original10 (1)

DESCRIPTION

banker customer relationshipTRANSCRIPT

1.1 MEANING:-

As soon as we open an account in a bank or the banker issue a draft or we deposit our

valuables in a bank, a relationship is created with the bank at that moment. However, the

relationships are not the same in all the cases. It means that for the different functions of

banks, the nature of relationship between the banker and the customer varies. The

commercial banks, their functions, different types of banks and the role played by the banks

in the economic development of a country. Now it will be appropriate to focus on the

relationship that exists between the banker and the customer in providing the different

services to the customers.

The word customer means a person who has bank account in his name and for whom the

banker undertakes to provide the facilities, which are enormously provided by banks. It must

also be remembered that all customers do not require all the services, i.e., an ordinary saver

does not require more sophisticated financial services but his banking needs are very much

limited.

Further, a customer needs banking services in that area which he lives or works for his

livelihood. Therefore, the aim of the banks should be to bring new areas and new

classes of people within their fold in order to tap potential deposits to optimum level

by providing wide range of banking services to the needs of different classes and

sectors of society and also by improvement in the quality and efficiency of services.

Efficiency and quality can be maintained not necessarily through automation alone

but through personal approach also. Thus in providing all these services, emphasis should be

laid on the quality of services rather than the quantity or variety of services. Banks

should try to understand the psychology of their customers while dealing with them. They

should satisfy their customers well so that not only their relationship with the banks

may continue but it will also become beneficial and pay dividends in the form of attracting

new customers to the banks. Thus, the relationship between the banker and customer is

not merely of debtors and creditors but it should also embrace the super added obligation

on the part of banker to honour the customer’s need effectively and efficiently.

The functions and services provided by banks to their customers give rise to certain

relationship between them, with the opening of an account by the customer with a banker.the

application for opening an account is considered as aletter of agreement for establishing the

banker-customer relationship. The application for opening an account is considered as aletter

of agreement for establishing the banker-customer relationship. Deposits are lifelines of

banks. The general view is that the banker-customer relationship is mainly that of a debtor

and a creditor with certain special features.

However, today the range of banking services is more extensive and indeed is expanding all

the time. So it must be expected that other relationships will arise besides that of debtor and

creditor. For instance, the relationship of principal and agent is present when the customer

instructs his bank to buy or sell stocks on his behalf and when items are held in safe-custody

the relationship is that of bailer and bailee. Where the bank’s executorships service takes on

the administration of a deceased’s estate, the relationship is that of trustee and beneficiary.

Duties akin to a trusteeship might also happen when a branch comes in to possession of funds

or property that belong to a third party, as when the bank has sold property in mortgage and

has a surplus to pass to the subsequent mortgage. Obviously, the relationship with the

customer in that situation is that of a mortgagor with a mortgagee on the customer.

The roads to progress and prosperity can easily be made through friendly behavior with the

customers. If the bankers wish to develop their organizational image, they have to offer better

services and cooperation, coupled with courteous service to gain a competitive edge. So the

relationships depend on the nature of transaction and changes from customer to customer. A

bank customer may be a creditor, a beneficiary and a bailor simultaneously when he/she

deposits money, remits money by mail transfer and/or forgets a document in the bank

inadvertently(not for security of any loan/advances).

Our primary concern will be to analyse the relationship that is created between a banker and

a customer on different occasions.

This unit will be interesting as you are going to learn the different aspects of the relationships

between the banker and the customer.

Banking is a trust-based relationship. There are numerous kinds of relationship between the

bank and the customer. The relationship between a banker and a customer depends on the

type of transaction. Thus the relationship is based on contract, and on certain terms and

conditions.

These relationships confer certain rights and obligations both on the part of the banker and on

the customer. However, the personal relationship between the bank and its customers is the

long lasting relationship. Some banks even say that they have generation-to-generation

banking relationship with their customers. The banker customer relationship is fiducial

relationship. The terms and conditions governing the relationship is not be leaked by the

banker to a third party.

1.2 OBJECTIVE OF STUDY:-

-The general objective is to explain the essentials of Banking operations and all forms of

relationships that may exist between a banker and customer.

The operational procedures in the present day banking operations.

The reciprocal rights and duties between a banker and a customer.

The different types of accounts and rules governing their conduct.

-The topic will give the definition of relevant concepts: Bank, Banker and Customer. The

fundamental relationship between a banker and a customer, and the different kinds of special

relationships that exist between the two parties.

-Also, the topic will go further to describe mandates which customers fill when opening bank

accounts.

-To examine the basic duties of a banker to a customer and vice-versa as well as the rights

which a customer has over the bank.

-To examine the implication of the duty of confidentiality (Secrecy) which the bankers owe

to its customers.

-The right of Bank to exercise lien over customers property in case of default, the

right of set-off and the right to appropriate payments.

-The roles the banks play and their responsibility in rendering these services.

-Enumerate the precautions to be taken by the bank while disclosing the information

regarding the customer.

-To explain how the relationship between the customer and banker comes to an end.

1.3 DATA COLLECTION

Primary data:-

The primary data survey done on the topic of banker-customer relationship which is on the customer point of view which are the services provided by the bank to the customer.

1.4 LIMITATION

Banker, businessman and even common man and women are dealing with loans and

advances. As the provisions of the limitation act,1963, a debt will become a bad debt after the

expity of 3 years from the date of the debt. The implication is that the debtor need not legally

pay the debt once 3 years are over provided there was no contract between the debtor and

creditor. But the banker is exempted from the limitation act. According to Article 122 of the

part II of the schedule to the limitation act 1963, the period of limitation for the refund of

bank deposits is 3 years with effect from the date of a customer making a demand for his

money. Sec 26 of the banking regulation act, 1949, has prescribed a period of 10 years to

consider a banking debt as bad debt. In the case of fixed deposit, a period of 10 years will be

calculated from the date of expiring of such fixed deposit. This is an advantage to the

customer. However, in the case of overdraft, the period of 3 years will commence from the

date on which it is made use of by the customer. In the case of safe custody deposit, the law

of limitation period commences from the date of demand.

The main problems is customer, services is to identify customers, expectations

and devising ways and means of meeting the reasonable ones.

banker has no general lien

1) On safe custody deposits.

2) On securities or bills of exchange entrusted for specific purpose.

3) On articles lefty by mistake or negligence.

4) On deposit account.

5) On stolen bond.

6) Until due date of the loan.

7) On trust account.

8) On title deeds of immovable properties.

Every times, a customer goes to a banker and casts a vote of confidence in him or

her. It is now up to the banker to keep faith with him.

There may be certain amount of risk involved in some of the service

expectations of customers, which can be reduced if the working of banks is based on trust,

character and capacity of the customers and staff. Lack of effective communication is also a

major problem.

There must be a two-way communication among customers, employees and will

motivate them to render satisfactory services to the customer.

CHAPTER NO.2 REVIEW OF LITERATURE

The significance of banks in modern market economies cannot be underestimated. Like any

other economy, banks have a very crucial role to play in the functioning of the markets.

Generally, the term bank and banker are used interchangeably. The bank is used strictly to

refer to the corporate body while the term banker may mean both the institution and the

individuals that work within the corporation. The relationship between a banker and a

customer depends on the activities, products or services provided by the bank to its

customers. Thus the relationship between a banker and its customers is a transactional

relationship. Bank’s business depends much on the strong bond with its customers. “Trust”

plays an important role in building healthy relationship between a banker and customer. Dr

H.L Hart, in the book, Law of Banking defines a bank/banker:

As a person or company carrying on the business of receiving money and collecting drafts for

customers subject to the obligation of honoring cheques drawn upon them from time to time

by customers to the extent of the amount available on their current account.

Section 2 of the UK Bill of Exchange Act 1882 provides that a banker is “any person whether

corporate or not who carries on the business of banking“. Similarly Section 258 (the

interpretation section) of the Nigerian Evidence Act 2011 defines Bank/Banker to mean a

bank licensed under the Banks and Other Financial Institutions Act Cap. B3LFN. 2004 and

includes anybody authorized under an enactment to carry on banking business.

A person becomes a customer of a bank when he goes to the bank and has an account opened

in his name, the bank accepts the money or cheque from him after which such a person

becomes entitled to be called a customer of the bank. A customer is also any person having

an account with a bank or for whom a bank has agreed to collect items and it includes a bank

having an account with another bank. This definition was held in the Court of Appeal case of

Oku V. Banigo (2003) FWLR (Pt. 175).

In Afribank Nigeria Plc V. Aminu Ishola Investment Ltd (2002) 7 NWLR (Pt. 765) 40, it was

held that the role or predominant business of bankers is the business of banking which

consists mainly in the receipt of monies on current or deposit account and the payment of

cheques issued by a customer. Therefore, the receipt of money from or on account of his

customer by a banker constitutes the banker as the debtor of the customer and the banker

undertakes to pay the money thus due from him to the customer against written orders of the

customer. Accordingly, the relationship so constituted is that of principal and agent and

therefore a cheque drawn on the banker by the customer represents the order of the principal

to his agent to pay, out of the principal's money in his hands, the amount stated on the cheque

to the payee endorsed on the cheque. See also the case of Balogun v. NBN (1978) 11 NSCC

135

Today in the economy of any country banks play a vital role. One cannot think of

the development of any nation without active assistance rendered by the banking and

financial institutions. Banking is a service industry and the bankers are expected to

give top priority to provide satisfactory service to their customers. Whether anyone is a

depositor, a borrower or any other person using other services provided by the banks,

the motto should be “Customer Satisfaction.”

The main thing, which a bank is providing, is “service” and the product of bank’s work

and its success depends on the range and the quality of the services it can provide to

the customers. To find out the present state of affairs and to suggest further new ways for the

next millennium, a survey of the city of certain banks in the city of Udaipur has been

undertaken. The researcher is of the opinion that there is indeed a need for proper

legislation to deal with the distinctive feature of banking business.

Prior to nationalization of the banks in July 1969, banks were very much market friendly

and even guiding the customers by giving personalized service by acting as their philosopher

and guide. But now the position is reverse and the table is turned. That’s why the public is

clamoring for the privatization of the banks to see at least the personalized service period of

the pre-nationalization era when the bankers were hearing the customers and were marketing

friendly.

Following are the instances when the bankers are unfriendly:

1. When parties go to bank, even on their own request for opening account no body helps

them.

2. There is no attitude of advance market friendliness in most of the branches and the

customers are neither even aware of the advance schemes nor do they know how to

prepare their projects or fill up the application forms.

3. Now-a-days, bankers are treating entry of customers into branch premises as a

nuisance.There who come for cash drafts are turned away. Even small notes brought by the

customers are not accepted by the banks.

If the bankers do not mend their ways and become market friendly as during the

prenationalization days, the days are not far off, the bank customer to form an association of

their own in their districts, states and at the national level to resist and control high handed

dis-service imparted across the counters to the customers in particular and at the public at

large. The banker-customer relationship is contractual. The relationship should not be merely

be of debtors and creditors, but it should also embrace the super-added obligations on the part

of the banker to humor the customer’s need effectively and efficiently. In this era smooth

functioning of banks depends too much on the relations between the banker and the

customers.

CHAPTER NO.3 BANK ACCOUNT AND SPECIAL TYPE OF CUSTOMERS

The relationship between a banker and a customer is of great significance. It depends upon

the services rendered by the banker to the customer. The relationship between a banker and a

customer depends on the activities; products or services provided by bank to its customers or

availed by the customer. Thus the relationship between a banker and customer is the

transactional relationship. Bank’s business depends much on the strong bondage with the

customer. “Trust” plays an important role in building healthy relationship between a banker

and customer.

Definition of banker

The Banking Regulations Act (B R Act) 1949 does not define the term ‘banker’ but defines

what banking is?

As per Sec.5 (b) of the B R Act “Banking' means accepting, for the purpose of lending or

investment, of deposits of money from the public repayable on demand or otherwise and

withdrawable by cheque, draft, order or otherwise."

According to section 3 of the NI Act, 1881, banker includes any person acting as a banker

and any post office savings bank.

To sum up a banker is who

1) Take deposit account

2) Take current accounts

3) Issue and pay cheques

4) Collect cheques crossed and uncrossed for his customers.

Money lender is not considered as a banker as mere lending does not constitute banking

business. Banker is an institution which borrows money by accepting deposits from the

public for the purpose of lending to those who are in need of money.

According to Sec. 2 of the Bill of Exchange Act, 1882, ‘banker includes a body of persons,

whether incorporated or not who carry on the business of banking.’

Sec.5(c) of BR Act defines "banking company" as a company that transacts the business of

banking in India. Since a banker or a banking company undertakes banking related activities

we can derive the meaning of banker or a banking company from Sec 5(b) as a body

corporate that:

(a) Accepts deposits from public.

(b) Lends or

(c) Invests the money so collected by way of deposits.

(d) Allows withdrawals of deposits on demand or by any other means.

Accepting deposits from the ‘public’ means that a bank accepts deposits from anyone who

offers money for the purpose. Unless a person has an account with the bank, it does not

accept deposit. For depositing or borrowing money there has to be an account relationship

with the bank. A bank can refuse to open an account for undesirable persons. It is banks right

to open an account. Reserve Bank of India has stipulated certain norms “Know Your

Customer” (KYC) guidelines for opening account and banks have to strictly follow them.

In addition to the activities mentioned in Sec.5 (b) of B R Act, banks can also carry out

activities mentioned in Sec. 6 of the Act.

Definition of customer

The term customer is not defined by law. Ordinarily, a person who has an account in a bank

is called a customer.

The term Customer has not been defined by any act. The word ‘customer’ has been derived

from the word ‘custom’, which means a ‘habit or tendency’ to-do certain things in a regular

or a particular manner’s . In terms of Sec.131 of Negotiable Instrument Act, when a banker

receives payment of a crossed cheque in good faith and without negligence for a customer,

the bank does not incur any liability to the true owner of the cheque by reason only of having

received such payment. It obviously means that to become a customer account relationship is

must. Account relationship is a contractual relationship.

It is generally believed that any individual or an organisation, which conducts banking

transactions with a bank, is the customer of bank. However, there are many persons who do

utilize services of banks, but do not maintain any account with the bank.

Thus bank customers can be categorized in to four broad categories as under:

(a)Those who maintain account relationship with banks i.e. Existing customers.

(b)Those who had account relationship with bank i.e. Former Customers

(c)Those who do not maintain any account relationship with the bank but frequently

visit branch of a bank for availing banking facilities such as for purchasing a

draft, encashing a cheque, etc. Technically they are not customers, as they do

not maintain any account with the bank branch.

(d)Prospective/ Potential customers: Those who intend to have account relationship

with the bank. A person will be deemed to be a 'customer' even if he had only

handed over the account opening form duly filled in and signed by him to the bank

and the bank has accepted the it for opening the account, even though no

account has actually been opened by the bank in its books or record.

The practice followed by banks in the past was that for opening account there has to be an

initial deposit in cash. However the condition of initial cash deposit for opening the account

appears to have been dispensed with the opening of ‘No Frill’ account by banks as per

directives of Reserve Bank of India. ‘No Frill’ accounts are opened with ‘Nil’ or with meager

balance.

The term 'customer' is used only with respect to the branch, where the account is

maintained. He cannot be treated as a ‘customer' for other branches of the same bank.

However with the implementation of’ ‘Core Banking Solution’ the customer is the customer

of the bank and not of a particular branch as he can operate his account from any branch of

the bank and from anywhere. In the event of arising any cause of action, the customer is

required to approach the branch with which it had opened account and not with any other

branch.

According to Dr. Hart, “a customer is one who has an account with a banker or for whom

a banker habitually undertakes to act as such.

Thus to constitute a customer, the following essential requisites must be fulfilled:

1) He must have some sort of an account.

2) Even a single transaction constitutes a customer.

3) The dealing must be of a banking nature.

A customer need not be a person. A firm, joint stock company, a society or any separate

legal entity may be a customer. Explanation to section 45-Z of the BR Act clarifies that a

customer includes a Government department and a corporation incorporated by or under any

law.

Types of Customer’s Account

Introduction of the prospective customer and preliminary investigations (know your customer

KYC)

Obtaining specimen Signatures

Mandate regarding operation of Account

Allocating Account number

Preliminary investigations /Introduction of Account

Introduction of a new account refers to proper investigations about the credentials of

prospective account holder by the banker. If proper introduction not obtained it would

tantamount to negligence on the part of banker. Retention of photo copy of CNIC of Account

Holder as well as introducer of account after verifying from originals.

Why Introduction & Preliminary Investigation:

(a). To avoid frauds

(b).Safeguard against unintended/inadvertent credits to an account by mistake, in case banker has

conducted proper preliminary investigations and obtained introduction it would be help in

follow up process

Negligence in seeking proper introduction & making necessary preliminary investigations

leads to deprivation of banker from seeking protection of law U/S 131 of Negotiable

Instruments Act 1881.

Inquiries about client (credit Reports/status inquiries) furnished by banks. In case

account opened by a banker without proper inquiries—the bank furnishing status inquiries

/etc. may at times launch itself into trouble.

Specimen Signatures:

If forged signatures on a Cheque entertained & Cheque passed by bank--bank shall be legally

responsible to make good the loss to Account Holder

Opening of Account of an Illiterate Person:

Photograph on S.S Card

Thump impression in the presence of bank officer to be affixed.

L.T.I (Gents)

R.T.I (Ladies)

Type of Accounts:

Individual’s Account

Joint Account

Minor’s Account

Legal Issues with respect to individual’s Account:

A banker’s authority to pay cheques is revoked in the following situations as per provisions

contained in section 122-A of Negotiable Instruments Act, 1881:

Countermand of payment (stop payment)

Notice of customer’s death

Notice of Adjudication of the Customer as insolvent

Joint Accounts

These accounts are not to be treated as partnership accounts. These are the accounts opened

in the name of two or more persons who are not partners

Operations of Joint Account:

--The mandate must bear the signatures of all the account holders.

Can be operated jointly by all the account holders

Can be operated by any one or more persons authorized to operate the account

Either or Survivor /s mandate.

Stop Payment Instructions in a Joint Account

Any one of the joint account holders can give stop payment instructions of any cheque to the

bank; however, for reinstatement of the payment of such cheque, such instructions must bear

signatures of all the account holders.

Minor’s Account

Minor does not have legal capacity to enter into a contract. As we know that legal

relationship between banker and his customer is a contractual relationship, as such minor is

not qualified under law to open an account. However, an account in the name of minor can be

opened when guardian of the minor shall operate this account. According to law, minor is a

person who has not attained the age of 18 years. Furthermore under section 3 of majority Act

1875, if a guardian is appointed by the court in respect of a person before he attains the age of

18 years, the majority extends to the age of 21 years.

Classified Accounts of the Customers

Partnership Account

Companies Account

Account of Clubs, Societies & Associations.

Agents’ Account

Trust Account

Executors & Administrators’ Account

Accounts of Local Bodies

Partnership Account:

“Partnership” is the relation between persons who have agreed to share the profits of a

business carried on by all or any of them acting for all Right to sue vests in registered firm.

Partner is treated as an agent of firm (Section 18 of Partnership Act. 1932) however; partner

has no authority to open an account on behalf of the firm (Section 19-2B)

Survivorship mandate

Joint and several mandates

Admission of new partner—responsibilities of incoming partner start from the date of

admission unless not otherwise agreed.

Bankruptcy of a partner-- ordinarily partnership stands dissolved.

Insolvency of firm—business of partnership vests in official receiver appointed by court,

operations in account are stopped, personal accounts of partners are also declared inoperative.

Accounts of Companies

Documents Required:

Resolution passed by Board of Directors for opening the account

Copy of Memorandum of Association

Copy of Articles of Association

Certificate of Incorporation

Certificate of commencement of business

Balance Sheet.

Operation of the account in line with the instructions contained in the board of directors

resolution, authorized directors to operate the account.

In case of winding up of a company, bank should stop operations in the account.

Accounts of Clubs, Societies & Association

Resolution passed by managing committee/executive committee/Governing body etc.

Certified copy of by- laws/rules

Signatures of the persons authorized to operate account.

Agent Account

Agent acts on behalf of the principal.

Agent can open an account under the authority of principal—based on power of attorney.

On revocation of power of attorney operation in the account will stand inoperative.

In case death of the agent operations should be stopped immediately however, Principal can

sign the cheques and the same are honored by the banks.

Account of Trusts:

Trusts are governed by Trust Act-1882

Any person who is competent to contract may create a trust.

Opening of Account

Account is opened in the name of the Trust.

All trustees to sign account opening form.

Executors & Administrator's Account

Executor is a person who is entrusted responsibilities of executing WILL.

An administrator is a person appointed by a court to look after the estate of a person who died

without leaving a WILL or the person appointed as executor is not competent to perform the

contract (for example minors, insolvent, lunatics)

The banks must carefully study the contents of the WILL before opening an account of

Executor/Administrator.

Accounts of Local Bodies:

The accounts must be in conformity with local bodies law/rules.

The request for opening an account must be made by competent authority.

‘Know Your Customer’ Guidelines and Customer:

Let us discuss another important aspect of banker- customer relation i.e. certain guidelines

that the banker has to follow when a customer opens accounts in the bank.. You are aware

that the relationship between the banker and the customer is created as soon as the customer

opens an account in the bank.

The RBI has issued certain guidelines for the management of the commercial banks. These

guidelines that bankers follow are known as Know Your Customer (KYC) Guidelines.

The Reserve Bank of India has issued these guidelines with the objectives of

Identifying depositors;

controlling financial frauds;

identifying money laundering and suspicious activities;

monitoring of large value cash transactions; and

preventing misuse of banking system for committing frauds.

The RBI has issued KYC guidelines for various aspects like, guidelines for new accounts,

existing customers, risk management and monitoring procedures, record keeping etc. In this

unit we will discuss the KYC Guidelines in respect of new customers and existing customers.

KYC Guidelines for new accounts-

The banker must comply with these guidelines when an individual or a corporation applies

for opening account in the bank-

The banker must verify the identity of a customer while opening an account. The new

customer while opening an account in a bank may give reference of an existing accountholder

or the person known to the bank as reference for his identification. The banker can also verify

the identity of the customer on the basis of the documents, such as – passport, driving license

etc. supplied by the new customer.

The Board of Directors of the banks should establish proper procedure to verify the

identification of the new customer and to monitor the suspicious nature of transactions in

accounts.

KYC Guidelines for existing accounts-

In case of existing customers, it is expected that bank had adopted appropriate KYC norms

while opening the accounts. In case of any default, the required norms should be completed at

the earliest.

Ceiling and monitoring of cash transactions

As per RBI guidelines issued under Section 35 (A) of the Banking Regulation Act, 1949:

(i)Banks are required to issue travellers cheques, demand drafts, mail transfers, and

telegraphic transfers for Rs.50, 000 and above only by debit to customers’ accounts or against

cheques and not against cash. While purchasing travellers cheques, demand drafts, mail

transfers, and telegraphic transfers for Rs.50, 000 and above purchaser has to mention his

Permanent Income Tax Account Number (PAN) on the application.

(ii) The banks are required to keep a close watch of cash withdrawals and deposits for Rs.10

lakhs and above in deposit, cash credit or overdraft accounts and keep record of details of

these large cash transactions in a separate register. Branches of banks are required to report

all cash deposits and withdrawals of Rs.10 lakhs and above as well as transactions of

suspicious nature with full details in fortnightly statements to their controlling offices.

Bankers’ Fair Practice Code:

Indian Banks’ Association has prepared a code, which sets standards of fair banking

practices. This document is a broad framework under which the rights of common depositors

are recognized. It is a voluntary Code that promotes competition and encourages market

forces to achieve higher operating standards for the benefit of customers. The Code applies to

current, savings and all other deposit accounts, collection and remittance services offered by

the banks, loans and overdrafts, foreign-exchange services, card products and third party

products offered by banks.

DUTIES OF BANKER

1) The banker should receive the customer’s money and credit his account.

2) He should receive cheques and bills sent by his customer for collection and the credit his

customer’s account without delay.

3) He should return the deposit as per the contract; he should honour customer’s cheques to

the extent of his balance in the account. He should use reasonable care in paying cheques

drawn upon him by his customers, to refrain from any action likely damage his customer’s

reputation.

4) He should maintain the secrecy of his customer’s account.

5) He should observe the customer’s instruction as mentioned in the mandate.

6) He should give reasonable notice before combining the accounts of his customer or closing

his account.

RIGHTS OF BANKER

A banker has certain obligations to the customers. At the same time banks enjoy certain rights

also. Now we will discuss some rights of the banker in relation to the bank accounts

maintained in a bank.

• Banker’s lien: In sub section 11.4.2 we have discussed the creditor and debtor

relationship between the banker and the customer, where the banker is the creditor and the

customer is the debtor. This relationship arises when an amount remains due by the customer

(debtor) to the banker (creditor). The banker can exercise his right of general lien by retaining

the properties of the customer till all the dues are paid by the customer. In the absence of any

agreement to the contrary, the banker can retain any goods and securities for general balance

of accounts. However, the banker cannot exercise this right over the goods or securities

which he has received in the capacity of agent or trustee of the customer.

• Rights of set- off: The right of set-off is a right to adjust the accounts between two

parties- creditor and the debtor. On the basis of right of set- off, the banker can adjust the

credit balance in the customer’s account against the amount due to the banker i.e. any debit

balance in the customer’s account. When a customer maintains two accounts in the same

capacity, the right of set- off enables the banker to combine the two accounts and adjust the

amount due from the customer. The banker can exercise this right if there is no agreement to

the contrary between them. In exercising this right, the banker must serve a notice to the

customer.

• Right of appropriation: When a debtor (customer) makes payment to a creditor

(banker), the debtor can instruct the creditor to adjust the amount for discharge of a particular

debt. If the debtor does not give any instruction to the creditor regarding the adjustment, the

creditor has the right to appropriate the amount against any debt. The creditor must inform

the debtor regarding such appropriation.

.Right to charge interest, commission, incidental charges etc. :Banker has an implied right to

charge for services rendered and sold to a customer. Bank charges interest on amount

advanced, processing charges for the advance, charges for non-utilization of credit facilities

sanctioned, charges commission, exchange, incidental charges etc. depending on the terms

and conditions of advance banks charge interest at monthly, quarterly or semiannually or

annually. Banks charge customers if the balance in deposit account falls below the prescribed

amount. Usually the bank informs such charges to the customer by various means.

• Rights under Garnishee Order: Generally a banker has the obligation to honour the

cheques of his customer. But in case a garnishee order is issued by the court, the banker

cannot make any payment from the account of the customer. The obligation of the banker to

honour the cheques stand suspended in that case.

Let us see how a garnishee order can affect the relationship between the banker and the

customer. Suppose Mr. A is the customer of SBI. He has taken a loan from his friend Mr. B.

But Mr. A fails to repay the loan to Mr. B and as a result Mr. B files a case against Mr. A.

Now Mr. B requests the court to issue an order on the bank of Mr. A directing the banker

(SBI) not to make any payment from the available balance in the account of Mr. A. If the

court issues such an order, it is known as ‘Garnishee Order’. Here, Mr. A (debtor) is known

as ‘judgement debtor’, Mr. B (creditor) is known as ‘judgement creditor’ and the SBI is

known as ‘garnishee’

General obligations of banker towards customer

Obligation to honour cheques- banker accepts the deposits from the customer with an

obligation to repay it to him on demand or otherwise. The banker is therefore under a

statutory obligation to honour his customer’s cheques because, it is recognized under section

31 of the NI Act, 1881-

The drawee of a cheque having sufficient funds of the drawer in his hands properly

applicable to the payment of such cheque must pay the cheque when duly required so to do,

and, in default of such payment, must compensate the drawer for any loss or damage caused

by such default.

Thus the banker is bound to honour his customer’s cheques provided the following

conditions are fulfilled-

(a) Sufficient balance in customer’s account

(b) Presentation of cheques within working hours of business

(c) Presentation of cheques within reasonable time after ostensible date of its issue

(d) Cheques should be presented at the branch where account is kept

(e) Fulfilment of requirements of law

Obligation to maintain secrecy and disclosure of information required by law- the banker is

under an obligation to take utmost care in keeping secrecy about the accounts of the

customers since it may affect his reputation, credit-worthiness and business. It was firmly laid

down in Tournier v. National Provincial and Union Bank of England Ltd. in India it was

made compulsory after 1970. The duty to maintain secrecy will be continuing even after the

account is closed or the death of the customer. This obligation is subject to certain

exceptions.

Obligation to keep a proper record of transactions- the banker must keep a proper record of

transactions of the customer. If he wrongly credits the account of the customer and intimates

him with the same and the customer acts upon the intimation bonafide and withdraws cash

the banker cannot contend that the entries were wrongly made. He shall not succeed in

recovery of money from the customer.

Obligation to abide by the instructions of the customer- the banker must abide by any

express instructions of the customer provided it is within the scope of their banker-customer

relationship. In the absence of any express instructions, the banker must according to

prevailing usages at the place where the banker conducts his business.

Customer’s obligations to his bank

The main customer’s obligations to his are:

-The customer is under the duty to exercise reasonable care when drawing his cheques, to

help prevent fraud or forgery,

-The customer must go to his bank when he requires payment; it is not the incumbent on the

banker to seek out the customer,

-Before drawing the cheques, the customer must ensure his account is put in funds to meet it,

-A customer must pay reasonable interest and commission and other charges for banking

services and this is implied when he/she opens an accout.

CHAPTER NO.4 RELATIONSHIP BETWEEN BANKER AND CUSTOMER

Classification of Relationship:

The relationship between a bank and its customers can be broadly categorized in to General

Relationship and Special Relationship.

If we look at Sec 5(b) of Banking Regulation Act, we would notice that bank’s business

hovers around accepting of deposits for the purposes of lending. Thus the relationship arising

out of these two main activities are known as General Relationship. In addition to these two

activities banks also undertake other activities mentioned in Sec.6 of Banking Regulation

Act. Relationship arising out of the activities mentioned in Sec.6 of the act is termed as

special relationship.

General Relationship:

1.Debtor-Creditor:

When a customer deposits money with his bank, the customer becomes a lender and the bank

becomes a borrower . the money handed over to the bank is a debt. The relationship between

the banker and the customer is that of a debtor and a creditor. The features of this relationship

are:-

a)the money is lent to the bank and the bank is free to use it in a way most beneficial to it.

The bank is not bound to keep such money intact. It is not bound to return the notes and coins

of the same denomination as it was deposited.

b)demand of payment should made by the customer. The banker is not required to repay the

debt voluntarily, unlike in the case of commercial debt.

c)demand should be made at the branch where the account exists. Except in the case of drafts,

travellers cheque, ATM/credit card etc., the bank is not required to make the payment to the

customer elsewhere (at other centres), although all the branches of a bank are constituents of

the same bank .in the above case. It was held that although the branches were agencies of one

principal bank, they were distinct for payment of customer’s cheques.

d)the demand should be made in a proper manner. The customer should demand payment not

verbally or by a mere telephone call but by cheque, draft, withdrawal form, order or

otherwise, further, Negotiable Instruments Act,1881,respectively.

2. Creditor–Debtor

Overdrawing the account: you have come across that that the current accountholders get

overdraft facility from the bank. Under this facility the accountholder can overdraw his

account i.e. withdraw more money than the balance available in the account. In case the

accountholder overdraws the account, the relationship between the banker and the customer

gets the shape of creditor and debtor relationship- the banker is the creditor and the

accountholder (customer) is the debtor. Till the overdrawn amount is returned by the

customer, the relationship between the two continues to be of creditor and debtor. As soon as

the overdrawn amount is returned by the customer, the relationship gets its original shape i.e.

banker becomes the debtor and the accountholder becomes the creditor.

Lending money to the customer:

Lending money is the most important activities of a bank. The resources mobilized by banks

are utilized for lending operations. Customer who borrows money from bank owns money to

the bank. In the case of any loan/advances account, the banker is the creditor and the

customer is the debtor. When a bank sanctions a loan to a customer, the relationship between

the two is that of the creditor and the debtor. The creditor (banker) charges interest on the

loan till it is paid back by the customer. When the loan is paid back fully, the relationship

reverses and gets the original shape of debtor (banker) and creditor (customer).

Special Relationship:

1.Relationship of Trustee and Beneficiary:-

Besides the debtor- creditor relationship between the banker and the customer, some other

types of relationships also exist between the two, depending on the services provided by the

bank. One of such relationships is that of trustee and beneficiary.

Perhaps you are aware that banks provide some services under which the customers can

keep their valuables like jewellery, share certificate etc. in safe custody of the bank. A trustee

holds property for the beneficiary, and the profit earned from this property belongs to the

beneficiary. If the customer deposits securities or valuables with the banker for safe custody,

banker becomes a trustee of his customer. The customer is the beneficiary so the ownership

remains with the customer.The customer remains the owner of such valuables though they are

in the custody of the banker. In this case the banker acts as trustee and the customer is the

beneficiary.

2. Relationship of Bailor and Bailee

The relationship between banker and customer can be that of Bailor and Bailee.

1. Bailment is a contract for delivering goods by one party to another to be held in trust

for a specific period and returned when the purpose is ended.

2. Bailor is the party that delivers property to another.

3. Bailee is the party to whom the property is delivered.

So, when a customer gives a sealed box to the bank for safe keeping, the customer became

the bailor, and the bank became the bailee.

Banks also keeps articles, valuables, securities etc., of its customers in Safe Custody and acts

as a Bailee. As a bailee the bank is required to take care of the goods bailed.

When the customer keeps his valuable in the safe custody of the banker, the banker besides

acting as trustee also acts as bailee. In that case the customer becomes the bailor. If the

customer (bailor) suffers any loss due to the negligence of duty on the part of the banker

(bailee), the customer can file a case in the court of law for the recovery of such loss.

3. Relationship of Agent and Principal

Thus an agent is a person, who acts for and on behalf of the principal and under the latter’s

express or implied authority and the acts done within such authority are binding on his

principal and, the principal is liable to the party for the acts of the agent

The banker acts as an agent of the customer (principal) by providing the following agency

services:

• Buying and selling securities on his behalf,

• Collection of cheques, dividends, bills or promissory notes on his behalf, and

• Acting as a trustee, attorney, executor, correspondent or representative of a customer.

Banker as an agent performs many other functions such as payment of insurance premium,

electricity and gas bills, handling tax problems, etc. The banker (agent) performs the

functions according to the instructions of the customer (principal) and for this the banker is

entitled to get commission from his principal.

4. Relationship of lessor and lessee

Providing safe deposit lockers is as an ancillary service provided by banks to customers.

While providing Safe Deposit Vault/locker facility to their customers bank enters into an

agreement with the customer. The agreement is known as “Memorandum of letting” and

attracts stamp duty.

The relationship between the bank and the customer is that of lessor and lessee. Banks lease

(hire lockers to their customers) their immovable property to the customer and give them the

right to enjoy such property during the specified period i.e. during the office/ banking hours

and charge rentals. Bank has the right to break-open the locker in case the locker holder

defaults in payment of rent. Banks do not assume any liability or responsibility in case of any

damage to the contents kept in the locker. Banks do not insure the contents kept in the lockers

by customers. In certain banks, this relationship is termed as licensor and licensee.

5. Relationship of Indemnifier and Indemnified

A contract by which one party promises to save the other from loss caused to him by the

conduct of the promisor himself or the conduct of any other person is called a contract of

indemnity. In the case of banking, this relationship happens in transactions of issue of

duplicate demand draft, fixed deposit receipt etc. here the bank is indemnified or indemnity

holder and customer is indemnifier. The underlying point in these cases is that either party

will compensate the other of any loss arising from the wrong/excess payment.

6. Relationship of Guarantor and guarantee-

Banks give guarantee on behalf of their customers and enter in to their shoes. Guarantee is a

contingent contract.

As per sec 31,of Indian contract Act guarantee is a " contingent contract ". Contingent

contract is a contract to do or not to do something, if some event, collateral to such contract,

does or does not happen. A bank as guarantor gives guarantee to its customer by issuing a

‘letter of credit’. It is a kind of credit facility to its customer to facilitate international trade. A

bank guarantee contains an undertaking to pay the amount without any demur on mere

demand of the principal amount on the ground for non-performance or breach of contract.

7. Relationship of Pledger and Pledgee

The relationship between customer and banker can be that of Pledger and Pledgee. This

happens when customer pledges (promises) certain assets or security with the bank in order to

get a loan. In this case, the customer becomes the Pledger, and the bank becomes the Pledgee.

Under this agreement, the assets or security will remain with the bank until a customer repays

the loan.

8. Relationship of Advisor and Client

When a customer invests in securities, the banker acts as an advisor. The advice can be given

officially or unofficially. While giving advice the banker has to take maximum care and

caution. Here, the banker is an Advisor, and the customer is a Client.

9.Relationship of Hypothecator and Hypothecatee

The relationship between customer and banker can be that of Hypothecator and Hypotheatee.

This happens when the customer hypothecates (pledges) certain movable or non-movable

property or assets with the banker in order to get a loan. In this case, the customer became the

Hypothecator, and the Banker became the Hypothecatee.

10. Other Relationships

Other miscellaneous banker-customer relationships are as follows:

• Obligation to honour cheques : As long as there is sufficient balance in the account of

the customer, the banker must honour all his cheques. The cheques must be complete and in

proper order. They must be presented within six months from the date of issue. However, the

banker can refuse to honour the cheques only in certain cases.

• Secrecy of customer's account : When a customer opens an account in a bank, the

banker must not give information about the customer's account to others.

• Banker's right to claim incidental charges : A banker has a right to charge a

commission, interest or other charges for the various services given by him to the customer.

For e.g. an overdraft facility.

• Law of limitation on bank deposits : Under the law of limitation, generally, a

customer gives up the right to recover the amount due at a banker if he has not operated his

account since last 10 years.

Rules and regulations

1. The banker-customer relationship once established it is often a long term one.(it may even

continue after the customer’s death, when the bank acts in the capacity of executor or trustee

of the deceased customer’s wealth)

2. It should always be remembered that the bank is not under legal obligation to accept every

applicant as a customer.

3. The banker must be satisfied with the responses to all inquiries before agreeing to open an

account for a prospective customer.

4. Banks will satisfy themselves about the identity of a person seeking to open an account, in

order to protect themselves, their customers and general public.

5. All banks should institute effective procedures for obtaining identification from new

customers.

Termination of the Banker Customer Relationship

The relationship between a bank and a customer ceases on:

• Termination by the Customer by closing the account i.e. Voluntary termination

The customer may at any time demand full repayment of his credit balance. It is suggested

that if the customer reduces the account to a nil balance, the account should not be closed

without confirmation from the customer that this is his intention.

It would seem that a customer with an overdrawn account may not terminate the banker-

customer contract without repaying the debt. The Banking Code and the Business Banking

Code, however, state that a bank must close an account when

asked to do so.

• Termination by the bank by closing of the account after giving due notice:-

It was stated in Joachimson that a bank may only close an account after giving reasonable

notice and making provision for outstanding cheques. In Prosperity Ltd v Lloyds Bank,19m it

was held that one month's notice was insufficient, but here the customer's banking

arrangements were unusually complex. The Banking Code and the Business Banking Code

declare that under normal circumstances a customer should be given at least 30 days' notice

before his account is closed - and this appears to include overdrawn accounts.

It has been observed that a bank's duty of secrecy survives the termination of the

contract. The customer may make claims arising from unauthorized debits (such as forged

cheques), which the customer raises for the first time after termination of the contract.

• Termination by Law:

a) Death of the customer;

b) Mental incapacity of the customer

c) Bankruptcy or insolvency of bank or customer.

d) The completion of the contract or the specific transaction

The contractual relationship will generally seize to exist upon the closure of the account.

However, it should be noted that some of the obligations may still exist after the account

has been closed. As a result of the increase in electronic banking, the legal nature of the

bank-customer relationship is constantly changing. English courts and financial regulators

have had to strive for a high level of flexibility in order to keep up with the introduction

of new systems and products by financial service providers.

Banks currently operating in the UK are taking steps to do away with cheques as a result of

the introduction of Electronic Funds Transfer at Point of Sale, Faster Payments, Direct

Debits and Telegraphic Transfers among others. The flexibility of English Law is

reflected in the recent Financial Services Act 2010 which has provided for the

amendment of the Financial Services and Markets Act (FSMA) 2000. Most of the

amendments by the Financial Services Act 2010 on consumer protection provisions in the

FSMA 2000 have come about as a result of the recent global financial crisis.

Banks in Africa also seem to be emulating these trends as we’ve seen in Europe and America.

For instance Nigeria is working on the cashless project which hopefully will reduce the

high usage of cash and accelerate electronic transfers. The changes that have been

brought about by these new technologies would certainly have an impact on the legal

nature of the bank-customer relationship. It then follows that as long as the business of

banking keeps changing, the legal nature of the bank-customer relationship will continue

to be adapted

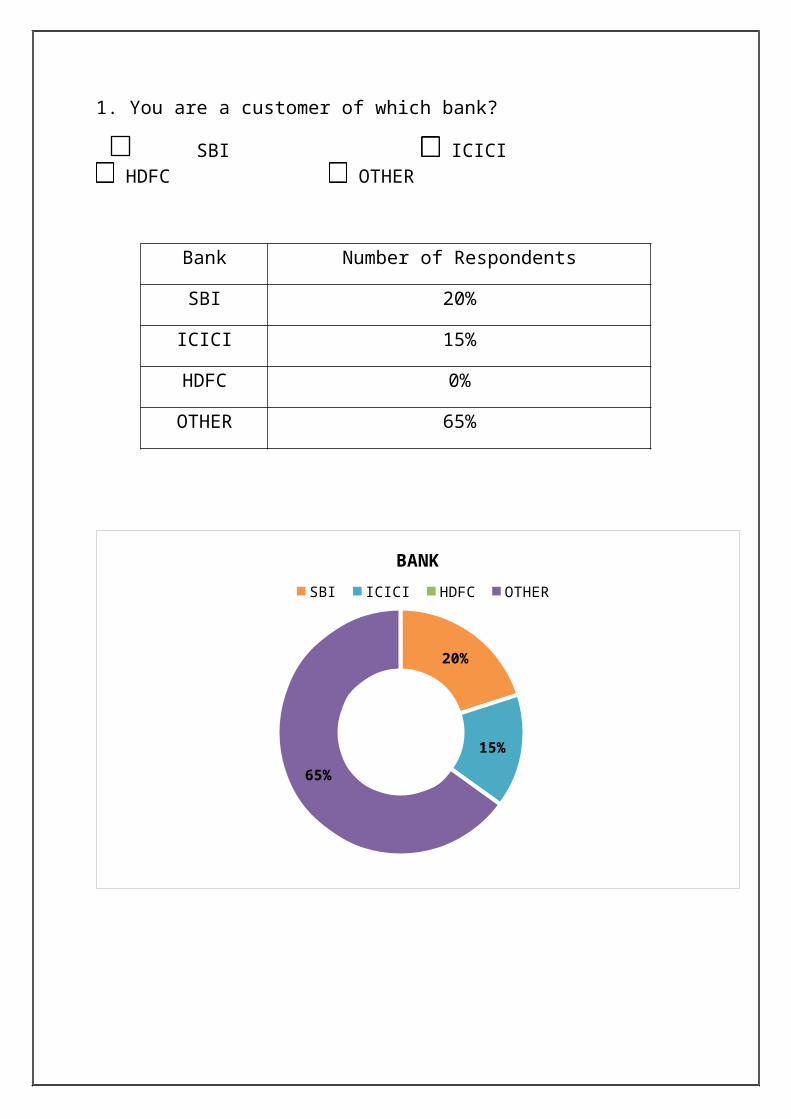

1. You are a customer of which bank?

SBI ICICI HDFC OTHER

Bank Number of Respondents

SBI 20%

ICICI 15%

HDFC 0%

OTHER 65%

20%

15%

65%

BANK

SBI ICICI HDFC OTHER

CONCLUSION:-

From the above table and chart, this can be seen that out of the total respondents every respondent having account in the OTHER bank but SBI has more

customers than ICICI and HDFC. The ICICI is also has more customers than HDFC.

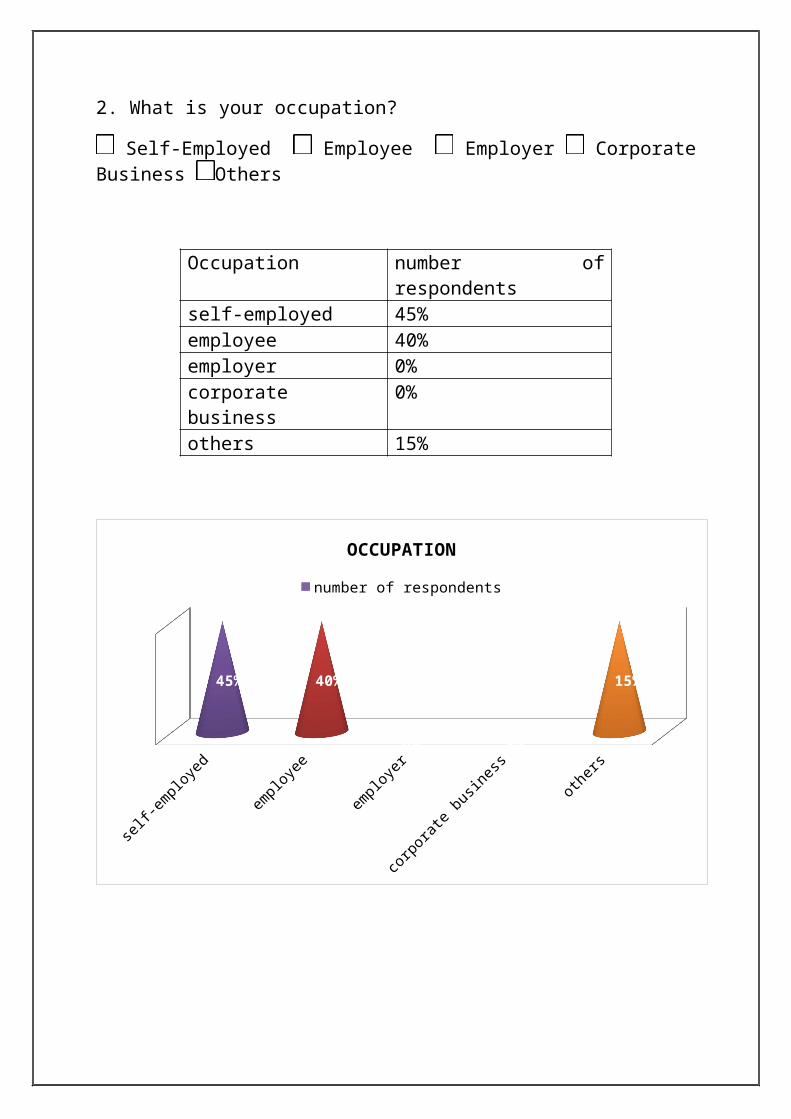

2. What is your occupation?

Self-Employed Employee Employer Corporate Business Others

Occupation number of respondents

self-employed 45%

employee 40%

employer 0%

corporate business 0%

others 15%

self-employed employee employer corporate business

others

45% 40%

0% 0%

15%

OCCUPATION

number of respondents

CONCLUSION:-

So it is concluded that the self-employed occupation is more than others and it is 45%. The next occupation is employee is of 40% is also more than other three and others occupation is of 15% are also more than other two.

3. Which type of account holder you are?

Individual Partnership Joint A/C Other

type of account holder number of respondents

individual 70%

partnership 0%

joint a/c 25%

other 5%

individual partnership joint a/c other0%

10%

20%

30%

40%

50%

60%

70%

80%

70%

0%

25%

5%

TYPE OF ACCOUNT HOLDER

number of respondents

CONCLUSION:-

As per the survey is concerned the individual account holder is of 70% and it is more than the others. The joint account holder is of 25% and the other type of account holder is of 5%.

4. Which type of account do you have with bank? Saving Recurring Current Fixed

type of account number of respondents

saving 85%

recurring 0%

current 0%

fixed 15%

saving; 85%

fixed;

15%

type of account

saving recurring current fixed

CONCLUSION:-

From the total number of respondents is of 20 people the number of respondents in the saving account is of 85% and it is more than the other type of account. The fixed account is of 15% and is more than the other two account type.

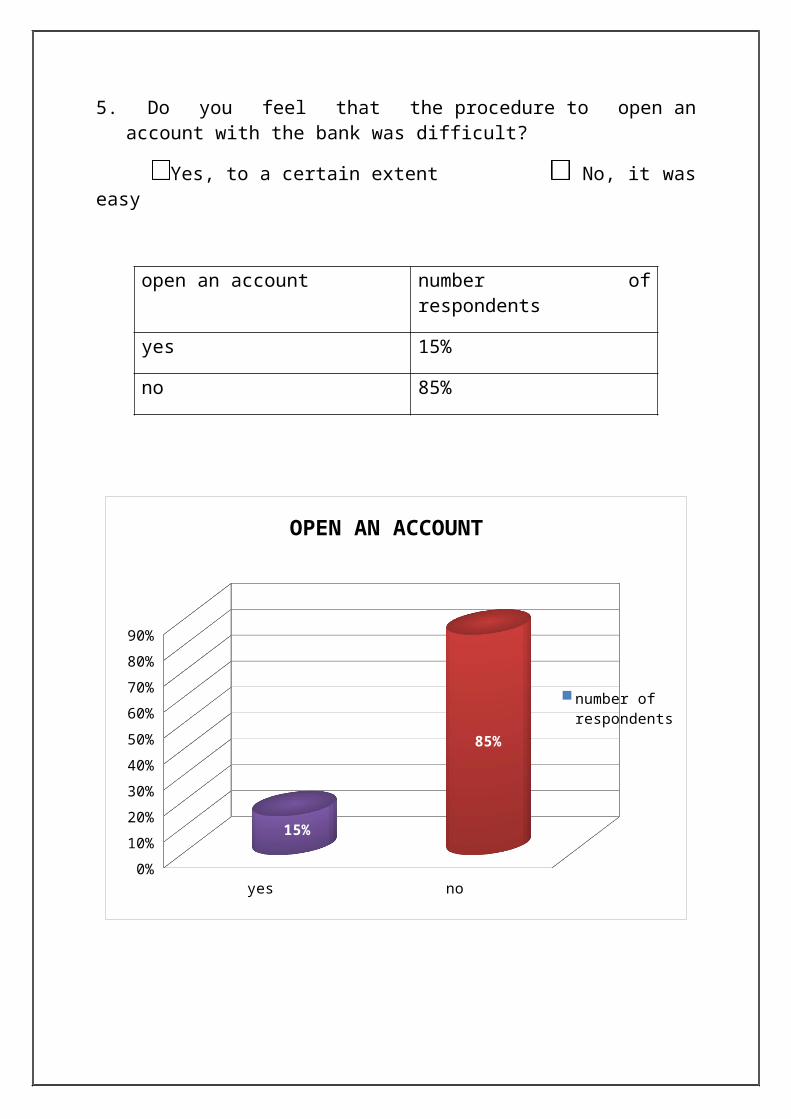

5. Do you feel that the procedure to open an account with the bank was difficult?

Yes, to a certain extent No, it was easy

open an account number of respondents

yes 15%

no 85%

yes no0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

number of respondents

OPEN AN ACCOUNT

85%

15%

CONCLUSION:-

The procedure to open an account with the bank is easy, it was not difficult the number of respondents feel. The 85% of number of respondent answered that the procedure is easy.

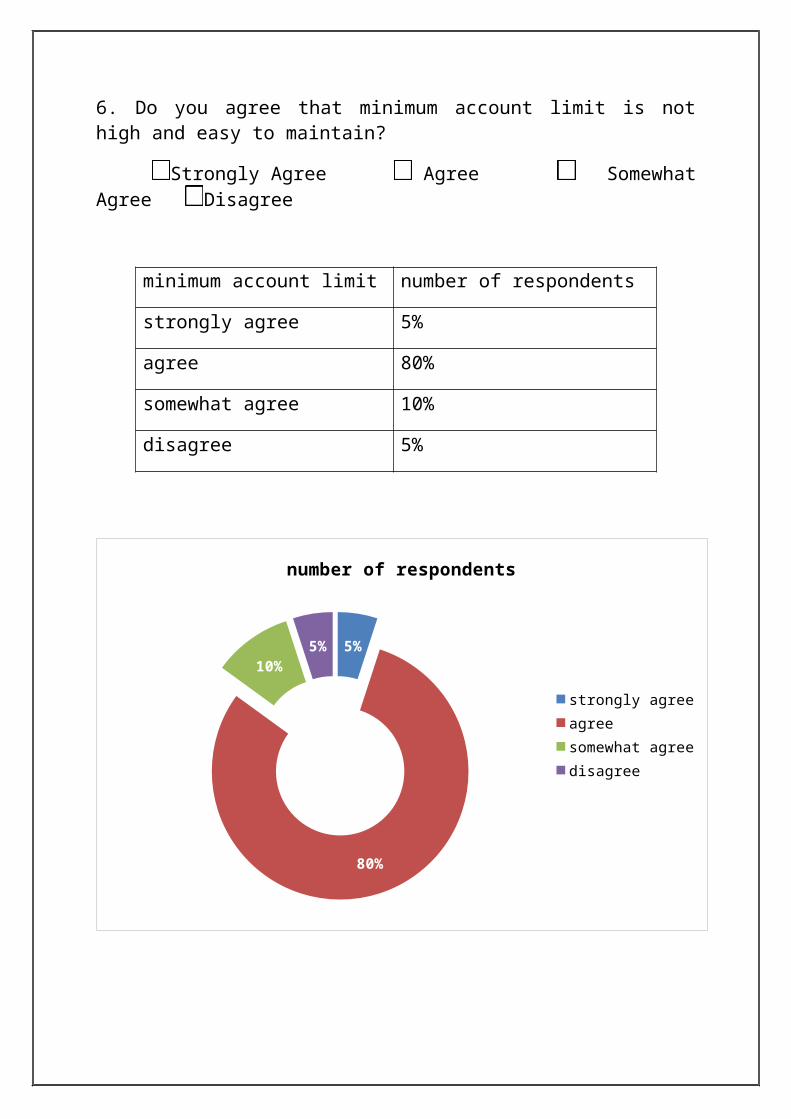

6. Do you agree that minimum account limit is not high and easy to maintain?

Strongly Agree Agree Somewhat Agree Disagree

minimum account limit number of respondents

strongly agree 5%

agree 80%

somewhat agree 10%

disagree 5%

5%

80%

10%5%

number of respondents

strongly agreeagreesomewhat agreedisagree

CONCLUSION:-

The total number of respondents answered that the minimum account balance is easy to maintain. From the total number of respondents is of 20 people and 80% number of respondents said that it is not difficult to maintain the minimum account balance.

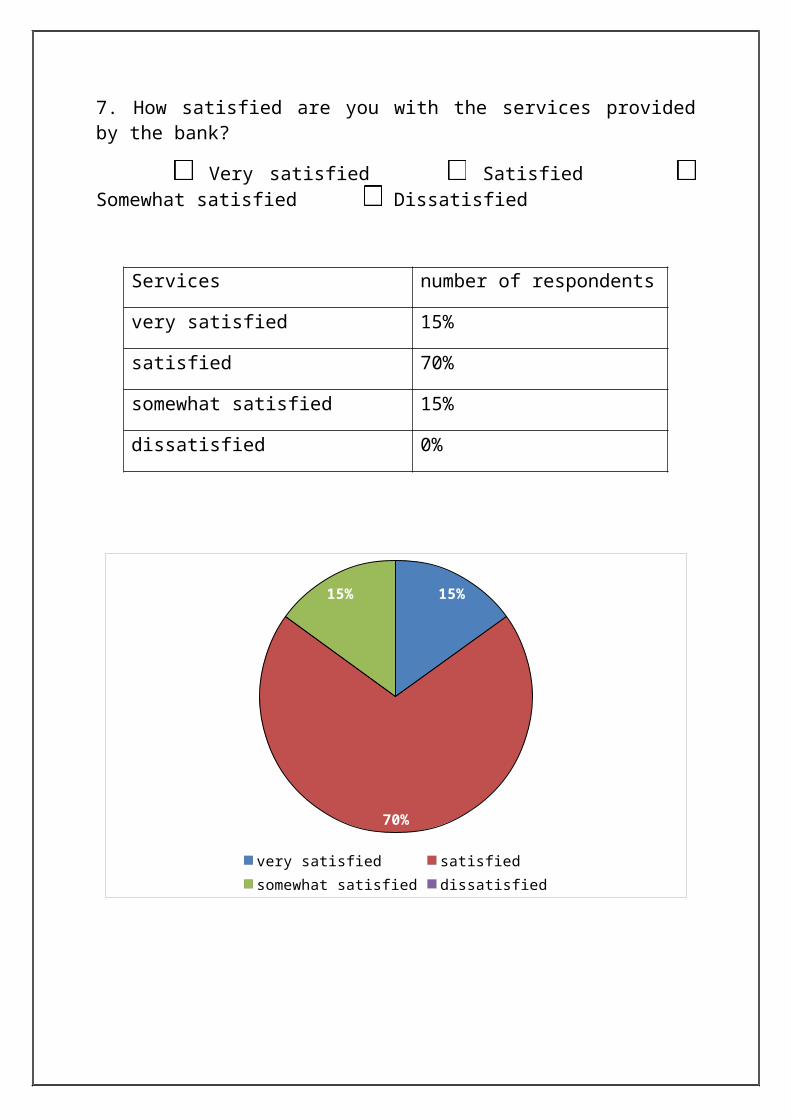

7. How satisfied are you with the services provided by the bank?

Very satisfied Satisfied Somewhat satisfied Dissatisfied

Services number of respondents

very satisfied 15%

satisfied 70%

somewhat satisfied 15%

dissatisfied 0%

15%

70%

15%

very satisfied satisfied somewhat satisfied dissatisfied

CONCLUSION:-

From the above table and chart, this can be seen that out of total respondents 70% respondents have satisfied with services provided by bank. The 15% respondents have very satisfied and 15% of respondents have somewhat satisfied.

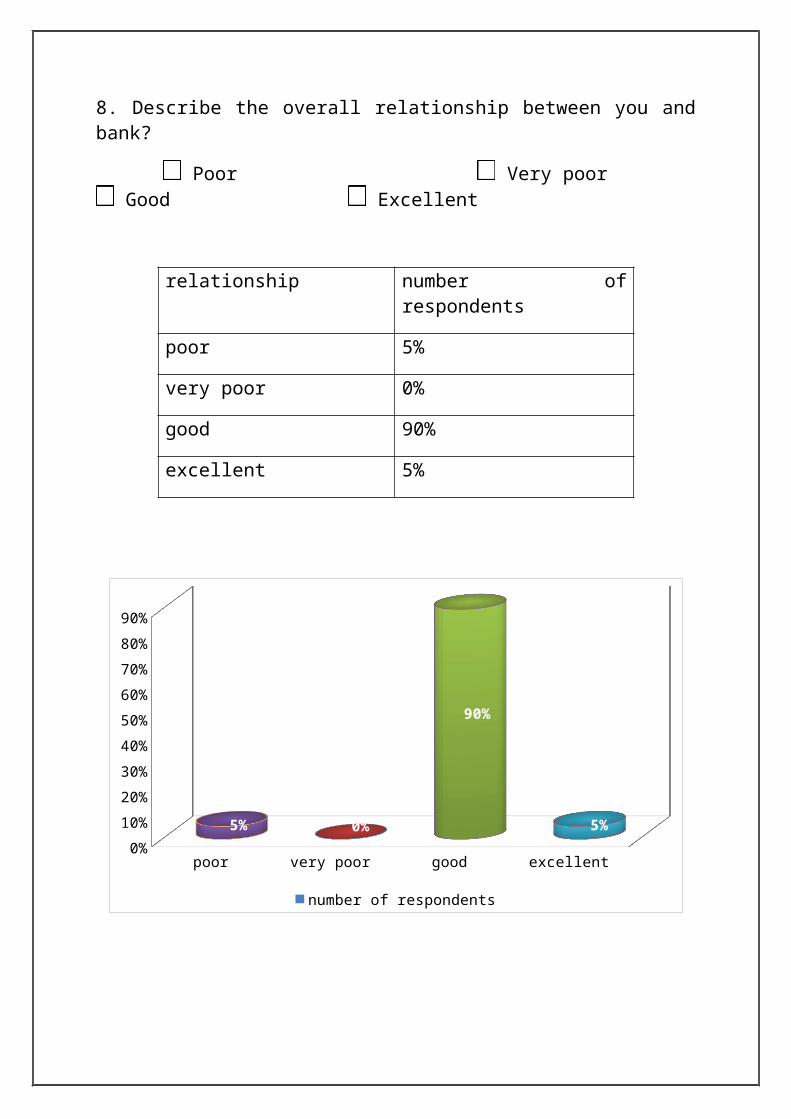

8. Describe the overall relationship between you and bank?

Poor Very poor Good Excellent

relationship number of respondents

poor 5%

very poor 0%

good 90%

excellent 5%

poor very poor good excellent0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

5% 0%

90%

5%

number of respondents

CONCLUSION:-

The number of respondents answered that their relationship with bank is good. The 5% respondents answered that their relationship is excellent and 5% respondents answered that their relationship is poor.

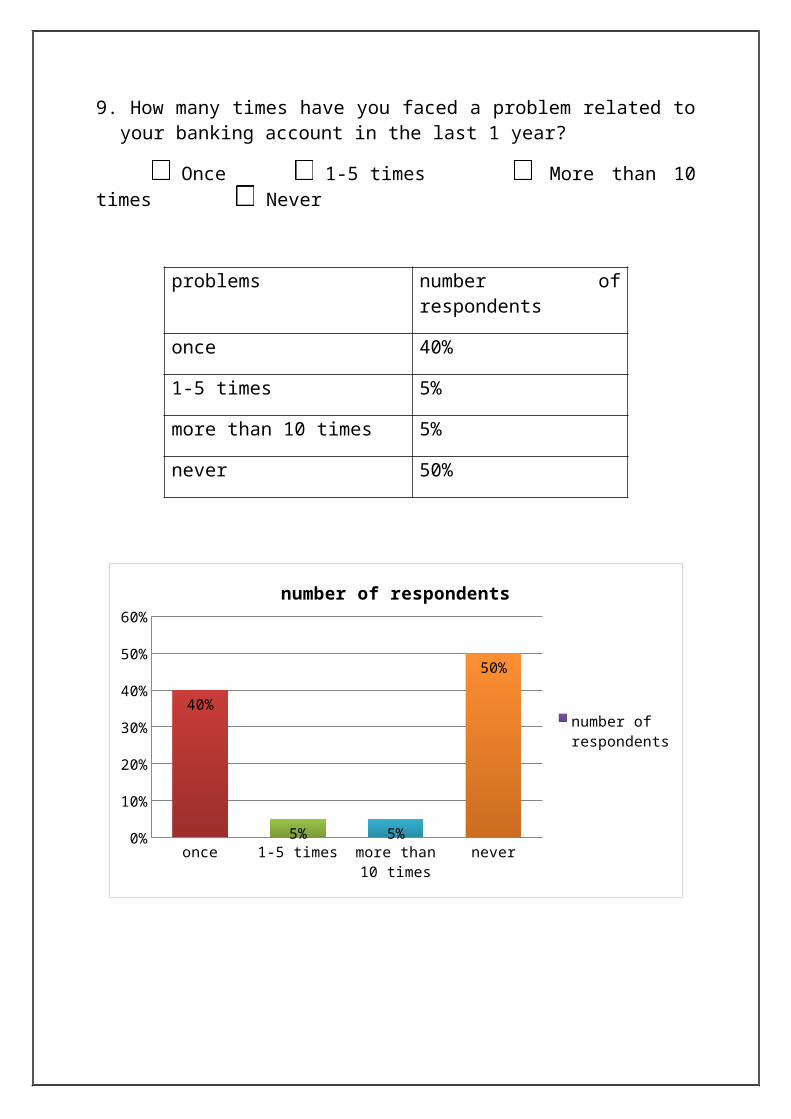

9. How many times have you faced a problem related to your banking account in the last 1 year?

Once 1-5 times More than 10 times Never

problems number of respondents

once 40%

1-5 times 5%

more than 10 times 5%

never 50%

once 1-5 times more than 10 times

never0%

10%

20%

30%

40%

50%

60%

40%

5% 5%

50%

number of respondents

number of respondents

CONCLUSION:-

The 50% respondents never faced a problem related to a banking account in the last one year. The 40% respondents faced a problem at once in the last one year.The remaining 5% respondents faced a problem one to five times and 5% respondents faced a problem more than 10 times in the last one year.

10. Is your business handled by banking executives in a timely and efficient manner?

Always Sometimes Rarely Never

business handled number of respondents

always 25%

sometimes 50%

rarely 15%

never 10%

always sometimes rarely never0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

25%

50%

15%10%

number of respondents

CONCLUSION:-

The 50% respondents answered that their business handled by banking executives in a timely and efficient manner. The remaining respondents answered that 25%, 15% and 10% respondents business handled by banking executives is always, rarely and never in a timely manner.

11. How long have you had these accounts in the bank?

Less than a year 1-3 years 3-8 years More than 8 years

long accounts number of respondents

less than a year 15%

1-3 years 20%

3-8 years 35%

more than 8 years 30%

less than a year

1-3 years 3-8 years more than 8 years

0%

5%

10%

15%

20%

25%

30%

35%

40%

15%

20%

35%

30%

number of respondents

number of respondents

CONCLUSION:-

The 35% of the total number of respondents has account with the bank for 3-8 years. The 30% number of respondents has more than 8 years with the bank. The 20% respondents have 1-3 years account with the bank. The remaining 15% respondents have account with the bank for less than a year.

12. How would you rate your bank on a scale of 4?

Excellent Good Neutral Poor

bank rated number of respondents

excellent 15%

good 75%

neutral 10%

poor 0%

15%

75%

10%

number of respondents

excellent good neutral poor

CONCLUSION:-

From the survey concluded that 75% total number of respondents rated that bank is good. The 15% respondents rated excellent and remaining 10% rated the bank is neutral.

13. Would you recommend to your acquaintances (friends, families, colleagues, etc) to open an account with your bank?

Yes No

recommend to acquaintances number of respondents

yes 80%

no 20%

80%

20%

number of respondents

yesno

CONCLUSION:-

From the above chart and table, the 80% number of respondents answered yes they will recommend to their acquaintances to open an account with their bank. The remaining 20% respondents answered no.

14. Which of the following associations do you have with the bank?

Banking Credit cards Loans Investing Others

associations number of respondents

banking 75%

credit cards 5%

loans 10%

investing 5%

others 5%

banking credit cards loans investing others0%

10%

20%

30%

40%

50%

60%

70%

80%75%

5%10%

5% 5%

number of respondents

CONCLUSION:-

The 75% numbers of respondents have their banking associations with their bank. The 10% respondents have their loan associations. The remaining 5% each is of investing, credit cards and others associations with their bank.

15. Would you like suggest any changes or improvement in any service or any feature of the bank

changes or improvement number of respondents

yes 45%

no 55%

45%

55%

number of respondents

yesno

CONCLUSION:-

From the above table and chart we can see that the 45% of the respondents answered yes and the remaining 55% answered no for suggestion related to the changes or improvement in any service or any feature of the bank.

CHAPTER NO.6 FINDINGS, SUGGESTIONS AND CONCLUSION

Suggestions

According to this report on banker customer relationship reveals various shortfalls and suggestions from various customers. The following gives the problems are critically dealt with and suggestions have been given which may prove fruitful in solving them, if not all, some of problems of the customers in the banks.

1. Firstly, the commercial banks are a bit reluctant to co-operate the customers and pay lessattention to the small customers. This discourages the small customers to deposit their small savings in banks. The mobilization of small savings is very useful for the economic development of the nations. Hence, small customers should not be discriminated againstby the bankers and specific facilities should be provided for these so called small customers.

2. The next thing, which the customers expect from the bankers, is the quick and fairservice. The customers mainly grumble about the delay in services and the unfriendlyattitude of the employees. For this purpose highly qualified, more experienced and creative staff that can work with complete sense of responsibility and involvement is required that can create banking habit with the customers.

3. Customers prefer to take advances from their provident funds rather than from banks dueto high rate of interest and complicated formalities. Providing advances easily andreducing the formalities included in getting them can solve this. At least commercialbanks should give reasonable overdrafts to their clients in turn of special need.

4. Customers get annoyed when bank employees discriminate them against by the bankemployees. Employees chat with each other while customer at the counter waiting to beserved. All this causes unnecessary delays. These drawbacks cannot be removed until and unless inner conscience of the employees is changes. Creating and developing interest in theemployees towards their jobs and providing proper training can do it.

5. Some of the customers are not satisfied with the banking hours because the present bankhours are colliding with their office hours. This causes inconvenience to them. Thisproblem can be solved by increasing the working hours of the bank or by automation ofthe whole of work as done by ICICI Bank.

6. Many customers give complaints and their complaints are not being taken intoconsideration, wherever the customers lodge a complaint the same should be treatedsympathetically and proper time should be taken into such complaints. Pahwa, Manvinder Singh (2000), “Customer Banker Relationship”, Indian Banking in the New Millennium, RBSA Publishers, pp 19-27

7. As previously discussed, many customers feel troubled by the bank strikes in the presenttimes when banks have become indispensable such irresponsible activities should endand bank strikes should be discouraged.

Conclusions

The commercial banks play a very important role in economic development of all nationsand customers’ services of commercial banks play yet another very important role for prosperityof banks. The entire business of banking rests a harmonious relationship and mutual trustbetween these two parties. It starts the moment an account is opened and ends immediately onthe closure of the account. Further, “The sound relations maintained between the two persons arealways fruitful and beneficial for both of them.”This study of banks of Udaipur has been undertaken to assess the quality of bank serviceor we can say to study the affairs regarding customer services of commercial banks withhypothesis “the qualities of the customers service in commercial banks is not satisfactory.”Quick and fair services to all the customers at all the time and is the dealing should be thenorms for the efficient customers services by banks and then only the Indian Sanskrit saying“Grahaka: Devo Bhava ” (Customer is God) will be satisfied.