paper- indian textile & apparal industry

TRANSCRIPT

8/2/2019 Paper- Indian Textile & Apparal Industry

http://slidepdf.com/reader/full/paper-indian-textile-apparal-industry 1/13

Textile & Apparel Industry

Building SustainableBusinesses in the Growing

Domestic Market

8/2/2019 Paper- Indian Textile & Apparal Industry

http://slidepdf.com/reader/full/paper-indian-textile-apparal-industry 2/13

Building Sustainable Businesses in the Growing Domestic Market |

Current Status of Indian Textile & Apparel Market 01

Evolving Indian Consumers and ChangingConsumption Patterns 02

Some Opportunities in Domestic Apparel Market 06

Strategies to Develop Competitive andSustainable Businesses 12

Conclusion 17

About Technopak 18

Contents

8/2/2019 Paper- Indian Textile & Apparal Industry

http://slidepdf.com/reader/full/paper-indian-textile-apparal-industry 3/13

| Building Sustainable Businesses in the Growing Domestic Market

Current Status o IndianTextile & Apparel MarketOverviewThe present size of Indian Textile and Apparel market is US$ 62 Billion out of which US$ 22 Billion iscontributed by exports while the rest US$ 40 Billion is domestic market.

Growing Textile and Apparel ExportsExports in Textiles and Apparel have registered a strong growth in the last few years with 11% CAGR from2004-05 to 2007-08. The single largest category is woven apparel followed by knitted apparel, made-upsand cotton based textiles.

Growing Domestic MarketIndian domestic textiles and apparel market is one of the fastest growing market in the world and offershuge market potential for textile and apparel manufacturers. It is expected to become one of the majorconsumption bases in near future. Out of the total market size of US $ 40 Billion, Clothing contributes US$ 30 Billion, while rest US$10 billion is contributed by Textiles (Home textiles, Technical textiles and othertextiles end-uses). The domestic market has shown a significant growth in past few years registering aCompounded Annual Growth Rate (CAGR) of ~13%. Despite the recent demand slump, the domesticmarket is expected to grow at around 9% in the next 5 years.

In this context , the industry needs to focus on the domestic market more intensely and understand themarket dynamics in more detail in order to tap the complete poten tial. Further we discuss these opportunitiesfor Indian textile and apparel companies in the domestic market and strategies for developing sustainablebusinesses with the changing requirements of the domestic market.

0

10

20

30

40

50

2006 2007 2008

2226

30

36

48

2004-05 2005-06 2006-07 2007-08

Woven Apparel

2011 2014

1 3 %

9 %

0

5

10

15

20

25

Knitted Apparel

Made-Ups

Cotton Products

Synthetics Products

Other Textile Products

U S $

B i l l i o n

U S $

B i l l i o n

2

14.3

22.4

22

3

4

22

23

3

5

1 1 % C A G

R

5

4

2

4

22

5

4

2

5

32

India export marketIndia domestic market

Source: UN Comtrade, Technopak Analysis, Values rounded off

Evolving Indian Consumersand Changing ConsumptionPatterns

Indian Textile and Apparel MarketUS $ 62 Billion

INR 265,500 Crore

TextilesUS $ 10 Billion

INR 43,500 Crore

ClothingUS $ 30 Billion

INR 128,500 Crore

TextilesUS $ 12 Billion

INR 50,000 Crore

ClothingUS $ 10 Billion

INR 43,500 Crore

Domestic Market

US $ 40 BillionINR 172,000 Crore

Exports

US $ 22 BillionINR 93,500 Crore

8/2/2019 Paper- Indian Textile & Apparal Industry

http://slidepdf.com/reader/full/paper-indian-textile-apparal-industry 4/13

| Building Sustainable Businesses in the Growing Domestic Market Building Sustainable Businesses in the Growing Domestic Market | 4

be used. While in 1991, consumption was more onbroader basic requirements, it is now focused onlifestyle and aspirational products.

More importantly, there are shifts occurring in theconsumption basket away from the traditionalspending categories such as apparel, homefurniture & furnishings categories and consumerelectronics. Both telecom and domestic transportspending are now in the top 5 consumer spendingcategories, while travel has also becomesignificant.

It is thus seen that new categories of consumptionare taking up share of wallet and their markets in

India have crossed the Rs.100,000 crore markreflecting huge opportunity. These categories onwhich consumers are spending more on are

Education (including training and coaching)•

Healthcare (reactive and preventive)•

Food services (Restaurants, Ready-To-Cook and Ready-to-eat)•

Home IT (Hardware, Software, Internet, Gaming) and mobiles•

Travel and tourism•

What does it mean for the Indian apparel market?New categories such as mobiles, education, healthcare etc are moving faster than textile and apparelbecause while the consumer still associates apparel with his basic need, the other categories areaspirational. His desire to blend in to the global environment is pushing him to spend more on non apparelcategories. Though the overall size of the apparel market is still growing at 9% CAGR and the aspirationalapparel category has the potential to grow much faster. Hence, Apparel will have to re-define itself in a newavatar to appeal to this evolved consumer i.e. as a category that fulfills a desire rather than a need.

Understanding catalysts of change that are propelling IndiaIndia has been witnessing sustained high growth of GDP since 1991 of ~ 6% per year leading tofundamental transformation of the economy. There are many growth drivers for these changes includefavorable demographics, dropping dependency ratio and rapidly rising education levels. A check on thelatest demographics show us a growing opportunity:

Predominantly young consumers: 72% of Indian population constitutes of people below 39 years, with•

32% between 20-39 years having high consumption potential.

Literacy rate to touch almost 90% by 2013 from present 70%; with female literacy touching 83% from•

present 69%

Dependency ratio reducing with 13 million new people join the workforce every year.•

Besides demographics, there is also a very promising broad-basing of economic activity geographicallyas well as into the various components of the gross domestic output . There is also a broad-basing of thenature of jobs that match the current skill sets of the population and this is helping in spreading out the

positive effect of economic growth.

What does the new Indian consumer want: Local preferences with a global appealIndian consumer is evolving and need based consumption categories have become low-involvement itemsfor the “core” consuming classes.

Spending is shifting from basic to discretionary. As has been already illustrated above, the share of food•

and grocery in the consumer’s wallet continue to drop – releasing money for discretionary expenditure.F&G share expected to decline from 36% in 2008 to 32% in 2013

The ‘shift to thrift’ is redefining value – in terms of price, brand and quality. Increasingly values the money•

earned; therefore product offer is not only about good pricing, but also about quality, convenience,

consistency, innovation, experience

Product needs to fulfill not just a basic need, but an aspiration. It necessarily does not need to be•

expensive or branded, however it should address the ‘Desire’ – the intangible sense of success or thepromise of success

Family ties are still the most important factor in an Indian’s life though family structures and how time is•

spent together is changing. Families are turning nuclear and children have become a focal point of allshopping and purchase decisions. Shopping & Eating Out remain top family leisure activities. With timepoverty, shopping with family helps increase time shared with family

Indian consumers waking up to their aspirations beyond basic needs Against the above backdrop of positive changes in demographics and economic activity, we are lookingat a consumer who has the capacity to spend, wants to spend and now has more options to spend. Theconsumption basket is expanding to include many more products on which discretionary income can

40% 36%32%

20% 20%20%

27%30% 32%

2003 2008 2013

9%10% 11%

4%4%

5%

Food & Grocery Rent, Utilities & Education Fuel, Transport & Communication

Savings & Investment Discretionary Expenditure

Increasing discretionary expenditure

Source: India Consumer Trends, Technopak analysis

~ 500 Million consumers (excluding BPL families)across Urban and Rural India (18+ years)

~ 270 Million in Rural India

~ 230 Million in Urban India

~ 80 Million in the top 100 cities

~ 75 Million in the top 70 cities

~ 45 Million in top 30 cities

~ 30 Million in the top 8 cities

Retail Categories Size (in Rs Cr)

Food & Grocery 1,250,000

Healthcare 1,65,000

Apparel & Home Textiles 1,40,000

Telecom 1,20,000

Jewelry & Watches 1,18,000

Personal Transport (Vehicles+Fuel+Repairs) 1,15,000

Travel and Leisure 60,000

CDIT 55,000

Home - Furniture, Furnishing etc 50,000

Personal Care 48,000

Eating out 24,000

Footwear 19,000

Health & Beauty Services 4,000

Source: Technopak Analysis

8/2/2019 Paper- Indian Textile & Apparal Industry

http://slidepdf.com/reader/full/paper-indian-textile-apparal-industry 5/13

Some Opportunities inDomestic Apparel Market

8/2/2019 Paper- Indian Textile & Apparal Industry

http://slidepdf.com/reader/full/paper-indian-textile-apparal-industry 6/13

| Building Sustainable Businesses in the Growing Domestic Market Building Sustainable Businesses in the Growing Domestic Market | 8

Segments with High Growth PotentialIt is evident that the Indian consumer is ready for change, demanding options and looking out for productthat suits and matches their needs and aspirations. With the back drop of changes, Indian apparel marketis moving away from the traditional segmentation to a much deeper and wider segmentation based onconsumer needs. Indian apparel market can be broken up into men, women and kids, but within eachthere are a number of segments that are emerging reflecting changing needs. Some of the segments thatare potential opportunities to watch out for are:

Women’s wear1.

Casual wear2.

Kids wear3.

School Uniforms4.Inner wear5.

Plus size clothing6.

Active wear / Exercise wear / Swimwear7.

Youth fashion / College fashion8.

All above segments are discussed further in detail:

1. Women’s WearWomen’s formal wear and ethnic wear markets are still ruled by unorganized players. With more womenexpected to enter corporate world, both these segments are good opportunities because of the marketsize

2. Casual WearCasual wear segments are expected to growbetween 10-15% as compare to 9% growth ofoverall Indian Apparel Market. More than 50% of theclothes in this category are bought by youth (age13-30)Increase of buying frequency of casual wear isspurred by:-

Preference for more comfort wear•

Increase in employability•

Acceptance of Casual wear in work places•

Casual wearMen's(Rs Crores)

Women’s(Rs Crores)

Shirts 3290 690

Trousers 2280 150

T-Shirts 3300 1330

Jackets 560 90

Sweaters 130 100

Jeans 2840 1240

TOTAL 12400 4600

Source: Technopak Analysis

2008 Casual Wear Market

(INR ‘000 Crore)

Casual

Men

Women

Children

12

5

6

3. Kids wearKids wear is a major category with few established players. Very few brands namely Lilliput, Gini andJony, Catmoss, Benetton, Disney, Barbie. Some brands have extended into this category though not verysuccessfully i.e. OYO by Spykar, Zapp by Raymond(closed down). It still holds a large opportunity which isclearly untapped.

4. School UniformsScope in organized retail of good quality uniforms is very high with very few organized players in this highgrowth potential segment

Uniforms form almost 40% of the Rs. 32,000 Crore Kids wear market in India. With literacy rates increasingand the private education market estimated at Rs. 172,000 crore, uniforms form an essential part of theapparel market

The impetus will come not only from sheer numbers at the lower price brackets, but from the rise of highend schooling education in the form of world schools and international schools .Present state of the market in this category

This category is highly fragmented and unorganized with hardly any large players. SKNL, is the only•

organized player and they are able to cater to a small part of the market.

Uniforms available are sub-standard quality of stitching and lack standardization•

Shopping for uniforms is a bad Shopping experience and uniform retailers are found in very low key•

markets

Internationally, most brands like Marks and Spencer, Next , JC Penny have brand extensions into uniformswhile there are some standalone uniform brands like K-12 gear, Academy Uniforms, First In Class etc

5. Inner wearInner wear market in India, estimated at Rs 14,000 Crores, is largely unorganized with more than 75%of the industry dominated by unorganized indigenous players. However there is a growing awareness ofphysical appearances among consumers leading to demand for more variety and designs which is drivingthe organized market growth. Some of the bott lenecks for growth of innerwear and subsequent opportunityfor modern retailers include:

Lack of innovation and product differentiation in this product•

Lack of standard sizing•

Low penetration and distribution levels•

Ethnic wear 47%

CasualMarket22%Party

Marker 1%

Nightwear 17%

FormalMarket13%

2008 Women’s wear Market of SEC

A&B is INR 25,300 Crore Urban Women’s Wear Market

64%

61% 52%62%

67% 51% 50% 47%

14%

86%

53%50%33%

36%

48% 49%

95%

5%

95%

5%

36%

64%

36%

39%

E t h n i c W e a r

S a r e e s

P e t i c o

a t s

B l o u s e s

T - s h i r t

W o v e n s h i r t s

L i n g e r i e

W o o l e n s

N i g h t w

e a r

J e a n s

W e s t e r n S u i t s

T r o u s e r s / S k i r t s

Urban-Branded Urban-Unbranded Source: Technopak Analysis

Inner wear Market Rs. 14,000 CroreKids wear Market Rs. 32,000 Crore

Women’sInner wear

8500

Men’sInner wear

5500

Source: Technopak Analysis

100%

80%

60%

40%

20%

0%I-BodySuits

I-T-shirts T-shirts Lowers Jeans Ethnicwear

Frocks

Low Economy Medium Premium Super Premium

8/2/2019 Paper- Indian Textile & Apparal Industry

http://slidepdf.com/reader/full/paper-indian-textile-apparal-industry 7/13

| Building Sustainable Businesses in the Growing Domestic Market Building Sustainable Businesses in the Growing Domestic Market | 10

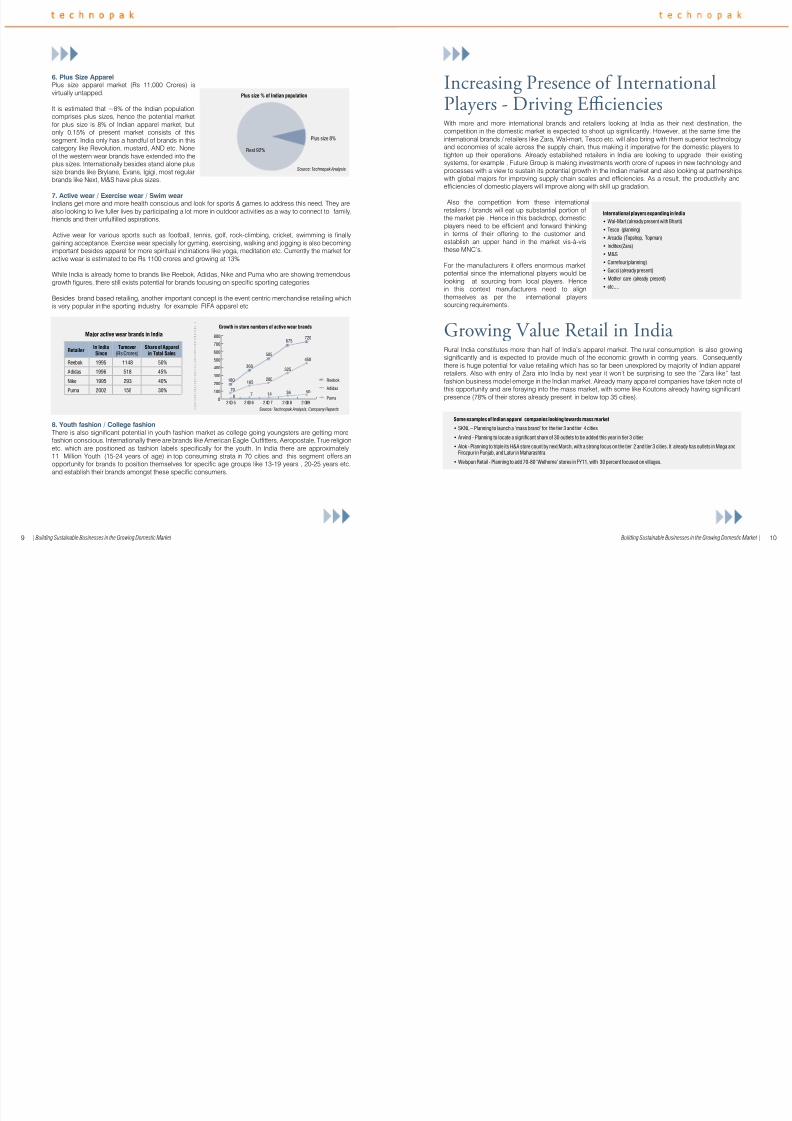

Increasing Presence o InternationalPlayers - Driving EfcienciesWith more and more international brands and retailers looking at India as their next destination, thecompetition in the domestic market is expected to shoot up significantly. However, at the same time theinternational brands / retailers like Zara, Wal-mart, Tesco etc. will also bring with them superior technologyand economies of scale across the supply chain, thus making it imperative for the domestic players totighten up their operations. Already established retailers in India are looking to upgrade their existingsystems, for example , Future Group is making investments worth crore of rupees in new technology andprocesses with a view to sustain its potential growth in the Indian market and also looking at partnershipswith global majors for improving supply chain scales and efficiencies. As a result, the productivity andefficiencies of domestic players will improve along with skill up gradation.

Also the competition from these internationalretailers / brands will eat up substantial portion ofthe market pie . Hence in this backdrop, domesticplayers need to be efficient and forward thinkingin terms of their offering to the customer andestablish an upper hand in the market vis-à-visthese MNC’s.

For the manufacturers it offers enormous marketpotential since the international players would belooking at sourcing from local players. Hencein this context manufacturers need to alignthemselves as per the international playerssourcing requirements.

Growing Value Retail in IndiaRural India constitutes more than half of India’s apparel market. The rural consumption is also growingsignificantly and is expected to provide much of the economic growth in coming years. Consequentlythere is huge potential for value retailing which has so far been unexplored by majority of Indian apparelretailers. Also with entry of Zara into India by next year it won’t be surprising to see the “Zara like” fastfashion business model emerge in the Indian market. Already many appa rel companies have taken note of

this opportunity and are foraying into the mass market, with some like Koutons already having significantpresence (78% of their stores already present in below top 35 cities).

6. Plus Size ApparelPlus size apparel market (Rs 11,000 Crores) isvirtually untapped.

It is estimated that ~8% of the Indian populationcomprises plus sizes, hence the potential marketfor plus size is 8% of Indian apparel market, butonly 0.15% of present market consists of thissegment. India only has a handful of brands in thiscategory like Revolution, mustard, AND etc. Noneof the western wear brands have extended into theplus sizes. Internationally besides stand alone plussize brands like Brylane, Evans, Igigi, most regularbrands like Next, M&S have plus sizes.

7. Active wear / Exercise wear / Swim wearIndians get more and more health conscious and look for sports & games to address this need. They arealso looking to live fuller lives by participating a lot more in outdoor activities as a way to connect to family,friends and their unfulfilled aspirations.

Active wear for various sports such as football, tennis, golf, rock-climbing, cricket, swimming is finallygaining acceptance. Exercise wear specially for gyming, exercising, walking and jogging is also becomingimportant besides apparel for more spiritual inclinations like yoga, meditation etc. Currently the market foractive wear is estimated to be Rs 1100 crores and growing at 13%.

While India is already home to brands like Reebok, Adidas, Nike and Puma who are showing tremendousgrowth figures, there still exists potential for brands focusing on specific sporting categories

Besides brand based retailing, another important concept is the event centric merchandise retailing whichis very popular in the sporting industry, for example FIFA apparel etc

8. Youth fashion / College fashionThere is also significant potential in youth fashion market as college going youngsters are getting morefashion conscious. Internationally there are brands like American Eagle Outfitters, Aeropostale, True religionetc. which are positioned as fashion labels specifically for the youth. In India there are approximately11 Million Youth (15-24 years of age) in top consuming strata in 70 cities and this segment offers anopportunity for brands to position themselves for specific age groups like 13-19 years , 20-25 years etc.and establish their brands amongst these specific consumers.

Plus size % of Indian population

Plus size 8%

Rest 92%

Source: Technopak Analysis

International players expanding in India

Wal-Mart (already present with Bharti)•

Tesco (planning)•

Arcadia (Topshop, Topman)•

Inditex (Zara)•

M&S•

Carrefour (planning)•

Gucci (already present)•

Mother care (already present)•

etc....•

0

100

200

300

400

500

600

700

800

180

360

2 00 5 2 00 6 2 00 7 2 00 8 2 009

505

675720

70

165

7 14 36 50

200

325

450

0

Growth in store numbers of active wear brands

Reebok

Adidas

Puma

Source: Technopak Analysis, Company Reports

RetailerIn IndiaSince

Turnover(Rs Crores)

Share of Apparelin Total Sales

Reebok 1995 1148 50%

Adidas 1996 518 45%

Nike 1995 293 40%

Puma 2002 158 30%

Major active wear brands in India

Some examples of Indian apparel companies looking towards mass market

SKNL – Planning to launch a ‘mass brand’ for the tier 3 and tier 4 cities•

Arvind - Planning to locate a significant share of 30 outlets to be added this year in tier 3 cities•

Alok - Planning to triple its H&A store count by next March, with a strong focus on the tier 2 and tier 3 cities. It already has outlets in Moga and•Firozpur in Punjab, and Latur in Maharashtra.

Welspun Retail - Planning to add 70-80 ‘Welhome’ stores in FY11, with 30 percent focused on villages.•

8/2/2019 Paper- Indian Textile & Apparal Industry

http://slidepdf.com/reader/full/paper-indian-textile-apparal-industry 8/13

| Building Sustainable Businesses in the Growing Domestic Market

Subsequently, this means a huge opportunity for Indian textile and apparel manufacturers to look towardscatering to the domestic value market . For manufacturers this means more emphasis on fashion at lowprices. Hence firms need to take designing more seriously along with improving operational efficiencies.Companies also need to establish strong supply relationships with these upcoming “value retailers” tobecome first partners of choice for their fast fashion requirements.

C e n t r a l

B i g

B a z a a r

L i f e s t y l e

P a n t a l o o n

R a y m o n d

K o u t o n s

W i l l s

L i f e s t y l e

F a b I n d i a

W e s t s i d e

S h o p p e r s

s t o p

10

7

40%

35% 33%

8%5%

41%

46%67% 64%

39%

11%

45%78%

10%

32%

51% 44%

29%

12%

15%7%

8%10%1%

9%

20%

25%

9%

31%

49%

30%

26%

9%50%

10%

113

58

27

9

37

19

18

8

45

22

402

184

~1400

~500

41

18

104

38

No. of store

No. of cities

Top4 Top15 Top35 Others

Hypermarkets Department stores / large format stores Exclusive stores

% share of retail presence across various cities

Strategies to DevelopCompetitive and SustainableBusinesses

8/2/2019 Paper- Indian Textile & Apparal Industry

http://slidepdf.com/reader/full/paper-indian-textile-apparal-industry 9/13

| Building Sustainable Businesses in the Growing Domestic Market Building Sustainable Businesses in the Growing Domestic Market | 14

There are also many successful examples of innovation at various levels from other industries that thetextile industry can get inspired from. Some of these examples are discussed below:

Innovation in other industries

Adopting Global Best PracticesCompanies also need to adopt best management practices like lean manufacturing , Kaizen, six sigmaetc. for improving overall efficiencies and productivity. This would not only improve the financial returns forcompanies but also make them more cost competitive in the market. In this textile and apparel companiescan take a cue from other industries in reaping respective benefits of best management practices. Someof these examples are given below:

Providing Value Added Services &Developing Niche PositioningService OrientationWith the growing domestic market and growing presence of international retailers suppliers need to alignthemselves as per requirements of the retailers. The big retailers would also be looking at sourcing fromestablished partners in the supply chain and would be expecting certain pre requisites from their suppliers.In this regard suppliers need to look at integrating and offering value added services to retailers like design,logistics, warehousing etc. in order to establish long term supply chain partnerships. Particularly logisticsand warehousing play a significant role in the Indian domestic market due to the long distances betweensupply bases and markets, and suppliers should look towards working closely with retailers in these areas.

Also textile and apparel companies should look at investing in IT and developing linkages across thesupply chain for driving efficiencies.

Niche PositioningWith growing specialization at the retail level, suppliers should also look at developing niche / specializedproduct competencies and offer customized solutions for respective retailers / brands based on theirspecific requirements. For example, an upmarket brand might be looking at large product depth / variety,while a value retailer would be looking at basic products but with high fashion content. Hence suppliersneed to position themselves appropriately and develop these specific skills in order to serve the specificrequirements of their buyers.

Innovating to “Survive”With increasing global competition and evolvingconsumerism it is slowly becoming a must for textilemanufacturer to be innovative. Firms need to exploreinnovation both in terms of processes, marketing andproducts. Activities like R&D and designing shouldbe treated as key success factors and a pre-requisiterather than an afterthought. Apart from process basedinnovations companies should also not shy awayfrom exploring new business models in the context ofthe ever changing consumption space. In this regardthere are many apparel companies who have already realized the importance of “business” innovation to“survive” in the increasingly competitive market place and are looking to differentiate their product offeringacross various levels.

Hug Shirt by Cute Circuit – Product innovation in apparel

Cute Circuit, based in UK, is a Fashionable Technology company that creates design excellence in the fields of Wearable Technology and•Interaction Design. The company has developed a shirt called The Hug Shirt™ - a shirt that makes people send hugs over distance.

It’s a smart textile product with sensors embedded in the shirt that feel the strength of the touch, the skin warmth and the heartbeat rate of• the sender and actuators that recreate the sensation of touch, warmth and emotion of the hug to the shirt of the distant loved one.

The Hug Shirt™ was nominated as one of the best Inventions of 2006 by Time Magazine.•

Price and Design InnovationTata Nano: By now Tata Nano has become a

household name. The “World’s Cheapest Car” byTata is a supreme example of innovation in priceand design and is an inspiration for other industries

to strive for similar objectives and results.

Suppy Chain InnovationStarted in the year 1984, Suguna poultry is today, a leading poultry Company in

India with a steadily increasing global presence. Its turnover exceeded Rs 2000crores in 2007-08. It’s pioneering efforts in contract farming have helped thousandsof farmers to grow along with the company. Suguna has reduced the number ofmiddle men in Trading, Feed Supplies, Medicine Supplies, Chick Supplies etc., bydirectly supplying all the above to farmers. Innovative use of IT has also helped

the company streamline its supply chain - a first of its kind in the poultry farmingindustry.

Manufacturing InnovationJain Irrigation is the pioneer of Micro Irrigation systems in India. It is the largest irrigation company in India & the only manufacturer ofcomplete drip irrigation systems in the world. In addition to the irrigation business, it is the largest manufacturer of Plastic pipes. Due to itssustained efforts, today it has a presence in 110 countries with a turnover of US $ 456 million . It has grown at a rate of 41% CAGR for thelast 5 years. Thus, because of its thrust on manufacturing innovation & having a global outlook, it has managed to grow phenomenally.

Best management practices in other industriesCompanies in other industries have been very active in implementing best management practices like lean manufacturing / six sigma etc helping

them achieve significant gains. Textile companies also need to get active in implementing these best practices to put themselves in a better position in the long term. Some of the examples of companies gaining from these are given below:

AsianPaints•madesavingsofmorethanRs20croresinayearafterimplementingoneSixSigmaproject.Capacitiesattheirmanufacturing•plants increased by more than 100% without any capital investment.

Wipro was able to save more than Rs 100 crores due to implementation of lean manufacturing / six sigma.•

Bharti Broadband made productivity enhancements, improved customer satisfaction and process effectiveness by implementing Six Sigma.•

Some prominent practitioners of Six Sigma processes are ICICI Bank, ITC and Reliance Industries. Also a whole host of BPOs like ICICI•OneSource and WNS have adopted Six Sigma processes as part of the service level agreements. Many other large Indian companies suchas HCL and Tata Motors have also adopted lean manufacturing principles very successfully

Examples of textile and apparel companieslooking to innovate

Ar vi nd Ltd . Pr oduc tinnovation

Planning to develop denim salwar-kameez and, maybe sarees toexpand in the rural market

RBR Garments Productinnovation

Producing 'novel' garmentsusing varied fabrics and fibre likeminerale fibre, soya bean fibre etc.

Levi's Marketinginnovation

Selling Jeans on EMI scheme

Need for specialized positioning :customized solutions

Value added Jeans supplier Formal shirts manufacturer Value fashion supplier Private label supplier Kids wear manufacturer etc..

One stop solution

Forecasting

Designing

Manufacturing Retailers / brands

Logistics

Warehousing

M a n u f a c t u r e r s

IT Linkages

Supply chain partnership

8/2/2019 Paper- Indian Textile & Apparal Industry

http://slidepdf.com/reader/full/paper-indian-textile-apparal-industry 10/13

| Building Sustainable Businesses in the Growing Domestic Market Building Sustainable Businesses in the Growing Domestic Market | 16

consumers in the other countries get aware of sustainability issues, it is going to put tremendous pressureon Indian manufacturers to comply. The young consumer is moving from the industrial economy to thesustainable economy and manufacturers/retailers globally have to build that into our processes. Hence companies need to gear up towards going green and give more weightage to environmentalfriendliness going forward.

Leveraging FTA’sHistorically, Free Trade Agreements have played a significant role in determining trade dynamics acrossthe World. Many trade agreements like NAFTA, EFTA, AGOA, GSP benefits have been instrumental indeveloping the textile and apparel industry of respective countries. India has also established a few tradeagreements with countries like Sri Lanka, Thailand, ASEAN etc. and further negotiations are in progress

with many countries like EU, Australia, Japan etc.

The major benefits of these FTA’s include:

Decreased sourcing costs of key products included in the agreements•

Availability of variety of products for the domestic market•

Hence it is important for firms to keep track of these agreements and understand the key benefits thatcan be leveraged from the respective countries both in terms of sourcing as well as marketing in thosecountries.

Developing ManpowerWith so many new industries growing like telecom, IT , automobiles, banking etc., one of the challengesfor the industry today is attracting skilled and qualified manpower and staff to work in the textile industry.While, many of the big textile companies regularly recruit from major textile institutes in technical grade(engineering, design, merchandising), there is still a general lack of interest amongst most of the Managerialgrade students joining the industry. In this except for a few big firms like ITC, A rvind etc. not many companieshave been able to recruit students from premier MBA/ Engineering institutes like IIM / IIT.

The industry needs fresh and innovative thoughts to improve its existing work practices and drive efficienciesin manufacturing and supply chain. The best way to do this is by reaching out to the young managerialtalent and give them the right ‘incentives’ to join the T&A industry.

T&A companies also need to increase the industry-academia interaction to nurture talent at the base level

and for other purposes also like Research & Development, training existing staff in best practices etc.The industry needs to reach out to the academia and in this regard can take cue from companies in otherindustries which are collaborating with academia in many ways.

Such industry- academia interaction helps in developing affinity for students to work in the industry infuture. There are 103 textile institutes in India along with 118 National Institutes of Fashion Technology,which can be tapped for this purpose.

The industry must make best efforts to attract higher and highest quality talent – at all levels – to providethe intellectual backbone for engineering a renaissance for itself in the next 10 years

Environmental Sustainability Environmental sustainability is the ability to maintain the qualities that are valued in the physical environment.It is clearly emerging that the world’s coastline and watersheds are increasingly affected by economicchanges and environmental degradation, consumers have become edgy about the effect of human activityon the environment. In such a scenario, environment sustainability has become an industry in itself.

With increasing concerns regarding the effect of the textile industry on the environment, at all stages of itschain, i.e. raw material, fiber, fabric, apparel, processing; more and more textile researchers, producersand manufacturers are looking to biodegradable and sustainable fibers as an effective wa y of reducing theimpact textiles have on the environment.

More and more people are now focusing on the responsibility of industry and consumer priorities, andintroducing new measuring tools for electricity and water usage, carbon footprint and traceability. As

Country Status

ASEAN Concluded

Sri Lanka Concluded

Thailand Concluded

S. Korea Concluded

Singapore Concluded

Chile Concluded

SAFTA Concluded

Afghanistan Concluded

Bhutan Concluded

Mercosur PTA Concluded

Turkey Negotiating

Australia Negotiating

New zealand Negotiating

GCC Negotiating

Taiwan Negotiating

EU Negotiating

US Negotiating

India’s Major Trade AgreementsExamples of Industry-Academia Collaboration in other industries

Company Industry Collaboration with Academic Institute

NASSCOM IT & ITES Collaborating with Ministry of HRD to set up new IIIT’s

TESCO Retail Runs a Retail Certification course with IIM-Bangalore

Airtel Telecom Has tied up with NMIMS to train its staff in the latest marketing techniques

Bharat Forge Aviation Has Partnered with BITS, Pilani to help its employees attaindegrees in manufacturing management

Patni Computers IT Have developed specialized courses in supply chainmanagement along with SP Jain Institute of Management

Top 5 sectors of preference for the students(B-School survey by AC Nielson)

FMCG

Management consulting,

IT consulting,

Banking and

Retailing

-----------------No Textiles ?

Source: Ministry of Commerce

8/2/2019 Paper- Indian Textile & Apparal Industry

http://slidepdf.com/reader/full/paper-indian-textile-apparal-industry 11/13

| Building Sustainable Businesses in the Growing Domestic Market Building Sustainable Businesses in the Growing Domestic Market | 18

Conclusion

The Indian domestic apparel market offers enormous opportunity going forwa rd due to various consumptiongrowth drivers inherent in the Indian economy. Overall consumption patterns are changing with decreasingapparel share of wallet and increase of more products in consumption basket. In this context apparel

companies need to study the domestic market dynamics more intensely in order to sustain apparel’s sharein the consumption basket.

A scan of the apparel market throws out some important opportunities that companies need to look moreclosely. Promising apparel segments like Women’s wear, Casual wear, Kids wear, Inner wear, Plus sizeclothing, School Uniforms, Active wear and youth fashion offer huge opportunity for apparel companies / brands / retailers as consumer demands get more specific going forward. Also the mass market offerssignificant opportunity for companies as value retailing takes its root in India. The increasing presence offoreign retailers in the domestic market is also expected to influence domestic players to improve theiroperations and offering to the customers.

To tap the above opportunities and sustain businesses in this changing consumption scenario, companiesneed to align themselves with the market requirements and de velop required competencies. Manufacturersneed to get more service oriented and look to develop a niche positioning for themselves amongst theirbuyers. With growing competition suppliers also need to have orientation towards innovation acrosstheir business in terms of products, processes and adopt best manufacturing practices to increasecompetitiveness. There also needs to be more focus given to hitherto overlooked areas like manpowerdevelopment, environment friendliness and leveraging t rade agreements for reducing sourcing costs.

About Technopak

We are a management consulting firm with a difference. Founded in 1991 on the principle of “concept” to“commissioning”, we are in the top 5 consulting firms in India by revenues. We are strategic advisors toour clients during the ideation phase, implementation guides through start-up phase, and trusted advisorsoverall. The industries we serve include Retail, Consumer Products, Fashion (Textiles & Apparel),Healthcare, Hospitality & Tourism, Leisure & Entertainment, Food & Agriculture and Education.

Our clients are leading Indian and international businesses, entrepreneurs, investment houses, multilateraldevelopment bodies and governments. Our 600+ clients include Aditya Birla Group, Apollo Hospitals, Arvind Limited, Asian Development Bank, Asian Paints, Temasek Holdings, Essar, GMR Group, GodrejGroup, Gujarat Government, Hospital Corporation of America, ICICI Limited, Hindustan Unilever Limited,International Finance Corporation, Lenovo International, Mahindra Group, Marks & Spencer, Mother DairyFoods, Ministries of Food Processing, Textiles & Commerce, Raymond, Reliance Industries, Samsung,Sequoia Capital, Starwood (Sheraton), Tata Group, United Nations Development Program, Walt Disney,Warburg Pincus and many other Indian and international leaders.

At Technopak, we foster innovation and creativity which challenge conventional thinking and generatepractical and far reaching solutions for our clients. In 2008, we worked with over 130 clients across 180+projects, in 20 countries besides India, a cross 5 continents.

Our key services are:

Business Strategy. Assistance in developing value creating strategies based on consumer insights,competition mapping, international benchmarking and client capabilities.

Start-Up Assistance. Leveraging operations and industry expertise to ‘commission the concept’ onturnkey basis.

Performance Enhancement. Operations, industry & management of change expertise to enhance theperformance and value of client operations and businesses.

Capital Advisory. Supporting business strategy and execution with comprehensive capital advisory in ourindustries of focus.

Consumer Insights. Holistic consumer & shopper understanding applied to offer implementable businesssolutions.

Services we offer in Management Consulting

8/2/2019 Paper- Indian Textile & Apparal Industry

http://slidepdf.com/reader/full/paper-indian-textile-apparal-industry 12/13

| Building Sustainable Businesses in the Growing Domestic Market

Services we offer through our Group Companies

Holistic consumer understanding applied to offer implementable business solutions revolving aroundshopper insights, trend insights, design and innovation insights, marketing communication and measuringcustomer delight.www.indiamindscape.com

Insights and innovation led product, packaging, space and strategic design, including design research,concepts, engineering and prototyping. A blend of unique, contemporary and relevant concepts andsolutions.www.foleydesigns.com

Planning, implementation and project management of plants, warehouses and entertainment centers with afocus on modernization, process improvement, technical valuation, power & water audit and environmentalengineering.www.technopak.com/engineering

Engineering

Technopak Financial Advisory Services (TFAS) is the financial and transaction advisory services arm ofTechnopak . With its team of experienced transaction professionals located in India and across US andEurope; TFAS offers its clients a global transaction ability, deep understanding of its industries of focus,and an efficient negotiating platform for stakeholders.

Technopak Financial Advisory Services

Strategizing, planning and managing creation, development and growth of brands through a scientific,

transparent and process-driven methodology.www.vertebrand.com

Services we offer through our Strategic Partnerships

World’s largest privately held real estate services firm. We offer, through them, comprehensive retail real estatesolutions to our clients.

www.cushwake.com

UK’s leading design consultancy for developing brand environments. We offer, through them, design solution

for retail environments.

www.dalziel-pow.co.uk

Global research and consulting firm specializing in the study of human behavior in retail, service, home, and on-

line environments. We offer consumer and shopper insights.

www.envirosell.com

Partners with Technopak for delivering Projects in India. They are one of the top architectural practices in the UKwith extensive experience in architectural and urban design projects in UK and internationally. The practice hasmajor specialism’s in Healthcare Architecture

www.devereuxarchitects.com

D E V E R E U X A R C H I T E C T S

8/2/2019 Paper- Indian Textile & Apparal Industry

http://slidepdf.com/reader/full/paper-indian-textile-apparal-industry 13/13

Technopak Advisors Pvt. Ltd.

Gurgaon4th Floor, Tower A, Building 8, DLF Cyber City, Phase II,Gurgaon 122 002, (National Capital Region of Delhi)(India)

T: +91-124-454 1111, F: +91-124-454 1199

BangalorePrestige Solitaire, Ground Floor, 6 Brunton Road,Off MG Road, Bangalore 560 025(India)

T: +91-80-4034 8600, F: +91-80-4034 8699

Mumbai101-105, 2nd Floor, Sunjana Tower,Sun Magnetica Service Road,Luis Wadi, Thane West,

Mumbai 400 602(India)

T: +91-22-2583 2222, F: +91-22-2583 8408

Website: www.technopak.com

Prashant Agarwal

Vice [email protected]

T: +91-9871195008

Ashish Dhir Associate Vice [email protected]

T: +91-9871654747

Priya Sachdeva

Senior [email protected]

T: +91-9312626145