mrf ltd detailed report with dec09 results...

TRANSCRIPT

1

MRF Limited

BUY Target Price: Rs.6825.00

CMP: Rs.6040.00 Market Cap. : Rs.25609.60mn.

Date: January 22nd

, 2010

Key Ratios:

Particulars FY08

(12 m)

FY09E

(12 m)

FY10E

(12 m)

OPM (%) 13 13 13

NPM (%) 4 5 5

ROE (%) 19 18 17

ROCE (%) 19 19 18

P/BV(x) 1.88 1.54 1.28

P/E(x) 10.12 8.49 7.72

EV/EBDITA(x) 1.03 3.42 3.38

Debt-Equity ratio 0.78 0.70 0.64

Key Data:

Sector Auto Tyres

Face Value Rs.10.00

52 wk. High/Low Rs.6899.00/1501.00

Volume (2 wk. Avg.) 13082

BSE Code 500290

SYNOPSIS • MRF is India`s largest tyre manufacturer, having a 22%

market share. The company derives over 95% of its

revenues from its core business i.e. tyres, the rest comes

from its presence in toys and paints. This focus on tyres

has enabled it to constantly increase capacities, and

maintain market leadership and profitability in most

segments. MRF exports its products to over 75 countries.

• The company has already declared and paid two interim

dividends of Rs 3 each per share for the year, thus

aggregating to a total dividend of Rs 25 per share for

FY09.

• Credit rating agency, CARE has assigned a AA+ rating to

the Long-term Bank Facilities of MRF (MRF). This rating is

applicable for facilities having tenure of over one year.

• The company signed the memorandum of understanding

(MoU) with government of Tamil Nadu for the new MRF

plant to be located at Perambulur, Trichy and also for

expansion of its existing plants in Tamil Nadu. This will be

MRF`s third plant to be established in Tamil Nadu.

• MRF will invest Rs 1.25 billion in production facility of the

tyres the product is produced after three years of in

house research. The production will start at its Medak

facility in Andhra Pradesh.

• The company’s Net sales and PAT are expected to grow at

a CAGR of 11% and 32% over FY08 to FY11E.

Share Holding Pattern:

V.S.R. Sastry

Vice President

Equity Research Desk

91-22-25276077

Dr. V.V.L.N. Sastry Ph.D.

Chief Research Officer

2

Table of Content

Content Page No.

1. Investment Highlights 03

2. Peer Group Comparison 07

3. Key Concerns 07

4. Financials 08

5. Charts & Graph 10

6. Outlook and Conclusion 12

7. Industry Overview 13

3

Investment Highlights

• Result Updates (Q4FY09)

For the fourth quarter, the top line of the company increased 5%YoY and stood at

Rs.14768.40mn against Rs.14021.40mn of the same period of the last year. The bottom

line of the company for the quarter stood at Rs.969.40mn from Rs.-46.70mn of the

corresponding period of the previous year i.e., an increase of 2176%YoY.

EPS of the company for the quarter stood at Rs.228.63 for equity share of Rs.10.00 each.

4

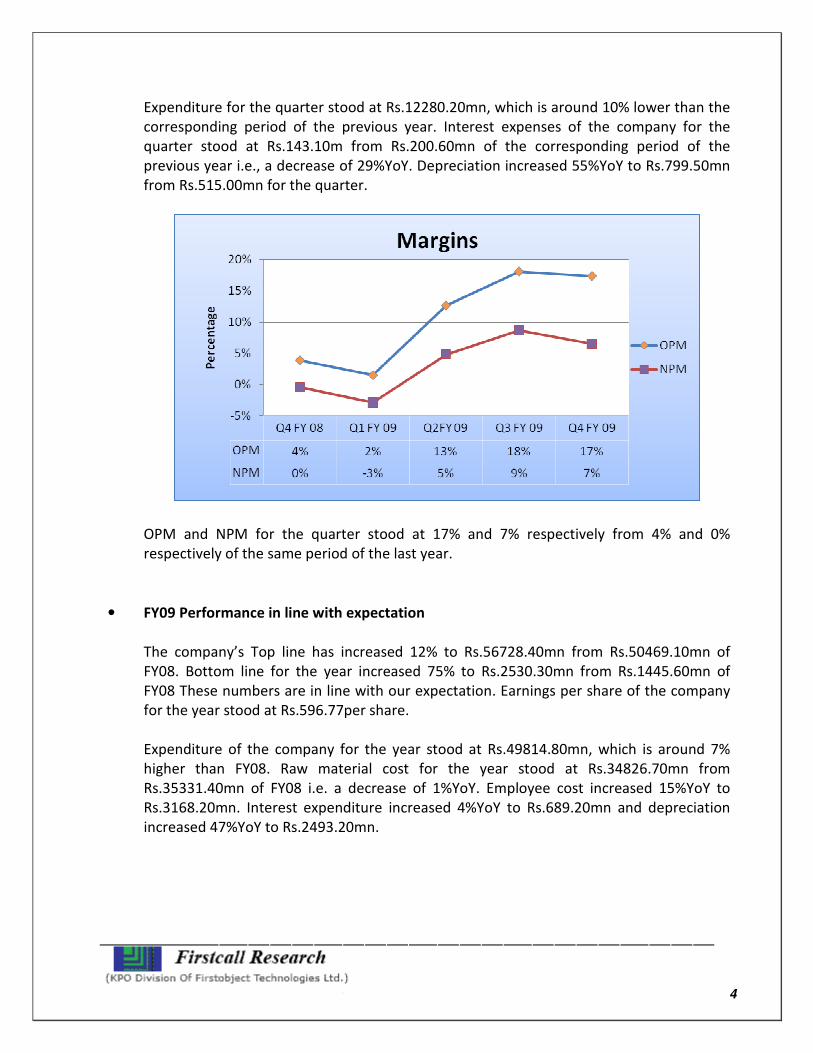

Expenditure for the quarter stood at Rs.12280.20mn, which is around 10% lower than the

corresponding period of the previous year. Interest expenses of the company for the

quarter stood at Rs.143.10m from Rs.200.60mn of the corresponding period of the

previous year i.e., a decrease of 29%YoY. Depreciation increased 55%YoY to Rs.799.50mn

from Rs.515.00mn for the quarter.

OPM and NPM for the quarter stood at 17% and 7% respectively from 4% and 0%

respectively of the same period of the last year.

• FY09 Performance in line with expectation

The company’s Top line has increased 12% to Rs.56728.40mn from Rs.50469.10mn of

FY08. Bottom line for the year increased 75% to Rs.2530.30mn from Rs.1445.60mn of

FY08 These numbers are in line with our expectation. Earnings per share of the company

for the year stood at Rs.596.77per share.

Expenditure of the company for the year stood at Rs.49814.80mn, which is around 7%

higher than FY08. Raw material cost for the year stood at Rs.34826.70mn from

Rs.35331.40mn of FY08 i.e. a decrease of 1%YoY. Employee cost increased 15%YoY to

Rs.3168.20mn. Interest expenditure increased 4%YoY to Rs.689.20mn and depreciation

increased 47%YoY to Rs.2493.20mn.

5

• Recommended a final dividend

The board of directors of the company has recommended a final dividend of Rs 19 per

share on the paid-up capital as at September 30, 2009.

The company has already declared and paid two interim dividends of Rs 3 each per share

for the above year, thus aggregating to a total dividend of Rs 25 per share for the year.

• Care assigns `AA+` & `PR+` ratings to MRF

Credit rating agency, CARE has assigned a AA+ rating to the Long-term Bank Facilities of

MRF (MRF). This rating is applicable for facilities having tenure of over one year.

Facilities with this rating are considered to offer high safety for timely servicing of debt

obligations and with this rating would have strong capacity for timely payment of short-

term debt obligations and carry lowest credit risk. Also, CARE has assigned PR1+ rating to

the Short-term Bank Facilities of the company. The above ratings are assigned for an

aggregate amount of Rs 8,450 million. CARE assigns `+` or `-` signs after the assigned

rating (wherever necessary) to indicate the relative position within the band covered by

the rating symbol.

Facility Amount (Rs million) Rating

Fund Based facilities 5600 AA+

Non-Fund based facilities 2850 PR1+

Total 8450

6

CARE has also assigned a PR1+ rating to the Rs.2 billion Commercial Paper Programme of

MRF. Instruments with this rating would have strong capacity for timely payment of short-

term debt obligations and carry lowest credit risk. The CP issue would have a maximum

maturity of 364 days and would be carved out of the working capital limits of the

company.

Rating Rationale

The ratings factor in the long operational track record of the company, its market

leadership position in the Indian Tyre industry with diverse product offerings, strong

brand image and wide distribution network, healthy growth in income and strong cash

accruals in the past and comfortable liquidity position. The ratings are constrained by the

low profitability margins, volatility in raw material prices which led to losses in Sep`08 and

Dec`08 quarters, not so favorable industry scenario consequent to the slowdown in

economic growth and the intensely competitive nature of the industry.

• Signing of ‘MOU’

The company signed the memorandum of understanding (MoU) with government of

Tamil Nadu for the new MRF plant to be located at Perambulur, Trichy and also for

expansion of its existing plants in Tamil Nadu. This will be MRF`s third plant to be

established in Tamil Nadu. The other factories in Tamil Nadu are located at Tiruvottiyur

and Arakonam. MRF is acquiring nearly 290 acres of land for its new facility in Perambulur.

• MRF to foray into aviation tyres

The company has announced entry in production of aviation tyres. The company will

invest Rs 1.25 billion in production facility of the tyres the product is produced after three

years of in house research. The production will start at its Medak facility in Andhra

Pradesh.

The company has announced its foray into the aviation tyre space with the unveiling of

Aero Muscle, a product born out of in-house research and perfected over the last three

years. The tyres were subjected to ground and flight trials. Upon completion of these,

MRF had been given provisional certificate for the commercial production of the approved

prototype aviation tyre. Tyres were approved for Chetak helicopters the Centre for

Military Airworthiness Certification and the Regional Centre for Military Airworthiness.

The company will also try to sell the tyres to private aviation company. This step according

to the company will help India by achieving self-sufficiency in such an import-substitute

product is always good for the country.

7

Peer Group Comparison

Name of the

company

CMP(Rs.)

(As on

January

22nd

, 2010)

Market Cap.

(Rs. Mn.)

EPS

(Rs.)

P/E (x) P/BV

(x)

Dividend

(%)

MRF 6040.00 25609.60 596.61 10.13 1.87 200.00

Apollo Tyres ltd 53.80 27116.50 4.93 10.91 2.00 45.00

Goodyear India 187.20 4318.10 26.90 6.96 2.74 60.00

Balakrishna

industries 543.70 10510.70 70.68 7.69 2.25 60.00

Key Concerns

� Recession in global economy

� Fluctuations in exchange rates

� High competition from global players

� Adverse Govt. policies

8

Financials Results Update

12 months ended Profit and Loss A/C (Standalone):

Value(Rs in million) FY08A FY09A FY10E FY11E

Description 12m 12m 12m 12m

Net Sales 50469.10 56728.40 62401.24 68641.36

Other Income 362.60 253.60 278.96 306.86

Total Income 50831.70 56982.00 62680.20 68948.22

Expenditure -46360.10 -49814.80 -54289.08 -59717.99

Operating Profit 4471.60 7167.20 8391.12 9230.23

Interest -662.50 -689.20 -756.76 -832.44

Gross Profit 3809.10 6478.00 7634.36 8397.79

Depreciation -1695.20 -2493.20 -2991.84 -3291.02

Profit before Tax 2113.90 3984.80 4642.52 5106.77

Tax -668.30 -1454.50 -1624.88 -1787.37

Net Profit 1445.60 2530.30 3017.64 3319.40

Equity Capital 42.40 42.40 42.40 42.40

Reserves 11165.50 13571.80 16589.44 19908.84

Face Value 10.00 10.00 10.00 10.00

Total No. of Shares 4.24 4.24 4.24 4.24

EPS 340.94 596.77 711.71 782.88

� Year ending September.

9

Quarterly ended Profit and Loss A/C (Standalone):

Value(Rs. in million) 31-Mar-08 30-Jun-09 30-Sep-09 31-Dec-09E

Description 3m 3m 3m 3m

Net Sales 14058.20 14382.10 14768.40 15211.45

Other Income 43.90 87.90 81.20 82.82

Total Income 14102.10 14470.00 14849.60 15294.28

Expenditure -12317.80 -11867.90 -12280.20 -12777.62

Operating Profit 1784.30 2602.10 2569.40 2516.66

Interest -202.80 -115.40 -143.10 -150.26

Gross Profit 1581.50 2486.70 2426.30 2366.40

Depreciation -550.80 -606.10 -799.50 -831.48

Profit before Tax 1030.70 1880.60 1626.80 1534.92

Tax -343.80 -623.60 -657.40 -537.22

Net Profit 686.90 1257.00 969.40 997.70

Equity Capital 42.40 42.40 42.40 42.40

Face Value 10.00 10.00 10.00 10.00

Total No. of Shares 4.24 4.24 4.24 4.24

EPS 162.00 296.46 228.63 235.31

10

Charts

• Net sales & PAT

• P/E Ratio (x)

11

• P/BV (X)

• EV/EBITDA(X)

12

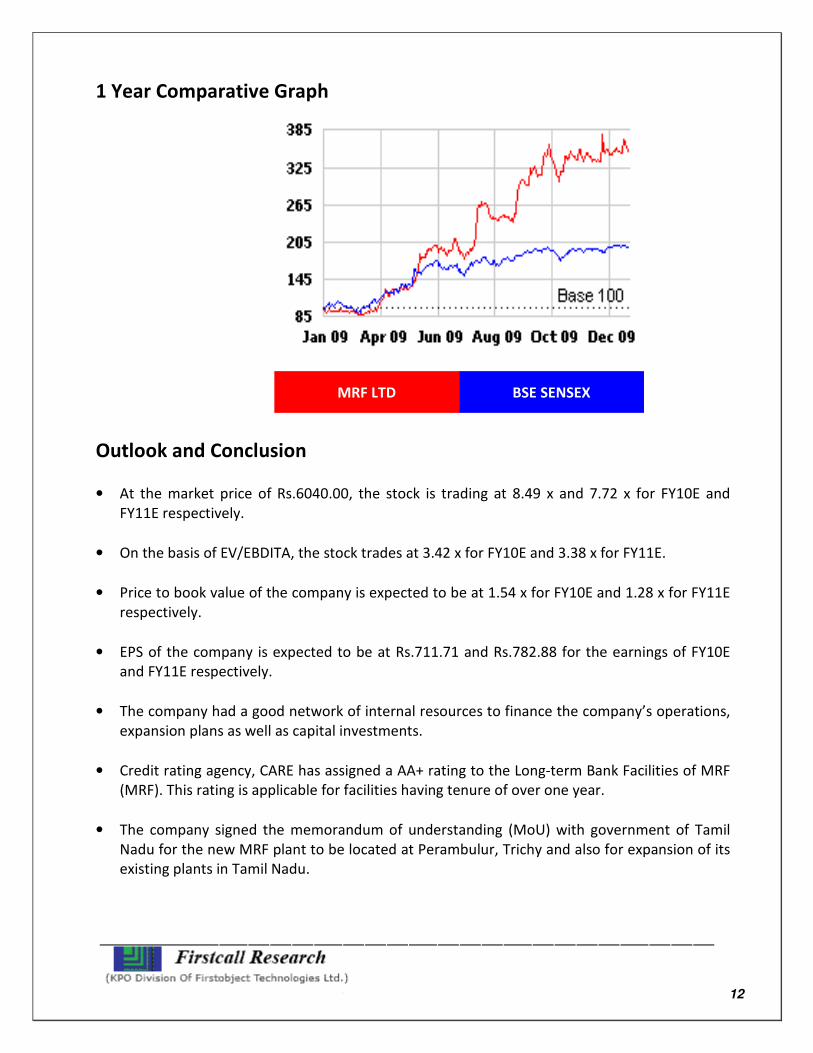

1 Year Comparative Graph

Outlook and Conclusion

• At the market price of Rs.6040.00, the stock is trading at 8.49 x and 7.72 x for FY10E and

FY11E respectively.

• On the basis of EV/EBDITA, the stock trades at 3.42 x for FY10E and 3.38 x for FY11E.

• Price to book value of the company is expected to be at 1.54 x for FY10E and 1.28 x for FY11E

respectively.

• EPS of the company is expected to be at Rs.711.71 and Rs.782.88 for the earnings of FY10E

and FY11E respectively.

• The company had a good network of internal resources to finance the company’s operations,

expansion plans as well as capital investments.

• Credit rating agency, CARE has assigned a AA+ rating to the Long-term Bank Facilities of MRF

(MRF). This rating is applicable for facilities having tenure of over one year.

• The company signed the memorandum of understanding (MoU) with government of Tamil

Nadu for the new MRF plant to be located at Perambulur, Trichy and also for expansion of its

existing plants in Tamil Nadu.

MRF LTD BSE SENSEX

13

• MRF will invest Rs 1.25 billion in production facility of the tyres the product is produced after

three years of in house research. The production will start at its Medak facility in Andhra

Pradesh.

• We recommend ‘BUY’ with a target price of Rs.6825.00 for long term.

Industry Overview

• Demand for tyres is derived from demand for automobiles. Therefore it is a ‘derived

demand’ product and its fortunes are very closely linked to those of the auto segment.

Within the tyre industry the trucks and buses (T&B) segment accounts for more than 70%

of sales. Though scooters and motorcycle tyre demand also plays a vital role, in value

terms, CVs gain significance.

• Tyre varieties can be divided into two categories – cross ply and radial. The domestic

industry is dominated by cross-ply tyres, due to the poor conditions of roads in the

country and overloading of CVs. This is also the reason why penetration of radial tyres in

the CV segment is negligible and finds presence only in the passenger car segment. On the

other hand, radial tyres dominate western markets. Radial tyres can be differentiated on

the type of belt used – fiberglass, steel and nylon. Worldwide, steel belted radials are

more popular due to their performance advantage.

• There are three major consumer segments for tyres namely replacement segment,

Original Equipment Manufacturers (OEMs) and exports. Though fortunes of the sector are

closely tied with the automobile industry, replacement demand continues to remain the

key growth driver. Replacement demand accounts for as high as 57% of industry volumes.

However, the contribution from OEM and replacement segments varies across sub-

segments in the auto sector. For instance, for the passenger car segment, demand is

balanced from replacement and OEM categories i.e. 50:50.

14

• Another key transition that is taking place in the industry is the entry of multinationals like

Good Year, Bridgestone and Michelin in the domestic market. MNC tyre makers have

cornered a higher market share in India in the last three years due to their international

relationships apart from superior technology. Since Honda, Hyundai and Toyota have an

international sourcing agreement with Bridgestone; it is also the preferred supplier in

India. Goodyear is believed to be the preferred supplier for Ford India.

• An extensive distribution network and strong brand recall are factors critical to tyre sales.

Brand building is given a lot of importance by manufacturers, who allot 2-3% of sales to

advertising. With the introduction of radial tyres, even technology has assumed

significance. All foreign cars introduced in the country are on radial tyres.

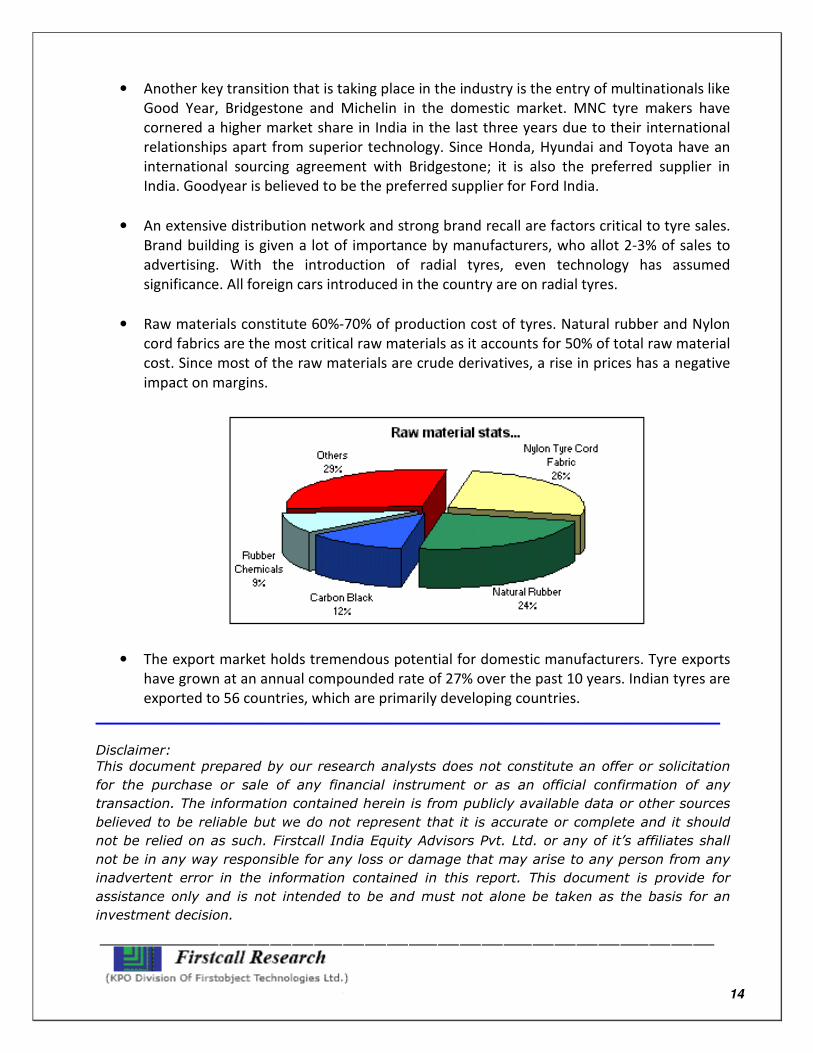

• Raw materials constitute 60%-70% of production cost of tyres. Natural rubber and Nylon

cord fabrics are the most critical raw materials as it accounts for 50% of total raw material

cost. Since most of the raw materials are crude derivatives, a rise in prices has a negative

impact on margins.

• The export market holds tremendous potential for domestic manufacturers. Tyre exports

have grown at an annual compounded rate of 27% over the past 10 years. Indian tyres are

exported to 56 countries, which are primarily developing countries.

____________________________________________________________

Disclaimer:

This document prepared by our research analysts does not constitute an offer or solicitation

for the purchase or sale of any financial instrument or as an official confirmation of any

transaction. The information contained herein is from publicly available data or other sources

believed to be reliable but we do not represent that it is accurate or complete and it should

not be relied on as such. Firstcall India Equity Advisors Pvt. Ltd. or any of it’s affiliates shall

not be in any way responsible for any loss or damage that may arise to any person from any

inadvertent error in the information contained in this report. This document is provide for

assistance only and is not intended to be and must not alone be taken as the basis for an

investment decision.

15

Firstcall India Equity Research: Email – [email protected]

B. Harikrishna Banking

B. Prathap IT

A. Rajesh Babu FMCG

C.V.S.L.Kameswari Pharma

U. Janaki Rao Capital Goods

E. Swethalatha Oil & Gas

D. Ashakirankumar Automobile

Rachna Twari Diversified

Kavita Singh Diversified

Nimesh Gada Diversified

Priya Shetty Diversified

Tarang Pawar Diversified

Neelam Dubey Diversified

Firstcall India also provides

Firstcall India Equity Advisors Pvt.Ltd focuses on, IPO’s, QIP’s, F.P.O’s, Takeover

Offers, Offer for Sale and Buy Back Offerings.

Corporate Finance Offerings include Foreign Currency Loan Syndications,

Placement of Equity / Debt with multilateral organizations, Short Term Funds

Management Debt & Equity, Working Capital Limits, Equity & Debt

Syndications and Structured Deals.

Corporate Advisory Offerings include Mergers & Acquisitions (domestic and

cross-border), divestitures, spin-offs, valuation of business, corporate

Restructuring-Capital and Debt, Turnkey Corporate Revival – Planning &

Execution, Project Financing, Venture capital, Private Equity and Financial

Joint Ventures

Firstcall India also provides Financial Advisory services with respect to raising

of capital through FCCBs, GDRs, ADRs and listing of the same on International

Stock Exchanges namely AIMs, Luxembourg, Singapore Stock Exchanges and

other international stock exchanges.

For Further Details Contact:

3rd Floor, Sankalp, The Bureau, Dr.R.C.Marg, Chembur, Mumbai 400 071

Tel.: 022-2527 2510/2527 6077/25276089 Telefax: 022-25276089

E-mail: [email protected]

www.firstcallindiaequity.com