mexico: fiscal sustainability

TRANSCRIPT

Report No. 20236-ME

Mexico:Fiscal Sustainability(In Two Volumes) Volume II: Background Papers

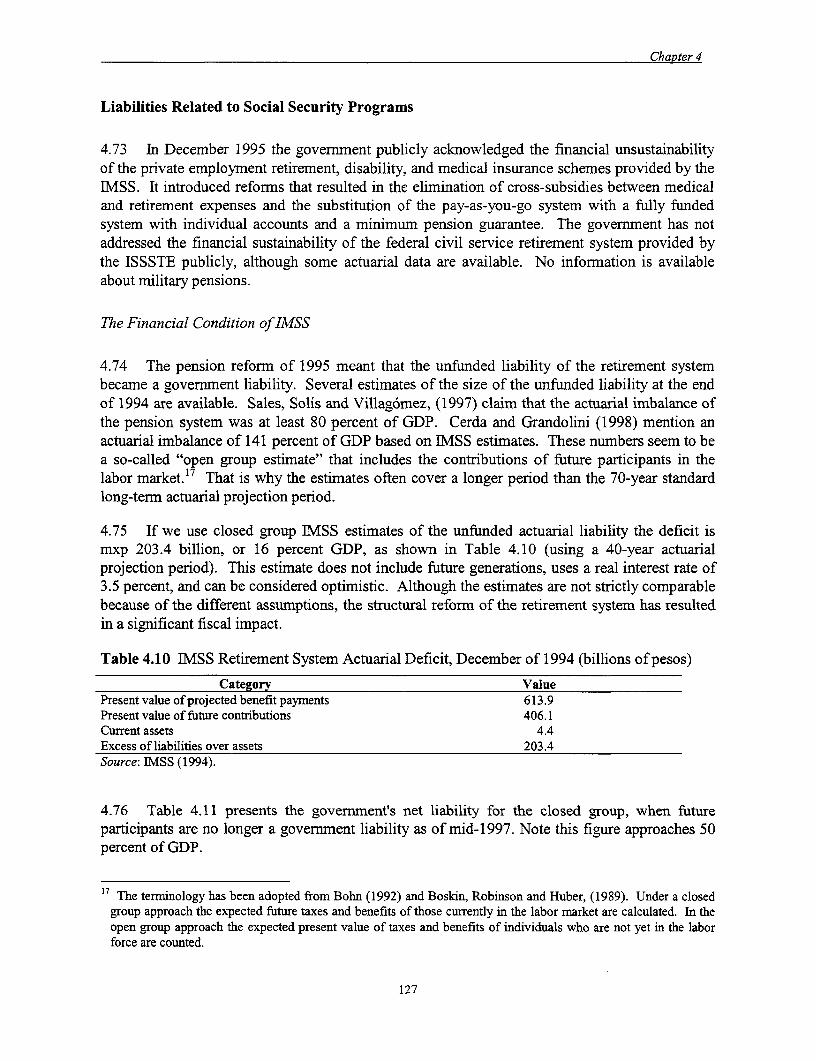

June 13, 2001

Mexico Country Management UnitPREM Sector Management UnitLatin America and the Caribbean Region

u

Document of the World Bank

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTSCurrency Unit - Mexican Peso (mxp$)

EXCHANGE RATE MARCH 17, 20009.35 MXP / 1 USD

WEIGHTS AND MEASURESMetric System

FISCAL YEARJuly I - June 30

ABBREVIATIONS AND ACRONYMSADE Acuerdo de Apoyo Inmediato a Deudores de la BancaADEFAS Adeudos de Ejercicios Fiscales AnterioresASA Aeropuertos y Servicios AuxiliaresBANCOMEXT Banco Nacional de Comercio Exterior, S.N.C.BANJERCITO Banco Nacional del Ejercito, Fuerza Aerea y Armada, S.N.C.BANOBRAS Banco Naciona] de Obras y Servicios Publicos, S.N.C.BANRURAL Banca Nacional de Credito Rural, S.N.C.BoM Banco de MexicoCAPUFE Caminos y Puentes Federales de Ingresos y Servicios ConexosCFE Comisi6n Federal de ElectricidadCNBV Comisi6n Nacional Bancaria y de ValoresCONASUPO Compafdia Nacional de Subsistencias PopularesEMBI Emerging Market Bond IndexFAMEVAL Fondo de Apoyo al Mercado de ValoresFARAC Fideicomiso de Apoyo a] Rescate de Autopistas

FIDEC Fondo para el Desarrollo ComercialFIDELIQ Fideicomiso Liquidario de Instituciones y Organizaciones Auxiliares del CreditoFINA Financiera Nacional AzucareraFINAPE Programa para el Financiamiento del sector Agropecuario y PesqueroFIRA Fideicomisos Instituidos en Relaci6n con la AgriculturaFNM Ferrocarriles Nacionales de MexicoFOBAPROA Fondo Bancario de Protecci6n al AhorroFOPYME Programa de Apoyo Financiero y Fomento a la Micro, Pequeina y Mediana EmpresaFOVI Fondo de Operaci6n y Financiamiento Bancario a la ViviendaGDP Gross Domestic ProductIMF International Monetary FundIMSS Instituo Mexicano del Seguro SocialINEGI Instituto Nacional de Estadistica, Geografia e InformaticaIPAB Instituto de Protecci6n al Ahorro BancarioISSSTE Instituto de Seguridad y Servicios Sociales de los Trabajadores del EstadoLFC Luz y Fuerza del CentroLOTENAL Loteria Nacional para la Asistencia PublicaMXP Mexican PesosNAFINSA Nacional Financiera, S.N.C.NIPA National Income Products AccountOECD Organization for Economic Co-operation and DevelopmentPEMEX Petr6leos MexicanosPIPSA Productora e Importadora de PapelSCNM Sistema de Cuentas Nacionales de MexicoSCT Secretaria de Comunicaciones y TransporteSHCP Secretaria de Hacienda y Credito PublicoVAT Value Added Tax

The Bank team that produced this report was headed by Stephen Everhart (LCSPE)-task manager, under the guidance ofMarcelo Giugale (LCCIC)-program team leader. Members of the Bank team include: Craig Bumside (DECRG), JoostDraaisma (LCCIC), Robert Duval (LCCIC), Andrew Feltenstein (IMF, Virginia Tech), Russ Murphy (Virginia Tech),Claudia Sepulveda (LCSPR), and Aaron Schwartzman (Emst & Young-Mexico). Production assistance was provided byMichael Geller and Elizabeth Toxtle (LCC IC).

The Bank appreciates the invaluable support and advice of Eliana Cardoso (LCSPE) and Vicente Fretes-Cibils(LCC4C). This study was undertaken under the general direction of Mr. Olivier Lafourcade (Director, LCCIC). Peerreviewers are: Messrs. Luis Serven (Lead Specialist - Regional Studies, LCSPR) and Anwar M. Shah (PrincipalEvaluation Officer, OEDCR).

VOLUME I: EXECUTIVE SUMMARYTABLE OF CONTENTS

Fiscal Sustainability-Mexico: A Synthesis

Rationale for the Study ..................................................... 1lIssues and Focus ...................................................... 2Fiscal Policy, Business Cycles, and Growth in Mexico ...................................................... 2Infrastructure, Extemal Shocks, and Mexico's Fiscal Accounts .......................... 3...........................3Infrastructure, Private Costs, and Payoffs from Additions to Infrastructure ................................................... 5Fiscal Impact of Contingent Liabilities ...................................................... 6Fiscal Deficit, Public Debt, and Fiscal Sustainability in Mexico ..................................................... 10An Extension: Balance Sheet Approach and Quality of Fiscal Adjustments ....................... I ........................ 16

The Mexican Case ..................................................... 19Implications of the Balance Sheet Approach ..................................................... 23

Conclusions: The Link Between Fiscal Sustainability and Fiscal Reform ................................................... 25References ..................................................... 27

List of Tables

Table E. 1 Estimate of the Overall Cost of the Financial Rescue, June 1999Table E.2 Contingent Liabilities Recognized by the Federal GovernmentTable E.3 Mexico Federal Debt as a Percentage of GDP

List of Figures

Figure E. 1 Concentration and Growth of Subnational Debt, 1994-1998: Selected StatesFigure E.2 Gross Federal Debt as Percent of GDP: Intemational BenchmnarksFigure E.3 Selected Latin American Eurobond SpreadsFigure E.4 Mexico Budget Indicators: 1980 - 1998Figure E.5 Tax Revenue as Percent of GDP, Selected Countries 1992 - 1998Figure E.6 Primary Deficit vs. Public Investment (percent of GDP)Figure E.7 Primary Deficit vs. Public Investment (percent of GDP) 5 UMI CountriesFigure E.8 Primary Deficit vs. Public Investment (percent of GDP) 6 LMI CountriesFigure E.9 Primary Deficit vs. Privatization Revenues (percent of GDP)Figure E. 10 Primary Deficit vs. Public Investment (percent of GDP) MexicoFigure E. 11 Primary Deficit vs. General Government Consumption (percent of GDP) MexicoFigure E. 12 Public Investment vs. Oil Prices MexicoFigure E. 13 Prograrnmable Expenditure Decomposition (percent of GDP) Mexico.Figure E. 14 Primary Deficit vs. Privatization Revenues (percent of GDP) MexicoFigure E. 15 Deficit Reduction and Oil DependenceFigure E.16 Components of Tax Revenues as a Percent of GDP, Mexico 1980-1998

iii

VOLUME II: BACKGROUND PAPERSTABLE OF CONTENTS

Chapter 1. Fiscal Policy, Business Cycles, and Growth in Mexico

Perspectives on Mexico's Fiscal Accounts from 1980-98 .............................................. 2The Business Cycle in Mexico ............................................. 3Trends and Cycles in Mexico's Fiscal Accounts ............................................. 6The Cyclically Adjusted Budget Surplus in Mexico ............................................. 16Methods for Computing the Cyclically Adjusted Budget Surplus ................. ............................. 17Budget Surplus Estimates for Mexico .............................................. 19How Fiscal Policy and Output Affect Each Other in Mexico .............................................. 23A Small VAR Model of the Mexican Economy ............................................. 24How Does the Fiscal Surplus Affect Output? ............................................. 25Dynamnic Behavior of the Fiscal Surplus ............................................. 27Policy Conclusions ............................................. 29References ............................................. 31Appendix ......................................... 33

Chapter 2. Infrastructure, External Shocks, and Mexico's Fiscal Accounts

Background ...................................... 43Model Structure ...................................... 45Production ...................................... 46Ba.ank.ing ...................................... 48Consumption ...................................... 48The Government ...................................... 49The Foreign Sector and Exchange Rate Determination ...................................... 49Money Supply ...................................... 50Data Sources, Calibration, and Simulation ...................................... 50Simulations ...................................... 55The Benchrnark Case ...................................... 55A Shock to Confidence in the Banking System ...................................... 55Trade Shock ...................................... 57Conclusion ...................................... 60References ...................................... 61Appendix ...................................... 62

Chapter 3. Infrastructure, Private Costs, and Payoffs from Additions to Infrastructure

Background ...................................... 68The Model ...................................... 72The Data ...................................... 74Sanple Horizon ...................................... 75Limitations ...................................... 75Estimation of the Model ...................................... 76Methods ....................................... 76Infreastructure ...................................... 76Estimation Limitations ...................................... 77Results .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78Overview ...................................... 79

iv

Payoffs from Additions to Infrastructure ........................................................................ 84Static Costs and Benefits of Increased Infrastructure ........................................................................ 85Optimal Infrastructure Stocks ........................................................................ 86Conclusions ....... ................................................................. 87References ....... ................................................................. 88Appendices ....... ................................................................. 90

Chapter 4. Fiscal Impact of Contingent Liabilities: The Case of Mexico

Coverage of the Study ........................................................................ 107Government Accounting Issues ........................................................................ 110Methodology ........................................................................ 111Deposit Insurance Scheme for Private Banks ......................... ............................................... 112The 1995 Banking Crisis ........................................................................ 113Expected Fiscal Costs of Resolution of the Crisis ........................................................................ 114Government Credit Assistance Programs ........................................................................ 120Characteristics of Direct Loans and Loan Guarantees ........................................................................ 121Expected Fiscal Cost of Government Credit Programs and the Budget ......................... ............................ 126Liabilities Related to Social Security Programs .............................. .......................................... 127The Financial Condition of IMSS ........................................................................ 127The Financial Condition of ISSSTE ........................................................................ 128Expected Fiscal Costs of Social Security Programs and the Budget ................................. ......................... 129Private Provision of Infrastructure and Government Guarantees ........................................... .................... 129Power Plants ....... ................................................................. 129Highways ........................................................................ 130The Fiscal Cost of Government Insurance Programs ................................................................. ....... 130Policy Implications ........................................................................ 132References ........................................................................ 134

Chapter 5. Fiscal Deficit, Public Debt and Fiscal Sustainability in Mexico

The Mexican Fiscal Accounts: Stylized Facts ........................... ............................................. 138Debt Management ........................................................................ 140Budget Indicators ........................................................................ 142Tax System ....... ................................................................. 143Government Expenditure Comnposition ........................................................................ 146Is Mexican Fiscal Policy Sustainable? ........................................................................ 148Accounting Approach to Fiscal Solvency ........................................................................ 148Pricing Approach to Fiscal Solvency ........................................................................ 149Intertemporal Approach to Fiscal Solvency: The Medium and Long Term ................. ............................. 151The Short and Medium Term ........................................................................ 152The Long Term: A Time Series Analysis 1980:01-1999:05 ....................................................................... 154Testing the Interternporal Budget Constraint: Unit Roots ........................................................................ 155The Case of a Stochastic Discount Rate ........................................................................ 156Testing for a Change in Regime ........................................................................ 157Testing the Intertemporal Budget Constraint: A Co-integration Approach .................. ............................. 160Testing Long-Run Relationship Between Government Spending Inclusive of Interest Payments andRevenue ....... ................................................................. 161Testing Long-Run Relationship Between Govermnent Spending Exclusive of Interest Payments,Interest Payments and Revenue ........................................................................ 163Policy Conclusions ........................................................................ 165References ........................................................................ 167Appendix ........................................................................ 169

v

List of Tables

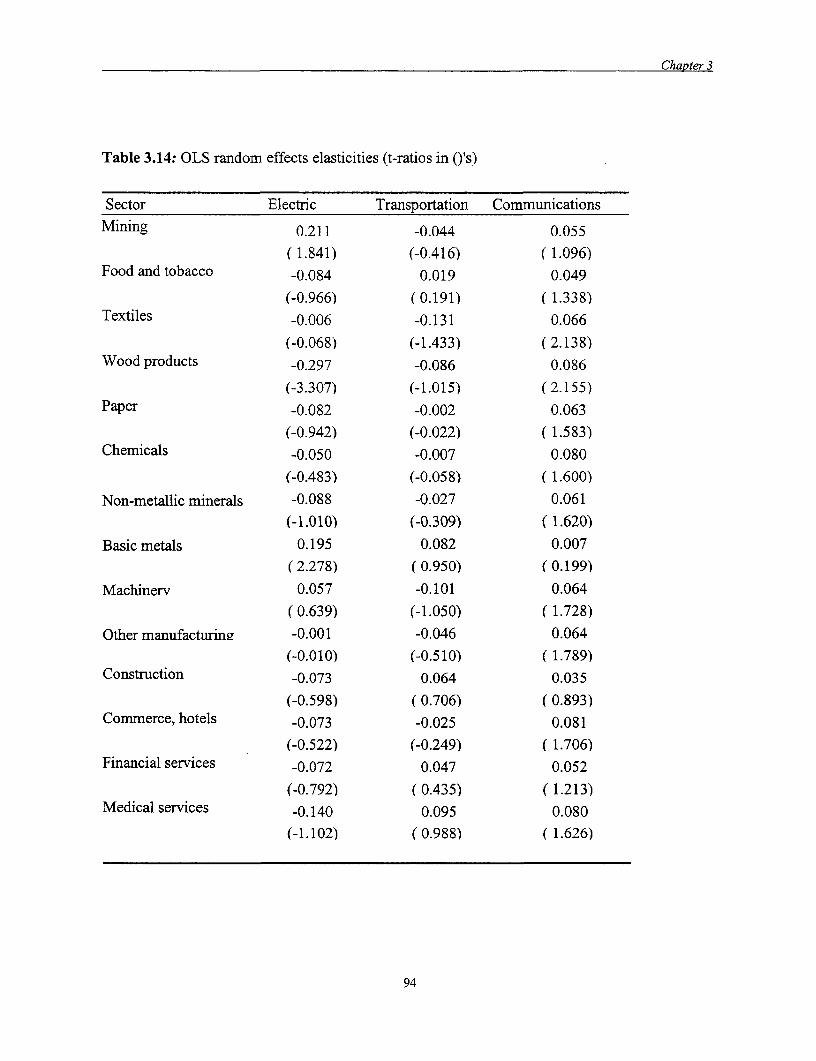

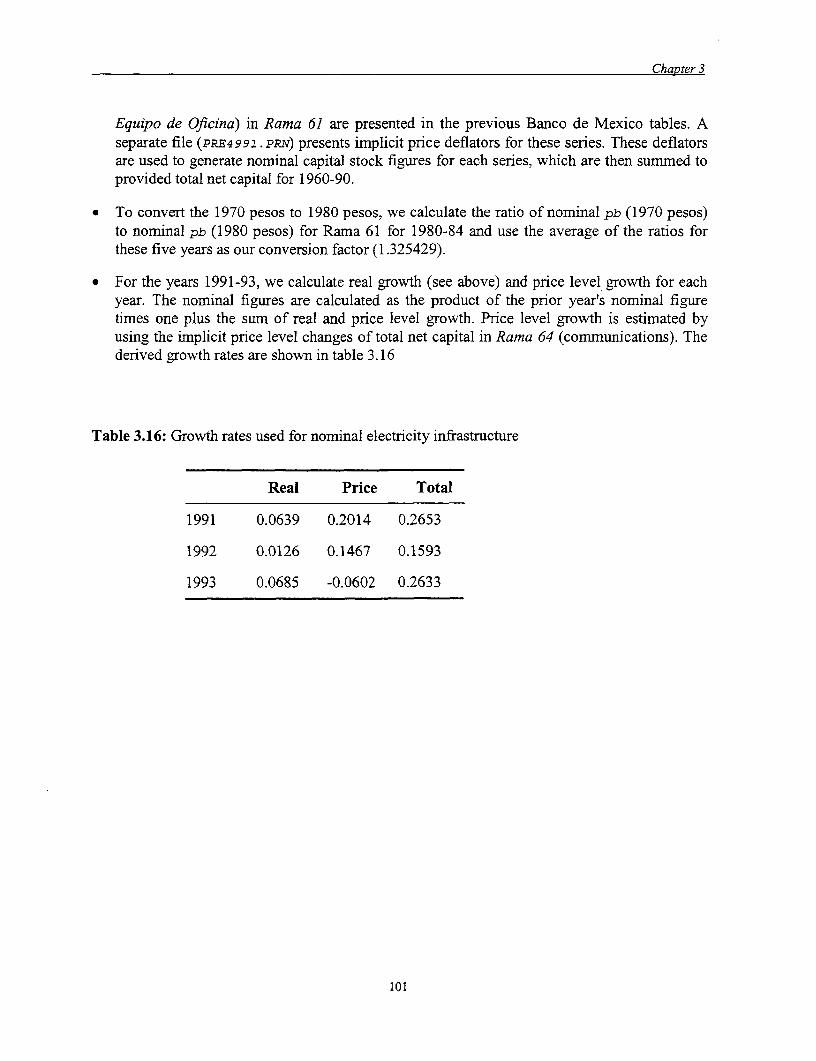

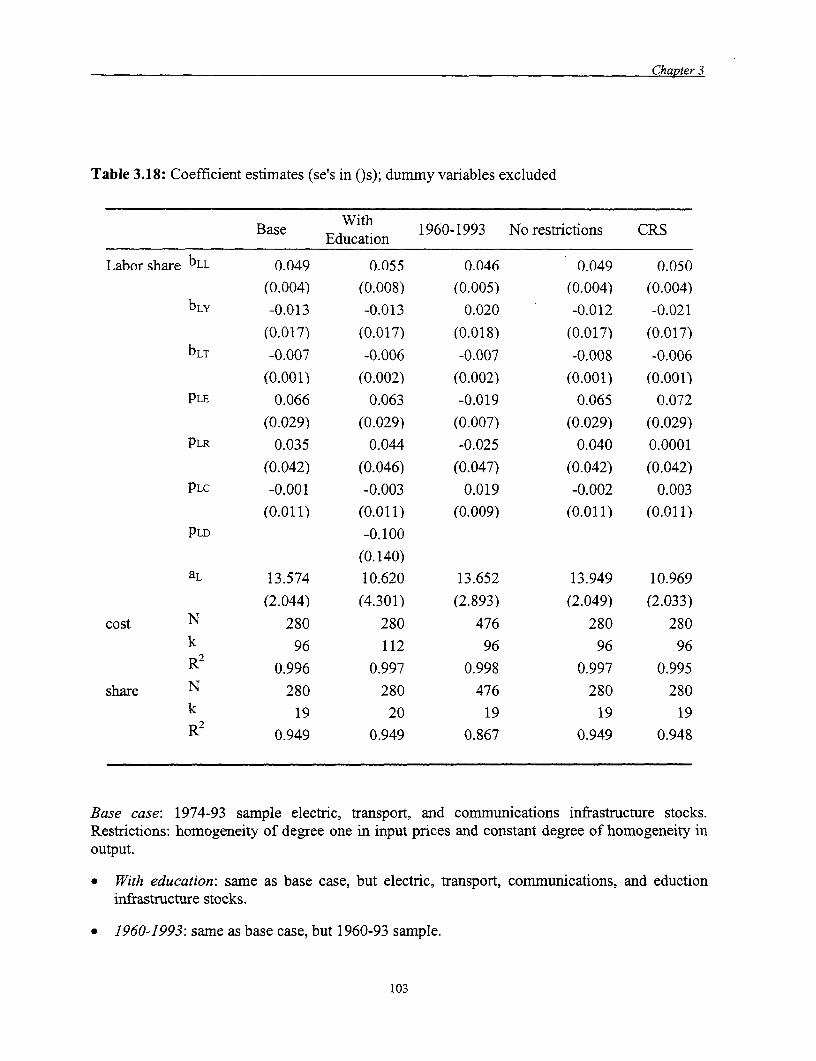

Table 1.1 Sunmmary Budget Figures, 1980-81 1997-98Table 1.2 Cyclical Properties of Public sector Revenue and ExpenditureTable 1.3 Main Components of Public Sector Revenue and Expenditure, 1980-81 and 1997-98Table 1.4 Estimnates of Revenue and Expenditure ElasticitiesTable 1.5 Impulse Response Functions from the VARTable 1.6 Variance Decomposition of OutputTable 1.7 Variance Decomposition of the Unadjusted Primary Fiscal SurplusTable l.Al Estimates of a Piecewise Linear Trend in the Logarithm of Seasonally Adjusted Real GDPTable 2.1 Real GDP, 1980-97Table 2.2 Stocks of Infrastructure, 1970-90Table 2.3 Cost Elasticities by Sector and Infrastructure TypeTable 2.4 A Benchmark Simulation, 1995-2000Table 2.5 Reduction in the Interest Elasticity of Money Demand, 1995-2000Table 2.6 Interest Elasticity Decline Combined with an Infrastructure Increase 1995-200Table 2.7 Trade Shock: Real World Income Stagnates, 1995-2000Table 2.8 Trade Shock Combined with an Infrastructure Increase, 1995-2000Table 2.9 Infrastructure Elasticities = 0Table 3.1 Compound Annual Growth Rates 1960-93Table 3.2 Infrastructure Compound Annual Growth Rates, 1960-93 and 1983-93Table 3.3 Physical Infrastructure, Average Annual Growth RatesTable 3.4 Correlations: Physical and Financial Infrastructure MeasuresTable 3.5 Primary Data: Means and Standard DeviationsTable 3.6 Estimated Private Sector Cost Elasticities with Respect to Public Infrastructure StocksTable 3.7 Estimated Private Sector Cost Elasticities with Respect to Public Infrastructure StocksTable 3.8 Estimated Private Sector Cost Elasticities with Respect to Public Infrastructure StocksTable 3.9 Estimated Private Sector Cost Elasticities with Respect to Public Infrastructure StocksTable 3.10 Mean ElasticitiesTable 3.11 Static Cost and Benefits of Increased InfrastructureTable 3.12 Optimal Infrastructure StocksTable 3.13 OLS Panel ElasticitiesTable 3.14 OLS Random Effects ElasticitiesTable 3.15 FGLS Elasticities - Hetero, ARITable 3.16 Growth Rates Used for Nominal Electricity InfrastructureTable 3.17 Coefficient EstimatesTable 3.18 Coefficient Estimates (se's in (s), Dunmy Variables ExcludedTable 4.1 Fiscal Risk MatrixTable 4.2 Federal Insurance Programs with Major Fiscal RisksTable 4.3 State Government DebtTable 4.4 State Government Pension Liabilities: 1997Table 4.5 Pro Forma Balance Sheet of FOBAPROA, February 1998Table 4.6 Estimation of the Cost of the Financial Rescue, June 1999Table 4.7 Executed Fiscal Cost on Programs of Financial and Debtors RescueTable 4.8 Estimates of Total Losses of Resolving Major Bank InsolvensesTable 4.9 Government Loans by Major Program Area, Fiscal 1997Table 4.10 IMSS Retirement System Actuarial Deficit, December of 1994Table 4.11 Government Net Liability as a Result of the 1995 Pension ReformTable 4.12 Pro Forma Balance Sheet of FARAC as of November 1998Table 4.13 Contingent Liabilities and Fiscal Deficit AdjustmentsTable 4.14 Contingent Liabilities Recognized by the Federal GovernmentTable 5.1 Accounting Approach Mexico in 1998Table 5.2 Short and Medium-Term Indicators of Fiscal Sustainability as a percentage of GDPTable 5.3 Testing for Nonstationarity in Undiscounted and Discounted Net Public Debt, 1980:01-

1999:05

vi

Table 5.4 The Zivot Andrews Unit Root Test for Undiscounted and Discounted Public DebtTable 5.5 Testing for Nonstationarity in Real Interest Rates, 1980:1-1998:07Table 5.6 Testing for Nonstationarity in Real Government Spending Inclusive Interest Payments

and Government Revenues, 1980:1-1999:05Table 5.7 Results of Co-integration Government Spending Inclusive Interest Payments and

Government Revenue, 1980:01-1999:05Table 5.8 Testing for Nonstationarity in Real Government Spending, Interest Payments and Government

Revenues, 1980:1-1999:05Table 5.9 Results of Co-integration Noninterest Government Spending, Interest Payments and Government

Revenue, 1980:01-1999:05

List of Figures

Figure 1.1 Real GDP in Mexico, 1980-98Figure 1.2 Seasonally Adjusted Real GDP, 1980-98Figure 1.3 (a) Trends and Cycles in Real GDP: HP TrendFigure 1.3 (b) Trends and Cycles in Real GDP: Deviations from TrendFigure 1.4 Trends in Public Sector Revenues, 1980-98Figure 1.5 Cyclical Components of Revenue, 1980-98Figure 1.6 Trends in Public Sector Expenditure, 1980-98Figure 1.7 Cyclical Components of Expenditure, 1980-98Figure 1.8 The Budget Surplus and the Fiscal Imnpulse, 1980-98Figure 1.9 Cyclical Fluctuation in Output Caused by Fiscal ShocksFigure l.Al Trends in Real GDPFigure l .A2 Cyclical comnponents of Real GDPFigure 3.1 Changes in Electric, Transport, and Communications InfrastructureFigure 3.2 Education Infrastructure IndexFigure 4.1 Contingent Liabilities related to Potential Crisis of the Banking SectorFigure 5.1 Mexico Public Net Debt and Primary Deficit (+) as a percentage of GDP, 1980 - 1998Figure 5.2 Mexico Overall and Primary Deficit (+) as a percentage of GDP, 1980-1998Figure 5.3 Mexico Domestic and Foreign Public Net Debt as a percentage of GDP, 1980-1998Figure 5.4 Public Sector Domestic Debt as a percentage of GDP, 1982-1998Figure 5.5 Mexico Public Foreign Debt: Term Structure, 1982-1998Figure 5.6 Mexico Budget Indicators, 1980-1998Figure 5.7 Total Tax Revenues as a percentage of GDP-Selected CountriesFigure 5.8 Oil Revenues as a percentage of Total RevenuesFigure 5.9 Seignorage as a Source of Government RevenueFigure 5.10 Federal Government Revenue Tax MixFigure 5.11 Total Expenditure of the Central Government as a percentage of GDP-Selected CountriesFigure 5.12 Total Governnent Expenditure (million p$1994)Figure 5.13 Expenditure CompositionFigure 5.14 Real Annualized Interest Rate CETES 28 daysFigure 5.15 Brady Bonds DiscountsFigure 5.16 EMBI Spread RateFigure 5.17 Credit Rating for Mexico (100 lowest chance of default)Figure 5.18 Mexican Net Public Debt, 1980:1 - 1999:5. Undiscounted at Market Value (in Bill. P$ 1994)Figure 5.19 Sequential Zivot-Andrews Unit Root Test for the Mexican Undiscounted and Discounted Public

Net Debt, 1980:1-1999:5Figure 5.20 Government Spending Inclusive Interest and Govermment Revenues, 1980:1-1999:5Figure 5.21 Governrment Spending, Interest Payments and Government Revenues: 1980:01-1999:05

vii

1FISCAL POLICY, BUSINESS CYCLES, AND GROWTH IN MEXICO

1.1 This chapter investigates one aspect of the sustainability of fiscal policy in Mexico. Itfocuses on the role fiscal policy plays in detennining output in the short and medium term. Italso looks at how fiscal policy, in turn, responds to the business cycle. Finally, it investigates thepersistence of fiscal policy and how the authorities can use this persistence to forecast thegovernment's financing needs.

1.2 The chapter looks at these particular issues for a number of reasons. A traditional rolefiscal policy plays in industrial economies is that of a cyclical stabilizer. Fiscal policy istypically designed to "lean against the wind." That is, it is usually designed to stimulate outputwhen the economy moves into recession and to be contractionary when an expansion broadens.This is usually accomplished in two ways. The first way is by having components in the budgetthat respond automatically to the business cycle, such as tax revenues (which respond positively)or unemployment benefits (an expenditure item that responds negatively). The second way is byusing discretionary components in the budget to provide a stimulus during bad times. A fiscalpolicy designed in this way leads to a strongly procyclical budget surplus.

1.3 Mexico's fiscal policy does not lean against the wind. The analysis in this chapter willshow that the budget surplus is quite strongly countercyclical, so that fiscal policy leans with thewind. The automatic stabilizers in place are weak, and are further weakened by the tendency ofanother automatic component of the budget, oil-based revenue, which responds sensitively toexogenous world oil prices, to move countercyclically. Furthermore, the discretionarycomponent of the budget surplus also tends to move countercyclically.

1.4 If fiscal policy simply did not matter, then whether or not it leaned with or against thewind would be of little consequence. However, in Mexico, as in many other countries, fiscalpolicy does matter. The analysis suggests that an increase in the discretionary surplus of 1percent of gross domestic product (GDP) causes GDP to decline by 0.6 percent in less than ayear. Because in Mexico such increases typically occur during contractions, and thesecontractions are relatively short-lived (typically less than two years), this implies thatdiscretionary policy exacerbates the cycle.

1.5 The results imply that Mexico's fiscal policy lacks a design that makes it a stabilizingfeature of the economy. Furthermore, it has not been designed to render itself more sustainable.With procyclical fiscal policy (a countercyclical fiscal surplus), deficits cause debt to accumulateduring economic expansions, but when the economic expansion inevitably ends, this debtsuddenly becomes extremely costly. To finance it, the government must either take drasticdiscretionary fiscal measures, or it must finance the debt by borrowing at high real interest rates,

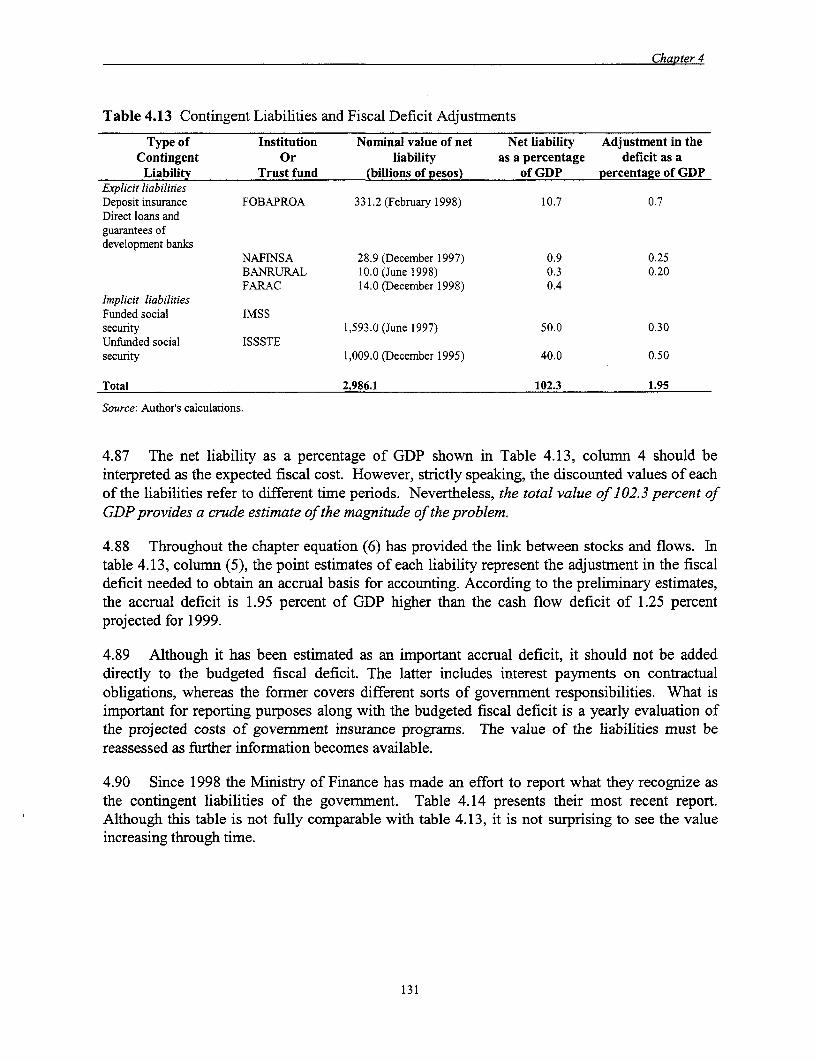

Chapter I

or by printing money and inducing rapid inflation. No matter which action the governmenttakes, the implications are similar: a worsening of the economic downturn. This chapter isintended to encourage policymakers to forrnulate fiscal policies that can smooth, rather thanexacerbate, real cycles, and that are therefore more readily sustained in the medium term.

1.6 The chapter begins by looking at the data. The sample period studied here-1980through mid-1998-spans several episodes in recent Mexican economic history. The choice ofperiod was largely driven by the availability of data. Quarterly national accounts data forMexico are available from 1980 onward, while monthly fiscal accounts are available from 1977onward. Trends and cycles in national accounts measures of real GDP are identified. Similarly,with GDP-based definitions of the business cycle in mind, this section describes the trends andcyclical fluctuations observed in various components of the public sector's fiscal accounts.

1.7 The second section of the chapter introduces the concept of the cyclically adjusted budgetsurplus. Historically, the main role of cyclically adjusted budget surplus measures has been astools in policy analysis in the knowledge that cyclical movements in output affect the publicsector's budget surplus. Cyclically adjusted budget surplus measures attempt to factor cyclicaleffects out of conventional measures. Once this is done, the adjusted measures are taken to beindicators of the stance of fiscal policy. This section examines a preferred definition of thecyclically adjusted budget surplus for Mexico. A question that naturally arises is whether this, orany other, adjusted budget measures are of particular use in policy analysis.

1.8 The third section of the chapter moves on to a more complex analysis of the data. Ratherthan working with simple indicators of the stance of fiscal policy, this section builds a simplestructural model of the Mexican economy that isolates several important features, namely:

* The nature of the feedback rule that implicitly determines fiscal policy, including theeffects of economic activity on the budget

- The exogenous shocks to the budget- The short- and medium-run effects of these shocks on economic activity* The extent to which forecasting the public sector's financing requirement is possible.

1.9 The main purpose of such a model is that the summary measures presented in the secondsection are typically useful in the context of a narrowly defined economic model. Furthermore,those summary measures are generally used to describe the effects of current policy on currentactivity. As such, given the lags with which fiscal policy is implemented and its effects are felt,the more forward-looking analysis of the third section should be of greater use to policymakers.

Perspectives on Mexico's Fiscal Accounts from 1980-98

1.10 This section examines quarterly data on Mexico's fiscal accounts from 1980 through mid-1998. While monthly budget data are available dating back to 1977, high-frequency data onGDP are only available from 1980 on. This section starts by defining the business cycle inMexico with reference to quarterly data on real GDP from the national accounts. It then dividesthe fiscal accounts into their revenue and expenditure components and looks at trends in revenueand expenditure.

2

Chapter I

The Business Cycle in Mexico

1.11 Figure 1.1 illustrates the behavior of real GDP in Mexico from 1980 through 1998. Theraw data show a clear pattern of seasonality. Overlying the general upward trend and cycles is apattern that indicates relatively low production in the first and third quarters and relatively highproduction in the second and fourth quarters. To identify these underlying features in the data, aseasonal adjustment filter was applied to the data.'

Figure 1.1 Real GDP in Mexico, 1980-98

1500 -

1400 -

1300-

1200-

1100

1000

900

800

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98

Source: National accounts.

1.12 Figure 1.2 shows the seasonally adjusted figures. This figure also delineates recessionsusing shading.2 Several episodes are worth noting namely:

* The recession of 1982 through mid-1983 associated with the debt crisis* The period of slow growth thereafter, followed by the recession of late 1985 and 1986* The implementation of the stabilization program in 1988, with an initial, slightly

recessionary, year* The long expansion of 1989-94* The short and intense recession of 1995 associated with the peso crisis and the

subsequent recovery.

1. The adjustment procedure mimics the X - 11 seasonal adjustment procedure used by the U.S. Bureau of theCensus.

2. The following definitions of expansions and recessions were used to generate the shading in figure 1.2. If theeconomy was not already deemed to be in a recession and seasonally adjusted real GDP fell for two successivequarters, these quarters were marked as the beginning of a recession. Until seasonally adjusted real GDP rose fortwo successive quarters, all subsequent quarters were also deemed to be part of the same recession. A similar,but opposite, definition was used to define an expansion, with the further assumnption that at the beginning of thesample (first quarter of 1980), the economy was in an expansion.

3

Chapter 1

Figure 1.2 Seasonally Adjusted Real GDP, 1980-98

1600

1500

~1300

1200-

1100

1000

900

80080 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98

Source: Author's calculations.

1.13 One way to describe the cyclical properties of fiscal policy would involve comparing thebehavior of revenue and expenditure during recessions to their behavior during expansions.However, with reference to figure 1.2, such an approach would clearly be unsatisfactory, becauseall expansions and all contractions are not alike. For example, the downturn after the peso crisisof December 1994 was much sharper and deeper than the ones experienced during the previousrecessions. It involved a cumulative decline in output of 9.7 percent, versus 6.8, 4.7, and 0.8percent in the previous recessions, and lasted two quarters, compared with six, five, and threequarters in the previous recessions. Similarly, the expansion since that recession has been morerapid than any of the previous expansions.

1.14 Furthermore, whether revenue and expenditure will differ according to whether output isrising or falling, rather than differing according to whether output is high or low is not obvious.The extent to which output, Y,, is high or low is typically measured with regard to some

benchmark, Y,<. That is, the business cycle is typically defined as Y,' = Y, / Y, . The literature

uses a number of benchmarks that can be the basis of a measure of the business cycle:

* The level of potential output* The trend in output as defined by a linear, possibly piecewise, trend in its logarithm* The trend in output as defined by the Hodrick and Prescott (HP) (1997) filter* The permanent component in output as defined by the Beveridge and Nelson (1981)

decomposition* The trend in output as defined by a peak-to-peak trend line.

4

Chapter 1

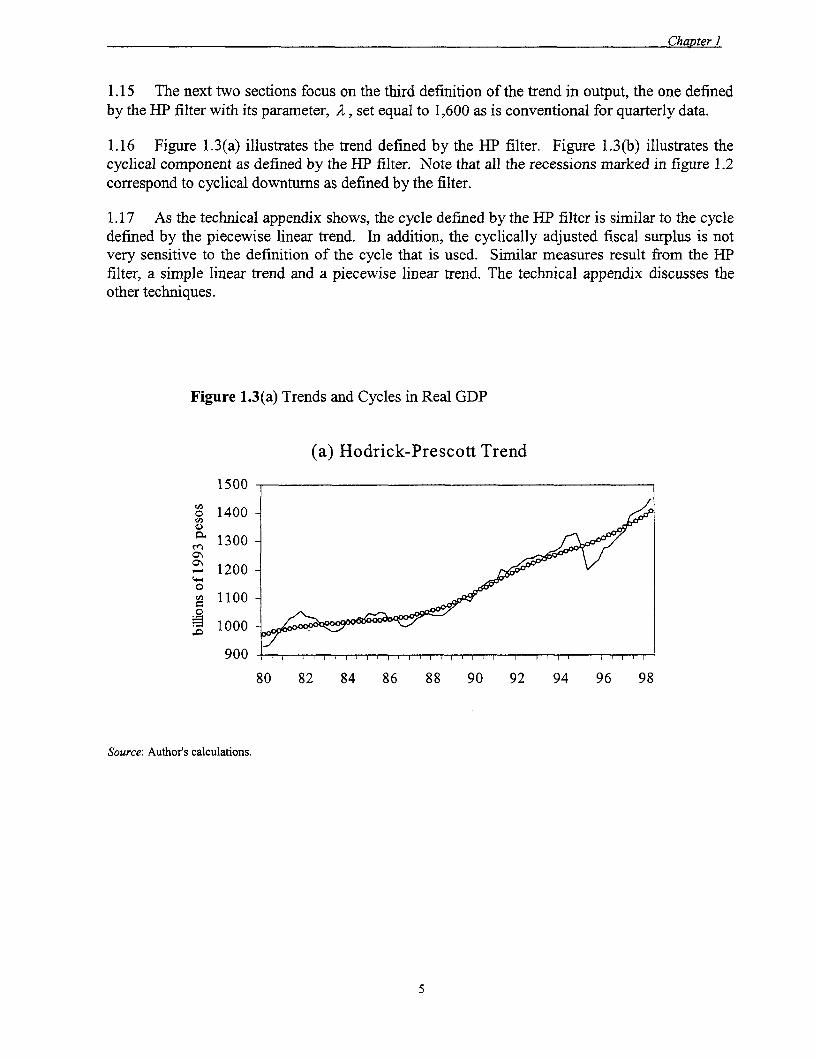

1.15 The next two sections focus on the third definition of the trend in output, the one definedby the HP filter with its parameter, A, set equal to 1,600 as is conventional for quarterly data.

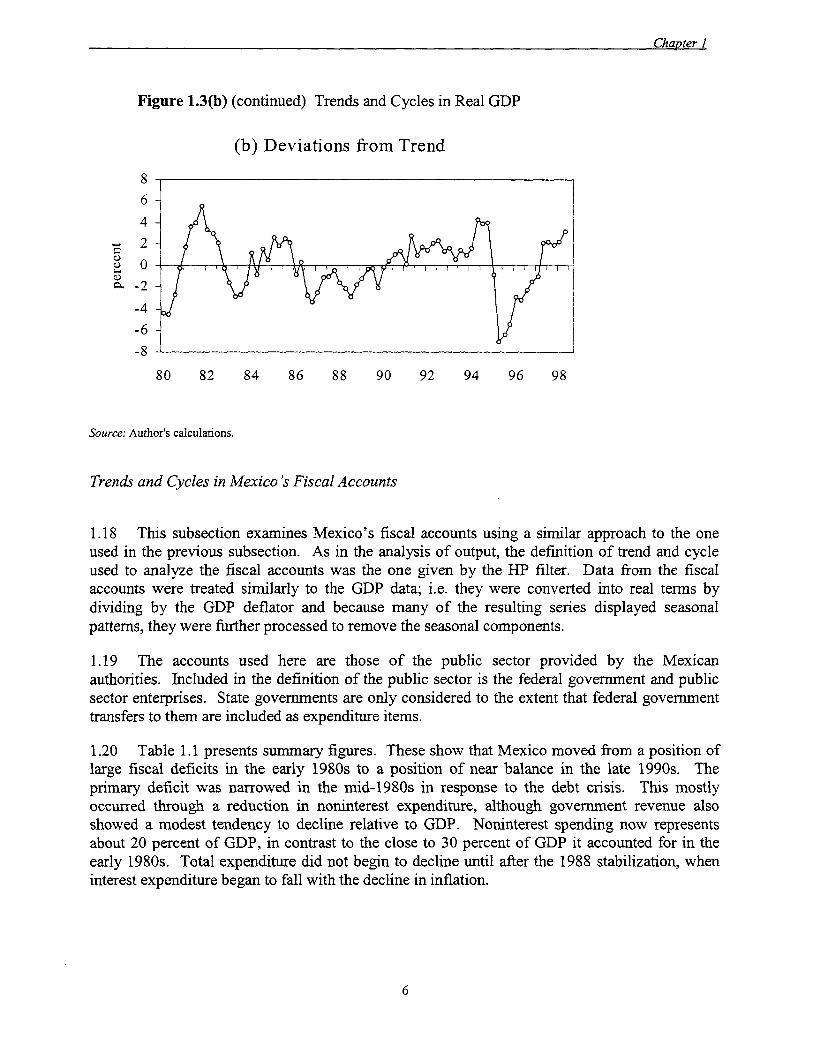

1.16 Figure 1.3(a) illustrates the trend defined by the HP filter. Figure 1.3(b) illustrates thecyclical component as defined by the HP filter. Note that all the recessions marked in figure 1.2correspond to cyclical downturns as defined by the filter.

1.17 As the technical appendix shows, the cycle defined by the HP filter is similar to the cycledefined by the piecewise linear trend. In addition, the cyclically adjusted fiscal surplus is notvery sensitive to the definition of the cycle that is used. Similar measures result from the HPfilter, a simple linear trend and a piecewise linear trend. The technical appendix discusses theother techniques.

Figure 1.3(a) Trends and Cycles in Real GDP

(a) Hodrick-Prescott Trend

1500 -

X 1400-

1300-

1200-

1100-

1000 I

900 -

80 82 84 86 88 90 92 94 96 98

Source: Author's calculations.

5

Chapter 1

Figure 1.3(b) (continued) Trends and Cycles in Real GDP

(b) Deviations from Trend

8- 6 -

0 -

-4-

-6-

80 82 84 86 88 90 92 94 96 98

Source: Author's calculations.

Trends and Cycles in Mexico 's Fiscal Accounts

1.18 This subsection examines Mexico's fiscal accounts using a similar approach to the oneused in the previous subsection. As in the analysis of output, the definition of trend and cycleused to analyze the fiscal accounts was the one given by the HP filter. Data from the fiscalaccounts were treated similarly to the GDP data; i.e. they were converted into real terms bydividing by the GDP deflator and because many of the resulting series displayed seasonalpatterns, they were further processed to remove the seasonal components.

1.19 The accounts used here are those of the public sector provided by the Mexicanauthorities. Included in the definition of the public sector is the federal government and publicsector enterprises. State governments are only considered to the extent that federal governmenttransfers to them are included as expenditure items.

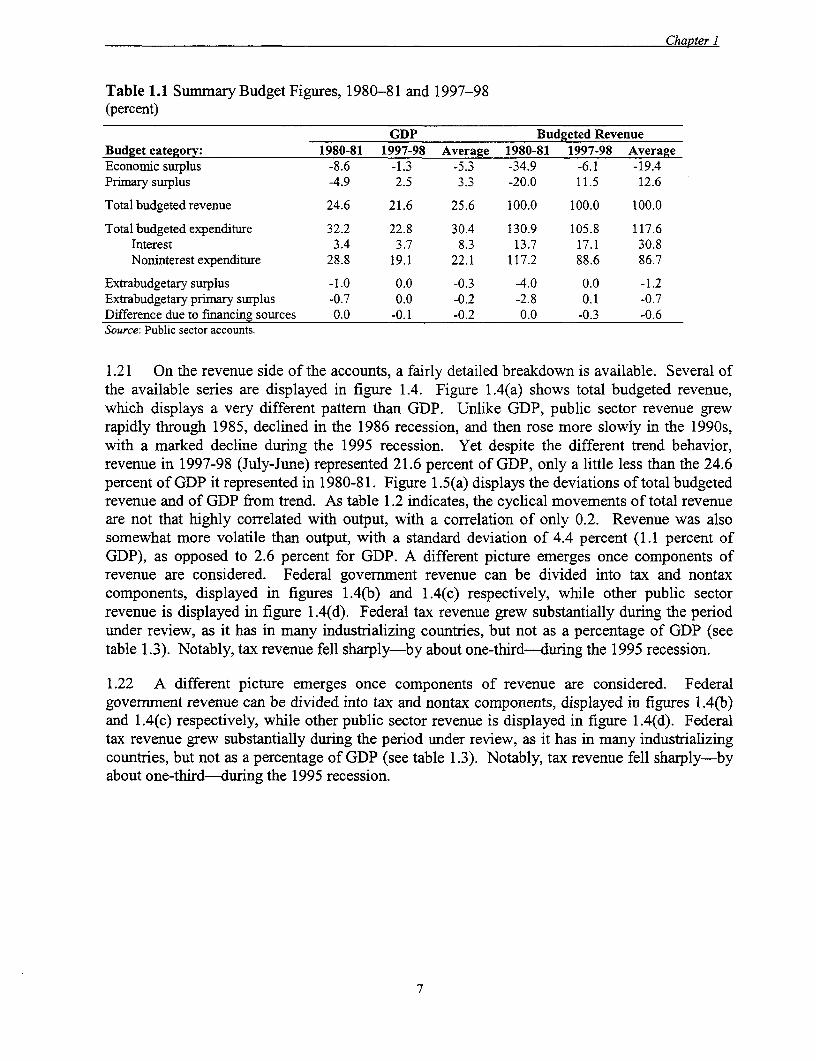

1.20 Table 1.1 presents summary figures. These show that Mexico moved from a position oflarge fiscal deficits in the early 1980s to a position of near balance in the late 1990s. Theprimary deficit was narrowed in the mid-1980s in response to the debt crisis. This mostlyoccurred through a reduction in noninterest expenditure, although government revenue alsoshowed a modest tendency to decline relative to GDP. Noninterest spending now representsabout 20 percent of GDP, in contrast to the close to 30 percent of GDP it accounted for in theearly 1980s. Total expenditure did not begin to decline until after the 1988 stabilization, wheninterest expenditure began to fall with the decline in inflation.

6

Chapter I

Table 1.1 Summary Budget Figures, 1980-81 and 1997-98(percent)

GDP Budgeted RevenueBudget category: 1980-81 1997-98 Average 1980-81 1997-98 AverageEconomic surplus -8.6 -1.3 -5.3 -34.9 -6.1 -19.4Primary surplus -4.9 2.5 3.3 -20.0 11.5 12.6

Totalbudgetedrevenue 24.6 21.6 25.6 100.0 100.0 100.0

Total budgeted expenditure 32.2 22.8 30.4 130.9 105.8 117.6Interest 3.4 3.7 8.3 13.7 17.1 30.8Noninterestexpenditure 28.8 19.1 22.1 117.2 88.6 86.7

Extrabudgetary surplus -1.0 0.0 -0.3 -4.0 0.0 -1.2Extrabudgetary primary surplus -0.7 0.0 -0.2 -2.8 0.1 -0.7Difference due to financing sources 0.0 -0.1 -0.2 0.0 -0.3 -0.6Source: Public sector accounts.

1.21 On the revenue side of the accounts, a fairly detailed breakdown is available. Several ofthe available series are displayed in figure 1.4. Figure 1.4(a) shows total budgeted revenue,which displays a very different pattern than GDP. Unlike GDP, public sector revenue grewrapidly through 1985, declined in the 1986 recession, and then rose more slowly in the 1990s,with a marked decline during the 1995 recession. Yet despite the different trend behavior,revenue in 1997-98 (July-June) represented 21.6 percent of GDP, only a little less than the 24.6percent of GDP it represented in 1980-81. Figure 1.5(a) displays the deviations of total budgetedrevenue and of GDP from trend. As table 1.2 indicates, the cyclical movements of total revenueare not that highly correlated with output, with a correlation of only 0.2. Revenue was alsosomewhat more volatile than output, with a standard deviation of 4.4 percent (1.1 percent ofGDP), as opposed to 2.6 percent for GDP. A different picture emerges once components ofrevenue are considered. Federal government revenue can be divided into tax and nontaxcomponents, displayed in figures 1.4(b) and 1.4(c) respectively, while other public sectorrevenue is displayed in figure 1.4(d). Federal tax revenue grew substantially during the periodunder review, as it has in many industrializing countries, but not as a percentage of GDP (seetable 1.3). Notably, tax revenue fell sharply-by about one-third--during the 1995 recession.

1.22 A different picture emerges once components of revenue are considered. Federalgovernment revenue can be divided into tax and nontax components, displayed in figures 1.4(b)and 1.4(c) respectively, while other public sector revenue is displayed in figure 1.4(d). Federaltax revenue grew substantially during the period under review, as it has in many industrializingcountries, but not as a percentage of GDP (see table 1.3). Notably, tax revenue fell sharply-byabout one-third---during the 1995 recession.

7

Chapter I

Figure 1.4. Trends in Public Sector Revenue, 1980-98

(a) Total Budgeted Revenue (b) Tax Revenue

ss________________ . __________ 40

75 355

65 3

45 20

90 8Z 84 86 S8 90 92 94 96 98 80 82 84 86 98 90 92 94 96 98

(c) Non-Tax Federal Revenue (d) Other Public Sector Revenue

25 145220

235

so 30

~~~~~~~~t5~~~~~~~~~~~~220

80 92 94 86 98 90 92 94 96 98 S0 S2 S4 96 SS 90 92 94 96 98

(e) Income Tax Revenue (h Revenue from Goods & Services Taxes

2 0 - _2___.5

is to0

o t

oo

90 92 84 96 99 90 92 94 96 9S go 92 94 36 99 90 92 94 96 99

(g) Revenue from Trade Taxes (h) Revenue from Hydrocarbon Fees

22 ~ ~ ~ ~ ~ ~ ~~~~~~~~~~~2

.14

90 9 2 94 86 99 90 92 94 96 99 to 92 84 36 99 90 92 94 96 98

(i) Revenue ofPEMEX (j) OtherNon-GovtPublic Sector Ravcoue

24- 24 -

20

2 96~~~~~~~~~~~~~~~~~2

012 16-

12

4

90 92 94 86 99 90 92 94 96 9n so 92 94 96 98 90 92 94 96 98

Source: Public sector- accounts.

8

Chapter I

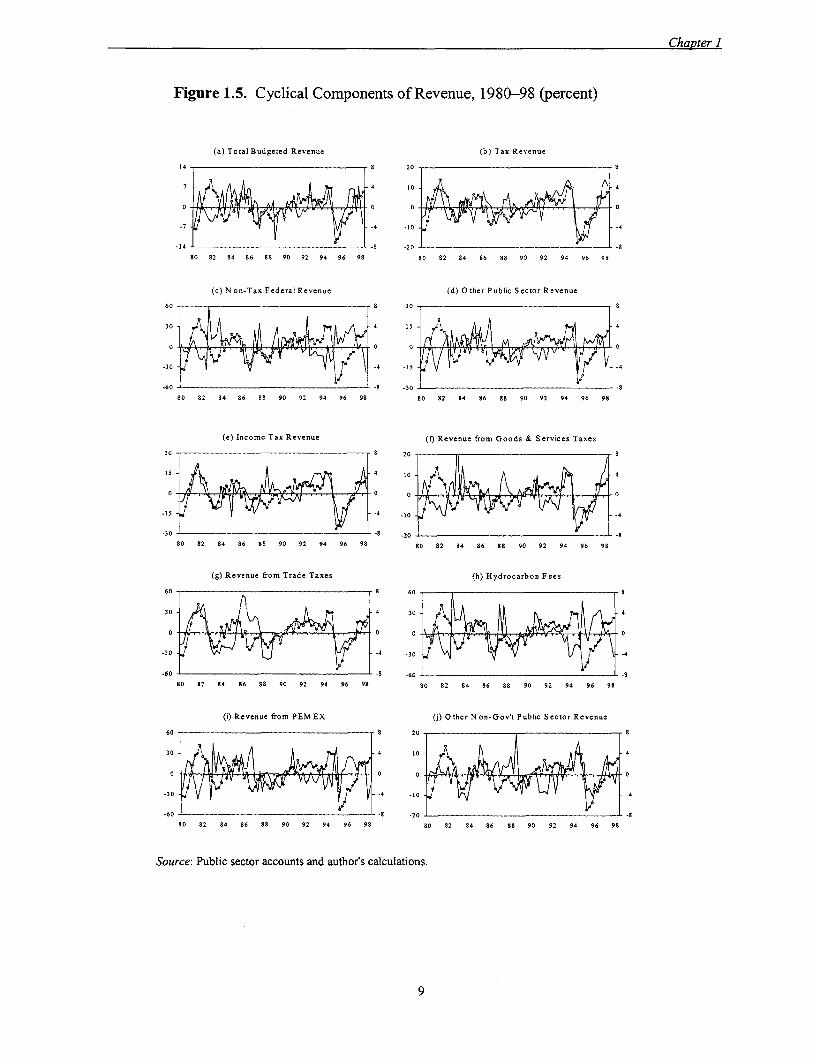

Figure 1.5. Cyclical Components of Revenue, 1980-98 (percent)

(a) Total Budgeted Revenue (b) Tax Revenue

14 - . .................... . 8 20

;. Y fd -4 0 -4

S0 82 84 86 88 90 92 94 96 98 S0 82 84 86 B8 90 92 94 96 98

(c) N on-Tax Federal Revenue (d) Other Public Sector Revenue

60 S8 0 8

(e) Inom Tax 4eeu ceu rmGos&Srie ae

-30 is

60 1 - 8 230 __ -.80 82 84 86 88 90 92 94 96 98 80 82 84 86 88 90 92 94 96 98

(e) Income Tax Revenue (t Revenue from Goods & Services Taxes

-60 -8 20 -8

80 82 84 86 88 90 92 94 96 98 80 82 94 86 88 90 92 94 96 98

(i) Revenue from Trade Taxe Othe ) Hydo carbon'Pbi FecoRes eu

60 5° 1 4

30 4~~~~~~~~~~~~~~~~~~-

-30 -8 -30

80 82 84 86 85 90 92 94 96 98 90 82 84 86 88 90 92 94 96 98

(i) Revenue from Trad X Tax O he Nutonoo Pbl SctorReven

60 9 20- 9

30 4 30 [ -

0 . 0 0 -

-30- -4 tO0 -4

60.3 -60------.- _________________________ -8

S0 82 84 86 88 90 92 94 96 98 80 82 84 86 88 90 92 94 96 98

Source: Reeucfo PM X(j thTN n-o' Public Sector acontendathrnuacuaios

60 20- 9~~~~~~~~

Chapter I

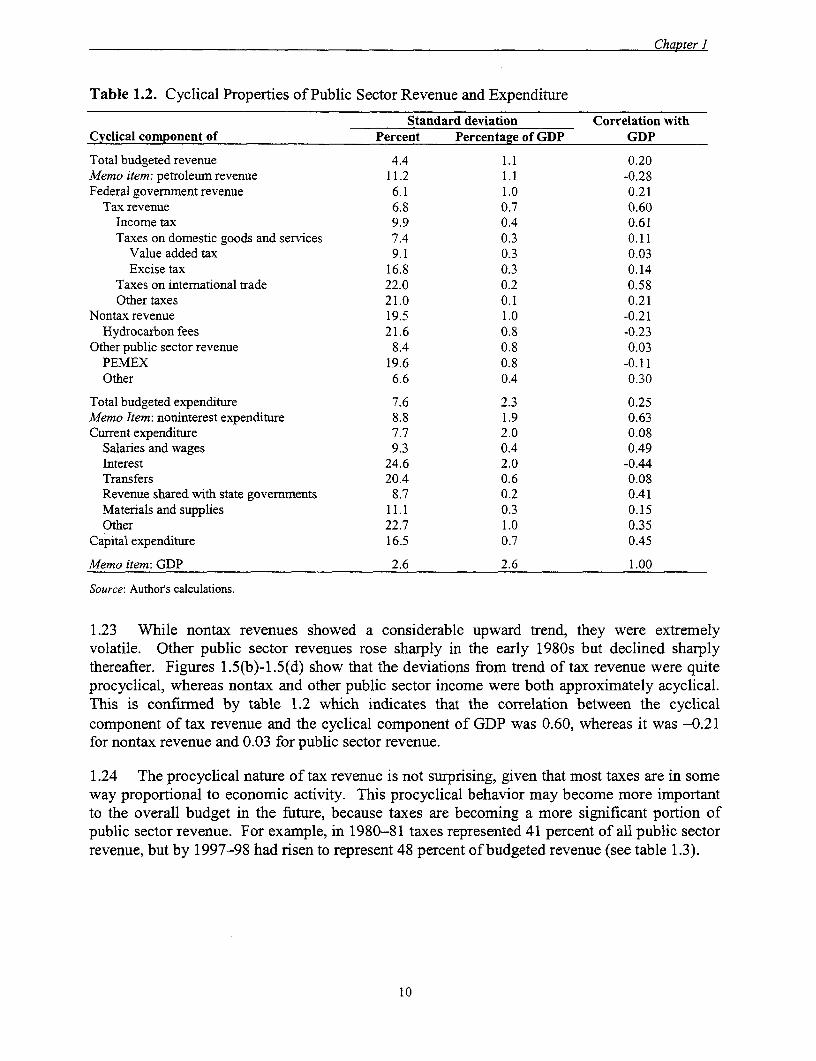

Table 1.2. Cyclical Properties of Public Sector Revenue and Expenditure

Standard deviation Correlation withCyclical component of Percent Percentage of GDP GDP

Total budgeted revenue 4.4 1.1 0.20Memo item: petroleum revenue 11.2 1.1 -0.28Federal government revenue 6.1 1.0 0.21

Tax Tevenue 6.8 0.7 0.60Income tax 9.9 0.4 0.61Taxes on domestic goods and services 7.4 0.3 0.11

Value added tax 9.1 0.3 0.03Excise tax 16.8 0.3 0.14

Taxes on international trade 22.0 0.2 0.58Other taxes 21.0 0.1 0.21

Nontax revenue 19.5 1.0 -0.21Hydrocarbon fees 21.6 0.8 -0.23

Other public sector revenue 8.4 0.8 0.03PEMEX 19.6 0.8 -0.11Other 6.6 0.4 0.30

Total budgeted expenditure 7.6 2.3 0.25Memo Item: noninterest expenditure 8.8 1.9 0.63Current expenditure 7.7 2.0 0.08

Salaries and wages 9.3 0.4 0.49Interest 24.6 2.0 -0.44Transfers 20.4 0.6 0.08Revenue shared with state governments 8.7 0.2 0.41Materials and supplies 11.1 0.3 0.15Other 22.7 1.0 0.35

Capital expenditure 16.5 0.7 0.45

Memo item: GDP 2.6 2.6 1.00

Source: Author's calculations.

1.23 While nontax revenues showed a considerable upward trend, they were extremelyvolatile. Other public sector revenues rose sharply in the early 1980s but declined sharplythereafter. Figures 1.5(b)-l.5(d) show that the deviations from trend of tax revenue were quiteprocyclical, whereas nontax and other public sector income were both approximately acyclical.This is confirmed by table 1.2 which indicates that the correlation between the cyclicalcomponent of tax revenue and the cyclical component of GDP was 0.60, whereas it was -0.21for nontax revenue and 0.03 for public sector revenue.

1.24 The procyclical nature of tax revenue is not surprising, given that most taxes are in someway proportional to economic activity. This procyclical behavior may become more importantto the overall budget in the future, because taxes are becoming a more significant portion ofpublic sector revenue. For example, in 1980-81 taxes represented 41 percent of all public sectorrevenue, but by 1997-98 had risen to represent 48 percent of budgeted revenue (see table 1.3).

10

Chapter I

Table 1.3. Main Components of Public Sector Revenue and Expenditure, 1980-81 and 1997-98(percent)

GDP Budgeted revenueBudget category: 1980-81 1997-98 Average 1980-81 1997-98 Average

Total budgeted revenue 24.6 21.6 25.6 100.0 100.0 100.0Memo item: petroleum revenue 8.2 7.4 9.5 33.3 34.1 36.3Federalgovernmentrevenue 14.6 15.1 15.6 59.3 69.8 61.5

Taxrevenue 10.1 10.3 10.4 41.2 47.7 41.0Income tax 5.1 4.3 4.5 20.8 20.0 17.9Taxes on domestic goods and services 3.5 4.9 4.7 14.4 22.7 18.4

Value added tax 2.6 3.1 2.9 10.4 14.5 11.5Excise tax 1.0 1.8 1.8 4.1 8.2 6.9

Taxes on intemational trade 1.0 0.6 0.8 4.3 2.6 3.0Other taxes 0.4 0.5 0.4 1.7 2.4 1.6

Nontax revenue 4.5 4.7 5.2 18.2 21.9 20.4Hydrocarbon fees 3.7 3.1 3.8 15.0 14.2 14.8

Other public sector revenue 10.0 6.5 10.0 40.7 30.1 38.5PEMEX 4.1 2.3 4.1 16.8 10.8 15.3Other 5.9 4.2 5.9 23.9 19.4 23.1

Totalbudgeted expenditure 32.2 22.8 30.4 130.9 105.8 117.6Memo item: noninterest expenditure 28.8 19.1 22.1 117.2 88.6 86.7Current expenditure 23.5 20.0 26.0 95.8 92.6 100.2

Salaries and wages 5.8 3.4 4.7 23.5 15.8 18.4Interest 3.4 3.7 8.3 13.7 17.1 30.8Transfers 2.9 5.0 2.8 11.7 23.2 11.5Revenue shared with state governments 2.2 3.0 2.7 9.1 14.0 10.6Materials and supplies 3.5 1.6 3.0 14.2 7.2 11.5Other 5.9 3.3 4.4 23.9 15.1 17.2

Capital expenditure *8.8 2.9 4.4 35.9 13.3 17.5

Source: Public Sector accounts.

1.25 Despite their overall procyclical nature, the trends and cycles across various taxcategories exhibit some interesting differences. Figures 1.4(e)-1.4(g) show the most importantcomponents of tax revenue: income tax; taxes on domestic goods and services, namely, valueadded tax (VAT) and excise tax; and taxes on international trade, which are dominated by importtaxes.

1.26 Table 1.3 shows that domestic goods and services taxes have been an increasinglyimportant part of revenue. In 1997-98 these taxes represented 48 percent of all tax revenues,versus 35 percent in 1980-81. Most of this increase has come from taxes of petroleum products:more than half of the increase in VAT receipts has come from PEMEX. Excise taxes on gasolinehave risen sharply, while other excise taxes have fallen. Taxes on domestic goods and servicesare the only tax component that appears to have been rising significantly during the study period.Income taxes have risen somewhat, while taxes from international trade are roughly at the samelevels now as they were in 1980, thus both have fallen as a share of revenue and GDP. Thedeclining reliance on import duties, the slow expansion of income taxation, and the expansion ofVAT are typical of countries at Mexico's stage of development. However, scope exists for thefurther expansion of VAT on commodities other than petroleum.

11

Chapter l

1.27 As concerns cyclical properties, figures 1.5(e)-1.5(g) show the cyclical components ofthe three types of taxes. Income taxes are clearly highly procyclical (table 1.2 indicates that thecorrelation with the cyclical component of GDP is 0.61), though clearly more volatile than thebusiness cycle itself. Taxes on domestic goods and services are not particularly procyclical (thecorrelation with GDP is just 0.11), but this pattern appears to have been changing since 1994.Revenue from trade taxes is highly procyclical (the correlation with GDP is 0.58), reflecting thehighly procyclical nature of imports.

1.28 The sole large component of nontax revenue is hydrocarbon fees, which are included infederal government revenue under one classification scheme, although they are sometimesclassified as PEMEX revenue.3 They are plotted in figure 1.4(h). They display little overalltrend, currently represent about 14 percent of all budgeted revenue, and have been somewhatcountercyclical (the correlation with GDP is -0.23), as indicated by Figure 1.5(h).

1.29 The single largest component of rest of public sector revenue is the revenue of PEMEX,which is displayed in figure 1.4(i). Even when hydrocarbon fees are classified as governmentrevenue PEMEX still represents 11 percent of all budgeted revenue and more than a third of therevenue generated by the nongovemrnment public sector. Although PEMEX's contribution hasdeclined in significance from about 17 percent of revenue in 1980-81, this figure is misleading.If all petroleum-based revenue is aggregated across the public sector, it currently represents 34percent of revenue as opposed to 33 percent of revenue in 1980-81 (see table 1.3). As figure1.5(i) indicates, and table 1.2 confirms, PEMEX's contribution to revenue is somewhatcountercyclical: the correlation with GDP is _0.11 .4

1.30 The rest of the public sector has declined slightly as a source of revenue (see table 1.3)and has somewhat procyclical income as indicated by figure 1.5(j) and table 1.2. Among theimportant contributors are the electrical utilities and railways.

1.31 On the expenditure side of the public sector flow of funds, a distinction will be madebetween interest on public debt and other forms of spending. Noninterest expenditure fell in theearly 1980s, as indicated in figure 1.6(a). This occurred just as interest expenditure (figure 1.6h)accelerated with the inflation rate. As table 1.3 indicates, noninterest expenditure has fallensharply as a fraction of GDP, from 29 percent in 1980-81 to just 19 percent in 1997-98. At thesame time, the public sector has moved to a substantial primary surplus position on budget, withbudgeted noninterest expenditure now representing 89 percent of budgeted revenue, as opposedto 117 percent in 1980-81. Interestingly, noninterest expenditure is highly procyclical, asindicated by figure 1.7(a) and table 1.2. The correlation of its cyclical component with thecyclical component of GDP is 0.63, and it is substantially more volatile than GDP with astandard deviation of 8.8 percent (1.9 percent of GDP), compared with 2.6 percent for GDP(table 1.2). This procyclical behavior of expenditure offsets the procyclical behavior of revenueand tends to make the primary budget close to neutral with respect to the cycle. As a recentstudy by the Inter-American Development Bank indicated (Gavin and others 1996), the public

3. In the "B" accounts of the Secretaria de Hacienda y Credito Puiblico the revenues from hydrocarbons areclassified as government revenue, but in the "G" accounts they are classified as revenues of PEMEX.Consolidation across the entire public sector makes this accounting difference irrelevant.

4. Looking more narrowly, the export revenues of PEMEX, which are more closely tied to the world oil price, aremore strongly countercyclical: the correlation with GDP is -0.29.

12

Chapter I

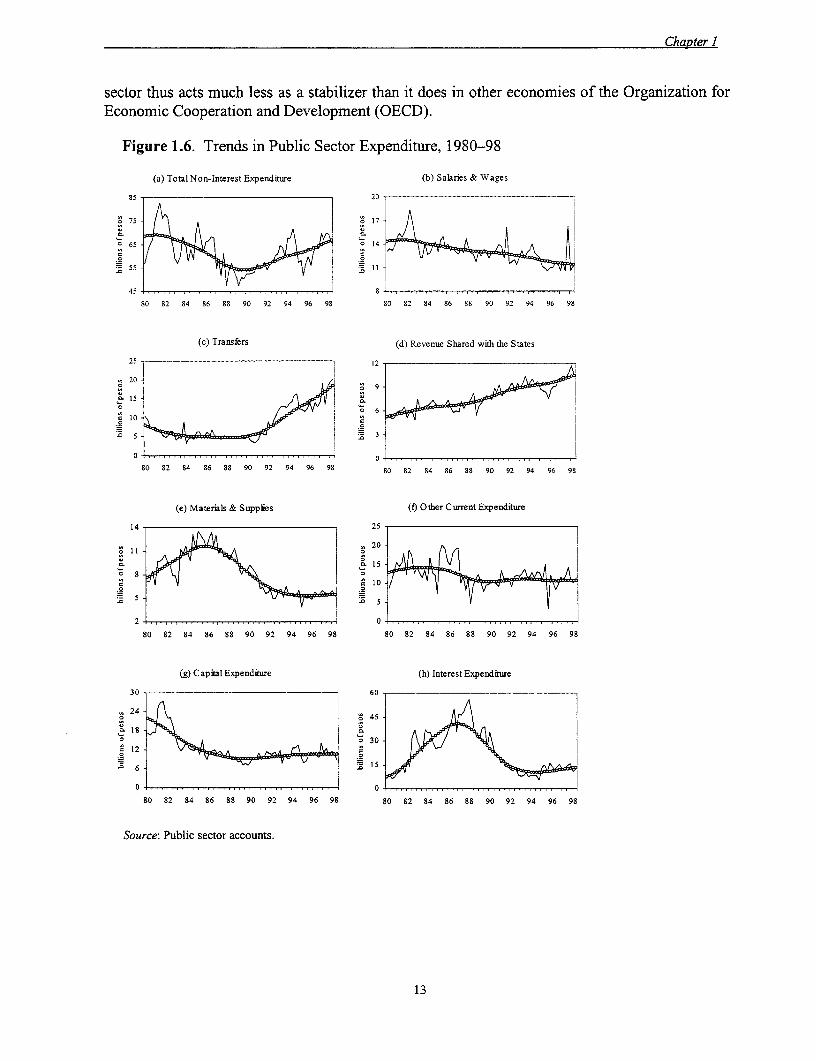

sector thus acts much less as a stabilizer than it does in other economies of the Organization forEconomic Cooperation and Development (OECD).

Figure 1.6. Trends in Public Sector Expenditure, 1980-98

(a) Total Non-Interest Expenditure (b) Salaries & Wages

85 20 -

o75- 1 -1

O65-~ 14-

55 1

45i 8S0 82 84 j6 88 90 92 94 96 98 S0 82 84 86 88 90 92 94 96 98

(c) Transfers (d) Revenue Shared with the States

25- 12

20-

10 O

.05

80 82 84 86 88 90 92 94 96 9S S0 82 84 86 8 90 92 94 96 98

(e) Materials & SuppEes (f) Other Current Expenditure

14- 25-

09 ~ ~ ~ ~ ~ ~ ~ ~ ~~~~~0

5-

(g) C apital Expenditure (h) Interest Expenditure

30 ~ ~ ~ ~ ~ ~ ~ ~~~~~~324

0. 19~ ~~~~~~~~~~~~~~1

80 82 84 86 88 90 92 94 96 98 80 82 84 86 88 90 92 94 96 98

Source: Public sector accounts.

13

Chapter I

Figure 1.7. Cyclical Components of Expenditure, 1980-98(percent)

(a) TotalNon-Interest Expenditure (b) Salaries & Wages

24- _ 8 40-

12- 4 20~ 4

0 k0 0 ~

-12- -4 -20-

-24 -8 -40 -8

80 82 84 86 88 90 92 94 96 98 80 82 84 86 88 90 92 94 96 98

(c) Transfers (d) Revenue Shared with the States

30- 4 15- 4

0 0 0 0

-30 ~ 4 1 -4

-60 - -- -30 -S

80 82 84 86 88 90 92 94 96 98 80 82 84 86 88 90 92 94 96 98

(e) Materials & Supplies () Other Current Expenditure

30-- 8 7018

is V 4 35- 4

0 - m A 0 0 - A ~~~~ 19.0A

-45 -8 7 0

80 82 84 86 88 90 92 94 96 98 80 82 84 86 88 90 92 94 96 98

(g) Capital Expendiure (h) Interest Expenditure

50 -- 8 80 ------- - ----------------- ---- 8

25- 4 40

0- 0W A N 0

-25 -4 -40 -

-5 ----5__._-- _ 8-0 ---- _............................................ _ ___ ..

80 82 84 86 88 90 92 94 96 98 80 82 84 86 88 90 92 94 96 98

Source: Public sector accounts and author's calculations.

1.32 Once expenditure is divided into its components, an even clearer picture emerges.Salaries and wages in the public sector, depicted in figure 1.6(b), have been declining in realterms almost steadily since 1980. Table 1.3 indicates that they now represent just 16 percent ofbudgeted revenue, compared with 24 percent in 1980-81. Most of the decline in the publicsector wage bill has been within the federal government, which is perhaps surprising given the

14

Chapter I

declining importance of the nongovernment component of the public sector. While the wage billhas fallen as the economy has expanded (figure 1.6b), figure 1.7(b) and table 1.2 indicate that themovements around this trend have been quite procyclical. Most of this procyclical behavior isnot due to the federal government wage bill, but is largely determined by the behavior of wageswithin the corporate public sector.5

1.33 Transfers have become an increasingly significant component of the overall public sectorbudget, as indicated by figure 1.6(c). By 1997-98 they represented 23 percent of budgetedrevenue as opposed to just 12 percent in 1980-81 (table 1.3). Because government transfers topublic sector corporations are netted out of this figure, this represents a substantial increase in theimportance of social programs within the economy. However, these transfers have not beencountercyclical as one might have expected. If anything, transfer payments appear to beprocyclical: figure 1.7(c) shows that spending on transfers rose rapidly during the early l990sand then declined sharply during the 1995 recession. On the other hand, table 1.2 indicates that,overall, transfers have been approximately acyclical.

1.34 The lack of cyclical variation in transfer payments deserves some further explanation.The figures used in this chapter for "transfer payments" correspond to that portion of thegovernment's spending category "Aid programs, subsidies and transfers" that is classified ascurrent expenditure. In 1997 this amounted to about 200 billion pesos. Economic classificationof expenditure is available for the entire "Aid programs, subsidies and transfers" category withcapital expenditures included. In 1997 this amounted to about 230 billion pesos. So currentexpenditures make up the bulk of this category. The portion of this overall budget dedicated toaid programs or social assistance spending was only about 32 billion pesos or about 15 percent ofcurrent transfers. Most of the rest of the transfer budget represents revenue sharing, subsidies orfinancing to public sector entities. Given these facts, it is not surprising that transfer spending isapproximately acyclical.

1.35 The federal government shares a substantial portion of its revenue with states, and thisrevenue sharing has increased in importance, as indicated by figure 1.6(d). Revenue distributedto the states rose from 9 percent of budgeted revenue in 1980-81 to 14 percent in 1997-98 (table1.3). It has also been procyclical, its cyclical component having a correlation of 0.41 with thecyclical component of GDP (table 1.2). This is similar in magnitude to the correlation of overalltax revenue with GDP.

1.36 Because the nongovernment public sector is responsible for most of the expenditure onmaterials and supplies, the decline of this component of the public sector is responsible for thedecline in this expenditure relative to public sector revenue from 14 percent in 1980-81 to 7percent in 1997-98.6 This pattern is confirmed by figure 1.6(e). Materials and suppliesexpenditures are only slightly procyclical, as indicated by figure 1.7(e). The correlation of theircyclical component with GDP is just 0.15 (table 1.2).

5. Disaggregated figures not presented in Table 1.2 indicate that the federal governnent's wage bill has a cyclicalcorrelation with GDP of just 0. 18, while the figure for the rest of the public sector is 0.58.

6. Figures not presented in table 1.3 indicate that, on average, more than 90 percent of materials and suppliesexpenditure is accounted for in the nongovernment sector.

15

Chapter 1

1.37 Other current expenditure, illustrated in figure 1.6(f), consists of several items includingpayments for services rendered by the private sector. It has declined significantly as a share ofrevenue from 24 percent in 1980-81 to just 15 percent in 1997-98 (table 1.3). This is largelydue to a decline in this type of spending by the federal government. It is somewhat procyclicalas indicated by Figure 1.7(f), and has a correlation with GDP of 0.35 (table 1.2).

1.38 Capital expenditure is the last category of noninterest expenditure. This has declinedsignificantly since its peak in 1982. Capital expenditure has declined from 36 percent ofbudgeted revenue in 1980-81 to just 13 percent in 1997-98 (table 1.3). The federal governmenthas halved its capital spending from 1 4 to less than 7 percent of budgeted revenue, while the restof the public sector has seen an enormous decline in capital spending from 22 percent of revenueto less than 7 percent. Capital spending has been quite procyclical, as indicated by figure 1.7(g).Its correlation with GDP was 0.45 (table 1.2) during the entire study period. Indeed, duringsevere recessions such as those in 1982 and 1995, capital spending was cut sharply.

1.39 The final item is interest expenditure, illustrated in figure 1.6(h). Inflation effects are thedriving force behind changes in the size of interest flows. Interest expenditure shot up in 1982and 1986, not only because public sector debt increased, but mainly because inflation accelerateddramatically. High real interest rates in the stabilization period after 1988 kept interestexpenditure at high lev-els, but declining debt eventually brought interest spending down. Itagain rose in significance in 1995 as inflation accelerated during the peso crisis, but by the timethe public sector's overall level of indebtedness was by then much lower than in the early 1980s.Interest expenditure is strongly countercyclical, its correlation with GDP being -0.45 (table 1.2),largely because in Mexico inflation has tended to be highest during periods of recession.

1.40 One way to deal with the inflation effects that dominate interest flows would be tocompute real rather than nominal interest flows. Even though the interest flows pictured infigure 1.6(h) are expressed in real terms (that is, they are expressed in constant peso termns), theyare nominal interest flows in the sense that they represent some average nominal interest ratetimes the nominal level of debt divided by the price level. Real interest flows, instead, would becomputed by calculating some average real interest rate times the nominal level of debt, dividedby the price level. Making accurate adjustments of this sort is quite difficult when a significantfraction of the debt is held outside Mexico and is denominated in many different foreigncurrencies. Furthermore, at times, significant portions of domestic debt have been indexed orissued in foreign currency. Hence no attempt at making inflation adjustments is made here. Thisis of little significance, because later sections argue that the focus should be on the primarybudget surplus, which excludes all interest expenditure.

The Cyclically Adjusted Budget Surplus in Mexico

1.41 This section outlines a methodological approach for computing cyclically adjusted budgetsurplus measures for Mexico. It examines several approaches that a variety of intemationalorganizations use and computes historical surplus figures using a preferred method. It then askswhether the adjusted surplus is a useful concept, that is, can it help policymakers make policydecisions?

16

Chapter I

Methods for Computing the Cyclically Adjusted Budget Surplus

1.42 Economists have long recognized that budget surplus figures tend to be procyclical. Inparticular, budget surpluses are procyclical in most OECD countries for a number of reasons thatwill be elaborated upon later. In the context of Keynesian macroeconomic theory, when thepublic sector runs a larger budget surplus than previously, the government is said to have acontractionary fiscal policy stance. However, if the budget surplus is larger simply because theeconomy is going through an expansionary phase of the business cycle, thinking of fiscal policyas contractionary may be inappropriate. Thus, many economists have proposed that budgetsurplus figures should somehow be adjusted to allow for the effects of the business cycle.

1.43 The literature on adjusted budget surplus measures can be traced back to the paper byBrown (1956), where he argued that to measure the stance of fiscal policy correctly one had todistinguish between "automatic" and "discretionary" policies. Brown's paper did not propose anadjusted measure of the budget surplus, because he explicitly argued in favor of the differentialtreatment of the various components of revenue and expenditure with reference to an explicitKeynesian model of the economy.

1.44 Since Brown's paper economists have sought a single indicator of the stance of fiscalpolicy, similar to the budget surplus as a percentage of GDP, but adjusted for the business cycle.A number of government and international agencies produce these sorts of measures includingthe OECD, the World Bank, the International Monetary Fund (IMF), the European Community(EC), and their various member goverunents. A number of indicators have been suggested.Chouraqui, Hagemann, and Sartor (1990) and Price and Muller (1994) present good discussionsof the various indicators. Blanchard (1990) and Buiter (1993) provide arguments against usingsingle indicators.

1.45 Cyclical adjustment of the budget usually begins with the decomposition of output intosome trend, or potential, component and its cyclical component. The technical appendixdescribes several methods including the one used here: the same method that the EC uses (seeEC 1995 for even greater detail regarding its method of estimating structural budget deficits),which adopts the HP filter-based trend in GDP as the measure of potential output.

1.46 To compute cyclically adjusted surplus measures the EC, IMF, and OECD estimate theelasticities of various components of revenue and expenditure with respect to output. They usethe estimated elasticities to make cyclical adjustments to these components of the budget.7 Atthis stage an important set of assumptions must be made: one must decide which revenue andexpenditure components fall into the automatic category and which fall into the discretionarycategory. Because the assumption is that the business cycle causes those that fall into theautomatic category, while those in the discretionary category potentially cause the cycle, onlythose components that fall into the automatic category should be adjusted.

7. Details of how the elasticities are estimated and used to make cyclical adjustments are provided in the technicalappendix.

17

Chapter I

1.47 For the purposes of this chapter, the following revenue and expenditure categories inMexican data were considered for adjustment:

* Income tax revenue, Rlt

* Taxes on domestic goods and services, excluding gasoline, R2 t

* Taxes on intemational trade, excluding taxes on PEMEX imports, R3t

* Other tax revenue, R4t

* Governnent transfers net of transfers to the public sector, X, .

Estimates of the elasticities of these revenue and expenditure categories with respect to thecyclical component of output are found in table 1.4. As the elasticity for transfer payments wasnot statistically significant, no adjustments to this item were made. Adjustments to the fourrevenue categories were made.

1.48 It should be reemphasized that the decision to adjust some revenue/expenditurecategories and not others is based on strong a priori assumptions about causality rather than on astatistical test. The notion is that tax revenues behave cyclically largely because most taxsystems rely on statutory tax rates on various types of economic activity-this naturally leads tocyclical movements in tax revenue. Similarly, in many countries transfer programs arestructured to respond automatically to business cycle movements. As a result, it seemsreasonable, from a theoretical perspective, to treat the cyclical movements of tax revenues andtransfers as being driven by the various factors that drive the business cycle, rather than being thecauses, themselves, of the business cycle. Expenditure categories such as wages and salaries andcapital expenditure are highly procyclical, but they are typically not adjusted for the cycle-theimplicit argument against adjustment is that these categories of expenditure are fundamentallymore discretionary. Of course, if all revenue and expenditure categories were adjusted theadjusted surplus would be uncorrelated, by construction, with the business cycle.

1.49 As described in more detail in the technical appendix, the adjusted surplus measure isgiven by

(1) At = At - Rj, [exp (eR>y )-1

i=,

where A, is the standard budget surplus measure, ej1 is the elasticity of Rj, with respect to

output and y, is the cyclical component of output, as measured using the HP filter.

1.50 As table 1.3 indicates, oil revenue represents about a third of the Mexican public sector'sbudgeted revenue. There is some question as to whether the cyclically adjusted budget measuresshould also reflect this fact. On the one hand, if one wants to make adjustments that purelyreflect the business cycle's effect on the budget, one would make no adjustments to oil revenue.On the other hand, if the purpose of estimating a cyclically adjusted fiscal surplus is to isolatethose components of the budget that are not driven by exogenous forces, correcting for oil prices

18

Chapter I

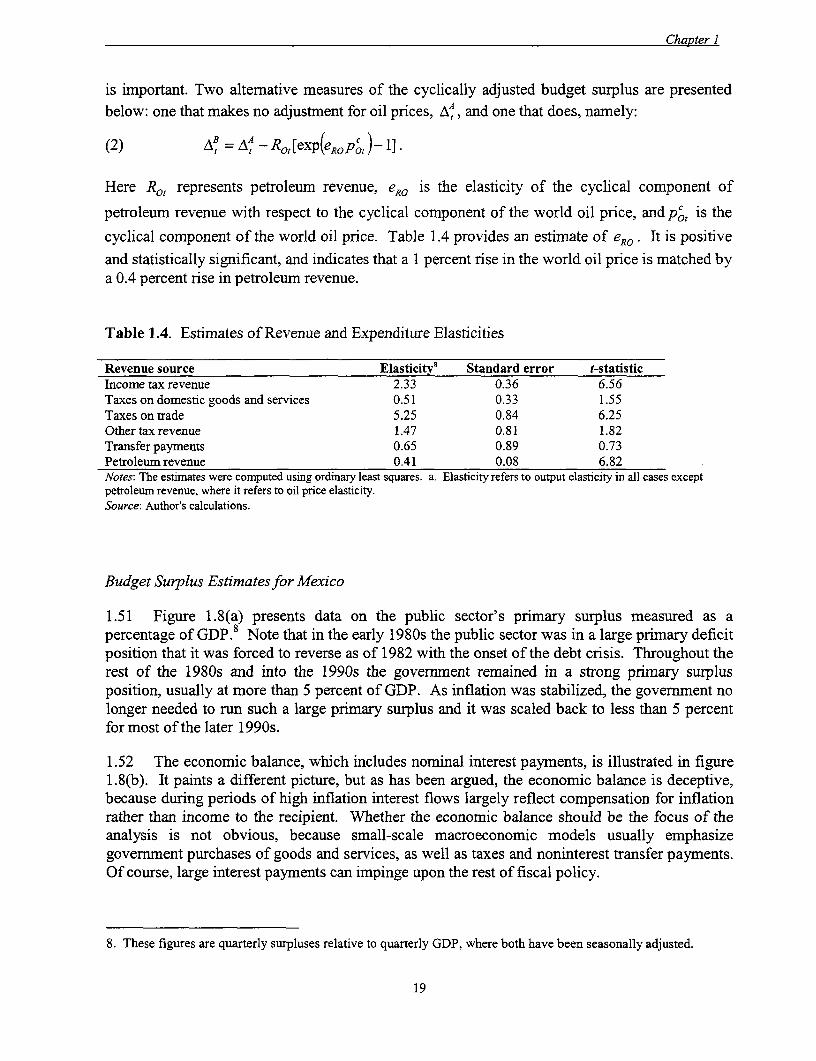

is important. Two alternative measures of the cyclically adjusted budget surplus are presentedbelow: one that makes no adjustment for oil prices, !A, and one that does, namely:

(2) A, = A - RO[exp(eROpt )-1].

Here Rot represents petroleum revenue, eRG is the elasticity of the cyclical component of

petroleum revenue with respect to the cyclical component of the world oil price, and po is the

cyclical component of the world oil price. Table 1.4 provides an estimate of eRO. It is positive

and statistically significant, and indicates that a 1 percent rise in the world oil price is matched bya 0.4 percent rise in petroleum revenue.

Table 1.4. Estimates of Revenue and Expenditure Elasticities

Revenue source Elasticitya Standard error t-statisticIncome tax revenue 2.33 0.36 6.56Taxes on domestic goods and services 0.51 0.33 1.55Taxes on trade 5.25 0.84 6.25Other tax revenue 1.47 0.81 1.82Transfer paymnents 0.65 0.89 0.73Petroleum revenue 0.41 0.08 6.82Notes: The estimates were computed using ordinary least squares. a. Elasticity refers to output elasticity in all cases exceptpetroleum revenue, where it refers to oil price elasticity.Source: Author's calculations.

Budget Surplus Estimates for Mexico

1.51 Figure 1.8(a) presents data on the public sector's primary surplus measured as apercentage of GDP.8 Note that in the early 1980s the public sector was in a large primary deficitposition that it was forced to reverse as of 1982 with the onset of the debt crisis. Throughout therest of the 1980s and into the 1990s the government remained in a strong primary surplusposition, usually at more than 5 percent of GDP. As inflation was stabilized, the government nolonger needed to run such a large primary surplus and it was scaled back to less than 5 percentfor most of the later 1990s.

1.52 The economic balance, which includes nominal interest payments, is illustrated in figure1.8(b). It paints a different picture, but as has been argued, the economic balance is deceptive,because during periods of high inflation interest flows largely reflect compensation for inflationrather than income to the recipient. Whether the economic balance should be the focus of theanalysis is not obvious, because small-scale macroeconomic models usually emphasizegovernment purchases of goods and services, as well as taxes and noninterest transfer payments.Of course, large interest payments can impinge upon the rest of fiscal policy.

8. These figures are quarterly surpluses relative to quarterly GDP, where both have been seasonally adjusted.

19

Chapter 1

1.53 The cyclically adjusted primary balance is illustrated in figure 1.8(c). At first glance, thecyclically adjusted balance and the standard measure of the primary balance appear to be quitesimilar. The difference between the two measures is plotted in figure 1.8(e), and at times it issubstantial. Whenever it is negative, it indicates that fiscal policy was more contractionary thanindicated by the standard primary surplus. Whenever it is positive, fiscal policy was moreexpansionary than indicated by the standard primary surplus. Note, for example, that fiscalpolicy looks more expansionary during the 1990-94 with the adjusted budget figures.

1.54 The adjustments for petroleum revenue can also be substantial. Petroleum revenuemoves closely with the world oil price, which is highly volatile. Figure 1.8(f) shows thatadjustments of revenue for exogenous movements in oil prices have amounted to as much as 2percent of GDP. For example, oil revenue shot up in 1991 because of the Gulf War. Removingthis effect from the data requires an adjustment in the amount of 2 percent of GDP; however,figure 1.8(d) shows that the overall picture is little changed by taking movements in oil revenuedue to oil prices into account. Other factors dominate movement in the budget surplus.

1.55 Using the primary balance as a summary measure, Mexico's fiscal policy is procyclical inthe following sense. Countercyclical policy, or leaning against the wind, is usually described asrunning deficits during recessions and surpluses during expansions. In other words, policy iscountercyclical when the budget surplus is procyclical. However, the correlation betweenMexico's primary surplus as a percentage of GDP and the GDP's cyclical component, measuredin percent, is -0.35. This indicates that Mexico has tended to run higher surpluses during hardtimes and smaller surpluses or deficits during good times.

1.56 The cyclical adjustment of the primary surplus only makes this fact starker. Thecorrelation between the cyclically adjusted primary surplus and GDP is -0.44.9 This suggeststhat discretionary policy, rather than leaning against the wind, seems to lean quite strongly withthe wind.

1.57 The finding here is consistent with the discussion in Gavin and others (1996). They studya number of Latin American countries and find that in the typical country, fiscal policy is muchmore procyclical than in the OECD. Both revenue and expenditure are typically much moresensitive to the business cycle than in the OECD, but the expenditure effect is stronger.

1.58 This finding may reflect the fact that during recessions, Mexico's public sector, like thatin many Latin American countries, faces a hard budget constraint. Perhaps discretionary policycannot be expansionary in the traditional sense because the government is liquidity constrained.But this begs the question: how did the government become liquidity constrained in the firstplace? Was procyclical fiscal policy itself the culprit? Whatever the reason, policymakersshould note that policy moves with the business cycle rather than against it.

9. This is to be expected, because the cyclical component of the budget surplus is highly correlated with the cyclicalcomponent of GDP. The cycle- and oil-adjusted budget surplus has a correlation with GDP of -0.40.

20

Chapter I

Figure 1.8. The Budget Surplus and the Fiscal Impulse, 1980-98

(a) Primary Balance (b) Economic Balance

15 5-

-15 ^20 s !

80 82 84 86 88 90 92 94 96 98 80 82 84 86 88 90 92 94 96 98

(c) Cyclically-Adjusted Primary Balance (d) Cycle- and Oil-Adjusted Primnary Balance

15 - . ..............15!

10- C 101S........ 1.5 2.0

80 82 84 86 88 90 92 94 96 98 80 82 84 86 88 90 92 94 96 98

(c) Cy(ca) Cyciedbased PriAdjustm ent (BaOilh) Cycal OR-Adjust me nt s

1.5- 2.0

10- ~~~~~~~~~~~10-

o E

05

_ 0 \ .3 \ F 94\t ~~~~ 0.

--0.5-

10- ~~~~~~~~~~~~~~-10.-1.0 -1.0

80 82 84 86 88 90 92 94 96 98 80 82 84 86 88 90 92 94 96 98

(g)o Fiscale: se b Cyc lAdjustment (h m ls Adjustment s

2.5- 21

o ~~~~~~~~~~~~~~~~~10-0.5-

5-1 ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~~~~~05 -

-2 1. -2

80 8 2 84 86 9 2 94 9 88 84 86 88 90 92 94 96 98 jS gour ical Ipublcseco bacdounts.eAjsmnt(Fsa mplebsdo Bt dutet

1~~~~~~~~~~~~2

Chapter 1

1.59 How are the cyclically adjusted budget figures useful to policymakers? Presumably theyare useful because they isolate the component of fiscal policy that is assumed to be exogenouswith respect to the business cycle from the part that is determined by the business cycle. Onecould argue that it is this component of policy that is discretionary, and policymakers should begiven some sense of the effects of these discretionary policies on economic activity.Underpinning the various approaches discussed is the assumption that a simple Keynesian modelcan be used to think about the economy. It is this model that allows the effects on output to beidentified. To summarize fiscal policy with one budget number one must assume that the sameKeynesian multiplier applies to government purchases of goods and services, taxes, and transferpayments. Because even the simplest Keynesian models are inconsistent with such anassumption, the possible limitations of the cyclically adjusted budget balance as an indicator offiscal policy are immediately obvious.

1.60 An altemative fiscal indicator that the IMF uses is the fiscal impulse (the discussion hereis loosely based on Chand 1993). This indicator compares the stance of fiscal policy in twosuccessive budget years, but it continues to treat governmnent purchases, taxes, and transfersvirtually symmetrically. The fiscal impulse measure is based on the so-called cyclical effect ofthe budget, which is defined as the difference between the actual budget surplus and the budgetsurplus that would have been achieved in the absence of discretionary policy. In its simplestform, this method treats all movements in government expenditure that are not proportional totrend output as discretionary. It further treats all changes in revenue because of changes in theaverage rate at which revenue is raised as discretionary. Thus the discretionary component of thebudget surplus is

AD = R, - rY, - (X, - xY,*)

=/, r-t )

where F is the ratio of revenue to output in a typical year, x is the ratio of expenditure to outputin a typical year, and the other variables are defined as before. The fiscal impulse is simplydefined as the negative of the change in the discretionary budget surplus, expressed as a fractionof GDP."'

1.61 The discretionary primary budget surplus for Mexico was calculated, along these lines,by setting r and x equal to their sample averages for 1980-98. The difference between theprimary budget balance and the discretionary primary budget balance is its nondiscretionarycomponent. While the IMF method makes bigger adjustments to the budget surplus fornondiscretionary fiscal policy than the methods described earlier, the overall picture remainsunchanged. The discretionary budget surplus remains countercyclical, and its correlation withthe cyclical component of GDP is -0.46. It is also highly correlated with the cyclically adjustedbudget surplus calculated previously. The correlation coefficient between the two series is0.998. Hence this section continues to use l .

10. The fiscal impulse is the negative of the change in the discretionary budget surplus, because budget deficits areassumed to provide a positive imnpulse to economic activity.

22

Chapter 1

1.62 The fiscal impulse, FI/A = _(YA _), in some sense measures the change in policy

stance. Whenever it is positive, policy is moving toward a more expansionary position. Figure1.8(g) shows the fiscal impulse calculated using the cyclically adjusted budget surplus, whilefigure 1.8(h) shows the fiscal impulse calculated using the cycle- and oil-adjusted budgetsurplus: FIB = -( _J - AB1). Both series are expressed as backward-looking, four-quarter,moving averages, because the quarterly observations are extremely volatile. The two measuresare almost perfectly correlated. They both indicate that in every case where Mexico has goneinto recession, fiscal policy has moved toward a more contractionary stance.

1.63 As Chand (1993) acknowledges, the IMF measure of discretionary fiscal policy, like thecyclically adjusted budget surplus measures, is somewhat flawed in that it treats governmentpurchases, transfers, and taxes symmetrically, at least with regard to the effects of theirdiscretionary components on output. Furthermore, the cyclically adjusted budget surplus andthe discretionary budget surplus are useful tools of policy analysis only to the extent that they areimportant factors in the determination of output. This is usually taken on faith, but whetherdiscretionary policy matters for economic activity, even if it is identified correctly, is notobvious. It will matter only if the economy behaves as if it were a simple Keynesian model. Thenext section addresses this issue for Mexico.

How Fiscal Policy and Output Affect Each Other in Mexico

1.64 Does discretionary fiscal policy actually affect output? Does it affect output in ways thatKeynesian macroeconomic models would predict? That is, is so-called expansionary fiscalpolicy actually expansionary? This section explores these questions in a more complexframework than the previous section by explicitly modeling the feedback between fiscal policyand output. Using a vector autoregressive (VAR) approach, the model is enhanced by explicitconsideration of oil prices (the main determinant of Mexico's terms of trade), the real exchangerate (a possible indicator of monetary policy, wealth effects, or public confidence), the U.S.Federal Funds rate (an indicator of U.S. monetary policy) and GDP in the United States (anindicator of the demand for Mexican exports).

1.65 The approach in the previous section is clearly somewhat limiting. Under the identifyingassumption that some revenue and expenditure components are endogenous to the business cyclewhile others are not, it allows the calculation of cyclically adjusted budget figures, but it does notpermit hypotheses about the dynamic effects of the cyclically adjusted budget to be tested.Furthermore, it does not take into account the full effects of such factors as the terms of trade,external demand, and world interest rates.

1.66 This section addresses the following questions using the VAR approach:

* How does discretionary policy affect economic activity?* What were the fiscal impulses to output in historical episodes?* Is there significant reverse causality from output to the budget not captured with the

methodology used in the previous section?

23

Chapter I

* Is there enough persistence in the budget to allow for short- or medium-term forecastingof financing?

The next subsection describes the time series included in the VAR. The second subsectionanswers the first two questions about effects on output. The third subsection deals with the lasttwo questions concerning feedback effects on the budget and the potential for forecasting.

A Small VAR Model of the Mexican Economy

1.67 A modified VAR is specified for a 6 x 1 vector of time series, zt, where z, consists of

* The logarithm of the world price of oil (expressed in constant 1993 pesos per barrel)* The logarithm of real GDP in the United States (measured in constant 1992 chained

dollars)* The U.S. federal funds rate (measured in percent per year)* The Mexican fiscal surplus (measured in percentage of GDP),* The logarithm of real GDP in Mexico (measured in constant 1993 pesos)* The logarithm of the real Mexico-U.S. exchange rate.

1.68 The logarithm of the oil price, pot, is included not only because oil prices affect thepublic sector budget balance, but also because they largely determine Mexico's terms of trade.They may therefore have an effect on economic activity as well as the real exchange rate. Thelogarithm of real GDP in the United States, Yut, is included because it can be used as an

exogenous indicator of the demand for Mexican exports. The U.S. Federal Funds rate, rut, isused as an indicator of monetary policy in the United States. Because Mexico's ability to borrowfunds might well depend on conditions in the world financial market, American monetary policyis likely to play some role in business cycle fluctuations in Mexico.

1.69 For the Mexican fiscal surplus the cycle- and oil-adjusted primary budget surplus as afraction of GDP, Xt = A, / Y,t, is used in the benchmark VAR. The unadjusted primary surplus