multiple: european private equity watch — issue 3 - ey issue 3 2014 private equity transaction...

TRANSCRIPT

Multiple Issue 3 2014

Private Equity Transaction Advisory Services

Record high for IPO exitsThe exit market in Europe has continued to perform very strongly in 2014. Q2 set a record for PE-backed IPO quarterly value, with volume reaching its highest level since 1998. Looking ahead, the pipeline for the buyout market looks strong for the second half of the year.

Multiple July 2014 | 2

About MultipleMultiple is a quarterly publication summarizing trends in buyouts* across Europe.

EY and Equistone Partners Europe are proud to sponsor the Centre for Management Buyout Research (CMBOR), whose data is analyzed in Multiple.

The following analysis and commentary is based on research recorded by CMBOR.

Countries covered: Austria, Belgium, Czech Republic, Denmark, Finland, France, Germany, Hungary, Ireland, Italy, Netherlands, Norway, Poland, Portugal, Romania, Spain, Sweden, Switzerland, Turkey and the UK.

*�Buyouts:�CMBOR�defines�buyouts�as�over�50%�of�shares�changing�ownership,�with�management�or�private�equity,�or�both, having a controlling stake upon deal completion. Equity funding must primarily be from private equity funds and the�bought-out�company�must�have�its�own�financing�structure,�e.g.,�management�buyout�(MBO)�or�management�buy-in (MBI).

For�full�details�on�the�CMBOR�methodology,�please�refer�to�page�15.

Welcom

e

Multiple July 2014 | 3

The data in this report was captured on 2 July 2014.

“ The IPO continues to flex its muscles by setting a record for quarterly value, with volume reaching its highest level since 1998. While questions remain on IPO fatigue, the pipeline is strong. In the previous quarter, IPO gains were largely confined to the UK and the Nordic region. However, IPOs spread across Europe this quarter, including France, Spain, Italy and Germany.

“ With local divestments across the UK and Europe holding up well this year, there appears to be greater primary buyout activity. Looking forward, more corporate mergers in Europe would generate further large divestments. Although this is happening in the US — where multibillion dollar deals are taking place — Europe has yet to see this activity.”Sachin Date, Europe, Middle East, India and Africa (EMEIA) Private Equity Leader, EY

Contents4 Headlines

5 Pipeline prospects

6 Current conditions

7 Market watch

8 Deal dynamics

9 Sector insights

11 Inside the deal

12 Country spotlight

16 Contacts

17 Further insights

Multiple July 2014 | 4

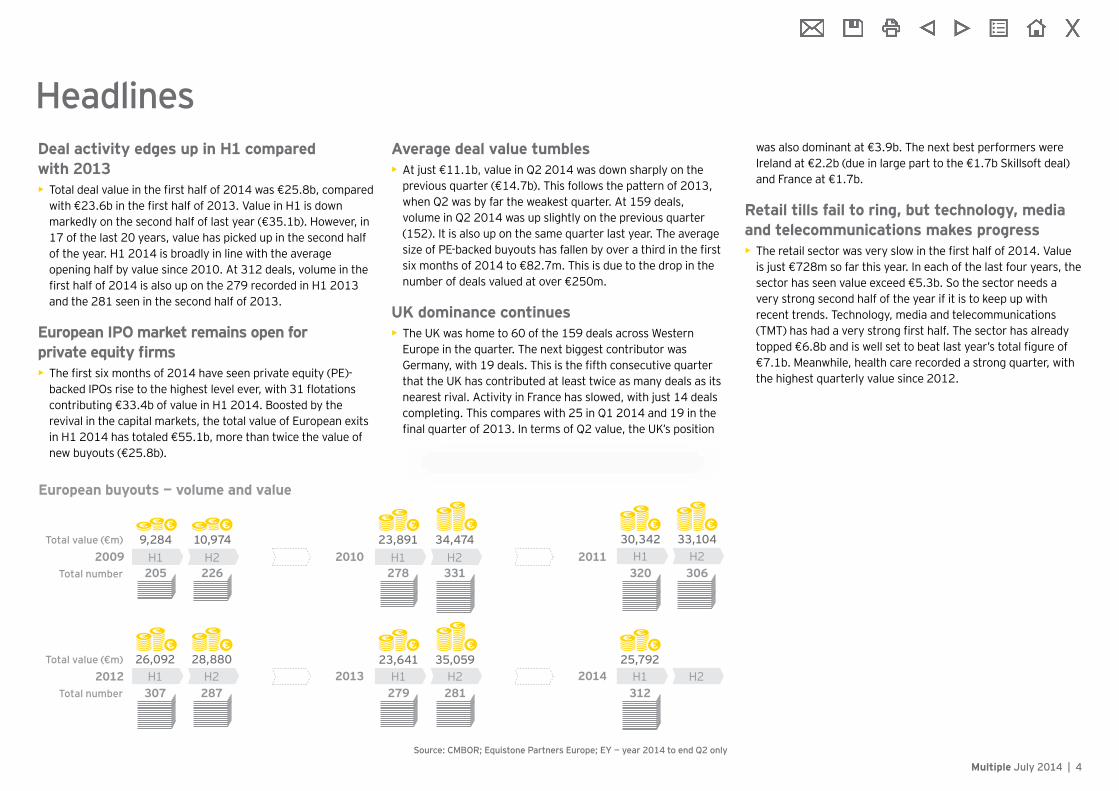

Deal activity edges up in H1 compared with 2013• Total�deal�value�in�the�first�half�of�2014�was�€25.8b,�compared�

with�€23.6b�in�the�first�half�of�2013.�Value�in�H1�is�down�markedly�on�the�second�half�of�last�year�(€35.1b).�However,�in�17�of�the�last�20�years,�value�has�picked�up�in�the�second�half�of�the�year.�H1�2014�is�broadly�in�line�with�the�average�opening�half�by�value�since�2010.�At�312�deals,�volume�in�the�first�half�of�2014�is�also�up�on�the�279�recorded�in�H1�2013�and�the�281�seen�in�the�second�half�of�2013.

European IPO market remains open for private equity firms• The�first�six�months�of�2014�have�seen�private�equity�(PE)-

backed�IPOs�rise�to�the�highest�level�ever,�with�31�flotations�contributing�€33.4b�of�value�in�H1�2014.�Boosted�by�the�revival in the capital markets, the total value of European exits in�H1�2014�has�totaled�€55.1b,�more�than�twice�the�value�of�new�buyouts�(€25.8b).

Average deal value tumbles• At�just�€11.1b,�value�in�Q2�2014�was�down�sharply�on�the�

previous�quarter�(€14.7b).�This�follows�the�pattern�of�2013,�when�Q2�was�by�far�the�weakest�quarter.�At�159�deals,�volume�in�Q2�2014�was�up�slightly�on�the�previous�quarter�(152).�It�is�also�up�on�the�same�quarter�last�year.�The�average�size�of�PE-backed�buyouts�has�fallen�by�over�a�third�in�the�first�six�months�of�2014�to�€82.7m.�This�is�due�to�the�drop�in�the�number�of�deals�valued�at�over�€250m.

UK dominance continues• The�UK�was�home�to�60�of�the�159�deals�across�Western�

Europe in the quarter. The next biggest contributor was Germany,�with�19�deals.�This�is�the�fifth�consecutive�quarter�that the UK has contributed at least twice as many deals as its nearest�rival.�Activity�in�France�has�slowed,�with�just�14�deals�completing.�This�compares�with�25�in�Q1�2014�and�19�in�the�final�quarter�of�2013.�In�terms�of�Q2�value,�the�UK’s�position�

was�also�dominant�at�€3.9b.�The�next�best�performers�were�Ireland�at�€2.2b�(due�in�large�part�to�the�€1.7b�Skillsoft�deal)�and�France�at�€1.7b.

Retail tills fail to ring, but technology, media and telecommunications makes progress • The�retail�sector�was�very�slow�in�the�first�half�of�2014.�Value�

is�just�€728m�so�far�this�year.�In�each�of�the�last�four�years,�the�sector�has�seen�value�exceed�€5.3b.�So�the�sector�needs�a�very strong second half of the year if it is to keep up with recent trends. Technology, media and telecommunications (TMT)�has�had�a�very�strong�first�half.�The�sector�has�already�topped�€6.8b�and�is�well�set�to�beat�last�year’s�total�figure�of�€7.1b.�Meanwhile,�health�care�recorded�a�strong�quarter,�with�the�highest�quarterly�value�since�2012.

Headlines

Source: CMBOR; Equistone Partners Europe; EY — year 2014 to end Q2 only

European buyouts — volume and value

Total value (€m)

Total number2009

Total value (€m)

Total number2012

H1 H2 2010

2013

H1 H223,891 34,474

205 226 278 331

10,9749,284 30,342 33,104H1 H2320 306

2011

201426,092 28,880

H1 H2307 287

23,641 35,059H1 H2279 281

25,792H1 H2312

Multiple July 2014 | 5

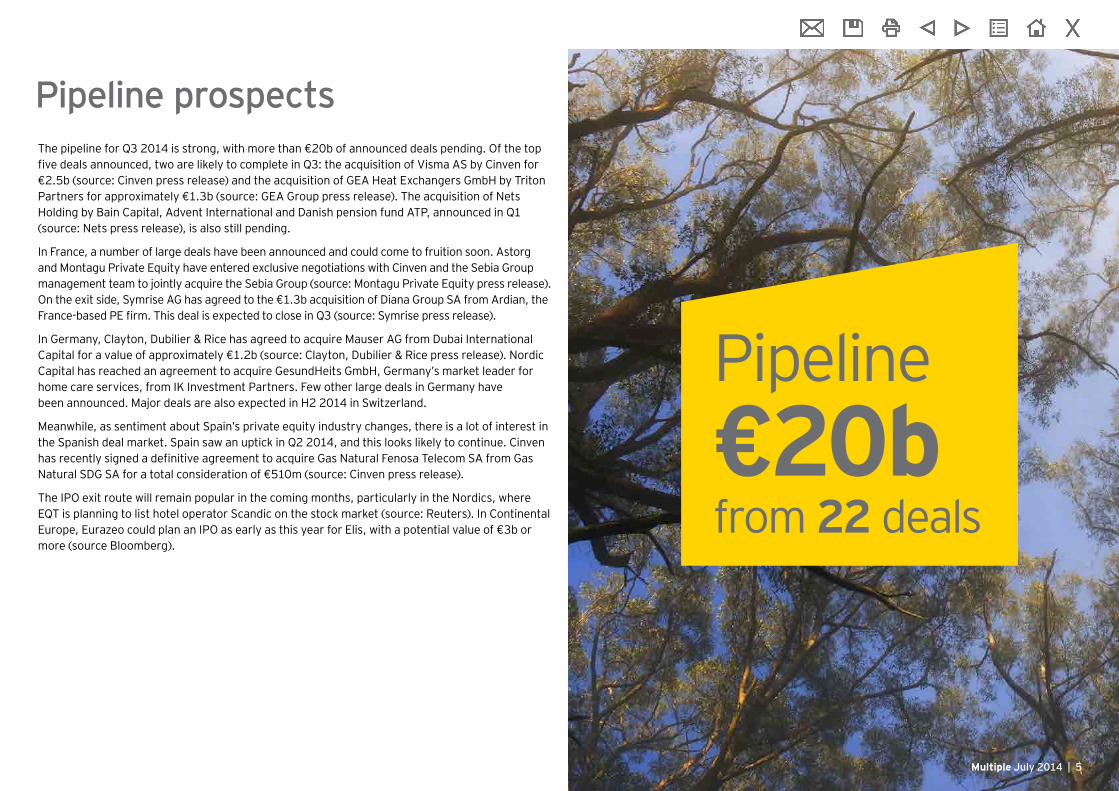

Pipeline€20bfrom 22 deals

Pipeline prospectsThe�pipeline�for�Q3�2014�is�strong,�with�more�than�€20b�of�announced�deals�pending.�Of�the�top�five�deals�announced,�two�are�likely�to�complete�in�Q3:�the�acquisition�of�Visma�AS�by�Cinven�for�€2.5b�(source:�Cinven�press�release)�and�the�acquisition�of�GEA�Heat�Exchangers�GmbH�by�Triton�Partners�for�approximately�€1.3b�(source:�GEA�Group�press�release).�The�acquisition�of�Nets�Holding�by�Bain�Capital,�Advent�International�and�Danish�pension�fund�ATP,�announced�in�Q1�(source: Nets press release), is also still pending.

In France, a number of large deals have been announced and could come to fruition soon. Astorg and Montagu Private Equity have entered exclusive negotiations with Cinven and the Sebia Group management team to jointly acquire the Sebia Group (source: Montagu Private Equity press release). On�the�exit�side,�Symrise�AG�has�agreed�to�the�€1.3b�acquisition�of�Diana�Group�SA�from�Ardian,�the�France-based�PE�firm.�This�deal�is�expected�to�close�in�Q3�(source:�Symrise�press�release).�

In Germany, Clayton, Dubilier & Rice has agreed to acquire Mauser AG from Dubai International Capital�for�a�value�of�approximately�€1.2b�(source:�Clayton,�Dubilier�&�Rice�press�release).�Nordic�Capital�has�reached�an�agreement�to�acquire�GesundHeits�GmbH,�Germany’s�market�leader�for�home care services, from IK Investment Partners. Few other large deals in Germany have been�announced.�Major�deals�are�also�expected�in�H2�2014�in�Switzerland.

Meanwhile,�as�sentiment�about�Spain’s�private�equity�industry�changes,�there�is�a�lot�of�interest�in�the�Spanish�deal�market.�Spain�saw�an�uptick�in�Q2�2014,�and�this�looks�likely�to�continue.�Cinven�has�recently�signed�a�definitive�agreement�to�acquire�Gas�Natural�Fenosa�Telecom�SA�from�Gas�Natural�SDG�SA�for�a�total�consideration�of�€510m�(source:�Cinven�press�release).

The IPO exit route will remain popular in the coming months, particularly in the Nordics, where EQT�is�planning�to�list�hotel�operator�Scandic�on�the�stock�market�(source:�Reuters).�In�Continental�Europe,�Eurazeo�could�plan�an�IPO�as�early�as�this�year�for�Elis,�with�a�potential�value�of�€3b�or�more (source Bloomberg).

Multiple July 2014 | 5

Multiple July 2014 | 6

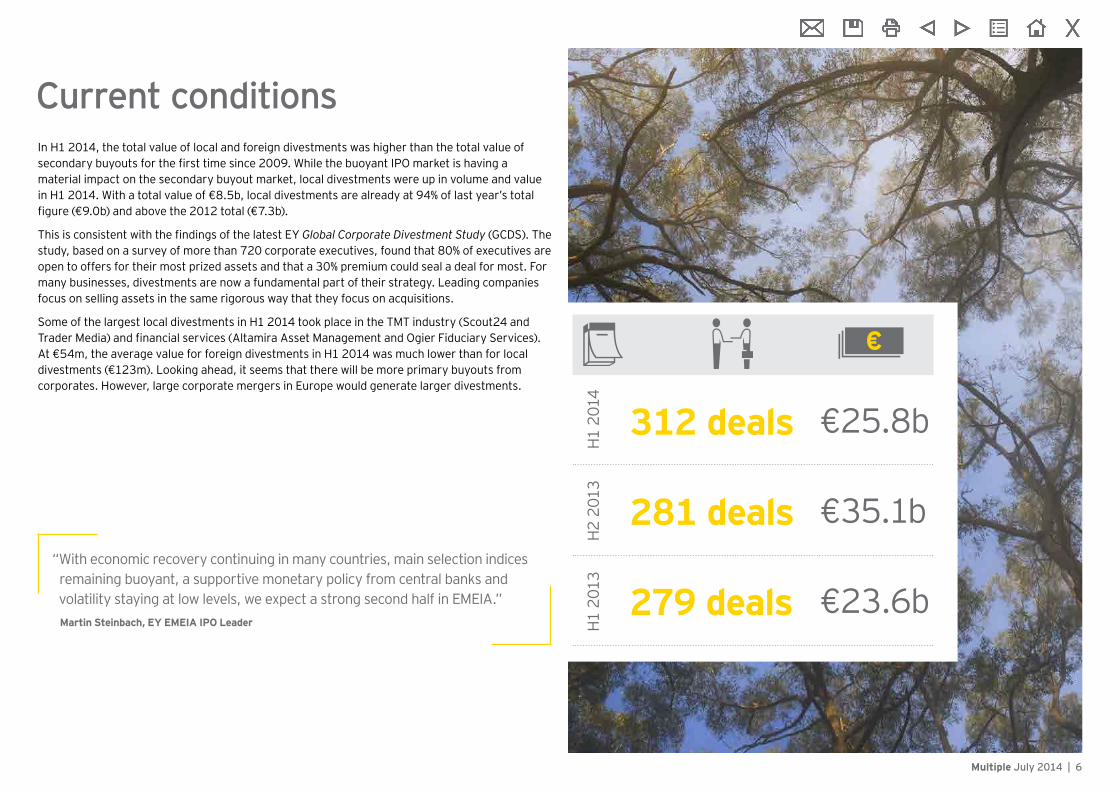

In�H1�2014,�the�total�value�of�local�and�foreign�divestments�was�higher�than�the�total�value�of�secondary�buyouts�for�the�first�time�since�2009.�While�the�buoyant�IPO�market�is�having�a�material impact on the secondary buyout market, local divestments were up in volume and value in�H1�2014.�With�a�total�value�of�€8.5b,�local�divestments�are�already�at�94%�of�last�year’s�total�figure�(€9.0b)�and�above�the�2012�total�(€7.3b).�

This�is�consistent�with�the�findings�of�the�latest�EY Global Corporate Divestment Study (GCDS). The study,�based�on�a�survey�of�more�than�720�corporate�executives,�found�that�80%�of�executives�are�open�to�offers�for�their�most�prized�assets�and�that�a�30%�premium�could�seal�a�deal�for�most.�For�many businesses, divestments are now a fundamental part of their strategy. Leading companies focus on selling assets in the same rigorous way that they focus on acquisitions.

Some�of�the�largest�local�divestments�in�H1�2014�took�place�in�the�TMT�industry�(Scout24�and�Trader�Media)�and�financial�services�(Altamira�Asset�Management�and�Ogier�Fiduciary�Services).�At�€54m,�the�average�value�for�foreign�divestments�in�H1�2014�was�much�lower�than�for�local�divestments�(€123m).�Looking�ahead,�it�seems�that�there�will�be�more�primary�buyouts�from�corporates. However, large corporate mergers in Europe would generate larger divestments.

Current conditions

312 deals €25.8b

281 deals €35.1b

279 deals €23.6bH1

�201

4H2�

2013

H1�2

013

“ With economic recovery continuing in many countries, main selection indices remaining buoyant, a supportive monetary policy from central banks and volatility staying at low levels, we expect a strong second half in EMEIA.”Martin Steinbach, EY EMEIA IPO Leader

Multiple July 2014 | 7

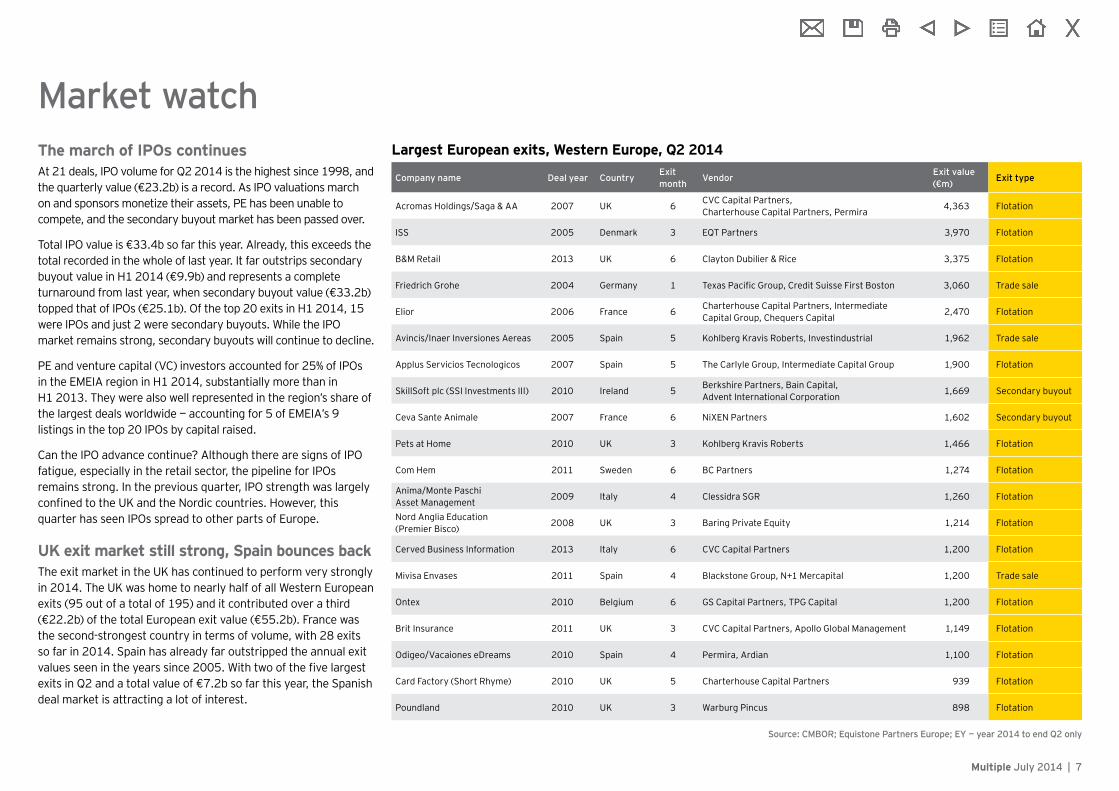

The march of IPOs continues At�21�deals,�IPO�volume�for�Q2�2014�is�the�highest�since�1998,�and�the�quarterly�value�(€23.2b)�is�a�record.�As�IPO�valuations�march�on and sponsors monetize their assets, PE has been unable to compete, and the secondary buyout market has been passed over.

Total�IPO�value�is�€33.4b�so�far�this�year.�Already,�this�exceeds�the�total recorded in the whole of last year. It far outstrips secondary buyout�value�in�H1�2014�(€9.9b)�and�represents�a�complete�turnaround�from�last�year,�when�secondary�buyout�value�(€33.2b)�topped�that�of�IPOs�(€25.1b).�Of�the�top�20�exits�in�H1�2014,�15�were�IPOs�and�just�2�were�secondary�buyouts.�While�the�IPO�market remains strong, secondary buyouts will continue to decline.

PE�and�venture�capital�(VC)�investors�accounted�for�25%�of�IPOs�in�the�EMEIA�region�in�H1�2014,�substantially�more�than�in�H1�2013.�They�were�also�well�represented�in�the�region’s�share�of�the�largest�deals�worldwide�—�accounting�for�5�of�EMEIA’s�9�listings�in�the�top�20�IPOs�by�capital�raised.

Can the IPO advance continue? Although there are signs of IPO fatigue, especially in the retail sector, the pipeline for IPOs remains strong. In the previous quarter, IPO strength was largely confined�to�the�UK�and�the�Nordic�countries.�However,�this�quarter has seen IPOs spread to other parts of Europe.

UK exit market still strong, Spain bounces backThe exit market in the UK has continued to perform very strongly in�2014.�The�UK�was�home�to�nearly�half�of�all�Western�European�exits�(95�out�of�a�total�of�195)�and�it�contributed�over�a�third�(€22.2b)�of�the�total�European�exit�value�(€55.2b).�France�was�the�second-strongest�country�in�terms�of�volume,�with�28�exits�so�far�in�2014.�Spain�has�already�far�outstripped�the�annual�exit�values�seen�in�the�years�since�2005.�With�two�of�the�five�largest�exits�in�Q2�and�a�total�value�of�€7.2b�so�far�this�year,�the�Spanish�deal market is attracting a lot of interest.

Market watchLargest European exits, Western Europe, Q2 2014

Company name Deal year Country Exit month Vendor Exit value

(€m) Exit type

Acromas Holdings/Saga & AA 2007 UK 6 CVC�Capital�Partners,� Charterhouse Capital Partners, Permira 4,363 Flotation

ISS 2005 Denmark 3 EQT�Partners 3,970 Flotation

B&M Retail 2013 UK 6 Clayton Dubilier & Rice 3,375 Flotation

Friedrich Grohe 2004 Germany 1 Texas�Pacific�Group,�Credit�Suisse�First�Boston 3,060 Trade sale

Elior 2006 France 6 Charterhouse Capital Partners, Intermediate Capital Group, Chequers Capital 2,470 Flotation

Avincis/Inaer Inversiones Aereas 2005 Spain 5 Kohlberg Kravis Roberts, Investindustrial 1,962 Trade sale

Applus Servicios Tecnologicos 2007 Spain 5 The Carlyle Group, Intermediate Capital Group 1,900 Flotation

SkillSoft plc (SSI Investments III) 2010 Ireland 5 Berkshire Partners, Bain Capital, Advent International Corporation 1,669 Secondary buyout

Ceva Sante Animale 2007 France 6 NiXEN Partners 1,602 Secondary buyout

Pets at Home 2010 UK 3 Kohlberg Kravis Roberts 1,466 Flotation

Com Hem 2011 Sweden 6 BC Partners 1,274 Flotation

Anima/Monte Paschi Asset Management 2009 Italy 4 Clessidra SGR 1,260 Flotation

Nord Anglia Education (Premier Bisco) 2008 UK 3 Baring Private Equity 1,214 Flotation

Cerved Business Information 2013 Italy 6 CVC�Capital�Partners 1,200 Flotation

Mivisa Envases 2011 Spain 4 Blackstone Group, N+1 Mercapital 1,200 Trade sale

Ontex 2010 Belgium 6 GS Capital Partners, TPG Capital 1,200 Flotation

Brit Insurance 2011 UK 3 CVC�Capital�Partners,�Apollo�Global�Management 1,149 Flotation

Odigeo/Vacaiones�eDreams 2010 Spain 4 Permira, Ardian 1,100 Flotation

Card Factory (Short Rhyme) 2010 UK 5 Charterhouse Capital Partners 939 Flotation

Poundland 2010 UK 3 Warburg Pincus 898 Flotation

Source: CMBOR; Equistone Partners Europe; EY — year 2014 to end Q2 only

Multiple July 2014 | 8

€1b plus €500m–€1b €100m–€500m Up to €100m Total number of deals

17

594

13

76488

2012

8

312

4

45255

H1 2014

Deal size

21

560

9

87443

2013

13

281

5

47216

H2 2013

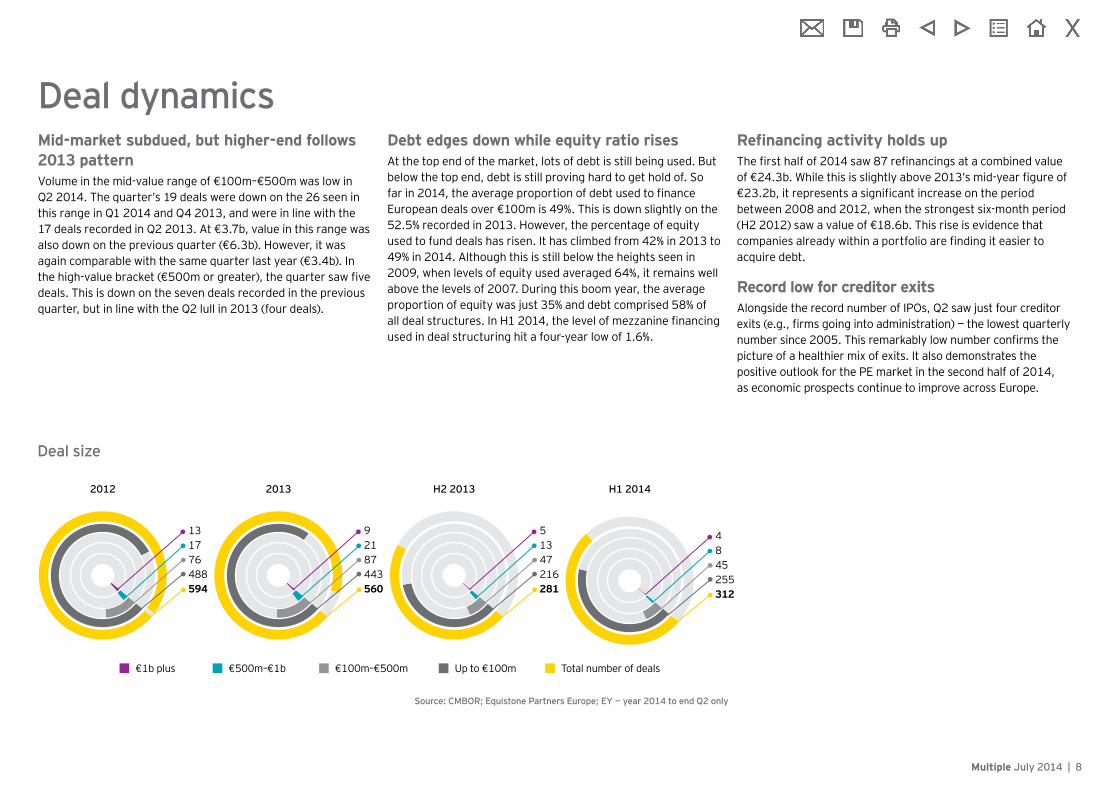

Deal dynamicsMid-market subdued, but higher-end follows 2013 pattern Volume�in�the�mid-value�range�of�€100m–€500m�was�low�in�Q2�2014.�The�quarter’s�19�deals�were�down�on�the�26�seen�in�this�range�in�Q1�2014�and�Q4�2013,�and�were�in�line�with�the�17�deals�recorded�in�Q2�2013.�At�€3.7b,�value�in�this�range�was�also�down�on�the�previous�quarter�(€6.3b).�However,�it�was�again�comparable�with�the�same�quarter�last�year�(€3.4b).�In�the�high-value�bracket�(€500m�or�greater),�the�quarter�saw�five�deals. This is down on the seven deals recorded in the previous quarter,�but�in�line�with�the�Q2�lull�in�2013�(four�deals).

Debt edges down while equity ratio risesAt the top end of the market, lots of debt is still being used. But below the top end, debt is still proving hard to get hold of. So far�in�2014,�the�average�proportion�of�debt�used�to�finance�European�deals�over�€100m�is�49%.�This�is�down�slightly�on�the�52.5%�recorded�in�2013.�However,�the�percentage�of�equity�used�to�fund�deals�has�risen.�It�has�climbed�from�42%�in�2013�to�49%�in�2014.�Although�this�is�still�below�the�heights�seen�in�2009,�when�levels�of�equity�used�averaged�64%,�it�remains�well�above�the�levels�of�2007.�During�this�boom�year,�the�average�proportion�of�equity�was�just�35%�and�debt�comprised�58%�of�all�deal�structures.�In�H1�2014,�the�level�of�mezzanine�financing�used�in�deal�structuring�hit�a�four-year�low�of�1.6%.

Refinancing activity holds upThe�first�half�of�2014�saw�87�refinancings�at�a�combined�value�of�€24.3b.�While�this�is�slightly�above�2013’s�mid-year�figure�of�€23.2b,�it�represents�a�significant�increase�on�the�period�between�2008�and�2012,�when�the�strongest�six-month�period�(H2�2012)�saw�a�value�of�€18.6b.�This�rise�is�evidence�that�companies�already�within�a�portfolio�are�finding�it�easier�to�acquire debt.

Record low for creditor exitsAlongside�the�record�number�of�IPOs,�Q2�saw�just�four�creditor�exits�(e.g.,�firms�going�into�administration)�—�the�lowest�quarterly�number�since�2005.�This�remarkably�low�number�confirms�the�picture of a healthier mix of exits. It also demonstrates the positive�outlook�for�the�PE�market�in�the�second�half�of�2014,�as economic prospects continue to improve across Europe.

Source: CMBOR; Equistone Partners Europe; EY — year 2014 to end Q2 only

Multiple July 2014 | 9

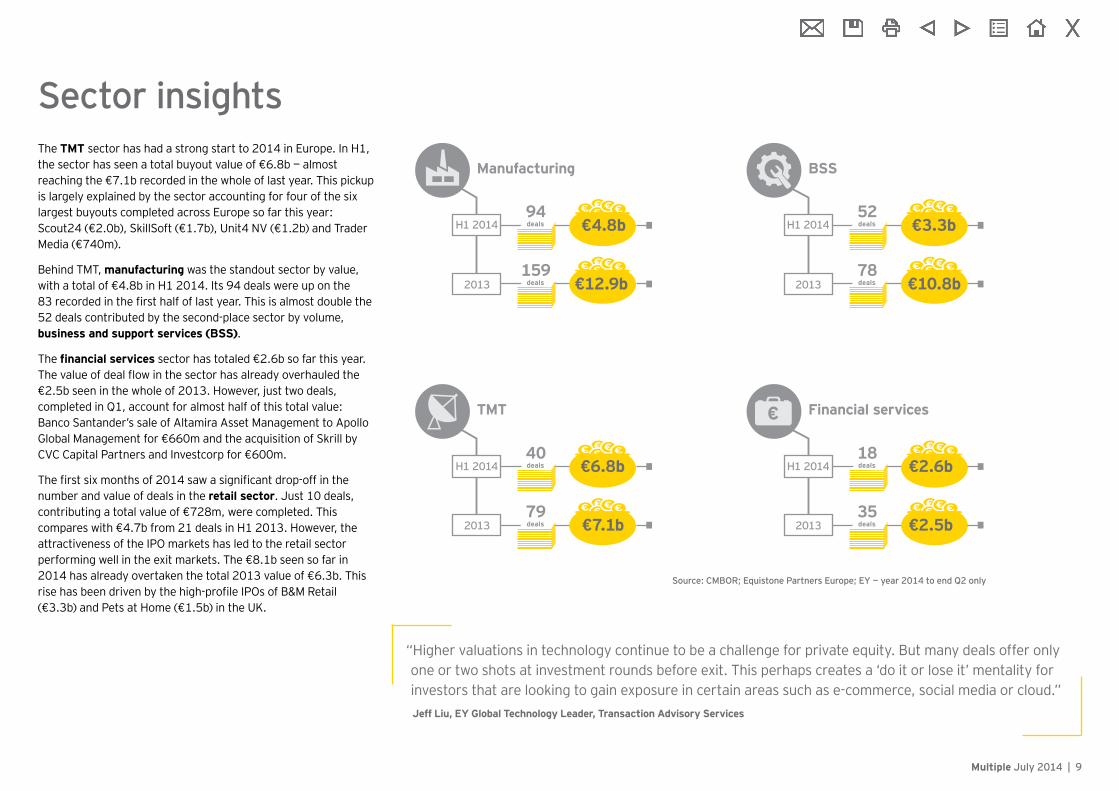

The TMT sector�has�had�a�strong�start�to�2014�in�Europe.�In�H1,�the�sector�has�seen�a�total�buyout�value�of�€6.8b�—�almost�reaching�the�€7.1b�recorded�in�the�whole�of�last�year.�This�pickup�is largely explained by the sector accounting for four of the six largest buyouts completed across Europe so far this year: Scout24�(€2.0b),�SkillSoft�(€1.7b),�Unit4�NV�(€1.2b)�and�Trader�Media�(€740m).�

Behind TMT, manufacturing was the standout sector by value, with�a�total�of�€4.8b�in�H1�2014.�Its�94�deals�were�up�on�the�83�recorded�in�the�first�half�of�last�year.�This�is�almost�double�the�52�deals�contributed�by�the�second-place�sector�by�volume,�business and support services (BSS).

The financial services�sector�has�totaled�€2.6b�so�far�this�year.�The�value�of�deal�flow�in�the�sector�has�already�overhauled�the�€2.5b�seen�in�the�whole�of�2013.�However,�just�two�deals,�completed�in�Q1,�account�for�almost�half�of�this�total�value:�Banco�Santander’s�sale�of�Altamira�Asset�Management�to�Apollo�Global�Management�for�€660m�and�the�acquisition�of�Skrill�by�CVC�Capital�Partners�and�Investcorp�for�€600m.

The�first�six�months�of�2014�saw�a�significant�drop-off�in�the�number and value of deals in the retail sector.�Just�10�deals,�contributing�a�total�value�of�€728m,�were�completed.�This�compares�with�€4.7b�from�21�deals�in�H1�2013.�However,�the�attractiveness of the IPO markets has led to the retail sector performing�well�in�the�exit�markets.�The�€8.1b�seen�so�far�in�2014�has�already�overtaken�the�total�2013�value�of�€6.3b.�This�rise�has�been�driven�by�the�high-profile�IPOs�of�B&M�Retail�(€3.3b)�and�Pets�at�Home�(€1.5b)�in�the�UK.

Sector insights

Manufacturing

deals €4.8b94

H1 2014

€12.9b

BSS

€3.3b

€10.8b

TMT

€6.8b

€7.1b

Financial services

€2.6bdeals 18

€2.5bdeals 35

159deals

deals 52

deals 78

deals 40

deals 79

2013

H1 2014

2013

H1 2014

2013

H1 2014

2013

Source: CMBOR; Equistone Partners Europe; EY — year 2014 to end Q2 only

“Higher valuations in technology continue to be a challenge for private equity. But many deals offer only one�or�two�shots�at�investment�rounds�before�exit.�This�perhaps�creates�a�‘do�it�or�lose�it’�mentality�for�investors that are looking to gain exposure in certain areas such as e-commerce, social media or cloud.”Jeff Liu, EY Global Technology Leader, Transaction Advisory Services

Multiple July 2014 | 10

Sector insights (continued)

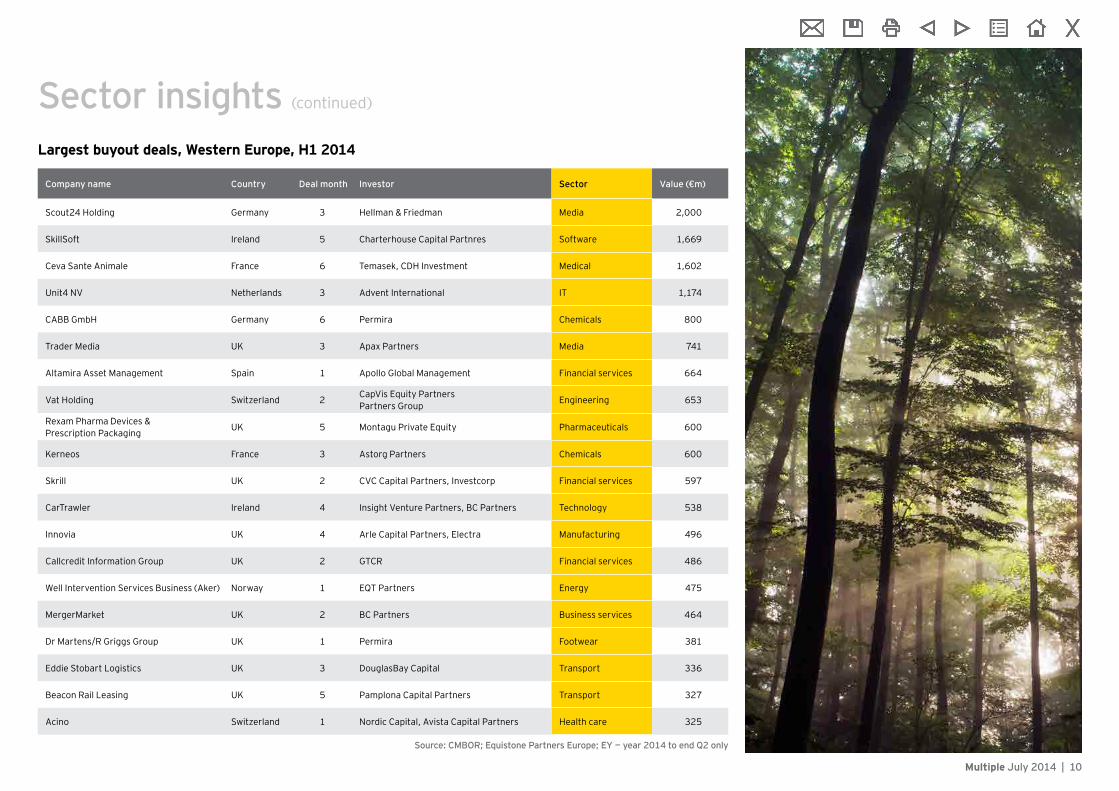

Largest buyout deals, Western Europe, H1 2014

Source: CMBOR; Equistone Partners Europe; EY — year 2014 to end Q2 only

Company name Country Deal month Investor Sector Value (€m)

Scout24�Holding Germany 3 Hellman & Friedman Media 2,000

SkillSoft Ireland 5 Charterhouse Capital Partnres Software 1,669

Ceva Sante Animale France 6 Temasek, CDH Investment Medical 1,602

Unit4�NV� Netherlands 3 Advent International IT 1,174

CABB GmbH Germany 6 Permira Chemicals 800

Trader Media UK 3 Apax Partners Media 741

Altamira Asset Management Spain 1 Apollo Global Management Financial services 664

Vat�Holding Switzerland 2 CapVis�Equity�Partners Partners Group Engineering 653

Rexam Pharma Devices & Prescription Packaging UK 5 Montagu Private Equity Pharmaceuticals 600

Kerneos France 3 Astorg Partners Chemicals 600

Skrill UK 2 CVC�Capital�Partners,�Investcorp Financial services 597

CarTrawler Ireland 4 Insight�Venture�Partners,�BC�Partners Technology 538

Innovia UK 4 Arle Capital Partners, Electra Manufacturing 496

Callcredit Information Group UK 2 GTCR Financial services 486

Well Intervention Services Business (Aker) Norway 1 EQT�Partners Energy 475

MergerMarket UK 2 BC Partners Business services 464

Dr Martens/R Griggs Group UK 1 Permira Footwear 381

Eddie Stobart Logistics UK 3 DouglasBay Capital Transport 336

Beacon Rail Leasing UK 5 Pamplona Capital Partners Transport 327

Acino Switzerland 1 Nordic Capital, Avista Capital Partners Health care 325

The H1 2014 results from CMBOR bring some positive news to the PE market. Contributing to this uptick is BC Partners’ successful acquisition of Mergermarket, the UK-based provider of global news, intelligence, analysis and data. This deal is one of the largest completed buyouts in Western Europe in 2014. Multiple speaks to Hamilton Matthews, CEO of Mergermarket, about this transaction and its approach to partnering with PE.

Q. After eight years of corporate ownership under Pearson, Mergermarket has found a new owner in PE

firm BC Partners. Can you tell us about the deal and how it fits into your current strategy?

Broadly, our sale was a typical corporate carve-out. Pearson had decided that its strategy was focused on more pure educational plays. Accordingly, the FT Group, which is owned by Pearson and which we were part of, has been broken up over the past few years. When Pearson appointed a new CEO last year, he encouraged�us�to�find�a�sensible�home.�Pearson�embarked�on�the�sale process last June, and went to market in September. The whole process moved very swiftly and was completed between Pearson�and�BC�Partners�by�November�2013.

The�buyers�in�the�final�round�were�big�buyout�firms,�along�with�some�bulge-bracket�corporates.�It’s�an�interesting�point�to�underline�that,�when�the�deal�is�right,�the�big�buyout�firms�will�dip into the mid-market.

Q. What were the main challenges to finding an appropriate buyer?

During the sale, Pearson was understandably and ultimately looking�for�the�best�price�—�that’s�the�key�motivation�for�virtually�all selling parties. Despite this, Pearson was very open and collaborative, and was eager to reach a decision with which Mergermarket’s�management�team�was�comfortable.

Both Pearson and Mergermarket agreed that BC Partners was the standout contender in the auction process, primarily because they offered the highest price, but also because of the firm’s�complete�understanding�of�our�business�and�the�market�in which we operate. Early on, BC Partners researched and took an�analytical�approach�to�our�business.�The�firm�had�done�its�homework, and was not asking the routine questions other bidders were.

Q. During the transaction process, what was the most important factor in ensuring successful completion?

The most important aspect of the sale was putting together a credible and accurate representation of what our business is and does. The idea of selling Mergermarket as a data company was�floated,�but�that�is�not�at�the�heart�of�what�we�do.�We�are�an editorial and media business — so it was essential to represent the business the right way.

For us, having the right support network was crucial. We had a very supportive seller and a very credible investment bank, JP Morgan Cazenove, which was great at connecting us with potential buyers.

Q. Post-acquisition, what is your focus over the next 12 months?

In the short term, there are a number of things on our plate. We have put together a value creation road map that will help us focus�on�five�key�streams.�

Part of this plan includes operations. We have placed a huge amount�of�emphasis�on�financial�analysis.�We�have�figured�out that our reporting function is so different from what Pearson required.

Another�aspect�of�what�we’re�after�is�earnings�before�interest,�taxes, depreciation, and amortization (EBITDA) growth. But we are not necessarily looking for cost savings. Rather, the emphasis�is�on�figuring�out�what�is�core�to�our�business.�For�instance, Xport Reporter was deemed not to be core, so we closed that business stream down.

At the same time, we are also looking at a handful of bolt-on acquisitions, and we have some really interesting leads. We are seeking out purchases in markets in which we do not currently operate. We are also exploring organic growth options to expand our offerings to segments where we are currently active. These extensions should complement existing products and help us tighten up our business plan.

Multiple July 2014 | 11

Inside the deal

UK

The�UK�continued�its�consistent�performance.�It�accounted�for�35%�of�all�buyout�value�in�H1�2014,�when�it�generated�€9.1b�from�111�deals.�This�is�€1.7b�higher�than�the�value�of�H1�2013,�when�€7.4b�was�garnered�from�87�deals.

The�exit�market�in�the�UK�has�remained�strong�so�far�in�2014.�Nearly�half�of�all�European�exits�(95�out�of�195)�have�taken�place�in�the�UK.�These�deals�have�contributed�40%�(€22.2b)�of�the�total�European�exit�value�(€55.2b).

H1: €9.1b from 111 buyouts — largest deal: €741.0m

Germany

Germany�was�the�second-strongest�market�in�terms�of�buyout�numbers�in�Q2�2014.�Its�19�deals�contributed�€1.4b�of�value�—�13%�of�the�total�sum�of�European�deals.�However,�this�was�50%�less�in�total�deal�value�than�the�€2.8b�seen�in�Q1.�

This�relatively�slow�start�to�2014�was�confirmed�on�the�exit�side.�Just�20�private�equity�exits�contributed�a�value�of�€6.1b�—�11%�of�the�total�European�market�in�H1�2014.�This�represents�little�more�than�a�third�of�2013�exit�value�in�the�country.�There�is�a�healthy�level of large exit deals in the pipeline in the engineering, manufacturing and industrials sectors.

H1: €4.3b from 35 buyouts — largest deal: €2.0b

Multiple July 2014 | 12

Country spotlight

France

Activity�in�France�has�slowed,�with�just�14�deals�completing�in�Q2�2014.�This�compares�with�25�in�Q1�2014�and�19�in�the�final�quarter�of�2013.�However,�at�€1.7b,�France�accounted�for�15%�of�all�Western�Europe’s�buyout�value�in�Q2.

With�28�exits�in�2014,�volume�has�been�holding�up�in�the�French�exits�market.�France�was�the�second�most�active�market�after�the�UK�(95).�The�total�exit�value�of�€5.9b�in�H1�2014�is�already�approaching�the�total�of�2013�(€7.9b),�and�it�is�far�above�2012’s�total�exit�value�(€3.8b).

H1: €3.4b from 39 buyouts — largest deal: €1.6b

Spain

There�was�a�strong�uptick�in�the�Spanish�buyout�market�in�Q2�2014.�The�quarter�saw�11�deals�completed,�compared�with�only�3�in�Q1.�The�largest�transaction�in�the�second�quarter�was�the�acquisition�of�Cementos�Balboa�by�KKR,�for�an�estimated�value�of�€225m.

Spain�has�also�seen�a�significant�increase�in�exit�values�so�far�this�year.�With�nine�deals�contributing�€7.2b,�H1�2014�has�already�outpaced�the�total�2013�figure�of�€1.3b.�Spain�accounted�for�4�of�the�top�15�exits�in�Q2�2014,�including�the�trade�sale�of�Avincis�and the Applus IPO.

H1: €1.2b from 14 buyouts — largest deal: €664.0m

Multiple July 2014 | 13

Country spotlight (continued)

Ireland

Netherlands

With�a�total�value�of�€2.2b�from�three�deals�in�H1�2014,�Ireland�has�recorded�its�highest�value�since�2010.�These�impressive�numbers were due, in large part, to the second-largest deal of the year. This is the acquisition of Skillsoft by Charterhouse Capital Partners�from�Berkshire�Partners,�Bain�Capital�and�Advent�International�Corporation.�This�secondary�buyout�was�valued�at�€1.7b.�

With�€1.8b�of�total�value�from�21�deals,�the�Dutch�buyout�market�has�almost�equaled�the�total�deal�value�seen�last�year�(€1.9b).�This�is�due�largely�to�the�€1.2b�acquisition�of�Dutch�software�company�Unit4�NV�by�global�private�equity�firm�Advent�International�in�Q1�2014.�

On the exits side, there have been four secondary buyouts and one trade sale so far this year. Together, they have raised just €251m.�This�is�significantly�lower�than�the�first�half�of�2013,�both�in�terms�of�value�(€621)�and�volume�(nine�exits).

H1: €2.2b from 3 buyouts — largest deal: €1.7b

H1: €1.8b from 21 buyouts — largest deal: €1.2b

Country spotlight (continued)

Multiple July 2014 | 14

Multiple July 2014 | 15

CMBOR methodologyThe data only includes the buyout stage of the PE market (MBO, MBI, institutional buyout (IBO) and buy-in management buyout (BIMBO)), and does not include any other stage, such as seed, start-up, development or expansion capital.

Unless otherwise stated, the data includes all buyouts, whether PE-backed or not, and there is no size limit to deals recorded.

In�order�to�be�included�as�a�buyout,�over�50%�of�the�issued�share�capital�of�the�company�has to change ownership, with either management or a PE company, or both jointly, having a controlling stake upon deal completion.

Buyouts and buy-ins must be either management-led or led by a PE company using equity capital primarily raised from one or more PE funds.

Transactions that are deemed not to adhere to the PE, MBO or MBI model are not included.

Transactions that are funded from other types of funds, such as real estate and infrastructure,�are�not�included.�Deals�in�which�a�PE�firm�buys�property�as�an�investment�are not included.

In order to be included, the target company (the buyout) must have its own separate financing�structure�and�must�not�be�held�as�a�subsidiary�of�a�parent�holding�company�after the buyout.

Firms�that�are�purchased�by�companies�owned�by�a�PE�firm�are�treated�as�acquisitions�and are not included in the buyout statistics. However, these deals are recorded in the “acquisitions by buyout companies” statistics.

All quoted values derive from the total transaction value of the buyout (enterprise value) and include both equity and debt.

The buyout location is the location of the headquarters of the target company and it is not related to the location of the PE company.

The quarterly data only counts information on transactions that formally close in that quarter and does not include announced deal information.

Multiple July 2014 | 15

Multiple July 2014 | 16

For more information, please visit ey.com/multiple.

Contacts

Marketing:Pierre VigourouxTransaction Advisory Marketing+�33�1�55�61�01�[email protected]

Sachin DateEMEIA Private Equity Leader+�44�20�7951�[email protected]

Multiple July 2014 | 17

Further insights

Global IPO Trends 2014 Q2After a bumper start to the year with the strongest first�quarter�since�2011,�global�IPO�activity�continued to climb in the second quarter.

Global Corporate Divestment Study 2014The�2014�Global Corporate Divestment Study focuses on how companies review their portfolios and the leading practices of those that are able to maximize divestment outcomes.

Global Integration Survey 2014Our�survey�reveals�five�key�practices�that�companies need to follow in order to deliver on their strategic goals when it comes to post-deal integration.

Global Private Equity Watch 2014PE�has�started�2014�with�a�renewed�sense�of�confidence�via�an�improvement�in�fund-raising conditions and an increase in exit pace and options.

Capital InsightsHow can companies combine the best traditional business methods with innovative approaches to help shape their destinies?

Global Capital Confidence Barometer April 2014The Global Capital Confidence Barometer surveyed�a�panel�of�more�than�1,600�executives�to identify boardroom trends and practices in the way companies manage their capital agendas.

View report View report

View report

View report

For more information, visit ey.com/privateequity.

For more information, visit ey.com/mergerintegration.

View report

For more information, visit ey.com/ipocenter.

View report

For more information, visit capitalinsights.info.

For more information, visit ey.com/ccb.

For more information, visit ey.com/divest.

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

About EY’s Transaction Advisory ServicesHow you manage your capital agenda today will define your competitive position tomorrow. We work with clients to create social and economic value by helping them make better, more informed decisions about strategically managing capital and transactions in fast-changing markets.�Whether�you’re�preserving,�optimizing,�raising�or�investing�capital,�EY’s�Transaction�Advisory�Services�combine�a�unique�set�of�skills, insight and experience to deliver focused advice. We help you drive competitive advantage and increased returns through improved decisions across all aspects of your capital agenda.

©�2014�EYGM�Limited.�All Rights Reserved.

EYG�no.�DE0560�

EMEIA Marketing Agency 1001290

ED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice.

ey.com/multiple

EY — recognized by mergermarket as top of the European league tables for accountancy advice on transactions in calendar year 2012 and 2013

The views of third parties set out in this publication are not necessarily the views of the global EY organization or its member firms. Moreover, they should be seen in the context of the time they were made.