nickel production and supply: market implications · nickel production and supply: market ......

TRANSCRIPT

Nickel Production and Supply: Market Implications

Metal Bulletin 5th International Nickel Conference

Mark Selby, President & CEO

RNC Minerals

April 24, 2017

www.royalnickel.com

2

Disclaimer

Cautionary Statements Concerning Forward-Looking Statements This presentation contains "forward-looking information" including without limitation statements relating to the future price and supply and demand and the implications the Indonesian ore export ban will have on the outlook for nickel; and statements relating to construction and production at the Dumont Nickel Project. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual outcome, events, results, performance or achievements of RNC to be materially different from any future outcome, events, results, performance or achievements expressed or implied by the forward-looking statements. Factors that could affect the outcome include, among others: future actions taken by the Indonesian government as well as mining companies operating in Indonesia; general business, economic, political and social uncertainties; availability of alternative nickel sources or substitutes; and financing to complete construction and achieve production at Dumont. For a more detailed discussion of such risks and other factors that could cause actual results to differ materially from those expressed or implied by such forward-looking statements, refer to RNC's filings with Canadian securities regulators available on SEDAR at www.sedar.com. Although RNC has attempted to identify important factors that could cause actual outcome, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause outcome, events or results to differ from those anticipated, estimated or intended. Forward-looking statements contained herein are made as of the date of this presentation and RNC disclaims any obligation to update any forward-looking statements, whether as a result of new information, future events or results or otherwise, except as required by applicable securities laws.

www.royalnickel.com

3

Nickel market supply/demand has performed better than other base metals over the past 3 years

Nickel market will need another 400-500kt to meet trend nickel demand by 2021 (and significantly more if forecasts for batteries come anywhere close to expectations!) Equivalent to doubling Chinese NPI industry at its peak

Very little visibility into future supply - extended period of low prices has resulted in very few opportunities for new supply and more dependence on future growth from higher political risk areas Underinvestment led to flat to declining production at most large nickel operations

Old, deep operations take several years and hundreds of millions of dollars to ramp-up

Nickel supply becoming highly dependent on higher political risk countries (Indonesia, Philippines)

Remaining ramp-up from new large HPAL projects uncertain Indonesian developments create massive uncertainty for the most active source of

new supply Project cupboard outside Indonesia largely empty

Relaxation of Indonesian ban has hurt nickel market in near-term but setting stage for very robust long-term nickel market outlook

Overview

www.royalnickel.com

Nickel- Favourable Supply / Demand Trends

Nickel supply / demand trends very favourable versus other base metals

4

0%

1%

2%

3%

4%

5%

6%

Demand Growth 2013-2016 (CAGR%)

-1%

0%

1%

2%

3%

4%

5%

6%

Refined Supply Growth 2013-2016 (CAGR%)

Source: Macquarie, RNC analysis

www.royalnickel.com 5

Source: Macquarie, RNC analysis

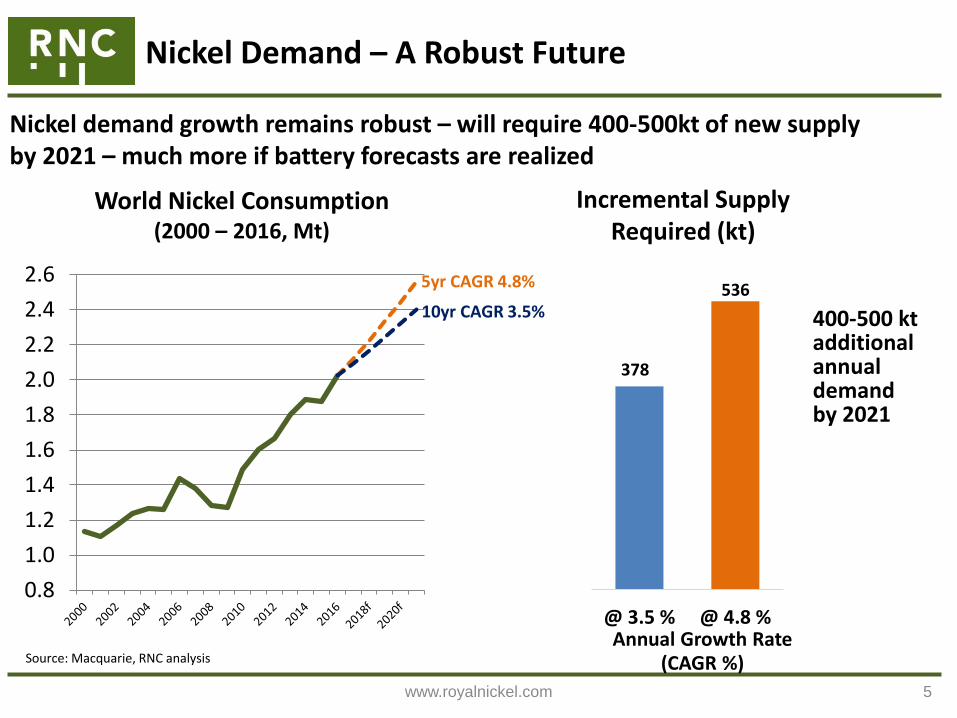

World Nickel Consumption (2000 – 2016, Mt)

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

400-500 kt additional annual demand by 2021

5yr CAGR 4.8%

10yr CAGR 3.5%

2,024

2,402

Nickel demand growth remains robust – will require 400-500kt of new supply by 2021 – much more if battery forecasts are realized

378

536

@ 3.5 % @ 4.8 %

Incremental Supply Required (kt)

Annual Growth Rate (CAGR %)

Nickel Demand – A Robust Future

www.royalnickel.com

Nickel Supply Shifting from the “Old Guard” to “Higher Risk”

6

2016 (2.0 Mt)

Nickel supply increasingly dependent on higher political risk countries as “Old Guard” has declined from 50% of global supply in 2006 to less than a third today

Source: CRU

11% 10%

7% 10% 4%

21% 21%

11% 16%

12%

12% 8%

5% 2% 5% 5% 4% 2%

15% 18%

Indonesia

New Caledonia

Philippines

Russia

Canada

Australia

China Colombia

Other

2006 (1.4 Mt)

Cuba

“Old Guard”

“Higher Risk”

Mined Nickel Production by Country — 2006 vs 2016

www.royalnickel.com

7

24%

76%

2016

40%

60%

2005

Other

Other

“The Big Six” Sulphide

“Big Six” Nickel Production (% of Total Supply)

Source: Company, Reports, Macquarie Research, Wood Mackenzie, RNC Analysis

“Big Six” Nickel Production (% of Total Supply)

“The Big Six” Sulphide

Nickel Supply Continued Decline of the “Big Six”

Nickel supply from the six largest sulphide producers was still 40% of global supply as late as 2005 – their influence continues to decline

www.royalnickel.com

8

Nickel Supply Decline of the “Big Six”

0102030405060708090

100

Mount Keith + Leinster Ni Production (kt)

0

20

40

60

80

100

Voisey’s Bay Ni Production (kt)

0

20

40

60

80

100

Vale Sudbury Ni Production (kt)

Source: Company reports, CRU, Wood Mackenzie

0

20

40

60

80

100

Vale Manitoba Ni Production (kt)

0102030405060708090

100

Jinchuan Ni Production (kt)

-6%

-32%

-17%

* 2017 guidance is 206-211 kt

180190200210220230240

Norilsk Ni Production (Polar + Kola, kt)

*

-1%

+14%

Nickel decline from the 6 largest sulphide operations has declined over the last decade (excluding Vosiey`s Bay ramp-up) as low nickel prices deterred investment

www.royalnickel.com

Nickel Supply – HPAL/FeNi Billion Dollar Ramp-ups

9

Source: Company reports

0

10

20

30

40

50

2012 2013 2014 2015 2016

Ambatovy

0

10

20

30

40

50

2012 2013 2014 2015 2016

Vale New Caledonia (Goro)

0

10

20

30

40

50

2012 2013 2014 2015 2016

Koniambo

0

10

20

30

40

50

2012 2013 2014 2015 2016

Ramu

The amount of additional nickel supply from the billion dollar laterite projects of the last decade is relatively uncertain…

www.royalnickel.com

Nickel Supply – Established HPAL Producers

10

Source: Company reports

0

10

20

30

40

2012 2013 2014 2015 2016

Murrin Murrin

0

10

20

30

40

2012 2013 2014 2015 2016

Ravensthorpe

05

10152025303540

2012 2013 2014 2015 2016

Moa Bay

…While established HPAL producers are facing challenges to maintain existing production levels

www.royalnickel.com

11

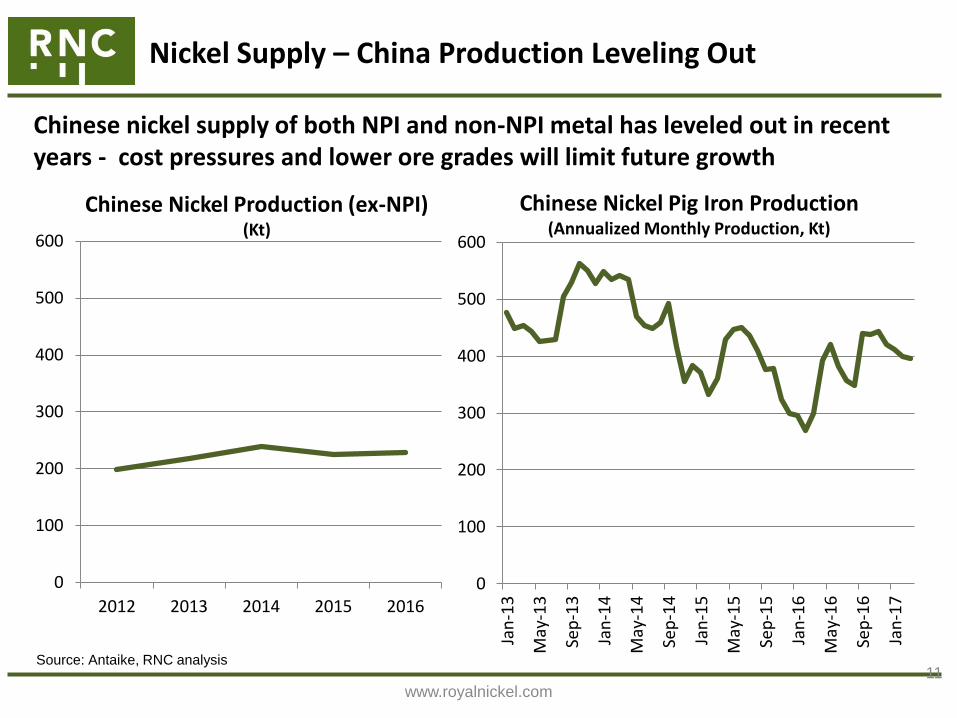

Nickel Supply – China Production Leveling Out

Source: Antaike, RNC analysis

Chinese nickel supply of both NPI and non-NPI metal has leveled out in recent years - cost pressures and lower ore grades will limit future growth

Chinese Nickel Pig Iron Production (Annualized Monthly Production, Kt)

0

100

200

300

400

500

600

Jan

-13

May

-13

Sep

-13

Jan

-14

May

-14

Sep

-14

Jan

-15

May

-15

Sep

-15

Jan

-16

May

-16

Sep

-16

Jan

-17

0

100

200

300

400

500

600

2012 2013 2014 2015 2016

Chinese Nickel Production (ex-NPI) (Kt)

www.royalnickel.com

Nickel Supply One-Time Benefits from Oil/Currency Largely Exhausted

12

Source: Thompson Reuters, Bloomberg

$0.60

$0.70

$0.80

$0.90

$1.00

$1.10

2012 2013 2014 2015 2016

Canadian $

$0.60

$0.70

$0.80

$0.90

$1.00

$1.10

2012 2013 2014 2015 2016

Australian $

6.0

6.2

6.4

6.6

6.8

7.0

2012 2013 2014 2015 2016

Chinese Yuan

20

40

60

80

2012 2013 2014 2015 2016

Russian Rouble

Nickel supply / costs benefited greatly from the decline in currency/oil prices over the last five years sustaining production as nickel prices fell

$40

$60

$80

$100

$120

2012 2013 2014 2015 2016

Oil WTI (US$)

www.royalnickel.com

Where is new project supply going to come from?

13

Nickel Supply - Little Momentum in Existing Supply & “Project Cupboard” Largely Empty

Source: CRU, RNC Analysis

By 2021, 400-500 kt of new supply is required, but “project cupboard” is empty — few projects in pipeline and 35+ years of inertia to overcome

TSX: RNX

Laterites – HPAL?

Laterites – FeNi?

NPI?

Sulphides?

400-500+ kt New

Supply Required

www.royalnickel.com

New Nickel Supply: Laterites – HPAL? Too High Cost, Too Much Risk?

HPAL projects not expected to play a major role in nickel supply going forward

HPAL projects have faced large capital overruns, delays, and commissioning issues. Industry will have little appetite for new projects

Improved Cobalt prices will help economics to some extent

Operating costs for many HPAL operations remain high

Operating costs are much higher than many other companies are indicating for their projects

Many jurisdictions with the most attractive resources for HPAL continue to be among the more difficult jurisdictions globally

Indonesian change in ban and domestic investment rules will not help investment case

14

Source: CRU, RNC analysis

www.royalnickel.com

New Nickel Supply: Laterites – FeNi? Little High Grade Left to Be Developed?

FeNi also not expected to play a major role in nickel supply going forward as the highest grade resources are already being developed and no new high grade discoveries have been made

The current set of projects have now developed ALL known saprolite deposits with large resource of 2%+ average grade or higher (Koniambo, Onca Puma, Barro Alto, Tagaung Taung)

NO NEW HIGH GRADE LATERITE DISCOVERIES HAVE BEEN MADE IN MORE THAN 30 YEARS TO REPLACE THESE PROJECTS IN THE PROJECT PIPELINE

Tagaung Taung was discovered in early 1980s, Onca Puma in the 1970s, Barro Alto in the 1960s and Koniambo in the 1900s

With several projects with grades 2%+ incurring multi-billion dollar price tags, what will capital cost of next generation of projects be ?

15

Source: CRU, RNC analysis

www.royalnickel.com

New Nickel Supply Sulphides — A Potential Answer, But Few Projects in Pipeline

Nickel sulphides are an attractive source of nickel production, but the pipeline is largely empty as there have been few new large scale discoveries. RNC’s Dumont project and First Quantum’s Enterprise projects are among the few large scale projects that could be in production with next few years

Over last several decades, the only large greenfield discoveries have occurred when exploration was occurring for other metals: Voisey’s Bay (diamonds), Kabanga (gold), Enterprise (copper)

Sirius Resources Nova-Bollinger discovery in Australia and Anglo American’s Sakatti discovery in northern Finland are the only large greenfield nickel discoveries made during a nickel-focused exploration program in recent decades

Sulphides have a number of inherent advantages over laterites

Typically use standard mine/mill facilities utilizing commonly used technology

Inherently less energy intensive to refine

Less capital intensive as smelting/refining facilities don’t typically need to be constructed

In the mid-1990s, Mt. Keith showed that large scale, lower grade, ultramafic nickel deposits could be profitably developed

Further growth in sulphide nickel production will likely come from large scale, lower grade deposits (following similar moves in both the copper and gold industries) such as RNC’s Dumont project, one of few large scale projects that could be in production by 2020

16

www.royalnickel.com

17

Ferro-nickel puck produced from

Dumont concentrate

Significant potential benefits to producers of suitable nickel sulphide concentrate feed such as RNC’s Dumont Project:

Lower costs due to simpler processing compared to traditional smelting and refining

Higher payabilities than traditional smelting and refining

Greater flexibility for more potential partners and customers

Roasted nickel concentrate is effectively a very high grade laterite ore feed – creates new source of demand for nickel sulphide concentrate, notably at a time when many NPI and ferronickel producers face feed shortages as a result of Indonesia’s nickel ore export ban

RNC’s strategic alliance with Tsingshan led to the development of the first integrated nickel pig iron (“NPI”) plant to directly utilize nickel sulphide concentrate as part of the stainless steel production process through concentrate roasting

Nickel Supply – RNC’s NiCal Roasting Process - A Significant Breakthrough

www.royalnickel.com

RNC foresaw significant growth in NPI and stainless production; however, recent Indonesian moves jeopardize future growth in the one area of nickel supply seeing active investment

The ban achieved many objectives with substantial investment in nickel capacity and downstream stainless steel production

Indonesian nickel production was expanding rapidly and it had became a global scale stainless steel producer

The relaxation of the ban and further changes to investment rules cause substantial investment uncertainty

18

Source: Company reports

Nickel Supply Indonesian Moves Create Significant Uncertainty

www.royalnickel.com

Nickel Supply —

Little Project Development for 35+ Years Today’s “empty cupboard” is a result of inertia from 35 years of relatively little project development after “nickel boom” in late 1960s (which discovered or advanced the development of many of the projects sitting in cupboard in 2001)

19

5.2%

1.4% 1.6% 1.4%

1.3%

1.7% 1.2%

2.8%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

1965-75 1975-90 1990-00 2000-10

Global Nickel Supply Growth “Traditional” vs. Alternative

1965–2010 (% CAGR)

< 2% growth for 35 years!

1965–75 saw a burst of new projects driven by inability of existing operations to meet global demand

1975–90 saw significant project rationalization

Collapse of former Soviet Union demand (20% of world total) provided supply during 1990s

Ni pig iron and demand destruction in 2000–10 closed gap caused by lack of new supply from weak project pipeline development

Stainless

Demand

Destruction

NPI

FSU

Collapse

Japan

FeNi

Source: Wood Mackenzie, Macquarie, RNC Analysis

www.royalnickel.com

Nickel Supply Many Projects Sitting in “Cupboard” For Decades

The bulk of the current wave of projects developed during last cycle were known for many decades: either discovered/developed too late during the 1965–75 period or inferior to other projects that were developed

Most of current project wave has sat “in the cupboard” for many decades (even back to the beginning of the last century)

20

Project Discovery

Koniambo Early 1900s

Goro Early 1900s

Ramu Early 1960s

Ambatovy Early 1960s

Barro Alto Early 1960s

Onca Puma Mid 1970s

Talvivaara Early 1980s

www.royalnickel.com

Nickel Supply Project Pipeline Largely Empty

21

The fundamental issue facing the nickel industry in 2017 is an empty “project cupboard” outside Indonesia At the beginning of the last decade prior to the significant run-up in nickel prices, the

“project cupboard” was very full with many projects known for decades Today’s picture is very, very different – few large scale feasibility study stage projects

Project Cupboard 2001 (20+kt)

TOTAL: 500+ kt

Project Cupboard 2017 (20+kt) TOTAL: ???

Barro Alto

Koniambo

Onca Puma

Tagaung Taung

Ambatovy

Goro

Ramu

Ravensthorpe

Weda Bay

Talvivaara*

Kabanga

Voisey’s Bay Sulphide

Laterite (HPAL)

Laterite (ferronickel)

• Nova Bollinger ramping up

• Terrafame (Talvivaara) ramping up

• Enterprise built, but capacity used for copper

• Dumont one of few construction ready projects

• Indonesia – new projects future ?

www.royalnickel.com

22

Nickel market supply/demand has performed better than other base metals over the past 3 years

Nickel market will need another 400-500kt to meet trend nickel demand by 2021 (and significantly more if forecasts for batteries come anywhere close to expectations!) Equivalent to doubling Chinese NPI industry at its peak

Very little visibility into future supply - extended period of low prices has resulted in very few opportunities for new supply and more dependence on future growth from higher political risk areas Underinvestment led to flat to declining production at most large nickel operations

Old, deep operations take several years and hundreds of millions of dollars to ramp-up

Nickel supply becoming highly dependent on higher political risk countries (Indonesia, Philippines)

Remaining ramp-up from new large HPAL projects uncertain Indonesian developments create massive uncertainty for the most active source of

new supply Project cupboard outside Indonesia largely empty

Relaxation of Indonesian ban has hurt nickel market in near-term but setting stage for very robust long-term nickel market outlook

Overview