mizuho dealer s eyemizuho bank | mizuho dealer’s eye january 31, 2014 2 tapering to the tune of...

TRANSCRIPT

Mizuho Dealer’s Eye February 2014

U.S. Dollar .................................................................... 1 Euro .............................................................................. 7 Canadian Dollar ......................................................... 12 British Pound .............................................................. 14 Singapore Dollar ........................................................ 18 Thai Baht .................................................................... 21 Malaysian Ringgit ...................................................... 24 Indonesian Rupiah ..................................................... 27

Philippine Peso ........................................................... 30 Korean Won ............................................................... 36 New Taiwan Dollar .................................................... 40 Hong Kong Dollar ...................................................... 45 Chinese Yuan ............................................................. 49 Australian Dollar ........................................................ 55 India Rupee ................................................................ 59

Mizuho Bank, Ltd.

Forex Division

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 1

Daisuke Karakama, Kenta Tadaide, Yuki Yamazaki, Market Economists, Forex Division

U.S. Dollar – February 2014

1. Review of the Previous Month

The dollar/yen pair weakened in January.

After opening the month at the lower-105 yen mark, the pair temporarily hit a monthly high of

105.45 yen as yields on 10-year U.S. government bonds moved firmly. It then dropped to the mid-104

yen level, though, as the NY Dow Jones moved bearishly after the markets reacted badly to the poor

performance of the Chinese Manufacturing PMI for December. The next day saw the pair falling to

around 104 yen as market participants began selling Asian stocks. It then dropped below 104 yen on

January 6 on the back of falling U.S. interest rates and a bearish Dow Jones. However, dollar buying

picked up on January 7 after the U.S. trade deficit for November unexpectedly shrank. As a result, the

currency pair rallied to the upper-104 yen mark. As dollar buying continued towards January 8, the

dollar regained the lower-105 yen level against its Japanese counterpart, with the pair also boosted by

the firm movements of the Nikkei Average. This level saw selling for profit taking, though, so the pair

weakened and traded with a heavy topside at the upper-104 yen mark. It strengthened to the 105 yen

level on January 9 on the back of firm European stock movements. In his press conference after the

ECB Governing Council meeting, though, ECB President Mario Draghi indicated that low interest

rates would be maintained for a long time. The euro/yen pair edged lower and the dollar/yen pair was

also dragged to the upper-104 yen level. January 10 saw the release of the much-anticipated U.S.

employment figures for December. The results fell significantly below expectations and the markets

reacted by selling the greenback, with the currency pair crashing to the upper-103 yen mark as a result.

January 13 saw more dollar selling on the back of the previous weekend’s terrible employment

news. With U.S. interest rates falling and the Dow Jones also sliding, the pair dropped further to hit the

upper-102 yen mark. It then rallied to the upper-103 yen level on January 14, though, due to dollar

buying by Japanese importers, with the greenback also being bought in the wake of the favorable

results of the U.S. retail sales data for December. Dollar buying ramped up on January 15 following an

upswing in the U.S. Producer Price Index (PPI) for December, so the pair gained to the upper-104 yen

mark. It then rose to just below 105 yen on January 16 due to: the firm movements of the Nikkei

Average; and Australian-dollar selling/U.S.-dollar buying after the markets reacted badly to a

substantial slump in the Australian employment data for December. However, the Dow Jones then

turned bearish, while U.S. interest rates also fell on the back of the results of the U.S. CPI data for

December. As a result, the currency pair moved with a heavy topside at the lower-104 yen mark.

The dollar gained across the board on January 21 due to: the firm movements of the Nikkei

Average; and reports in a U.S. newspaper that, if all went well, the FOMC was set to announce further

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 2

tapering to the tune of $10 billion when it met on January 28–29. During this time, the currency pair

gained to the upper-104 yen level. The Bank of Japan’s Monetary Policy Committee (MPC) met on

January 22. As expected, it decided to maintain the status quo. Some observers had expected further

easing, though, so they reacted by selling the dollar in disappointment, with the pair temporarily

breaking below 104 yen as a result. It soon recovered to the lower-104 yen mark, though, due to buying

from Japanese importers. It then hit the upper-104 yen level on January 23 in tandem with a bullish

Nikkei Average. However, the markets switched into risk-off mode after the preliminary China HSBC

Manufacturing PMI data for January dropped below 50 for the first time in six months. As the cross

yen came under selling pressure, the dollar/yen pair fell back to around 104 yen. The Argentine peso

then suffered sharp losses after the Argentine authorities allowed it to weaken. This led to a sell-off of

emerging-economy currencies and a rise in risk aversion. As yen buying increased, the dollar/yen pair

dropped below 103 yen. It then fell temporarily to a monthly low of 101.77 yen on January 27 while

activating stop losses. As concerns about emerging economies eased off towards the month’s end, the

pair rallied to the upper-102 yen mark and moved firmly thereafter.

96

98

100

102

104

106

13/10 13/11 13/12 14/01

(USD) USD/JPY

2. Outlook for This Month:

Emerging economy concerns and real-demand yen selling

Expected Ranges Against the yen: JPY101.00–105.00

The dollar/yen pair is expected to float up and down throughout February.

Since entering 2014, the pair has weakened on the back of two shocks: the “U.S. employment data

shock” and the “Argentine shock.” An optimistic mood has been spreading since November 2013,

though, with the dollar appreciating one-sidedly from 98 yen to 105 yen, so perhaps a little adjustment

is only natural. Though the pair fell, the most noticeable thing was how it was supported by buying

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 3

from Japanese importers when it broke below 102 yen, thus avoiding a dip below 100 yen. Concerns

about the emerging economies have flared up since the Argentine shock. The central banks of Turkey

and South Africa hiked interest rates to protect their currencies, but this has failed to calm market jitters

and things could remain tense in February. However, Japan is now struggling with a large trade deficit,

having recorded a record-high deficit in 2013, so the yen will face strong selling pressure on the supply

and demand front. Furthermore, at the January FOMC meeting, the FRB decided to reduce the scale of

its asset purchases once again and now seems to be steadily edging down the path towards a

normalization of monetary policy. Under these circumstances, the dollar/yen pair will probably float

around the lower-100 yen mark in February.

The trigger for growing concerns about emerging economies was the sharp fall in the value of the

Argentine peso after the Argentine authorities indicated they were prepared to tolerate peso

depreciation. However, Argentina defaulted in 2001 and has since been locked out of international

financial markets, so the Argentine shock is unlikely to spill over directly into other countries.

Nonetheless, since the Argentine shock, market participants have been lifting funds from emerging

markets and other countries with current account deficits and high inflation. Markets in the emerging

economies have been moving bearishly since the FRB touched on the possibility of QE tapering in

May 2013, so if negative news emerges from one or two of these countries, it could well lead to a flight

away from all emerging-economy assets. This trend is likely to be of a temporary nature and the

markets will gradually regain composure as time passes, but for now, with concerns about a Chinese

economic slowdown also bubbling away, skittish trading looks set to continue for the time being.

At the FOMC meeting on January 28–29, the FRB decided to taper its asset purchases by $10

billion to $65 billion a month (U.S. treasuries - $35 billion; MBS - $30 billion). In the accompanying

statement, the FOMC stated that “it likely will be appropriate to maintain the current target range for

the federal funds rate well past the time that the unemployment rate declines below 6-1/2 percent,

especially if projected inflation continues to run below the Committee's 2 percent longer-run goal.”

This was much as the markets had been expecting. Though the FOMC meeting took place against a

backdrop of instability in the emerging economies and plummeting currencies/stocks, its

accompanying statement made no mention of the situation in the emerging economies. It seems the

FRB is prepared to tolerate current levels of market turbulence as it continues to edge calmly towards a

normalization of monetary policy. A market consensus has been growing that the FRB will continue to

taper its asset purchases by $10 billion from hereon, so the recent announcement did not change the

market forecast for a mid-2015 commencement of interest rate rises. As risk aversion spreads across

the globe, yields on 10-year U.S. government bonds are trending downwards, but they will start rising

again once things calm down and this will probably act to bolster the dollar/yen pair.

Based on the aforementioned circumstances, the dollar/yen pair is likely to hover up and down in

February. More time will be needed before concerns about the emerging economies cool off. As global

stocks weaken, U.S. interest rates will probably face downwards pressure. However, when the pair hits

lows, it will likely face buying demand from Japanese importers, so it is expected to trade firmly in a

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 4

range between 101–105 yen.

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 5

Dealers' Market Forecast

(Note: These opinions do not necessarily agree with the other contents of this report.)

Bullish on the dollar (8 bulls: 100.00–106.00, Core: 101.00–105.25)

Fujisaki

101.00

–

106.00

The yen is expected to slide on the back of Japan’s large trade deficit and widening Japanese/U.S. interest-rate

differentials. Concerns remain about some emerging economies, so the markets are expected to switch into

risk-off mode for a time. As a result, the yen’s slide is likely to be slow-paced.

Kato

101.00

–

106.00

The dollar/yen pair will move in an adjustive range in February. This will be the main trend, not dollar

bullishness. Buoyant global stock markets may also face some adjustment and the currency pair’s topside is likely

to be capped by yen buying in the cross-yen markets.

Noda

100.00

–

105.00

Though market participants are keeping a close eye in the movements of emerging-market currencies, at this

moment in time there is no talk of the Argentine crisis spilling over into other countries. February will see the

release of settlement results, but the yen is expected to gradually start edging down again in line with the

fundamentals.

Yano

101.00

–

105.00

The U.S. has recently posted a number of bearish economic indicators, as evinced by the December employment

data, but this is mainly due to the impact of the cold weather. Once this particular factor is out of the way, the

economic recovery will continue. Japanese and U.S. monetary policies also suggest that interest-rate differentials

will widen from hereon. “Fundamentals” and “interest-rate differentials” will both boost the dollar/yen pair, so

February is also likely to see yen depreciation.

Takada

100.00

–

105.50

The dollar/yen pair’s topside will probably be tested in February on the back of the strong U.S. economic recovery

and steady QE tapering. Stocks will undergo some adjustment in the wake of uncertainty about emerging markets,

so some temporary yen buy-backs are likely, but the pair’s room on the downside will be capped.

Toriba

101.50

–

105.50

Ongoing QE tapering and bearish stock markets will see the dollar/yen pair moving with a heavy topside, though

its room on the downside will also be capped. The pair will also be supported by funds flowing back to developed

countries from emerging economies, so the pair’s movements will form a dip in February. The beginning of the

month will see the release of several jobs-related indicators, such as the employment data and the unemployment

rate, so market participants should pay attention to these results.

Shimoyama

101.00

–

105.00

Market participants should be wary of the risk-off mood emanating from emerging economies, but each country is

developing policy responses, so risk appetite is set to gradually recovery from here on. The dollar/yen pair will

also be boosted by fundamentals such as Japan’s trade deficit, so it is expected to make gains in February.

Inoue

101.00

–

105.00

Risk aversion has swept the markets on the back of the problems in Argentina, Turkey and elsewhere. However,

the impact on global markets will be limited and market concerns will gradually ease off. The dollar/yen pair is

likely to strengthen due to: dollar buying as the U.S. economic recovery kicks off again; and dollar buying by

Japanese importers.

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 6

Bearish on the dollar (4 bears: 98.00–104.50, Core: 99.25–103.75)

Nishijima

98.50

–

103.50

Concerns about the emerging economies and a Chinese economic slowdown continue to smolder away. Under

these circumstances, the markets will see more risk-aversive yen buying. If the U.S. employment data and the

debate about raising the debt ceiling are seen as negative factors, the dollar/yen pair is likely to undergo some

further adjustment.

Yamashita

98.00

–

103.50

It will take time before concerns about emerging markets are assuaged, despite the best efforts of central banks. As

the Chinese economic slowdown intensifies, stock markets are likely to slide across the globe. There seems to be a

dearth of new factors on the Japanese side too, so the dollar/yen pair looks set to trade with a heavy topside.

Sato

100.00

–

104.00

The financial markets will continue to be rattled by events in China and elsewhere. Japanese firms are also

expected to repatriate funds towards the end of the fiscal year, so the dollar/yen pair is likely to trade with a heavy

topside.

Omi

100.50

–

104.50

Dollar buying will pick up again as the risk-off mood recedes, but there is a lack of factors capable of pushing the

dollar higher. As a result, the greenback will be sold-back when it hits highs at the 104 yen level.

(As of January 31)

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 7

Daisuke Karakama, Masakatsu Fukaya, Yuki Yamazaki, Market Economists, Forex Division

Euro – February 2014

1. Review of the Previous Month

In January, the euro/dollar pair dropped back from its end-of-year high around $1.38 to float in a range

between $1.35–1.37.

After opening the month at the upper-$1.37 mark, the pair plummeted to around $1.36 due to:

dollar buying on the back of high U.S. interest rates; and an unwinding of the positions built up at the

end of 2013. Despite a downswing in the U.S. Non-Manufacturing ISM Report on Business for

December (released January 6) and firm European stock movements, the pair fell further to hit the

mid-$1.35 level. This was down to dollar buying as the markets reacted warmly to: the significant

upswing in the U.S. November trade balance (released January 7); the December U.S. ADP

employment statistics (January 8); and the release of the FOMC minutes. During this time, the single

currency also fell to around 142 yen against its Japanese counterpart. With the ECB Governing Council

meeting looming, the euro/dollar pair rallied to the lower-$1.36 level on January 9, but it dropped back

to the lower-$1.35 mark after ECB President Mario Draghi spoke emphatically about forward guidance

in his press conference after the meeting. The dollar then fell sharply on January 10, though, after the

U.S. employment data for December fell significantly below market expectations. The euro bounced

back to the upper-$1.36 level against the greenback and the lower-143 yen mark against the Japanese

unit.

The trend continued into the next week and the euro/dollar pair strengthened to around $1.37 on

January 14. The euro/yen pair then rose to the lower-142 yen mark on the back of yen bearishness.

This also provided a boost to the euro/dollar pair, which continued trading firmly at the upper-$1.36

mark. However, this trend reversed on January 15. Speculation over further easing by the ECB

increased after Germany’s GDP growth rate for 2013 swung downwards. The dollar was bought during

this time on the back of some buoyant U.S. indicators. As a result, the euro/dollar pair dropped to the

lower-$1.35 level on January 17, with the euro/yen pair also falling to the lower-141 yen mark.

Amid a dearth of new factors, on January 20 the euro temporarily hit monthly lows of $1.3508 and

140.33 yen against the U.S. and Japanese units. The euro/dollar pair continued to trade with heavy

topside around the mid-$1.35 mark thereafter. It then shot up to the mid-$1.36 level, though, when euro

buying intensified after the markets reacted warmly to a (preliminary) eurozone PMI for January

(released January 23) hitting its highest level for 32 months. The pair temporarily hit a monthly high of

$1.3740 towards January 24 as dollar selling accelerated on the back of falling U.S. interest rates.

Emerging markets were rocked towards January 29 when the Argentine peso crashed. The shockwaves

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 8

subsided for a time when Turkey’s central bank hiked interest rates sharply, but risk aversion remained

strong and the euro was sold as a result, with the euro/dollar pair dragged to the lower-$1.36 mark by a

bearish euro/yen pair. Moves away from the single currency intensified on January 30 after the markets

reacted badly to the poor results of the German CPI data for January, with the euro/dollar pair

weakening to the mid-$1.35 level. This trend continued thereafter and the pair remained at this level

towards January 31.

130

132

134

136

138

140

142

144

146

1.33

1.34

1.35

1.36

1.37

1.38

1.39

13/10 13/11 13/12 14/01

(JPY)(USD) EUR/USD EUR/JPY

2. Outlook for This Month:

The ECB Governing Council meeting

Expected Ranges Against the US$: US$1.3400–1.3800

Against the yen: JPY137.00–144.00

The euro is expected to move bearishly in February.

The euro/dollar pair traded with a heavy topside when it gained to around $1.38. With

U.S./European interest-rate differentials also widening, the pair was substantially adjusted down to the

$1.36 mark entering 2014. Dollar buying then eased off, though, as the December U.S. employment

data swung downwards and U.S. interest rates peaked out. As a result, the pair is now trading without a

clear sense of direction. As expected, the ECB Governing Council decided to maintain the status quo

when it met on January 9, but in his press conference after the meeting, ECB President Mario Draghi

strengthened his forward guidance by saying that “we firmly reiterate our forward guidance that we

continue to expect the key ECB interest rates to remain at present or lower levels for an extended

period of time.”

Under these circumstances, February may well see some changes. A lot will depend on the results

of the ECB Governing Council meeting scheduled for February 6. With regards to the outlook for ECB

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 9

monetary policy, since the end of the year we have been saying that “it wouldn’t be at all strange if

something happens at some point.” It is growing more likely, though, that the ECB will need to

implement some further easing. Draghi spoke about the triggers for ECB action, one being “an

unwarranted tightening of the short-term money markets” and the other “a worsening of our

medium-term outlook for inflation.” With regards to the former, the situation has certainly worsened

since the last meeting on January 9. At that time, the Euro Overnight Index Average (EONIA) stood at

0.16%. On January 16, it topped the ECB’s benchmark rate (0.25%) and rose close to 0.30%. It then hit

0.35% on January 20. It has since dropped to around 0.18% due to an injection of funds after the ECB

carried out a 1-week refinancing operation on January 21. Nonetheless, it remains 2bp above its level

at the time of the last meeting and is now 10bp higher compared to its average level up until last

summer when concerns of rising interest rates began sweeping the markets.

If this rise reflects a decline in excessive liquidity because banks are making early repayments of

the funds borrowed under the Long Term Refinancing Operation (LTRO), then EONIA will face more

upwards pressure from hereon as repayments continue. This is something the ECB will need to keep a

close eye on. Turning to inflation, though, and the eurozone CPI data for December revealed that core

inflation had only risen by 0.7% year-on-year, a record low. However, some say this is down to

technical factors, so it is too early to conclusively say the mid-term outlook is worsening.

Under the aforementioned circumstances, if the ECB does make a move, it probably has three

choices at this moment in time, namely (1) a strengthening of forward guidance, (2) policy rate cuts

(possibly to negative territories) or (3) a Long Term Refinancing Operation (LTRO). Judging from

recent statements by ECB officials, though, the ECB is likely to try strengthening forward guidance

first of all. The ECB seems quite cautious with regards to the idea of another LTRO. Even if one is

implemented, it will probably be directed towards lending to the private sector only and will likely be

introduced in the latter half of the year, after the results of the stress tests are released.

At the same time, the euro has been adjusted down to $1.36, while some data is pointing to an

economic recovery within the eurozone, so the ECB is likely to postpone any further easing for now.

Even if this is the case, though, the ECB meeting will probably strike a dovish tone, just like it did in

January. As a result, the markets will continue to speculate over further easing, and this will act to push

the euro lower.

The euro/dollar pair could be bolstered if the greenback moves with a heavy topside on the back of

uncertainty about the U.S. economy. It might also receive a fillip from a healthy supply and demand

environment (the eurozone current account surplus is now at record highs, while funds will flow back

into the zone in advance of the stress tests). The supply and demand situation seems particularly tilted

towards euro buying and this could help market participants feel more relaxed about purchasing the

single currency. This will help underpin the unit’s downside.

In light of the above, the euro/dollar pair is likely to float up and down in February while gradually

edging lower. However, if the ECB takes an aggressive easing stance by cutting interest rates and so on,

the single currency may well drop even further, so caution will be necessary.

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 10

Dealers' Market Forecast

(Note: These opinions do not necessarily agree with the other contents of this report.)

Bullish on the euro (5 bulls: 1.3400–1.4000, Core: 1.3500–1.3900)

Fujisaki

1.3400

–

1.4000

The euro is expected to move firmly on the back of a ballooning current account surplus and expectations for fund

repatriations into the eurozone. If emerging-economy currencies fall further, expectations for fund repatriations

could grow even stronger. There are still concerns about the economic situation in southern Europe and the quality

of the assets held by Europe’s financial institutions, but these will be offset by the healthy supply and demand

situation.

Yamashita

1.3500

–

1.3900

The German economy remains strong, so the euro will probably be sought as concerns about emerging economies

grow stronger. Furthermore, Sabine Lautenschläger, the hawkish vice president of the Bundesbank, has joined the

ECB’s executive board. She could challenge the strong easing stance of some of the ECB’s more dovish

members. All in all, the euro is expected to move firmly in February.

Sato

1.3500

–

1.4000

The euro will trade firmly on the back of the eurozone’s ballooning trade surplus. If the situation remains unstable

in the emerging economies, funds will probably flow back into the eurozone. This is also likely to bolster the

single currency.

Nishijima

1.3500

–

1.3900

The euro will be bought for a time as risk aversion increases due to the unstable situation in the emerging

economies. The economies of Germany and other European nations are currently swinging upwards, so the single

currency will continue to trade firmly.

Inoue

1.3600

–

1.3900

The ECB Governing Council strengthened its forward guidance when it met in January, but the impact on the

currency markets was negligible. With the eurozone maintaining a trade surplus for about a year now, the euro is

likely to continue moving firmly due to supply and demand factors.

Bearish on the euro (7 bears: 1.3200–1.3800, Core: 1.3300–1.3780)

Kato

1.3300

–

1.3800

The negative impact of euro appreciation is gradually starting to make itself felt on the eurozone’s economy.

Funds are being repatriated into the eurozone in advance of the stress tests, but when this trend cools off, the

markets will probably react by selling the single currency.

Noda

1.3300

–

1.3800

The end of 2013 saw a round of fund repatriations, with the euro rising as a result. However, this trend will cool

off in February. Concerns about the situation in the emerging economies will also see a slight increase in risk

aversion, so the euro will face downwards pressure this month.

Yano

1.3400

–

1.3800

At its January meeting, the ECB Governing Council discussed a continuation of forward guidance and the

possibility of further easing. On the other hand, the U.S. has commenced tapering and the next policy change

looks set to be an interest rate hike. The divergence in these policy stances is likely to weigh down the euro’s

topside.

Takada

1.3200

–

1.3800

The euro will trade with a heavy topside on the back of QE tapering in the U.S. If the markets focus on the

eurozone’s moribund economic indicators, this could lead to a euro sell off, with the single currency crashing, so

caution will be necessary.

Omi

1.3400

–

1.3700

The euro/dollar pair is probably no longer attractive to buyers as the pound is making gains and the dollar/yen

pair’s topside is growing heavier. The pair will continue to trend downwards and its downside will edge lower.

Toriba

1.3300

–

1.3800

The euro is moving firmly at the moment on the back of: the eurozone’s healthy trade surplus; and fund

repatriations by financial institutions in advance of the stress tests. However, Europe’s fundamentals show no

signs of any overarching recovery, while the gap between ECB and FRB monetary policies remains large. The

euro’s room on the topside will remain capped.

Shimoyama 1.3400 The ECB has reiterated its intentions to remain on the easing path. At the same time, though funds have been

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 11

–

1.3800

flowing back into the eurozone in advance of the bank stress tests, this trend is cooling down. As a result, the euro

is likely to face downwards pressure this month. With the dollar also expected to strengthen, the discrepancy

between the two currencies will see the euro/dollar pair trending downwards.

(As of January 31)

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 12

Katsuhiko Takahashi, Americas Treasury Division

Canadian Dollar – February 2014

1. Review of the Previous Month

The beginning of the month was marked by an unwinding of the trends that occurred in the latter half

of 2013, with European currencies like the euro, pound and Swiss franc all being sold off. During this

time, commodity currencies like the Canadian and Australian dollars were bought back, with the U.S.

dollar/Canadian dollar pair gaining to the mid-C$1.06 mark. The greenback was then bought against

the major currencies after the U.S. November trade deficit shrunk by more than expected. With Canada

also posting a larger-than-expected trade deficit and the Canadian Ivey Purchasing Managers Index

dropping to its lowest level since 2009, the U.S. unit was bought and the Canadian unit sold. The

Canadian dollar was also hit by the ongoing slump in crude oil prices. All of this saw the currency pair

gaining to the mid-C$1.07 mark. Thereafter, the much-anticipated U.S. December employment data

turned out to be significantly down on market expectations. However, Canada’s December

employment data (released on the same day) also posted a substantial fall in the number of people in

work, while the unemployment rate rose sharply from 6.9% to 7.2%. As a result, though the greenback

was sold across the board at this time, it actually gained on its Canadian counterpart, with the currency

pair rising to the lower-C$1.09 level.

The loonie was bought back mid-January, with the pair dropping down to around C$1.0850.

However, it slide was halted and it bounced back to C$1.0989 after Bank of Canada governor Stephen

Poloz commented that low inflation was the bank’s largest concern and there remained uncertainty

about the U.S. economic recovery.

U.S. long-term interest rates rose in the latter half of the month after some news agencies reported

that the next FOMC meeting would announce a further reduction in the amount of asset purchases. The

U.S. dollar strengthened as a result, with the currency pair hitting C$1.10. The January 22 Bank of

Canada Monetary Policy Committee (MPC) meeting decided to keep the policy rate fixed. The

accompanying statement said the direction of monetary policy from here on would be decided by the

data, but it also lowered its outlook for inflation in 2014. This served to rouse market speculation about

interest rate cuts. The Canadian dollar saw more selling in the wake of the statement, with the currency

pair jumping from close to C$1.0970 to around C$1.1090. As concerns about the emerging economies

increased thereafter, yields on U.S. treasuries fell and the Canadian unit was bought back for a time.

However, the FOMC then decided to implement more QE tapering, so the Canadian dollar came under

pressure from the difference between U.S. and Canadian monetary policies. As a result, the pair

temporarily hit C$1.1199, its highest level in 54 months, to finish the month trading at highs.

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 13

90

92

94

96

98

100

1.02

1.04

1.06

1.08

1.1

1.12

13/10 13/11 13/12 14/01

(JPY)(CAD) USD/CAD CAD/JPY

2. Outlook for This Month:

U.S./Canadian interest-rate differentials; and the movements of emerging-economy currencies

Expected Ranges Against the US$: C$1.0800–1.1670

Against the yen: JPY87.00–97.00

The U.S. has commenced QE tapering. If the U.S. economy recovers, speculation may well grow about

an early interest rate hike. This speculation is likely to lead to U.S.-dollar buying in the currency

markets. At the same time, the markets are growing more sensitive to the release of bearish Canadian

economic indicators, so Canadian interest rates may well come under downwards pressure. Shrinking

U.S./Canadian interest rate differentials are becoming a factor pushing the Canadian unit down against

its U.S. counterpart. However, inflation in the U.S. is moving stably at low levels. Furthermore, the

FRB is usually quite cautious about the idea of an interest rate hike, so the FRB’s low-interest policy

looks set to continue for now. On the other hand, the Canadian unit’s weakness is helping exports and

is also leading to inflationary pressure within Canada, so this shrinkage of U.S./Canadian interest rate

differentials will gradually ease off. Canada’s economy is strongly dependent on the U.S. economy, so

the U.S. economic recovery will act to support the loonie in the long term. However, the markets will

remain fixated on the movements of emerging-economy currencies. The Canadian dollar does not have

any particular correlation with these movements. Nonetheless, until the markets regain composure,

interest rate movements and economic trends are unlikely to have much of an impact on the U.S.

dollar/Canadian dollar pair.

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 14

Kenji Nakajima, Europe Treasury Division

British Pound – February 2014

1. Review of the Previous Month

The pound swayed up and down in January, but on the whole it traded flatly against the dollar and fell

against the yen.

The beginning of the month was marked by concerns of an economic slowdown in China following

the bearish results of a Chinese manufacturing indicator. With export-related stocks and so on sliding

across Europe, the euro edged lower and the pound was also pulled downwards. Due to UK’s own

independent factors, such as a worse-than-expected Manufacturing PMI for December (market

expectations – 58.4; result – 57.3), the pound/dollar pair dropped from around $1.66 to around $1.64

towards January 3. During this time, the pound/yen pair fell from the upper-174 yen mark to around

171 yen.

The second week saw the yen strengthening on January 6 as risk tolerance levels declined when:

the Nikkei Average plunged temporarily by over 400 yen; and the China HSBC/Markit Services PMI

for December weakened on the previous month. The dollar/yen pair fell from around 105 yen to the

lower-104 yen mark, with sterling subsequently falling to the mid-170 yen mark and the mid-$1.63

level against its Japanese and U.S. counterparts, respectively. However, stocks then stopped sliding and

the dollar/yen pair was bought back to the upper-104 yen mark. As a result, the pound/yen pair was

dragged up to around 172 yen, while the pound/dollar pair also rallied to the lower-$1.64 level. The

dollar was sold again thereafter when the U.S. Non-Manufacturing ISM Report on Business for

December fell below expectations, with the report’s New Orders Index dropping to its lowest level

since May 2009. U.S. stock markets fell and the yen was bought, with the dollar/yen pair sliding to

around 104 yen. The pound/yen pair also dropped back to the mid-170 yen mark at this time. Hopes for

a global economic recovery grew on January 8 following the previous day’s U.S. exports growth and

improvements in the German jobs market. As Japanese stocks moved firmly, the dollar/yen pair gained

to around 105 yen and the pound/yen pair followed suit by rising to the mid-172 yen mark. The

euro/pound pair dropped from around GBP0.83 to the lower-GBP0.82 mark (euro bearishness/pound

bullishness) towards January 9, the date of the ECB Governing Council meeting. This slide was down

to the different levels of business confidence in the eurozone and the UK together with a divergence in

the monetary policies of the two areas (the pound was marked by strong expectations for an early

interest rate hike, while the euro continued to face speculation over further easing). This saw the pound

gaining to around $1.65 against the greenback. The pound/yen pair was also dragged higher to hit the

lower-173 yen mark on January 9. The UK November Industrial and Manufacturing Production figures

were released on January 10. The figures dropped below market forecasts and sterling reacted by

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 15

dipping to around $1.64 against the dollar and the lower-172 yen mark against the Japanese unit. The

U.S. employment data for December was then released. The unemployment rate had dropped to 6.7%,

its lowest level since October 2008, and this saw the pound/dollar pair temporarily dropping to the

upper-$1.63 mark. However, nonfarm payrolls only grew by 74,000, the lowest gain since January

2011. As a result, the pound/dollar pair strengthened to around $1.65. As risk tolerance levels declined,

the yen was bought and the pound/yen pair temporarily slid to the lower-171 yen level. However, it

was then pulled back to the mid-172 yen mark by a bullish pound/dollar pair.

The yen market saw more adjustment on January 13 as risk tolerance levels continued falling on the

back of significantly-worse-than-expected U.S. nonfarm payroll results for December released on

January 10. As the dollar/yen pair dropped from around 104 yen to the upper-102 yen mark, the

pound/yen pair also weakened to the mid-168 yen level. The pound/dollar pair was pulled down by the

pound/yen pair’s slide to hit the mid-$1.63 mark. The dollar/yen pair then strengthened to around 104

yen on January 14 due to: real-demand dollar buying; and the firm results of the U.S. retail sales data

for December. During this time, the pound/yen pair also bounced back to the mid-171 yen mark. The

UK then released its CPI data for December. Inflation was up 2.0% year-on-year. This was below the

Bank of England’s target and expectations grew that inflation would remain capped going forward. As

anticipation for an early rate hike receded, the pound/dollar pair moved somewhat bearishly for a time,

though it soon rallied to the mid-$1.64 mark on the back of the firm movements of the pound/yen pair.

On January 15, the pound/dollar pair dropped back to the lower-$1.63 level in the wake of the buoyant

results of the NY FRB Manufacturing Index for January. The markets received a surprise on January

16 when the U.S. January Insured Unemployment Rate topped 3 million. The dollar/yen pair reacted

by dropping from the upper to the lower-104 yen mark. During this time, the pound/yen pair also fell to

the mid-170 yen level. The UK retail sales figures for December were posted on January 17. They

significantly outperformed market expectations and this saw the pound/dollar pair gaining to the

mid-$1.64 mark, while the pound/yen pair also rallied to the upper-171 yen mark.

The ILO UK unemployment rate for September–November was released on January 22. The rate

had fallen to 7.1%, below market expectations for 7.3%. This was close to the 7.0% target that the

BoE’s forward guidance said would trigger discussions about an interest rate hike. Sterling

strengthened across the board and the pound/dollar pair also gained to the upper-$1.65 mark. January

23 saw the release of the better-than-expected results of the January French Manufacturing and

Services PMIs and the January German Manufacturing PMI (all three were preliminary results). As a

result, the euro/dollar pair rose from the mid-$1.35 level to the mid-$1.36 mark. The pound/dollar pair

was also dragged higher to hit the lower-$1.66 mark. In an interview in a UK newspaper on January 24,

Martin Weale, a member of the BoE’s Monetary Policy Committee (MPC), said he did not agree with

the idea of lowering the 7% unemployment rate threshold contained in the BoE’s forward guidance.

The pound/dollar pair reacted by hitting the upper-$1.66 level. However, BoE Governor Mark Carney

then stated at the World Economic Forum in Davos that there was no pressing need for a rate hike, so

the pair dropped back below $1.65. The pound/yen pair opened the week at the lower-171 yen mark

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 16

and maintained its upwards momentum to hit the mid-173 yen level on January 23. China and the U.S.

then released some bearish economic indicators, though. At the same time, after Argentina’s foreign

currency reserves plummeted, the country’s central bank decided to stop intervening to buy the peso.

As a result, the peso was sold off sharply, soon followed by the currencies of other emerging

economies. Naturally, investor risk tolerance levels took a nosedive. As stocks fell across the globe, the

yen was bought, and with BoE Governor Mark Carney pouring cold water on expectations for an early

BoE rate hike, the pound/yen pair broke below 169 yen towards January 24.

On January 27, it was revealed that China Credit Trust, a Chinese trust fund, had reached an

agreement with investors after previously having difficulties meeting repayments on a high-yield trust

product. It now seemed the Chinese shadow banking sector would avoid a default, so the risk-evasive

yen buying seen at the end of the previous week now cooled off. On January 28, the Turkish central

bank convened an emergency monetary policy committee meeting. It declared it would take whatever

measures were needed to stabilize prices. The Turkish lira had plunged to record lows against the

dollar, but it now rallied somewhat. This also contributed to yen selling, with the pound/yen pair

rallying to the mid-170 yen level. The pound/dollar pair was also dragged higher to hit the upper-$1.65

mark. The UK GDP data for October–December was released on January 28. GDP was up 0.7% on the

previous quarter. This was essentially in accord with market expectations for a 2.8% q-o-q rise. The

pound/dollar pair had weakened for a time from the lower-$1.66 mark to the lower-$1.65 level. This

was due to a bout of selling to lock-in profits now a number of economic indicators had been released.

With growth up for the fourth successive quarter, though, the GDP data seemed to confirm the UK

economy’s ongoing recovery, so the pair soon bounced back. It then moved in a range around the

upper-$1.65 mark. At the emergency MPC meeting on January 28, Turkey’s central bank had reached

a decision to hike all its main policy rates sharply. As a result, risk appetite increased on January 29

and the pound/yen pair gained to the mid-171 yen level. However, the Turkish lira and other

emerging-economy currencies were sold off again, so the pound/yen pair weakened on the back of risk

aversion. South Africa’s central bank also hiked policy rates thereafter, but the size of the hike was

seen as insufficient, so risk-aversive movements continued. Many European banks have invested funds

into the emerging economies, which partly explains why the euro and pound was sold during this time.

BoE Governor Mark Carney then reiterated that a stronger economic recovery was needed before the

BoE implemented monetary tightening. He also said an interest rate hike was not on the cards in the

near future. As a result, the pound/yen pair dropped to the lower-168 yen mark towards January 30,

while the pound/dollar pair also weakened to the mid-$1.64 level.

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 17

154

156

158

160

162

164

166

168

170

172

174

176

1.58

1.6

1.62

1.64

1.66

1.68

1.7

13/10 13/11 13/12 14/01

(JPY)(USD) USD/GBP GBP/JPY

2. Outlook for This Month:

The possibility that forward guidance will be strengthened; the inflation outlook; and concerns about emerging economies

Expected Ranges Against the US$: US$1.6200–1.6700

Against the yen: JPY165.00–174.00

The pound is expected to trade with a heavy topside in February. The UK’s (ILO) unemployment rate

has plummeted, while the 2013 GDP growth rate hit a six-year high (up 1.9%) and the economy seems

to be recovering steadily. The UK is also likely to post some firm economic indicators this month, too.

However, prices are moving stably, while BoE Governor Mark Carney and other top BoE figures have

clearly expressed caution about the idea of an early interest rate hike, so market expectations for such a

hike are being capped accordingly. The February 6 BoE Monetary Policy Committee (MPC) is likely

to strengthen forward guidance, while the Quarterly Inflation Report (released February 12) is also

expected to downgrade the inflation outlook. As a result, even if the UK does post some robust

economic indicators this month, any pound appreciation will be limited in nature. Furthermore, the

Turkish lira and South African rand remain unstable, despite last month’s emergency MPC meetings

and the unexpected interest rate hikes, so there are still concerns about the emerging economies. Many

European banks have invested funds into these economies, so investors may well adopt risk-aversive

stances with regards to European currencies. Under these circumstances, the pound is likely to trade

with a heavy topside in February.

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 18

Tomohiro Yamaguchi, Singapore Treasury Department

Singapore Dollar – February 2014

1. Review of the Previous Month

The Singapore dollar moved bearishly in January on the back of continued speculation over U.S.

quantitative easing as well as the worsening outlook for the Chinese economy.

The FRB finally decided to implement QE tapering mid-December. The Singapore unit

subsequently weakened against its U.S. counterpart in the latter half of December. When the RMB

began rising towards the end of the year, though, the Singapore dollar was also dragged higher to

approach the New Year trading at the lower-S$1.26 mark against the greenback. On January 2, though,

Singapore posted some worse-than-expected GDP figures for October–December, with GDP falling an

annualized 2.7% from the previous quarter. With China’s Manufacturing PMI for December also

dropping below forecasts, the mood from the end of the year suddenly darkened, with the Singapore

dollar sliding as a result. On January 7, the unit broke below its recent low against the U.S. dollar to hit

S$1.27 for the first time since September last year. It then fell to close to the mid-S$1.27 level on the

back of: the buoyant results of the December U.S. ADP employment statistics, released on January 8;

and high hopes with regards to the U.S. employment data, due for release on January 10. The actual

employment results confounded these hopes, though, with nonfarm payrolls increasing at their lowest

rate for around three years. This saw the greenback moving bearishly across the board, with the

Singapore dollar also shooting back up to the lower-S$1.26 mark.

As the markets began to take in the previous week’s shocking U.S. employment data, speculation

grew that the results would not affect the schedule for QE tapering. This saw the U.S. unit bouncing

back and the Singapore dollar weakening again. The same week saw the release of a number of U.S.

economic indicators, some good and some bad. However, the U.S. did post some robust retail sales

data for November and a healthy January Philadelphia FRB Manufacturing Index. This stoked

speculation that the GDP data for October–December would be revised upwards when it was released

at the end of the month.

In the week beginning January 20, Asian currencies continued moving bearishly against the dollar

on the back of speculation that the FOMC would implement some more QE tapering. Even Singapore,

with its comparatively healthy fundamentals, saw its currency adjusted downwards on successive days.

The China HSBC Manufacturing PMI data for January (released on January 23) then dropped below

50 (the key level for determining whether the economy is expanding or contracting) for the first time in

six months. The evening of January 23 also saw an Argentine peso crash after Argentina’s central bank

decided to stop intervening to buy the unit. As risk aversion intensified, the Singapore dollar dropped

to the lower-S$1.28 mark, its lowest level since August 2013.

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 19

Concerns about emerging economies eased off the following week and the markets slipped into

wait-and-see mode in advance of the FOMC meeting. During this time, the Singapore dollar returned

to the lower-S$1.27 mark. At the much-anticipated meeting on January 29, the FOMC announced

some further QE tapering. This was in line with expectations, but with long-term U.S. dollar interest

rates dropping down to levels last seen in November, the Singapore unit was not sold like it had been

directly after the December FOMC meeting. However, Turkey, South Africa and emerging markets in

South and Central America began struggling once again, so risk aversion remained in place. Under

these circumstances, the Singapore dollar moved with a lack of direction to trade in a range around

S$1.27 in advance of the Chinese New Year holidays.

77

78

79

80

81

82

83

84

1.23

1.24

1.25

1.26

1.27

1.28

1.29

13/10 13/11 13/12 14/01

(JPY)(SGD) USD/SGD SGD/JPY

2. Outlook for This Month:

The Singapore unit will continue to trade bearishly against the U.S. dollar, though it could move firmly against other Asian currencies

Expected Ranges Against the US$: S$1.2600–1.2900

Against the yen: JPY78.50–81.50

The Singapore unit will continue to move bearishly in February on the back of the U.S. economic

recovery and the instability in the emerging markets. However, its room on the downside will probably

be capped.

Singapore’s sound fundamentals make the Singapore unit more attractive than other Asian

currencies, yet it still weakened last month due to position unwinding. Observers had estimated that the

Singapore dollar’s nominal effective exchange rate (NEER) was moving at the top of the Monetary

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 20

Authority of Singapore’s policy band, but it seems the NEER dropped back closer to the policy band’s

central value at the end of January. This is turn suggests that market participants have now unwound

their positions to a certain extent. The beginning of February will be marked by a lack of movement

due to the Chinese New Year holidays. As a result, the Singapore unit is likely to kick off the month

fluctuating gently around its end-of-January levels. After that, though, it will probably move bearishly

against the greenback due to: U.S. dollar bullishness on the back of QE tapering; and instability in the

emerging economies after some emerging-market currencies suffered sharp falls. However, once a

round of position adjustments is out of the way, the Singapore dollar will once again be regarded as a

stable currency, so it may start trading firmly again, especially against other Asian currencies.

Singapore’s December CPI data only rose 1.5% year-on-year, its lowest growth in eight months.

The main reason for this fall, though, was a dip in the price of vehicle Certificates of Entitlement

(COEs). Inflationary pressures remain strong due to a tight labor market, so the recent CPI slide is

unlikely to prompt the MAS to change its policy of guiding the Singapore unit higher. Based on the

aforementioned circumstances, the Singapore dollar’s downside will probably be capped in February.

Singapore economic indicators to watch out for this month include the January export statistics

(February 17), the final October–December GDP data (February 21) and the January CPI data

(February 24).

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 21

Hiroshi Seki, Bangkok Treasury Department

Thai Baht – February 2014

1. Review of the Previous Month

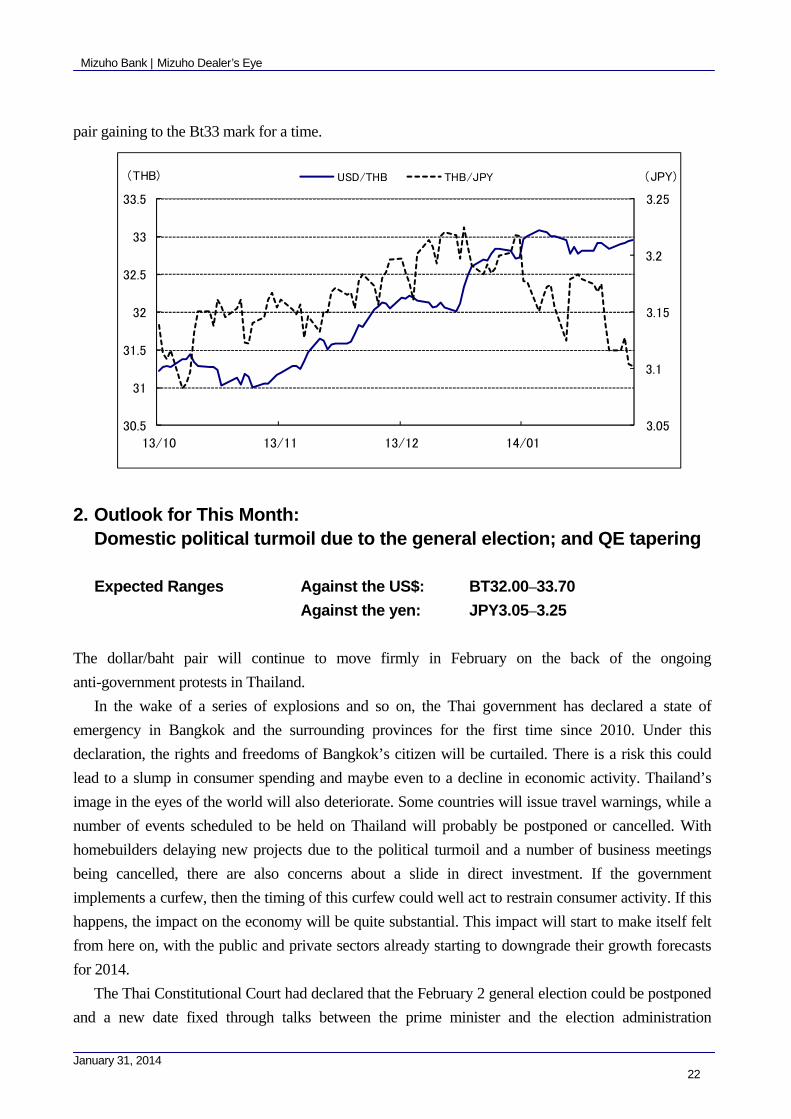

The baht hit a four-year low in January.

The dollar/baht pair kicked off the month trading at Bt32.82 on January 2. At the beginning of the

year, Suthep Thaugsuban, the leader of the anti-government protesters, announced a series of

large-scale demonstrations in Bangkok, beginning on January 13. As a result, the Thai SET Index

plummeted and the pair shot up at the start of trading. As political instability continued, the markets

then switched into risk-off mode on January 6 after the China HSBC Services PMI for December fell

sharply on the previous month. All of this saw the pair rising to Bt33.15 whilst activating stop losses.

This was its highest level since February 2010. There was some adjustment thereafter, but concerns

about the upcoming demonstrations saw the pair moving firmly at the Bt33 mark.

On January 10, the U.S. released some worse-than-expected employment data for December. The

greenback was sold and the currency pair dropped to the Bt32 mark. Though the anti-government

protestors blocked off a major Bangkok intersection on January 13, the markets were relieved things

did not turn violent, so overseas investors moved to buy back Thai stocks. As this trend continued,

intermittent dollar selling by a major exporter saw the pair plunging to Bt32.70 on January 14. Prime

Minister Yingluck Shinawatra then affirmed that the general election would not be postponed and

would go ahead as planned on February 2. This saw the pair recovering temporarily to Bt32.90.

Exporters continued to sell the dollar, though, while the baht was also bought back due to falling U.S.

long-term interest rates. As a result, the pair hit a monthly low of Bt32.66 on January 17.

However, the baht slid downwards again after several people were injured on January 17 and

January 19 when bullets were fired at anti-government demonstrators. The Thai government declared a

state of emergency on January 21. This saw the currency pair rallying to the Bt33 level on January 22.

The Bank of Thailand’s Monetary Policy Committee (MPC) then met and defied expectations for an

interest rate cut by keeping policy rates fixed. The Thai unit was bought back and the pair dropped

once again to Bt32.80. Towards the end of the month, though, the markets switched decisively into

risk-off mode amid a crash in the value of the Argentine peso and concerns of a Chinese economic

slowdown. All of this meant the currency pair continued to move in narrow range of Bt32.80–90 in

advance of the FOMC meeting.

On January 28, Prime Minister Yingluck Shinawatra reiterated that the general election would go

ahead as planned on February 2. As political tensions boiled up, the dollar/baht pair strengthened

temporarily to around Bt32.95. As expected, the January 29 FOMC meeting decided to taper asset

purchases to the tune of $10 billion a month. Falling U.S. stocks and risk aversion saw the currency

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 22

pair gaining to the Bt33 mark for a time.

3.05

3.1

3.15

3.2

3.25

30.5

31

31.5

32

32.5

33

33.5

13/10 13/11 13/12 14/01

(JPY)(THB) USD/THB THB/JPY

2. Outlook for This Month:

Domestic political turmoil due to the general election; and QE tapering Expected Ranges Against the US$: BT32.00–33.70

Against the yen: JPY3.05–3.25

The dollar/baht pair will continue to move firmly in February on the back of the ongoing

anti-government protests in Thailand.

In the wake of a series of explosions and so on, the Thai government has declared a state of

emergency in Bangkok and the surrounding provinces for the first time since 2010. Under this

declaration, the rights and freedoms of Bangkok’s citizen will be curtailed. There is a risk this could

lead to a slump in consumer spending and maybe even to a decline in economic activity. Thailand’s

image in the eyes of the world will also deteriorate. Some countries will issue travel warnings, while a

number of events scheduled to be held on Thailand will probably be postponed or cancelled. With

homebuilders delaying new projects due to the political turmoil and a number of business meetings

being cancelled, there are also concerns about a slide in direct investment. If the government

implements a curfew, then the timing of this curfew could well act to restrain consumer activity. If this

happens, the impact on the economy will be quite substantial. This impact will start to make itself felt

from here on, with the public and private sectors already starting to downgrade their growth forecasts

for 2014.

The Thai Constitutional Court had declared that the February 2 general election could be postponed

and a new date fixed through talks between the prime minister and the election administration

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 23

commission. As a result, Prime Minister Yingluck Shinawatra discussed the issue with the commission.

At one point it seemed the election might be postponed, but in the end it was decided to stick to the

February 2 date. Citing the security situation, the electoral authorities had called for a postponement,

but the government side rebuffed this suggestion. During the negotiations, anti-government factions

protested outside the meeting venue. Shots were fired and two of the protesters were injured. In the

wake of the decision not to postpone the election, Suthep Thaugsuban, the leader of the anti-Thaksin

faction, declared he would do whatever it took to stop the election going ahead. Demonstrations look

set to heat up as the election approaches. Even if the election does go ahead, there are also no signs of

the government and the protesters then reaching a compromise aimed at defusing the situation. As a

result, the domestic situation is growing more uncertain by the day.

Most observers were expecting the January 22 MPC meeting to implement a 0.25% rate cut to

prevent an economic downturn, but the MPC decided not to cut rates on the grounds that current

monetary policy was accommodative enough already. Three of the seven members had called for a

0.25% cut, but the other four had voted to maintain the status quo.

In his statement after the meeting, BoT Governor Prasarn Trairatvorakul explained the reasoning

behind the MPC’s decision. He said that although economic growth had suffered as a result of the

political turmoil that began in October 2013, current policy rate levels were supporting the economic

recovery. Furthermore, the government had only just implemented a state of emergency, so it was

difficult to predict how the political situation would develop from here on. With the reaction of the

markets also hard to gauge, he continued, it was difficult to predict what impact a rate cut would have.

It seems the MPC was also worried that if it did implement a rate cut, this would make it difficult to

implement a further cut if the turmoil was still ongoing at the time of the next meeting. At any rate,

though Prasarn decided not to cut rates for the time being, the reaction of the markets was muted, so it

seems market participants are factoring in to a certain degree a rate cut to be announced at the next

MPC meeting on March 12.

The U.S. announced QE tapering in December, meanwhile, and it now looks like the FOMC will be

discussing further cuts in asset purchases each time it meets from here on. Though the December U.S.

employment data fell significantly below expectations, the January 29 meeting nonetheless cut the

amount of purchases for the second successive month. The dollar/baht pair will be supported by

expectations for a Thai rate cut and strong ongoing demand for the greenback due to the monetary

policy shift in the U.S. The U.S. economy is slowly but steadily growing again, so the baht is unlikely

to be pulled higher by dollar-related factors in the near future. As long as the political situation in

Thailand remains tense, the currency pair thus looks set to swing upwards.

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 24

Takashi Miyachi, Singapore Treasury Department

Malaysian Ringgit – February 2014

1. Review of the Previous Month

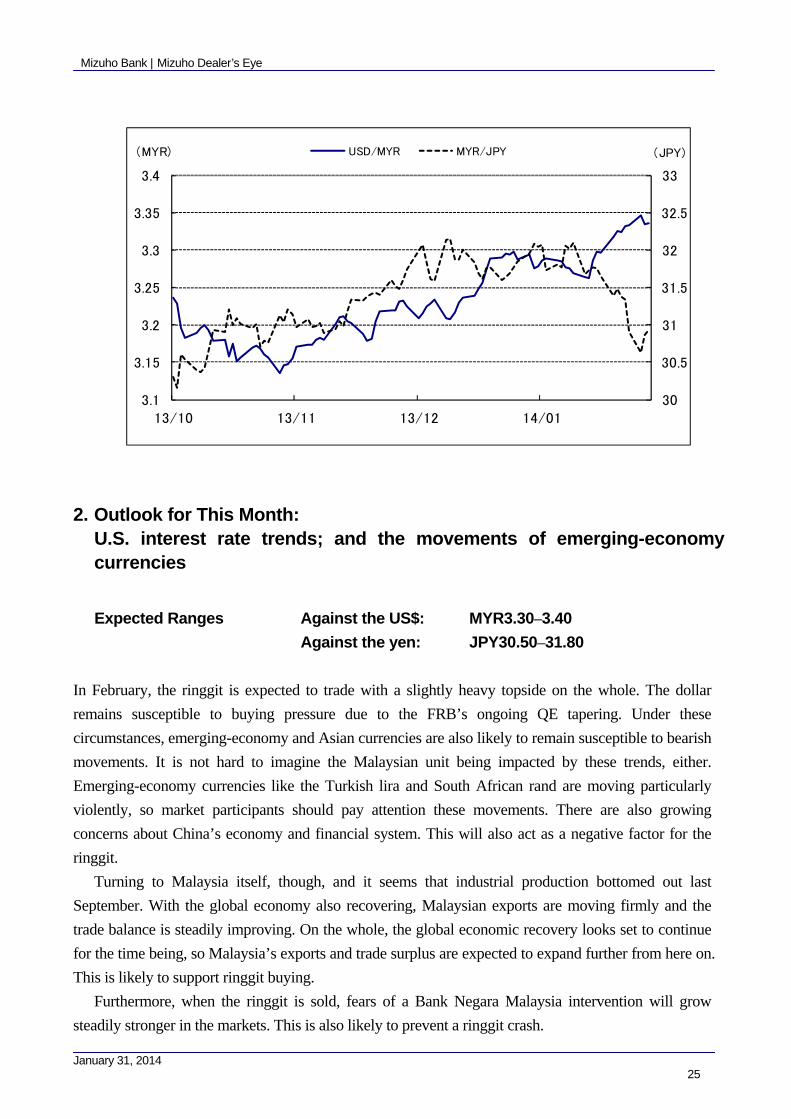

The Malaysian ringgit strengthened to around MYR3.25 from the beginning to the middle of January

on the back of dollar selling and the release of some buoyant Malaysian economic indicators. However,

it was then dragged lower as emerging-economy and Asian currencies were sold off across the board.

It hit the upper-MYR3.34 mark towards the end of the month, its lowest level since May 2010.

The ringgit opened January at the upper-MYR3.27 level against the dollar. Asian currencies then

moved bearishly on the back of the weak results of the Chinese Manufacturing PMI for December

(released January 1) and the China HSBC Manufacturing PMI data for December (released January 2).

The ringgit was also pulled down to the lower-MYR3.30 mark on January 3. As Asian currencies then

edged back upwards, the Malaysian unit moved firmly at the mid-MYR3.28 mark. Malaysia’s

November trade balance was released on January 8. At 9.72 billion ringgit, the surplus was higher than

expected. The Malaysian unit was subsequently bought to the lower-MYR3.27 level. The ringgit rose

further on January 9 following the bullish results of Malaysia’s industrial production data for

November, with the data outperforming market expectations by rising 4.4% on the previous year.

Asian currencies began trending upwards again on January 10 in advance of the release of December’s

U.S. employment data, with the ringgit also breaking below MYR3.27 to hit the mid-MYR3.26 mark.

At the beginning of the next week, on January 13, the dollar began falling on the back of the

worse-than-expected results of the U.S. December employment data, released during overseas trading

time the previous week. The dollar was sold for a time and the ringgit was bought to a monthly high of

just around MYR3.25, though dollar selling was short-lived in the end. The greenback was bought

from mid-January onwards after: the U.S. released some robust economic indicators; and the World

Bank upgraded its outlook for the global economy. As a result, the Malaysian unit edged down to the

upper-MYR3.29 level. Emerging-economy and Asian currencies continued to move bearishly from

January 20 onwards. The ringgit broke through the key MYR3.30 mark on January 20 and continued

falling on the back of concerns about an intervention by Bank Negara Malaysia, Malaysia’s central

bank. By January 27, it had dropped to the upper-MYR3.34 level. Towards the month’s end, the ringgit

was dragged below MYR3.32 for a time on the back of the turbulent movements of the Turkish lira

and other emerging-economy currencies, though it then moved bearishly again to hit the

upper-MYR3.34 level. Bank Negara Malaysia’s Monetary Policy Committee (MPC) met on January

29. Though the accompanying statement was somewhat hawkish, the MPC decided to keep policy

rates unchanged, so the impact on the markets was limited.

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 25

30

30.5

31

31.5

32

32.5

33

3.1

3.15

3.2

3.25

3.3

3.35

3.4

13/10 13/11 13/12 14/01

(JPY)(MYR) USD/MYR MYR/JPY

2. Outlook for This Month:

U.S. interest rate trends; and the movements of emerging-economy currencies

Expected Ranges Against the US$: MYR3.30–3.40

Against the yen: JPY30.50–31.80

In February, the ringgit is expected to trade with a slightly heavy topside on the whole. The dollar

remains susceptible to buying pressure due to the FRB’s ongoing QE tapering. Under these

circumstances, emerging-economy and Asian currencies are also likely to remain susceptible to bearish

movements. It is not hard to imagine the Malaysian unit being impacted by these trends, either.

Emerging-economy currencies like the Turkish lira and South African rand are moving particularly

violently, so market participants should pay attention these movements. There are also growing

concerns about China’s economy and financial system. This will also act as a negative factor for the

ringgit.

Turning to Malaysia itself, though, and it seems that industrial production bottomed out last

September. With the global economy also recovering, Malaysian exports are moving firmly and the

trade balance is steadily improving. On the whole, the global economic recovery looks set to continue

for the time being, so Malaysia’s exports and trade surplus are expected to expand further from here on.

This is likely to support ringgit buying.

Furthermore, when the ringgit is sold, fears of a Bank Negara Malaysia intervention will grow

steadily stronger in the markets. This is also likely to prevent a ringgit crash.

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 26

However, Malaysia’s December CPI data (released January 22) finally topped the 3% mark to

reach +3.2% year-on-year. Prices have been rising since the subsidy cuts last year and this is now

starting to impact the core CPI.

Malaysia has a particularly high level of household debt compared to other Asian countries, so

steadily rising inflation is expected to have a negative effect overall. Also, a large proportion of

Malaysian government bonds are in the hands of overseas investors, so if the prices of these bonds

drop due to inflation, this may see funds flowing out of Malaysia again. This in turn could also see the

ringgit trending lower once more.

Based on Malaysia’s fundamentals, the ringgit is likely to swing up and down this month, but

emerging-economy and Asian currencies will continue to be swayed by the FRB’s monetary policy. If

it becomes even clearer that the FRB is intent on normalizing monetary policy, the dollar will face even

more upwards pressure, so on the whole, the ringgit will probably edge lower again this month.

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 27

Satoshi Koizumi, PT. Bank Mizuho Indonesia

Indonesian Rupiah – February 2014

1. Review of the Previous Month

The dollar/rupiah pair opened January trading at the IDR12,200 level. It bounced back to around

IDR12,000 on January 13 in the wake of the January 10 release of the December U.S. employment

data. It moved bearishly thereafter to hit the IDR12,200 mark once again.

The beginning of January saw the release of some fairly buoyant Indonesian economic indicators.

On January 2, Indonesia posted a better-than-expected November trade surplus of $780 million. The

end-of-December foreign currency reserves were also up $2.4 billion on the previous month. However,

the Indonesian unit continued to face strong selling pressure and subsequently weakened to IDR12,285

on January 7. The U.S. posted some worse-than-expected December employment data on January 10.

This was met with dollar selling and the rupiah shot up to a one-month high around IDR12,000 on

January 13. The rupiah was then sold and the dollar/rupiah pair returned to the IDR12,200 level due to:

export settlements and other real-demand factors; some bearish Chinese economic indicators; and

growing investor concerns about emerging markets after the Argentine peso crashed (the country’s

central bank decided to stop intervening to buy the peso). At the Bank Indonesia monetary policy

committee meeting on January 9, the bank’s target rate and the FASBI overnight deposit facility rate

were kept at 7.50% and 5.75%, respectively. This was in line with most forecasts.

Stock and bond markets fluctuated violently in January. The Jakarta Stock Exchange Composite

Index opened the month at the mid-4,200 mark. It was bolstered by buying from overseas investors to

temporarily hit 4,500 points on January 23. It then dropped back to around 4,300 as stock prices fell

across the globe in the wake of the aforementioned peso crash and deteriorating Chinese economic

indicators.

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 28

0.82

0.84

0.86

0.88

0.9

0.92

10650

10950

11250

11550

11850

12150

12450

13/10 13/11 13/12 14/01

(JPY)(IDR) USD/IDR IDR/JPY

2. Outlook for This Month:

The rupiah will continue to trend downwards amid a dearth of buying factors

Expected Ranges Against the US$: IDR12,150–12,500

Against the yen: IDR116.00–123.00

The rupiah is expected to move bearishly in February, too. The unit will continue to face selling

pressure on the back of Indonesia’s current account deficit. With risk aversion flaring up due to

worsening Chinese indicators released in January or global stock market slides, the rupiah is likely to

be sold. The battle between this selling pressure and buying interventions by Bank Indonesia will

continue this month. Against this backdrop, the rupiah is expected to edge lower against the greenback.

Key economic indicators this month include the December trade balance and January inflation rate

(released February 3), the end-of-January foreign currency reserves data (release date not set) and the

Indonesian GDP growth rate for October–December (February 5). The GDP forecast is for growth in

the region of +5.6% on the same period last year. This would represent Indonesia’s lowest rate of

growth since October–December 2009 (+5.62% y-o-y). If the actual figure drops below the forecast,

this will probably be met by rupiah selling, especially considering the growing concerns about

emerging economies.

3. Topics

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 29

The impact on the rupiah due to the ban on exporting unprocessed minerals

On January 12, Indonesia instituted a ban on exports of unprocessed minerals. What impact will this

have on the rupiah?

Exports are still permitted for copper concentrates with a minimum purity of 15%, so the ban is

unlikely to affect the big exporters. Exports of nickel and bauxite are forbidden, though.

According to Bank Indonesia data, exports of nickel and bauxite amounted to around $2.1 billion in

fiscal 2012. This represented 6.7% of total mineral exports (including coal and copper) and 4% of total

exports that year. Coal accounts for around 83% of Indonesia’s total mineral export revenue (as of

fiscal 2012). Next up is copper at around 8%, followed by nickel and bauxite. Based on this data, the

slide in export revenue due to a commencement of the ban will be quite muted, so the short-term

impact on the rupiah will be modest.

Indonesia’s Coordinating Minister for Economic Affairs, Hatta Rajasa, did discuss the impact on

exports. He stated that the ban would dampen exports for a maximum of 2 years, with the Indonesian

economy suffering accordingly. Furthermore, countries heavily reliant on Indonesian mineral exports

(like Japan, which imports over 40% of its nickel from Indonesia) will be cautious about the possibility

of further export restrictions from hereon. They could decide to try reducing their dependence on

mineral imports from Indonesia, so market participants should watch closely to see how things develop

from here on.

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 30

Yasunori Sugiyama, Manila Branch

Philippine Peso – February 2014

1. Review of the Previous Month

Foreign exchange market

In 2014, the U.S. dollar/Philippine peso exchange market opened at PHP 44.35 on Thursday, January

2, roughly at the same level as the closing rate at the end of the previous year. As the U.S. dollar

remained strong, the exchange rate rose to PHP 44.66 to the U.S. dollar by Friday, January 3. In order to

keep the peso from depreciating sharply, the central bank of the Philippines placed offers in the market to

sell the U.S. dollar at the PHP 44.50 and 44.60 level on January 3. However, the central bank did not

actively intervene, and the amount of intervention was kept low. Trading closed for the week at PHP

44.65 to the U.S. dollar on January 3.

The Tokyo market opened on Monday, January 6. Even though the U.S. dollar/Japanese yen exchange

rate remained low, Asian stock markets were weakening and thus Asian currencies were dominantly sold

in the market. Following this trend, peso-selling dominated the U.S. dollar/peso exchange market as well.

Further, even though the central bank of the Philippines placed offers for the peso at the PHP

44.75–44.80 level to slow down the trend, the peso continued depreciating and reached PHP 44.85 to the

U.S. dollar by the afternoon of the same day. The central bank of the Philippines then placed orders to

sell U.S. dollar against peso at the PHP 44.75–44.80 level again on Wednesday, January 8. As the

announcement of the December employment statistics of the U.S. was coming near, there were few

market participants that would actively go against this market intervention by the central bank of the

Philippines by buying the U.S. dollar. As a result, the U.S. dollar/peso exchange rate fell to the PHP

44.60–44.70 level. In the end, trading closed for the week at PHP 44.71 to the U.S. dollar on Friday,

January 10.

The December employment statistics of the U.S. were released in the previous week on Friday,

January 10, revealing that the number of non-agricultural employees was lower than expected. In

response to this, the U.S. dollar/peso exchange market opened at PHP 44.55 on Monday, January 13 with

a weaker U.S. dollar and a stronger peso, compared to PHP 44.71 to the U.S. dollar, the closing rate of

the previous rate. There were few market participants, and there was no active trading, as the Tokyo

market was closed. The U.S. dollar/peso pair thus continued hovering around at the PHP 44.50–44.60

level throughout the day. On Tuesday, January 14, the downtrend for the Japanese yen started to recover,

as the media reported the growing current deficit of Japan, while the Nikkei Average fell remarkably.

Under such conditions, the U.S. dollar/peso exchange market saw the appreciation of the U.S. dollar

partly as a result of short-covering from the previous day. Furthermore, the U.S. dollar continued

Mizuho Bank | Mizuho Dealer’s Eye

January 31, 2014 31

appreciating on Wednesday, January 15. As a result, the peso reached PHP 45.00 to the U.S. dollar. Even

though the media announced that the November amount of OFW remittances remained at the two billion

level for the second consecutive month, the market was not impacted by this news. Although the

exchange rate almost fell below the PHP 45.00 level, the market closed without the exchange rate falling

below the PHP 45.00 level as a result of the offers placed by the central bank of the Philippines. On

Thursday, January 16, however, importers actively bought the U.S. dollar for their mid-month demands