[email protected] mary k. samsa · counseling with associated risk assessment with respect to...

TRANSCRIPT

Departments

Practice Areas

EducationJ.D., DePaul University -

College of Law, 1996, High Honors

M.S.T., DePaul University - College of Commerce, 1992

B.S., magna cum laude, University of Illinois, 1988

AdmissionsIllinois

Court AdmissionsU.S. District Court,

Northern District of Illinois

Business

Employee Benefits and Executive Compensation

[email protected] Chicago

Phone: 312.873.3667Fax: 312.819.1910

MARY K. SAMSA Shareholder

Mary K. Samsa is a member of the Employee Benefits and Executive Compensation practice group. In her 15+ years of practice, she has represented a wide range of organizations including, but not limited to, Fortune 100 public companies, privately-held companies, multinational organizations, not-for-profit hospital systems as well as educational institutions. Her primary practice focuses on executive compensation (for both taxable and tax-exempt entities) where she regularly advises on nonqualified deferred compensation arrangements, executive employment arrangements (including the rebuttable presumption of reasonableness for tax-exempt entities), equity compensation arrangements, SEC reporting, Section 162(m) compliance and change in control issues, to name just a few.

Ms. Samsa has also developed significant experience in international employee benefit issues whereby her relationship with attorneys in over 100 countries enable her to provide rapid turnaround on time-sensitive international mobile employee tax and employment issues.

Ms. Samsa also maintains a core practice with respect to qualified retirement plans for both taxable and tax-exempt entities (including defined benefit, 401(k), 403(b) and 457(b)). She frequently interfaces with Boards of Directors, Compensation Committees and Retirement/Investment Committees on employee benefit governance matters and fiduciary counseling with associated risk assessment with respect to legal and regulatory compliance. The Legal 500 US writes that Ms. Samsa provides "practical and thorough advice on retirement and executive compensation" matters.

Memberships and Affiliations

■ American Bar Association ■ Tax and International Sections

■ American Benefits Council ■ Policy Committee

■ Empowering Women Network (EWN) ■ Global Equity Organization, Founder, Midwest Chapter ■ Illinois State Bar Association

■ Employee Benefits Section■ National Association of Stock Plan Professionals ■ Society for Human Resource Management (SHRM)

Distinctions

■ Ranked in Chambers USA 2010

EXPERIENCE

Ms. Samsa's representative experience includes:

■ Counseled a public mobility company in benefit plan integrations or terminations associated with corporate acquisitions and divestitures of various business divisions including: benefit plan freezes, mergers and consolidations with protected benefits;

benefit plan terminations and respective governmental agency filings; broad-based severance package design and implementation; executive change-in-control agreements; and employee transition services.

■ Assisted a hospital system with respect to its benefit plan integration issues associated with merger of another similar size hospital system including: compliance review of frozen plans acquired due to merger and filing of corresponding EPCRS with IRS to correct errors detected; termination of frozen plans following sign off of EPCRS by IRS and associated governmental filings; preparation of employee communications regarding errors and corrections; and assist with employee transition services in migration to surviving entity's benefits and payroll platform.

■ Implemented for a hospital system the consolidation of roughly 15+ annuity contract vendors under its 403(b) plan to simplify administration and take advantage of the IRS and DOL provided orphan contract rules for exclusion of certain pre-2009 contracts from inclusion in the newly required 2009 audited financial statements and Form 5500 filings.

■ Advised a public consumer products manufacturer on its evaluation of securities lending losses sustained with its defined contribution plan trustee to identify potential fiduciary exposure, if any, and possible proactive steps to take given ramp up in litigation related to this issue.

■ Coordinated for a US-based international pharmaceutical and medical device company the extension of a broad-based equity compensation plan to 65 jurisdictions and globally advised on: underlying drafting of the main omnibus plan document which is international in scope; securities law, exchange control laws, labor laws, acquired rights issues, data privacy and tax laws by jurisdiction; and preparation and submission of necessary governmental filings.

■ Assisted a public electronic technologies company in the consolidation of its medical, dental, vision and insurance plans for its 25+ operating companies into a single health and welfare plan at the parent-company level to achieve economies of scale and provide negotiating leverage on fee structure by combining all 40,000 employees under one plan umbrella.

PUBLICATIONS & PRESENTATIONS

May 2010 ERISA Fiduciary and Claim Procedures, Chapter 3M. Lee Smith PublishingCo-Author

May 2010 Expatriate Deferred Compensation Arrangement and Sections 409A and 457APractical Law Corporation (PLA)

May 2010 Applying Section 409A to Non-US Share Schemes Practical Law Corporation (PLC)

April 29, 2010 Worker Misclassification: Ouch! That's Gonna Leave a MarkNationally Broadcast AT&T Webinar

April 15, 2010 The Brave New World of Say on PayGlobal Equity Organization Annual Conference; Chicago, Illinois

March 9, 2010 Compensation Risk Analysis, Methodology for SEC FilersCommittee Training Presentation; Lincolnshire, Illinois

February 6, 2010

2010 IRS Employment Tax Audits: Are Your Programs Up To ParNationally Broadcast AT&T Webinar

February 4, 2010

Issue Spotting and Knowing What to Look For on the Employee Benefit Side of a TransactionChicago Bar Association

January 28, The Brave New World of 403(b): Issue Spotting for the Future

2010 Nationally Broadcast AT&T Webinar

October 21, 2009

Corporate Fiduciary StructuresCommittee Training Presentation; Rocky Hills, Connecticut

October 8, 2009

Leading the Way Through ChangeCorporate Leadership Series; Chicago, Illinois

September 22, 2009

Say on Pay: Part DeuxGlobal Equity Organization MidwestOne-Day Meeting, Chicago, Ilinois

July 2009 Chapter Entitled: United StatesPart of the Globe Business Publishing Series called Buys-Ins and Buy-Outs —The Elimination of Defined Benefit Pension Scheme Liability Co-Author

June 2009 Chapter Entitled: Protecting Your Stock PlanPart of the GEOConference Industry BookCo-Author

April 2009 Overcoming the New 403(b) Challenges—2009 Audits and Form 5500 FilingsBenefits & Compensation Law for Nonprofits

October 2008 Year-End Defined Contribution Plan CheckupJournal of Compensation and Benefits Law Alert

May 8, 2008 Moving Employees Internationally Here Today, Gone Tomorrow - But Still Needing Benefits Southern Employee Benefits ConferencePresentation given in Aventura, Florida

February 26, 2008

403(b) Best Practices and UpdateBlue Prairie Group Webinar

February 14, 2008

2008 The Year for Tax-Exempt Compliance: New Requirements for Tax-Except Compensation and Benefits Programs, and How to ComplyConference sponsored by Seyfarth Shaw

November 2007

Can Medical Tourism Cure What Ails YouBenefits & Compensation Law AlertCo-Author

October 2007 Chapter Entitled: 2006 Pension Reform in the United StatesPart of the Ius Laboris series called Deficit Reductions Across the WorldCo-Author

June 29, 2007 Integrating and Encompassing Corporate Governance Standards Into Your Global Equity ProgramGlobal Equity Organization’s Annual Conference Presentation given in London, UK

May 15, 2007 European Legal Stock UpdatesGlobal Equity Organization Midwest Chapter MeetingPresentation given in Chicago, Illinois

May 2007 Identifying Your Disqualified Persons for Excess Benefit Transactions

Benefits & Compensation Law for NonprofitsAuthor

April 25, 2007 Stock Option Backdating: New Rules and Enforcement TrendsM. Lee Smith Publishers LLC Audio Conference

January 24, 2007

SEC Executive Compensation Disclosure RulesNationally Broadcast AT&T Webinar

January 2007 Gearing Up for the New SEC Disclosure Requirements—Part II Benefits & Compensation Law Alert

December 2006

Gearing Up for the New SEC Disclosure Requirements—Part I Benefits & Compensation Law Alert

October 18, 2006

Knock, Knock . . . Who's There? The IRS - Planning and Internal Compliance ReviewM. Lee Smith Publishers Teleconference, National

October 2006 The Employer’s Immigration Handbook Kluwer Law International. First Ed.Editor

October 2006 PPA Provisions Affect Qualified Retirement Plan of NonprofitsBenefits & Compensation Law for Nonprofits, Vol. 22, No. 10

September 13 2006

Compensation: Covering the Globe – A Symposium Chicago Compensation AssociationPresentation given in Chicago, Illinois

August 17, 2006

The Pension Protection Act of 2006: The Good, The Bad and The UglyNationally Broadcast AT&T Webinar

June 2006 Redesign Options for Nonqualified PlansBenefits & Compensation Law for Nonprofits

March 25, 2006

Employee Benefit Issues in International Mergers and AcquisitionsJohn Marshall Law SchoolPresentation given in Chicago, Illinois

March 2006 Executive Compensation Audits: New Developments, Best-Practice GuidesBenefits & Compensation Law for Nonprofits

December 2005

Department of Treasury Issues Proposed Regulations on the Tax Treatment of Supplemental WagesBenefits & Compensation Law for NonprofitsCo-Author

October 7, 2005

IRS Executive Compensation Enforcementllinois Hospital AssociationPresentation given in Naperville, Illinois

October 2005 Use of Electronic Media for Employee Benefit Notices, Elections and ConsentsBenefits and Compensation Law AlertCo-Author

September 23, 2005

Addressing Recent Litigation in Your Award Agreements (A Multijurisdictional Panel Discussion)GEO Annual ConferencePresentation given in London, England

September 15, 2005

Getting Ahead of the Curve with Your 401(k) PlanPreparing for an IRS Compliance Audit, Plan Sponsor Advisors Full-Day SeminarPresentation given in Chicago, Illinois

July 2005 Keep Your Eye on the Ball with Your 457(f) PlanBenefits and Compensation Law Alert

June 12, 2005 Compliance Issues Facing Multinationals in Jurisdictions Other Than EuropeGlobal Equity Organization Midwest Chapter MeetingPresentation given in Chicago, Illinois

Spring 2005 Five Key Contractual Issues to Consider When Switching 403(b) VendorsBNA Tax ManagementCo-Author

April 27, 2005 The American Jobs Creation Act of 2004: How the New Legislation Impacts Your Organization’s Nonqualified Deferred Compensation PlansPresentation given in Chicago, Illinois

April 4, 2005 Current Issues with Section 457(f) Plans: Legislative and Regulatory UpdateEnrolled Actuaries MeetingPresentation given in Washington, D.C.

Fall 2004 Equity Alternatives for U.S. ESOP Companies with Non-U.S. EmployeesThe Journal of Employee Ownership Law and Finance, Volume 16, No. 4, NCEOCo-Author

June 2004 International Employee Equity Plans: Participation Beyond BordersKluwer Law International First Ed. 2003Editor and Author of U.S. Chapter at 571, First Ed. 2003. Analyzed the legal ramifications (domestic and international) of extending equity-based compensation plans in over 30 jurisdictions

1

Retirement Plan Adviceand Other Governmental Initiatives

Presented by:Mary K. Samsa

©2010 Polsinelli Shughart PC

Agenda

• Investment Advice – Participant and Beneficiaries• Fee Disclosure Rules• 401(k) Questionnaire• IRS Employment Tax Audits

2

©2010 Polsinelli Shughart PC

Investment Advice– Participant and Beneficiaries

• Pension Protection Act of 2006 (PPA) introduced a new prohibited transaction exemption whereby qualified “fiduciary advisors” can offer personally-tailored investment advice to help EEs manage their defined contribution plan accounts

– Portfolio recommendations must be generated based on an unbiased computer model that has been certified and audited by an independent third party

– Fiduciary advisors must provide investment advice by charging a flat fee that does not vary depending on the investment option chosen

©2010 Polsinelli Shughart PC

Investment Advice– Participant and Beneficiaries (proposed)

• Proposed regulations on implementation of this rule released February 26, 2010 – became effective May 27, 2010– Eliminated the class exemption – so no “off-model” advice (e.g., no

individualization of the computer model)– With respect to fee-leveling, fiduciary advisors providing investment

advice under this PTE may not receive compensation from any other party, including any affiliate of the advisor, on the basis of their recommendations

– Advice must be based on generally-accepted investment theories that take into account historic risks/returns of different assets

3

©2010 Polsinelli Shughart PC

Investment Advice– Participant and Beneficiaries (proposed)

• Proposed regulations (continued)– Investment management fees/expenses for the advice must be

taken into account– Individual participant information is considered– The plan fiduciaries authorize the use of the advice arrangement– Arrangement must be audited/certified annually

©2010 Polsinelli Shughart PC

Fee Disclosure Rules

• Interim final regs on implementation of fee disclosure rules released July 16, 2010 – become effective July 15, 2011

• Applies only to defined contribution plans and defined benefit plans (not to health and welfare plans – to be issued separately)

-

4

©2010 Polsinelli Shughart PC

Fee Disclosure Rules

• Applies if at least $1,000 will be received in compensation in connection with services to the plan that include:– Certain fiduciary advisory services– Recordkeeping or brokerage service for participant-directed

accounts with respect to investment options made available– Other services for which indirect compensation is received (such as

accounting, auditing, actuarial, consulting, custodial, legal, recordkeeping, etc.)

• FOCUS: Amount of compensation received for plan services and potential conflicts of interest that might compromise the quality of those services

©2010 Polsinelli Shughart PC

Fee Disclosure Rules

• Information which must be disclosed in WRITING– Description of services– All direct and indirect compensation to be received by provider, its

affiliates or subcontractors• Direct compensation is compensation received directly from the

plan• Indirect compensation is generally received from any source

other than the plan sponsor, service provider, affiliate or subcontractor

– Attempt to capture some of this already on Schedule C of Form 5500

5

©2010 Polsinelli Shughart PC

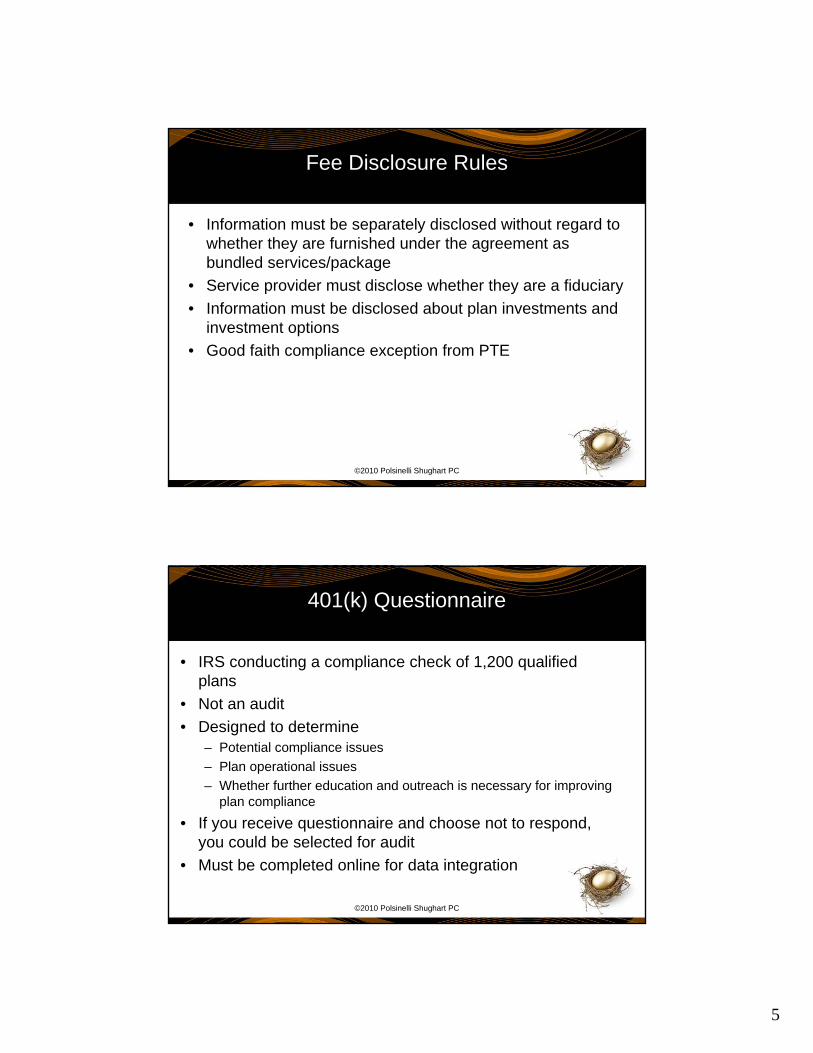

Fee Disclosure Rules

• Information must be separately disclosed without regard to whether they are furnished under the agreement as bundled services/package

• Service provider must disclose whether they are a fiduciary• Information must be disclosed about plan investments and

investment options• Good faith compliance exception from PTE

©2010 Polsinelli Shughart PC

401(k) Questionnaire

• IRS conducting a compliance check of 1,200 qualified plans

• Not an audit• Designed to determine

– Potential compliance issues– Plan operational issues – Whether further education and outreach is necessary for improving

plan compliance

• If you receive questionnaire and choose not to respond, you could be selected for audit

• Must be completed online for data integration

6

©2010 Polsinelli Shughart PC

401(k) Questionnaire

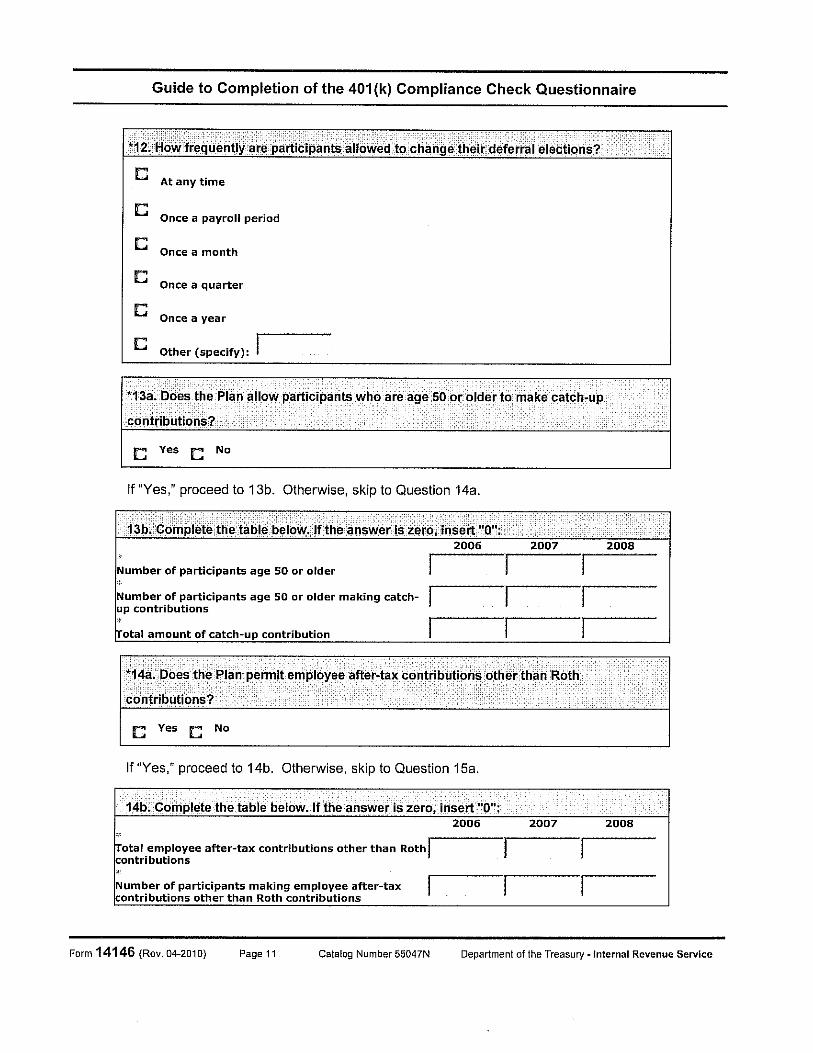

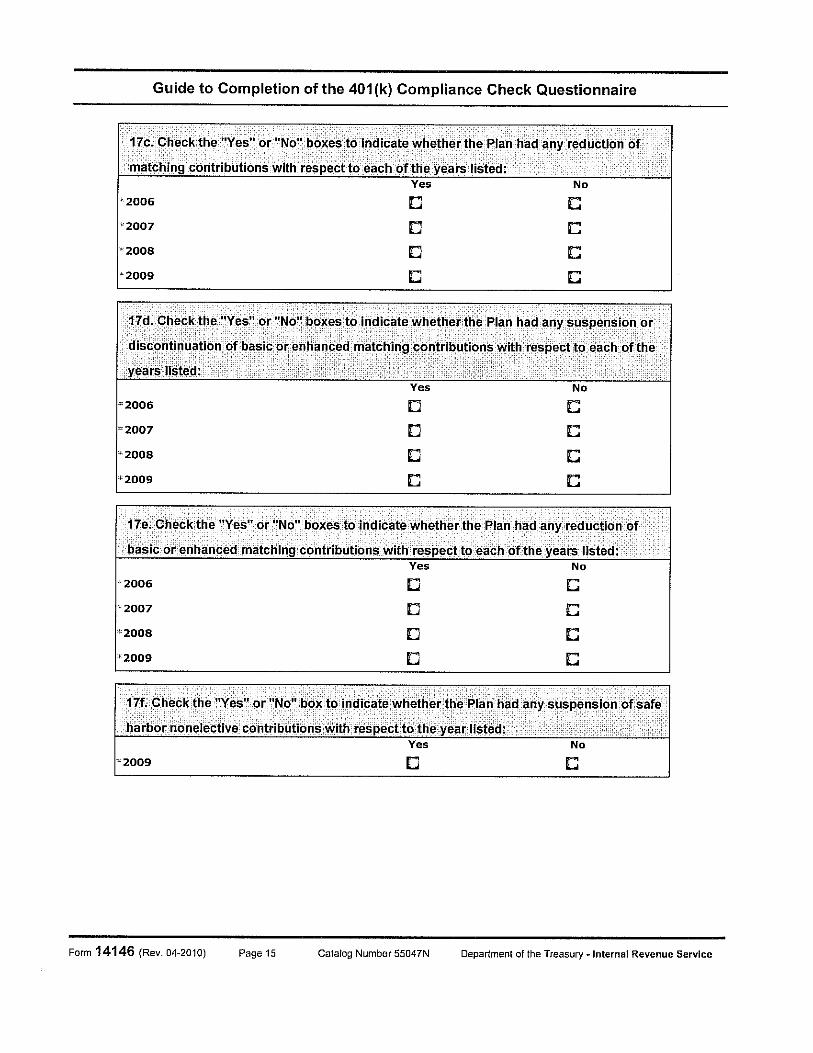

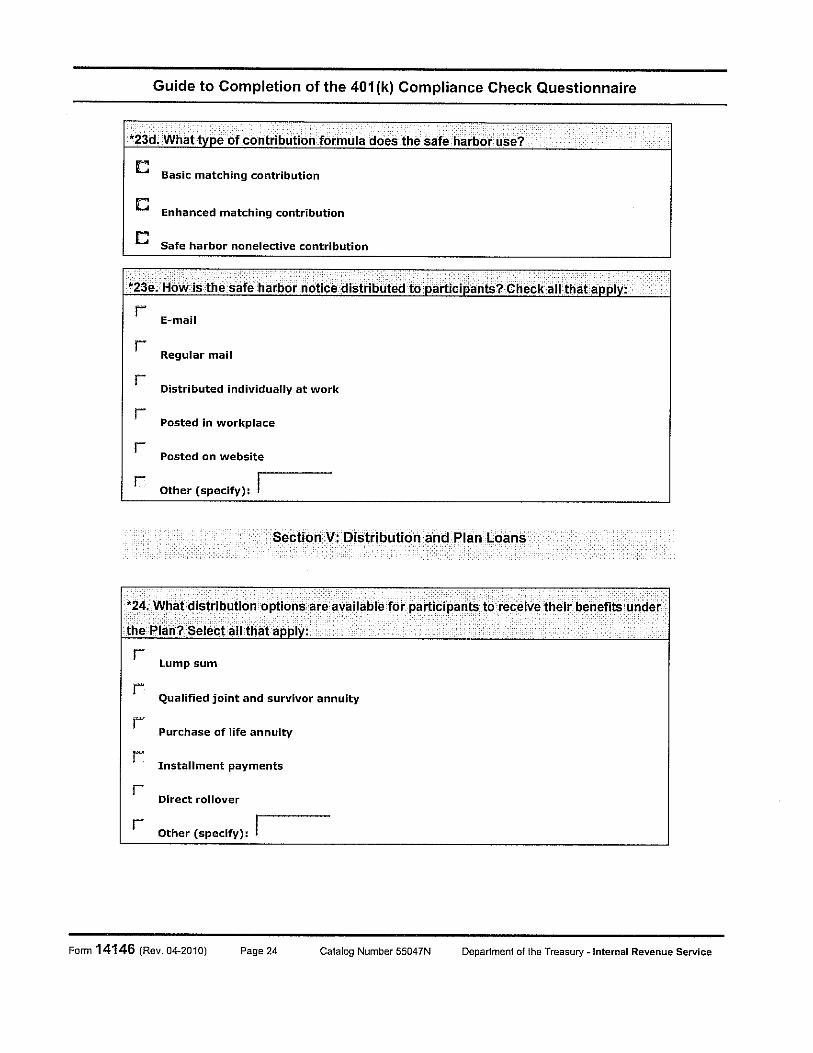

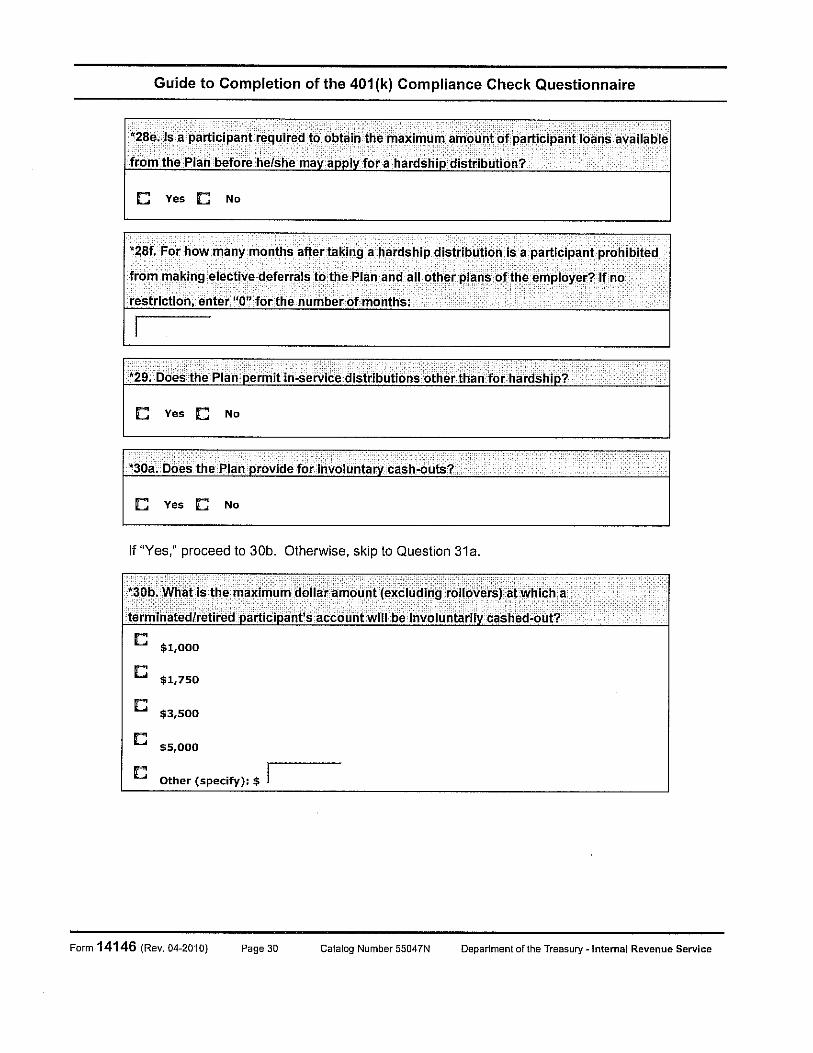

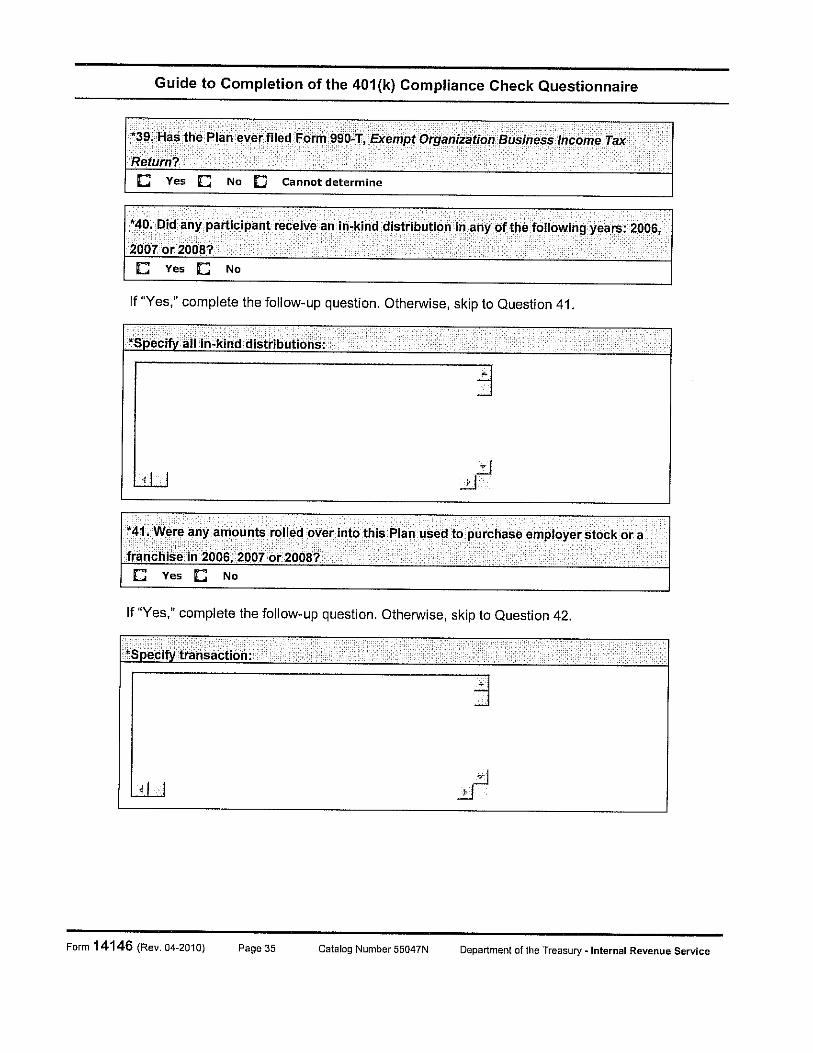

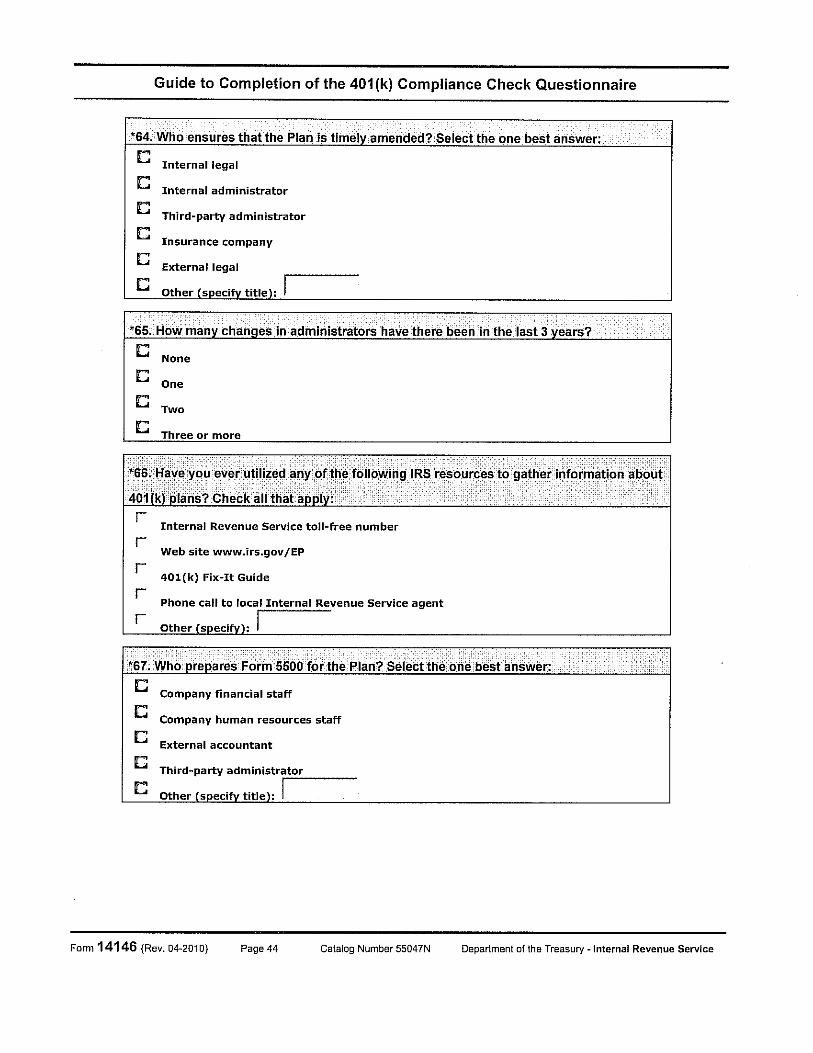

• Broad array of topics must be responded to– 401(k) plan participation– Employer and employee contributions– Nondiscrimination rules– Distributions and plan loans– Plan administration– Automatic contribution arrangements– Previous use of IRS voluntary correction program

• Questionnaire is 46 pages so somewhat time consuming to respond to

©2010 Polsinelli Shughart PC

IRS Employment Tax Audits

• In November 2009, IRS launchedits latest National Research Program (NRP)– NRP focus is detailed examination of employment taxes– Approximately 6,000 audits over the next three years– Desired result: assessments ($$$) plus statistical data regarding

overall employment tax compliance– Develop baseline for taxpayer voluntary compliance procedures– IRS is allocating 250 of its most experienced

auditors to this

7

©2010 Polsinelli Shughart PC

IRS Employment Tax Audits

• Why employment taxes?– “Tax Gap” – difference between taxes that are actually owed and

taxes are actually paid– Will raise revenue, reduce deficit and fund other government

programs

©2010 Polsinelli Shughart PC

IRS Employment Tax Audits

• Taxes which are the focus– Income taxes – deducted from employee wages– FICA (Social Security (OASDI) and Medicare

(HI)) – deducted from employee wages but matched by employer

– FUTA (federal unemployment) – paid by employer

8

©2010 Polsinelli Shughart PC

IRS Employment Tax Audits

• Key areas which are being audited– Employee/independent contractor classifications– Code Section 409A audits– Golden parachute payments following change in control and

collection of the 20% excise tax– Reporting of equity compensation – in particular incentive stock

options (ISOs) and employee stock purchase plans (ESPPs)– Fringe benefit programs

• Everything is taxable unless it meets a Code Section exception• Verification that benefits are non-taxable fringes

©2010 Polsinelli Shughart PC

Questions ?

9

About the Presenter

Mary K. SamsaPolsinelli Shughart PC

161 N. Clark StreetSuite 4200

Chicago, Illinois 60601 312.873.3667

Mary K. Samsa is a shareholder in the Employee Benefits and Executive Compensation practice group. She regularly advises public companies, privately-held companies, multinational organizations, not-for-profit hospital systems as well as educational institutions with respect to qualified retirement plans (including defined benefit, 401(k), 403(b) and 457(b)). She frequently interfaces with Boards of Directors, Compensation Committees and Retirement/Investment Committees on employee benefit governance matters and fiduciary counseling with associated risk assessment with respect to legal and regulatory compliance.

polsinelli.com

Retirement Plan Adviceand Other Governmental Initiatives

TYPICAL EMPLOYEE BENEFIT COMPLIANCE REVIEW SCOPE AND PROCEDURES

103911.1

Issue

Description

Comments/Recommendations

Decision

1.

Scope of Review -- Entities

Identify all entities in the controlled group of related entities, and then decide whether to review the benefit plans of all of them or only of some of them.

We recommend an initial meeting to discuss which employee benefit plans are made available at which entities.

2.

Scope of Review -- Plans

Identify for each entity all the employee benefit plans, programs and arrangements that will be reviewed, and decide: (a) whether to exclude any types of programs, (b) whether to exclude any individual programs, and (c) which programs to prioritize (if any).

We recommend reviewing all retirement and health/welfare plans. To manage the project more efficiently, and to recognize the differences inherent in retirement plans and health/welfare programs, we recommend to separate the review of the retirement plan(s) from that of the health/welfare programs

3.

Scope of Review -- Time Period

Decide on how far back to go in time, when reviewing these benefit programs. Many of the governmental initiatives are currently going back three years.

For manageability, it seems best to initially focus on the current status of these benefit programs. After the review of the current status is completed, a decision can be made on whether to undertake an added review of prior years and prior plans (based partly on what is found for the current status), usually two to three prior years.

4.

Scope of Review -- Depth

Decide whether to just review the “form” of these benefit programs (i.e., whether the plans, programs and arrangements comply on their face), or also to review “operations” (i.e., whether the plans, programs and arrangements comply in the manner in which they are administered). If operation is to be reviewed, consider whether both “sampling” and “interviewing” is desired.

Because good administration starts with having proper plan documents, it seems best to review “form” first, and then review “operation.”

5.

Scope of Review -- Intensity

Decide whether to limit the review to “major” issues (for form and/or for operation). Then, build customized checklists for the specific form/operation items that will be reviewed. Consider whether to review service provider actions as well as company’s actions.

We recommend a fairly thorough review of its plans (which would include a determination of whether the actions of service providers might result in a significant risk of liability). As noted above, we will provide checklists showing the form and operational issues to be analyzed, for each type of benefit program being reviewed. These lists may evolve as the project progresses, and as new issues are discovered.

6.

Scope of Review -- Special Issues

Identify any “special issues” regarding company’s benefit plan, programs and arrangements that should be considered when building the checklists for the specific matters to be reviewed and when conducting the reviews.

Do you have any special issues or areas of concern, which should be included in the checklists and specifically addressed?

TYPICAL EMPLOYEE BENEFIT COMPLIANCE REVIEW SCOPE AND PROCEDURES

-2-

Issue

Description

Comments/Recommendations

Decision

7.

Scope of Review -- Business Goals

Decide whether to add consideration of “business side” questions to the review, such as (a) whether benefit programs have been cost effective, (b) how programs compare to industry standards, and (c) whether service providers have been effective.

Do you have any business-related concerns with respect to your employee benefit programs?

* * *

* * *

* * *

* * *

1.

Procedures -- Contacts

Decide on the main contacts for for obtaining information, and also the “cc” contacts.

Key contacts can be determined at the initial meeting.

2.

Procedures -- Location of Data

Determine the extent to which the information needed is available at company’s main offices, and the extent to which certain information (whether in the form of written data, documents, oral history, or personnel) is available only at specific locations.

We believe that a thorough review can be completed with minimal travel, by maintaining an extranet site.

3.

Procedures -- Division of Labor

Decide on the general extent to which work will be done by outside counsel, and by the company, and on how much “on-site” work is expected. Decide also on the manner in which information will be made available to personnel.

Division of labor can be discussed and established during the initial meeting, understanding that it may be revisited and restructured at the client’s request.

4.

Procedures

-- Attorney/Client Privilege

Decide on work and communication procedures that will maximize the ability of the company to maintain “the privilege” for written materials produced in this review.

We can provide an outline setting out ways to preserve the privilege and dangers regarding the privilege (based on a review of current legal authorities).

TYPICAL EMPLOYEE BENEFIT COMPLIANCE REVIEW SCOPE AND PROCEDURES

-3-

Issue

Description

Comments/Recommendations

Decision

5.

Procedures -- Report Format

Make initial decisions on the desired format for the interim and final reports on the results of the compliance review.

This will be in part determined by the conclusions on attorney-client privilege, noted above. Some clients prefer that no report be put in writing. Others prefer a report. If a report is desired, we recommend first the preparation of a comprehensive draft report for the core team that will include major and minor findings (please note that this includes proactive ideas on ways to enhance the legal and business footings of the plans) and recommended actions to remediate the problems. After this report is reviewed by the core team, we would revise it and would describe the agreed upon remediation strategies. This document then serves as the workplan for future actions, rather than merely a look at the past. Finally, we recommend the preparation of an executive summary (which will include a description of overall findings, including all the things being done correctly, the workplan for remediation steps, and the progress made to date in carrying out the remediation workplan). This executive summary is typically the only document that is provided to senior management (other than general counsel and human resources) and to the Board.

6.

Procedures -- Timing Issues

Identify any special issues or desires on timing matters, such as contract renewals and items to prioritize. Consider overall timing scenarios for completion of segments of the project.

Because the project is certain to evolve and early on is subject to many variables, we do not recommend setting strict detailed deadlines for individual steps of the project. However, special timing issues may include (a) pending premium renewals, (b) expiring service provider contracts, (c) the period during which the corporate auditors are on site, and (c) any commitments made to senior management or to the Board concerning the completion of this or any other benefits-related project.

7.

Procedures -- Employee

Relations

Decide on the manner in which this overall project will be communicated to the employees who will be assisting and providing information.

The company should let people know that the goal is not to assign blame for benefit plan problems. When referring to the review project, we recommend not referring to it as an “audit.”

Polsinelli Shughart PC provides this material for informational purposes only. The material provided herein is general and is not intended to be legal advice. Nothing herein should be relied upon or used without consulting a lawyer to consider your specific circumstances, possible changes to applicable laws, rules and regulations and other legal issues. Receipt of this material does not establish an attorney-client relationship.

Copyright © 2010 Polsinelli Shughart PC.