online video ads within a changing media landscape · 2019. 7. 8. · online video ads within a...

TRANSCRIPT

Online video ads within a changing media landscape

July 2019

Giovanni Frasca, Media & Digital Expert

The world’s leading experts in helping clients navigate media decisions to

grow great brands

2

Extensive sample

& data partnerships

Vertical market

expertise

Global scale

& capabilities

22 Years

experience

CrossMediacampaigns

Connect touchpoint planning studies

Context Lab digital pilot studies

Digitalcampaigns

What does the future

of marketing look like?

Marketers around the world still struggle with marketing performance

Source: Kantar, Getting Media Right 2018

facing marketers today

Measuring

and proving

ROI

01Understanding

omni-channel

behavior

02Optimising

media

investment

03

Technological revolutions drive marketing: the ERA OF MASS MEDIA was all

about reaching a mass audience

1948Era of mass-

media

Gibbs

toothpaste:

first TV ad

Technological revolutions drive marketing:

The jungle of channels in the

ERA OF ENGAGEMENT

6

Radio

Cinema

Sponsorship

Outdoor

Search

Audio

Voice

Events Experiential

Influencers

Branded contentNative ads

Linear TV

Addressable TV/VOD

Online ads (trackable)

Google, Facebook, etc. Point of Sale

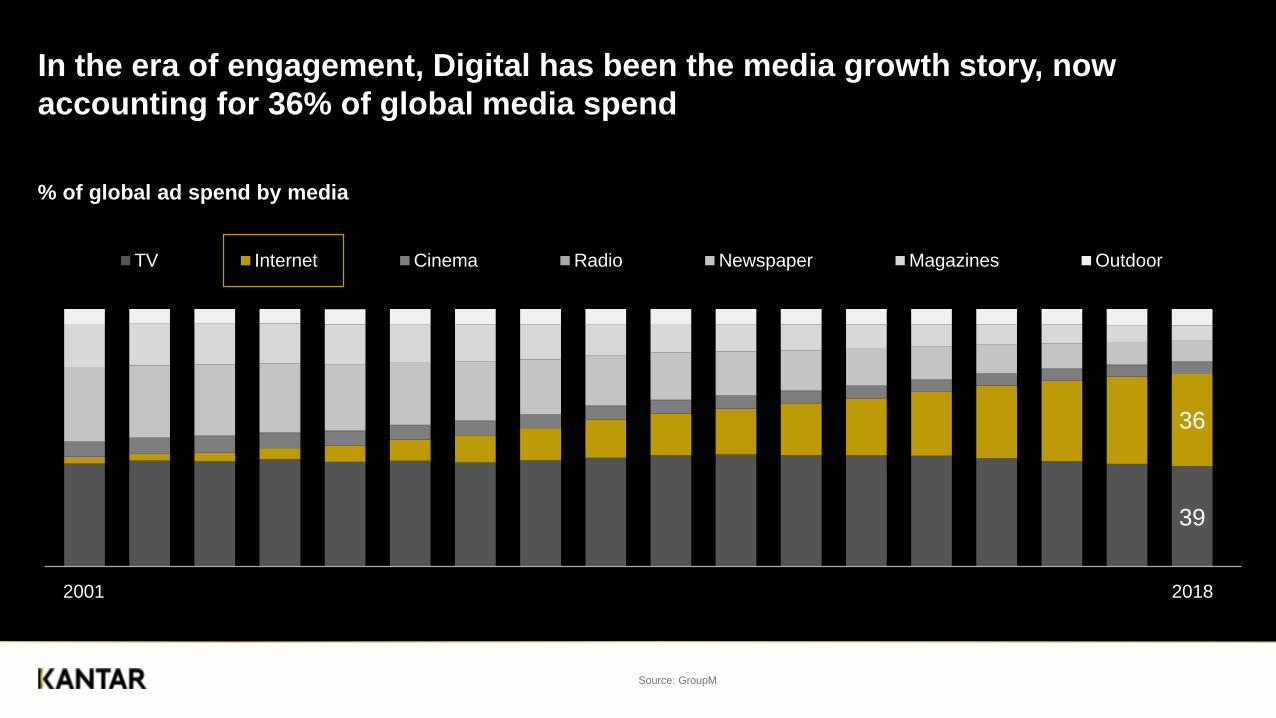

% of global ad spend by media

In the era of engagement, Digital has been the media growth story, now

accounting for 36% of global media spend

Source: GroupM

39

36

TV Internet Cinema Radio Newspaper Magazines Outdoor

2001 2018

It’s been a long time since we proved that online video ads work better than

display formats in building brand favourability and purchase intent

Source: Dynamic Logic Global Marketnorm data, Q2 2011 8

1,2

0,91,0

Online video (N=291) Rich media (N=1016) Simple flash (N=1027)

BRAND FAVOURABILITY

1,1

0,80,7

Online video (N=291) Rich media (N=1016) Simple flash (N=1027)

PURCHASE INTENT

Average Impact on brand metrics (% uplift)

And indeed investment for digital video ads is growing at a much faster pace

than overall digital advertising and non-video displays across Europe

Source: IAB Europe Conference, June 2019

13,9

6,6

27,9

TOTAL DIGITAL NON-VIDEO DISPLAY DIGITAL VIDEO

% of digital advertising market growth, H1 2018 – across 28 European countries

Source: global CrossMedia database (500 campaigns up 2014, 801 campaigns since 2015)

Share of spend

We too observed an increased share of spend in online videos within Kantar

CrossMedia database when looking at more recent campaigns

36% 33%

Up to 2014 2015-2018

5% 6%

Up to 2014 2015-2018

TV share of ad spend decreased by 8% Online videos share of ad spend increased by 19%

The increase in ad spend for online videos translated at first in higher reach

Source: global CrossMedia database (500 campaigns up 2014, 801 campaigns since 2015) 11

Average Reach (%)

70% 65%

Up to 2014 2015-2018

24% 31%

Up to 2014 2015-2018

TV reach decreased by 7% Online videos reach increased by 31%

At the same time, online videos improved their average brand contribution

Source: global CrossMedia database (500 campaigns up 2014, 801 campaigns since 2015) 12

Average brand contributions (across all brand KPIs)

1,27%

1,08%

2015-2018 >2014

TV average brand contribution

decreased by 15%

0,26%

0,40%

2015-2018 >2014

Online videos average brand contribution

increased by 54%

Finally, the increase in share of spend for Online videos did not impact their

efficiencies, showing that there is still room for further investment

Source: global CrossMedia database (500 campaigns up 2014, 801 campaigns since 2015) 13

Average cost effectiveness indices (across all brand KPIs): 100 = average

76

67

2015-2018 >2014

TV average cost effectiveness

decreased by 13%

125

133

2015-2018 >2014

Online videos average cost effectiveness

increased by 6%

remains the most impactful

ad channel for now, but the

crown is slipping…

Change in KPIs comparing campaigns up to

2014 vs. campaigns 2015-2018TV Online videos

Share of spend Down 8% Up 19%

Average reach Down 7% Up 31%

Contributions to brand KPIs Down 15% Up 54%

Relative cost effectiveness index (100 = average) Down 13% Up 6%

Source: global CrossMedia database (500 campaigns up 2014, 801 campaigns since 2015)

START WITH AN IDEA,

NOT A TV AD

15

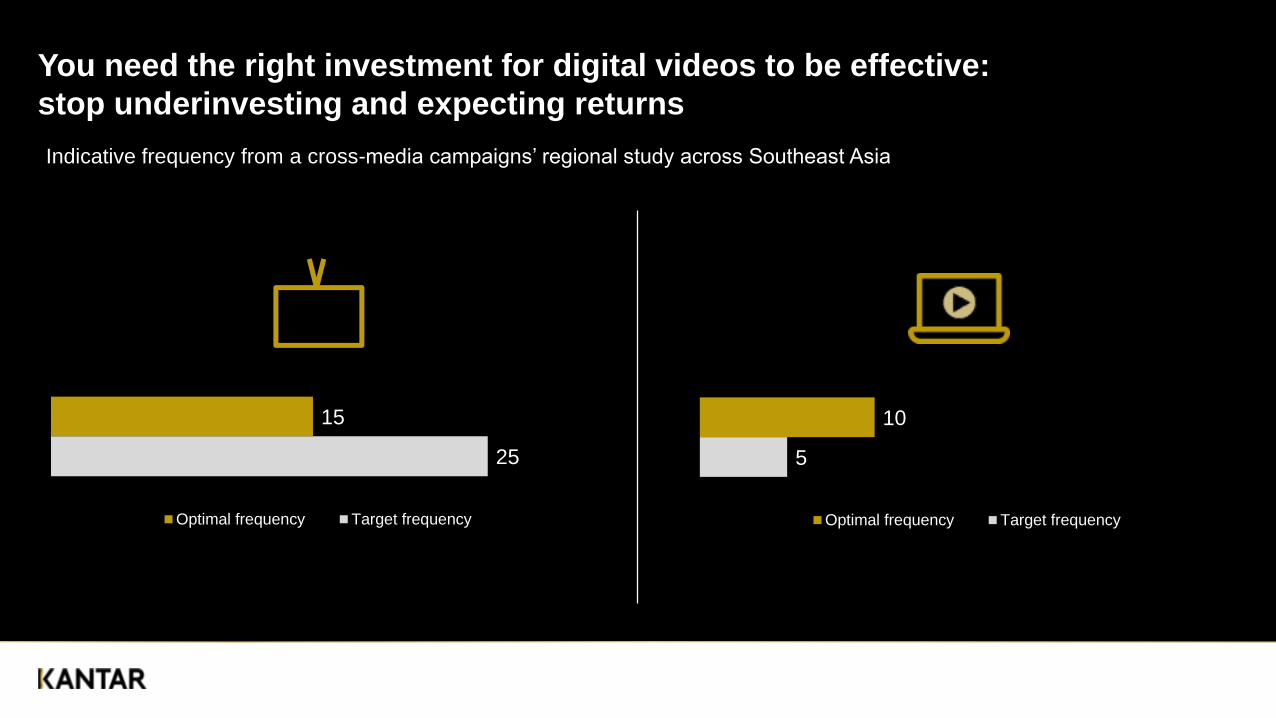

You need the right investment for digital videos to be effective:

stop underinvesting and expecting returns

Indicative frequency from a cross-media campaigns’ regional study across Southeast Asia

25

15

Optimal frequency Target frequency

5

10

Optimal frequency Target frequency

Indeed frequencies of online videos are still among the lowest we record in our

studies – only print & cinema have lower frequencies

Source: global CrossMedia database (801 campaigns since 2015) 17

2

3

5

5

6

8

8

9

15

16

0 2 4 6 8 10 12 14 16 18

Cinema

Magazines

Newspapers

Online Video

Online Display

POS

Outdoor

TV

Radio

Average Frequency

Avoid to get sucked into the TV black hole: you can win the share of voice

battle with a better integration of digital channels

189

44

47

8

14

7

44

16

26

19

28

23 26

74

6

Share of total

spendAwareness Association Motivation

TV

YouTube

Other online

OOH

Radio

Give each channel a

role: create a reason

for being for each

touchpoint in the

ecosystem

Source: Kantar CrossMedia campaign - Indonesia

Indeed, integrated and customised campaigns are most effective… but are not

the majority!

Data Source: Kantar CrossMedia studies, 2015-2017, (223 studies).

Categories: Food & Bev, Household, Retail, Travel, Personal care, Financial services, Technology, Automobiles

Overall Campaign Contribution is a measure of campaign impact on a combination of all brand KPIs (awareness, associations, motivation) 19

Base: (57) (64) (102)

100

131

157

Not well integrated Integrated – similar ads, but NOT well customised to

individual media

Integrated AND most mediawere customised well

Overall campaign contribution

by campaign type

Nature of multimedia campaigns

26%

29%

46%

Integrated AND

most media were

customised wellNot very well

integrated

Integrated – similar

ads, but NOT well

customised to

individual media

We have seen that

17%of campaign

performance comes

from synergy effects*

There are three conditions required for

synergy to occur between channels:

OVERLAPS IN REACH

SYNCHRONOUS OR

OVERLAPPING PHASING

CREATIVE INTEGRATION

01

02

03

*Source: Kantar CrossMedia average – Europe studies only 20

With Online videos we can target audiences that TV struggles to

reach

Source: Kantar Millward Brown and Collective Europe R&F studies 2013-2015 N=12 studies

Average incremental reach of online video

among light TV viewers:

Average incremental reach of online

video among total audience:

5%2%

21

3 creative

assumptions

to avoid

22

I can use

my TV ad online

and get double

the impact

01Editing

my TV ad

for different

channels will be

most efficient way to

spend my

media budget

02I can take

a completely

different approach

on each channel

03

The poorest digital creative can even make people less favourable towards the brand,

and confuse people as to the brand’s meaning.

But digital ads, when not developed & deployed properly, can be harmful

23

% impacted

11

7 7

3

1 1

-3

-5 -5

MESSAGE ASSOCIATION BRAND FAVORABILITY PURCHASE INTENT

Top 20% performing ads Average Bottom 20% performing ads

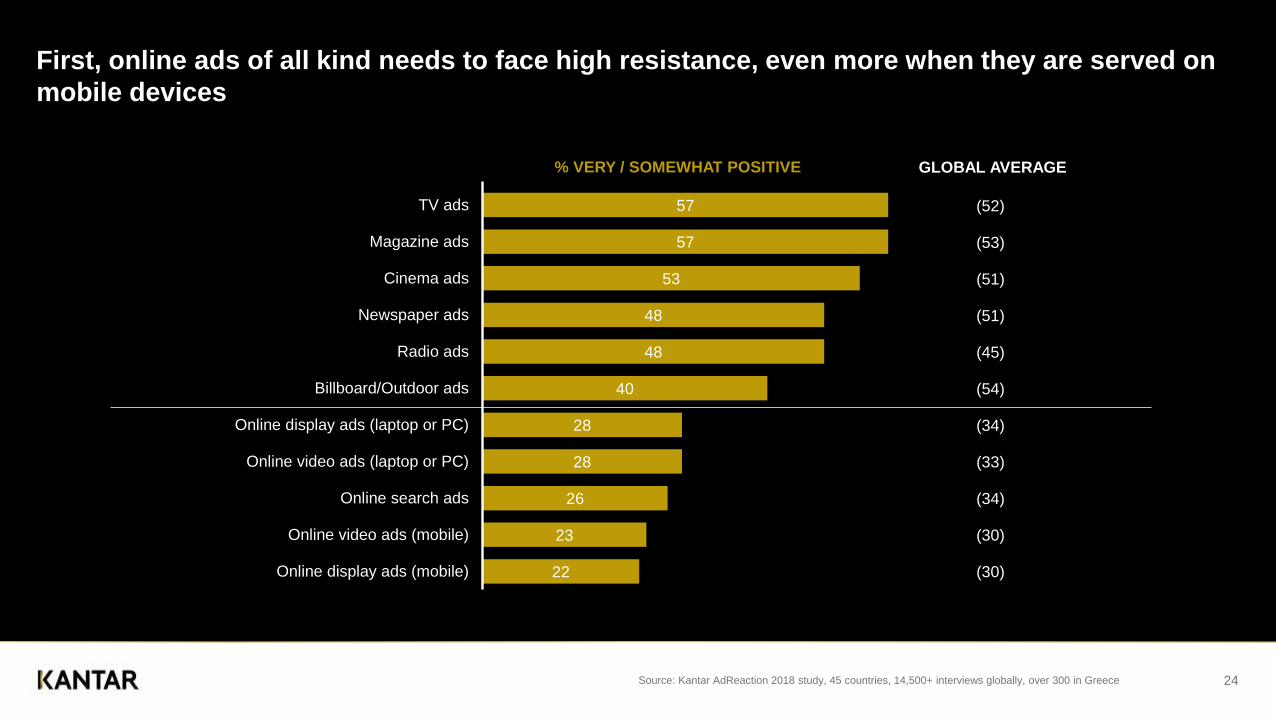

First, online ads of all kind needs to face high resistance, even more when they are served on

mobile devices

Source: Kantar AdReaction 2018 study, 45 countries, 14,500+ interviews globally, over 300 in Greece 24

57

57

53

48

48

40

28

28

26

23

22

TV ads

Magazine ads

Cinema ads

Newspaper ads

Radio ads

Billboard/Outdoor ads

Online display ads (laptop or PC)

Online video ads (laptop or PC)

Online search ads

Online video ads (mobile)

Online display ads (mobile)

GLOBAL AVERAGE

(52)

(53)

(51)

(51)

(45)

(54)

(34)

(33)

(34)

(30)

(30)

% VERY / SOMEWHAT POSITIVE

Formats that give control to viewers are the first step to win this resistance

25Source: Kantar AdReaction 2016 study, 42 countries, 13,000+ interviews globally, over 300 in Greece

But to win in a skippable video context you need to positively engage the audience with

enjoyable content in order to delay the skip

Source: Kantar 26

Smart For Four

“Reverse Parking”

UK Pre Roll

Context

Social

Context

Impact

(Percentile)77 57

Played whole ad 63% 24%

Average of ad

viewed

73%

23 sec

32%

10sec

Generate emotion, try to appeal to all senses, brand early…

27

Generate

an

emotional

response

01Use music

and audio to

engage

02Brand early

and utilise

companion

banners

03If long-form,

keep your

canvas clean

04If short-form,

keep it simple

but not

simplistic

05

And always have in mind your target audience…

28Source: Kantar IAB Tremor Video Cross Screen Study

a/b indicates statistically higher performance at the 90% confidence level

9,510,9

12,6

16-19 y.o. 20-34 y.o. 35-49 y.o.

Observed Skip time among skippers (in seconds)

Based on 12 YouTube ads

635554 52

Brand appeal Persuasion

18-34 Smartphone video ad (T2B %)

10-second (a) 30-second (b)

685961

51

Brand appeal Persuasion

18-34 Tablet video ad (T2B %)

10-second (a) 30-second (b)

49 4360 56

Brand appeal Persuasion

35-54 Smartphone video ad (T2B %)

10-second (a) 30-second (b)

63 6072

64

Brand appeal Persuasion

35-54 Tablet video ad (T2B %)

10-second (a) 30-second (b)

But if you get your YouTube creative right, there are good returns to be enjoyed

Source: Kantar Global MarketNorms Database 2019, n=16,075 studies 29

0%

1%

2%

3%

4%

5%

6%

7%

Online Ad Awareness Message Association Brand Favorability Purchase Intent

YouTube

Average

Average improvement generated in brand KPIs (%)

Kantar and Google joined forces in the YouTube Works Awards to highlight

effective advertising content and campaigns on YouTube

Source: YouTube Works awards 2019 30

Forget about this guy

32

The future of marketing

can look a lot more like this

Thank you!

Giovanni FrascaMedia & Digital Expert