note 1: statement of significant accounting policies … · notes to the financial statements 93...

TRANSCRIPT

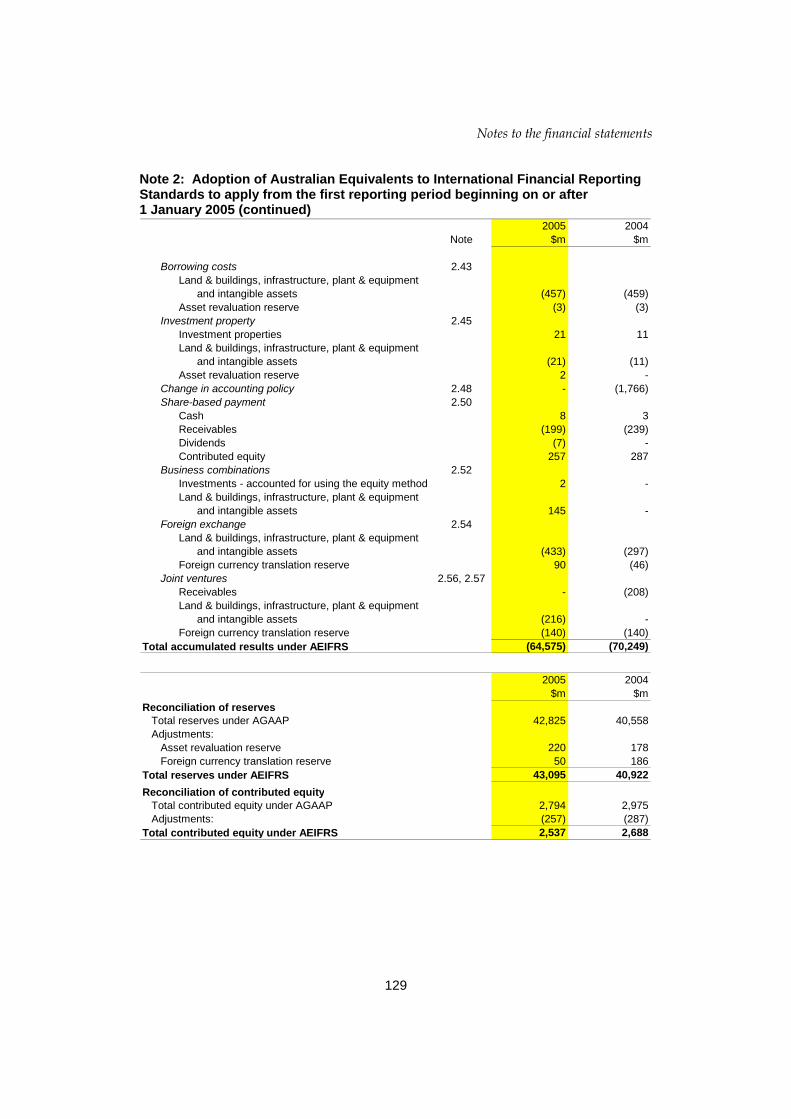

Notes to the financial statements

93

Note 1: Statement of significant accounting policies

1.1 The purpose of this note is to disclose the significant accounting policies applied in the financial report of the Australian Government.

Basis of accounting

1.2 The financial report of the Australian Government is required by section 55 of the Financial Management and Accountability Act 1997, and the regulations of that Act. It is a general purpose financial report.

1.3 The report has been prepared on an accrual basis in accordance with the regulations, and applicable Australian Accounting Standards (AAS) including AAS 31 Financial Reporting by Governments, other authoritative announcements of the Australian Accounting Standards Board, Consensus Views of the Urgent Issues Group and Statements of Accounting Concepts. Any departures from the AAS, other authoritative announcements of the Australian Accounting Standards Board, Consensus Views of the Urgent Issues Group and Statements of Accounting Concepts, have been disclosed in the notes to these financial statements.

The reporting entity

1.4 For the purposes of this financial report, the Australian Government, means the Executive (consisting principally of the Ministers and their departments), the legislature (that is, the Parliament) and the judiciary (that is, the courts). For the purposes of this financial report, the Australian Government reporting entity (referred to as the reporting entity) includes Australian Government Departments of State, Parliamentary Departments, prescribed agencies, Commonwealth authorities, Commonwealth companies limited by shares and Commonwealth companies limited by guarantee in which the Australian Government holds a controlling interest.

1.5 Where the ‘Australian Government’ is referred to throughout this report it is intended to also mean the ‘Commonwealth of Australia’ which includes the Executive, Legislative and Judicial function of government.

1.6 Where control of an entity is obtained during a financial year, results are included in the Consolidated Statement of Financial Performance and Consolidated Statement of Cash Flows from the date on which control commenced. Where control of an entity ceases during a financial year, results are included for that part of the year for which control existed.

Notes to the financial statements

94

Note 1: Statement of significant accounting policies (continued)

1.7 For the purposes of this financial report the control of another entity by the Australian Government complies with the requirements under AAS 24 Consolidated Financial Report.

1.8 The existence of control in the context of this consolidated financial report does not in any way indicate that there is necessarily control over the manner in which statutory/professional functions are performed by an entity.

1.9 A detailed list of entities controlled by the Australian Government is provided in Note 50.

1.10 Australian Government universities have not been consolidated in this financial report, but the value of total net assets has been recognised as an investment. Similarly, the total value of net assets of entities, in which the Australian Government holds a share of the assets but does not significantly influence, have also been recognised as an investment. Details of those entities are included in Note 50.

Sectors

1.11 The sector classification of Government entities broadly follows that defined by the Australian Bureau of Statistics (ABS) for the purposes of the Government Finance Statistics (GFS); this, in turn, is based on international standards issued by the International Monetary Fund.

General government sector

1.12 The general government (GG) sector provides public services that are mainly non-market in nature, and for the collective consumption of the community, or involve the transfer or redistribution of income. These services are largely financed through taxes and other compulsory levies, although user charging and external funding have increased in recent years.

Public non-financial corporations sector

1.13 The primary function of the public non-financial corporations (PNFC) sector is to provide goods and services that are mainly market, non-regulatory, and non-financial in nature, financed mainly through sales to the consumers of these goods and services.

Notes to the financial statements

95

Note 1: Statement of significant accounting policies (continued)

Public financial corporations sector

1.14 The public financial corporations (PFC) sector comprises entities that have one or more of the following characteristics as their principal activity. They:

• perform central banking functions;

• accept demand, time or savings deposits; or

• have the authority to incur liabilities and acquire financial assets in the market on their own account.

Basis of consolidation

1.15 The consolidated financial report of the reporting entity includes the balances of assets and liabilities of the Australian Government and its controlled entities held at the end of the financial year, and the revenues and expenses of the Australian Government and its controlled entities during the year.

1.16 The Consolidated Statement of Financial Performance is presented by nature. An additional schedule has been provided which presents consolidated revenues and expenses by function. This schedule details expenses broadly consistent with the Classifications of the Functions of Government used by the ABS (for example: defence, housing, and education). This additional schedule does not represent a Statement of Financial Performance in accordance with AASB 1018 Statement of Financial Performance.

1.17 The Consolidated Statement of Financial Performance, Statement of Financial Position, Statement of Cash Flows, Schedule of Commitments and Schedule of Contingencies have also been disaggregated by Australian Government sector. Sectors and purposes have been determined by applying GFS reporting principles used by the ABS.

1.18 In the process of reporting the Australian Government as a single economic entity, all material transactions and balances between government controlled entities are eliminated. Where circumstances arise and their effect is considered material, dissimilar accounting policies are amended to ensure consistent policies are adopted in this consolidated financial report.

Foreign currency translation

1.19 Transactions are translated to Australian dollars at the rate of exchange applicable at the date of the transaction.

1.20 Balances and investments are translated at the exchange rates applicable at balance date.

Notes to the financial statements

96

Note 1: Statement of significant accounting policies (continued)

1.21 Foreign exchange holdings contracted for sale beyond 30 June (including those under swap contracts) have been valued at market exchange rates.

Changes in accounting policy

1.22 Changes in accounting policy have been identified in this note under the appropriate headings.

Revenue

Appropriation revenue

1.23 From 1 July 1999, the Australian Government Budget has been prepared under an accruals framework. Within agencies financial reports, the full amount of the appropriation for departmental outputs for the year (less any savings offered up at Additional Estimates and not subsequently released) is recognised as revenue. Appropriations for departmental capital items dependent on specified future events requiring future performance are recognised directly into equity. Appropriations for capital items that are not dependent on specified future events requiring future performance are recognised directly into equity at 1 July.

1.24 As these appropriations are all internal to government, they have been eliminated upon consolidation into this financial report.

Taxation revenue

1.25 Taxation revenues are recognised when the Australian Government gains control of and can reliably measure or estimate the future economic benefits that flow from taxes and other statutory charges. One method of taxation revenue recognition, known as the tax liability method, recognises taxation revenue the earlier of when an assessment of a tax liability is made or payment is received by the Australian Taxation Office or the Australian Customs Service.

1.26 The Australian Government recognises taxation revenue according to the tax liability method. This method provides certainty in the recording of revenue and is consistently applied in the financial statements prepared by the Australian Government under the Charter of Budget Honesty Act 1998 and the Financial Management and Accountability Act 1997 — principally the Budget, Mid-Year Economic and Fiscal Outlook, Final Budget Outcome and the Consolidated Financial Statements. Similar revenue recognition policies are also used internationally by other governments preparing consolidated accrual financial reports.

Notes to the financial statements

97

Note 1: Statement of significant accounting policies (continued)

1.27 This method is permitted under Australian Accounting Standards in circumstances when there is an ‘inability to reliably measure tax revenues when the underlying transactions or events occur’ (Australian Accounting Standard AAS31 Financial Reporting by Governments, paragraph 15.2.1). This recognition policy means that taxation revenue is generally measured at a later time than would be the case if it were measured at the time the taxation liability arose (that is, the economic transaction method).

1.28 The Australian Taxation Office (ATO) applies an alternative method, known as the economic transaction method, where taxation revenue is recognised when the Government, through the application of legislation by the ATO to taxable and other relevant activities, gains control of the future economic benefits that flow from taxes and other statutory charges. However, whilst the economic transaction method is conceptually a more accurate representation of taxation revenue, it can produce volatile estimates for some key items of taxation revenue. Companies and gross amounts for other individuals generally exhibit the highest level of volatility as they are the most difficult to estimate due to impacts of economic conditions on final taxable income for these classes of taxpayers.

1.29 If all taxation revenue had been measured in these statements according to the economic transaction method, the 2004-05 revenue would have an adjustment of $2,096 million attributable to the 2003-04 year in net terms. The 2003-04 revenue would have included an adjustment of $28 million attributable to the 2002-03 year.

1.30 The economic transaction method will continue to be assessed by relevant government agencies to determine if its adoption is appropriate across all of the Australian Government’s Budget-related forecast and outcomes documentation.

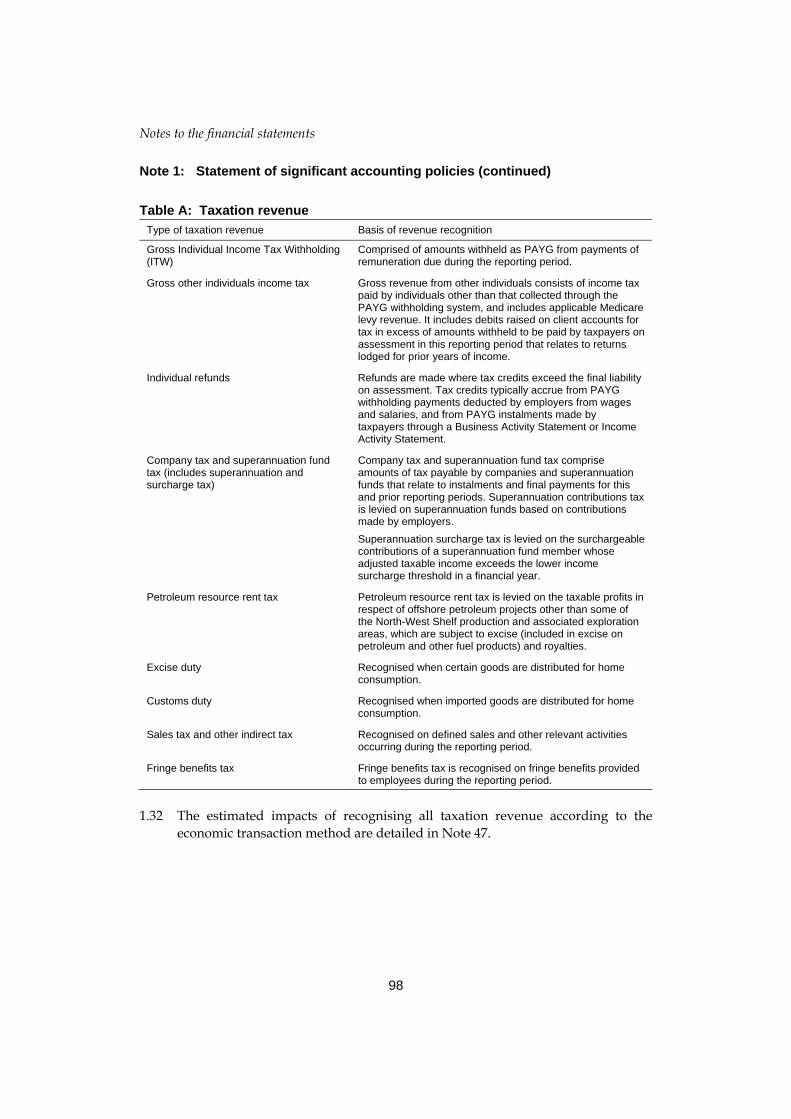

1.31 More detail on the bases of recognition for each major type of taxation revenue under this approach is provided in Table A.

Notes to the financial statements

98

Note 1: Statement of significant accounting policies (continued)

Table A: Taxation revenue Type of taxation revenue Basis of revenue recognition

Gross Individual Income Tax Withholding (ITW)

Comprised of amounts withheld as PAYG from payments of remuneration due during the reporting period.

Gross other individuals income tax Gross revenue from other individuals consists of income tax paid by individuals other than that collected through the PAYG withholding system, and includes applicable Medicare levy revenue. It includes debits raised on client accounts for tax in excess of amounts withheld to be paid by taxpayers on assessment in this reporting period that relates to returns lodged for prior years of income.

Individual refunds Refunds are made where tax credits exceed the final liability on assessment. Tax credits typically accrue from PAYG withholding payments deducted by employers from wages and salaries, and from PAYG instalments made by taxpayers through a Business Activity Statement or Income Activity Statement.

Company tax and superannuation fund tax (includes superannuation and surcharge tax)

Company tax and superannuation fund tax comprise amounts of tax payable by companies and superannuation funds that relate to instalments and final payments for this and prior reporting periods. Superannuation contributions tax is levied on superannuation funds based on contributions made by employers. Superannuation surcharge tax is levied on the surchargeable contributions of a superannuation fund member whose adjusted taxable income exceeds the lower income surcharge threshold in a financial year.

Petroleum resource rent tax Petroleum resource rent tax is levied on the taxable profits in respect of offshore petroleum projects other than some of the North-West Shelf production and associated exploration areas, which are subject to excise (included in excise on petroleum and other fuel products) and royalties.

Excise duty Recognised when certain goods are distributed for home consumption.

Customs duty Recognised when imported goods are distributed for home consumption.

Sales tax and other indirect tax Recognised on defined sales and other relevant activities occurring during the reporting period.

Fringe benefits tax Fringe benefits tax is recognised on fringe benefits provided to employees during the reporting period.

1.32 The estimated impacts of recognising all taxation revenue according to the

economic transaction method are detailed in Note 47.

Notes to the financial statements

99

Note 1: Statement of significant accounting policies (continued)

1.33 Provisions are raised for any doubtful taxation debts and any probable credit amendments, and are based on a review of outstanding accounts as at year end. This includes examination of individual large debts and disputed amounts with reference to historic collection patterns. In prior years, the ATO relied on management estimates of the collectability of debts less than $1 million in calculating the provision for bad and doubtful debts. During the 2004-05 financial year, after consultation with the Australian Government Actuary, the ATO revised its methodology for estimating the provision on this group of debts. This changed methodology has contributed in part to an increase of $1,881 million in bad and doubtful debt expenses.

1.34 Consistent with the intent of the Intergovernmental Agreement on Australian Government-State Financial Arrangements, Goods and Services Tax (GST) is collected by the Australian Government as an agent for the States and Territories, and appropriated to the States. As such, it is not shown as Australian Government revenue in this financial report. For further details on the amounts of GST collected by the States and Territories, refer Note 46.

1.35 On behalf of the States and Territories, the Australian Government imposes mirror taxes which replace State taxes in relation to Australian Government places that may be constitutionally invalid. Mirror taxes are collected and retained by the States and Territories, under the Commonwealth Places (Mirror Taxes) Act 1998. Governments bear the administration costs of collecting mirror taxes. For further details on the amounts of mirror taxes collected on behalf of the States and Territories, refer Note 46.

1.36 Expenses paid through the tax system are tax concessions that are available to beneficiaries regardless of whether or not they pay taxes. Expenses paid through the tax system include the Family Tax Benefit and Private Health Insurance Rebate. Under these schemes, recipients can be compensated in one of two ways; either as a direct payment to the recipient (or, in the case of the Private Health Insurance Rebate, the recipients health insurance fund) or through the tax system as a rebate. The compensation of recipients through a tax rebate is classified as an expense, rather than as an offset to revenue, consistent with payments made under these programmes through other delivery mechanisms. These rebates are classified as an expense as the programmes provide the same benefit to recipients, whether through tax rebate or direct benefit. The rebate is calculated independently of the normal procedure for determining a tax liability and the amount of the benefit does not depend upon the amount of tax actually paid or a taxpayer’s marginal rate of taxation.

Notes to the financial statements

100

Note 1: Statement of significant accounting policies (continued)

1.37 The Automotive Competitiveness and Investment Scheme (ACIS) provides customs duty credits to Australian automotive producers that can be used to discharge duty on imports of certain automotive products, or sold or transferred to another party. An expense and associated liability is recognised when import duty credits are issued to ACIS participants. Customs duty, representing revenue forgone, is recognised when import duty credits are redeemed.

1.38 Tax expenditures refer to tax concessions that are designed to provide a benefit to a specified activity or class of taxpayer. Tax expenditures can be delivered in a variety of ways: by a tax exemption, tax rebate, tax deduction, reduced tax rate or by deferring a tax liability. Tax expenditures constitute revenue foregone rather than an outgoing of the Australian Government.

1.39 The cost of tax expenditure schemes cannot generally be reliably measured until the underlying tax revenue item, to which the tax expenditure is applied, becomes due and payable. Therefore, tax expenditures are not separately identified in this financial report. The Australian Government Treasury issues an annual Tax Expenditures Statement (unaudited), which provides a list of tax expenditures provided by the Australian Government to individuals and businesses.

Charges for goods and services

1.40 Revenue from the sale of goods is recognised upon the delivery of goods to customers or in accordance with the sales contract.

1.41 Revenue from the rendering of a service is recognised by reference to the stage of completion of contracts or in accordance with agreements to provide services. The stage of completion is determined according to the proportion that costs incurred to date bear to the estimated total costs of the transaction.

Interest and dividends

1.42 Interest revenue is recognised on a proportional basis taking into account the interest rates applicable to the financial assets. Dividend revenue is recognised when the right to receive a dividend has been established.

Disposal of non-current assets

1.43 Revenue from disposal of non-current assets is recognised when control of the asset has passed to the buyer.

Notes to the financial statements

101

Note 1: Statement of significant accounting policies (continued)

Expenses

Depreciation and amortisation

1.44 Depreciation of non-financial physical assets (excluding inventories) is generally provided on a straight-line basis at rates based on the expected useful lives of those assets. Depreciation rate details are provided in paragraph 1.75.

1.45 Amortisation is provided on intangibles, leasehold improvements and on assets that are subject to finance leases and is calculated on a straight-line basis, generally over the useful life of the intangibles or the term of the relevant leases.

Grants

1.46 In this consolidated financial report, grants which fall under Australian Government/State funding arrangements are recognised as an expense in the reporting period in which goods and services are delivered by the grantee to intended beneficiaries.

1.47 Grant liabilities are recognised to the extent that the services required to be performed by the grantee have been performed or the grant eligibility criteria have been satisfied. A commitment is recorded when the Australian Government has a binding agreement to make the grants but services have not been performed or criteria satisfied. Where grant monies are paid in advance of performance or eligibility, prepayment is recognised.

Leases

1.48 A distinction is made between finance leases which effectively transfer from the lessor to the lessee substantially all the risks and benefits incidental to ownership of leased non-current assets, and operating leases under which the lessor effectively retains substantially all such risks and benefits.

1.49 Where a non-current asset is acquired by means of a finance lease, the asset is capitalised at the present value of the minimum lease payments at the inception of the lease and a liability recognised for the same amount. Leased assets are amortised over the period of the lease. Lease payments are allocated between the principle component and the interest expense.

Personal benefits

1.50 Personal benefits are divided into two categories: period-based and pay-day based.

1.51 Period-based personal benefits are paid in arrears following an entitlement period. Period-based personal benefits owing at the end of the financial year are included as liabilities.

Notes to the financial statements

102

Note 1: Statement of significant accounting policies (continued)

1.52 A liability is recognised for pay-day based personal benefits as they are also paid fortnightly in arrears.

1.53 The provision for doubtful debts on the recovery of personal benefits paid through the Department of Family and Community Services is based on an actuarial assessment, conducted by the Australian Government Actuary (AGA) in May 2005. The provision is based on a program based percentage applied based on the historical trends in debt recovery for each program. Overall the provision reflects 18 per cent of the total debt balance at 30 June.

1.54 In 2004-05 the accounting policy for certain subsidy and personal benefit expenses has been changed to recognise liabilities when an equitable or constructive obligation has been created. These expenses relate to the family tax benefit (FTB), first child tax offset (baby bonus), private health insurance rebate, super co-contribution, energy grants (credits) scheme, fuel sales grant scheme, FBT transitional grants scheme and certain other schemes administered by the ATO, as well as the family tax benefit administered by the Department of Family and Community Services. In previous years, these schemes were expensed when beneficiaries lodged their tax return. From 1 July 2004, assets and liabilities associated with these payments are now recognised in the year the beneficiaries became entitled to the payments. The effect of this accounting policy change in the current financial year is an increase in personal benefit expenses of $2,413 million, an increase in subsidy expenses of $1,054 million and a decrease in the operating result of $3,467 million. Furthermore, payables are increased by $3,991 million while personal benefits recoverable have increased by $524 million.

Spending against appropriation

1.55 Section 83 of the Constitution provides that no money shall be drawn down from the Treasury of the Australian Government except under appropriations made by law.

1.56 Under Section 31 of the Financial Management and Accountability Act 1997, the Minister for Finance may enter into a net appropriation agreement with an agency Minister. Appropriation Acts nos 1 and 3 (for the ordinary annual services of government) authorise the supplementation of an agency’s annual net appropriation by amounts received in accordance with its Section 31 Agreement, for example, receipts from charging for goods and services. One of the conditions which must be satisfied under Section 31 of the FMA Act in order for an annual net appropriation to be increased lawfully in this way is that the Agreement is made between the Finance Minister and the agency Minister or by officials expressly delegated (where permitted) or authorised by them. An agency’s chief executive is taken to be so authorised.

Notes to the financial statements

103

Note 1: Statement of significant accounting policies (continued)

1.57 For the following agencies that operated and recorded Section 31 monies as though a valid Section 31 agreement existed, the Section 31 agreement was subsequently found to be ineffective, in most cases as the agency and/or Finance signatory did not have express delegation or authority for signing the Agreement. Where required, agencies have entered into a new agreement with the Minister for Finance in 2004-05 to retrospectively capture all monies that were subject to an ineffective prior agreement. This variation does not validate past breaches of Section 83 of the Constitution. The agencies subject to a section 83 breach were:

• Australian Bureau of Statistics; • Australian Competition and Consumer Commission; • Australian Electoral Commission; • Australian Federal Police; • Australian Security Intelligence Organisation; • Australian Secret Intelligence Service; • Australian Transaction Reports and Analysis Centre (AUSTRAC); • Bureau of Meteorology; • Centrelink; • Department of Family and Community Services; • Department of Finance and Administration; • Department Foreign Affairs and Trade; • Department of Health and Ageing; • Department of Transport and Regional Services; • Human Rights and Equal Opportunity Commission; • Office of Film & Literature Classification; • Office of National Assessments; and • Office of the Inspector-General of Intelligence & Security.

Further details can be found in the 2004-05 financial report for the respective agencies.

Assets

Cash

1.58 For the purpose of the statement of cash flows, cash includes: cash at bank and on hand, short term deposits at call, investments in short term money market instruments, and which are used in the cash management function on a day-to-day basis, net of outstanding bank overdrafts.

Gold holdings

1.59 Gold holdings (including gold on loan to other institutions) are valued at market value at balance date.

Notes to the financial statements

104

Note 1: Statement of significant accounting policies (continued)

Government securities

1.60 The Reserve Bank of Australia values its investments in government securities at market value at balance date, except for securities held under repurchase agreements, which are valued at contract price. The Reserve Bank of Australia holds foreign government securities and domestic government securities. Australian Government domestic government securities are eliminated from this financial report on consolidation.

International Monetary Fund (IMF) quota

1.61 The IMF quota represents Australia’s membership subscription to the IMF. The investment is denominated in Special Drawing Rights and is valued at the Australian dollar equivalent.

Investments — International financial institutions

1.62 These investments represent Australia’s membership in the Asian Development Bank, the International Bank for Reconstruction and Development, the International Finance Corporation and the European Bank for Reconstruction and Development. These investments are recognised at historical cost.

Higher Education Contribution Scheme (HECS) and Student Supplement Loan Scheme

1.63 Students undertaking tertiary level studies are required to contribute towards the cost of the courses undertaken. Students may elect to pay up-front or defer the required payment. Where the payment is deferred, the amount of HECS payable by students is recorded as an asset and is recovered by the Australian Taxation Office through the PAYG income tax system when the student’s income reaches a minimum repayment threshold. Loans advanced to students under the Student Supplement Loan Scheme are recognised as an asset (receivable) and a liability.

Business undertaken on the National Interest Account

1.64 Under Part 5 of the Export Finance Insurance Corporation (EFIC) Act 1991, the Australian Government may undertake transactions which the Minister for Trade considers to be in the national interest. At 30 June 2005, the Australian Government reported National Interest receivables of $2,373.6 million (2004: $2,824 million). These receivables comprise sovereign amounts owed to the Australian Government relating to export transactions on the National Interest Account. Repayment periods for these loans vary. The Australian Government has agreed to forgive payments receivable in relation to Nicaragua and Ethiopia. Additionally, Australia has agreed to forgive 80 per cent of the Iraq debt, including late interest, with the residual 20 per cent rescheduled from 2011 to 2028. Payments from the Solomon Islands are due to recommence in 2005.

Notes to the financial statements

105

Note 1: Statement of significant accounting policies (continued)

1.65 Recoverability of National Interest loans is reviewed annually on a country by country basis based on an assessment of the likelihood of recovery including each country’s capacity to pay. Each country has acknowledged their debt to the Australian Government. In funding loans made under the National Interest provisions of the EFIC Act, the Australian Government, through EFIC, has incurred borrowings of $1,697 million (2004: $2,103 million) and derivative financial instrument payables of $98 million at 30 June 2005 (2004: $105 million).

Inventory

Held for sale or resale

1.66 Inventories held for sale or resale are recorded at cost or, when no longer required, are valued at net realisable value.

1.67 During early 2004-05, the Defence Housing Authority determined that properties acquired with the intent to sell should be accounted for as Development Properties under AASB 1019, Inventories. In previous years these properties were classified as Property, Plant and Equipment. As a result of this change in accounting policy, the consolidated operating result was increased by $26 million in 2004-05 while consolidated net assets as at 30 June 2005 has decreased by $37 million.

Not held for sale or resale

1.68 Inventories not held for sale or resale are valued at historic cost or weighted average cost. Inventory is considered obsolete or obsolescent based upon current inventory levels and expectations of contributed capability levels. Where inventory is no longer required, it is held at net realisable value.

Non-financial physical assets (excluding inventories)

1.69 Non-financial assets (excluding inventory) are stated at historical cost or valuation, except as otherwise indicated. The majority of Australian Government entities have valued these assets at fair value. Specialist military equipment is measured on the cost basis with the revalued amount of this class as at 30 June 2001 deemed to be its cost going forward. Public access communication assets are also measured at cost with the revalued amount of this class as at 30 June 2000 deemed to be their cost going forward.

1.70 Revaluations undertaken up to 30 June 2002 were completed on a deprival basis; revaluations since that date are at fair value. This change in accounting policy is required by AASB 1041 Revaluation of Non-Current Assets.

Notes to the financial statements

106

Note 1: Statement of significant accounting policies (continued)

1.71 Details pertaining to valuations can be found in the audited financial statements of individual Australian Government controlled entities, which are tabled in Parliament. During 2004-05, material revaluations occurred within the following Australian Government controlled entities:

• Australian Postal Corporation; • Australian Submarine Corporation Pty Limited; • Commonwealth Scientific and Industrial Research Organisation; • Department of Defence; • Department of Finance and Administration; • National Capital Authority; • National Archives of Australia; and • National Gallery of Australia.

1.72 The majority of the valuations were performed by the Australian Valuation Office. The valuation basis used for each class of depreciable assets are as follows:

Land Fair value or cost Buildings Fair value or cost Specialist military equipment Cost Public access communication assets Cost Other infrastructure, plant & equipment Fair value or cost Heritage and cultural assets Fair value or cost Computer software Cost Other intangibles Cost

1.73 AAS 10 Recoverable Amount of Non-Current Assets requires that the carrying

amounts of non-current assets be reviewed to determine whether they are in excess of their recoverable amounts. In assessing recoverable amounts, the relevant cash flows have been discounted to their present value.

1.74 Certain heritage assets and internally generated software have not been recognised at this time, as reliable measurement of these assets is not yet possible.

1.75 Land, being an asset with an unlimited useful life, is not depreciated. Buildings, plant and equipment are depreciated on a straight-line basis over the useful life of the asset, or over the lesser of the lease term and useful life for selected leasehold improvements. Intangible assets are amortised on a straight-line basis over their useful lives. Depreciation and amortisation rates applying to each class of depreciable assets are based on the following useful lives:

Notes to the financial statements

107

Note 1: Statement of significant accounting policies (continued)

2004-05 2003-04

Buildings(a) 2-200 years 3-200 years Specialist military equipment 2-54 years 2-54 years Public access communication assets 3-55 years 3-55 years Other infrastructure, plant & equipment 1-100 years 1-100 years Heritage and cultural assets 1-5000 years 1-825 years Computer software 2-28 years 2-33 years Other intangibles 2-20 years 3-20 years

(a) This depreciation range excludes certain leasehold improvements, which have depreciation rates of up to 50 per cent.

Liabilities

Government securities

1.76 Government securities are measured on an amortised cost basis using the effective method (or market yield at the time of issuance). Where a security is issued at a premium or discount, the premium or discount is recognised at that time and included in the book value of the liability administered on behalf of government.

1.77 For Treasury Capital Indexed Bonds, the principle value appreciates over time with the rate of inflation. As future inflation rates are not certain, an estimate of the Australian Government’s future redemption cost on maturity is not disclosed in the financial statements.

1.78 Borrowings are recognised on a gross basis, that is, they include borrowings on behalf of the State and Territory governments.

Australian currency on issue

1.79 Australian currency issued represents a liability of the Reserve Bank of Australia in favour of the holder. Currency issued for circulation, including demonetised currency, is measured at face value. When the Reserve Bank issues currency notes to the commercial banks, it receives in exchange funds equal to the full face value of the notes issued.

Superannuation

1.80 The superannuation liability represents the present value of the reporting entity’s unfunded liability to employees for past services as estimated by the actuaries of the respective superannuation plans. Additional information on superannuation is included in Notes 37 and 42.

Notes to the financial statements

108

Note 1: Statement of significant accounting policies (continued)

Employee benefits

1.81 The liability for leave and other entitlements includes provision for annual leave and long service leave. No provision has been made for sick leave as all sick leave is non-vesting and the average sick leave taken by employees is less than the annual entitlement for sick leave.

1.82 The liability for annual leave reflects the total annual leave entitlements of all employees at 30 June 2005 and is recognised at the nominal amount. The nominal amount is calculated with regard to the rates expected to be paid on settlement of the liability.

1.83 The liability for long service leave is recognised and measured at the present value of the estimated future cash flows to be made in respect of all employees at 30 June 2005. The provision is calculated using expected future increases in wages and salary rates including related on-costs and is discounted using applicable government bond rates. In determining the present value of the liability, attrition rates and pay increases through promotion and inflation have been taken into account.

Provisions

1.84 A provision is recognised when there is a legal, equitable or constructive obligation as a result of a past event and it is probable that a future sacrifice of economic benefits will be required to settle the obligation, the timing or amount of which is uncertain. If the effect is material, provisions are determined by discounting the expected future cash flows (adjusted for expected future risks) required to settle the obligation at a rate that reflects current market assessments of the time value of money and the risks specific to the liability. The unwinding of the discount is treated as part of the expense related to the particular provision.

1.85 Where some or all of the economic benefits required to settle a provision are expected to be recovered from a third party, the recovery receivable is recognised as an asset when it is probable that the recovery will be received and it is measured on a basis consistent with the measurement of the related provision. In the Statement of Financial Performance, the expense recognised in respect of a provision is presented net of the recovery. In the Statement of Financial Position, the provision is recognised net of the recovery receivable only when the Australian Government reporting entity:

• has a legally recognised right to set-off the recovery receivable and the provision; and

• intends to settle on a net basis, or to realise the asset and the liability simultaneously.

Notes to the financial statements

109

Note 1: Statement of significant accounting policies (continued)

Workers compensation — outstanding claims

1.86 This consolidated financial report includes as a provision an estimate of outstanding claims. This estimate, which is based on an assessment by an independent actuary, includes claims (whether reported or not) where the related incident occurred on or before the balance date. The actuary’s assessment has been based on current rates and costs of settlement adjusted for inflation, imputed investment return and administration expenses and includes the use of statistical information relating to the development of claims over a number of years.

The liability also includes a prudential margin or safety margin to cover the uncertainties inherent in the estimates of liability. This prudential margin for 2005 has been set at 10.6 per cent of outstanding liabilities (2004: 10.6 per cent).

Provision for outstanding benefits

1.87 The provision for the unpresented and outstanding claims provides for claims received but not assessed and claims incurred but not received. The provision is based on an actuarial assessment taking into account historical patterns of claim incident and processing. No discounting is applied to the provision due to the generally short time period between claim incidence and settlement. The provision also provides for the expected payment from Reinsurance Trust Fund in relation to the amount provided for unpresented and outstanding claims.

1.88 The provision also allows for an estimate of operating expenses to cover the cost of processing outstanding claims. Medibank Private’s policy is to reflect only the proportion of management expenses associated with the processing of benefits. The ratio at 30 June 2005 is 2.79 per cent (2004: 3.11 per cent).

Provision for HIH Claims Support Scheme

1.89 HIH Claims Support Limited (HCS) was established as a not-for-profit company to provide Australian Government funded assistance to policyholders suffering financial hardship as a result of the failure of the HIH Group Companies and the appointment on 15 March 2001, of the Provisional Liquidators of the HIH Group Companies. The HCS Trust was established in order to perform its obligations under the Commonwealth Management Agreement dated 6 July 2001. As the beneficiary of this Trust, the Australian Government is entitled to any residual balance of the Trust, after the collection of recoveries and making of payments to claimants.

Notes to the financial statements

110

Note 1: Statement of significant accounting policies (continued)

An actuarial assessment was conducted by an independent actuary as at February 2005, and the results of the review indicated that the overall cost of the scheme discounted to present value is estimated to be $800 million. This estimate incorporates an allowance for future inflation and provides for the estimated costs of both the claim handling expenses and the scheme management fees.

Following a strategic review, the scheme was closed to new applications on 27 February 2004, however, the Government has established a gateway facility for special circumstances claims. Future applications will continue to be lodged under the gateway, but at a substantially reduced level.

HIH Claims Support Limited was wound-out of the scheme by the end of August 2004, and a new claims manager commenced taking over the claims management, payment and recovery services from 1 September 2004.

The Australian Government will continue to assess the estimated liability in future years. Further assessments will also include quantifying possible recoveries to be made by the new claims manager (which will be acting as an agent of the Australian Government).

Provision for United Medical Practice/Australasian Medical Insurance Ltd (UMP/AMIL)

1.90 On 29 April 2002, the boards of United Medical Protection Limited and Australasian Medical Insurance Limited (UMP/AMIL) sought the appointment of a Provisional Liquidator. Due to the market share of medical liability coverage provided by UMP/AMIL, and to ensure adequate insurance coverage for medical practitioners, the Australian Government provided an indemnity to the Provisional Liquidator.

On 10 November 2003, the UMP Group was released from provisional liquidation by the NSW Supreme Court. As a result the indemnity provided by the Australian Government is no longer in operation. However, a number of other schemes have been introduced by the Government to ensure affordable medical indemnity cover remains available to medical practitioners. These include:

Notes to the financial statements

111

Note 1: Statement of significant accounting policies (continued)

• Claims Incurred But Not Reported (IBNR) Scheme: The Government established the IBNR Scheme to fund the unfunded incurred but not reported liabilities of certain Medical Indemnity Insurers (MIIs) through a levy on medical practitioners in those MIIs with unfunded IBNR liabilities that were declared participating members of the scheme by the Minister for Health and Ageing. An amount of $245 million (30 June 2004: $259 million) has been recognised as a liability which represents the estimated liability to the UMP Group for claims that result from incidents that have occurred prior to 30 June 2002.

• Premium Support Scheme (PSS): Under the PSS, all medical practitioners and other health professionals are supported at a rate of 80 per cent for the component of their Medical Indemnity costs that exceed 7.5 per cent of their gross private medical income. The HIC administers the scheme through the MIIs. Members of the MIIs pay their premium less the subsidy amount, and the MIIs claim a subsidy from HIC. A liability of $12.3 million (30 June 2004: $6.4 million) has been recognised for the PSS.

• High Costs Claim (HCC) Scheme: The HCC Scheme provides for the Australian Government to reimburse medical indemnity insurers half of any insurance payout over $300,000, up to the limit of a practitioner’s cover. An amount of $180 million (30 June 2004: $142.8 million) has been recognised as a liability in recognition of amounts due under the scheme to eligible insurers as at 30 June 2005.

• Exceptional Claims Scheme (ECS): The ECS assumes 100 per cent of the liability for claims (either singular or multiple) that are above the limit of a practitioner’s insurance contract limit. There has been no payments made under the scheme for 2004-05 (2003-04: nil) and actuarial data indicate that no payments are expected to be made for 2005-06, accordingly no liability has been recorded.

• UMP Support Payments Scheme: The UMP Support Payments Scheme allows for the collection of contributions from medical practitioners and other health professionals who were members of UMP as at 30 June 2000 to partially fund payments made under the IBNR Scheme. Contributions payable under the Scheme have been recognised as revenue at the date of imposition (1 May 2004).

Notes to the financial statements

112

Note 1: Statement of significant accounting policies (continued)

• Run-off Cover Scheme (ROCS): The scheme provides free run-off cover for specific groups of medical practitioners including those retired and over 65, on maternity leave, retired for more than three years, retired due to permanent disability or the estates of those who have died. The scheme is funded through the collection of support payments imposed as a tax on MII’s. ROCS commenced on 1 July 2004. Based on advice from the Australian Government Actuary, a liability of $41 million (30 June 2004: $40 million) has been recorded, representing the present value of any future claims that may be made by doctors who were eligible for ROCS at the commencement of the scheme.

Special Employee Entitlements Scheme for Ansett employees

1.91 The Special Employee Entitlement Scheme for Ansett employees was established by the Australian Government on 9 October 2001 under section 22 of the Air Passenger Ticket Levy (Collection) Act 2001 to provide a safety net arrangement for staff of the Ansett Group of companies who were terminated after 12 September 2001 due to their employer’s insolvency.

At 30 June 2005 the Australian Government has recognised a liability that reflects the obligation of the Australian Government under the scheme. Estimates of other expenses that may be payable, subject to future events such as outstanding court action in relation to the scheme, have been included in the contingent liabilities. The liability has been reduced by recoveries from the administrator of the Ansett Group which were applied to the payments under the scheme. An estimate of the potential recoveries has been disclosed as a contingent asset. The amounts payable by the Australian Government under the scheme are met through a special appropriation created under the Act.

Unfunded superannuation provision for Australian universities

1.92 Funding responsibility for universities has varied from time to time between the Australian Government and the States. A number of universities have employees or former employees who are members of state superannuation schemes which are unfunded or partly funded. In these schemes current employer contributions for benefits cover many past years of accruals of benefit rights for individual members. Accordingly, there are cost sharing arrangements for these schemes in place between the Australian Government and the States. The Australian Government makes payments to the universities which are then used to pay the required amount of employer contributions to the schemes. The Australian Government is then reimbursed by the States for their share of the costs.

Notes to the financial statements

113

Note 1: Statement of significant accounting policies (continued)

As a result of the introduction of AASB 1044 Provisions, Contingent Liabilities and Contingent Assets and UIG 51 Recovery of Unfunded Superannuation of Universities, the Australian Government recognised a provision (liability) in 2002-03. AASB 1044 requires the recognition of a provision where it is probable that a future sacrifice of economic benefit will be required and where the amount of the provision can be measured reliably. It should be noted that inclusion of a provision as a liability in the Consolidated Financial Statements does not constitute recognition of a legal obligation or policy commitment.

The Australian Government Actuary provided an estimate of the provision. The Australian Government Actuary noted that the estimates are based on figures calculated by respective State actuaries for the universities and that these calculations were at different dates and on different actuarial bases — reporting dates varied from June 2003 to December 2003.

In accordance with the generally accepted accounting principles, the statements recognise a receivable from the States as the estimated reimbursement to the Australian Government by the States. In recognition of the uncertain nature of the receivable a provision for doubtful debt against that receivable has also been recognised. The Consolidated Financial Statements include, in Note 38, a grant provision for the total unfunded superannuation liability of $2,751 million (2003-04: $2,819 million) of which the Australian Government’s share is estimated to be $2,405 million (2003-04: $2,456 million).

The Australian Government also reports, in Note 21, a receivable from the States of $646 million with an associated provision for doubtful debts of $300 million. It should be noted that a process commenced in 2002-03 under which it is intended that the Australian Government and States will assess future costs and agree upon simplified arrangements. Negotiations on improved arrangements with the States are continuing.

Claims for asbestos related diseases

1.93 A provision of $756 million (2004: $862 million) has been recognised in the financial statements in respect of the Australian Government’s estimated potential liability for asbestos related disease (ARD) claims. The provision is based on an independent actuarial assessment as at 30 June 2005 and is discounted to present value at rates consistent with market yields on long-term Commonwealth bonds. The provision represents the best estimate of the Australian Government’s exposure, consistent with the requirements of AASB 1044 Provisions, Contingent Assets and Contingent Liabilities.

Notes to the financial statements

114

Note 1: Statement of significant accounting policies (continued)

The provision includes an allowance for the Australian Government’s ARD defendant legal costs and other direct expenses and is shown gross of cross-claim recoveries from third parties. A receivable has also been recognised in relation to third-party recoveries but has been fully provided for until more reliable information is available on the collectability of third-party recoverables. As such, a contingent asset has also been recorded in the Schedule of Contingent Liabilities and Contingent Assets.

Reserves

Asset revaluation

1.94 The asset revaluation reserve includes the net revaluation increments and decrements arising from the revaluation of non-current assets in accordance with AAS 1041 Revaluation of Non-current Assets.

Foreign currency reserve

1.95 The foreign currency translation reserve records the foreign currency differences arising from the translation of self-sustaining foreign operations.

Investments reserve

1.96 The investments reserve records the Australian Government’s interest in the net assets of portfolio agencies and companies, excluding Departments of State, as at 30 June 1997 (subject to subsequent changes in ownership interest). The date of 30 June 1997 represents the deemed acquisition date to facilitate consolidated financial reporting.

Statutory funds

1.97 The statutory funds reserve comprises amounts set aside out of profits under a specific Act or Statute.

Other reserves

1.98 Other reserves include amounts set aside out of profits for purposes other than those detailed above, including general reserves.

Financial instruments

1.99 Accounting policies in relation to financial instruments are disclosed in Note 40.

Commitments

1.100 Commitments are obligations or undertakings to make future payments to other entities that exist at the end of the reporting period and have not been recognised as liabilities in the Statement of Financial Position.

Notes to the financial statements

115

Note 1: Statement of significant accounting policies (continued)

Contingent liabilities and contingent assets

1.101 In this consolidated financial report contingent liabilities are possible liabilities that arise from past events, the existence of which will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the Australian Government.

1.102 In this consolidated financial report contingent assets are possible assets that arise from past events, the existence of which will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the Australian Government.

Asset sales programme

1.103 Amounts disclosed in Note 12 include assets sold by the Australian Government through its asset sales programme. These assets typically comprise the sale of Australian Government controlled entities or significant assets of those entities.

Borrowing costs

1.104 AAS 34 Borrowing Costs requires borrowing costs that are directly attributable to the acquisition, construction or production of a qualifying asset to be capitalised as part of the cost of the asset. In this regard, specific borrowing costs of $90 million incurred in 2004-05 (2003-04: $74 million) are directly attributable to expenditure on qualifying assets and have been capitalised as part of the carrying amount of non-financial physical assets (excluding inventories).

1.105 To the extent that funds have been borrowed generally by the Australian Office of Financial Management as part of the Australian Government’s debt management strategy, these borrowing costs have not been applied to other general government entities’ qualifying assets.

Insurance

1.106 Australian Government entities operating in the general government sector are members of the Australian Government’s self managed fund for insurable risks, Comcover. This excludes workers compensation where the risk continues to be managed by Comcare. Australian Government entities operating outside the general government sector adopt their own insurance strategies, which includes both self-insurance and commercial insurance coverage.

Rounding

1.107 All amounts in this consolidated financial report have been rounded to the nearest million dollars, unless otherwise noted.

Notes to the financial statements

116

Note 1: Statement of significant accounting policies (continued)

Current year figures and comparative figures

1.108 Comparative figures have been adjusted to conform to changes in presentation in these financial statements where required.

Balance dates

1.109 Most entities controlled by the Australian Government have 30 June balance dates. Where entities have balance dates other than 30 June they are incorporated into this financial report as at their latest balance date. This approach has not materially affected the revenues and expenses to 30 June 2005 or the assets and liabilities reported as at 30 June 2005.

Materiality

1.110 AAS 5 Materiality states that an item or an aggregate of items is required to be recognised, measured or disclosed in a financial report where its omission, misstatement or non-disclosure could affect either resource allocation decisions by users of the report, or the discharge of accountability by management or the governing body of an entity. It also provides guidance as to quantitative thresholds for determining the materiality of a particular item or aggregate of items. These financial statements are compiled having regard to AAS 5. This includes consistent application between the Consolidated Financial Statements and the Final Budget Outcome.

Audit of Australian Government controlled entities

1.111 This financial report is consolidated from audited financial statements of Australian Government entities, with the exception of the following Australian Government controlled entities and other investments, for which financial statements are not yet finalised. Nevertheless, the financial statements in this report include the financial results for these entities as at the time of publication. Final 2004-05 audited financial statements for these entities will be included in their respective annual reports. The following entities had not finalised their audited financial statements for the 2004-05 reporting period as at 2 December 2005:

• IIF Investments Pty Ltd; • IIF (CM) Investments Pty Ltd; • IIF Bioventures Pty Ltd; • IIF Newport Pty Ltd; • IIF Foundation Pty Ltd; • Army and Airforce Canteen Service; • Billioara Pty Ltd; • Billioara Unit Trust; • Bowen Basin Holdings Pty Ltd;

Notes to the financial statements

117

Note 1: Statement of significant accounting policies (continued)

• Bowen Basin Holdings Trust; • Bowen Basin Investments Pty Ltd; • Bowen Basin Investments Trust; • Aboriginal and Torres Strait Islander Educational and Cultural Advancement

Account; • Aboriginal and Torres Strait Islander Services; and • Australian Technology Group Pty Ltd.

Note 2: Adoption of Australian Equivalents to International Financial Reporting Standards to apply from the first reporting period beginning on or after 1 January 2005

2.1 The Australian Accounting Standards Board has issued Australian Accounting Standards to apply from the first reporting period beginning on or after 1 January 2005. The new standards are the Australian Equivalents to International Financial Reporting Standards (AEIFRS). The standards being replaced are to be withdrawn with effect from 2005-06, but continue to apply in the meantime, including reporting periods ending on 30 June 2005. The new standards cannot be adopted early.

2.2 For-profit entities complying with AEIFRS will be able to make an explicit and unreserved statement of compliance with International Financial Reporting Standards (IFRS) as well as a statement that the financial report has been prepared in accordance with Australian Accounting Standards.

2.3 AEIFRS contain certain additional provisions that will apply to not-for-profit entities, including Australian Government agencies. Some of these provisions are in conflict with IFRS, and therefore the Australian Government will only be able to assert that the financial report has been prepared in accordance with Australian Accounting Standards.

2.4 AASB 1047 Disclosing the Impacts of Adopting Australian Equivalents to International Financial Reporting Standards requires entities to disclose, in respect of annual or interim reporting periods ending on or after 30 June 2005:

(a) an explanation of how the transition to AEIFRS is being managed;

(b) a narrative explanation of the key differences in accounting policies arising from adopting AEIFRS;

(c) any known or reliably estimable information about the impacts on the financial report had it been prepared using AEIFRS; and

Notes to the financial statements

118

Note 2: Adoption of Australian Equivalents to International Financial Reporting Standards to apply from the first reporting period beginning on or after 1 January 2005 (continued)

(d) if the impacts of the above are not known or reliably estimable, a statement to that effect.

2.5 The following disclosures address these requirements.

Management of transition to AEIFRS

2.6 The Australian Government has dedicated significant resources to manage the successful implementation of AEIFRS.

2.7 Under the Financial Management and Accountability Act 1997 and the Commonwealth Authorities and Companies Act 1997, each wholly-owned entity is responsible for ensuring their financial reports comply with Finance Minister’s Orders (FMOs) made under these Acts, which also requires compliance with Australian Accounting Standards. To this end, each entity has undertaken steps to prepare for the adoption of AEIFRS as applicable to that entity. The transition plan adopted by each entity was disclosed in their 2003-04 and 2004-05 financial reports.

2.8 At a whole of government level, the Australian Government (through the Department of Finance and Administration) has provided resources to assess the impacts of AEIFRS, and provided advice to Australian Government entities and the Australian Government on transitional planning issues, the impacts of AEIFRS and policy guidance. This has included:

• The release of a number of FinanceBriefs relating to the adoption of AEIFRS to assist controlled entities in the implementation of AEIFRS;

• Finance providing regular updates to keep Chief Financial Officers (CFOs) of Australian Government entities informed on progress and issues relating to international adoption. Furthermore, Finance set up a consultative group of a cross-section of CFOs to discuss practical implementation issues and areas of concern regarding interpretation between the entities and auditors;

• The preparation of revised accounting policies to take effect from 1 July 2005, with retrospective restatement of comparative information, included as guidance in the 2004-05 FMOs. The accounting policies of controlled entities have been reviewed, taking into account AEIFRS and relevant FinanceBriefs issued by Finance; and

Notes to the financial statements

119

Note 2: Adoption of Australian Equivalents to International Financial Reporting Standards to apply from the first reporting period beginning on or after 1 January 2005 (continued)

• In relation to the Consolidated Financial Statements, the following key steps have been undertaken by Finance:

– Identification of major accounting policy differences between current AASB standards and AEIFRS (which are detailed in FinanceBriefs and the 2004-05 FMOs);

– Implementation of system changes necessary to capture agency data under AEIFRS;

– The collection of agency AEIFRS adjustments for the production of AEIFRS compliant financial statements on an agency basis; and

– Preparation of an AEIFRS compliant balance sheet as at 30 June 2005 during the 2004-2005 Consolidated Financial Statements process.

2.9 Australian Government entities have reviewed AASB pending standards as they were placed on the AASB web site. Issues relevant to the Australian Government were identified and an assessment made on the need for specialist advice. A number of Australian Government entities have sought specialist advice on the implications of AEIFRS.

2.10 The accounting policies of controlled entities of the Australian Government have been reviewed, taking into account AEIFRS and relevant FinanceBriefs issued by Finance. Revised accounting policies to take effect from 1 July 2005, with retrospective restatement of comparative information, have been endorsed by Finance and included as guidance in the 2004-05 FMOs.

2.11 Key financial management staff have been trained in AEIFRS.

2.12 System changes necessary to capture agency AEIFRS information and prepare consolidated financial reports and budgeted statements under the AEIFRS were completed in July 2005. This included the testing and implementation of those changes.

2.13 Consultants were engaged where necessary to assist with each of the above steps.

Notes to the financial statements

120

Note 2: Adoption of Australian Equivalents to International Financial Reporting Standards to apply from the first reporting period beginning on or after 1 January 2005 (continued)

Expected key differences in accounting policies

2.14 The Australian Government believes that the first financial report prepared under AEIFRS (at 30 June 2006) will be prepared on the basis that the Australian Government will be a first time adopter under AASB 1, First time Adoption of Australian Equivalents to International Financial Reporting Standards. Changes in accounting policies under AEIFRS are applied retrospectively that is as if the new policy had always applied except in relation to the exemptions available and prohibitions under AASB 1. This means that an AEIFRS compliant balance sheet has to be prepared as at 1 July 2004. This will enable the 2005-06 financial statements to report comparatives under AEIFRS.

2.15 The following represents the material estimated impacts and movements in these financial statements as if prepared under AEIFRS. Whilst it should not be taken as an exhaustive list of all the differences between current Australian Accounting Standards and AEIFRS, it does represent the major expected changes. Final decisions on the accounting policies to be applied will be made by the Minister for Finance in the preparation of the FMOs for 2005-06.

2.16 These impacts do not include those relating to the Department of Defence, with the exception of AASB 119 Employee Benefits, as reliable estimates were not available for the preparation of the Consolidated Financial Statements for 2004-05. The key areas where Defence’s accounting policies are expected to change include AASB 116 Property, Plant and Equipment, AASB 136 Impairment of Assets, AASB 102 Inventories, AASB 119 Employee Benefits, AASB 139 Financial Instruments: Recognition and Measurement, and AASB 138 Intangible Assets.

2.17 The quantitative impacts of AEIFRS represent Australian Government entities’ best estimates of the impacts of the changes as at reporting date. The actual effects of the impacts of AEIFRS may differ from these estimates due to:

• continuing review of the impacts of AEIFRS on Australian Government entities’ operations;

• ongoing amendments to the AEIFRS and AEIFRS Interpretations;

• the issuing of new Standards and Interpretations; and

• emerging interpretation as to the accepted practice in the application of AEIFRS and the AEIFRS Interpretations.

Notes to the financial statements

121

Note 2: Adoption of Australian Equivalents to International Financial Reporting Standards to apply from the first reporting period beginning on or after 1 January 2005 (continued)

2.18 The anticipated impacts are largely the result of applying AASB 116 Property, Plant and Equipment, AASB 138 Intangible Assets, AASB 5 Non-Current Assets Held for Sale and Discontinued Operations, AASB 102 Inventories, AASB 119 Employee Benefits, AASB 139 Financial Instruments: Recognition and Measurement, AASB 140 Investment Properties, AASB 123 Borrowing Costs, AASB 108 Changes in Accounting Policies, Changes in Accounting Estimates and Errors, AASB 2 Share-Based Payment, AASB 3 Business Combinations, AASB 128 Investments in Associates and AASB 131 Interests in Joint Ventures.

Property, plant & equipment

2.19 In anticipation of the AASB 116 Property, Plant and Equipment requirement that property, plant and equipment assets be measured at fair value or historical cost, Australian Government entities have been advised that all property, plant and equipment assets, other than public access communication assets, should be recorded at fair value in the opening balance sheet prepared as at 1 July 2004.

2.20 AASB 116 requires that the present value of an obligation to decommission an asset and/or restore the site be recognised as part of the cost of the asset and as a liability, where the obligation qualifies for recognition as a provision under AASB 137 Provisions, Contingent Liabilities and Contingent Assets.

2.21 The expected impact of the above changes on fair value gains and losses, depreciation, borrowing costs and suppliers expenses resulting from applying AASB 116 is a reduction in the operating result of $29 million. Provisions are expected to increase by $37 million (2004: $8 million), and the asset revaluation reserve is expected to increase by $239 million (2004: $239 million). The expected impact on land and buildings, infrastructure, plant and equipment is not material.

Intangible assets

2.22 Intangible assets are currently measured on the cost basis under AASB 1041 Revaluation of Non-Current Assets. However, the carrying amounts of some of these assets include amounts arising from revaluations in the years before the cost basis was adopted.

2.23 AASB 138 Intangible Assets does not permit intangibles to be measured at valuation unless there is an active market for the intangible. Most intangibles held by Australian Government entities are not traded in active markets. Accordingly, where intangibles are recorded at valuation, Australian Government entities will derecognise the valuation component of the carrying amount of these assets on adoption of the AEIFRS.

Notes to the financial statements

122

2.24 The expected impact of applying AASB 138 is a reduction in intangible assets of $60 million (2004: -$76 million), a reduction in the asset revaluation reserve of $20 million (2004: -$20 million), and an increase in the operating result of $16 million.

2.25 Overall intangible assets are expected to increase by $3,094 million (2004: $2,741 million) due to a reclassification of $3,154 million (2004: $2,817 million) from other non-financial assets following a review of the classification of Telstra’s software assets developed for internal use and deferred expenditure to ensure the criteria of AASB 138 are met.

Non-Current assets held for sale

2.26 Under AASB 5 Non-Current Assets Held for Sale and Discontinued Operations, assets that meet the ‘held for sale’ criteria under that Standard will be measured at the lower of their carrying amount and their fair value less costs to sell. Assets will cease to be depreciated while they are held for sale.

2.27 Proceeds from the disposal of non-current assets are currently recognised as revenue and the carrying amounts of the asset disposed of are recognised as an expense. Under AEIFRS, the net of these amounts will be recognised as a net gain or loss in the Income Statement.

2.28 The expected impact of applying AASB 5 is to reduce land and buildings, infrastructure, plant and equipment by $111 million (2004: -$161 million) and recognise assets held for sale of $113 million (2004: $161 million). The asset revaluation reserve at 30 June 2005 is not expected to change (2004: -$44 million). The operating result is expected to increase by $2 million following a reduction in depreciation and amortisation of $1 million and a reduction in the value of assets sold of $1 million.

Inventory

2.29 Under AASB 102 Inventories, inventories held for distribution by not-for-profit entities will be measured at the lower of cost and current replacement cost.

2.30 The expected impact of adopting AASB 102 is a reduction in inventories of $5 million (2004: -$6 million), and an increase in the operating result of $1 million due to the recognition of a fair value gain.

Notes to the financial statements

123

Note 2: Adoption of Australian Equivalents to International Financial Reporting Standards to apply from the first reporting period beginning on or after 1 January 2005 (continued)

Employee benefits

2.31 Under current AASB 1028 Employee Benefits, wages and salaries, annual leave and sick leave must be measured at their nominal amounts, regardless of whether they are expected to be settled within twelve months of reporting date. The provision for long service leave is measured at the present value of estimated future cash outflows. Under the new AASB 119 Employee Benefits standard, all non-current employee entitlements, including non-current annual leave entitlements, must be discounted to their present value using the market yield on Australian Government bonds.

2.32 The expected impact on employee provisions of applying the AASB 119 requirement to discount non-current annual leave entitlements is a decrease of $14 million (2004: $13 million). The operating result is expected to increase following a reduction in employee expenses of $1 million.

2.33 On adoption of AEIFRS, AASB 119 requires the Australian Government to recognise the net position of each superannuation scheme as a transitional adjustment in the balance sheet, with a corresponding entry to retained profits. The transitional adjustment is based on an actuarial valuation of each scheme at transition date determined in accordance with AASB 119. Under current AGAAP, an asset or liability is not recognised in the statement of financial position for the net position of the defined benefit schemes that Telstra sponsors in Australia and Hong Kong.

2.34 AASB 119 also requires that the defined benefit obligation is discounted using the government bond rate, rather than the expected rate of return on plan assets, thus increasing the unfunded superannuation liability.

2.35 These adjustments will result in a $1,007 million (2004: $1,274 million) defined benefit pension asset for superannuation schemes sponsored by certain public financial corporations and public non-financial corporations, primarily Telstra, Australia Post and the Reserve Bank of Australia, a decrease in employee provisions of $2 million (2004: -$15 million), the recognition of land and buildings, infrastructure, plant and equipment of $24 million (2004: $0 million) and a reduction in the operating result following an increase in depreciation expenses of $2 million.

Notes to the financial statements

124

Note 2: Adoption of Australian Equivalents to International Financial Reporting Standards to apply from the first reporting period beginning on or after 1 January 2005 (continued)

2.36 In respect of the superannuation liability for the Commonwealth Superannuation Scheme, the Public Sector Superannuation Scheme, the Parliamentary Contributory Superannuation Scheme, the Defence Force Retirement and Death Benefits Scheme and the Military Superannuation and Benefits Scheme, AASB 119 requires expected future benefits to be discounted to their present value using the market yield on Australian Government bonds. Given the significant long-term nature of the superannuation liabilities (up to 40 years), and the yield on bonds only extends to 10 years, there are differing interpretations of the application of the requirements of AASB 119. Consequently, the Australian Heads of Treasuries has referred this issue to its Accounting and Reporting Advisory Committee (HoTARAC) for review and recommendations. The review has commenced, with a possible outcome being a referral to the Australian Accounting Standards Board for formal interpretation. Until the review is complete, a reliable estimate of the total impact cannot be determined. Recent actuarial assessments for these schemes indicate a $1,500 million increase in the Australian Government’s unfunded liability assuming no change in the rate used to discount the liability to its present value. The actuarially estimated impacts of changing the discount rate from the existing investment return rate of 6.0 per cent to a rate based on the market yield of Australian Government bonds (5.2 per cent at 30 June 2005) would be to increase the liability by a further $11,500 million, which would result in a total adjustment of $13,000 million at 30 June 2005.

2.37 The Australian Government has elected to early adopt the revised AASB 119. This revised version permits a number of options for recognising actuarial gains and losses on an ongoing basis. The Australian Government has elected to apply the option to recognise actuarial gains and losses directly in accumulated results, which is expected to increase the 2004-05 operating result by $785 million. Other components of superannuation costs will be recognised in the income statement.

Financial instruments

2.38 As required by AASB 139 Financial Instruments: Recognition and Measurement, financial assets and liabilities held for trading will be measured at fair value, with movements in fair value recognised in the operating result. Financial assets and liabilities for which an active market exists are expected to be designated as held at fair value through the operating result or as available-for-sale. Other loans and receivables are expected to continue to be measured at amortised cost. Derivative financial instruments will be recognised in the balance sheet at their fair value.

Notes to the financial statements

125

Note 2: Adoption of Australian Equivalents to International Financial Reporting Standards to apply from the first reporting period beginning on or after 1 January 2005 (continued)

2.39 Financial assets, except those classified as ‘held at fair value through profit and loss’, will be subject to impairment testing.

2.40 The Australian Government is required to comply with AASB 132/139 from 1 July 2005. An exemption is available under AASB 1 such that comparative information does not need to be restated under these standards. The Australian Government has elected to apply the exemption and accordingly, there will be no impact on the 30 June 2005 financial statements.

Borrowing costs

2.41 The benchmark treatment required under AEIFRS is to expense borrowing costs, however, AASB 123 Borrowing Costs does allow the alternative treatment of capitalising these costs where they relate to qualifying assets.

2.42 It is intended that the Australian Government, through the Finance Minister’s Orders, will elect to expense all borrowing costs.

2.43 The expected impact will be to decrease property, plant and equipment by $457 million (2004: -$459 million) and decrease the asset revaluation reserve by $3 million (2004: -$3 million). The operating result for the year ended 30 June 2005 is expected to increase $2 million due to an increase in borrowing costs of $91 million and a decrease in depreciation of $93 million.

Investment property