organic purchasing trends in the current climate lorcan bourke bord bia & chair of the daff...

Post on 19-Dec-2015

214 views

TRANSCRIPT

Organic Purchasing Trends in the Current Climate

Lorcan Bourke Bord Bia & Chair of the DAFF Organic Market Development Group

Introduction – ‘The Current Climate’

Consumer Sentiment

Background – Food Price Deflation

December 2007 = €178-1.7%!

How much did it cost last year?

What about December 2006?

December 2006 = €161+10.5%!

A basket of 85 commonly bought SKU’s costs €175 today

Vs.

1. Differential cost comparison of a basket of groceries products in ROI vs. NI 2. Consumers shopping North of border/UK

Background - Sterling Exchange Rate

In RoI shoppers are now shopping around more for the offers and visiting on average 2.8 multiples in a 4 weekly period

2.5

2.5

2.4 2.4 2.42.5 2.4

2.5 2.5 2.52.5 2.5 2.5 2.6

2.6 2.6 2.62.6

2.8

4 W/e17

Jun07

4 W/e15Jul07

4 W/e12

Aug07

4 W/e09

Sep07

4 W/e07Oct07

4 W/e04

Nov07

4 W/e02

Dec07

4 W/e24

Feb08

4 W/e23

Mar08

4 W/e20Apr08

4 W/e18

May08

4 W/e15

Jun08

4 W/e13Jul08

4 W/e10

Aug08

4 W/e07

Sep08

4 W/e05Oct08

4 W/e02

Nov08

4 W/e30

Nov08

4 W/e28

Dec08

Shopping around more

Source: TNS Worldpanel, 52 w/e 28th December 08

No of stores visited for multiples

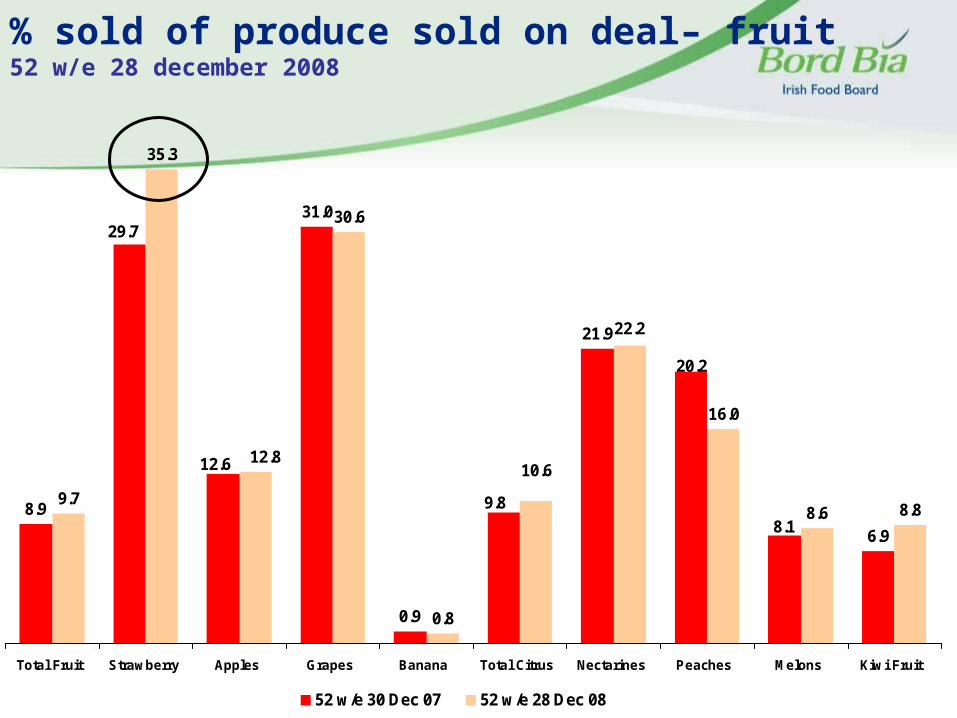

% sold of produce sold on deal– fruit52 w/e 28 december 2008

8.9

31.0

0.9

21.9

6.9

9.7

35.3

30.6

0.8

16.0

8.6 8.8

12.6

29.7

9.8

20.2

8.1

12.810.6

22.2

Total Fruit Strawberry Apples Grapes Banana Total Citrus Nectarines Peaches Melons Kiwi Fruit

52 w/e 30 Dec 07 52 w/e 28 Dec 08

Discounters Increase Market Share of Grocery

14.3 14.6

18.3

Discounters

% change year on year % Change 12 weekly% Change 4 weekly

different retailer?

Trade Down retailer?

Source: TNS Worldpanel, w/e 28th December

08

Growth has happened for the discounters through a combination of HH increased spend in- store and HH switching from other stores

Conclusions on ‘Current Climate’

• The unstable economic conditions has transformed consumers ‘mindset’ and retailers have responded

• We are currently experiencing the most price aggressive mainstream retail environment we have seen for many years (with a knock-on for all suppliers)

• Consumer sentiment is nervous and people are seeking to spend what money they have more wisely i.e. being ‘smarter’ about their purchases

• Any products consumers are paying a ‘premium’ for – the premium must be rationalised / justified and defensible in their minds

Overview of organic produce

0

10

20

30

40

50

60

70

80

90

1001998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

£m’s

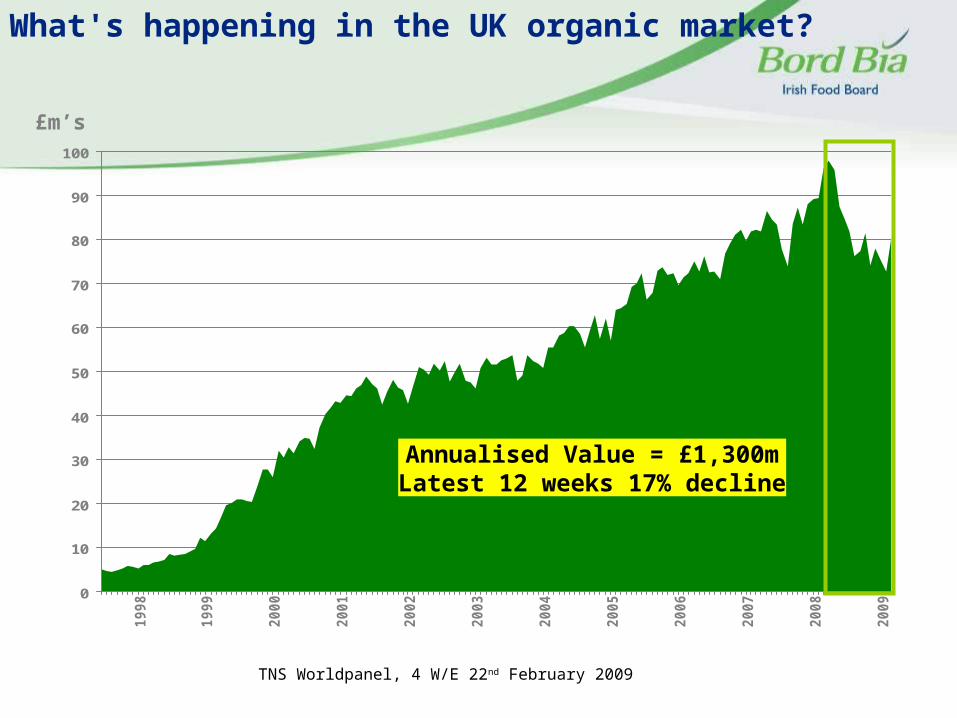

What's happening in the UK organic market?

Annualised Value = £1,300mLatest 12 weeks 17% decline

TNS Worldpanel, 4 W/E 22nd February 2009

Fruit and Vegetables account for 44% of total organic volume sold in the UK

-60

-50

-40

-30

-20

-10

0

10

20

30

Sw

ee

t H

om

eC

oo

kin

g

Ric

e/N

oo

dle

s/P

as

ta

Oil/

Flo

ur/

Am

bie

nt

Sa

uc

es

/Vin

eg

ar

Pa

ck

et

Bre

ak

fas

t

Fre

sh

Po

ult

ry+

Ga

me

Alc

oh

ol

Da

iry

Pro

du

cts

Ca

nn

ed

Go

od

s

Fre

sh

Me

at

Ta

ke

Ho

me

So

ftD

rin

ks

Ho

t B

ev

era

ge

s

To

tal O

rga

nic

Fru

it+

Ve

g+

Sa

lad

s

Bis

cu

its

Ch

ille

dC

on

ve

nie

nc

e

Bre

ad

& M

orn

ing

go

od

s

% c

han

ge

in O

rgan

ic v

olu

me

(pac

ks)

52 w/e % change 12 w/e % change

TNS Worldpanel, 52 % 12 W/E 22nd February 2009

So what's happening in Ireland - Total organic market size

95156.9

120689.5

16151.825394.9 28222.7

0

20000

40000

60000

80000

100000

120000

140000

52 w/e 27 Jan 08 52 w/e 25 Jan 09 12 w/e 28 Jan 07 12 w/e 27 Jan 08 12 w/e 25 Jan 09

Organic

+26.8%

+57.2% +11.1%

000’s euros

annually there is strong growth in the organic market however in the short term growth has slowed down

Which markets are driving the growth of organic YoY? The top 6 organic markets

24.5

6.2

43.8

1113.8

18

05

101520253035404550

Fru

it+

Ve

g+

Sa

lad

s

Fre

sh

Me

at

Bis

cu

its

To

tal M

ilk

Bre

ak

fas

tC

ere

als

Yo

gh

urt

s

% Chg Yoy

Organic fresh produce

Organic market for fresh produce is worth €48 million and growing by

31.9% - organic is 4% of total F&V

Penetration is high at 82% of the population +10.6% YoY

Shoppers are buying the organics sector more often 13 times a year up from 11

Each HH spends on average €38 euros on organic per annum +€4.40

Fresh Produce: organic spilt of the total marketthe discounters are the number 2 retailer in termsof organics - YoY direct sales are increasing

25.8

14.9

9.8

16.4

19.2

3

1.2 0.9

25.6

13.5

8.8

12.8

17.9

4.7

1.7

5.6

Tesco Dunnes Super quinn Super valu TotalDiscounters

OtherMultiples

Green grocer Roadsidestalls

30-Dec-07 28-Dec-08

2.6

3.8

4.5

3 333.2

2.7

Total Fruit & Veg Total Vegetables Potatoes Total Fruit

52 w/e 30 Dec 0752 w/e 28 Dec 08

Which segment of the produce market is driving organic sales?Vegetables is the key sector and up YoY

Key lines in growth are:

Leeks, turnips, swedes,

cumcumber, spinach and

carrots

Total Organic Fresh Produce market sales (quarterly)

6970.47344.4

8325.1 8398.8

9387.59841

11221.211742.4

11432.2

2447.18 2497.08 2624.86 2620.953001.57 3151.64

3481.483877.25 4050.94

0

2000

4000

6000

8000

10000

12000

14000

12 w/e 31Dec 06

12 w/e 25Mar 07

12 w/e 17Jun 07

12 w/e 07Oct 07

12 w/e 30Dec 07

12 w/e 23Mar 08

12 w/e 15Jun 08

12 w/e 05Oct 08

12 w/e 28Dec 08

000's EUROS Volume/000s

+35%

+22%

In the latest quarter value has declined slightly through lower prices. Volume continues to increase quarterly.

Organic vs. Non Organic - Meat

Total Market - Total Meat - Organic Value up 21.7% worth €1833k52 w/e 27

Jan 0852 w/e 25

Jan 09Actual

Change% Change

Expenditure (€000s) 8459 10292 1833 21.7Volume (000s Kgs) 1097 1135 38 3.5Penetration % 23.49 21.44 -2.05 -8.7Purchase Frequency 4.06 4.63 0.56 13.9AWP (Spend per Buyer) 24.21 31.48 7.26 30.0AWP (Kgs per Buyer) 3.14 3.47 0.33 10.6Trip Spend 5.96 6.80 0.84 14.1Trip Volume (Kgs) 0.77 0.75 -0.02 -2.9Price per Kg 7.71 9.07 1.36 17.6

* Penetration contribution includes Population growth of 2.6%

Contribution = €1471k

Contribution = €910k Contribution = -€548k

1135k Kgs +3.5%Contribution = €362k

Penetration % *

€9.07 +17.6%

21.4% -8.7%AWP (Kgs per Buyer)

3.5 Kgs +10.6%

Price per Kg

Expenditure (€000s)€10.3m +21.7%

Increase of €1833k

Volume (000s Kgs)

4.6 trips +13.9%Trip Volume (Kgs)

0.7 Kgs -2.9%Contribution = €1161k

Purchase Frequency

Contribution = -€251k

-1000 -500 0 500 1000 1500 2000 2500 3000

Penetration % Purchase Frequency

Trip Volume (Kgs) Price per Kg

Organic meat is in strong growth of 22% but 18% of the growth is from price increases – as the price increases less

HH are purchasing

Poultry and lamb is the only

sector where organic is growing

Organic spilt by meat typethe growth of organic is from the poultry sector

0.7

1.1

0.7 0.7

1.2

1.1

0.9

1.3

1.1

0.8

Total Meat Total Beef Total Lamb Sausages Total Poultry

52 W/e 27 Jan 08 52 W/e 25 Jan 09

Poultry and lamb are the only segments where organic is growing

Price differential between organic and non-organic

€12.86

€6.25

€8.98

€6.07

€8.95

€6.07

Total Beef Total Poultry

Total Market Non Organic Organic

Organic Performance Eggs

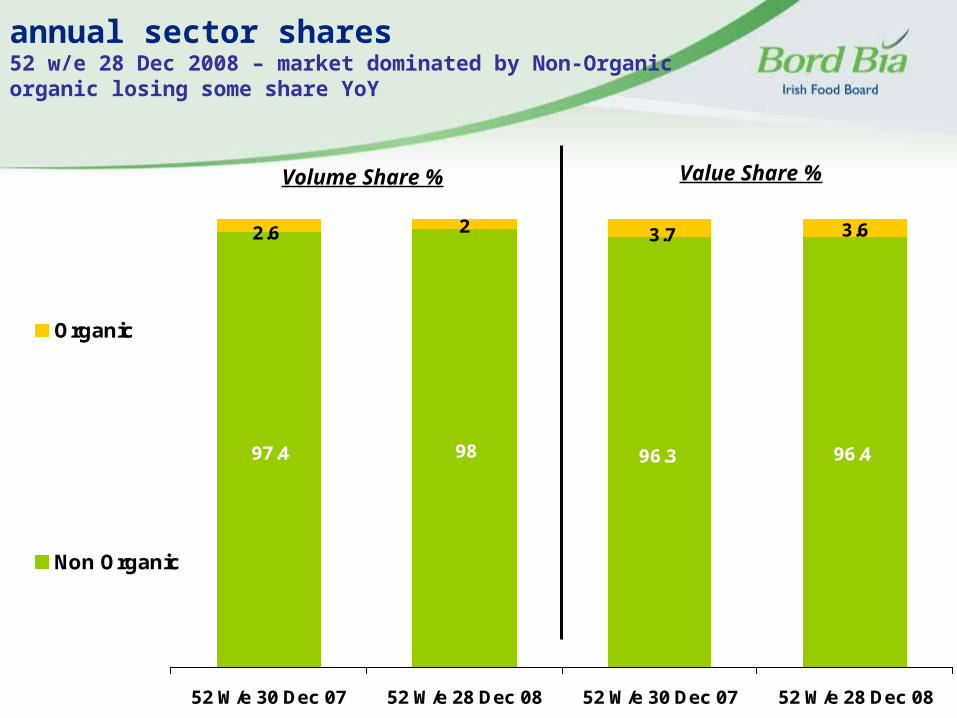

annual sector shares 52 w/e 28 Dec 2008 – market dominated by Non-Organic organic losing some share YoY

96.496.39897.4

2.6 2 3.7 3.6

52 W/e 30 Dec 07 52 W/e 28 Dec 08 52 W/e 30 Dec 07 52 W/e 28 Dec 08

Organic

Non Organic

Volume Share % Value Share %

Organic eggs vs. non organic : annual key diagnostics 52 w/e 28 Dec 2008 – penetration for organic eggs is still very niche – they are double the

price of non-organic

11.0

92.293.1

9.5

94.995.5

Total Eggs Non Organic Organic

52 w/e 30 Dec 07

52 w/e 28 Dec 08

209.8 206.4

45.4 44.8

216219.1

Total Eggs Non Organic Organic

52 W/e 30 Dec 07

52 W/e 28 Dec 08

22 21.5

6 6.6

22.823.3

Total Eggs Non Organic Organic

52 W/e 30 Dec 0752 W/e 28 Dec 08

€0.2

€0.3

€0.2

€0.4

€0.2€0.3

Total Eggs Non Organic Organic

52 W/e 30 Dec 0752 W/e 28 Dec 08

% PenetrationVolume per Buyer (Units)

Price per eggFrequency of Purchase

Is sales of organic food in Ireland recession proof & WHY ???

28

Irish Consumer Research on ‘Response to the Recession’

Methodology• In order to better understand consumer spending plans for the year ahead, TNS mrbi

asked a national sample of adults the following question for a list of core spending categories -

• Interviewing was conducted via PhoneBus®, TNS mrbi’s telephone omnibus, which interviews a sample of 1,000 adults aged 15+ years.

• Respondents are selected using RDD (Random Digit Dialling), thereby ensuring that unlisted households are as likely to be contacted for the interview as listed households.

• A combination of quota controls and weighting is used to ensure the PhoneBus® sample is representative of the national population in terms of gender, age, social class and region.

• Fieldwork for the data presented in this report took place between 10th March – 19th March 2009, during which time 1,016 interviews were successfully completed.

Q. In the year ahead, will you spend less or at least as much on…… ?

75%

72%

68%

66%

65%

63%

62%

56%

54%

49%

49%

49%

48%

47%

46%

45%

42%

34%

25%

28%

32%

34%

35%

37%

38%

44%

46%

51%

51%

51%

52%

53%

54%

55%

58%

66%On buying electrical items for the house

On cigarettes or other tobacoo products

On doing up your house e.g. painting, new furniture

On holidays/short breaks abroad

On going out for a drink

On eating lunch out of home

On going out for an evening meal

On concerts

On holidays/short breaks in Ireland

On renting DVDs

On going to sporting events

On going to the cinema

On cosmetics like make-up, aftershave, perfume etc.

On newspapers or magazines

On organic food

On your mobile phone

On groceries for the household

On entertaining at home

Consumer Spend Plans For 2009

+5

+6

+4

=

+2

+5

+2

+7

+4

= *

+3

+2

+4

-1

+5 *

+5

+9

+5

Will spend at least as much Will spend less

Spend Less % Change Vs. Jan ‘09

* New categories added in Feb ’09. Change Vs. Feb ’09.

Organic Bucks the Trend – Reasons

• People are saying that they are going to spend less on groceries, however no such decline appears (yet !) to exist in terms of Organic spend.

WHY ?

Will it remain so ???

Attitudes – Who Buys Organic Food?

Adult (18+) Grocery Shoppers

100%

(2.00m)

Current Organic Buyers

52%

(1.04m)

Non-Buyers of Organic

48%

(0.96m)

Evolving

Considerers

9%

(0.17m)

Rejectors

39%

(0.78m)

Organic

Believers

17%

(0.35m)

Health

Managers /

Status

Seekers

28%

(0.55m)

Core Buyers - Purchased

Organic in the Past Month

Aspirational

Improvers

7%

(0.14m)

Peripheral Buyers

Purchased Organic in

Past 3–6 Months

2333

4256

6514

19

25

2320

14

19

14

1410

30

2013

5 317

7 5 2 1

Behaviour – Are Consumers Ready To Pay A Price Premium For Organic?(n=1,000)

Definitely buy

Probably buy

Unsure

Probably not buy

Definitely not buy

• In the current economic climate, 47% of all consumers would ‘definitely’ or ‘probably’ buy if a 10% premium is charged. At higher premiums, this interest drops off sharply.

• However, among the core organic buying segment* – those who have purchased organic in the last 1 month (45% of respondents) – the outlook is healthier as 73% are ‘definitely’ or ‘probably’ willing to pay up to a 10% premium.

10% 15% 20% 25% 30%

Extra Extra Extra Extra Extra

% % % % %

If you were considering buy organic food rather than non-organic food, how

likely or not would you be to buy organic if you had to pay …

* n = 577

Anecdotal – behaviour shifts

• Consumers staying in and treating themselves to premium products e.g. organic food

A Clear Message to Consumers???

Reasons to buy ……..