overview presentation on demerger...overview presentation on demerger july 2007 this presentation is...

TRANSCRIPT

OVERVIEW PRESENTATION ON DEMERGER

July 2007This presentation is being made only to and is directed only at (a) persons who have professional experience in matters relating to investments falling within Article 19(1) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”) or (b) high net worth entities, and other persons to whom it may otherwise lawfully be communicated, falling within Article 49(1) of the Order (all such persons together being referred to as “relevant persons”). Any person who is not a relevant person should not act or rely on this presentation or any of its contents.

PAGE 1

OVERVIEW OF THE MONDI DEMERGER

� Dual listed company structure (DLC)

� Primary listings:

� Mondi plc – LSE main market

� Mondi LTD – Johannesburg Stock Exchange

� Secondary listing – Mondi plc on the Johannesburg Stock Exchange

Listing

� 100% demerger

� No capital raising by either Mondi or Anglo American

� For every 20 Anglo American plc Ordinary Shares held:

� 5 Mondi Plc (“MPLC”) Ordinary Shares

� 2 Mondi Limited (“MLTD”) Ordinary Shares

Structure

� Goldman Sachs International (UK)

� UBS Limited (UK, SA)Joint Sponsors

Friday 01 June 2007

Monday 25 June 2007

Tuesday 03 July 2007

Time Table

� Mondi prospectus published and circular sent to Anglo American shareholders

� Anglo American shareholder meeting

� Expected admission to listing, start of trading

PAGE 2

EXPERIENCED MANAGEMENT TEAM

Relevant experience� CFO BPB plc � CFO De La Rue plc � CFO Ransomes plc

Relevant experience� Corporate Development

Director Mondi Europe� VP Corporate Finance

Anglo American

Relevant experience� Member of Management

Board MBP� Production Director MBP

Relevant experience� CEO MP Corr. Bus.� CEO MP Bag Conv. and

Flex.� Plant Manager Bags

Maastricht� Corporate Controller

Frantschach Group

Relevant experience� Member of Board of

Management of Zellstoff Pöls

� CFO MBP� Senior Consultant Ernst

& Whinney

Relevant experience� CEO Mondi Europe� Financial Director Mondi Group� Divisional Finance Manager Anglo American

Relevant experience� Chairman Pensions

Trustees AMEC plc� Director UK Airports and

Heathrow Airport BA� HR Director BA

Kurt Mitterböck(Technical/

Procurement)55 years old

Peter Oswald (CEO MP)

44 years old

Günther Hassler (CEO MBP)48 years old

Andrew King(Strategy/BD)37 years old

Paul Hollingworth

(CFO)47 years old

David Hathorn(CEO)

45 years oldMervyn Walker

(HR/Legal)48 years old

PAGE 3

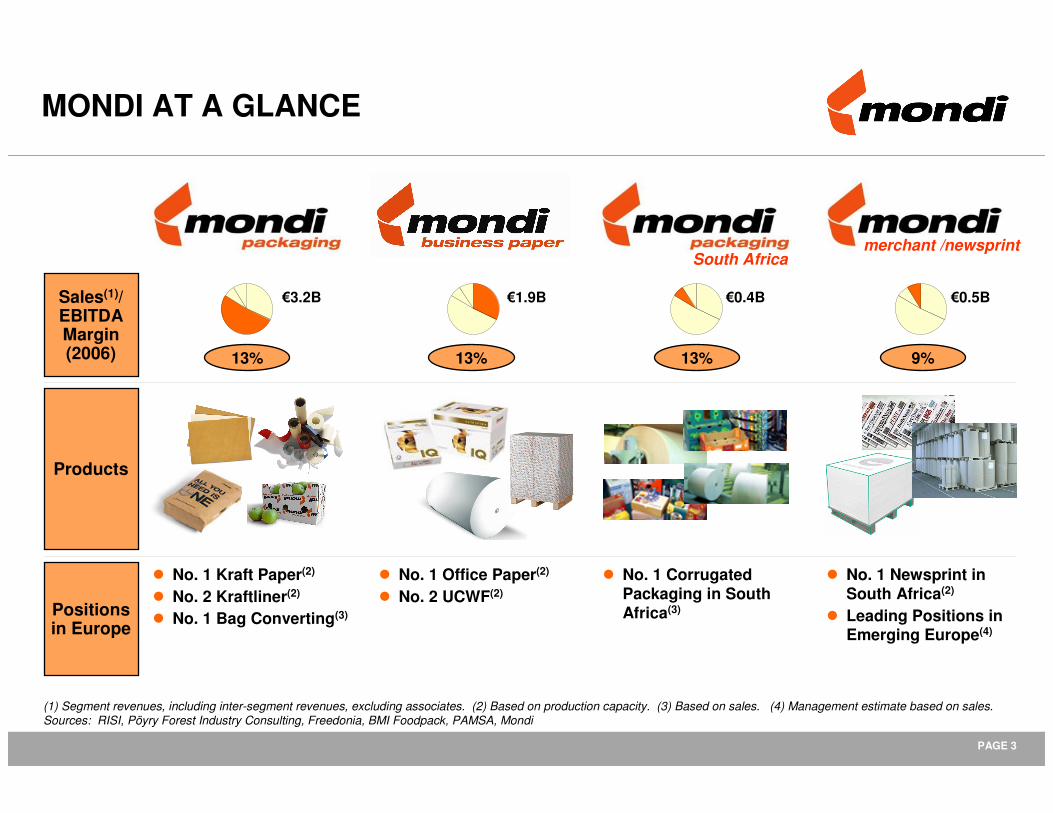

MONDI AT A GLANCE

Sales(1)/EBITDA Margin (2006)

Products

Positions in Europe

�0.4B

South Africa

�0.5B

merchant /newsprint

13% 9%

�3.2B

13%

� No. 1 Kraft Paper(2)

� No. 2 Kraftliner(2)

� No. 1 Bag Converting(3)

� No. 1 Corrugated Packaging in South Africa(3)

� No. 1 Newsprint in South Africa(2)

� Leading Positions in Emerging Europe(4)

�1.9B

13%

� No. 1 Office Paper(2)

� No. 2 UCWF(2)

(1) Segment revenues, including inter-segment revenues, excluding associates. (2) Based on production capacity. (3) Based on sales. (4) Management estimate based on sales.Sources: RISI, Pöyry Forest Industry Consulting, Freedonia, BMI Foodpack, PAMSA, Mondi

PAGE 4

ROCEMondiGroup

MondiGroup

vs.peers (index)

MONDI GROUP OUTPERFORMANCE VS. PEERS

21% 17% 11% 9%18%

Notes: (a) Mondi ROCE figures stated as reported by Mondi. (b) Competitors' ROCE figures average unweighted.Source: Public filings of peers and Mondi internal filings

8%

147197 203

131 144109

2001 2002 2003 2004 2005 2006

Ø peer= 100

Strong asset base

Leading market position

+

Focus on performance

+

Outperforming its peers

=

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

(10.0)% (5.0)% 0.0% 5.0% 10.0% 15.0% 20.0%

Sales CAGR in Local Currency 2001-2006 (%) �6bn Sales 2006

SCA

Int.Paper

M-real Smurfit-Stone

UPM

DS Smith

MeadWestvaco

Domtar

Portucel¹

PCA

StoraEnso

Weyer-hauser

Mondi

SmurfitKappa²

Wei

ghte

d A

vera

ge R

OC

E3

2001

-200

6

Sappi

(1) Data per 2001-2005A. (2) Data per 2003-2006A. (3) ROCE = EBIT (before special items)/CE = St borrowing + Lt borrowing + pref. equity + minority interest + total common equity– cash and near cash.

PAGE 5

MONDI STRATEGIC DRIVERS

� Upstream production cost advantages� Vertically integrated

Strong asset base

+

=

� Comprehensive Business Excellence programmes� Proven M&A/integration track record

� Rigorous asset allocation management

Focus on performance

� Outperformed peers measured by ROCE over the cycleOutperforming its peers

� Well placed to benefit from any upcycle

� Continued focus on profitability and value-added growth in attractive segments

Value creation

� Leading market positions � High exposure to attractive product segments and geographies

Strong market position

+

PAGE 6

1. Walki Wisa 9%2. Mondi 8%3. Amcor NA4. Stora Enso NA5. Schoeller NA

1. Avery Dennison 24%2. Raflatac 16%3. Mondi 9%4. Loparex 7%5. Huhtamaki 4%

1. Smurfit Kappa 27%2. Mondi 12%3. SCA 11%4. Ilim Pulp 8%5. Europac 5%

1. Mondi 21%2. Billerud 14%3. UPM 9%4. Segezha 7%5. Stora Enso 7%

LEADING MARKET SHARES

Strong market position

1. Smurfit Kappa 18%2. SCA 9%3. Mondi 4%4. DS Smith 4%4. International Paper 4%4. SAICA 4%

Corrugated Packaging(2)(3)Kraftliner(1)

1. Mondi 15%2. Segezha 7%3. Smurfit Kappa 5%4. Brit. Polythene 4%5. Bischof + Klein 3%

Bag

Bag Converting(4)Kraft Paper(1)

Corrugated

Flexibles

Extrusion Coating (4)(5)Release Liner(4)(5)

Top 5 Uncoated Woodfree

Top 5 Office Paper

Mondi BP generates approximately 65% of UCWF sales in faster growing Office Paper segment

Stora Enso

M-Real

Mondi

IP

Portucel

16%

11%

13%

10%

10%

Stora Enso

M-Real

Mondi

IP

Portucel

17%

14%

16%

13%

11%

(1) Based on capacity. (2) Based on demand. (3) Based on ICCA forecasts of market size for 2006. (4) Based on sales. (5) No public information available, market shares are Mondi estimates.Sources: Mondi, RISI, ICCA, Freedonia, Pöyry Forest Industry Consulting, company filings, Henry Poole

Packaging Office Paper

PAGE 7

(1) Excluding acquisitions.Sources: Pöyry Forest Industry Consulting, Mondi

SIGNIFICANT EXPOSURE TO GOOD GROWTH SEGMENTS

Mondi Group Sales 2006 Mondi Group Net Operating Assets 2006Strong market position

Emerging MarketsMature Markets

0

100

200

300

400

500

600

2004 2005 2006

Capital Expenditures (�M)(1)

70%

30%

75%

25%

Mature markets: �0.5B

� ~47% maintenance� ~53% expansion

Emerging markets:�1.1B

� ~34% maintenance

� ~66% expansionLarge investments create major upside in cyclical upturn

61%

39%

+

Strong market position

Strong asset base

55%45% 38%62%

PAGE 8

UPSTREAM PRODUCTION COST ADVANTAGES LOW-COST POSITIONS

Universal Office Paper

Note: The graphs show delivered cost to Frankfurt, Germany.Sources: Pöyry Forest Industry Consulting, Mondi

Mondi Paper Machines

+

Unbleached KraftlinerWhite-top Kraftliner

Cumulative capacity (Kt/a)

00 3,000

100% of Mondi Unbleached

Kraftliner capacity

�/t 1,500

91% of Mondi Universal Office Paper Capacity

00 3,500Cumulative capacity (Kt/a)

Cumulative capacity (Kt/a)

�/t 800

1,400

100% of Mondi White-top Kraftliner

capacity

00

�/t 500

Strong market position

Strong asset base

PAGE 9

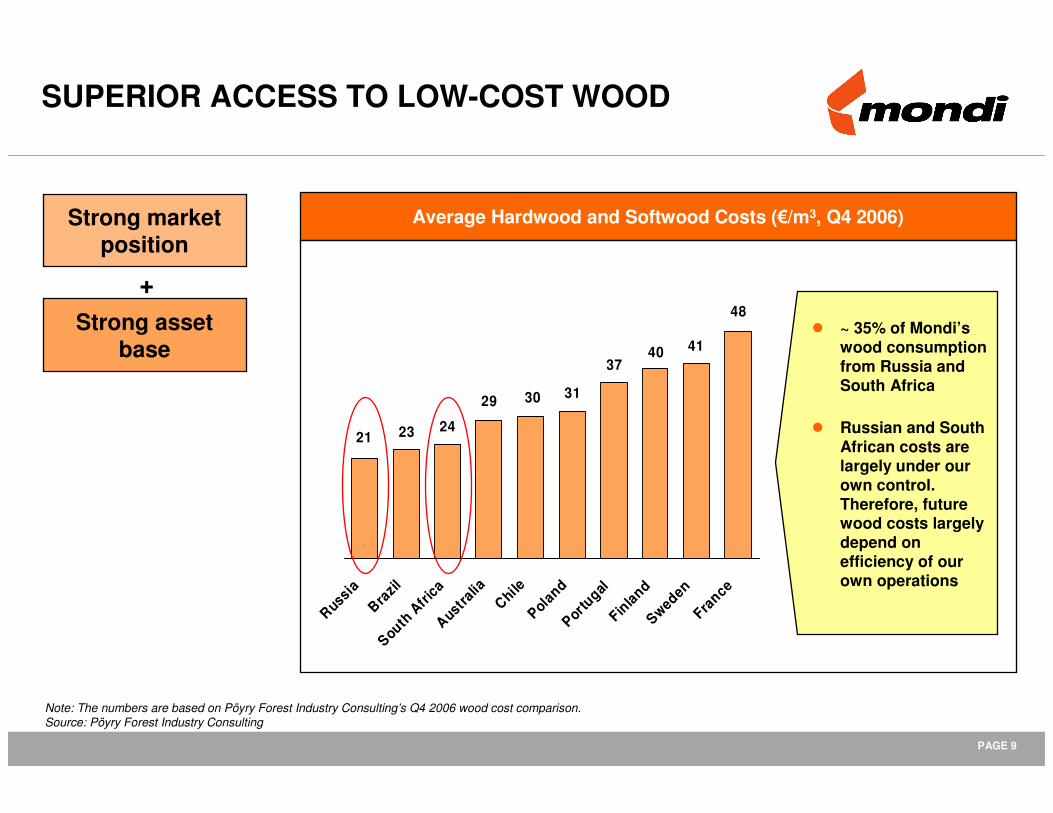

SUPERIOR ACCESS TO LOW-COST WOOD

Average Hardwood and Softwood Costs (�/m3, Q4 2006)

� ~ 35% of Mondi’s wood consumption from Russia and South Africa

� Russian and South African costs are largely under our own control. Therefore, future wood costs largely depend on efficiency of our own operations

48

3029

23

40 4137

31

2421

RussiaBra

zilSouth

Afri

caAustra

liaChile

PolandPortu

galFinlandSweden

France

+

Strong market position

Strong asset base

Note: The numbers are based on Pöyry Forest Industry Consulting’s Q4 2006 wood cost comparison.Source: Pöyry Forest Industry Consulting

PAGE 10

PLANNED MAJOR INVESTMENTS

SYKTYVKAR MILL EXPANSION� Modernisation and Expansion� Investment cost of �525M

� 3-4 yr investment period� Completion expected mid-2010

Universal Business Paper Cost Curve

200

400

600

800

1,000

1,200

0 1,000 2,000 3,000 4,000Cumulative capacity (1 000 t/a)

Syktyvkar PM14

�/t

+

Strong market position

Strong asset base

CONTAINERBOARD EXPANSION� New 470,000t lightweight recycled

containerboard machine and corrugated box plant� Capacity of c.250M m2/year

� Investment cost c.�350M� In final feasibility

� Start up mid-late 2009

100

150

200

250

300

350

0 5,000 10,000

Cumulative capacity (1 000 t/a)

�/t

Recycled Fluting Cost Curve

PM CEE Light

� Likely to be located at our Polish operations

� Additional volume is required to supply the high growth Emerging European markets

� Targeted to be clear cost leader in Europe

� Exposed to strong growth in demand for UCWF and containerboard in the domestic Russian market

� Well located to exploit the low-cost wood resources

PAGE 11

BENEFITING FROM INTEGRATED VALUE CHAIN

(1) Refers to Mondi’s demand and self-sufficiency of packaging paper (including MP and MPSA). Paper is the end product for non-packaging businesses.Notes: 2006 figures. Forestry figures are based on annual allowable cut (excluding firewood).Source: Mondi

Mondi’s own availability

Mondi’s own demand

Forestry Pulp Paper

Potential self sufficiency 51%

7.6mm3

14.8mm3

91%

3.5Mt

3.8Mt

154%(1)

5.8MtPackaging: 3.3Mt

2.1Mt(1)

+

Strong market position

Strong asset base

PAGE 12

DISCIPLINED AND VALUE-ORIENTED M&A

� Sustainable low-costadvantage

� Restructuring and optimisation potential

� Attractive positions in Emerging Markets

(1) Acquisition of part of business. (2) Share currently held: Syktyvkar 98%, Ruzomberok 51%. Mondi acquired 19.4% of Syktyvkar shares in 1997, 71.9% in 2002 and the remaining 6.7% thereafter. (3) Multiple average of Mondi weighted by Enterprise Value.

Note: The acquisition of Lenco, a South African Plastics Business, is excluded as regulator approval has not yet been received. Source: Mondi

Target

Napiag (A)

S&E (D, ITA), NBG (A)

Stambolijski (BG)

Akrosil (US, NL)

Bauernfeind (Europe)

Copamex (MEX)(1)

Syktyvkar (RUS)(2)

La Rochette (F, UK)

Danisco (UK)

Ruzomberok (SK)(2)

AssiDomän (Europe)(1)

Year

2007

2006

2006

2006

2004

2004

2002

2002

2001

2000

2000

Business

Flexibles

Flexibles

Bag

Flexibles

Corrugated

Bag

MBP

Corrugated

Corrugated

MBP

Bag, Flex.

EV/EBITDA multiple:

Mondi4.4x(3)

Regular review of acquisitions and integration to optimise value

M&A Strategy Major M&A Deals since 2000

+

Strong market position

Strong asset base

+Focus on

performance

PAGE 13

PERFORMANCE IMPROVEMENTSIN ACQUIRED COMPANIES

(1) First full year of acquisition. (2) Including forest workers. (3) CAGR.Note: Tons per capita based on employees year average Source: Mondi

Syktyvkar(2) (tonnes per capita)

2002 200683

Swiecie (tonnes per capita)

1997 2006

132902

24% p.a.(3)

� Leverage synergies with existing operations

� Transfer know-how

� Improve efficiency

� Improve product mix

� Closures/divestitures of underperforming sites

Ruzomberok (tonnes per capita)

2000 2006160

484

Integration Principles

(1)

(1)

(1)

135

20% p.a.(3)

13% p.a.(3)

+

Strong market position

Strong asset base

+Focus on

performance

PAGE 14

ACQUISITIONS PRIMARY GROWTH DRIVER

2000 Organicgrowth 2000-06

Acquiredgrowth 2000-06

2006

(1) (1)

(1) Growth figures refer to Compound Annual Growth Rate (CAGR), calculated as change in volume FY 2000 vs. FY 2006. (2) Any volume growth 12 rolling months after the first consolidation date is accounted for as organic growth.

Source: Mondi

2,768

5,784

Breakdown of Paper Production Volume Growth (Kt)

Of which 542 subsequent to M&A(2)

Total Growth: 3,016� Organic: 1,206

� Acquired: 1,810

CAGR(1) : 13%

5%

8%+

Strong market position

Strong asset base

+Focus on

performance

PAGE 15

RIGOROUS ASSET MANAGEMENT

Note: Closures and divestitures including activities within MBP and MP.Source: Mondi

� Reduced Testliner capacity by 11% in 2004(~110Kt; 2 plants)

� Closed 11% of corrugated board capacity (~280mm2) since 2004

� Sale/conversion of Dunaújváros in 2006 represents a substantial capacity reduction in UCWF (~110Kt from 2007 onwards)

� Closed 32 packaging converting plants since 2002

� Divested 30 packaging converting plants since 2002

+

Strong market position

Strong asset base

+Focus on

performance

PAGE 16

300

600

900

1,200

FIVE YEAR RECORD

Group Revenue

EBITDA

% Margin

Underlying Operating Profit

% Margin

Capital Employed

% Return

5,751 5,051 5,005 5,385 5,364

726N/A 873 779 718

12.6%N/A 17.4% 14.5% 13.4%

377 686 579 459 386

6.6%13.6% 11.7% 8.5% 7.2%

4,757 3,339 3,496 4,422 4,667

8%21% 17% 11% 9%

Note: N/A – not previously disclosed publicly.

2006IFRS

2002UK GAAP

2003UK GAAP

2004IFRS

2005IFRS

Uncoated Woodfree Prices Kraftliner PricesUncoated Woodfree Prices Kraftliner Prices

�/tonne

PAGE 17

Group Revenue (�M) EBITDA Margin (%) Operating Margin(1) (%)

BUSINESS UNIT THREE YEAR RECORD

Mondi Packaging 3,1672,848 2,902 13.014.9 14.1 7.18.7 7.8

Business Paper 1,8891,766 1,752 12.514.5 14.1 5.58.1 7.4

MPSA 360348 359 12.814.7 11.7 9.711.5 8.9

Merchant and Newsprint 539521 509 8.99.0 7.5 5.45.2 3.5

Other and Inter-company (204)(98) (158) –– – –– –

Total 5,7515,385 5,364 12.614.5 13.4 6.68.5 7.2

20062004 2005 20062004 2005 2004 2005 2006

(1) Underlying Operating Profit Margin.

CAGR

5.5%

3.4%

1.7%

1.7%

3.3%

PAGE 18

MONDI GROUP KEY FINANCIALS

Capital Expenditure

� Major recent capex investments include:

� Richards Bay – RB 720 � 250M� Merebank – PM 31 rebuild � 175M� Ruzomberok – Pulp mill rebuild � 136M

� Capex targeted at low cost resource� Maintenance capex targeted at circa 60% of depreciation and

amortisation

Cost Base

� There will be increased corporate costs post demerger

Cost Structure 2006

Personnel Costs 17%

Variable Selling Expense 10%

Energy 7%

Maintenance 6%

Other Variable Costs16%

Other Operating Expenses

6%

Depreciation/ Amortisation

7%

Wood, Pulp and Fibre 33%

0

100

200

300

400

500

600

700

2004 2005 20060%2%4%6%8%10%12%14%16%

Mature MarketsEmerging Markets

460

618551

�M

8.0%

11.5%10.3%

Capex/Sales

0

100

200

2004 2005 2006

2.8%

3.9% 3.6%

% of cash cost

Gross Cost Reduction Initiatives (�M)

PAGE 19

MONDI GROUP KEY FINANCIALS

Borrowing Facilities Dividends

� Net debt at demerger estimated at circa �1.5B

� Targeting investment grade rating

� Negotiating a new �1.75B committed debt facility

� �1.55B of new facility in Mondi plc for five years with

ZAR 2B (�0.2B) in Mondi LTD for three years

� In addition Mondi has existing Group committed

facilities of circa �0.9B at varying maturities

� Targeting one covenant of net debt to EBITDA of 3.5x

� Cross guarantees will be in place between Mondi plc

and Mondi LTD

� Would expect to make an interim dividend payment in 2007

� Dividends will be determined by new board going forward, and expected to take into account:

� Actual Mondi trading

� Both peer group and market dividend policies

� Target of 2-3 times earnings coverage on average over the cycle

� In the absence of unforeseen circumstances, the Board would have recommended distributing a dividend of 20 Euro cents per share for 2006 assuming that the demerger had been effective for the full year

(1)

(1) Implied underlying Mondi shares outstanding of 518 million, being the pro forma combined number of shares that is expected to be in issue upon admission.

OVERVIEW PRESENTATION ON DEMERGER APPENDIX

July 2007

PAGE 21

INDUSTRY FUNDAMENTALS: EUROPEAN CONTAINERBOARD AND CORRUGATED PACKAGING

� Demand

� Demand for corrugated packaging in Europe grew by 2.7% per annum from 2000 to 2006, driven by strong growth in Emerging Europe of 11% per annum(1). Over the 2004 to 2006 period, demand grew by around 2.4Mt

� Future demand growth is expected to be broadly in line with these historic trends

� 2.7% growth on 2006 demand of around 25Mt represents around 0.68Mt

� Supply� Total European containerboard capacity increases

between 2004 and 2006 of around 3.8Mtpa offset by capacity closures of around 2.4Mtpa, gave a net increase in capacity over the period of around 1.4Mtpa (excluding capacity creep)

� Recent significant capacity increases now absorbed into the market. No new paper machines announced to come on line in 2007/2008

� Rationalisation of kraftliner capacity in North America has contributed to reduced imports to Europe

200

250

300

350

400

450

500

550

600

650

2001 2002 2003 2004 2005 2006 2007

�/to

nne

Kraftliner 175gTestliner 2

(2)

(1) Growth on tonnage basis 2000 to 2006 based on 2006 forecasts. (2) Q4 2001 – Q1 2007.Sources: ICCA, RISI, Pöyry Forest Industry Consulting

(2)

PAGE 22

INDUSTRY FUNDAMENTALS: EUROPEAN UNCOATED WOODFREE PAPER

� Demand� European uncoated woodfree demand grew by 3%

per annum in the period from 2000 to 2006, driven by strong growth in the office paper segment of around 4% per annum(1)

� Within the office paper segment, growth mainly attributed to strong growth in Emerging Europe. Growth in Emerging Europe was around 7% over 2005-2006(2)

� Moderate demand growth anticipated to continue, with Emerging Europe exhibiting the strongest growth in the region albeit at lower levels than experienced over the 2000 to 2006 period

� 3% demand growth on total 2006 demand of around 11.8Mt represents around 0.35Mt

� Supply� Announced European capacity closures in 2006 of

180Ktpa, with further closures of 540Ktpa announced for 2007

� Global capacity is expected to grow in line with demand, with most new capacity planned for Asia in response to strong Chinese demand growth.

� Only announced major expansion in Europe is a new 500Ktpa machine at Portucel’s Setubal mill, planned for commissioning in 2009

600

700

800

900

1,000

1,100

1,200

2001 2002 2003 2004 2005 2006 2007

�/to

nne

UCWF

(3) (3)

(1) Volume growth based on 2000 to 2006 demand estimates by Pöyry Forest Industry Consulting. (2) Demand estimates by Pöyry Forest Industry Consulting. (3) Q4 2001 – Q1 2007.

Sources: Mondi, Pöyry Forest Industry Consulting, CEPIFINE, RISI

PAGE 23

Note: Dotted lines represent average 1990 - Q1 2007.Source: Pöyry Forest Industry Consulting

+

Strong market position

Strong asset base

+Focus on

performance

=Outperforming

its peers

MONDI WELL PLACED TO BENEFIT FROM UPTURN IN PAPER PRICING

300

400

500

600

700

800

900

1,000

1,100

1,200

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Uncoated Woodfree A4 B-Grade Copy Office Paper

Kraftliner 175g

Average Delivered Prices in Europe

�/to

nne

PAGE 24

Growth of Office PCs Drives Office Paper Growth

OFFICE PAPER DEMAND GROWTH EXPECTED TO CONTINUE

Office Paper used for “Work in progress”and “Reading”

Office Paper used for “Archiving”and “Distributing”

� Paper with inherent advantages

� Flexibility/portability� Possibility to annotate� Navigation

� Electronic processes often with advantages –ongoing substitution

� Overall increase in number of Office Paper users over-riding effect

(1) According to IDC.Sources: BCG, EIU, EMGE, IDC, Mondi, PPI

0

2

4

6

8

10

12

14

16

18

20

0 100 200 300 400 500

United States

United Kingdom

Germany

Italy

MexicoPoland

RussiaChina

Office PCs per1,000 heads (2003)

Office Paper consumption per head (kg, 2003)

PC penetration CAGR 2003-2010(1)

+4%

+6%

+6%

+9%

+16%

+19%

+6%

+8%

Detailed Understanding of Usage Patterns Strong market position

PAGE 25

KEY FEATURES OF THE DLC STRUCTURE

� Single Corporate Group

� MPLC and MLTD separate legal entities with separate stock exchange listings

� Unified boards and management

� Head office located in South Africa by December 2008

� Shareholders of both companies effectively vote together as a single decision making body

� Cross guarantees between MPLC and MLTD

� Any takeover offer must be made to shareholders of both MPLC and MLTD

MPLC Ordinary Shareholders

MLTD Ordinary Shareholders

MPLC MLTD

Non - African Operations African Operations

SINGLE CORPORATE GROUP

Sharing Agreement

Equalisation Ratio 1:1

PAGE 26

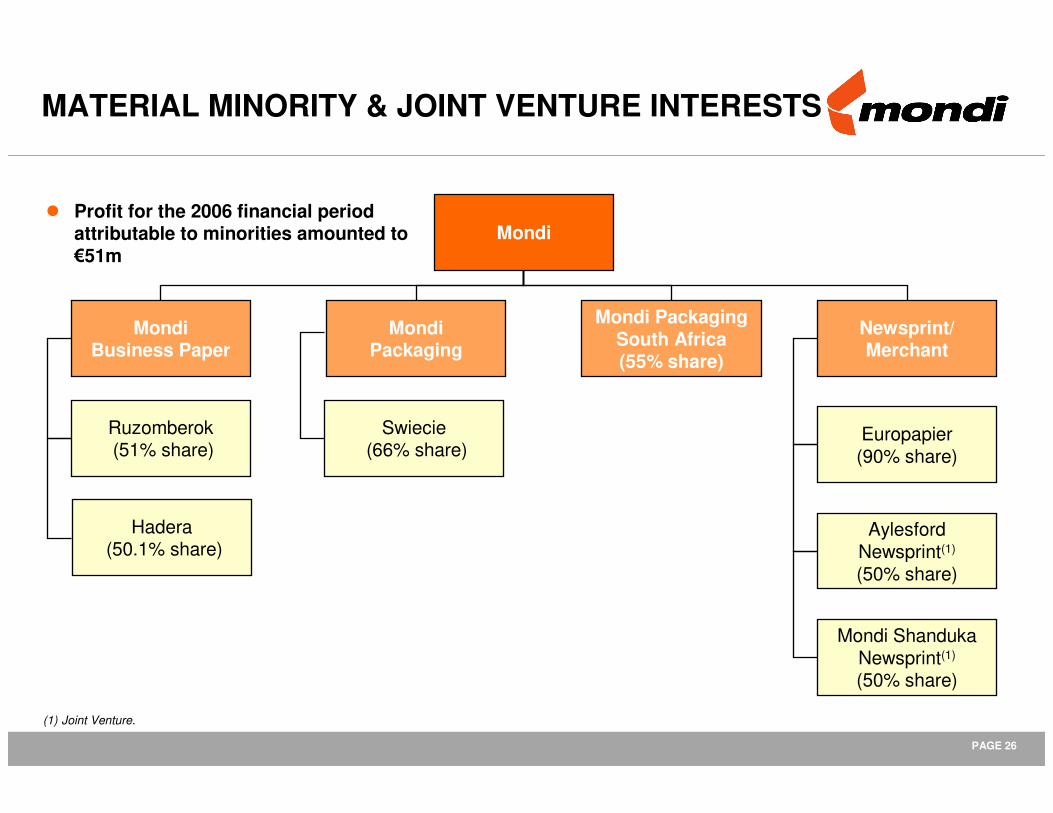

(1) Joint Venture.

Mondi Business Paper

MondiPackaging

Mondi Packaging South Africa (55% share)

Newsprint/Merchant

Mondi

Europapier (90% share)

Swiecie(66% share)

Aylesford Newsprint(1)

(50% share)

Ruzomberok(51% share)

Mondi Shanduka Newsprint(1)

(50% share)

Hadera(50.1% share)

MATERIAL MINORITY & JOINT VENTURE INTERESTS

� Profit for the 2006 financial period attributable to minorities amounted to �51m