minutes of the meeting of the audit committee · minutes of the meeting of the audit committee ....

TRANSCRIPT

1

2

MINUTES OF THE MEETING OF THE AUDIT COMMITTEE

OF THE BAROSSA COUNCIL held on Tuesday 20 December 2016 , commencing at 11.37am in the

Council Chambers, 43-51 Tanunda Road, Nuriootpa 1. WELCOME

The Chair, Mr Peter Brass, welcomed everyone to the meeting at 11.37am. 2. PRESENT

Mr Peter Brass, Mr James Heuzenroeder, Ms Tanya Johnston, Cr John Angas, Cr Scotty Milne

Invited Staff Members Mr Martin McCarthy, Chief Executive Officer Ms Jo Thomas, Director Community Projects Ms Tania Paull, Acting Group Manager Corporate Services Ms Vicky Rohrlach, Acting Manager Financial Services Ms Nicole Rudd, Internal Control Compliance Officer Ms Annette Randall, Executive Assistant (Minute Secretary) In Attendance Ms Susan Law, Managing Director Australia, LKS Quaero Pty Ltd Mr Sam Robinson, Director Leadership and Culture, LKS Quaero Pty Ltd

3. APOLOGIES

Mr Mark Lague, Group Manager Corporate Services 4. CONFIRMATION OF MINUTES FROM PREVIOUS MEETING MOVED Ms Johnston that the Minutes of the Ordinary Audit Committee Meeting held 19 October 2016, be confirmed as a true and correct record of the proceedings of that meeting Seconded Mr Heuzenroeder CARRIED 2016-17/13 5. BUSINESS ARISING FROM PREVIOUS MINUTES Nil Mr Brass approved the request to consider the Confidential Report 9.1.1 at this point in the meeting so that the attending Consultants from LKS Quaero Pty Ltd could leave the meeting at the closure of the confidential matter.

3

9.1 CONFIDENTIAL MATTER – 11.38AM 9.1.1 SERVICE REVIEW PROJECT – PRESENTATION OF STAGE 1 DRAFT REPORT The matter of the agenda item being a Report on the commercial in confidence draft report for Stage 1 of the Service Review Project and pursuant to Section 90(3) (d) of the Local Government Act 1999 (“the Act”) being commercial information of a confidential nature (not being a trade secret) the disclosure of which— (i) could reasonably be expected to prejudice the commercial position of the person who supplied the information, or to confer a commercial advantage on a third party; and (ii) would, on balance, be contrary to the public interest; and being information that must be considered in confidence in order to ensure that the Audit Committee does not disclose commercially sensitive information while the Service Review Report is still in draft format and subject to further development and consideration. There is strong public interest in enabling members of the public to observe Council’s transparent and informed decision-making. This helps to ensure accountability, maintain transparency of public expenditure, facilitate public participation, assist public awareness and allow for the scrutiny of information. Attendance at an Audit Committee meeting is one means of satisfying this interest. The public will only be excluded from a Council meeting when the need for confidentiality pursuant to Section 90(2) of the Act outweighs the public interest of open decision-making. In this matter, the reason that receipt, consideration or discussion of the information or matter in a meeting open to the public would be contrary to the public interest is that it contains draft information in a format that relies on the commercial in confidence methodology and intellectual property of the consultant engaged to conduct the Service Review. On balance, the above reason which supports the need for confidentiality pursuant to Section 90(2) of the Act outweighs the factors in favour of the public interest of open decision-making. MOVED Cr Milne that the Audit Committee, (1) Under the provisions of Section 90(2) of the Local Government Act 1999, make

an order that the public be excluded from the meeting with the exception of the Chief Executive Officer, Community Project Director, Acting Group Manager Corporate Services, Acting Manager Financial Services, Internal Control Compliance Officer, Managing Director Australia and Director, Leadership and Culture of consultants LKS Quaero Pty Ltd, and the Minute Secretary, in order to consider in confidence a report relating to the Service Review Project, Presentation of Stage 1 Draft Report and in accordance with Section 90(3) (d) of the Local Government Act 1999 (“the Act”) being commercial information of a confidential nature (not being a trade secret) the disclosure of which— (i) could reasonably be expected to prejudice the commercial position of the person who supplied the information, or to confer a commercial advantage on a third party; and (ii) would, on balance, be contrary to the public interest;

(2) Accordingly, on this basis, the Audit Committee is satisfied that public interest in

conducting meetings in a place open to the public has been outweighed by the need to keep the information and discussion confidential to comply with the

4

Audit Committee’s obligation not to release draft report information in a format that relies on the commercial in confidence methodology and intellectual property of the consultant (LKS Quaero Pty Ltd) engaged to conduct the Service Review.

Seconded Mr Heuzenroeder CARRIED 2016-17/14

RESUMPTION OF OPEN COMMITTEE MEETING – 1.05PM The open meeting of the Committee resumed at 1.05pm. Ms Law and Mr Robinson left the meeting at this time.

In the matter 9.1.1 – Service Review Project – Presentation of Stage 1 Draft Report, MOVED Cr Milne that the Audit Committee: (1) Confidential Resolution (2) Confidential Resolution (3) Confidential Resolution (4) Confidential Resolution (5) Confidential Resolution (6) Having considered this matter in confidence under Section 90(2) and 90(3)(d) of

the Local Government Act 1999, makes an order pursuant to Section 91(7), that the agenda report, associated documents and minutes, other than the minutes relating to this confidentiality order of the Confidential Audit Committee Meeting held on 20 December 2016 in relation to confidential item 9.1.1 Service Review Project, Presentation of Stage 1 Draft Report, be kept confidential and not available for public inspection other than information required to be released in accordance with any relevant requirements of Section 91(8) of the Local Government Act 1999: and

(7) In accordance with (6) above and section 91(9)(c) of the Local Government

Act 1999, authorises the Chief Executive Officer to review and revoke the order. Seconded Mr Heuzenroeder CARRIED 2016-17/15

6. CONSENSUS AGENDA 7. ADOPTION OF CONSENSUS AGENDA

7.1 ITEMS FOR EXCLUSION FROM THE CONSENSUS AGENDA Nil

7.2 RECEIPT OF CONSENSUS AGENDA

5

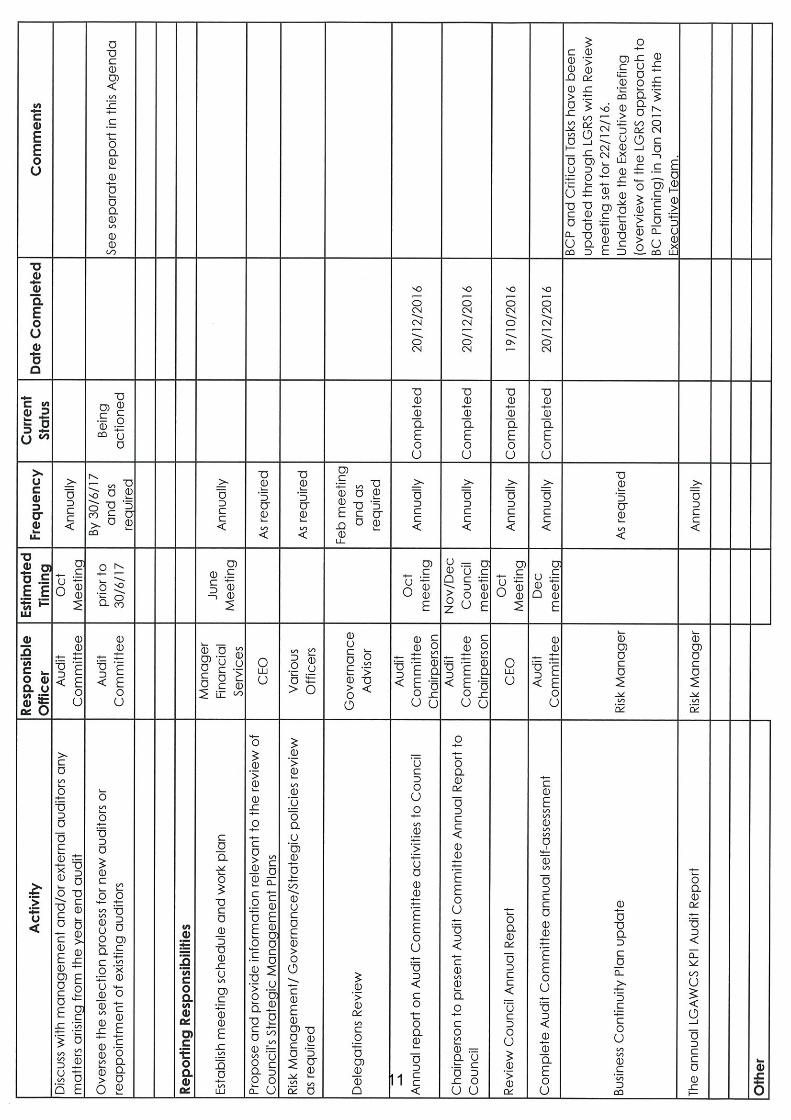

MOVED Mr Heuzenroeder that the items contained in the Consensus Agenda be received and that any recommendations contained therein be adopted. Seconded Cr Angas CARRIED 2016-17/16 8. DEBATE AGENDA 8.1.1 DRAFT AUDIT COMMITTEE 2017 WORK PLAN B4256 Mr Brass requested that the Work Plan be aligned to the financial year rather than the calendar year and include timing of meetings. He also suggested that officers contact the external auditors and request their planned audit dates for 2017. Mr Brass will liaise further with Mr Lague in regard to suitable dates. MOVED Mr Heuzenroeder that the Audit Committee approve the draft Audit Committee Work Plan for 2017, subject to alignment with the financial year and inclusion of dates. Seconded Ms Johnston CARRIED 2016-17/17 PURPOSE Draft Audit Committee Work Plan for 2017 is provided for approval. REPORT The draft work plan has been formulated based on a model developed by the Local Government Association. The work plan has been prepared to include all proposed reports, policy reviews, compliance reviews for 2017 and will be used for action tracking during 2017. ATTACHMENTS OR OTHER SUPPORTING REFERENCES Attachment: Audit Committee Work Plan 2017 COMMUNITY PLAN / CORPORATE PLAN / LEGISLATIVE REQUIREMENTS

Corporate Plan

How We Work – Good Governance

6.2 Ensure that Council’s policy and process frameworks are based on principles of sound

governance and meet legislative requirements. 6.16 Provide contemporary internal administrative and business support services in accordance with

mandated legislative standards and good practice principles.

Legislation

Local Government Act 1999 – Section 126 FINANCIAL, RESOURCE AND RISK MANAGEMENT CONSIDERATIONS Adoption and adherence to an annual work plan is a risk management tool. COMMUNITY CONSULTATION Not required under legislation or Council’s Public Consultation Policy.

6

ACTIONS: • Acting Manager Financial Services align the Work Plan for 2017 to the financial year and

include dates. • Acting Manager Financial Services to request planned audit dates from the external auditors.

10.1 AUDIT COMMITTEE ACTION TRACKING MOVED Cr Milne that the progress of the Audit Committee Action Tracking report be received. Seconded Cr Angas CARRIED 2016-17/18 11. OTHER BUSINESS Nil 12. NEXT MEETING To be advised. 13. CLOSURE OF MEETING There being no further business, Mr Brass wished everyone a Merry Christmas and healthy and safe New Year and closed the meeting at 1.10pm.

Confirmed:

Chairman: ...................................... Date: .............................

7

AUDIT COMMITTEE

REPORTS FOR INFORMATION

28 FEBRUARY 2017

CONSENSUS AGENDA

6.1 REPORTS FOR INFORMATION

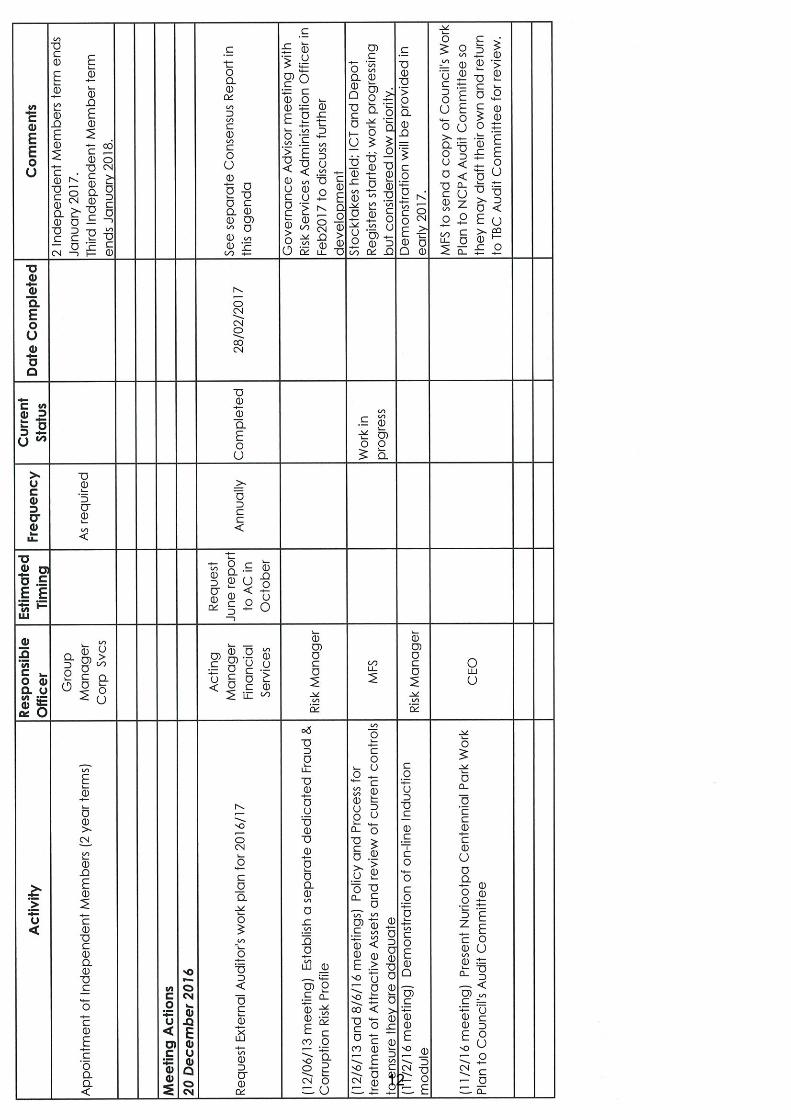

6.1.1 UPDATED AUDIT COMMITTEE WORK PLAN The following was resolved at the 20 December 2016 Audit Committee meeting: MOVED Mr Heuzenroeder that the Audit Committee approve the draft Audit Committee Work Plan for 2017, subject to alignment with the financial year and inclusion of dates. Seconded Ms Johnston CARRIED 2016-17/17” The updated Audit Committee Work Plan is attached. Please also note that the Action Tracking document has been incorporated into the Work Plan so that we have all work/actions in one location.

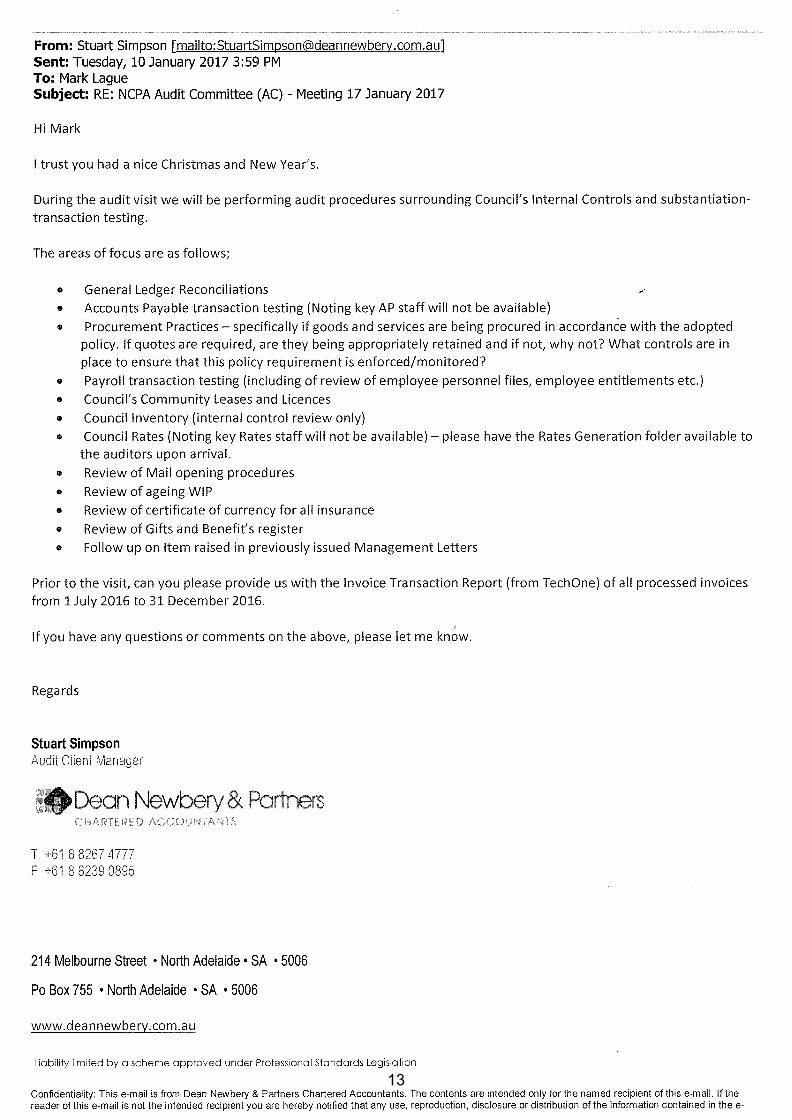

6.1.2 DEAN NEWBERY & PARTNERS – INTERIM AUDIT WORK PLAN As requested by the Audit Committee at the 20 December 2016 meeting, Dean Newbery & Partners have provided a work plan for the current interim audit. (Copy attached.)

6.1.3 LOCAL GOVERNMENT (BUILDING UPGRADE AGREEMENTS) REGULATIONS 2016 An excerpt from the Council Meeting Minutes of 24 January 2017, in relation to the Local Government (Building Upgrade Agreements) Regulations 2017, is attached. The full report is available on Council’s website (Link provided here: Agenda Council Meeting 24 January 2017 – page 13).

6.1.4 THE BAROSSA COUNCIL QUARTER 2 – 2016-17 PERFORMANCE REPORT

A copy of the report to the 21 February 2017 Council Meeting in relation to The Barossa Council Quarter 2 – 2016-17 Performance Report, is available on Council’s website (Link provided here: Agenda Council Meeting 21 February 2017 – page 86).

6.1.5 PROGRESS REPORT – RISK MANAGEMENT & WORKPLACE HEALTH AND SAFETY

A Progress Report on Risk Management and Workplace Health and Safety is attached.

RECOMMENDATION: That Reports for Information items 6.1.1 to 6.1.5 be received.

8

9

10

11

12

13

5.1 DEBATE OF ITEMS EXCLUDED FROM THE CONSENSUS AGENDA 4.3.1 GROUP MANAGER CORPORATE SERVICES - CONSENSUS 4.3.1.1 LOCAL GOVERNMENT (BUILDING UPGRADE AGREEMENTS) REGULATIONS 2016 B4692 The State Government’s consultation on its proposed Building Upgrade Finance scheme, of which the draft Local Government (Building Upgrade Agreements) Regulations 2016 (“the Regulations”) are a part, concluded on 20 January 2017. A copy of the draft Regulations is attached for Members’ information. Also attached, is a fact sheet on the Building Upgrade Finance (“BUF”) mechanism. In summary, the purpose of BUF is to help building owners to access loans to improve the energy, water and environmental efficiency of existing commercial buildings (and industrial, etc). In an Australian first, heritage works to or within heritage buildings, including works associated with Building Code and disability access compliance, will be eligible to access the mechanism. Residential buildings are not eligible to access the mechanism. Under the BUF mechanism, a local council, a commercial building owner and a financier can voluntarily enter into a building upgrade agreement. Under this agreement, the building owner agrees to undertake upgrade works in respect of their building, the financier agrees to advance money to the building owner for the purpose of funding the upgrade works, and the council agrees to declare a building upgrade charge against the land on which the building is situated. This charge is then paid by the building owner to the council a repayment of finance. The council then passes the repayment on to the financier once received from the building owner. As a result of the arrangement, the loan is effectively tied to the property rather than the property owner. In the event of the transfer of ownership of the property, the charge can remain with the property if the purchaser so agrees. The building upgrade charge effectively secures the loan, as it is ranked in priority to mortgages and liabilities to the Crown should the council exercise its statutory power of sale in respect of the charge. This provides heightened security to financiers, allowing them to offer the finance to building owners on more attractive terms. The Corporate Management Team has been considering the proposed legislation and processes in regard to additional resources and systems required to establish, maintain, operate, register and report on the additional arrangements.

Cr Milne referred to the draft Local Government (Building Upgrade Agreements) Regulations 2016 and asked whether there was compulsion upon Council to be involved or is there an option to opt out if they choose.

Mr Mark Lague, Group Manager Corporate Services advised that the draft Regulations consultation phase has recently concluded and that further information will be provided to Council as it comes to hand. MOVED Cr Milne that the report 4.3.1.1 be received and that further information on the draft Local Government (Building Upgrade Agreements) Regulations 2016 be provided to Council when it is available. Seconded Cr Miller CARRIED 2014-18/905

14

INTERNAL AUDIT COMMITTEE RISK MANAGEMENT REPORT – February 2017

15

Risk Management Framework The Risk Management Framework has finished its Consultation period and has been reviewed by CMT with several requirements for simplification requested. ControlTrack/Risk Manager/ Sky Trust The Control Track “Risk Manager” project has now been suspended. The preliminary work that was undertaken to start populating parts of the Organisations risk register in the Risk Manager platform is now being used to trial a new platform called “Sky Trust”. Council has developed a Project Scope for the potential Implementation of the Sky Trust Intelligence System. The system will primarily be used for an injury, incident and hazard management software solution for The Barossa Council with further functions available. These functions include Human Resource Management, Training Management, Quality Management, Contractor Management, Project Management, Asset Management and Internal Audit Management. All these functions have been made available to Council via a LGAWCS funded initiative and there would be significant benefit to our organisation in the future integration of these functions. Mutual Liability Claims

Mutual Liability Claim – 1/10/16 to 31/12/16 Current claims 21 Open Mutual Liability Claims as at 31/12/16. Finalised claims 4 MLS finalized during 1/10/16 to 31/12/16:-

1. McCrystal – Discontinuance of Plantiff’s and WorkCover recovery claim against Council.

2. Gripton – Denial letter issued from MLS. 3. Hakkareinen – Successful claim against

Council – Paid $2,500 to claimant. 4. Marion – Claimant decided not to claim

against Council.

2016 KPI Audit and 2017 KPI Action Plan The 2016 KPI Audit was undertaken on the 19th December 2016 with LGAWCS Regional Risk Coordinator – Murray Mallee Region. The audit scope involved 11 sub-elements of the PSSI and 14 sub - elements of the IM standards from the Code of Conduct. Over the 25 sub - elements Council received 19 conformances, 3 observations and 3 non – conformances. The non-conformances included;

• 2.1.1 Legislative Compliance • 3.7.1 Contingency Planning • 3.8.6 Contractor Management Systems

These non - conformances have been addressed in the 2017 Draft KPI Action Plan that will be presented to CMT in March 2017 and then submitted to The LGAWCS for approval.

16

AUDIT COMMITTEE

CORRESPONDENCE

28 FEBRUARY 2017

CONSENSUS AGENDA 6.2 CORRESPONDENCE

6.2.1 UPDATED INFORMAL GATHERINGS POLICY Further to Correspondence item 6.2.2 of the 20 December 2016 Audit Committee meeting, attached is subsequent correspondence from Council’s Governance Officer to the Chair of the Audit Committee regarding an update to the Informal Gatherings Policy.

RECOMMENDATION: That Correspondence item 6.2.1 be received.

17

18

19

20

21

22

23

AUDIT COMMITTEE

COORDINATOR INTERNAL CONTROL

28 FEBRUARY 2017 8.1 DEBATE AGENDA 8.1.1 INTERNAL FINANCIAL CONTROL REPORT

B343 PURPOSE To provide an update on internal control work performed since the last Audit Committee meeting.

RECOMMENDATION That the report on Internal Financial Controls be received and noted. REPORT Attached is a copy of the Internal Financial Control Report for October 2016 to January 2017.

ATTACHMENTS OR OTHER SUPPORTING REFERENCES Supporting References Local Government Act 1999 – Section 125, 126, 129 (1) (b) Local Government (Financial Management) Regulations 2011, 14(e) COMMUNITY PLAN / CORPORATE PLAN / LEGISLATIVE REQUIREMENTS Community Plan

How We Work – Good Governance

Corporate Plan How We Work – Good Governance 6.2 Ensure that Council’s policies and process frameworks are based on principles of sound governance and meet legislative requirements. 6.4 Ensure that decisions regarding expenditure of Council’s budget are based on an assessment of whole of life costs, risks associated with the activity and advice contained within supporting plans. Legislative Requirements Local Government Act 1999 – Section 125, 126, 129 (1) (b) Local Government (Financial Management) Regulations 2011, 14(e) FINANCIAL, RESOURCE AND RISK MANAGEMENT CONSIDERATIONS The regular monitoring and review of Council’s financial internal controls and risk assessments will significantly facilitate the on-going safeguarding of Council assets. The control and review of risks is a core officer function and responsibility. The introduction of the new system supports officers by providing a consistent framework and process. COMMUNITY CONSULTATION Not required under legislation or Council’s Public Consultation Policy.

24

THE BAROSSA COUNCIL

INTERNAL FINANCIAL CONTROL REPORT

Responsible: Coordinator - Internal Control

TRIM Reference: 17/10906

Presented to… CMT: Audit Committee:

23 February 2017 via email 28 February 2017

Last Report Presented: 19 October 2016

Period: October 2016 to January 2017

Prepared by: Nicole Rudd – Coordinator Internal Control

Legislative Requirement Local Government Act, 1999 Local Government (Financial Management) Regulations 2011

• Section 125 - Part 2, Regulation 4(2), (4), (5) (a-c) • Section 129(1)(b) - Part 6, Division 1, Regulation 19 (1)(b), (2), (3) • Section 129 (3) (b) • Section 130

The following report has been developed to assist the Corporate Management Team (CMT) in the monitoring, action and review of the Internal Financial Control function of Council. This report is also provided to the Audit Committee for information on the status of Internal Financial Control.

1. Internal Financial Control Self-Assessment - ControlTrack ControlTrack is a self-assessment tool used to assess and review Council’s Internal Financial Controls which facilitate the management of risks in relation to the financial operations of Council. Given that the newly developed Control Manager tool (to replace ControlTrack) is still in the pilot phase (and not being tested by us), we have decided to stay with the existing ControlTrack software to carry out this next self-assessment. We have developed a 3 year cycle (based on what has been happening) for the assessment of the controls relating to financial risks of Council as per the following: 1st year: All financial risks and controls to be assessed/reviewed and rated. 2nd year: All Extreme/High rated risks and their associated controls to be assessed/

reviewed and rated. Any controls that were assigned to a new assessor (eg new staff/change in role)

Any controls that were not assessed in the last cycle. 3rd year: All Extreme/High rated risks and their associated controls to be assessed/

reviewed and rated. Any controls that have had incomplete action plans against them from the

last cycle. 4th year: Begin new cycle – same as 1st year.

25

We are in our 3rd year of the cycle and will progress with having all the Extreme/High rated risks assessed together with any controls which have outstanding action plans against them. This body of work will begin at the beginning of March 2017 with a targeted end date of 30 June 2017. This cycle may change depending on the new software release. Further information to be provided when it comes to hand. 2. External audits/correspondence from Auditors, Dean Newbery & Partners Interim ‘Internal Control’ Audit The 1st interim audit by Dean Newbery & Partners was carried out on the 17/18 January 2017. A response from the Auditors is yet to be received. 3. Inspections/Internal Audits /Compliance Testing/Reviews 3.1 Accounts Payable

a) The process for checking and authorising accounts payable payments has been reviewed and documented. This will ensure there is a consistent approach to the way each of the Authorisers carry out this task each time the task is carried out. As part of this process – further internal control testing is now in place.

b) There is now a checking process in place to ensure that there have not been any changes to the bank file extracted from Technology One to the file that is uploaded for payment at the bank.

3.2 Financial Delegations

An internal review of the financial delegations applied within the Technology One Financials compared to the Delegations Register will begin shortly. Any anomalies will be corrected and reported back to CMT. We are working on an automated scheduled report which will be delivered to Finance Staff on a regular basis to action a check of the delegations.

4. Incidents and Corrective & Preventative Actions (CAPA) Incident

ID # Identifying

Source Directorate CAPA required?

CAPA ID #

CAPA Completed?

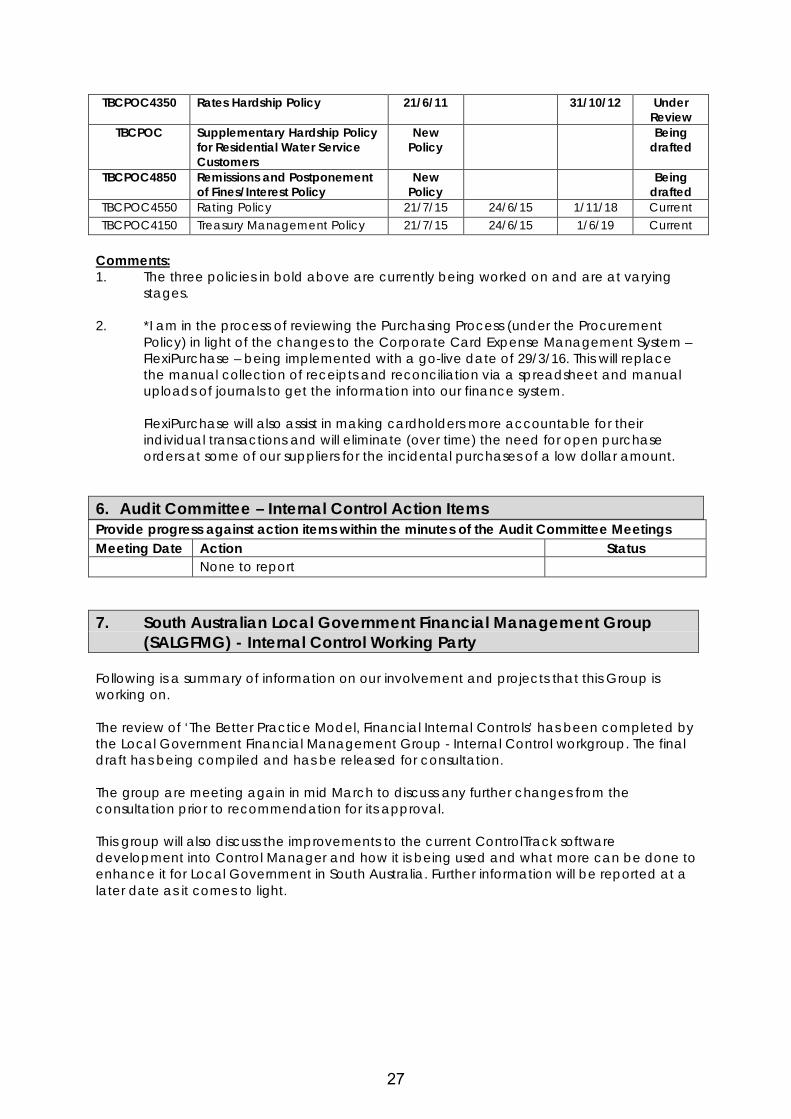

Nothing further to report 5. Finance Policy & Process Development/Review

Document Register Code

Finance Document Council

Approval Date

Audit Committee

Date Review

Date Status

TBCPOC4050 Asset Accounting Policy 21/6/16 19/10/16 26/6/18 Current TBCPOC4400 Budget and Business Plan and

Review Policy 10/9/14 29/10/14 10/9/17 Current

TBCPOC4450 Community Assistance Scheme Policy

21/10/15 N/A 1/6/19 Current

TBCPOC4650 Debt Recovery Policy 21/7/15 24/6/15 1/11/18 Current TBCPOC4750 Disposal of Land and Other

Assets Policy 10/9/14 29/10/14 10/9/18 Current

TBCPOC4200 Funding Policy 21/7/15 24/6/15 1/6/19 Current TBCPOC4050 Procurement Policy * 21/6/16 19/10/16 30/6/18 Current TBCPOC4700 Prudential Management Policy 15/7/14 29/10/14 15/7/17 Current

26

TBCPOC4350 Rates Hardship Policy 21/6/11 31/10/12 Under Review

TBCPOC Supplementary Hardship Policy for Residential Water Service Customers

New Policy

Being drafted

TBCPOC4850 Remissions and Postponement of Fines/Interest Policy

New Policy

Being drafted

TBCPOC4550 Rating Policy 21/7/15 24/6/15 1/11/18 Current TBCPOC4150 Treasury Management Policy 21/7/15 24/6/15 1/6/19 Current

Comments: 1. The three policies in bold above are currently being worked on and are at varying

stages. 2. *I am in the process of reviewing the Purchasing Process (under the Procurement

Policy) in light of the changes to the Corporate Card Expense Management System – FlexiPurchase – being implemented with a go-live date of 29/3/16. This will replace the manual collection of receipts and reconciliation via a spreadsheet and manual uploads of journals to get the information into our finance system.

FlexiPurchase will also assist in making cardholders more accountable for their

individual transactions and will eliminate (over time) the need for open purchase orders at some of our suppliers for the incidental purchases of a low dollar amount.

6. Audit Committee – Internal Control Action Items Provide progress against action items within the minutes of the Audit Committee Meetings Meeting Date Action Status None to report

7. South Australian Local Government Financial Management Group

(SALGFMG) - Internal Control Working Party Following is a summary of information on our involvement and projects that this Group is working on. The review of ‘The Better Practice Model, Financial Internal Controls’ has been completed by the Local Government Financial Management Group - Internal Control workgroup. The final draft has being compiled and has be released for consultation. The group are meeting again in mid March to discuss any further changes from the consultation prior to recommendation for its approval. This group will also discuss the improvements to the current ControlTrack software development into Control Manager and how it is being used and what more can be done to enhance it for Local Government in South Australia. Further information will be reported at a later date as it comes to light.

27

AUDIT COMMITTEE

GROUP MANAGER, CORPORATE SERVICES REPORTS

28 FEBRUARY 2017 8.1 DEBATE AGENDA 8.1.2 TREASURY MANAGEMENT REVIEW

B2237 PURPOSE Pursuant to Section 140 of the Local Government Act 1999, and in accordance with Council’s Treasury Management Policy, Council must undertake an annual performance review of its Treasury Management activities.

RECOMMENDATION That the report on Council’s 2016 Treasury Management activities be received and noted.

REPORT The key principles within Council’s Treasury Management Policy are as follows: Council will: • Maintain target ranges for its Net Financial Liabilities ratio; • Generally only borrow funds when it needs cash and not specifically for particular

projects; • Not retain and quarantine money for particular future purposes unless required by

legislation or agreement with other parties; • Apply any funds that are not immediately required to meet approved expenditure

(including funds that are required to be expended for specific purposes but are not required to be kept in separate bank accounts) to reduce its level of borrowings or to defer and/or reduce the level of new borrowings that would otherwise be required.

Comments regarding the 2016 performance with regard to the above principles are outlined below:

Net Financial Liabilities Ratio Council’s policy regarding its net financial liabilities is that they shall not exceed 100% of total operating revenue (adopted February 2010). As at 30 June 2016, Council’s net financial liabilities represented 29% of total operating revenue, and it is projected to increase to 41% as at 30 June 2017. Accordingly, Council is currently operating within its policy threshold.

28

Loan Borrowings Council’s policy relative to loan borrowings states that the use of internal reserves be considered prior to consideration of external loan borrowings. A second cash advance debenture facility with variable interest rate was set up for Nuriootpa Centennial Park Authority to a maximum value of $260,000. The total variable borrowings are now $1,260,000 and are fully drawn down as of May 2016. There were no new fixed borrowings in 2016. The use of internal cash reserves has continued to be used in funding Council’s capital works programs and has subsequently minimised the net interest cost to Council. A summary of the fixed interest rate borrowings are shown below:

Debenture Loan Summary

No. Loan Amount

Interest Rate

Final Payment Date

Principal Outstanding as at 31 December 2016

94 1,500,000 6.75% 16/09/17 152,791 96 2,000,000 6.02% 15/05/18 288,945 97 700,000 5.65% 16/06/18 99,081 98 2,000,000 6.65% 15/01/19 482,663

100 1,954,200 6.45% 15/03/20 633,985 101 2,500,000 6.24% 15/03/21 1,002,950 102 5,000,000 6.62% 16/10/21 2,228,717 103 100,000 6.80% 15/11/21 44,880 104 2,900,000 6.90% 15/03/22 1,414,321 105 7,000,000 7.02% 16/11/24 5,538,892 106 2,000,000 6.85% 15/04/26 1,486,520 107 113,000 4.75% 16/07/22 74,039 108 515,000 6.20% 15/01/34 479,481 109 125,000 5.30% 15/09/29 113,431

14,040,696

A summary of the variable interest rate borrowings are shown below:

Cash Advance Loan Summary (Nuriootpa Centennial Park Authority)

No. Total Facility Loan Amount

Current Interest Rate

Facility End Date

Principal Outstanding as at 31 December 2016

CA110 1,000,000 3.75% 15/06/20 1,000,000 CA111 260,000 3.75% 15/03/21 260,000

1,260,000

29

Investments Council currently holds investments with National Australia Bank (NAB) and the Local Government Finance Authority (LGFA). Council’s total investments as at 31 December 2016 were:

Variable Interest Rate

$’000

< 1 year Fixed $’000

> 1 year < 5 years

$’000

> 5 years $’000

TOTAL $’000

Interest Rate Range

LGFA

2,312

6,244

0

0

8,556

1.50% to

2.35% NAB Investment A/c

4,454

0

0

0

4,454

2.00% to

2.25% TOTAL

6,766

6,244

0

0

13,010

The level of funds invested during the year is presented in the graph below. The graph excludes Council’s separate operating bank account which was maintained at minimum working capital levels in accordance with the Policy.

ATTACHMENTS OR OTHER SUPPORTING REFERENCES Policy Treasury Management Policy

COMMUNITY PLAN / CORPORATE PLAN / LEGISLATIVE REQUIREMENTS Corporate Plan

How We Work – Good Governance

6.2 Ensure that Council’s policy and process frameworks are based on principles of sound

governance and meet legislative requirements. 6.3 Align operational strategy to strategic objectives and measure organisational

performance to demonstrate progress towards achieving our goals.

30

6.16 Provide contemporary internal administrative and business support services in accordance with mandated legislative standards and good practice principles.

Legislative Requirements Local Government Act 1999, Section 140

FINANCIAL, RESOURCE AND RISK MANAGEMENT CONSIDERATIONS Financial A review of investments and borrowings is required as per the Treasury Management Policy and Local Government Act.

COMMUNITY CONSULTATION No separate consultation is required under Council’s Public Consultation Policy.

31

AUDIT COMMITTEE

GROUP MANAGER, CORPORATE SERVICES REPORTS

28 FEBRUARY 2017

8.1 DEBATE AGENDA 8.1.3 2017/18 AUDIT COMMITTEE BUDGET

B343 PURPOSE To consider a draft 2017/18 budget for the Committee’s operations. RECOMMENDATION That the 2017/18 Consultant budget of $XXX and Training budget of $XXX be endorsed for consideration by Council. REPORT The budget for 2017/18 is being prepared by completing the base budget for activities that are externally and internally required by the Audit Committee. In the Audit Committee budget, two items that require review are Consultant and Training/Seminar expenditure. In the past, consultants have been used to undertake reviews and compliance checks for taxation and accounting, along with purchase and implementation of the internal control tracking tool. The training budget has previously been used by independent members to attend LGA programs. A proposed 2017/18 budget to support the operations of the Audit Committee is outlined in the following table: Audit Committee Financial Statement as at 6 January 2017:

January YTD

Actuals

Original Budget

2016/17 + Q1 Adj

January YTD

Budget % YTD

Draft 2017/18 Budget

496 - Audit Committee Salaries (preparation of reports/agendas, attendance at meetings – CEO, Director C&CS, Manager Financial Services, Minute Secretary) 7,387 14,455 51% 14,816

*

Consultants (provision for sundry project work undertaken as part of Committee work plan or specifically requested by Council) 0 0 0% 0

~

Training / Seminar expenses 0 1,000 0% 1,000 ~

Sitting Fees (Independent Members) 2,150 5,550 39% 5,615 # Advertising 0 500 0% 500 ~ Insurance & Other 531 526 100% 545

Total 496 - Audit Committee 10,068 22,031

46% 22,476

32

* Provides for 2.5% increase for salary costs as per current Enterprise Agreement. Depending

on cost centre allocations, this amount may change when the budget is finalised. ~ Training and advertising expenses are set at the same amounts as the previous budget and

may change after review by Council. # Provides for Sitting Fees as follows: Chairperson $555, Independent Members x 2 - $355 to

attend 4 meetings each and the annual report attendance at Council meeting for the Chairperson; to be adopted by Council – only provided for Audit Committee members information.

ATTACHMENTS OR OTHER SUPPORTING REFERENCES Policy Budget & Business Plan and Review Policy COMMUNITY PLAN / CORPORATE PLAN / LEGISLATIVE REQUIREMENTS Corporate Plan

How We Work – Good Governance

6.4 Ensure that decisions regarding expenditure of Council’s budget are based on an

assessment of whole of life costs, risks associated with the activity and advice contained within supporting plans.

6.16 Provide contemporary internal administrative and business support services in accordance with mandated legislative standards and good practice principles.

Legislative Requirements Local Government (Financial Management) Regulations 2011 - Reg 9(1)(b) LGA Information paper no. 25 – Monitoring Council Budget Performance FINANCIAL, RESOURCE AND RISK MANAGEMENT CONSIDERATIONS Financial Funding to support the operations of the Audit Committee is required to ensure resources are adequate to undertake this vital role within Council and is included in the annual budget.

COMMUNITY CONSULTATION Will be included as part of the draft 2017/18 Budget/Business Plan consultation and adoption process.

33

AUDIT COMMITTEE

GROUP MANAGER, CORPORATE SERVICES REPORTS

28 FEBRUARY 2017 8.1 DEBATE AGENDA 8.1.4 MID-YEAR BUDGET REVIEW 2016/17 (AS AT 31 DECEMBER 2016)

B2734 PURPOSE The Mid-year Budget Review for 2016/17 (as at 31 December 2016) was presented to Council at its 21 February 2017 Council Meeting, and the budget variations contained therein were adopted. RECOMMENDATION That the Mid-year Budget Review for 2016/17 (as at 31 December 2016) be received. REPORT The report provides information as to the financial position of Council, containing budget update reports which include Executive Summary, Uniform Presentation of Finances, Key Performance Indicators, Summary of Operating Budget Variance Adjustments and Summary of Capital Budget Variance Adjustments. The proposed variances between the original budget and this budget update are listed on the operating and capital budget adjustment pages. The report also includes details of new initiatives and capital expenditure adjustments. ATTACHMENTS OR OTHER SUPPORTING REFERENCES Attachment 1: Mid-year Budget Review as at December 2016 Policy Budget & Business Plan and Review Policy COMMUNITY PLAN / CORPORATE PLAN / LEGISLATIVE REQUIREMENTS Corporate Plan

How We Work – Good Governance

6.2 Ensure that Council’s policy and process frameworks are based on principles of

sound governance and meet legislative requirements. 6.3 Align operational strategy to strategic objectives and measure organisational

performance to demonstrate progress towards achieving our goals. 6.4 Ensure that decisions regarding expenditure of Council’s budget are based on an

assessment of whole of life costs, risks associated with the activity and advice contained within supporting plans.

6.9 Provide access to Council’s plans, policies and processes and communicate with the community in plain English.

34

6.16 Provide contemporary internal administrative and business support services in accordance with mandated legislative standards and good practice principles.

Legislative Requirements Local Government Act 1999 Sect 123 (13) Local Government (Financial Management) Regulations 2011 Regulation 9 (1)(a) FINANCIAL, RESOURCE AND RISK MANAGEMENT CONSIDERATIONS Financial To enable Council to make effective and strategic financial decisions, a quarterly budget review report is provided. This report contains budget adjustments for decisions Council has made since the last review and other adjustments to meet financial changes in capital and/or operational areas. The document contains comments and implications for the Long Term Financial Plan as a result of this review.

COMMUNITY CONSULTATION Community Consultation was part of the original budget adoption process in June 2016, as per legislation.

35

Mid-year Budget Review 2016-17 – as at 31 December 2016 | The Barossa Council | Page 1

Annual Budget and Business Plan 2016-17

Mid-year Budget Review As at 31 December 2016

Budget Update Report

Executive Summary 2

Uniform Presentation of Finances 3

Key Performance Indicators 4

Summary of Operating Budget Variance Adjustments 5

Summary of Capital Budget Variance Adjustments 9

Statement of Comprehensive Income 11

Statement of Financial Position 12

Statement of Changes in Equity 13

Statement of Cash Flows 14

Annual Business Plan Report

Operating Result – The Barossa Council (Includes New Initiatives - Operating) 15

Subsidiary Result – Nuriootpa Centennial Park Authority (NCPA) 16

Functional Reporting Operating Expenditure 17

Capital Works Program 18

36

Financial Statements - Actual Report

Executive Summary This report is a Mid-year Budget Review as at 31 December 2016 for the 2016-17 financial year pursuant to Regulations 7, 9 and 10 of the Local Government (Financial Management) Regulations 2011 under the Act. Unless otherwise indicated figures shown are for the 2016-17 financial year and the variance report comparison is actual to original budget.

The proposed Revised Budget adjustments include a number of ‘one-off’ variations shown as Favourable (F) or Unfavourable (U). Only larger variances are highlighted below. For further details and information on the note numbers refer to variance adjustments on pages 3 and 5-10 within this report.

(1-6) Decrease in accommodation income at Nuriootpa Centennial Park $35k (U); Warren Reservoir Project grant funding now treated as Operating $245k (F); Warren Reservoir Project additional funding $70k (F); Grassy Groundcover Project change in funding basis (net) $181k (F); Increased interest income on Council’s investments $27k (F); Workers Compensation and Income Protection recoupments more than budgeted $54k (F); Reduction in Visitors Centre booking commissions $8k (U). Net $548k (F).

(7-9) Reduction in Nuriootpa Centennial Park expenses due to reduced accommodation occupancy rates $39k (F); Net Increase in Waste Levy and Recycling expenditure $19k (U); Warren Reservoir Project expenditure $415k (U); Increase in Street Lighting charges $67k (U); Mount Pleasant Golf Club contribution $15k (U); Grassy Groundcover Project expenditure $84k (U); Reduction in Depreciation charge $190k (F). Net $406k (U).

(10) Resheeting budget reallocated to Footpath Upgrade Program $136k (F); Increase in costs for CWMS Jetter Truck $11k (U); Reduction in Resheet Budget due to revised program $145k (F). Net $279k (F).

(11) Williamstown Hall Lighting Project $13k (U); Increased costs in Hoffnungstahl Road Seal upgrade $145k (U); Warren Reservoir Project expenditure now Operating $345k (F). Net $51k (F).

(12-13) Warren Reservoir Project grant funding now Operating $245k (U); Williamstown Hall Lighting Project contribution $13k (F); NBN costs in respect of Land held for Sale $11k (U). Net $243k (U).

Long Term Financial Plan (LTFP) - Review

Since the adoption of the Budget, Council has made decisions on projects that have material financial implications not only for the 2016-17 year (these are included within the yearly budget wherever possible) but also may effect the longer term. In some cases not all information is available for these projects and not included in the budget review. The following list is a summary of these types of projects:

A review of the Council’s Asset condition, useful and remaining lives to more accurately reflect the actual service needs and consumption of the assets will continue. It is expected that Council’s understanding and management of this important function could potentially improve the operating result in the LTFP. Selected asset types are made of two components mainly within the transport asset class. The second component being a long life asset. Current practice in the past is not to depreciate these second components. Council's initial review and findings are that if the long life application was applied to the second component and additionally applied to asset types that have not had a long life component, depreciation may in fact be reduced in future years. A long life will be assessed, assigned and then attached to the second asset component for relevant asset types during 2016-17.

Use of Discretionary fundings from future years may affect other available funds/restrict other service expansion.

37

Mid-year Budget Review 2016-17 – as at 31 December 2016 | The Barossa Council | Page 3

($'000)

938

(3,809)

(1,013)

39

(3,845)Proposed Full- year Revised Budget - Net Lending / (Borrowing)

Funding Source for the movement in Net Lending / (Borrowing)Original Full year Budget Net Lending / (Borrowing)

Carried Forward Budget Adjustments – Report on Financial Results.

Funds were held for these projects in cash and investments at 30 June 2016

Other Budget Adjustments - September Budget Update. Funds required for these items will decrease Councils cash and

investments. This amount includes amendments approved at the Council meetings held July and August 2016; refer to

information on Budget Variance Adjustments within this report .

Budget Adjustments - December Mid-year Budget Review. Funds required for these items will increase Councils cash and

investments

($'000) ($'000) ($'000) ($'000) ($'000)

1-6 36,446 32,627 37,083 548 37,631

7-8 35,616 16,595 36,343 406 36,749

830 16,032 740 142 882

10 5,301 1,757 8,261 (279) 7,982

9 7,502 3,751 7,502 (190) 7,312

425 149 425 0 425

(2,626) (2,143) 334 (89) 245

11 3,886 944 6,505 (51) 6,454

12 1,195 1,155 1,961 (232) 1,729

13 173 148 254 (11) 243

2,518 (359) 4,290 192 4,482

938 18,534 (3,884) 39 (3,845)

Uniform Presentation of Financesfor the year ending 30 June 2017

The following is a high level summary of both operating and capital investment activities of the Council prepared in a uniform and consistent basis.

All Councils in South Australia voluntarily have agreed to summarise annual budgets and long term financial plans on the same basis.

The arrangement ensures that all Councils provide a common ‘core’ of financial information, which enables meaningful comparisons of each Council’s finances.

Net Lending / (Borrowing) for Financial Year

*Revised Budget i s the Fi rs t Quarter Budget Update for the year, adopted by Counci l at the November 2016 meeting and materia l financia l information received s ince

that time has been included.

Less Proceeds from Sale of Surplus Assets

Less Proceeds from Sale of Replaced Assets

Less Expenses

Operating Surplus / (Deficit)

Less Net Outlays on Existing Assets

Capital Expenditure on Renewal and Replacement of Existing Assets

Less Net Outlays on New and Upgraded AssetsCapital Expenditure on New and Upgraded Assets

Less Amounts Received Specifically for New and Upgraded Assets

Less Depreciation, Amortisation and Impairment

Note

Income

Original Full

Year Budget

Actuals at

31 Dec 2016

*Full year

Revised

Budget in Last

Update

Budget

Adjustments

Quarter 2

Proposed Full

Year Revised

Budget (RB)

38

Mid-year Budget Review 2016-17 – as at 31 December 2016 | The Barossa Council | Page 4

Key Performance Indicators (KPI)

Refer also to comments for KPI’s in adopted Budget Update – Quarterly As at 30 September 2016

Key Performance Indicators (KPI) Original Budget

30 June 17

Proposed Full Year Revised Budget (RB)

Operating Surplus / (Deficit) ($’000)

830 882

Target To achieve an operating breakeven position, or better, over any five year period.

Notes Operating Surplus decreased as a result carried forwards from 2015-16.

Operating Surplus Ratio 2.3% 2.3%

Target To achieve an operating surplus ratio of between -2% to 10, over a rolling 3 year period.

Notes Previously this ratio had been reported as a three year average but as the methodology for this ratio has changed for the 2016-17 year onwards, the ratio reported is for the current year only. This expected result is within the target range of (2%) to 10%.

Net Financial Liabilities ($’000) 15,003 14,144

Target Council's level of net financial liabilities is no greater than its annual operating revenue and not less than zero.

Notes Decrease to liabilities as a result of cash holdings being slightly higher than when Council had adopted its 2016-17 original budget (refer also to carry forward expenditure not spent).

Net Financial Liabilities Ratio 41% 38%

Target Net financial liabilities ratio is greater than zero but less than 100% of total operating revenue.

Notes This ratio has decreased; refer to the comments in the Net Financial Liabilities indicator above.

Interest Cover Ratio 2.4% 2.2%

Target Net interest is greater than 0% and less than 8% of operating revenue.

Notes Minimal change on this ratio, due to increased income (refer Notes 1-5 for further details).

Asset Sustainability Ratio* 101% 81%

Target Capital outlays on renewing/replacing assets net of proceeds from sale of replaced assets is greater than 80% but less than 110% of Infrastructure Asset Management Plans (previously Depreciation) over a rolling 3 year period.

Notes Expenditure on Renewal & Replacement Assets has decreased as a result of averaging 3 years and the ratio for the three years: 2014-15 actual - 103%, 2015-16 actual - 36% and 2016-17 Revised Forecast - 104%. *The Asset Sustainability Ratio is now using planned expenditure data from the Councils Infrastructure and Asset Management Plans (IAMP). Council IAMP’s have been revised - where information on planned expenditure has not been included depreciation for that asset class/portfolio has been included. For the 2016-17 year an amount of $5,782k has been used for this calculation for planned expenditure.

39

Summary of Operating Budget Variance Adjustments

Business

Unit

Type of

Adjustment

Adjustment Title Major Reason for Adjustment Adjustment $

Favourable/

(Unfavourable)

Sub Total per type

$

Reserve $

From/(To)

Net

Operating Adjustments

DES Reduction Dog Impound Fees - Reduction in Income Trending lower than expected (500) (500)Note 1 (500)

NCPA Reduction NCPA Income adjustments To align with NCPA budget review (2,000) (2,000)NCPA Reduction NCPA Income adjustments To align with NCPA budget review (500) (500)NCPA Reduction NCPA Income adjustments To align with NCPA budget review (15,000) (15,000)NCPA Reduction NCPA Income adjustments To align with NCPA budget review (14,810) (14,810)NCPA Reduction NCPA Income adjustments To align with NCPA budget review (3,200) (3,200)

Note 2 (35,510)

WES Transfer Warren Reservoir Project Warren Reservoir project - transfer to operating - grant funding - Assets will be owned by SA Water

245,000 245,000

WES Addition Warren Reservoir Project Warren Reservoir project - additional grant funding received 70,000 70,000 CCS Reduction Library Operating Grant Adjusted to actual grant funding received (155) (155)DES Addition Grassy Ground Cover Project funding

changesChanges in funding basis - Now from Federal Grant and Reserve held by Adelaide Hills Council- Grant

140,000 140,000

CCS Addition Library Operating Grant - Books & Databases

Adjusted to actual grant funding received 1,133 1,133

Note 3 455,978

CCS Addition Investment interest income Increase in income on investments due to greater cash holdings than anticipated 20,000 20,000 CCS Addition Cash at Bank interest income Increase in income on Cash at bank due to greater cash holdings than anticipated 7,000 7,000

NCPA Addition NCPA Income adjustments To align with NCPA budget review 1,000 1,000 Note 4 28,000

DES Reduction Grassy Groundcover Project Changes in funding basis - Now from Federal Grant and Reserve held by Adelaide Hills Council

(49,105) (49,105)

Executive Addition Barossa Regional Procurement Group Project Revenue

Additional revenue as a result of shared costs for Salary Increase and Legal Advice approved by Barossa Regional Procurement Group CEOs

5,781 5,781

CCS Addition NRM Levy Greater amount reimbursed than estimated for Revenue for Administration Costs for the NRM Levy

274 274

Note 5 (43,050)

CCS Addition Work Cover Insurance Work Cover Insurance recoupment 3,000 3,000 CCS Reduction Workers Compensation Rebate Income Adjustment to actuals for Workers Compensation Rebate Income 2016/17 (1,528) (1,528)CCS Addition Income Protection Insurance Income Protection Insurance recoupment 51,000 51,000 DES Addition Grassy Ground Cover Project funding

changesChanges in funding basis - Now from Federal Grant and Reserve held by Adelaide Hills Council - Contribution

90,000 90,000

CCS Transfer Schoolies Bus Contributions Reallocate income budget from Donations to Contributions - Other 0 0 CCS Reduction Booking Commissions Reduction in enquiries/bookings, therefore reduced commissions (8,000) (8,000)CCS Reduction Quiet Waters Out of Print Quiet Waters Book Sold Out (300) (300)WES Addition Sale of land, Seelanders Road, Angaston Following Council resolution, a portion of Seelanders Road Reserve is to be sold 6,388 6,388 CCS Addition Cycle Award grant Safe Cycling Award grant received 2,000 2,000 CCS Addition Visitors Centre - Coffee sales Coffee Sales are tracking above budget 200 200

Note 6 142,760

WES Transfer Project Coordinator Replacement Project Coordinator role, transferring from outside staff wages to inside staff salaries

0 0

WES Transfer Depot staff wages Transfer depot staff wages from footpath to supervisor account 0 0 NCPA Addition NCPA Expenditure adjustments To align with NCPA budget review (11,851) (11,851)NCPA Addition NCPA Expenditure adjustments To align with NCPA budget review (2,076) (2,076)CCS Addition Visitors Centre - Travel allowance Travel of BVC staff to and from Nuri office - meetings etc. No pool or staff cars

available for manager or staff(300) (300)

DES Transfer Planning Services Contract Staff Budget transfer to provide additional relief staff to planners whilst graduates are trained and whilst staff are on leave

20,000 20,000

CCS Transfer Gallery Project Officer Increase in Project Officer hours for financial year. Funds reallocated from Contracting to increase the Gallery Project Officers hours to ensure projects are delivered

(7,235) (7,235)

Executive Addition Barossa Regional Procurement Group Project Officer Salary

Salary Cost Increase Approved by Barossa Regional Procurement Group CEOs & fully offset via revenue

(5,200) (5,200)

Mid-Year Budget Review 2016-17 as at 31 December 2016 | The Barossa Council | Page 5

40

Summary of Operating Budget Variance Adjustments

Business

Unit

Type of

Adjustment

Adjustment Title Major Reason for Adjustment Adjustment $

Favourable/

(Unfavourable)

Sub Total per type

$

Reserve $

From/(To)

Net

CCS Addition Risk Services Administration Support Current Salary being covered by Return To Work Plan. Proposal to pay for 20 days of administration officer to help with backlog of WHS work

(5,359) (5,359)

CCS Transfer IT Team restructure Salary savings allocated to contractor costs to support ongoing service delivery 15,000 15,000 DES Addition Grassy Groundcover Project Breakdown of expenditure across project activities - salaries (6,686) (6,686)CCS Transfer Workers Compensation Insurance Adjustment to actuals for Workers Compensation Insurance (offset against

contingency building insurance from Quarter 1 adjustments)4,541 4,541

Note 7 834

CCS Addition Contractors Pest Control - Barossa Regional Gallery

Due to negotiated Council wide contracts there has been an increase in costs (1,600) (1,600)

CCS Addition Contractors Cleaning Services Due to negotiated Council wide contracts there has been an increase in costs (3,720) (3,720)WES Transfer Tour Down Under contribution to Southern

Barossa AllianceTransfer of TDU budget and contribution to the Southern Barossa Alliance. SBA to directly manage budget lines

0 0

DES Transfer Waste Management Increase in Waste Levy and decrease to Recycling sorting charges 0 0 DES Addition Waste Management Increase in Waste Levy and decrease to Recycling sorting charges (19,000) (19,000)DES Addition Servicing of Fire Extinguishers - Mount

Pleasant NRCCharges not previously allocated to MPNRC therefore no budget line exists (338) (338)

DES Transfer Servicing of Fire Extinguishers - Barossa Bushgardens NRC

Charges not previously allocated to BBG therefore no existing budget line 0 0

CCS Addition New Fire Equip servicing Contract Cycle Hub and CWA hall now serviced monthly (250) (250)CCS Addition Contractors Fire Equipment Servicing Due to negotiated Council wide contracts there has been an increase in costs (1,720) (1,720)CCS Reduction Talunga Toilet Reallocate budget to capital - Quoted price exceeds capital budget 11,060 11,060 CCS Transfer Angaston Hall - Building Maintenance Reallocate budget - additional funds required 0 0 CCS Transfer Office Repairs & Maintenance Reallocate budget - additional funds required 0 0 CCS Transfer Office Repairs - Other Services Reallocate budget - additional funds required 0 0 CCS Transfer Williamstown Caravan Park Trees Remedy fallen tree in caravan park 0 0 CCS Addition Barossa Regional Gallery emergency repairs Repairs required at the Gallery (1,167) (1,167)

CCS Transfer Lyndoch Green pavilion painting Reallocate budget to cover painting of Lyndoch Green pavilion 0 0 CCS Transfer WQVJP Residence Reallocate budget to cover painting of WQVJP residence 0 0 CCS Transfer Office Painting Reallocate budget to cover painting - office repairs 0 0 CCS Transfer Office Building Operational Expenses Reallocate budget to cover painting - Office Building Operational 0 0 CCS Transfer Bethany Reserve Painting Reallocate budget to cover painting at Bethany Reserve 0 0 CCS Transfer The Rex Reallocate budget from Direct Purchases to Contractors - Building Maintenance

Services0 0

CCS Addition Contractor Hygiene Services Barossa Regional Gallery

Due to negotiated Council wide contracts there has been an increase in commitment to cost

(164) (164)

DES Transfer Planning Services Contract Staff Budget transfer to provide additional relief staff to planners whilst graduates are trained and whilst staff are on leave

(20,000) (20,000)

CCS Transfer Domestic Waste Collection Domestic Waste Collection actual larger than anticipated 0 0 CCS Addition Security Monitoring Barossa Regional

GalleryCorrect budget for Building Security Monitoring (1,452) (1,452)

CCS Addition Nuriootpa Pool - Toddler pool Damage due to wear and tear identified after flood clean up works. Cost not originally budgeted and to be taken from reserve

(7,750) 7,750 0

CCS Transfer Gallery Project Officer Increase in Project Officer hours for financial year. Funds reallocated from Contracting to increase the Gallery Project Officers hours to ensure projects are delivered

7,235 7,235

CCS Transfer IT - Photocopiers Changes to lease and print costs - reallocate savings in lease costs to print costs 0 0

CCS Transfer IT Team restructure Salary savings allocated to contractor costs to support ongoing service delivery (15,000) (15,000)Executive Transfer Civic Receptions/Australia Day budget Transfer budget from Civic Receptions to Australia Day budget 0 0 WES Transfer Warren Reservoir Project Warren Reservoir project - transfer to operating - expenditure - Assets will be owned

by SA Water(345,000) (345,000)

WES Addition Warren Reservoir Project Warren Reservoir expenditure offset by additional grant funding received (70,000) (70,000)CCS Transfer Newcastle Street Drainage Detailed Design Reallocate budget from Community assets to Stormwater Drainage 0 0

NCPA Reduction NCPA Expenditure adjustments To align with NCPA budget review 10,000 10,000

Mid-Year Budget Review 2016-17 as at 31 December 2016 | The Barossa Council | Page 6

41

Summary of Operating Budget Variance Adjustments

Business

Unit

Type of

Adjustment

Adjustment Title Major Reason for Adjustment Adjustment $

Favourable/

(Unfavourable)

Sub Total per type

$

Reserve $

From/(To)

Net

CCS Addition Management Fee - Nuriootpa Swimming Pool 2015/16 year

CPI increase was omitted from the fees charged (930) (930)

CCS Reduction Remove Wellbeing Budget Negotiated out as part of the indoor staff Enterprise Bargain 4,000 4,000 Executive Addition Legal Advice Consultant Expenditure Contract Legal Advice - additional expense approved by Barossa Regional

Procurement Group CEOs and offset via revenue(775) (775)

CCS Transfer Hardware Refresh changes Lease costs reduced as part of Cloud Strategy, YR 1 savings allocated to Hardware Refresh implementation $15k and Cloud Data Recovery Implementation $15K

0 0

CCS Transfer Barossa Cycle Hub Reallocate budget from Direct Purchases to Consultants 0 0 NCPA Reduction NCPA Expenditure adjustments To align with NCPA budget review 1,307 1,307 CCS Transfer Lyndoch Hall Reallocate budget - additional funds required 0 0 CCS Addition Library Management System Fee Adjusted Actual Library Management System Fee updated - 2 x RFID units fee (1,812) (1,812)CCS Addition Unspent Library material grant funds for

databasesUnspent Library material grant funds for databases - funding received 15/16 (1,194) (1,194)

CCS Addition Library Digital databases - Public Library Services (PLS)

Library Digital databases - paid direct from materials grant funding - PLS (9,641) (9,641)

CCS Transfer Eden Valley Caravan Park Cleaning Cleaning products increased due to increased occupancy and purchase in bulk 0 0 NCPA Reduction NCPA Expenditure adjustments To align with NCPA budget review 14,000 14,000 CCS Addition Safe Cycle Award grant expenditure Grant monies to be spent on additional Cycle Hub signage and promotion (2,000) (2,000)Executive Addition Naturalisation Ceremonies Additional funds required to support naturalisation ceremonies (500) (500)CCS Addition Phone system resources Equipment required as part of the new phone system to meet and provide customer

service and employee appropriate tools(360) (360)

DES Transfer Dog and Cat Control Reallocate budget from Contributions Dog and Cat Management Board to Direct Purchases

0 0

DES Transfer Dog and Cat Control Reallocate budget from Printing to Direct Purchases 0 0 NCPA Addition NCPA Expenditure adjustments To align with NCPA budget review (2,600) (2,600)CCS Addition Street Lighting charges Increase in street lighting - unmetered usage charges with new contract through LGA (67,000) (67,000)

NCPA Reduction NCPA Expenditure adjustments To align with NCPA budget review 14,000 14,000 CCS Addition Gas charges and usage Increase in gas charges and use (300) (300)NCPA Reduction NCPA Expenditure adjustments To align with NCPA budget review 3,000 3,000 CCS Transfer Eden Valley Fuel Allocation for fuel almost expended. Discussion with MPInc and caretaker 0 0 CCS Transfer Talunga Park Fuel Allocation for fuel almost expended. Discussion with MPInc and caretaker 0 0 NCPA Reduction NCPA Expenditure adjustments To align with NCPA budget review 2,000 2,000 NCPA Reduction NCPA Expenditure adjustments To align with NCPA budget review 20,000 20,000 CCS Reduction Book easy Commission Reduction in booking therefore less commission needs to be paid to BookEasy 2,000 2,000 CCS Transfer Income Protection Insurance Adjustment to actuals for Income Protection Insurance (offset against contingency

building insurance from Quarter 1 adjustments)0 0

CCS Transfer Workers Compensation Insurance Adjustment to actuals for Workers Compensation Insurance (offset against contingency building insurance from Quarter 1 adjustments)

(4,541) (4,541)

Executive Addition Southern Barossa Hub - The Big Project community consultation

Unbudgeted advertising costs to consult on the feasibility study (2,480) (2,480)

CCS Addition Advertising - Rating & valuation Rating and valuation amendment of quarter one adjustment (291) (291)Executive Addition Southern Barossa Hub - The Big Project

community consultationUnbudgeted printing costs to consult on the feasibility study (270) (270)

CCS Transfer First Aid Training Increased First Aid Training required - transferred from First Aid Kit replacement budget

0 0

CCS Transfer Staff Training - IT Services Reallocate funds within cost centre to match expense 0 0 CCS Transfer Staff Training - Accommodation Transfer training budget to provide for accommodation costs to attend both days of

the financial management conference0 0

NCPA Reduction NCPA Expenditure adjustments To align with NCPA budget review 2,000 2,000 Executive Transfer Public Relations - postage Postage for quarterly ratepayer newsletter has been attributed to printing budget line 0 0

Executive Addition Southern Barossa Hub - The Big Project community consultation

Unbudgeted postage costs to consult on the feasibility study (750) (750)

NCPA Addition NCPA Expenditure adjustments To align with NCPA budget review (55) (55)Executive Transfer Elected member Phone Costs Correct mobile costs for EM transfer done in Q1 review 0 0

Mid-Year Budget Review 2016-17 as at 31 December 2016 | The Barossa Council | Page 7

42

Summary of Operating Budget Variance Adjustments

Business

Unit

Type of

Adjustment

Adjustment Title Major Reason for Adjustment Adjustment $

Favourable/

(Unfavourable)

Sub Total per type

$

Reserve $

From/(To)

Net

CCS Transfer Mobile Phone Costs SMS charges for Library System added 0 0 Executive Transfer Mobile Broadband Costs Broadband costs were budgeted for under mobile phone requiring a transfer to new

account0 0

Executive Transfer Mobile Broadband Additional Cost Additional broadband expense to be offset by software savings within cost centre 0 0 CCS Addition Mt Pleasant Golf Club - contribution Council resolution (15 November 2016) to provide a monthly contribution to the club

until 30 June 2017(15,000) (15,000)

DES Addition Building compliance budget Ongoing ERD Court case requires additional funding to maintain (5,000) (5,000)CCS Transfer Property Identification Code (PIC) Increase in cost of PIC due to late fees. Renewal Notice provided after expiry date 0 0

NCPA Addition NCPA Expenditure adjustments To align with NCPA budget review (3,700) (3,700)CCS Reduction Remove Wellbeing Budget Negotiated out as part of the indoor staff Enterprise Bargain 1,000 1,000 DES Transfer Mitel 5320e phones and Samsung J3

mobilesPurchase new desk phones and mobile phones to complement new corporate communications system

0 0

CCS Reduction Tourism Barossa Booking Commission Less enquires/bookings made online therefore less commission to be paid to Tourism Barossa for online bookings

1,000 1,000

NCPA Addition NCPA Expenditure adjustments To align with NCPA budget review (5,500) (5,500)Executive Transfer Service Review Budget Transfer Service Review Budget to Support Ancillary Costs 0 0 Executive Transfer Council Meals Transfer budget for Council Meals to correct account 0 0 DES Addition Grassy Groundcover Project Breakdown of expenditure across project activities (77,749) (77,749)

Note 8 (597,007)

CCS Reduction Depreciation 16-17 Depreciation review based on 15-16 actuals and known asset changes 189,986 0 Note 9 189,986

Note: for reconciliation purposes the report includes Approved Carried Forwards 141,491 141,491 7,750 (40,745)NET TOTAL - Operating Adjustments

Mid-Year Budget Review 2016-17 as at 31 December 2016 | The Barossa Council | Page 8

43

Summary of Capital Budget Variance Adjustments

Business

Unit

Type of

Adjustment

Adjustment Title Reason for Budget Adjustment/Carried Forward Adjustment $

Favourable/

(Unfavourable)

Sub Total per

type $

Reserve $

From/(To)

Net

Capital Expenditure on Renewal and Replacement of

existing assets

WES Transfer Resheet Budget reallocated to Footpath Upgrade Program

Budget changes as a result of Tender and WES Director's Report approved at 15/11/16 Council meeting Item 8.2.1

136,000 136,000

WES Transfer Penrice Road Reallocate budget from Road Resealing contingency to cover additional costs of asphalt works

0 0

WES Transfer Road Seal, Hoffmann Avenue, Tanunda Savings achieved from Hoffmann Ave and Light Pass/Magnolia asphalt overlays reallocated to Church Street, Williamstown

10,590 10,590

WES Transfer Road Seal, Light Pass Road, Tanunda Savings achieved from Hoffmann Ave and Light Pass/Magnolia asphalt overlays reallocated to Church Street, Williamstown

19,234 19,234

WES Transfer Church Street Williamstown Asphalt Overlay Addition to reseal program using savings achieved from Hoffmann Ave and Light Pass/Magnolia asphalt overlays

(29,824) (29,824)

WES Transfer Research Road Nuriootpa - Proposed Reseal Program Amendment

Saving - Due to the Sept 30th flood damage sustained on this section of road 32,461 32,461

WES Transfer 7 Steps Road - Proposed Reseal Program Amendment Addition to reseal program due to urgent need using savings from Research Road (16,085) (16,085)

WES Transfer Centenary Ave Nuriootpa - Proposed Reseal Program Amendment

Addition to reseal program due to urgent need using savings from Research Road (16,376) (16,376)

WES Transfer Lyndoch Gravity Mains Aligning capital spend to correct asset - Tanunda CWMS Drain Renewal used as required in Lyndoch

0 0

WES Transfer Oval Renewal Program Transfer program budget to individual assets as per oval works program 0 0

WES Transfer Jetter Truck Reallocate additional funds required for Jetter truck purchase from Stockwell Upgrade not required at this time

(11,000) (11,000)

WES Transfer Vehicle - Senior Environmental Health Officer Reallocate funding to replace Senior Environmental Health Officer Vehicle 0 0 WES Transfer DWES Vehicle Purchase Budget transfer from contingency for purchase of DWES vehicle. Purchase price

within allowance0 0

WES Reduction General Inspector Vehicle purchase Budget transfer from contingency for purchase of General Inspector vehicle 0 0

WES Addition Revised Resheeting Program Budget reallocations due to revised Resheet Program 145,231 145,231 CCS Addition Library materials grant expenditure adjustment to actuals Library materials grant expenditure adjustment to actuals for capital book purchases 8,702 8,702

Note 10 278,933

278,933 0 0 Capital Expenditure on New and Upgraded assets

CCS Addition Williamstown Hall Lighting Expenses Budget for install expense - 100% offset by community contribution (13,436) (13,436)CCS Addition Talunga Toilet Reallocate budget from operating - Quoted price exceeds capital budget (11,060) (11,060)WES Transfer Hoffnungsthal Road Upgrade Earthworks, stormwater drainage and pavement construction costs higher than

budget estimate when no design available(145,231) (145,231)

WES Transfer Warren Reservoir Project Warren Reservoir project - transfer to operating - expenditure - Assets will be owned by SA Water

345,000 345,000

WES Transfer Oval Upgrade Program Transfer program budget to individual assets as per oval works program 0 0 WES Transfer Revised Footpath Upgrade Program Budget changes as a result of Tender and WES Director's Report approved at

15/11/16 Council meeting Item 8.2.1(136,000) (136,000)

WES Transfer Stockwell CWMS Reallocate additional funds required for Jetter truck purchase from Stockwell Upgrade not required at this time

11,000 11,000

Note 11 50,273

NET TOTAL - Asset Renewal/Replacement Adjustments

Mid-Year Budget Review 2016-17 as at 31 December 2016 | The Barossa Council | Page 944

Summary of Capital Budget Variance Adjustments

Business

Unit

Type of

Adjustment

Adjustment Title Reason for Budget Adjustment/Carried Forward Adjustment $

Favourable/

(Unfavourable)

Sub Total per

type $

Reserve $

From/(To)

Net

Amounts received specifically for New and Upgraded

Assets/Profit & loss for asset disposal

WES Transfer Warren Reservoir Project Warren Reservoir project - transfer to operating - grant funding - Assets will be owned by SA Water

(245,000) (245,000)

CCS Addition Williamstown Hall Lighting Community Contribution Input budget to match community contribution to lighting project 13,436 13,436 Note 12 (231,564)

Asset Sales adjustments

CCS Addition Surplus Land Sales Additional costs of sale for NBN Telstra cost on parcels (10,768) (10,768)Note 13 (10,768)

(192,059) 0 (192,059)

Note: for reconciliation purposes the report includes Approved Carried Forwards 86,874 86,874 0 (192,059)

NET TOTAL - Asset New/Upgrade Adjustments

NET TOTAL - Capital Adjustments

Mid-Year Budget Review 2016-17 as at 31 December 2016 | The Barossa Council | Page 1045

Mid-year Budget Review 2016-17 – as at 31 December 2016 | The Barossa Council | Page 11 46

Mid-year Budget Review 2016-17 – as at 31 December 2016 | The Barossa Council | Page 12

47

Mid-year Budget Review 2016-17 – as at 31 December 2016 | The Barossa Council | Page 13

Accumulated

Surplus

Asset

Revaluation

Reserve

Other

Reserves

Total

Equity

($'000) ($'000) ($'000) ($'000)

70,136 254,232 7,012 331,380

69,181 254,249 7,428 330,858

1,613 1,613

0 0 0 0

0 2,866 0 2,866

0 0 0 0

(714) 0 714 0

70,080 257,115 8,142 335,337

70,136 254,232 7,012 331,380

69,181 254,249 7,428 330,858

2,220 2,220

0 0 0 0

0 2,866 0 2,866

0 0 0 0

(714) 0 714 0

70,687 257,115 8,142 335,944

Balance at the End of Period

Balance at end of previous reporting period

30 September 2016 (Original Budget 2016-17)

Restated opening balance (2015-16 Financia l Statements)

Net Surplus / (Deficit) for year

Other Comprehensive Income

Statement of Changes in Equityas at 31 December 2016

Transfer between reserves

Gain on revaluation of infrastructure, property,

plant and equipment

Transfer to accumulated surplus on sale of

infrastructure, property, plant and equipment

Original Budget (restated at end previous reporting period)

Balance at end of previous reporting period

Transfer between reserves

Balance at the End of Period

Proposed Full Year Revised Budget (RB)

Restated opening balance (2015-16 Financia l Statements)

Net Surplus / (Deficit) for year

Other Comprehensive Income

Gain on revaluation of infrastructure, property, Transfer to accumulated surplus on sale of

infrastructure, property, plant and equipment

48

Mid-year Budget Review 2016-17 – as at 31 December 2016 | The Barossa Council | Page 14

($'000) ($'000)

36,243 37,344

202 230

(27,043) (28,366)

(204) (204)

(1,061) (1,061)

8,137 7,943

1,195 1,438

425 425

173 243

0 0

0 0

(5,301) (7,982)

(3,886) (6,454)

0 0

0 0

(7,394) (12,330)

0 0

0 0

1,640 1,640

0

(1,932) (1,932)

0 0

(1,640) (1,640)

(1,932) (1,932)

(1,189) (6,319)

3,862 9,299

2,673 2,980 Cash and Cash Equivalents at End of Period

Repayment of Finance Lease Liabilities

Repayment of Internal Borrowings

Net Cash Provided by (or Used in) Financing

Activities

Net Increase / (Decrease) in Cash Held

Cash and Cash Equivalents at Beginning of

Period

Loans Received

Finance Lease Funds

Proceeds from Internal Borrowings

Payments

Repayments of Borrowings

Receipts

Sale of Replaced Assets

Sale of Surplus Assets

Net Purchase of Investment Securities

Repayments of Loans by Community Groups

Payments

Expenditure on Renewal / Replacement of

Assets

Expenditure on New / Upgraded Assets

Net Purchase of Investment Securities

Loans made to Community Groups

Net Cash Provided by (or Used in) Investing

Activities

Cash Flows from Financing Activities

Amounts Specifically for New or Upgraded

Assets

Cash Flows from Operating Activities

Receipts

Operating Receipts

Investment Receipts

Payments

Operating payments to Suppliers and

Employees

LandFill rehabilitation expense

Finance Payments

Net Cash Provided by (or Used in) Operating

Activities

Cash Flows from Investing Activities

Receipts

Statement of Cash Flowsas at 31 December 2016

Original Full

Year Budget

Proposed

Full Year

Revised

Budget (RB)

49

Mid-year Budget Review 2016-17 – as at 31 December 2016 | The Barossa Council | Page 15

Initiative Funding From Res Allocation

Department Description/Update in italics Complete Y/N

Exp Rev Net

Mt Pleasant Hall - Ramp for Disabled access 8,000 8,000 -8,000 Community Facilities

Scheduled for Q3 - Committee have since requested that $s approved foreach of this items be merged into new purpose of A/C for hall. Report toDecember meeting proposed as change of approval condition.

N

Volunteer Coordinator - Internal 70,304 70,304 Community Services

A volunteer coordinator is now employed 4 days a week, to be joined shortlyby an administrator one day per week. work).Draft Volunteer Policy and Process will be submitted to CMT for approval

early in 2017The VIC Volunteers are logging hours through Better impact database;Barossa Regional Gallery will follow shortly.Volunteer Supervisors receive support from Karen.All new volunteers are filtered through the VRC and placed in a best fitvolunteer position with Council; this has included setting up an interviewsystem for all new internal volunteers. Any potential volunteers that do not fitwith current vacancies within Council are being directed to external volunteeropportunities through the VRC.The VRC Volunteers along with Karen are entering all outstanding hours forVolunteers, across Council, into the database and ensuring that all Volunteer details are up to date and paperwork is current. Starting with YAC, HACC,Library and VRC.

Y

World Heritage Bid 15,000 15,000 Development and

Environmental Services

Progress reports to Council when milestones reached. CommunityInformation Sessions conducted in November 2016.Stage 1 (National Heritage bid) due February 2017.

N

Community Plan Service Review 110,000 110,000 Executive Tenders closed 3/11 appoint to be made in week commencing 7/11. Projectplan completed and approved by Audit Committee. First draft report present

to Audit Committee further work being undertaken on service levels and

finalisation of report at present.

N

SBA - Administration Support 7,200 7,200 -7,200 Community Facilities

Subject to funds from reserves (ie from ex S41's now under SBA umbrella)being available. Community groups have still not committed to being part ofSBA therefore not agreeing to this request. Hold

N

ACBA - Salters Gully Master Plan 20,000 20,000 -17,000 Community Facilities

Next stage of ACBA 3 year plan and will be funded from reserves. Scheduledfor Q3

N

ACBA - Signage 14,000 14,000 0 Community Facilities

Next stage of ACBA 3 year plan and will be funded from reserves. Scheduledfor Q3

N

Mt Pleasant Hall - Island Bench to Kitchen 3,000 3,000 -3,000 Community Facilities

Scheduled for Q3 - Committee have since requested that $s approved foreach of this items be merged into new purpose of A/C for hall. Report toDecember meeting proposed as change of approval condition.

N

Mt Pleasant Hall - Kitchen Bench Space 2,000 2,000 -2,000 Community Facilities

Scheduled for Q3 - Committee have since requested that $s approved foreach of this items be merged into new purpose of A/C for hall. Report toDecember meeting proposed as change of approval condition.

N

Mt Pleasant Hall - Commercial Fridge 3,000 3,000 -3,000 Community Facilities