audit committee - coorong district council committee... · council received the audit committee...

TRANSCRIPT

Coorong District Council

Audit Committee Agenda 2 May 2017

AUDIT COMMITTEE

Coorong Civic Centre Boardroom 95-101 Railway Terrace, Tailem Bend

Tuesday 2 May at 9.00am

AGENDA Welcome Committee Members: Rex Mooney (Presiding Member)

Cr Neville Jaensch, Mayor Cr Peter Wright Cr Bob Simcock Cr Mick O’Hara

Present David Mosel Acting CEO/Director Infrastructure & Assets Judy Thompson, Finance Manager Sacha Holme, Senior Finance Officer

Apologies Vincent Cammell, CEO Nat Traeger, Director Community & Corporate

1. Confirmation of Minutes from 14 March 2017

Refer Appendix 1 Council received the Audit Committee Minutes from the 14 March 2017 meeting at their 21 March 2017 meeting. Recommendation: That the Audit Committee receives and notes the minutes from the previous meeting held 14 March 2017.

2. Work Schedule as at 2 May 2017 Refer Appendix 2 The format and content details have been updated by the Finance Manager since the last meeting. The Audit Committee Work Program – 2017 has been updated noting progress where applicable and policies being reviewed. Recommendation: That the Audit Committee receives and notes the work program.

Coorong District Council

Audit Committee Agenda 2 May 2017

3. Internal Controls and Risk Management Systems Refer Appendix 3

An Internal Control Plan was presented to the audit committee in December 2016; in March 2017 the risk areas were reviewed by UYH Haines Norton. It should be noted that the review was undertaken by representatives that are not the consultants that Council were using to support the finance function when a permanent resource was not on hand. The report has been completed and has shown a significant improvement since the first review in April/May 2014. Copy of the report is attached.

Recommendation: That the Audit Committee recommends that Council adopts the Internal Control report from UYH Haines Norton.

4. Budget Review as at 31 March 2017

The Local Government (Financial Management) Regulations 2011 Section 9, require that council must prepare and consider a report at least twice between 30 Sept and 31 May showing a revised forecast of the operating and capital investment activities compared to those set out in the budget as per the Model Financial Statements entitled “Uniform Presentation of Finances”. This is the third budget review for 2016/17. Statement of Comprehensive Income a) Operating Surplus / Deficit

The 3rd Budget review 2016/17 reports an adjustment to the operating deficit increase of $20k. The major key contribution for the change expenditure not allocated via budget review 2. Other changes are listed below. Income

Rates General – no change Statutory Charges – no change User Charges - no change Other Grants & Subsidies – Overall increase in grants/subsidies successfully

received of $20k. Investment Income – no change Reimbursement – no change Other income - no change

Coorong District Council

Audit Committee Agenda 2 May 2017

Expenditure

Note Employees Expense – Increase for new position of $20k Contractual Services, Materials & Other Expenses – Increase relating to grant

received expense not allocated in Budget 2 $25k Depreciation – no change. Finance Costs – no change.

Summary of Financial Performance & Position Statement (SFPPS)

2016/17 Actuals

to 31/3/17 $'000

2016/17 Budget Year to

Date $'000

2016/17 Original Budget $'000

2016/17 Budget

Review 1 $'000

2016/17 Budget

Review 2 $'000

2016/17 Budget

Review 3 $'000

Income 13,351 13,706 13,922 13,922 14,366 14,386 less Expenses 10,357 10,753 14,336 14,336 14,699 14,739

2,993 2,953 -414 -414 -333 -353

less Net Outlays on Existing Assets Capital Expenditure on renewal

and replacement of Existing Assets

1,439

1,439 4,112 4,112 4,112 4,112 less Depreciation, Amortisation

and Impairment 2,841 2,856 3,808 3,808 3,717 3,717 less Proceeds from Sale of

Replaced Assets 167 204 408 408 408 408

-104 -104 -13 -13

less Net Outlays on New and Upgraded Assets

Capital Expenditure on New and Upgraded Assets (including investment property & real estate developments)

275 270 540 540 540 540

less Amounts received specifically for New and Upgraded Assets 344 184 367 367 367 367

less Proceeds from Sale of Surplus Assets

(including investment property and real estate developments)

18 150 150 150 150

-87 87 23 23 23 23

Net Lending / (Borrowing) for Financial Year 3,080 2,866 -333 -333 -343 -363

Coorong District Council

Audit Committee Agenda 2 May 2017

2016/17 Original Budget $'000

2016/17 Budget Review 2 $'000

2016/17 Budget

Review 3 $'000

KPIs Operating Surplus Ratio -2.98% -2.32% -2.45%

Net Financial Liabilities Ratio 41.09% 31.62% 31.7%

Asset Sustainability Ratio 133.07% 133.07% 133.07%

Recommendation: That the Audit Committee recommends that Council adopts the Budget Review 3.

5. Long Term Financial Plan Information Only: The Long Term Financial Plan is currently being review as part of the 2017/18 budget and will be updated with the 2016/17 4th Review.

6. Treasury Management Report as at 31 March 2017 Purpose

Information Only: To keep the Council informed of their outstanding Loan liabilities and Community Loans Assets.

The report covers the period 1st January 2017 to 31st March 2017

Strategic Plan Ref

Reliability of financial reporting

New Loans Loan approved Tintinara Golf Club and was drawn down 15th February 2017.

Outstanding Loans

Weighted Average Interest Rate as at 30th June was 5.21%

Coorong District Council

Audit Committee Agenda 2 May 2017

The table below details the Council’s outstanding loans.

Council Loans DATE LOAN AMOUNT BALANCE CURRENT

PURPOSE OF LOAN From To PERIOD OF LOAN 30/06/2016 BALANCE 31/03/2017

Tailem Bend Land 15/02/2002 15/02/2017 110,000 50,000 11,267.38 -

Land & Buildings 15/06/2005 15/06/2020 190,000 70,000 68,935.48 61,224.40

Office & Town Hall 16/12/2014 16/06/2029 1,250,000 100,410 1,137,633.74 1,107,512.53

DEB 24 Cash Advance CWMS 40,000 -

DEB 27 - Cash Advance Office Building Redevelopment 37,101 1,094,712.00 -

DEB 18 Cash Advance Meningie Bowling Club 50,000 -

DEB 21 Cash Advance Lake Albert Golf Club 70,000 12,400.00 21,150.00

DEB 22 Cash Advance Tintinara Bowling Club 100,410 - -

DEB 23 Cash Advance Tailem Bend Bowling Club 100,000 7,000.00 7,000.00

DEB 25 Cash Advance Border Downs Tintinara Netball Club 40,000 10,000.00 -

DEB 29 Cash Advance Meningie Cheese Factory Museum 37,101 16,000.00 8,000.00

DEB 30 Cash Advance Tintinara Golf Club 35,000 - 35,000.00

2,357,948.60 1,239,886.93

(Highlighted are due to be finalised in 16/17)

Council has approved the range limits set out below

Type of loan Proportion of the Debt Portfolio Minimum Maximum

Floating Rate Debentures 50% 80% Fixed Rate Credit Foncier 20% 50%

Coorong District Council

Audit Committee Agenda 2 May 2017

Portfolio Structure

The chart below summarises the current and projected structure of the loan relative to the Policy ranges. (Community Loans not included)

Projections of committed and approved payments

The charts below summarise the projections of committed and approved principal and interest payments for the next ten financial years. (Community Loans not included)

0%

20%

40%

60%

80%

100%

120%

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029

Loan Principle Portfolio

Percentage Fixed Percentage VariableYear ending 30/6

$-

$50,000.00

$100,000.00

$150,000.00

$200,000.00

$250,000.00

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

Projected Principle and Interest Repayments included CAD

Total Council Principle Repayment LTFP Financial Charges

Coorong District Council

Audit Committee Agenda 2 May 2017

Community Assets (Outstanding Loans to Outside Bodies) COMMUNITY ORGANISATION DATE LOAN AMOUNT BALANCE CURRENT Interest

Applicable PURPOSE OF LOAN From To PERIOD OF LOAN 30/06/2016 BALANCE 31/03/2017

DEB 18 Cash Advance Meningie Bowling Club 50,000 Interest

bearing

DEB 21 Cash Advance Lake Albert Golf Club 70,000 12,400.00 21,150.00 Interest

bearing

DEB 22 Cash Advance Tintinara Bowling Club 100,410 - - Interest

bearing DEB 23 Cash Advance Tailem Bend Bowling

Club 16/11/2019 100,000 7,000.00 7,000.00 Interest

bearing

DEB 25 Cash Advance Border Downs Tintinara

Netball Club 40,000 10,000.00 - Interest

bearing

DEB 29 Cash Advance Meningie Cheese Factory Museum

15/10/2025 37,101 16,000.00 8,000.00 Interest bearing

DEB 30 Cash Advance Tintinara Golf Club 15/02/2017 15/02/2023 6 35,000 35,000.00 Interest

bearing

Tailem Bend Bowling Club 24/07/2015 24/07/2020 5 5,000 5,000.00 4,000.00 Interest

Free

Meningie Bowling Club 5/07/2016 30/06/2021 5 32,524 29,271.60 Interest Free

Meningie Football Club 5/07/2016 30/06/2026 10 100,000 95,000.00 Interest Free

Tintinara Bowling Club 5/07/2016 30/06/2021 5 35,000 31,500.00 Interest Free

Tailem Bend Golf Club 26/11/2016 25/11/2021 5 5,000 5,000.00 Interest Free

610,035

235,922

7. That the relevant policies as outlined in the Council Agenda Item Schedule for 2016-2017 are reviewed in accordance with their review cycle. (Work Schedule Item 7.6) In accordance with the schedule mentioned above, the policies identified as being relevant to be directed to the Audit Committee for this meeting are as follows:

Coorong District Council

Audit Committee Agenda 2 May 2017

7.1 Rating Policy, Refer Appendix 4 Review process amended to annually in accordance with model policy from the

LGA

Cosmetic changes only 7.2 Rate Rebate Policy, Refer Appendix 4 Review process amended to annually in accordance with model policy from the

LGA

Cosmetic changes only

Recommendation: That the Audit Committee recommends that Council adopts the following Policies as reviewed: Rating Policy Rate Rebate Policy

8. Asset Management Plans Item 7.8 on the Audit Committee work program relates to asset management plans for building & structures, water supply and stormwater assets. Director Infrastructure & Assets David Mosel will be in attendance to give an update of management plans for all asset classes.

9. 2017/18 Annual Business Plan/Budget Draft

Council’s draft 2017/18 Annual Business Plan & Budget (ABP) has been prepared and is currently undergoing a period of community engagement. In accordance with the 2017/18 ABP & Budget timetable, Council is seeking comment from the Audit Committee prior to its formal consideration for adoption on 27 June 2017. The Audit Committee has the responsibility to ensure Council is aware of the impact on ongoing financial sustainability being proposed and ensuring the level of consistency with Council's strategic plans. (Work Schedule Item 7.4) Refer Appendix 5 The draft 2017/18 Annual Business Plan & Budget shows a proposed operating Deficit of $501k. It is also proposed that there will be a 3.2% rate increase in Council Rates. Any additional revenue derived from rates will be growth and property valuations. It is noted the ABP the administration will continue to process any changes to valuation right up until the Council adopts the 2017/18 budget. Fees and charges have been adjusted with slight increases. Statutory charges will be updated when information is received. Refer Appendix 5

Coorong District Council

Audit Committee Agenda 2 May 2017

Council proposes to undertake Operational projects of $504k and renewal and new Capital Expenditure (including admin Costs) of $4.670m. The consultation period is from the 19th April until the 30th May 2017. Council officers have initiated a new engagement method this year in addition to the legislative special council meeting that is required by the Local Government Act 1999. Community ‘drop in’ sessions will be held across the district where the community is invited to take advantage of informal opportunities to ask questions of and make comment on the draft plan. Sessions will be hosted during working hours at each Council office and any feedback/questions will be captured as part of the community engagement process. It is aimed that after completion of the community engagement period and Special Council meeting, any required amendments will be made to the Annual Business Plan in order for it to be adopted at the 27 June 2017 Council meeting. Recommendation: That the Audit Committee advises Council that they are satisfied with the proposed draft 2017/18 Annual Business Plan & Budget.

10. Other Business (general discussion)

11. Close

12. Next Meeting The next meeting has been scheduled for 3 October 2017.

o Meeting with Auditor (confirmed with Auditor) o 2016/17 4th Budget Review o 2017/18 Draft Financial Statements o 2017/18 1st Budget Review

Coorong District Council

Audit Committee Agenda 2 May 2017

Appendix 1

Audit Committee minutes from 14 March 2017

Coorong District Council

Audit Committee Minutes 14 March 2017

AUDIT COMMITTEE

Coorong Civic Centre Boardroom 95-101 Railway Terrace, Tailem Bend

Tuesday 14 March at 9.00am

MINUTES Welcome Committee Members: Rex Mooney (Presiding Member) (via Teleconference)

Cr Neville Jaensch, Mayor Cr Bob Simcock Cr Mick O’Hara Cr Vern Leng

Present Vincent Cammell, CEO Nat Traeger, Director Community & Corporate Judy Thompson, Finance Manager Sacha Holme, Finance Officer Corinne Garrett, Consultant - UHY Haines Norton Dario Nazzari. Senior Consultant – UHY Haines Norton (via teleconference) Cr Julie Barrie

Apologies Cr Peter Wright

1. Confirmation of Minutes from 13 December 2016 Moved Cr Simcock Seconded Cr O’Hara That the Audit Committee receives and notes the minutes from the previous meeting held 13 December 2016 with an inclusion that the appointment of external auditor is a public resolution.

Carried

2. Work Schedule as at 14 March 2017 The Audit Committee Work Program – 2017 has been updated noting progress where applicable and policies being reviewed. Moved Cr Leng Seconded Cr Simcock That the Audit Committee receives and notes the work program.

Carried

3. Internal Controls and Risk Management Systems

Coorong District Council

Audit Committee Minutes 14 March 2017

Moved Cr Simcock Seconded Cr Leng The Audit Committee receive and note the update of internal controls and risk management systems.

Carried

4. Budget Review as at 31st December 2016 The Local Government (Financial Management) Regulations 2011 Section 9, require that council must prepare and consider a report at least twice between 30 Sept and 31 May showing a revised forecast of the operating and capital investment activities compared to those set out in the budget as per the Model Financial Statements entitled “Uniform Presentation of Finances”.

Moved Cr Simcock Seconded Cr O’Hara That the Audit Committee recommends that Council adopts the Budget Review 2 as at 31 December 2016.

Carried

5. Long Term Financial Plan The Long Term Financial Plan has been updated to reflect the changes at the 2nd budget review for 2016/17. Moved Cr Leng Seconded Cr O’Hara That the Audit Committee receives and notes Long Term Financial Plan at the 2nd Budget Review.

Carried

6. Treasury Management Report as at 31st December 2016 Purpose

The report covered the period 30th September to 31st December 2016

Strategic Plan Ref

Reliability of financial reporting

New Loans No new loans this period.

Outstanding Loans

Weighted Average Interest Rate as at 30th June was 5.21%

Moved Cr O’Hara Seconded Cr Simcock

Coorong District Council

Audit Committee Minutes 14 March 2017

That the Treasury Management Report as at 31 December 2016 be accepted.

Carried

7. That the relevant policies as outlined in the Council Agenda Item Schedule for 2016-2017 are reviewed in accordance with their review cycle. (Work Schedule Item 7.6) In accordance with the schedule mentioned above, the policies identified as being relevant to be directed to the Audit Committee for this meeting were reviewed. 7.1 Acquisition of Goods & Services Policy

Review process amended to annually in accordance with model policy from the LGA

7.2 Disposal of Council Land & Other Assets Policy Review process amended to annually in accordance with model policy from the

LGA

Cosmetic changes only

7.3 Treasury Management Policy Review process amended to annually in accordance with model policy from the

LGA

Cosmetic changes only 7.4 Prudential Management Policy Review process amended to annually in accordance with model policy from the

LGA

Included requirement for a WHS Management Plan to be developed for all construction projects exceeding $450k (this was not picked up in the last review).

7.5 Risk Management Policy Review process amended to annually in accordance with model policy from the

LGA Cosmetic changes only Moved Cr O’Hara Seconded Cr Leng That the Audit Committee recommends that Council adopts the following Policies as reviewed:

Coorong District Council

Audit Committee Minutes 14 March 2017

Acquisition of Goods & Services Policy Disposal of Council Land & Other Assets Policy Treasury Management Policy Prudential Management Policy Risk Management Policy

Carried 8. Asset Management Plans

Item 7.8 on the Audit Committee work program relates to asset management plans for building & structures, water supply and stormwater assets. Director Infrastructure & Assets David Mosel provided an update of management plans for all asset classes. Moved Cr Leng Seconded Cr Simcock That the verbal report by Director Infrastructure & Assets be noted.

Carried

9. Other Business (general discussion)

10. Next Meeting The next meeting will held on 2 May 2017.

11. Close The Presiding Member closed the meeting at 10.40am.

Coorong District Council

Audit Committee Agenda 2 May 2017

Appendix 2

Audit Committee Work Program - 2017

Coorong District Council DRAFT Audit Committee Work Program – 2017

1

Activity Meeting Date

Responsible Officers

Current Status/Outcomes

Date Completed

Follow up Action (for next year’s work

program)

1. Financial Reporting

Monitor the integrity of the financial statement reports referred to in sections 1.1 to 1.9 below to review any significant financial reporting issues and judgements which they may contain Specifically - review and challenge where necessary:

the consistency in application of, and/or any changes to, accounting policies; the method used to account for significant or unusual transactions where different approaches are possible; whether Council has followed appropriate accounting standards and made appropriate estimates and judgements, taking into account the views of the

external auditor; the clarity of disclosure in Councils financial reports and the context in which statements are made; all information presented with the financial statements, such as the operating and financial review and the corporate governance statement (in so far as it

relates to the audit and risk management); and significant adjustments to the financial report (if any) arising from the audit process.

1.1 Mid-Year Budget Review 2016-17 14/3/17 Presented at 14/3/17 audit committee meeting

14/3/17

1.2 Review and comment on Councils Annual Business Plan / Annual Budget. Specifically in relation to its consistency with strategic management plans as well as the expected impact on Councils financial sustainability.

2/5/17 Draft Final

2/5/17

1.3 Final Budget Review 2016-17, Budget Review 3 2/5/17 2/5/17

1.4 Annual Financial Statements – 2016-17 Project Plan -Preparation & Audit

2/5/17 Interim dates 11th & 12th May 2017 EOY audit dates 12th -14th September 2017

1.6 Annual Financial Statements – 2016/17 Oct 17 TBC

Coorong District Council DRAFT Audit Committee Work Program – 2017

2

Activity Meeting Date Responsible Officers

Current Status/Outcomes

Date Completed

Follow up Action (for next year’s work program)

1.7 Financial Performance Report – 2016-17 – compares audited statements with original budget and explains variances

Dec 17 TBC

1.8 2017-18 Budget Review # 1 Dec 17 TBC

2. Internal Controls and Risk Management Systems

2.1 Review Councils internal financial control framework, together with associated policies & procedures documents.

2/5/17 3qtr audit report UHY Haines Norton report include 2/5/17

2.2 Review risk assessment decision making framework. TBA

2.3 Review & comment on risk register. TBA

2.4 Review and comment on Councils’ disaster recovery plan as well as the business continuity plan

2/5/17 Ongoing – update to the next audit committee

3. Internal Financial Audit

3.1 Develop an internal audit program. Staff to develop a cyclical audit program to ensure that the internal controls as identified in the internal control framework are operating effectively.

Presented 13/2/16

3.2 Review the internal audit annual work program, and receive twice yearly summary reports on work undertaken outlining any significant issues discovered.

Report after each quarter Review Program Dec 17

Coorong District Council DRAFT Audit Committee Work Program – 2017

3

Activity Meeting Date Responsible Officers

Current Status/Outcomes

Date Completed

Follow up Action (for next year’s work program)

3.3 Having regard to results of its own work program and the Council’s available resources, risks and anticipated benefits and costs, the Audit Committee should identify whether there are key functions where it might recommend that an efficiency and economy audit be performed.

Ongoing

4. External Audit

4.1 Liaise with the Councils’ external auditor on the scope and planning of annual audits, including any issues arising from audits and the resolution of such matters.

Oct 17 TBC Meeting confirmed with Auditors to attend the Audit Committee Meeting 3rd October 2017

4.2 All correspondence between the Auditor & Council is to be tabled for consideration. The audit committee will review and comment on the Councils response to, and actions taken as a result of issues raised from any external audit.

Ongoing Interim dates 11th & 12th May 2017 EOY audit dates 12th -14th September 2017

4.3 Recommend the engagement of the Councils’ external auditor, including the appointment, reappointment, and removal of the Councils’ external auditor.

2021 Current 5 year contract expires 30 June 2021 Interim Audit to be undertaken 11 & 12 May 2017

Dec 2016 Confirm dates for 16/17 Final Audit

4.5 Obtain written assurances from Council management to confirm that Councils auditors do not provide additional non audit services.

Oct 17 TBC

5. Reporting Requirements of the Audit Committee

5.1 Ensure that significant, urgent matters identified through the work program are formally and promptly reported to Council.

Ongoing

Coorong District Council DRAFT Audit Committee Work Program – 2017

4

5.2 Table the minutes of audit meetings together with updated Audit Committee work programs as part of the agenda of the next Council meeting, ensuring recommendations are considered and adopted as required.

Ongoing

Activity Meeting Date Responsible Officers

Current Status/Outcomes

Date Completed

Follow up Action (for next year’s work program)

5.3 Prepare annually a report to Council on the Audit Committees performance over the past year and include the report in the Annual Report of Council.

Oct 17 TBC

5.4 Review terms of reference on an annual basis. Oct 17 TBC

6. Financial Governance

6.1 Ensure that management develop a comprehensive schedule of finance policies to be developed or reviewed. With the relevant policies included in the audit committee work program.

14/3/17

6.2 Initial Policies to be scheduled include: Whistle Blower Fraud & Corruption Prevention Annual Business Plan & Budget Policy Debt Recovery & Financial Hardship Policy Prudential Management Policy Strategic Rating Policy Asset Accounting Policy Disposal of Council Land & Other Assets Policy Acquisition of Goods & Services Policy Rate Rebate Policy Internal Financial Control Policy Infrastructure & Asset Management Policy

Oct 2017 Oct 2017 Oct 2017 Oct 2017 May 2018 May 2018 May 2018 May 2018 May 2018 June 2016 Nov 2018

Top 4 will be presented/review for October meeting Review policies presented 1) Rate Rebate

Policy 2) Funding Policy

to audit committee 2/5/17

Coorong District Council DRAFT Audit Committee Work Program – 2017

5

Treasury Management Policy Risk Management Policy Funding Policy Community Group Loan Policy

March 2018 May 2018 April 2016 April 2016

7. Strategic Planning

7.1 Prepare and update Asset Management Plans for all classes of assets. Buildings, water supply and stormwater assets currently do not have asset management plans. Prepare Project Plans for Audit Committee to monitor.

Plan Presented Dec 16 Monitor progress

7.2 Update Long Term Financial Plan as soon as practical after the adoption of the Annual Business Plan.

14/3/17 Mid yr 2/5/17 Draft Annual Budget

Presented at the audit committee 14/3/17 Presented at the audit committee 2/5/17

Coorong District Council

Audit Committee Agenda 2 May 2017

Appendix 3

UHY Haines Norton Internal Controls Report

UHY Haines Norton Page 1

Internal Financial Controls

2017 Quarter 3 Review

For the Coorong District Council

April 2017

UHY Haines Norton Page 2

Contents Introduction ...................................................................................................................................... 3

Legislation ..................................................................................................................................... 3

Internal Financial Controls ............................................................................................................. 3

Better Practice Model .................................................................................................................... 3

Risk Management Standard ........................................................................................................... 3

Risk and Control Assessment Process ................................................................................................ 4

Assessing Risks .............................................................................................................................. 4

Likelihood .................................................................................................................................. 4

Consequence ............................................................................................................................. 4

Council Risk Frameworks ............................................................................................................... 5

Risk Level ................................................................................................................................... 5

Core and Additional Controls ......................................................................................................... 6

Quarter 3 2017 Risk Assessment ........................................................................................................ 6

Methodology ................................................................................................................................. 7

Limitations..................................................................................................................................... 7

Risk Levels ..................................................................................................................................... 7

Inherent/Raw Risk Assessment – Risk Levels Without Controls .................................................. 7

Evaluation of Controls ................................................................................................................... 8

Evaluation of Effectiveness of Controls ...................................................................................... 8

Level of risks with 2014 controls in place ................................................................................... 9

Level of risks with current controls in place ................................................................................ 9

Summary of Results ..................................................................................................................... 10

Conclusion ................................................................................................................................... 10

Appendix 1 – Assessment of 2017 Quarter 3 Risks

Appendix 2 – Residual Risk Summary for Individual Business Risks

Appendix 3 - Summary of Suggested Improvements for Extreme and High Residual Risk Areas

UHY Haines Norton Page 3

Introduction

Legislation Section 125 of the Local Government Act 1999 states that:

‘Council must ensure that appropriate policies, practices and procedures of internal control are

implemented and maintained in order to assist the Council to carry out its activities in an efficient

and orderly manner to achieve its objectives, to ensure adherence to management policies, to

safeguard the Council’s assets and to secure (as far as possible) the accuracy and reliability of

Council records’

Internal Financial Controls Internal financial controls are a framework of policies, procedures and practices that assist an

organisation in directing, monitoring and measuring the use of their resources. Controls assist in

preventing and detecting fraud and theft, and also diminishing the effect of error.

Better Practice Model The Local Government (Financial Management) Regulations 2011, s19(3) requires that an auditor

must assess the internal controls of a Council based on the criteria in the Better Practice Model –

Internal Financial Controls.

The ‘Better Practice Model’ outlines the key financial risks faced by Local Government in South

Australia and the suggested controls which assist in limiting exposure to these risks. This report has

used the Better Practice Model for assessing the financial controls for the Coorong District Council.

Risk Management Standard The Australia/New Zealand Risk Management Standard AS/NZS ISO 31000-2009 – Risk Management-

Principles and guidelines outlines the process for risk management with the interacting process steps

being: (see diagram following)

Communication and consultation

Establishing the context

Risk identification

Risk analysis

Risk evaluation

Risk treatment

Monitoring and review

The Better Practice Model identifies the normal risks in financial management along with possible

controls.

UHY Haines Norton Page 4

Process for Risk Management

Risk and Control Assessment Process

Assessing Risks Assessing risk involves determining how likely it is that an event will occur and then determining the

consequence if that event were to occur, resulting in a risk ‘level’.

Likelihood

The Better Practice Model measures the likelihood of a risk occurring as:

E. Almost certain Is expected to occur in most circumstances

D. Likely to occur Will probably occur in most circumstances

C. Possible Might occur at some time

B. Unlikely Could occur at some time

A. Rare May occur only in exceptional circumstances

Consequence

There are a number of consequences if an event occurs. The Better Practice Model categorises the

consequences of risks as:

Socio-political & community issues

Business impact

Financial cost and delay in operations

Legal issues

Public safety and environment

UHY Haines Norton Page 5

All of the consequences listed above, except for public safety and environment are considered by

Local Government when assessing internal financial controls. Although there can be a financial

impact to Local Government resulting from public safety and environmental issues, those risks are

not controlled in this framework. It is important to appreciate that Local Government entities are

also subject to a variety of additional risks that are not covered in this framework.

Council Risk Frameworks The Better Practice Model outlines a standard risk matrix of consequences of risk. Council needs to

consider their own businesses, communities and structures and determine if their risk ‘tolerance’ or

consideration of consequence is different to this standard model.

Referring to the consequence table below, a smaller council may consider the loss of $5,000 as a

greater consequence than ‘insignificant’. A larger council may consider that a higher financial impact

than $100,000 would be termed catastrophic.

If Council determines and resolves a different tolerance to risk than that outlined in the Better

Practice Model, the Internal financial controls would need to be re-assessed against the new

consequence table.

The consequences of risks occurring are graded as summarised in the table below (Refer: Appendix 1

for full risk table from Better Practice Model):

Impact measurement

Political/Community – effect on public image or level of community concern

Cost/Financial Impact

Delay in routine tasks Legal issues

1.Insignificant Insignificant level Less than $5k

up to ½ day

2.Minor Minor level $5k to $20k 1 day

3.Moderate Moderate level $20k to $50k 1-3 days Noncompliance and breach of regulation

4.Major Major/Significant $50k to $100k 3-5 days Serious breach, prosecution/fine

5.Catastrophic Huge effect, community outrage

Over $100k Over 5 days Failure of programs

Major breach, litigation

Risk Level

The following table shows the resulting risk level when the consequence and likelihood of an event occurring has been determined.

Consequence Insignificant Minor Moderate Major Catastrophic

Likelihood 1 2 3 4 5

Almost Certain E Moderate High High Extreme Extreme

Likely D Low Moderate High Extreme Extreme Possible C Low Low Moderate High Extreme

Unlikely B Low Low Low Moderate High

Rare A Low Low Low Moderate High

The risk levels attained require management attention and actions need to be prioritised to address the risks with the highest levels first.

Risk level Management Response

Extreme Intolerable, immediate management attention required High Significant, management actions required

Moderate Tolerable, specific monitoring or response procedures required

Acceptable Manage by routine procedures.

UHY Haines Norton Page 6

Core and Additional Controls The model suggests a number of controls which can be implemented to address risk levels. The

controls suggested are divided between ‘Core’ and ‘Additional’. Core controls are more critical and

the external auditors may place more emphasis on these.

The Coorong District Council has undertaken an initial assessment of their core and additional

controls back in 2014. From this assessment, all of the extreme and the majority of the high residual

risks have been identified for testing in quarter 3 of 2017. The results of which are reflected in this

report.

Quarter 3 2017 Risk Assessment The following risks have been identified for assessment in quarter 3 of 2017.

UHY Haines Norton Page 7

Methodology Assessment of risk is a subjective exercise and the Standard places emphasis on communication and

consultation. UHY Haines Norton’s assessors consulted with relevant staff and management in

discussing each risk, the possible controls within the Better Practice Model and the controls

currently in place for the Coorong District Council.

Limitations The scope of this assessment covered controls in place for the first three quarters of the 2016/17

financial year. This period of assessment does not necessarily encompass all controls identified for

assessment, ie. some end of year processes. In these cases we have looked at prior year processes to

give an indication as to the effectiveness of the control.

Due to significant staff changes in the Finance Department, there has been a significant loss of

knowledge and in some cases evidence of processes that were carried out. For example, the

employee who undertook the rating function is no longer employeed and there has been a loss of

evidence of certain procedures that were carried out.

This assessment has been prepared based on the information and feedback provided by

management and staff of the Coorong District Council. Accordingly the contents of this document

cannot be regarded as definitive advice until a complete internal audit of Council’s internal financial

controls is undertaken.

Risk Levels

Inherent/Raw Risk Assessment – Risk Levels Without Controls

The inherent or raw risk level is the level of risk without any controls in place. This assessment

assists organisations in understanding what their highest risk areas are.

The following graph shows the level of risk without any of the controls in place for the risks being

assessed in quarter 3 of 2017.

Extreme75%

High25%

Moderate0%

Low0%

"Raw" Risk Levels without Controls

UHY Haines Norton Page 8

Evaluation of Controls Appendix 1 – Assessment of 2017 Quarter 3 Risks considers each risk category and business process,

details the possible controls and the suggested actions to improve the effectiveness of the controls.

Controls identified were tested to assess their effectiveness.

The effectiveness of each control (as discussed with management and staff) is shown.

Evaluation of Effectiveness of Controls

The controls in the Model are assessed in the following manner:

1. Ineffective

The control has not been implemented. Urgent management action is required to implement the

described control processes.

2. Requires significant improvement

The control has been implemented, but with significant deficiencies in the consistency and

effectiveness of the implementation. Significant management action is required to implement

processes to improve the effectiveness of the control.

3. Partially effective

The control has been implemented but with some deficiencies in the consistency and/or

effectiveness in which it has been applied.

4. Majority effective

The control has been implemented and in the majority of cases has been consistently and/or

effectively applied. There is potential to enhance the effectiveness of the control, but only with

minor adjustments.

5. Effective

The control has been fully implemented and has in all cases been consistently and/or effectively

applied.

UHY Haines Norton Page 9

Level of risks with 2014 controls in place

The following graph shows the level of risk based on the 2014 assessment for the quarter 3 risks

being assessed.

Level of risks with current controls in place

The following graph shows the level of risks with the current controls in place.

Extreme25%

High70%

Moderate0%

Low5%

Risk Levels with 2014 Controls

Extreme5%

High35%

Moderate55%

Low5%

Risk Levels with 2017 Controls

95% of risks are

extreme or high

40% of risks are

extreme or high

UHY Haines Norton Page 10

Summary of Results We can see that there has been substantial improvement in the controls assessed in quarter 3 2017.

In 2014, these controls resulted in an extreme or high residual risk in 95% of business risks. These

same business risks have dropped to 40% extreme or high residual risks. We have summarised a

table in Appendix 2 to show the individual business risks and their assessed residual risk for both

2014 and 2017.

Whilst there has been improvement, there is still work that needs to be undertaken to reduce these

risk levels further. We have provided a summary of our suggested improvements in Appendix 3.

In addition to these suggestions, we would like to highlight some general observations that we think

should be brought to your attention.

General Observation 1

We understand that there has been considerable turnover of staff within the Finance Department.

This has highlighted the lack of documentation of finance processes. In our view, every process that

is undertaken within an employees role should be documented and retained to allow another

employee to be able to undertake this function without assistance. This is important in the event of

a loss of knowledge through either employee termination or leave of absence. We understand that

this has been a challenge for Council this financial year and there has been a loss of knowledge and

even evidence of process.

General Observation 2

Currently there is a lack of segregation of duties within the Finance Department. We understand that

due to limited resources, there are employees who are performing multiple financial functions that

we consider should be segregated. This increases your risk of fraud within these areas by not only

allowing the employee to carry out the fraud, but making detection of the fraud improbable. Ideally

IT enforced segregation of duties should be established to ensure that employees cannot access

financial functions that are not within their job descriptions. We understand that due to Council’s

size, segregation of some high risk financial functions may not be practical. In the event of these

circumstances, it is extrememly important to implement other controls to increase the likelihood of

detection of fraud or errors. For example, we would suggest that a high emphasis be placed on the

use of exception reports. These should be produced and reviewed by segregated employees who do

not perform the function that the exception report is reporting on.

Conclusion Overall, we commend Council on their improvement of the controls surrounging the business risks

identified for quarter 3 2017 assessment. To be able to reduce the extreme or high residual risks by

55% since 2014 requires a large amount of focus and resources. Whilst this improvement is

encouraging, there is still work to be undertaken to reduce the risks further.

Appendix 2 – Residual Risk Summary for Individual Business Risks

Risk # Risk

Inherent

Risk

Residual Risk

in 2014

Residual Risk

in 2017

2.1.3 Budgets are inaccurately reported with differences in the budget adopted by Council and that exercised by Council Extreme High Moderate

2.2.1 GL does not contain accurate financial information Extreme High Moderate

3.1.1 Cash floats and petty cash are inadequately safeguarded High High Moderate

3.7.5 Fixed asset maintenance and/or renewals are inadequately planned Extreme Extreme High

3.8.1 Projects are either inaccurately recorded or not recorded at all Extreme Extreme High

3.8.2 Over expenditures on projects may not be detected Extreme Extreme High

3.9.3 Clubs/Community Groups not able to repay Loans/Grants to Council. Extreme High High

4.1.3 Disbursements are not authorised properly Extreme High Moderate

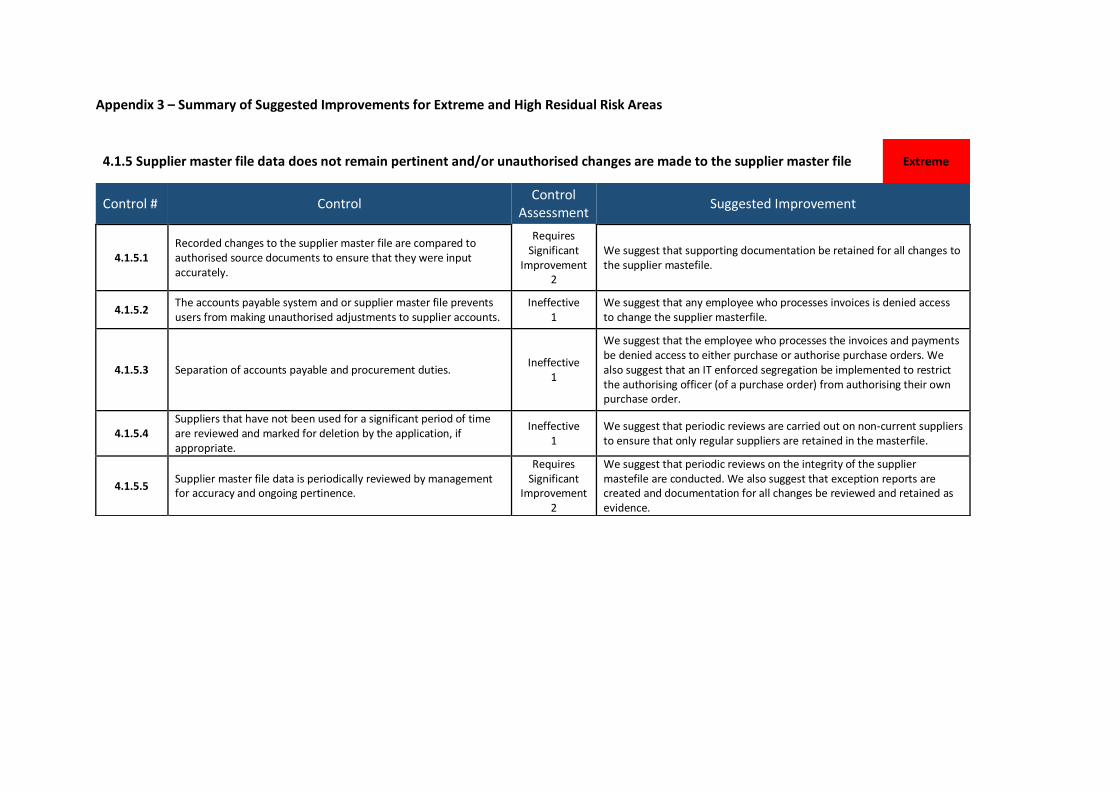

4.1.5 Supplier master fi le data does not remain pertinent and/or unauthorised changes are made to the supplier master fi le Extreme Extreme Extreme

4.4.2 Payroll master fi le does not remain pertinent Extreme High High

4.5.1 Tax liabilities are either inaccurately recorded or not recorded at all High High Moderate

5.1.2 Rates and rate rebates are either inaccurately recorded or not recorded at all. Extreme High High

5.2.2 Grant funding is not claimed by council on a timely basis or not claimed at all Extreme Extreme High

5.5.1 Receipts are either inaccurately recorded or not recorded at all Extreme High Moderate

5.5.2 Receipts are not deposited at the bank on a timely basis Extreme High Moderate

6.1.3 Purchase orders are either recorded inaccurately or not recorded at all High High Low

6.1.5 Supplier master fi le data does not remain pertinent and/or unauthorised changes are made to the supplier master fi le High High Moderate

6.2.6 Salary sacrifice transactions are inaccurately processed Extreme High Moderate

6.3.1 Council reimburses expenses to Elected Members of a personal nature High Low Moderate

7.1.1 Council is not able to demonstrate that all probity issues have been addressed in the contracting process Extreme High Moderate

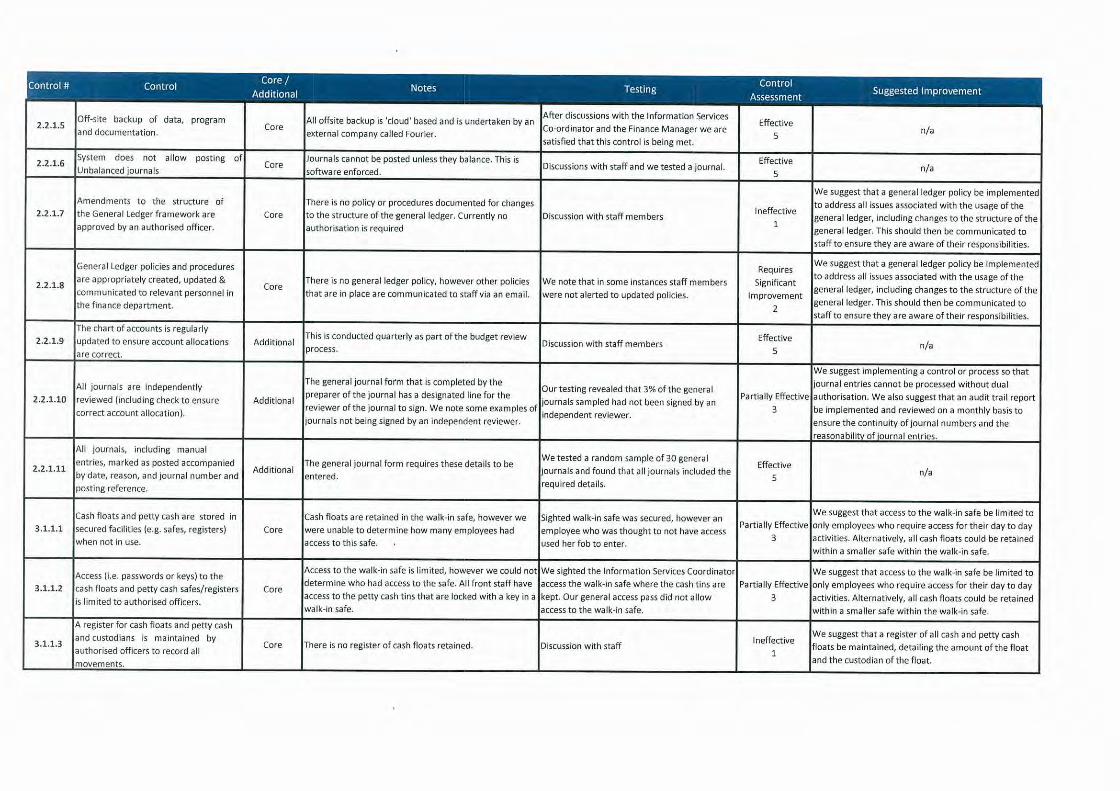

Appendix 3 – Summary of Suggested Improvements for Extreme and High Residual Risk Areas

4.1.5 Supplier master file data does not remain pertinent and/or unauthorised changes are made to the supplier master file Extreme

Control # Control Control

Assessment Suggested Improvement

4.1.5.1 Recorded changes to the supplier master file are compared to authorised source documents to ensure that they were input accurately.

Requires Significant

Improvement 2

We suggest that supporting documentation be retained for all changes to the supplier mastefile.

4.1.5.2 The accounts payable system and or supplier master file prevents users from making unauthorised adjustments to supplier accounts.

Ineffective 1

We suggest that any employee who processes invoices is denied access to change the supplier masterfile.

4.1.5.3 Separation of accounts payable and procurement duties. Ineffective

1

We suggest that the employee who processes the invoices and payments be denied access to either purchase or authorise purchase orders. We also suggest that an IT enforced segregation be implemented to restrict the authorising officer (of a purchase order) from authorising their own purchase order.

4.1.5.4 Suppliers that have not been used for a significant period of time are reviewed and marked for deletion by the application, if appropriate.

Ineffective 1

We suggest that periodic reviews are carried out on non-current suppliers to ensure that only regular suppliers are retained in the masterfile.

4.1.5.5 Supplier master file data is periodically reviewed by management for accuracy and ongoing pertinence.

Requires Significant

Improvement 2

We suggest that periodic reviews on the integrity of the supplier mastefile are conducted. We also suggest that exception reports are created and documentation for all changes be reviewed and retained as evidence.

3.7.5 Fixed asset maintenance and/or renewals are inadequately planned High

Control # Control Control Assessment Suggested

Improvement

3.7.5.1

Asset Management Plans (including plans to obtain sufficient funding to cover expected capital investment) are prepared. The capital investment required is reviewed regularly for appropriateness.

Partially Effective

3

We suggest that Asset Management Plans for Stormwater and Water Supply be developed and implemented as soon as practical.

3.7.5.3 Asset Management Plans exist for all major asset classes and all changes to the asset management plan must be approved by Council.

Partially Effective

3

We suggest that Asset Management Plans for Stormwater and Water Supply be developed and implemented as soon as practical.

3.8.1 Projects are either inaccurately recorded or not recorded at all High

Control # Control Control Assessment Suggested

Improvement

3.8.1.2 Management review costing methodology used for projects to ensure appropriate method of full cost attribution is in place.

Ineffective 1

We suggest that a policy be developed to detail the process of project costing, including the methodology for full cost attribution and plant hire.

3.8.1.3 Overhead rates including plant hire are reviewed and revised on a regular basis.

Partially Effective

3

We suggest that all plant hire rates are reviewed and revised on a regular basis. This process should be documented as evidence of review.

3.8.2 Over expenditures on projects may not be detected High

Both core and additional controls appear to be operating effectively, however due to the raw risk rating of extreme, the presence of operating controls can only reduce the

residual risk to ‘high’. As such, we suggest that the current controls are constantly monitored to ensure they remain effective.

3.9.3 Clubs/Community Groups not able to repay Loans/Grants to Council. High

Control # Control Control

Assessment Suggested Improvement

3.9.3.2 Loan receivable reconciliations are prepared on a regular basis and reviewed by an independent person.

Requires Significant

Improvement 2

We suggest that all loans receivable are reconciled on a regular basis and regular monitoring of the outstanding balances should be undertaken.

3.9.3.3

Council establishes clear policy for issuing funds to Clubs / Community Groups. Policy details appropriate approval of funds issued in accordance with Delegations of Authority and compliance with Conflict of Interest Policy.

Majority Effective

4

We suggest that the Community Group Loan Policy be updated to include procedures for addressing any conflict of interest issues.

3.9.3.5

Management reviews ageing profile of loan receivables to identify all outstanding receipts not received in accordance with original collection schedule. All outstanding items are immediately investigated to ensure timely recovery of outstanding amounts.

Ineffective 1

We suggest that community loans are reviewed for ageing to ensure that the community groups are meeting the terms of their agreement. Any outstanding payments should be promptly followed up.

3.9.3.6 Council to identify security held and any impairment issues against loans receivables from Clubs and Community groups.

Requires Significant

Improvement 2

We suggest that impairment of the community loans is assessed on an annual basis to ensure the true collectability is reflected.

4.4.2 Payroll master file does not remain pertinent High

Control # Control Control

Assessment Suggested Improvement

4.4.2.1 Access to payroll/provision master file is restricted to authorised officers only.

Ineffective 1

We suggest that council review user access levels and ensure that only the employees who require access to the payroll masterfile in their day to day duties are given access.

4.4.2.2 Any changes to the payroll master files are approved by management.

Ineffective 1

We suggest that a segregated employee who does not have access to make changes to the payroll masterfile is commissioned to review and sign off the payroll masterfile exception report.

4.4.2.3 Payroll master file data is periodically reviewed for accuracy and pertinence.

Ineffective 1

We suggest that council review the integrity of the payroll masterfile periodically and exception reports be reviewed by an independent employee who does not have access to make changes to the payroll masterfile.

4.4.2.4 Departmental managers periodically review listings of current employees within their departments and notify the personnel department of necessary changes.

Ineffective 1

We suggest that Departmental Managers are provided a list of current employees on a regular basis. Departmental Managers should then be required to confirm all employees as current. This review should be formally documented and retained as evidence.

4.4.2.5 Recorded changes to the payroll master files are compared to authorised source documents to ensure accurate input.

Partially Effective

3

We suggest that the payroll masterfile exception reports be reviewed by an independent employee who does not have access to make changes to the payroll masterfile.

5.1.2 Rates and rate rebates are either inaccurately recorded or not recorded at all. High

Control # Control Control

Assessment Suggested Improvement

5.1.2.2 Management regularly reviews the calculation methodology within the rate application system and for a sample of ratepayers to ensure correct calculation and methodology has been used.

Ineffective 1

Considering we could not determine whether this control existed (due to the employee who generated the rates no longer being employed and a lack of evidence that the control did exist), we suggest that a procedure is put in place to ensure that controls are documented and can be demonstrated.

5.1.2.3 Regular review of exempt properties to ensure still valid, interest flag switched off and rate rebates.

Ineffective 1

Considering we could not determine whether this control existed (due to the employee who generated the rates no longer being employed and a lack of evidence that the control did exist), we suggest that a procedure is put in place to ensure that controls are documented and can be demonstrated.

5.1.2.5 Employees responsible for processing rate notices cannot process payment of their own rates.

Ineffective 1

Whilst it is not always possible to prohibit the employee responsible for processing the rates notice from processing their own rates, we do suggest that a review is conducted by an independent employee on the properties owned by this employee.

5.1.2.6 Regular independent review of the rates aged receivables reports and independent check of rates payable by rates staff.

Ineffective 1

We suggest that there is a regular review of the rates ageing at the time of the monthly reconciliation. We also suggest that the amounts owing by the rates staff are reviewed regularly.

5.1.2.8 Rates are generated using test data prior to the rates billing run. Ineffective

1

Considering we could not determine whether this control existed (due to the employee who generated the rates no longer being employed and a lack of evidence that the control did exist), we suggest that a procedure is put in place to ensure that controls are documented and can be demonstrated.

5.1.2.9 Rate model outcomes reconciled to billing run outcomes prior to generation of rates.

Ineffective 1

Considering we could not determine whether this control existed (due to the employee who generated the rates no longer being employed and a lack of evidence that the control did exist), we suggest that a procedure is put in place to ensure that controls are documented and can be demonstrated.

5.1.2.12 Reconciliation of rates notices produced and rates to rates posted / distributed.

Ineffective 1

Considering we could not determine whether this control existed (due to the employee who generated the rates no longer being employed and a lack of evidence that the control did exist), we suggest that a procedure is put in place to ensure that controls are documented and can be demonstrated.

5.1.2.13 Fine write-offs approved by authorised officer.

Requires Significant

Improvement 2

We suggest that an exception report be generated to show all of the fine write offs processed within the rates module each month. This report should be reviewed by a segregated employee and matched to an approval authorisation.

5.2.2 Clubs/Community Groups not able to repay Loans/Grants to Council. High

Control # Control Control

Assessment Suggested Improvement

5.2.2.1

Council has a clear policy on Grant funding detailing assessment process, recognition, treatment, claim collection, community expectations and funding period and, disclosure of any conflicts of interest.

Ineffective 1

We suggest that a grant funding policy is created to address the requirements surrounding the application, recording and maintaining of grant funding.

5.2.2.2

Management performs regular review of all grant income and to monitor compliance with both the terms of grants and Council’s Grant policy (including claiming and collecting funds on a timely basis).

Ineffective 1

We suggest that a grant funding policy is created to address the requirements surrounding the application, recording and maintaining of grant funding.

5.2.2.5 Council establishes a grant revenue register which records details such as reporting deadlines, amount and instalments expected and key milestones.

Ineffective 1

We suggest that a grant revenue register is created to assist with the maintenance and reporting requirements of grant funding.

Coorong District Council

Audit Committee Agenda 2 May 2017

Appendix 4

Revised Policies

Rating Policy Strategic Reference Providing leadership for the community and

ensuring efficient and effective management of the community’s resources

File reference AR16/8698

Responsibility Community & Corporate Department

Revision Number Original

Effective date 27 June 2016

Last revised date May 2017

Minutes reference 136/16

Next review date Annually

Applicable Legislation Local Government Act, 1999

Related Policies 2017/18 Annual Business Plan & Budget

Related Procedures N/A

1. Purpose

The purpose of this policy is to outline Council’s approach towards rating its community in 2017/18 and to meet the requirements of the Local Government Act 1999 (SA) (the Act), with particular reference to Section 123. This Section requires Council to set out its rates structure and policies (as part of the Annual Business Plan) each financial year.

2. Scope

The policy covers:

method used to value land

adoption of valuations

business impact statement

Council’s revenue raising powers

differential general rates

single farm enterprise

service charges

Natural Resource Management levy (the Council’s collection role)

pensioner concessions

other concessions

Rating Policy – 2017/18

NOTE: Electronic version in the TRIM System is the controlled version Printed copies are considered uncontrolled. Before using a printed copy, verify that it is the current version

Page 2 of 12

payment of rates

late payment of rates

remission and postponement of rates

rebate of rates

rate capping

sale of land for non-payment of rates

objections

disclaimer

3. Strategic Focus

In setting its rates for the 2016/2017 financial year, Council has considered the following:

Strategic Management Plan 2016-2020

Reviewed Long Term Financial Plan 2017/18-2026/27

The 2017/18 Annual Business Plan & Budget

Current economic climate and relevant factors such as inflation, interest rates & the introduction of a carbon tax

Specific issues faced by its community, which include: - the need to update and maintain capital equipment to enable servicing of the

road network and other essential infrastructure;

- the maintenance and improvement of community assets to enable the District to be promoted as an attractive place in which to live, work, invest and visit;

- the sustainable management of waste and the promotion of recycling programs;

- the fostering and promoting of recreational activities for all ages.

The budget context for the 2016/2017 financial year

The impact of rates and service charges on the community, including: - households, businesses and primary producers;

- the broad principle that the rate in the dollar should be the same for all properties except where there is clearly a different level of services available to ratepayers or some other circumstance which warrants variation from the broad principle;

- minimising the level of general rate required by levying fees and charges for goods and services on a user pays basis, where possible and equitable, to recover the full cost of operating or providing the service or goods, with provision for concessions to those members of the community unable to meet that cost.

Council has increased general rates by 3.2% to set a budget that will provide Council with sufficient revenue to meet its business plan objectives and to absorb cost increases. The Strategic Management Plan 2016-2020 provides the strategic direction of Council over a five year period while the budget provides detail for the 2017/18 year and the rates are set at a level to meet those strategic directions.

Rating Policy – 2017/18

NOTE: Electronic version in the TRIM System is the controlled version Printed copies are considered uncontrolled. Before using a printed copy, verify that it is the current version

Page 3 of 12

Council must raise revenue sufficient for the purpose of governance, administration and to provide appropriate goods and services for the community. The goods and services are especially those that would not be provided by private enterprise, e.g. infrastructure, waste management, community, regulatory, environmental health services and street lighting.

Rates are a system of taxation on the community for local government to deliver the goods and services expected by the community. All ratepayers receive benefits from paying rates. In considering the impact of rates on the various sectors of the community, Council has determined its rates so that they apply in a consistent manner and are commensurate with the level of services provided in the urban and rural areas.

Council conducts community engagement on a broad range of issues relating to specific programs and the future directions for the area. These opportunities are advertised in local papers, Council newsletters and special interest email groups. Council encourages feedback at anytime and can be done so by visiting www.coorong.sa.gov.au or posting to;

Chief Executive Officer Coorong District Council PO Box 399 TAILEM BEND SA 5260

4. Valuation Methodology

Council has adopted the use of capital value as the basis for valuing land within the Council area. Council considers that this method of valuing land provides the best of the options available to Council as prescribed in the Act and therefore the fairest method of distributing the rate responsibility across all ratepayers.

Council may adopt one of the following three valuation methodologies to value the properties in its area (Section 151 of the Act). They are:

Capital Value – the value of land, buildings and other improvements

Site Value – the value of the land and any improvements which permanently affect the amenity of use of the land, such as drainage works, but excluding the value of buildings and other improvements.

Annual Value – a valuation of the rental potential of the property.

In adopting capital value as the basis for valuing land, Council believes that this more appropriately addresses the principles of taxation and is a better indication of capacity to pay.

Council does not determine property valuations but chooses to exercise the right under Section 151 of the Act to adopt the capital valuations as assessed by the Valuer General through the State Valuation Office. If a ratepayer is dissatisfied with a property valuation then an objection may be made as detailed in Section 21 of this Policy.

5. Business Impact Statement Council has considered the impact of rates on businesses in the Council area, including primary production. Council maintains contact with the business community both directly and through the Regional Development Australia Murraylands and Riverland.

Rating Policy – 2017/18

NOTE: Electronic version in the TRIM System is the controlled version Printed copies are considered uncontrolled. Before using a printed copy, verify that it is the current version

Page 4 of 12

Council has also considered:

Those elements of Council’s Strategic Management Plan 2016-2020 relating to business development.

Coorong District Council Development Plan.

The equity of the distribution of the rate burden – including the decision to provide a differential rate between residential, commercial/industrial, primary production and vacant land as outlined under the heading “Differential General Rates”. Council considers that all ratepayers have access to broadly comparable services and are generally similarly impacted upon by prevailing economic conditions.

Council’s policy on facilitating local economic development including: - preference for local suppliers where price, quality and service provision are

comparable to suppliers outside the Council area;

- support for and contribution to tourism marketing;.

- support for and contribution to the Murraylands Regional Development Board.

Current local, state and national economic conditions and expected changes during the next financial year. Changes in the valuation for 2017/18 based on the general valuation assessment, where the capital value has increased by ***%.

Specific infrastructure maintenance issues that will principally benefit businesses and primary producers include: - up-grading the pavement structure and sealing major roads both rural and

urban, partly as a result of the need for roads to carry heavier vehicles to service industry.

6. Council’s Revenue Raising Powers

All land within a Council area, except for land specifically exempt (e.g. Crown land held for a public purpose, Council occupied land and land prescribed in the Act – refer Section 147 of the Act), is rateable. The Act provides for a Council to raise revenue for the broad purposes of the Council through a general rate, which applies to all rateable properties, or a differential general rate, which applies to different classes of properties.

Council can raise separate rates, for specific areas of the Council or service rates or charges for specific services. Council also raises revenue through fees and charges, which are established having consideration to the cost of the service provided and any equity issues. The list of applicable fees and charges is available on Council’s website www.coorong.sa.gov.au or by contacting one of the Council offices.

7. Differential General Rates

The Act allows Councils to ‘differentiate’ rates based on the use of the land, the locality of the land, the use and locality of the land or on some other basis determined by Council.

Rating Policy – 2017/18

NOTE: Electronic version in the TRIM System is the controlled version Printed copies are considered uncontrolled. Before using a printed copy, verify that it is the current version

Page 5 of 12

Coorong District Council applies different rates on the basis of land use. Land use is recognised by other State taxing agencies and is easily identified and understood by our communities. It is therefore considered the most appropriate method for applying different rates by the majority of councils.

Definitions of the use of the land are prescribed by regulation and are as follows:

(1) Residential (2) Commercial – Shops (3) Commercial – Office (4) Commercial – Other (5) Industrial – Light (6) Industrial – Other (7) Primary Production (8) Vacant Land (9) Other

For ease of classification and for the application of rates, Council categorises these into the following differentials:

Residential/Other (1 & 9) Commercial/Industrial (2-6) Primary Industry (7) Vacant (8)

As part of the valuation assessment process the State Valuation Office applies a land use to each assessment to identify the predominant use of the land. This land use is used by various taxing authorities. Council generally applies this land use for general rating purposes however under the Act, Council is the relevant authority that determines land use for rating purposes and our rating land use must meet the definitions under Development Regulations. As such the local government land use may vary from that used by other taxing authorities.

If a ratepayer believes that a particular property has been wrongly classified as to its land use, then an objection may be made as detailed below.

Differential rates better reflect consumption of council services but can also be tailored to support other key objectives, e.g. economic development, encourage capital development, or recognise the value of a specific land use sector.

Council’s budget contains rate revenue of $6.741m net of rebates and discounts (a 3.2% increase in net general rate revenue from the 2016/17 budget). Council is proposing to apply the following rate in the dollar to give effect to the increase in rate revenue to the following property classifications.

Rating Policy – 2017/18

NOTE: Electronic version in the TRIM System is the controlled version Printed copies are considered uncontrolled. Before using a printed copy, verify that it is the current version

Page 6 of 12

Summary - Differential Rate Revenue

Differentiating Factor/ 2016-17 2017/18 Land Use Rate in $ Rate in $ Vacant 0.4754

Primary Industry 0.3368

Residential/Other 0.3962

Commercial/Industrial 0.3962

Bulk Handling 1.1292

8. Fixed Charge Council has historically determined that a fixed charge is applied to all rateable assessments and there are no changes to this in 2017/18. Fixed charges in previous years have been $310 in 2010/11, $325 in 2011/12, $345 in 2012/13, $300 in 2013/14 and $300 in 2014/15 and 2015/16.

The primary reason for imposing a fixed charge is to ensure that all rateable properties make a base contribution to the cost of administering Council activities and maintaining the services and physical infrastructure that supports each property.

In applying the fixed charge only one charge can be imposed on two or more adjoining assessments with the same owner and occupier (contiguous).

Where a ratepayer believes that they may be eligible for a reduction in the fixed charge applied to contiguous assessments an objection may be made as detailed in Section 21.

Council has decided to keep the fixed charge at $XXX for 2017/18.

9. Separate Rates & Service Charges

Community Wastewater Management Schemes (CWMS) This service charge is set to cover the costs associated with operating and developing the Community Wastewater Management Schemes (CWMS) in townships throughout the Council area. Ongoing comparative reviews of Council’s CWMS charges reveals Council is charging considerably less for this service than other councils in its vicinity.

Council is currently progressing through a detailed CWMS Business Plan, which will provide a clear indication of the ongoing costs associated with maintaining CWMS systems. Over the next few years Council will seek to gain full cost recovery from its CWMS service charge.

Council has decided to charge the following CWMS charges for 2016/2017:

Tailem Bend, Meningie, Tintinara & Wellington East:

$XXX – per occupied unit

$XXX – per vacant allotment

Rating Policy – 2017/18

NOTE: Electronic version in the TRIM System is the controlled version Printed copies are considered uncontrolled. Before using a printed copy, verify that it is the current version

Page 7 of 12

Water Supply Council provides water supply systems to residential and commercial properties in the small townships of Wellington East and Peake. The full cost of operating these systems is raised from a range of service charges as follows:

Wellington East and Peake water supply; a Service Charge comprised of $XXX plus $XXX per kilolitre for usage in excess of 125 kilolitres per annum;

Kerbside Waste Management Council provides a comprehensive kerbside waste management collection service, including a yellow recycling bin, green organic waste bin and red residual general waste bin, to divert recyclables and green organics waste from landfill dumps.

These initiatives and increase in service levels resulted in the implementation of a Kerbside Waste Management Charge, which is in accordance with Councils financial strategies and its Long Term Financial Plan. The charge for 2014/2015 was $240 and 2015/2016 was $290 was only applied to those ratepayers who are recipients of the increased service levels and are within the kerbside collection boundary. This fee has increased to $325 in 2016/2017 in an effort to migrate towards a self funding cost system, so that those benefitting from the service are paying for it.

10. Natural Resource Management (NRM) Levy

The NRM Levy is a State Government tax imposed under the Natural Resources Management Act 2004. Council is obliged to collect the levy on behalf of the SA Murray Darling Basin and South East NRM Boards.

For that part of the Council area covered by the South Australian Murray Darling Basin Natural Resources Management Board, the levy is based property capital valuations and the rate is 0.02377 cents in the dollar. For that part of the Council area covered by the South East Natural Resource Management Board, the levy for the following land uses will be per property:

a. $XXX per rateable property with the land use of Residential, Vacant & Other; b. $XXX per rateable property with the land use of Commercial – Shop, Office or

Other; c. $XXX per rateable property with the land use of Industrial – Light or Other;

and d. $XXX per rateable property with the land use of Primary Production

The NRM levy is shown as a separate charge on the rates notice.

11. Single Farm Enterprise

Section 152(2)(d) of the Act provides that where a Council declares a general rate which is based in whole or in part, on a fixed charge:

“If two or more pieces of rateable land within the area of the Council constitute a single farm enterprise only one fixed charge may be imposed against the whole of the land”.

A single farm enterprise must be comprised of two or more pieces of rateable land which are farm land and are occupied by the same person or persons. To enable properties to

Rating Policy – 2017/18

NOTE: Electronic version in the TRIM System is the controlled version Printed copies are considered uncontrolled. Before using a printed copy, verify that it is the current version

Page 8 of 12

be identified as single farm enterprises it will be necessary for ratepayers to complete an application form to provide details to Council to enable Council to identify the land concerned.

An application form can be obtained from any of the Council offices.

12. Pensioner Concessions/State Seniors Concession/Other Concessions

An eligible pensioner may be entitled to a concession on their principal place of residence. All pensioner concession applications are administered by the State Government.

13. Payment of Rates Council has decided that the payment of rates will be by four instalments, due on:

9 September 2016

9 December 2016

9 March 2017 and

9 June 2017.

Council is offering a discount of judy

1.5% for the payment of all rates, in full, by 9 September 2016.

A notice will be sent to each ratepayer 30 days prior to each quarterly instalment being due.

Rates may be paid

By post to Coorong District Council at PO Box 399, Tailem Bend SA 5260

In person by cash, cheque, credit card or EFTPOS at the Meningie or Tailem Bend Offices during the hours of 8.30am to 5.00pm, or Tintinara Office during the hours of 11.00am to 3.00pm, Monday to Friday (noting that Meningie close for lunch between 12.30pm and 1.30pm)

Electronic payments available via the ‘web’, log onto www.coorong.sa.gov.au and follow the prompts or over the counter using CREDIT cards

By BPAY - see rate notice for biller code & reference number

By Post BPAY – see rate notice for biller code & reference number

By EFT Transfer to Council’s Bank Account (please quote Asst No as Reference)

BSB 105-170 Account No 015437140 Account Name Coorong District Council

14. Merchant Fee for Payment by Credit Card

Council has decided to collect the merchant fee charged for the use of credit cards. This fee will be calculated at the time of making payments and your receipt will show the amount of fee charged

Rating Policy – 2017/18

NOTE: Electronic version in the TRIM System is the controlled version Printed copies are considered uncontrolled. Before using a printed copy, verify that it is the current version

Page 9 of 12

15. Late Payment of Rates The Act provides that Councils impose an initial penalty of 2% on any payment for rates, whether by instalment or otherwise, that is received late. A payment that continues to be late is then charged a prescribed interest rate on the expiration of each month that it continues to be late. For the 2016/2017 financial year, compound interest will be charged, per month, of the amount in arrears, at the prescribed percentage as set by the Local Government Finance Authority.

When the Council receives a payment in respect of overdue rates the Council applies the payment as follows:

First – to satisfy any costs awarded in connection with court proceedings.

Second – to satisfy any interest costs.

Third – in payment of any fines imposed.

Fourth – in payment of rates, in chronological order (starting with the oldest rate account).