missouri agent may-june 2011

DESCRIPTION

Missouri Agent is a bimonthly magazine published by the Missouri Association of Insurance Agents. Its target audience is the independent insurance industry, particularly member agencies of the association. This issue focuses on the annual Leadership Conference.TRANSCRIPT

Age

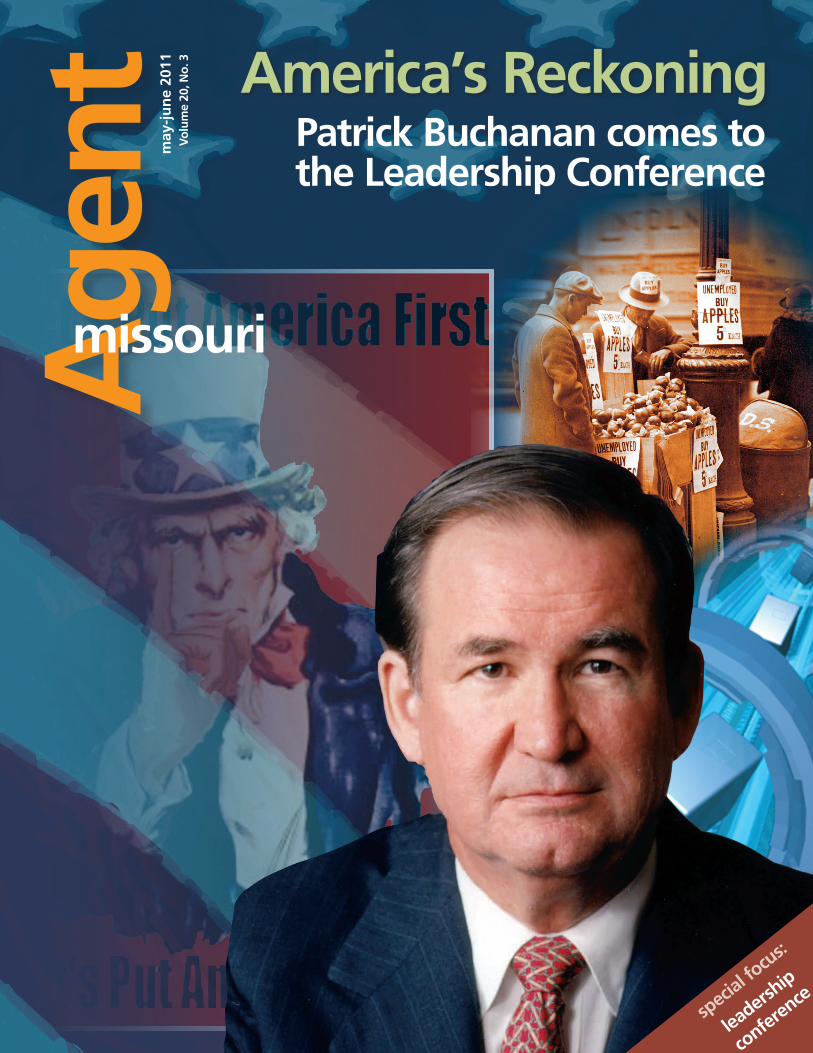

ntAmerica’s Reckoning

Patrick Buchanan comes to the Leadership Conference

missouri

spec

ial fo

cus:

leaders

hip

confer

ence

may

-ju

ne

2011

Vo

lum

e 20

, No.

3

For more details, contact your Business Development Manager or Customer Service at 1.800.442.0593 or [email protected]

The MEM DifferenceIn today’s market, the lowest price stands out. In the long-run, we believe value does. Missouri Employers Mutual has earned our 16-year reputation as the work comp market leader by offering competitive rates combined with exceptional service and a dedication to safe workplaces.

That’s a value unbeatable in any market or economic condition.

For a true work comp partner for you and your clients, contact MEM.

www.mem-ins.com

WHAT’S MISSOURI’S BEST VALUE FOR THE WORK COMP DOLLAR?

Introducing . . . www.worksafecenter.coman online tool to keep Missouri workplaces safe

may-june2011 missouriagent 3

contentsSpecial Focus: Leadership ConferenceExcerpt: Day of Reckoning by Patrick Buchanan 20The Quality Journey from Best Practices 22

The Many Faces of Insurance Issues 7What Is Trusted Choice? 12Small Agency Conference Scrapbook 24

AdvertisersAmerisafe 10BankDirect Capital Finance 28BC&M 14Big “I” Professional Liability 8Capital Premium Financing 17CFM Insurance 29Couri Insurance Associates 6EMC Insurance Cos. 30FCCI Insurance Co. 34Illinois Casualty Co. 33JM Wilson 36MAIA Education 19MAIA Partners 40

DepartmentsFrom the President 5The Legal Side 9From the DIFP 10Technicalities 15Technology 17

Errors & Omissions 29Missouri News 33Agency News 35Company Partner News 37Classifieds 38

missouriagent

3315 Emerald Lane, P.O. Box 1785, Jefferson City, MO 65102-1785 • 800-617-3658 in Mo. Phone 573-893-4301 • FAX 573-893-3708E-mail: [email protected]: www.missouriagent.org

Publisher Larry CaseEditor Amy J. HoffmanAdvertising Manager Amy J. Hoffman

Officers of the MAIAPresident Scott Brothers, CIC, JoplinPresident-Elect Byron Robison, SpringfieldVice President Doug Clift, CIC, St. LouisSecretary-Treasurer Brian Harrison, CIC, Columbia IIABA National Director Mitchell C. Mills, ClintonPIA National Director Richard Minor, CIC, Hannibal Past President Belinda Brenizer, CIC, Edina

Board of DirectorsRegion 1 Ricky Baker, CIC, ChillicotheRegion 2 Steve Heying, CIC, St. PetersRegion 3 Chris Rupp, LUTCF, CIC, LibertyRegion 4 Wil Turner, CIC, BeltonRegion 5 Rick Naught, CIC, CPCU, Jefferson CityRegion 6 Jim Baxendale, CPCU, St. LouisRegion 7 Greg Rebman, CIC, St. LouisRegion 8 Jane Dobrinic, CIC, CPCU, St. LouisRegion 9 Randy Smart, MarionvilleRegion 10 Kevin Krueger, LUTCF, BolivarRegion 11 Steve Rackley, CIC, CISR, GainesvilleRegion 12 Randy Baker, KennettAt-Large #1 Shane Davolt, Kansas CityAt-Large #2 Ted Schroeder, UnionAt-Large #3 Dean Mandis, WildwoodCo. Rep. Matt Hartigan, Overland Park, Kan.Co. Rep Tony Weishaar, Maryland Heights

Staff of the MAIAExecutive Vice President Larry CaseVice President of Operations Sheryl Van LeerVice President of Marketing Lindsay Schmidt, AIPInsurance Services Manager Leona LoethenEvents Manager Jeanne Blomberg, AIPDatabase Administrator Laura BerendzenCustomer Service Representative Theresa Flippin, AIPCustomer Service Representative Monica Mize, AIPEditor Amy J. HoffmanMembership Services Representative Kelli Findley, AIPEducation Director Emily KoenigsfeldAdministrative Assistant Dawn ChristianEducation Coordinator Julie Case

MISSOURI AGENT (USPS 709-210) is published bimonthly by the Missouri Association of Insurance Agents, 3315 Emerald Lane, Jefferson City, MO 65109, phone 573-893-4301. Periodical postage paid at Jefferson City, Mo.

The MAIA does not necessarily endorse any of the com-panies advertising in this publication. Subscription rate for members is $25 per year, which is included in dues.

Address & Other Changes

Notify the MAIA if you change your address, change your agency name, or drop or change producers (who are voting members of the association). Write to MAIA, P.O. Box 1785, Jefferson City, MO 65102-1785 or e-mail [email protected].

POSTMASTER: Send address changes to Missouri Agent, P.O. Box 1785, Jefferson City, MO 65102-1785.

© 2011 Missouri Association of Insurance Agents

On the Cover: Keynote speaker Patrick Buchanan brings his take on politics and history when he headlines the 2011 MAIA Leadership Conference.

Volume 20, No. 3

MEM Insurance 2Meramec Valley Mutual Insurance 16M.J. Kelly 35Missouri Rural Services 32Ringwalt & Liesche 13RLI 27SECURA 39State Auto Group 18 Surplus Lines Association of Mo. 12United Fire Group 11West Bend 4WineryPak Insurance Programs 37

Age

nt

America’s ReckoningPatrick Buchanan comes to the Leadership Conference

missouri

spec

ial fo

cus:

leaders

hip

confer

ence

may

-ju

ne

2011

Vo

lum

e 20

, No.

3

The best relationships make it easy.

“West Bend has been great to work with and the ease of doing business has been one of the reasons we look to you as number one.”

“I really enjoy the relationship I have with all the associates at West Bend!”

“I feel West Bend goes above and beyond with their underwriting staff already. Everyone is accessible and their field marketing reps also act as a sounding board and valuable resource to our agency.”

“Never change the fact that management is accessible to the agency if needed and allowed to discuss an underwriting decision with a graceful out for all, thereby keeping our mutual client the main focus and all of our business relations intact.”

“West Bend is a great company and easy to do business with ... flexible and a good team partner.”

“I think West Bend is doing an excellent job already, the quoting online is great, the new customer service department is awesome. I love working with them!!!”

So when it comes to doing business, make West Bend

your first call.

We’re the easy choice.

That’s what our agents say. In a nationwide ease-of-doing-

business survey, West Bend

scored first or second every

year for the past five years.

And when it comes to making

it easy to do business, agents

point to the relationships they

share with West Bend.

But don’t take our word for it. Here’s what our agents have to say ...

may-june2011 missouriagent 5

Just what is good leadership?Lead, follow or get out of the way: Ironic though it may sound, a good leader knows when and how to do each of these seemingly divergent tasks.

He or she usually leads by example, or at least tries to, and “example” sometimes involves showing other people how to do their jobs but sometimes simply means allowing people to do what they know how to do – to turn ‘em loose and get out of the way.

Therefore, leadership requires a con-fident and deci-sive person, who not only has vision but who also has the ability to inspire others. And a true leader knows that success is an ongoing process and not a single destination.

Since we in the association fill a good many leadership roles, reciting this litany of qualities may sound like patting oneself on the back, but that is not my intention. Recognition of qualifi-cations is merely a key component to trying to live up to them. And we all face risks in tackling the responsibilities of leadership positions.

Leadership cannot be about dithering or dou-bletalk; it embraces decisiveness and directness. It is about steering and navigating with as much forethought, insight and wisdom as possible.

A leader identifies and nurtures potential. He or she gives rein to those who have ideas, tal-ent and focus – and reins in those who veer off course. A leader helps bring out the best in indi-viduals and helps individuals to work together, to blend into effective and positive teams.

Optimism, enthusiasm and positive energy are essentials. Leaders necessarily must root out negativity. In other words, leaders must pave the way (and clear the way) for progress and productivity.

As I noted, we in the agency business are leaders. We run small businesses; we are in-volved with our communities; and we are active

in various other orga-nizations, including this one. And we al-ways need to prepare and help those grow-ing in our industry.

The 2011 MAIA Leadership Conference is scheduled for July 20-22 this year. Support and par-ticipate in this event.

Let the developing leaders in your agency, as well as your current leaders, benefit from these seminars. They will hear industry-recognized experts present our continuing Best Practices series and will benefit from well-known con-servative Patrick Buchanan’s insightful keynote persentation.

They will also have the opportunity to meet with insurance company representatives and important vendors, and, perhaps most impor-tantly, they will have the chance to network with their peers from around the state.

Just what is good leadership? It is not only leading but caring about participants, processes and outcomes.

Leaders give guidance, direction and encour-agement. They know when to say, “No” – and when to say, “Go for it.”

Scott BrothersMAIA president

A true leader knows that

success is an ongoing

process and not a single

destination.

fromthepresident

may-june2011 missouriagent 7

The many faces of insurance issuesRepresenting the interests of our members and your clients is one of the primary functions of our association and one on which we expend a lot of time, energy and resources. Never dull, never boring, it puts us in many different set-tings and situations. We have the opportunity to meet a lot of people from many different professions and all walks of life. I personally have the great privilege of encountering the many different faces of the insurance industry.

Even though this aspect of my job many times requires long hours, includes unique challenges and presents obvious conflicts, successful con-clusions are perhaps the most rewarding part of my job. However, it can also be one of the most distasteful and un-enjoyable aspects when one is surrounded by the uncaring, the uninformed, the unethical or the unscrupulous, and some of those multiple faces happen to be worn by the same person.

Recently, there seems to have been more than the usual share of controversy and chal-lenge. As an example, a usual ally, the National Association of Insurance Commissioners, has publically expressed the importance of keeping producers involved in the counsel, sale and de-livery of health insurance. However, when pre-sented with two specific opportunities to back up their statements, they chose instead to live up to their reputation and history of inaction. Abandoning the producer community on this issue cut producers off at the knees and made it clear that their earlier pronouncements were nothing more than hollow rhetoric.

Apparently, the commissioners were accept-ing marching orders from Health and Human Services Secretary Kathleen Sebelius and some of the self-anointed consumer groups. It’s likely they collectively plotted their strategy over drinks and a jukebox playing old O’Jays tunes. There is really no reason to address any specific comments toward Secretary Sebelius, as her record clearly speaks for itself. Besides, we all have years of validation that nothing positive ever comes out of Kansas anyway.

With regard to some of the so-called consum-er advocates, there are few more transparent in their hypocrisy and doublespeak than these folks. They proclaim to want consumers to have choices and have access to information and re-sources in order to make informed decisions. It would seem that they would want consumers to

have the advice and counsel of educated, regu-lated and professional independent insurance producers, who represent multiple insurers, provide professional risk assessment, customize coverage and help guide consumers through the claims process.

Nevertheless, some of these groups continue to support legislation to eliminate produc-ers from the process and cut any potential for providing compensation for producer services. Some apparently take such position because they simply have no clue about how insurance works and view it as a commodity with all policies being the same. However, the federal health reform has exposed others as simply being self-serving. Their ultimate goal is to line their pock-ets with federal grant money as insur-ance “navigators,” an entity which has been created under the act.

Of course, when any insurance issue comes up, we are always communicating with our company “partners.” Many times, they emphatically indicate that they want to work with us to meet market, regulatory or logistical challenges only to suddenly turn to silent partners when we ask them to discuss workable solutions and then transcend to oppo-nents when viable proposals are introduced to address the issues. (Can you say earthquake?)

In other instances, some will express their loy-alty to their producer distribution channel yet turn around and reduce or eliminate adequate compensation for you. (Can you say health in-surance?) They even go so far as to align with some of the consumer groups and support bypassing your involvement in the process alto-gether. What great business partners!

So, as you can see, the faces of insurance is-sues hold some smiles, some frowns and some nasty scowls. It’s often difficult to imagine that there could be any worse combination to deal with than insurance and politics.

We prefer and will continue to face the issues head-on. Other dealings are merely a waste of time. And, I am way too old to change my style. Besides, it just doesn’t fit me. To quote Abraham Lincoln, “If I were two-faced, would I be wearing this one?”

Larry CaseMAIA executive vice president

myturn

You’re an independent agent.

Don’t forget

your helmet.

Protect.Our superior coverage and

expert claims teams are in your

corner in the event of a claim.

Prevent.Our risk management

resources keep your agency

from making common

preventable mistakes.

Prosper.When you know you have the

best E&O protection, you can

focus on growing your most

important asset–your business.

www.independentagent.com/EO

The Big “I” Professional Liability Program

The Big “I” and Swiss Re are jointly committed to providing IIABA members with leading

edge agency E&O products and services. The IIABA and its federation of 51 state

associations endorse Swiss Re’s comprehensive professional liability program.

Insurance products underwritten by Westport Insurance Corporation, Overland Park, Kansas.

Westport is a member of the Swiss Re group of companies and is licensed in all 50 states and the District of Columbia. ©2008 Swiss Re

may-june2011 missouriagent 9

Noncompete agreements for insurance agencies: a primerIf you or your agency is considering using a con-tract to restrict an employee or contractor’s abil-ity to take what you view as your business, cross your t’s and dot your i’s: You can protect your customer base and confidential information, but crafting an appropriate agreement will de-pend on multiple factors.

Most covenants not to compete involve an employer-employee relationship. If the person is an independent contractor or consultant, the agency should consider having a contract that sets forth the terms of the business arrange-ment with the independent contractor or con-sultant, and in which a noncompete and con-fidentiality agree-ment are ancillary.

This is the kind of circumstance reflected in a case of first impression in Missouri, Renal Treatment Centers-Missouri, Inc. v. Braxton, 945 S.W.2d 557 (Mo. App. 1997), in which otherwise valid covenants not to compete were recognized as being applicable to independent contractors.

As general background, in Missouri, cove-nants not to compete – that is, agreements that restrict someone’s ability to take business or customers – are enforceable subject to “reason-ableness” restrictions: Are you trying to protect your customers and the good will you have built with them, and are the restrictions you intend to impose limited in time (for example, one year) and geographic area (for example, the ter-ritory within which your producer or principal actually worked)?

Certain professions and categories of persons cannot be bound by noncompetition agree-ments, and these include the legal profession and employees who provide secretarial or cleri-cal services.

Covenants not to compete are considered to be restraints on trade, and they are enforceable

only to the extent that they protect “legiti-mate” interests. Legitimate interests include customer contacts, trade secrets and confiden-tial information.

Trade secrets, defined in RSMo. 417.453, include formulas, patterns, compilations and programs (among other things) that provide an employer economic value and are subject to efforts to maintain their secrecy.

Confidential information may be broader than trade secrets and can include customer lists and contacts, assuming this information otherwise is not public in the form used by the employer.

In order to have an en-forceable noncompete that prevents someone from absconding with business, you or your agency will want to be in a position to show that the person had contacts of the kind enabling him or her to

influence customers, which typically means the person was with your agency long enough to have developed relationships with your custom-ers. One would also want to include a confiden-tiality agreement as part of the covenant not to compete, and in some cases using a confidenti-ality agreement alone can result in protecting business contacts and customers.

As obvious as it might sound, the most effec-tive time to consider requiring a noncompete or confidentiality agreement is at the front end of your business relationship, whether it is with an employee or an independent contractor.

Mary Jo Shaney is stepping in as a guest writer for Lewis E. Melahn, J.D. Shaney is a partner at White Goss Bowers March Schulte & Weisenfels, Kansas City. She handles business and employ-ment litigation and advice. Shaney can be reached at 816-502-4731.

Mary Jo Shaney, Esq.partner, White Goss Bowers Schulte & Weisenfels

thelegalside

The most effective time to consider requiring a noncom-pete or confidentiality agree-ment is at the front end of your business relationship.

10 missouriagent may-june 2011

I’m pleased to report on the significant role that Missouri is playing at the National Asso-ciation of Insurance Commissioners, a role that was enhanced during the spring meeting in Austin, Texas.

You may be aware that the NAIC released A Consumer’s Guide to Earthquake Insurance during the meeting. This 14-page brochure walks consumers through the factors they should consider in deciding whether earth-quake insurance is right for them. As always, the NAIC encourages consumers to work closely with their insurance agents. Special recognition goes to Angela Nelson, director of our Consumer Affairs Division, who led the national working group that wrote the guide.

The guide’s release is well timed, given the earthquakes in Japan and New Zealand, as well as the concerns I shared with you about

NAIC spring meeting:Missouri’s leadership grows

Missouri’s earthquake insurance market in the last issue of Missouri Agent.

In the past month, I have been interviewed by the St. Louis Post-Dispatch, A.M. Best and Re-uters on this issue, and I told them we are in the midst of a perfect storm with earthquakes: there is public awareness; our market continues to contract in Missouri; and the Federal Emergency Management Agency and the State Emergency Management Agency just held a multi-state earthquake preparedness exercise in late April, the largest ever of its kind. On top of all that, Gov. Jay Nixon proclaimed February to be Earth-quake Awareness Month, and Feb. 11, 2011, marked the 200th anniversary of the great New Madrid quake.

In late April, my team and I had a productive meeting with Glenn Pomeroy, CEO of the Califor-nia Earthquake Authority, who came to Jefferson

fromtheDIFP

John M. Huffdirector, Missouri Department of Insurance, Financial Institutions and Professional Registration

may-june2011 missouriagent 11

United Fire Group®Cedar Rapids, Iowa www.ufgAgent.com

UNITED FIRE AGENT RON HAMMERBERGPRESIDENT, FIRST IOWA INSURANCE AGENCY INC.

CEDAR RAPIDS, IOWA

Independent agents are the backbone of our insurance business. So, when you talk, we listen. Your requests have prompted us to develop an automated cancellation notifi cation system for the notifi cation of third parties.

The benefi ts of this system include:

No reduced number of days notice for non-payment

Notice to parties of interest for insured-initiated cancellation and company-initiated cancellation

Notice to parties of interest for all requested lines of business

UW1730, notifi cation endorsement for cancellation, non-renewal or material change in coverage

Contact your United Fire marketing team at 800-343-9125 to learn more about this automated cancellation notifi cation system. Go ahead… We’re listening!

AT UNITED FIRE GROUP...

▼▼

▼▼

City to share his state’s experiences. We will con-tinue to be heavily engaged on this issue, rais-ing awareness and working with the industry. I’m committed to ongoing dialogue with insur-ance commissioners in some of our neighboring states, including Arkansas, Illinois and Tennes-see, since this affects our entire region.

In other business from the spring meeting, Angela Nelson accepted another prominent assignment. She will chair the newly created Transparency and Readability Working Group. This panel will examine whether standard, plain language can be applied to the policies sold by property and casualty insurers nationwide.

The early hearings on this issue have been heated. Consumer groups want standardized policy forms with increased consumer readabil-ity. The industry is resisting such changes, saying standardized forms and consumer disclosures

will open insurers up to increased litigation. They also argue against public transparency of policy forms due to the cost and proprietary na-ture of some companies’ forms. Instead, many parts of the industry are advocating increased consumer education.

At the spring meeting, we also heard testi-mony on marked differences in levels of cover-age in homeowners insurance policies between companies. As agents, you are often the first line of defense for consumers who want to learn more about their insurance needs. But I believe we can and should do more as regula-tors to increase consumer literacy of insurance. This working group is a great opportunity for an open discussion to identify the ways that in-surers, agents, regulators and consumer groups can work collaboratively to achieve that goal.

What is

Marketing wiz Michael Dell’s last name is placed on everything connected with the company: office signs, ads, websites, bills, computer boxes and, of course, the computers themselves.

But you’ll also see something else connected with the Dell brand: “Intel Inside.” As an “in-gredient brand,” Intel Inside provides value to the “host brand,” Dell.

To be successful as a recognizable consumer brand, Intel relies not only on national adver-tising (Maybe you’ve seen the Blue Man Group spots.) but also on getting computer makers, distributors and retailers to use Intel Inside wherever they can.

A similar strategy is being employed to build the Trusted Choice consumer brand. Trusted Choice is an ingredient that adds value to your agency. It does not replace your agency’s brand. It enhances your agency’s brand be-cause it delivers to consumers and businesses

exactly what they say they want from an insur-ance provider.

Still, we continue to see confusion among agents and brokers over what Trusted Choice of-fers. This isn’t a market-access program or an on-line managing general agency. It’s not simply a logo. It’s not just a national advertising or public relations program. Nor is it an association name.

Instead, Trusted Choice is a long-term brand-ing strategy to position participating agents and brokers as the preferred consumer choice for insurance and financial services. Just as Intel Inside reminds us of smarter, better and faster computers, Trusted Choice represents advocacy, customization and choice.

Like Intel Inside, the key to the Trusted Choice strategy is participation: We depend on an in-tegrated team of participating agents, brokers, local boards, state affiliates and carriers to con-sistently remind consumers of the value of the Trusted Choice way of doing business.

from TrustedChoice.com

SUPPORT YOUR MISSOURI WHOLESALERSFor all hard-to-place, Excess and Surplus Lines and specialty accounts.

Call the people that support your organization.

P. O. Box 67 • Jefferson City, MO 65102-0067(573) 635-0736

3D Star Insurance Services 314-436-3318 Fax 314-436-4309 www.3dstarinsurance.comAmerican Surplus Lines Agency, Inc. 913-888-8400 877-642-2752 Fax 866-936-0400 www.ASLAINC.netBohrer, Croxdale & McAdoo 417-869-2550 800-779-2550 Fax 417-869-5102 www.bcmins.comBurns & Wilcox - St. Louis 314-819-0400 800-331-4128 Fax 314-819-0440 www.burns-wilcox.comChris-Leef General Agency, Inc. 913-631-1232 800-548-0491 Fax 913-631-1128 www.chris-leef.comContinental American Agency, Inc. 314-241-7969 866-764-8451 Fax 314-241-1474 www.caains.comDavidson-Babcock, Inc. 913-469-1188 800-203-3223 Fax 913-469-1177 www.davidson-babcock.comGateway Underwriters Agency, Inc. 314-238-0070 800-325-7652 Fax 314-238-0065 www.gua-stl.comGraham-Rogers, Inc. 918-336-2800 800-456-8123 Fax 918-336-7196 www.graham-rogers.comGresham & Associates 417-823-3924 866-251-9646 Fax 417-823-3979 www.gresham-inc.comJ.M. Wilson 816-561-6700 800-507-8656 Fax 816-561-3331 www.jmwilson.comMed James, Inc. - Kansas City 913-663-5500 800-255-6503 Fax 888-216-2014 www.medjames.comMed James, Inc. - Springfield 417-886-3535 800-255-6503 Fax 417-886-2295 www.medjames.comMed James, Inc. - St. Louis 636-524-0080 866-255-6503 Fax 636-524-0088 www.medjames.comMidwestern General 816-246-1200 Fax 816-246-1290 www.mgakcmo.comM.J. Kelly Company 417-883-2688 800-725-7211 Fax 800-678-7211 www.mjkelly.comM.J. Kelly of St. Louis LLC 314-416-4343 877-416-4343 Fax 314-416-4344 www.mjkstlouis.comS.A. Freerks & Associates 314-436-2682 800-342-2601 Fax 314-436-1532 www.safains.comSwett & Crawford 314-821-2699 Fax 314-822-2135 www.swett.comWestrope 816-842-8222 Fax 816-842-3081 www.westrope.com

Association of Missouri

P

32972_Surplus Lines:Layout 1 6/1/10 2:06 PM Page 1

Trusted Choice?

12 missouriagent may-june 2011

We urge member agents and brokers to get involved by taking the following steps*:

• Fully integrate Trusted Choice into your firm’s culture, operations, workflows and marketing.

• Use the Pledge of Performance to educate consumers and prospects about what you deliver to them. It will help you close sales.

• Be visible in the community with the Trusted Choice logo on your advertising, signage, business cards and letterhead.

• Leverage the logo and Pledge of Performance on your website.

• Use the tag-able ads for your local print, ra-dio and TV campaigns (information available at www.TrustedChoice.com/agents).

• Run local print, TV or radio ads that are timed with nationwide Trusted Choice ad-vertising flights. Check www.TrustedChoice.com/agents for dates of upcoming ad flights.

• Make sure your information is updated at the Agency Locator on www.TrustedChoice.com because all leads from national advertis-ing and public relations campaigns are driv-ing consumers there.

Be smart like Michael Dell. Burnish your agen-cy’s brand by actively participating in Trusted Choice, your ingredient brand.

*Agencies that have submitted their signed license agreements are encouraged to take advantage of the wide array of Trusted Choice advertising and marketing tools, and only those agencies will be included on the Agency Locator. If you have not signed your license agreement, you may contact the MAIA office at 800-617-3658 for assistance or visit www.TrustedChoice.com/licenseagreement to down-load the form.

may-june2011 missouriagent 13

may-june2011 missouriagent 15

Does insurance always follow the vehicle?

Insurance follows the vehicle. For 25 years in the insurance business, I have always been taught that insurance follows the vehicle. In other words, if I lend my car to you, my insurance policy becomes the primary coverage, and your policy is secondary.

Recent experiences have shown that not all companies’ policies respond this way. A few years ago, I had a family insured that had young children. I also had their parents’ auto insurance coverage with another carrier.

The family decided that they were going to take the kids on vacation, and they decided to borrow the parents’ conversion van for the trip. On the way to the destination, they were involved in an accident, and they were at fault. We initially turned the claim in to the parents’ carrier, which had the conversion van insured. They promptly notified us that their policy was secondary to the driver’s policy.

Really? That is not what we have been telling the insurance public. We turned the claim into the driver’s insurance carrier. They responded that their coverage was secondary. This was consistent with everything we have always been taught. The claim was ultimately resolved by both companies agreeing to pay half. This was a small claim with minor property damage. Would it have been resolved the same way if it had been a large bodily injury claim?

I was surprised and agitated by the way the parents’ company’s policy responded. I spoke to my marketing representative with the company. She had her own vehicle insured with the com-pany and didn’t realize this is how the policy would respond.

I spoke to a person who was the head of claims for the area. She responded that the company had notified all policyholders when they made the change. The change was con-tained in their “Amendatory Endorsement Other Insurance Provision.” It reads, “Any insur-ance we provide for use of your ‘covered auto’ by any person other than ‘you’ will be excess over any other collectible insurance, self-insur-ance or bond.”

I told her we as agents – or at least I person-ally – weren’t notified about the change. In

fact, our company marketing representative didn’t know that the policy responded in this manner. The claims person also told me that they changed their policy because another large carrier had changed its policy form.

I also found out that at least one other state would not allow a carrier to have this type of policy. Our company’s auto policy still responds in this manner in Missouri, but it has made a change in how the claim is handled. It now will pay the entire claim and subrogate against the driver’s carrier.

Recently, I was informed that another carrier has lowered its coverage to the state’s minimum liability limits if a permissive driver (who is not a named insured) is involved in accident. I re-ceived a copy of the company’s “Amendments of Policy Provisions – Missouri.” Under “Part A Liability Coverage,” it reads:

Under Insuring Agreement, Item 2 under the definition of “Covered Person” is de-leted and replaced by the following: 2. Any person other than those identified in paragraph 1 using your covered auto with your permission. The limits of liability for this person shall be equal to minimum lim-its of liability required by Section 303.190 of the Revised Statutes of Missouri, which are $25,000 per person, $50,000 per occur-rence, and $10,000 for property damage.

Insurance follows the vehicle. For most car-riers, this is correct, but it certainly is not true with every carrier in every state. And with oth-ers, the regular policy limits may not apply. How do your carriers respond to permissive drivers? As agents, we need to know how to properly advise our insureds.

Greg Rebman, CIC, is the agency manager of O’Connor Insurance Group, St. Louis. He has been a member of the MAIA Technical Committee since 2005. You can reach Rebman at 314-576-7080.

Greg RebmanMAIA Technical Committee O’Connor Insurance Group

technicalities

16 missouriagent may-june 2011

A Note from MATC

One of the items presented to the Insurance Services

Office at the 2010 Mid-America Technical Conference

dealt with requests to agents from personal lines clients

to provide cities, counties and private businesses with

proof of liability insurance for the homeowner.

Usually, these requests result from the rental of pri-

vate halls or public meeting space, or the use of public

parks for birthday parties, wedding receptions, family

reunions or other activities. These are all activities that

would be covered under the personal liability section of

the homeowners policy as long as it is not business use.

There is not an ACORD form to communicate this

evidence. If there is a request to add anyone as an ad-

ditional insured, there is no means to do so with the

homeowners program.

That forces agents to either issue a certificate using an

ACORD form that is not designed for use with the hom-

eowners policy or to purchase for their client a special

event policy, where coverage can be provided for the

use of the facility, and add an additional insured.

ISO has asked us to provide examples of where an

agent has received a request and what is being request-

ed so that it might better understand the problem. Any

agents who have examples are asked to provide them to

the Missouri Association of Insurance Agents. You may

send examples to Executive Vice President Larry Case at

[email protected], or you may call him with questions

at 800-617-3658.

To: Missouri producers

Re: Homeowners certificates of insurance

may-june2011 missouriagent 17

service as unique as a two dollar bill sm

It’s easy. Let us finance your insureds’ premiums.With exclusive profit sharing programs and a sta� that speaks 9 di�erent

languages, financing insurance premiums has never been so easy or so profitable.

We finance. Insureds benefit. You profit.

How can you make more moneyfrom your existing business?

Several plans available. Contact us today for details.

[email protected] www.capitalpremium.net

Social media time-saversAs a marketing process manager for Progres-sive, I speak with independent agents across the country about the importance of social media. For most, finding time in their busy schedule is one of the biggest concerns.

But you don’t have to dedicate hundreds of hours to see a return from social media. A well-defined strategy (and a few time-saving tools) can help you strike a balance between the time you invest and the value your investment adds.

When it comes to social media planning, there’s no right or wrong level of involvement. The most important factor is consistency. Start by setting goals for your agency’s participation. Whether it’s regular interaction with custom-ers on Facebook, a tweet every few days, or a weekly blog post, you can strengthen your so-cial media presence by having clear goals in sight.

Here are three levels of social media involve-ment to consider based on the time you want to commit and the goals you set.

Listen (1-2 hours a week) This should be the first step of any social media strategy. After you’ve set up your agency’s ac-counts on sites like Facebook (www.facebook.com), Twitter (twitter.com) and LinkedIn (www.linkedin.com), study what people are saying on the platform. Check sites like Google Places (www.google.com/places) or Yelp! (www.yelp.com) for customer reviews of your agency. Friend your customers and follow their updates, track your competitors’ tweets, and watch how people respond. Note what’s working, record the questions and topics that dominate the conversation, and think through how you’d respond.

By first using social media as a listening tool, you’ll learn best practices for status updates, tweets and blog posts before creating your own. Plus, you can apply what you’re learning from online chatter to shape quoting and in-person conversations with your customers.

Time-savers• Clearly outline actions and responsibilities

within your agency to prevent redundancy, maintain focus and meet your social media goals. For example, you could assign a single person in your agency to review Facebook,

Twitter and LinkedIn for one hour, twice a week.

• “Like” competitor Facebook pages from your personal profile to more easily follow their updates when you’re online.

• Search Twitter and third-party directories like WeFollow (wefollow.com) and Twellow (www.twellow.com) to identify popular profiles associated with insurance. Create Twitter lists to organize the people you follow by category (customers, competitors, etc.), and use programs like Hootsuite (hootsuite.com) or Tweetdeck (www.tweetdeck.com) to monitor your Twitter lists at a glance.

• Use a reputation management tool to monitor what people are saying about your agency. Consider using free ser-vices like SocialMention (www.socialmen-tion.com) and Google Alerts (www.google.com/alerts), or more robust paid services like ChatMeter (www.chatmeter.com), Location-Monitor (locationmonitor.com) or Trackur (www.trackur.com).

Matt Markomarketing process manager, Progressive

continued on page 18

technology

18 missouriagent may-june 2011

• Create a Google Reader (www.google.com/reader) account for one-stop monitoring of key in-surance blogs and publications. Content hubs can save you hours each week by better organizing content for quick review.

Respond (2-5 hours a week) After taking some time to listen, join the con-versation by responding to questions, posts and comments with a helpful link or thought-ful answer. Note that while answering ques-tions or directing people to another online resource builds goodwill and trust, “hijacking” an online conversation to explicitly promote your agency can undermine your efforts.

Provide helpful advice over time and as-sociate comments with your agency through hyperlinks or a simple signature with contact information. Remember, showing your value doesn’t require you to give “pro bono” ad-vice. Asking the right questions and outlining relevant points customers should consider can demonstrate the value of an independent agent and lead to a follow-up phone call.

Time-savers• Focus on a few active online communities

rather than jumping around looking for every opportunity to respond. You’ll get to

know the members better, and your partici-pation will build credibility that can lead to references across the social network.

• Develop a list of frequently asked questions for common topics, along with your respons-es and online resources you can share. Using these responses as a starting point can save time when responding to similar questions or comments.

Publish (5+ hours a week) The final level of social media engagement is proactively communicating to your audience. Although most businesses prefer to jump right into engagement, by listening and responding first, you’ll be more comfortable with the me-dium and your audience. By starting slow, you’ll also have a better understanding of the time you have for social media, and you’ll be more likely to provide the consistent presence necessary to build trust.

Time-savers• Put a process in place to keep your involve-

ment consistent and efficient. Assign a pro-ducer, a CSR or a marketing intern from a local college as your social media manager to ensure a single point of contact. Make sure they work alongside everyone in your agency to get questions answered and develop con-tent without bottlenecks. Remember that effective social media engagement is timely and human. Delayed responses and overly-corporate language limit your effectiveness.

• Share any quality information you think fol-lowers may be interested in. It doesn’t always need to be about insurance. Not only can this save you time developing your own content, it provides value to fans, followers and read-ers, and increases the chance that others will share your content with their communities.

• Distribute the work among a few employees to keep it manageable. This adds variety to your posts and prevents disruption due to vacation, job changes or illness.

• Mix up your content. A thought-provoking question can be as effective as a blog post and takes a fraction of the time to compose. Discussing community events or commenting on your favorite sports team can also engage your audience without the research and writ-ing time longer posts may require. Plus, con-sumers will appreciate seeing the personality of your agency and its employees.

Matthew Marko is a mar-keting process manager for Progressive Insurance. He works to provide local marketing strategies, tools and co-branded collat-eral to help independent agencies grow their busi-nesses. E-mail him at [email protected]. Marko prepared this article for ACT.

For more information about ACT, contact Jeff Yates, ACT executive direc-tor, at [email protected]. This article reflects the views of the author and should not be construed as an official statement by ACT.

technology continued from page 17

CISR — William T. Hold Seminar Filed for 8 CE credits in Missouri Tuition: $158 ($140 Early Bird Discount*)CIC — James K. Ruble Graduate Seminar Approved for 16 CE credits in MissouriTuition: $395 (There is no Early Bird Discount for

Professional DevelopmentEducation

Title Description/Date/Location

*Early Bird Discount price applies to registrations received at least two weeks prior to class date.

E&O — A Practical Guide to Agency E&O Risk Management Approved for 6 ethics CE credits in Mo.Tuition: $120

This errors and omissions seminar focuses on providing practical guidelines and tools for effective loss control. The session incorporates real-life scenarios agency employ-ees probably have already encountered. Open to members only.

Date and Location: May 11, MAIA Headquarters, Jefferson City

CISR — Personal Auto Approved for 8 p-c CE credits in Mo.Tuition: $181 ($163 Early Bird Discount*)

Students will analyze the personal auto policy and its major endorsements; learn how the PAP responds to owned, rented or borrowed vehicles; examine the personal umbrella policy and how it benefits insureds; and define who qualifies as an insured.

Dates and Locations: May 18, DoubleTree Hotel, Chesterfield May 24, MAIA Headquarters, Jefferson City June 28, DoubleTree Hotel, Springfield

CISR — Dynamics of Service Approved for 8 general CE credits in Mo.Tuition: $181 ($163 Early Bird Discount*)

Dynamics of Service is all about building proven techniques for effective customer service, and it is designed for anyone who values clients and customers. The course is open to all agency personnel, regardless of affiliation or professional designation.

Date and Location: June 1, DoubleTree Hotel, Chesterfield

Young Agents Conference Approved for up to 5 p-c CE credits in Mo.Tuition: $205 first agent, $105 additional agents from same agency

This conference is designed for new insurance producers. It offers three educational sessions, which examine life in the insurance industry and “Maximizing Your Internet Presence,” as featured in The Anderson Agency Report.

Dates and Location: June 5-7, The Landing, Van Buren

Risk Specialist Series — Insuring Small Commercial Risks Approved for 12 p-c credits in Mo.Tuition: $250 ($199 Early Bird Discount by June 10)

Participants will cover the essential elements of the commercial property policy, time element coverages, recommended endorsements and various inland marine forms.

Dates and Location: June 15-18, Hilton Garden Inn, Independence

CIC — Commercial Property Approved for 16 p-c CE credits in Mo.Tuition: $413 ($396 Early Bird Discount*)

This Risk Specialist course will address lease issues, certificates of insurance, cover-age gaps, businessowners policy comparisons, commercial casualty exposures and more. Open to members only.

Dates and Location: June 22-23, MAIA Headquarters, Jefferson City

20 missouriagent may-june 2011

specialfocus leadershipconference

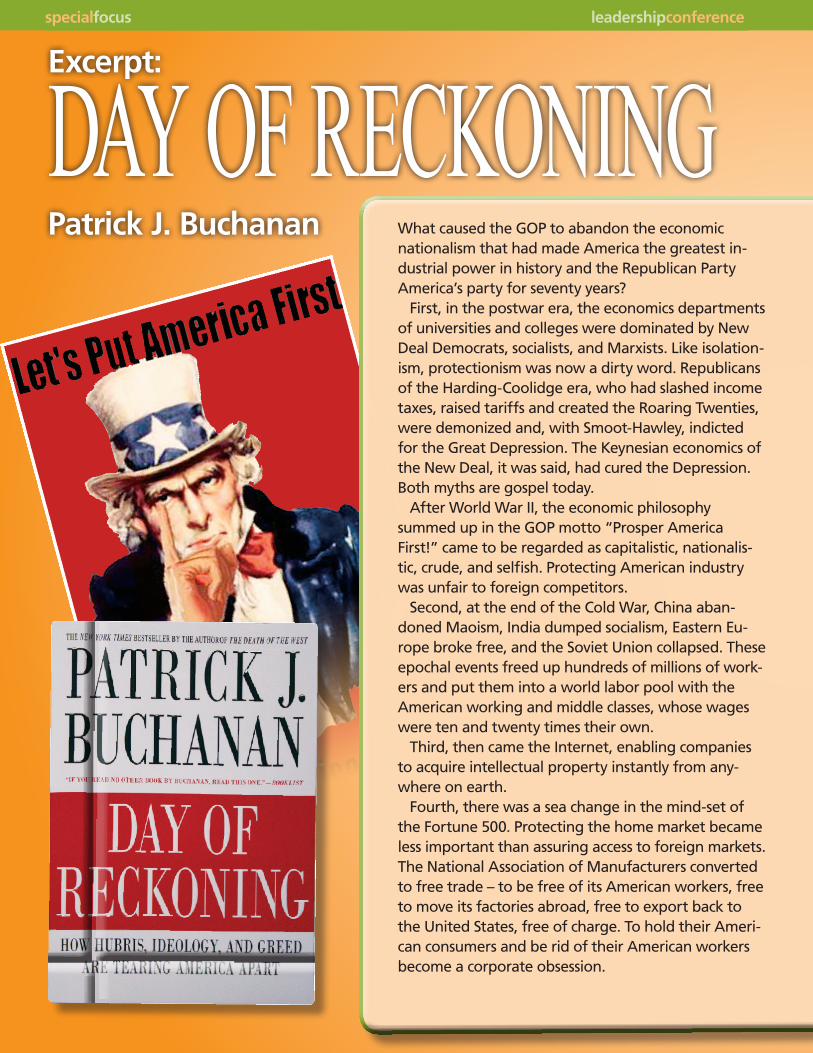

Excerpt:

DAY OF RECKONINGPatrick J. Buchanan What caused the GOP to abandon the economic

nationalism that had made America the greatest in-dustrial power in history and the Republican Party America’s party for seventy years?

First, in the postwar era, the economics departments of universities and colleges were dominated by New Deal Democrats, socialists, and Marxists. Like isolation-ism, protectionism was now a dirty word. Republicans of the Harding-Coolidge era, who had slashed income taxes, raised tariffs and created the Roaring Twenties, were demonized and, with Smoot-Hawley, indicted for the Great Depression. The Keynesian economics of the New Deal, it was said, had cured the Depression. Both myths are gospel today.

After World War II, the economic philosophy summed up in the GOP motto “Prosper America First!” came to be regarded as capitalistic, nationalis-tic, crude, and selfish. Protecting American industry was unfair to foreign competitors.

Second, at the end of the Cold War, China aban-doned Maoism, India dumped socialism, Eastern Eu-rope broke free, and the Soviet Union collapsed. These epochal events freed up hundreds of millions of work-ers and put them into a world labor pool with the American working and middle classes, whose wages were ten and twenty times their own.

Third, then came the Internet, enabling companies to acquire intellectual property instantly from any-where on earth.

Fourth, there was a sea change in the mind-set of the Fortune 500. Protecting the home market became less important than assuring access to foreign markets. The National Association of Manufacturers converted to free trade – to be free of its American workers, free to move its factories abroad, free to export back to the United States, free of charge. To hold their Ameri-can consumers and be rid of their American workers become a corporate obsession.

may-june2011 missouriagent 21

Patrick Buchanan is the featured keynote speaker for the 2011 Leadership Conference. See the brochure inserted in this magazine for more information.

specialfocus leadershipconference

Finally, the trade deals of the late twentieth century were enabling acts for companies to shed national identities and loyalties and reinvent themselves as global companies, the new masters of the universe.

Hamilton’s vision was history. Patriotism yielded to globalism. Our old cherished independence was to be set aside for a new and higher “interdependence.” All nations must now engage in the mutual sacrifice of sovereignty to create the New World Economic Order. Rich nations must annually transfer a slice of their wealth to poor nations. First World workers must compete fairly with Third World workers. There will be pain, but these are the birth pangs of the brave new world we are about to enter.

Behind this vision lies a dirty little secret. The desig-nated beneficiary of the global economy is the global company. The hidden agenda of the global economy is the empowerment of the global company.

In the global economy, the Middle American worker politicians once courted with promises of “a chicken in every pot” and a “full dinner pail” has become the unwanted American – except as a consumer.

U.S. workers must now compete for jobs in their own country with tens of millions of immigrants, legal and illegal. Meanwhile, their factories are shut down and moved to Mexico and China. Knowledge-industry jobs are outsourced to South Asia. Corporate America has been empowered to go abroad and hire bright young men and women to come and take the jobs of middle-aged Americans at half their salaries. Mexi-can trucks now roll on American roads, and in India, long-haul truck drivers are being trained to come to America and take the jobs of American truckers. There was a time when an American could, on a single in-come, support a wife and half a dozen kids and look forward to a secure retirement. In the new America, where the commands of globalism trump the call of patriotism, the American dream is receding. For many, it has already died.

The hidden agenda of the global economy is the empowerment of the global company.

Use these lists to audit your agency’s or company’s quality performance. The full “Quality Journey” quiz is available for free download in the Tool Kit at the Best Practices website, bp.reaganconsulting.com/toolkit, under the “Customer Service” link.

What matters most to your organization in terms of quality customer service?

Here’s a list of 20 things that quality organizations do for their customers. Rank them in order of importance from 1 (most important) to 20 (least important) for your organization. Distribute blank copies of this list to your employees and have them rank the items. Do your employees prioritize the same items you do?

You Employees

We provide prompt courteous, quality service.

We have regular customer contact.

We tell our customers exactly when services will be performed.

We ask clients exactly what they expect from our agency.

Our management is available to all customers.

We return telephone calls promptly.

We always follow up.

We always ask, “How can we do it better?”

We contact our customers more than annually.

When a customer has a problem, we show sincere interest in solving it.

We are never too busy to respond to our customer requests.

We maintain error-free records.

Our physical facilities are visually appealing.

Our operating hours are convenient for our customers.

We employ technically knowledgeable staff.

We review our customers’ insurance needs annually.

We hire people with a service attitude.

We cultivate a positive office environment.

We practice honesty and integrity in all our dealings.

We perform service right the first time.

specialfocus leadershipconference

22 missouriagent may-june 2011

How do you stack up against the competition?

Here’s the same list. This time, give your organization 2 points for each thing you always do and 1 point for things you sometimes do; then grade your closest competitor. Total the scores to see how you stack up against the competition. After you’ve completed this part of the assessment, it might be enlightening to ask your employees to do this competitive analysis separately.

Scoring: 2 – We always do this. 1 – We sometimes do this. 0 – We don’t do this.

You Competition

We provide prompt courteous, quality service.

We have regular customer contact.

We tell our customers exactly when services will be performed.

We ask clients exactly what they expect from our agency.

Our management is available to all customers.

We return telephone calls promptly.

We always follow up.

We always ask, “How can we do it better?”

We contact our customers more than annually.

When a customer has a problem, we show sincere interest in solving it.

We are never too busy to respond to our customer requests.

We maintain error-free records.

Our physical facilities are visually appealing.

Our operating hours are convenient for our customers.

We employ technically knowledgeable staff.

We review our customers’ insurance needs annually.

We hire people with a service attitude.

We cultivate a positive office environment.

We practice honesty and integrity in all our dealings.

We perform service right the first time.

Scoring: You can be assured that anything less than a perfect 40 is going to have a negative impact on your market share, customer retention, profitability and growth. Look closely at the items you ranked as most important. If you scored less than 2 on any of them, you may be facing potentially severe customer retention issues. Use these findings as your priority action list for improvement in the coming year.

specialfocus leadershipconference

may-june2011 missouriagent 23

Customer service is one of the topics that will be covered in Best Practices education sessions at the 2011 Leadership Conference. See the brochure for more information, or register now online at www.missouriagent.org.

24 missouriagent may-june 2011

2011 small agency conference

CIC Conferees (back row): Jon Rittman, Jeffrey Murphy, Tim Wahl, Janet Wil-son, Caleb Walker; (front row): Gayle Popkey, Barbara Grubb, Ryan Sanders, Sandra Bell, Elizabeth Jegel

CISR Conferees L-R: Ryan Smarr, Chris Meckem, Tina Goss, Brooke Thoma-son, Theresa Leech, Margaret Lowder, Denise Probst, Stephanie House, Kyle McGirl

Tenured CICs L-R: Rick Naught, Mike Keith, Belinda Brenizer, Dan Baker, Scott Brothers

26 missouriagent may-june 2011

2011 conferment ceremony

Ron Mattli and Matt Kujath (left and middle), CRM conferees

Relax... You’ve offered each of your clients a personal umbrella policy.

Right? It might not be quite as relaxing as a day at the beach, but knowing you’ve done everything in your power to protect the customers who trust you to help them will go a long way towards easing your mind.

Offering each and every client an umbrella not only protects those who choose to purchase the coverage. It protects your agency from liability. And it protects your book of business, since studies show that customers who have multiple policies are less likely to move their business elsewhere.

As a Big “I” member, you have access to a stand alone personal umbrella program from A+ rated carrier RLI, featuring:

� Limits up to $5 million available� You can keep your current homeowner/auto insurer� New drivers accepted - no age limit on drivers� Up to one DWI/DUI per household allowed� Auto limits as low as 100/300/50 in certain cases� Competitive, low premiums for increased limits of liability� Simple, self-underwriting application that lets you know immediately if the insured is accepted� E-signature and credit card payment options� Immediate coverage available in all 50 states plus D.C.

So cover your clients... protect your agency... and profit from umbrella sales!

To access log onto www.bigimarkets.com or visit www.iiaba.net/Umbrella.

®

We Aspire to AchieveMutually

Unparalleled customer service • 24/7 accessibility • Web-based quoting and account status • Flexible payment options

Mark reinVice President, sAles

cell: 847-331-6705 • email: [email protected]

www.bankdirectcapital.com

Through flexible terms and competitive pricing, BankDirect has helped a number of agents accomplish what they needed to

succeed. We ASPIRE to do that for you as well.

relationshipsProsperous

“ I have worked with a number of premium finance companies over the years and none of them have been as creative and committed to the relationship

with the agency as BankDirect – AGENCY PRINCIPAL ”

full_page_ad_Rein.indd 2 3/19/2009 9:49:05 PM

may-june2011 missouriagent 29

Homeowners: the new No. 1

For many years, commercial casualty (general liability and umbrella) was the No. 1 underlying loss type for errors and omissions. However, ac-cording to the final 2010 results, there is a new No. 1 in town: homeowners. Just short of 20 percent of all E&O claims allege issues dealing with the homeowners line of business.

Drilling down further, there are several issues to look at. Valuation is one of the major issues; dogs are not exactly E&O’s best friend; and car-rier binding guidelines rounds out the top 3 problems areas. In addition, Utica is experienc-ing claim activity dealing with issues surround-ing personal property that would be better cov-ered under an inland marine policy or floater. Let’s examine each of these in more detail.

Valuation For many years, carriers have been providing their agents with various tools to determine the appropriate homeowners limit. These are designed to provide, when given the proper, accurate inputs, a respectable, somewhat ac-curate estimated value for the home. The key is “proper, accurate inputs,” as without these, the output may not be a valid representation of an appropriate homeowners limit and definitely should not be relied upon.

Many would contend that even with the proper inputs, the calculated value may not be accurate due to significant fluctuations in the price of home building products. When calculat-ing the amount, advise the customer in writing that this is not a guarantee the home can be replaced for this amount.

For homes with a degree of uniqueness, it is questionable whether the estimators should be relied upon at all. In many of these situations, calling in a licensed appraiser may be the best course of action.

Based on the economy in your area, it may be possible for customers to buy a home for much less than it would cost to actually replace it. Communicate to your customers that there is no correlation between market value and re-

placement cost. Some individuals contendthe customer should advise you, as the agent, the amount for which they want the home insured. This does have some merit, provided, again, that the customer thinks of what it would cost to replace the home as opposed to its market value.

DogsDogs are becoming much more of an issue, largely due to the unknown breed of many dogs. If your cus-tomers contact your agency to state they are get-ting a dog, they might not know the actual breed combination given the cross-breeding that takes place. With carri-ers experiencing losses involving dog bites, they are trying to find ways to address this issue.

Curtis M. Pearsallspecial consultant,Utica National Agents E&O Program

continued on page 31

&errors omissions

AkitaAlaskan MalamuteChow ChowDoberman PinscherGerman Shepherd DogPit Bull

Presa CanarioRottweilerSiberian HuskyStaffordshire Bull TerrierWolf Hybrids

Common dog breed restrictions

Emails and teleconferencing may be time-savers, but there is no substitute for the one-to-one relationships with insurance professionals who know you and your community. Early on, EMC Insurance Companies realized the value of being close to agents and policyholders. That value continues to pay off in products and services tailored to individual market needs. Whatever the future holds, insurance will always be a relationship business and EMC will continue to keep those relationships as close to your office as possible.

We’re celebrating our 100th year by planning for our next 100 years.

Tanya Wentzel, Des Moines Branch Marketing ManagerTroy Boysen, Minneapolis Branch Commercial UnderwriterConnie Jarzynka, Omaha Branch Claims Adjuster

Kansas City Branch: 800.821.4702 | Home Office: Des Moines, IA www.emcins.com

© Copyright Employers Mutual Casualty Company 2011 All rights reserved

may-june2011 missouriagent 31

Emails and teleconferencing may be time-savers, but there is no substitute for the one-to-one relationships with insurance professionals who know you and your community. Early on, EMC Insurance Companies realized the value of being close to agents and policyholders. That value continues to pay off in products and services tailored to individual market needs. Whatever the future holds, insurance will always be a relationship business and EMC will continue to keep those relationships as close to your office as possible.

We’re celebrating our 100th year by planning for our next 100 years.

Tanya Wentzel, Des Moines Branch Marketing ManagerTroy Boysen, Minneapolis Branch Commercial UnderwriterConnie Jarzynka, Omaha Branch Claims Adjuster

Kansas City Branch: 800.821.4702 | Home Office: Des Moines, IA www.emcins.com

© Copyright Employers Mutual Casualty Company 2011 All rights reserved

When you receive that call, advise your cus-tomers verbally and in writing that there are certain breeds insurance companies have put on their “prohibited” lists. To avoid any problems down the road, customers should try to ascer-tain the breed of the dog they are considering. Posting this information on your website would be beneficial for those customers who might not contact you verbally. It wouldn’t be surpris-ing at some point for carriers to include in their policy form a list of excluded dog breeds.

Carrier guidelinesEach of your carriers has specific guidelines detailing the circumstances that allow you to bind without first securing their blessing. They do this for a reason. It provides your agency with the ability to bind coverage for those risks that meet the guidelines. It also provides your carriers with recourse against your agency if a risk you bound without their blessing that does not meet their guidelines suffers a loss. As evidenced in the claim example below, carriers take these guidelines seriously (and so should your agency).

The agency wrote coverage for a log cabin for an insured through a carrier it represented. The client had been with another carrier and had a history of late premium payments and reinstatements. The new carrier claimed it would not have written the risk had it known of the prior risk history and also stated it does not write coverage for log homes. The insured knew it was log home but did not disclose that to the carrier.

After paying a loss of $532,117, the carrier filed suit, alleging the credit history and dis-tance from a firehouse (which was understated) were not disclosed and that had they been, it would not have written the risk. The carrier did not bring up the aspect of the house being a log cabin.

There was also a question of fact regarding a discussion between the agent and the carrier before the risk was written. The agent said she disclosed the credit history over the phone and

was given a green light to write the risk. The underwriter denies this. The case was settled by paying the carrier the full amount, $532,117.

Some lessons to be learned from this example include the following:

1. Provide your carrier with a full and accurate description of the risk.

2. If you discuss the risk with the underwriter and he or she gives you the go-ahead, docu-ment the conversation back to the under-writer and put a copy of this documentation in the file.

3. Stay on top of the guidelines, and don’t bind a risk you don’t have authority to bind. There is no upside to misleading your carriers.

Homeowners coverage or inland marine floater?There are many scenarios where there are cov-erage differences between insuring an item under a homeowners policy as part of the con-tents limit rather than insuring those items on an inland marine floater. While there may be some coverage for jewelry under an HO policy, most forms do not provide mysterious disap-pearance as a covered peril. This peril is typically covered under a jewelry floater.

Plus, items that are breakable would prob-ably not have breakage coverage unless insured under a floater. In addition to these peril issues, establishing the proper value is more common with a floater, and thus at claims time, the cus-tomer is more apt to get a fair settlement.

It is definitely recommended that you advise your clients verbally and in writing that when they receive their policies, they must review them to ensure everything is in order. The agen-cy should also review policies to make sure they match what was requested.

Take the time to educate your staff on these issues. With homeowners now the leading underlying line of business in E&O claims, this education may just save you from such a claim.

errors&omissions continued from page 29

may-june2011 missouriagent 33

www.ilcasco.com

Restaurants Fine Dining

Fast Food Delivery Taverns

Wineries Nightclubs

Banquet Facilities Convenience Stores

Fraternal Organizations

Food and Beverage Insurance Specialists

Agent shaves to saveIf you met Mara Raglin, St. Charles, for the first time before March 5, 2011, you would probably have said that her hair was among her most striking features. Long, auburn and wound in cork-screw curls, it was the sort of hair that many women long for.

And if you met Mara Raglin shortly after that Saturday, you would certainly have said that her hair was among her most striking features – ac-tually her lack of it. That was the day that Mara, her husband, Rand, and other members of her St. Baldrick’s Foundation team stepped up in front of scores of observers to have their heads shaved in an effort to raise money to research cures for children’s cancers.

A producer for JBJ Insurance, St. Charles, Raglin was drawn into the St. Baldrick’s Founda-tion activities through friends, but her partici-pation seems providential given that the foun-dation has grown out of a single event in the reinsurance industry in 2000.

That year, three reinsurance executives, John Bender, Tim Kenny and Edna McDonnell, held a head-shaving party on St. Patrick’s Day hoping to raise $17,000 for kids with cancer. The execu-tives and their colleagues instead raised more than $104,000, shattering their own expecta-tions and giving rise to an annual event that has now become the world’s largest volunteer-driv-en fundraising program for childhood cancer research in the world.

Raglin became familiar with the St. Baldrick’s Foundation when non-industry friends, who have been participating for years, invited her to watch a head-shaving event in 2010.

“You see the sick children and your heart breaks, so you almost have no choice but to get involved,” Raglins says.

She, herself, had a friend in grade school named Charles who struggled with liver cancer throughout his childhood, eventually passing away when he was 15 years old. Raglin currently has several other friends and family members

continued on page 34

missourinewsEXTRA!

Mara Raglin goes bald to raise money for children’s cancer research.

34 missouriagent may-june 2011

fighting various types of cancer, so the need for research funding is something that she has seen up close.

As March 2011 approached, Raglin, with her husband and a team of friends, commit-ted as a shavee and signed up to join a head-shaving event at Helen Fitzgerald’s Irish Grill in St. Louis. The St. Baldrick’s Foundation co-

ordinates such events around the world each year in March.

Raglin’s team prepared for the event with intense fundraising efforts.

Donors included friends, family

members, strangers and corporate sponsors, such as Pepsi Max, Timber Creek Bar and Grill, JBJ In-surance Group, and Mike Shanahan Jr. Together, they raised more than $20,000, with Raglin her-self responsible for more than $2,700.

The next step was simply to show up on the morning of March 5, 2011, and take the place of honor in the “barber’s” chair. With her (previ-ously) shoulder-plus length hair, Raglin was able to go an extra step by donating her shaved hair to Locks of Love to be made into a wig for a child with cancer.

“I am now bald for two reasons,” states Raglin in a note to her donors, “to stand in solidarity with kids with cancer, and most important, to raise money for childhood cancer research.”

Adding the funds raised by every team, the event at Helen Fitzgerald’s raised more than $250,000, which the St. Baldrick’s Foundation will donate to research projects through the process of grant awards. The foundation also supports the education of young physicians who commit to childhood cancer research as a specialty. St. Baldrick’s donated more than $14 million in fund-ing in 2010 alone, and the foundation has raised more than $103 million since the first event in 2000. Only the U.S. Government funds more childhood cancer research grants.

Find out more about the St. Baldrick’s Founda-tion and keep track of updates for events in 2012 at www.stbaldricks.org.

missourinews continued from page 33

Mara and Rand Raglin with their children.

may-june2011 missouriagent 35

Rackley Insurance acquires Arkansas agencyRackley Insurance Agency, Gainesville, owned by Steve Rackley, has acquired Thompson Insurance, Mountain Home, Ark. Thompson Insurance will retain its name and its current business operations, and its previous owners, Mike Thompson and Max Freeman, will serve in an advisory capacity for three years. With the acquisition, Rackley Insurance has become a member of the Bainswest Insurance Group, a consortium of 12 agencies in Arkansas and east-ern Oklahoma that ranks No. 53 in the nation’s top 100 independent insurers.

Burns & Wilcox acquires Cleveland brokerageBurns & Wilcox, Farmington Hills, Mich., has acquired NorthCoast Excess & Surplus Agency, a wholesale brokerage and underwriting man-ager based in Cleveland. Jeff Burke, president of NorthCoast, has joined Burns & Wilcox as a senior producer.

Clark-Lami-Hembree celebrates 50 yearsEstablished in 1961, Clark-Lami-Hembree Insurance is celebrating its 50th year of helping

clients make informed insurance decisions. The agency attributes its success to its company partners and the foundation laid by John T. Clark, the agency’s founder, and Arno Lami, his partner, as well as staff members both past and present.

“We are very thankful to our customers for allowing us to be their insurance connection. These relationships built over time between our associates and customers are key to our suc-cess,” says Chuck Hembree, agency president.

2010 Best Practices agencies announcedIIABA and Reagan Consulting have announced the 2010 Best Practices Agencies. Earning the distinction in Missouri are: AHM Financial Group, St. Louis; BancorpSouth Insurance Services, Springfield; Ollis and Co., Springfield; and The Insurancenter, Joplin.

MAIA members earn company recognitionCBIZ Insurance Services, St. Joseph, has been included in the 23 agencies that were named to the 2010 President’s Club by MAIA Company Partner Accident Fund. The annual award is pre-

Don’t forget to finance with M. J. Kelly’s in house financing, BARCO Finance.

Tired of waiting on hold or leaving voice mail? Not with M. J. Kelly

Company. We value your business and your time! We believe in per-

sonal service—knowledgeable professionals providing quick turn-

around on quotes. M. J. Kelly is celebrating 35 years of business. Like

you, we’ve weathered storms. Our growth is steady; our company is

strong; and our service is exemplary. We stand the test of time (yours

and ours). Call us for personal service and professional solutions.

Call us for

special events

including

parades,

weddings,

rodeos, concerts,

horse shows,

tractor pulls,

demolition

derbies, camps,

picnics, and

much more.

Don’t forget to finance with M. J. Kelly’s in house financing, BARCO Finance.

Tired of waiting on hold or leaving voice mail? Not with M. J. Kelly

Company. We value your business and your time! We believe in per-

sonal service—knowledgeable professionals providing quick turn-

around on quotes. M. J. Kelly is celebrating 35 years of business. Like

you, we’ve weathered storms. Our growth is steady; our company is

strong; and our service is exemplary. We stand the test of time (yours

and ours). Call us for personal service and professional solutions.

Call us for

special events

including

parades,

weddings,

rodeos, concerts,

horse shows,

tractor pulls,

demolition

derbies, camps,

picnics, and

much more.

continued on page 36

agencynews

36 missouriagent may-june 2011

KNOWLEDGECOMES FROM EXPERIENCE

“I go the distance on my bike—just like my 30-year journey with J.M. Wilson. I lead a great team of managers and underwriters that work hard to help our agents be successful.”

Sandi Fritz, CIC Vice President, Underwriting and Branches—and fixture on the bike trail

Connect with Sandi on LinkedIn!

Managing General Agency Since 1920

Property/Casualty • Professional Liability • Surety Commercial Transportation • Personal Lines • Premium Finance

800.666.5692 jmwilson.com

sented to select independent insurance agen-cies, which meet specific criteria for written premium and sustained profitability.

Dysart Insurance Agency, Marshall, and Naught-Naught Insurance Agency, Eldon, have both been named to the 2010 President’s Club by MAIA Company Partner Grinnell Mutual Reinsurance Co. Each year, Grinnell honors its top 50 agencies achieving outstanding produc-tion and profitability over a five-year period.

Several member agencies have been recog-nized as 2011 Pinnacle Agencies by MAIA Com-pany Partner Columbia Insurance Group. The following agencies have met the production guidelines to qualify: Barker-Philips-Jackson,

Springfield; DeWitt Insurance, Manchester; Gene E. Wills Insurance Agency, Jackson; Insurance Consultants, Chesterfield; Naught-Naught Insur-ance Agency, Jefferson City; Plaza Insurance Cen-ter, Columbia; Scott Agency, Montgomery City; Smart Insurance Agency, Marionville; and Weiss Insurance Agency, Chesterfield.

Connell producer featured in SBJJay Hickman, Springfield, a producer with Connell Insurance, Hollister, was featured in the March 28-April 3, 2011, issue of Springfield Business Journal. The “5Q” column outlined Hickman’s entrepreneurial endeavors and his re-cent introduction into the insurance industry.

In memoriamJim Tate, Dexter, passed away March 16, 2011, at the age of 76. Tate began his career in insurance in 1958 as an underwriter. Eleven years later, he joined the Ben Cowan Insurance Agency, Dexter. When Mr. Cowan retired, Tate took ownership of the agency and merged with Countywide Insurance Agency, Dexter. He retired in 1999.

Tate was a member of the First Presbyterian Church, Dexter, a veteran of the United States Air Force, and a former Alderman for Dexter Ward 3. He leaves behind his wife, Shirley; two sons, Kevin and Keith; and one daughter, Kathy.

New faces, new placesDoug Anderson, Kansas City, has joined Lockton

Cos., Kansas City, as a senior vice president and producer.

Ryan Brown and Scott Schulte, St. Louis, have joined Lockton Cos., St. Louis, as producers.

Jay Hickman, Springfield, has joined Connell Insurance, Hollister, as a producer.

Tracy Musolf and Mark Seely, Kansas City, have been promoted at Lockton Cos., Kansas City, to practice leaders.

New membersAdvisor Assurance, Troy Hendee, RogersvilleThe Blue Chip Consortium, David Miller, Webster

GrovesCastillo Insurance Agency, Rob Castillo,

GladstoneInsurance directConnect, Marc Majnerich,

ChesterfieldLittlejohn and Associates, Randy Littlejohn, St.

LouisM&T Insurance Agency, Mark Tomlin, St. PetersNorth Missouri Insurance, Karen Lawson,

CameronRon Graham Insurance Agency, Cindy Politte,

Park Hills

agencynews continued from page 35

may-june2011 missouriagent 37

INSURANCE PROGRAMS.®

WINERYPAK

YOUR TOTAL WINERY INSURANCE SOLUTION.

Your business. Our specialty.

888-386-5701 • www.WineryPak.com© 2010 WineryPak, LLC. All rights reserved.UNDERWRITTEN BY MEMBER COMPANIES OF GREAT AMERICAN INSURANCE GROUP.

If you’re an insurance professional targeting the winemaking or distilled spiritsindustries, now you can provide more of the coverages your clients and prospectsneed, in one inclusive program.

WineryPak® offers coverage for:•WINERY AND VINEYARD OPERATIONS • SPECIAL EVENTS & HOSPITALITY• FARM & RANCH COVERAGES • BONDS • CROP INSURANCE • CYBER RISK

Berkshire Hathaway to acquire LubrizolBerkshire Hathaway and The Lubrizol Corp. have announced a definitive agreement for Berkshire Hathaway to acquire 100 percent of outstanding Lubrizol shares for $135 per share in an all-cash transaction. It will be one of the biggest acquisitions in Berkshire Hathaway his-tory. After the close of the transaction, which is expected to be completed during third quarter 2011, Lubrizol will operate as a subsidiary of Berkshire Hathaway.

QBE acquires Renaissance ReQBE has announced that it has completed its acquisition of the U.S. admitted insurance businesses of Renaissance Re, which include a U.S. crop and small specialist program insur-ance business. The acquisition supports QBE’s commitment to growing the business through product diversification and new distribution channels.

FCCI names new president, CEOThe board of directors for FCCI Insurance Group has announced that Craig Johnson, Sarasota, Fla., will become the new president and CEO of the company. Johnson will succeed G.W. Jacobs, who retires May 31. Johnson joined FCCI in 2003 and has since served in several leadership posi-tions. Jacobs is retiring after 12 years as presi-dent and 22 years of total service.

Columbia welcomes new VPThe board of directors for Columbia Insurance Group has appointed Bryon Smith, Austin, Texas, as vice president of the company. Smith will retain his position as branch manager in Austin, where he has accumulated 25 years of experience on all sides of the commercial prop-erty and casualty business.

The Hartford makes Most Ethical list, donates $100,000 to JapanThe Hartford is one of just five insurers to make the list of 112 companies deemed the “World’s

companypartnernews

continued on page 38

38 missouriagent may-june 2011