navigating growth in africa - kantar uk. · the pyramid’ (bop) ... brand navigating growth in...

TRANSCRIPT

In Focus

Navigating growth in Africa

Opinion LeaderFinding faster growth: New markets

Share this

In Focus

2

Share this

Navigating growth in Africa

Introduction 03

Urbanisation: an easier target but not that easy 07

The opportunity for brands 15

Voices from Africa 20

Media and mobile 10

Weighing up growth prospects 18

1

2

4

6

3

5

In Focus

3

Share this

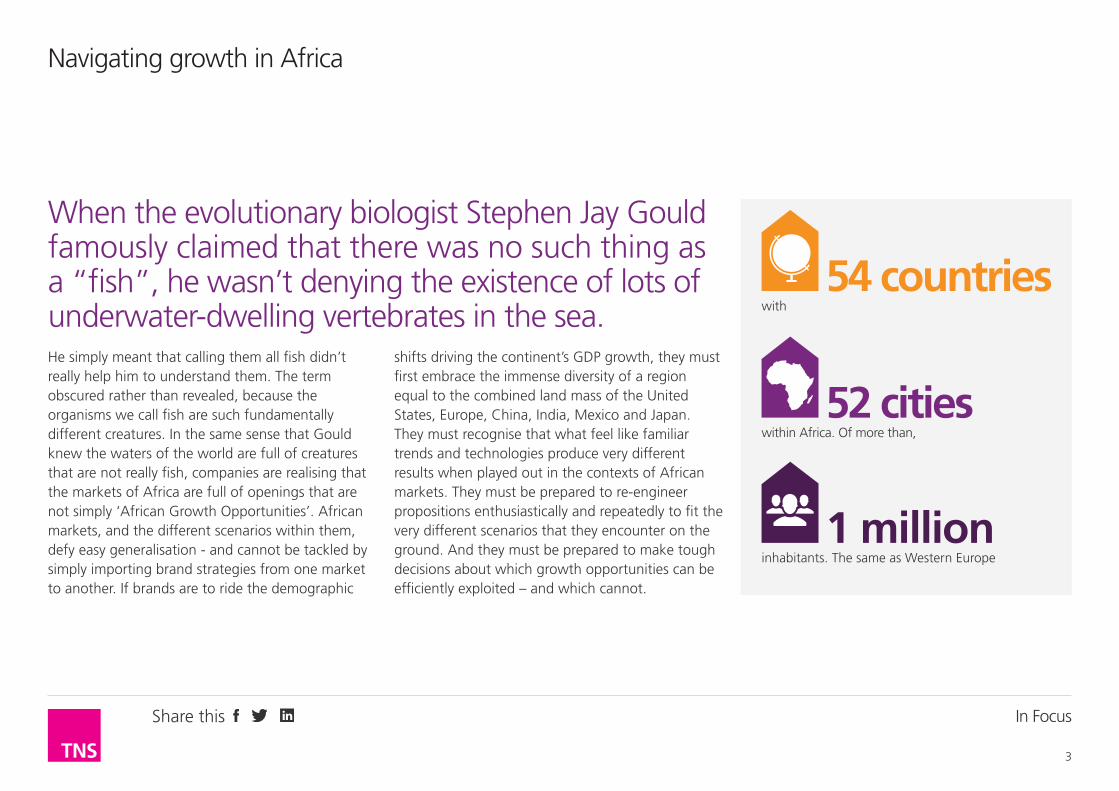

He simply meant that calling them all fish didn’t really help him to understand them. The term obscured rather than revealed, because the organisms we call fish are such fundamentally different creatures. In the same sense that Gould knew the waters of the world are full of creatures that are not really fish, companies are realising that the markets of Africa are full of openings that are not simply ‘African Growth Opportunities’. African markets, and the different scenarios within them, defy easy generalisation - and cannot be tackled by simply importing brand strategies from one market to another. If brands are to ride the demographic

Navigating growth in Africa

shifts driving the continent’s GDP growth, they must first embrace the immense diversity of a region equal to the combined land mass of the United States, Europe, China, India, Mexico and Japan. They must recognise that what feel like familiar trends and technologies produce very different results when played out in the contexts of African markets. They must be prepared to re-engineer propositions enthusiastically and repeatedly to fit the very different scenarios that they encounter on the ground. And they must be prepared to make tough decisions about which growth opportunities can be efficiently exploited – and which cannot.

inhabitants. The same as Western Europe

1 million

within Africa. Of more than,

52 cities

with

54 countries

When the evolutionary biologist Stephen Jay Gould famously claimed that there was no such thing as a “fish”, he wasn’t denying the existence of lots of underwater-dwelling vertebrates in the sea.

In Focus

4

Share this

The fluid border of the consumer economyThe border between poverty and this middle-class existence is a constantly shifting one, in Africa as in other emerging markets. Members of the’floating’ lower middle class face the ever-present danger of slipping back into poverty and their consumer attitudes overlap in many respects with those of the upper reaches of the BoP. An income of even $8 per day would represent immense hardship in the eyes of developed market consumers (it represents less than half the income of the recognised poverty line in the UK, for example). However, the increase in disposable incomes and consumer choice is expanding African markets, just as Africa’s demographic trends and new technologies enable brands to compete in them through new channels.

The opportunity in numbersEvidence of the value of African markets has been mounting relentlessly in recent years. Africa contributed six of the world’s ten fastest-growing economies between 2001 and 2010 and is projected to represent seven of the top ten between 2011 and 2015. Its GDP growth is expected to reach 5.7 percent in 2013, the highest for any global region. Foreign direct investment in the continent has increased by around 50 percent since 20051. Although 60 percent of Africa’s population continues to survive on less than $2 per day, these ‘Base of the Pyramid’ (BoP) consumers are emerging into the mainstream consumer economy at an increased rate, able to buy consumer goods on a reasonably regular basis. Over a third of the population in many countries now falls within the ‘middle class’, with an income of between $2 and $8 per day. McKinsey’s Lions on the Move study predicts that half of all African households will have some disposable income by 2020.

Navigating growth in Africa

50%

1/3

60%increase in foreign direct investment since 2005

of income is between $2 and $8 per day

of Africa’s population survives on less than $2 per day

In Focus

5

Share this

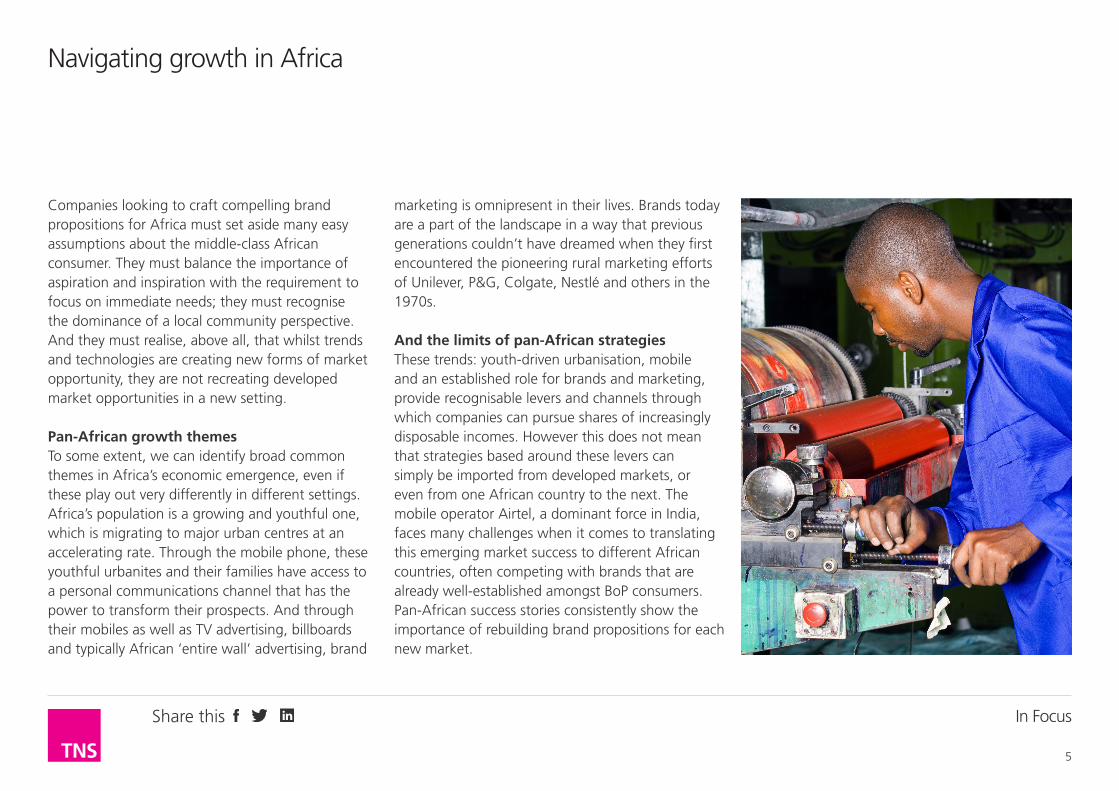

marketing is omnipresent in their lives. Brands today are a part of the landscape in a way that previous generations couldn’t have dreamed when they first encountered the pioneering rural marketing efforts of Unilever, P&G, Colgate, Nestlé and others in the 1970s.

And the limits of pan-African strategiesThese trends: youth-driven urbanisation, mobile and an established role for brands and marketing, provide recognisable levers and channels through which companies can pursue shares of increasingly disposable incomes. However this does not mean that strategies based around these levers can simply be imported from developed markets, or even from one African country to the next. The mobile operator Airtel, a dominant force in India, faces many challenges when it comes to translating this emerging market success to different African countries, often competing with brands that are already well-established amongst BoP consumers. Pan-African success stories consistently show the importance of rebuilding brand propositions for each new market.

Companies looking to craft compelling brand propositions for Africa must set aside many easy assumptions about the middle-class African consumer. They must balance the importance of aspiration and inspiration with the requirement to focus on immediate needs; they must recognise the dominance of a local community perspective. And they must realise, above all, that whilst trends and technologies are creating new forms of market opportunity, they are not recreating developed market opportunities in a new setting.

Pan-African growth themesTo some extent, we can identify broad common themes in Africa’s economic emergence, even if these play out very differently in different settings. Africa’s population is a growing and youthful one, which is migrating to major urban centres at an accelerating rate. Through the mobile phone, these youthful urbanites and their families have access to a personal communications channel that has the power to transform their prospects. And through their mobiles as well as TV advertising, billboards and typically African ‘entire wall’ advertising, brand

Navigating growth in Africa

In Focus

6

Share this

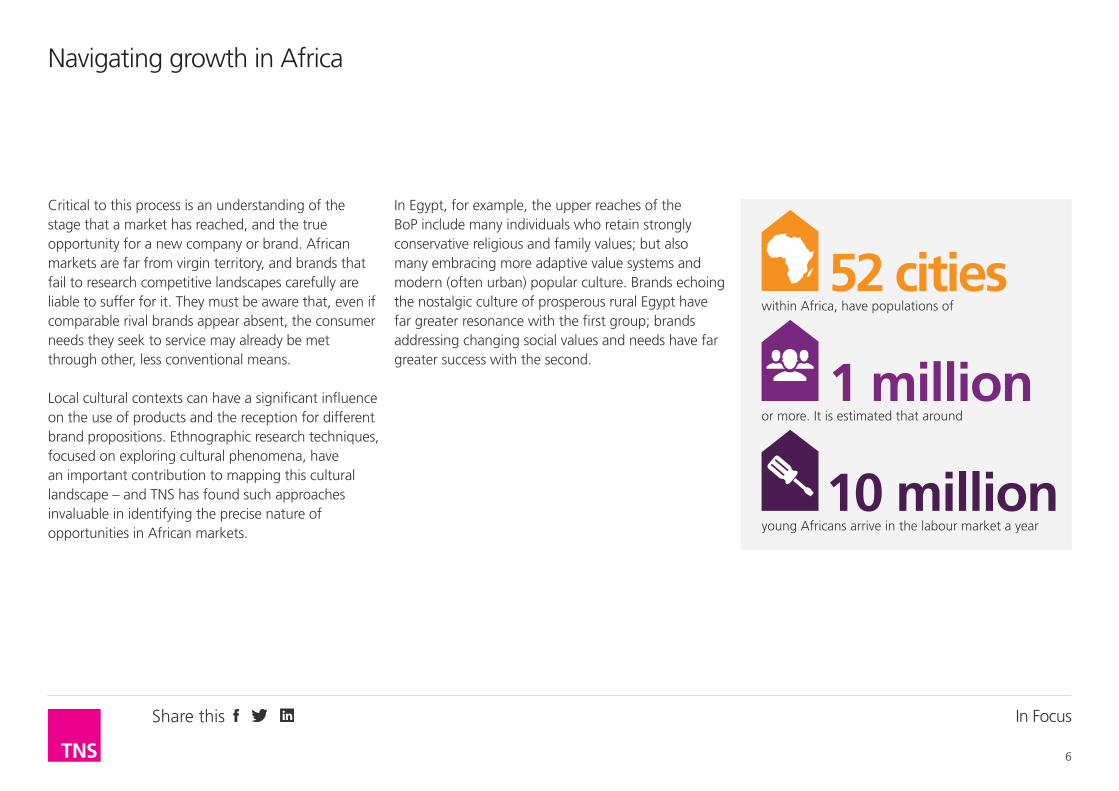

Critical to this process is an understanding of the stage that a market has reached, and the true opportunity for a new company or brand. African markets are far from virgin territory, and brands that fail to research competitive landscapes carefully are liable to suffer for it. They must be aware that, even if comparable rival brands appear absent, the consumer needs they seek to service may already be met through other, less conventional means.

Local cultural contexts can have a significant influence on the use of products and the reception for different brand propositions. Ethnographic research techniques, focused on exploring cultural phenomena, have an important contribution to mapping this cultural landscape – and TNS has found such approaches invaluable in identifying the precise nature of opportunities in African markets.

Navigating growth in Africa

In Egypt, for example, the upper reaches of the BoP include many individuals who retain strongly conservative religious and family values; but also many embracing more adaptive value systems and modern (often urban) popular culture. Brands echoing the nostalgic culture of prosperous rural Egypt have far greater resonance with the first group; brands addressing changing social values and needs have far greater success with the second.

52 cities

10 million

1 million

within Africa, have populations of

young Africans arrive in the labour market a year

or more. It is estimated that around

In Focus

7

Share this

Urbanisation: an easier target but not that easy

In Focus

8

Share this

Urbanisation: an easier target but not that easyFor brands, the accelerating urbanisation of Africa appears to provide more accessible target audiences for brand propositions by bringing concentrated populations within easy reach of product distribution and marketing. Africa today includes 52 cities with populations of 1 million or more; the same number as can be found in Western Europe. It is estimated that around 10 million young Africans arrive in the labour market each year – and many of these travel to rapidly growing cities in order to seek work. In doing so, they provide a large, concentrated audience that can be reached efficiently through outdoor media, served products without relying on unreliable African roads, and who can serve as a powerful conduit for brand advocacy, through the many Africans that return to their rural roots for short visits or longer stays. It is noticeable that Western multi-nationals such as P&G and Unilever have shifted research budgets from tracking the attitudes of rural population to gaining a deeper understanding of emerging urban consumers. For most brands, Africa’s cities now provide the obvious entry point to their surrounding markets.

Urbanisation: an easier target but not that easy

In Focus

9

Share this

Yet city life does not equate to developed market opportunities and standards of living, nor to consumers adopting the behaviour patterns and attitudes of developed market urban consumers. There are huge variations as well between the consumer landscapes of Johannesburg, Nairobi, Kinshasa, Cairo and Benghazi. African cities encompass great inequality, with many urban populations remaining in the BoP, and most continue to be blighted by blackouts and energy rationing that have a huge influence on their inhabitants’ priorities.

At the same time, brands cannot afford to confuse the relative unfamiliarity of rural Africa with a relative lack of importance. Patchy data in rural areas can blind companies to the contribution they make to current revenues, leading them to miss significant opportunities, or undermine existing business models when they shift focus to fast-growing cities. Rural tracker surveys in the alcoholic beverages sector, for example, show higher per capita consumption in small towns and rural areas that gives these markets disproportionate influence when it comes

to growing beer brands. Similarly, mobile banking services – a great force driving inclusion and helping to grow markets across Africa – have seen their growth accelerate significantly following take-up in rural areas.

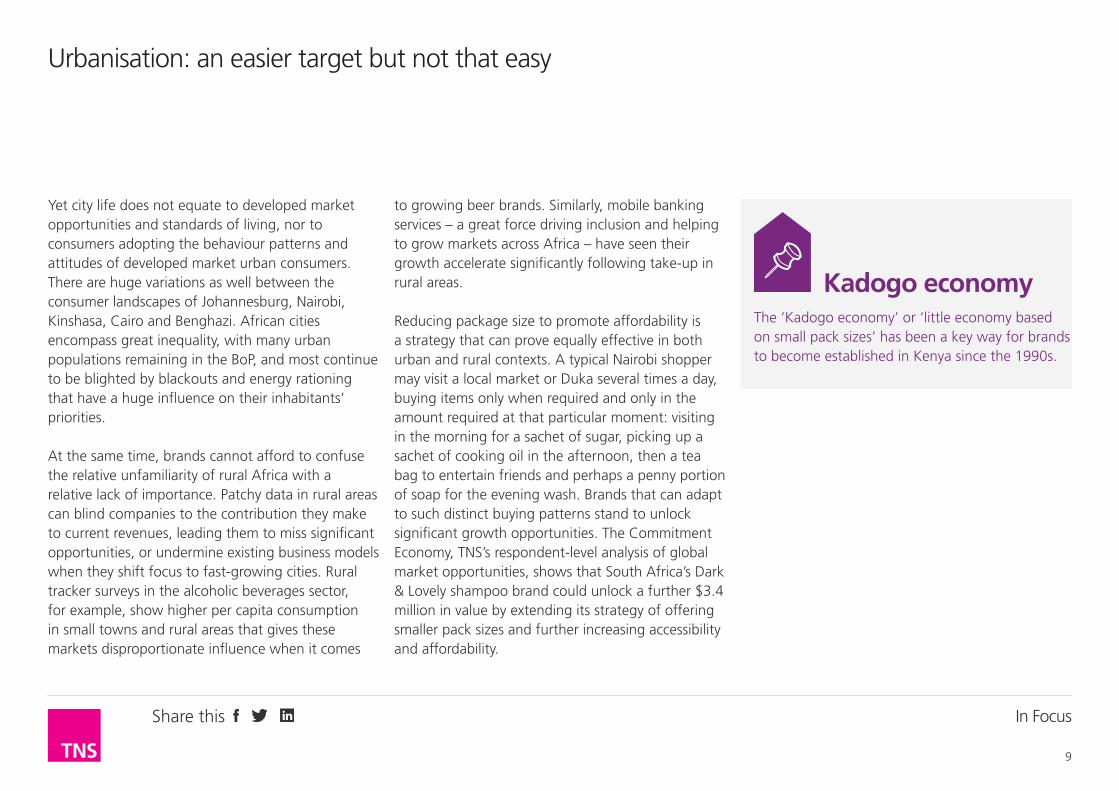

Reducing package size to promote affordability is a strategy that can prove equally effective in both urban and rural contexts. A typical Nairobi shopper may visit a local market or Duka several times a day, buying items only when required and only in the amount required at that particular moment: visiting in the morning for a sachet of sugar, picking up a sachet of cooking oil in the afternoon, then a tea bag to entertain friends and perhaps a penny portion of soap for the evening wash. Brands that can adapt to such distinct buying patterns stand to unlock significant growth opportunities. The Commitment Economy, TNS’s respondent-level analysis of global market opportunities, shows that South Africa’s Dark & Lovely shampoo brand could unlock a further $3.4 million in value by extending its strategy of offering smaller pack sizes and further increasing accessibility and affordability.

Kadogo economyThe ‘Kadogo economy’ or ‘little economy based on small pack sizes’ has been a key way for brands to become established in Kenya since the 1990s.

Urbanisation: an easier target but not that easy

In Focus

10

Share this

Media and mobile

In Focus

11

Share this

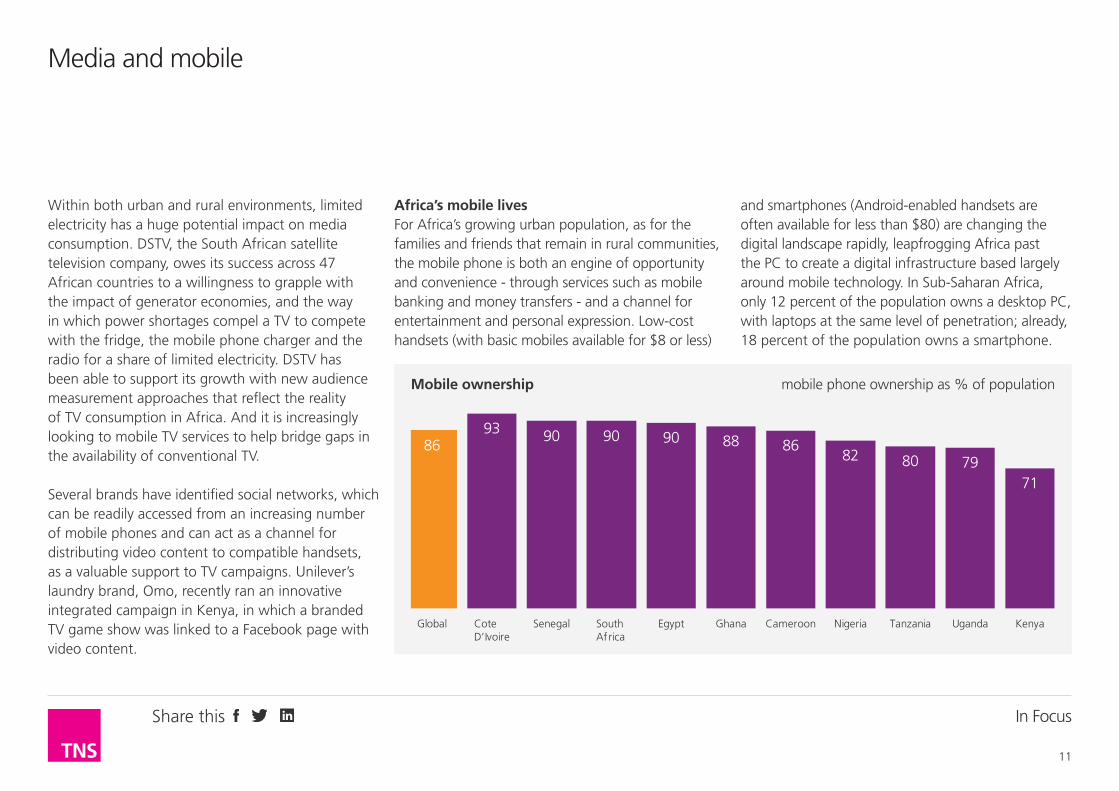

Within both urban and rural environments, limited electricity has a huge potential impact on media consumption. DSTV, the South African satellite television company, owes its success across 47 African countries to a willingness to grapple with the impact of generator economies, and the way in which power shortages compel a TV to compete with the fridge, the mobile phone charger and the radio for a share of limited electricity. DSTV has been able to support its growth with new audience measurement approaches that reflect the reality of TV consumption in Africa. And it is increasingly looking to mobile TV services to help bridge gaps in the availability of conventional TV.

Several brands have identified social networks, which can be readily accessed from an increasing number of mobile phones and can act as a channel for distributing video content to compatible handsets, as a valuable support to TV campaigns. Unilever’s laundry brand, Omo, recently ran an innovative integrated campaign in Kenya, in which a branded TV game show was linked to a Facebook page with video content.

Africa’s mobile livesFor Africa’s growing urban population, as for the families and friends that remain in rural communities, the mobile phone is both an engine of opportunity and convenience - through services such as mobile banking and money transfers - and a channel for entertainment and personal expression. Low-cost handsets (with basic mobiles available for $8 or less)

Media and mobile

and smartphones (Android-enabled handsets are often available for less than $80) are changing the digital landscape rapidly, leapfrogging Africa past the PC to create a digital infrastructure based largely around mobile technology. In Sub-Saharan Africa, only 12 percent of the population owns a desktop PC, with laptops at the same level of penetration; already, 18 percent of the population owns a smartphone.

86

Global

93

Cote D’Ivoire

Senegal

90

South Africa

90

Egypt

90

Ghana

88

Cameroon

86

Nigeria

82

Tanzania

80

Uganda

79

Kenya

71

Mobile ownership mobile phone ownership as % of population

In Focus

12

Share this

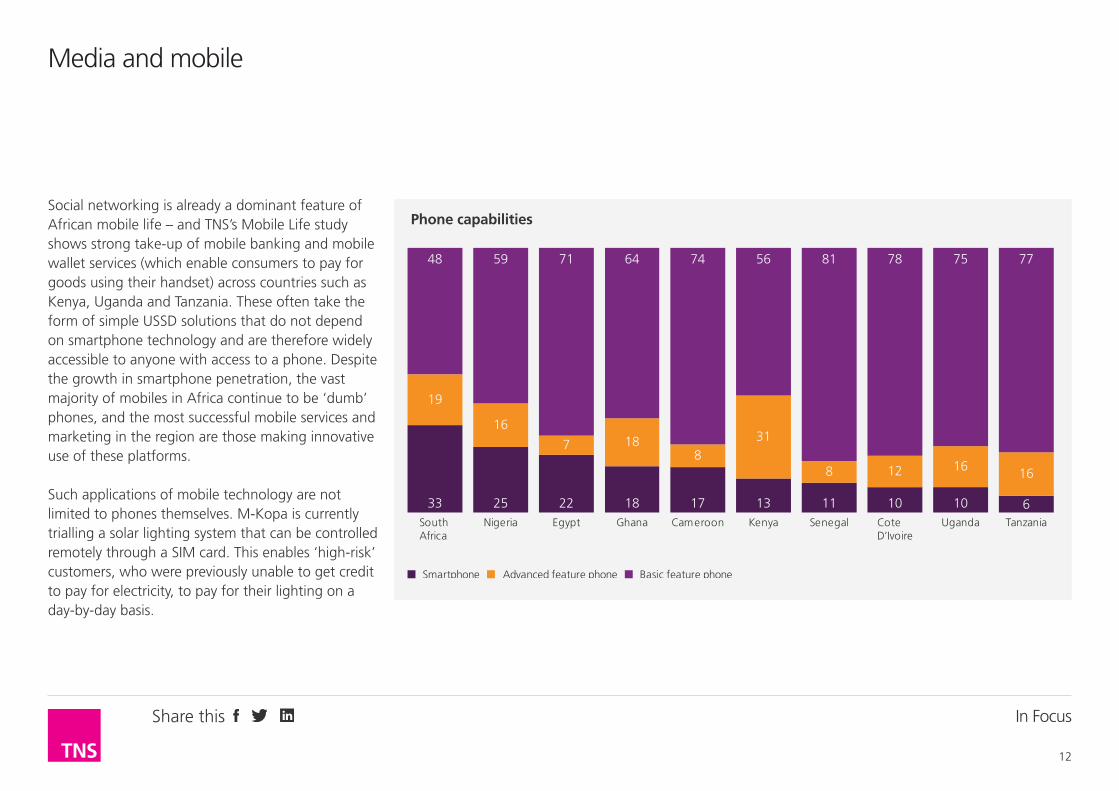

Social networking is already a dominant feature of African mobile life – and TNS’s Mobile Life study shows strong take-up of mobile banking and mobile wallet services (which enable consumers to pay for goods using their handset) across countries such as Kenya, Uganda and Tanzania. These often take the form of simple USSD solutions that do not depend on smartphone technology and are therefore widely accessible to anyone with access to a phone. Despite the growth in smartphone penetration, the vast majority of mobiles in Africa continue to be ‘dumb’ phones, and the most successful mobile services and marketing in the region are those making innovative use of these platforms.

Such applications of mobile technology are not limited to phones themselves. M-Kopa is currently trialling a solar lighting system that can be controlled remotely through a SIM card. This enables ‘high-risk’ customers, who were previously unable to get credit to pay for electricity, to pay for their lighting on a day-by-day basis.

Kenya

13

31

56

South Africa

33

19

48

Nigeria

25

16

59

Egypt

22

7

71

Ghana

18

18

64

Cameroon

17

8

74

Senegal

11

8

81

CoteD’Ivoire

10

12

78

Uganda

10

16

75

Tanzania

6

16

77

Smartphone Advanced feature phone Basic feature phone

Phone capabilities

Media and mobile

In Focus

13

Share this

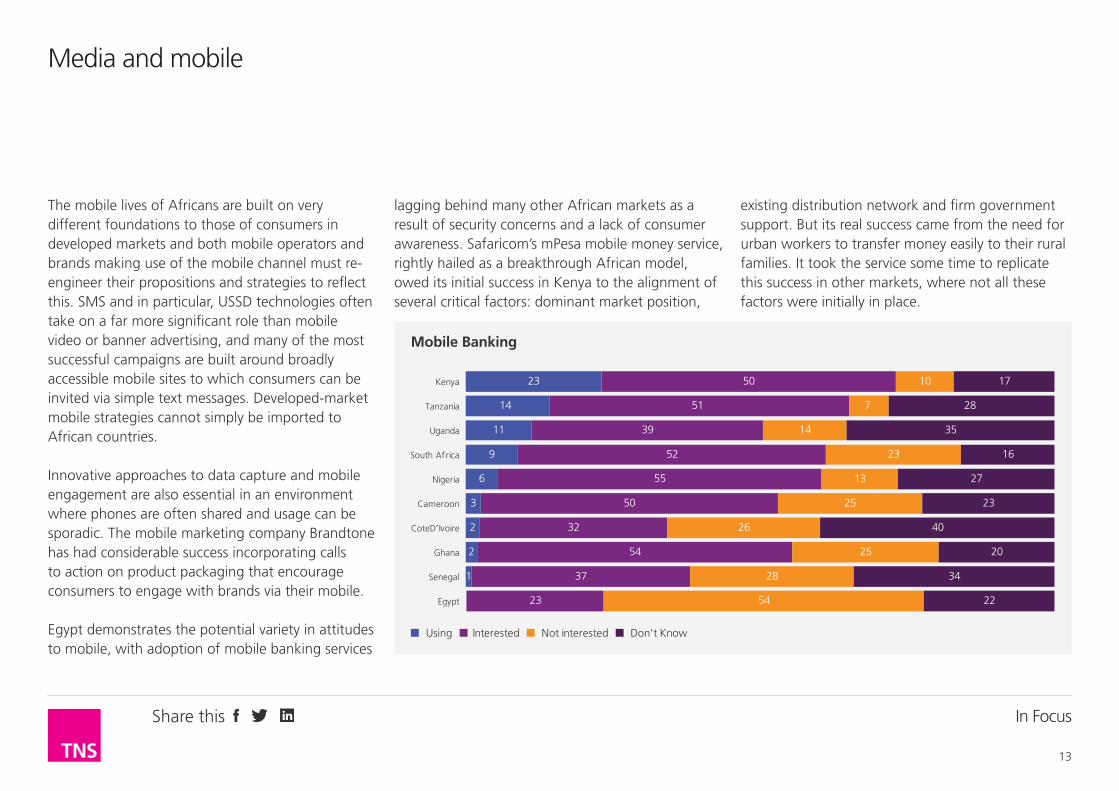

The mobile lives of Africans are built on very different foundations to those of consumers in developed markets and both mobile operators and brands making use of the mobile channel must re-engineer their propositions and strategies to reflect this. SMS and in particular, USSD technologies often take on a far more significant role than mobile video or banner advertising, and many of the most successful campaigns are built around broadly accessible mobile sites to which consumers can be invited via simple text messages. Developed-market mobile strategies cannot simply be imported to African countries.

Innovative approaches to data capture and mobile engagement are also essential in an environment where phones are often shared and usage can be sporadic. The mobile marketing company Brandtone has had considerable success incorporating calls to action on product packaging that encourage consumers to engage with brands via their mobile.

Egypt demonstrates the potential variety in attitudes to mobile, with adoption of mobile banking services

lagging behind many other African markets as a result of security concerns and a lack of consumer awareness. Safaricom’s mPesa mobile money service, rightly hailed as a breakthrough African model, owed its initial success in Kenya to the alignment of several critical factors: dominant market position,

existing distribution network and firm government support. But its real success came from the need for urban workers to transfer money easily to their rural families. It took the service some time to replicate this success in other markets, where not all these factors were initially in place.

9 52 23 16South Africa

11 39 14 35Uganda

14 51 7 28Tanzania

23 50 10 17Kenya

23 54 22Egypt

1 37 28 34Senegal

2 54Ghana 25 20

2 32 26 40CoteD’Ivoire

3 50 25 23Cameroon

6 55Nigeria 13 27

Using Interested Not interested Don't Know

Mobile Banking

Media and mobile

In Focus

14

Share this

The mobile operator MTN, currently the only African representative in the world’s top 100 brands, owes its success to a continual process of innovation to ensure affordability in different markets. This has involved adapting to the secondary handset market, through which second-hand mobile phones reach emerging middle-class and BoP communities – and has driven a strategy of offering airtime in small package sizes that echo the penny packs of FMCG brands. It has also led to a demand for constant innovation to stay ahead in highly competitive markets – in which rival operators bring out new tariffs on an almost weekly basis.

Brands leveraging mobile as a channel, either through social media, SMS or the application of mobile wallet technology, must therefore shed many developed market assumptions about intimate, personalised and always-on devices. For most Africans, the sharing of airtime and handsets is a natural extension of existing habits and cultural values, as well as a logical means of controlling costs. The mobile phone and the media consumed through it are experienced on an occasional basis, with emerging middle-class consumers buying a few

hours of BlackBerry Messenger airtime for a specific task, for example. Brands must adapt their strategies to such a frequently interrupted, frequently shared channel if they are to succeed. Please Call Me (PCM) messages, a USSD-based service which sends

recipients a phone number to call accompanied a 115-character advertising message, are an African innovation that brands have leveraged with great success. PCM campaigns advertise everything from airlines and car insurance to local village stores.

Media and mobile

In Focus

15

Share this

The opportunity for brands

In Focus

16

Share this

The marketing generation – and their demandsBrands themselves represent a new form of opportunity in many African markets. Until relatively recently the role of marketing was restricted to the FMCG category; today it plays a role in driving awareness and choice across mobile, banking and more. Brands are highly valued by emerging middle-class consumers, especially where brand propositions reflect priority needs and can provide accessible quality and credibility.

In the aftermath of the Arab Spring, North African countries such as Egypt, Libya, Morocco and Algeria have demonstrated a strongly heightened degree of consumer empowerment, with traditional monopolies questioned and challenged, and brands playing an increasingly visible role in newly dynamic markets. Successful branding owes much to local political and cultural nuance, with heightened nationalism in the wake of revolution and political change leading many local and global brands to adopt patriotic messaging and images. Religion can often play a similar role: both Coca-Cola and

Pepsi have sought to associate their brands with the festival of Ramadan; Coca-Cola through a post-Revolution sense of happiness and optimism, Pepsi through a corporate responsibility programme linked to Ramadan themes of charity and giving.

The importance of localised brand propositions is shown by the evolution of South Africa’s Tiger Brands, a market leader in bread and other categories. Tiger Brands has moved from a simple export strategy to one in which it takes control of every aspect of branding, distribution and strategy in the markets that it targets. When expanding into Nigeria, Tiger Brands acquired a local flour manufacturer, providing a ready-made distribution and transportation network, and retained the local branding due to its strength in the market. In other situations, Tiger Brands has adopted a similar acquisition-led approach but introduced its own brands when research showed that these had greater potential to leverage the infrastructure of the acquired company.

The opportunity for brands

In Focus

17

Share this

Competition in the marketing hotspotsGreater attention to brand positioning in part reflects the demands of emerging middle-class consumers for robust propositions that can help to meet their daily aspirations and challenges. However, it is also a response to an increasingly competitive marketing landscape. Tiger Brands cannot expect to have it its own way in a market such as Nigeria; Western multinationals such as Coca-Cola, Pepsi, P&G and Unilever compete with Chinese and Turkish brands that in many markets benefit from far stronger cultural ties.

If there is a risk to companies switching attention from rural regions to focus on urban centres it lies in the greater competition that they face in these environments, and the ‘Power in the Market’2

opportunities that they sacrifice through narrowing the availability of their products. Brand loyalty is extremely strong amongst the BoP consumers who inhabit many rural areas and many of whom will go onto form the emerging middle class. First mover advantage can be highly significant, and brands that are committed enough to establish distribution over broader areas may be more likely to obtain it.

Kadogo economyIn Nigeria’s laundry detergent market, The Commitment Economy study shows that So Klin of China has stolen a march on P&G’s Ariel and Unilever’s Omo by adopting their traditional strategy of increasing accessibility through broader distribution and smaller pack sizes. Were the western multinationals to fight back by re-establishing distribution and increasing marketing support in key areas, they could regain up to $15 million in value.

The opportunity for brands

In Focus

18

Share this

Weighing up growth prospects

In Focus

19

Share this

Weighing up growth prospectsUnderstanding the precise size and shape of such market opportunities is essential for companies weighing up the decision to pursue them. There is no shortage of growth opportunities in Africa, but the number that can be realised efficiently is significantly narrower. Companies must take hard-headed decisions about which forms of growth they have the will, budget and appetite for risk to invest in – and which challenges they are prepared to overcome. In any given situation, the success of their investment will depend hugely on their ability to re-engineer their brand proposition to fit the precise growth opportunity that they have identified.

None of these caveats make Africa any less of a compelling opportunity for global brands. Opportunities must be precisely defined, but the scale of each opportunity is vast nonetheless. By embracing the diversity of the African cultural and marketing landscape, companies give themselves a greater chance of fulfilling them.

Weighing up growth prospects

In Focus

20

Share this

Voices from AfricaTNS uses fictionalised realities, stories compiled from the many different interviews conducted by our researchers, to help bring to life the experiences of consumers in different markets.

In Focus

21

Share this

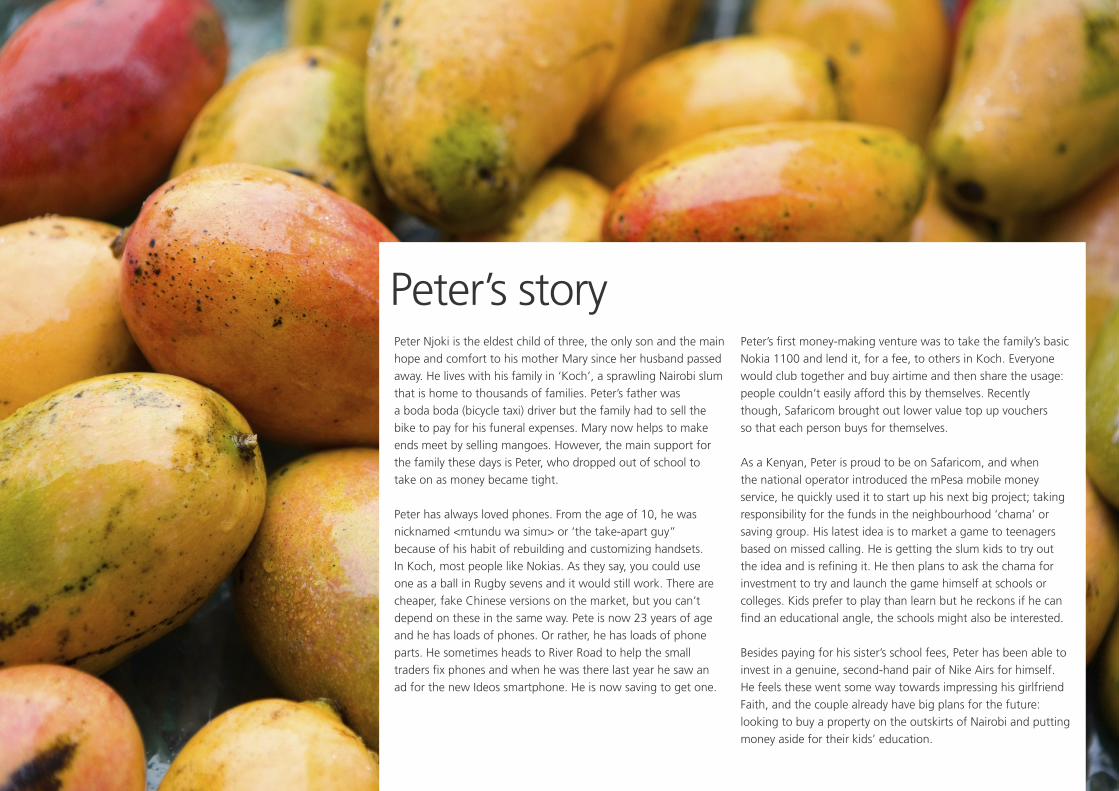

Peter’s storyPeter Njoki is the eldest child of three, the only son and the main hope and comfort to his mother Mary since her husband passed away. He lives with his family in ‘Koch’, a sprawling Nairobi slum that is home to thousands of families. Peter’s father was a boda boda (bicycle taxi) driver but the family had to sell the bike to pay for his funeral expenses. Mary now helps to make ends meet by selling mangoes. However, the main support for the family these days is Peter, who dropped out of school to take on as money became tight.

Peter has always loved phones. From the age of 10, he was nicknamed <mtundu wa simu> or ‘the take-apart guy” because of his habit of rebuilding and customizing handsets. In Koch, most people like Nokias. As they say, you could use one as a ball in Rugby sevens and it would still work. There are cheaper, fake Chinese versions on the market, but you can’t depend on these in the same way. Pete is now 23 years of age and he has loads of phones. Or rather, he has loads of phone parts. He sometimes heads to River Road to help the small traders fix phones and when he was there last year he saw an ad for the new Ideos smartphone. He is now saving to get one.

Peter’s first money-making venture was to take the family’s basic Nokia 1100 and lend it, for a fee, to others in Koch. Everyone would club together and buy airtime and then share the usage: people couldn’t easily afford this by themselves. Recently though, Safaricom brought out lower value top up vouchers so that each person buys for themselves.

As a Kenyan, Peter is proud to be on Safaricom, and when the national operator introduced the mPesa mobile money service, he quickly used it to start up his next big project; taking responsibility for the funds in the neighbourhood ‘chama’ or saving group. His latest idea is to market a game to teenagers based on missed calling. He is getting the slum kids to try out the idea and is refining it. He then plans to ask the chama for investment to try and launch the game himself at schools or colleges. Kids prefer to play than learn but he reckons if he can find an educational angle, the schools might also be interested.

Besides paying for his sister’s school fees, Peter has been able to invest in a genuine, second-hand pair of Nike Airs for himself. He feels these went some way towards impressing his girlfriend Faith, and the couple already have big plans for the future: looking to buy a property on the outskirts of Nairobi and putting money aside for their kids’ education.

In Focus

22

Share this

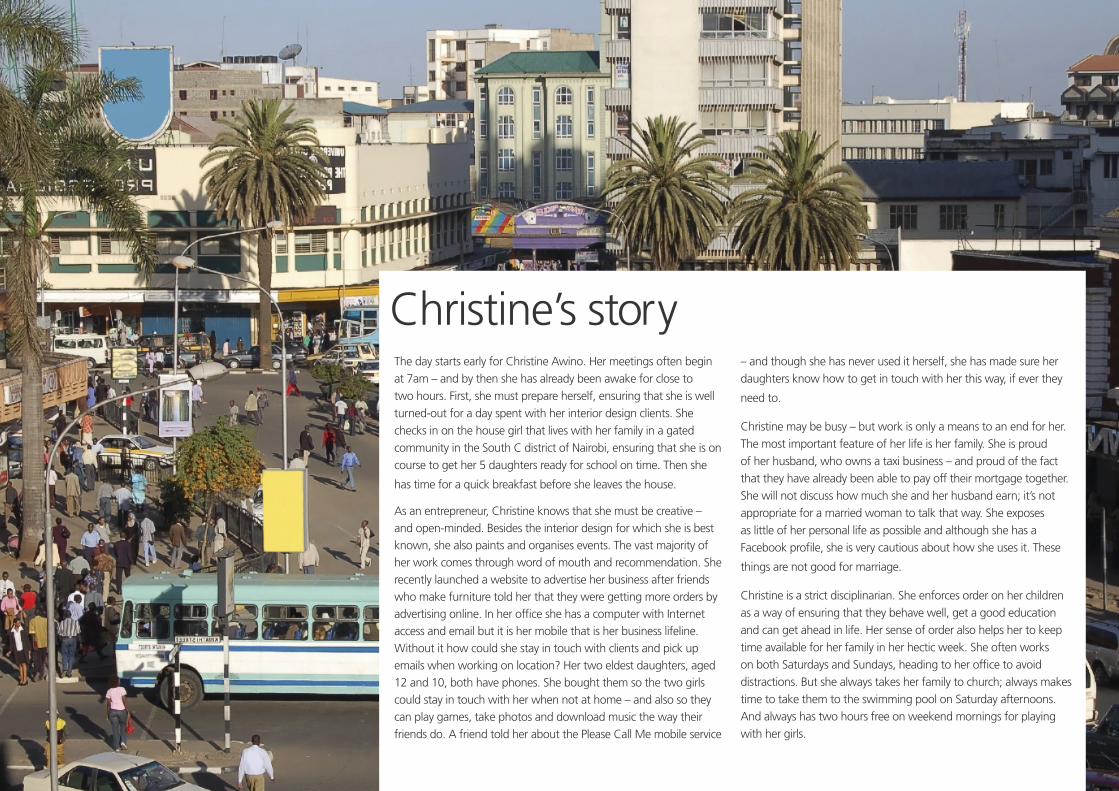

Christine’s storyThe day starts early for Christine Awino. Her meetings often begin at 7am – and by then she has already been awake for close to two hours. First, she must prepare herself, ensuring that she is well turned-out for a day spent with her interior design clients. She checks in on the house girl that lives with her family in a gated community in the South C district of Nairobi, ensuring that she is on course to get her 5 daughters ready for school on time. Then she

has time for a quick breakfast before she leaves the house.

As an entrepreneur, Christine knows that she must be creative – and open-minded. Besides the interior design for which she is best known, she also paints and organises events. The vast majority of her work comes through word of mouth and recommendation. She recently launched a website to advertise her business after friends who make furniture told her that they were getting more orders by advertising online. In her office she has a computer with Internet access and email but it is her mobile that is her business lifeline. Without it how could she stay in touch with clients and pick up emails when working on location? Her two eldest daughters, aged 12 and 10, both have phones. She bought them so the two girls could stay in touch with her when not at home – and also so they can play games, take photos and download music the way their friends do. A friend told her about the Please Call Me mobile service

– and though she has never used it herself, she has made sure her daughters know how to get in touch with her this way, if ever they

need to.

Christine may be busy – but work is only a means to an end for her. The most important feature of her life is her family. She is proud of her husband, who owns a taxi business – and proud of the fact that they have already been able to pay off their mortgage together. She will not discuss how much she and her husband earn; it’s not appropriate for a married woman to talk that way. She exposes as little of her personal life as possible and although she has a Facebook profile, she is very cautious about how she uses it. These

things are not good for marriage.

Christine is a strict disciplinarian. She enforces order on her children as a way of ensuring that they behave well, get a good education and can get ahead in life. Her sense of order also helps her to keep time available for her family in her hectic week. She often works on both Saturdays and Sundays, heading to her office to avoid distractions. But she always takes her family to church; always makes time to take them to the swimming pool on Saturday afternoons. And always has two hours free on weekend mornings for playing with her girls.

In Focus

23

Share this

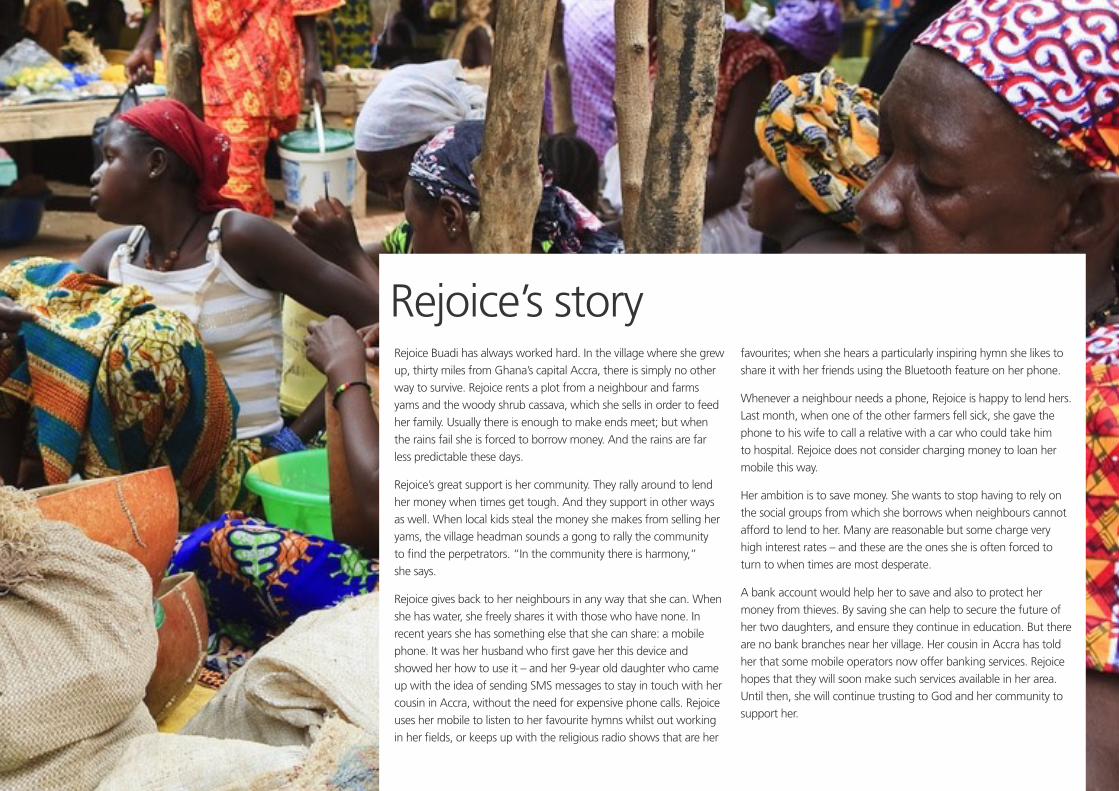

Rejoice’s storyRejoice Buadi has always worked hard. In the village where she grew up, thirty miles from Ghana’s capital Accra, there is simply no other way to survive. Rejoice rents a plot from a neighbour and farms yams and the woody shrub cassava, which she sells in order to feed her family. Usually there is enough to make ends meet; but when the rains fail she is forced to borrow money. And the rains are far less predictable these days.

Rejoice’s great support is her community. They rally around to lend her money when times get tough. And they support in other ways as well. When local kids steal the money she makes from selling her yams, the village headman sounds a gong to rally the community to find the perpetrators. “In the community there is harmony,” she says.

Rejoice gives back to her neighbours in any way that she can. When she has water, she freely shares it with those who have none. In recent years she has something else that she can share: a mobile phone. It was her husband who first gave her this device and showed her how to use it – and her 9-year old daughter who came up with the idea of sending SMS messages to stay in touch with her cousin in Accra, without the need for expensive phone calls. Rejoice uses her mobile to listen to her favourite hymns whilst out working in her fields, or keeps up with the religious radio shows that are her

favourites; when she hears a particularly inspiring hymn she likes to share it with her friends using the Bluetooth feature on her phone.

Whenever a neighbour needs a phone, Rejoice is happy to lend hers. Last month, when one of the other farmers fell sick, she gave the phone to his wife to call a relative with a car who could take him to hospital. Rejoice does not consider charging money to loan her mobile this way.

Her ambition is to save money. She wants to stop having to rely on the social groups from which she borrows when neighbours cannot afford to lend to her. Many are reasonable but some charge very high interest rates – and these are the ones she is often forced to turn to when times are most desperate.

A bank account would help her to save and also to protect her money from thieves. By saving she can help to secure the future of her two daughters, and ensure they continue in education. But there are no bank branches near her village. Her cousin in Accra has told her that some mobile operators now offer banking services. Rejoice hopes that they will soon make such services available in her area. Until then, she will continue trusting to God and her community to support her.

In Focus

24

Share this

About the authors

1. The Economist 2. ‘Power in the mind’ is a measure TNS uses alongside ‘power in the market’ to establish the growth opportunities for brands – see You can’t always get what you want to learn more.

ReferencesYou may be interested in...

Video: Peter’s story >

Base of the pyramid in context >

Digital media in sub-saharan Africa >

Mobile commerce reaches the tipping point >

TNS has a strong presence in Africa, with teams in 17 markets across the region. This piece was developed in collaboration with a number of experts, including:

Melissa Baker Bob BurgoyneKarin Du ChenneTamer El NaggarCharlotte GarinSteve Hamilton-ClarkNeil Higgs

Zoë Lawrence Kim MacIlwaineAggrey Maposa Arnold Miller Margarita PutterRyan Versfeld Anastacia Wangari

In Focus

25

Share this

About In FocusIn Focus is part of a regular series of articles that takes an in-depth look at a particular subject, region or demographic in more detail. All articles are written by TNS consultants and based on their expertise gathered through working on client assignments in over 80 markets globally, with additional insights gained through TNS proprietary studies such as Digital Life, Mobile Life and The Commitment Economy.

About TNS TNS advises clients on specific growth strategies around new market entry, innovation, brand switching and stakeholder management, based on long-established expertise and market-leading solutions. With a presence in over 80 countries, TNS has more conversations with the world’s consumers than anyone else and understands individual human behaviours and attitudes across every cultural, economic and political region of the world. TNS is part of Kantar, one of the world’s largest insight, information and consultancy groups.

Please visit www.tnsglobal.com for more information.

Get in touch If you would like to talk to us about anything you have read in this report, please get in touch via [email protected] or via Twitter @tns_global