outlook on asian lng - siew

TRANSCRIPT

(C) 2016 IEEJ, All rights reserved

Outlook on Asian LNG- Market Dynamics and Pricing -

Yukari YamashitaThe Institute of Energy Economics, Japan (IEEJ)

27 October 2016Singapore International Energy Week 2016

Think tank Roundtable A

Asia/WorldEnergyOutlook2016

(C) 2016 IEEJ, All rights reserved

Introduction

Findings from “Asia/ World Energy Outlook 2016”

Energy Situation in Asia

Scenario Study: Supply Disruption of Oil and Gas

Climate Change Measures

Today’s Discussion Points

2

(C) 2016 IEEJ, All rights reserved

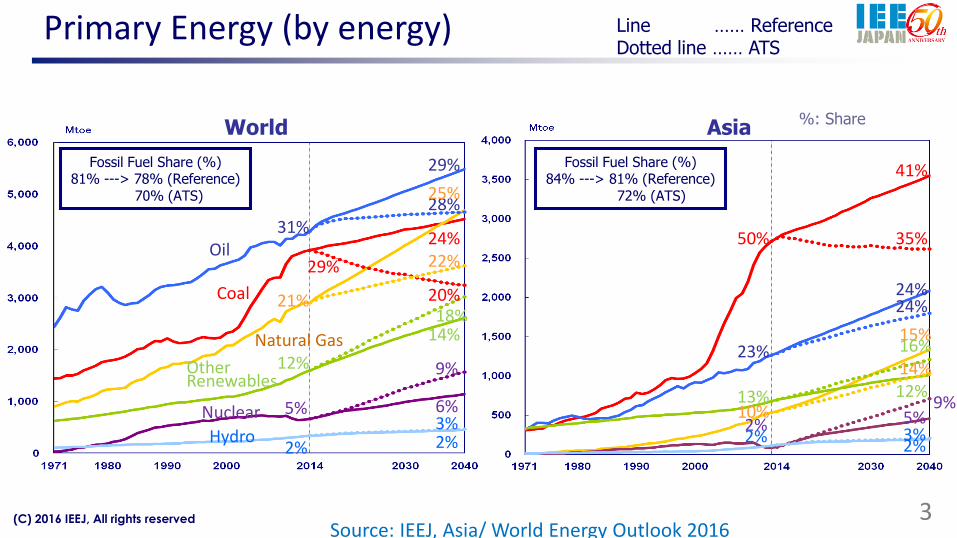

Primary Energy (by energy) Line …… ReferenceDotted line …… ATS

World Asia

Oil

Coal

Natural Gas

OtherRenewables

Nuclear

Hydro

31%

%: Share

29%

28%

23%

24%24%

50%

41%

35%24%

20%

29%

21%

25%

22%

10%

15%

14%12%

14%

9%

13% 12%

16%

5% 6%

18%

2% 5%9%

2%2%2% 2%

3%

Fossil Fuel Share (%)81% ---> 78% (Reference)

70% (ATS)

Fossil Fuel Share (%)84% ---> 81% (Reference)

72% (ATS)

3

3%

Source: IEEJ, Asia/ World Energy Outlook 2016

(C) 2016 IEEJ, All rights reserved

Huge Improvement in Energy Intensity

4

Annual Growth Rate (World:2014-2040) GDP and Primary Energy Demand

0.0

2.0

4.0

6.0

8.0

2000 2010 2020 2030 2040

GDP

Energy

Y2000=1.0

OECD2.9%

0.9%

1.2%

2.8%

1.2%

2.2%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

GDP Population Energy

ー: Y2000-2014

0.0

2.0

4.0

6.0

8.0

2000 2010 2020 2030 2040

GDP

Energy

Y2000=1.0

non OECD

Source: IEEJ, Asia/ World Energy Outlook 2016

(C) 2016 IEEJ, All rights reserved

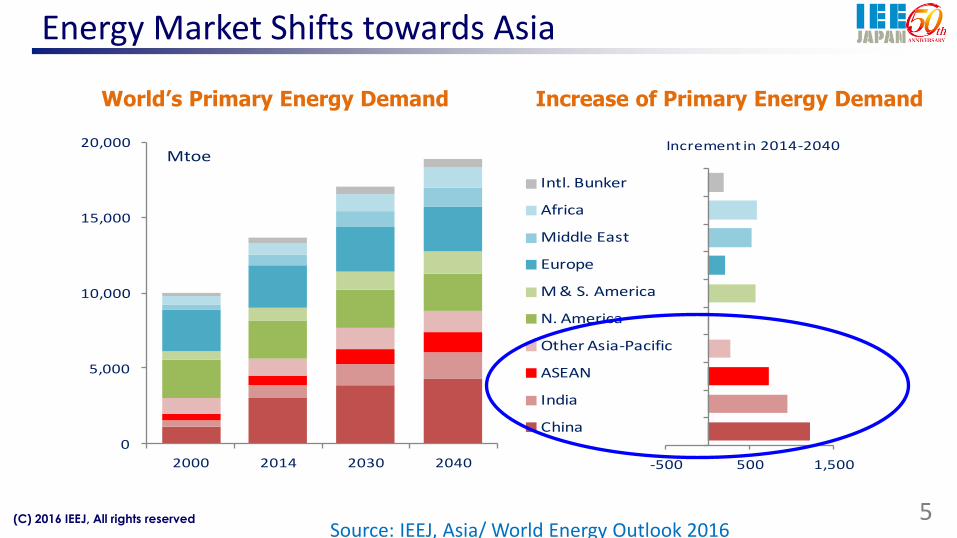

Energy Market Shifts towards Asia

5

World’s Primary Energy Demand Increase of Primary Energy Demand

-500 500 1,500

Increment in 2014-2040

0

5,000

10,000

15,000

20,000

2000 2014 2030 2040

Intl. Bunker

Africa

Middle East

Europe

M & S. America

N. America

Other Asia-Pacific

ASEAN

India

China

Mtoe

Source: IEEJ, Asia/ World Energy Outlook 2016

(C) 2016 IEEJ, All rights reserved

0 2,000 4,000 6,000

Coal

Oil

Natural gas

Non-fossil fuel

2014 2014-2040

Mtoe

0 100 200 300 400 500

Coal

Oil

Natural gas

Non-fossil fuel

2014 2014-2040

Mtoe

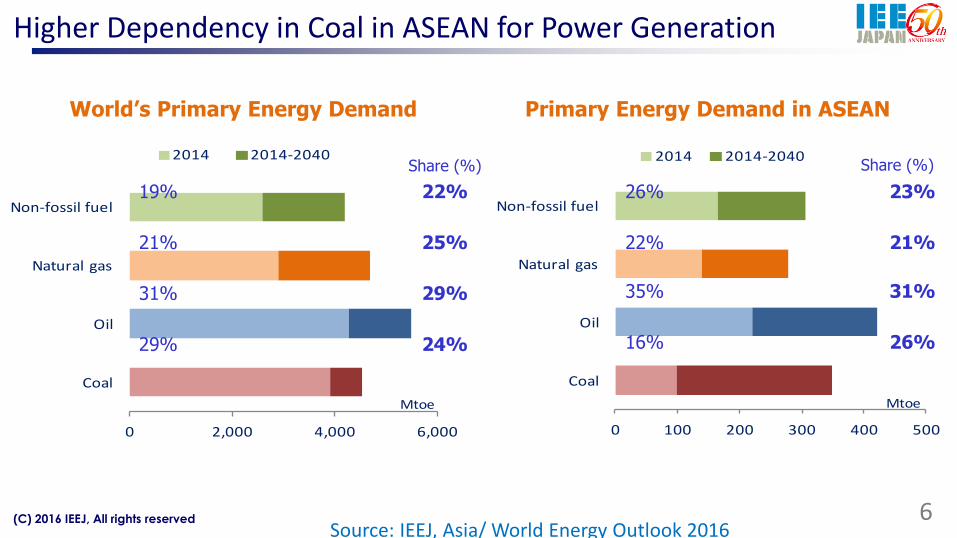

Higher Dependency in Coal in ASEAN for Power Generation

6

Primary Energy Demand in ASEANWorld’s Primary Energy Demand

22%

25%

29%

24%

19%

21%

31%

29%

23%

21%

31%

26%

26%

22%

35%

16%

Share (%) Share (%)

Source: IEEJ, Asia/ World Energy Outlook 2016

(C) 2016 IEEJ, All rights reserved

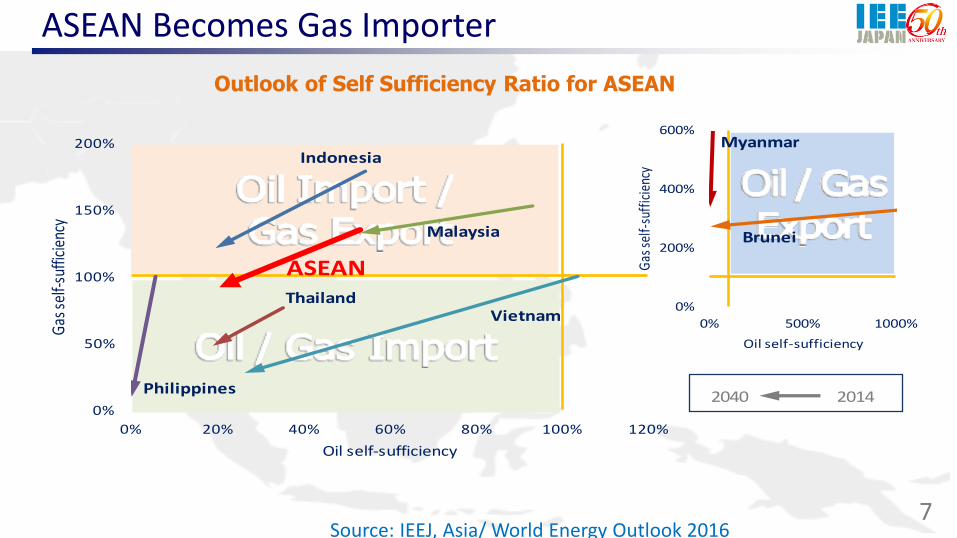

ASEAN Becomes Gas Importer

Outlook of Self Sufficiency Ratio for ASEAN

7

201420400%

50%

100%

150%

200%

0% 20% 40% 60% 80% 100% 120%

Gas

self-

suffi

cien

cy

Oil self-sufficiency

Indonesia

Malaysia

VietnamThailand

Philippines

ASEAN

0%

200%

400%

600%

0% 500% 1000%

Gas

self-

suff

icie

ncy

Oil self-sufficiency

Brunei

Myanmar

Source: IEEJ, Asia/ World Energy Outlook 2016

(C) 2016 IEEJ, All rights reserved

Supply Disruption of Oil and Gas

Asia/WorldEnergyOutlook 2016

(C) 2016 IEEJ, All rights reserved

0%

1%

2%

3%

0

1

2

3

2000 2005 2010 2015

As a

% o

f no

min

al G

DPO

il im

po

rts

($ t

rilli

on

)

Oil Imports

Oil imports as a % of nominal GDP

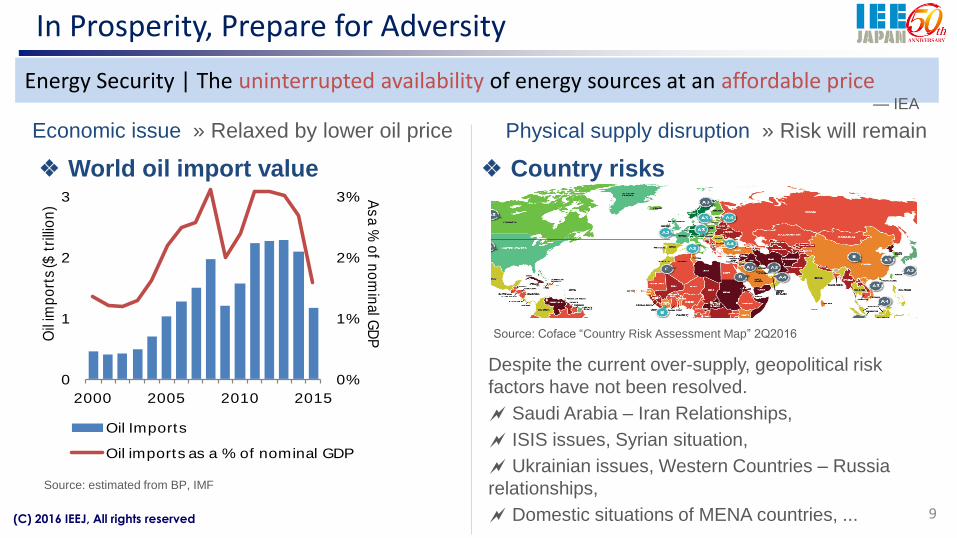

Despite the current over-supply, geopolitical risk

factors have not been resolved.

Saudi Arabia – Iran Relationships,

ISIS issues, Syrian situation,

Ukrainian issues, Western Countries – Russia

relationships,

Domestic situations of MENA countries, ...

In Prosperity, Prepare for Adversity

Energy Security | The uninterrupted availability of energy sources at an affordable price

9

Economic issue » Relaxed by lower oil price Physical supply disruption » Risk will remain

Source: Coface “Country Risk Assessment Map” 2Q2016

❖ World oil import value ❖ Country risks

— IEA

Source: estimated from BP, IMF

(C) 2016 IEEJ, All rights reserved

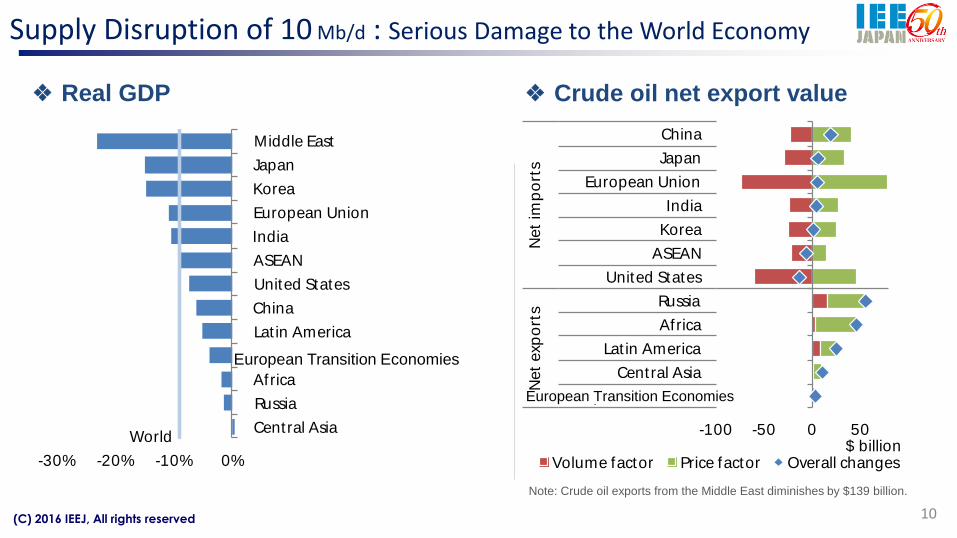

Supply Disruption of 10 Mb/d : Serious Damage to the World Economy

10

❖ Real GDP ❖ Crude oil net export value

Note: Crude oil exports from the Middle East diminishes by $139 billion.

World

-30% -20% -10% 0%

Central Asia

Russia

Africa

European t ransit ion …

Lat in America

China

United States

ASEAN

India

European Union

Korea

Japan

Middle East

-100 -50 0 50

European t ransit ion …

Central Asia

Lat in America

Africa

Russia

United States

ASEAN

Korea

India

European Union

Japan

China

Net

exp

ort

sN

et

imp

ort

s

$ billionVolume factor Price factor Overall changes

European Transition Economies

European Transition Economies

(C) 2016 IEEJ, All rights reserved

World

-10% 0%

China

Russia

United States

Lat in America

Africa

India

ASEAN

European Union

Japan

Korea

Central Asia

Middle East

European …

World

-20% -10% 0%

China

United States

Lat in America

India

Africa

ASEAN

Korea

Japan

European Union

Middle East

Central Asia

Russia

European …

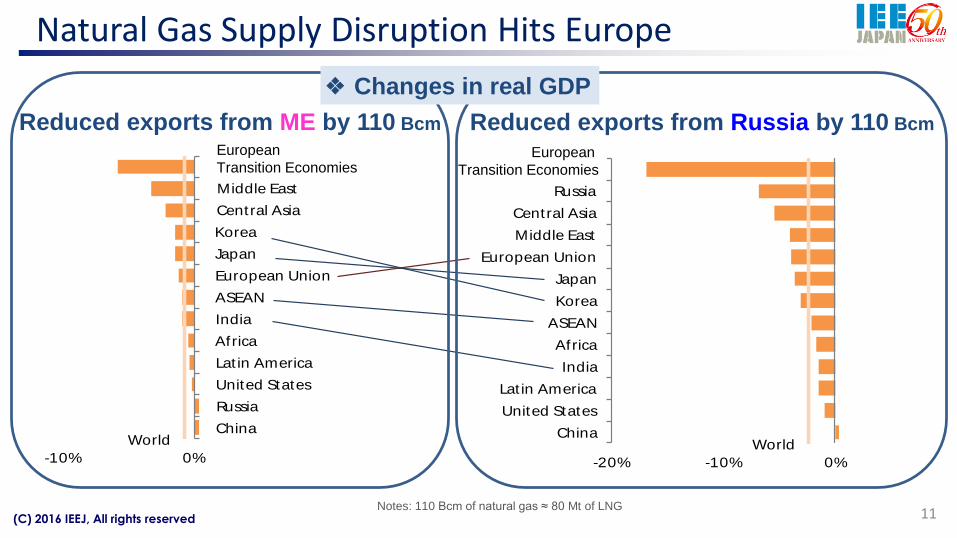

Natural Gas Supply Disruption Hits Europe

11

Reduced exports from ME by 110 Bcm Reduced exports from Russia by 110 Bcm

Notes: 110 Bcm of natural gas ≈ 80 Mt of LNG

European

Transition EconomiesEuropean

Transition Economies

❖ Changes in real GDP

(C) 2016 IEEJ, All rights reserved

Climate Change Measures |

Paris Agreement, Advanced Technologies Case, Hydrogen

Asia/WorldEnergyOutlook 2016

(C) 2016 IEEJ, All rights reserved

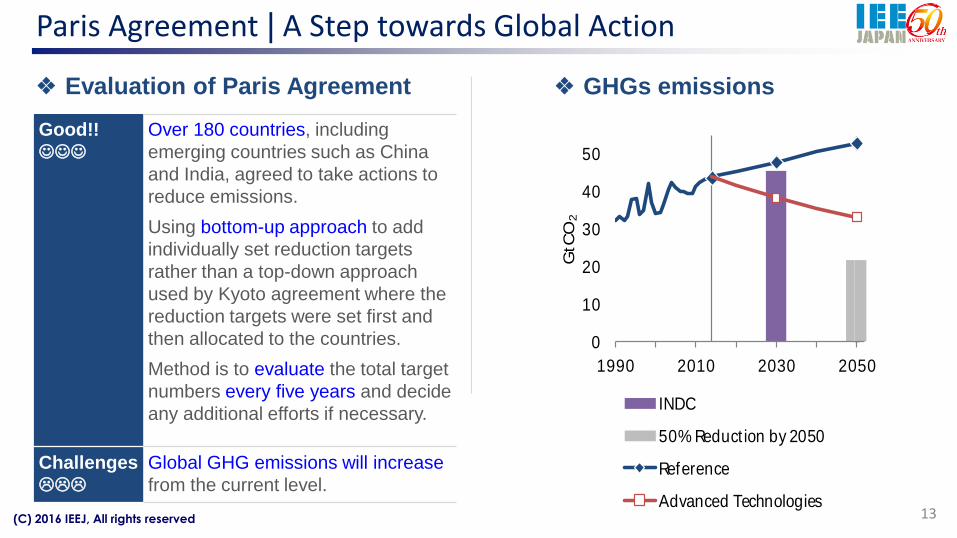

Paris Agreement | A Step towards Global Action

13

❖ Evaluation of Paris Agreement ❖ GHGs emissions

Good!!

Over 180 countries, including

emerging countries such as China

and India, agreed to take actions to

reduce emissions.

Using bottom-up approach to add

individually set reduction targets

rather than a top-down approach

used by Kyoto agreement where the

reduction targets were set first and

then allocated to the countries.

Method is to evaluate the total target

numbers every five years and decide

any additional efforts if necessary.

Challenges

Global GHG emissions will increase

from the current level.

0

10

20

30

40

50

1990 2010 2030 2050

GtC

O2

INDC

50% Reduct ion by 2050

Reference

Advanced Technologies

(C) 2016 IEEJ, All rights reserved

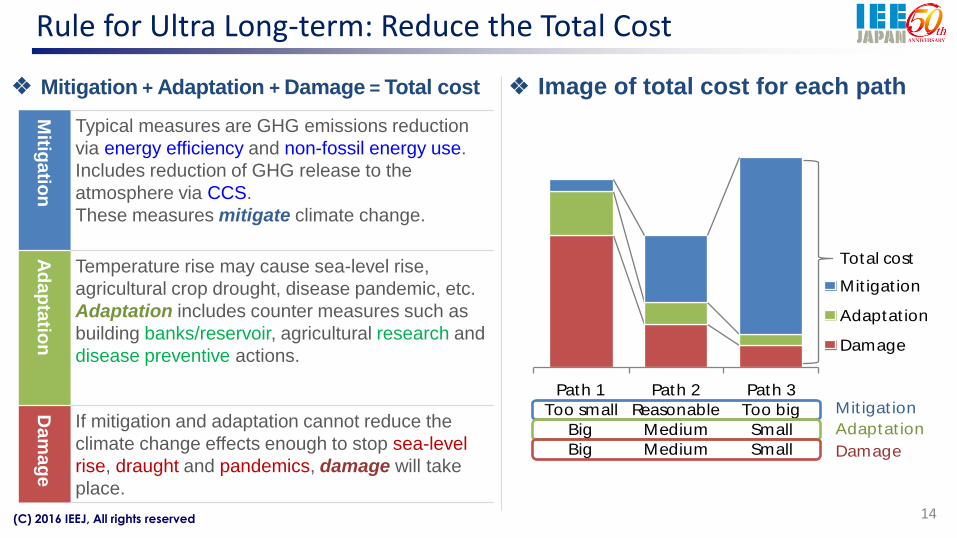

Rule for Ultra Long-term: Reduce the Total Cost

14

❖ Mitigation + Adaptation + Damage = Total cost ❖ Image of total cost for each path

Mitig

atio

n

Typical measures are GHG emissions reduction

via energy efficiency and non-fossil energy use.

Includes reduction of GHG release to the

atmosphere via CCS.

These measures mitigate climate change.

Ad

ap

tatio

n

Temperature rise may cause sea-level rise,

agricultural crop drought, disease pandemic, etc.

Adaptation includes counter measures such as

building banks/reservoir, agricultural research and

disease preventive actions.

Da

ma

ge

If mitigation and adaptation cannot reduce the

climate change effects enough to stop sea-level

rise, draught and pandemics, damage will take

place.

Path 1

Too small

Big

Big

Path 2

Reasonable

Medium

Medium

Path 3

Too big

Small

Small

Mit igat ion

Adaptat ion

Damage

Total cost

Mit igat ion

Adaptat ion

Damage

(C) 2016 IEEJ, All rights reserved

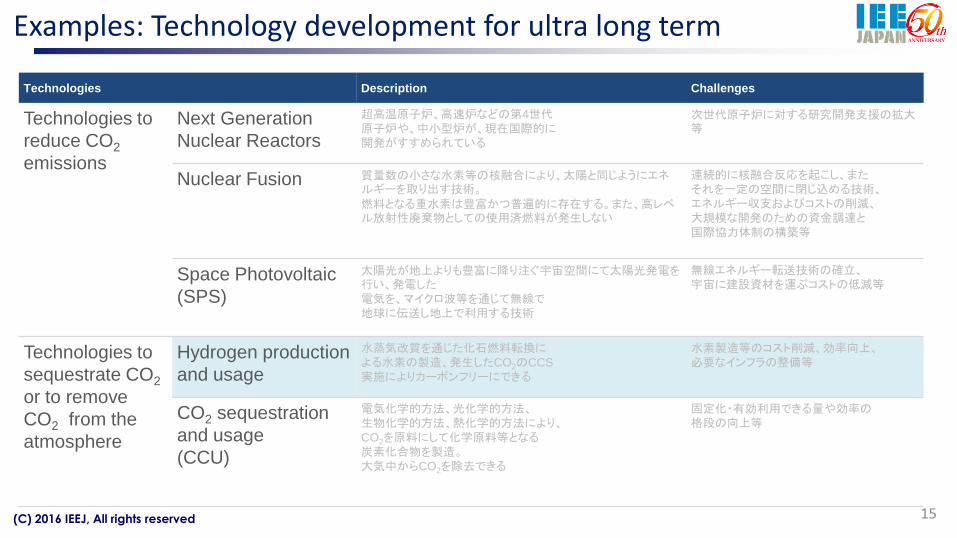

Examples: Technology development for ultra long term

15

Technologies Description Challenges

Technologies to

reduce CO2

emissions

Next Generation

Nuclear Reactors

超高温原子炉、高速炉などの第4世代原子炉や、中小型炉が、現在国際的に開発がすすめられている

次世代原子炉に対する研究開発支援の拡大等

Nuclear Fusion 質量数の小さな水素等の核融合により、太陽と同じようにエネルギーを取り出す技術。燃料となる重水素は豊富かつ普遍的に存在する。また、高レベル放射性廃棄物としての使用済燃料が発生しない

連続的に核融合反応を起こし、またそれを一定の空間に閉じ込める技術、エネルギー収支およびコストの削減、大規模な開発のための資金調達と国際協力体制の構築等

Space Photovoltaic

(SPS)

太陽光が地上よりも豊富に降り注ぐ宇宙空間にて太陽光発電を行い、発電した電気を、マイクロ波等を通じて無線で地球に伝送し地上で利用する技術

無線エネルギー転送技術の確立、宇宙に建設資材を運ぶコストの低減等

Technologies to

sequestrate CO2

or to remove

CO2 from the

atmosphere

Hydrogen production

and usage

水蒸気改質を通じた化石燃料転換による水素の製造、発生したCO2のCCS

実施によりカーボンフリーにできる

水素製造等のコスト削減、効率向上、必要なインフラの整備等

CO2 sequestration

and usage

(CCU)

電気化学的方法、光化学的方法、生物化学的方法、熱化学的方法により、CO2を原料にして化学原料等となる炭素化合物を製造。大気中からCO2を除去できる

固定化・有効利用できる量や効率の格段の向上等

(C) 2016 IEEJ, All rights reserved

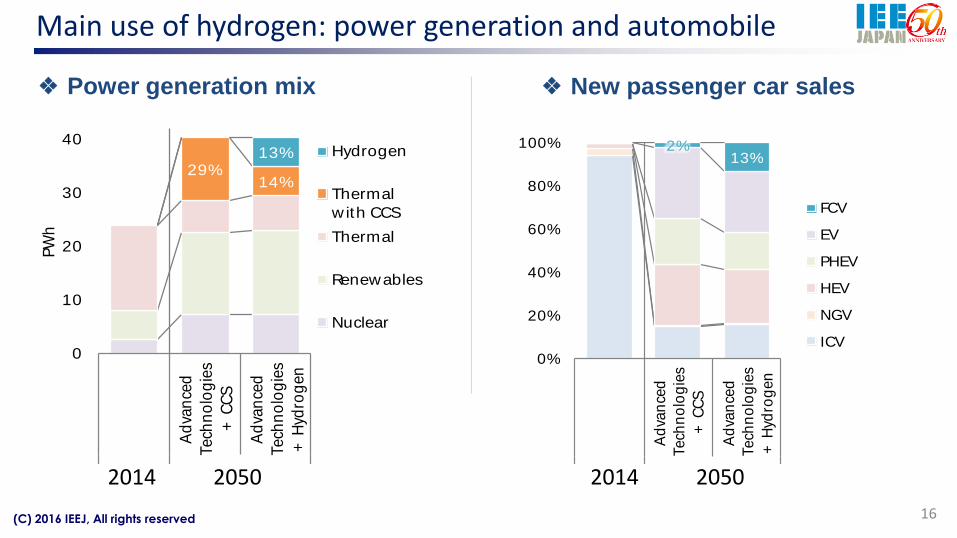

Main use of hydrogen: power generation and automobile

16

❖ Power generation mix ❖ New passenger car sales

29%14%

13%

0

10

20

30

40

Ad

van

ced

Tech

no

log

ies

+ C

CS

Ad

van

ced

Tech

no

log

ies

+ H

ydro

gen

PW

h

Hydrogen

Thermal

w ith CCS

Thermal

Renewables

Nuclear

2%13%

0%

20%

40%

60%

80%

100%

Ad

van

ced

Tech

no

log

ies

+ C

CS

Ad

van

ced

Tech

no

log

ies

+ H

ydro

gen

FCV

EV

PHEV

HEV

NGV

ICV

2014 2050 2014 2050

(C) 2016 IEEJ, All rights reserved

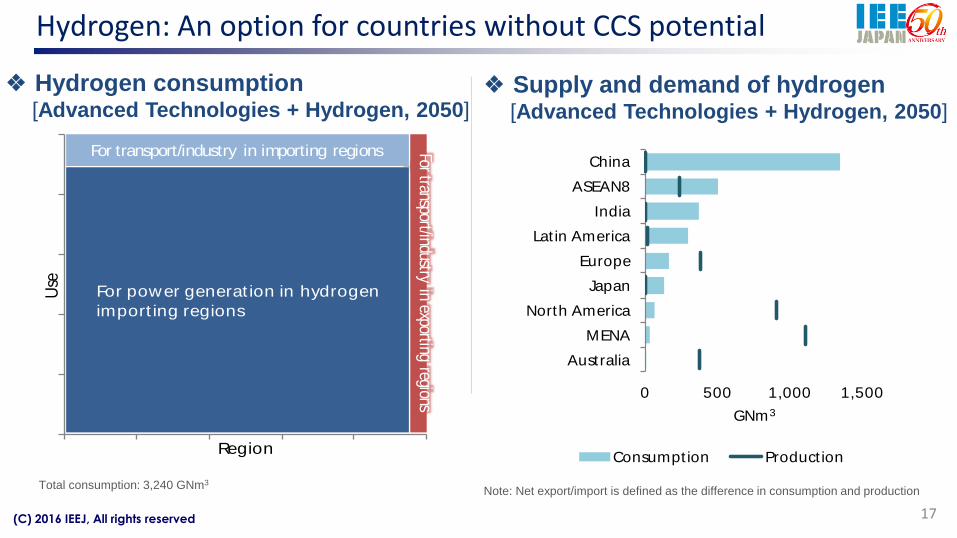

Use

Region

For power generat ion in hydrogen

import ing regions

For transport/industry in importing regions For transport/industry in exporting regions 0 500 1,000 1,500

Australia

MENA

North America

Japan

Europe

Lat in America

India

ASEAN8

China

GNm3

Consumpt ion Product ion

Hydrogen: An option for countries without CCS potential

17

❖ Supply and demand of hydrogen[Advanced Technologies + Hydrogen, 2050]

❖ Hydrogen consumption[Advanced Technologies + Hydrogen, 2050]

Note: Net export/import is defined as the difference in consumption and productionTotal consumption: 3,240 GNm3

(C) 2016 IEEJ, All rights reserved

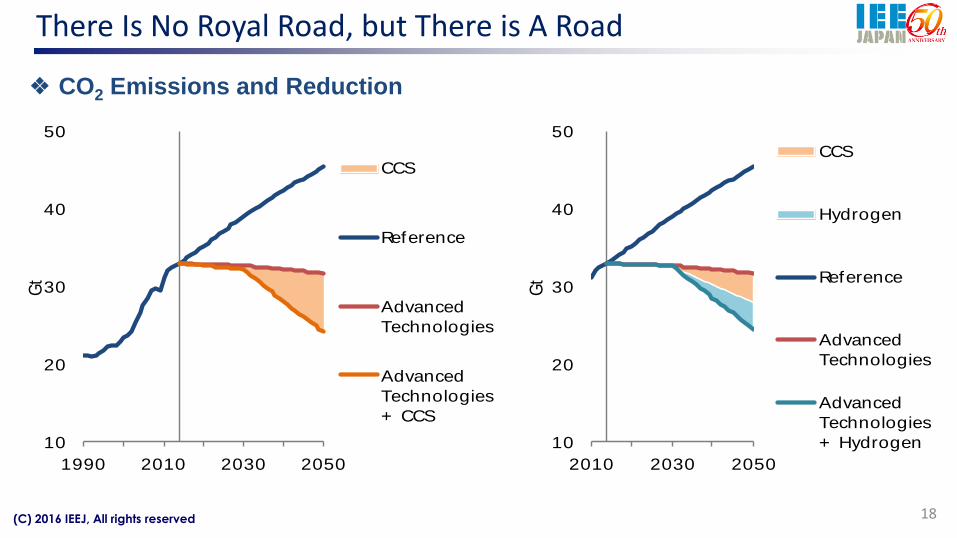

There Is No Royal Road, but There is A Road

18

❖ CO2 Emissions and Reduction

10

20

30

40

50

1990 2010 2030 2050

Gt

CCS

Reference

Advanced

Technologies

Advanced

Technologies

+ CCS

10

20

30

40

50

2010 2030 2050

Gt

CCS

Hydrogen

Reference

Advanced

Technologies

Advanced

Technologies

+ Hydrogen

(C) 2016 IEEJ, All rights reserved

IEEJ’s Asia/World Energy Outlook 2016Will be available at the site below:

http://eneken.ieej.or.jp/en/whatsnew/424.html

Asia/WorldEnergyOutlook2016

(C) 2016 IEEJ, All rights reserved

a) Will the current lower price situation induce demand for gasand expand Asian LNG market?

b) How will LNG and natural gas compete with other sources in the energy mix?

c) Will Japan achieve its “LNG Market Strategy” as announced in May 2016?

d) Based on recent market developments, are there new price indices available to buyers for price index diversification? How can an alternative price index be developed for the Asian LNG market?

e) What are the challenges ahead for LNG sellers and buyers? How can consumers and producers co-operate to increase LNG demand in Asia?

f) What are the differences between EU and Asian LNG markets in terms of creating LNG hubs in the region? What are the prospects of creating an LNG hub in Asia?

Some Points for Today’s Discussion

20

(C) 2016 IEEJ, All rights reserved

a) Will the current lower price situation induce demand for gasand expand Asian LNG market?

b) How will LNG and natural gas compete with other sources in the energy mix?

c) Will Japan achieve its “LNG Market Strategy” as announced in May 2016?

d) Based on recent market developments, are there new price indices available to buyers for price index diversification? How can an alternative price index be developed for the Asian LNG market?

e) What are the challenges ahead for LNG sellers and buyers? How can consumers and producers co-operate to increase LNG demand in Asia?

f) What are the differences between EU and Asian LNG markets in terms of creating LNG hubs in the region? What are the prospects of creating an LNG hub in Asia?

Today’s Panelists

21

Mr. Nandakumar PONNIYA Baker and McKenzie, Wong & Leow

Mr. Damien CRIDDLE The Global LNG Exchange (GLX)

Mr. Keita ENJOJITokyo Gas Asia

Dr. Xunpeng SHIEnergy Studies Institute National University of Singapore

(C) 2016 IEEJ, All rights reserved

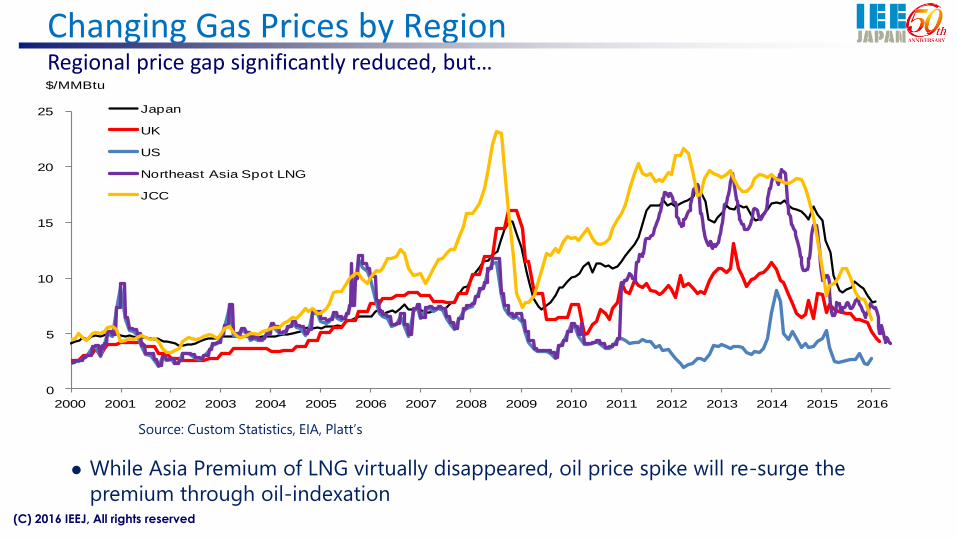

Changing Gas Prices by RegionRegional price gap significantly reduced, but…

0

5

10

15

20

25

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Japan

UK

US

Northeast Asia Spot LNG

JCC

$/MMBtu

Source: Custom Statistics, EIA, Platt’s

While Asia Premium of LNG virtually disappeared, oil price spike will re-surge the

premium through oil-indexation

(C) 2016 IEEJ, All rights reserved

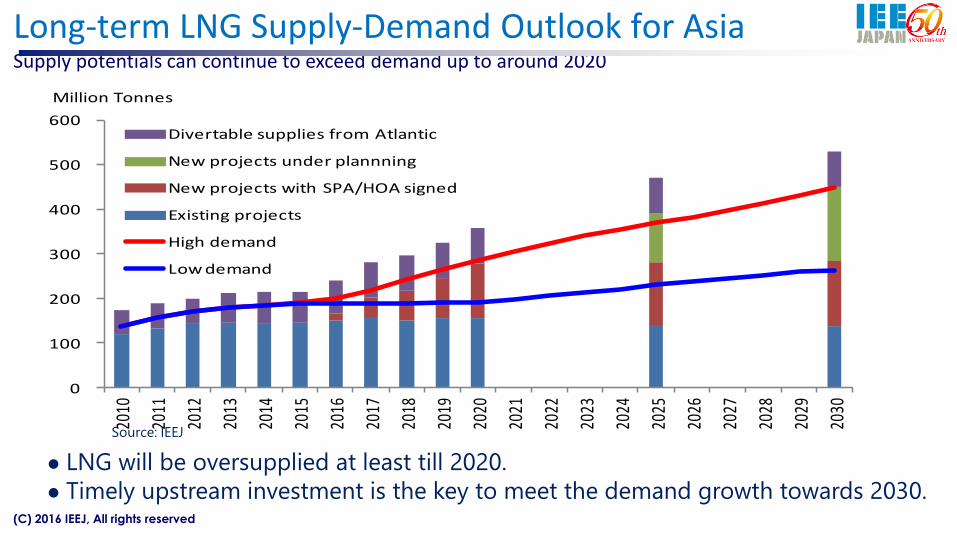

Long-term LNG Supply-Demand Outlook for AsiaSupply potentials can continue to exceed demand up to around 2020

Source: IEEJ

LNG will be oversupplied at least till 2020.

Timely upstream investment is the key to meet the demand growth towards 2030.

0

100

200

300

400

500

600 20

10

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

Divertable supplies from Atlantic

New projects under plannning

New projects with SPA/HOA signed

Existing projects

High demand

Low demand

Million Tonnes

(C) 2016 IEEJ, All rights reserved

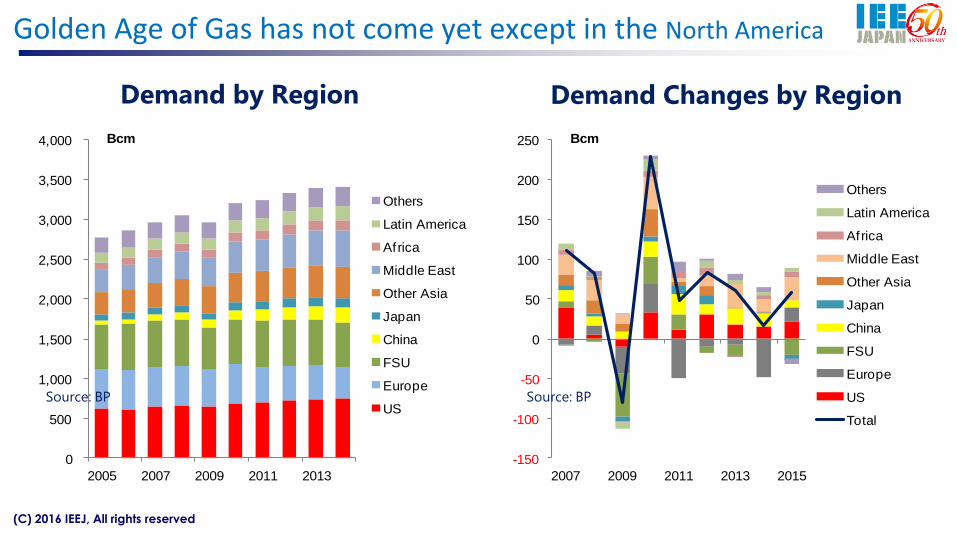

Golden Age of Gas has not come yet except in the North America

Demand by Region Demand Changes by Region

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2005 2007 2009 2011 2013

Bcm

Others

Latin America

Africa

Middle East

Other Asia

Japan

China

FSU

Europe

US

-150

-100

-50

0

50

100

150

200

250

2007 2009 2011 2013 2015

Bcm

Others

Latin America

Africa

Middle East

Other Asia

Japan

China

FSU

Europe

US

Total

Source: BP Source: BP

(C) 2016 IEEJ, All rights reserved

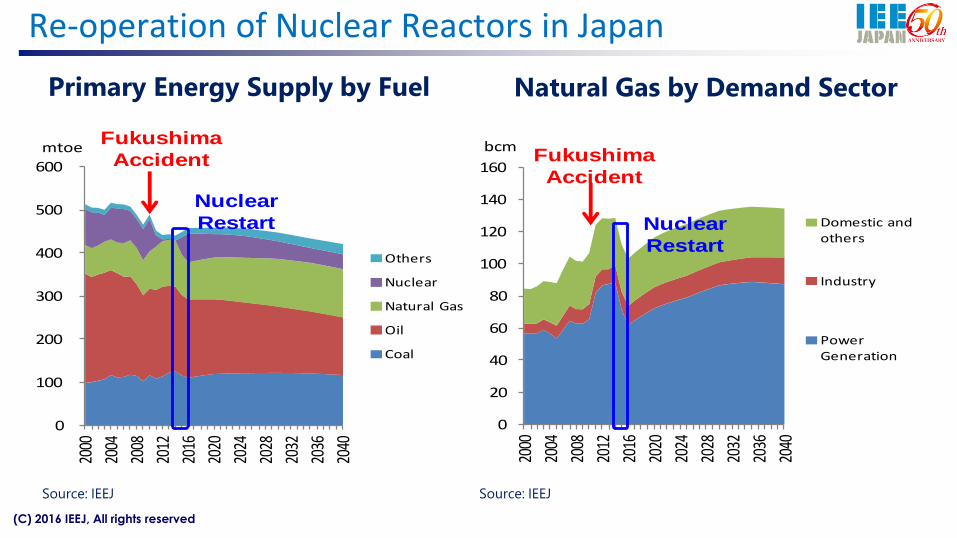

0

100

200

300

400

500

600

2000

2004

2008

2012

2016

2020

2024

2028

2032

2036

2040

Others

Nuclear

Natural Gas

Oil

Coal

mtoe

0

20

40

60

80

100

120

140

160

2000

2004

2008

2012

2016

2020

2024

2028

2032

2036

2040

Domestic and others

Industry

Power Generation

bcmFukushima

Accident Fukushima

Accident

Nuclear

Restart Nuclear

Restart

Re-operation of Nuclear Reactors in Japan

Primary Energy Supply by Fuel Natural Gas by Demand Sector

Source: IEEJ Source: IEEJ

(C) 2016 IEEJ, All rights reserved

METI’s Strategy for LNG Market : for Improved Transparency and Fluidity

Asian Premium of LNG has diminished significantly, but can widen again if oil prices

rise

Asia needs more rationale LNG pricing to reflect market fundamentals accurately

Calling for more liquid LNG market in Asia, the government formulated an LNG

strategy in May 2016, focusing on the following issues

Improved Tradability

Abolishing destination clause

Financial support for projects with supply flexibility

Benchmark Prices Reflecting Supply and Demand

Encouraging spot price discovery

LNG forward/futures at TOCOM

Open and Adequate Infrastructure Developments

More strict third party access

Incentives for infrastructure developments

26

(C) 2016 IEEJ, All rights reserved

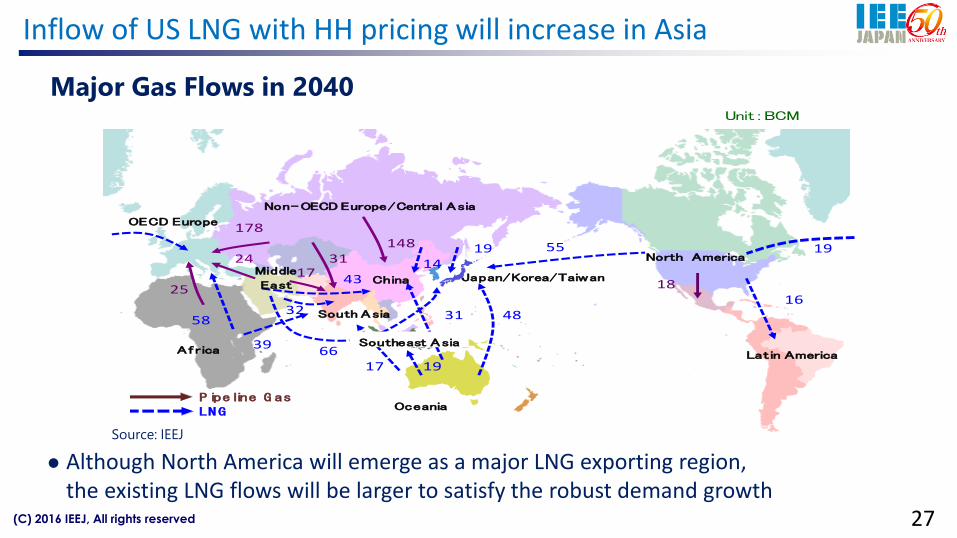

Inflow of US LNG with HH pricing will increase in Asia

19

Unit:BCM

55

31 4832

25

148178

58

19

1731

16

24 1443

66

North America

Latin America

Non-OECD Europe/Central Asia

Japan/Korea/TaiwanChina

Oceania

South Asia

Middle

East

Af rica

OECD Europe

39

18

1917

Southeast Asia

Pipeline G as

LNG

Source: IEEJ

Major Gas Flows in 2040

Although North America will emerge as a major LNG exporting region,the existing LNG flows will be larger to satisfy the robust demand growth

27

(C) 2016 IEEJ, All rights reserved

Spot/Short term trading is growing in Asia

Spot and Short-term Trades Spot Trades in 2015

Trinidad & Tobago, 63

Russia/Europe, 60

Nigeria, 56

Others, 42

Asia, 34

Middle East, 33

Total 332 cargoes

(2015 Actual)

28%

0%

5%

10%

15%

20%

25%

30%

35%

0

10

20

30

40

50

60

70

80

2000 2003 2006 2009 2012 2015

Middle EastLatin AmericaNorth AmericaEurope

Other Asia

China

India

Taiwan

Korea

Japan

Spot/short-term %

Million Tonnes

Source: GIIGNL Source: ICIS Heren

28

(C) 2016 IEEJ, All rights reserved

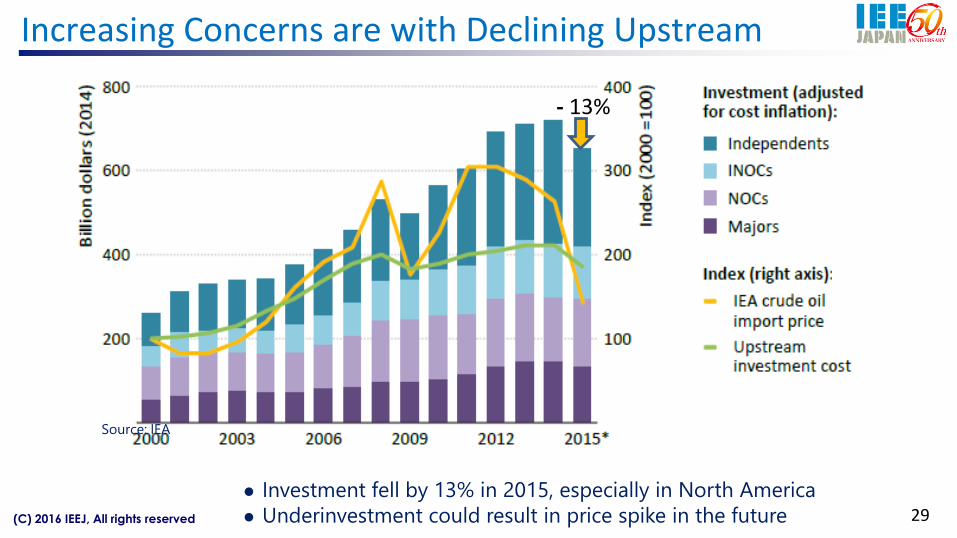

Increasing Concerns are with Declining Upstream

Source: IEA

Investment fell by 13% in 2015, especially in North America

Underinvestment could result in price spike in the future 29

- 13%

(C) 2016 IEEJ, All rights reserved

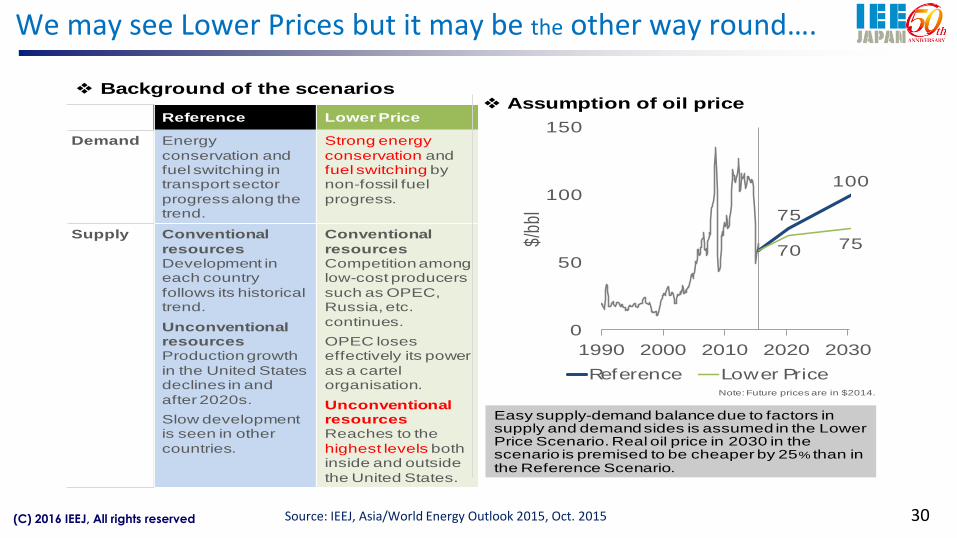

We may see Lower Prices but it may be the other way round….

Easy supply-demand balance due to factors in supply and demand sides is assumed in the Lower Price Scenario. Real oil price in 2030 in the scenario is premised to be cheaper by 25% than in the Reference Scenario.

❖ Background of the scenarios❖Assumption of oil price

Reference Lower Price

Demand Energy

conservation and fuel switching in transport sector

progress along the trend.

Strong energy

conservation and fuel switching by non-fossil fuel

progress.

Supply Conventional

resourcesDevelopment in each country

follows its historical trend.

Unconventional resourcesProduction growth

in the United States declines in and

after 2020s.

Slow development is seen in other

countries.

Conventional

resourcesCompetition among low-cost producers

such as OPEC, Russia, etc.

continues.

OPEC loses effectively its power

as a cartel organisation.

Unconventional resourcesReaches to the

highest levels both inside and outside

the United States.

Note: Future prices are in $2014.

75

100

70 75

0

50

100

150

1990 2000 2010 2020 2030

$/bb

l

Reference Lower Price

Source: IEEJ, Asia/World Energy Outlook 2015, Oct. 2015 30

(C) 2016 IEEJ, All rights reserved

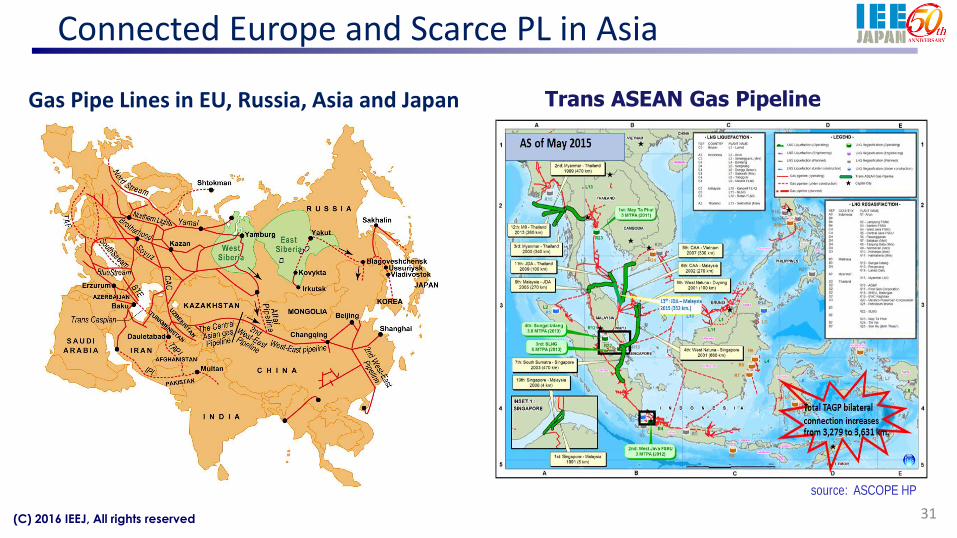

Connected Europe and Scarce PL in Asia

31

source: ASCOPE HP

Gas Pipe Lines in EU, Russia, Asia and Japan Trans ASEAN Gas Pipeline