natixis_global_inflation_fund_janvier.2011

DESCRIPTION

Natixis_global_inflation_fund_janvier.2011TRANSCRIPT

In order to interpret correctly the consequences of the current environment on the indexed bond market, it is important to go back to the fundamentals of this atypical asset class.

An inflation-linked bond has a principal (and coupons), valued depending on real inflation. While a nominal bond’s principal remains stable throughout the entire period (see chart 1), the

redemption of an inflation-linked bond upon maturity corresponds to the inflated principal (the bond is redeemed at par if there is deflation over the period). In return for the excess performance related to inflation, the investor accepts a return expressed as a real rate, lower than the nominal rate.

• changes in real interest rates: an inflation-linked bond’s price reacts to changes in real interest rates (linked to growth expectations) in the same way as a so-called conventional bond reacts to changes in nominal interest rates.

• inflation expectations: for a given maturity, this difference between the nominal and real interest rates represents the breakeven rate and correspond to the inflation expected by the market over the period.

FLASH EXPERTISEJanuary 2011

Natixis Global Inflation FundBenefit from a favourable access to the inflation-linked bond market

CORPORATE AND INVESTMENT BANKING / INVESTMENT SOLUTIONS / SPECIALIZED FINANCIAL SERVICES

www.am.natixis.com

The dual sensitivity of inflation-linked bonds

Historically low interest rates that could rise in the medium term, the issue of inflation levels in developed countries, shifting from fears of persistent deflation to inflationary tensions due to the quantitative easing policies, emerging economies set to benefit from robust growth rates but that also stand to suffer severe inflationary pressure… What are the consequences for inflation-linked bonds? What is the outlook for Natixis Global Inflation Fund?

Year Inflation rate

OII

1 0.50 %2 0.75 %3 1.40 %4 1.80 %5 2.20 %6 2.50 %7 3.25 %8 3.00 %9 2.75 %10 2.50 %

i.e. 22.6% over 10 years Or 2.06% per year of inflation

The price of an inflation-linked bond therefore varies depending on:MARKER

At a constant nominal interest rate, an increase in the breakeven rate implies a decrease in the real interest rate.

Chart 1 - Theoretical change in principal of an inflation-linked bond compared with a nominal bond (theoretical change in inflation)

MARKERDuring the term of an infla-tion-linked bond, the market price of the inflation-linked bond applies to this inflated principal. Even at an un-changed price, its valuation therefore increases in line with actual inflation, unlike a nominal bond.

Expected inflation + Risk premium

Expected growth Real rateNominal rate

Fixed-rate bondInflation-linked bond

Breakeven+

www.am.natixis.com

FLASH EXPERTISE / January 2011

If the inflation recorded at the end of the period is higher than the inflation expected at issuance, the inflation-linked bond will offer better returns than a nominal bond issued at the same time. Conversely, if real inflation upon maturity is lower than expected inflation, the investor will record a loss compared with the nominal bond.

The dual sensitivity of inflation-linked bonds is therefore a key element in their valuation. In order to invest in this asset class, one must therefore analyse:n growth expectations, which have an impact on the real interest

rate component and therefore on the ILB’s price;

n the outlook for inflation, which determines the return of inflation-linked bonds and therefore their performance relative to the nominal bond market.

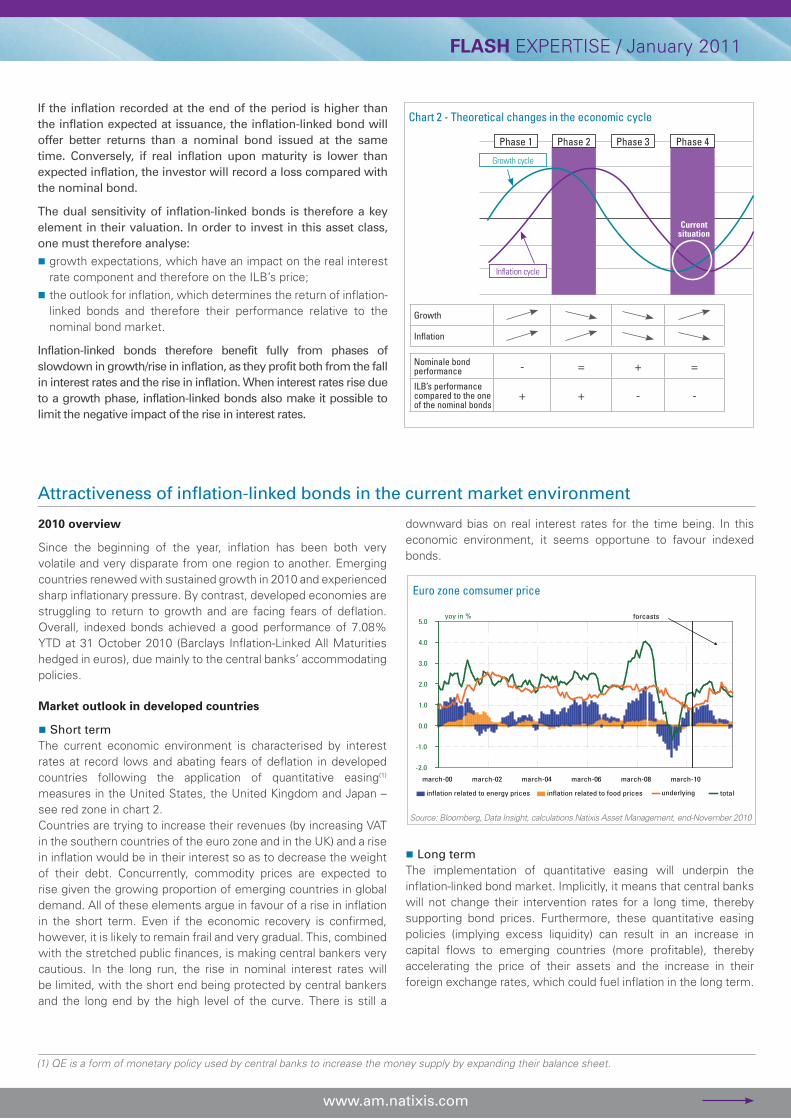

Inflation-linked bonds therefore benefit fully from phases of slowdown in growth/rise in inflation, as they profit both from the fall in interest rates and the rise in inflation. When interest rates rise due to a growth phase, inflation-linked bonds also make it possible to limit the negative impact of the rise in interest rates.

(1) QE is a form of monetary policy used by central banks to increase the money supply by expanding their balance sheet.

2010 overview

Since the beginning of the year, inflation has been both very volatile and very disparate from one region to another. Emerging countries renewed with sustained growth in 2010 and experienced sharp inflationary pressure. By contrast, developed economies are struggling to return to growth and are facing fears of deflation. Overall, indexed bonds achieved a good performance of 7.08% YTD at 31 October 2010 (Barclays Inflation-Linked All Maturities hedged in euros), due mainly to the central banks’ accommodating policies.

Market outlook in developed countries

n Short term The current economic environment is characterised by interest rates at record lows and abating fears of deflation in developed countries following the application of quantitative easing(1) measures in the United States, the United Kingdom and Japan – see red zone in chart 2.Countries are trying to increase their revenues (by increasing VAT in the southern countries of the euro zone and in the UK) and a rise in inflation would be in their interest so as to decrease the weight of their debt. Concurrently, commodity prices are expected to rise given the growing proportion of emerging countries in global demand. All of these elements argue in favour of a rise in inflation in the short term. Even if the economic recovery is confirmed, however, it is likely to remain frail and very gradual. This, combined with the stretched public finances, is making central bankers very cautious. In the long run, the rise in nominal interest rates will be limited, with the short end being protected by central bankers and the long end by the high level of the curve. There is still a

downward bias on real interest rates for the time being. In this economic environment, it seems opportune to favour indexed bonds.

n Long termThe implementation of quantitative easing will underpin the inflation-linked bond market. Implicitly, it means that central banks will not change their intervention rates for a long time, thereby supporting bond prices. Furthermore, these quantitative easing policies (implying excess liquidity) can result in an increase in capital flows to emerging countries (more profitable), thereby accelerating the price of their assets and the increase in their foreign exchange rates, which could fuel inflation in the long term.

Attractiveness of inflation-linked bonds in the current market environment

Euro zone comsumer price

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

march-00 march-02 march-04 march-06 march-08 march-10

inflation related to energy prices inflation related to food prices underlying total

yoy in % forcasts

Source: Bloomberg, Data Insight, calculations Natixis Asset Management, end-November 2010

Chart 2 - Theoretical changes in the economic cycle

Phase 1 Phase 3

Growth

Inflation

Nominale bond performance - = + =

ILB’s performance compared to the one of the nominal bonds

+ + - -

Growth cycle

Inflation cycle

Current situation

Phase 2 Phase 4

www.am.natixis.com

FLASH EXPERTISE / January 2011

Natixis Global Inflation Fund: Several strategies to make the most of the different growth and inflation cycles in a global universe

Illustration of the strategy in 2010

In early 2010, the investment team had set up a position on the short end of the curve by investing 10% of the fund’s assets in OATi 2011 so as to benefit from the carry (on a monthly inflation from February to March) of 0.6% and 0.5%, i.e. more than 7% and 6%, respectively, on an annual basis.

-0,5

-0,4

-0,3

-0,2

-0,1

0,0

0,1

0,2

0,3

0,4

0,5

0,6

0,7mom, in %

01/0902/09

03/0904/09

05/0906/09

07/0908/09

09/0910/09

11/0912/09

01/1002/10

03/1004/10

05/1006/10

07/1008/10

09/1010/10

(2) United States, euro zone, United Kingdom, Japan

Source: Bloomberg, end-2010

France: inflation carry

Natixis Global Inflation Fund seeks to tap the specific opportunities offered by the indexed bond market:

n in a global universe, so as to make the most of the different growth and inflation cycles in G7 countries and emerging countries,

n combined with diversification strategies on inflation carry and currencies in emerging countries.

a) Core strategiesInflation carry strategyObjective: To benefit from actual inflation

By definition, indexed bonds appreciate with monthly actual inflation (see chart 1). In order to make the most of this inflation carry without exposing the portfolio to movements in real interest rates, the investment team chose to invest in the shortest maturities. Depending on inflation expectations for the different geographic regions (G4(2) and diversification into emerging countries), two types of strategies on seasonal inflation are used:

n inflation carry via overexposure of the asset indexed to a given inflation,

n or arbitrage of one inflation in favour of another. These strategies are expressed as a percentage of the asset.

Slope strategiesObjective: To benefit from deformations in the real interest rate curve

The real interest rate curve depends on growth anticipations in the short, medium and long term, as well as on flows. Significant inflation carry (see inflation carry strategy) triggers massive purchases of short-term securities by the market and therefore a steepening of the curve, and vice versa.

Illustration of the strategy in 2010

The investment team played a flattening of the euro real interest rate curve related to the negative carry reported (-0.8% in early 2010!) with sales of short-term securi-ties (6% of 2012 OAT€i) and purchases of long-term securities (2020 OAT€i).

Real interest rate directional strategyObjective: To reduce or increase the portfolio’s sensitivity to movements in real interest rates

Real interest rates reflect the market’s growth anticipations, which depend on the economies’ position in the cycle (see chart 2). Based on its opinions on real interest rates, the investment team adopts over- or underexposure strategies in relation to the index’s sensitivity. It taps the sensitivity of inflation-linked bonds to real interest rates.

Illustration of the strategy in 2010

In early 2010, the investment team purchased 5% of 2017 TIPS (US inflation-linked bonds) as even though indicators pointed to an improvement in the US manufacturing sector, our outlook was for US growth to remain weak.

MARKER

www.am.natixis.com

FLASH EXPERTISE / January 2011

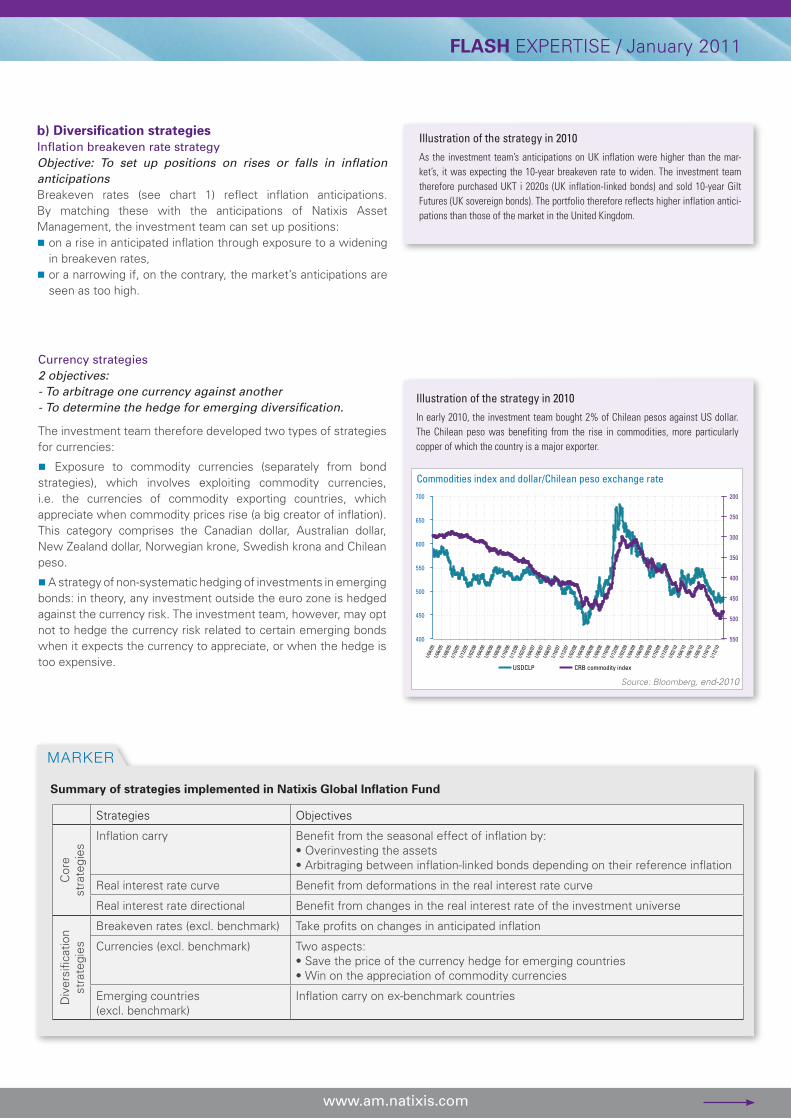

Currency strategies2 objectives: - To arbitrage one currency against another- To determine the hedge for emerging diversification.

The investment team therefore developed two types of strategies for currencies:

n Exposure to commodity currencies (separately from bond strategies), which involves exploiting commodity currencies, i.e. the currencies of commodity exporting countries, which appreciate when commodity prices rise (a big creator of inflation). This category comprises the Canadian dollar, Australian dollar, New Zealand dollar, Norwegian krone, Swedish krona and Chilean peso.

n A strategy of non-systematic hedging of investments in emerging bonds: in theory, any investment outside the euro zone is hedged against the currency risk. The investment team, however, may opt not to hedge the currency risk related to certain emerging bonds when it expects the currency to appreciate, or when the hedge is too expensive.

Illustration of the strategy in 2010

In early 2010, the investment team bought 2% of Chilean pesos against US dollar. The Chilean peso was benefiting from the rise in commodities, more particularly copper of which the country is a major exporter.

Strategies Objectives

Cor

e

stra

tegi

es

Inflation carry Benefit from the seasonal effect of inflation by: • Overinvesting the assets • Arbitraging between inflation-linked bonds depending on their reference inflation

Real interest rate curve Benefit from deformations in the real interest rate curve

Real interest rate directional Benefit from changes in the real interest rate of the investment universe

Div

ersi

ficat

ion

stra

tegi

es

Breakeven rates (excl. benchmark) Take profits on changes in anticipated inflation

Currencies (excl. benchmark) Two aspects: • Save the price of the currency hedge for emerging countries• Win on the appreciation of commodity currencies

Emerging countries (excl. benchmark)

Inflation carry on ex-benchmark countries

Summary of strategies implemented in Natixis Global Inflation Fund

b) Diversification strategiesInflation breakeven rate strategyObjective: To set up positions on rises or falls in inflation anticipations Breakeven rates (see chart 1) reflect inflation anticipations. By matching these with the anticipations of Natixis Asset Management, the investment team can set up positions:n on a rise in anticipated inflation through exposure to a widening

in breakeven rates, n or a narrowing if, on the contrary, the market’s anticipations are

seen as too high.

Illustration of the strategy in 2010

As the investment team’s anticipations on UK inflation were higher than the mar-ket’s, it was expecting the 10-year breakeven rate to widen. The investment team therefore purchased UKT i 2020s (UK inflation-linked bonds) and sold 10-year Gilt Futures (UK sovereign bonds). The portfolio therefore reflects higher inflation antici-pations than those of the market in the United Kingdom.

400

450

500

550

600

650

700

1/04

/05

1/06

/05

1/08

/05

1/10

/05

1/12

/05

1/02

/06

1/04

/06

1/06

/06

1/08

/06

1/10

/06

1/12

/06

1/02

/07

1/04

/07

1/06

/07

1/08

/07

1/10

/07

1/12

/07

1/02

/08

1/04

/08

1/06

/08

1/08

/08

1/10

/08

1/12

/08

1/02

/09

1/04

/09

1/06

/09

1/08

/09

1/10

/09

1/12

/09

1/02

/10

1/04

/10

1/06

/10

1/08

/10

1/10

/10

1/12

/10

200

250

300

350

400

450

500

550

USDCLP CRB commodity index

Commodities index and dollar/Chilean peso exchange rate

Source: Bloomberg, end-2010

www.am.natixis.com

FLASH EXPERTISE / January 2011

With its different strategies and diversification in emerging markets, we are confident in Natixis Global Inflation Fund’s ability to make the most of low interest rates and higher inflation in the medium term, to stand up well to anticipations for rises in interest rates, and therefore continue to generate constant performance.

Disclaimer

This document is intended for professional clients. It may not be used for any purpose other than that for which it was intended and may not be reproduced, disseminated or disclosed to third parties, whether in part on in whole without prior authorization in writing from Natixis Asset Management. No information contained in this document may be interpreted as being contractual in any way. This document is produced purely for informational purposes. It is a presentation created and prepared by Natixis Asset Management based on sources considered to be reliable. Natixis Asset Management reserves the right to change the information in this document at any time without notice, and in particular anything relating to the description of the investment process, which under no circumstances constitutes a commitment from Natixis Asset Management.

Natixis Asset Management will not be held liable for any decision taken or not taken on the basis of the information in this document, nor for any use that a third party might make of the information. The Funds are authorized for sale in France and possibly in other countries where the sale is not contrary to local legislation. Prior to any investment, investors must check that they are legally authorized to invest in a Fund. The risks and fees connected to investment in a Fund are described in the relevant prospectus. The prospectus and periodic documents are available from Natixis Asset Management upon request. The prospectus must be given to the investor prior to the subscription.

c) Performances

Since the beginning of the year and over one year, the fund has met its investment objective, with an outperformance of 0.44% and a performance of 7.52% for the I share.

Avg Annual Total Return (month end) Fund % Index %

1 month 0.68 0.78

YTD 7.52 7.08

1 year 7.77 7.62

Source: Natixis Asset Management, end-October 2010

These performances confirm the attractiveness of a Global Inflation positioning, making it possible to benefit from the different cycles of growth and inflation in developed and emerging countries.In addition, the detailed performance attribution (see chart below) shows the interest of using multiple strategies as well as the quality of our anticipations drawn up in-house, based on a rigorous methodology perfected by Natixis Asset Management (on real interest rates and spreads and different inflations).

Inflation carry arbitrage

Real interest rate curve

Real interest rate directional

Breakeven rates Emerging countries

Currencies Difference in performance vs.

benchmark

Performance gross

10/2010 + + 0 0 0 ++ 1,01 8,09

2009 0 - + + 0 0 -0,04 8,61

2008 + 0 - ++ 0 0 0,66 5,75

2008*: as from 31 OctoberBenchmark for Natixis Global Inflation Fund: Barclays World Government Inflation-Linked All Maturities hedged in euros.

Source: Natixis Asset Management, 31 October 2010.

Performance figures concern past years. Past performance is not a reliable indication of future performance.The fund’s net performances are obtained after deduction of the total expense ratio (I share: 0.65%; I-H share: 0.65%; R share: 1%).

www.am.natixis.com

FLASH EXPERTISE / January 2011

ADDITIONAL NOTES

The funds mentioned in this material are not registered or authorized in all jurisdictions and may not be available to all investors in a jurisdiction. The provision of this material does not constitute an offer of services, nor an offer or recommendation to purchase or sell shares in any financial instrument. Investors should consider the investment objectives, risks and expenses of any investment carefully before investing. In the case of a fund, these can be found in the fund’s prospectus or offering memorandum, which should be read carefully before investing. If you would like further information about any of the funds, including charges, expenses and risk considerations, contact the sender of this document or your financial advisor for a free prospectus, simplified prospectus, copy of the Articles of Incorporation, the semi and annual reports, and/ or other materials and translations that are relevant to your jurisdiction. Any reference to a ranking, a rating or an award provides no guarantee for future performance results and is not constant over time. Performance data shown represents past performance and is not a guarantee of future results. More recent performance may be lower or higher. Principal value and returns fluctuate over time (including as a result of currency fluctuations) so that shares, when redeemed, will be worth more or less than their original cost. Performance shown is net of all fund expenses, but does not include the effect of sales charges or correspondent bank charges, and assumes reinvestment of distributions. If such charges were included, returns would have been lower. The analyses, opinions, and certain of the investment themes and processes referenced herein represent the views of the author(s) referenced as of the date indicated. These, as well as the portfolio holdings and characteristics shown, are subject to change. There can be no assurance that developments will transpire as may be forecasted in this material.

In certain cases, this material is provided by one of the Natixis Global Associates entities listed below, each of which is a subsidiary of Natixis Global Asset Management, the holding company of a diverse line-up of specialised investment management and distribution entities worldwide, each of which conduct any regulated activities only in and from the jurisdictions in which they are licensed or authorized. Their services and the products they manage are not available to all investors in all jurisdictions. Although Natixis Global Associates believes that the information provided in this material to be reliable, it does not guarantee the accuracy, adequacy, or completeness of such information.

In the UK: This material is provided by Natixis Global Associates UK Limited which is authorised and regulated by the UK Financial Services Authority (register no. 190258). This material is intended to be communicated to and/or directed at persons (1) in the United Kingdom, and should not to be regarded as an offer to buy or sell, or the solicitation of any offer to buy or sell securities in any other jurisdiction than the United Kingdom; and (2) who are authorised under the Financial Services and Markets Act 2000; or are high net worth businesses with called up share capital or net assets of at least £5 million or in the case of a trust assets of at least £10 million; or any other person to whom the material may otherwise lawfully be distributed in accordance with the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or the (Promotion of Collective Investment Schemes) (Exemption) Order 2001 (the "Intended Recipients"). To the extent that this material is issued by Natixis Global Associates UK Limited, the fund, services or opinions referred to in this material are only available to the Intended Recipients and this material must not be relied nor acted upon by any other persons. Registered Address: Cannon Bridge House, 25 Dowgate Hill, London, EC4R 2YA.

In the E.U. (outside of the UK): This material is provided by Natixis Global Associates S.A. or one of its branch offices listed below. Natixis Global Associates S.A. is a Luxembourg management company that is authorized by the Commission de Surveillance du Secteur Financier and is incorporated under Luxembourg laws and registered under n. B 115843. Registered office of Natixis Global Associates S.A.: 2-8 Avenue Charles de Gaulle, L-1653 Luxembourg, Grand Duchy of Luxembourg. France: Natixis Global Associates International (n.509 471 173 RCS Paris). Registered office: 21 quai d'Austerlitz, 75013 Paris. Italy: Natixis Global Associates S.A. Succursale Italiana (Bank of Italy Register of Italian Asset Management Companies no 23458.3). Registered office: Via San Clemente, 1 - 20122, Milan,MI, Italy. Germany: Natixis Global Associates S.A., Zweigniederlassung Deutschland (Registration number: HRB 88541). Registered office: Im Trutz Frankfurt 55, Westend Carrée, 7. Floor, Frankfurt am Main 60322, Germany. Netherlands: Natixis Global Associates S.A., Nederlands filiaal (Registration number 50774670). Registered office: Evert van de Beekstraat 310, 1118CX Schiphol, the Netherlands. Sweden: Natixis Global Associates S.A. (Luxembourg) Nordics Filial (Registration number 516405-9601 - Swedish Companies Registration Office). Registered office: Master Samuelsgatan 60, 8th Floor, Stockholm 111 21, Sweden.

In Switzerland: This material is provided to Qualified Investors by Natixis Global Associates Switzerland Sàrl. Registered office: place de la Fusterie 12, 1204 Genève.

In the DIFC: This material is provided in and from the DIFC financial district by Natixis Global Associates Middle East, a branch of Natixis Global Associates UK Limited, which is regulated by the DFSA. Related financial products or services are only available to persons who have sufficient financial experience and understanding to participate in financial markets within the DIFC, and qualify as Professional Clients as defined by the DFSA. Registered office: PO Box. 118257, 5th Floor, Building 8, Gate Village, DIFC, Dubai, United Arab Emirates.