north american private equity in review - hoganlovells.com · north american private equity...

TRANSCRIPT

North American PrivateEquity in ReviewAugust 2007

In association with:

MER 403 NA PE in Review AW.qxd 20/8/07 16:48 Page 1

895 Broadway4th FloorNew YorkNY 10003, USA

t: +1 212 686-5606f: +1 212 [email protected]

80 StrandLondonWC2R 0RLUnited Kingdom

t: +44 (0)20 7059 6100f: +44 (0)20 7059 [email protected]@mergermarket.com

Suite 2001Grand Millennium Plaza181 Queen’s Road, CentralHong Kong

t: +852 2158 9700f: +852 2158 [email protected]

mergermarket. Part of The Mergermarket Group

Contents

Bowne foreword 3

Hogan & Hartson foreword 5

Continued buyouts: private equity IPOs lead to increasing regulatory pressure 6

Buyout deal size trends 9

Exit deal size trends 11

Industry trends 12

Hot sectors: Telecommunications, Media & Technology 22

Hot sector: Consumer 23

Hot sector: Financial Services 24

Tracking exits 25

Notes 28

Contacts 30

MER 403 NA PE in Review AW.qxd 20/8/07 16:48 Page 2

North American Private Equity in Review 3

Bowne is pleased to present the fifth edition of the NorthAmerican Private Equity in Review. This comprehensive reporthighlights the latest trends within the North American privateequity market, covers activity across various industry sectors andprovides an analysis of buyout and exit trends for the first half of2007. This report will provide useful insights for dealmakers andtheir advisors.

Buyout firms invested a record amount of capital in 2006 withover $426bn having been invested in the portfolio companies theyacquired. Amazingly, the first half of 2007 has already trumped allof 2006 with over $460bn having been invested so far this year.Additionally, the first half of 2007 saw 93 buyout deals valued inexcess of $500m which puts the year well on track to surpassthe 111 transactions that the whole of 2006 witnessed.

With regards to specific industry activity, the Telecommunicationssector set itself apart in that it accounted for four of the top tenannounced buyouts in H1 2007. Despite only accounting for just2% of overall buyout volume activity, the sector was buoyed bythe announced $48bn buyout of Canadian telecom provider BCE.The deal saw Teachers Private Capital, the private investment armof Ontario Teachers Pension Plan, Madison Dearborn Partners andProvidence Equity Partners team up on the acquisition. They wereable to beat competing offers from Cerberus Capital Managementas well as strategic rival Telus, who itself is speculated to be atarget of buyout firms. This marked the largest ever buyout,trumping the $44bn private equity acquisition of energy firm TXU,which was announced only a few months previous. Other notabletelco buyouts include the acquisition of Alltel by Goldman SachsCapital Partners and Texas Pacific Group for $26.9bn and that ofCablevision Systems by noted industry executive Charles Dolanfor $22.5bn. In terms of pure volume of activity, the Industrials& Manufacturing sector remained an attractive industry for buyoutinvestors as it accounted for just over 22% of all volume activity.The Consumer and Business services sectors followed with16% and 14% of volume activity respectively.

While buyout firms continue to make acquisitions at a recordpace, the exit market has remained healthy as well, trackingslightly behind the first half 2006 with 286 exits so far this year.The Technology sector saw the highest level of exit activity

accounting for over 23% of overall volume. One possibility for this could be the continued residual effects of the bargainshopping within the sector that followed the dot-com bust in the early part of the decade. These deals are now being exitedwith lucrative returns. Additionally, the secondary buyout marketremains healthy as well with 97 SBO deals having taken place so far in 2007 compared to 78 over the same period in 2006.

Another interesting development to keep an eye on within theNorth American private equity landscape involves the fallout overthe announcement made by the Canadian government last fallconcerning the taxation of income trusts. Income trusts will nolonger be given favorable tax conditions and there is, thereforemuch speculation that many mid-market Canadian companiesthat were once candidates to form an income trust will nowbecome targets for US private equity firms. It is also speculatedthat many income trusts that have already been established maysoon break up, and back into a traditional corporate entity. Indeed,the potential opportunity that the US’ neighbors to the northrepresent for buyout firms will be an interesting development to keep an eye on.

Bowne has in-depth global experience with the management and distribution of confidential financial documents, ranging from web-enabled technologies to extensive printing capabilities.Bowne Virtual Dataroom™, a customized secure website, is used by Private Equity professionals for portfolio management as well as by deal owners to post diligence documents forauthorized prospective buyers to view.

We at Bowne enjoy a special relationship with our private equitypartners. If you would like more information about how we canhelp you execute your strategy, please visit our website atwww.bowne.com/virtual. Additionally, resources relating to recent regulatory developments affecting private equity andhedge funds can be obtained at Bowne’s Securities Connectwebsite, www.securitiesconnect.com.

Bowne forewordIn the first half of 2007, the private equity market exhibited continued remarkable activity, breaking records

just set in 2006. As the openness of debt providers towards private equity may have recently peaked, private

equity funds continue to hold vast amounts of capital to invest in buyouts.

MER 403 NA PE in Review AW.qxd 20/8/07 16:48 Page 3

MER 403 NA PE in Review AW.qxd 20/8/07 16:48 Page 4

North American Private Equity in Review 5

Hogan & Hartson forewordHogan & Hartson is pleased to present the half year 2007 edition of North American Private Equity in Review

in association with Bowne and mergermarket. This comprehensive report highlights the most recent trends

and developments in the North American private equity market, addressing deal activity across industry

sectors as well as the value and volume trends for both buyouts and exits.

The first six months of 2007 set a new high for private equitydeal making. North America saw $460bn in buyout deal value,which is already more than total deal value for the full year of2006. Q2 2007, in particular, was massive with $342.1bn inbuyout value. It’s a very similar picture with half year exitvalues of $90.8bn, already close to last year’s full year total of $103.6bn.

One of the most important features of the year is the rise inthe value of large-cap private equity transactions. Indeed, dealsvalued $500m and above reached a combined $441bn for thehalf year, already surpassing 2006, which had $386.7bn in thisdeal band. The long-standing record $25bn purchase of RJRNabisco by Kohlberg Kravis Roberts in1989 was easilysurpassed by a range of large LBO’s in 2007. The largest of these was the $48.1bn acquisition of Canadian telecomcompany BCE by a consortium of investors, which includedKKR in June. Club or consortium deals remain prevalent. Infact, three of the top 10 largest buyouts completed in 2007involved a consortium.

The investment capital raised by private equity in the past yearremains at an aggressive level. In February, Providence EquityPartners closed its sixth fund, Providence Equity Partners VI,on $12bn, tripling the size of its previous one, which closed at$4.3bn in 2004. It took the firm only four months to raise thenew vehicle. Additionally, in April, Goldman Sachs closed itssixth global fund, GS Capital Partners VI, on $20bn, which isthe largest private equity fund to date.

In terms of industry sectors, Industrials/Chemicals/Engineeringaccounted for 22% of buyout volume, followed by Consumerwith 16%, and Business Services with 14%. In value terms,Telecommunications was the leading sector with $113.6bn,followed by Business Services with $83.2bn, and FinancialServices with $73.6bn. The half year has also been notable forprivate equity firms making significant investments in industrysectors where they have not been previously been historicallyactive. Most notably in the Technology sector where therehave been over 20 technology buyouts in 2007 so far.

The year also continued to witness the ongoinginstitutionalization of private equity as an investment class.Specific landmark events included Blackstone’s $4.75bn IPO in June. Additionally, investors traditionally regarded as hedgefunds, like Cerberus, continue to become increasingly involvedin private equity buyouts. At the same time public scrutiny ofprivate equity continues to flow in from regulators and themedia, and is sure to compel the asset class to continueefforts that bolster its public image in coming months.

Hogan & Hartson is an international law firm with more than1,000 lawyers practicing in 22 offices worldwide. Our privateequity practice brings a strong “sector approach” to dealstructuring, bringing to bear a legal team that couplestransactional experience with our leading national andinternational regulatory lawyers. Through our private equitycoordinating group, we exchange information across officesconcerning best practices, transactions, industry knowledge,business contacts, deal opportunities, and documentprecedents. Our lawyers recently have participated inleveraged acquisitions and venture capital investmentsinvolving companies and private investment funds in theUnited States, Germany, the United Kingdom, France, Russia,Belgium, Poland, the Netherlands, Denmark, Mexico, China,and other parts of Asia. We have the substantive depth toserve as special acquisition, financing, regulatory, andsecurities counsel, and strive to build relationships based uponthe simple principle that whatever the issue, we will deliverthe answers you need, when you need them.

Richard K.A. Becker, Partner Kevin C. Clayton, Partner George A. Hagerty, Partner Jeffrey M. Hurlburt, Partner David A. Winter, Partner Hogan & Hartson LLP

MER 403 NA PE in Review AW.qxd 20/8/07 16:48 Page 5

6 North American Private Equity in Review

Drivers for this pace continue to include investors’ pursuit of superior returns generated by alternative asset classes,relatively inexpensive acquisition financing and, in the UnitedStates, avoidance of prospective Sarbanes-Oxley compliancecosts through going private transactions or M&A exits, asopposed to public offerings. The continued success of certainprivate equity funds and increased profile of private equity as a result of a continuing parade of mega-buyouts has led toincreased public and regulatory scrutiny of the sector. Itremains unclear whether developing issues in the regulatoryenvironment, particularly with respect to taxation of carriedinterest and publicly traded partnerships, concerns aboutleverage ratios and dividend recapitalizations, or increasingfinancing costs will slow this pace.

The private equity asset class continued to generate above-market returns in 2006. A desire to monetize investor interestin private equity fund returns led two large alternativeinvestment funds, Fortress Investment Group and TheBlackstone Group, each of which includes substantial privateequity components, to complete initial public offerings of theirmanagement vehicles in the first half of 2007. Kohlberg KravisRoberts has also filed for an IPO and tripled the size of theoffering to accommodate investor interest, though recentmarket concerns relating principally to the credit market appearto have delayed the offering. While the sector’s returns hadalready generated substantial media interest in the sector,these offerings seemed to trigger additional regulatory scrutiny, both in the United States and abroad.

After the Fortress IPO and shortly before Blackstone’s filing,U.S. and U.K. legislators began discussing changes to thetaxation of certain publicly traded partnerships and the taxtreatment of carried interest. The Senate Finance Committee,the House of Commons Treasury Select Committee, and theEuropean Parliaments Financial Services Forum all heldhearings to discuss taxation of private equity professionals and buyout leverage issues.

The U.S. discussion focused primarily on the taxation of carriedinterests and the tax treatment of distributions from publiclytraded partnerships–such as the Fortress and Blackstonevehicles. Tax on carried interest is currently deferred–due onlywhen profit is realized–and carried interest is eligible fortaxation at capital gains rates, which can be 20 percent lowerin the United States (30 percent lower in the United Kingdom)than the rates at which ordinary income is taxed. Critics of thecurrent rules argue that carried interest is compensation forservices and should be taxed as such, rather than as if it wasrisk capital. Defenders note that carried interests are in factinterests at risk and should be taxed accordingly. Changes tothis structure could have implications to partnerships outsidethe sector, and private equity funds are lobbying legislators fortheir preferred outcomes. Legislation has been introduced, butfunds and related trade associations have been very proactivein arguing for their perspective on the issue, and thelegislation’s prospects are not clear.

Continued Buyouts: privateequity IPOs lead to increasingregulatory pressureIn the first half of 2007, private equity transactions and new fundraisings continued at the torrid pace of

2006, with Hogan & Hartson LLP involved in all segments of market activity, from the $20bn Archstone-Smith

buyout to sub-$1m venture financings.

MER 403 NA PE in Review AW.qxd 20/8/07 16:48 Page 6

North American Private Equity in Review 7

In addition to tax issues, United Kingdom legislators andinternational ratings agencies (Moody’s Investors Service) have also expressed public concern about leverage used inmore recent buyouts and about dividend recapitalizations–anincreasingly popular source of liquidity for private equity funds.Historically low interest rates have allowed buyout firms tocontinue to use substantial leverage to increase transactionreturns, with leverage ratios up to 10 times EBITDA in sometransactions. These leverage ratios have led to concern thatbuyout firms are saddling acquired companies with levels ofdebt that may be unsustainable with rising interest rates. Anassociation of British private equity funds has responded tothese concerns by proposing a code of conduct for buyoutfirms. The proposed code would provide for greater disclosureabout acquisition terms, debt loads and decisions regardingmanagement of acquired entities, with the hope that greatertransparency will allay these concerns.

Similar concerns have been voiced by Moody’s with respect to the increasing use of dividend recapitalization structures,where an entity borrows in order to dividend out some portionof the borrowed funds to its investors. A relatively lacklusterIPO market over the past several years had led to a continuedincrease in dividend recapitalizations as a vehicle for privateequity fund investors to receive returns on their investments.As the IPO market has become more active in 2007 for privateequity-backed companies, it remains to be seen whether theincrease in dividend recapitalizations will continue.

Finally, we may see increased scrutiny by courts andgovernment agencies in the buyout sector. While fewdevelopments have occurred in the antitrust class actionagainst 13 private equity firms and the U.S. Department of Justice investigation of five such firms related to theanticompetitive effects of club bids initiated in late 2006, the U.S. Federal Trade Commission’s (FTC) involvement in the Kinder Morgan transaction and the Delaware ChanceryCourt’s decision in the Netsmart matter indicate additionalscrutiny for take private transactions.

In the Kinder Morgan matter, the FTC required certain of thetransaction’s private equity sponsors to cede control of theirportfolio companies with overlapping businesses. Netsmartinvolved the sale of a small public corporation to private equityfirms, and the court took issue with the sale process used bythe company, describing it as “a microcosm of the currentdynamic in the mergers and acquisitions market.” ViceChancellor Strine attacked the board’s conclusion that strategicbuyers would not have been interested in the company. TheChancery Court has issued similar rulings expressing concernsabout disclosure issues and conflicts in buyout transactions inthe Topps and Lear cases. We continue to counsel our clientsto use care in construction of Delaware-compliant dealprotection measures, and advise that board committees besubstantively involved in all aspects of a sale process. Clientscontinue to be sensitive to perceived conflicts of interest, andthis sensitivity is likely to serve them well in the near term.

It remains to be seen how the increased regulatory scrutinywill affect the private equity sector, and the extent of theimpact of a tightening of credit markets, but as funds seek to deploy the unprecedented amounts of capital they now have under management and interest rates remain, for now, at historically low levels, private equity is likely to continue as the principal driver of acquisition activity for the balance of 2007. Moreover, there is little if any evidence that thefundraising prospects for successful private equity firms areabout to turn, although history suggests that a shift in thisregard may not be preceded by much warning.

Richard K.A. Becker, Partner Kevin C. Clayton, Partner George A. Hagerty, Partner Jeffrey M. Hurlburt, Partner David A. Winter, Partner Hogan & Hartson LLP

MER 403 NA PE in Review AW.qxd 20/8/07 16:48 Page 7

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 8

North American Private Equity in Review 9

Buyout deal size trends

• In the two quarters of 2007, North American buyout volumedipped from 233 to 224 deals. Despite this slide, volumeremains steadily above the 200 marker.

• Exit volumes have increased steadily from 129 to 157 for the half year. Exits have notably been above the 100 deal marker since Q2 of 2005.

0

50

100

150

200

250

Q1

2003

Q2

2003

Q3

2003

Q4

2003

Q1

2004

Q2

2004

Q3

2004

Q4

2004

Q1

2005

Q2

2005

Q3

2005

Q4

2005

Q1

2006

Q2

2006

Q3

2006

Q4

2006

Q1

2007

Q2

2007

Buyouts number of deals Exits number of deals

Vo

lum

e o

f d

ea

ls

Buyout and exit trends by volume

0

300,000

250,000

200,000

150,000

100,000

50,000

350,000

Q1

2003

Q2

2003

Q3

2003

Q4

2003

Q1

2004

Q2

2004

Q3

2004

Q4

2004

Q1

2005

Q2

2005

Q3

2005

Q4

2005

Q1

2006

Q2

2006

Q3

2006

Q4

2006

Q1

2007

Q2

2007

Buyouts value ($m) Exits value ($m)

Va

lue

of

de

als

($

m)

Buyout and exit trends by value

• The first half of the year has proved exceptional for NorthAmerican private equity deal flow in terms of value. Buyoutvalue for H1 2007 comes to a grand total of $460.2bn, thehighest it’s ever been to date. Additionally, exits also addedup to a value top at $90.8bn for H1 2007.

• Overall, buyout value has increased steadily for the most part, with a drastic increase to end H1 2007. In Q1, exitsconstituted 20.5% of buyout value and in a similar vein, Q2 exits accounted for 19.5% of buyout value.

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 9

Buyout deal size trends

10 North American Private Equity in Review

1,000

900

800

700

600

500

400

300

200

100

0

2003 2004 2005 2006 H1 2007

> $500m

$251m - $500m

$101m - $250m

$15m - $100m

< $15m

Not disclosed

Vo

lum

e o

f d

ea

ls

Buyout deal sizes by volume

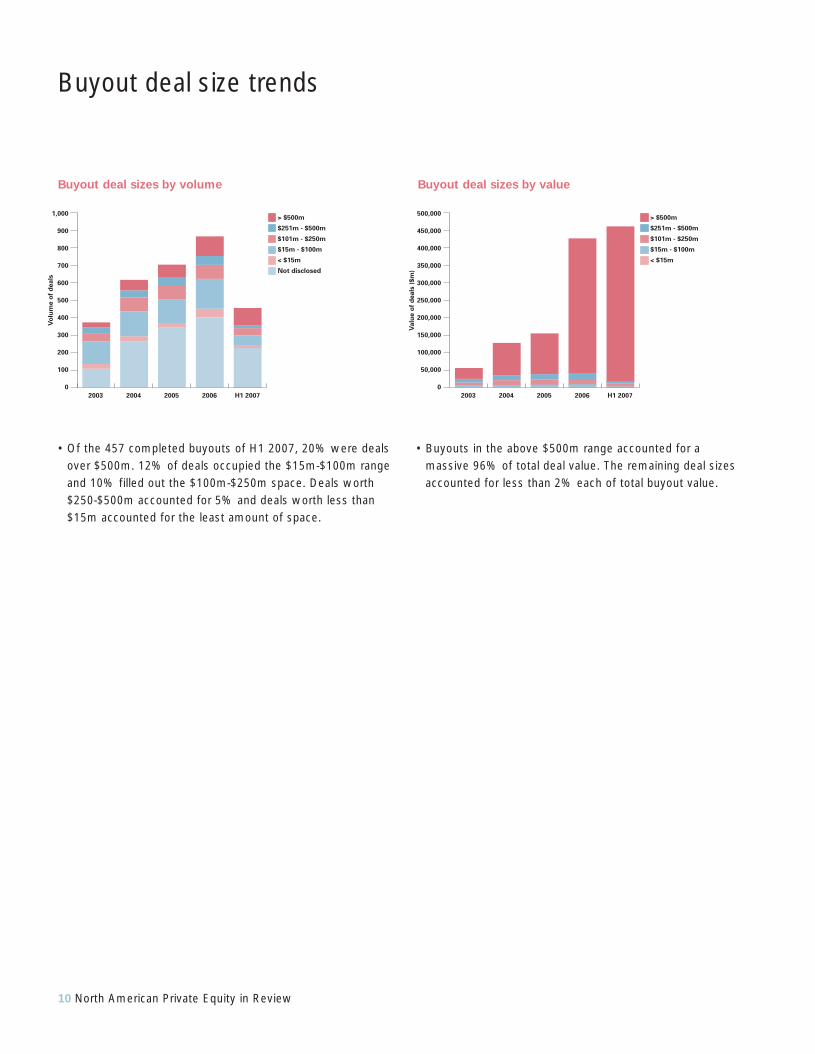

• Of the 457 completed buyouts of H1 2007, 20% were dealsover $500m. 12% of deals occupied the $15m-$100m rangeand 10% filled out the $100m-$250m space. Deals worth$250-$500m accounted for 5% and deals worth less than$15m accounted for the least amount of space.

• Buyouts in the above $500m range accounted for a massive 96% of total deal value. The remaining deal sizesaccounted for less than 2% each of total buyout value.

500,000

450,000

400,000

350,000

300,000

250,000

200,000

150,000

100,000

50,000

0

2003 2004 2005 2006 H1 2007

> $500m

$251m - $500m

$101m - $250m

$15m - $100m

< $15m

Va

lue

of

de

als

($

m)

Buyout deal sizes by value

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 10

North American Private Equity in Review 11

Exit deal size trends

0

20

40

10

30

50

60 35,000

30,000

Q1

2003

Q2

2003

Q3

2003

Q4

2003

Q1

2004

Q2

2004

Q3

2004

Q4

2004

Q1

2005

Q2

2005

Q3

2005

Q4

2005

Q1

2006

Q2

2006

Q3

2006

Q4

2006

Q1

2007

Q2

2007

Volume of deals Value of deals ($m)

Vo

lum

e o

f d

ea

ls

Va

lue o

f d

eals

($m

)25,000

20,000

15,000

10,000

5,000

0

Secondary buyout trends by volume and value

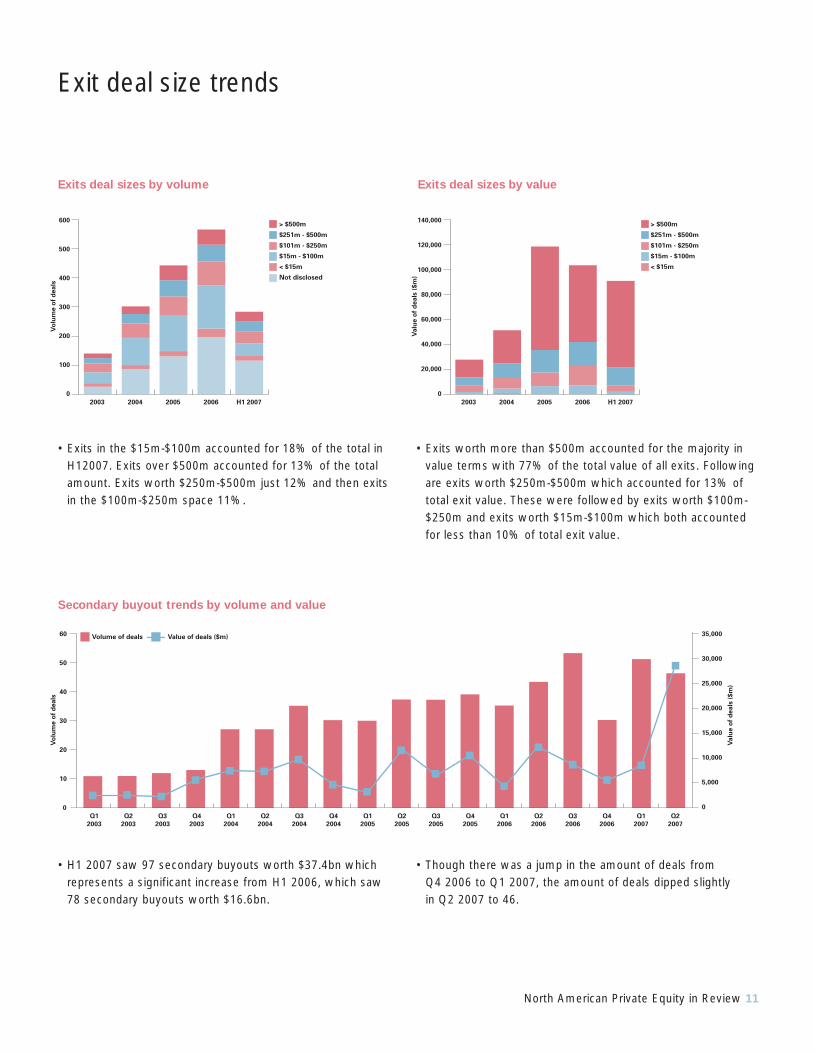

• H1 2007 saw 97 secondary buyouts worth $37.4bn whichrepresents a significant increase from H1 2006, which saw 78 secondary buyouts worth $16.6bn.

• Though there was a jump in the amount of deals from Q4 2006 to Q1 2007, the amount of deals dipped slightly in Q2 2007 to 46.

• Exits in the $15m-$100m accounted for 18% of the total inH12007. Exits over $500m accounted for 13% of the totalamount. Exits worth $250m-$500m just 12% and then exitsin the $100m-$250m space 11%.

• Exits worth more than $500m accounted for the majority invalue terms with 77% of the total value of all exits. Followingare exits worth $250m-$500m which accounted for 13% oftotal exit value. These were followed by exits worth $100m-$250m and exits worth $15m-$100m which both accountedfor less than 10% of total exit value.

600

500

400

300

200

100

0

2003 2004 2005 2006 H1 2007

> $500m

$251m - $500m

$101m - $250m

$15m - $100m

< $15m

Not disclosed

Vo

lum

e o

f d

ea

ls

140,000

120,000

100,000

80,000

60,000

40,000

20,000

0

2003 2004 2005 2006 H1 2007

> $500m

$251m - $500m

$101m - $250m

$15m - $100m

< $15m

Va

lue

of

de

als

($

m)

Exits deal sizes by valueExits deal sizes by volume

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 11

12 North American Private Equity in Review

Industrials/Chemicals/

Engineering

Financial Services

Business Services

Consumer

Energy, Mining, Oil & Gas

Technology

Media

Telco

Leisure

Transport

Lifesciences/Healthcare

Construction

Agriculture

Defence

18.1%

6.9%

10.3%

24.7%

5%

0.2%

6.1%4.1%

16%

3.8%

3.4%

1.4%Industrials/Chemicals/

Engineering

Financial Services

Business Services

Consumer

Energy, Mining, Oil & Gas

Technology

Media

Telco

Leisure

Transport

Lifesciences/Healthcare

Construction

Agriculture

Defence

9.6%

14%

16.2%

6.1%

5.5%

0.4%0.2%

2%

9.4%

3.5%

22.1%

3.5%

5%

2.4%

Volume mix buyouts by industry sectorValue mix buyouts by industry sector

• In terms of total buyout deal value three sectors formed themajority of deals for H1 2007. The Telecom sector made astrong lead with 25% of deals in terms of value, followed byBusiness Services with 18%, and then Financial Serviceswith 16%. The Business Services and Telecom sectors haveshown the greatest growth in value from 2006 to 2007, duein particular to the $27bn First Data buyout and the $48.1bnBCE buyout, both in Q2 2007.

• Buyouts for the first half of the year were mainly composedof four sectors. The Industrials, Chemicals & Engineeringsectors attracted the greatest number of deals this past yearwith 22% of total buyout volume, followed by the Consumersector with 16% and Business Services with 14% andFinancial Services with 10% of total deals for H1 2007.

• Though there was an adequate representation from allsectors in terms of exit values, the Telecom sector accountedfor the most, with 18% of the total value. This was followedby Energy, Mining, Oil & Gas, which accounted for 14% ofthe total value of exits. Industrials, Chemicals & Engineeringcame in with 11%, Financial Services saw 10%, and Leisurecame in with 9% consecutively.

• Exits in terms of volume were dominated by five sectors.Technology came in with the most with 24% of the totalamount of exits. Industrials, Chemicals & Engineeringfollowed with 18% and the Consumer and Business Services both came in with 12% of exits each.Lifesciences/Healthcare accounted for 10% of the total amount of exits for H1 2007.

Industrials/Chemicals/

Engineering

Telecom

Energy, Mining, Oil & Gas

Financial Services

Leisure

Technology

Consumer

Business Services

Lifesciences/Healthcare

Media

Transport

Construction

Defence

13.9%

10.7%

9.9%

8.4%

6.4%

0.1%

8.3%

0.4% 0.1%

18.2%

9%

8.6%

6.1%

Industrials/Chemicals/

Engineering

Technology

Business Services

Consumer

Lifesciences/Healthcare

Energy, Mining, Oil & Gas

Financial Services

Media

Leisure

Construction

Transport

Telecom

Defence

18.2%

11.9%

11.5%

5.6%

2.8%

1%

4.5%

1.7%0.3%

23.8%

10.1%

6.6%

1.7%

Volume mix exits by industry sectorValue mix exits by industry sector

Industry trends

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 12

North American Private Equity in Review 13

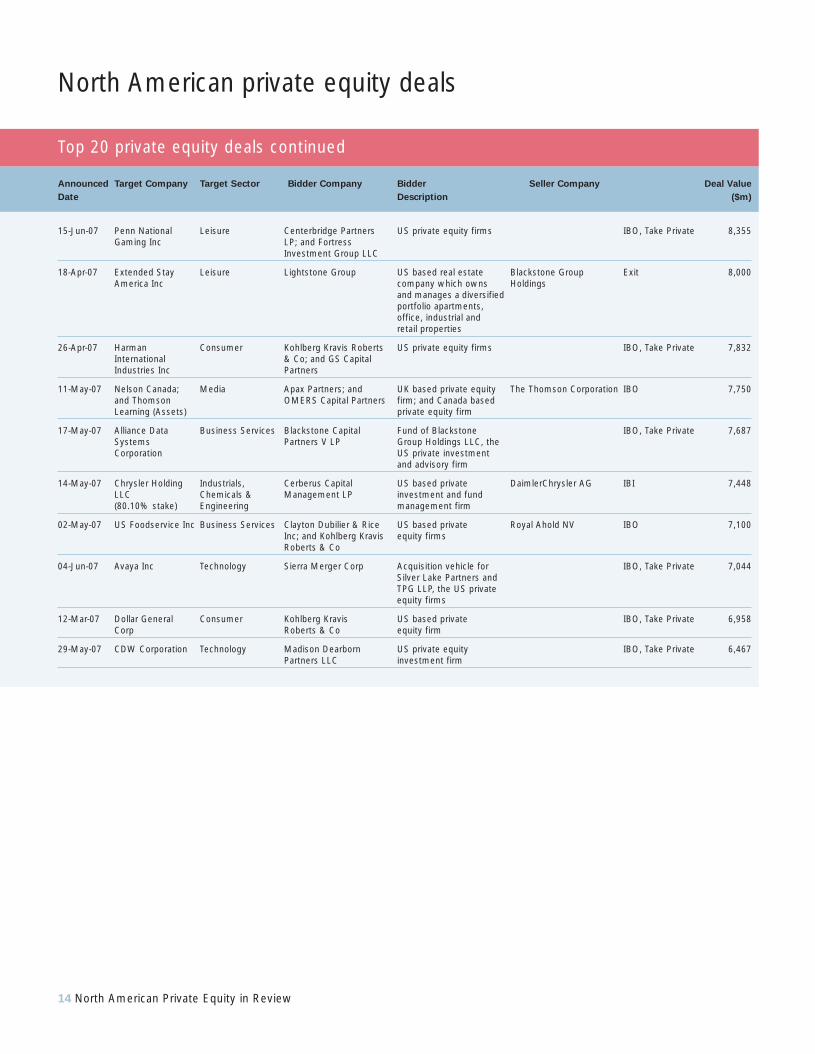

North American private equity deals

Top 20 private equity deals

Announced Target Company Target Sector Bidder Company Bidder Seller Company Deal Type Deal Value

Date Description ($m)

30-Jun-07 BCE Inc Telecommun- Teachers Private Capital; Private investment arm IBO, Take Private 48,059ications Madison Dearborn of the Ontario Teachers

Partners LLC; and Pension Plan; US privateProvidence Equity equity firmsPartners Inc

26-Feb-07 TXU Corp Energy, Mining, TXU Acquisition Consortium of investors IBO, Take Private 44,161Oil & Gas Consortium led by Kohlberg Kravis

Roberts & Co, TPG LLP, and Goldman Sachs throughits private equity arm. Minority equity investors include Citigroup Inc, Citigroup Venture Capital Equity Partners Ltd, JPMorgan Chase & Co, Lehman Brothers Private Equity, Morgan Stanley, and Morgan Stanley AIP Private Markets

02-Apr-07 First Data Business Services Kohlberg Kravis US based private equity IBO, Take Private 26,964Corporation Roberts & Co firm. Other providers of

equity finance include Goldman Sachs, Deutsche Bank AG, Credit Suisse, HSBC Holdings plc, Citigroup Inc, and GMI Investment Partners Inc

20-May-07 Alltel Corporation Telecommun- GS Capital Partners; US private equity firms IBO, Take Private 26,862Inc ications and TPG LLP

16-Apr-07 SLM Corporation Financial Services SLM Acquisition Corp Consortium led by JC IBO, Take Private 24,662Flowers & Co LLC. Other investors include Bank ofAmerica Corporation, JPMorgan Chase & Co, and Friedman, Fleischer & Lowe

02-May-07 Cablevision Telecommun- Charles Dolan family Charles Dolan and sons, IBO, Take Private 22,465Systems ications who control CablevisionCorporation and its Voom satellite

subsidiary

29-May-07 Archstone-Smith Financial Services Archstone-Smith A partnership sponsored by IBO, Take Private 19,820Trust Acquisition Co Tichman Speyer and Lehman

Brothers through its private equity arm

19-Jun-07 Intelsat Holdings Telecommun- BC Partners Ltd UK based private equity Apax Partners Worldwide SBO 15,823Limited ications firm LLP; Apollo Management

LP; Madison Dearborn Partners LLC; and Permira Advisors Ltd

19-Jun-07 HD Supply Business Services Bain Capital LLC; Clayton US based private equity The Home Depot Inc IBO 10,325Dubilier & Rice Inc; and firmsThe Carlyle Group LLC

26-Feb-07 Station Casinos Inc Leisure Fertitta Colony Partners An acquisition vehicle IBO, Take Private 8,462formed by Frank J. Fertitta III, Chairman and CEO of Station, Lorenzo J. Fertitta, Vice Chairman and President of Station, and Colony Capital LLC

Note: The Top 20 Deals table continues on the next page.

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 13

14 North American Private Equity in Review

Top 20 private equity deals continued

Announced Target Company Target Sector Bidder Company Bidder Seller Company Deal Value

Date Description ($m)

15-Jun-07 Penn National Leisure Centerbridge Partners US private equity firms IBO, Take Private 8,355Gaming Inc LP; and Fortress

Investment Group LLC

18-Apr-07 Extended Stay Leisure Lightstone Group US based real estate Blackstone Group Exit 8,000America Inc company which owns Holdings

and manages a diversifiedportfolio apartments, office, industrial and retail properties

26-Apr-07 Harman Consumer Kohlberg Kravis Roberts US private equity firms IBO, Take Private 7,832International & Co; and GS Capital Industries Inc Partners

11-May-07 Nelson Canada; Media Apax Partners; and UK based private equity The Thomson Corporation IBO 7,750and Thomson OMERS Capital Partners firm; and Canada basedLearning (Assets) private equity firm

17-May-07 Alliance Data Business Services Blackstone Capital Fund of Blackstone IBO, Take Private 7,687Systems Partners V LP Group Holdings LLC, theCorporation US private investment

and advisory firm

14-May-07 Chrysler Holding Industrials, Cerberus Capital US based private DaimlerChrysler AG IBI 7,448LLC Chemicals & Management LP investment and fund(80.10% stake) Engineering management firm

02-May-07 US Foodservice Inc Business Services Clayton Dubilier & Rice US based private Royal Ahold NV IBO 7,100Inc; and Kohlberg Kravis equity firmsRoberts & Co

04-Jun-07 Avaya Inc Technology Sierra Merger Corp Acquisition vehicle for IBO, Take Private 7,044Silver Lake Partners and TPG LLP, the US private equity firms

12-Mar-07 Dollar General Consumer Kohlberg Kravis US based private IBO, Take Private 6,958Corp Roberts & Co equity firm

29-May-07 CDW Corporation Technology Madison Dearborn US private equity IBO, Take Private 6,467Partners LLC investment firm

North American private equity deals

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 14

North American Private Equity in Review 15

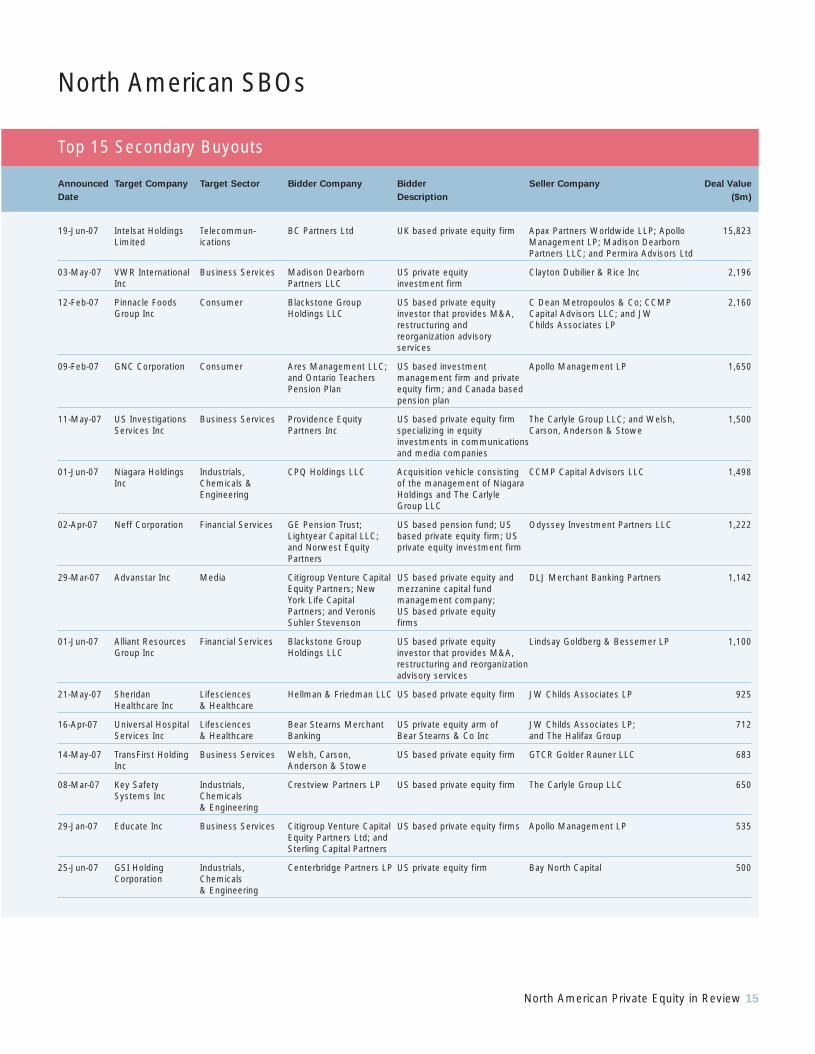

North American SBOs

Top 15 Secondary Buyouts

Announced Target Company Target Sector Bidder Company Bidder Seller Company Deal Value

Date Description ($m)

19-Jun-07 Intelsat Holdings Telecommun- BC Partners Ltd UK based private equity firm Apax Partners Worldwide LLP; Apollo 15,823Limited ications Management LP; Madison Dearborn

Partners LLC; and Permira Advisors Ltd

03-May-07 VWR International Business Services Madison Dearborn US private equity Clayton Dubilier & Rice Inc 2,196Inc Partners LLC investment firm

12-Feb-07 Pinnacle Foods Consumer Blackstone Group US based private equity C Dean Metropoulos & Co; CCMP 2,160Group Inc Holdings LLC investor that provides M&A, Capital Advisors LLC; and JW

restructuring and Childs Associates LPreorganization advisory services

09-Feb-07 GNC Corporation Consumer Ares Management LLC; US based investment Apollo Management LP 1,650and Ontario Teachers management firm and privatePension Plan equity firm; and Canada based

pension plan

11-May-07 US Investigations Business Services Providence Equity US based private equity firm The Carlyle Group LLC; and Welsh, 1,500Services Inc Partners Inc specializing in equity Carson, Anderson & Stowe

investments in communications and media companies

01-Jun-07 Niagara Holdings Industrials, CPQ Holdings LLC Acquisition vehicle consisting CCMP Capital Advisors LLC 1,498Inc Chemicals & of the management of Niagara

Engineering Holdings and The Carlyle Group LLC

02-Apr-07 Neff Corporation Financial Services GE Pension Trust; US based pension fund; US Odyssey Investment Partners LLC 1,222Lightyear Capital LLC; based private equity firm; USand Norwest Equity private equity investment firmPartners

29-Mar-07 Advanstar Inc Media Citigroup Venture Capital US based private equity and DLJ Merchant Banking Partners 1,142Equity Partners; New mezzanine capital fund York Life Capital management company;Partners; and Veronis US based private equitySuhler Stevenson firms

01-Jun-07 Alliant Resources Financial Services Blackstone Group US based private equity Lindsay Goldberg & Bessemer LP 1,100Group Inc Holdings LLC investor that provides M&A,

restructuring and reorganization advisory services

21-May-07 Sheridan Lifesciences Hellman & Friedman LLC US based private equity firm JW Childs Associates LP 925Healthcare Inc & Healthcare

16-Apr-07 Universal Hospital Lifesciences Bear Stearns Merchant US private equity arm of JW Childs Associates LP; 712Services Inc & Healthcare Banking Bear Stearns & Co Inc and The Halifax Group

14-May-07 TransFirst Holding Business Services Welsh, Carson, US based private equity firm GTCR Golder Rauner LLC 683Inc Anderson & Stowe

08-Mar-07 Key Safety Industrials, Crestview Partners LP US based private equity firm The Carlyle Group LLC 650Systems Inc Chemicals

& Engineering

29-Jan-07 Educate Inc Business Services Citigroup Venture Capital US based private equity firms Apollo Management LP 535Equity Partners Ltd; and Sterling Capital Partners

25-Jun-07 GSI Holding Industrials, Centerbridge Partners LP US private equity firm Bay North Capital 500Corporation Chemicals

& Engineering

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 15

16 North American Private Equity in Review

Private equity activity tables - buyouts

Buyouts - Volume

Rank Company Name Number of Deals Value ($m)

1 The Carlyle Group 12 20,364

2 Sun Capital Partners 9 407

3 GS Capital Partners 8 84,211

4 Kohlberg Kravis Roberts & Co 7 97,199

5 Providence Equity Partners 7 58,426

6 Citigroup Venture Capital Equity Partners 6 55,220

7 American Capital Strategies 6 947

8 The Riverside Company 6 -

9 Lehman Brothers Private Equity 5 64,231

10 Madison Dearborn Partners 5 62,666

Buyouts - Value

Rank Company Name Number of Deals Value ($m)

1 Kohlberg Kravis Roberts & Co 7 97,199

2 GS Capital Partners 8 84,211

3 TPG 4 79,012

4 Lehman Brothers Private Equity 5 64,231

5 Madison Dearborn Partners 5 62,666

6 Providence Equity Partners 7 58,426

7 Citigroup Venture Capital Equity Partners 6 55,220

8 Teachers Private Capital 1 48,059

9 Morgan Stanley AIP Private Markets 1 44,161

10 JC Flowers & Co 2 24,662

Note: The tables are based on private equity houses as the bidder on buyouts and buyins announced between 01/01/2007 and 06/30/2007, where the target is North American, excluding lapsedand withdrawn deals.

The Private Equity Activity Tables reflect the activity of buyout firms, venture capitalists, investment firms, financial institutions and all parties whose activities wholly involve, or include makingprivate equity investments. Please note that the values in the 'Value' column do NOT reflect the equity contribution of the investors but represent the total values of deals they were involved in.

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 16

North American Private Equity in Review 17

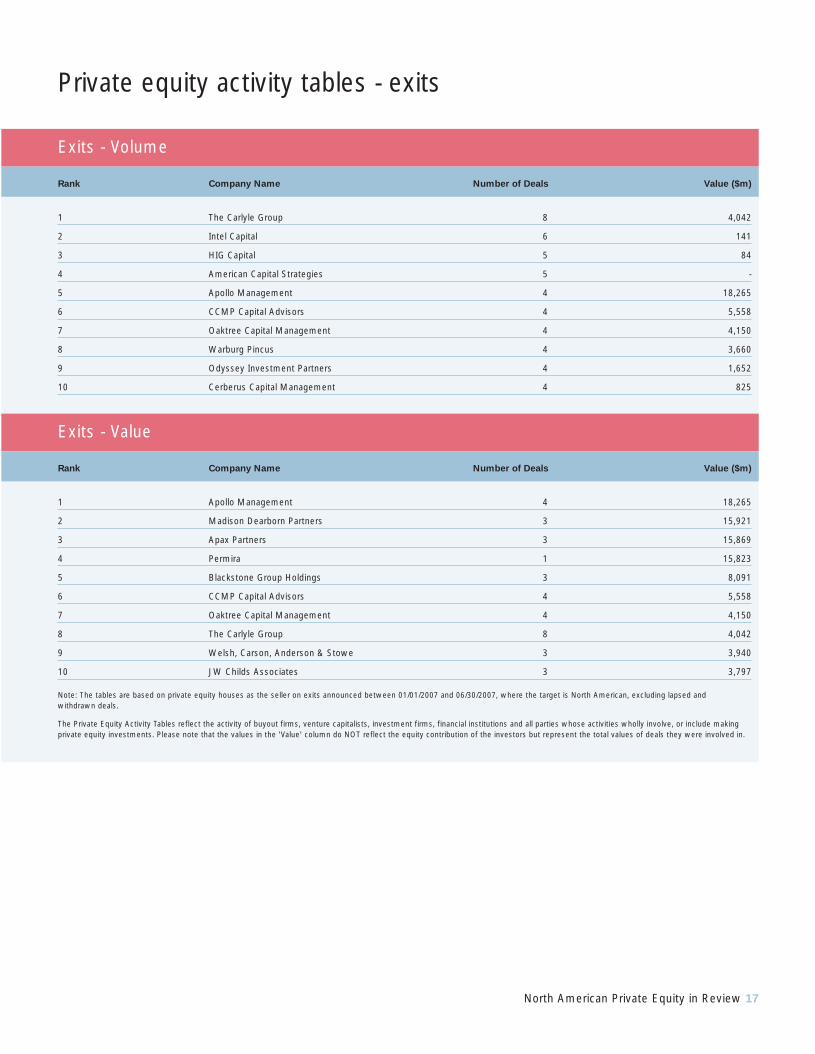

Private equity activity tables - exits

Exits - Volume

Rank Company Name Number of Deals Value ($m)

1 The Carlyle Group 8 4,042

2 Intel Capital 6 141

3 HIG Capital 5 84

4 American Capital Strategies 5 -

5 Apollo Management 4 18,265

6 CCMP Capital Advisors 4 5,558

7 Oaktree Capital Management 4 4,150

8 Warburg Pincus 4 3,660

9 Odyssey Investment Partners 4 1,652

10 Cerberus Capital Management 4 825

Exits - Value

Rank Company Name Number of Deals Value ($m)

1 Apollo Management 4 18,265

2 Madison Dearborn Partners 3 15,921

3 Apax Partners 3 15,869

4 Permira 1 15,823

5 Blackstone Group Holdings 3 8,091

6 CCMP Capital Advisors 4 5,558

7 Oaktree Capital Management 4 4,150

8 The Carlyle Group 8 4,042

9 Welsh, Carson, Anderson & Stowe 3 3,940

10 JW Childs Associates 3 3,797

Note: The tables are based on private equity houses as the seller on exits announced between 01/01/2007 and 06/30/2007, where the target is North American, excluding lapsed and withdrawn deals.

The Private Equity Activity Tables reflect the activity of buyout firms, venture capitalists, investment firms, financial institutions and all parties whose activities wholly involve, or include makingprivate equity investments. Please note that the values in the 'Value' column do NOT reflect the equity contribution of the investors but represent the total values of deals they were involved in.

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 17

18 North American Private Equity in Review

Financial Advisor activity tables - buyouts

Buyouts - Volume

Rank Company Name Number of Deals Value ($m)

1 Citigroup 25 221,076

2 Lehman Brothers 14 113,636

3 Credit Suisse 14 58,561

4 Goldman Sachs 13 127,602

5 JPMorgan 12 86,132

6 Deutsche Bank 11 111,424

7 Merrill Lynch 11 87,464

8 UBS 11 10,924

9 Morgan Stanley 9 80,116

10 Wachovia 8 23,516

Buyouts - Value

Rank Company Name Number of Deals Value ($m)

1 Citigroup 25 221,076

2 Goldman Sachs 13 127,602

3 Lehman Brothers 14 113,636

4 Deutsche Bank 11 111,424

5 Merrill Lynch 11 87,464

6 JPMorgan 12 86,132

7 Morgan Stanley 9 80,116

8 Credit Suisse 14 58,561

9 Banc of America Securities 6 57,280

10 TD Securities 2 48,247

Note: The tables are based on financial advisors to the bidder on buyouts and buyins announced between 01/01/2007 and 06/30/2007, where the target is North American, excluding lapsed and withdrawn deals.

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 18

North American Private Equity in Review 19

Financial Advisor activity tables - exits

Exits - Volume

Rank Company Name Number of Deals Value ($m)

1 Goldman Sachs 18 12,382

2 Credit Suisse 16 22,578

3 Lehman Brothers 13 11,079

4 Harris Williams & Co 12 833

5 Banc of America Securities 10 12,839

6 JPMorgan 10 8,560

7 Morgan Stanley 10 4,660

8 CIBC World Markets 8 2,843

9 UBS 8 1,899

10 Robert W Baird & Co 7 232

Exits - Value

Rank Company Name Number of Deals Value ($m)

1 Credit Suisse 16 22,578

2 Merrill Lynch 5 13,817

3 Banc of America Securities 10 12,839

4 Goldman Sachs 18 12,382

5 Bear, Stearns & Co 4 11,100

6 Lehman Brothers 13 11,079

7 JPMorgan 10 8,560

8 Blackstone Group Holdings 1 8,000

9 Morgan Stanley 10 4,660

10 Deutsche Bank 2 4,180

Note: The tables are based on financial advisors to the seller/target on exits announced between 01/01/2007 and 06/30/2007, where the target is North American, excluding lapsed andwithdrawn deals.

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 19

20 North American Private Equity in Review

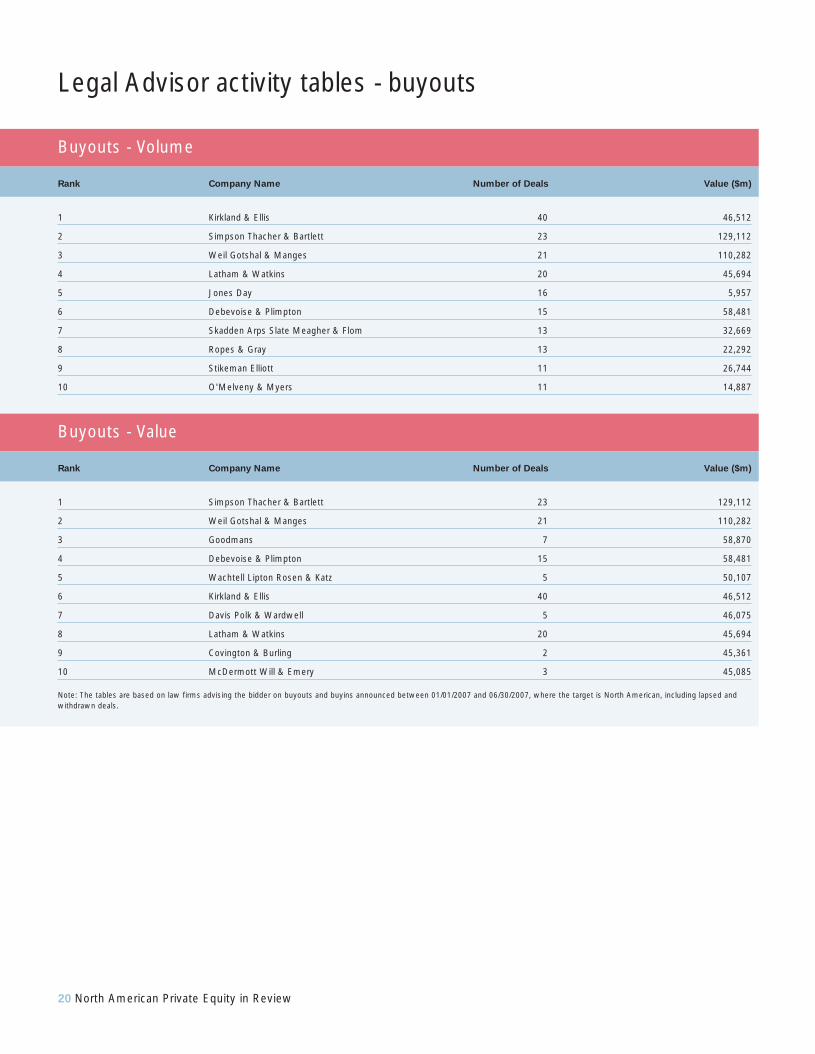

Legal Advisor activity tables - buyouts

Buyouts - Volume

Rank Company Name Number of Deals Value ($m)

1 Kirkland & Ellis 40 46,512

2 Simpson Thacher & Bartlett 23 129,112

3 Weil Gotshal & Manges 21 110,282

4 Latham & Watkins 20 45,694

5 Jones Day 16 5,957

6 Debevoise & Plimpton 15 58,481

7 Skadden Arps Slate Meagher & Flom 13 32,669

8 Ropes & Gray 13 22,292

9 Stikeman Elliott 11 26,744

10 O'Melveny & Myers 11 14,887

Buyouts - Value

Rank Company Name Number of Deals Value ($m)

1 Simpson Thacher & Bartlett 23 129,112

2 Weil Gotshal & Manges 21 110,282

3 Goodmans 7 58,870

4 Debevoise & Plimpton 15 58,481

5 Wachtell Lipton Rosen & Katz 5 50,107

6 Kirkland & Ellis 40 46,512

7 Davis Polk & Wardwell 5 46,075

8 Latham & Watkins 20 45,694

9 Covington & Burling 2 45,361

10 McDermott Will & Emery 3 45,085

Note: The tables are based on law firms advising the bidder on buyouts and buyins announced between 01/01/2007 and 06/30/2007, where the target is North American, including lapsed andwithdrawn deals.

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 20

North American Private Equity in Review 21

Legal Advisor activity tables - exits

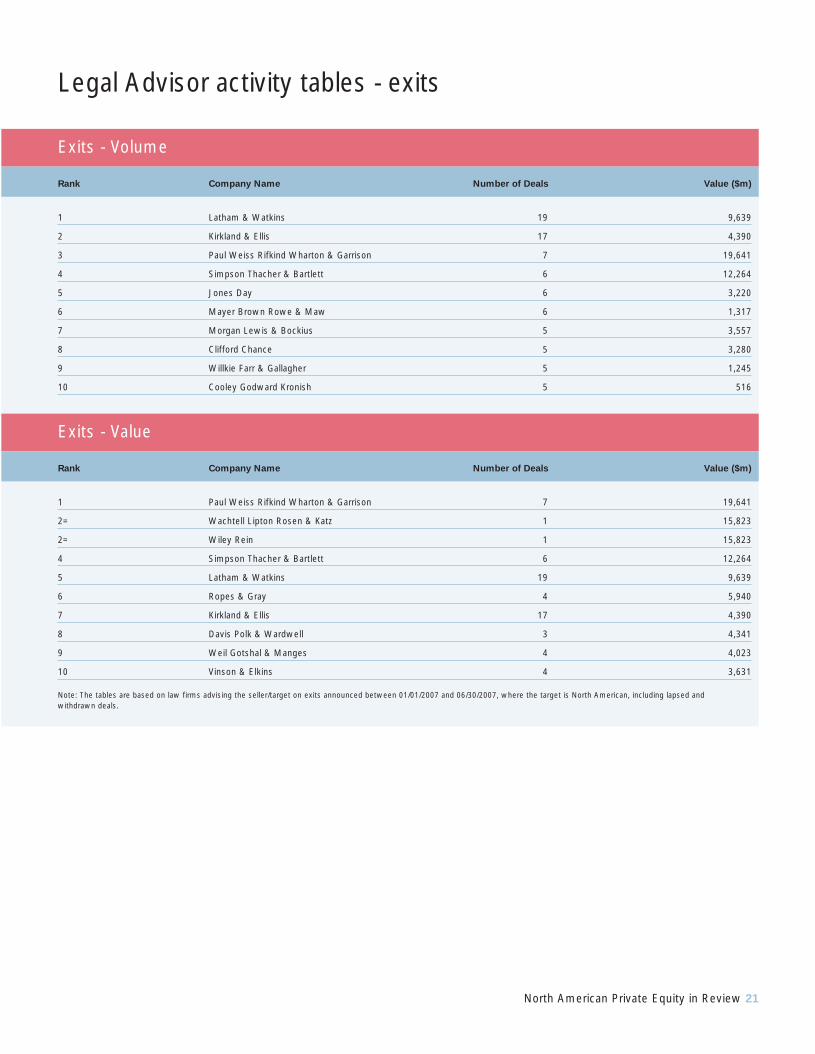

Exits - Volume

Rank Company Name Number of Deals Value ($m)

1 Latham & Watkins 19 9,639

2 Kirkland & Ellis 17 4,390

3 Paul Weiss Rifkind Wharton & Garrison 7 19,641

4 Simpson Thacher & Bartlett 6 12,264

5 Jones Day 6 3,220

6 Mayer Brown Rowe & Maw 6 1,317

7 Morgan Lewis & Bockius 5 3,557

8 Clifford Chance 5 3,280

9 Willkie Farr & Gallagher 5 1,245

10 Cooley Godward Kronish 5 516

Exits - Value

Rank Company Name Number of Deals Value ($m)

1 Paul Weiss Rifkind Wharton & Garrison 7 19,641

2= Wachtell Lipton Rosen & Katz 1 15,823

2= Wiley Rein 1 15,823

4 Simpson Thacher & Bartlett 6 12,264

5 Latham & Watkins 19 9,639

6 Ropes & Gray 4 5,940

7 Kirkland & Ellis 17 4,390

8 Davis Polk & Wardwell 3 4,341

9 Weil Gotshal & Manges 4 4,023

10 Vinson & Elkins 4 3,631

Note: The tables are based on law firms advising the seller/target on exits announced between 01/01/2007 and 06/30/2007, where the target is North American, including lapsed and withdrawn deals.

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 21

22 North American Private Equity in Review

In fact, the Telecommunications sector had the largest deal ofthe year, with a consortium of investors acquiring CanadianTelecom operator BCE for $48.1bn in June to claim the positionas the biggest announced deal ever in the history of buyouts,and Canada’s largest takeover to date. Bell Canada is a telecomcompany with diversified interests that include wireless,wireline, and Internet services. It generates much of its cash flowfrom 8.64m fixed phone lines and 5.8m wireless subscribers.

This sector is red-hot, and BCE certainly made it so; currentlythere are four Telecom deals in the top 20 buyouts of the year.Other top Telecom deals include the fourth ranked acquisition ofAlltel by TPG Capital and GS Capital Partners for $26.9bn in May.Alltel is an Arkansas-based provider of wireless communicationservices to over 12m customers in 36 states. Coming in asnumber six in the top 20 deals of the year, Cablevision waspurchased for $22.5bn in May. The eighth largest deal of theyear was also a Telecom deal, and saw Intelsat agree to beacquired by BC Partners for $15.8bn in June.

The Technology space was also no stranger to buyouts withthree Tech deals in the top 20 buyouts of the year. Indeed, thethird largest deal of the year was KKR’s $27bn takeover of FirstData Corporation in early April. First Data is a Colorado-basedcompany that is a leading provider of electronic commerce andpayment solutions for businesses worldwide. Furthermore,KKR has now have been in involved in four of the top tenbiggest buyouts of all time: RJR Nabisco, HCA and TXU. KKRwas the sole private equity house in the bidding process forFirst Data and offered $34 a share, a premium of about 26%over First Data's closing price in late March. Another Tech dealthat made the top 20 buyouts of the year, is number ten for theyear, Alliance Data Systems agreeing to be acquired byBlackstone for $7.7bn in May.

Potential Media acquisitions have also made the headlines. The fourteenth largest acquisition of H1 2007 saw NelsonCanada and Thomson Learning Assets agree to be acquired by Apax and OMERS Capital for $7.8bn in May.

The future looks promising for further acquisitions in thesesectors, as mergermarket intelligence indicates that there are currently 469 potential targets in the North American TMT landscape. On the Telecom front, one of these potentialdeals could include Sprint Nextel Corporation, a Virginia-basedtelecom firm worth $60.8bn that stated it may participate in"M&A scenarios" within next 12 months according to analysts.Meanwhile, the Technology front could see MicroStrategy, a Virginia-based provider of business intelligence software,exploring alternatives for its non-core Internet services sites in a $919m acquisition.

Hot sectors: Telecommunications, Media & TechnologyWhilst the Industrials sector still brings in the most buyout deals (22% share), Telecoms accounts for the

leading share of buyout deal value – almost 25% worth $114bn. Technology, meanwhile, saw $17.6bn and

Media $15.5bn. Of the top 20 buyouts of 2007 so far, there have been seven deals in the Telecommunications,

Media and Technology sectors.

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 22

North American Private Equity in Review 23

The largest Consumer buyout was $7.8bn buyout of HarmanInternational. Harman, based in Delaware, agreed to be acquiredby private equity giant KKR and GS Capital in April. Harmanengages in the development, manufacture, and marketingof audio products and electronic systems worldwide. Theconsortium offered $120 per share and offered shareholdersin the company the exclusive option of receiving some of thatcompensation in the form of stock in the new privately heldcompany, as well as a share in any profit made if the companyis later sold or listed. This option, known as stub equity, allowsHarman shareholders to exchange as many as 8.3m existingshares or 13% of the total outstanding, for a 27% stake in themore highly leveraged private company. Harman has remaineda trusted name in audio equipment since the 1950s and evenafter the buyout Dr. Sidney Harman, the founder and executivechairman, will continue to serve as executive chairman and thecompany will continue to be called Harman International.

The next largest Consumer deal saw Dollar General agree to be taken over by KKR in March for $6.9bn. Dollar General is a discount retailer that offers convenience and value tocustomers by offering consumable basic items that arefrequently used and replenished, as well as a selection of basic apparel, low priced housewares and seasonal items. Four private equity firms participated in the due diligenceprocess for Dollar General, but KKR was the only company to submit a bid and win them.

Looking forward, the sector looks ripe for further M&A andbuyouts, with mergermarket intelligence indicating that thereare 432 potential targets in the North American landscape. Atpresent these include JC Penney, a Texas-based retail apparelchain, Washington-based retailer Nordstrom and Tiffany, a NewYork jewelry retailer, according to mergermarket intelligence.

Hot sector: ConsumerThe Consumer sector witnessed two of the year’s top 20 buyouts overall, and accounted for 7%

of buyout deal value.

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 23

24 North American Private Equity in Review

The top Financial Services deal involved SLM, a Delawarecorporation headquartered in Reston, VA, and commonlyknown as Sallie Mae. SLM is the nation's leading provider of saving and paying for college programs. SLM agreed to be taken over by a consortium headed by J.C. Flowers in April for $24.4bn.

The end of 2006 brought Blackstone’s acquisition of EquityOffice Properties Trust for $37.8bn and a new year of increasedinterest in real estate buyouts. Equity Office is headquarteredin Chicago, IL and is a building owner and manager with aportfolio of whole or partial interests in 580 buildings in 16states and the District of Columbia. The transaction highlightedthe ongoing demand for office real estate among privateinvestors. In fact, the seventh deal in the top 20 buyouts, andanother real estate deal, was Tishman Speyer and LehmanBrothers’ acquisition of Archstone-Smith in May for $19.8bn.Archstone-Smith is headquartered in Englewood, CO, and isengaged in apartment investment and operations. TishmanSpeyer is one of the leading owners, developers, operators,and fund managers of first-class real estate in the world.

The future looks solid for more acquisitions to be built up in theFinancial Services sector. In fact, mergermarket data indicatesthat there are 450 potential targets on the North Americanfront for the sector. These include SunTrust Banks, a Georgia-based financial institution worth $27.6bn, which is reportedlynot excluding any options in its turnaround plans.

Hot sector: Financial ServicesIn recent years, the Financial Services sector has become a solid provider of private equity buyouts. In H1

2007, there have been 44 buys in the Financial Services sector for the half year to date totalling $73.6bn,

accounting for 16% of buyout deal. As per usual, deal flow in the sector has been dominated by real estate

deals, yet there have still been transactions in the investment brokering and banking areas as well.

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 24

North American Private Equity in Review 25

In terms of volume, Technology accounts for a 24% share.Industrials, Chemicals & Engineering is second with 18%, and Business Services saw 12%.

The top pure exit of the year occurred in the Leisure sector,and saw the Lightstone Group, an owner and operator of real estate, agree to acquire Extended Stay America, a hoteloperator, from Blackstone for $8bn in April.

Among the half-year’s top 20 exits, the Energy sector rankedthe highest with four exits in the top 20. The largest deal saw Horizon Wind Energy, a wind power generation developerand operator, sold by Goldman Sachs to Energias de Portugal(EDP), a Portuguese energy company, for $2.2bn in cash in March.

The next Energy sector exit in the top 20 saw CPV WindVentures sold by Competitive Power Ventures and ArcLightCapital Partners to Iberdrola, a Spanish energy company for $2.1m. The acquisition is in line with the Internationalexpansion strategy of Iberdrola, who expects to haverenewable power projects with 7,000MW capacity in various operations by 2009 and over 10,000MW in 2011.

Coming in as another of the top exit for the year is atransaction that saw North American Oil Sands Corporation(NAOSC), a Canadian energy company, being sold byParamount Resources (a Canadian oil and natural gasexploration company), ARC Financial Corporation and fundsmanaged by Ontario Teachers Pension Plan to Statoil forC$2.2bn (US$1.96bn). NAOSC’s recoverable will add to Statoil’sproduction after 2010, and will also enable the company toexpand its oil and natural gas exploration activities in NorthAmerica. NAOSC will benefit from Statoil’s capabilities in theareas of reservoir modeling, oil recovery and project execution.

Finally, coming in last and rounding out the top 10 exits isanother Energy exit. The transaction saw Vetco Gray, a USbased supplier of products and services for oil and gas drillingand production, being sold off by Vetco International Limited, a UK based investment holding company owned by CCMPCapital Advisors, a US based private equity firm, as well as the UK funds 3i Group plc and Candover Investments. Thebuyer was the Italian energy unit of the US GE conglomerate,GE Oil and Gas. The price paid was $1.9bn, on a debt and cash free basis. The sale of Vetco, which reported annualrevenues of $1.3bn in 2005 and is expected to generaterevenues of $1.6bn in 2006, marks a partial exit for the privateequity investors, who have already recapitalized the businesstwice in 2005 and are expected to receive 3.5 times their initial investment in 2004.

In summary, exit performance in coming months – across a range of sectors – is sure to provide compelling viewing.Furthermore, both secondary buyouts and sales to strategicbuyers will need to be lucrative if the private equity industryis to maintain its recent break-neck pace.

Tracking exitsThe amount of exit deals in North America has remained strong this year with 286 exits totalling $90.8bn

already for H1 2007. The Telecom sector brought in the leading amount of exit deal value with 18% share

of the total for the year. Energy, Mining, Oil & Gas came in second with 14% and Industrials, Chemicals

& Engineering saw almost 11%.

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 25

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 26

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 27

28 North American Private Equity in Review

NotesNotes

The following notes pertain to data contained inthis publication:

• Deals included are buyouts or exits where the deal value is greater than or equal to $5m.

• Where no deal value has been disclosed, deals are included if the turnover of the Target is greater than or equal to $10m of if the Target employs more than 100 people.

• Deals are included within the analysis, charts and graphs for each section if the dominant geography of the Target is North American.

• Please refer to individual notes beneath each Activity Table for the precise criteria by which each table has been run.

• The Sector Trend analysis is based on deals using the dominant industry of the target.

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 28

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 29

30 North American Private Equity in Review

Contacts Bowne Contacts

William P. PendersPresident and COO, Financial CommunicationsTel: +1 212 658 5828

Matt LaMuragliaSr. Vice President, Director of SalesTel: +1 212 658 5850

Erika CravenVice President, Strategic MarketingTel: +1 212 658 5813

mergermarket Contacts

Erik WickmanHead of North American Sales, RemarkTel: +1 212 686 3329Email: [email protected]

Elias LatsisHead of ResearchTel: +44 (0)20 7059 6100Email: [email protected]

Abigail RobertsEditor, mergermarket AmericasTel: +1 212 686 6526Email: [email protected]

Analysis: Priya IdicullaData: Gwen CetonEditor: Ed LucasProduction: Gwen Ceton & Steve Jeal

Hogan & Hartson Contacts

Wasington, D.C.David A. WinterTel: +1 202 637 6511Email: [email protected]

North VirginiaRichard K.A. BeckerTel: +1 703 610 6123Email: [email protected]

London/Washington, D.C.Jeffrey M. HurlburtTel: +44 (0)20 7367 0226Tel: +1 202 637 2868Email: [email protected]

DenverGeorge A. HagertyTel: +1 303 454 2464Email: [email protected]

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 30

This publication contains general information and is not intended to becomprehensive nor to provide financial, investment, legal, tax or other professionaladvice or services. This publication is not a substitute for such professional adviceor services, and it should not be acted on or relied upon or used as a basis forany investment or other decision or action that may affect you or your business.Before taking any such decision you should consult a suitably qualifiedprofessional adviser.

Whilst reasonable effort has been made to ensure the accuracy of theinformation contained in this publication, this cannot be guaranteed and neitherMergermarket nor any of its subsidiaries nor any affiliate thereof or other relatedentity shall have any liability to any person or entity which relies on theinformation contained in this publication, including incidental or consequential

damages arising from errors or omissions. Any such reliance is solely at theuser’s risk.

mergermarket

mergermarket is an unparalleled, independent Mergers &Acquisitions (M&A) proprietary intelligence tool. Unlike anyother service of its kind, mergermarket provides a completeoverview of the M&A market by offering both a forwardlooking intelligence database and an historical deals database,achieving real revenues for mergermarket clients.

Remark

Remark offers bespoke services such as Thought Leadershipstudies, Research Reports or Reputation Insights that enableclients to assess and enhance their own profile and developnew business opportunities with their target audience. Remarkachieves this by leveraging mergermarket’s core research,intelligence gathering expertise and connections within thefinancial services industry.

To find out more please contact:[email protected] or tel +44 (0)20 7059 6124

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 31

895 Broadway4th FloorNew YorkNY 10003, USA

t: +1 212 686-5606f: +1 212 [email protected]

80 StrandLondonWC2R 0RLUnited Kingdom

t: +44 (0)20 7059 6100f: +44 (0)20 7059 [email protected]@mergermarket.com

Suite 2001Grand Millennium Plaza181 Queen’s Road, CentralHong Kong

t: +852 2158 9700f: +852 2158 [email protected]

mergermarket. Part of The Mergermarket Group

MER 403 NA PE in Review AW.qxd 20/8/07 16:49 Page 32