modeling low carbon scenarios for the european power · pdf filem o dell ing the lowest - cost...

TRANSCRIPT

NTNU investment model for European power Study I Study II Study III Conclusions

Modeling low carbon scenarios for theEuropean power sector

Christian Skar and Asgeir Tomasgard

NTNU � Trondheim

Norwegian University of

Science and Technology

Department of Industrial Economics and Technology Management

CREE model forum April, 2016

NTNU investment model for European power Study I Study II Study III Conclusions

EMPIRE

EMPIRE: European Model for Power system Investments with Renewable Energy

Capacity expansion model for the European power market

Investments are made under uncertainty about operational conditions

Embedded calculation of hourly optimal system operation

Five year time steps

Developed at NTNU

NTNU investment model for European power Study I Study II Study III Conclusions

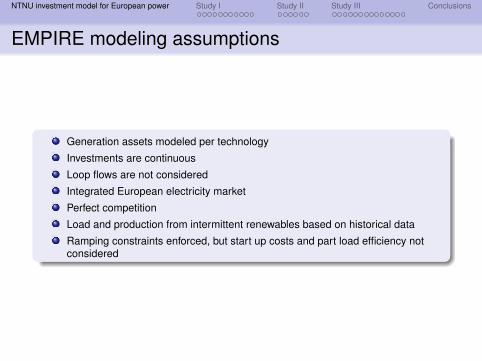

EMPIRE modeling assumptions

Generation assets modeled per technology

Investments are continuous

Loop flows are not considered

Integrated European electricity market

Perfect competition

Load and production from intermittent renewables based on historical data

Ramping constraints enforced, but start up costs and part load efficiency notconsidered

NTNU investment model for European power Study I Study II Study III Conclusions

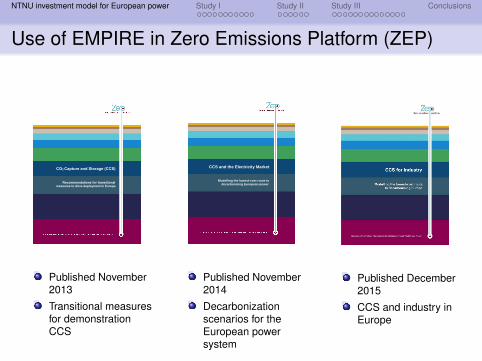

Use of EMPIRE in Zero Emissions Platform (ZEP)

1

CO2 Capture and Storage (CCS)

Recommendations for transitional measures to drive deployment in Europe

Published November2013

Transitional measuresfor demonstrationCCS

CCS and the Electricity Market Modelling the lowest-cost route to decarbonising European power

Published November2014

Decarbonizationscenarios for theEuropean powersystem

Published December2015

CCS and industry inEurope

NTNU investment model for European power Study I Study II Study III Conclusions

Recent NTNU studies

Transmission expansion

Role of CCS in Europe decarbonization

Using fuel prices, electricity demand and CO2

prices from the EU 2013 reference scenario

The generation technology parameter data isthe same as used for the previous ZEP studies.

Recent study done at NTNU

Using the EUreference scenario:

EU ENERGY, TRANSPORT AND GHG EMISSIONS

TRENDS TO 2050REFERENCE SCENARIO 2013

Disclaimer

This is not a ZEP study. Members of ZEP have not yet had the opportunity to commenton the analysis, nor the results, and the following part of the presentation is solely theresponsibility of the authors.

NTNU investment model for European power Study I Study II Study III Conclusions

Decarbonizing European power (carbon price)

ReferenceSkar, C., G. L. Doorman, G. A. Pérez-Valdés, and A.Tomasgard. 2016. “A multi-horizon stochastic programmingmodel for the European power system.” CenSES WorkingPaper, March 2016.

NTNU investment model for European power Study I Study II Study III Conclusions

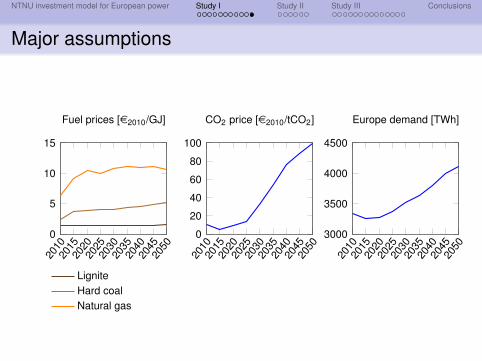

Major assumptions20

1020

1520

2020

2520

3020

3520

4020

4520

50

0

5

10

15

Fuel prices [e2010/GJ]

LigniteHard coalNatural gas

2010

2015

2020

2025

2030

2035

2040

2045

2050

0

20

40

60

80

100

CO2 price [e2010/tCO2]

2010

2015

2020

2025

2030

2035

2040

2045

2050

3000

3500

4000

4500

Europe demand [TWh]

NTNU investment model for European power Study I Study II Study III Conclusions

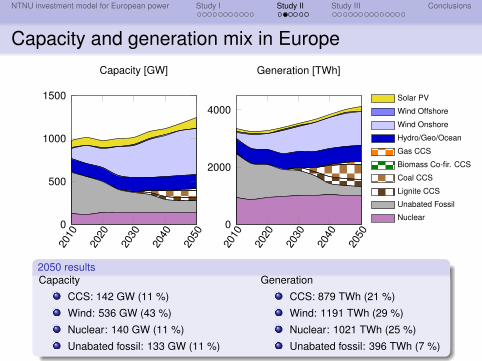

Capacity and generation mix in Europe20

10

2020

2030

2040

2050

0

500

1000

1500

Capacity [GW]

2010

2020

2030

2040

2050

0

2000

4000

Generation [TWh]

Solar PV

Wind Offshore

Wind Onshore

Hydro/Geo/Ocean

Gas CCS

Biomass Co-fir. CCS

Coal CCS

Lignite CCS

Unabated Fossil

Nuclear

2050 resultsCapacity

CCS: 142 GW (11 %)

Wind: 536 GW (43 %)

Nuclear: 140 GW (11 %)

Unabated fossil: 133 GW (11 %)

Generation

CCS: 879 TWh (21 %)

Wind: 1191 TWh (29 %)

Nuclear: 1021 TWh (25 %)

Unabated fossil: 396 TWh (7 %)

NTNU investment model for European power Study I Study II Study III Conclusions

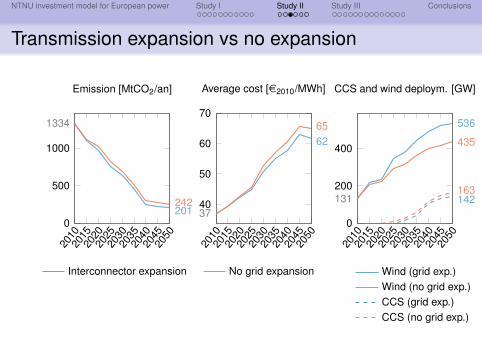

Transmission expansion vs no expansion20

1020

1520

2020

2520

3020

3520

4020

4520

50

0

500

1000

1334

201242

Emission [MtCO2/an]

Interconnector expansion No grid expansion

2010

2015

2020

2025

2030

2035

2040

2045

2050

40

50

60

70

37

6265

Average cost [e2010/MWh]

2010

2015

2020

2025

2030

2035

2040

2045

2050

0

200

400

131 142163

536

435

CCS and wind deploym. [GW]

Wind (grid exp.)Wind (no grid exp.)CCS (grid exp.)CCS (no grid exp.)

NTNU investment model for European power Study I Study II Study III Conclusions

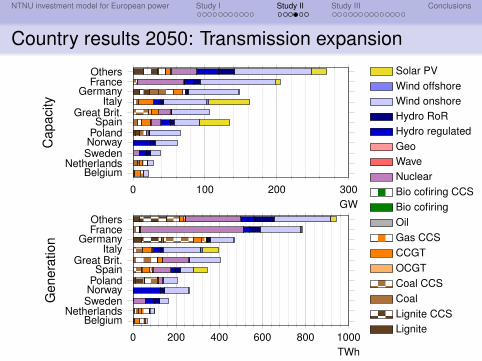

Country results 2050: Transmission expansion

0 100 200 300GW

OthersFrance

GermanyItaly

Great Brit.Spain

PolandNorwaySweden

NetherlandsBelgium

Cap

acity

Solar PVWind offshoreWind onshoreHydro RoRHydro regulatedGeoWaveNuclearBio cofiring CCSBio cofiringOilGas CCSCCGTOCGTCoal CCSCoalLignite CCSLignite

0 200 400 600 800 1000TWh

OthersFrance

GermanyItaly

Great Brit.Spain

PolandNorwaySweden

NetherlandsBelgium

Gen

erat

ion

NTNU investment model for European power Study I Study II Study III Conclusions

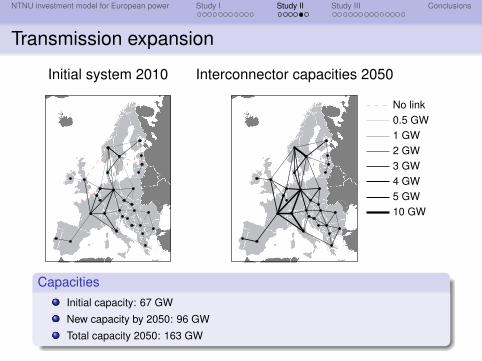

Transmission expansion

Initial system 2010 Interconnector capacities 2050

No link0.5 GW1 GW2 GW3 GW4 GW5 GW10 GW

CapacitiesInitial capacity: 67 GW

New capacity by 2050: 96 GW

Total capacity 2050: 163 GW

NTNU investment model for European power Study I Study II Study III Conclusions

Conclusions

Driven by the EU ETS price from the European referencecase 2013 an emission reduction of more than 80 % isachieved displacing unabated fossil fuel generation withonshore wind and CCSBy allowing interconnector expansion, more wind powerwas deployed, which significantly reduces the systemoperational costsOnly small differences are observed for the total emissions

NTNU investment model for European power Study I Study II Study III Conclusions

The role of CCS in Europe and support policies

ReferenceSkar, C., G. L. Doorman, G. Guidati, C. Soothill, and A.Tomasgard. 2016. “Modeling transitional measures to driveCCS deployment in the European power sector.” CenSESWorking Paper, March 2016.

NTNU investment model for European power Study I Study II Study III Conclusions

Carbon catpure and storage cost and technologicaldata

CCS assumptions

2025 2030 2035 2040 2045 2050Capital cost [e2010/kW]Lignite CCS 2600 2530 2470 2400 2330 2250Coal CCS 2500 2430 2370 2300 2230 2150Gas CCS 1350 1330 1310 1290 1270 1250Efficiency [%]Lignite CCS 37 39 40 41 42 43Coal CCS 39 40 41 41 42 43Gas CCS 52 54 56 57 58 60CCS T&S cost [e2010/tCO2] 19 18 17 15 14 13

NTNU investment model for European power Study I Study II Study III Conclusions

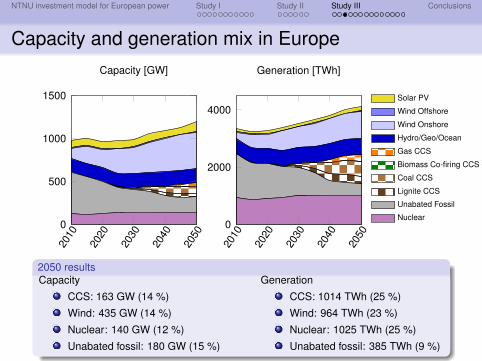

Capacity and generation mix in Europe20

10

2020

2030

2040

2050

0

500

1000

1500

Capacity [GW]

2010

2020

2030

2040

2050

0

2000

4000

Generation [TWh]

Solar PV

Wind Offshore

Wind Onshore

Hydro/Geo/Ocean

Gas CCS

Biomass Co-firing CCS

Coal CCS

Lignite CCS

Unabated Fossil

Nuclear

2050 resultsCapacity

CCS: 163 GW (14 %)

Wind: 435 GW (14 %)

Nuclear: 140 GW (12 %)

Unabated fossil: 180 GW (15 %)

Generation

CCS: 1014 TWh (25 %)

Wind: 964 TWh (23 %)

Nuclear: 1025 TWh (25 %)

Unabated fossil: 385 TWh (9 %)

NTNU investment model for European power Study I Study II Study III Conclusions

CO2 emissions, power price and 2050 annual costs20

1020

1520

2020

2520

3020

3520

4020

4520

50

0

500

1000

1334

243

Emission [MtCO2/an]

Baseline

2010

2015

2020

2025

2030

2035

2040

2045

2050

60

80

100

45

80

Power price [e2010/MWh]

Baseli

ne

0

50

100

150

200

250

300

2050 costs [bne2010/an]

Capital andfix. O&MFuel andvar. O&MEUACCS T&S

NTNU investment model for European power Study I Study II Study III Conclusions

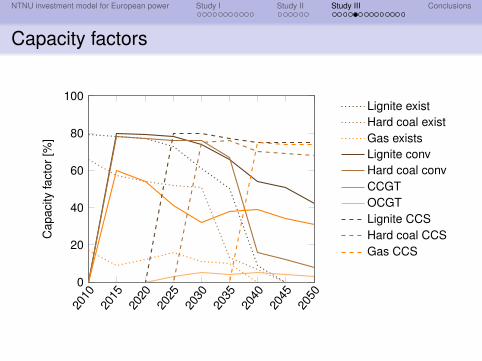

Capacity factors

2010

2015

2020

2025

2030

2035

2040

2045

2050

0

20

40

60

80

100

Cap

acity

fact

or[%

]

Lignite existHard coal existGas existsLignite convHard coal convCCGTOCGTLignite CCSHard coal CCSGas CCS

NTNU investment model for European power Study I Study II Study III Conclusions

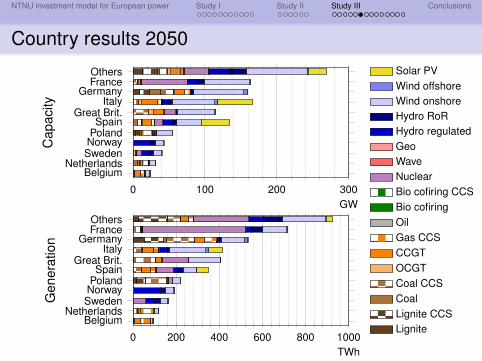

Country results 2050

0 100 200 300GW

OthersFrance

GermanyItaly

Great Brit.Spain

PolandNorwaySweden

NetherlandsBelgium

Cap

acity

Solar PVWind offshoreWind onshoreHydro RoRHydro regulatedGeoWaveNuclearBio cofiring CCSBio cofiringOilGas CCSCCGTOCGTCoal CCSCoalLignite CCSLignite

0 200 400 600 800 1000TWh

OthersFrance

GermanyItaly

Great Brit.Spain

PolandNorwaySweden

NetherlandsBelgium

Gen

erat

ion

NTNU investment model for European power Study I Study II Study III Conclusions

Motivation

What if we cannot use CCS?

Nuclear has a public relations issue in EuropeOnly leaves renewable energies as low carbon solutionWhat is the cost?

NTNU investment model for European power Study I Study II Study III Conclusions

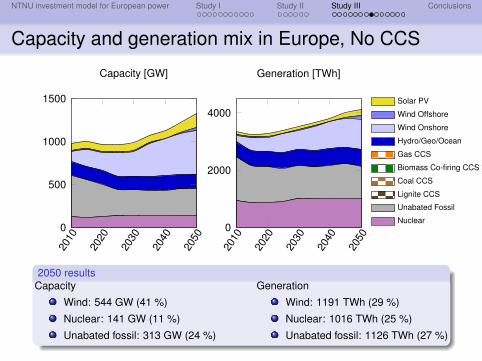

Capacity and generation mix in Europe, No CCS20

10

2020

2030

2040

2050

0

500

1000

1500

Capacity [GW]

2010

2020

2030

2040

2050

0

2000

4000

Generation [TWh]

Solar PV

Wind Offshore

Wind Onshore

Hydro/Geo/Ocean

Gas CCS

Biomass Co-firing CCS

Coal CCS

Lignite CCS

Unabated Fossil

Nuclear

2050 resultsCapacity

Wind: 544 GW (41 %)

Nuclear: 141 GW (11 %)

Unabated fossil: 313 GW (24 %)

Generation

Wind: 1191 TWh (29 %)

Nuclear: 1016 TWh (25 %)

Unabated fossil: 1126 TWh (27 %)

NTNU investment model for European power Study I Study II Study III Conclusions

Comparison: CO2 emissions, power price and 2050annual costs

2010

2015

2020

2025

2030

2035

2040

2045

2050

0

500

1000

1334

243

496

Emission [MtCO2/an]

BaselineNoCCS

2010

2015

2020

2025

2030

2035

2040

2045

2050

60

80

100

45

8088

Power price [e2010/MWh]

Baseli

neNoC

CS

0

50

100

150

200

250

300

2050 costs [bne2010/an]

Capital andfix. O&MFuel andvar. O&MEUACCS T&S

NTNU investment model for European power Study I Study II Study III Conclusions

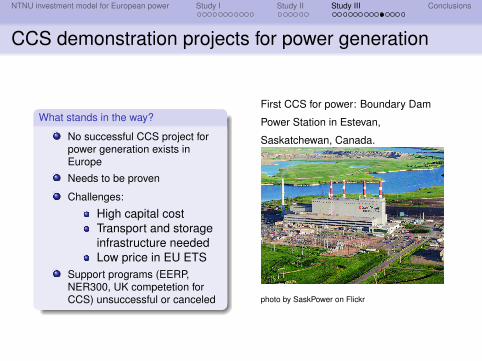

CCS demonstration projects for power generation

What stands in the way?

No successful CCS project forpower generation exists inEurope

Needs to be proven

Challenges:

High capital costTransport and storageinfrastructure neededLow price in EU ETS

Support programs (EERP,NER300, UK competetion forCCS) unsuccessful or canceled

First CCS for power: Boundary Dam

Power Station in Estevan,

Saskatchewan, Canada.

photo by SaskPower on Flickr

NTNU investment model for European power Study I Study II Study III Conclusions

Transitional measures to inscentivize demonstrationprojects

Demonstration CCS

Project Capital cost Efficiency Post-demo

Capital cost Efficiency

Until 2020 [e2010/kW] [%] 2025 [e2010/kW] [%]Lignite CCS 2600 31 2600 37Coal CCS 2500 33 2500 39Gas CCS 1350 48 1350 52

Schemes evaluated

Capital grants

Feed-in premiums

Emission performance standard

NTNU investment model for European power Study I Study II Study III Conclusions

Capital grants (CAPEX support)

Design: given share of the capital costs covered

Different levels tried

Result: a support level of 2000 e2010/kW needed to spurinvestments

Result: 4.1 GW of lignite CCS deployed. Cost: 6.5 bne(2015NPV)

NTNU investment model for European power Study I Study II Study III Conclusions

Feed-in premiums (OPEX support)

TypeFlat SRMC End Gas Lignite Total 2015 NPV LCOS

[e/MWh] [%] [GW] [GW] [GW] [bne] [e/MWh]45.0 2030 No deployment50.0 2030 1.9∗ 1.9 6.6 40.055.0 2030 5.0∗ 5.0 20.9 43.730.0 2050 No deployment35.0 2050 5.0 5.0 12.6 31.3

20.0 2030 No deployment25.0 2030 4.1 4.1 6.2 15.810.0 2050 No deployment15.0 2050 2.8 2.8 4.0 15.017.5 2050 4.1 4.1 6.6 17.520.0 2050 5.0 5.0 9.4 20.020.0 2030 No deployment

(L) 15.0 (G) 32.5 2050 1.2 2.8 4.1 6.9 18.8(L) 17.5 (G) 32.5 2050 0.9 4.1 5.0 8.7 18.8

SRMC: short-run marginal costFuel + variable O&M + carbon price + CCS transport and storageDetermines the dispatch!(L) – lignite CCS, (G) – natural gas CCS

NTNU investment model for European power Study I Study II Study III Conclusions

Emission performance standard from 201520

1020

1520

2020

2520

3020

3520

4020

4520

50

0

500

1000

1334

243107

Emission [MtCO2/an]

Baseline 450 gen EPS

225 Euro EPS 225 gen EPS

2010

2015

2020

2025

2030

2035

2040

2045

2050

60

80

100

45

91

8077

Power price [e2010 /MWh]

2010

2015

2020

2025

2030

2035

2040

2045

2050

0

100

200

300

163

339

CCS deployment [GW]

Specific emissions for unabated generation

Coal: 786 gCO2/kWh

Gas CCGT: 336 gCO2/kWh

Gas OCGT: 505 gCO2/kWh

NTNU investment model for European power Study I Study II Study III Conclusions

Conclusions

CCS can be a major contributor to cost-efficientdecarbonization of European powerWithout CCS decarbonization will be more expensive –even for less emission reductionSupport schemes needed to secure deployment ofdemonstration CCS

CAPEX support can help CCS with low fuel costsOPEX support needed for gas CCS

Emissions performance standard (EPS) is an effectiveemission reduction mechanism

A limit of 225 gCO2/kWh for generators drive down emissionsResults in a transitional period with high prices

NTNU investment model for European power Study I Study II Study III Conclusions

Thank you for your attention

Questions?