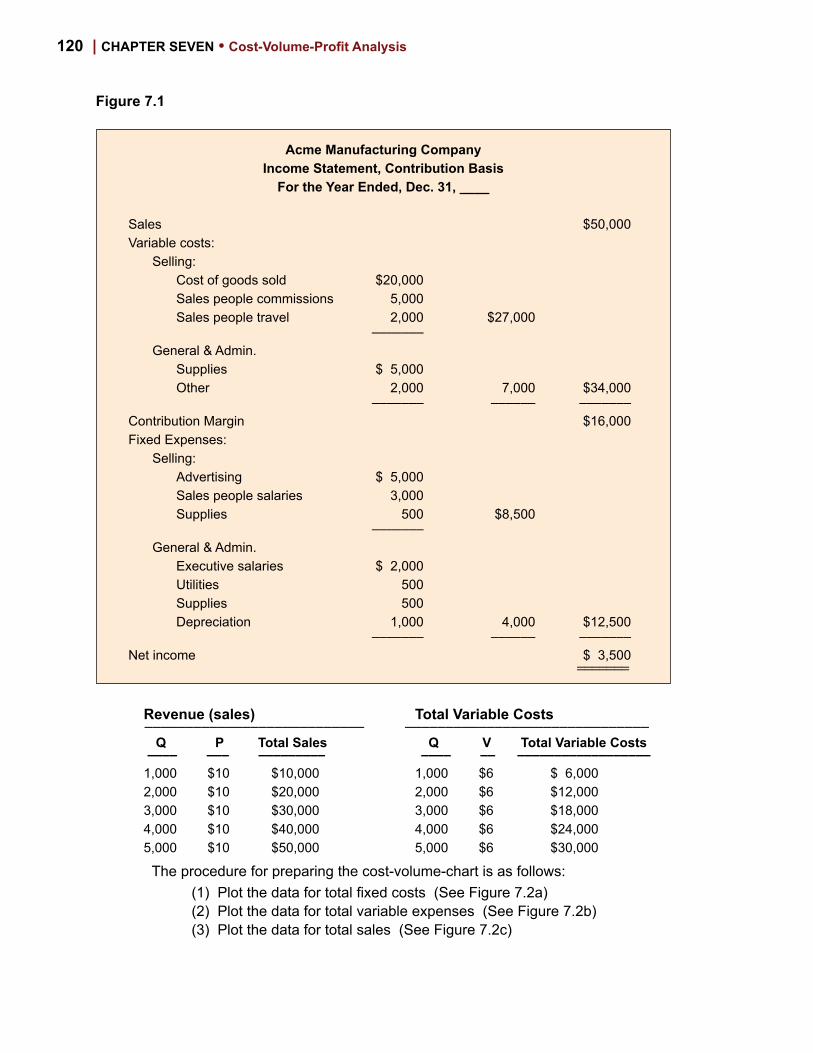

The contribution margin percentage is the percentage that each dollar of sales contributions towards fixed expenses and desired net income. The total contribution required to attain the desire income goal can be computed by simply dividing total desired contribution by the contribution margin percentage.Contribution Margin Income Statement - Cost-volume-profit analysis may be made an integral part of financial reporting. Companies who do this generally prefer to prepare income statements in which fixed costs, variable cost, and contribution margin are explicitly shown. For example, assume that during the year the Acme Company had sales of $50,000 and fixed and variable costs as follows:

Fixed Expenses Variable ExpensesSelling Selling Advertising $5,000 Sales people commissions $ 5,000

Sales people salaries $3,000 Sales people travel $ 2,000Supplies $ 500 Cost of goods sold $20,000

General & Admin. General & Admin.Utilities $ 500 Supplies $ 5,000Supplies $ 500 Other $ 2,000Executive salaries $2,000Depreciation $1,000

Based on the above data, the following income statement may be prepared as shown in Figure 7.1.

Graphical Illustration of Cost-volume-profit AnalysisBecause the fundamental relationships of cost-volume-profit analysis are basically

mathematical in nature, the elements of cost-volume-profit analysis can be illustrated graphically. The general procedure is to plot the revenue and cost functions on the same graph. In order to illustrate the cost-volume-profit graphically, the following data has been assumed:

Price $10Variable cost rate $6Fixed expenses $20,000

For purposes of preparing the graph, assume different levels of quantity starting with 1,000 units and increasing activity by increments of 1,000 units. The following calculations are helpful in plotting the graph.

120 | CHAPTER SEVEN • Cost-Volume-Profit Analysis

Figure 7.1

Acme Manufacturing CompanyIncome Statement, Contribution Basis

For the Year Ended, Dec. 31, ____

Sales $50,000 Variable costs: Selling: Cost of goods sold $20,000 Sales people commissions 5,000 Sales people travel 2,000 $27,000 ––––––– General & Admin. Supplies $ 5,000 Other 2,000 7,000 $34,000 ––––––– –––––– ––––––– Contribution Margin $16,000 Fixed Expenses: Selling: Advertising $ 5,000 Sales people salaries 3,000 Supplies 500 $8,500 ––––––– General & Admin. Executive salaries $ 2,000 Utilities 500 Supplies 500 Depreciation 1,000 4,000 $12,500 ––––––– –––––– ––––––– Net income $ 3,500 _______ _______

Revenue (sales) Total Variable Costs ––––––––––––––––––––––––––– ––––––––––––––––––––––––––––––

Q P Total Sales Q V Total Variable Costs –––– ––– ––––––––– –––– –– –––––––––––––––––– 1,000 $10 $10,000 1,000 $6 $ 6,000 2,000 $10 $20,000 2,000 $6 $12,000 3,000 $10 $30,000 3,000 $6 $18,000 4,000 $10 $40,000 4,000 $6 $24,000 5,000 $10 $50,000 5,000 $6 $30,000

The procedure for preparing the cost-volume-chart is as follows:(1) Plot the data for total fixed costs (See Figure 7.2a)(2) Plot the data for total variable expenses (See Figure 7.2b)(3) Plot the data for total sales (See Figure 7.2c)

Management Accounting | 121

Figure 7. 2 2a 2b

2c

Figure 7.2c represents the completed cost-volume-profit graph. The graph represents an excellent visual means of presenting the basic concepts and cost behavior relationships inherent in cost-volume-profit analysis. An enlarged version of Figure 7.2c is presented is Figure 7.3. Notice that the Acme Company’s break even point can easily be seen to be 5,000 units. Assume that the Acme Company desires to attain an income level of $7,000. The level of sales that will result in this amount of income is $67,500. The graph can be easily used to shown net income and net loss as has been done in Figure 7.3a.

In addition, the concept of contribution margin can be visually represented in Figure 7.3. Notice that in Figure 7.3 that variable cost has been plotted before fixed cost. Note that in Figure 7.3B, the total contribution margin area is indicated by an arrow. By definition total contribution margin is simply total sales less total variable expenses, and this is exactly what is shown in Figure 7.3B. Also, notice that at break even point, the total contribution margin is equal to fixed costs, as illustrated by chart 7.3B. The break even point may be defined in several ways. One definition defines break even point as that level of sales where total contribution margin is equal to total fixed expenses as illustrated in 7.3B. Another definition defines break even point as that level of sales where sales = total expenses (Figure 7.3A). Obviously, in both definitions, net income is zero at break even point.

Fixed Cost Total Fixed and Variable Cost

Volume (Quantity)Volume

Cos

t $

Cos

t $

40000

20000

60000

50000

40000

30000

20000

10000

00 2000 4000 6000 80000 2000 4000 6000 8000

Cost-Volume-Profit Chart

Volume (Quantity)

Sal

es/C

ost (

$)

70000

60000

50000

40000

30000

20000

10000

00 2000 4000 6000 8000

122 | CHAPTER SEVEN • Cost-Volume-Profit Analysis

Figure 7.3 • Graphical Illustration of Contribution Margin

(000)

2,500 5,000 6,750 2,500 5,000 6,750

(000)

Net Income

Volume (units) Volume (units)

Net Loss

Contributionmargin

Contribution margin = fixed expenses

80

70

60

50

40

30

20

10

0

80

70

60

50

40

30

20

10

0

A B

Basic Assumptions of Cost-volume-profit AnalysisIn the next section, illustrations will be given on how cost-volume-profit analysis

may be used as a profit planning and decision-making tool. However, effective use of cost-volume-profit analysis for planning purposes requires understanding of certain basic assumptions. Unless the following assumptions are substantially met, any attempt to use cost-volume-profit analysis in a real world situation may prove to be inaccurate and misleading.

Cost-volume-profit analysis assumptions may be summarized as follows:1. Within a relevant range of volume, the variables price, quantity,

fixed costs, and variable costs are subject to managerial control.

2. Price and the variable cost rate are constant within the relevant range of activity.

This assumption simply means that variable costs and revenues are assumed to vary linearly with changes in volume. State differently, changes in volume have no effect on price, the variable cost rate, and fixed costs.

3. In a multiple product company, the sales mix ratio remains constant with changes in total sales.

Management Accounting | 123

4. In a company that uses absorption costing, unless sales equals production, there exists no unique break even point. When direct costing is used, no problems arise when production varies from sales. In direct costing, fixed manufacturing overhead is treated as a period charge. Direct costing and absorption are discussed in some depth in chapter 6.

Cost-Volume-Profit Analysis: A Decision-making Analysis ToolPrevious discussion of C-V-P was based on the assumption that price, the variable

cost rate, and fixed costs remain constant with increases or decreases in quantity. Changes in quantity do not cause changes in the other variables. However, price, the variable cost rate, and fixed costs can change for reasons other than changes in volume. Management can at any time decide to increase or decrease price. Suppliers at any time can increase or decrease the cost per unit of materials. Many, if not most, variable costs and expenses can be changed by management simply by making the decision to do so.

Since price, variable costs, and fixed costs can be increased or decreased at the will of management, the cost-volume-profit equations can be used to perform what-if analysis. In broad terms, six basic questions may be asked regarding changes in revenues and costs:

PriceWhat is the effect on break even point and target income point of an increase in price?What is the effect on break even point and target income point of a decrease in price?

Variable cost rateWhat is the effect on break even point and target income point of an increase in the variable cost rate?What is the effect on break even point and target income point of a decrease in the variable cost rate?

Fixed ExpensesWhat is the effect on break even point and target income point of an increase in fixed costs?What is the effect on break even point and target income point of a decrease in fixed costs?

An effective way to answers these questions is to use a P/V graph. A P/V graph shows the relationship of net income to volume (sales dollars or units). A P/V graph is shown in Figure 7.4. In this graph, volume is the independent variable and net income the dependent variable. To illustrate how a P/V graph is constructed, assume the following:

124 | CHAPTER SEVEN • Cost-Volume-Profit Analysis

Figure 7.5 • Changes in Net Income Line

In Figure 7.5 is illustrated the effect on break even point and net income of changes in price, variable cost, and fixed expenses. In chart A, an increase in price shifts the line upwards and to the left. The result is a decrease in break even point. In Chart B, a decrease in price has the opposite effect. Break even point has increased in chart C. The increase in variable expenses caused the income line to shift downwards and to the right. The opposite is true of a decrease in the variable expense rate. Break even point has decreased. An increase in fixed expenses will cause the income line to shift to the left and upwards. The result is a decease in break even point. The

$ $ $

$$$

Increase in Price

Net

Inco

me

Net

Inco

me

Net

Inco

me

Net

Inco

me

Net

Inco

me

Net

Inco

me

Decrease in Price Increase in Variable Cost

Decrease in Fixed CostIncrease in Fixed CostDecrease in Variable Cost

A

Q Q Q

Q Q Q

B C

FED

6000

5000

4000

3000

2000

1000

0

-1000

-2000

-3000

-4000

P/V Chart

Volume (units)

2000 4000 6000

Net

Inco

me

$

Net Income

Q

Price (P) $10Variable cost rate (V) $8Fixed Costs (F) $5,000Based on this data, the table below

may be prepared.

Q P(Q) V(Q) F NI –––––––––––––––––––––––––––––––––––––––

1,000 10,000 8,000 5,000 (3,000)

2,000 20,000 16,000 5,000 (1,000)

3,000 30,000 24,000 5,000 1,000

4,000 40,000 32,000 5,000 3,000

5,000 50,000 40,000 5,000 5,000

Figure 7.4

Management Accounting | 125

opposite is true for an increase in fixed expenses. Whether a given change is good or bad for fixed expenses such as advertising can not be stated. For example, an increase in advertising might cause an increase in sales with a resulting increase in net income.

The P/V graph can effectively be used to illustrate changes in price, the variable cost rate, and fixed costs. A change in one of these variables will cause a shift or movement in the net income line.

Changes in Price - An increase in price will most likely result in a decrease in sales. However, a decrease in sales does not necessarily mean a decrease in net income. Regarding the units that are sold, the contribution margin is greater. Consequently, less units of sales are required to attain a profit goal. Given an increase in price, management will probably want to ask the question: how many units of sales can be lost and the same net income earned?

This question can be answered by using the following equation: I + FQ = ––––––– P - V

The procedure is simply to compute Q, or quantity, at the new price and then subtract this quantity from the quantity of sales before the price change.

Illustration Last year, at a sales volume of 5,000 units, the Ace Manufacturing Company’s income statement show the following:

Sales (5,000 x $10) $50,000ExpensesVariable ($8 x 5000) 40,000Fixed 5,000 –––––– 45,000 ––––––Net income $ 5,000 –––––– ––––––

Management is considering increasing price to $12 per unit. At the new price, the quantity necessary to earn the same income would be:

5,000 + 5,000 10,000Q = ––––––––––––– = ––––––– = 2,500 12 - 8 4

At the new price, only 2,500 units need to be sold to earn $5,000. The company can lose one half of its sales without suffering any loss in income. The effect of the change in price on break even point and net income at different levels of sales is shown in Figure 7.5A. Note that in Figure 7.6, the income function shifts upward and to the left. BEP point is now 1,250 units and the income previously earned at 5,000 units can now be earned at 2,500 units.

P/V Chart$

10000

7500

5000

2500

0

-2500

-5000

-7500

P=$12.00 P=$10.00

units1,250 2,500 3,750 5,000

Figure 7.6 • P/V Chart

126 | CHAPTER SEVEN • Cost-Volume-Profit Analysis

Multiple Product Business and Sales MixThe break even point and target income point for a multiple product business

can be computed using equation 8. This equation requires that variable cost be expressed as a percentage of sales. A number of questions arise unique to multiple product business. One of these problems pertains to the fact that the sale of multiple products give rise to a sales mix ratio. The term sales mix refers to the ratio of the units sold for each product. If product A is sold at the rate of 10,000 units per year and product B at the rate of 20,000 per year, then the sales mix ratio is 1:2.

There are two methods for computing the variable cost percentage in a multiple product business. The first method was previously discussed and presented as equation 7

TVEv = ––––– S

The second method involves using the sales mix ratio and knowing the variable cost rates of each product: Mathematically, this method may be defined as follows:

∑ ViQiv = –––––––– (9) ∑ PiQi

i = 1, nWhere:

v - aggregate percentage variable cost Vi - variable cost rate of product i Qi - quantity of product i Pi - price of product iTo illustrate, assume the following:

Product A Product BPrice $12.00 $ 8.00Variable cost $ 8.00 $ 2.00Quantity 1,000 400Fixed cost $300 $1,000

Based on the above information, the variable cost percentage may be calculated as follows:

∑PiQi = 12(1,000) + 8(400) = 12,000 + 3,200 = 15,200

∑ViQi ) = 8(1,000) + 2(400) = 8,000 + 800 = 8,800

∑ ViQi 8,800v = ––––– = –––––– = .5789 ∑ PiQi 15,200

Changes in the Sales Mix RatioA number of questions arise concerning changes in the sales mix ratio:

1. Does a change in the sales mix ratio have an affect on the variable cost percentage?

2. Can a separate break even point be computed for each product?

Management Accounting | 127

3. Is the most profitable product the product with largest contribution margin?

4. Should the product that generates the highest volume of sales dollars also be the product that is promoted the most?

5. Is it possible for sales to increase and costs per unit to remain the same and yet for net income to decrease?

Effect of a Change in the Sales Mix Ratio on the Variable Cost Percentage Computing a break even point in a multiple product business is based on the assumption that the sales mix remains the same. In the above example, the sales mix ratio was 2.5 to 1. Based on this ratio, the break even point is:

1,300 1,300BEP = ––––––––––– = ––––––– = 3,087 1 - .5789 .4211

Suppose, in fact, the ratio become the opposite; that is 1:2.5. The variable cost percentage then becomes.

8.00(400) + 2.00(1000) 5,200v = –––––––––––––––––––– = ––––––––– = .40625 12.00(400) + 8.00(1000) 12,800

The break even point is now: 1,300 1,300BEP = –––––––– = ––––––––– = 2,189 1 - .40625 .59375

If a significant change is the sale mix ratio occurs, then the previous computation of the break even point based on the original sales mix is unreliable.Computing Break even Point for each Product - It is still possible to compute a break even point for each product separately; however, now care must be taken to not include common fixed costs in the total fixed costs for each product. Common fixed costs are those costs that occur whether or not the particular product is sold. For example, salaries to top management are most likely to be common in nature. Assuming there are no common costs in the fixed costs of products A and B, then the individual product break even points may be computed as follows:

Product A Product B

300 300 1,000 1,000BEP = ––––– = –––– = 900 BEP = –––––– = ––––– = 1,333 1 - .67 .33 1 - .25 .75

Contribution Margin Rate Differences - It is highly unlikely that the contribution margin rate of each product will be the same. The question is: will the product with the largest contribution margin rate be the most profitable? The answer is no. Net income also depends on the quantity sold. Because the contribution rate is the greatest, this is no guarantee that this product will even be profitable. Using the same data as previously, net income for products A and B may be computed as shown in Figure 7.7:

As can clearly be seen, product B which has a greater contribution margin rate

128 | CHAPTER SEVEN • Cost-Volume-Profit Analysis

($6.00 versus $4.00 for product A) is not the most profitable product. While product A does have the greater sales volume in dollars this does not mean that the product with the highest sales volume will be the most profitable. Profitability also depends on the contribution margin rate and the amount of fixed expenses. Increasing Sales, Constant Costs, and Decreasing Net Income - One of the unusual phenomenons in a business is that sales can be increasing and costs can be constant yet the business is experiencing a decrease in net income. This situation can happen when there is a substantial shift in the sales mix from the product with the greatest contribution margin rate to the products with a lower contribution margin rate.

To illustrate, assume that all costs remain the same in our example except that the sales mix becomes 1,100 to 300. Based on this mix, net income for each product may be computed as seen in Figure 7.8:

Figure 7.8 • Effect of a Change in Sales Mix Ratio

Product A Product B

Income Statement

Sales ($12 x 1,100) $13,200Variable expenses ($8 x 1100) 8,800 –––––––Contribution margin 4,400Fixed Expenses 1,000 –––––––Net income $ 3,400 ––––––– –––––––

Income Statement

Sales ($8 x 300) $2,400Variable expenses ($2 x 300) 600 ––––––Contribution margin 1,800Fixed Expenses 300 ––––––

Net income $1,500 ––––––– –––––––

Product A Product B

Income StatementSales ($12 x 1,000) $12,000Variable expenses ($8 x 1000) 8,000 –––––––Contribution margin 4,000Fixed Expenses 1,000 –––––––Net income $ 3,000 ––––––– –––––––

Income StatementSales ($8 x 400) $3,200Variable expenses ($2 x 400) 800 ––––––Contribution margin 2,400Fixed Expenses 300 ––––––Net income $2,100 ––––––– –––––––

Figure 7.7 • Effect of Different Contribution Margin Rates

Management Accounting | 129

Combined income then is:

Income Statement

Sales $15,600Variable expenses 9,400 –––––––Contribution margin 6,200Fixed Expenses 1,300 ––––––– Net income $ 4,900 ––––––– –––––––

Previously, combined sales was $15,200 ($12,000 + $3,200). Now combined sales is $15,600 ($13,200 + $2,400); however net income is now $4,900 ($3,400 + $1,500) whereas it was previously $5,100 ($3,000 + $2,100). Even though sales increased by $400, net income has decreased by $200. This decrease in net income happened despite that fact that price, the variable cost rates, and fixed costs remained the same.

A multiple product business requires close monitoring of the profitability of each product. General rules for managing and promoting each product based on price, variable cost rates and fixed cost are difficult to formulate. The computation of break even or target income point does not tell management which product will be become the most profitable. However, the effect of changes or shifts in the sales mix can easily be calculated.

The best approach to evaluating multiple products is to prepare segmental income statements. This management accounting tool is discussed in depth in chapter 15. A product that is not making a significant contribution to fixed expenses should be a candidate for discontinuance. If after all attempts to increase the segmental contribution have failed, the only course of action is to discontinue the product. Adding and discontinuing products is a constant and ongoing process. The role of the management accounting and the use of the appropriate management accounting tools becomes extremely important in a multiple product business.

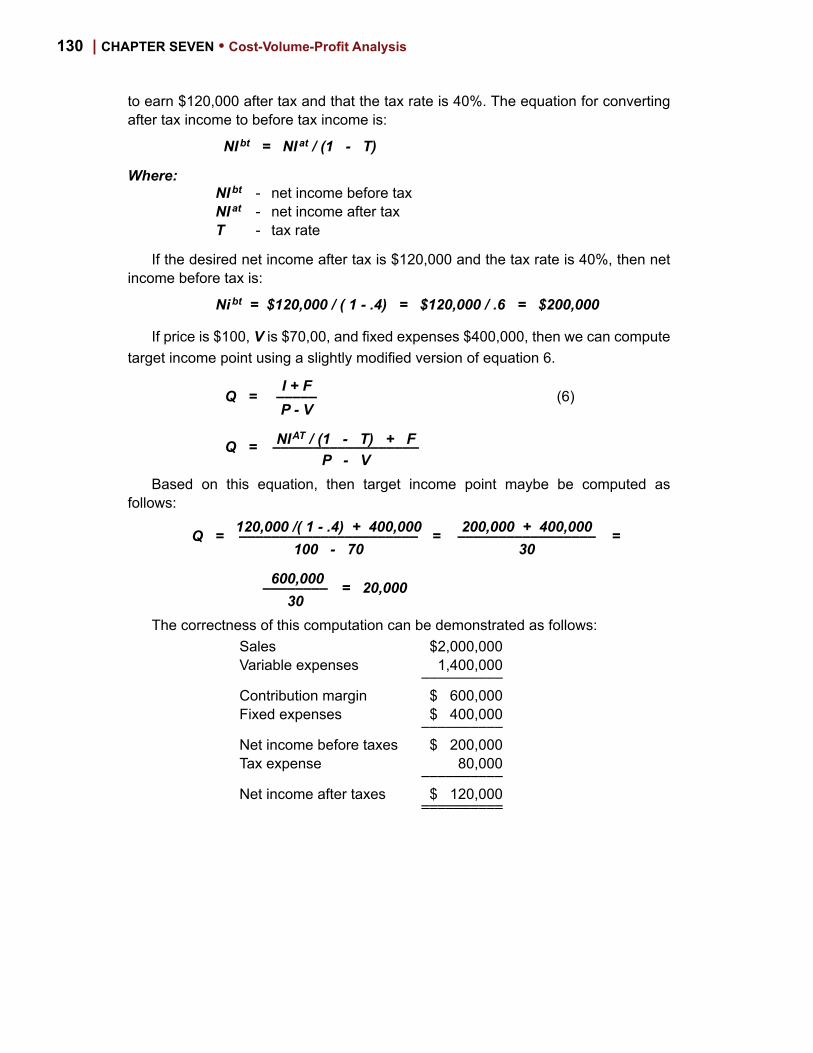

Computing Target Income Point After TaxesIn order to compute a target income point, it is necessary to specify the desired

level of income. However, the concept of net income is somewhat ambiguous. Net income can be before taxes or after taxes. Up to this point in this chapter, it has been assumed that the desired level of net income is net income before taxes, although this assumption was never explicitly made.

Net income after income taxes in many instances is more useful in making decisions. For example, a dividend policy is easier to formulate based on net income after taxes. Also, in planning cash flow, net income after taxes is more useful. However, net income before tax and after tax are obviously not independent of each other. In order to specify net income after tax as the goal in computing target income point, it is still necessary to know net income before tax. To illustrate, assume that the goal is

130 | CHAPTER SEVEN • Cost-Volume-Profit Analysis

to earn $120,000 after tax and that the tax rate is 40%. The equation for converting after tax income to before tax income is:

NI bt = NI at / (1 - T)

Where:NI bt - net income before taxNI at - net income after taxT - tax rate

If the desired net income after tax is $120,000 and the tax rate is 40%, then net income before tax is:

Ni bt = $120,000 / ( 1 - .4) = $120,000 / .6 = $200,000

If price is $100, V is $70,00, and fixed expenses $400,000, then we can compute target income point using a slightly modified version of equation 6.

I + FQ = ––––– (6) P - V

NI AT / (1 - T) + FQ = –––––––––––––––––– P - V

Based on this equation, then target income point maybe be computed as follows:

120,000 /( 1 - .4) + 400,000 200,000 + 400,000Q = –––––––––––––––––––––– = ––––––––––––––––– = 100 - 70 30

600,000 –––––––– = 20,000 30

The correctness of this computation can be demonstrated as follows:Sales $2,000,000Variable expenses 1,400,000 ––––––––––Contribution margin $ 600,000Fixed expenses $ 400,000 ––––––––––Net income before taxes $ 200,000Tax expense 80,000 ––––––––––Net income after taxes $ 120,000 –––––––––– ––––––––––

Management Accounting | 131

SummaryCost-volume-profit analysis is a powerful analytical tool. It can be effectively used

in many different kinds of decisions. Cost-volume-profit analysis is based on the theory of cost behavior and as such it is imperative that the management accounting and also management have a good understanding of cost behavior. Because cost-volume-profit analysis is based on a number of critical assumptions, it is also important to recognize when the use of this tool is valid and when it is not. If the data used in cost-volume-profit analysis extends too far beyond the relevant range, the results obtained can be inaccurate and misleading. Nevertheless, as long as the assumptions on which cost-volume-profit analysis is based hold true, then the tool can provide very useful information concerning decisions to be made and the evalu-ation of results already obtained.

Q. 7.1 Define the following terms:a. Fixed cost i. Contribution margin rateb. Variable cost j. Variable cost ratec. Semi-variable cost k. Break even pointd. Step cost l. Target income pointe. Average fixed cost m. Contribution margin income f. Average variable cost statementg. Relevant range n. Sales mixh. Contribution margin o. Net income before tax

Q. 7.2 Define the following mathematically.a. Salesb. Total variable costc. Total fixed costd. Net income

Q. 7.3 What are the two basic equations from which formulas for break even point or target income point may be derived?

Q. 7.4 Explain how cost-volume-profit analysis may be used as a tool for decision-making. (Give several examples.)

Q. 7.5 What are the basic assumptions that underlie cost-volume-profit analysis?

Q. 7.6 What equation may be used to answer the question: how many units must be sold in order to attain a desired level of net income?

What equation may be used to answer the question: how many dollars of sales are required in order to attain a desired level of net income?

Q. 7.7 Draw a graph illustrating break even point. On this chart, show total sales, total variable cost, and total fixed costs. Shade in the areas of net loss and net income.

132 | CHAPTER SEVEN • Cost-Volume-Profit Analysis

Q. 7.8 Define the following mathematical expressions:

a. P(Q) - V(Q)b. P - Vc. 1 - vd. Q(P - V )

Q. 7.9 If total contribution margin is $100,000 and fixed expenses is $80,000, then the difference ($100,000- $80,000 = $20,000) is called?

Q. 7.10 When total fixed expenses equals total contribution margin, then this point is called?

Q. 7.11 What effect do the following changes have on break even point:

a. Increase in priceb. Decrease in pricec. Increase in the variable cost rated. Decrease in the variable cost ratee. Increase in fixed expenses f. Decrease in fixed expenses

Q. 7.12 What assumption must be made in order to use cost-volume-profit analysis in a multiple product business?

Q. 7.13 What effect does a change in the sales mix ratio have on the variable cost percentage?

Q. 7.14 Assume a business has three products. What equation may be use to compute the variable cost percentage?

Q. 7.15 Draw a chart that illustrates the use of this equation:

I = P(Q) - V(Q) - FNote: ( use only one line to prepare this chart)Explain how this chart shows break even point.

Q. 7.16 Given that price, the variable cost rates, and fixed costs have not changed, explain how net income can decrease even though total sales has increased.

Management Accounting | 133

Exercise 7.1 • Contribution Margin Income Statement

The management accountant has done an analysis of costs and has arrived at the following cost-volume-profit analysis data based on general ledger information for the year ended December 31, 20xx.

Sales $ 100,000Variable expenses Selling $ 20,000 General and administrative $ 10,000 Cost of goods sold $ 50,000Fixed Selling $ 5,000 General and administrative $ 2,000 Cost of goods sold $ 10,000

Units sold 1,000Desired level of income $ 50,000

Required:

1. Prepare a contribution margin income statement.

2. Determine the units that must be sold to attain the desired level of net in-come.

Exercise 7.2 • Preparing a Break even Graph

Based on the following information, prepare a break even chart.Price $ 80.00Variable cost rate $ 60.00Fixed expenses $ 50,000Desired net income $ 80,000

Exercise 7.3 • Contribution Margin Income Statement

Income Statement(Sales - 10,000 units)

Sales $200,000Expenses $150,000 ––––––––Net income $ 50,000 –––––––– ––––––––

134 | CHAPTER SEVEN • Cost-Volume-Profit Analysis

It has been determined that of the $150,000 of expenses, $100,000 were fixed. The desired company net income is $150,000.Required:

1. Based on the above information, prepare a contribution margin income statement.

2. Answer the following:

a. Contribution margin per unit of product ––––––––––––––––––––

b. Variable cost rate ––––––––––––––––––––

c. Total desired contribution ––––––––––––––––––––

d. Break even point ––––––––––––––––––––

e. Target income point ––––––––––––––––––––

––––––––––––––––––––Exercise 7.4 • Cost-Volume-Profit Relationships

Cost-Volume-Profit Chart$

A

B

C

D

E

IK

J M

NL

G

F H

Q

Based on the above cost-volume-profit chart, identify the following line segments: Line Segments

–––––––––––––––1 A - B –––––––––––––––––––––––––––––––––––––––––2 C - D –––––––––––––––––––––––––––––––––––––––––3 E - F –––––––––––––––––––––––––––––––––––––––––4 G - H –––––––––––––––––––––––––––––––––––––––––5 I - J –––––––––––––––––––––––––––––––––––––––––6 K - L –––––––––––––––––––––––––––––––––––––––––7 M - N –––––––––––––––––––––––––––––––––––––––––

Management Accounting | 135

Exercise 7.5 • Computing New Target Income Point

The owner of the Brown Retail Company believes that current sales volume is less than potential because of inadequate advertising. He has tentatively decided to increase his advertising budget by $2,000. Last year’s income statement was as follows:

Sales (1,000 units @ $20.00) $20,000Variable expenses $10,000 –––––––Contribution margin $10,000Fixed expenses $ 6,000 –––––––Net income $ 4,000 ––––––– –––––––

Advertising, if increased, will change from $2,000 to $4,000. The maximum market potential is probably between 1,300 and 1,400 units of product.Required: Evaluate this proposed increase in advertising. To offset the increase in advertising, by how much must sales increase in units.

Exercise 7.6 • Computing Break even point and Target Income Point

The following information from the records of the Ajax Manufacturing Company has been provided to you:

Sales price: Product A $ 60.00 Product B $ 40.00 Product C $ 100.00

Variable costs: Product A $ 45.00 Product B $ 30.00 Product C $ 40.00

Units sold: Product A $ 1,000 Product B $ 2,000 Product C $ 3,000

Fixed costs for each product was determined as follows: Product A $ 40,000 Product B $ 30,000 Product C $ 80,000

Common fixed costs of the business are $200,000.

136 | CHAPTER SEVEN • Cost-Volume-Profit Analysis

Required:1. Compute the variable cost percentage for each product.2. Compute the contribution margin percentage for each product.3. Compute the break even point of each product.4. Compute the break even point of the business as a whole.5. Explain how it is possible for each product to break even yet the business

as a whole is operating at a loss. 6. Suppose the sales mix ratio rather than 1:2:3 becomes 3:1:2. How would

this change in the sales mix ratio affect the variable cost percentage?

Exercise 7.7 • Computing Target Income Point After Taxes

The Acme Manufacturing Company income statement for the year ended was as follows:

Sales (10,000 units) $ 200,000Variable expenses 120,000 _______Contribution margin $ 80,000Fixed expenses 60,000 _______Net income $ 20,000Tax expense 8,000 _______Net income after taxes $ 12,000 _______ _______

Required:The company would like to have an after tax income of $50,000. What level of sales is required to attain this level of after tax net income?