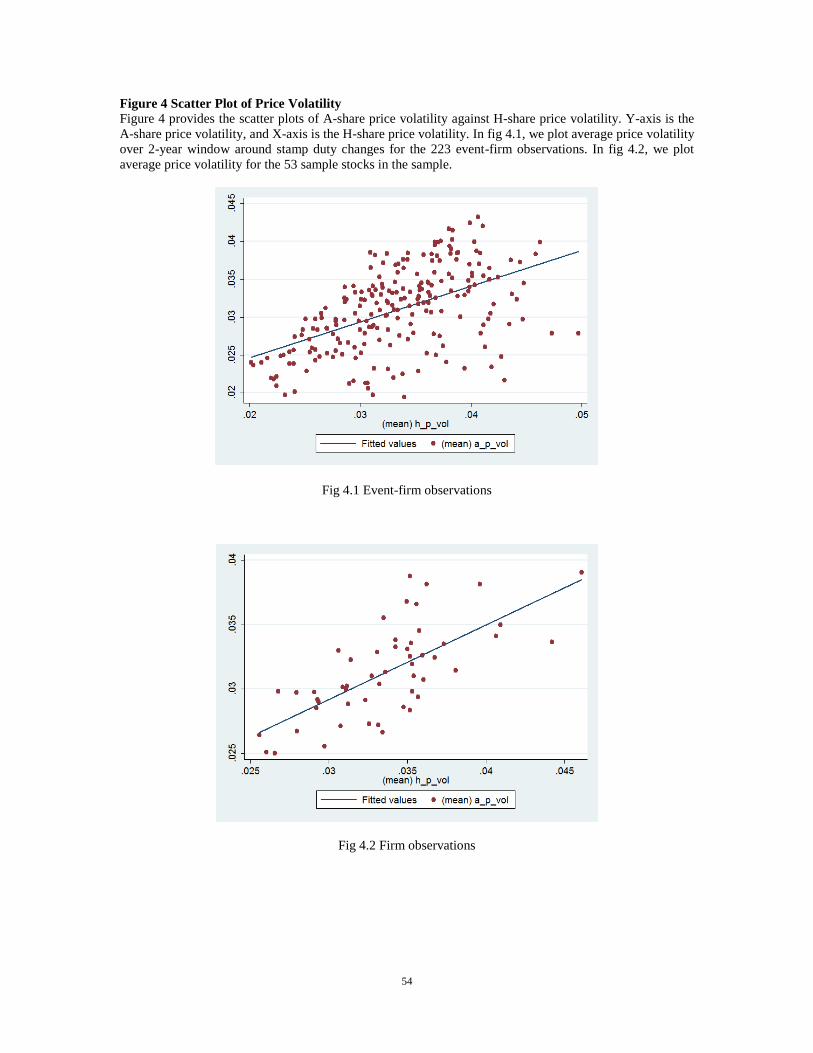

one corporate fundamental and two transaction...

TRANSCRIPT

1

Preliminary version; please do not circulate

One Corporate Fundamental and Two Transaction Taxes:

When Does “Sand in the Wheel” Reduce Financial Price Volatilities?

Yongheng Deng (NUS)

Xin Liu (NUS)

Shang-Jin Wei (Columbia, CEPR, and NBER)

Preliminary version: Oct 2013

Abstract

As the existing literature on the effects of transaction tax on financial price volatility is

characterized by ambiguity and contradictory results, this paper re-examines the question

by using a design that has a cleaner control for counterfactuals. In particular, we examine

the universe of 53 Chinese companies that are simultaneously listed in two stock

exchanges in Hong Kong and Mainland China. While arbitrage is limited by binding

capital controls, the underlying corporate fundamentals are identical for the twin shares in

the two stock exchanges. More importantly, Mainland China implemented seven discrete

and sizable changes to the stamp duties in 1997-2008 that do not directly affect trading in

Hong Kong. In contrast to Jones and Seguin (1997), we find a significantly negative

relation between stamp duty increase and price volatility. However, this average effect

masks some interesting heterogeneity. In particular, in later periods where institutional

investors have become a more significant part of traders’ pool or for stocks with a

relatively significant share of institutional ownership, we find an opposite effect for a

change in stamp duties. This suggests that the effect of transaction taxes depends crucial

on the relative importance of institutional versus retail traders.

2

3

1. Introduction

One of the Economics Nobel Prize recipients in 2013 is known for his pioneering

work that questions whether financial prices are excessively volatile. The possibility of

excessive volatility has motivated some to advocate the use of a transaction cost to

dampen short-term speculation and to reduce such volatility. Prominent proponents of

such an approach include Tobin (1978, 1984), Stiglitz (1989), and Summers and

Summers (1989). In contrast, opponents argue that security transaction taxes (STT) could

discourage fundamental-based traders more than they do noise traders, resulting in higher,

not lower, volatility in the financial market (e.g. Grundfest (1990), Grundfest and Shoven

(1991), and Kupiec (1996)). Interestingly, a large number of papers that have investigated

this question have not resolved this debate because some find a negative effect while

others find an opposite effect, and the conclusions do not appear tol be converging in

more recent publications.

One of the empirical challenges is to have a proper counterfactual: what would have

happened to the price volatility had the transaction tax not changed? Most papers use a

treatment and a control group, but cannot definitively rule out the possibility that the

control group differs from the treatment group in some systematic way that makes it not a

suitable counterfactual.

We study this topic by looking at price volatilities for Chinese companies that are

simultaneously listed in Hong Kong and Mainland China. There are referred to as H-

shares and A-shares, respectively. A few features of this set of cross-listings make them

especially suitable for our purpose. First, the A and H shares of a company have identical

cash flow and voting rights. So they have identical underlying corporate fundamentals. At

4

the same time, the Hong Kong and Mainland stock exchanges are legally segmented by

China’s massive and binding capital controls. Chinese residents can legally only trade in

A shares, whereas Hong Kong and foreign residents can legally only trade in H shares.

An evidence of market segmentation (or difficulty in arbitraging between the two markets)

is the gap in the A and H prices of the same companies. Second, during our sample of

1993-2012, investors in the two markets face very different stamp duties (transaction

costs) in terms of both levels and changes. For example, in 1997, while H-share investors

faced a stamp duty of 0.3%, A-share investors faced a stamp duty of 1%, or more than 3

times higher. More importantly for our empirical identification, A-share investors

experienced seven large and discrete adjustments in stamp duty during the sample period1,

while H-share investors experienced only negligible changes in the stamp duty. The

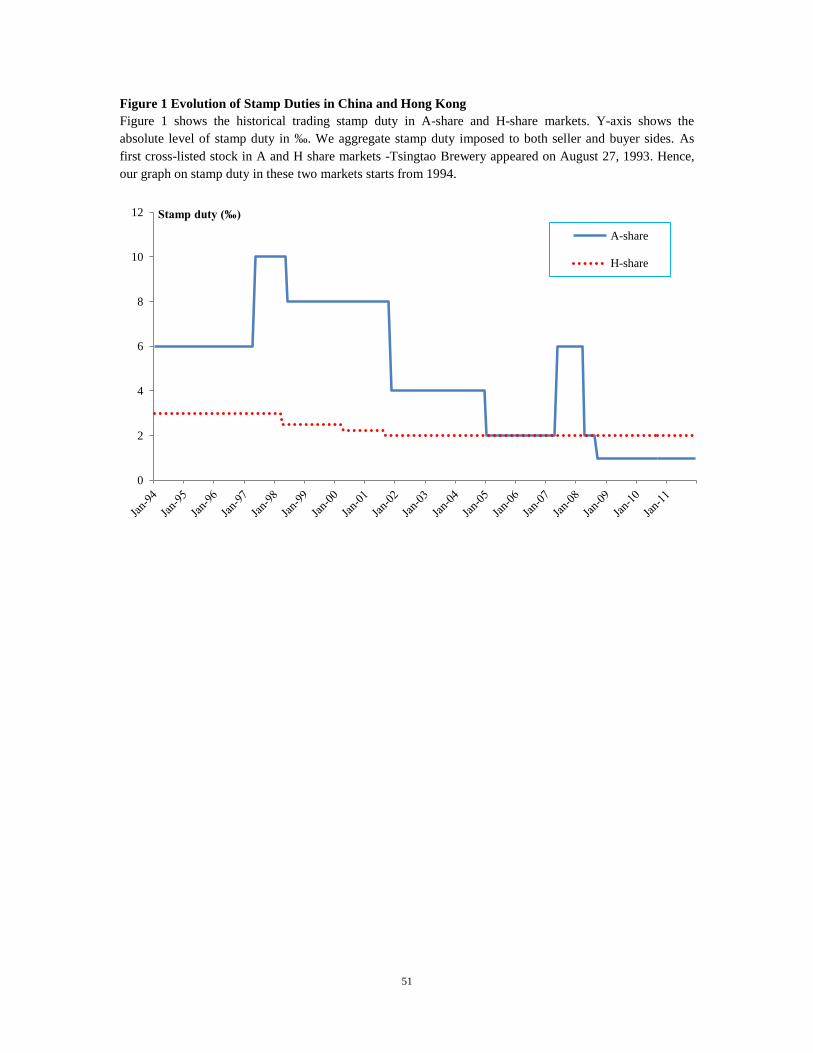

evolution of the stamp duties in the two markets is presented in Figure 1.

We exploit these features and study how a change in the stamp duty in the A-share

market (with no corresponding change in the H-share market) affects the stock price

volatility in the A-share market (relative to that of the H-share market). The counter-

factual for an A-share volatility in the absence of a change in the transaction cost in the

A-share market is the corresponding H-share volatility (or its linear transformation). This

is a natural counter-factual because the corporate fundamentals underlying an H-share are

literally the same as those for its corresponding A-share except for market segmentation.

In comparison, the counterfactuals in existing empirical literature are only a “similar”

portfolio of stocks to the one in treatment. For example, in Jones and Seguin (1997),

while the treatment group is a portfolio of stocks on the NYSE/AMEX, the control group

1 There were three more changes in the stamp duties in the A-share market before 1993. However, since the

first cross-listed Chinese stock (Tsingtao Brewery) only emerged on August 27, 1993, we have to exclude

these events by our difference-in-differences research design.

5

is a portfolio of stocks on NASDAQ. In this sense, our counterfactual is cleaner than all

others in the existing empirical literature.

It is useful to bear in mind two important institutional features about the Chinese stock

market. First, as the Shenzhen and Shanghai Stock Exchanges were only established in

1990 and 1991, virtually all investors in China have an extremely short history of trading,

and most lack basic knowledge about finance, accounting or economics. Second, at least

up to 2006, because mutual funds, pension funds, and other institutional investors were

either non-existent or too few to be significant, trading in the Chinese stock market was

overwhelmingly dominated by retail investors. If a transaction costs can reduce

unnecessary price volatility by discouraging noise trading, the effect has a better chance

to materialize than in perhaps most other security markets studied in the existing

empirical literature. In this sense, the study of the Chinese market can provide unique

value added to this literature.

The microstructure literature, such as De Long et al (1990), suggests that the fraction

of “noise trader” to “informed trader” affects the process of price discovery and the noise

to signal ratio. Uninformative trading by noise traders moves security price away from its

intrinsic value and generates excessive volatility which is the essential goal of STT to

tackle. In contrast, trading by informed traders contributes to price discovery, which in

turn lowers price volatility. Therefore, when a STT is imposed on the market, both

fundamental-based and non-fundamental-based traders would be discouraged from

trading. However, their reductions in transaction have opposite implications on price

volatility. What we observe in reality reflects the net effect of the two competing effects.

6

For this reason, we will also examine the role of institutional share in affecting results

on price volatility. Following many studies which point out that institutional investors are

fundamental-based rational traders, we use institutional ownership to proxy for the

fraction of fundamental-based trader. As a matter of fact, comparing to developed market,

the Chinese financial market is dominated by retail investors. In fact, in Jones and Seguin

(1997), their findings are based on an event in 1975 when the institutional ownership in

US stock market was about 22%, a level that China did not reach until 2009.

There are two key findings in the paper. First, pooling over the seven discrete changes

in stamp duties, we find a negative relationship between transaction tax and price

volatility, opposite to the influential papers by Jones and Seguin (1997) and Umlauf

(1993). Our findings of a lower price volatility in higher transaction tax regimes are

consistent and robust in various forms of firm and portfolio level estimations. We

interpreted it as evidence that a Tobin tax may achieve its intended objective in an

immature market where retail investors dominate. However, this is not the end of the

story. Second, we find that, with a significant presence of institutional investors, the

effect of a higher transaction cost is reversed. For example, for the two most recent

changes in transaction costs (a decrease in April, 2008, and another decrease in

September 2008) when the share of institutional ownership in Chinese stocks was closer

to the level in the United States in the early 1970s, transaction costs and price volatility

are positively related. Also, across individual stocks, transaction costs and price volatility

are more likely to be positively related for stocks with a relatively high institutional

trading but negatively related for stocks with relatively low or no institutional trading.

These findings are only suggestive evidence at this point. If this holds up to further

7

scrutiny when more data becomes available, it might provide a way to reconcile

seemingly contradictory findings in the existing empirical literature.

The rest of the paper is organized as follows. Section 2 supplies some background

information. . Section 3 describes the data and descriptive statistics. Section 4 provides

the statistical analysis. Section 6 concludes.

2. Background Information

In this section, we provide two types of background information, First, we briefly

review the existing empirical literature, highlighting the design of control and treatment

groups as well as the main findings. We then present some basic background about the

Chinese and Hong Kong stock exchanges and the seven discrete events of stamp duty

changes in Mainland China.

2.1 Existing empirical literature

Our study with unique A-H twin shares as treatment-control pairs contributes to the

literature with an improved understanding of the Tobin tax. Only a few studies find

empirical evidence supporting the proponent’s view of STT. Liu and Zhu (2009) find that

commission deregulation in Japan is associated with a statistically and economically

significant increase in price volatility, which suggests that imposing higher transaction

costs might be feasible to stabilize the market by curbing short-term noise trading. Hanke

et al (2010) also show evidence to support that a Tobin tax would reduce speculative

trading. However, neither study uses a control group that can be said to be the same

8

as the treatment group. Our study provides additional empirical evidence to support the

advocates of Tobin tax.

Moreover, since more studies2 find the opposite effect of STT on price volatility, this

paper contributes to the literature by providing a potential explanation for the

inconsistencies in empirical evidences. Umlauf (1993) studies the volatility impact of the

inception and increase of Swedish tax and finds that volatility significantly increased in

response to the introduction of taxes although stock price levels and turnover declined.

Jones and Seguin (1997) find consistent results with Umlauf (1993) that a reduction in

transaction costs is associated with a decline in stock return volatility. They argue that

increasing the costs of trading through transaction taxes, increasing margin requirements,

or reducing the availability of low-cost substitutes like equity futures may in fact

encourage, rather than reduce the impact of noise traders and volatility. In addition,

findings of no significant impact of STT on market volatility cast doubt on STT as an

effective policy instrument. Roll (1989) uses the cross-country data to study the matter

and finds that transaction taxes are inversely but insignificantly correlated with market

volatility. Hu (1998) finds with Asian market data that increases in STT reduce the stock

price, but have no significant impact on price volatility or turnover.

Lastly, our study has broad implications for other security classes. Several researchers

study the question with the housing market instead. Fu et al (2012) use the Singapore

housing market and show that prices become less informative and volatility significantly

increases in the affected market following the transaction tax increase. Sheffrin and

Turner (2001) find a capital gains tax with full loss offset at ordinary tax rates would

2 See e.g. Hau (2006), Habemeier and Kirilenko (2001), Lanne and Vesala (2010), Aliber, Chowdhry, and

Yan (2002), Chuo and Wang (2006), Green, Maggioni and Murinde (2000), Atkins and Dyl (1997), and

Westerhold (2003), Baltagi et al (2006), and Phylakti and Aristidou (2007)

9

generate a benefit to households by reducing the volatility of housing returns; however,

the effect on the rate of return exceeds the benefits of volatility reduction. Aregger et al

(2012) show that transaction taxes have no impact on house price growth based on

evidence from the variation of tax rates across Swiss cantons, while capital gains taxes

exacerbate house price dynamics.

2.2 Stamp Duties in the Chinese Stock Market

The history of the stock trading stamp duty in China goes back to the early 90s, shortly

after the establishment of Shanghai Stock Exchange (SSE) and Shenzhen Stock

Exchange (SZSE). The stock trading stamp duty was first introduced on Shenzhen Stock

Exchange on June 28, 1990. While there were three adjustments in the duty during 1990-

1992, there were no cross listed stocks at the time. So these adjustments are not part of

our sample.

The stamp duty is regarded by the government as a revenue-generating tool as much

as an instrument to reduce price volatility. After 1992, the year in which China Securities

Regulatory Commission (CSRC) was established, a surge in the stock market transaction

volume made stamp duty a noticeable source of revenue. While at the beginning, the

revenue was shared 50-50 between the central government and local governments, the

sharing rule has been adjusted a few times, progressively more in favor of the central

government. After 2002, 97% of the stamp duty revenue has been accrued to the central

government. The dominance of the revenue consideration makes it plausible that

adjustments in the stamp duty are not an endogenous response to changes in stock price

volatility. (Conversations with a former CEO of the Shanghai Stock Exchange also

10

suggest to us that adjustments in stamp duties are not made to alter price volatility. The

former CEO states that the stock exchange always advocates for a low stamp duty to

minimize transaction costs, and their policy advocacy sometimes but not always carries

the day when the overall index is low, but periodically the Ministry of Finance would

decide to raise the duty.)

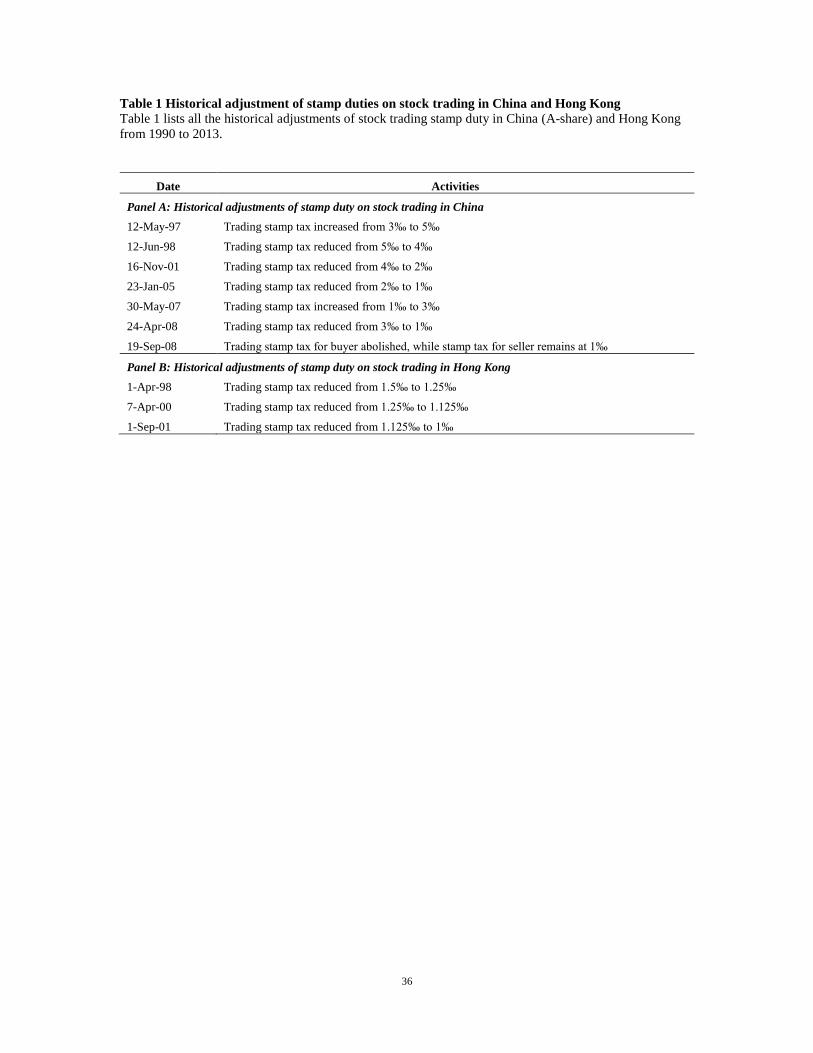

As shown in Table 1, China experienced seven adjustments in stock trading stamp

duty during the sample period. After an increase in stamp duty in 1997, the duty was

adjusted downwards stamp between 1998 and 2007, but raised in 2007, before two more

downwards adjustments in 2008.

The historical stamp duty adjustments in Hong Kong Stock Exchange (HKEX) are

also reported in table 1. Not only the level of the stamp duty in Hong Kong is low, the

magnitudes of the adjustments are also substantially smaller when compared to the A-

share market. In any case, the duty stays at a low constant level of 1‰ of transaction

value for buyer and seller after 2001. In our statistical analysis, we will ignore the

adjustments in the stamp duties in Hong Kong. (In an appendix table, we will perform a

robustness check that accounts for the duty adjustments in the Hong Kong market.)

2.3 A short history of institutional investors in China

The Chinese stock market, for much of its 30-plus-year history, is known to be

dominated by retail investors. Figure 2 provides a graphical illustration of evolution of

institutional investors in China based on the quarterly institutional holding information

from the WIND database. First, figure 2a shows the time series of outstanding

institutional investors in the Chinese domestic stock market. Next, figure 2b shows the

11

share of institutional holding as of the entire A-share market based on market

capitalization over the years. In 1975, the year of the sample used in Jones and Seguin

(1997), the share of institutional holding in the United States reached 22%. China did not

reach this level until 2008. (Both the number of institutional investors and the share of

institutional holding have exploded since 2008, though the stamp duty in the A-share

market stays at a low level of 0.1% set in September 2008.)

It is convenient to think of the history of Chinese institutional investors in three stages.

First, in the early stage between 1990 and 1997, the financial market is overwhelmingly

populated by retail investors, whereas institutional investors were negligible both in

numbers and in trading volume. The second stage - emerging stage from 1998 to 2005,

when mutual funds and insurance companies, though very few pension funds or hedge

funds, began to emerge in the Chinese stock market. Finally, since 2006, a growth stage

sets in when institutional investors have grown at a high speed, eventually catching up

with the US level by 2012 in terms of its relative importance in both trading and

shareholding.

3. Empirical Results

3.1 Data

There are seven discrete changes in the stamp duties in the Chinese market during our

sample period of 2004-2009, which constitute our events3. They are both listed in Table 1

and graphed in Figure 1. While there are also independent changes in the stamp duties in

3 There were also adjustments in stamp duties in Shenzhen Stock Exchanges in 1990 and 1991. Since there

were no cross-listed firms at these times, they are not part of our sample. During our sample, the stamp

duties are set jointly by the Ministry of Finance and the China Securities Regulatory Commission, and

always common to both Shanghai and Shenzhen Stock Exchanges.

12

Hong Kong, the changes are negligibly small when compared to the changes in the

Mainland. The comparison can be most clearly seen in Figure 1. In this paper, we will

ignore stamp duty changes in Hong Kong. Because the changes in Hong Kong are not

systematically related to those in the Mainland (and are very small in magnitude anyway),

they mainly add noise to our inferences.

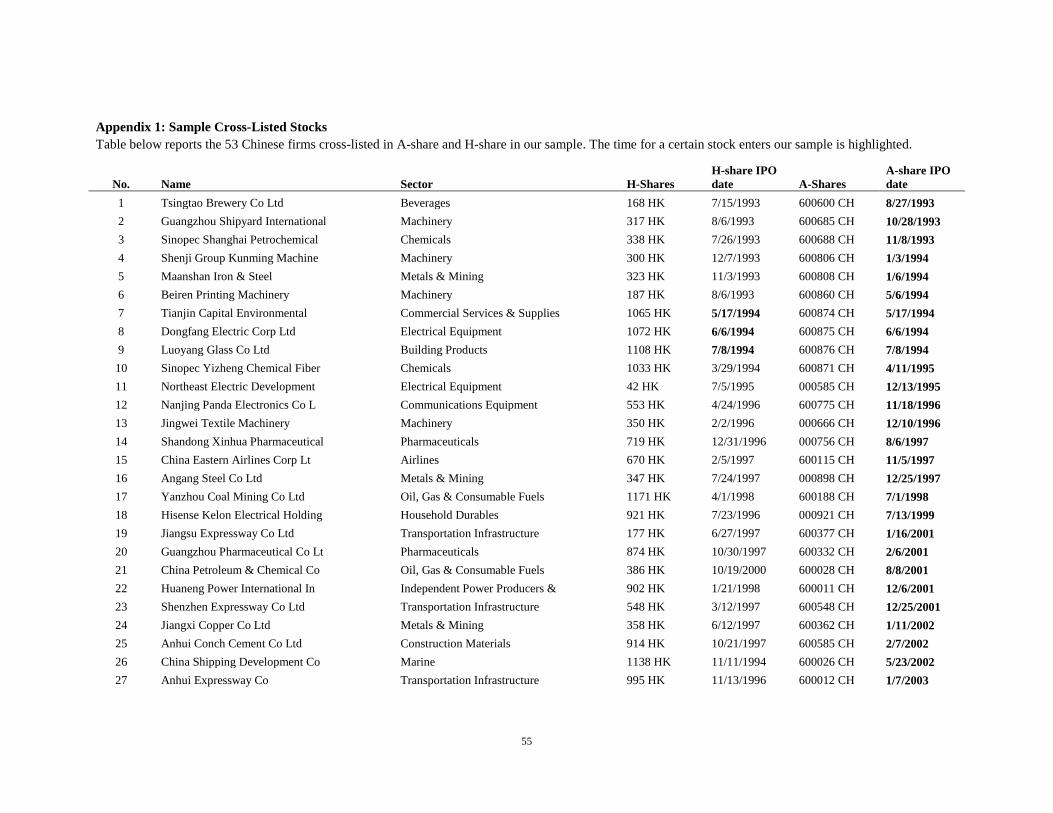

Our sample of stocks consists of the universe of 53 Chinese companies that are cross-

listed in both Mainland China and Hong Kong and have unbroken daily closing price data

for 12 months before and 12 months after at least one of the stamp duty events. Because

the last stamp duty event took place in September 2008, stocks that become cross-listed

after 2008 do not make into our sample. Appendix 1 provides a list of these companies in

the sample and their IPO dates on both stock exchanges, sorted by the date they first

became cross-listed.

Because the number of cross-listed stocks increases gradually during the sample

period, the total number of unique firm-event observations is 223, less than 7 x 53. Daily

information of A- and H-share stocks comes from China Securities Market and

Accounting Research Database (CSMAR), Reuter Datastream and Pacific Basin Capital

Market Database (PACAP).

The summary statistics of our sample is reported in table 2. In panel A, we first show

the mean and median of sample firms’ financial characteristics. Firm financials are

obtained from CSMAR, which reflects the values of the latest annual filing prior to each

event. However, since same firm could enter into our sample for multiple times due to

adjacent events, duplicated observations are eliminated to avoid biases from multiple-

13

counting. The average size of a firm in our sample measured by total asset is RMB350

billion, while the median is about RMB15 billion. The mean and median of annual

revenue are about RMB58 billion and RMB10 billion respectively. On average,

EBIT/sales is 9.7% and annual sales growth is about 17.4%. In addition, the sample firms

have relative low leverage measured by long term debt to total asset at an average of 8.8%

and average cash to total asset is about 11.5%.

Panel B provides the stock characteristics of A- and H-shares in our sample

respectively. Average market capitalization of A-share in our sample is RMB121billion,

while the corresponding value of H-share is about RMB40 billion4, suggesting that

domestic A-share serves as the primary market for these Chinese firms. It is easy to see

that the capital controls that produce the segmentation of the Hong Kong and China stock

markets are binding: H-share stocks see a 50% discount in stock price relative to the A-

share stocks. Although daily transaction volume, return and price volatility are

comparable, A-share is more liquid as suggested by Amihud illiquidity ratio.

In panel C, we also provide the statistics of institutional holding of our sample A-shares

in the latest quarter prior to stamp duty changes. The average fraction held by

institutional investors of the market capitalization of tradable shares is about 20%, while

the average quarterly change in institutional holding is about 9% in our sample. In

addition, on average, our sample firms have 24 institutional investors, while the median is

9.

3.2 Price Response to Stamp Duty Changes

We start with examining the short-term price response of cross-listed A-H shares

around stamp duty changes. As Schwert and Seguin (1993) points out, increases in STT

4 We convert the HKD to RMB with historical daily exchange rate at each trading date.

14

could affect stock price in two ways. First, it might lead to increases in stock price,

because if STT could reduce excessive volatility, the required rate of return from

investors would go down and share price would go up. In contrast, STT is a type of

transaction cost which would raise the required rate of return and therefore put

downwards pressure on stock price. To examine this in the context of stamp duty in

China, a diff-in-diff regression is adopted in the paper and daily stock returns within (-

2days, +2days) window around stamp duty changes5 are tested as following:

(1)

and

are the daily returns of the treatment and control shares respectively,

and equals to one if day t is in the higher stamp duty period and zero

otherwise. For example, for an upward adjustment in the stamp duty, the observations

after the event date will be classified as with higher tax, and vice versa. Furthermore, we

also control for the difference in base interest rate in these two markets in the regression

with the interaction term between control share daily return and difference between

interest rate of mainland and Hong Kong at time t, because interest rate could affect the

stock price via several channels, e.g. change in discount rate affects the fundamental

value of the firm. The historical adjustments in base interest rate in China and Hong

Kong are shown in Appendix 2. Also, Ci,t represents the firm-year fixed effects, and F

reflects other fixed effects in the regression, e.g. month fixed effect. The results on price

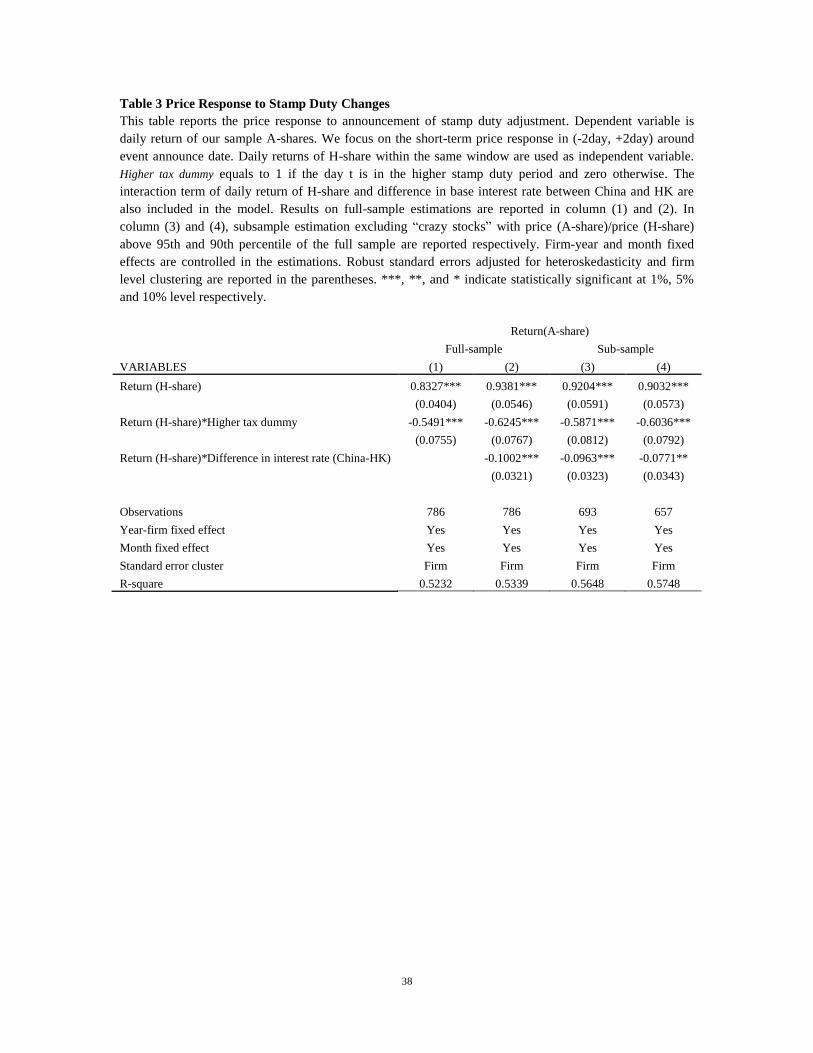

response with respect to stamp duty changes are shown in Table 3. In column 1, the

simple difference-in-differences regression gives a negative and significant estimate of

5 Note that, in general the announcement date is the same as the implementation date

15

the interaction term between H-share return and higher tax dummy, suggesting a short-

term return reduction about 64% (=0.5491*0.07%/0.06%) in high tax regime. When

incorporating interest rate difference between the two markets into the model, similar

results are obtained as shown in column 2. The coefficient on the interaction term

between H-share return and interest rate difference is negative and significant. In other

words, if the A-share market has a high interest rate, the required rate of return would be

higher and stock price would be lower, which is reflected in the realized return.

In order to mitigate any potential bias due to outliers, we further conduct subsample

analyses by eliminating potential outlier stocks. In column 3 and 4, observations with A-

share price over H-share price exceeding 95th

and 90th

percentile of the sample are

dropped in the regression,. Overall, consistent results are found both in full sample and

subsamples, suggesting a significant negative impact of STT on short-term stock return.

3.3 Average Effect on Price Volatility

Firm level price volatility

In this sub-section, we examine the effect of stamp duty changes on price volatility.

For event m, the treatment group consists of A-share stocks in our sample, while the

control group includes their corresponding H-share stocks. We follow Jones and Seguin

(1997) to run the following model:

, (2)

16

, where and

are the fitted values from a 12-lag auto-regression6 of the price

volatility of the stock i in event m for treatment and control groups respectively. Daily

estimated stock standard deviations within the 1-year time window before and after the

event date are considered in the regression. Because we can match stocks in the treatment

and control groups one by one, we can work with firm level data rather than portfolio

level data (which is necessary in Jones and Seguin, 1997).. Since there are multiple

events with opposite adjustment directions (increase/decrease) in our studies, we revise

Jones and Seguin (1997)’s model by replacing with

to align sample observations. equals to

one if the trading day t is in the higher stamp duty period and zero otherwise. Interaction

terms between estimated standard deviation of control group and

are also included in the regression.

In addition, as in figure 3, there is a positive relationship between the magnitude of

stamp duty adjustments and the degree of effect on price volatility. Intuitively, one could

argue that larger increase or reduction of transaction cost is associated with larger

impacts on investors trading behaviors. Therefore, the magnitude of the A-share stamp

duty adjustment is also incorporated in the regressions as following:

(3)

6 ∑

, where is the unsigned daily stock return scaled by √ as Jones and Seguin (1997)

17

, where refers to the absolute magnitude of A-share

stamp duty change in event m. Interaction term of H-share price volatility and difference

in base interest rate between China and Hong Kong are also incorporated in the

estimation, while firm-year and month fixed effects are controlled. Robust standard errors

adjusted for heteroskedasticity are clustered at firm level in our regression estimations.

The results of diff-in-diff regressions are reported in table 4. Column 1 shows the

regression result followed equation (2). The price volatility of H-share stocks is

positively and significantly correlated with A-share stocks, reflecting the effectiveness of

control. The negative and significant coefficient of the interaction term between H-share

price volatility and suggests that, on average, increases in stamp duty

result in a reduction in price volatility. From Table 2, we know that the average daily

price volatility in the A-share market is 0.0310, whereas that in the H-share market is

0.0332. A typical increase in the stamp duty in the sample (by 0.2%) would reduce the A-

share volatility by about 2% (= 0.0198 x 0.0332/0.0310). So the effect is economically

moderate even though it is statistically significant. To put it another way, it would take a

much bigger increase in the stamp duty than actually practiced in China and other

countries to induce an economically large reduction in price volatility.

In addition, unlike the negative coefficient in the estimation of stock return, the

interaction term between H-share price volatility and the difference in the interest rates in

the two markets is positive and significant, indicating the higher interest rate in mainland

relative to Hong Kong, the higher the portion of price volatility of the A-shares is linked

to the price volatility of H-share.

18

In column 2 of table 4, we further incorporate the magnitude of A-share stamp duty

changes into the regressions followed equation (3). However, the results show that the

triple interaction term is insignificant. As there is only a small number of stamp duty

changes, there may not be enough statistical power to detect the effect of the size of a

stamp duty change.

To ensure that the results are not driven by outlier stocks, we also perform a regression

in a subsample where we exclude those stocks whose A share price premium over H

share exceeds the 95th

and 90th

percentiles. The results are reported in Column 3 and 4 of

Table 4. The coefficient on the interaction between a higher tax dummy and the H-share

volatility is still negative and statistically significant. The point estimate is modestly

bigger in absolute term. In other words, by excluding potential outlier stocks, the effect of

a higher transaction tax on volatility becomes somewhat bigger, but still economically

modest.

In panel B of table 4, we further examine the price volatility response followed the

following model as Jones and Seguin (1997).

, (4)

The model is tested in full sample as well as in subsamples which exclude stock

observations with A share price premium over H share at 1th, 5th, and 10th

percentiles

respectively. In subsamples, we find consistently negative and significant coefficients for

the High_tax_dummy, which are consistent with our earlier estimations under different

functional forms.

19

3.4 Additional Robustness Checks

Additional robustness checks are conducted and shown in table 5. First, we re-estimate

our sample by dividing it into two subgroups based on the direction of the stamp duty

changes. This enables us to capture any asymmetric effect of stamp duty changes. We

report the results with the subsample of stamp duty increases in the first column, and

those with stamp duties decreases in the second column. The coefficients on the

interaction between a dummy for higher tax regime and H-share volatility are negative

and statistically significant. A formal t-test does not reject the null that the two

coefficients are the same. Interestingly, the point estimates are 50% larger than that in

Column 1 of Table 4. Of course, one important difference between these regressions and

the on in Column 1 of Table 4 is that they do not impose the restrictions that the

coefficients on the large number of fixed effects as well as those on H-share volatility are

the same between the two subsamples.

Recognizing that firms in the financial service sector and the utility sector may be

different from other manufacturing firms, we also perform a regression for a subsample

that excludes financial and utility firms. The result is reported in Column 3 of Panel A of

Table 5. This does not change the basic pattern that a higher transaction cost is associated

with a lower price volatility; the magnitude is statistically significant but economically

modest.

The validity of an event study approach depends on the maintained assumption that

the event in question – a change in the stamp duty in our case – is the only major event

during the event window. To gain additional confidence, we manually check for each

20

sample firm in the CSMAR database on event disclosure for any significant event around

each event date. Several companies underwent a reform where previously non-traded

shares were converted to tradable during 2005-2008. Some of the conversions were close

to our event dates. In Column 4, Panel A of Table 5, we re-estimate the model for the

subsample of firms without any key events recorded in CASMAR/Factiva/Bloomberg

over the event windows. Reassuringly, we find qualitatively similar results as the full

sample.

In panel B of table 5, we divide the firms into two subsamples of high and low

volatility (based on A-share volatility relative to the sample mean), and re-estimate the

model. In both subsamples, a higher transaction cost is associated with a lower price

volatility, but the effect is stronger for the high-volatility subsample.

Taken together, our findings suggest that price volatility of treatment A-shares relative

to control H-shares is lower in high stamp tax regime and the results are robust in various

subsamples. We interpret our findings as evidence to support the advocates’ view on

Tobin tax and argue that in China context, on average, stamp duty does have a positive

effect on curbing speculation and reducing excessive volatility. At the same time, we find

that the economic effect of a change in stamp duties is relatively modest. Given that the

changes in the size of the stamp duty in China are already on the high side when

compared to other countries’ practices, we conclude that an increase in the transaction

cost can only modestly reduce the price volatility.

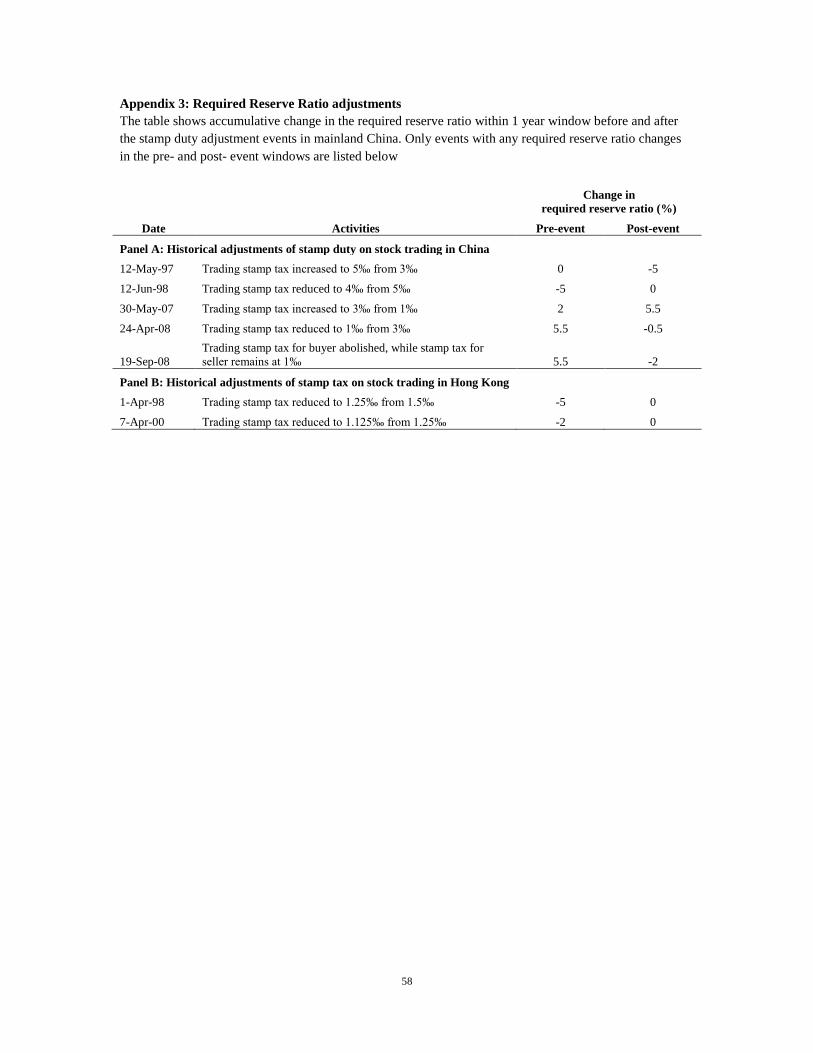

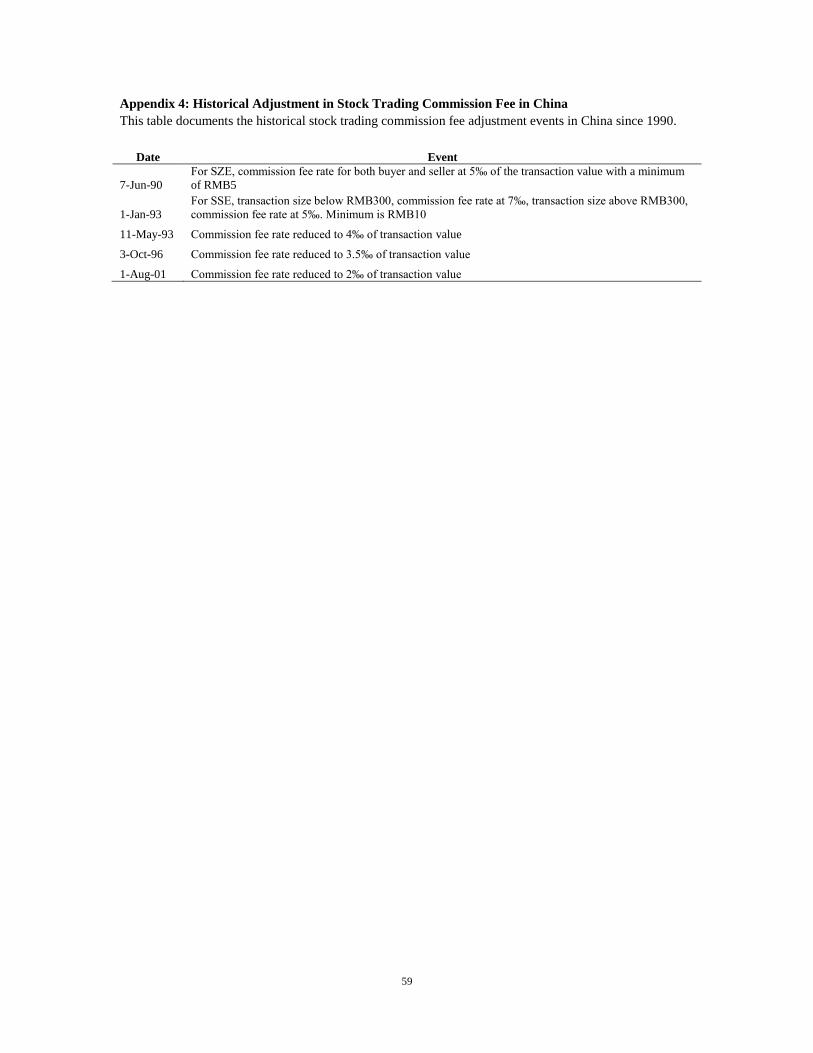

Events such as adjustments in required reserve capital rate (Appendix 3) and

commission fee (Appendix 4), which could potentially affect the price volatility, are also

checked and consistent results are found.

21

Portfolio level price volatility

Most studies in the existing literature form portfolios to examine the effects of stamp

duty. This is mostly out of necessity as there is a lack of stock by stock correspondence

between the treatment and control groups. Nevertheless, for comparison purpose, we

follow Jones and Seguin (1997) to re-estimate the model with portfolio level data in this

section. Equally weighted portfolios of full sample and subsamples are estimated

followed equation (5).

(5)

and

are the fitted values from a 12-lag auto-regression of the portfolio price

volatility for event m and day t for treatment and control groups respectively. Subs-

portfolios are also formed based on the size of tradable shares of A-share stocks. The

details methods are as following. At each event date, the entire A-share stocks are sorted

into 5 quintiles based on their market capitalization of tradable shares. Next, we form size

portfolios with our sample based on their corresponding size quintiles.

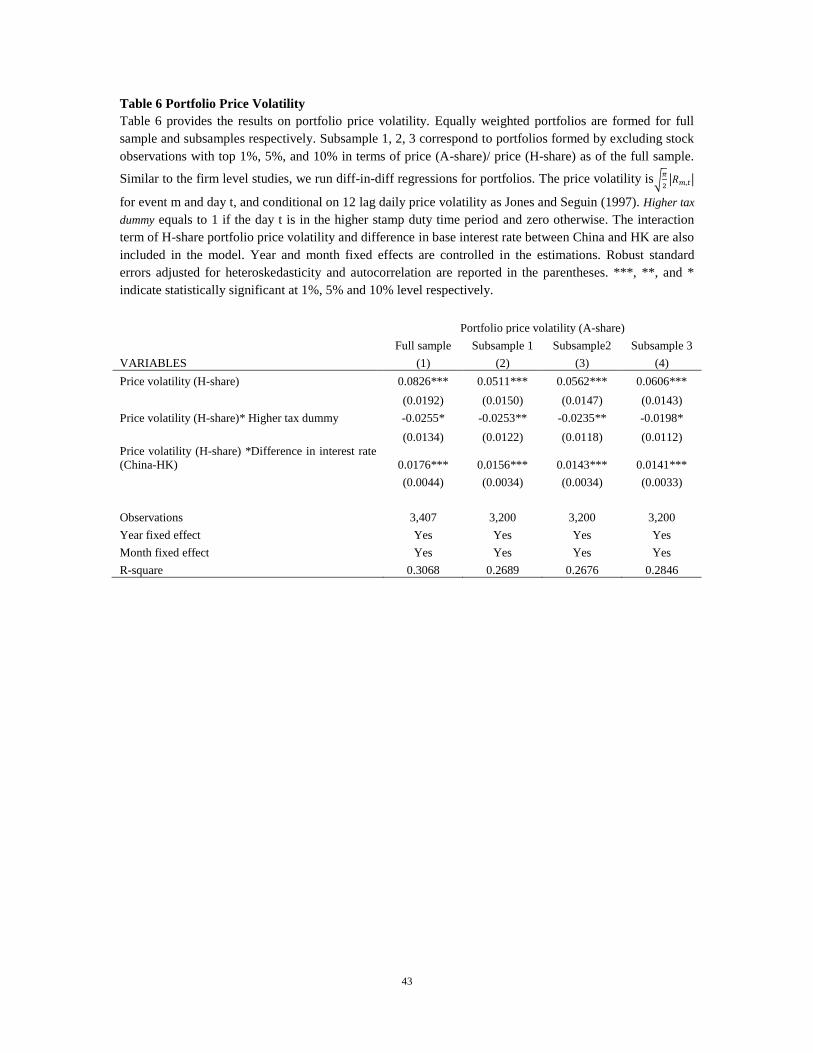

Table 6 shows the regression results. The portfolio of small firms includes sample

firms from the lowest size quintile, while the portfolio of big firms includes sample firms

from the highest quintile. In column 1, we show that full sample estimation with portfolio

level data provides similar result as firm level analyses. In terms of magnitude, the effect

is strengthened with portfolio level data. In addition, as shown in column 2 and 3,

significant negative effects of stamp duty on price volatility are found in portfolios

22

constructed with small and large firms respectively. In unreported analysis, we form

value weighted portfolios and find similar results.

Initial level of stamp duties

We now examine the role of initial level of stamp duty on the response of price

volatility to stamp duty changes. The model is shown as below,

(6)

Ex ante, the effect could go either way. On one hand, higher initial level of stamp duty

prior to adjustment could cause a larger reduction in price volatility when transits from a

low tax regime to a high tax regime. Intuitively, if an investor is taxed at 2‰ and another

investor is taxed at 4‰, suppose a 2‰ increase in stamp duty for both investors, one

could argue that the second investor with higher initial level of stamp duty could response

more in reducing her investment activities. On the other hand, one could also argue that

the relation between initial level of stamp duty and price volatility response is positive,

because the effect of stamp duty has exhausted as the level of stamp duty rises, resulting

in a diminishing effect on price volatility changes. We will let the data to speak to the

issue.

In table 7, we incorporate additional terms reflecting initial level of stamp duty prior to

changes into the model. Particularly, we include a triple interaction term of H-share price

volatility, , and initial level of stamp duty. Column 1 and 2 show the

23

results of full sample. Unlike table 4, we find that the adverse effect of stamp duty on

price volatility change is fully loaded on the triple interaction term. In addition, the

negative coefficient for the triple interaction term suggests that a higher initial level of

stamp duty is associated with larger impact on price volatility reduction when moving

from a low tax regime to a high tax regime.

In Columns 3 and 4 of Table 7, we exclude potential outlier stocks as defined earlier,

and find qualitatively similar results as before.

3.4 Trading Volume

We also investigate the impact of stamp duty changes on trading volume. Unlike price

volatility, empirical evidences appear to agree that increases in stamp duty reduce trading

volume. In our paper, share turnover is adopted as a proxy for trading volume, and is

measured as daily trading volume scaled by market capitalization. Firm level data are

examined in diff-in-diff regression model as following,

(7)

where and

are the daily share turnover of the stock i day t for

event m for treatment and control groups respectively. Several interaction terms between

control group share turnover and , and interest rate difference in the

two markets are incorporated in the regressions as in equation (7).

Our results in table 8 are consistent with the literature which finds a negative relation

between stamp duty and trading volume. In addition, similar as price volatility

24

estimations, magnitude of stamp duty changes doesn’t have a significant effect on share

turnover. In table 9, we replicate firm level turnover estimations with portfolio level data.

Equally weighted portfolios are constructed as in section 4.2.3. Overall, portfolio level

results are similar to firm level ones. However, the magnitude of impact is larger in

portfolios.

4 Institutional Share and the Effect of Stamp Duty on Price Volatility

We have argued that the effect of a higher transaction cost on price volatility depends

out whether the transaction cost drives out more informed fundamental-based traders or

more non-fundamental-based noise traders. The negative effect we have found so far

could reflect the fact that young Chinese stock market has been dominated by non-

fundamental based noise traders.

We now aim to extract more insight by exploring possible heterogeneous price

volatility response both across time periods and across stocks.

As shown in figure 2, the institutional share in the Chinese financial market was non-

existent in the early part of the sample period and remains significantly lower than in

developed markets. For example, in Jones and Seguin (1997), institutional ownership in

the U.S. stock market around the commission deregulation in 1975 is about 25%, while

for China, the number was anywhere near that level only in the tail end of the sample

period, i.e., after 2007. If a greater share of institutional trading implies a proportionately

smaller role of speculative noise trading, it would be interesting to examine whether the

effect of a higher transaction cost on price volatility is reversed in the later part of the

sample period.

25

Evolution of Institutional Investors in China

Guided by Figure 2b, we can divide the entire history of the Chinese equity market

into three periods: (1) The infant stage (1990-1997): after the Shanghai and Shenzhen

stock exchanges were established in 1990, there was virtually no institutional investors,

and the market was almost entirely dominated by retail investors; (2) The toddler stage

(1998-2005): institutional investors have emerged though still not significant in trading.

Investors became relatively less naive after having experienced several ups and downs in

the stock market in the preceding years. (3) The growth stage (after 2006): Institutional

investors start to grow at a high speed and play more important role in the Chinese stock

markets, while some of the retail investors have also become more sophisticated and

more exposed to the knowledge of finance and economics. At the same time, the number

of stocks has increased dramatically. While the exact dividing lines among the three

periods are somewhat arbitrary, they roughly divide the history of the Chinese equity

market (from late 1990 to now) into three stages of equal length, and are meant to capture

the evolution of the relative importance of institutional traders in the market.

We implement the same regression specification as in Column 1 of Table 4 for each

time period, and report the results in Table 10. We focus our discussions on the

coefficients for the interaction term between a dummy for a higher tax regime and H-

share volatility. Interestingly, we see a negative coefficient for the first two historical

periods (1990-1997, and 1998-2005) but a positive coefficient in the more recent period

(after 2006). This intriguing pattern of signs is consistent with the notion that, in earlier

periods when the market is dominated by retail traders, a higher transaction cost reduces

26

price volatility, whereas in the most recent period when institutional investors have

started to play a more important role in the market. It is also interesting to note that, when

we allow the effects to be different in different time periods, the volatility suppressing

effect of a higher transaction cost has also become bigger in the earlier periods. The

coefficients (-0.0720 and -0.0683, respectively) are more than three times as big as the

corresponding coefficient in Table 4.

This result has the potential to explain the different findings of ours and opponents’ of

Tobin tax in the literature, such as Jones and Seguin (1997). As pointed out earlier, the

institutional share in the Chinese financial market in growth era is about the similar level

as in the U.S. market around commission deregulation in 1975 discussed by Jones and

Seguin (1997). Therefore, our findings highlight the importance of investor structure in

driving mixing empirical evidences in the literature. We argue that a thorough

understanding of investor structure studied enables us to get a better comparison of

empirical findings.

Instead of looking at three sub-periods, we can perform separate event studies for

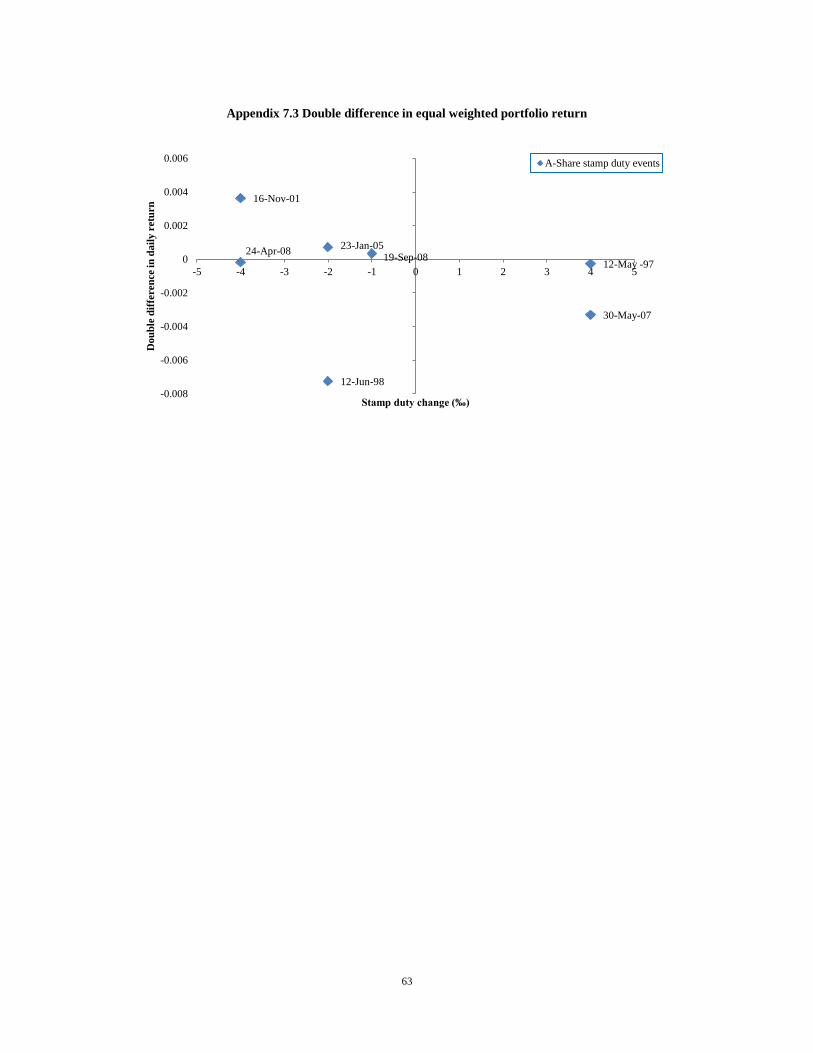

each of the seven changes in the stamp duties. Figure 3 provides the graphical

illustrations of the effects of each stamp duty changes on price volatility over 1-year and

6-month windows. Double difference7 in price volatility is calculated as the change in

price volatility of treatment group (A-share sample stocks) subtracts the change in price

volatility of the control group (H-share sample stocks). Overall, consistent patterns in

price volatility responses to stamp duty changes are found in figure 3, suggesting that

increase in stamp duty leads to reduction in price volatility, while decrease in stamp duty

in general leads to the opposite effect. Figure 3 also shows a positive relation between the

7 Double difference is calculated as

27

magnitude of stamp duty changes and its effect on price volatility. We also plot similar

graphs for share turnover and return, and a consistent negative relationship between

stamp duty and share turnover is found both with firm and portfolio level data.

Institutional Share and Price Volatility

While the results in the previous subsection are suggestive, we cannot read too much

into a data pattern from three time periods. Next, we use three direct measures of

institutional ownership in the estimations, constructed with institutional ownership level

and number of institutional investors8. First, we adopt the reported information from

WIND on institutional ownership at firm level on quarterly basis. The first available data

starts from the 2nd

quarter of 1998. For firms without information on institutional

ownership reported in the database, we consider them have zero institutional ownership

at the reporting time.

Our second measure is the change of institutional ownership in the latest quarter prior

to the stamp duty changes in our sample. We consider the absolute value of the

institutional holding changes as a proxy for institutional trading at stock level.

Our last measure of the relative importance of institutional investors at the stock-

event level is the number of institutional investors in logarithm. The regression results are

reported in table 11. Consistently negative relations between stamp duty changes and

price volatility for stocks with low institutional ownership are found in full sample and

subsamples excluding outlying stocks.

8 Information on institutional ownership for sample A-shares is obtained from WIND database one quarter

prior to stamp duty changes. For firms without any institutional ownership information reported, we

consider them as zero.

28

Interestingly, the coefficients on the trip interaction terms are all positive and

statistically significant. In column 1, in estimation with institutional ownership level, as

institutional ownership level increases, the negative effect of stamp duty increases on

price volatility reduces. However, the coefficient estimation is insignificant. As we

substitute the institutional ownership with more direct proxy of institutional trading in

column 2, our results confirm that stocks with more institutional trading lower the

negative effect of stamp duty on price volatility, Similarly, in column 3, when use natural

logarithm of the total number of institutional investors, we find a positive coefficient,

which suggests that increases in institutional share weaken the effect of stamp duty in

reducing price volatility.

In columns 4 to 6, the subsample eliminates observations with A-share price over H-

share price above 90th

percentile are performed and consistent results are found in

subsamples, confirming that the results are not driven by any outliers.

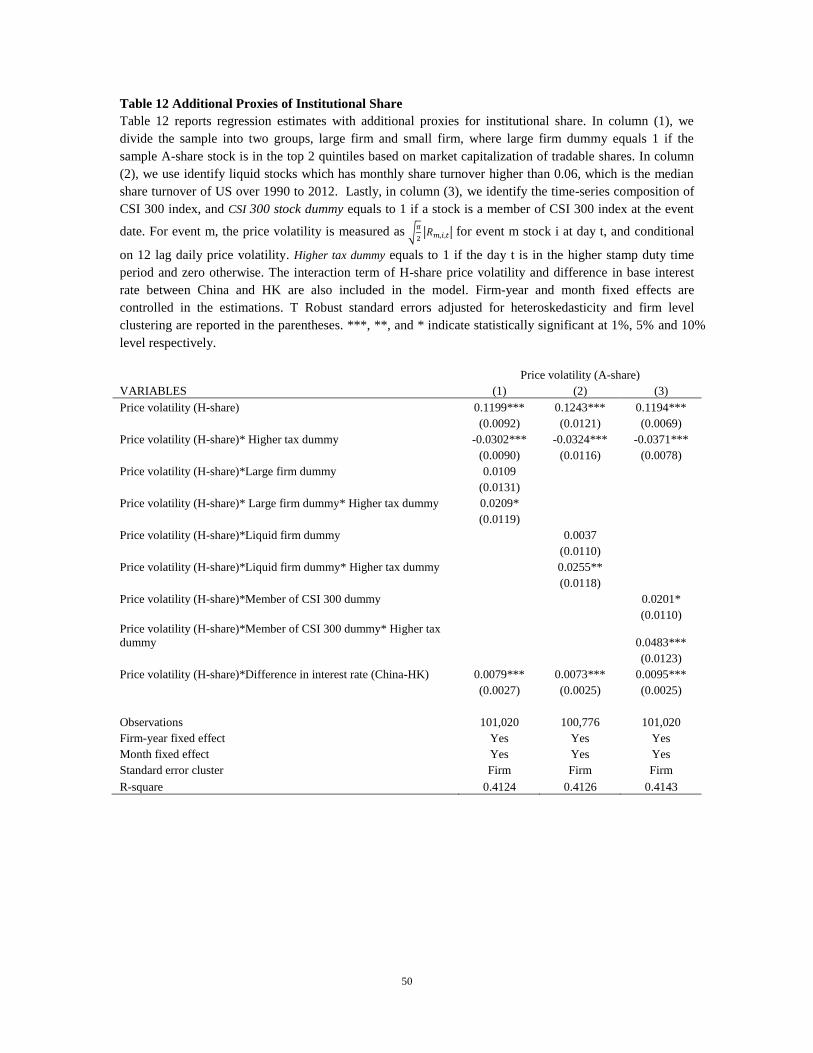

Additional Proxies for Institutional Trading

Some additional regression estimations are performed and results are reported in table

12. First, we define a large firm dummy which equals to one if the sample firm is the top

two size quintiles based on free float market capitalization around each event, and zero

otherwise. Firm size is argued in many studies as proxy for institutional ownership.

Therefore, one should expect to find a smaller price volatility response in the event of

stamp duty increases among large firms as they attract more institutional investing.

Result shown in column 1 confirms with this conjecture.

29

Next, we test how firm liquidity affects our results. On average, A-share stocks are

more liquid than stocks in the U.S. market9. Therefore, we use the median monthly share

turnover level of 0.06 in the U.S. market between 1990 and 2012 as a cutoff point. Share

turnover is measured as monthly trading volume over market capitalization. Hence, we

construct a liquidity firm dummy which equals to one if firm’s average monthly share

turnover over the one year period prior to stamp duty change is higher than 0.06, and zero

otherwise. In column 2 of table 12, we find that price volatilities of liquid firms reduce

less to stamp duty increases.

Lastly, we use the membership of some indices as proxies of institutional trading. In

particular, we examine how being a member of CSI 300 index affect the role of stamp

duty in lowering price volatility. Established in April 2005, CSI 300 accounts for over 60%

of SSE and SZSE A-share markets based on market capitalization, and a growing number

of funds benchmark upon it. We argue that a stock become member of CSI 300 would

naturally increase its exposure to institutional trading. Therefore, we expect being a

member of CSI 300 would lower the negative impact of stamp duty increases on price

volatility. In column 3, our results confirms with our conjecture, suggesting that inclusion

in CSI 300 has positive impact on price volatility.

Overall, our findings on institutional share confirm our conjecture that stocks with

more institutional investors experience smaller reduction in price volatility in response to

increases in stamp duty. The rationale behind it is that the competing effects of stamp

duty changes on price volatility are highly correlated with the fraction of informed and

noise traders. In some cases, as institutional investors play more and more significant role

in trading certain securities, increases in stamp duty could even result in increases in

9 Median of monthly share turnover between 1990 and 2012 are 0.06 (U.S.) and 0.12 (China A-share).

30

price volatility of those stocks, as in these stocks, large reduction in institutional trading

deters price discovery process and leads to higher volatility, and this effect dominates the

price volatility reduction from reduced noise trading.

5 Conclusion

Although many studies have been conducted with the goal to tackle the long-lasting

debate over Tobin tax, mixed empirical evidences have been found so far in the literature.

A potential problem in the existing studies is that the treatment and the control groups

may not have truly identical corporate fundamentals. Unlike existing studies, our paper

studies the effect of transaction cost on eliminating excess volatility and dampening the

speculation with a unique sample consisting of all the cross-listed A and H-shares in

China. The historical stamp duty adjustments in China A-share market are adopted as

natural experiments and we argue that the twin-share offers a clean treatment-control pair

with identical fundamentals but different transaction cost environments. Diff-in-diff

regressions are estimated at both firm and portfolio levels which show that increase in

stamp duty relates to reduction in price volatility, share turnover, and return.

Furthermore, we make effort to understand the reasons discrepancies in empirical

evidences on the topic. We argue that investor structure plays a key role in the story,

because reduction in trading by informed and noise traders due to stamp duty increases

could lead to completely opposite effect on price volatility. Therefore, from market

perspective, the aggregate effect of stamp duty on price volatility combines the two

competing effects driven by informed and noise traders respectively, and highly depends

on the relative proportion of each group in the market or in a security. In the literature,

31

institutional investors are commonly considered as informed trader, while retail investors

are considered as noise trader. In our analyses, various proxies of institutional trading are

incorporated into the estimations, and all of these proxies suggest that increases in the

fraction of institutional share weakened the negative effect of stamp duty on price

volatility.

In addition, our studies shed lights on disentangling the mixed evidences in the

literature. As Tobin tax is introduced to deter speculation of noise traders, and the effects

of transactions tax decreases as the fraction of noise trader drops. Developed markets

such as U.S. have much higher institutional ownership on average than emerging markets

like China, and informed institutional investors would have different response to

transaction tax. Hence, the different empirical findings on transaction tax could be

primarily driven by the different nature of the examined markets.

In summary, our findings largely support the proponents of security transaction tax

such as Tobin (1984), Stiglitz (1989) and Summers and Summers (1989), but only in a

setting in which institutional investors do not play a significant role in the market. We

argue that China offers a unique context which is close to the market condition as Tobin

first suggested security transaction tax. In this setting, when noise traders play important

role in the stock market and lead to excessive market volatility, transaction tax such as

stamp duty could serve as an effective method to curb speculation and improve stability

of the financial market. In particular, we highlight the role of investor structure in

disentangling the mixed evidences found in the literature. Finally, the paper has many

policy implications which not only apply to stock market but also to markets with broad

asset classes.

32

33

Reference

Aliber, Robert Z., Chowdhry, Bhagwan and Yan, Shu, 2002, “Some Evidence that a

Tobin Tax on Foreign Exchange Transactions may Increase Volatility”, European

Finance Review 7: 481–510, 2003

Amihud, Yakov, 2002, “Illiquid and Stock Returns: Cross-Section and Time-Series

Effects”, Journal of Financial Markets, 5, 31-56

Aregger, N., Brown, M. and Enzo, R., 2012, “Can a Transaction Tax or Capital Gains

Tax Smooth House Prices?”, working paper

Atkins, Allen B. and Dyl, Edward A., 1997, “Stock Price Volatility, Transaction Costs

and Securities Transactions Taxes”, Managerial and Decision Economics, 18(7-8),

709-718

Baltgi, Badi H., Li, Dong and Li, Qi, 2006, “Transaction Tax and Stock Market Behavior:

Evidence from an Emerging Market”, Empirical Economics, 31(2), 393-408

Chou, Robin K., and Wang, George H. K., 2006, “Transaction Tax and Market Quality of

the Taiwan Stock Index Futures”, Journal of Futures markets, 26, 1195-1216

Chow, Gregory C. (1960). "Tests of Equality between Sets of Coefficients in Two Linear

Regressions". Econometrica 28 (3): 591–605

De Long, Bradford, Andrei Shleifer, Lawrence H. Summers, and R. J. Waldman, 1990,

“Noise Trader Risk in Financial Markets”, Journal of Political Economy, 98(4),

703-38

Fu, Yuming, Qian, Wenlan, and Yeung, Bernard, 2012, “Financial Transaction Tax: the

Double-edged Sword Effects on Price Stability”, Working paper

Green, Christopher J., Maggioni, Paolo and Murinde, Victor, 2000, “ Regulatory Lessons

for Emerging Stock markets from A Century of Evidence on Transactions Costs

and Share Price Volatility in the London Stock Exchange”, Journal of Banking &

Finance, 24(4), 577-601

Grundfest, Joseph A., 1990, “The Damning Facts of a New Stocks Tax”, Wall Street

Journal, July 23rd

Grundfest, Joseph A., and Shoven, John B., 1991, “Adverse Implications of a Securities

Transaction Exercise Tax”, Journal of Accounting, Auditing, and Finance, 6,(4),

409-442

34

Habermeier, Karl and Kirilenko, Andrei A., 2001, “Securities Transaction Taxes and

Financial Markets”, IMF working paper

Hanke, Michael, Huber J., Kirchler, M. and Sutter, M., 2010, “The Economic

Consequences of A Tobin Tax – An Experimental Analysis”, Journal of

Economic Behavior & Organization, 74(1-2), 58-71

Hau, Harald, 2006, “The Role of Transaction Costs for Financial Volatility: Evidence

from the Paris Bourse”, Journal of the European Economic Association, 4(4),

862-890

Hu, Shing-yang, 1998, “The Effects of the Stock Transaction Tax on the Stock Market –

Experiences from Asian Markets”, Pacific-Basin Finance Journal, 6(3-4), 347-

364

Jones, Charles M., and Seguin, Paul J., 1997, “Transaction Costs and Price Volatility:

Evidence from Commission Deregulation”, The American Economic Review,

87(4), 728-737

Kupiec, Paul H., 1996, “Noise Traders, Excessive Volatility, and a Securities

Transactions Tax”, Journal of Financial Services Research, 10, 115-129

Lanne, Markku, and Vesala, Timo, 2010, “The Effect of A Transaction Tax on Exchange

Rate Volatility”, International Journal of Finance & Economics, 15(2), 123-133

Liu, Shinhua and Zhu, Zhen, 2009, “Transaction Costs and Price Volatility: New

Evidence from the Tokyo Stock”, Journal of Financial Services Research, 36(1),

65-83

Phylakti, Kate S. and Aristidou, Antonis., 2007, “Security Transaction Taxes and

Financial Volatility: Athens Stock Exchange”, Applied Financial Economics,

17(18), 1455-1467

Roll, Richard, 1989, “Price Volatility, International Market Links, and Their Implications

for Regulatory Policies”, Journal of Financial Services Research, 3, 211-246

Sheffrin, Steven M. and Turner, Tracy M., 2001, “Taxation and House-Price Uncertainty:

Some Empirical Estimates”, International Tax and Public Finance, 8, 621-636

Stiglitz, Joseph E., 1989, “Using Tax Policy to Curb Speculative Short-term Trading”,

Journal of Financial Services Research, 3(2-3), 101-115

35

Summers, Lawrence H. and Summers, Victoria P., 1989, “When Financial Markets Work

Too Well: A Cautious Case for a Securities Transaction Tax”, Journal of

Financial Services Research, 3(2-3), 261-286

Tobin, James, 1978, “A Proposal for International Monetary Reform”, Eastern Economic

Journal, 4, 153-159

Tobin, James, 1984, “On the Efficiency of the Financial System”, Lloyd Bank Review,

153, 1-15

Umlauf, Steven R., 1993, “Transaction Taxes and the Behavior of the Swedish Stock

Market”, Journal of Financial Economics, 33(2), 227-240

Westerholm, Joakim, 2003, “The Impact of Transaction Costs on Turnover, Asset Prices

and Volatility: The Cases of Sweden’s and Finland’s Security Transaction Tax

Reductions”, The Finnish Journal of Business Economics, 2(3), 213-241

36

Table 1 Historical adjustment of stamp duties on stock trading in China and Hong Kong

Table 1 lists all the historical adjustments of stock trading stamp duty in China (A-share) and Hong Kong

from 1990 to 2013.

Date Activities

Panel A: Historical adjustments of stamp duty on stock trading in China

12-May-97 Trading stamp tax increased from 3‰ to 5‰

12-Jun-98 Trading stamp tax reduced from 5‰ to 4‰

16-Nov-01 Trading stamp tax reduced from 4‰ to 2‰

23-Jan-05 Trading stamp tax reduced from 2‰ to 1‰

30-May-07 Trading stamp tax increased from 1‰ to 3‰

24-Apr-08 Trading stamp tax reduced from 3‰ to 1‰

19-Sep-08 Trading stamp tax for buyer abolished, while stamp tax for seller remains at 1‰

Panel B: Historical adjustments of stamp duty on stock trading in Hong Kong

1-Apr-98 Trading stamp tax reduced from 1.5‰ to 1.25‰

7-Apr-00 Trading stamp tax reduced from 1.25‰ to 1.125‰

1-Sep-01 Trading stamp tax reduced from 1.125‰ to 1‰

37

Table 2 Summary Statistics

Table 2 reports the summary statistics of our sample. There are 223 firm-event observations in our sample.

Panel A shows the financial characteristics of the sample firms cross-listed both in A- and H-share markets.

The financial information acquired from CSMAR reflects the latest annual filing prior to each event date.

However, because the same firm enters into our sample multiple times given adjacent events, duplicated

observations for firms with same annual filing are eliminated in reporting the financial characteristics. In

panel B, the stock characteristics of A- and H-shares in our sample are reported respectively. The mean

values of the key stock characteristic variables over a 2-year window around each event date are reported.

Panel C reports the mean and median of institutional holding of sample A-shares in the latest quarter prior

to a certain stamp duty change. Institutional holding information is obtained from WIND database, and

institutional ownership is shown as a fraction of total market capitalization of tradable shares in the same

reporting period. Absolute change in institutional holding reflects the aggregate change in institutional

holding within the one quarter prior to stamp duty changes. Number of institutional investors is also

reported in the table. All the variables are reported in RMB, and for H-shares, we convert the HKD to RMB

based on the historical daily exchange rate.

Panel A: Financial Characteristics

Currency: RMB Mean Median

No. observations 223

Total asset (mil) 349,843 15,057

Sales (mil) 58,205 9,784

Cash/Total asset 11.5% 9.2%

EBIT/Sales 9.7% 6.3%

Net income margin 6.6% 4.9%

Sales growth 17.4% 15.5%

Debt/Total asset 9.3% 5.5%

Panel B: Stock Characteristics

Currency: RMB A-share H-share

Market Capitalization (mil) 120,857 40,129

Stock price 13.4 6.7

Average value of daily transaction volume (mil) 268 256

Average daily return 0.06% 0.07%

Average daily price volatility 0.0310 0.0332

Average daily share turnover 0.0057 0.0115

Amihud illiquidity ratio 0.0015 0.0360

Panel C: Institutional Holding Characteristics

Mean Median

Institutional ownership (% of tradable shares) 19.7 12.6

Absolute institutional ownership change (% of tradable shares) 8.6 4.1

Number of institutional investors 24 9

38

Table 3 Price Response to Stamp Duty Changes

This table reports the price response to announcement of stamp duty adjustment. Dependent variable is

daily return of our sample A-shares. We focus on the short-term price response in (-2day, +2day) around

event announce date. Daily returns of H-share within the same window are used as independent variable.

Higher tax dummy equals to 1 if the day t is in the higher stamp duty period and zero otherwise. The

interaction term of daily return of H-share and difference in base interest rate between China and HK are

also included in the model. Results on full-sample estimations are reported in column (1) and (2). In

column (3) and (4), subsample estimation excluding “crazy stocks” with price (A-share)/price (H-share)

above 95th and 90th percentile of the full sample are reported respectively. Firm-year and month fixed

effects are controlled in the estimations. Robust standard errors adjusted for heteroskedasticity and firm

level clustering are reported in the parentheses. ***, **, and * indicate statistically significant at 1%, 5%

and 10% level respectively.

Return(A-share)

Full-sample Sub-sample

VARIABLES (1) (2) (3) (4)

Return (H-share) 0.8327*** 0.9381*** 0.9204*** 0.9032***

(0.0404) (0.0546) (0.0591) (0.0573)

Return (H-share)*Higher tax dummy -0.5491*** -0.6245*** -0.5871*** -0.6036***

(0.0755) (0.0767) (0.0812) (0.0792)

Return (H-share)*Difference in interest rate (China-HK)

-0.1002*** -0.0963*** -0.0771**

(0.0321) (0.0323) (0.0343)

Observations 786 786 693 657

Year-firm fixed effect Yes Yes Yes Yes

Month fixed effect Yes Yes Yes Yes

Standard error cluster Firm Firm Firm Firm

R-square 0.5232 0.5339 0.5648 0.5748

39

Table 4 Stamp Duties and Stock Price Volatility

Table 4 provides results of multivariate analyses on daily price volatility with respect to stamp duty

changes. The price volatility is measured as √

| | for event m stock i at day t, and conditional on 12

previous daily price volatility followed Jones and Seguin (1997). Higher tax dummy equals to 1 if the day t is

in the higher stamp duty period and zero otherwise, i.e. for a positive stamp duty adjustment, the

observations after the event date will be classified as with higher tax, and vice versa. The interaction term

of H-share price volatility and difference in base interest rate between China and HK are also included in

the model. In Panel A, we estimate our sample price volatility followed the equation shown below:

Results on full-sample estimations

are reported in column (1) and (2), and size of change in stamp duties is included and corresponding

interaction terms are added in the regressions. In column (3) and (4), subsample estimations excluding

observations of “crazy stocks” which has price(A-share)/price(H-share) of top 5 and 10 percentiles of the

sample are reported respectively. In Panel B, we re-estimate our sample with full sample and subsamples

excluding stock observations with price (A-share)/ price (H-share) above 1, 5, and 10 percentiles of full

sample respectively followed the equation as

Firm-year and month fixed effects are controlled in the estimations. Robust standard errors adjusted

for heteroskedasticity and firm level clustering are reported in the parentheses. ***, **, and * indicate

statistically significant at 1%, 5% and 10% level respectively.

Panel A Price volatility (A-share)

Full-sample Sub-sample

VARIABLES (1) (2) (3) (4)

Price volatility (H-share) 0.1373*** 0.1212*** 0.1273*** 0.1241***

(0.0089) (0.0095) (0.0099) (0.0098)

Price volatility (H-share)* Higher tax dummy -0.0198** -0.0216** -0.0265*** -0.0263***

(0.0075) (0.0090) (0.0091) (0.0091)

Price volatility (H-share)*Size of change in A-share stamp

duty

0.0013 0.0005 0.0007

(0.0010) (0.0009) (0.0009)

Price volatility (H-share)*Size of change in A-share stamp

duty* Higher tax dummy

0.0023 0.0025* 0.0020

(0.0015) (0.0015) (0.0015)

Price volatility (H-share)*Difference in interest rate

(China-HK)

0.0072*** 0.0068** 0.0070***

(0.0026) (0.0025) (0.0025)

Observations 101,020 101,020 83,777 79,373

Year-firm fixed effect Yes Yes Yes Yes

Month fixed effects Yes Yes Yes Yes

Standard error cluster Firm Firm Firm Firm

R-square 0.4112 0.4120 0.4126 0.4137

40

Panel B Price volatility (A-share)

Full sample Subsample 1 Subsample 2 Subsample 3

VARIABLES (1) (2) (3) (4)

Price volatility (H-share) 0.1270*** 0.1304*** 0.1283*** 0.1251***

(0.0087) (0.0087) (0.0086) (0.0086)

Higher tax dummy -0.0004 -0.0004* -0.0005** -0.0006**

(0.0003) (0.0003) (0.0003) (0.0003)

Observations 101,020 87,289 83,777 79,373

Year-firm fixed effect Yes Yes Yes Yes

Month fixed effect Yes Yes Yes Yes

Standard error cluster Firm Firm Firm Firm

R-square 0.4107 0.4089 0.4111 0.4121

41

Table 5 Robustness Checks

Several robustness checks are conducted and results are shown in following table. Firm level data are

estimated with diff-in-diff regressions. In panel A, we first divide our sample into two subsamples based on

the direction (increase or decrease) of stamp duty adjustments. In column (3), we exclude the financial and

utility firms based on the industry classification (indcd=1 refers to financial firms and indcd=2 refers to

utility firms) from CSMAR. In column (4), we manually check and exclude the firm observations with

significant event, e.g. massive non-tradable shares transfer to tradable shares, over the event window. In

panel B, we divide the sample into two groups based on A-share price volatility. High volatility group

includes stocks with price volatility higher than (and include) sample mean, while low volatility group

contains the rest. For event m, the price volatility is measured as √

| | for event m stock i at day t, and

higher tax dummy equals to 1 if the day t is in the higher stamp duty time period and zero otherwise. The

price volatility of A-share and H-share used in the regression are the estimated standard deviation of returns

conditional on 12 previous daily price volatility followed Jones and Seguin (1997). The interaction term of

H-share price volatility and difference in base interest rate between China and HK are also included in the

model at monthly frequency. Firm-year and month fixed effects are controlled in the estimations. Robust

standard errors adjusted for heteroskedasticity and firm level clustering are reported in the parentheses. ***,

**, and * indicate statistically significant at 1%, 5% and 10% level respectively.

Panel A Price volatility (A-share)

(1) (2) (3) (4)

VARIABLES

Reduce

stamp duty

events

Increase

stamp duty

events

Sub-industry

(excl.

financial &

utility

sectors)

Sub-sample

(excl. firms

with

significant

event)

Price volatility (H-share) 0.1293*** 0.1945*** 0.1140*** 0.1150***

(0.0100) (0.0201) (0.0100) (0.0125)

Price volatility (H-share)* Higher tax dummy -0.0317*** -0.0330* -0.0205** -0.0189**

(0.0077) (0.0169) (0.0096) (0.0082)

Price volatility (H-share) *Difference in interest rate

(China-HK) 0.0099*** 0.003 0.0080*** 0.0079***

(0.0024) (0.0044) (0.0026) (0.0028)

Observations 77,542 23,478 66,242 68,403

Firm-year fixed effect Yes Yes Yes Yes

Month fixed effect Yes Yes Yes Yes

Standard error cluster Firm Firm Firm Firm

R-square 0.3990 0.2856 0.3942 0.4223

42

Panel B Price volatility (A-share)

(1) (2)

VARIABLES High volatility Low volatility

Price volatility (H-share) 0.1048*** 0.0299***

(0.0068) (0.0036)

Price volatility (H-share)* Higher tax dummy -0.0157** -0.0065*

(0.0068) (0.0034)

Price volatility (H-share) *Difference in interest rate (China-HK) -0.0059** 0.0064***

(0.0024) (0.0010)

Observations 43,800 57,220

Firm-year fixed effect Yes Yes

Month fixed effect Yes Yes

Standard error cluster Firm Firm

R-square 0.2065 0.2656

43

Table 6 Portfolio Price Volatility

Table 6 provides the results on portfolio price volatility. Equally weighted portfolios are formed for full

sample and subsamples respectively. Subsample 1, 2, 3 correspond to portfolios formed by excluding stock

observations with top 1%, 5%, and 10% in terms of price (A-share)/ price (H-share) as of the full sample.

Similar to the firm level studies, we run diff-in-diff regressions for portfolios. The price volatility is√

| |

for event m and day t, and conditional on 12 lag daily price volatility as Jones and Seguin (1997). Higher tax

dummy equals to 1 if the day t is in the higher stamp duty time period and zero otherwise. The interaction

term of H-share portfolio price volatility and difference in base interest rate between China and HK are also

included in the model. Year and month fixed effects are controlled in the estimations. Robust standard

errors adjusted for heteroskedasticity and autocorrelation are reported in the parentheses. ***, **, and *

indicate statistically significant at 1%, 5% and 10% level respectively.

Portfolio price volatility (A-share)

Full sample Subsample 1 Subsample2 Subsample 3

VARIABLES (1) (2) (3) (4)

Price volatility (H-share) 0.0826*** 0.0511*** 0.0562*** 0.0606***

(0.0192) (0.0150) (0.0147) (0.0143)

Price volatility (H-share)* Higher tax dummy -0.0255* -0.0253** -0.0235** -0.0198*

(0.0134) (0.0122) (0.0118) (0.0112)

Price volatility (H-share) *Difference in interest rate

(China-HK) 0.0176*** 0.0156*** 0.0143*** 0.0141***

(0.0044) (0.0034) (0.0034) (0.0033)

Observations 3,407 3,200 3,200 3,200

Year fixed effect Yes Yes Yes Yes

Month fixed effect Yes Yes Yes Yes

R-square 0.3068 0.2689 0.2676 0.2846

44

Table 7 Effects of Initial Size of Stamp Duties

Table 7 examines the effects of initial size of stamp duties on price volatility. Initial size of stamp duties is

included and corresponding interaction terms are added in the regressions. The price volatility is measured

as √

| | for event m stock i at day t, and conditional on 12 previous daily price volatility followed Jones

and Seguin (1997). Higher tax dummy equals to 1 if the day t is in the higher stamp duty period and zero

otherwise, i.e. for a positive stamp duty adjustment, the observations after the event date will be classified

as with higher tax, and vice versa. The interaction term of H-share price volatility and difference in base

interest rate between China and HK are also included in the model. Results on full-sample estimations are

reported in column (1) and (2). In column (3) and (4), subsample estimation excluding “crazy stocks” with

price (A-share)/price(H-share) above 95th and 90th percentile of the full sample are reported respectively.

Firm-year and month fixed effects are controlled in the estimations. Robust standard errors adjusted for

heteroskedasticity and firm level clustering are reported in the parentheses. ***, **, and * indicate

statistically significant at 1%, 5% and 10% level respectively.

Price volatility (A-share)

Full-sample Sub-sample

VARIABLES (1) (2) (3) (4)

Price volatility (H-share) 0.1509*** 0.1305*** 0.1359*** 0.1333***

(0.0113) (0.0112) (0.0114) (0.0112)

Price volatility (H-share)* Higher tax dummy 0.0093 0.0281*** 0.0212** 0.0195*

(0.0115) (0.0103) (0.0103) (0.0103)

Price volatility (H-share)*Initial size of A-share stamp

duty -0.0013 0.0001 -0.0003 -0.0003

(0.0011) (0.0010) (0.0010) (0.0010)

Price volatility (H-share)*Initial size of A-share stamp

duty* Higher tax dummy -0.0062*** -0.0089*** -0.0083*** -0.0081***

(0.0015) (0.0013) (0.0013) (0.0013)

Price volatility (H-share)*Difference in interest rate

(China-HK)

0.0099*** 0.0093*** 0.0095***

(0.0026) (0.0025) (0.0025)

Observations 101,020 101,020 83,777 79,373

Firm-year fixed effect Yes Yes Yes Yes

Month fixed effect Yes Yes Yes Yes

Standard error cluster Firm Firm Firm Firm

R-square 0.4128 0.4141 0.4147 0.4158

45

Table 8 Stamp Duties and Share Turnover

Table 8 provides results of diff-in-diff regressions on share turnover. 1-year window before and after stamp

duty changes is considered in the estimations. Daily share turnover is calculated as

for

event m stock i at day t, and Higher tax dummy equals to 1 if the day t is in the higher stamp duty period and

zero otherwise, i.e. for a positive stamp duty adjustment, the observations after the event date will be

classified as with higher tax, and vice versa. Size of changes in A-share stamp duties and corresponding

interaction terms are added in the regressions. The interaction term of H-share turnover and difference in

base interest rate between China and HK are also included in the model. Results on full-sample estimations

are reported in column (1) and (2). In column (3) and (4), subsample estimations excluding “crazy stocks”

with price(A-share)/price(H-share) above 95th

and 90th percentiles of the full sample are reported

respectively. Firm-year and month fixed effects are controlled in the estimations. Robust standard errors

adjusted for heteroskedasticity and firm level clustering are reported in the parentheses. ***, **, and *

indicate statistically significant at 1%, 5% and 10% level respectively.

Share turnover (A-share)

Full-sample Sub-sample

VARIABLES (1) (2) (3) (4)

Share turnover (H-share) 0.1264*** 0.1291*** 0.1408*** 0.1391***

(0.0119) (0.0150) (0.0154) (0.0153)

Share turnover (H-share)* Higher tax dummy -0.0730*** -0.0874*** -0.0933*** -0.0922***

(0.0105) (0.0161) (0.0155) (0.0153)