november 2012 investor...

TRANSCRIPT

November 2012 Investor Presentation

2

FORWARD-LOOKING STATEMENTS

This presentation and our accompanying comments include “forward-looking statements.”

These statements relate to future events or our future financial performance and are subject to known

and unknown risks, uncertainties and other factors that may cause our actual results, levels of activity,

performance or achievements to differ materially from those expressed or implied by these forward-

looking statements. This presentation and our accompanying comments do not purport to identify the

risks inherent in an investment in Domino’s Pizza and factors that could cause actual results to differ

materially from those expressed or implied in the forward-looking statements. These risks include but

are not limited to those risk factors identified in Domino’s Pizza, Inc.’s Annual Report on Form 10-K for

the fiscal year ended January 1, 2012, as well as other SEC reports filed by Domino’s Pizza, Inc. from

time to time. Although we believe that the expectations reflected in the forward-looking statements are

based upon reasonable estimates and assumptions, we cannot guarantee future results, levels of

activity, performance or achievements. We caution you not to place undue reliance on forward-looking

statements, which reflect our estimates and assumptions and speak only as of the date of this

presentation. We undertake no obligation to update the forward-looking statements to reflect

subsequent events or circumstances. In light of the above, you are urged to review the disclosures

contained in the Domino’s Pizza, Inc. SEC reports, including the risk factors contained therein.

This presentation contains trade names, trademarks and service marks of other companies. We do not

intend our use or display of other parties’ trade names, trademarks and service marks to imply a

relationship with, or endorsement or sponsorship of, these other parties.

3

INVESTMENT THESIS

Domestic Business

• Popular brand

• Primarily franchised

• Value-adding Supply Chain

International Business

• Entirely franchised

• Highly profitable master franchise business model

• Consistently strong sales and store growth

Leveraging Technology

• Online and mobile ordering

• Digital marketing

Balance Sheet

• Franchise business run efficiently, with leverage

• Cash deployed to benefit shareholders

4

OVER 10,000 UNITS WORLDWIDE

52% of Global Retail Sales 48% of Global Retail Sales

• 4,509 Franchised Stores

• 387 Company-Owned Stores

• 19 Company-Owned Supply

Chain Facilities

Domestic International

• 5,144 Franchised Stores

• Currently No Company-Owned Stores

• 6 Company-Owned Supply Chain

Facilities

As of Q3 2012

5 ¹As of FY 2011

DOMESTIC PIZZA UNIT ECONOMICS

Franchise model generates sustainable returns

• Focused and efficient operating model

— Delivery and carryout

• Low cost to open / operate

— $150,000 - $300,000 average cost range for new store

— Minimal square footage

— Makeline + oven + POS system

• Strong cash-on-cash returns

• Average reported annual EBITDA per domestic franchise store is

between $50,000 and $75,0001

6 Source: The NPD Group/CREST® - year-ending February 2012

DOMESTIC MARKET SHARE

Pizza Delivery Market Share

22%

29%

49%

11%

26% 63%

Total QSR Pizza Market Share

Domino’s Pizza Small Chains & Independents Major Pizza Chains

7

Supporting Strong Domestic Business

DOMESTIC SUPPLY CHAIN

• Sells and delivers food & equipment to U.S. franchisees

• Provides consistency

– Produces fresh dough

– System-wide ingredients & equipment

• Franchise partnership

– Profit-sharing agreement

8

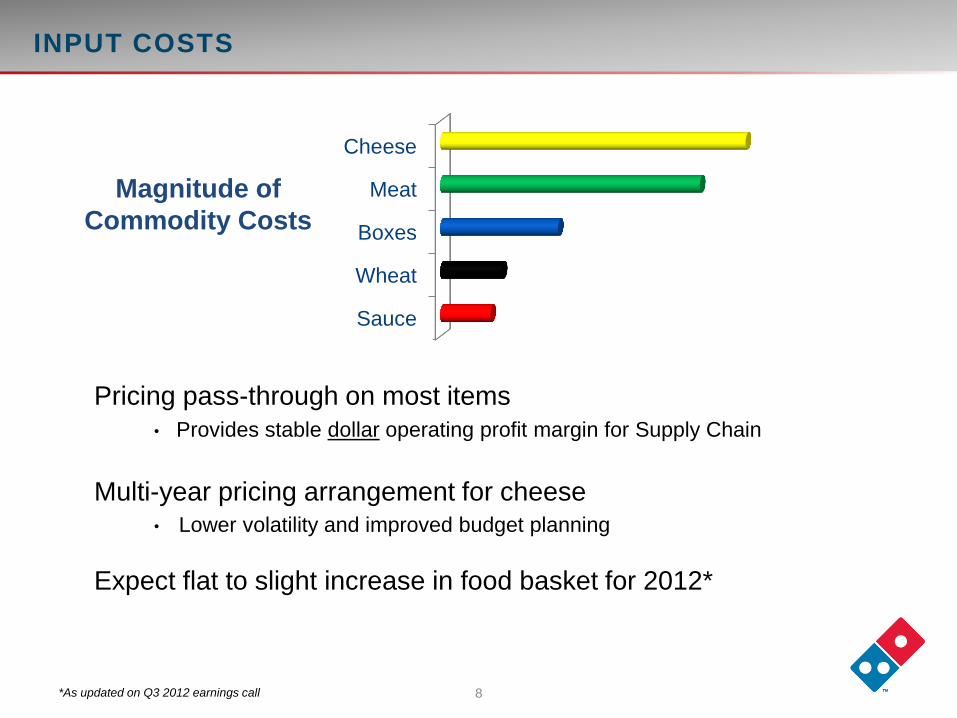

INPUT COSTS

Pricing pass-through on most items

• Provides stable dollar operating profit margin for Supply Chain

Multi-year pricing arrangement for cheese • Lower volatility and improved budget planning

Expect flat to slight increase in food basket for 2012*

Magnitude of

Commodity Costs

Cheese

Meat

Boxes

Wheat

Sauce

*As updated on Q3 2012 earnings call

9

Q3 2012 DOMESTIC RECAP

• SSS +3.3%

• About 40% delivery orders coming from digital channels

• New logo and store design

– Allows franchisees flexibility on timing and scale

Recent News

• Introduced Pan Pizza

– Made from fresh dough

10

3,223 3,469

3,726

4,072

4,422

4,835

2006 2007 2008 2009 2010 2011

Excludes the impact of foreign currency exchange rates

INTERNATIONAL PERFORMANCE

• International profits driven by franchise royalties – 91% of 2011 International operating income

• Limited Domino’s Pizza investment through master franchise model

• Five-year International retail sales CAGR of 13%*

• International is ranked among top five publicly-traded restaurant

companies in terms of store count

*FY 2006 – 2011

International Store Growth International Same Store Sales Growth

4.0%

6.7%

6.2%

4.3%

6.9% 6.8%

2006 2007 2008 2009 2010 2011

INTERNATIONAL OPPORTUNITY

Top 10 Markets Q3 2012

Store Count

Delivery Market

Position

Potential

Store Count

United Kingdom 693 1 1,100

Mexico 584 1 700

India 508 1 1,000

Australia 456 1 650

South Korea 367 1 450

Canada 366 2 450

Turkey 253 1 600

Japan 228 3 700

France 208 1 850

Taiwan 140 2 150

TOTAL 3,803 6,650

Delivery market position and potential store count based on Domino’s Pizza International estimates.

• Potential for nearly 3,000 additional restaurants in Domino’s top 10 international markets alone

• Next five target markets are as diversified as the top ten (store counts as of Q3 2012):

Netherlands (120), Spain (117), Malaysia (94), New Zealand (85), Saudi Arabia (80)

12

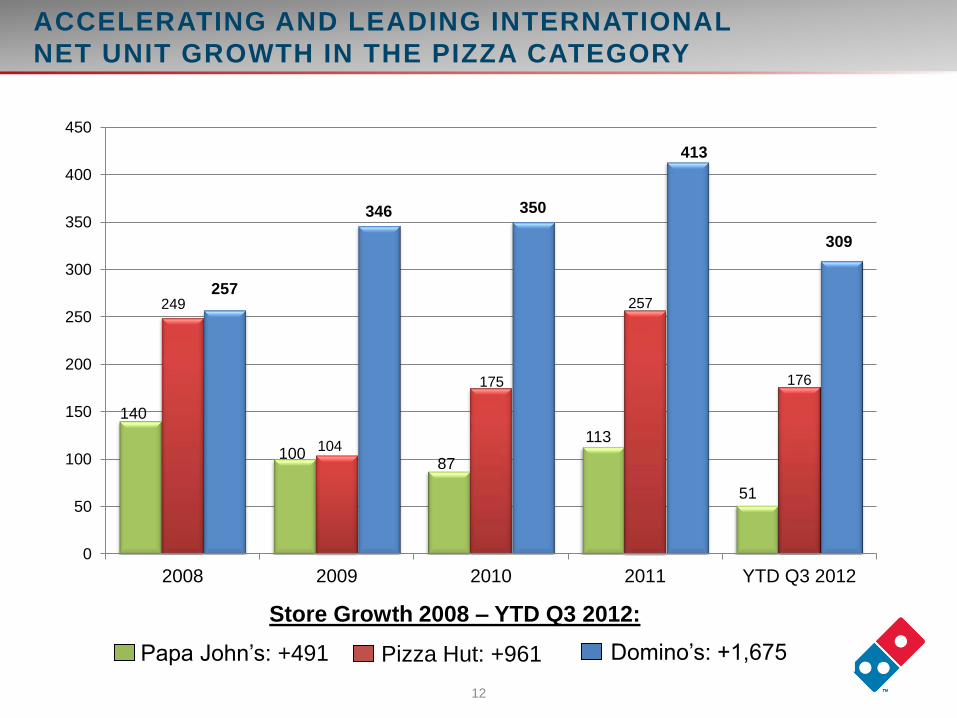

Store Growth 2008 – YTD Q3 2012:

Pizza Hut: +961 Domino’s: +1,675 Papa John’s: +491

ACCELERATING AND LEADING INTERNATIONAL

NET UNIT GROWTH IN THE PIZZA CATEGORY

140

100 87

113

51

249

104

175

257

176

257

346 350

413

309

0

50

100

150

200

250

300

350

400

450

2008 2009 2010 2011 YTD Q3 2012

13

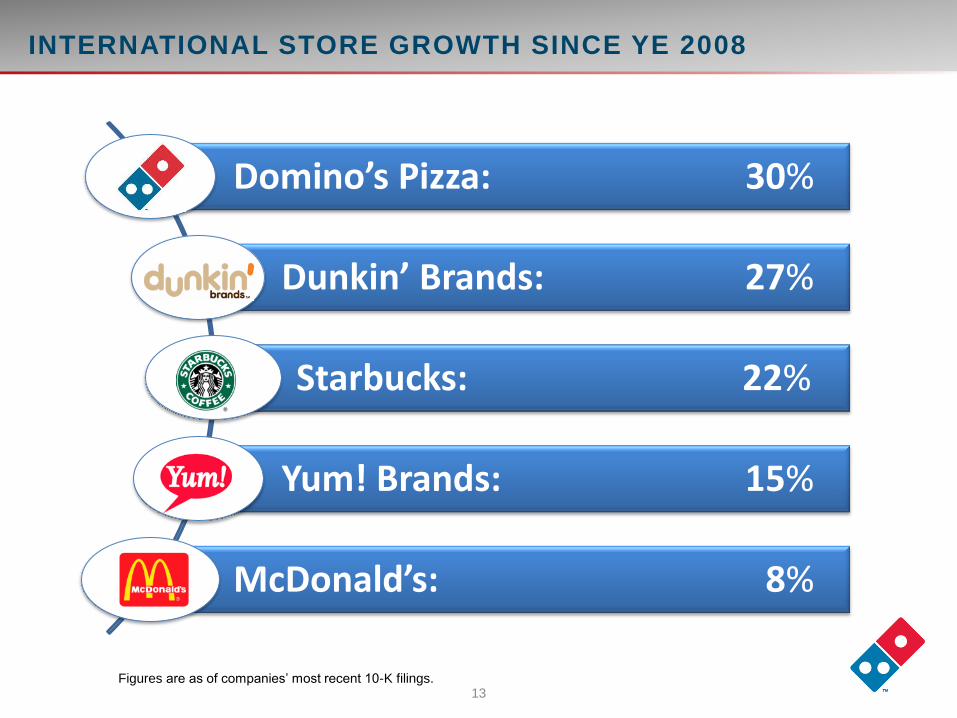

Domino’s Pizza: 30%

Dunkin’ Brands: 27%

Starbucks: 22%

Yum! Brands: 15%

McDonald’s: 8%

Figures are as of companies’ most recent 10-K filings.

INTERNATIONAL STORE GROWTH SINCE YE 2008

14

STRONG INTERNATIONAL FRANCHISE BASE

890

752

511

611

2,380

JUBI

DOM

• India

• Sri Lanka

DMP

• Australia

• New Zealand

• Netherlands

• France

• Belgium

Alsea

• Mexico

• Colombia

Four publicly-traded Domino’s Pizza master franchisees

make up more than half of total international store count

Rest of

International • United Kingdom

• Ireland

• Germany

International master franchisee store count pie chart as of Q3 2012. Master franchisee market capitalization as of 9/7/2012.

Market Cap

$685.7M

Market Cap

$1,396.1M

Market Cap

$1,454.8M

Market Cap

$903.5M

15

Q3 2012 INTERNATIONAL RECAP

• SSS +5.0%

• 75 consecutive quarters of positive same store sales growth

• Store count grew by net 121 units

• New market openings: Macedonia and Nigeria

16

TECHNOLOGY

• Surpassed $1 billion in digital sales

in one year in the U.S.

1

• Both mobile apps, iPhone and

Android, are in the top 10 free app

lifestyle, and food and drink

rankings in the iTunes store and

on Google Play.

• Mobile ordering apps

have been downloaded

almost 3.5 million times.

1 – First achieved in the twelve months ending April 2012

FEBRUARY 2012

JUNE 2011

JUNE 2012

17

5.5

4.7

4.1

3.2

4.8

3.7

3.1 3.0

7.2

7.7

6.7

5.5

4.9 5.0

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Q3 2012

SUCCESSFUL HISTORY OF OPERATING WITH LEVERAGE

Total Debt to EBITDA

18

CAPITAL STRUCTURE

• $1.563 billion debt of Senior Notes outstanding as of Q3 2012

─ 5.216% interest rate

─ 7-year term to Anticipated Repayment Date

─ Required principal payments equal to 1.5% - 2.5% of debt annually until leverage is 4.5x or less

• $100 million VFN facility

─ $39.7 million letters of credit issued as of Q3 2012

─ No borrowings outstanding as of Q3 2012

“Whole-business securitization” secured with most cash flows of the company

19

GROWING EPS

Q3 2012 Adjusted EPS Up Almost 23% Over Q3 2011

(1) EPS amounts are adjusted for items affecting comparability. Items adjusting reported EPS are detailed in the respective Earnings Release or Form 8-K.

0.35 0.33

0.27

0.40 0.42

0.40

0.35

0.52

0.47 0.47

0.43

1.35

1.69

0.70

0.90

1.10

1.30

1.50

1.70

1.90

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

1st Quarter 2nd Quarter 3rd Quarter 4th Quarter Full Year2010 2011 2012

20

CONSISTENT GLOBAL PERFORMANCE

Avg: +2.5%

Avg: +5.6%

3.6%

2.2%

6.7% 6.8%

4.5%

2.8%

0.0%

4.0%

2.6% 1.3% 1.8%

4.9%

-4.1%

-1.7%

-4.9%

0.5%

9.9%

3.5% 2.3%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 YTDQ3

2012

U.S. Same Store Sales 1994 - YTD 2012

8.9%

3.8%

5.2%

11.1%

3.4% 3.6% 3.7%

6.4%

4.1% 4.0%

5.9% 6.1%

4.0%

6.7% 6.2%

4.3%

6.9% 6.8%

5.1%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 YTDQ3

2012

International Same Store Sales 1994 - YTD 2012

21

Domestic Same Store

Sales

+1% to +3%

International Same Store

Sales

+3% to +6%

Global Net Units

+350 to +450

Global Retail Sales

+5% to +8%

Outlook does not constitute specific earnings guidance. Domino’s does not provide quarterly or annual earnings estimates.

LONG RANGE OUTLOOK

22

DEPLOY CAPITAL TO BUILD SHAREHOLDER VALUE

Invest in growing the business, and

1Subsequent to Q3 2012, the Company repurchased 106,573 shares at an average price of $34.98, as stated in the Q3 2012 Form 8-K, with further

details provided in the Form 10-Q.

Deleverage

• Moderate amortization

requirements under

current debt structure.

Repurchase Shares

• Through the first three

quarters of 2012,

repurchased 1.3 million

shares at an average

price of $31.971.

• In July 2012, Board

authorized replenishment

of Open Market

Repurchase Program to

$200 million, the third

time the Board authorized

repurchases since DPZ

went public in 2004.

Pay Dividends

• Paid $3.00 per share

special dividend as part

of recapitalization in

March 2012.

23

PROVEN BUSINESS MODEL

Powerful global brand with more than 50 years of:

Strong product demand

Strong unit economics

Consistent cash flow based upon franchise model

THANK YOU!

Contact Information

Lynn Liddle: [email protected]

Jenny Fouracre: [email protected]

Stacy Haas: [email protected]

Or call us at:734-930-3008