mgmt-165 chapter 03 slides - kids in prison program copyright © 2013 by the mcgraw-hill companies,...

TRANSCRIPT

McGraw-Hill/Irwin Copyright © 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Financial Statements Analysis and Financial

Models

Chapter 3

3-1

Key Concepts and Skills

Know how to standardize financial statements

for comparison purposes

Know how to compute and interpret important

financial ratios

Be able to develop a financial plan using the

percentage of sales approach

Understand how capital structure and dividend

policies affect a firm’s ability to grow

3-2

Chapter Outline

3.1 Financial Statements Analysis

3.2 Ratio Analysis

3.3 The DuPont Identity

3.4 Financial Models

3.5 External Financing and Growth

3.6 Some Caveats Regarding Financial Planning Models

3-3

3.1 Why Evaluate Financial

Statements? Internal uses

Performance evaluation – compensation and comparison between divisions

Management – identify problem areas (e.g., too little or too much cash, too little or too much inventory)

Planning for the future – guide in estimating future cash flows

External uses Creditors

Suppliers

Customers

Stockholders / Investors

3-4

3.1 Financial Statements Analysis

Common-Size Balance Sheets

Compute all accounts as a percent of total assets

Common-Size Income Statements

Compute all line items as a percent of sales

Standardized statements make it easier to compare

financial information, particularly as the company

grows.

They are also useful for comparing companies of

different sizes, particularly within the same industry.

3-5

3.2 Ratio Analysis

Ratios also allow for better comparison through time

or between companies.

As we look at each ratio, ask yourself:

How is the ratio computed?

What is the ratio trying to measure and why?

What is the unit of measurement?

What does the value indicate?

How can we improve the company’s ratio? (This is

hard! Typically no good answer… Ratios may

help highlight an issue, not much more)

3-6

Categories of Financial Ratios

Short-term solvency or liquidity ratios

Long-term solvency or financial leverage

ratios

Asset management or turnover ratios

Profitability ratios

Market value ratios

3-7

Balance Sheet, Greene Co.

3-8

Income Statement, Greene Co.

3-9

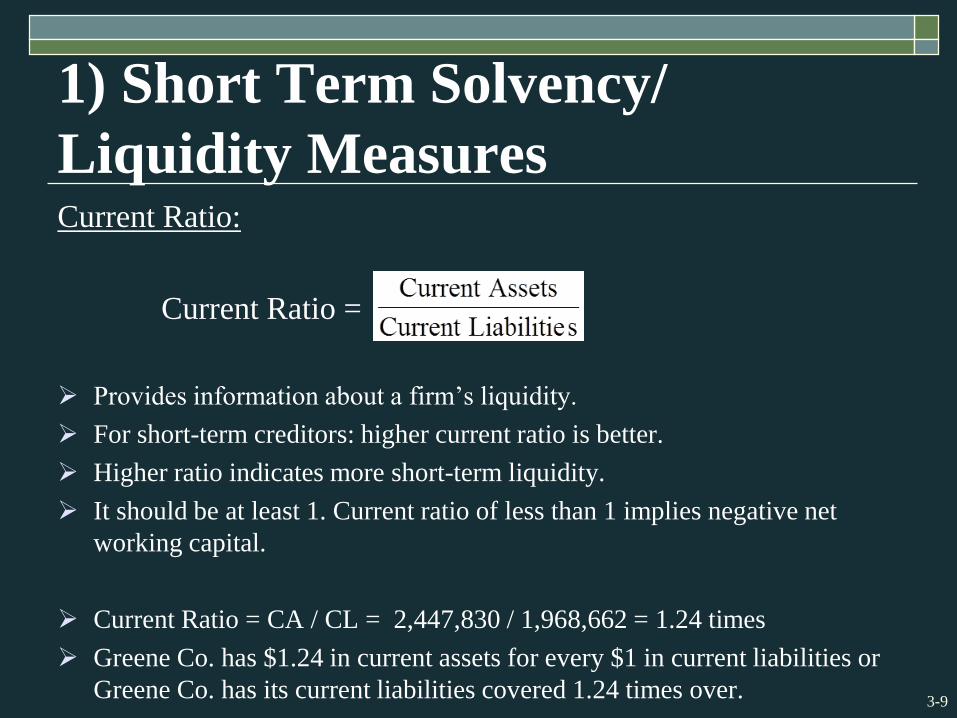

1) Short Term Solvency/

Liquidity MeasuresCurrent Ratio:

Current Ratio =

Provides information about a firm’s liquidity.

For short-term creditors: higher current ratio is better.

Higher ratio indicates more short-term liquidity.

It should be at least 1. Current ratio of less than 1 implies negative net

working capital.

Current Ratio = CA / CL = 2,447,830 / 1,968,662 = 1.24 times

Greene Co. has $1.24 in current assets for every $1 in current liabilities or

Greene Co. has its current liabilities covered 1.24 times over.

3-10

1) Short Term Solvency or

Liquidity MeasuresQuick or Acid - Test Ratio:

Quick Ratio =

Provides information about a firm’s liquidity.

Large inventories could be a sign of short-term trouble.

Quick Ratio = (2,447,830 – 300,459) / 1,968,662 = 1.09 times

3-11

1) Short Term Solvency/

Liquidity Measures

Cash Ratio:

Cash Ratio =

Cash Ratio = 680,623 / 1,968,662 = .346 times

3-12

Note on Liquidity

Concerns a firm’s ability to pay its bills over a

short period of time.

But is it ability to convert assets to cash

quickly?

No. You can convert anything to cash quickly

if you lower the price enough! (e.g. price of a

house).

Hence, it is ability to convert assets to cash

quickly without a significant loss in value.

3-13

Another Word of Caution about

Liquidity Is a higher current ratio a good thing?

Sufficiently high is good for short-term solvency.

However, too high is not good. Liquid assets earn lower returns in general… So too much in Current Assets/Liabilities compromises earning capacity of the firm, and reduces stock price.

Investors would prefer that the firm invested in profitable projects. If the firm is sitting on too much cash, investors will wonder if the executives are incapable or unwilling to come up with such projects, or why no dividends are paid or why no stock is bought back.

REMEMBER: objective of the firm is to maximize owner wealth!

3-14

Examples

Kirk Kerkorian’s takeover bid for Chrysler in April

1995 is a perfect example of investor dissatisfaction

with excess liquidity. At the time, Chrysler’s

management had accumulated $7.3 billion in cash

and marketable securities as a cushion against an

economic down-turn. Mr. Kerkorian instigated a

takeover bid because Chrysler’s management

refused to pay this cash to stockholders.

More recently, Apple sitting on $137 billion!

3-15

Consider the Scenario:

The current ratio exhibits no change over a two or three year

period, while the quick ratio experiences a steady decline.

How could this occur? Is it bad?

Implies:

-Co. is operating with lower levels of most liquid assets

-Situation should be monitored

-Problem could arise should a large amount of current

liabilities come due for payment at the same time

-But may not be major concern the company has sufficient

line of credit at a bank

-May indicate larger levels of inventory relative to current

liabilities. Slowing sales? Need to look at more ratios!

3-16

2)Long-Term Solvency or

Leverage Measures This group of ratios measures the level of indebtedness and the

ability to service debt.

Total Debt Ratio:

Total Debt Ratio =

Two Variations

Debt-Equity Ratio =

Equity Multiplier =

Assets Total

Equity Total - Assets Total

Equity Total

Debt Total

Equity Total

Debt) Total Equity Total(

Equity Total

Assets Total

3-17

2)Long-Term Solvency or

Leverage Measures Total Debt Ratio = (TA – TE) / TA

- (5,862,989 – 2,984,513) / 5,862,989 = .491 times or 49.1%

The firm finances slightly over 49% of their assets with

debt.

The firm has $0.49 in debt for every $1 in assets.

Debt-Equity Ratio = TD / TE =

= (1,968,662+909,814) / 2,984,513 = .964 times

Equity Multiplier = TA / TE = 1 + TD/TE =

= 1 + .964 = 1.964

3-18

2)Long-Term Solvency or

Leverage Measures Times Interest Earned (TIE) = EBIT / Interest =

= 1,174,690 / 5,785 = 203 times

- Informs us if the firm has its interest obligations covered.

- EBIT is not a good measure of cash available to pay

interest because it includes non-cash expenses

(depreciation and amortization). Hence,

Cash Coverage = EBITDA / Interest =

=(EBIT + Depreciation+Amortization) / Interest =

= (1,174,900 + 124,647) / 5,785 = 225 times

3-19

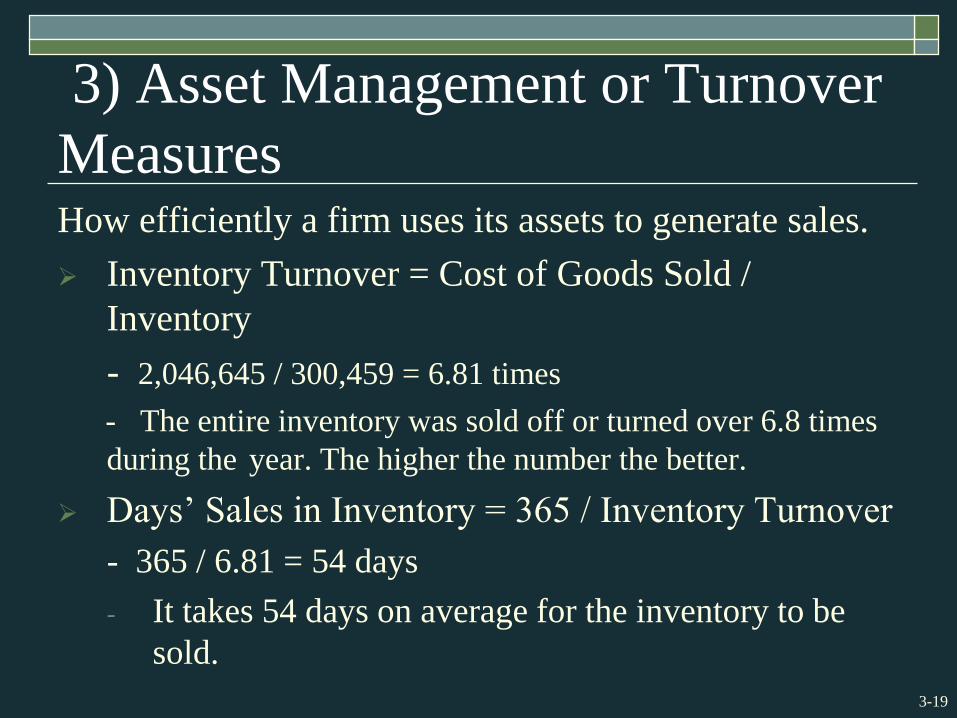

3) Asset Management or Turnover

MeasuresHow efficiently a firm uses its assets to generate sales.

Inventory Turnover = Cost of Goods Sold /

Inventory

- 2,046,645 / 300,459 = 6.81 times

- The entire inventory was sold off or turned over 6.8 times

during the year. The higher the number the better.

Days’ Sales in Inventory = 365 / Inventory Turnover

- 365 / 6.81 = 54 days

- It takes 54 days on average for the inventory to be

sold.

3-20

3) Asset Management or Turnover

MeasuresHow fast the firm collects on its sales?

Receivables Turnover = Sales / Accounts Receivable

- 5,250,538 / 1,051,438 = 4.99 times

- Collected the outstanding accounts and lent the money

again 4.99 times during the year.

- Easier to interpret in days.

Days’ Sales in Receivables = 365 days / Receivables

Turnover

- 365 / 4.99 = 73 days

- This ratio is also called average collection period.

- This firm collects its credit sales in 73 days on average.

3-21

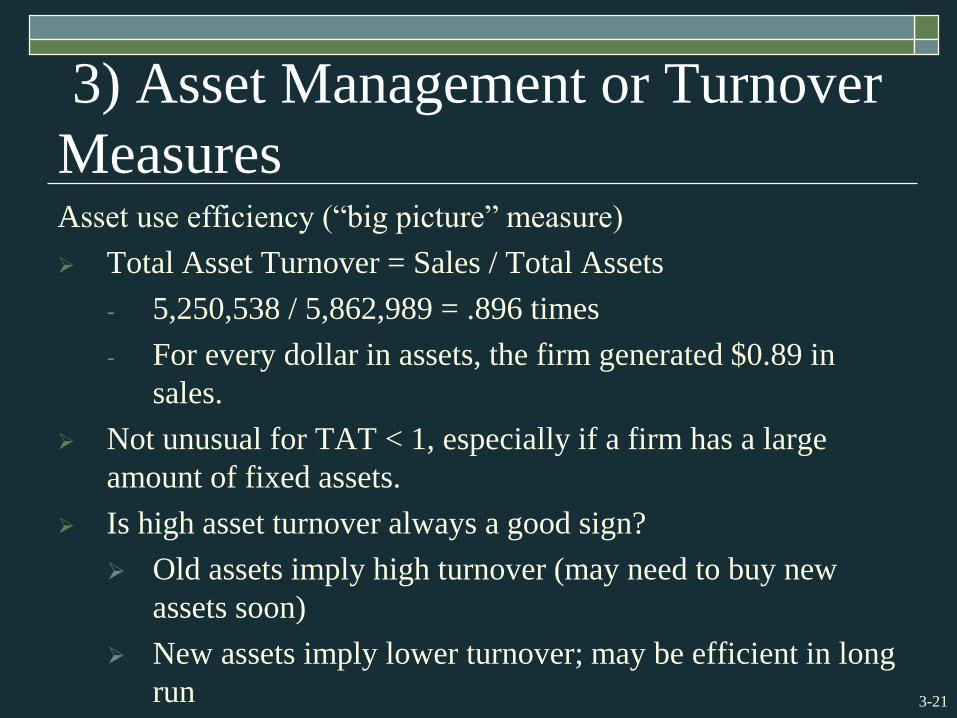

3) Asset Management or Turnover

MeasuresAsset use efficiency (“big picture” measure)

Total Asset Turnover = Sales / Total Assets

- 5,250,538 / 5,862,989 = .896 times

- For every dollar in assets, the firm generated $0.89 in

sales.

Not unusual for TAT < 1, especially if a firm has a large

amount of fixed assets.

Is high asset turnover always a good sign?

Old assets imply high turnover (may need to buy new

assets soon)

New assets imply lower turnover; may be efficient in long

run

3-22

4) Profitability Measures Profit Margin = Net Income / Sales

– 756,410 / 5,250,538 = .1441 times or 14.41%

– Greene co. generates about 14 cents in profit for each

dollar in sales.

Return on Assets (ROA) = Net Income / Total Assets

– 756,410 / 5,862,989 = .1290 times or 12.90%

– A measure of profit per dollar of assets

Return on Equity (ROE) = Net Income / Total Equity

– A measure of how the stockholders fared during the year.

– 756,410 / 2,984,513 = .2534 times or 25.34%

– For every dollar in equity, the firm generated 25 cents in

profit

3-23

5) Market Value Measures

Market Price (12/31/09) = $91.54 per share

Shares outstanding = 193,000

EPS = Net income/Shares Outstanding = 756,410/193,000 =

$3.92

Price-Earnings (PE) Ratio = Price per share / Earnings per

share

- 91.54 / 3.92 = 23.35 times

- High PE indicates that firm has prospects for future

growth.

Price-Sales Ratio = Price per share/sales per share

- This ratio is used if a firm has negative earnings for

extended period of time.

3-24

5) Market Value Measures

Market-to-book ratio = market value per share /

book value per share

Book Value per share = Common equity/Shares

outstanding

Book Value per share = (2,984,513 / 193,000) =

$15.46

Market-to-Book ratio = 91.54 / 15.46 = 5.92 times

- A value less than one indicates that the firm has not

been very successful in creating value.

Market Capitalization=PxShares

outstanding=91.54x193,000=17,667,220

3-25

3.3Tying Ratios Together: The Du

Pont Identity Shows relationship between ROE and ROA

Gives us a way to decompose ROE

ROE = Net Income (NI) / Total Equity (TE)

Multiply by Total Assets (TA)/Total Assets (TA) and then

rearrange

ROE = (NI / TE) x (TA / TA)

ROE = (NI / TA) x (TA / TE) = ROA * Equity Multiplier

Multiply by sales/sales and then rearrange

ROE = (NI / TA) (TA / TE) (Sales / Sales)

ROE = (NI / Sales) (Sales / TA) (TA / TE)

ROE = Profit Margin * Total Asset Turnover * Equity

Multiplier

3-26

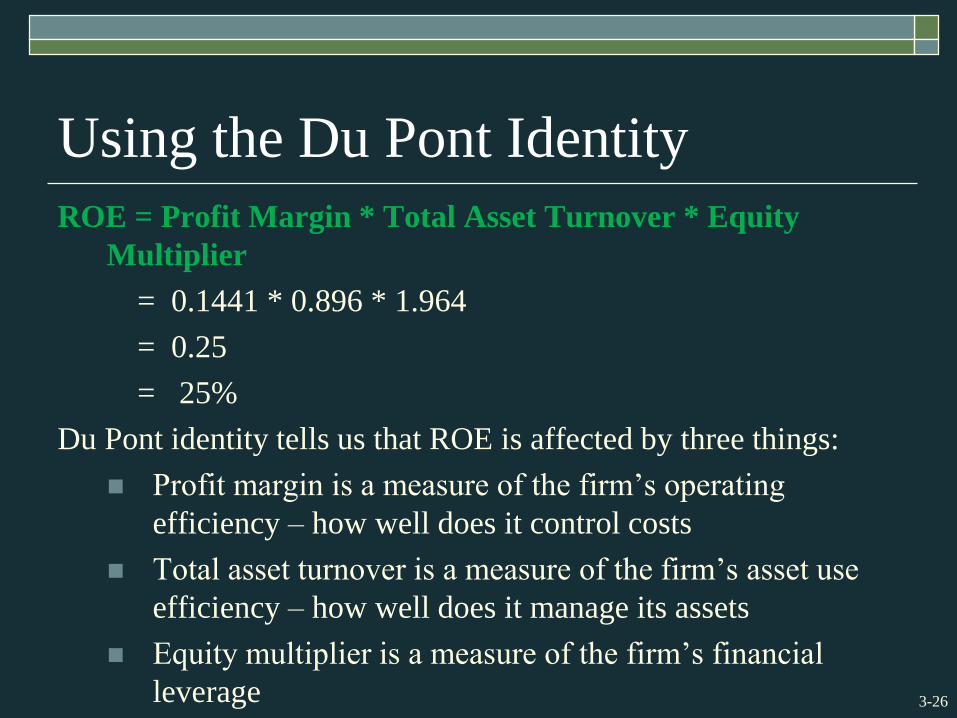

Using the Du Pont Identity

ROE = Profit Margin * Total Asset Turnover * Equity

Multiplier

= 0.1441 * 0.896 * 1.964

= 0.25

= 25%

Du Pont identity tells us that ROE is affected by three things:

Profit margin is a measure of the firm’s operating

efficiency – how well does it control costs

Total asset turnover is a measure of the firm’s asset use

efficiency – how well does it manage its assets

Equity multiplier is a measure of the firm’s financial

leverage

3-27

Using Financial Statements

Ratios are not very helpful by themselves: they

need to be compared to something

Time-Trend Analysis

Used to see how the firm’s performance is

changing through time

Peer Group Analysis

Compare to similar companies or within industries

SIC and NAICS codes

3-28

Limitations of Ratio Analysis Ratio analysis is more useful for small, narrowly focused

firms as compared to large multidivisional firms (e.g. GE).

Different accounting practices can distort comparisons. For

instance, outside the US, financial statements may not

conform to GAAP.

A firm may have some ratios that make it look “good” and

others “bad”. So it might be difficult to tell if a company is

doing well or not.

Different firms might use different accounting procedures.

Different firms might end their fiscal years at different times.

One time (extraordinary) events.

3-29

3.4 Financial Models

Investment in new assets – determined by

capital budgeting decisions

Degree of financial leverage – determined by

capital structure decisions

Cash paid to shareholders – determined by

dividend policy decisions

Liquidity requirements – determined by net

working capital decisions

3-30

Financial Planning Ingredients Sales Forecast – many cash flows depend directly on the level

of sales

Pro Forma Statements – setting up the plan as projected (pro forma) financial statements allows for consistency and ease of interpretation

Asset Requirements – the additional assets that will be required to meet sales projections

Financial Requirements

Plug Variable – determined by management decisions about what type of financing will be used (makes the balance sheet balance)

Economic Assumptions – explicit assumptions about the coming economic environment

3-31

Percent of Sales Approach Some items vary directly with sales, others do not.

Separate balance sheet and income statement accounts into two groups depending on whether they do vary with sales.

Can then calculate financing needed to support predicted sales.

Percentage of sales approach is a quick way to generate pro forma statements.

Income Statement

Costs may vary directly with sales

Depreciation and interest expense may not vary directly with sales

Dividends are a management decision and generally do not vary directly with sales (but dividend payout ratio = Cash dividends / Net income may reflect company policy, so reasonable to assume that is fixed)

3-32

Percent of Sales Approach

Balance Sheet

Initially assume all assets, including fixed, vary directly with sales.

Accounts payable also normally vary directly with sales.

Notes payable, long-term debt, and equity generally do not vary with sales because they depend on management decisions about capital structure. The changes in these sources of funds are what we are trying to determine.

The change in the retained earnings portion of equity will come from the dividend decision.

External Financing Needed (EFN)

The difference between the forecasted increase in assets and the forecasted increase in liabilities and equity.

3-33

Percent of Sales and EFN Instead of creating pro forma statements, External Financing

Needed (EFN) can also be calculated by the formula on the next page.

Use Rosengarten e.g. from book

Sales: this year $1000, next year $1250

Costs: this year $800 (80% of sales), next year $1000 (80% of sales)

Accounts Payable: only liability that changes with Sales: this year $300 (30%) , next year 375 (30%)

Assets: this year $3000 (300%), needed next year $3750 (300%); therefore, new funding needed = $750

Profit Margin (PM)=13.2%; dividend payout ratio=33.3%

3-34

Percent of Sales and EFN

565$

)667.0125013.0()2503.0()2503(

)1(Sales) Projected(ΔSalesSales

LiabSpon Sales

Sales

Assets

dPM

3-35

3.5 External Financing and Growth

At low growth levels, internal financing (retained

earnings) may exceed the required investment in

assets.

As the growth rate increases, the internal financing

will not be enough, and the firm will have to go to the

capital markets for financing, that is, the higher the

rate of growth in sales or assets, the greater the need

for external financing.

Examining the relationship between growth and

external financing required is a useful tool in

financial planning.

3-36

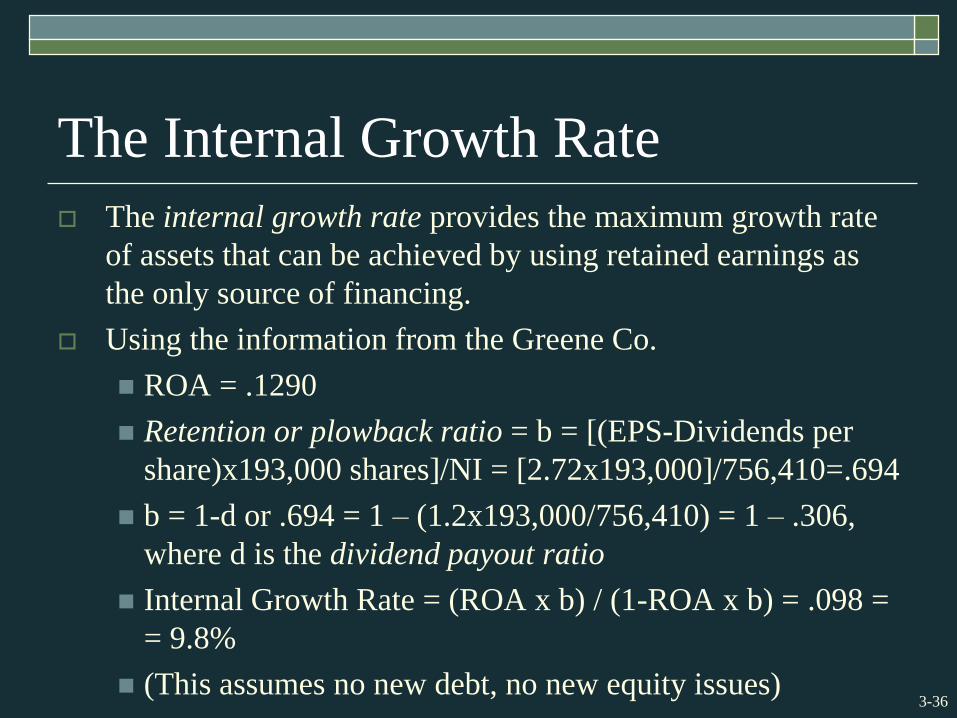

The Internal Growth Rate

The internal growth rate provides the maximum growth rate

of assets that can be achieved by using retained earnings as

the only source of financing.

Using the information from the Greene Co.

ROA = .1290

Retention or plowback ratio = b = [(EPS-Dividends per

share)x193,000 shares]/NI = [2.72x193,000]/756,410=.694

b = 1-d or .694 = 1 – (1.2x193,000/756,410) = 1 – .306,

where d is the dividend payout ratio

Internal Growth Rate = (ROA x b) / (1-ROA x b) = .098 =

= 9.8%

(This assumes no new debt, no new equity issues)

3-37

The Sustainable Growth Rate

The sustainable growth rate provides the maximum growth

that can be achieved without additional external equity

financing while maintaining a constant debt-to-equity ratio,

that is, the maximum growth rate without increasing financial

leverage.

Using the information from the Greene Co.

ROE = .2534

b = .694

Sustainable Growth Rate = (ROE x b) / (1-ROE x b) = .213

= 21.3%

3-38

Determinants of Growth

Profit margin – operating efficiency

Total asset turnover – asset use efficiency

Financial leverage – choice of optimal debt

ratio

Dividend policy – choice of how much to pay

to shareholders versus reinvesting in the firm

3-39

3.6 Some Caveats

Financial planning models do not indicate

which financial polices are the best.

Models are simplifications of reality, and the

world can change in unexpected ways.

Without some sort of plan, the firm may find

itself adrift in a sea of change without a rudder

for guidance.

3-40

Quick Quiz

How do you standardize balance sheets and income statements?

Why is standardization useful?

What are the major categories of financial ratios?

How do you compute the ratios within each category?

What are some of the problems associated with financial statement analysis?

3-41

Quick Quiz

What is the purpose of financial planning?

What are the major decision areas involved in developing a plan?

What is the percentage of sales approach?

What is the internal growth rate?

What is the sustainable growth rate?

What are the major determinants of growth?