north dakota petroleum council - ndoil.org€¢explore for, produce, transport and market...

TRANSCRIPT

Oil & Gas Market Perspectives

Helen Currie, Chief EconomistSeptember 28, 2017

North Dakota Petroleum Council

Cautionary Statement

The following presentation includes forward-looking statements. These statements relate to future events, such as anticipated revenues, earnings, business strategies, competitive position or other aspects of our operations, operating results or the industries or markets in which we operate or participate in general. Actual outcomes and results may differ materially from what is expressed or forecast in such forward-looking statements. These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions that may prove to be incorrect and are difficult to predict such as our ability to complete the sale of our announced dispositions on the timeline currently anticipated, if at all; the possibility that regulatory approvals for our announced dispositions will not be received on a timely basis, if at all, or that such approvals may require modification to the terms of of our announced dispositions or our remaining business; business disruptions during or following the sale of our announced dispositions, including the diversion of management time and attention; our ability to liquidate the common stock issued to us by Cenovus Energy Inc. as part of our sale of assets in western Canada at prices we deem acceptable, or at all; the ability to deploy net proceeds from our announced dispositions in the manner and timeframe we currently anticipate, if at all; operational hazards and drilling risks; potential failure to achieve, and potential delays in achieving expected reserves or production levels from existing and future oil and gas development projects; unsuccessful exploratory activities; unexpected cost increases or technical difficulties in constructing, maintaining or modifying company facilities; international monetary conditions and exchange controls; potential liability for remedial actions under existing or future environmental regulations or from pending or future litigation; limited access to capital or significantly higher cost of capital related to illiquidity or uncertainty in the domestic or international financial markets; general domestic and international economic and political conditions, and changes in tax, environmental and other laws applicable to ConocoPhillips’ business; and other economic, business, competitive and/or regulatory factors affecting ConocoPhillips’ business generally as set forth in ConocoPhillips’ filings with the Securities and Exchange Commission (SEC). We caution you not to place undue reliance on our forward-looking statements, which are only as of the date of this presentation or as otherwise indicated, and we expressly disclaim any responsibility for updating such information

2

• Explore for, produce, transport and market hydrocarbons, including crude oil, natural gas, natural gas liquids (NGL), liquefied natural gas (LNG) and bitumen

• Operations and activities in 17 countries

• Exploration in 12 countries

• Production in 11 countries

• 12,200 employees worldwide

• Six operating segments

• Alaska

• Lower 48

• Canada

• Europe and North Africa

• Asia Pacific and Middle East

• Other International

Company Profile As of June 30, 2017

17COUNTRIES WITH OPERATIONS AND ACTIVITIES

HOUSTON, TXCOMPANY HEADQUARTERS

COPNYSE TICKER

12,200EMPLOYEES WORLDWIDE

3 Information in this presentation does not reflect the impacts of the Canadian transaction announced on March 29, 2017, or the San Juan Basin transaction announced on April 13, 2017.

Highly Differentiated, Diverse Portfolio

4

1 Largest independent E&P by production and proved reserves. Full year 2017 estimated production is on a pro-forma basis as if announced transactions were completed on Jan. 1, 2017 and excludes Libya.2 Cost of Supply (CoS) is the Brent equivalent price that generates a 10 percent return on a point forward and fully-burdened basis. Resources are post announced transactions.3Assumes closing Barnett and Panhandle transaction.4Burden = capital infrastructure + foreign exchange + price-related inflation + G&A.

<$50/BBL Cost of Supply Resource3

(Fully Burdened)

ConocoPhillips in the Bakken, As of June 30, 2017

Average Daily Net Production, 2016

5

6

Crude Oil Market Outlook

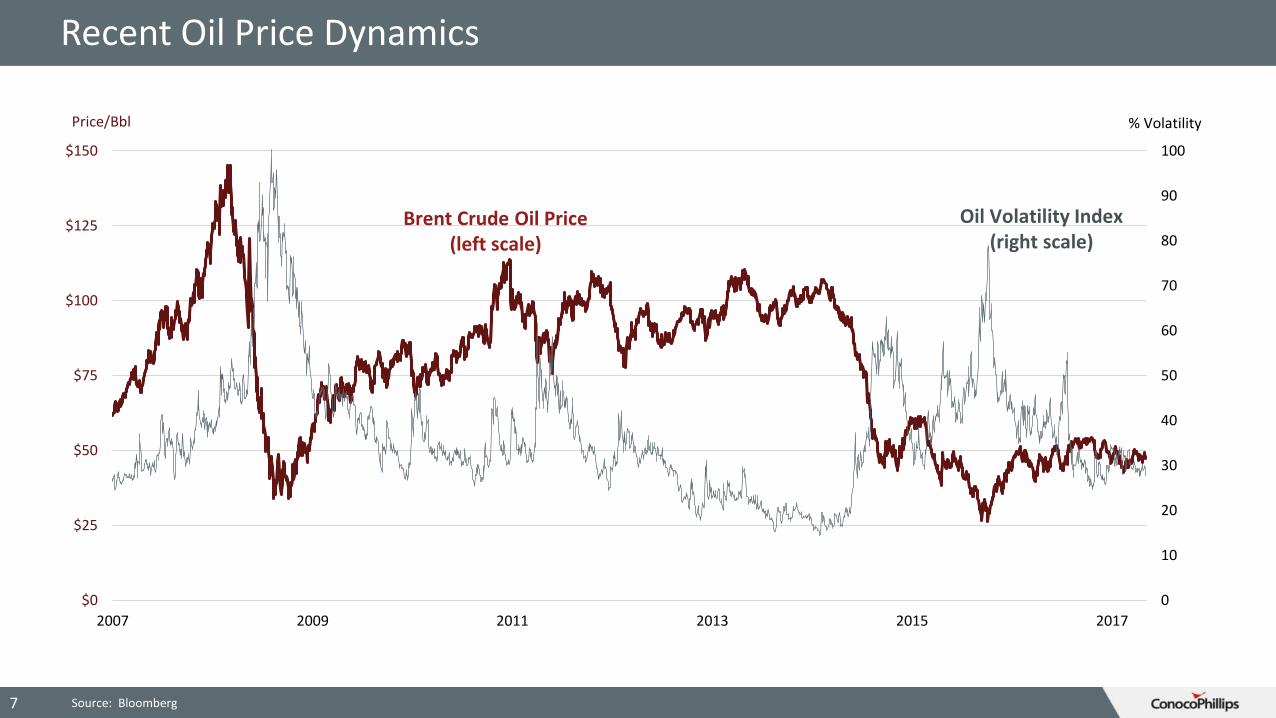

Recent Oil Price Dynamics

0

10

20

30

40

50

60

70

80

90

100

$0

$25

$50

$75

$100

$125

$150

2007 2009 2011 2013 2015 2017

Brent Crude Oil Price(left scale)

Oil Volatility Index(right scale)

Price/Bbl % Volatility

7 Source: Bloomberg

Macroeconomic Environment

8

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Global Economic Activity is Turning Out Better Than Expected at Start of 2017

Real Global GDP Growth %

Cyclical Upturn in Global Trade (20%)

Anti-trade policies diminish global

growth (8%)

Base Case (50%)

Source: Oxford Economics for GDP (using real US$ at PPP exchange rates); Bloomberg for FX

75

80

85

90

95

100

105

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17

U.S. Dollar Weakening in 2017 vs Major Currencies(DXY Spot Index)

Wea

ker

USD

Stro

nge

r U

SD

80

85

90

95

100

105

Q4 17 2018 2019 2020

Range Median Forecast

Consensus View on U.S. Dollar(DXY Spot Index)

Could see more USD weakness as U.S. FRB is slower to curtail

QE vs other central banks

More upside (strength) to USD as U.S. FRB normalizes

interest rates

Stronger Global GDP Growth + Weaker USD Should Support Oil and Gas Demand Growth

Market Rebalancing is Taking Longer Than Expected

9

0

1

2

3

4

Iran Syria Iraq

Libya Yemen Neutral Zone

Nigeria Venezuela Sudan

Supply Disruptions Fell in 2016 and 2017MMBD

Vienna Agreement Cuts Partly Offset by Return of Disrupted Supplies

49.9347.66 47.95 47.62 47.65 47.60 47.82 47.85

0

5

10

15

20

25

30

35

40

45

50

55

Baseline January Feb March April May June July

Monthly Output By Vienna Members Remains Below the Agreement Supply Baseline

Saudi Iraq Rest of OPEC Russia Rest of Non-OPEC

MMBD

Rest of OPEC includes Equatorial Guinea

Source: International Energy Administration, industry consultants Source: PIRA Energy Group

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$0 $20 $40 $60 $80 $100 $120

Fisc

al B

reak

-Eve

n P

rice

s ($

/bb

l)

Current Account Break-Even Prices ($/bbl)

Most OPEC Countries + Russia 2018 Breakeven Prices Are Above Average Market Prices

Venezuela

Nigeria

Algeria

LibyaQatarAngola

SaudiEcuador

Kuwait

Iran

Iraq

UAE

Russia

OPEC & Russia Breakeven Prices

• Austerity measures have not been enough to cut Fiscal B/E below $60

• Forex reserves and sovereign wealth funds enable countries to go longer with Current Account deficits

• Financial instability may threaten several countries (e.g. Venezuela, Libya and Algeria)

10

Insufficient revenue from oil to balance current account or domestic

budget

2018 Brent futures price

Insufficient revenue from oil to balance domestic budget

Insufficient revenue from oil to balance

current account

Source: Breakeven prices from IHS Markit -- The use of this content was authorized in advance by IHS Markit. Any further use or redistribution of this content is strictly prohibited without written permission by IHS. All rights reserved.

(2.0)

(1.5)

(1.0)

(0.5)

0.0

0.5

1.0

1.5

2.0

94

95

96

97

98

99

100

101

102

2015 2016 2017 2018 2019 2020

Inventory Change (right axis)

Supply (left axis)

Demand (left axis)

Global Oil Supply and Demand Balance (MMBD)

1111 Source: COP, Energy Aspects. Non-OPEC/Other supply includes NGL’s, including OPEC’s, biofuels and refinery process gain

Global Rebalancing

Global oil demand has responded positively to low oil prices

Ongoing risks to oil demand growth

▪ Decelerating global economyo Anti-trade policies

▪ Strong U.S. dollar weakens demand response outside U.S.

▪ Removal of subsidies in many developing countries hurts demand when oil prices recover

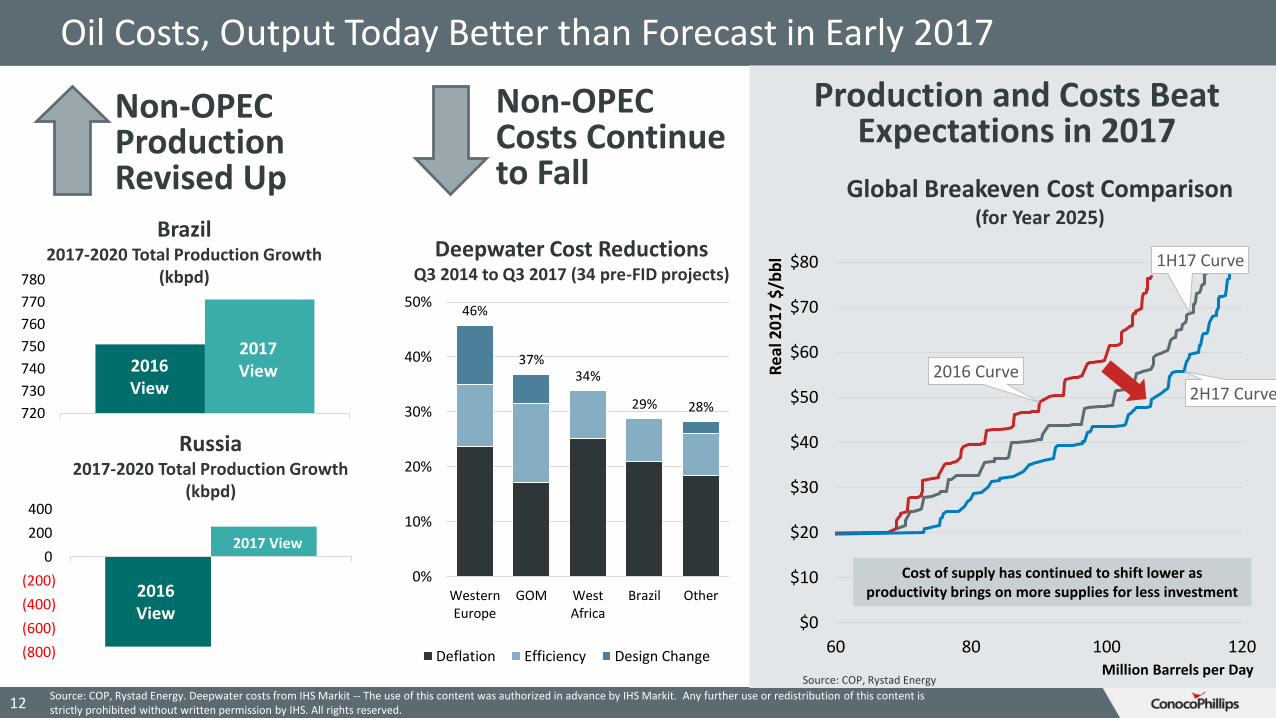

Oil Costs, Output Today Better than Forecast in Early 2017

12

1H17 Curve

2016 Curve2H17 Curve

$0

$10

$20

$30

$40

$50

$60

$70

$80

60 80 100 120

Global Breakeven Cost Comparison (for Year 2025)

Million Barrels per Day

Cost of supply has continued to shift lower as productivity brings on more supplies for less investment

Re

al 2

01

7 $

/bb

l

Source: COP, Rystad Energy. Deepwater costs from IHS Markit -- The use of this content was authorized in advance by IHS Markit. Any further use or redistribution of this content is strictly prohibited without written permission by IHS. All rights reserved.

(800)

(600)

(400)

(200)

0

200

400

2017 View

2016 View

720

730

740

750

760

770

780

2017 View2016

View

Russia2017-2020 Total Production Growth

(kbpd)

Non-OPEC Production Revised Up

46%

37%34%

29% 28%

0%

10%

20%

30%

40%

50%

WesternEurope

GOM WestAfrica

Brazil Other

Deflation Efficiency Design Change

Non-OPEC Costs Continue to Fall

Deepwater Cost Reductions Q3 2014 to Q3 2017 (34 pre-FID projects)

Brazil2017-2020 Total Production Growth

(kbpd)

Production and Costs Beat Expectations in 2017

Source: COP, Rystad Energy

U.S. Oil Production Rebounding in 2017

0

1

2

3

4

5

6

7

8

9

10

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

L48 Onshore

AK

GoM

Million Barrels per Day

U.S. Oil Production

13 Source: U.S. Energy Information Administration

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Million Barrels per Day

Tight Oil Production

Permian

Eagle Ford

Bakken

U.S. Tight Oil Improved Through 2015-2017 Price Downturn

14

0

200

400

600

800

1,000

1,200

2010 2011 2012 2013 2014 2015 2016 2017

Source: WoodMackenzie NAWAT

Average Horizontal Drilling Speed (ft/day)

0

200

400

600

800

1,000

1,200

2010 2011 2012 2013 2014 2015 2016 2017

Average Horizontal Oil IP Rate (barrels/day)

0

5

10

15

20

25

30

35

40

45

2010 2011 2012 2013 2014 2015 2016 2017

Average Horizontal Fracture Stages (number of stages)

LARGER FRACS FASTER DRILLING BIGGER WELLS

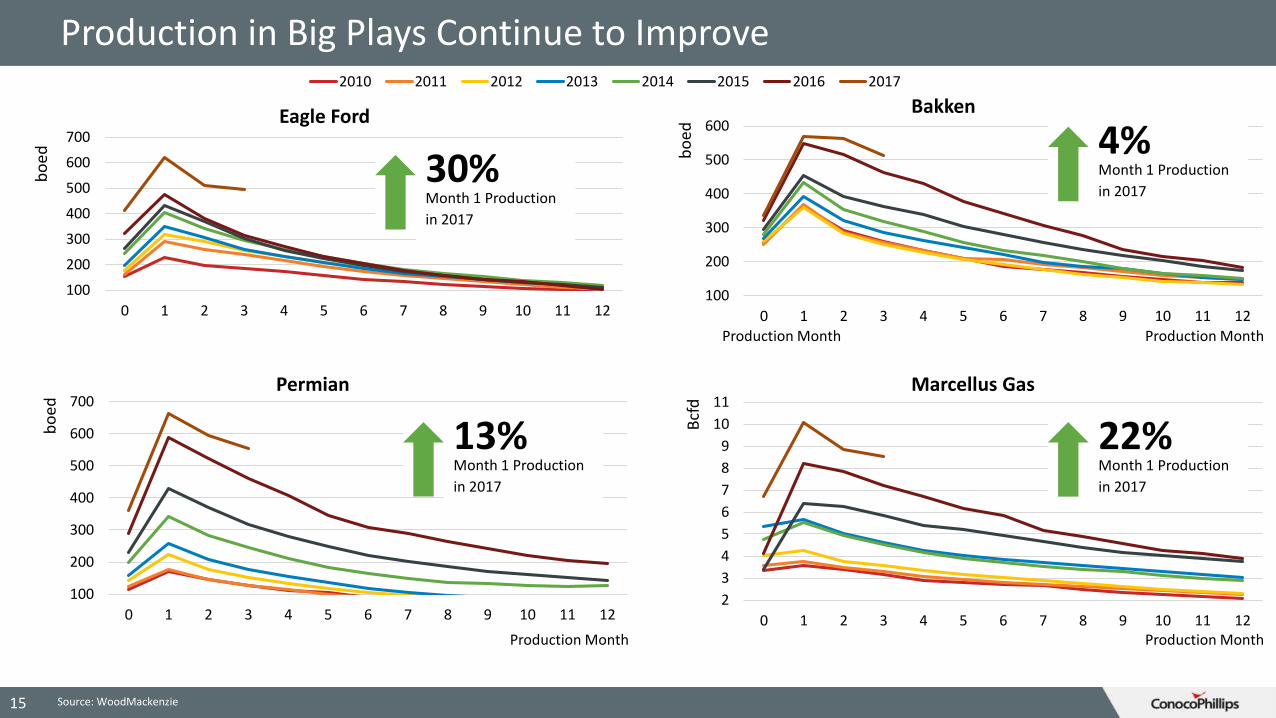

Production in Big Plays Continue to Improve

15

100

200

300

400

500

600

700

0 1 2 3 4 5 6 7 8 9 10 11 12

bo

ed

Production Month

Eagle Ford

2010 2011 2012 2013 2014 2015 2016 2017

100

200

300

400

500

600

0 1 2 3 4 5 6 7 8 9 10 11 12

bo

ed

Production Month

Bakken

100

200

300

400

500

600

700

0 1 2 3 4 5 6 7 8 9 10 11 12

bo

ed

Production Month

Permian

2

3

4

5

6

7

8

9

10

11

0 1 2 3 4 5 6 7 8 9 10 11 12

Bcf

d

Production Month

Marcellus Gas

22% Month 1 Production

in 2017

4% Month 1 Production

in 201730% Month 1 Production

in 2017

13% Month 1 Production

in 2017

Source: WoodMackenzie

U.S. Crude Oil Export Destinations

0.0

0.2

0.4

0.6

0.8

1.0

1.2

2014 2015 2016 2017

Canada Argentina

Australia Bahama

Brazil China

Colombia Curacao

Denmark Dominican Republic

France Georgia

Germany Gibraltar

Greece Guatemala

Hong Kong India

Israel Italy

Japan Liberia

Malaysia Marshall Islands

Mexico Netherlands

Nicaragua Nigeria

Norway Panama

Peru Singapore

South Africa South Korea

Spain Switzerland

Thailand UK

Million Barrels per Day

U.S. Crude Oil Exports Helped Meet Energy Needs of 38 Countries Since 2014

16 Source: U.S. Energy Information Administration

Brent Price Outlooks

17

$30

$40

$50

$60

$70

$80

$90

$100

$110

2017 2018 2019 2020 2021 2022 2023 2024 2025

Brent Prices in Nominal $/bbl

Analysts’ Range

Futures 14-Sep-2017

Lower for Longer: Consensus Views are Down Sharply vs Early 2017 and 2016 Outlooks

18

Natural Gas Markets Outlook

Recent Gas Market Performance

Japan LNG

U.K. NBP

U.S. Henry Hub$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$20

2014 2015 2016 2017

Regional Price Indicators ($/mmbtu)

19

• North America, Europe and Asia prices have recovered from 2016 lows

• Demand growth is absorbing new production and supporting market price levelso Asia’s LNG imports in January

through August are up 16 million tonnes (+13%) over the same period in 2016 led by China, South Korea and Japan

• U.S. sets global price floor

Sources Bloomberg, IHS Markit

North America Gas Production Continues Strong

-

10

20

30

40

50

60

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Gas Production from Top U.S. Unconventional Plays(Bcfd)

20

Utica

Eagle Ford

Permian

Niobrara/Rockies

Bakken

Source: U.S. Energy Information Administration

0

20

40

60

80

100

120

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Future North American Production led by Shale(Bcfd)

Shale Gas

Other

Gas from Tight Oil

0

5

10

15

20

Mar

cellu

s +

Uti

ca

Per

mia

n

Can

ada

Eagl

e Fo

rd

Hay

nes

ville

Nio

bra

ra

Sco

op

/Sta

ck

Bak

ken

Marcellus/Utica will continue growth with infrastructure additionsPermian gas/NGL infrastructure will govern oil growth

Growth in production 2016-2025 (Bcfd)

Source: COP, Wood Mackenzie; U.S. and Canada production combined

North America Gas Demand Supported by Exports

21

80

80

81

81

82

82

83

83

842015 2016 2017

U.S. and Canada Natural Gas Consumption (Bcfd)

Source: COP, EIA, industry consultants

0

3

6

9

12

15

2016-2020 2020-2025

U.S. and Canadian Natural Gas Demand Growth (Bcfd)

Industrial

Power

Residential / Commercial

Other

LNG Exports

Mexico

Source: COP

0.0

1.0

2.0

3.0

4.0

5.0

Pipe Exports to Mexico LNG Exports

2015 2016 2017

U.S. and Canada Natural Gas Net Exports (Bcfd)

Recent Market Performance Outlook for Demand

U.S. LNG Export Destinations

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0Argentina Barbados

Brazil Chile

China Dominican Republic

Egypt India

Italy Japan

Jordan Kuwait

Malta Mexico

Netherlands Pakistan

Poland Portugal

South Korea Spain

Taiwan Thailand

Turkey United Arab Emirates

United Kingdom

BCF per Day

Supplied Energy to More Than 20 Countries in 2016-2017

22 Source: U.S. Energy Information Administration

Many New Markets are Looking to Start Importing LNG

23 Source: Wood Mackenzie

Existing / Former Importer

Likely new market

Possible new market

Less likely new market

Opportunities are centered on emerging markets in Central America, Africa, and Southern Asia

2016

China

JKT

India

Southern Europe

Northwest Europe

Southern Cone

Southeast Asia

Middle East

Bunkers

All Else

2030

Henry Hub Price

24 Source: CMEGroup, Investment Banks, Consultants

$2.0

$2.5

$3.0

$3.5

$4.0

$4.5

$5.0

$5.5

$6.0

2017 2018 2019 2020 2021 2022 2023 2024 2025

Analysts’ Range

Futures 14-Sep-2017

Henry Hub Prices in Nominal $/MMBtu

Take Away MessagesOil Markets

• Market rebalancing is underway – will take longer than expected

• Lower cost structure and continuing productivity improvements enable larger resource base to be economic

Natural Gas Markets

• North American market demand growth continues to be met via low cost shale gas supplies & associated gas from tight oil

• Global gas markets will be more highly correlated as U.S. exports grow

Government Policy Suggestions

• Provide adequate resource access

• Avoid policies that disincentivize investment

• Recognize that even in low-carbon scenarios, oil & gas will still be needed

• Recognize the pressures imposed on the E&P industry by the price downturn