nexans group presentation oct 08 .ppt [mode de … presentation_oct20… · europe leader strategy...

TRANSCRIPT

Group presentation

October 2008

Safe Harbor

This presentation contains forward-looking statements relating to the Group’s expectations for futurefinancial performance including sales and profitabilityfinancial performance, including sales and profitability.

The forward looking statements contained in this presentation are dependent on known and unknownrisks, expectations and assumptions, uncertainties and other factors which may cause the Group’s actual

lt f d bj ti t b t i ll diff t f th i di t d b th f d l kiresults, performance and objectives to be materially different from those indicated by the forward lookingstatements.

These forward looking statements depend, amongst other things, on the following assumptions and risks :(1) the rates of economic growth in the areas where Nexans operates remaining at current levels until2009; (2) the continued strong demand of the energy infrastructure market, in particular in developingcountries, and in the Oil & Gas sector; (3) the possibility to pass on to final customers increases in thecosts of raw materials, energy and transport; (4) the management of risks associated with sales in turnkeycosts of raw materials, energy and transport; (4) the management of risks associated with sales in turnkeyprojects; (5) the effect of currency fluctuations being neutral; (6) the Company being able to modifycustomer and supplier payment terms relating to metals; (7) the Company being able to reduce its costbase through realization of restructuring actions in the anticipated time frame; (8) the Company being ablet hi d ti it i t (9) t ti f k t (10) th b f b t ti lto achieve productivity improvements; (9) retention of key customers, (10) the absence of substantialcapacity increases by competitors in Nexans’ key markets, (11) the Company successfully integratingacquisitions ; and (12) the Company being able to adapt its organization.

Investor relations :

Michel Gédé[email protected]

Angéline Afanoukoe [email protected]@nexans.com [email protected]

Tel: 33 1 56 69 84 81 - Fax: 33 1 56 69 86 40

AGENDA

I.I. Nexans in the Cable IndustryNexans in the Cable Industry

II.II. Financial performanceFinancial performance

III.III. Strategy & MT TargetsStrategy & MT Targets

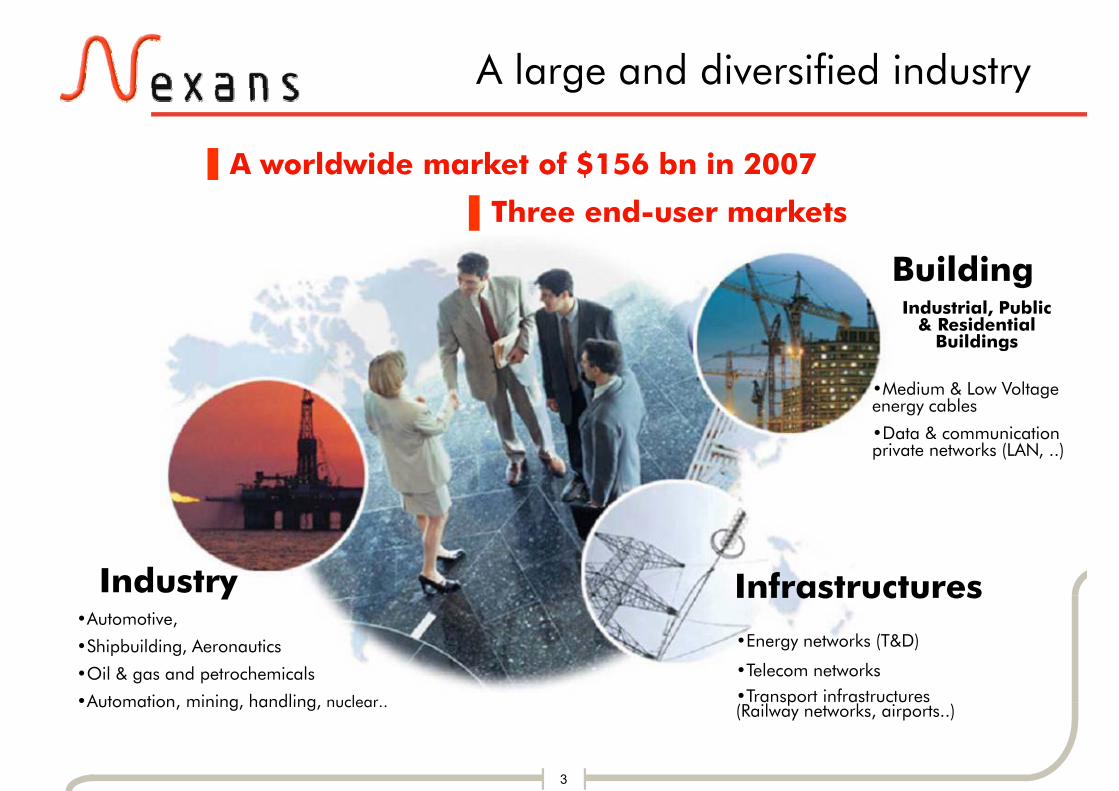

A large and diversified industryg y

▌A worldwide market of $156 bn in 2007

B ildi

▌ $

▌Three end-user markets

BuildingIndustrial, Public

& Residential Buildings

•Medium & Low Voltage energy cables

•Data & communication a a co u ca o private networks (LAN, ..)

Industry InfrastructuresA t ti

•Energy networks (T&D)

•Telecom networks•Transport infrastructures

•Automotive,

•Shipbuilding, Aeronautics

•Oil & gas and petrochemicals

•Automation mining handling nuclear

3

p(Railway networks, airports..)•Automation, mining, handling, nuclear..

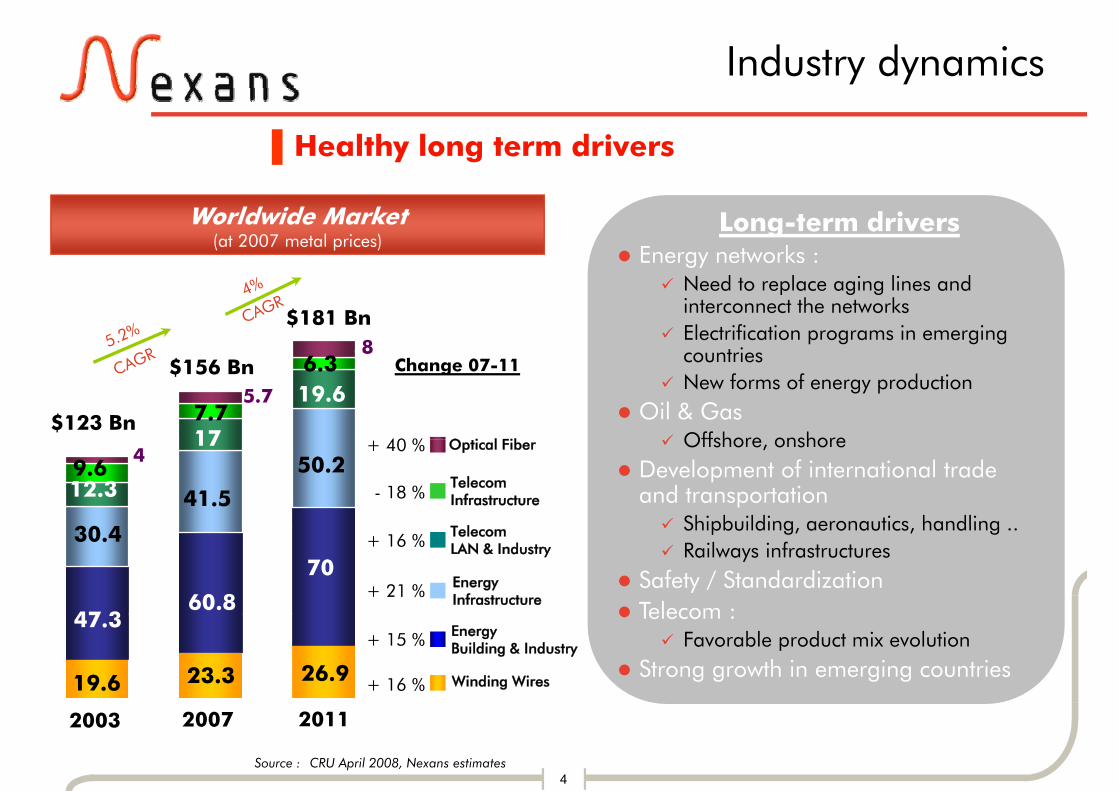

Industry dynamics

▌Healthy long term drivers

Worldwide Market(at 2007 metal prices)

Long-term driversEnergy networks :

$181 Bn8

gyNeed to replace aging lines and interconnect the networksElectrification programs in emerging

t i$156 Bn

7.7

6.3

17

19.65.7

8Change 07-11

40 % O i l Fib$123 Bn

countriesNew forms of energy production

Oil & GasOffshore onshore

41.5

50.217

- 18 %Telecom Infrastructure

T l

+ 40 % Optical Fiber

30 4

9.612.3

4Offshore, onshore

Development of international tradeand transportation

Shipbuilding aeronautics handling

+ 21 %60.8

70Energy Infrastructure

+ 16 % Telecom LAN & Industry

47 3

30.4 Shipbuilding, aeronautics, handling ..Railways infrastructures

Safety / StandardizationTelecom :

26.923.3

+ 15 %

Winding Wires+ 16 %

Energy Building & Industry

47.3

19.6

Telecom : Favorable product mix evolution

Strong growth in emerging countries

4Source : CRU April 2008, Nexans estimates

201120072003

Nexans:the world-wide market leaderthe world wide market leader

2007 Cable & Wire sales in M€main listed players

8,005(6,512 exc.

EW)Madeco W&C(proforma for Nexans, GC and LS)

4,300ePDIC

5,118

4,800eo/w SE~ 2,200e

PDIC

1,4841 409

2,816

2,367 ,

3,300e

2,300eCommscopeBelden

1,409

GC Prysmian Draka Leoni 2,300e2,000e

1,549

pGC y

El Sewedy

1,198

SEI TaihanFujikuraFurukawaLS

El Sewedy Cables

Automotive wiring systemsbreakdown non availableTelecom Cables

5

Sources : Financial communication of corresponding companies, Nexans estimates

Energy CablesElectrical Wires Note : 1 € = 1.37 USD

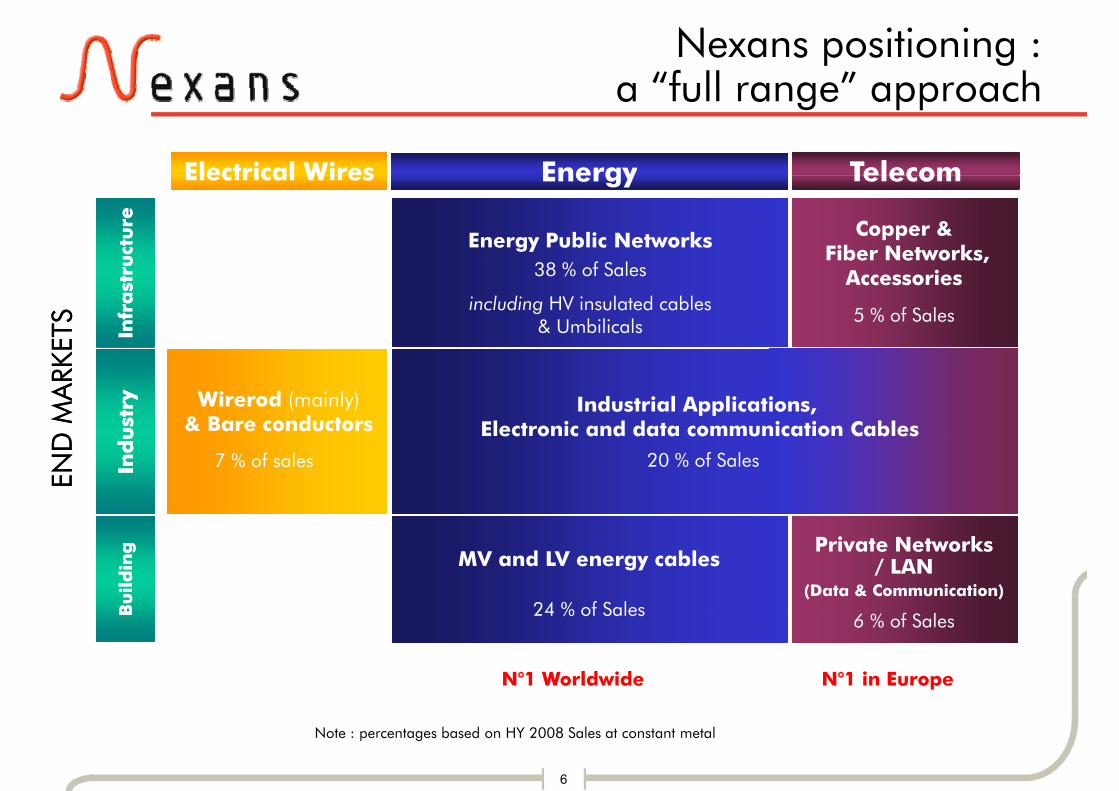

Nexans positioning : a “full range” approacha full range approach

Electrical Wires TelecomEnergyElectrical Wires

Energy Public Networks Copper &Fiber Networks, u

ctu

reu

ctu

re

38 % f S l

TelecomEnergy

ETS

ETS

Accessoriesincluding HV insulated cables

& UmbilicalsInfr

ast

ruIn

fra

stru 38 % of Sales

5 % of Sales

D M

ARK

D M

ARK

Wirerod (mainly)& Bare conductors

Industrial Applications,Electronic and data communication Cablesu

stry

ust

ry

END

END

7 % of sales Ind

Ind

20 % of Sales

MV and LV energy cablesPrivate Networks

/ LAN (Data & Communication)

Bu

ild

ing

Bu

ild

ing

24 % of Sales6 % f S l

N°1 Worldwide N°1 in Europe

24 % of Sales6 % of Sales

6

Note : percentages based on HY 2008 Sales at constant metal

A multi-regional strategy

Our markets are of multi-regional naturewith a need for local presence

Europe Leader strategy

with a need for local presence

p51 % of sales*

h ll l

gyAbove 10% market shares

Challenger position, present only in selected business segments :

Strong positions in Canada (Energy) 15% f LAN k t i th USA

North America17 % of sales*

15% of LAN market in the USA

Selective approach in North-East AsiaAsia-Pacific Profitable market shares on selected

business (HV, Shipyards, ..)Leading player in Australasia

Asia-Pacific12 % of sales*

Leading player on selected regionsMiddle East South America

ROW20 % of sales*

7

Middle East, South America20 % of sales

* based on 2007 Sales by destination, at actual metal prices – proforma with Madeco

AGENDA

I.I. Nexans in the Cable IndustryNexans in the Cable Industry

II.II. Financial performanceFinancial performance

III.III. Strategy & MT TargetsStrategy & MT Targets

Nexans is growing faster than its marketsthan its markets

organic growth of Cable activities +9 3% /yearorganic growth of Cable activities +9.3% /yearsince 2003 vs +5.2% market CAGR (*)

S l

I M€

Sales (at constant metal prices)

Organic growth by cable In M€ types

4,822

2003 2007

3,924

9

(*) Compounded Annual Growth rate

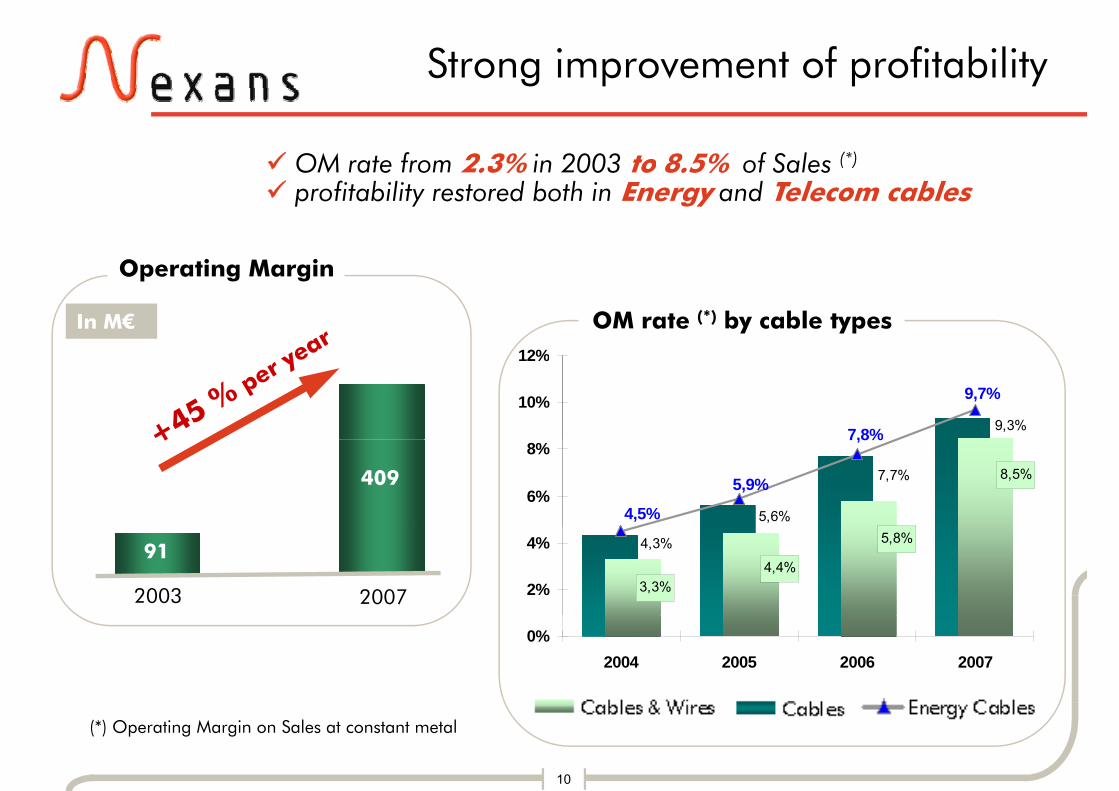

Strong improvement of profitability

OM rate from 2.3% in 2003 to 8.5% of Sales (*)

O ti M i

profitability restored both in Energy and Telecom cables

12%

Operating Margin

In M€ OM rate (*) by cable types

9,3%

9,7%

7,8%

10%

12%

5,6%

7,7% 8,5%

4,5%

5,9%

7,8%

6%

8%

409

4,3%

3,3%4,4%

5,8%

2%

4%

20072003

91

0%2004 2005 2006 2007

10

(*) Operating Margin on Sales at constant metal

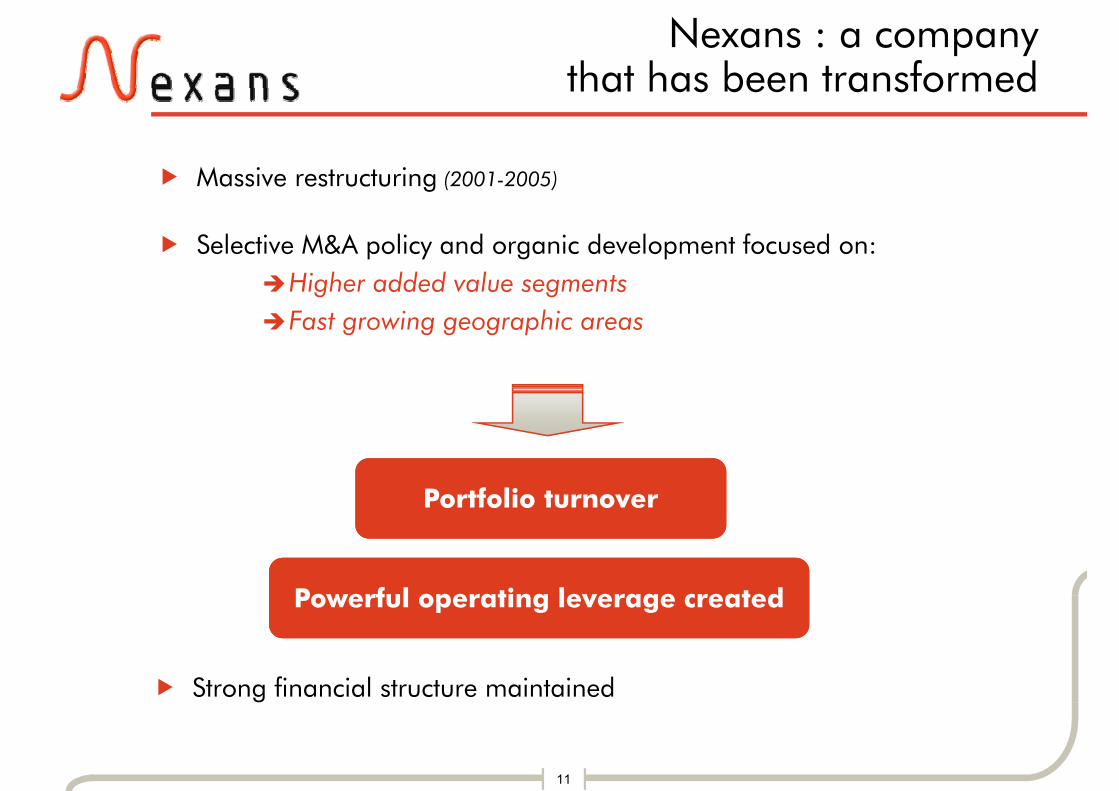

Nexans : a company that has been transformedthat has been transformed

Massive restructuring (2001 2005)Massive restructuring (2001-2005)

Selective M&A policy and organic development focused on:Higher added value segmentsFast growing geographic areas

Portfolio turnoverPortfolio turnover

Powerful operating leverage createdPowerful operating leverage created

Strong financial structure maintained

11

Geographic & business mix re-orientationDivestituresDivestitures

Distribution NorwayJune 2005Winding Wires USA

TianjinJuly 2007

August 2004

SimcoeApril 2007

Winding Wires EuropeFebruary 2005 February 2005 January 2007

AgroMay 2002

Distribution SwitzerlandFebruary 2006

Telecom CopperSantander

12

590 M€ yearly sales OUT590 M€ yearly sales OUTFebruary 2008Santander

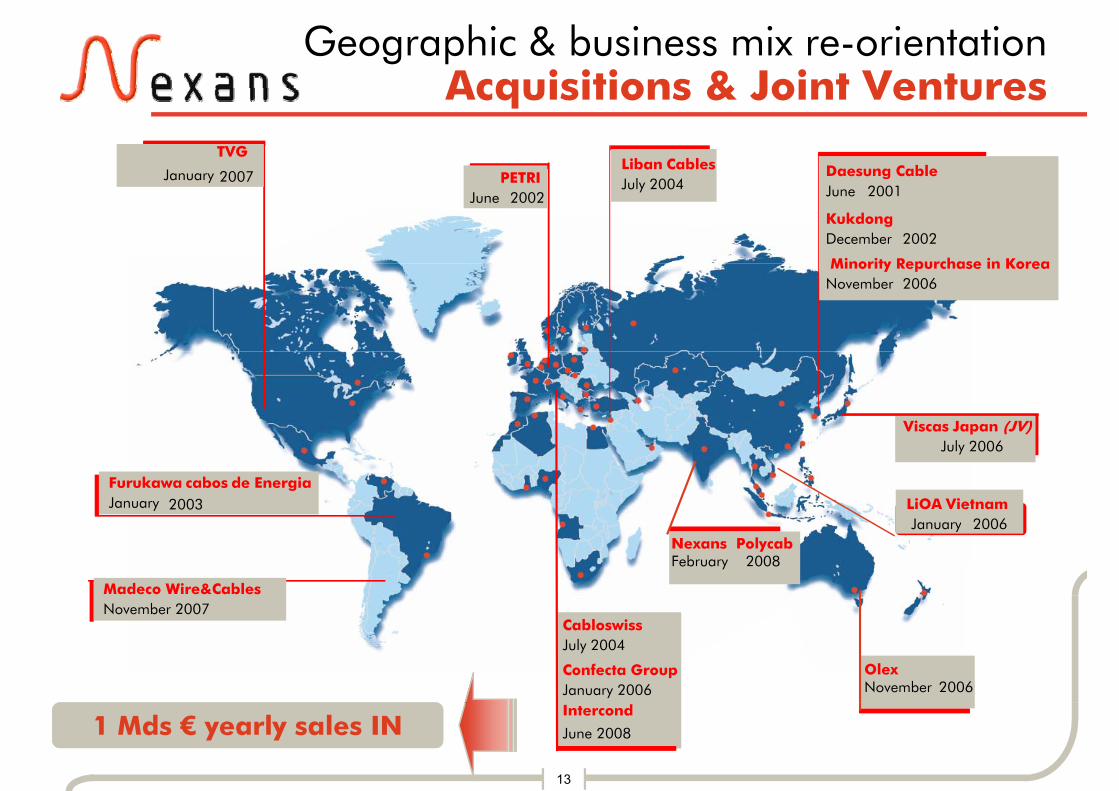

Geographic & business mix re-orientationAcquisitions & Joint VenturesAcquisitions & Joint Ventures

Liban CablesPETRI Daesung Cable2007

TVG

JanuaryJuly 2004PETRI

June 2002

Minority Repurchase in Korea

KukdongDecember 2002

Daesung CableJune 2001

2007January

Minority Repurchase in Korea November 2006

Viscas Japan (JV)

LiOA VietnamJanuary 2006

July 2006

Furukawa de EnergiaJanuary

cabos2003

January 2006Nexans PolycabFebruary 2008

Madeco Wire&CablesNovember 2007

OlexNovember 2006

Confecta GroupJanuary 2006

CabloswissJuly 2004

13

1 Mds € yearly sales IN1 Mds € yearly sales IN June 2008

Intercond

Higher exposure to specialty products

2,328

1,7301,932In M€

•Naval Shipboard•Automotive•Robotics•N l

OEMs

430327386

476BUILDING

•LAN•S f t

+ 18 %

+ 9 %

+ 23 % •Nuclear•Handling

Specialty Product

of which 430327393362

•Safety•Heating cables

+ 9 %

•High Voltage•U bili l

INFRASTRUCTURE+ 22 %

+ 9 %

Priority segments:893661 734+ 11 %

•Umbilicals•Energy accessories•Railway•xDSL•FTTx•Windmill

Priority segments:

Specialty products in Sales : 41 % 43 % 48 %

2005 2006 2007

Development plan in place for each priority segment

Constant monitoring through Country organization

in Sales :

14

Co s a o o g oug Cou y o ga a o

Primary target of M&A operations

Higher exposure to fast growing areas

Sales from high growth areas (*)Sales from high growth areas ( )at constant metal price (M€)

1 280X 6 in 5 years

860

+ 49 %X 6 in 5 years

• 30% through internal growth

• 70% through acquisitions

522

+ 65 %

+ 140 %

86070% through acquisitions

in M€

218

+ 140 %in M€

2006Pro-forma with Olex

2002 2005 2007Pro-forma with Madeco (**)

% of totalSales :

12 % 18 % 25 %5 %

15

(*) Including China, Vietnam, South Korea, Middle-East, Morocco, Australasia and Latin America(**) based on estimated 2007 Sales for Madeco, 1 € = 1.35 USD

Strong financial structure protectedg p

J 30 08D 31 07 June 30, 08Dec. 31, 07(in Million €)

Long term fixed assets 1,192 1,209of which goodwill 192 201gDeferred tax assets 48 45Non-current assets 1,240 1,254Working capital 1,222 1,556g p , ,Assets (net) held for sale 105 1

Total to finance 2,567 2,811

Net financial debt 290 457reserves 434 448Deferred tax liabilities 85 105Shareholder’s equity and Minority interests 1,758 1,801

Total financing 2,567 2,811

Gearing 25 %Leverage (Net debt / 12m EBITDA) = 0 8 x

Gearing 25 %Leverage (Net debt / 12m EBITDA) = 0 8 x

16

Leverage (Net debt / 12m EBITDA) = 0.8 xLeverage (Net debt / 12m EBITDA) = 0.8 x

AGENDA

I.I. Nexans in the Cable IndustryNexans in the Cable Industry

II.II. Financial performanceFinancial performance

III.III. Strategy & MT TargetsStrategy & MT Targets

Our medium term objectivesj

A Nexans group:

More Profitable

Less Cyclical

More Streamlined

With more Synergies between businessesWith more Synergies between businesses

18

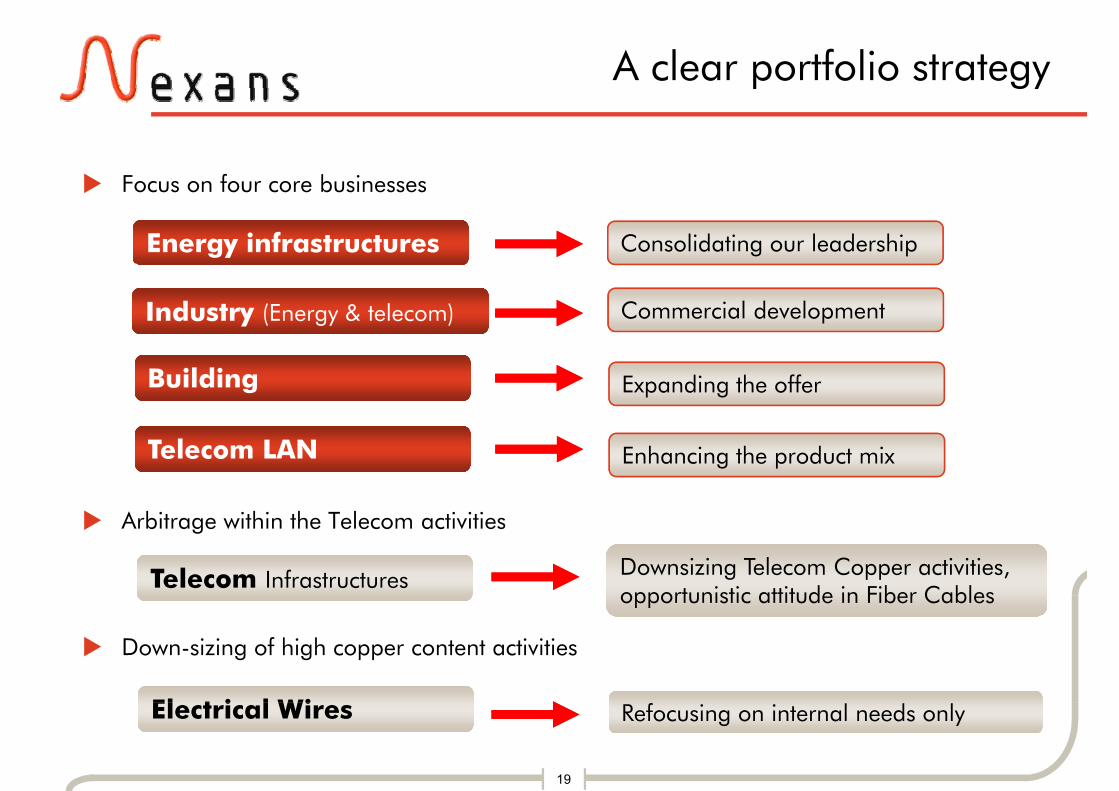

A clear portfolio strategy

F f b i

p gy

Focus on four core businesses

Energy infrastructuresEnergy infrastructures Consolidating our leadershipConsolidating our leadership

Industry (Energy & telecom)Industry (Energy & telecom) Commercial developmentCommercial development

BuildingBuilding Expanding the offerExpanding the offer

l l

Arbitrage within the Telecom activities

Telecom LANTelecom LAN Enhancing the product mixEnhancing the product mix

Arbitrage within the Telecom activities

Telecom InfrastructuresTelecom Infrastructures Downsizing Telecom Copper activities, opportunistic attitude in Fiber CablesDownsizing Telecom Copper activities, opportunistic attitude in Fiber Cables

Down-sizing of high copper content activities

El t i l WiEl t i l Wi

19

Electrical WiresElectrical Wires Refocusing on internal needs onlyRefocusing on internal needs only

Energy infrastructure: greater visibility and improved profitabilityvisibility and improved profitability

Marked increase in order b kl

Solid fundamentalsbacklog

Position of co-leader in the world

Powerful growth drivers :2 years' businessin High Voltage 1 year

2004

Network renovationNew energy sourcesEmerging economies 2007

g gand Umbilical

1 year

Increasing weight of HighAppropriate resources

Emerging economies

g g gVoltage(12 % of Sales in 2007)

Capacity X 2 in two yearsfor HV submarine+ 45%~ 570 M€

I 2008

Submarine & umbilical

~ 390 M€

In 2008 :

- Sustained growth

- Increasing contribution to Group

umbilical

Underground

Aerial

20

Increasing contribution to Group profits2005 2006 2007

Industry: High potential for growth and profitabilityfor growth and profitability

Appropriate resources Backed by growth sectors

Oil & Gas :2007/2011 Capex of this industry increased by 25% vs 2002/2006 period

New sales organization for global marketsMulti-site offering structure by 25% vs 2002/2006 period

Shipyards : order backlog X 3in 5 years (Hyundai, Mitsubishi ...)

Multi site offering structureCapacity freed up by re-examining customer and product portfolios

1,005

805

in M€ + 42%Other Transportation :

Alstom : order backlog entries doubled in 2007

Petrochemicals & nuclear

706805 2007

Airbus 5 years' order backlog

Mining Industries

In 2007 : Profitability up sharplyHarnesses

O h

Transportation

In 2008 :

- Continued growth- Potential for higher marginsOP i t

Other industries

3 % 5 6 % 8 7 %

2005(*) 2006(*) 2007

21

Potential for higher marginsOP margin rate 3 % 5.6 % 8.7 %

(*) Restated for segmentation changes made in 2007

Building: strength of Nexans business modelNexans business model2002/2007 : a different business model

A balanced product mix

Residential

Industrial & Commercial

Building~65%

~35%

business model

Significant changes:

• D l t f d t tf li

residential US very limited : 30 M€/year

Construction ~35% • Development of product portfolios

• Geographic redistribution

• Industrial restructuring (Nexans = balanced breakdown in Europe

(Maintenance & renovation = 43 % of the market)

A geographical balance

g (26 M€ over 4 years)

A geographical balance

In % of Sales (*)

France Benelux 35 %In 2008 :

- Pressure on margins (observed in N th A i d lik l i E )

France - Benelux 35 %

Scandinavia 9 %

Other Europe 24 %North America and likely in Europe)

- Business model holding upNorth America 15 %

Asia-Pacific 7 %

Emerging economies 10 %

22

(*) at constant metal prices

Emerging economies 10 %

Telecom: clarified positioningp g

LANLAN

Systems offering under developmentConfirmed in

“Core B siness” acti itConfirmed in

“Core B siness” acti ity g pProgression of 10 Gigabit

“Core Business” activity“Core Business” activity

Fiber Optic

Growth opportunitiesGrowth opportunitiesRollout in progress in EuropeTechnology and service offeringPotential partnerships

Telecom copper Infrastructurepp

Lack of critical size Divestiture of Santander plant completed in May 2008

Divestiture of Santander plant completed in May 2008

23

Electrical Wires: ongoing down-sizingg g g

F t d i iFaster down-sizing

37 % reduction

Weight in Nexans Sales (*)

18 %in external sales in 2007

Improved margins(prices and costs control)

10 % of Sales18 %

(prices and costs control)

20072006

Optimized capital employed

Capital employed reduced to

Reduction program stepped up:

Reduction program stepped up:

p p y~180 M€ at December end 2007 Objective: minimal

external sales in 2009Objective: minimal

external sales in 2009

24(*) at constant metal prices

2009 objectives

Operating marginunder favourable

8,5%

~10% under favourable economic environment

4,4%5,8% ~ 7% under depressed

economic environment

2006 2007 200920082005

New targets including announced M&A operations

Achieved results

Free Cash Flow excluding metal impacts (*)

Organic growth of Cable activities

Achieved results

+8,2%

+12,1%+6%

/year

Sales

+ 33

+ 275

(74)

2005

2006 2007

+ 33

25

2005 2006 2007 20092008 (*) Free Cash Flow excl. metal = Cash from operations + ▲ WCR at constant metal – Capex - Dividends

Q3 ‘08 trading update :Sustained growth in cable activities Sustained growth in cable activities

7.4 % organic growth of cable activities (*) Sales (**)

by destination

Electrical Wires down-sizingAsia Pacific

North America

at Sept.’08 end

In M€

Sales at constant metal prices Rest of World

18%

17%

13%

1,166 1,165FX

Consolidation

Cable activities

(34)

52%

scope(10)

(34)75

Electrical Wires

(32)Europe

+ 7.4 %

26

(*) Excluding Electrical Wires

Q3 ’07 Q3 ‘08(**) at current metal prices

Outlook for 2008

A i ti ti f fi t h lf 2008 i t dAssuming continuation of first-half 2008 economic trends

Above 6 % organic growth in cable activities for the year

Increase of operating margin compared to 2007

Net debt between 500 M€ and 600 M€ after acquisitions financing (Intercond et Madeco) and including the cancellation financing (Intercond et Madeco) and including the cancellation of the harnesses divestiture

27

•Appendices

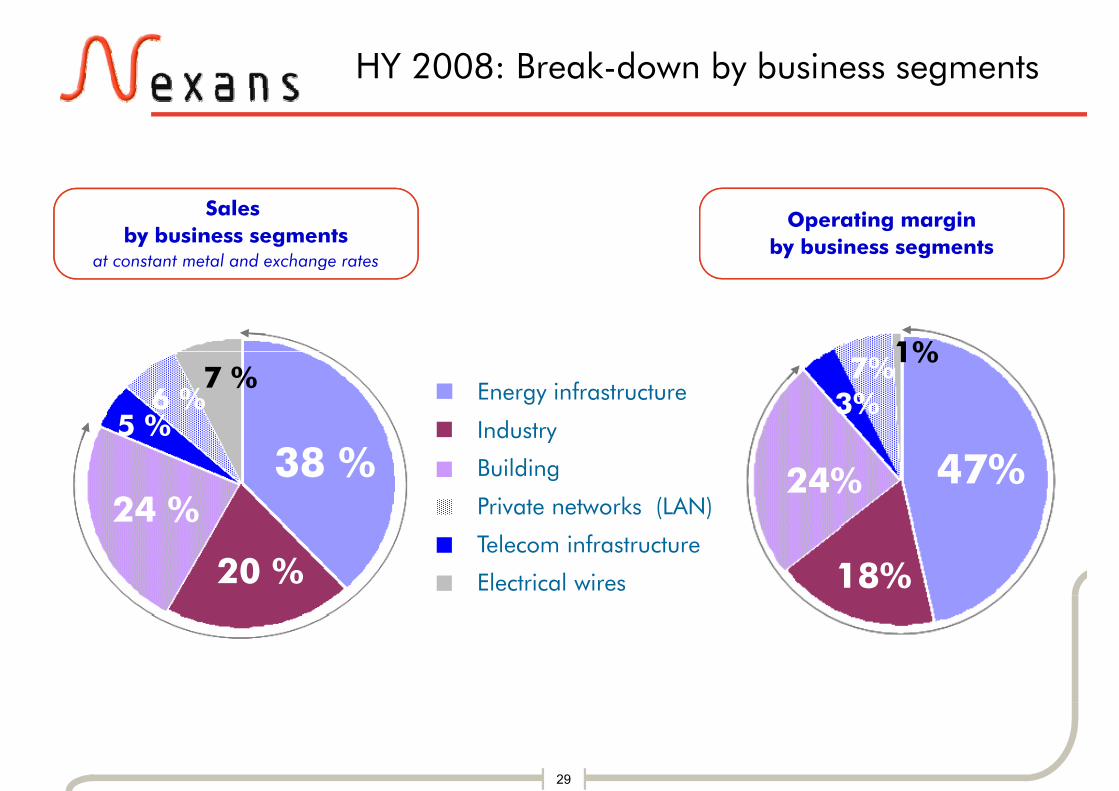

HY 2008: Break-down by business segments

Sales by business segments

at constant metal and exchange rates

Operating marginby business segments

at constant metal and exchange rates

1%

Industry

Energy infrastructure

5 %6 %

7 %3%7%1%

Building

y

Private networks (LAN)

38 %24 %

47%24%

Telecom infrastructure

Electrical wires20 % 18%

29

Sales & Operating margin by business

In M€ HY 2007 HY 2008

p g g y

In M€ HY 2007

Sales* OM

HY 2008

% Sales* OM %

Energy infrastructure 784 56 7.2 % 919 106 11.4 %

Industry 510 39 7.7 % 482 41 8.6 %

B ildi 589 65 10 9 % 571 55 9 7 % Building 589 65 10.9 % 571 55 9.7 %

Private network (LAN) 147 18 12.3 % 149 15 10.4 %

T l I f t t 129 9 7 1 % 118 8 6 8 % Telecom Infrastructure 129 9 7.1 % 118 8 6.8 %

Other 5 (4) - 5 (7) -

Total Cable 2 164 183 8 4 % 2 244 218 9 7 %Total Cable 2,164 183 8.4 % 2,244 218 9.7 %

Electrical Wires 287 4 1.4 % 175 2 1.1 %

Total Group 2,451 187 7.6 % 2,419 220 9.1 %

30

* Sales at constant metal prices

Very high growth in Energy networksEnergy networks

Organic growth of

Sustained

Organic growth of Cable activities 2007 Q1 Q2 HY ’08 Q3

Sustained Energy

infrastructureactivity

Energy infrastructure 10.2% 16.4 % 22.6 % 19.7 % 22.7 %

Industry 17.5 % 3.8 % 6.1 % 4.8 % - 2.3 %

Growth in

Industry 17.5 % 3.8 % 6.1 % 4.8 % 2.3 %

Building 10.4 % -0.7 % -7.7 % -4.2 % -3.5 %priority industry

segmentsPrivate networks (LAN) 13.9 % 2,5 % 3.4 % 3.2 % 2.7 %

Slow downin Building

increased by

Telecom infrastructure 9.9 % -8.5 % 3.5 % -2.2 % 1.5 %

increased by base effectTotal Cable 12.1 % 6.4 % 7.8 % 7.2 % 7.4 %

Electrical Wires - 32.8 % - 36.1 % -30.3 %

31

Higher profitability in two of our main core businessesin two of our main core businesses

Operating margin rate HY '07 HY '08Operating margin rate HY 07 HY 08

Energy Infrastructure 7.2 % 11.4 % Energy i f

Industry 7.7 % 8.6 %

infrastructure accelerating

Building 10.9 % 9.7 %

k ( AN)

Consolidationof industry

iPrivate networks (LAN) 12.3 % 10.4 %

Telecom infrastructure 7.1 % 6.8 %

margins

Total Cable 8.4 % 9.7 %

Building margins

holding up

Electrical Wires 1.4 % 1.1 %

Total Group 7.6 % 9.1 %

32

p

Highly reactive to cost hikesg y

Operating costsImpact

HY 2008 (*) Actions

8% SelectingOther fixed costs

∆ margin on variable costs HY ‘08/’07

4%13%

8% Increase under control

Productivity

Selectingcustomers

Other fixed costs

Payroll

Energy, transportationInfrastructure :

+ 2.4 pts ~ 20 M€ Partial

pass throughPlastics and components 15%

p

Industry : 0 6

60% ~ 40 M€Full

pass through

Copperand

Al i

+ 0.6 pt

Building :Aluminum Building :- 0.3 pt

(*) Impact of rising costs at HY 2008 vs 2007 average

HY ‘08: 3.3 Bn€ Group: + 2.7 pts100 %

33

Strong operating leverage maintained

Excluding Electrical Wires

g p g g

(in Million €) June 07 June 08Sales cable activities, at current metal prices 2,937 3,029

l bl 6Sales cable activities, at constant metal prices 2,163 80 2,243

Margin on variable costs 687 751

Margin on variable costs (%) 31.8 % 33.5 %

Indirect costs (*) (453) (481)

EBITDA (**) 234 270

EBITDA margin (%) 10.8 % 12 %

Depreciation (51) (52)

Operating margin cable activities 183 35 218

44 %

p g g

Operating margin rate (on Sales at constant metal prices) 8.4% 9.7%

34

(*) Includes factory indirect costs excluding Depreciation + R&D + SG&A

(**) Operating margin before depreciation

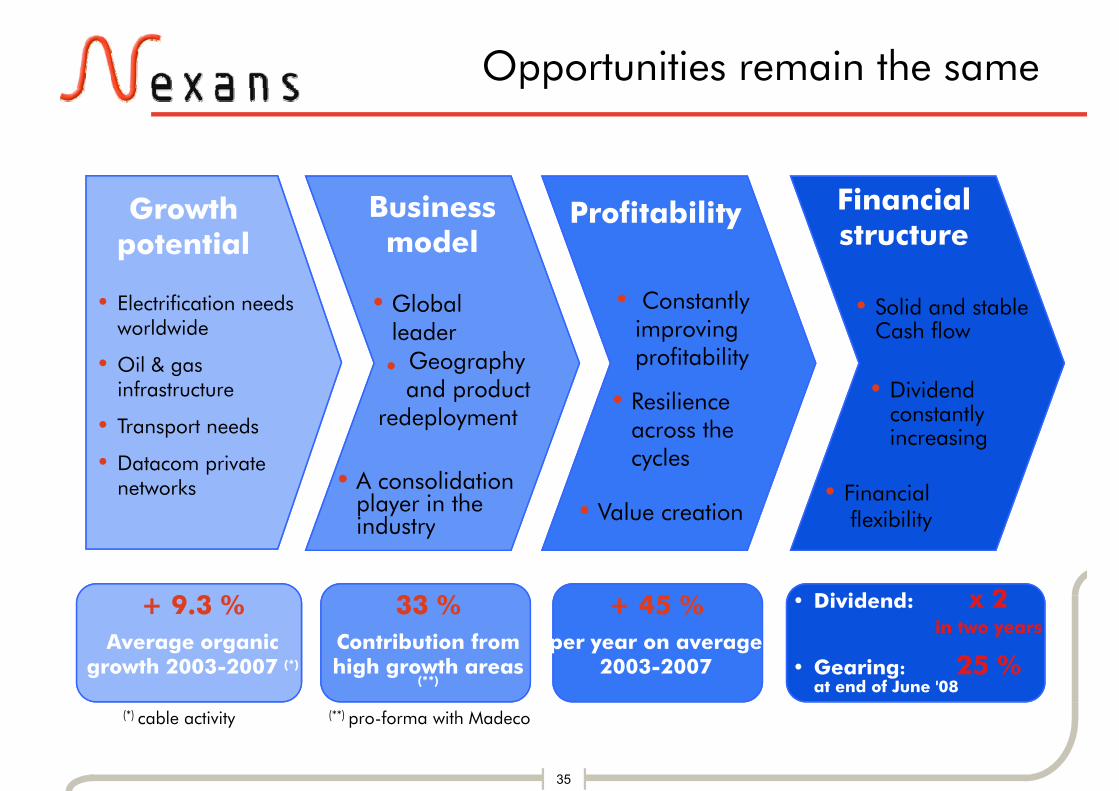

Opportunities remain the samepp

Growth potential

Business model

Profitability Financial structure

• Electrification needs worldwide

• Global leader

• Constantly improving

fit bilit

• Solid and stable Cash flow

h• Oil & gas infrastructure

• Transport needs

• profitability

• Resilience across the

• Dividend constantly increasing

Geographyand product

redeployment

• Datacom private networks • A consolidation

player in the industry

cycles

• Value creation

increasing

• Financialflexibilityindustry e b y

• Dividend: x 2+ 9.3 % 33 % + 45 %in two years

• Gearing: 25 % at end of June '08

Average organicgrowth 2003-2007 (*)

Contribution from high growth areas

(**)

per year on average 2003-2007

35

(**) pro-forma with Madeco(*) cable activity