mobile financial and banking services development in africa

TRANSCRIPT

African

Develop

ment Ba

nk Grou

p

Mobile Financial and BankingServices Development in Africa

Working

Pape

r Serie

s

Christian Lambert NGUENA

Indus

triali

se A

frica

n° 32

3

July 2

019

3

tri

Working Paper No 323

Abstract

Using a new database for mobile financial & banking services across countries, we analyze pro-poor and inclusive growth in developing countries and show the importance of mobile financial & banking development. This paper uses several econometric techniques to investigate mobile finance & banking benchmarking, determinants, and real impacts on inclusive growth in developing countries in Africa. The statistical benchmarking analysis reveals that there is a positive link between mobile banking development and economic development. Estimation of our model, using different specification and estimation techniques, shows the same result: a positive impact of mobile finance & banking development on both pro-poor

and inclusive economic growth. These main findings suggest that policies to boost mobile finance & banking development in Africa should be viewed as measures that would yield fruit in the medium to long terms. Moreover, we find determinants of mobile finance & banking to be: banking sector domestic credit, human capital, remittances, credible monetary policy, infrastructure, and trade. Since mobile banking development matters for pro-poor and inclusive growth, African governments should pursue good performance in terms of these determinants by implementing specific and robust economic policies.

Rights and Permissions

All rights reserved.

The text and data in this publication may be reproduced as long as the source is cited. Reproduction for commercial purposes is forbidden. The WPS disseminates the findings of work in progress, preliminary research results, and development experience and lessons, to encourage the exchange of ideas and innovative thinking among researchers, development practitioners, policy makers, and donors. The findings, interpretations, and conclusions expressed in the Bank’s WPS are entirely those of the author(s) and do not necessarily represent the view of the African Development Bank Group, its Board of Directors, or the countries they represent.

Working Papers are available online at https://www.afdb.org/en/documents/publications/working-paper-series/

Produced by Macroeconomics Policy, Forecasting, and Research Department

Coordinator Adeleke O. Salami

This paper is the product of the Vice-Presidency for Economic Governance and Knowledge Management. It is part of a larger effort by the African Development Bank to promote knowledge and learning, share ideas, provide open access to its research, and make a contribution to development policy. The papers featured in the Working Paper Series (WPS) are those considered to have a bearing on the mission of AfDB, its strategic objectives of Inclusive and Green Growth, and its High-5 priority areas—to Power Africa, Feed Africa, Industrialize Africa, Integrate Africa and Improve Living Conditions of Africans. The authors may be contacted at [email protected].

Correct citation: Nguena, C. L. (2019), Mobile Banking and Financial Services Development in Africa, Working Paper Series N° 323, African Development Bank, Abidjan, Côte d’Ivoire.

1

Mobile Financial and Banking Services Development in Africa

Christian Lambert Nguena 1

JEL classification: G21, R1, O4

Keywords: Mobile finance & banking, Africa, principal component analysis, financial innovation, financial inclusion

1 Senior Lecturer and Researcher at the University of Dschang [contact: [email protected]]. This research paper was improved by comments received from participants at the 72nd Annual Conference of the International Institute of Public Finance ((IIPF).

2

1. Introduction

It is empirically and theoretically established that an important part of growth is supported by

investment and business performance. For this major factor of economic development, we

emphasize the importance of a healthy and developed financial system. In Africa, the main

concerns are the inclusion and depth aspects of the financial system, which tend to largely

explain the lower level of the contribution of the supply side of the economy (Ndebbio, 2004;

Meisel and Mvogo, 2007; Nguena and Tsafack, 2015). In general, mobile financial & banking

services offer great potential to improve financial inclusion of the poor through inclusive

financial services, particularly digital payment services (Gutierrez and Singh, 2013). With its

main advantages being instantaneity, freedom from having to hold cash, privacy, security,

perceived ease of use, compatibility, and social influence, mobile baking is assumed to be more

adapted to African behavior and could therefore improve the inclusiveness of the financial

sector and unleash investments and economic development.

In sub-Saharan Africa, 75 percent of the population does not have access to any form

of formal financial services. This situation, which contributes to the success of informal finance

options like rotating savings and credit associations (ROSCAS), is too important to be ignored.

There exists a well-documented literature on the positive link between the level of development

of the financial system and economic development (Roubini and Sala-i-Martin, 1992; King and

Levine, 1993a,1993b; Easterly, 1993; Gertler and Rose, 1994; Levine , 1997; Beck and others,

2000; Khan and Senhadji, 2000; Thiel, 2001; Wachtel, 2001; Christopoulos and Tsionas, 2004;

Levine, 2004; Deisting and others 2012; Lansana, 2012; Mbate, 2013).

Alongside such evidence, the importance of informal financial institutions is also well

established in the literature (see the seminal paper by Besley, 1996). There have been many

recommendations even from formal financial institutions to forge strategic links with informal

financial institutions (Aliber, 2002). Possible reasons for the failure of the traditional financial

system in terms of greater inclusion are mainly: long distances to the nearest bank, low levels

of trust, and unwillingness to allow a third party like a bank to manage their very limited

disposable income (Aliber, 2002).

Mobile finance & banking (also known as M-Banking, mbanking, SMS Banking) is a

term used for making account transactions, payments, credit applications, and other banking

transactions through a mobile device such as a mobile phone, with or without a link to a

traditional banking account. The advantage is that mobile financial services can work without

a link to a traditional banking account, while mobile banking services are connected to a

3

banking account. These new modes of carrying out financial transactions constitute what we

call financial innovation. Mobile finance & banking has experienced fast growth globally.

According to Telecom Trends International Inc., there are now 1.3 billion mobile phones being

used around the world, a growth trend which has emerged over the past 20 years, compared to

the more than 2.5 billion landlines built over the last century. The number of mobile phones is

expected to be 4.5 billion by 2016, compared to 1.5 billion television sets in use today. Mobile

banking is currently the largest trend after micro-finance, gaining more than 90 million

customers over the past 30 years. Based on this large potential, it is rational to ask the question

of how mobile finance & banking can be used to facilitate economic development, on the one

hand, and how to mobilize funds for use in economic development (e.g., through microfinancial

institutions), on the other hand. More specifically, how can these new financial modes help, in

term of financial inclusiveness and thus improve the reduction of poverty with inclusive

growth.

The mobile phone revolution is the origin of change in many Africans’ lives, providing

not just telecommunications but also access to basic financial services in the form of phone-

based money transfers and storage (Jonathan and Camilo, 2008; Ondiege, 2010; Demombynes

and Thegeya, 2012; Nguena, 2012, 2015). In fact, the substantial penetration rates of mobile

telephony, which is transforming cell phones into pocket-banks in Africa, provide

opportunities for countries on the continent to increase affordable and cost-effective means of

bringing on board a large portion of the population that, until recently, had been excluded from

formal financial services for decades (Tchouto and Nguena, 2015).

This transformation has been appealing not only for banks and micro financial

institutions (MFIs) but also to financial regulators and governments, as well as development

partners providing support to ameliorate the lives of Africans via sustained growth and poverty

reduction policies. The Economist (2008) described the phenomenon with the following

sentence: “A device that was a yuppie toy not so long ago has now become a potent for

economic development in the world’s poorest countries.” In line with Aker and Mbiti (2010,

p. 208), at the Connect Africa summit in 2007, Paul Kagame, president of Rwanda asserted:

“In ten short years, what was once an object of luxury and privilege, the mobile phone has

become a basic necessity in Africa.” These perceptions have been investigated by Asongu

(2014), who finds mobile phone penetration mitigates African inequality, due to its positive

correlation with informal financial sector development (Asongu, 2013).

Against this background, while mobile banking has grown at a breathtaking pace in

certain countries (e.g., Kenya), most African nations still need to take full advantage of the

4

many benefits procured by these mobile banking services. One current policy challenge is to

understand why some African countries are more advanced in mobile phone penetration and

mobile banking than others. There is a wealth of literature to substantiate the relevance of this

empirical problem statement.

As emphasized by Maurer (2008), and confirmed in subsequent work (Jonathan and

Camilo, 2008; Thacker and Wright, 2012), academic research on the adoption and

socioeconomic effects of mobile banking (payments) systems in the developing world is scarce.

From a broad point of view, most studies on mobile banking have been theoretical and

qualitative in nature (Maurer, 2008; Jonathan and Camilo, 2008; Merritt, 2010; Thacker and

Wright, 2012; Asongu, 2013, 2014). Moreover, the few existing empirical works hinge on

country-specific and micro-level data (collected from surveys) for the most part (Demombynes

and Thegeya, 2012). The purpose of this study is to fill the existing gap by empirically testing

if mobile banking development matters for pro-poor and inclusive growth in African

developing countries.

This paper’s specific objectives are: (i) to empirically determine the impact of mobile

banking development on pro-poor and inclusive economic growth, and (ii) to empirically

estimate the determinants of mobile banking development in Africa. To the best of our

knowledge, this paper is unique and breaks new ground, using newly available data from the

World Bank on mobile phone penetration and mobile banking. Apart from some stylized facts

about African countries, it is an in-depth study of the distinguishing features of mobile banking,

i.e.,mobile phone usage to pay bills, mobile phone usage to pay/receive money, and Internet

usage per capita. Additionally, an aspect of capitalism is taken into account by considering the

economic freedom index.

The contribution of this paper to the literature is threefold. First, we deviate from the

mainstream literature on African mobile usage, which is based on qualitative and

microeconomic assessments (Maurer, 2008; Jonathan and Camilo, 2008; Merritt, 2010;

Thackerand Wright, 2012; DemombynesandThegeya, 2012). The paper therefore complements

the existing literature with a macroeconomic empirical assessment of the impact of mobile

banking development on pro-poor and inclusive growth. It also examines the determinants of

the burgeoning mobile banking phenomenon. Second, this study uses the only mobile banking

data available, first published by the World Bank in 2013. Our analysis thus differs from recent

studies that have used mobile penetration as a proxy for mobile banking (Ondiege, 2010;

Asongu, 2013). Instead, we construct indicators of mobile finance & banking such as mobile

phone usage in the payment of bills, mobile usage in the sending/receiving of money, and

5

Internet usage per capita. Third, the coexistence of a less-developed financial system, which is

generally a more bank-based system than a market-based system, on one hand, and increasing

and rapid adoption of financial innovations, on the other hand, increases the importance of this

study for the economic welfare of practically all African countries.

Our empirical analysis highlights the following results: a positive impact on the mobile

banking index in both pro-poor and inclusive economic growth. These main findings suggest

that policies to boost mobile finance & banking development in Africa should be viewed as

measures that would yield positive gains in the medium to long run. Moreover, we find

determinants of mobile banking to be: banking sector domestic credit, human capital,

remittances, credible monetary policy, infrastructure, and trade. Therefore, since mobile

banking development matters for pro-poor and inclusive growth, African governments should

pursue good performance by implementing supportive policies in these determinant areas.

The rest of the paper is organized as follows: the second section presents the literature

review on mobile finance & banking development, growth, poverty, and income distribution;

the third section focuses on stylized facts and benchmarking; the fourth section is dedicated to

the econometric methodology; the fifth section presents and discusses the results; and the sixth

section concludes the study.

2. Mobile Finance & Banking Development, Growth, Poverty, and Income Distribution:

Selected Literature Review

2.1 Mobile finance & banking development and pro-poor and inclusive growth

There are few studies that have investigated the role of mobile finance & banking development

for economic development and poverty reduction.

Since a seminal paper by Hardy (1980), which investigates the impact of telephones

per capita on economic growth, a growing number of studies have attempted to identify

telecommunications as an essential component of economic infrastructure, fostering

productivity and economic growth. The implications of telecommunications infrastructure for

economic development have evolved out of both direct and indirect benefits to economic

growth from telecommunications expansion. For example, a more efficient flow of information

reduces communication and transaction costs, and faster information diffusion enhances

market efficiency and competition as well as the potential for technological catch-up.

In the literature, the relationship between telecommunications investment and

economic growth has been examined in various ways. Several studies have employed time-

6

series analysis, such as Granger causality tests and modified Sims tests, and have focused on

the strength and direction of the causal relationship between telecommunications infrastructure

investment and economic growth. For instance, Cronin and others (1991, 1993a, 1993b) and

Wolde-Rufael (2007) confirm a two-way causal relationship in the United States between

telecommunications infrastructure investment and economic growth. In a similar study,

however, Beil and others (2005) conduct Granger-Sims causality tests for a time series of 50

years in the United States and find a one-way causality from economic growth to

telecommunications investment. Dutta (2001) applies Granger causality tests for a cross section

of 30 developing and industrialized countries for three different years, and finds a bi-directional

causality for both developing and industrialized countries. Perkins and others (2005) also

identify a bi-directional causality in South Africa using a PSS F-test (Pesaran and others, 2001).

A few other studies have attempted to quantify the impact of telecommunications on

economic growth by incorporating telecommunications infrastructure investment explicitly

into a macro (aggregate) production function or a cross-country growth framework. Madden

and Savage (2000) extend Mankiw and others (1992) to develop a supply-side growth model

where “teledensity” (the number of main telephone lines per 100 persons) and the share of

telecommunications investment in national income are controlled for as telecommunications

capital proxies. Their results from data on 43 countries, over the 1975–1990 period, suggest a

significant, positive, cross-country relationship between telecommunications capital and

economic growth.

In another study, Roller and Waverman (2001) endogenize telecommunications

infrastructure into aggregate economic activity. They first specify a micro model of the demand

for and supply of telecommunications infrastructure, and jointly estimate the micro model with

the macro production function. They find a significant causal relationship between

telecommunications infrastructure and aggregate output. Datta and Agarwal (2004) extend the

cross-country growth framework of Barro (1991) and Levine and Renelt (1992) to examine the

effects of telecommunications infrastructure on economic growth; they find a positive impact

and conclude there is a necessity to invest in telecommunications infrastructure. In a dynamic

panel model built on Islam (1995), they control for lagged, real gross domestic product (GDP)

per capita to test for convergence, while testing separately the direction of causality between

the teledensity and economic growth using the first-lagged values of teledensity.

Previous studies attest to the fact that telecommunications infrastructure investment is

positively correlated with economic growth, but far fewer studies have investigated how mobile

telecommunications has played a specific role in economic growth, especially in a region where

7

a disproportionate rate of growth in mobile telecommunications exists, relative to the level of

land-line telephony. The growth of mobile telephony in Africa, especially in sub-Saharan

Africa, epitomizes such a case. Due to the highly investment-intensive nature of land-line

telecommunications infrastructure deployment, Africa accounted for less than 2 percent of the

main telephone lines worldwide in 2006, while Asia had a 48 percent share (International

Telecommunication Union (ITU), 2007).

However, the breakthroughs in mobile phone technology in the last decade, combined

with relatively cheap mobile phone infrastructure, have led to Africa’s achieving a significant

annual growth in mobile telephone penetration. For instance, the number of mobile subscribers

in Africa surpassed the number of land lines in 2001 (Gray, 2006), and the number of mobile

subscribers in the region increased by 46.2 percent between 2001 and 2005 (ITU, 2007).

Mobile penetration in Africa by the end of 2006 was 22.0 subscribers per 100 persons, while

in Asia it was 29.3. And Africa was the only region where mobile telephone services generated

more revenue than land-line telephone services in 2005, accounting for more than 60 percent

of total telecommunications revenue in the region (ITU, 2007). The growth in mobile telephone

subscriptions in sub-Saharan African countries is shown in figure A.1 in the appendix.

Vodafone Group (2005) reported that, in a typical developing country, an increase of

10 mobile phones per 100 people boosts GDP growth by 6 percent. Ovum (2006) reports that

the mobile services industry contributed US$7.8 billion towards GDP in India. Enriquez and

others (2007) estimate the contribution of mobile operators and mobile-related companies and

report that, in China, mobile-related companies contribute twice as much to GDP as mobile

operators. Deloitte (2008) reports that in all six countries analyzed (Bangladesh, Malaysia,

Pakistan, Serbia, Thailand, and Ukraine) mobile phones have a significant impact on GDP. Lee

and others (2012) find that mobile cellular phone expansion is an important determinant of the

rate of economic growth in sub-Saharan Africa.

Using interactive quantile regressions, Asongu and Odhiambo (2017) examined the

correlations between mobile banking and inclusive development (quality of growth, inequality,

and poverty) among individuals in 93 developing countries for the year 2011. They found that

increasing mobile banking dynamics to certain threshold levels would increase (decrease)

quality of growth (inequality) in quantiles at the high-end of inclusive development

distributions, for the most part. As policy, encouraging the growth of mobile banking

applications would be a substantial tool to use in responding to immiserizing growth,

inequality, and poverty in developing countries.

8

Overall, studies with an explicit focus on mobile finance & banking development,

especially of Africa, are relatively scarce in the literature. Additionally, the majority of studies

focus on the impact of telecommunications, mobile telephony, 3G technology, mobile data

services, and mobile phone penetration on economic growth, instead of focusing on mobile

finance & banking development and pro-poor and inclusive growth. The need to empirically

verify our research question for African countries is an important contribution to the existing

literature.

2.2 Determinants of mobile finance &banking

Innovation and adoption of new technologies have attracted so much attention in the literature;

and this has generated many models and theories, which are believed to affect the innovation

adoption. For example, the Theory of Reasoned Action (TRA), the Theory of Planned

Behavior (TPB), and the Technology Acceptance Model (TAM) have been used in many

studies in developed countries. Among the research studies on innovation are studies that focus

on mobile banking and electronic banking. In addition to these theoretical models, which are

mainly based on a micro approach, there are two main theoretical lines along which the

determinants of mobile banking can be discussed: the first line takes into consideration the

macroeconomic environment of the country, and the second line presents some statistics on the

proliferation of mobile telephony in Africa.

The first line is based on the characteristics of the macroeconomic context in which

mobile banking is practiced in Africa. The macroeconomic environment is linked and favorable

to the development of mobile banking for the following reasons: First, from an international

perspective, Africa is generally less internationally connected and has a less developed banking

and financial system. Therefore, the virtual connection offered by mobile telecommunications

to households is an excellent alternative tool for banking and finance. Second, increasing levels

of fund transfers from abroad to Africa can be mobilized by a well-established mobile banking

sector, given a higher level of mobile penetration. Third, mobile banking can help boost

investment activities. This first line of theoretical discussion is the main focus of our

investigation.

Mobile money is now a common platform for banks, the underserved, and the unbanked

population. Its acceptability highly depends on how individuals perceive innovation attributes

such as simplicity, convenience, security, cost, flexibility, and accessibility (Porteous, 2007).

The different perceptions of an innovation have a direct impact on intended usage and actual

9

usage of the innovation (Venkatesh, 2000). Mobile banking is a new technology in many parts

of the world and can thus be adopted or rejected by users depending on the factors that affect

perceptions (Ngugi and others, 2010). The development of a new service or technology in

mobile banking has been studied for many years by academicians.

In a global context of various financial innovations, Fox and Vandroogenbroeck (2017)

study the recent incursion of telecom operators into the financial sphere, particularly in Africa,

in order to account for the outsized development of mobile banking, and to determine whether

the traditional banking system is challenged by these new actors. They also highlight the

characteristics of mobile banking in Africa, with an emphasis on the differences with developed

countries. However, they use comparison and a vast empirical literature approach, rather than

an econometric investigation, to attain their objectives.

In a first attempt, Gutierrez and Singh (2013) use individual data on 37,000 individuals

in 35 countries to explore factors associated with mobile banking usage. They find that a

supporting regulatory framework is associated with a higher usage of mobile banking by the

general population as well as by the unbanked.

Using a survey and a research model, based on the technology acceptance model, to

determine the factors that affect the adoption of mobile banking in New Zealand, Malhotra

(2011) highlights perceived risk (information and service quality, financial risk, security risk

concerns, psychological risk factors, size and design issues, speed and efficiency, and usage

costs), as a major inhibitor of the adoption of mobile banking, while perceived trust and

perceived usefulness do not significantly affect adoption. Abdinoor and Mbamba (2017) assess

consumers’ adoption of mobile financial services in Tanzania using the TAM and find that

mobile financial service adoption is positively related to individual awareness, perceived

usefulness, and perceived benefit but is negatively related to cost effects. Nevertheless, the

study shows that the demographic characteristics of respondents (sex, age, and income level)

are among the factors that determine the adoption of mobile financial services.

Maradung (2013) investigates the factors affecting the adoption of mobile money

services in the banking and financial industries of Botswana, in light of the TAM and

demographic variables (age of individuals, income, education level, bank account).The results

show that gross income and ownership of bank accounts, age of individuals (with more young

people than older people), gender (with more males than females), and employment status (with

more employed individuals than unemployed) are the main determinants of the preference to

use mobile money services. However, the education level of individuals does not have any

effect on the preference to use mobile money services to access banking and financial services.

10

Dzokoto and Mensah (2011) investigate the adoption of mobile money transfers using data

from interviews conducted with 35 low-income clients, 35 middle-class clients, 25 merchants,

and 25 market women who are mobile money vendors in Ghana. They find that customers

value mobile money as safe, fast, and convenient services and that the major challenges to its

adoption are lack of trust and technological literacy.

Tiwari and others (2007) critically examine the phenomenon of mobile commerce in a

given business field in order to identify the potential benefits. The study focuses on the

application and uses of mobile banking in Germany. The acceptance of mobile banking by

customers is surveyed between June 28, 2005 and July 21, 2005 in Hamburg. A total of 488

individuals, between 18 and 65 years of age, answered a three-page questionnaire giving

information on their perceived preferences and willingness to pay for 17 different financial

services offered for mobile banking. The services are bundled into 3 groups: mobile

accounting, mobile brokerage, and mobile financial information. The survey findings

unambiguously show that the rate of usage and adoption of mobile banking is remarkable. The

banks studied are found to be increasingly persuaded to include mobile services in their product

portfolios (Tiwari and others, 2007).

In South Africa, M-Pesa, born from a Vodacom and Nedbank partnership, did not live

up to expectations. In 2011, it had registered just over 100,000 users, which is far from the 10

million (out of the 13 million unbanked population) that it expected to register in three years

after being launched (AllAfrica.com, 2011). Despite its partnership with local banks to offer

mobile banking services, it did not experience a breakthrough and adoption by the local

population. According to the CEO of Vodacom at the time, the failure of M-Pesa in South

Africa can be attributed to the fact that the South African banking sector is more developed

(AllAfrica.com, 2011).

A study to investigate the factors that affect the adoption of mobile banking by Korir

(2012) is guided by four factors: covering age, cost, education, and the security of the platform

under survey. The study targets a sample of 400 respondents in the Garissa District who are

customers of Kenya Commercial Bank, Ltd. The authors find that there is a need for banks to

develop a technically reliable and easy to understand mobile banking system that is cost

effective for their customers—the study reveals that some of these customers admit that the

cost of accessing mobile banking services is high. The author also finds that many behavioral

implications have not been considered in depth regarding perception and attitude (Korir, 2012).

Thando (2013) examines the perception and adoption of mobile payment platforms

(MPP) by entrepreneurs in Zimbabwe. The author uses a database of 1,842 registered agents

11

of the MPP that is supplied by Green Mobile in Zimbabwe. Of the 1,842 agents, 558 are

informal entrepreneurs. These informal agents facilitate registration by customers to use the

MPP. The author finds that most informal entrepreneurs have positive perceptions of the

service provider. However, he suggests that the service providers need to put in more effort

and time in educating the entrepreneurs about the functioning and added benefits of using the

platform (Thando, 2013).

Gakure and others (2013) undertake a descriptive analysis of the factors that contribute

to the performance of Mkesho in the Nairobi Region. According to the survey, the Mkesho

Account was launched by M-Pesa and Equity as an accessible and affordable bank account that

allows users to deposit and withdraw money from their account using an M-Pesa Account from

their handset. The main objective of the study is to investigate the factors that account for the

low adoption of Mkesho services by subscribers. The total number of registered users of

Mkesho during the survey period in May 2013 was about 700,000 people, which formed the

survey population. The study samples a total of 100 respondents, representing 0.0142 percent

of the population. The results show that 80 percent of the respondents do not use the Mkesho

services and only 20 percent of the subscribers use the service. This implies that most

customers had ceased to use the services of Mkesho, thus leading to a decline in the service.

The findings also identify the presence of other competitive and substitute products like

Mshwari, which are simple and easy to use. The lack of awareness about Mkesho by consumers

was a cause for the low adoption of the Mkesho service. This shows that there are more

underlying factors that affect the adoption of mobile technology besides perception and

attitudes.

This section explored the different theories advanced to explain the factors of mobile

banking penetration. As highlighted above, a multitude of research models have been proposed

to better predict the development of these services. However, it is found that there is still a lot

to be discovered on the determinants of these technologies, especially in Africa, using a macro

approach. First, a common aspect of a majority of these studies is that they use a micro

approach and/or a one-country focus to identify the determinants of mobile banking. Second,

the context of application of these studies is sometimes a continent other than Africa. Third,

the macro environment is ignored in the majority of methodologies applied and the literature

focuses more on the micro environment. Consequently, studies inform us more on the micro

factors of mobile banking development, and less on the macro factors, such as economic policy,

external flows, human development, institutional economy, economic development, and

business and capitalism. Fourth, the methodologies used are generally observation theories,

12

surveys, and statistical analyses, with fewer studies using an econometric analysis approach for

their empirical investigation.

3. Mobile Finance & Banking in Africa: Stylized Facts, Statistical Issues, and

Benchmarking

Developing countries, including African countries, could use the opportunity of mobile

banking to provide financial services to the unbanked individuals, given that the number of

mobile phones is more than the number of bank accounts. Africa ranked among the largest

continents in mobile penetration, with a higher growth rate of mobile phone subscribers,

whereas it has a lower number of bank branches. Mobile banking is a cheap way to offer

financial services in Africa. The fast-growing smartphone market in Africa, with prices

bottoming out and with more phone possibilites, is directly correlated with the growth of

mobile banking. As for broadband, connectivity is limited and has still not reached many areas

in Africa, and Internet usage is much lower compared to mobile phone diffusion.

The advancement of mobile communications and wireless technologies has led to a

rapid development in the sector of banking services using mobile phones. A good system with

much potential has the capacity to attract many customers who opt for banking services through

their mobile phones. The dynamism in the present era of technology, when many more options

are available, makes the mobile banking system attract more customers to use mobile banking

services. Recently, Africa has witnessed a very high growth in cellular phones usage, with

around 650 million customers in 2012. The lower access rate of formal banking highlighted

above, and the important volume of immigrant transfers, has contributed to unleashing the

increasingly effective and potential demand of financial services innovation. The banking

services started slowly in 2000 in Zambia, South Africa (which launched the biometrical

payment system in 2012), and the Philippines. Other countries have introduced innovations,

such as Kenya with the launch of M-PESA (a money transfer through SMS) and M-Shwari (a

banking service without folders) in 2007.

Interestingly, the provision rate of mobile banking (2.7 percent) appears to be less than

that of traditional banking (5 percent) in this case. However, the development of mobile

banking can improve communication and information exchange, formal savings, remittances

and reduce operating costs. More interestingly, informal finance, which appears to be important

in the African context, can be reabsorbed by the formal system and allows for data availability,

good investment, and well-informed governmental financial policy implementation.

13

However, recent studies of mobile banking adoption reveal that the adoption of mobile

banking services is still very low compared to the other banking channels (Wessels and

Drennan, 2010; Laukkanen and Kiviniemi, 2010; Zhou and others, 2010). Although, there are

many advantages of mobile banking, when compared with developed countries like the United

States, the United Kingdom, and Finland, the adoption of mobile banking in Africa is in its

infancy. Mobile banking has recently attained greater significance in Africa and there is a lack

of empirical studies related to the adoption of mobile banking and mobile phone penetration.

Additionally, there are no theoretical studies applied to the African context on the subject.

In order to present the results of our benchmarking exercise, it is important to recognize

that mobile penetration is a necessary but insufficient condition for mobile banking. Mobile

penetration is influenced by regulation in the mobile phone market, whereas mobile banking is

influenced by regulations in the banking industry. The figures in the appendix show that the

two are, of course, symbiotic and positively related.

Moreover, there is a mitigated link between mobile banking development indices and

pro-poor and inclusive growth in Africa. As shown in the figures in the appendix, depending

on the proxy of mobile banking development, there is either a positive or negative link with

pro-poor and inclusive growth.

Considering this information and conjectures, we need to carry out an econometric

assessment of the situation.

4. Data, Model, and Econometric Strategy

4.1 Data

Within the population of African countries, we examine a sample of 49 sub-Saharan African

countries, using data from the African Development Indicators (ADI), Governance

Development Indicators (GDI), and Financial Development and Structure Database (FDSD) of

the World Bank (WB).The mobile banking data is from the World Bank and the index of

economic freedom is from the Heritage Foundation. Other databases from the Gates

Foundation and Mastercard Foundation are not suitable to our investigation and were not

available for African countries.

Tables A.3 and A.4 along with A.6 in the appendix provide more details about a clear

and precise description of the data sources, the databases used, and the variables. In order to

construct our dependent variable, we used the principal component analysis.

Principal Component Analysis

14

The potentially high degree of substitution between Internet users, mobile bills, and mobile

send/received variables imply that some information could be redundant. Therefore, we employ

Principal Component Analysis (PCA) to mitigate the redundancy of common information in

the dependent variables. PCA is a widely employed statistical technique that is used to reduce

a large group of correlated variables into a smaller set of uncorrelated variables, which

represent a substantial degree of variation in the original dataset. These common factors are

called principal components (PCs). The criterion used to retain common factors is from Kaiser

(1974) and Jolliffe (2002), who recommend only PCs which have eigenvalues greater than the

mean value (greater than one). The underlying logic for using PCA is that, given the potentially

high correlation (degree of substitution) between mobile banking and mobile phone

penetration, more general policy implications may be obtained if the dependent variables are

represented by a common factor.

Without going into depth about the PCA technique, as it can be seen from table A.5 in

the appendix that the first PC, of both mobile bills and mobile send and received, accounts for

around 80 percent of the variation in all three constituents, while it accounts for 69 percent for

Internet users. The criteria applied to determine how many common factors to keep are taken

from Kaiser (1974) and Jolliffe (2002). Kaiser recommends dropping factors with an

eigenvalue less than one.

4.2 Models and methodology

In order to check the impact of mobile banking development on pro-poor and inclusive growth

and the determinants of mobile banking, we will use two different models.

The first model is based on the Cobb-Douglas function as follows:

{(𝑃𝑟𝑜𝑃𝑜𝑜𝑟&𝐼𝑛𝑐𝑙𝑢𝑠𝑖𝑣𝑒𝐺𝑟𝑜𝑤𝑡ℎ)𝑖,𝑡 = 𝛼0 + 𝛼1(𝑀𝑜𝑏𝑖𝑙𝑒𝐵𝑎𝑛𝑘𝑖𝑛𝑔)𝑖,𝑡 + 𝛼2𝑓(𝑋𝑖,𝑡) + 𝜀𝑖,𝑡

𝜀𝑖,𝑡 ~ 𝑖𝑖𝑑𝑁(0, 𝜎𝜀2)

(1)

where the left-hand-side includes variables on pro-poor and inclusive economic growth,

such as GDP per capita growth, poverty index, and GINI growth. The right-hand-side includes

variables on mobile banking (mobile banking index, mobile bills, mobile sent/received,

Internet users) and other control variables identified in the literature as fundamental factors of

inclusive and pro-poor economic growth. These include technological innovation; economic

15

policy; business and bank; economic development and physical capital; external flows; human

development; institutional and knowledge economy areas.

The estimation approach for the first model follows the study conducted by

Andrianaivo and Kpodar (2011), which are among the few panel data studies that focus on the

effects of mobile Information and Communication Technologies (ICT) on economic growth.

In these papers, the issue of reverse causality between mobile telecoms expansion and

economic growth is addressed by specifying a dynamic panel data model and estimating the

parameters using either the Generalized Method of Moments (GMM) technique or Least

Squares Dummy Variables (LSDV).

The econometric approach undertaken is the dynamic panel data estimation method

introduced by Arellano and Bond (1991). The choice of this approach is motivated by two main

factors. First, this technique allows the potential endogeneity of mobile banking data to be

addressed by using the lags of these variables as instruments. Second, a panel data technique

allows the best exploitation of the information contained in the dataset such as the cross-

country variation in the sample (at a given point in time, different countries are characterized

by different levels of mobile banking) and the time-series variation (for each country, mobile

data usage substantially varies over time).

For the mobile finance and banking development determinants model, due to the cross-

sectional structure of our data, we follow the theoretical model and the empirical specification

previously presented in the literature for this data structure (Andrés, 2006).The box in the

appendix presents the main lines for discussing the determinants of mobile banking.

i

n

c

cc

p

h

hhi YXMobileBank 1

21

10 (2)

Overall, for this second model, the dependent variable includes the “mobile banking

index,” “Internet users,” “mobile phone usage in the payment of bills,” and “mobile phone

usage in the sending/receiving of money,” respectively. As in the first model, independent

variables ( is a vector of determinants; is the set of control variables) are made up of

characteristics identified in the literature and concern technological innovation (Gutierrez and

Singh, 2013); economic policy; business and bank; economic development and physical

capital; external flows; household development; and institutional economy. All variables are

expressed in logarithm form, and to ensure a robustness analysis, we implement several

estimations of different specifications. is the constant; is the error term.

16

In order to estimate this model as explained above, we use the cross-sectional

estimation method. We choose this estimation method and this sample for the following main

reasons:

The data used concern only a specific point in time, with multiple variables at the time

of the data snapshot. First, the data can better help answer questions such as “Are there

systematic factors that are associated with mobile banking development?” Second, time

is assumed to have a random effect that produces only variance, not bias.

African countries generally have homogeneous characteristics and allow us to expect

that we can avoid outliers, which are data points with extreme values that could have a

negative effect on our estimators.

5. Presentation and Discussion of Estimation Results

In this section, we present and discuss the results of our main empirical investigations

concerning mobile banking development and pro-poor and inclusive growth, and we further

examine the determinants of mobile banking development.

5.1 Mobile finance & banking development, and pro-poor and inclusive growth

The results presented in table A.1 in the appendix show that there is an overall positive impact

of mobile banking development on pro-poor & inclusive growth. More specifically, mobile

banking impacts positively on GDP per capita with a higher rate when we consider our index.

Independent of the mobile banking proxy used, the sign is positive. Additionally, there is a

negative impact of both the mobile banking index and other proxies on GINI and poverty index.

When we consider the economic freedom index, there is a positive impact on GDP per capita

and a negative impact on GINI growth.

The control variables also have the expected signs, with exceptions in the case of net

interest margin, return on asset for GDP per capita growth, and public investment for GINI

growth. This may imply that business and bank activities/profits are not useful when we

consider its importance in terms of pro-poor and inclusive growth, and that states focusing on

increasing investment cannot help but have good results in terms of the reduction of

inequalities.

Overall, our estimates have the expected signs and we can therefore extrapolate the

usefulness of mobile banking development in the case of Africa. What about the determinants

of mobile finance & banking sector development in Africa?

17

5.2 Mobile finance & banking determinants

Table A.2 in the appendix presents results for the four different models when we consider four

different proxy variables for mobile finance &banking.

When we consider the estimation using the mobile banking development indices we

built with principal component analysis, we find that domestic credit, human capital, education,

remittances, trade openness, credible monetary policy, and infrastructure are key determinants

of mobile banking development in Africa. Human development is the strongest positive

determinant since its impact coefficient is the highest (1.968), followed by urban population

(0.455), infrastructure (0.155), domestic credit (0.097), education (0.040), credible monetary

policy (0.015), trade openness (0.010) and remittances (0.001).

Knowledge level and active population are relevant as human capital indicators in terms

of mobile banking development in Africa. Infrastructure development appears to be a mobile

banking development determinant since mobile phones function with a higher

telecommunications infrastructure and people are more comfortable when they are dealing with

good institutional infrastructure. A credible monetary policy appears to be important and is

therefore legitimized as contributing to mobile finance & banking development in Africa.

The urban population is also instrumental to mobile finance & banking development in

Africa. We can see that the urban population is a positive determinant of mobile banking when

we consider the estimation with a mobile banking index. This can be explained by the fact that

this variable is closely related to and thus drives the demand for mobile banking assets in

African countries. From a theoretical point of view, it is not surprising that domestic credit

positively impacts our dependent variable. By having higher financial capacity compared to

credit, the willingness to use mobile financial and banking services increases. Trade openness

and remittances are determinants of mobile banking development in Africa because those two

activities tend to increase financial capacity.

Some variables seem to hamper mobile finance & banking development, depending on

the economic environment. These variables are: net interest margin, return of asset, and bank

density. This could be explained by the fact that the way the traditional market is working and

gaining profitability seems to reduce the potential and development of the mobile banking

sector. This ambiguous empirical result might mean that the hypothesis of banking

development as a catalyzer of mobile banking should is relative since it seems to be relatively

detrimental. In fact, we can see that the banking sector is more developed than the financial

sector in Africa but we still have a low depth of mobile banking.

18

Focusing more on developing financial markets than on developing banks is imperative

in this context and should be encouraged by a clear government policy. This finding is a

contribution to the recent literature on financial development in Africa because previous works

have not highlighted this result. It is important to mention that this result does not imply the

implementation of policies against the existence of traditional banks because banks in Africa

are pioneers of mobile banking and financial services development. The finding suggests that

the government should now focus more on financial market development in order to boost

mobile banking and financial services development in Africa.

Financial markets and stock markets are less developed in almost all African countries.

A study by Beck and others (2011) shows that more banking development and less stock market

development is a key feature of the financial structure—this could be another reason why

several African countries have a weak mobile banking market since their financial structure is

more bank-based than market-based. In fact, we can see that this financial structure failed to

improve the mobile banking depth in Africa. For almost all these countries, there are several

public and private banks but the mobile banking depth remains low yet stable. Hence, policy

makers who are willing to boost mobile banking in Africa should strongly consider

strengthening the development of stock markets.

When we consider the mobile billing index, the determinants of mobile banking

development, in order of importance are: human development (2.045), infrastructure (0.144),

credible monetary policy (0.094), trade openness (0.045) and remittances (0.022). These results

are closely related to the ones obtained using the constructed index of mobile banking

development. The more interesting marginal information we have is the fact that human

development becomes a stronger determinant than before. The impact of trade openness,

credible monetary policy, and remittances impact are also higher relative to the previous

estimation. All of these results are consistent with the existing literature.

When we consider the Internet users index, the determinants are, in order: human

development (5.21), credible monetary policy (1.055), infrastructure (0.293), remittances

(0.122), and trade openness (0.045).

Finally, when we consider the mobile sent/received index, we have the following

determinants: human development (1.682), domestic credit (1.467), credible monetary policy

(0.253), infrastructure (0.082), remittances (0.048) and trade openness (0.002). Related to the

results presented in the paragraph above, there is a determinant specific to this proxy, which is

domestic credit. Domestic credit is therefore a factor of sending and receiving money using a

mobile phone, and not of bills payment using a mobile phone or Internet usage.

19

Overall, one determinant appears to be consistent to all our models, namely human

development. This determinant is positively and significantly related to mobile banking

development independent of the method used and proxy used. More interestingly, it presents

the highest impact relative to other determinants as highlighted by the results of this

investigation.

5.3 Robustness check

In order to verify that our results are robust and consistent with Young and Kroeger (2015), we

implement additional estimations by replacing some variables with their proxy, and by

changing the specification and estimation method. When changing the specification, we are

guided by the maximization of the number of observations relative to that of the main

estimation. Practically, it consists of either adding control variables, which might affect the

dependent variable, or removing some other control variables, with the aim of maximizing the

number of observations.

As can be seen in table A.1, for example, for the economic policy explanatory variables,

instead of using trade openness, CMP, and public investment, we use financial openness alone

to verify the robustness of our estimation. We do the same for business and bank proxies:

instead of considering interest rate spread and return on assets, as in the main estimation, we

use net interest margin, domestic credit, bank density, and return on equity. For economic

development and capital proxies, we use population growth, urban population, infrastructure,

and GDP per capita growth in place of GDP growth; for external flows, we replaced foreign

investment with foreign aid and remittances; for human development proxies, net transfers

have been replaced by human development, household expenditure, and domestic savings; for

institutional economy, governance is considered in place of education. Additionally, for our

robustness check, we moved among the three proxies of mobile banking and financial

development in Africa, which are mobile billing, mobile sent/received, and Internet users.

Our results are irrefutable since we have the same sign and significant variables as in

the main results discussed. By replacing some variables with their proxy, we were able to verify

whether we obtain the same result, independent of the fact that we use different measures for

the same variable. Overall, from the estimation results, we find that results remain unchanged

in terms of sign and significance of coefficients. Our findings also remain unchanged when

controlling for mobile finance & banking development with alternative indices.

20

6. Conclusion and Policy Recommendation

This paper uses a new database on mobile finance & banking across countries and several

econometric techniques to investigate the impact of mobile finance & banking on pro-poor &

inclusive growth, and identifies the main determinants of mobile finance &banking

development in Africa.

We begin by using a theoretical framework and highlighting stylized facts. Mainly, the

statistical analysis reveals that there is a positive link between mobile finance & banking

development and pro-poor & inclusive growth in Africa.

The estimation of our model of pro-poor & inclusive growth, using different

specifications, shows a positive impact of mobile finance & banking indices on both pro-poor

and inclusive economic growth in Africa.

Based on the result of this first analysis, the paper goes further by undertaking several

econometric analyses, which yield the following key findings. Concerning mobile banking

development determinants, we find that domestic credit, human capital, remittances, trade

openness, CMP, and infrastructure are key determinants of mobile banking development in

Africa, independent of the proxy used. Human development is the strongest positive

determinant since its impact coefficient is the highest. The CMP is also important and is

therefore legitimated as contributing to mobile finance & banking development in Africa.

Overall, African governments in their pursuit of good performance, in terms of mobile

banking development, should implement policies mainly oriented toward domestic credit

access facilitation, human capital development, remittances facilitation, trade openness, CMP,

and infrastructure development.

21

Appendix

Figure A.1: Mobile sent/received and mobile phone penetration in Africa

Figure A.2: Mobile bills and mobile phone penetration in Africa

Source: Author’s calculation. Source: Author’s calculation.

Figure A.3: Internet users and mobile phone penetration in Africa

Figure A.4: Mobile sent/received and mobile bills in Africa

Source: Author’s calculation. Source: Author’s calculation.

Figure A.5: Mobile sent/received and mobile banking in Africa

Figure A.6: Mobile bills and mobile banking in Africa

Source: Author’s calculation. Source: Author’s calculation.

y = 0,0633x + 5,0142R² = 0,024

0

10

20

30

40

50

60

70

0 20 40 60 80 100 120 140 160

Mo

bile

ban

kin

g (s

ent/

rece

ived

)

Mobile phone penetration

Mobilebanking(sent/received) = f(Mobilephonepenetration)Linear(Mobilebanking(sent/received) = f(Mobilephonepenetration))

y = -0,0137x + 4,0675R² = 0,0077

0

5

10

15

20

25

30

0 20 40 60 80 100 120 140 160

Mo

bile

Ban

kin

g (m

ob

ile b

ills)

Mobile phone penetration

Mobilebanking(mobilebills) =f(Mobilephonepenetration)

Linear(Mobilebanking(mobilebills) =f(Mobilephonepenetration))

y = 0,0015x - 0,0857R² = 0,0014

-2

-1

0

1

2

3

4

5

0 20 40 60 80 100 120 140 160

Inte

rnet

use

rs

Mobile phone penetration

Mobilebanking= f(mobilepenetration)

Linear(Mobilebanking= f(mobilepenetration))

y = 1,666x + 3,1734R² = 0,4047

0

10

20

30

40

50

60

70

0 5 10 15 20 25 30

Mo

bile

sen

t/re

ceiv

ed

Mobile bills

Mobilesent/received =f(mobilebills)

Linear(Mobilesent/received =f(mobilebills))

y = 0,0888x - 0,7672R² = 0,8181

-2

-1

0

1

2

3

4

5

0 10 20 30 40 50 60 70

Mo

bile

sen

t/re

ceiv

ed

Mobile banking

Mobilesent/received = f(Mobilebanking)

Linear(Mobilesent/received = f(Mobilebanking))

y = 0.2324x - 0.7633R² = 0.8181

-2

-1

0

1

2

3

4

5

6

0 5 10 15 20 25 30

Mo

bile

bill

s

Mobile banking

Mobilebills =f(Mobilebanking)

Linear(Mobilebills =f(Mobilebanking))

22

Figure A.7: Mobile banking and pro-poor growth in Africa

Figure A.8: Mobile bills and pro-poor GDP in Africa

Source: Author’s calculation. Source: Author’s calculation.

Figure A.9: Mobile sent/received and pro-poor GDP in Africa

Figure A.10: Mobile banking and pro-poor GDP in Africa

Source: Author’s calculation. Source: Author’s calculation.

Figure A.11: Mobile bills and pro-poor GDP in Africa Figure A.12: Mobile banking and pro-poor GDP in Africa

Source: Author’s calculation. Source: Author’s calculation.

y = 0,0235x + 2,5369R² = 7E-05

-10

-5

0

5

10

15

-2 -1 0 1 2 3 4 5

GD

P p

er c

apit

a gr

ow

th

Mobile banking

GDP percapitagrowth =f(Mobilebanking)

Linear(GDP percapitagrowth =f(Mobilebanking))

y = -0,0177x + 2,5813R² = 0,0004

-10

-5

0

5

10

15

0 5 10 15 20 25 30GD

P p

er c

apit

a

Mobile bills

GDP percapita =f(Mobilebills)

Linear(GDP percapita =f(Mobilebills))

y = 0,0061x + 2,4848R² = 0,0007

-10

-5

0

5

10

15

0 10 20 30 40 50 60 70GD

P p

er c

apit

a

Mobile sent/received

GDP percapita =f(Mobilesent/received)

Linear(GDP percapita =f(Mobilesent/received))

y = -0,3887x + 4,7669R² = 0,0175

-10

-5

0

5

10

15

20

-2 -1 0 1 2 3 4 5

GD

P g

row

th

Mobile banking

GDPgrowth =f(Mobilebanking)

Linear(GDPgrowth =f(Mobilebanking))

y = -0,0604x + 4,9725R² = 0,004

-10

-5

0

5

10

15

20

0 5 10 15 20 25 30

GD

P g

row

th

Mobile bills

GDPgrowth=f(Mobile bills)

Linear(GDPgrowth=f(Mobile bills))

y = -0,0392x + 5,1313R² = 0,0257

-10

-5

0

5

10

15

20

0 10 20 30 40 50 60 70

GD

P g

row

th

Mobile sent/received

GDPgrowth =f(Mobilesent/received)

Linear(GDPgrowth =f(Mobilesent/received))

23

Table A.1: Impact of mobile finance & banking on pro-poor & inclusive growth (panel data estimation) GDP Per Capita growth GINI growth Poverty

Mobile Banking Development &Technological innovation

Internet users 0.175** 0.043*** --- -0.01*** -0.01*** --- -0.52** ---

(0.015) (0.000) (0.000) (0.000) (0.008)

Mobile billing 0.042** --- --- --- -0.97** --- -0.053** --- (0012) (0.021) (0.019) Mobile S/R --- 0.007* --- 0.01*** --- --- --- ---

(0.086) (0.000)

Mobile banking -2.65 0.422*** 1.729*** --- --- -0.68** --- -0.001 (0.375) (0.000) (0.000) (0.009) (0.348) Economic freedom 1.058*** 0.175*** --- -0.009*** 0.124 --- 0.14 --- (0.000) (0.000) (0.000) (0.245) (0.702) Economic policy

Trade openness 1.05*** --- 0.315 -2.377 -3.008 -0.22*** 0.031 -0.008**

(0.000) (0.112) (0.433) (0.199) (0.008) (0.342) (0.022)

Financial openness 0.458 --- 0.155 --- --- -0.411 --- 0.086 (0.428) (0.455) (0.183) (0.175)

Money Supply -0.11* --- 0.191* --- --- 0.529 --- -1.001 (0.071) (0.076) (0.806) (0.444) CMP 0.055** --- 0.102* --- --- -0.078** --- -0.177 (0.004) (0.058) (0.016) (0.753) Public Investment -1.01 --- -0.971 --- --- 1.22*** --- 0.01***

(0.239) (0.354) (0.000) (0.007)

Business / Bank

Net Interest Margin

-1.22** -0.89* -2.65 2.067 -0.093 -1.42** 1.083 0.78***

(0.003) (0.052) (0.185) (0.709) (0.808) (0.015) (0.301) (0.001)

Domestic credit -2.030 0.104 -2.68 --- --- -1.68*** --- -2.15**

(0.249) (0.688) (0.184) (0.000) (0.035)

Interest Rate Spread

--- --- 1.058 --- --- 3.082 --- 1.452 (0.866) (0.113) (0.682)

Bank Density 10.6*** 3.89** 2.96** --- --- 1.022 --- 0.175 (0.000) (0.012) (0.025) (0.529) (0337) Return on Assets -1.55 0.632 -9.6*** --- --- 0.328 --- 1.002 (0.539) (0.556) (0.008) (0.193) (0.997) Return on Equity 0.150 -0.04 0.78** --- --- -0.017 --- -1.447 (0.470) (0.585) (0.013) (0.670) (0.887)

Economic development & capital

Infrastructure 5.009 0.21 1.435* -2.099 -1.093 -0.86*** -0.409 -1.55**

(0.922) (0.235) (0.064) (0.222) (0.603) (0.000) (0.189) (0.026)

Population growth --- 1.62 -35.18 --- --- 0.448 --- 0.117 (0.804) (0.105) (0.341) (0.102) Urban population --- 12.0*** 17.27*** --- --- 1.547 --- 0.448 (0.000) (0.000) (0.391) (0.993)

External Flows

Foreign Investment

0.289 --- 1.09** 0.306 0.139 -0.496* 0.089 -1.008 (0.133) (0.029) (0.312) (0.362) (0.062) (0.721) (0.229)

Foreign Aid --- 0122 2.099 0.185 -0.051 -0.002 -1.04 -0.018 (0.288) (0.422) (0.285) (0.502) (0.989) (0.955) (0.575) Remittances --- --- 0.009 -0.187 -0.75*** -0.060 -0.009** 0.001 (0.339) (0.431) (0.000) (0.814) (0.017) (0.113)

Human Development

Human Development

0.056 2.099 -0.081 --- 0.045 --- 1.89 --- (0.427) (0.449) (0.966) (0.272) (0.978)

Household expenditure

--- --- 1.007 0.054 --- --- --- --- (0.109) (0.839)

Domestic Savings --- --- -0.001 --- -0.341 -0.286 -0.504 -0.777 (0255) (0.152) (0.221) (0.348) (0.969)

Net transfer --- --- 0.089 --- --- -3.098 --- -1.55 (0.599) (0.822) (0.333) Institutional Economy

Education -0.099 0.006 -1.449 2.51*** --- -1.49*** --- -0.646***

(0.437) (0.111) (0.118) (0.000) (0.000) (0.002)

Governance --- --- 1.001 -3.627 0.922 -17.8*** 1.001 -2.05***

(0.221) (0.736) (0.934) (0.003) (0.444) (0.001)

Constant -28.65 -432*** -468*** -85.8*** -216*** -96.68 -12.6** 88.12 (0.375) (0.000) (0.000) (0.000) (0.000) (0.109) (0.018) (0.447) LSDV R² 0.981 0.903 0.985 0.901 0.809 0.999 0.706 0.802 Within R² 0.859 0.805 0.960 0.801 0.801 0.850 0.622 0.702 LSDV Fisher 41.9*** 42.4*** 98.06*** 29.95*** 29.5*** 37.5*** 18.9*** 24.7***

Cross Sections 6 30 6 37 38 22 18 22 Observations 25 190 25 251 238 145 109 145

Source: Author’s calculations. Note: OLS with HACSE: Ordinary Least Squares with Heteroscedascticity and Autocorrelation Consistent Standard Errors. LSDV: Least Squares Dummy Variable. *; **; ***: denote significance levels at 10%, 5% and 1%, respectively.

24

Table A2: Determinants of Mobile finance & banking (cross-sectional estimation)

Mobile billing Mobile sent/received Internet users Mobile banking Financial openness --- 0.044 --- -2.058 --- 0.045 --- -0.001 (0.225) (0.805) (0.205) (0.119) Economic policy

Trade openness 0.045** --- 0.002** --- 0.045** --- 0.010** --- (0.010) (0.050) (0.027) (0.013) CMP 0.094** --- 0.253* --- 1.055** --- 0.015** --- (0.014) (0.072) (0.048) (0.043) Public Investment 0.0004 --- -0.059 --- 0.001 --- -0.006 --- (0.991) (0.811) (0.257) (0.621)

Business/ Bank

Net Interest Margin --- -0.361 --- -0.060 --- 0.175 --- -0.050**

(0.378) (0.879) (0.448) (0.021)

Domestic credit --- -0.284 --- 1.467** --- 1.022 --- 0.097*

(0.204) (0.035) (0.809) (0.078)

Interest Rate Spread -0.208 --- 0.102 --- 1.001 --- 2.006 --- (0.124) (0.805) (0.560) (0.117) Bank Density --- -0.708 --- -0.403 --- -0.008 --- -0.205**

(0.120) (0.277) (0.608) (0.034)

Return of Assets 1.069 --- 1.855 --- 0.001 --- -1.009* ---

(0.205) (0.907) (0.308) (0.066) Return of Equity --- -0.170 --- 0.022 --- -1.008 --- -0.051 (0.338) (0.723) (0.905) (0.109)

Economic develop-ment& capital

GDP growth 0.122 --- 0.078 --- --- -0.001 0.044 --- (0.669) (0.244) (0.803) (0.477) Population growth --- 1.099 --- 1.001 --- 0.924 --- 0.305 (0.144) (0.703) (0.334) (0.112) Urban population --- 0.802 --- 1.077 --- 1.001 --- 0.455*

(0.338) (0.201) (0.129) (0.072)

Infrastructure --- 0.144** --- 0.082* --- 0.293** --- 0.155*

(0.018) (0.065) (0.042) (0.084)

GDP per capita growth

--- 0.008 --- 0.177 -0.000 --- --- 1.054 (0.188) (0.933) (0.449) (0.117)

External Flows

Foreign Investment -1.007 --- -1.089 --- 0.001 --- -0.042 --- (0.233) (0.924) (0.155) (0.415) Foreign Aid --- 0.071 --- 0.048 --- -0.188 --- 0.001 (0.577) (0.199) (0.805) (0.408) Remittances --- 0.022** --- 0.048*** --- 0.122* --- 0.001**

(0.039) (0.000) (0.075) (0.028)

Net transfer 1.093 --- 1.008 --- --- 1.098 1.001 --- (0.445) (0.551) (0.228) (0.198) Human Develo- pment

Human Development --- 2.045* --- 1.682** 5.21** 4.65** --- 1.968**

(0.056) (0.048) (0.013) (0.020) (0.012)

Household expenditure

--- 1.244 --- 1.0001 --- 0.009 --- 0.018 (0.533) (0.444) (0.210) (0.227)

Domestic Savings --- 0.008 --- 0.166 -0.003 --- --- 1.077 (0.288) (0.222) (0.589) (0.447)

Institutio-nal economy

Education -0.024 --- 0.065 --- --- -0.369 -0.003 0.040*

(0.277) (0.279) (0.364) (0.527) (0.052)

Governance --- 0.100 --- 0.044 -0.369 --- --- --- (0.277) (0.111) (0.304)

Constant -0.572 11.07* 3.711 15.78** -2.72*** -3.14*** -0.98*** 1.320 (0.413) (0.077) (0.650) (0.031) (0.000) (0.007) (0.000) (0.107)

Adjusted R² 0.420 0.608 0.489 0.169 -0.169 0.397 0.030 -0.197 Fisher 5.87*** 3.869 45.1*** 0.935 1.393 5.31*** 3.80** 3.108**

RAMSEY RESET 1.968 n.a 1.083 4.79** 0.336 1.800 0.571 0.230 (0.179) (0.375) (0.031) (0.721) (0.204) (0.572) (0.797) Observations 20 8 17 18 18 20 34 20

Source: Author’s calculations. Note: *,**,***: denote significance levels of 10%, 5%, and 1% respectively. The regressions are based on heteroscedasticity consistent standard errors.

25

TABLE A.3: MOBILE FINANCE & BANKING DEVELOPMENT IMPACT ON INCLUSIVE / PRO-POOR

ECONOMIC GROWTH

Variables category Proxy

Mobile Finance & Banking Development (4) Internet users per capita, Mobile Billing, Mobile S/R, Mobile Banking

Economic policy (5) CMP, Trade openness, financial openness, public investment, M3

Business/Bank(6) Investment incentives (Domestic credit, NIM, IRS, Bank density, ROA, ROE)

Economic development and physical capital (3) Market size, market growth, market structure

(Infrastructure, Popg, Population)

Institutional Economy (3) Governance, Education (SSE).

External Flows (3) FDI, Development Assistance, Remittances

Human development (4) Net transfer, HDI, HHCExp, Domestic savings

Source: Author’s calculations. Note: CMP: Credible Monetary Policy. Mobile S/R: Mobile phone used to send and receive money. M3: Money Supply. GFCF: Gross Fixed Capital Formation. NIM: Net Interest Margin. IRS: Interest Rate Spread. ROA: Return on Assets. ROE: Return on Equity. GDPg: GDP growth. Popg: Population growth. SSE: Secondary School Enrollment. Ubanpop: Urban population. FDI: Foreign Direct Investment. HDI: Human Development Index. HHCExp: Household Consumption Expenditure. TABLE A.4: MOBILE FINANCE & BANKING DETERMINANTS

Variables category Proxy

Economic policy (4) CMP, Trade openness, financial openness, public investment.

Business/Bank (7) Investment incentives (Domestic credit, NIM, IRS, Bank density, ROA, ROE)

Economic development and physical capital (6) Market size, market growth, market structure

(Infrastructure, GDPg, GDP per capita growth, Inequality, Popg, Population)

Institutional Economy (3) Governance, Education (SSE).

External Flows (3) FDI, Development Assistance, Remittances

Human development (4) Net transfer, HDI, HHCExp, Domestic savings

Source: Author’s constructions. Note: CMP: Credible Monetary Policy. M3: Money Supply. GFCF: Gross Fixed Capital Formation. NIM: Net Interest Margin. IRS: Interest Rate Spread. ROA: Return on Assets. ROE: Return on Equity. GDPg: GDP growth. Popg: Population growth. SSE: Secondary School Enrollment. Ubanpop: Urban population. FDI: Foreign Direct Investment. HDI: Human Development Index. HHCExp: Household Consumption Expenditure. Table A.5: PCA result for the construction of the mobile finance & banking index

Principal

Components

Component Matrix (Loadings) Proportion Cumulative

Proportion

Eigen

Value

MBills MSR Internet First PC 0.805 0.809 0.690 0.896 0.896 1.596 Second PC -0.805 0.809 0.690 0.156 1.000 0.386

Source: Author’s constructions. Note: PC: Principal Component. MBill: Mobile phone used to pay bills. MSR: Mobile phone used to send and receive money. Internet: Internet users (per capita).

26

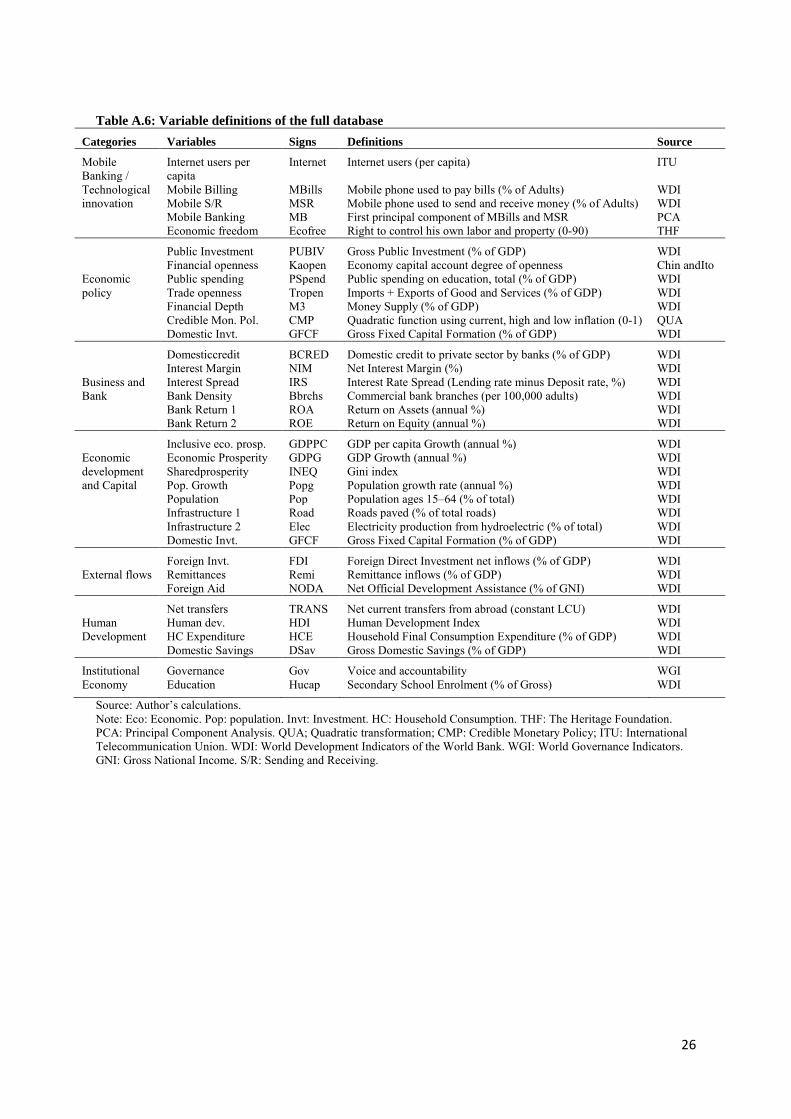

Table A.6: Variable definitions of the full database

Categories Variables Signs Definitions Source

Mobile Banking / Technological innovation

Internet users per capita

Internet Internet users (per capita) ITU

Mobile Billing MBills Mobile phone used to pay bills (% of Adults) WDI Mobile S/R MSR Mobile phone used to send and receive money (% of Adults) WDI Mobile Banking MB First principal component of MBills and MSR PCA Economic freedom Ecofree Right to control his own labor and property (0-90) THF

Economic policy

Public Investment PUBIV Gross Public Investment (% of GDP) WDI Financial openness Kaopen Economy capital account degree of openness Chin andIto Public spending PSpend Public spending on education, total (% of GDP) WDI Trade openness Tropen Imports + Exports of Good and Services (% of GDP) WDI Financial Depth M3 Money Supply (% of GDP) WDI Credible Mon. Pol. CMP Quadratic function using current, high and low inflation (0-1) QUA Domestic Invt. GFCF Gross Fixed Capital Formation (% of GDP) WDI

Business and Bank

Domesticcredit BCRED Domestic credit to private sector by banks (% of GDP) WDI Interest Margin NIM Net Interest Margin (%) WDI Interest Spread IRS Interest Rate Spread (Lending rate minus Deposit rate, %) WDI Bank Density Bbrchs Commercial bank branches (per 100,000 adults) WDI Bank Return 1 ROA Return on Assets (annual %) WDI Bank Return 2 ROE Return on Equity (annual %) WDI

Economic development and Capital

Inclusive eco. prosp. GDPPC GDP per capita Growth (annual %) WDI Economic Prosperity GDPG GDP Growth (annual %) WDI Sharedprosperity INEQ Gini index WDI Pop. Growth Popg Population growth rate (annual %) WDI Population Pop Population ages 15–64 (% of total) WDI Infrastructure 1 Road Roads paved (% of total roads) WDI Infrastructure 2 Elec Electricity production from hydroelectric (% of total) WDI Domestic Invt. GFCF Gross Fixed Capital Formation (% of GDP) WDI

External flows

Foreign Invt. FDI Foreign Direct Investment net inflows (% of GDP) WDI Remittances Remi Remittance inflows (% of GDP) WDI Foreign Aid NODA Net Official Development Assistance (% of GNI) WDI

Human Development

Net transfers TRANS Net current transfers from abroad (constant LCU) WDI Human dev. HDI Human Development Index WDI HC Expenditure HCE Household Final Consumption Expenditure (% of GDP) WDI Domestic Savings DSav Gross Domestic Savings (% of GDP) WDI

Institutional Economy

Governance Gov Voice and accountability WGI Education Hucap Secondary School Enrolment (% of Gross) WDI

Source: Author’s calculations. Note: Eco: Economic. Pop: population. Invt: Investment. HC: Household Consumption. THF: The Heritage Foundation. PCA: Principal Component Analysis. QUA; Quadratic transformation; CMP: Credible Monetary Policy; ITU: International Telecommunication Union. WDI: World Development Indicators of the World Bank. WGI: World Governance Indicators. GNI: Gross National Income. S/R: Sending and Receiving.

27

Box: Determinants of Mobile Banking

There are two main lines of discussion about the determinants of mobile banking. The first line takes into consideration the macroeconomic environment of the country; the second line presents some statistics on the proliferation of mobile telephony in Africa. The first line covers the characteristics of the macroeconomic context in which mobile banking is involved in Africa. The macroeconomic environment is favorable to the development of mobile banking because of the following reasons: First, from an international perspective, generally, we have in Africa a less internationally connected and developed banking and financial system. Therefore, the virtual connection offered by mobile telecommunications to households is an excellent alternative tool for banking and finance. Second, the context of an increasing level of fund transfers from abroad to Africa can be mobilized by well-established mobile banking, given a higher level of mobile penetration. Thirdly, it can help boost the investment activities.

The second line of discussion presents a picture of the proliferation of mobile banking with some statistics. The story of the growth of mobile phones in Africa is one of a massive and unexpected change in communications technology (Mbiti and Weil, 2011). From being virtually unconnected in the 1990s, more than 60 percent of Africa now has mobile phone coverage, and there are currently over ten times as many mobiles as landline phones in use (Aker and Mbiti, 2010). Aker and Mbiti have further stressed how African mobile phone coverage has progressed at a staggering rate over the past decade. In 1999, only 11 percent of the African population had mobile phone coverage, primarily in Southern (Kenya and South Africa) and Northern (Egypt, Algeria, Libya, Morocco, and Tunisia) Africa. By 2008, 60 percent of the population (477 million) could get a signal and an area of 11.2 million square kilometers (equivalent to the United States and Argentina combined) had mobile phone coverage. It was projected that by 2012, most villages in Africa would have coverage, with only a handful of countries relatively unconnected. Kenya has undergone a remarkable information and communication technology (ICT) revolution. By the 1990s, less than 3 percent of Kenyan households owned a telephone, and less than 1 in 1000 Kenyan adults had mobile phone service (Demombynes and Thegeya, 2012). However, by 2011, 93 percent of Kenyan households owned a mobile phone. The M-PESA mobile-banking network is largely credited for this dramatic change.

Source: Based on a literature review by the author.

28

The number of fixed telephone suscriptions in Africa is very low: Libya is the country with more subscriptions and has 11.3 per 100 inhabitants.