of orange county (a component unit of the …a component unit of the county of orange, california)...

TRANSCRIPT

(a Component Unit of the County of Orange, California)

● ● ● www.occhildrenandfamilies.com

● ● ●

Comprehensive Annual Financial Report For the Fiscal Year Ended June 30, 2013

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY

(a Component Unit of the County of Orange, California)

COMPREHENSIVE ANNUAL FINANCIAL REPORT For the Fiscal Year Ended June 30, 2013

Prepared by:

Michael Garcell, CPA

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY (a Component Unit of the

County of Orange, California)

COMPREHENSIVE ANNUAL FINANCIAL REPORT

For the Year Ended June 30, 2013

Michael Garcell, CPA

Finance Manager

CHILDREN AND FAMILIES COMMISSION

OF ORANGE COUNTY FOR THE YEAR ENDED JUNE 30, 2013

Table of Contents INTRODUCTORY SECTION: Page(s)

Letter of Transmittal………………………………………………………………………………………. i

Board of Commissioners…………………………………………………………………………............... iv

Organization Chart………………………………………………………………………………………… v

FINANCIAL SECTION:

Independent Auditors’ Report……...…………………………………………………………….……….. 1

Management’s Discussion and Analysis (Required Supplementary Information).........................……….. 3

Basic Financial Statements:

Statement of Net Position………………………………………………………………………..…….. 15

Statement of Activities………………………………………………………………………………… 16

Governmental Fund Balance Sheet……………………………………………………………………. 17

Reconciliation of the Governmental Fund Balance Sheet to the Statement of Net Position………….…………………………………………………………

18

Governmental Fund Revenues, Expenditures and Changes in Fund Balance…………………………………………..…….………

19

Reconciliation of the Change in Fund Balance to the Changes in Fund Balance to the Statement of Activities………………………..……………

20

Statement of Revenues, Expenditures and Changes in Fund Balance – Budget and Actual……………..………………………..………………..…………

21

Notes to Basic Financial Statements…………………………………………………………………… 22

OTHER SUPPLEMENTARY INFORMATION:

Schedule of First 5 California Funding………………………………………………………………… 34

STATISTICAL SECTION:

Financial Trends

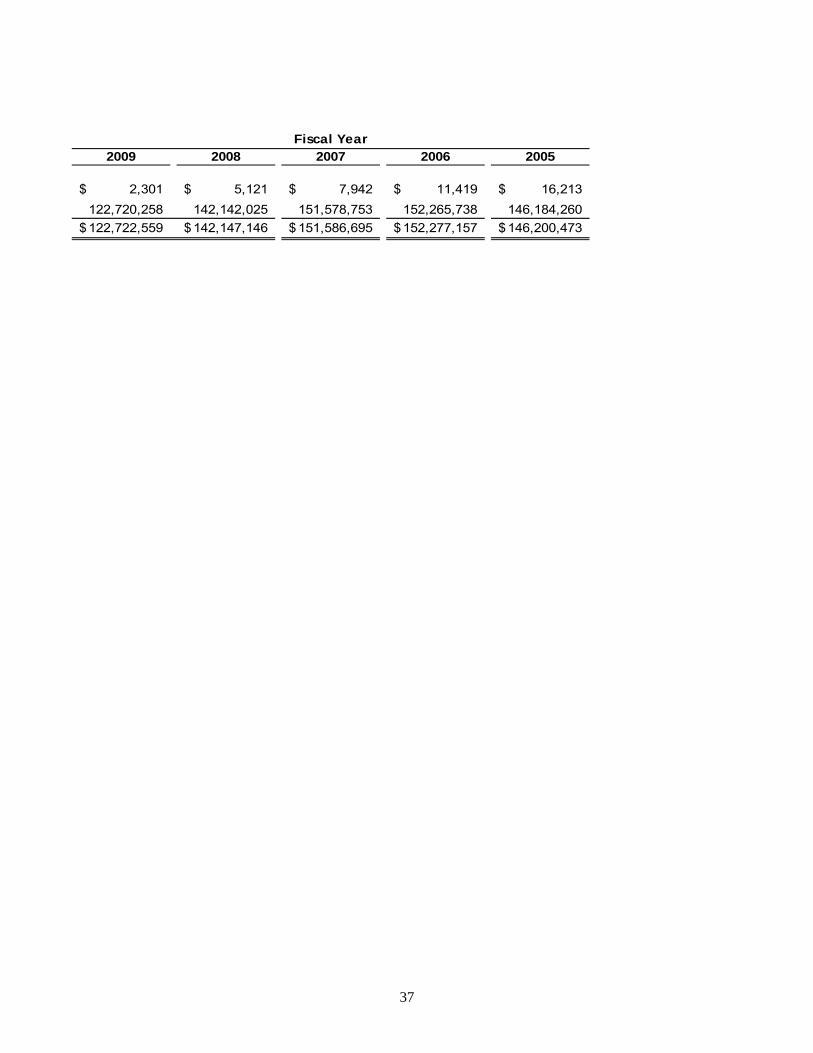

Net Position by Component………………………………………………….………………………… 36

Changes in Net Position..………………………………………………………………………………. 38

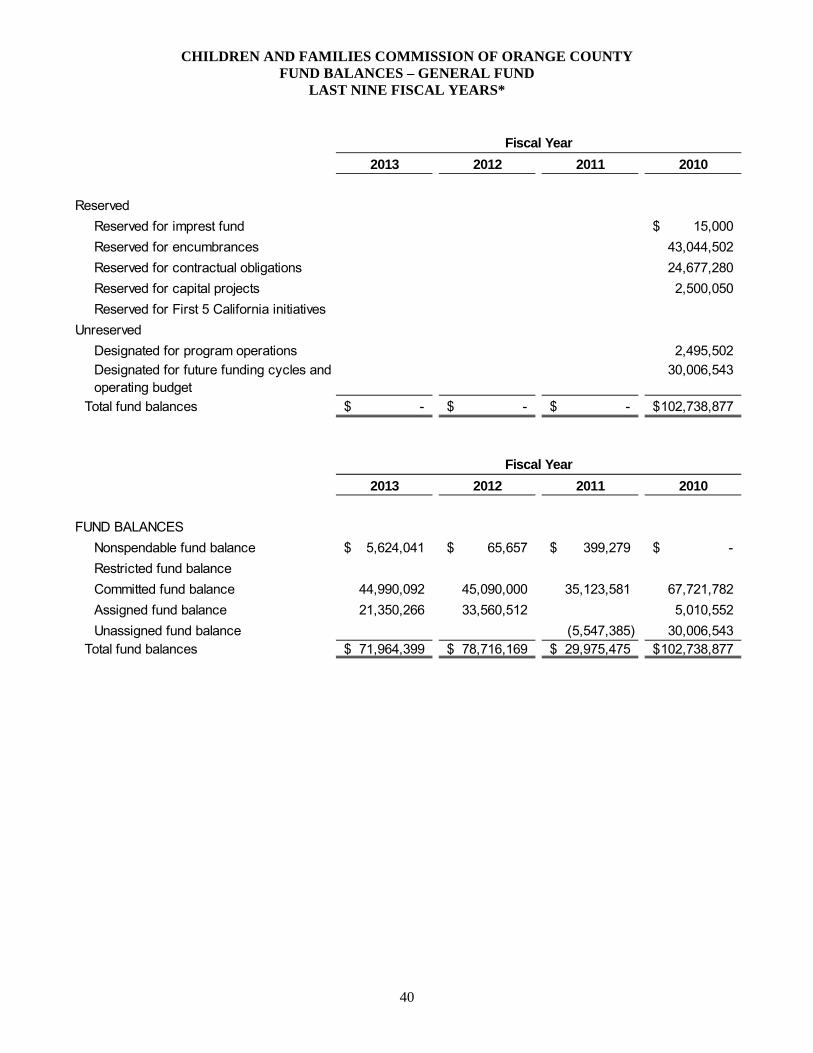

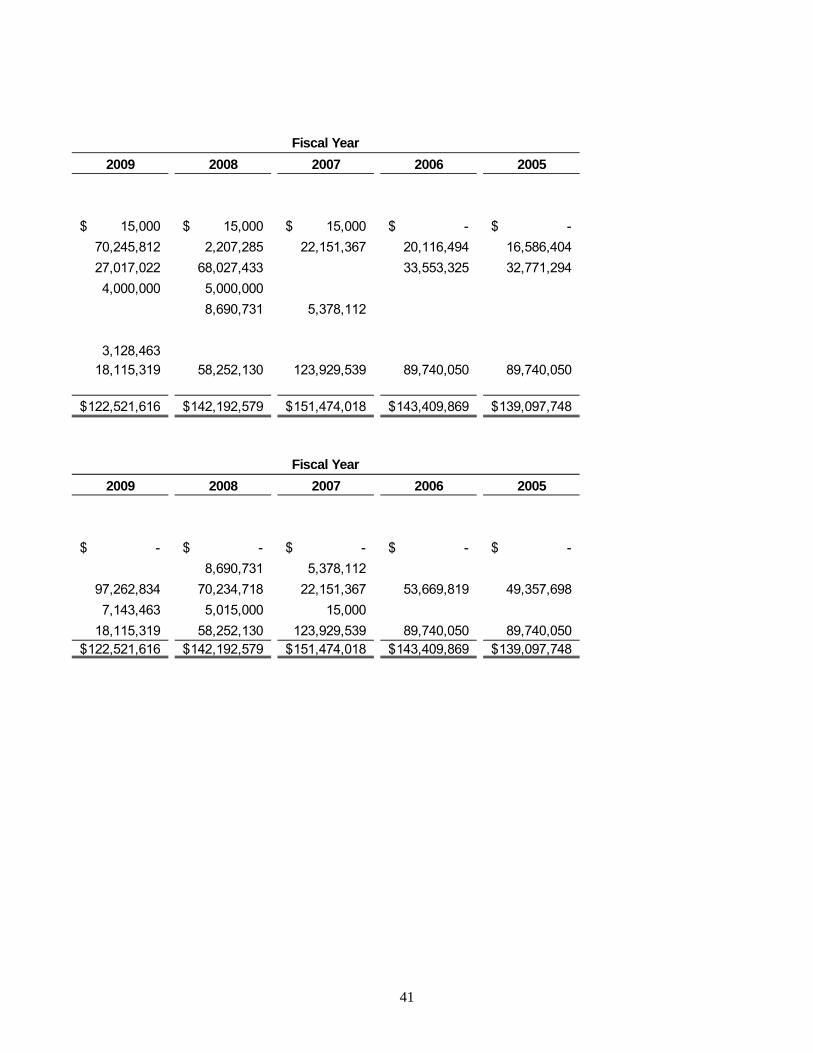

Fund Balances – General Fund………………………………………………………………………… 40

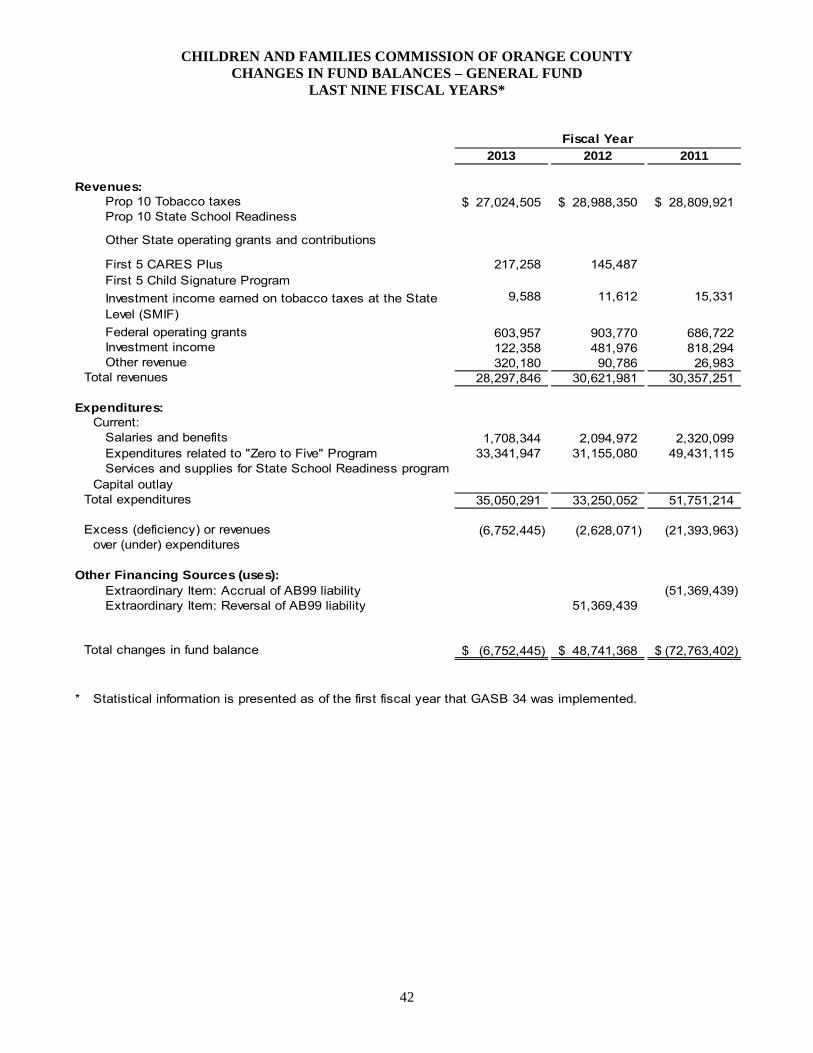

Changes in Fund Balance – General Fund……………………………………………………………... 42

Revenue Capacity

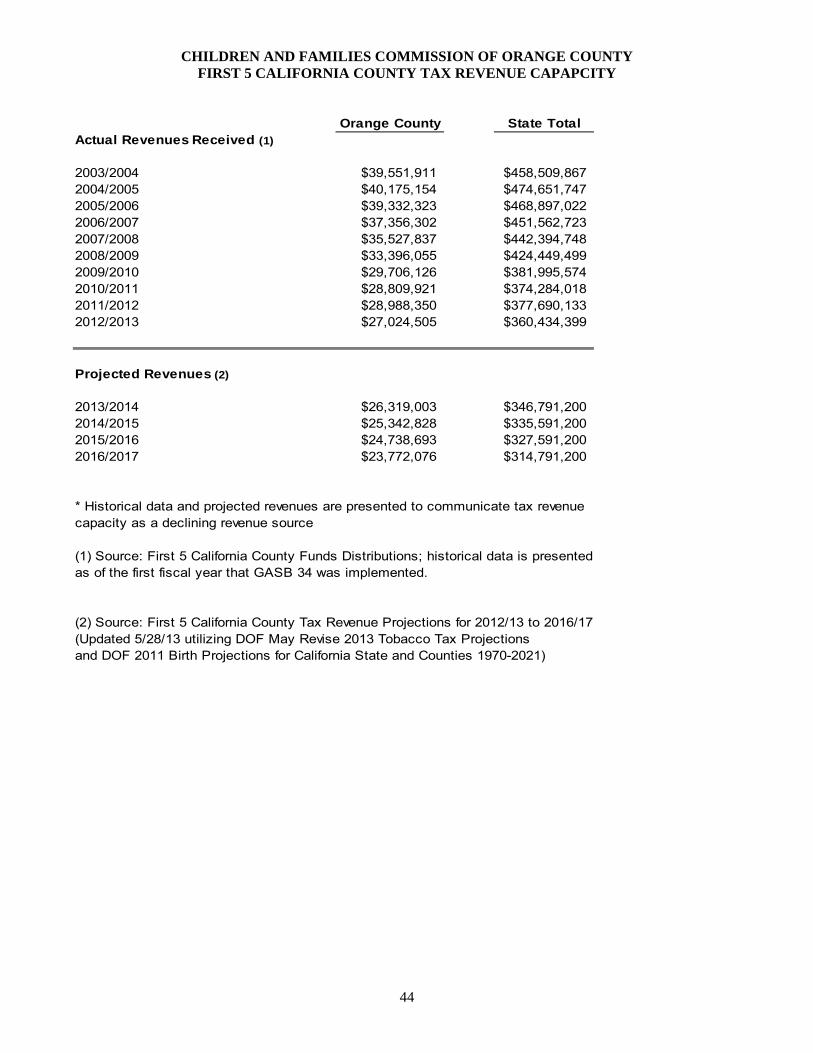

First 5 California County Tax Revenue Capacity……………………………………………………… 44

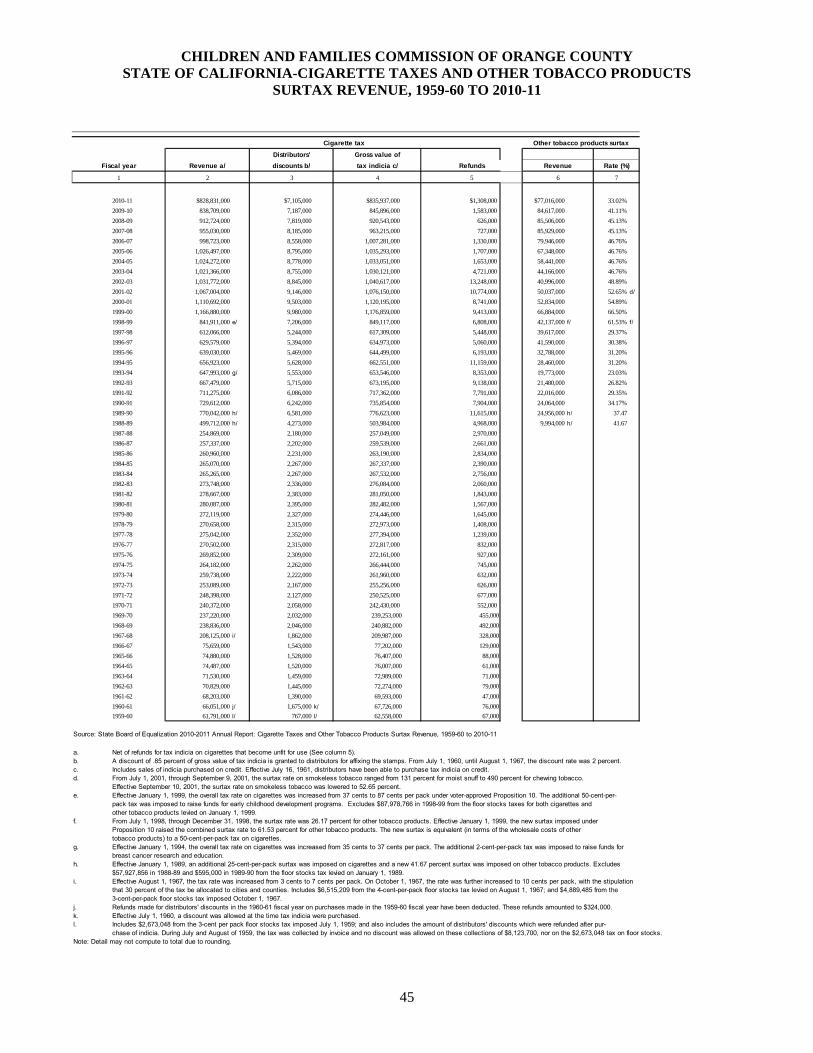

State of California-Cigarette Taxes and Other Tobacco Products Surtax Revenue…………………... 45

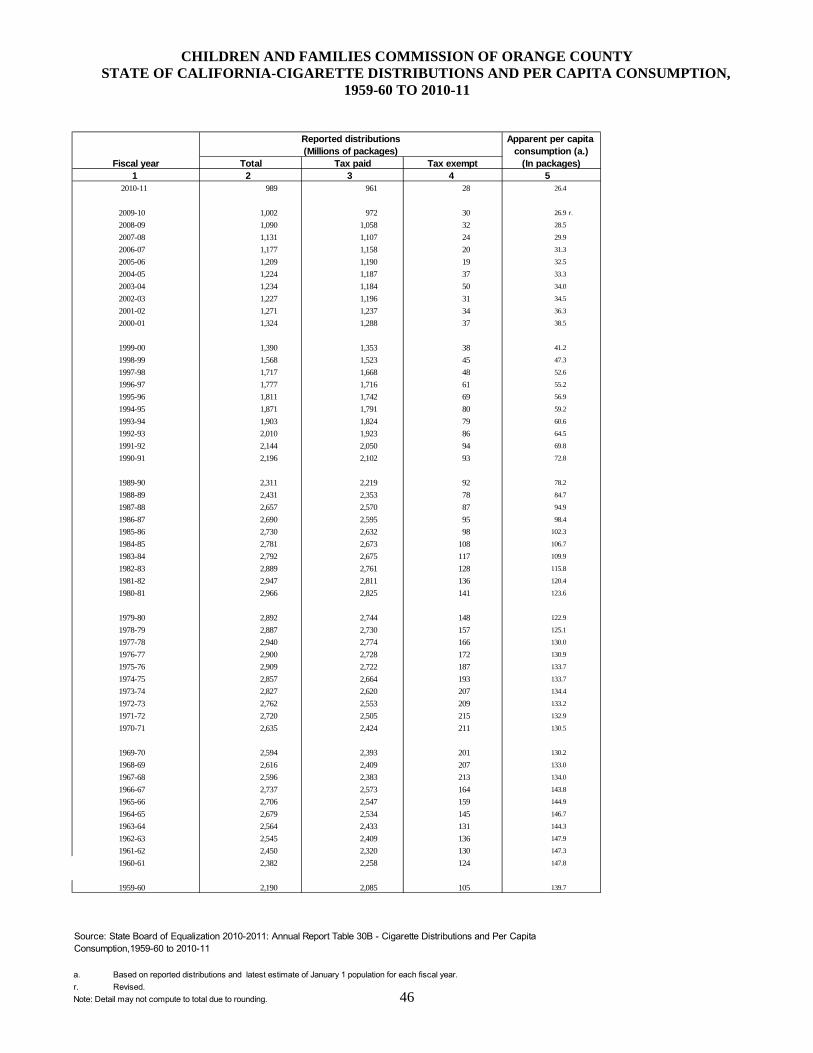

State of California-Cigarette Distributions and Per Capita Consumption……………………………... 46

Demographic Information

Demographic Data……………………………………………………………………………………... 47

Live Births, California Counties……………………………………………………………………….. 48

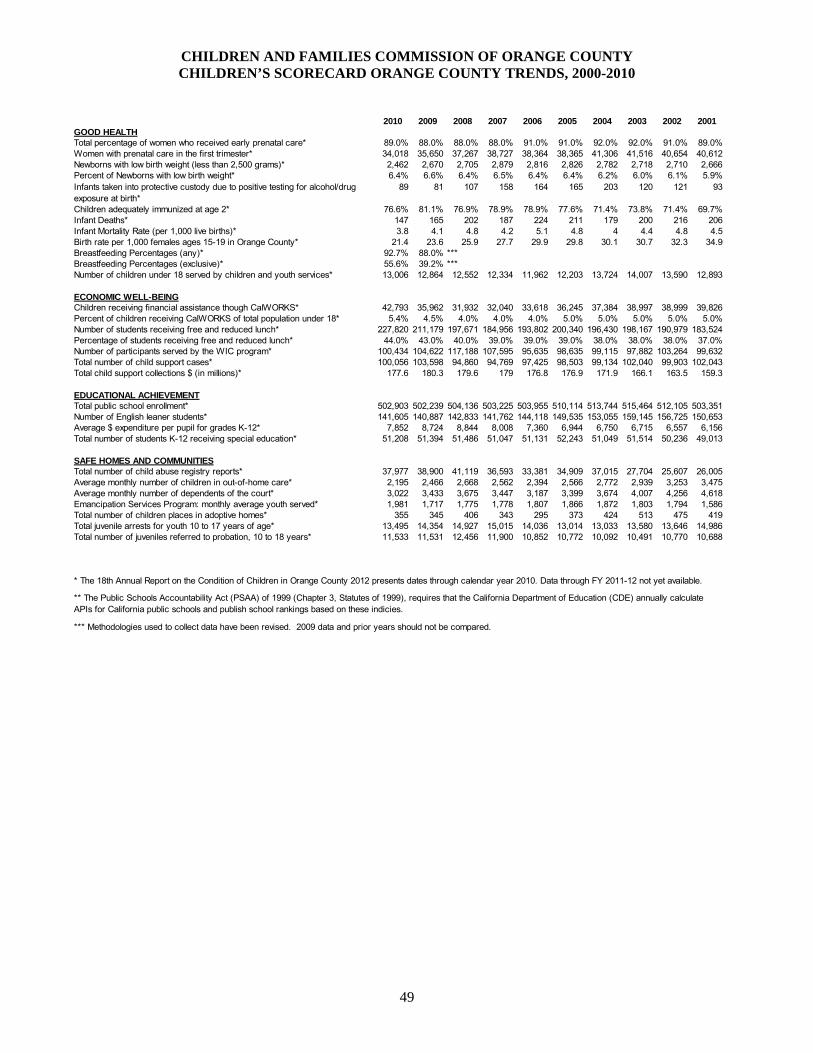

Children’s Score Card Orange County...………………………………………………………………. 49

STATISTICAL SECTION (Continued):

Operating Information

Capital Assets Statistics………………………………………………………………………………... 50

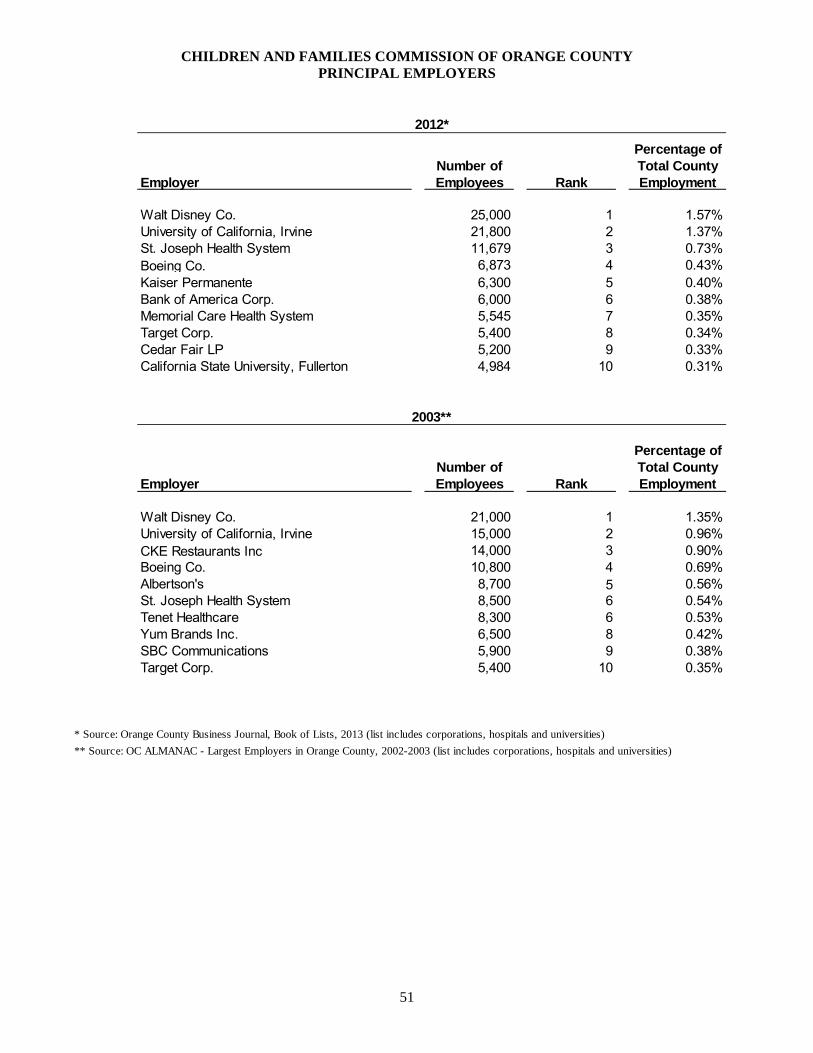

Principal Employers……………………………………………………………………………………. 51

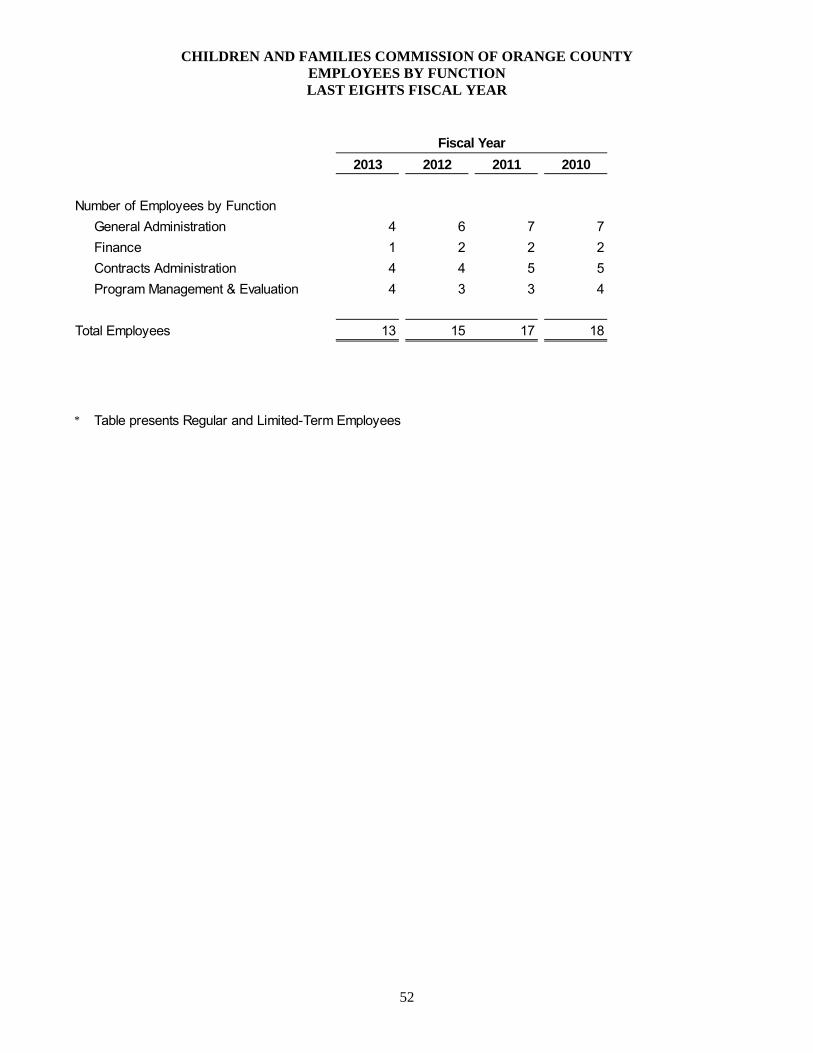

Employees by Function………………………………………………………………………………… 52

COMPLIANCE SECTION:

Independent Auditors’ Report on Internal Control Over Financial Reporting and On Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards………………………………… 54

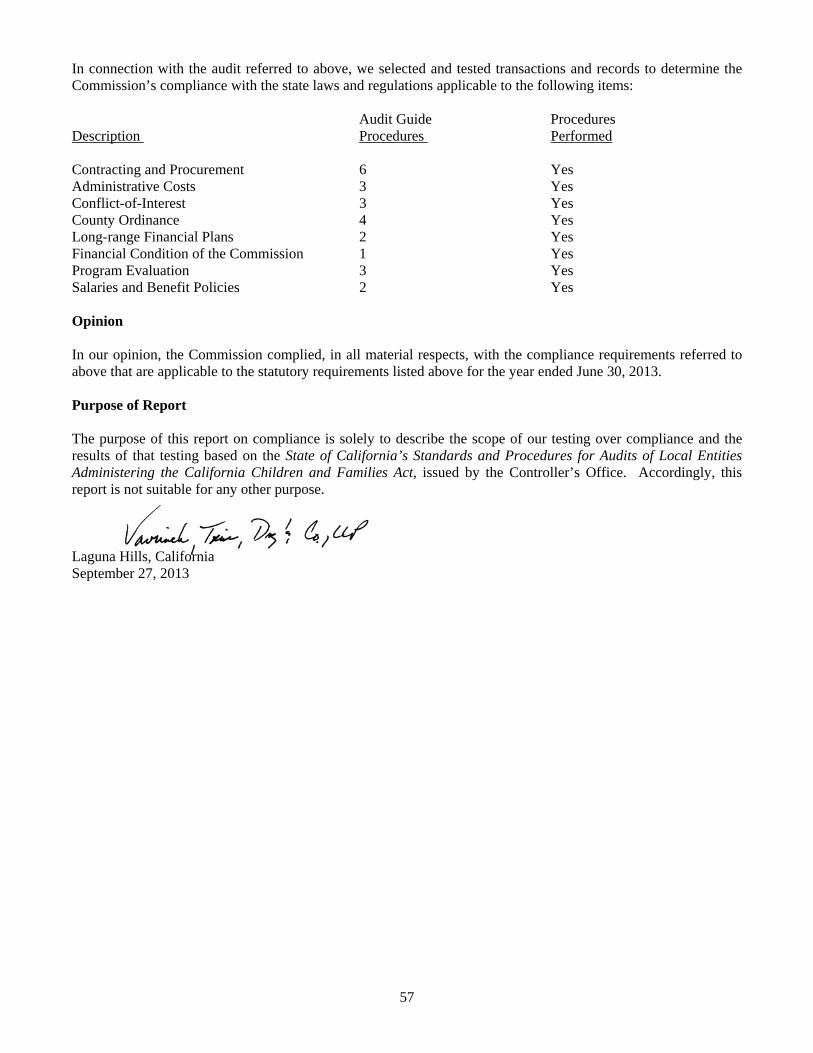

Independent Auditors’ Report on State Compliance…………………………………………………... 56

i

17320 Red Hill Avenue, Suite 200 Irvine, California 92614 714-834-5310 FAX: 949-474-2243

October 2, 2013 Board of Commissioners Children and Families Commission of Orange County 17320 Redhill Avenue Suite 200 Irvine, CA 92614 Dear Commissioners, The Comprehensive Annual Financial Report (CAFR) of the Children and Families Commission of Orange County (the Commission) is hereby submitted. This report contains financial statements that have been prepared in conformity with United States generally accepted accounting principles (GAAP) prescribed for governmental entities. Responsibility for the accuracy of the data and the completeness and fairness of the presentation, including all disclosures, rests with the management of the Commission. To the best of our knowledge and belief, the enclosed data is accurate in all material aspects and is reported in a manner that presents fairly the financial position and changes to the financial position of the Children and Families Commission of Orange County. All disclosures necessary to enable the reader to gain an understanding of the Commission’s financial activities have been included. The CAFR has been audited by the independent certified public accounting firm of Vavrinek, Trine, Day & Co., LLP. The goal of the independent audit was to provide reasonable assurance about whether the basic financial statements of the Commission for the year ended June 30, 2013, are free of material misstatement. The independent certified public accounting firm has issued an unmodified (“clean”) opinion on the Commission’s financial statements as of and for the year ended June 30, 2013. The independent auditors’ report is located at the front of the financial section of this report. This letter of transmittal is designed to complement and should be read in conjunction with the Management’s Discussion and Analysis (MD&A) that immediately follows the independent auditors’ report. The MD&A provides a narrative introduction, overview, and an analysis of the basic financial statements. Profile of the Commission The Commission was established by the Orange County Board of Supervisors in September 1999 following the passage of Proposition 10, through which California voters made an unprecedented investment in early childhood development. Our activities have been built to develop, adopt, promote and implement early childhood development. Since inception, the Commission has made a lasting positive impact in Orange County through its expenditures of approximately $616 million toward grants, programs and operations that improve the well-being of young children and families in Orange County.

ii

Relevant Financial Policies Financial Plan The Long-Term Financial Plan was reviewed and revised in April 2013 to address current economic issues, emerging program needs, and future demand on Commission resources. The revised Long-Term Financial Plan includes one-time catalytic funding investments focused on key Commission priorities. The goal of catalytic funding is to reduce or eliminate future ongoing support for several major programs. First round catalytic investments totaling $45 million were made to support Autism/Early Developmental programs, Children’s Dental, Emergency Shelters, Early Literacy & Math, Healthy Child Development, and VISTA program transition. Round two catalytic funding priorities consist of investments in Partnerships for Children’s Health, Prevention Program Planning, Nutrition and Fitness, Vision Screening and Capacity Building. Staff will continue to monitor and report on the total $55 million catalytic allocation as expenses are realized. The FY 2013-2014 Operating Budget, presented in April 2013, includes the funding actions taken earlier this year to fund catalytic programs and renew funding for core programs that support the four goal areas. The step-down approach continues to be embedded in the approved Long-Term Financial Plan, and assumes a reduction of base budget program spending from $30 million to $27.6 million in FY 2013/14 and $25.1 million in FY 2014/15. The budget plan continues the reduction of program spending gradually, depending on actual revenue, to bring the total budget in line with the forecasted revenue and a reduction in fund balance not already allocated to Catalytic funding. Strategic Plan Although changes in the long-term funding plan were made, the Commission will continue to utilize the Strategic Plan adopted in April 2013 for fiscal year 2013-2014 detailing our continuing commitment to partnering with the Orange County community to improve the lives of expectant parents, children from the prenatal stage through age 5 and their families. This will be the guide by which we will plan, develop, implement and evaluate our activities through 2014. Other Financial Information Internal Control The management of the Commission is responsible for establishing and maintaining internal controls designed to ensure that the assets of the public entity are protected from loss, theft, or misuse. Management is also responsible for ensuring that adequate accounting data are compiled to allow for the preparation of the basic financial statements in conformity with accounting principles generally accepted in the United States of America. Internal controls are designed to provide reasonable, but not absolute, assurance that these objectives are met. The concept of reasonable assurance recognizes that: (1) the cost of a control should not exceed the benefits likely to be derived; and (2) the valuation of costs and benefits requires estimates and judgments by management.

iii

Budgetary Control The objective of budgetary control is to ensure that spending is limited to the total amount authorized by the Board of Commissioners. The initial budget for fiscal year 2012-2013 was adopted on April 4, 2012 with subsequent adjustments approved in November 7, 2012 and April 3, 2013. The Executive Director has the discretion to adjust the budget as defined within the budget policy of the Board of Commissioners. Monthly financial highlights are provided to the Board of Commissioners. Risk Management The Commission manages its risk exposure in part through the purchase of Workers Compensation, Property, General Liability, Auto, Crime and Directors and Officers insurance through the County of Orange. Awards and Acknowledgements The Government Finance Officers Association of the United States and Canada (GFOA) awarded a Certificate of Achievement for Excellence in Financial Reporting to the Commission for its Comprehensive Annual Financial Report (CAFR) for the fiscal year ended June 30, 2012. This was the third consecutive year that the government has achieved this prestigious award. In order to be awarded a Certificate of Achievement, the government must publish an easily readable and efficiently organized CAFR. This report must satisfy both accounting principles generally accepted in the United State of America and applicable legal requirements. A Certificate of Achievement is valid for a period of one year only. We believe that our current CAFR continues to meet the Certificate of Achievement program’s requirements and we are submitting it to the GFOA to determine its eligibility for another certificate. I would like to express my sincere appreciation to Commission staff and the staff of the certified public accounting firm of Vavrinek, Trine, Day & Co., LLP. I hope this report will be of interest and use to those in the County of Orange, other governmental agencies, and the public interested in the financial activity of the Commission. Sincerely,

Christina Altmayer Executive Director

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY

BOARD OF COMMISSIONERS FOR THE FISCAL YEAR ENDED JUNE 30, 2013

iv

BOARD MEMBERS (9)

Michael L. Riley, Ph.D. (M)

Social Services Agency Chair

Kimberly Cripe (A) Vice Chair

Sandra Barry (A) Chair Pro-tem

Katherine Ahn, DDS (A)

Hugh Hewitt (A)

Maria E. Minon, M.D. (A)

Janet Nguyen (M) Board of Supervisors

Mark Refowitz (M) Health Care Agency

Sandra Pierce (A)

(M) Mandatory members (A) At-large members

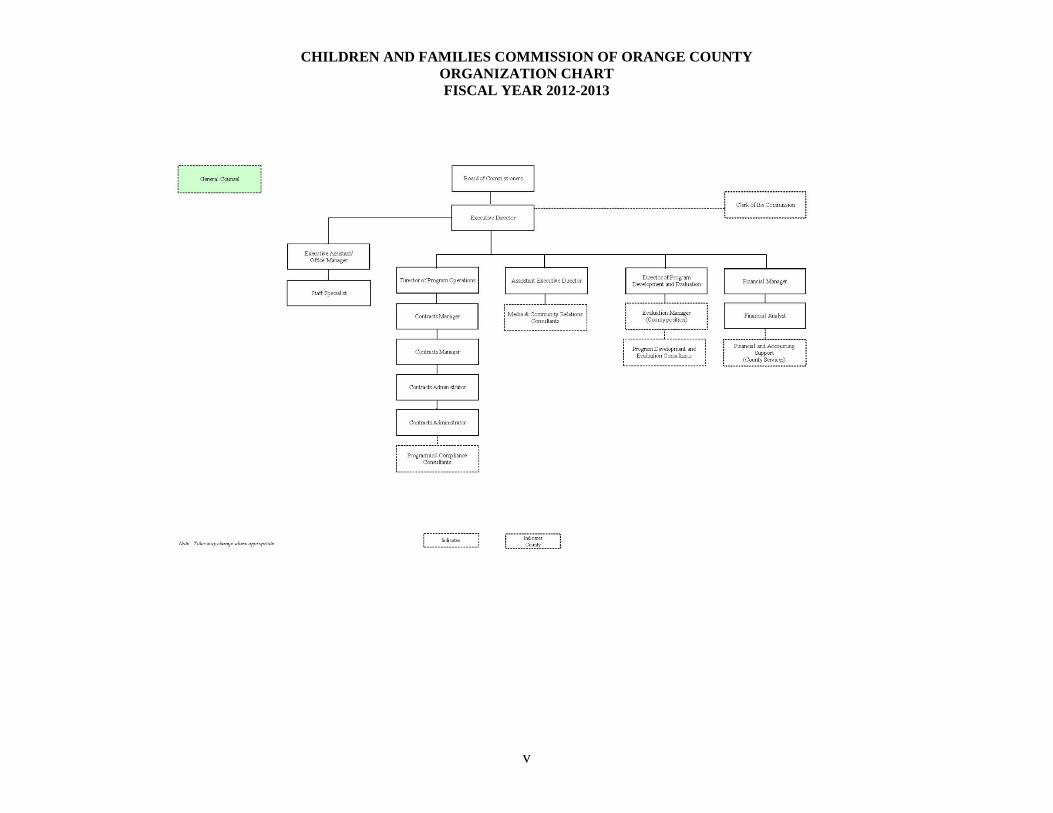

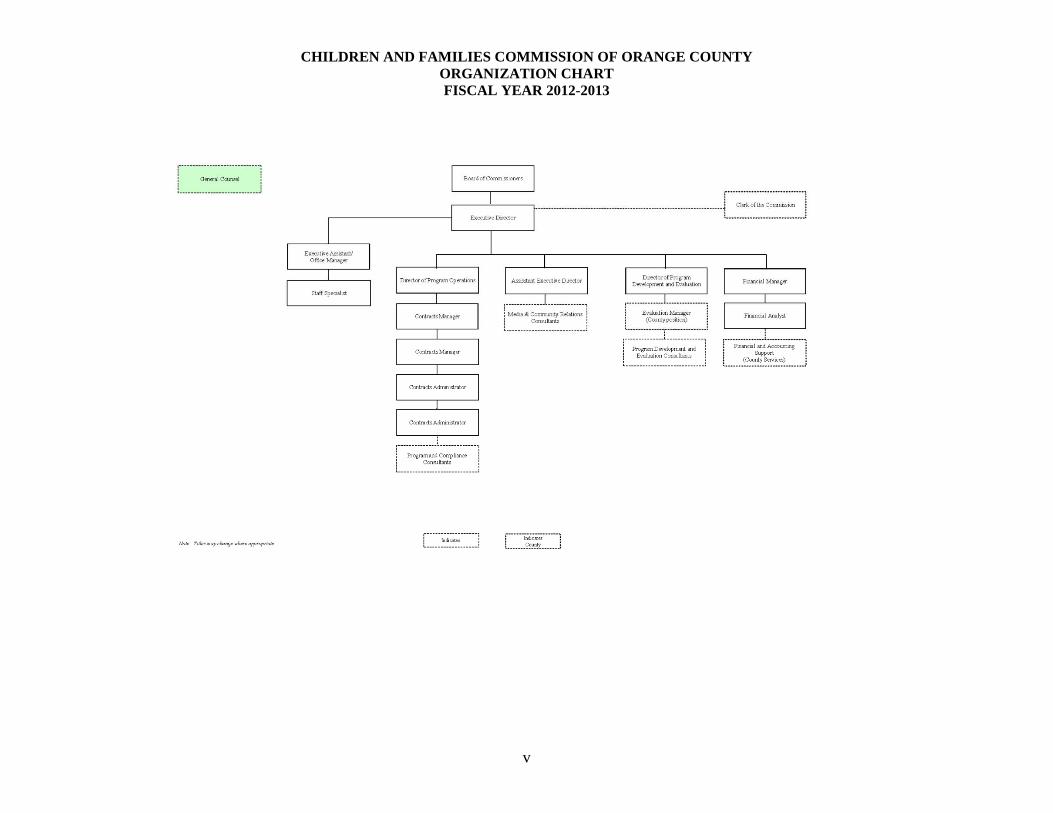

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY ORGANIZATION CHART FISCAL YEAR 2012-2013

v

vi

1

INDEPENDENT AUDITORS’ REPORT

To the Board of Commissioners Children and Families Commission of Orange County Report on the Financial Statements We have audited the accompanying financial statements of the governmental activities and the general fund of the Children and Families Commission of Orange County (Commission), a component unit of the County of Orange, California, as of and for the year ended June 30, 2013, and the related notes to the financial statements, which collectively comprise the Commission’s basic financial statements as listed in the table of contents. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditors’ Responsibility Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions. Opinions In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities and general fund of the Commission as of June 30, 2013, and the respective changes in financial position thereof and the respective budgetary comparison for the General Fund for the year then ended in accordance with accounting principles generally accepted in the United States of America.

Vavrinek, Trine, Day & Co., LLPCertified Public Accountants

VALUE THE D IFFERENCE

FRESN O • L AGUN A H I L LS • PALO ALTO • P LEASANTON • RAN C HO CUC AMON GA • R I v E R S I d E • SACRAMENTO

25231 Paseo De Alicia, Suite 100 Laguna Hills, CA 92653 Tel: 949.768.0833 Fax: 949.768.8408 www.vtdcpa.com

2

Emphasis of Matter As described in Note 1 to the financial statements, the Commission adopted Governmental Accounting Standards Board (GASB) Statement No. 63, Financial Reporting of Deferred Outflows of Resources, Deferred Inflows of Resources, and Net Position, effective July 1, 2012. Our opinion is not modified with respect to this matter. Other Matters Required Supplementary Information Accounting principles generally accepted in the United States of America require that the Management’s Discussion and Analysis on pages 3 through 14 be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. Other Information Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the Commission’s basic financial statements. The Introductory Section, Schedule of First 5 California Funding (Schedule), and Statistical Section are presented for purposes of additional analysis and are not a required part of the basic financial statements. The Schedule is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the Schedule is fairly stated in all material respects in relation to the basic financial statements as a whole. The introductory and statistical sections have not been subjected to the auditing procedures applied in the audit of the basic financial statements and, accordingly, we do not express an opinion or provide any assurance on them. Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated September 27, 2013, on our consideration of the Commission’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the Commission’s internal control over financial reporting and compliance. Laguna Hills, California September 27, 2013

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY MANAGEMENT’S DISCUSSION AND ANALYSIS

(UNAUDITED) JUNE 30, 2013

3

As management of the Children and Families Commission of Orange County (Commission), we offer readers of the Commission’s Comprehensive Annual Financial Report this overview and analysis of the financial activities for the fiscal year ended June 30, 2013. Please read in conjunction with the Commission’s basic financial statements and accompanying notes.

Financial Highlights

The assets of the Commission exceeded its liabilities by $72 million at the end of the current fiscal year, a decrease of $6.57 million (8.3%) from the prior fiscal year. The decrease is due to Round 1 and 2 Catalytic expenditures above the Commission’s annual program budget.

As of June 30, 2013, the Commission’s governmental fund statements reported an ending fund balance totaling $72 million, a decrease of $6.75 million (8.6%) from the prior fiscal year.

The total ending fund balance of $72 million was classified into three categories. The Commission’s breakdown is as follows: $5.62 million as non-spendable, $49.99 million as committed, $21.35 as assigned.

Overview of the Financial Statements

This comprehensive annual financial report consists of two parts, this management’s discussion and analysis and the basic financial statements, including government-wide financial statements, governmental fund financial statements and notes to the basic financial statements. The Commission’s financial statements, prepared in accordance with generally accepted accounting principles (GAAP), offer key, high-level financial information about the activities during the reporting period. Government-Wide Financial Statements. The government-wide financial statements are designed to provide readers with a broad overview of the Commission’s finances and activities. These statements are prepared using the full accrual basis of accounting and a total economic resource measurement focus, in order to provide both long-term and short-term information about the Commission’s overall financial status. A detailed definition of these methods is described in Note 1 of the basic financial statements. The Statement of Net Position presents information on all of the Commission’s assets and liabilities with the difference between assets and liabilities reported as net position. Changes in net position may serve as a useful indicator of whether the financial position of the Commission is improving or declining. The Statement of Activities presents changes in the Commission’s net position during the fiscal year. All changes in net position are reported as soon as the underlying event giving rise to the change occurs, regardless of the timing of related cash flows. Thus, revenues and expenses are reported in this statement for some items that will only result in cash flows in future fiscal periods (e.g., uncollected taxes and earned but unused vacation leave).

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY MANAGEMENT’S DISCUSSION AND ANALYSIS

(UNAUDITED) JUNE 30, 2013

4

Fund Financial Statements. A fund is a grouping of related accounts that is used to maintain control over resources that have been segregated for specific activities or objectives. Fund accounting is used to ensure and demonstrate compliance with finance-related and legal requirements. All of the Commission’s activities are accounted for in the general fund. Governmental funds are used to account for essentially the same functions reported as governmental activities in the government-wide financial statements. However, unlike the government-wide financial statements, governmental fund financial statements focus on near-term inflows and outflows of spendable resources, as well as on balances of spendable resources available at the end of the year. Such information may be useful in evaluating the Commission’s near-term financing requirements. Because the focus of government funds is narrower than that of the government-wide financial statements, it is useful to compare the information presented for governmental funds with similar information presented for governmental activities in the government-wide financial statements. By doing so, readers may better understand the long-term impact of the Commission’s near-term financial decisions. Reconciliations are presented for the Balance Sheet of governmental funds and the Statement of Revenues, Expenditures and Changes in Fund Balances of governmental funds to facilitate comparison between governmental funds and governmental activities. Governmental Fund Financial Statements are prepared on a modified accrual basis, which means that they measure only current financial resources and uses. Capital assets and long-term liabilities are not presented in the Governmental Fund Financial Statements, as they do not represent current available resources or obligations. The Commission adopts an annual appropriated budget for the general fund. A budgetary comparison statement for the general fund is presented in the basic financial statements to demonstrate compliance with the adopted budget. Notes to the Financial Statements. The notes provide additional information that is essential to a full understanding of the data provided in the government-wide and fund financial statements. The notes to the financial statements can be found immediately following the basic financial statements.

Analysis of the Commission’s Government-wide Financial Statements

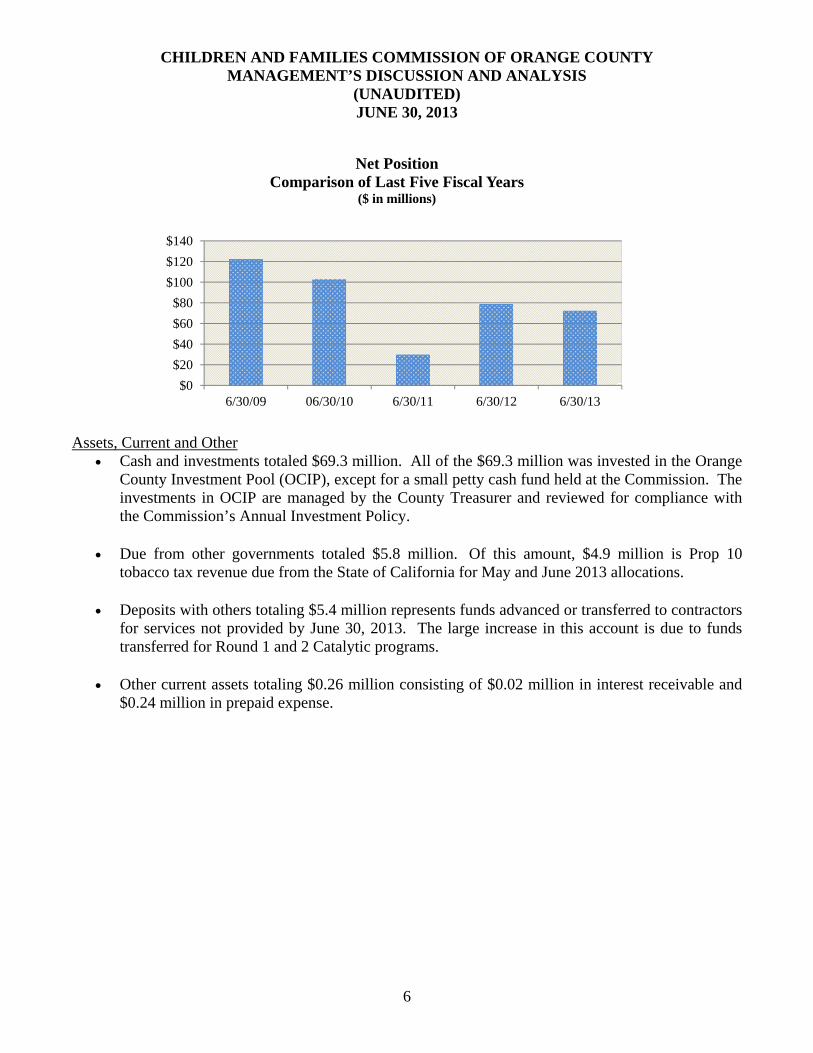

Net Position. Net position may serve over time as a useful indicator of a government’s financial position. In the case of the Commission, net position was $72.41 million at the end of the current fiscal year, an 8% decrease from the prior fiscal year. Following is a summary of the government-wide Statement of Net Position comparing balances at June 30, 2013 and June 30, 2012.

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY MANAGEMENT’S DISCUSSION AND ANALYSIS

(UNAUDITED) JUNE 30, 2013

5

The Commission’s net position as of June 30, 2013 is considered unrestricted because their use is not for a purpose narrower than the purpose of the Commission and were comprised of the following:

Percent Increase FY 2012-13 FY 2011-12 (Decrease)

Assets: Cash and investments $69,280,830 $83,017,827 -17% Imprest cash 15,000 15,000 -

Interest receivable 19,931 71,795 -72% Deposit with others 5,380,606 93,625 +5,647% Due from County of Orange 881 3,738 -76% Due from other governments 5,836,164 6,151,327 -5% Prepaid expense 243,435 65,657 +271% Total assets $80,776,847 $89,419,968 -10%

Liabilities: Accounts payable and accrued liabilities $2,847,704 $3,862,837 -26% Due to County of Orange 9,593 77,574 -88% Due to other governments 3,673,252 3,898,071 -6% Retentions payable 1,634,093 2,384,936 -31% Accrued wages and benefits 70,254 76,718 -8% Compensated absences: Payable within one year 77,336 87,838 -12% Payable after one year 53,482 46,509 15% Total liabilities 8,365,714 10,434,483 -20% Net Position: Unrestricted 72,411,134 78,985,485 -8% Total net position $72,411,134 $78,985,485

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY MANAGEMENT’S DISCUSSION AND ANALYSIS

(UNAUDITED) JUNE 30, 2013

6

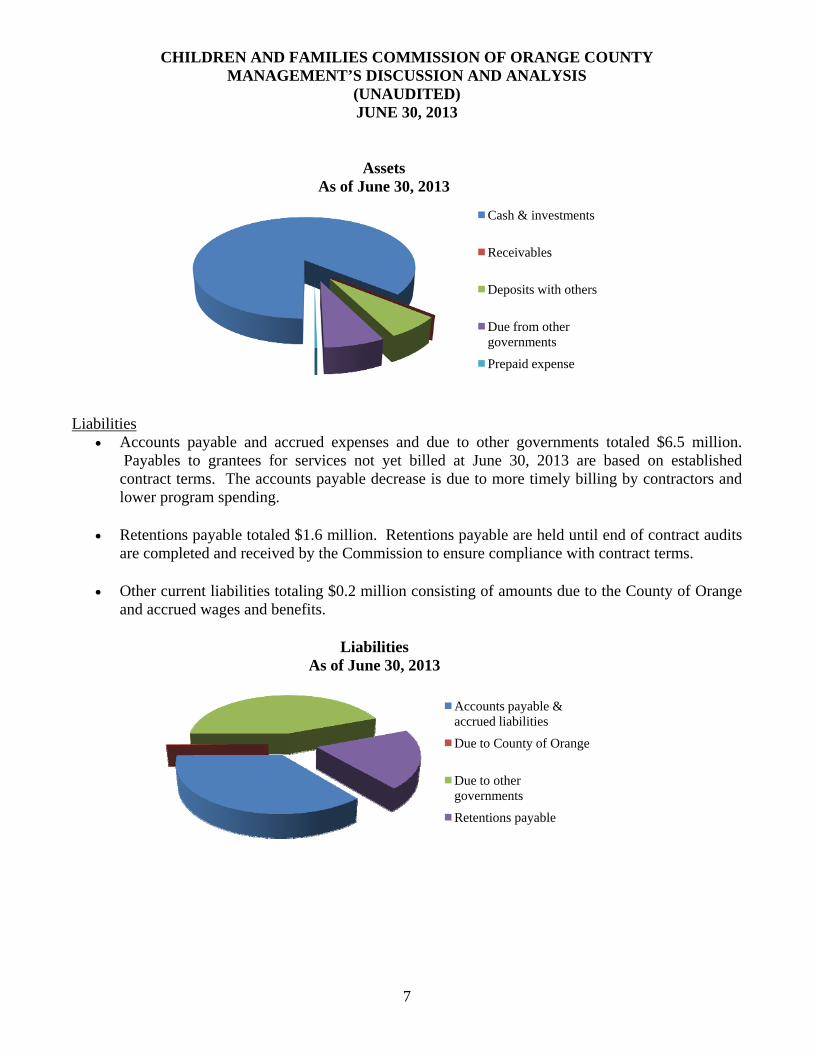

Assets, Current and Other

Cash and investments totaled $69.3 million. All of the $69.3 million was invested in the Orange County Investment Pool (OCIP), except for a small petty cash fund held at the Commission. The investments in OCIP are managed by the County Treasurer and reviewed for compliance with the Commission’s Annual Investment Policy.

Due from other governments totaled $5.8 million. Of this amount, $4.9 million is Prop 10 tobacco tax revenue due from the State of California for May and June 2013 allocations.

Deposits with others totaling $5.4 million represents funds advanced or transferred to contractors for services not provided by June 30, 2013. The large increase in this account is due to funds transferred for Round 1 and 2 Catalytic programs.

Other current assets totaling $0.26 million consisting of $0.02 million in interest receivable and $0.24 million in prepaid expense.

$0

$20

$40

$60

$80

$100

$120

$140

6/30/09 06/30/10 6/30/11 6/30/12 6/30/13

Net PositionComparison of Last Five Fiscal Years

($ in millions)

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY MANAGEMENT’S DISCUSSION AND ANALYSIS

(UNAUDITED) JUNE 30, 2013

7

Liabilities Accounts payable and accrued expenses and due to other governments totaled $6.5 million.

Payables to grantees for services not yet billed at June 30, 2013 are based on established contract terms. The accounts payable decrease is due to more timely billing by contractors and lower program spending.

Retentions payable totaled $1.6 million. Retentions payable are held until end of contract audits are completed and received by the Commission to ensure compliance with contract terms.

Other current liabilities totaling $0.2 million consisting of amounts due to the County of Orange and accrued wages and benefits.

AssetsAs of June 30, 2013

Cash & investments

Receivables

Deposits with others

Due from other governments

Prepaid expense

LiabilitiesAs of June 30, 2013

Accounts payable & accrued liabilities

Due to County of Orange

Due to other governments

Retentions payable

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY MANAGEMENT’S DISCUSSION AND ANALYSIS

(UNAUDITED) JUNE 30, 2013

8

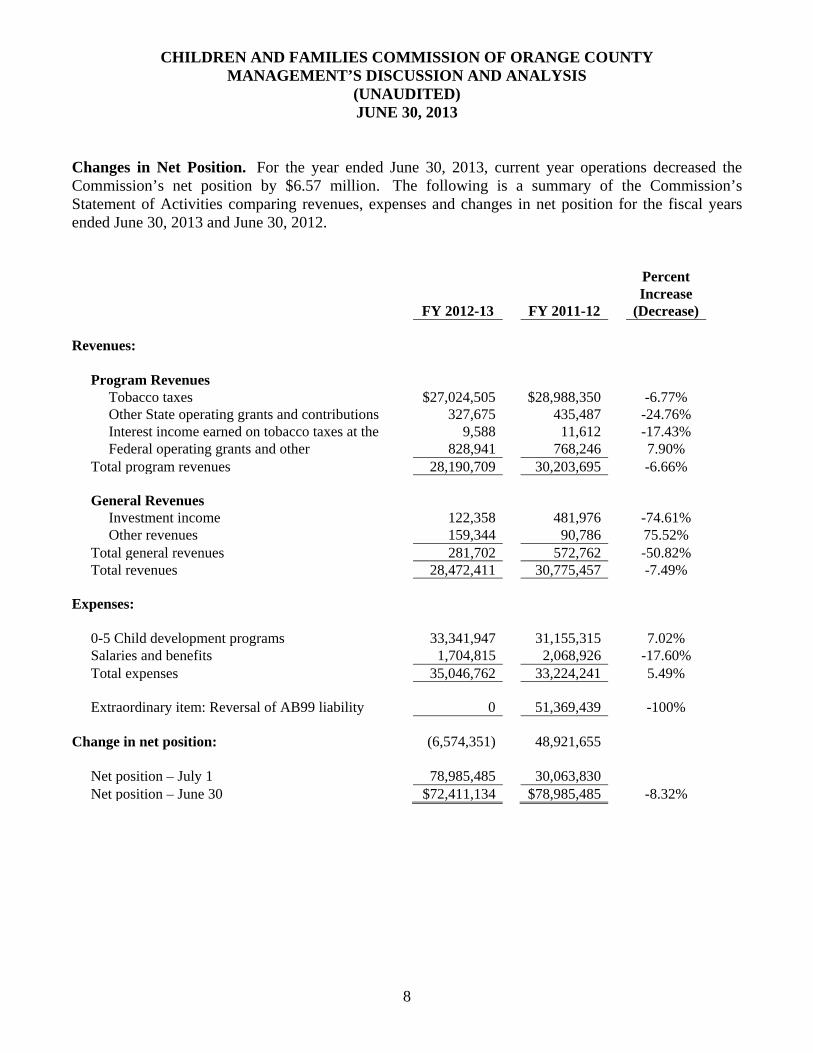

Changes in Net Position. For the year ended June 30, 2013, current year operations decreased the Commission’s net position by $6.57 million. The following is a summary of the Commission’s Statement of Activities comparing revenues, expenses and changes in net position for the fiscal years ended June 30, 2013 and June 30, 2012. Percent Increase FY 2012-13 FY 2011-12 (Decrease) Revenues: Program Revenues Tobacco taxes $27,024,505 $28,988,350 -6.77% Other State operating grants and contributions 327,675 435,487 -24.76% Interest income earned on tobacco taxes at the 9,588 11,612 -17.43% Federal operating grants and other 828,941 768,246 7.90% Total program revenues 28,190,709 30,203,695 -6.66% General Revenues Investment income 122,358 481,976 -74.61% Other revenues 159,344 90,786 75.52% Total general revenues 281,702 572,762 -50.82% Total revenues 28,472,411 30,775,457 -7.49% Expenses: 0-5 Child development programs 33,341,947 31,155,315 7.02% Salaries and benefits 1,704,815 2,068,926 -17.60% Total expenses 35,046,762 33,224,241 5.49% Extraordinary item: Reversal of AB99 liability 0 51,369,439 -100% Change in net position: (6,574,351) 48,921,655 Net position – July 1 78,985,485 30,063,830 Net position – June 30 $72,411,134 $78,985,485 -8.32%

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY MANAGEMENT’S DISCUSSION AND ANALYSIS

(UNAUDITED) JUNE 30, 2013

9

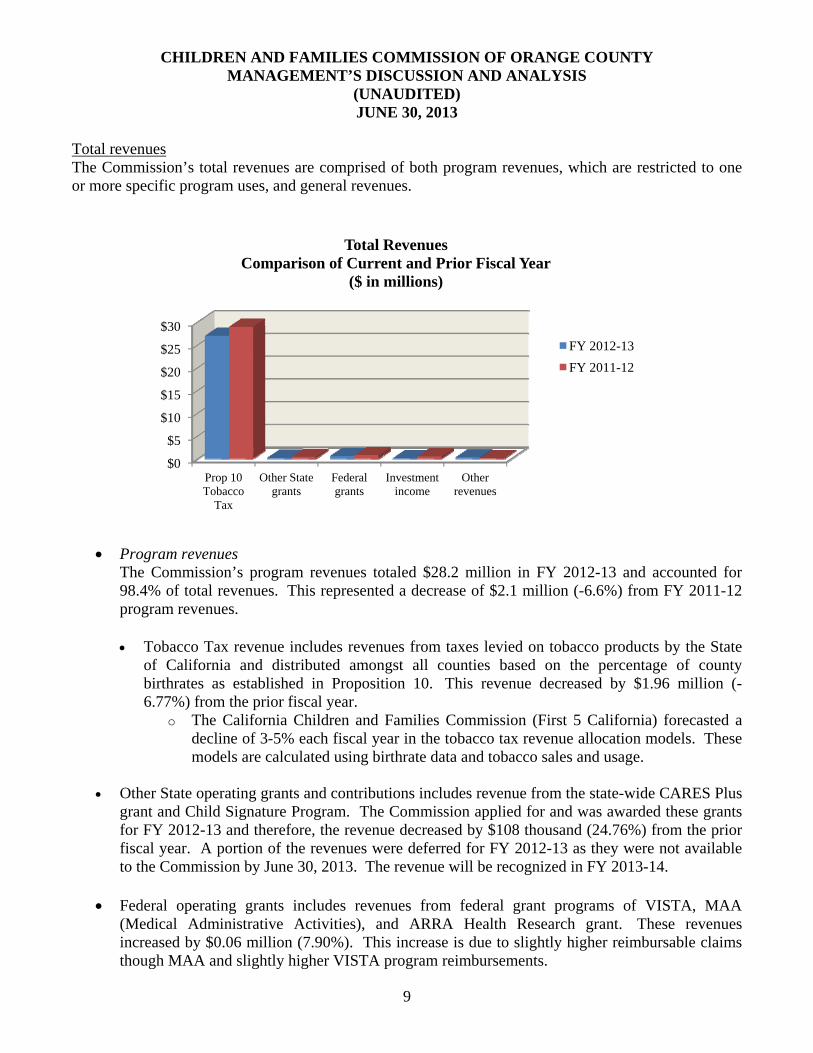

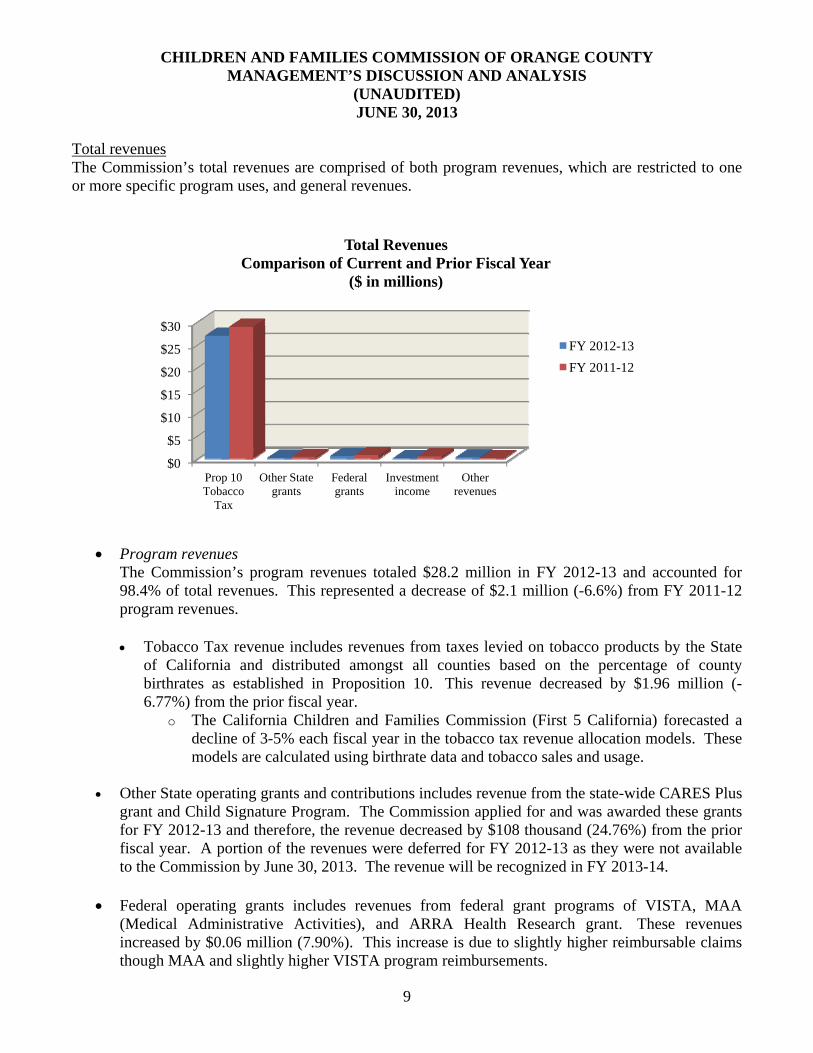

Total revenues The Commission’s total revenues are comprised of both program revenues, which are restricted to one or more specific program uses, and general revenues.

Program revenues

The Commission’s program revenues totaled $28.2 million in FY 2012-13 and accounted for 98.4% of total revenues. This represented a decrease of $2.1 million (-6.6%) from FY 2011-12 program revenues. Tobacco Tax revenue includes revenues from taxes levied on tobacco products by the State

of California and distributed amongst all counties based on the percentage of county birthrates as established in Proposition 10. This revenue decreased by $1.96 million (-6.77%) from the prior fiscal year.

o The California Children and Families Commission (First 5 California) forecasted a decline of 3-5% each fiscal year in the tobacco tax revenue allocation models. These models are calculated using birthrate data and tobacco sales and usage.

Other State operating grants and contributions includes revenue from the state-wide CARES Plus

grant and Child Signature Program. The Commission applied for and was awarded these grants for FY 2012-13 and therefore, the revenue decreased by $108 thousand (24.76%) from the prior fiscal year. A portion of the revenues were deferred for FY 2012-13 as they were not available to the Commission by June 30, 2013. The revenue will be recognized in FY 2013-14.

Federal operating grants includes revenues from federal grant programs of VISTA, MAA

(Medical Administrative Activities), and ARRA Health Research grant. These revenues increased by $0.06 million (7.90%). This increase is due to slightly higher reimbursable claims though MAA and slightly higher VISTA program reimbursements.

$0

$5

$10

$15

$20

$25

$30

Prop 10 Tobacco

Tax

Other State grants

Federal grants

Investment income

Other revenues

Total RevenuesComparison of Current and Prior Fiscal Year

($ in millions)

FY 2012-13

FY 2011-12

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY MANAGEMENT’S DISCUSSION AND ANALYSIS

(UNAUDITED) JUNE 30, 2013

10

General revenues The Commission’s general revenues totaled $282 thousand in FY 2012-13 and accounted for 1% of total revenues. General revenues include all revenues that do not qualify as program revenues, such as investment income and other miscellaneous revenues.

Investment income, decreased by $0.36 million (75%) from the prior fiscal year. The

decrease in investment income from the Orange County Investment Pool (OCIP), which is administered by the County Treasurer, is due to the overall lower returns in the fixed income markets combined with less available investable cash balances as well as a negative fair value adjustment posted for the Commission’s proportionate share in the county investment pool at year end.

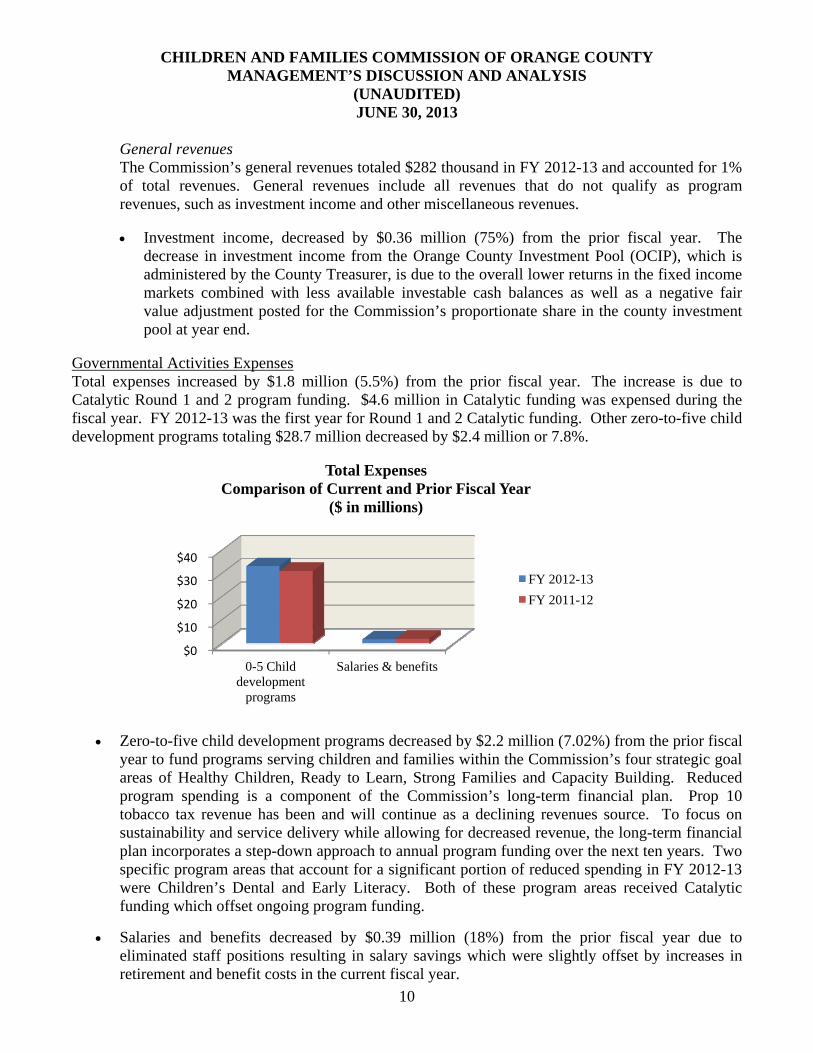

Governmental Activities Expenses Total expenses increased by $1.8 million (5.5%) from the prior fiscal year. The increase is due to Catalytic Round 1 and 2 program funding. $4.6 million in Catalytic funding was expensed during the fiscal year. FY 2012-13 was the first year for Round 1 and 2 Catalytic funding. Other zero-to-five child development programs totaling $28.7 million decreased by $2.4 million or 7.8%.

Zero-to-five child development programs decreased by $2.2 million (7.02%) from the prior fiscal year to fund programs serving children and families within the Commission’s four strategic goal areas of Healthy Children, Ready to Learn, Strong Families and Capacity Building. Reduced program spending is a component of the Commission’s long-term financial plan. Prop 10 tobacco tax revenue has been and will continue as a declining revenues source. To focus on sustainability and service delivery while allowing for decreased revenue, the long-term financial plan incorporates a step-down approach to annual program funding over the next ten years. Two specific program areas that account for a significant portion of reduced spending in FY 2012-13 were Children’s Dental and Early Literacy. Both of these program areas received Catalytic funding which offset ongoing program funding.

Salaries and benefits decreased by $0.39 million (18%) from the prior fiscal year due to eliminated staff positions resulting in salary savings which were slightly offset by increases in retirement and benefit costs in the current fiscal year.

$0

$10

$20

$30

$40

0-5 Child development

programs

Salaries & benefits

Total ExpensesComparison of Current and Prior Fiscal Year

($ in millions)

FY 2012-13

FY 2011-12

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY MANAGEMENT’S DISCUSSION AND ANALYSIS

(UNAUDITED) JUNE 30, 2013

11

Analysis of the Commission’s Governmental Fund Statements As noted earlier, the Commission uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. Governmental Funds. The child development functions are contained in the general fund of the Commission. The focus of the Commission’s governmental funds is to provide information on near-term inflows, outflows and balances of spendable resources. Such information is useful in assessing the Commission’s financing requirements. In particular, fund balance may serve as a useful measure of a government’s net resources, both committed and available for future operational needs. As of the end of the current fiscal year, the Commission’s general fund reported total ending fund balance of $71.9 million, a decrease of $6.8 million (8.6%) in comparison with the prior fiscal year. Total fund balance decreased due to the initial distributions of Catalytic funding in the amount of $4.6 million. The remaining decrease of $2.2 million was fund balance used to bridge the gap between current year revenue and expenditures as planned for in the Commission’s financial plan.

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

Fund Balance ClassificationsAs of June 30, 2013

($ in millions)

Nonspendable

Committed

Assigned

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY MANAGEMENT’S DISCUSSION AND ANALYSIS

(UNAUDITED) JUNE 30, 2013

12

General Fund Budgetary Highlights Budget Amendments. The budget amendments are approved annually during the fiscal year for the General Fund in order to reflect the most current revenue trends and to account for shifts in funding objectives.

Total budgeted revenues were increased by $1.85 million in the Prop 10 tobacco tax revenue line item. The increase was based on a higher projection of tobacco tax distributions by the California Department of Finance and the establishment of budgeted revenues for CARES Plus, VISTA and ARRA Health Research grants.

o Tobacco tax revenues – increase of $1.2 million based on prior-year receipts. FY 2011-

12 revenue actually increased from the prior-year. Budgeted tobacco tax revenues were adjusted to reflect a 3.5% decline from the higher FY 2011-12 tobacco tax revenue receipts.

o Other program revenues – increase of $.65 million was due to First 5 California, federal grant revenues, and partner reimbursements to be received through program grants.

Total budgeted appropriations were increased by $1.8 million in the 0-5 child development

program expenditures line item. The major components of the increase are summarized as follows:

o Healthy Children – increase of $1.37 million mostly for the carryover of prior year

unspent funds in Community Clinics and Pediatric Health Services programs.

o Strong Families – increase of $0.3 million for the carryover over of prior year unspent funds in Homeless Prevention programs.

o Early Learning - decrease of $0.4 million of funding set-aside in Early Literacy programs.

o Capacity Building – increase of $0.54 million comprised of $0.13 million of carryover of

prior year unspent funds in Capacity Building Grants and $0.41 million in new appropriations to VISTA for reimbursable expense though the federal grant award.

Budget to Actual Comparisons. This section contains an explanation of the significant differences between the Commission’s Final Budget amounts and actual amounts recorded for revenues and expenditures for FY 2012-13 as detailed on the Statement of Revenues, Expenditures and Changes in Fund Balance – Budget and Actual.

Total actual revenues were less than budgeted revenues in FY 2012-13 by $1.27 million. A decrease in actual Prop 10 tobacco tax revenues of 6.77% from the prior year was most of the variance.

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY MANAGEMENT’S DISCUSSION AND ANALYSIS

(UNAUDITED) JUNE 30, 2013

13

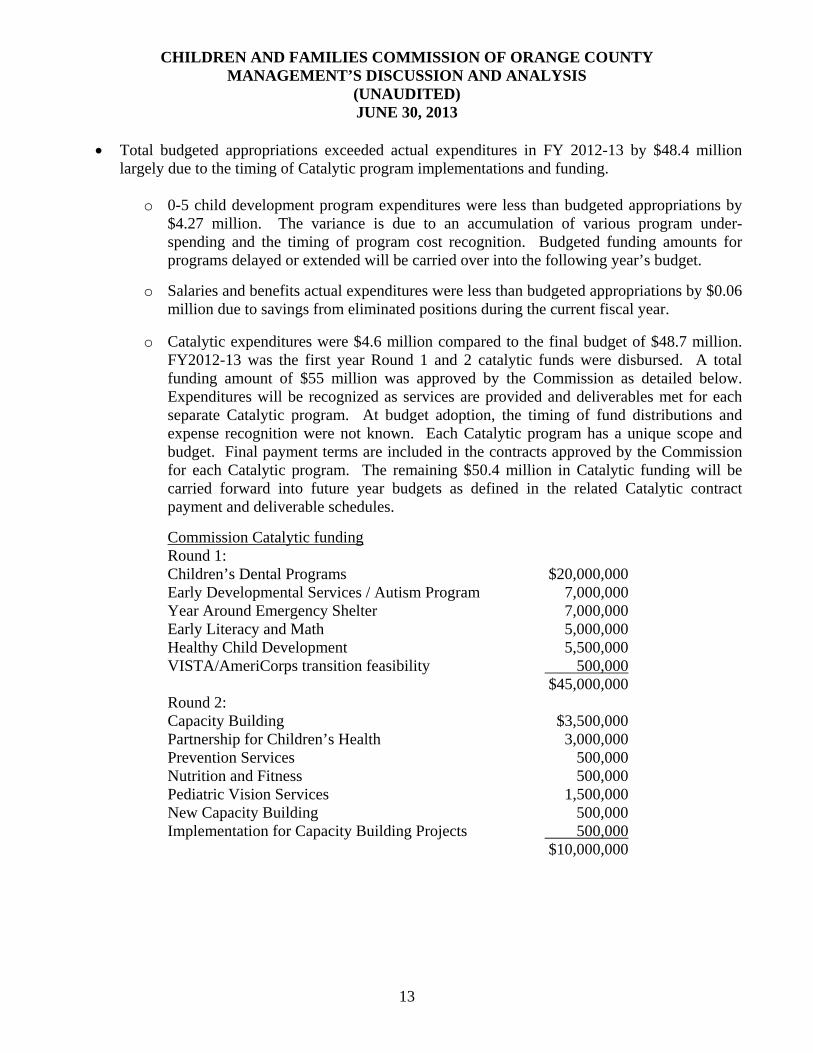

Total budgeted appropriations exceeded actual expenditures in FY 2012-13 by $48.4 million largely due to the timing of Catalytic program implementations and funding.

o 0-5 child development program expenditures were less than budgeted appropriations by $4.27 million. The variance is due to an accumulation of various program under-spending and the timing of program cost recognition. Budgeted funding amounts for programs delayed or extended will be carried over into the following year’s budget.

o Salaries and benefits actual expenditures were less than budgeted appropriations by $0.06 million due to savings from eliminated positions during the current fiscal year.

o Catalytic expenditures were $4.6 million compared to the final budget of $48.7 million. FY2012-13 was the first year Round 1 and 2 catalytic funds were disbursed. A total funding amount of $55 million was approved by the Commission as detailed below. Expenditures will be recognized as services are provided and deliverables met for each separate Catalytic program. At budget adoption, the timing of fund distributions and expense recognition were not known. Each Catalytic program has a unique scope and budget. Final payment terms are included in the contracts approved by the Commission for each Catalytic program. The remaining $50.4 million in Catalytic funding will be carried forward into future year budgets as defined in the related Catalytic contract payment and deliverable schedules.

Commission Catalytic funding Round 1: Children’s Dental Programs $20,000,000 Early Developmental Services / Autism Program 7,000,000 Year Around Emergency Shelter 7,000,000 Early Literacy and Math 5,000,000 Healthy Child Development 5,500,000 VISTA/AmeriCorps transition feasibility 500,000 $45,000,000 Round 2: Capacity Building $3,500,000 Partnership for Children’s Health 3,000,000 Prevention Services 500,000 Nutrition and Fitness 500,000 Pediatric Vision Services 1,500,000 New Capacity Building 500,000 Implementation for Capacity Building Projects 500,000 $10,000,000

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY MANAGEMENT’S DISCUSSION AND ANALYSIS

(UNAUDITED) JUNE 30, 2013

14

Related Events The State projects a continuing decrease of State Tax Allocations revenue and a decrease in the share allocated to the Children and Families Commission of Orange County due to a proportionally lower birth rate combining for a projected annual revenue decrease estimated at 3.5% per year. The Commission’s financial plan will continue planned reductions in annual program funding to account for declining revenues. While the financial plan does assume portions of fund balance will be used in future years to bridge some of the gap between needed services and projected revenue, the Commission still maintains a minimum fund balance of 25% of the annual operating budget.

Requests for Financial Information This comprehensive annual financial report is intended to provide the public with an overview of the Commission’s financial operations and condition for the fiscal year ended June 30, 2013. Questions concerning any of the information provided in this report or requests for additional financial information should be addressed to the Executive Director, Children & Families Commission of Orange County, 17320 Red Hill Avenue, Suite 200, Irvine, California 92614.

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY STATEMENT OF NET POSITION

JUNE 30, 2013

See accompanying notes to the basic financial statements.

15

ASSETSCash and investments in County Treasury 69,280,830$ Imprest cash 15,000 Interest receivable 19,931 Deposits with others 5,380,606 Due from County of Orange 881 Due from other governments 5,836,164 Prepaid expense 243,435

TOTAL ASSETS 80,776,847

LIABILITIES

Accounts payable and accrued liabilities 2,847,704 Due to County of Orange 9,593 Due to other governments 3,673,252 Retentions payable 1,634,093 Accrued wages and benefits 70,254 Compensated absences:

Payable within one year 77,336 Payable after one year 53,482

TOTAL LIABILITIES 8,365,714

NET POSITIONUnrestricted 72,411,134

TOTAL NET POSITION 72,411,134$

GOVERNMENTALACTIVITIES

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY STATEMENT OF ACTIVITIES

FOR THE YEAR ENDED JUNE 30, 2013

See accompanying notes to the basic financial statements.

16

Program Revenues

Operating GrantsExpenses And Contributions

Governmental Activities:Child development 35,046,762$ 28,190,709$ (6,856,053)$

General Revenues:Investment income 122,358 Miscellaneous 159,344

Total General Revenues 281,703

Change in Net Position (6,574,351)

Net Position, July 1 78,985,485

Net Position, June 30 72,411,134$

Net (Expense) Revenueand Changes in Net Position

Governmental Activities

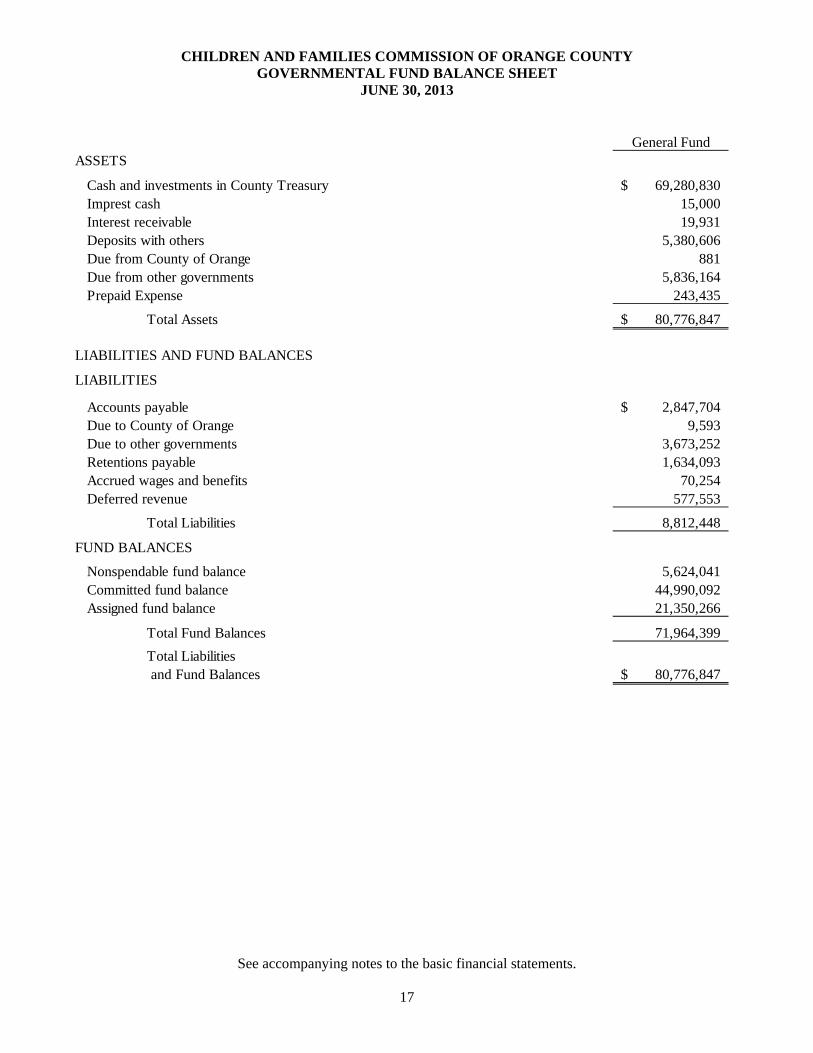

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY GOVERNMENTAL FUND BALANCE SHEET

JUNE 30, 2013

See accompanying notes to the basic financial statements.

17

ASSETS

Cash and investments in County Treasury 69,280,830$ Imprest cash 15,000 Interest receivable 19,931 Deposits with others 5,380,606 Due from County of Orange 881 Due from other governments 5,836,164 Prepaid Expense 243,435

Total Assets 80,776,847$

LIABILITIES AND FUND BALANCES

LIABILITIES

Accounts payable 2,847,704$ Due to County of Orange 9,593 Due to other governments 3,673,252 Retentions payable 1,634,093 Accrued wages and benefits 70,254 Deferred revenue 577,553

Total Liabilities 8,812,448

FUND BALANCES

Nonspendable fund balance 5,624,041 Committed fund balance 44,990,092 Assigned fund balance 21,350,266

Total Fund Balances 71,964,399

Total Liabilities and Fund Balances 80,776,847$

General Fund

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY RECONCILIATION OF GOVERNMENTAL FUND BALANCE SHEET

TO THE STATEMENT OF NET POSITION JUNE 30, 2013

See accompanying notes to the basic financial statements.

18

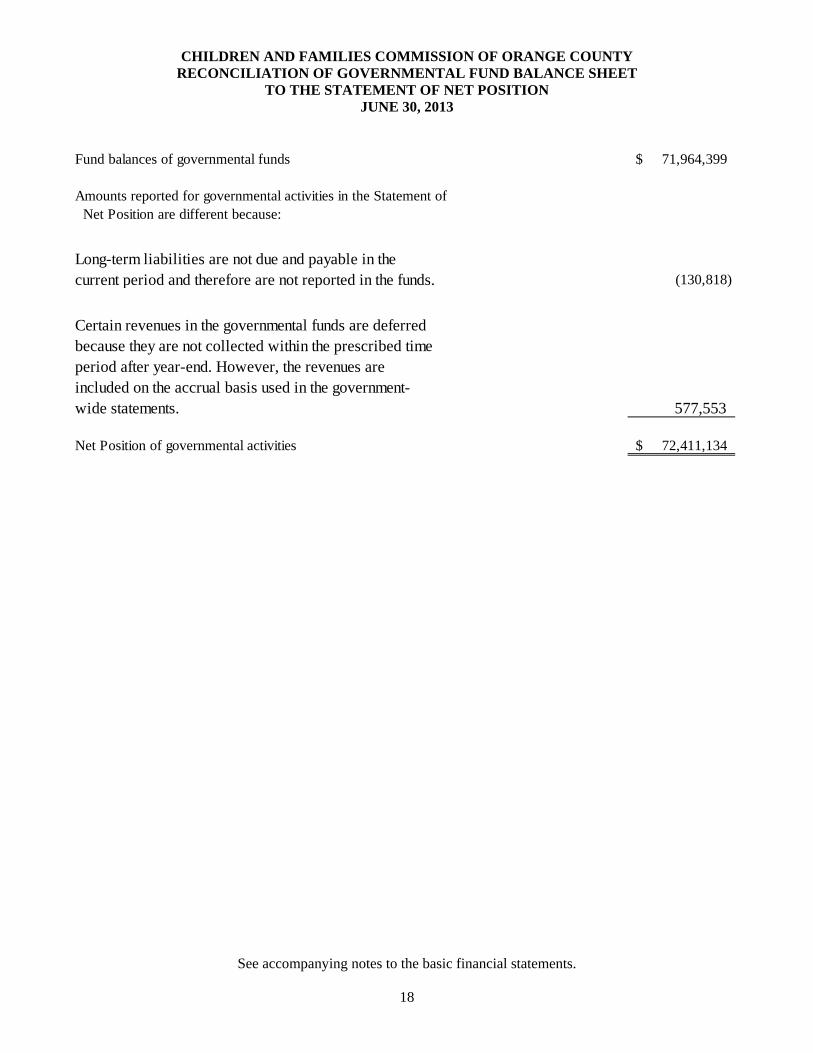

Fund balances of governmental funds 71,964,399$

Amounts reported for governmental activities in the Statement of Net Position are different because:

(130,818)

577,553

Net Position of governmental activities 72,411,134$

Long-term liabilities are not due and payable in the current period and therefore are not reported in the funds.

Certain revenues in the governmental funds are deferred because they are not collected within the prescribed time period after year-end. However, the revenues are included on the accrual basis used in the government-wide statements.

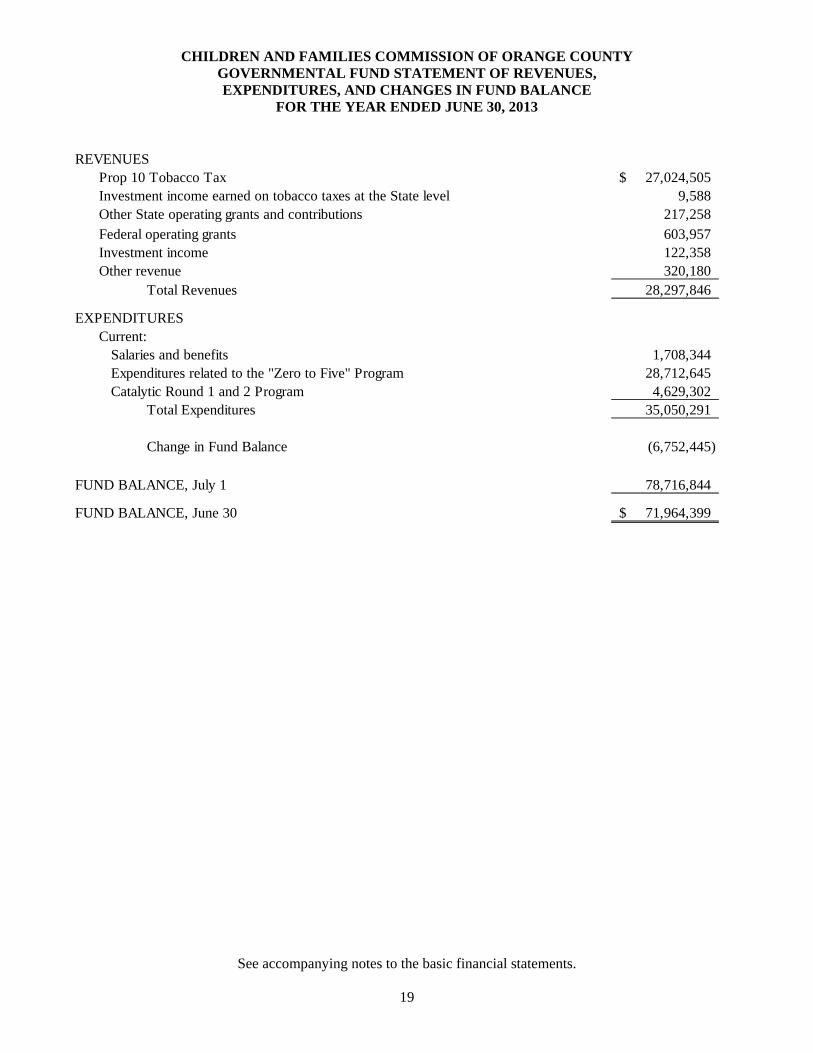

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY GOVERNMENTAL FUND STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCE

FOR THE YEAR ENDED JUNE 30, 2013

See accompanying notes to the basic financial statements.

19

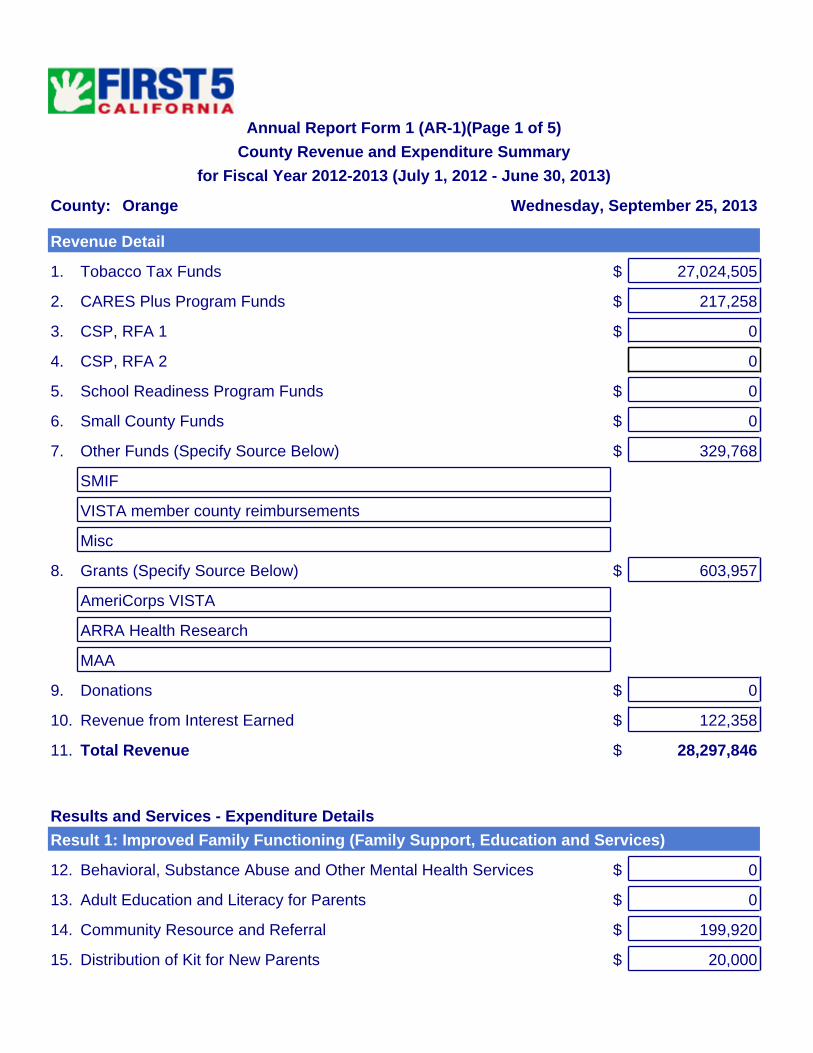

REVENUESProp 10 Tobacco Tax 27,024,505$ Investment income earned on tobacco taxes at the State level 9,588 Other State operating grants and contributions 217,258

Federal operating grants 603,957 Investment income 122,358 Other revenue 320,180

Total Revenues 28,297,846

EXPENDITURESCurrent:

Salaries and benefits 1,708,344 Expenditures related to the "Zero to Five" Program 28,712,645 Catalytic Round 1 and 2 Program 4,629,302

Total Expenditures 35,050,291

Change in Fund Balance (6,752,445)

FUND BALANCE, July 1 78,716,844

FUND BALANCE, June 30 71,964,399$

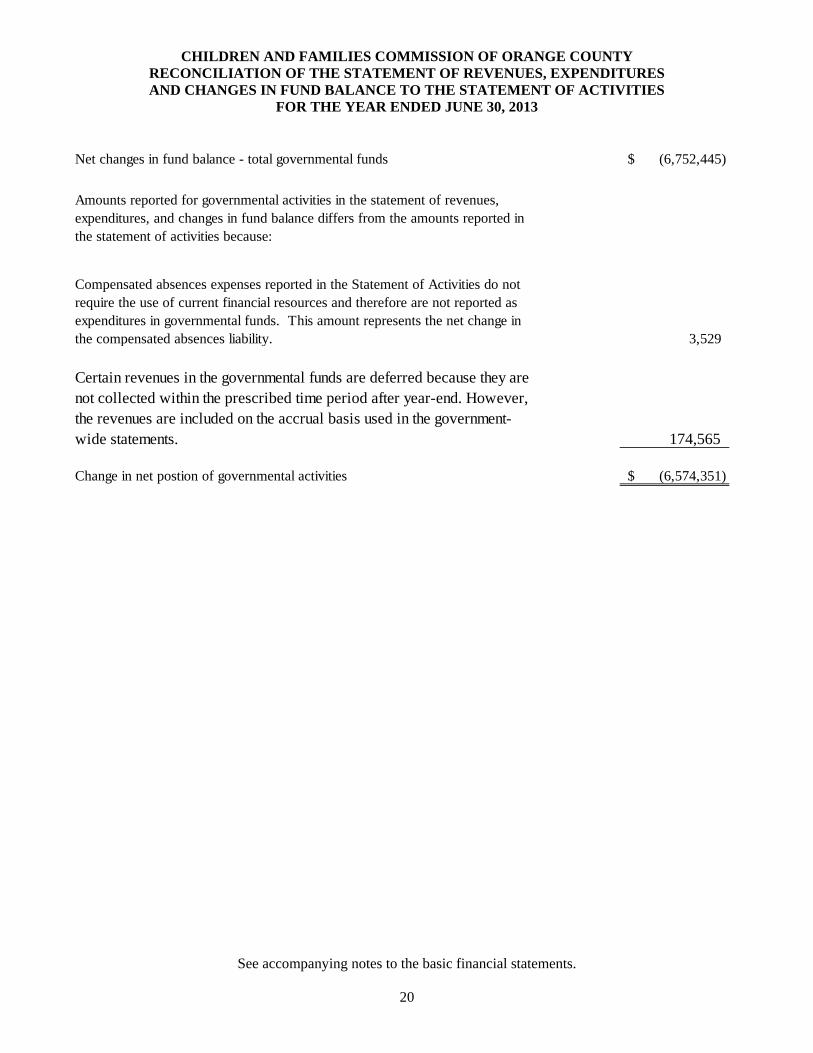

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY RECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCE TO THE STATEMENT OF ACTIVITIES

FOR THE YEAR ENDED JUNE 30, 2013

See accompanying notes to the basic financial statements.

20

Net changes in fund balance - total governmental funds (6,752,445)$

3,529

174,565

Change in net postion of governmental activities (6,574,351)$

Certain revenues in the governmental funds are deferred because they are not collected within the prescribed time period after year-end. However, the revenues are included on the accrual basis used in the government-wide statements.

Amounts reported for governmental activities in the statement of revenues, expenditures, and changes in fund balance differs from the amounts reported in the statement of activities because:

Compensated absences expenses reported in the Statement of Activities do not require the use of current financial resources and therefore are not reported as expenditures in governmental funds. This amount represents the net change in the compensated absences liability.

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY STATEMENT OF REVENUES, EXPENDITURES, AND

CHANGES IN FUND BALANCE – BUDGET AND ACTUAL GENERAL FUND

FOR THE YEAR ENDED JUNE 30, 2013

See accompanying notes to the basic financial statements.

21

Variance withFinal Budget -

Actual Positive Original Final Amounts (Negative)

REVENUESProp 10 Tobacco Tax 26,809,800$ 27,971,800$ 27,024,505$ (947,295)$ Investment income earned on tobacco taxes at the State level - - 9,588 9,588 Other State operating grants and contributions 300,000 425,000 217,258 (207,742) Federal operating grants 455,195 880,126 603,957 (276,169) Investment income 150,000 150,000 122,358 (27,642) Other revenue - 143,000 320,180 177,180

Total Revenues 27,714,995 29,569,926 28,297,846 (1,272,080)

EXPENDITURESCurrent:

Salaries and benefits 1,825,000 1,772,000 1,708,344 63,656 Expenditures related to the "Zero to Five" Program 31,161,628 32,989,182 28,712,645 4,276,537 Catalytic Round 1 and 2 Program Funding 45,000,000 48,730,000 4,629,302 44,100,698

Total Expenditures 77,986,628 83,491,182 35,050,291 48,440,891

Net Change in Fund Balance (50,271,633) (53,921,256) (6,752,445) 49,712,971

FUND BALANCE, July 1 78,716,844 78,716,844 78,716,844 -

FUND BALANCE, June 30 28,445,211$ 24,795,588$ 71,964,399$ 49,712,971$

Budgeted Amouts

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY NOTES TO BASIC FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2013

22

NOTE 1 – ORGANIZATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES Reporting Entity The Children and Families Commission of Orange County (Commission) was established by the Orange County Board of Supervisors in 1999 under the provisions of the California Children and Families Act of 1998 (Act). The Commission is a public entity legally separate and apart from the County. The purpose of the Commission is to develop, adopt, promote and implement early childhood development and school readiness programs in the County of Orange consistent with the goals and objectives of the Act. The Commission’s programs are funded primarily by taxes levied by the State of California on tobacco products. A governing board of nine members, which are appointed by the County Board of Supervisors, oversees the Commission. Three members are considered Mandatory Members, comprised of representatives of the County Health Care Agency, Social Services Agency and Board of Supervisors. Other members are considered At-Large Members. The Board of Supervisors Mandatory Member serves for a one-year term without limitation on the number of terms he/she may serve. Other Mandatory Members serve until removed by the Board of Supervisors. At-Large Members serve for terms ranging from two to four years, not to exceed eight consecutive years. The County Board of Supervisors may remove any Commission Member at any time. The Commission is considered a component unit of the County of Orange. Upon termination of the commission, all assets of the Commission shall be returned to the State of California. The liabilities of the Commission shall not become liabilities of the County upon either termination of the Commission or the liquidation or disposition of the Commission’s remaining assets. Basis of Accounting and Measurement Focus The basic financial statements of the Commission are composed of the following:

Government-wide financial statements

Fund financial statements

Notes to the basic financial statements

Government-Wide Financial Statements Government-wide financial statements consist of the statement of net position and the statement of activities. These statements are presented on an economic resources measurement focus. All economic resources and obligations of the reporting government are reported in the financial statements. The government-wide financial statements have been prepared on the accrual basis of accounting. Under the accrual basis of accounting all assets and liabilities of the Commission are included on the statement of net position. The difference between the Commission’s assets and liabilities is its net position. Net position represent the resources the Commission has available for use in providing services. The Commission’s net position is classified as:

Net Investment in Capital Assets – This amount represents the Commission’s capital assets, net of accumulated depreciation.

Unrestricted – This category represents neither restrictions or invested in capital assets and may be used by the Commission for any purpose though they may not be necessarily liquid.

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY NOTES TO BASIC FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2013

23

NOTE 1 – ORGANIZATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) Government-Wide Financial Statements, (Continued) The statement of activities presents a comparison of the direct expenses and program revenues for the Commission’s governmental activities. Program revenues include grants and contributions restricted for the operational requirements of a particular program. Grants and similar items are recognized as revenue as soon as all eligibility requirements have been met. Program revenues include tobacco taxes, First 5 CARES Plus, First 5 CSP, and federal revenues. General revenues are all revenues that do not qualify as program revenues and include investment income and miscellaneous income. Revenues, expenses, gains, losses, assets and liabilities resulting from exchange and exchange-like transactions are recognized when the exchange takes place. Revenues, expenses, gains, losses, assets and liabilities resulting from non-exchange transactions are recognized in accordance with the requirements of GASB Statement No. 33 which defines the time requirements and purpose restrictions on the use of resources. Fund Financial Statements The fund financial statements consist of the balance sheet, the statement of revenues, expenditures and changes in fund balance, and the statement of revenues, expenditures and changes in fund balance – budget and actual of the Commission’s general fund. These statements are presented on a current financial resources measurement focus. Generally, only current assets and current liabilities are included on the balance sheet. The statement of revenues, expenditures and changes in fund balance for the governmental fund generally presents increases (revenues) and decreases (expenditures) in net current assets. All operations of the Commission are accounted for in the general fund. The fund financial statements have been prepared on the modified accrual basis of accounting. Revenues are recognized in the accounting period in which they become both measurable and available to finance expenditures of the current period. Revenues are considered available if they are received within 60 days after year-end. Revenues susceptible to accrual include tax revenues, grant revenues and investment income. Expenditures are recognized in the accounting period in which the fund liability is incurred except for compensated absences, which are recognized when due and payable at year-end. Capital assets, net of accumulated depreciation Equipment is not considered to be financial resources and therefore, is not reported as an asset in the fund financial statements. Equipment is capitalized and reported at cost, net of accumulated depreciation in the government-wide financial statements. There were no additions to the capital assets in the current year. Capital assets are recorded at cost. The Commission capitalizes assets with cost in excess of $5,000 and a useful life greater than one year. The Commission depreciates capital assets using a straight-line method over the estimated useful life of each asset. The estimated useful life used for the capital assets, comprised only of equipments, ranges from 5 to 10 years.

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY NOTES TO BASIC FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2013

24

NOTE 1 – ORGANIZATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) Adjustments Between Fund Financial Statements and Government-Wide Financial Statements Deferred Revenue Under the modified accrual basis of accounting, revenue is recognized in the fund financial statements if it has been collected after year-end within the Commission’s established availability period of 60 days. All other accrued revenues due the Commission are deferred at year-end in the fund financial statements. Deferred revenue of $577,553 at June 30, 2013 was recognized as revenue in the government-wide financial statements. Long-Term Liabilities Compensated absence obligations are considered long-term in nature and are reported in the fund financial statements as expenditures in the period paid or when due and payable at year-end under the modified accrual basis of accounting. The compensated absences have been accrued in the government-wide financial statements and are included in long-term liabilities. The compensated absences are liquidated by the general fund. Deposits with Others The Deposits with Others account includes funds that were transferred or advanced to program providers, but the related services were not provided before June 30, 2013. Due to Other Governments Due to other governments represents amounts owed to grantees and governmental agencies for services provided to the Commission in accordance with the Commission’s strategic plan. Retentions Payable The Commission retains a percentage of amounts billed by grantees and vendors in accordance with executed contracts. Upon fulfilling the requirements of the grantee agreement or contract, the amounts are released. Use of Estimates The preparation of financial statements in conformity with generally accepted accounting principles in the United States requires management to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying notes. Actual results could differ from those estimates. The Commission’s significant estimates are recorded in accounts payable and due to other governments and pertain to accruals for services provided by grantees and vendors but not invoiced as of June 30, 2013. Budget and Budget Reporting The Commission is required by County ordinance to prepare a budget each year based on estimates of revenues and expected expenditures. The Commission’s Board of Commissioners adopted an annual budget of expenditures for the year ended June 30, 2013, which is prepared on the modified accrual basis of accounting. The accompanying statement of revenues, expenditures and changes in fund balance – budget and actual includes the budgeted expenditures for the year, along with management’s estimate of revenues for the year. The legal level of budgetary control is at the total fund level.

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY NOTES TO BASIC FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2013

25

NOTE 1 – ORGANIZATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) Fund Balance GASB Statement No. 54, Fund Balance Reporting and Governmental Fund Type Definitions statement established fund balance classifications that comprise a hierarchy based primarily on the extent to which a government is bound to observe constraints imposed upon the use of the resources reported in governmental funds. The Commission established the following classifications and definitions of fund balance:

Nonspendable – Resources that cannot be spent because they are not in an expendable form (e.g. prepaid asset, inventory) or must be maintained intact (e.g. endowment principal). Restricted – Resources that are constrained to specific purposes by an external provider (e.g. grantors, contributors, governmental laws and regulations) or by constitutional provisions or enabling legislation. Committed – Resources with self-imposed limitations, evidenced by the Commission’s formal action (resolution), and require both the approval of the highest level of decision making authority (Board of Commissioners) and the same formal action to remove or modify the limitations. Includes legally enforceable multi-year contracts not yet spent, specific agreements approved but not yet executed. Assigned – Resources with self-imposed limitations but do not require approval by the highest level of decision making authority (may be a body, committee or individual designated by Board of Commissioners) or the same level of formal action to remove or modify limitations. Includes appropriation of a portion of existing fund balance sufficient to eliminate subsequent year’s budget deficit, resources assigned to specific program for which there is an approved budget, and resources approved by the Commission for a long range financial plan.

Unassigned – Resources that cannot be reported in any other classification. The Commission’s spending priority is to spend restricted fund balance first, followed by committed, assigned and unassigned fund balance.

Minimum Fund Balance Policy The policy of the Commission is to maintain a minimum fund balance equal to 25% of the Commission’s annual operating budget. The fund balance will be used to mitigate the impact on contracted services due to unanticipated circumstances and events, provide adequate resources for cash flow, and to mitigate short-term effects of revenue shortages. The amount of the minimum fund balance is subject to approval by the Board of Commissioners as part of the annual budget adoption. Encumbrances The Commission utilizes an encumbrance system as a management control technique to assist in controlling expenditures. Unencumbered appropriations lapse at the end of the fiscal year.

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY NOTES TO BASIC FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2013

26

NOTE 1 – ORGANIZATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) Effect of New Governmental Accounting Standards Board (GASB) Pronouncements GASB Statement No. 60 – In December 2010, GASB issued Statement No. 60, Accounting and Financial Reporting for Service Concession Arrangements. This statement is to improve financial reporting by addressing issues related to service concession arrangements. This statement was effective July 1, 2012. The Commission has determined that this statement did not have a material impact on the financial statements. GASB Statement No. 61 – In December 2010, GASB issued Statement No. 61, The Financial Reporting Entity: Omnibus. The objective of this statement is to improve financial reporting for governmental financial reporting entities. This statement modifies certain requirements for inclusion of component units in the financial reporting entity and amends the criteria for reporting component units as if they were a part of the primary government in certain circumstances. This statement was effective July 1, 2012. The Commission has determined that this statement does not have a material impact on the financial statements. GASB Statement No. 62 – In June 2011, GASB issued Statement No. 62, Codification of Accounting and Financial Reporting Guidance Contained in Pre-November 30, 1989 FASB and AICPA Pronouncements. The objective of this statement is to incorporate into the GASB’s authoritative literature certain accounting and financial reporting guidance that is included in FASB and AICPA pronouncements issued on or before November 30, 1989 which does not conflict with our contradict GASB pronouncements. This statement was effective July 1, 2012. The Commission has determined that this statement did not have a material impact on the financial statements. GASB Statement No. 63, Financial Reporting of Deferred Outflows of Resources, Deferred Inflows of Resources, and Net Position, was issued in June 30, 2011. This statement provides financial reporting guidance for deferred outflows of resources and deferred inflows of resources. This statement also amends the net asset reporting requirements in Statement No. 34, Basic Financial Statements—and Management’s Discussion and Analysis—for State and Local Governments, and other pronouncements by incorporating deferred outflows of resources and deferred inflows of resources into the definitions of the required components of the residual measure and by renaming that measure as net position, rather than net assets. The Commission implemented this statement effective July 1, 2012. GASB Statement No. 65 – In March 2012, GASB issued Statement No. 65, Items Previously Reported as Assets and Liabilities. This statement establishes accounting and financial reporting standards that reclassify, as deferred outflows of resources, certain items that were previously reported as assets and liabilities and recognizes, as outflows of resources or inflows of resources, certain items that were previously reported as assets and liabilities. This statement is effective for periods beginning after December 15, 2012. The Commission has not determined the effect of this statement. GASB Statement No. 66 – In March 2012, GASB issued Statement No. 66, Technical Corrections – 2012 – an amendment of GASB Statement No. 10 and No. 62. This statement is to improve accounting and financial reporting for a governmental financial reporting entity by resolving conflicting guidance that resulted from the issuance of two pronouncements, Statement No. 54, Fund Balance Reporting and Governmental Fund Type Definitions, and No. 62, Codification of Accounting and Financial Reporting Guidance Contained in Pre-November 30, 1989 FASB and AICPA Pronouncements. This statement is effective for financial statements beginning after December 15, 2012. The Commission has not determined the effect of this statement.

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY NOTES TO BASIC FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2013

27

NOTE 1 – ORGANIZATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) Effect of New Governmental Accounting Standards Board (GASB) Pronouncements (Continued) GASB Statement No. 67 – In June 2012, GASB issued Statement No. 67, Financial Reporting for Pension Plans – an amendment of GASB Statement No. 25. This statement results from a comprehensive review of the effectiveness of existing standards of accounting and financial reporting for pensions with regard to providing decision-useful information, supporting assessments of accountability and interperiod equity, and creating additional transparency. This statement is effective June 30, 2014. The Commission has not determined the effect of this statement. GASB Statement No. 68 – In June 2012, GASB issued Statement No. 68, Accounting and Financial Reporting for Pensions – an amendment of GASB Statement No. 27. This Statement replaces the requirements of Statements No. 27 and No. 50 related to pension plans that are administered through trusts or equivalent arrangements. The requirements of Statements No. 27 and No. 50 remain applicable for pensions that are not administered as trusts or equivalent arrangements. The requirements of this Statement are effective for financial statements for fiscal years beginning after June 15, 2014. The Commission has not determined the effect of this statement. GASB Statement No. 69 – In January 2013, GASB issued Statement No. 69, Government Combinations and Disposals of Government Operations. This Statement establishes accounting and financial reporting standards related to government combinations and disposals of government operations. This Statement is effective for periods beginning after December 31, 2013. The Commission has not determined the effect of this statement. GASB Statement No. 70 – In April 2013, GASB issued Statement No. 70, Accounting and Financial Reporting for Nonexchange Financial Guarantees. This Statement improves accounting and financial reporting by state and local governments that extend and receive nonexchange financial guarantees. This Statement is effective for periods beginning after June 15, 2013. The Commission has not determined the effect of this statement. NOTE 2 – CASH AND INVESTMENTS Cash and investments are classified in the financial statements as follows: Cash and investments in County Treasury 69,280,830$ Imprest Cash 15,000

Total Cash and Investments 69,295,830$

Cash and investments consisted of the following at June 30, 2013: Orange County Investment Pool:

Equity in pooled Money Market fund 69,280,830$ Imprest Cash 15,000

Total Cash and Investments 69,295,830$

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY NOTES TO BASIC FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2013

28

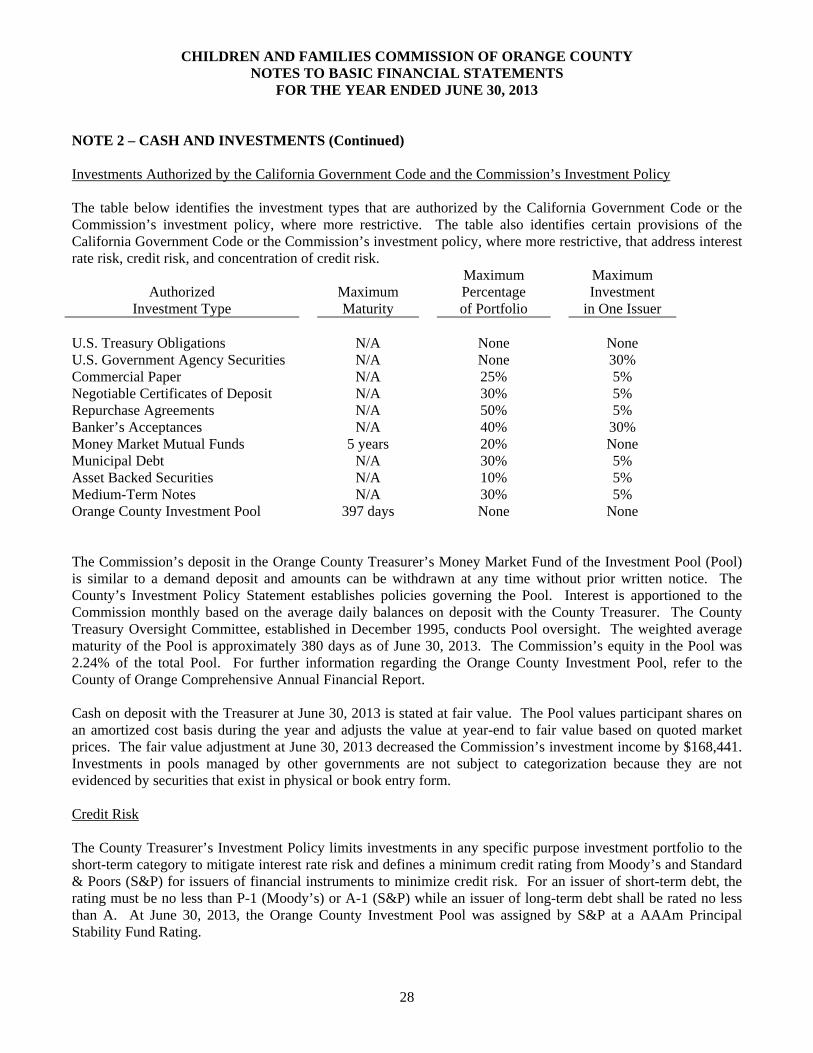

NOTE 2 – CASH AND INVESTMENTS (Continued) Investments Authorized by the California Government Code and the Commission’s Investment Policy The table below identifies the investment types that are authorized by the California Government Code or the Commission’s investment policy, where more restrictive. The table also identifies certain provisions of the California Government Code or the Commission’s investment policy, where more restrictive, that address interest rate risk, credit risk, and concentration of credit risk.

Authorized Investment Type

Maximum Maturity

Maximum Percentage of Portfolio

Maximum Investment

in One Issuer U.S. Treasury Obligations U.S. Government Agency Securities

N/A N/A

None None

None 30%

Commercial Paper Negotiable Certificates of Deposit Repurchase Agreements Banker’s Acceptances Money Market Mutual Funds Municipal Debt Asset Backed Securities Medium-Term Notes Orange County Investment Pool

N/A N/A N/A N/A

5 years N/A N/A N/A

397 days

25% 30% 50% 40% 20% 30% 10% 30% None

5% 5% 5%

30% None 5% 5% 5%

None

The Commission’s deposit in the Orange County Treasurer’s Money Market Fund of the Investment Pool (Pool) is similar to a demand deposit and amounts can be withdrawn at any time without prior written notice. The County’s Investment Policy Statement establishes policies governing the Pool. Interest is apportioned to the Commission monthly based on the average daily balances on deposit with the County Treasurer. The County Treasury Oversight Committee, established in December 1995, conducts Pool oversight. The weighted average maturity of the Pool is approximately 380 days as of June 30, 2013. The Commission’s equity in the Pool was 2.24% of the total Pool. For further information regarding the Orange County Investment Pool, refer to the County of Orange Comprehensive Annual Financial Report. Cash on deposit with the Treasurer at June 30, 2013 is stated at fair value. The Pool values participant shares on an amortized cost basis during the year and adjusts the value at year-end to fair value based on quoted market prices. The fair value adjustment at June 30, 2013 decreased the Commission’s investment income by $168,441. Investments in pools managed by other governments are not subject to categorization because they are not evidenced by securities that exist in physical or book entry form. Credit Risk The County Treasurer’s Investment Policy limits investments in any specific purpose investment portfolio to the short-term category to mitigate interest rate risk and defines a minimum credit rating from Moody’s and Standard & Poors (S&P) for issuers of financial instruments to minimize credit risk. For an issuer of short-term debt, the rating must be no less than P-1 (Moody’s) or A-1 (S&P) while an issuer of long-term debt shall be rated no less than A. At June 30, 2013, the Orange County Investment Pool was assigned by S&P at a AAAm Principal Stability Fund Rating.

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY NOTES TO BASIC FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2013

29

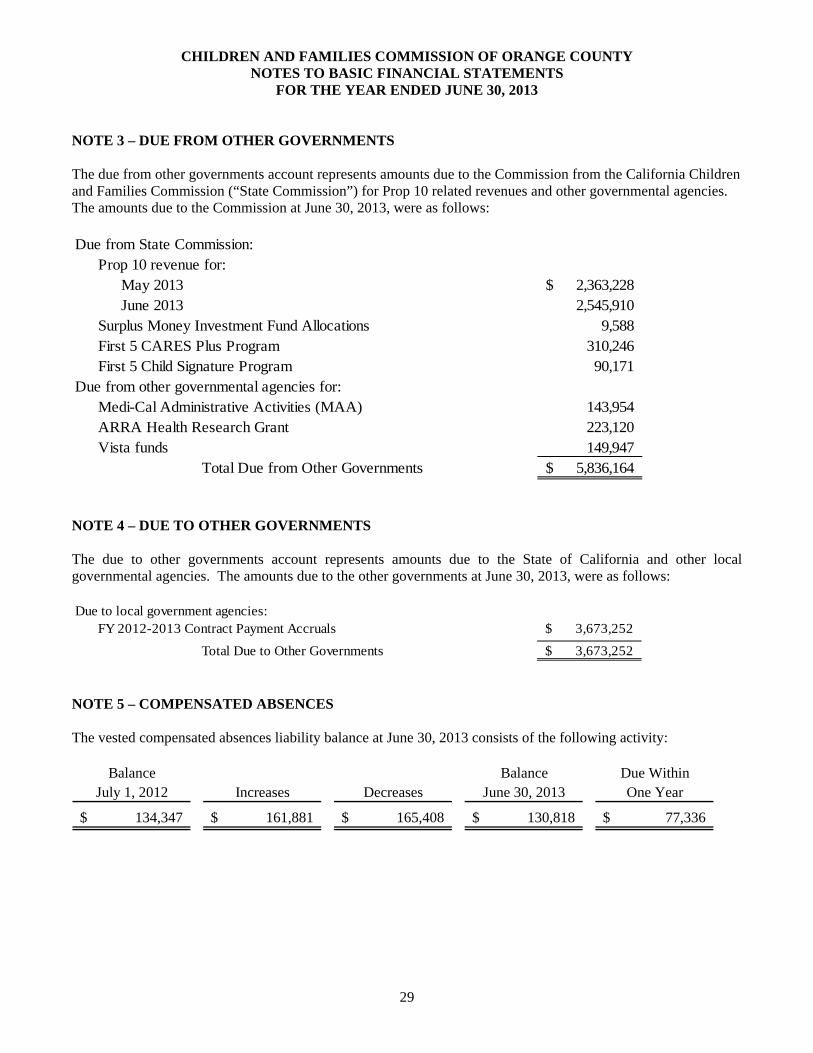

NOTE 3 – DUE FROM OTHER GOVERNMENTS The due from other governments account represents amounts due to the Commission from the California Children and Families Commission (“State Commission”) for Prop 10 related revenues and other governmental agencies. The amounts due to the Commission at June 30, 2013, were as follows: Due from State Commission:

Prop 10 revenue for:May 2013 2,363,228$ June 2013 2,545,910

Surplus Money Investment Fund Allocations 9,588 First 5 CARES Plus Program 310,246 First 5 Child Signature Program 90,171

Due from other governmental agencies for:Medi-Cal Administrative Activities (MAA) 143,954 ARRA Health Research Grant 223,120 Vista funds 149,947

Total Due from Other Governments 5,836,164$

NOTE 4 – DUE TO OTHER GOVERNMENTS The due to other governments account represents amounts due to the State of California and other local governmental agencies. The amounts due to the other governments at June 30, 2013, were as follows: Due to local government agencies:

FY 2012-2013 Contract Payment Accruals 3,673,252$

Total Due to Other Governments 3,673,252$

NOTE 5 – COMPENSATED ABSENCES The vested compensated absences liability balance at June 30, 2013 consists of the following activity:

Balance Balance Due WithinJuly 1, 2012 Increases Decreases June 30, 2013 One Year

134,347$ 161,881$ 165,408$ 130,818$ 77,336$

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY NOTES TO BASIC FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2013

30

NOTE 6 – FUND BALANCE Fund balance is classified using a hierarchy based primarily on the extent to which a government is bound to observe constraints imposed upon the use of the resources reported in governmental funds. Fund balance at June 30, 2013 consists of the following:

June 30, 2013Nonspendable:

Prepaid retirements 243,435$ Deposits with Others 5,624,041

Committed for:Contractual obligations 44,990,092

Assigned for:Budgeted programs 21,350,266

Total Due from Other Governments 71,964,399$

Fund Balance Category Descriptions Nonspendable – consists of prepaid retirement contributions for FY 2013-2014. Refer to Note 8 for further details. Also included are the amounts transferred to contractors for services not provided by June 30, 2013. Committed for contractual obligations – consists of contract amounts approved by Commission action as of June 30, 2013 for FY 2013-2014 and future years of Commission Round 1 and 2 Catalytic funding. Assigned for budgeted programs – consists of FY 2013-2014 contracts that were approved by Commission action and included in the FY 2013-2014 Operating Budget. NOTE 7 – CONTINGENCIES The Commission is involved in various legal proceedings from time to time in the normal course of business. In management’s opinion, the Commission is not involved in any legal proceeding that will have a material adverse effect on financial position or changes in financial position of the Commission. NOTE 8 – DEFINED BENEFIT PENSION PLAN Plan Description. All full-time employees of the Commission participate in the Orange County Employees Retirement System (OCERS), which is a cost-sharing, multiple-employer, defined benefit pension plan. OCERS provides for retirement, death, disability and cost-of-living benefits, and is subject to the provisions of the County Employees Retirement Act of 1937 and other applicable statutes.

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY NOTES TO BASIC FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2013

31

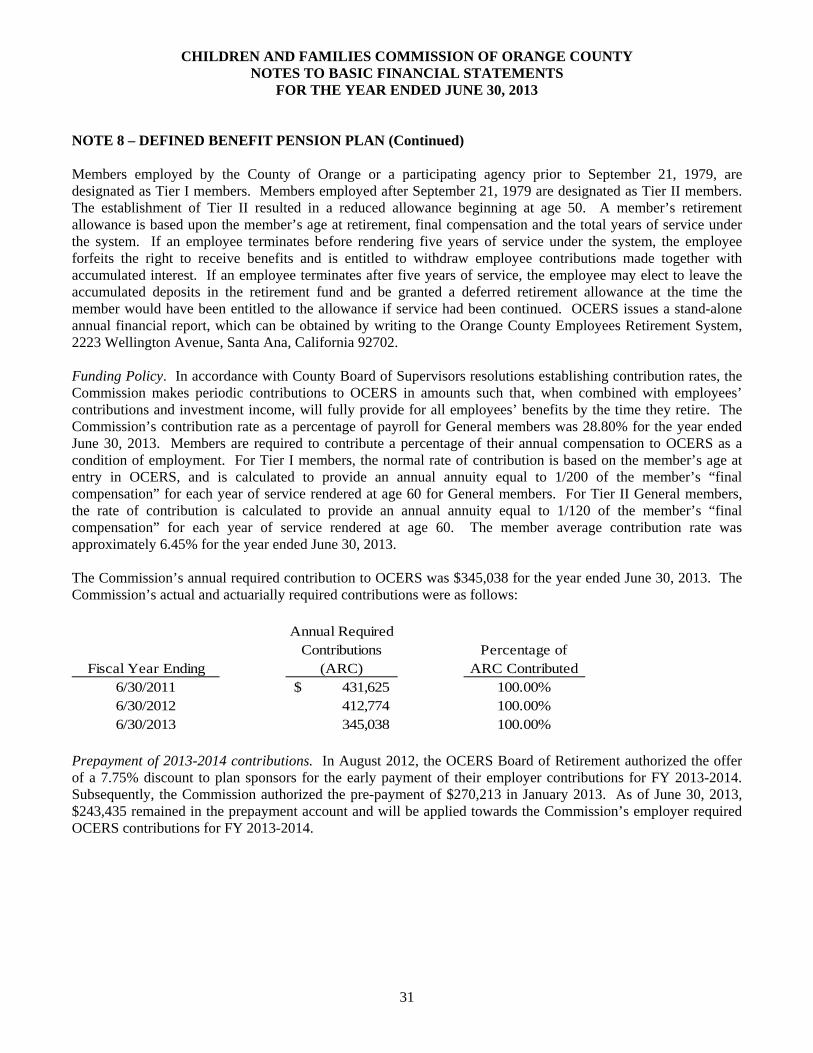

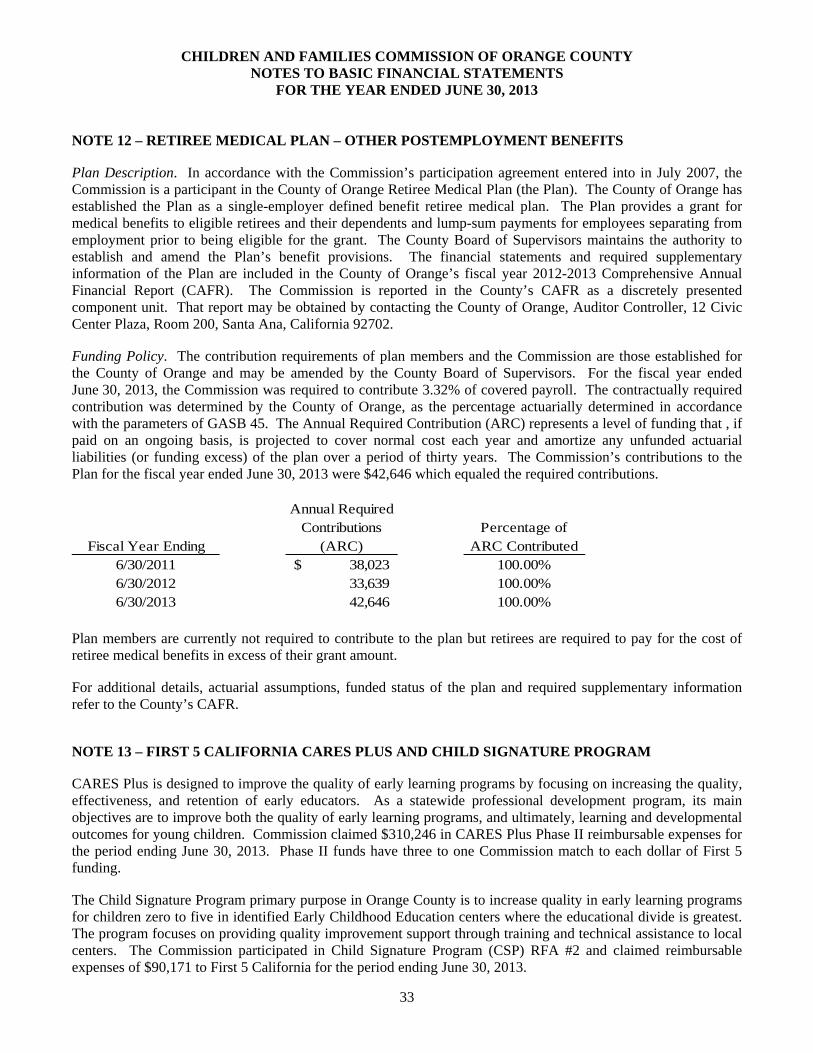

NOTE 8 – DEFINED BENEFIT PENSION PLAN (Continued) Members employed by the County of Orange or a participating agency prior to September 21, 1979, are designated as Tier I members. Members employed after September 21, 1979 are designated as Tier II members. The establishment of Tier II resulted in a reduced allowance beginning at age 50. A member’s retirement allowance is based upon the member’s age at retirement, final compensation and the total years of service under the system. If an employee terminates before rendering five years of service under the system, the employee forfeits the right to receive benefits and is entitled to withdraw employee contributions made together with accumulated interest. If an employee terminates after five years of service, the employee may elect to leave the accumulated deposits in the retirement fund and be granted a deferred retirement allowance at the time the member would have been entitled to the allowance if service had been continued. OCERS issues a stand-alone annual financial report, which can be obtained by writing to the Orange County Employees Retirement System, 2223 Wellington Avenue, Santa Ana, California 92702. Funding Policy. In accordance with County Board of Supervisors resolutions establishing contribution rates, the Commission makes periodic contributions to OCERS in amounts such that, when combined with employees’ contributions and investment income, will fully provide for all employees’ benefits by the time they retire. The Commission’s contribution rate as a percentage of payroll for General members was 28.80% for the year ended June 30, 2013. Members are required to contribute a percentage of their annual compensation to OCERS as a condition of employment. For Tier I members, the normal rate of contribution is based on the member’s age at entry in OCERS, and is calculated to provide an annual annuity equal to 1/200 of the member’s “final compensation” for each year of service rendered at age 60 for General members. For Tier II General members, the rate of contribution is calculated to provide an annual annuity equal to 1/120 of the member’s “final compensation” for each year of service rendered at age 60. The member average contribution rate was approximately 6.45% for the year ended June 30, 2013. The Commission’s annual required contribution to OCERS was $345,038 for the year ended June 30, 2013. The Commission’s actual and actuarially required contributions were as follows:

Fiscal Year Ending

Annual Required Contributions

(ARC)Percentage of

ARC Contributed6/30/2011 431,625$ 100.00%6/30/2012 412,774 100.00%6/30/2013 345,038 100.00%

Prepayment of 2013-2014 contributions. In August 2012, the OCERS Board of Retirement authorized the offer of a 7.75% discount to plan sponsors for the early payment of their employer contributions for FY 2013-2014. Subsequently, the Commission authorized the pre-payment of $270,213 in January 2013. As of June 30, 2013, $243,435 remained in the prepayment account and will be applied towards the Commission’s employer required OCERS contributions for FY 2013-2014.

CHILDREN AND FAMILIES COMMISSION OF ORANGE COUNTY NOTES TO BASIC FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2013

32

NOTE 9 – COMMITMENTS The Commission leases office space from a third party under a long-term operating lease. The latest lease expires on October 31, 2016 (FY 2016-17). The future minimum rental payments due under the lease are as follows.

FY 2013-14 111,470$ FY 2014-15 68,607 FY 2015-16 68,607 FY 2016-17 22,869

271,553$