memoire viktoriya dronova mci-iai(1)

TRANSCRIPT

MBA ESG Viktoriya Dronova

35 Avenue Philippe Auguste MBA MCI/IAI

75011 PARIS School year 2012/2013

Ukraine-Europe:

present and future of

economic relations

September 2013

Under the supervision of Pierre Deplanche, Stratégie et

consulting MBA-ESG director.

Ukraine-Europe: present and future of economic relations

Table of contents

INTRODUCTION 5

1. UKRAINIAN BUSINESS CLIMATE AND TRADE RELATIONS WITH THE EU 7

1.1. Major characteristics of the Ukrainian economy and business environment. 7 1.1.1. Ukraine key figures 7 1.1.2. Economic conditions in Ukraine 7 1.1.3. Ukraine’s economy strengths 8 1.1.4. Ukraine’s economy weaknesses 9 1.1.5. Ukraine’s Risk assessment 10 1.1.6. Business Climate 12 1.1.7. Foreign direct investments in Ukraine 13

1.2. The role of Ukrainian government in foreign business activities. 16 1.2.1. Issues affecting the business in Ukraine 16 1.2.2. Starting a Business in Ukraine 16 1.2.3. Custom procedures 17 1.2.4. Corruption 18 1.2.5. Court system 19 1.2.6. Technical barriers to trade 19 1.2.7. Taxes and VAT Refund 20 1.2.8. Land reforms 21 1.2.9. Foreign currency regulations 22

1.3. EU-Ukraine trade relations 24 1.3.1. Trade 24 1.3.2. EU foreign direct investments in Ukraine 25

2. MAIN ATTRACTIVE SECTORS ANALYSIS FOR EUROPEAN INVESTMENTS IN UKRAINE 27

2.1. Agribusiness 27 2.1.1. Ukraine’s agribusiness sector at a glance 27 2.1.2. Competition in the Ukrainian agricultural sector 30 2.1.3. Investments opportunities for EU companies 31

2.2. Biomass-based energy production sector 33 2.2.1. Global trends 33 2.2.2. Ukraine competitiveness in production of biomass-based energy 33 2.2.3. European investments in biomass-based energy sector in Ukraine 34

2.3 The National Projects as practical tools of FDI attraction 35

3. POTENTIAL AND RISK OF THE EUROPEAN –UKRAINIAN COLLABORATION 37

3.1. Possibility and goal of the EU-Ukraine Association Agreement 37 3.1.1. Background of the Association Agreement 37 3.1.2. Ukraine’s interests in the Association Agreement 38 3.1.3. European Union’s interests in the Association Agreement 39

3.1.4. European Union’s expectations from Ukraine 40

3.2. Political reality in Ukraine: its influence on the relations with the European Union. 42 3.2.1. Ukraine between East and West 42 3.2.2. The risk for Ukraine for signing an Association Agreement with the EU 43 3.2.3. The lack of democratic freedom 44

CONCLUSION 46

BIBLIOGRAPHY 49

5

Introduction

The topic of this thesis is ―Ukraine-Europe: present and future of economic relations‖. The

choice of the subject was driven by the actuality of current affairs between Ukraine and the

European Union and in particular the preparation for the signing in November 2013 of the

EU-Ukraine Association Agreement and its core element, the Deep and Comprehensive Free

Trade Agreement. Presently, the question is debated actively in the press of Ukraine and the

EU Commission respectively. The possible ratification of these agreements would signify

closer economic integration, which would lead to a new historical stage in the development

of the EU-Ukraine relations.

This study is motivated by main problematic, which comprises the question whether Ukraine

and the European Union can be reliable economic and business partners to each other. In the

pages that follow, it will be argued that their existing relations may evaluate into a

trustworthy alliance.

This research may also contribute to the EU companies willing to implement their businesses

in Ukraine as conveniences and precautions of doing business in Ukraine are accurately

framed in the theoretical part.

The solution to the problem is to determinate the credibility of actual economic and business

partnerships and investigate future potential of the collaboration between the European Union

and Ukraine. This work is focused on three directions:

Ukraine’s competitiveness features

The EU-Ukraine present relations and existing potential

Nearest future prospectivity

This research is divided into introduction, three chapters, conclusion and bibliography. Each

chapter is split into subchapters related to the section content.

To begin with, the first chapter ―Ukrainian business climate and trade relations with the EU‖

is the largest constituent of the thesis. It includes findings of major Ukraine’s economic

environment characteristics, internationally evaluated risk assessment and the government’s

importance in the business. Besides, the EU-Ukraine trade relations’ status is observed.

The second chapter ―Main attractive sectors analysis for European investment in Ukraine‖

begins by laying out the empirical dimensions of the research. On the assumption of deep

searching, it is understood that Ukraine is an emerging marketplace of compelling

opportunities to European investment. Two promising sectors, where the EU businesses can

generate profit, were identified.

The third chapter ―Potential and risk of the European-Ukrainian collaboration‖ sets out the

arguments in favor of further EU-Ukraine economic integration. Containing pioneering

aspects of cooperation, the EU-Ukraine Association Agreement is related to transition to a

high level economic partnership. The last chapter assesses the mutual interests of the EU and

Ukraine in deep economic cooperation. However, the ambitions of the EU and Ukraine to

approach economically and politically can end up due to unfinished democratic and judiciary

reforms on the part of the Ukrainian government and due to a strong outside pressure on

Ukraine from Russia.

6

Finally, this work underlines the progress of the EU’s foreign policy towards Ukraine, a

country of the Commonwealth Independent States accounting only twenty two years of

independence from the Soviet regime. The preference in these relations is given to the

priority fields, in particular trade and investment.

The EU is interested in improving the cooperation in Ukraine in the areas of justice, security

and home-affairs. Indeed, a country like Ukraine which has common borders with the

European Union represents a strong economical and security interest for the EU. On the other

hand, Ukraine has its own ambitious strategy of integration into the European economical,

legal and political spaces. Nevertheless, many domestic reforms remain necessary to improve

the business environment and develop strong economic ties with the European Union.

7

1. Ukrainian business climate and trade relations with the EU

1.1. Major characteristics of the Ukrainian economy and business

environment.

1.1.1. Ukraine key figures

Population: 47 732 079 (25th

in the world, population density – 80 p/km2)

Capital: Kiev

Major languages: Ukrainian (official), Russian

Major religion: Christianity

Life expectancy: 64 years (men), 75 years (women) (UN)

Monetary unit: 1 Hryvnya

Main exports: Military equipment, metals, pipes, machinery, petroleum products,

textiles, agricultural products.

Central Bank : National Bank of Ukraine (NBU)

President: Viktor Yanukovitch

Prime-minister: Mykola Azarov

Major cities: Kharkiv, Lviv, Dnepropetrovsk and Odessa.

Parliament: Verkhovna Rada.

Human Development Index (Rank): 78/187

GDP (current US$): 176.3 billion in 20121

1.1.2. Economic conditions in Ukraine

After years of important growth, Ukraine experienced in 2009 one of the worst recession in

Europe. The growth shrunked by 15% under the combined effects of the slowdown in the

economic activity, the diminution of the foreign funding and the drop in the world steel

demand. The country coped with a collapse of its industrial activity, a currency crisis, a rise

in inflation and a weakening of its banking sector leading Ukraine to call on the International

Monetary Fund (IMF). The country returned to a fragile growth in 2010 (3.7%) and in 2011

(+4.7%) due to a recovery of the foreign trade, the political stabilization of the country and

good harvests. Due to the recession in the euro zone that severely eroded its exportations,

Ukraine growth slowed in 2012 (2%). The government expects for 2013 a minimum growth

of 2.5% but the World Bank forecasts are much more modest (1%).

The Ukrainian economy is in a difficult period. In 2012, the external deficit widened, the

currency reserves are at their lowest level since 2010, the country access to credit is limited

whereas a 3.3 billion EUR debt expires in the end of 2013. The government priority is to

increase the social expenses to rise up the living standard of the population. The government

also continues the reforms necessary for an EU-Ukraine association agreement. Negotiations

are underway with IMF and they could lead to a new loan agreement of 15 billion USD, after

the suspension of the last agreement due the absence of significant progresses on the reforms

programme.

1 World Bank data

8

The economic crisis had important social consequences in Ukraine. The level of real wages

fell and the unemployment rate strongly increased, although it went down to 7.4% in 2012.

Table 1: Main Ukraine macroeconomic indicators

Economy Indicators 2009 2010 2011 2012 2013

(e)

GDP, current prices (billions USD) 117.23 136.42 163.42 176.24 181.6

GDP, constant prices (% change) -14.8 4.1 5.2 0.15 3.5

GDP per capita, current prices (USD) 2550 2980 3584 3877

(e)

4015

General government structural balance

(% GDP)

-2.1 -3.7 -2.8 -4.3 -4.4

General government gross debt (% GDP) 35.4 40.5 36.8 37.4 42.2

Inflation rate (%) 15.9 9.4 8.0 0.6 0.5

Unemployment rate (% total labor force) 8.8 8.1 7.9 8.0 8.2

Source: IMF - World Economic Outlook Database- http://www.imf.org/external/pubs/ft/weo/2013/01/weodata/weoselser.aspx?c=926&t=1, [consulted the 7th of august 2013]

Note: (e) Estimated data

1.1.3. Ukraine’s economy strengths

Ukraine is the second largest country in Europe, strategically located at the crossroads

between Europe, Russia and Central Asia. The country has access to the Black Sea through

the ports of Odessa and Sebastopol and it is a key energy transit country for Russian oil and

gas exports to Western Europe (see Figure 1).

Figure 1: EU countries and Ukraine geography

9

Once called the ―breadbasket of Europe‖, Ukraine has traditionally specialized in agriculture.

It has 324 784 square kilometers of arable land, the largest such area in Europe. In the 1990s,

agriculture accounted for around 20% of GDP but its share gradually declined to 9% of GDP

in 2012 following a reallocation of labor from agriculture into the industry and services

sectors. Agriculture still accounted for 25% of total exports in 2009 (WTO, 2010), and the

country is the world’s largest exporter of barley and the seventh largest exporter of wheat.

However, agriculture exports consist mainly of goods with a low degree of processing.

Ukraine is the world’s eighth-largest producer and fourth-largest exporter of steel, and the

fifth-largest exporter of nitrogen-based fertilizers. Industry valued added accounted for 30%

of GDP in 2010 (World Bank, 2011), while the share of total exports represented by fuels and

mining products was 12.3% and that accounted for by manufactured products was 62%

according to the WTO.

The labor force is highly skilled, thanks to the legacy of the rigorous and scientifically

oriented education system of the Soviet Union, and relatively inexpensive. For instance,

Ukraine as universal literacy and high general school enrolment: the combined gross of

enrolment ratio in education of both sexes was 90% in 2009, higher than those of Czech

Republic (83.4%) and Poland (87.7%). According to the World Bank (2011), female labor

participation is also higher than the average for Europe and Central Asia (see Figure 2).

Figure 2: Ukraine’s labor force has a high level of tertiary education

Source: World Bank (2011), World Bank Development Indicators, http://data.worldbank.org

1.1.4. Ukraine’s economy weaknesses

Ukraine economy is poorly diversified and highly depends on steel and imported gas prices.

Indeed, steel accounts for more than one third of total good exports. In July 2008, the IMF

estimated that a 10% decline in steel prices would slow Ukraine’s annualized GDP growth by

between ½ and ¾ of a percentage point over a full year (IMF, 2008).

0

10

20

30

40

50

Ukraine Europe and Central Asia (all income levels)

Europe and Central Asia (developing only)

Labour force with tertiary education (% total) 2005

10

Ukraine is also vulnerable to gas price increases from its main supplier which is Russia. For

example in 2006, Ukraine had to pay almost twice the old price for Russian gas after Russia

stopped the gas supplies. However, Ukraine is trying to rectify this situation by switching

towards greater use of local coal.

Besides, the political insecurity makes it difficult to apply a consistent economic policy,

macroeconomic stability being a prerequisite to attracting foreign investment and switching

to a long term sustainable growth path.

Another main weakness of Ukraine is its banking system. Deposits from firms and

households as well as lending to the private sector are very tiny even when compared to very

poor countries. Empirical analyses demonstrate a strong positive link between the functioning

of the financial system and long-run growth (Ross Levine, 1997). In fact, empirical evidence

shows that the development of the financial system is a precursor and a necessary condition

for sustained growth and economic transformation, especially in transition economies like

Ukraine.

1.1.5. Ukraine’s Risk assessment

In a competitive commercial environment, payment facilities are a decisive factor in carrying

off a contract. It’s therefore essential for exporters to evaluate the Ukraine political and

commercial risks. Political risks include wars, riots, foreign currency shortages or arbitrary

government decisions. The commercial risk can be a non-payment after a buyer's arbitrary

decisions or bankruptcy.

Ukrainian economy is evaluated by several international rating agencies, well-known credit

insurers and foreign financial institutions in order to estimate of the average credit risk on

Ukraine’s businesses. Among them, we will consider two European credit insurers: the Office

national du ducroire (ONDD), the Belgian public credit insurer and Coface, a French

company specializing in export credit insurance.

According to the point of view of ONDD: ―The Ukrainian economy overheated and the

credit boom at home was becoming ever more financed by means of foreign debt. High

external financing needs pushed the country towards the extreme need of international help,

which was the only one option left.‖2 ONDD - Country risks synthesizing chart was made of

risk assessment for Ukraine. The relevant mark is given to two directions: export transactions

and direct investments (see Figure 3 below).

2 Stricter cover terms for medium and long term transactions on the Ukraine. ONDD. Retrieved from:

http://www.ondd.be

11

Figure 3: Ukraine’s risk assessment

Source: ONDD (July 2013), http://www.ondd.be

As far as Coface is concerned, they have a ranking system which is made up from seven-

levels. In ascending order of risk, these are: A1, A2, A3, A4, B, C and D. The rank attributed

to Ukraine in 2013 was: ―D‖ for the Country Risk Assessment, ―D‖ standing for high risk

profile of the economic and political environment, very bad payment record.3

Several factors explain these bad evaluations from ONDD, Coface and others. First of all,

there is a degradation of the economical situation that should result in a drop in economic

growth in 2013. In Q1 2013, the GDP decreased (-1.3% vs. Q1 2012), confirming the

recession observed since mid 2012. The Ukrainian economy suffers from a weak external

demand taking into account the bad economical performances of its partners (Euro zone,

Russia and other CEI countries) that should perpetuate a great part of the year 2013.

The private consumption is likely to be penalized by the rise in inflation expected in 2013

(notably the food price increase). This inflation should be increased by gas tariff increases

demanded by the IMF as a counter part of a new loan.

Another reason is the fragility of the public finances and the balance of payments. The public

expenses slightly increase, reaching 52% of the GDP in the Q1 2013 (46% in 2012).

The slowdown of the exportations and the surge in the imported gas prices largely

contributed to the rise in the deficit in 2012 and this deterioration should continue in 2013.

There is a high risk of devaluation in 2013 that would a negative impact on the household

consumption but also huge repercussions on the sovereign default and the risk of bank

default. Whatever the strategy chosen by the government in 2013 (rise in gas prices and/or

devaluation), the risk of social dissatisfaction is high.

3 Risk countries. Economic studies. Ukraine. Coface 2012. Retrieved from : http://www.coface.fr

12

On the political aspect, the Party of Regions from the president Viktor Yanoukovitch won the

legislative elections of October 2012. However, the main opposition parties didn’t recognize

this victory, accusing the Party of Regions of fraud. The continuing detention of Julia

Timoshenko and the president’s will to reinforce the links with Russia participate in the rising

dissatisfaction of the western part of the country, which is largely in favor of a rapprochement

with the European Union.

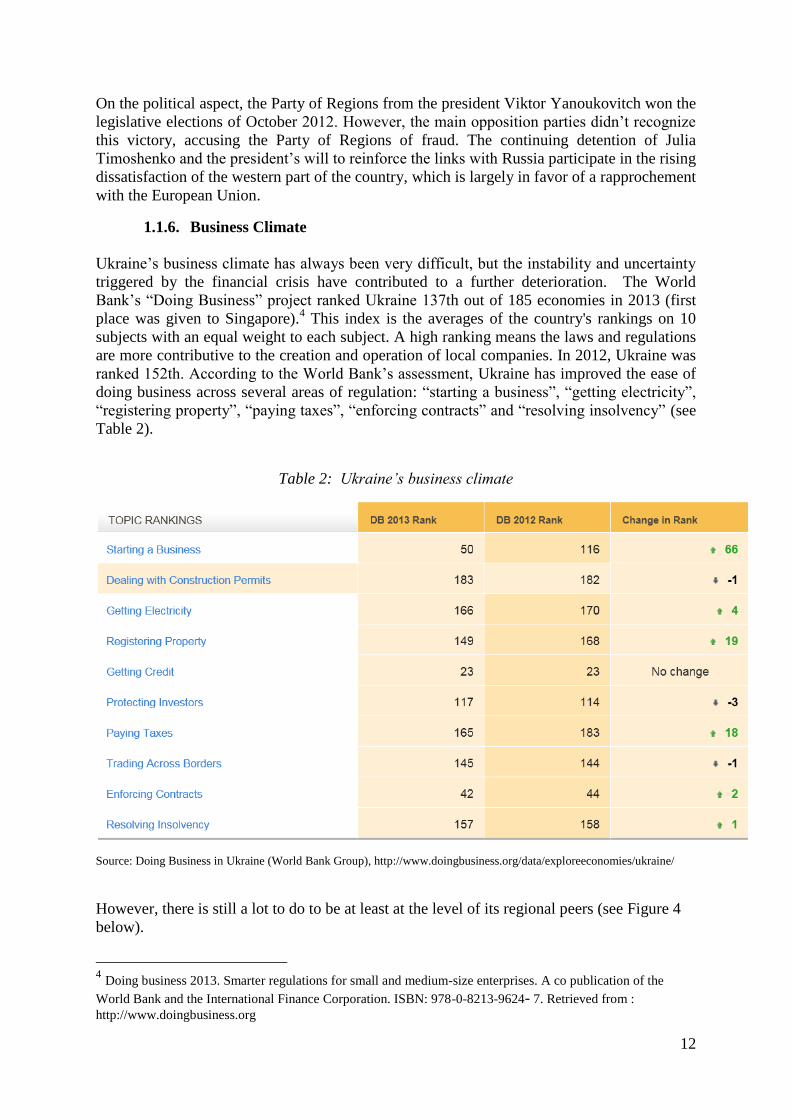

1.1.6. Business Climate

Ukraine’s business climate has always been very difficult, but the instability and uncertainty

triggered by the financial crisis have contributed to a further deterioration. The World

Bank’s ―Doing Business‖ project ranked Ukraine 137th out of 185 economies in 2013 (first

place was given to Singapore).4 This index is the averages of the country's rankings on 10

subjects with an equal weight to each subject. A high ranking means the laws and regulations

are more contributive to the creation and operation of local companies. In 2012, Ukraine was

ranked 152th. According to the World Bank’s assessment, Ukraine has improved the ease of

doing business across several areas of regulation: ―starting a business‖, ―getting electricity‖,

―registering property‖, ―paying taxes‖, ―enforcing contracts‖ and ―resolving insolvency‖ (see

Table 2).

Table 2: Ukraine’s business climate

Source: Doing Business in Ukraine (World Bank Group), http://www.doingbusiness.org/data/exploreeconomies/ukraine/

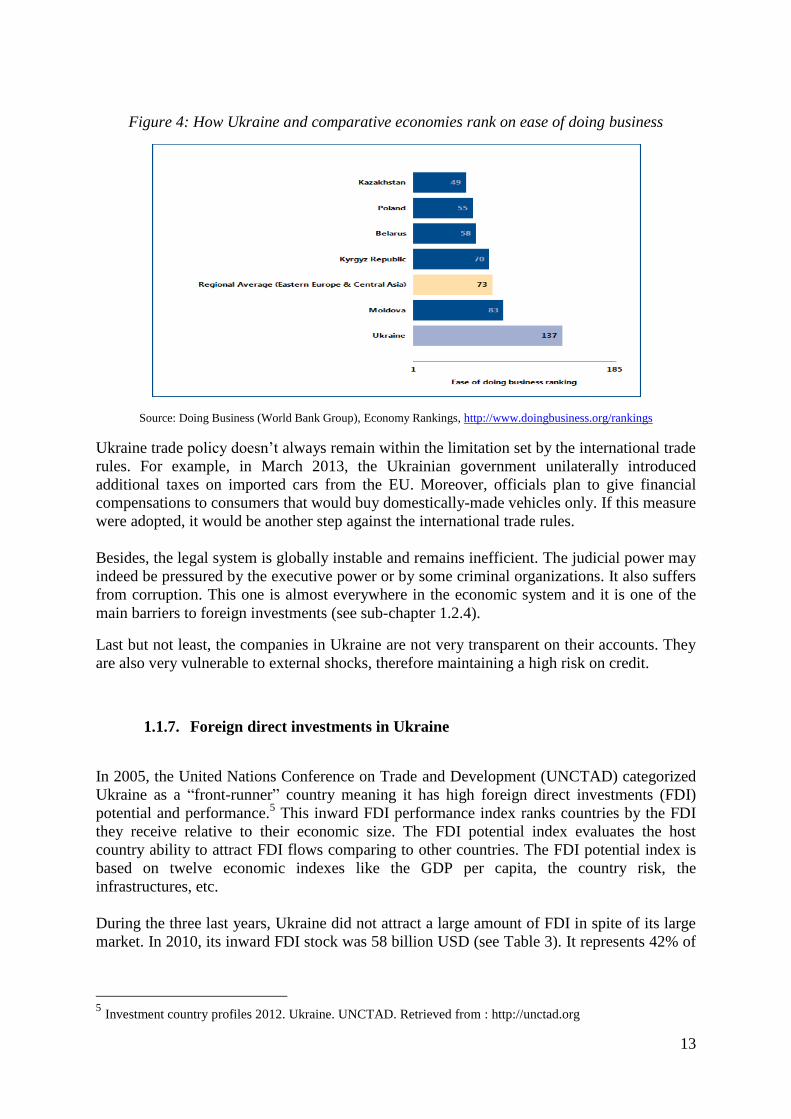

However, there is still a lot to do to be at least at the level of its regional peers (see Figure 4

below).

4 Doing business 2013. Smarter regulations for small and medium-size enterprises. A co publication of the

World Bank and the International Finance Corporation. ISBN: 978-0-8213-9624- 7. Retrieved from :

http://www.doingbusiness.org

13

Figure 4: How Ukraine and comparative economies rank on ease of doing business

Source: Doing Business (World Bank Group), Economy Rankings, http://www.doingbusiness.org/rankings

Ukraine trade policy doesn’t always remain within the limitation set by the international trade

rules. For example, in March 2013, the Ukrainian government unilaterally introduced

additional taxes on imported cars from the EU. Moreover, officials plan to give financial

compensations to consumers that would buy domestically-made vehicles only. If this measure

were adopted, it would be another step against the international trade rules.

Besides, the legal system is globally instable and remains inefficient. The judicial power may

indeed be pressured by the executive power or by some criminal organizations. It also suffers

from corruption. This one is almost everywhere in the economic system and it is one of the

main barriers to foreign investments (see sub-chapter 1.2.4).

Last but not least, the companies in Ukraine are not very transparent on their accounts. They

are also very vulnerable to external shocks, therefore maintaining a high risk on credit.

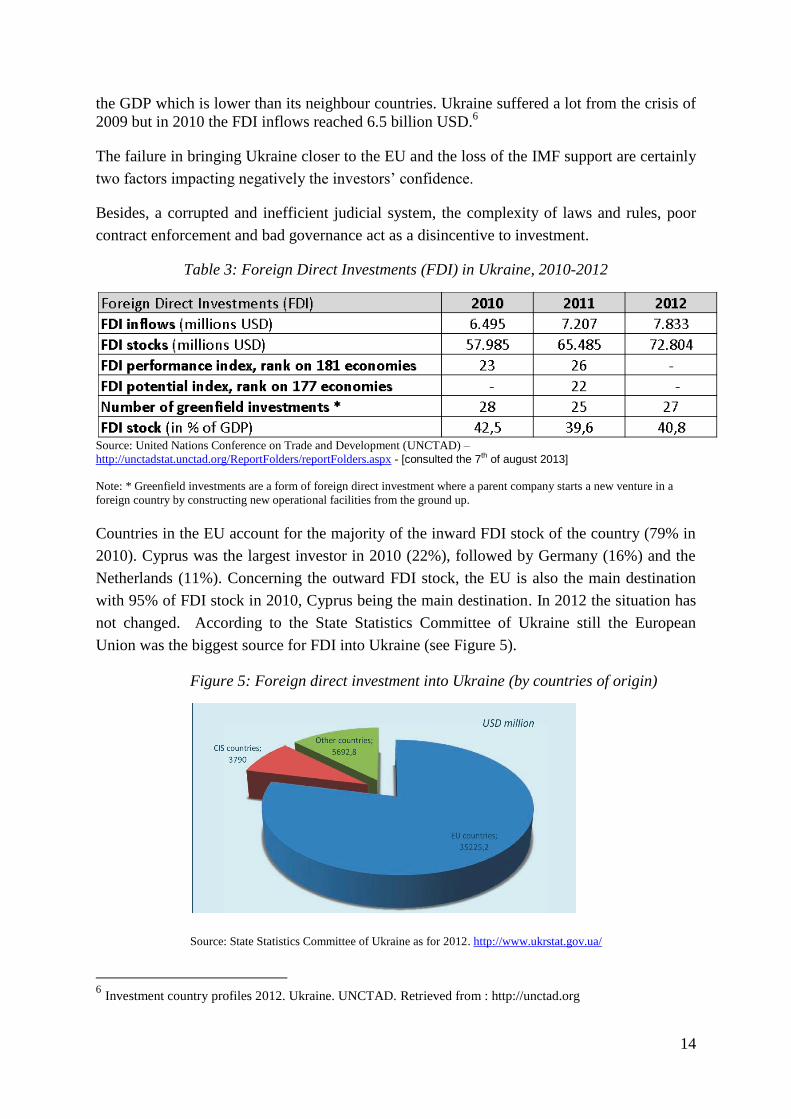

1.1.7. Foreign direct investments in Ukraine

In 2005, the United Nations Conference on Trade and Development (UNCTAD) categorized

Ukraine as a ―front-runner‖ country meaning it has high foreign direct investments (FDI)

potential and performance.5 This inward FDI performance index ranks countries by the FDI

they receive relative to their economic size. The FDI potential index evaluates the host

country ability to attract FDI flows comparing to other countries. The FDI potential index is

based on twelve economic indexes like the GDP per capita, the country risk, the

infrastructures, etc.

During the three last years, Ukraine did not attract a large amount of FDI in spite of its large

market. In 2010, its inward FDI stock was 58 billion USD (see Table 3). It represents 42% of

5 Investment country profiles 2012. Ukraine. UNCTAD. Retrieved from : http://unctad.org

14

the GDP which is lower than its neighbour countries. Ukraine suffered a lot from the crisis of

2009 but in 2010 the FDI inflows reached 6.5 billion USD.6

The failure in bringing Ukraine closer to the EU and the loss of the IMF support are certainly

two factors impacting negatively the investors’ confidence.

Besides, a corrupted and inefficient judicial system, the complexity of laws and rules, poor

contract enforcement and bad governance act as a disincentive to investment.

Table 3: Foreign Direct Investments (FDI) in Ukraine, 2010-2012

Source: United Nations Conference on Trade and Development (UNCTAD) –

http://unctadstat.unctad.org/ReportFolders/reportFolders.aspx - [consulted the 7th of august 2013]

Note: * Greenfield investments are a form of foreign direct investment where a parent company starts a new venture in a

foreign country by constructing new operational facilities from the ground up.

Countries in the EU account for the majority of the inward FDI stock of the country (79% in

2010). Cyprus was the largest investor in 2010 (22%), followed by Germany (16%) and the

Netherlands (11%). Concerning the outward FDI stock, the EU is also the main destination

with 95% of FDI stock in 2010, Cyprus being the main destination. In 2012 the situation has

not changed. According to the State Statistics Committee of Ukraine still the European

Union was the biggest source for FDI into Ukraine (see Figure 5).

Figure 5: Foreign direct investment into Ukraine (by countries of origin)

Source: State Statistics Committee of Ukraine as for 2012. http://www.ukrstat.gov.ua/

6 Investment country profiles 2012. Ukraine. UNCTAD. Retrieved from : http://unctad.org

15

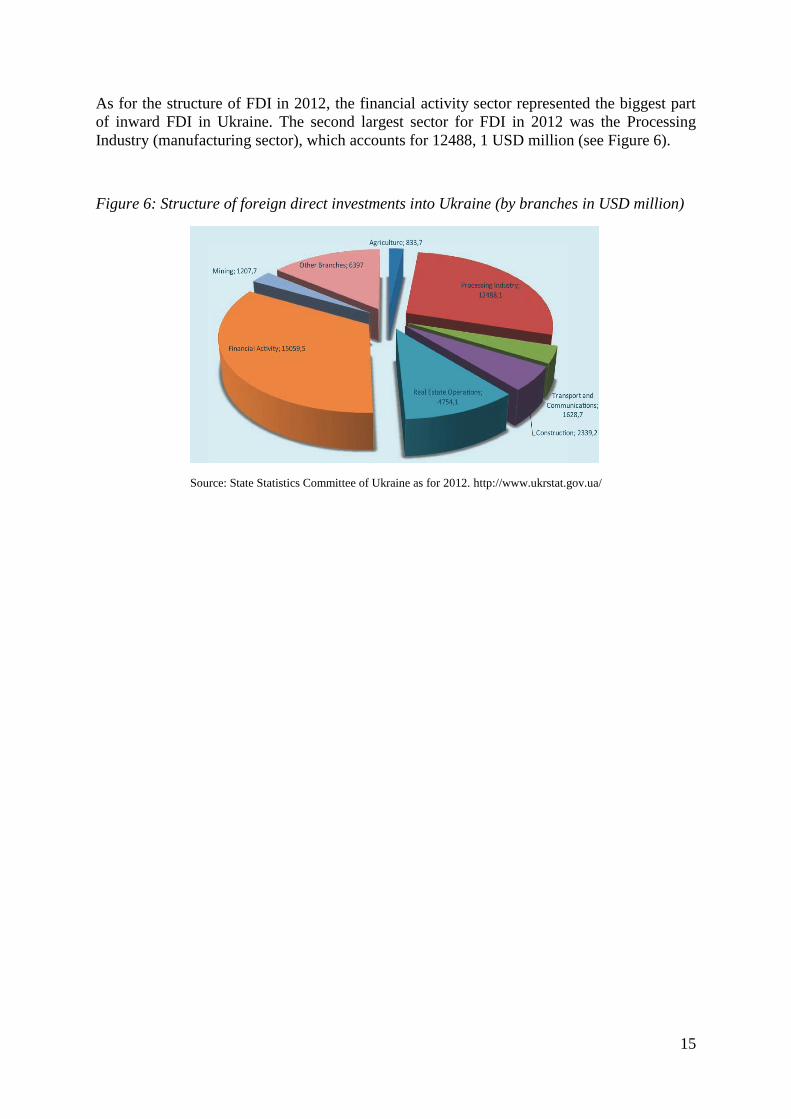

As for the structure of FDI in 2012, the financial activity sector represented the biggest part

of inward FDI in Ukraine. The second largest sector for FDI in 2012 was the Processing

Industry (manufacturing sector), which accounts for 12488, 1 USD million (see Figure 6).

Figure 6: Structure of foreign direct investments into Ukraine (by branches in USD million)

Source: State Statistics Committee of Ukraine as for 2012. http://www.ukrstat.gov.ua/

16

1.2. The role of Ukrainian government in foreign business activities.

1.2.1. Issues affecting the business in Ukraine

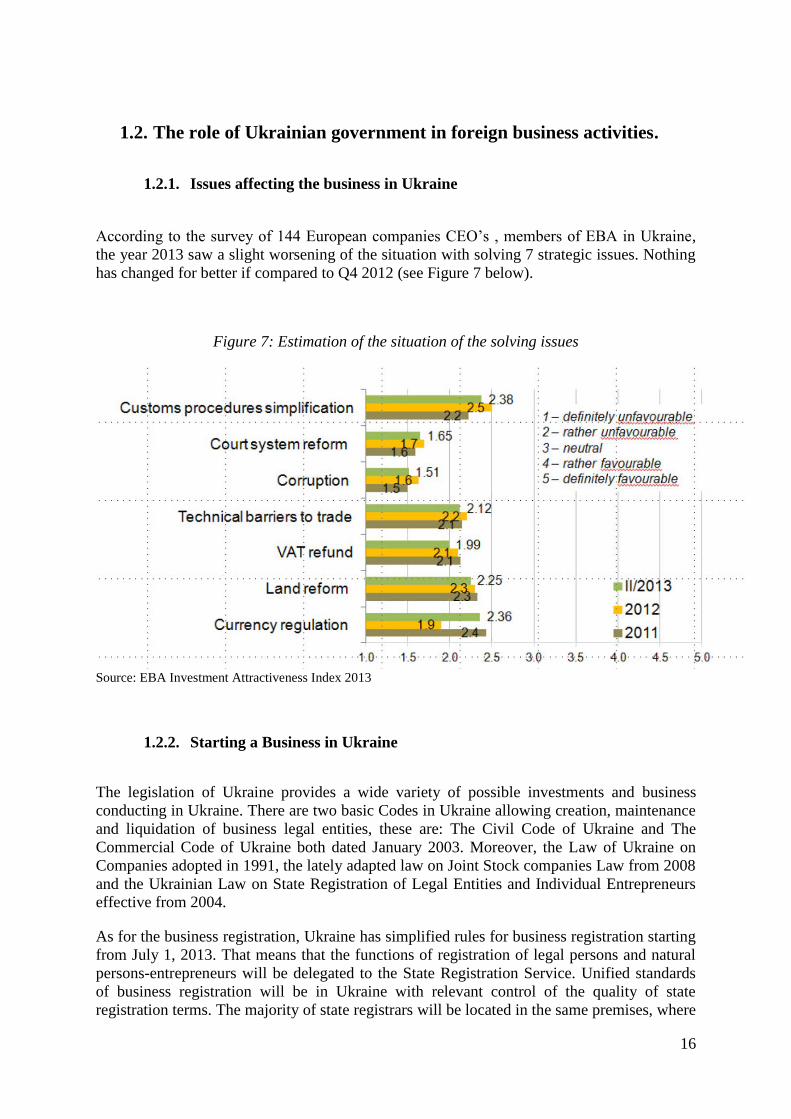

According to the survey of 144 European companies CEO’s , members of EBA in Ukraine,

the year 2013 saw a slight worsening of the situation with solving 7 strategic issues. Nothing

has changed for better if compared to Q4 2012 (see Figure 7 below).

Figure 7: Estimation of the situation of the solving issues

Source: EBA Investment Attractiveness Index 2013

1.2.2. Starting a Business in Ukraine

The legislation of Ukraine provides a wide variety of possible investments and business

conducting in Ukraine. There are two basic Codes in Ukraine allowing creation, maintenance

and liquidation of business legal entities, these are: The Civil Code of Ukraine and The

Commercial Code of Ukraine both dated January 2003. Moreover, the Law of Ukraine on

Companies adopted in 1991, the lately adapted law on Joint Stock companies Law from 2008

and the Ukrainian Law on State Registration of Legal Entities and Individual Entrepreneurs

effective from 2004.

As for the business registration, Ukraine has simplified rules for business registration starting

from July 1, 2013. That means that the functions of registration of legal persons and natural

persons-entrepreneurs will be delegated to the State Registration Service. Unified standards

of business registration will be in Ukraine with relevant control of the quality of state

registration terms. The majority of state registrars will be located in the same premises, where

17

people got accustomed to see them.

Ukrainian government has a strong influence on the foreign business activities, at the point of

conducting business in Ukraine; foreign companies have to face a number of obstacles such

as:

custom procedures

corruption

court system

technical barriers

taxes/VAT refund

land reforms

currency regulation

1.2.3. Custom procedures

The quality of customs operations and simple customs clearance of goods are an inevitable

part of a country's trade potential. Adapting Ukraine’s customs laws is a main goal for the

Ukrainian state so that its legislation is aligned with the EU’s. Therefore, in March 2012, the

Ukrainian parliament (Verkhovna Rada) adopted the new Customs code of Ukraine. The

main improvements in the custom procedures compared to the previous legislation are

detailed below:

the customs clearance becomes possible at any customs office, regardless of the

importer's place of registration (before, entities had to ask for permission for customs

clearance in a customs office different from the one they used to register);

there is now the possibility to amend customs declarations within three years after

customs clearance without penalties;

goods can be re-exported by non-residents if there is a failure to fulfill contractual

commitment and customs duty will be reimbursed;

there is an imposed four hours time limit for customs clearance procedures

(previously customs clearance had to be finished within a day, but in reality it took

more time);

the possibility of relevant experts and professionals to participate in the procedure of

customs is provided for;

a list of documents to be submitted for customs clearance is established (at the level

of the Code);

Full introduction of e-declarations by the end of 2013;

In case there are different interpretations of laws, a decision will be taken in favor of

the importer.

The new Customs code has brought some improvements but customs treatment of royalties

remains unclear and international investor’s community underlines that the Customs Code is

18

still far from the standards of WTO7. Notwithstanding the improvements, further positive

changes could be made in the following areas:

implementation of the WTO’s Customs Valuation Decisions;

responsibility for customs offences (the current fines are very high);

introduction of centralized customs clearance;

bringing foreign exchange control in line with new customs regulations.

1.2.4. Corruption

One of the biggest threats to the foreign business activities in Ukraine is the systemic

corruption. In May 2011 TORO, the Transparency International national contact group in

Ukraine, published an assessment of the institutions in the country, which concluded:

Corruption in Ukraine is a systemic problem existing across the board and at all

levels of public administration. Both petty and grand scale corruption are flourishing.

Among the institutions which are perceived by the public to be highly corrupt are

political parties, legislature, police, public officials and the judiciary. Ukrainian

society can be characterized as a society with a high tolerance for corrupt practices. 8

In particular, the corruption at the customs service is a major problem for the development of

foreign business activities. The custom authorities have been enjoying the right to

independently execute court rulings at the borders. In most of the cases, the EU companies

have to struggle against the unauthorized confiscation of some part of the goods upon the

arrival to the Ukrainian borders. The local official customs officers then demand a bribe to

allow the further circulation of the goods on the Ukrainian territory.

Other possible corruptions are linked with the every-day activities like the simple

registration-licensing to establish a plant or the opening of a restaurant or a shop. This may

include acquiring the permit and getting an approval from the sanitizing commission. For

example, the foreign companies are obliged to pass the administration bureaucratic offices,

most of them would propose an extra fee for their services to facilitate their life and save

time.

Ukraine presidents, the former one Viktor Yuschenko in 2005 and the current one Viktor

Yanuckovich in 2010 and 2012 made fighting corruption the top priority of their

administration. Under the pressure of the EU authorities and the IMF, the government made

steps forward to simplify the rules of conducting business in Ukraine for European

companies and not only European ones.

Anti-corruption efforts were notably held in 2010, when the public organization Anti-

Corruption Council of Ukraine (ACCU) was established. The purpose of the ACCU is to

7 Interfax-Ukraine (24 May, 2012). American Chamber of Commerce: New Customs Code promotes relaxation

of custom procedures. The Kyiv post. Retrieved from: http://www.kyivpost.com/content/politics/american-

chamber-of-commerce-new-customs-code-to-p-1-128160.html 8 Transparency International. Ukraine 2011. Retrieved from:

http://www.transparency.org/whatwedo/nisarticle/ukraine_2011

19

ensure transparency among Ukraine’s public central and local authorities.9 It has been

followed by the new Customs Code of Ukraine in April 2012 (see chapter above) with also

the purpose of reducing the level of corruption.

Despite of these governmental efforts, there is still a lot of area for improvements. Indeed,

Transparency International organization gave in 2012 a Corruption Perceptions Index rank of

144/175 and a score of 26/100. The Corruption Perceptions Index ranks countries based on

how corrupt a country’s public sector is perceived to be. Scores range from 0 (highly corrupt)

to 100 (very clean). 10

1.2.5. Court system

It has been only recently that court system has begun the transformation reforms. The Law of

Ukraine No. 2453-VI ―On the Court System and the Status of Judges‖ provided a new

judicial system of Ukraine.

In Ukraine, the constitutional court and the system of general jurisdiction courts are based on

the principles of territoriality. Generally speaking, the judicial system comprises four levels

of courts as follows:

Local courts of general jurisdiction (combining criminal and civil jurisdiction);

Appeal courts

High courts with specialized jurisdiction

The Supreme Court covering all cases11

.

The Highest Commercial Court of Ukraine is the supreme body for resolving economic

disputes but for the foreign entities it also advised to apply for the International Commercial

Arbitration Court at the Ukrainian Chamber of Commerce and Industry. It can be very

efficient to settle commercial disputes.

However, the judicial system of Ukraine is not very predictable for the businesses and system

of commercial courts is not always fair. It is also very well-known for being corrupted12

.

Therefore, both foreign and local firms don’t trust the judicial system in business matters as it

was underlined by the US Department of State in 201213

.

1.2.6. Technical barriers to trade

Technical Barriers to Trade (TBT) between the EU and Ukraine are technical regulations

referred usually to safety issues and national standards of Ukraine applied by the government

and its officials to ban the import of goods coming from the EU member states. In many

cases, the government is using the technical barriers to protect the local manufactures and

judge the foreign goods as unsuitable for the Ukrainian market. Until a new national

9 United Nations Office on Drugs and Crime. Anti-Corruption Council of Ukraine. Retrieved from :

http://www.unodc.org/ngo/showSingleDetailed.do?req_org_uid=21953 10

Transparency International: Corruption by country. Retrieved from:

http://www.transparency.org/country#UKR_DataResearch 11

Government portal of Ukraine : Judicial power. Retrieved from :

http://www.kmu.gov.ua/control/en/publish/article?art_id=246406533&cat_id=246405235 12

Klaus Schwab. World Economic Forum. Global Competitiveness report 2012-2013. Retrieved from :

http://www.weforum.org/issues/global-competitiveness 13

US Department of State. 2012 Investment Climate Statement – Ukraine. Retrieved from :

http://www.state.gov/e/eb/rls/othr/ics/2012/191257.htm

20

standards body is created, the standards adoption is under the responsibility of the Ministry

for Economic Development and Trade.

Unfortunately, regardless the standardization, Ukraine still remains in its transition state from

a soviet standardization model to an EU standardization model. In the soviet one, standards

are obligatory imposing a bureaucratic burden on the manufacturers. In the EU, standards are

voluntary.

In 2009, the EU launched a Sector Policy Support Program worth of 39 million Euros with an

end date in December 2013 in order to facilitate trade between EU member states and

Ukraine. The goal is also to eliminate trade barriers including the modernization of the

institutional framework for quality assurance. 14

This way, Ukraine will progressively adapt

its technical regulations and standards to those of the EU.

Due to its obligations as a member of the WTO and its responsibilities indicated on the WTO

Agreement on Technical Barriers to Trade, the Ukrainian Government adopted in 2012 the

Amendments which simplified the procedures for introduction of the products into Ukrainian

market by removing the obligation to register the declaration of conformity for the producers.

1.2.7. Taxes and VAT Refund

The hostile corporation tax legislation used to be the main cause explaining why international

companies refused to go to the Ukrainian market. The vote of the first Tax Code of Ukraine

in December 2010 was therefore a major event. It brought together Ukrainian tax legislation

in its entirety. The Code adjusted rates and benefits, and also the process of tax imposition.

The Prime-Minister of Ukraine, Mykola Azarov, while introducing the draft version of the

Code said: ―A new Tax Code in Ukraine will create one of the most attractive investment

regimes in Europe. We will set low taxes, probably the lowest taxes in Europe.”15

Among the reforms, one concerned the corporate income tax (CIT) rate that has been

gradually reduced from 25% in 2011 to 19% in 2013. A last rate decrease is planned for 2014

(16%). The Tax Code also introduced favorable regulations for a number of industries. For

example, until 1 January 2021, hotels as well as electricity and light industry companies,

shipbuilding and aircraft companies are simply exempted from CIT. Besides, until 1 January

2016, companies with an income not exceeding UAH 3 million per year, and whose staff

numbers not more than 25 employees, are not subject to CIT at all. There are a number of

other benefits and privileges, which are given to companies, which provide services in the

area of information technology.

The timely value-added tax (VAT) recovery is also a major issue. It’s one of the reasons that

discourage foreign companies from conducting business in Ukraine. In reality, with the

current procedure, it is almost impossible to get a VAT refund in Ukraine. In order to better

regulate the issue of VAT refunds, the Tax Code obliges the Ukrainian state to pay interest

14

EU Cooperation News. (2 April 2013) . Interview on legal and product safety with Stefanos Ioakeimidis,

Team Leader of an EU-funded project and with Dmytro Lutsenko, Legal Expert, Opening doors of EU-Ukraine

Trade. Newsletter of the delegation of the European Union to Ukraine. Retrieved

from: http://euukrainecoop.com/2013/02/04/eu-ukraine-trade/ 15

Interfax-Ukraine (3 September, 2010). Azarov: Ukraine to have lowest taxes in Europe. The Kyiv post .

Retrieved from: http://www.kyivpost.com/content/business/azarov-ukraine-to-have-lowest-taxes-in-europe-

80962.html

21

for the late payment of refunds. In Ukraine the VAT rate is 20% and it is planned to decrease

it to 17% by 2014.16

Nevertheless, it is not enough to have a good legislation. Powerful institutions are also

necessary for the laws to work properly. In fact, Ukraine still copes with strong difficulties

for VAT collection and refund. A survey done by the American Chamber of Commerce in

Ukraine revealed that among its 26 member companies, the cumulative VAT arrears reached

almost UAH 3.4 billion in February 2012. More than half of this total was composed of

overdue VAT.17

The European Union is aware of what the European companies have to tackle with in

Ukraine and some failed commitments of the Ukrainian government. José Manuel Pinto

Teixeira, Ambassador, Head of Delegation of the European Union to Ukraine on conducting

business in Ukraine said in July 2012:

Taxation difficulties, problematic VAT refund and tax losses carry forward as well as

pressure from state authorities (17%) still have the lead. Coming up next are

complaints over unstable political course and court system in Ukraine, hot-off-the-

press Law on Personal Data Protection, and destructive corruption (14%).

European businesses and members of EBA have not perceived any real improvements

in the business and investment climate in Ukraine in recent months. I am not

surprised but I find it disappointing that so many issues still remain unresolved,

despite frequent calls for action from the EU and the EBA, and commitments made by

the Ukrainian government to improve the business climate. 18

The government should tackle with the tax reforms, as they are part of challenge that serves

to create a business friendly environment both for Ukrainian entrepreneurs and for foreign

investors. A key undertaking is the effort to weed out regulations while encouraging growth

and discouraging corruption.

1.2.8. Land reforms

Since many years the land reform is a subject of discussion in Ukraine. After the

independence the first round of farm reforms initiated privatization of land. In 1992, all land

were owned by the state whereas in 2013, the state owned only 48.9% of land and 51% of

land were owned by private entities19

.

In the end of 2011, the primary draft bill on land market was voted. It precised the market

organization and its way of operating. The very important issue in the land reform principle is

avoiding the monopolization on the market by imposing the limitation of land ownership at

100 hectares regardless of location. The development of new land reforms is still an in-work-

16

Jaroslawa Z. Johnson and Anna Iakubenko. (06.11.2011) Ukraine adopts first Tax Code. Lexology. Retrieved

from: http://www.lexology.com/library/detail.aspx?g=41644abe-f8fb-42a6-8063-3d572535b8dc

17 The American Chamber of Commerce in Ukraine. Reforming the Ukrainian Tax System – Important for the

Country’s Future Prosperity. Retrieved from: http://blog.chamber.ua/2012/02/reforming-the-ukrainian-tax-

system-important-for-the-countrys-future-prosperity/ 18

European Business Association Press-release (10.07.2012). Ukraine’s Attractiveness: Fair to Middling.

Retrieved from: http://www.eba.com.ua/en/press-room 19

ForUm. Land reform: to be or not to be? (11.06.2013). Retrieved from:

http://en.for-ua.com/analytics/2013/06/11/134501.html

22

process nowadays. For example, in 2012, the parliament voted some changes to the Land

Code and foreign companies were allowed to buy Ukrainian lands.

However, even if the government recognizes the necessity of land reforms, unfortunately for

the business entities, the second reading of this document is still frozen due to various

political forces. The President Viktor Yuschenko declared in April 2013: « We want to carry

out the reform without infringing the interests of land plot owners. This is the main issue ».20

If the Ukrainian government finally passes the reform, in some years, Ukraine may have a

real competitive land market. Then, it will maybe attract foreign investments into the

agribusiness industry.

1.2.9. Foreign currency regulations

There are numerous currency control difficulties faced by foreign investors in Ukraine.

Foreign currency operations are ruled by the 1993 Cabinet of Ministers decree, On the

System of Currency Regulation and Currency Control. They also follow numerous

implementation rules created by the National Bank of Ukraine (NBU). The key issues

regarding Ukraine’s current exchange control regulation are that:

Payments under foreign trade contracts between resident and a non-resident should be

in foreign currency only;

Payments in foreign currency between residents of Ukraine are forbidden (a specific

license is required);

Salaries to Ukrainian staff must be paid un UAH currency (but expatriate employees

can be paid in hard currency);

Foreign loans must be registered with the National Bank of Ukraine before funds are

transferred to Ukraine. A maximum interest rate may be applied to foreign currency

loans obtained from non residents;

If a Ukrainian company makes an advance payment to a foreign company, this

company must realize the actual importation of the goods or services concerned

within 180 days following the date of the advance payment. This 180-day period may

be extended only based on an individual permission granted by the Ministry of

Economic Development and Trade. The non respect of this 180-day period may lead

to important fines for the Ukrainian company;

Payments by Ukrainian companies for services given by nonresident for amounts

exceeding EUR 100,000 (annually) require confirmation from the Foreign Markets

Monitoring Center that the fee for the services doesn’t not exceed market prices.

Otherwise, the bank will disallow the transfer.

On November 2012, the Parliament of Ukraine has increased control over foreign currency

circulation in Ukraine. The National Bank of Ukraine introduced a temporary requirement on

mandatory conversion of a foreign currency transferred to Ukraine from abroad. The

Resolutions # 475 and # 479 were adopted that modify the settlement periods under export

and/or import agreements and put on a obligatory necessity for the foreign businesses to

20

Interfax-Ukraine (3 September, 2010). Viktor Yanukovich: Interests of land plot owners should be

considered in land reform, Yanuckovich says. Kyiv Post. Retrieved from:

23

convert the foreign currency revenues into national currency Hryvnia.21

These regulations

impact eventually all international businesses as well as individuals that receive foreign

currency from abroad.

21

Adam Mycyk, Inna Antipova (28 November 2012). Ukraine changes to foreign currency control regulation.

Lexology. Retrieved from : http://www.lexology.com/library/detail.aspx?g=4361bf46-4849-456b-8de0-

1019b5506d71

24

1.3. EU-Ukraine trade relations

1.3.1. Trade

The trade relations between EU and Ukraine really started in 1998 when a Partnership and

Cooperation Agreement entered in the force. It provides a comprehensive and ambitious

framework for cooperation between the EU and Ukraine, in all key areas of reform. Ukraine

is a priority partner country within the European Neighborhood Policy and the Eastern

Partnership.22

In 2012 Ukraine was the EU’s 22nd largest trading partner and the 19th largest export market

in value (23.79 million Euros).

In 2012, the EU was Ukraine’s first largest trade partner with 31% of the total trade with the

world. 21.8% of Ukrainian exports of goods went to the EU and 39.9% of import of goods

came from the EU.

Ukraine mainly exports iron, steel, mining products, cereals, and electric machinery. The

main goods the EU exports to Ukraine are machinery and transport equipment, chemicals,

textile and clothing and agricultural products (see Figure 8).

Figure 8: EU27 Merchandise Trade with Ukraine by product (2012)

Source: Eurostat (Comext; Statistical Regime 4)

Ukrainian exports to the EU are to a large extent already liberalised thanks to the Generalised

System of Preferences (GSP), granted by the EU to Ukraine since 1993. In 2011, total

preferential exports to the EU under GSP reached a level of 72.2% of the eligible product.

Preferential imports to the EU from Ukraine include machinery and mechanical appliances,

plants, oils, base metals, chemicals and textiles.

22

EU around the Globe. Countries. Ukraine. European Union External Action.

Retrieved from: http://www.eeas.europa.eu/ukraine/

25

Figure 9: EU trade in goods balance with Ukraine 2010-2012

Source: Eurostat (Comext; Statistical Regime 4)

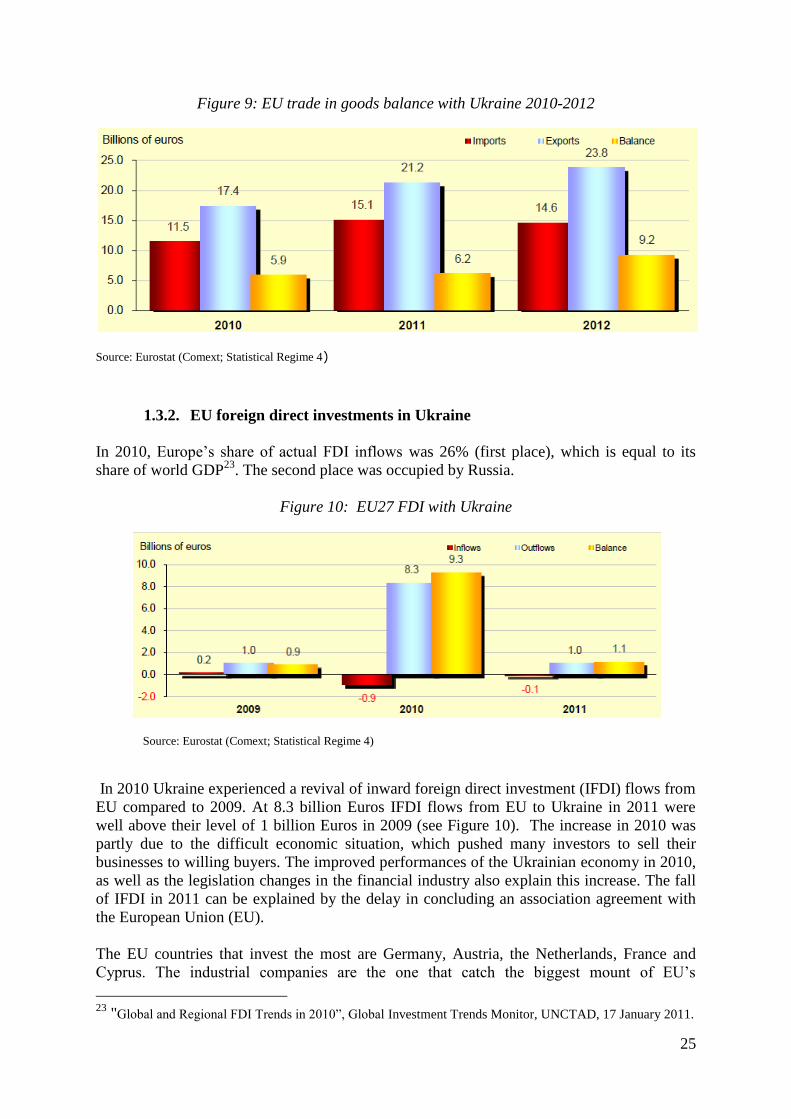

1.3.2. EU foreign direct investments in Ukraine

In 2010, Europe’s share of actual FDI inflows was 26% (first place), which is equal to its

share of world GDP23

. The second place was occupied by Russia.

Figure 10: EU27 FDI with Ukraine

Source: Eurostat (Comext; Statistical Regime 4)

In 2010 Ukraine experienced a revival of inward foreign direct investment (IFDI) flows from

EU compared to 2009. At 8.3 billion Euros IFDI flows from EU to Ukraine in 2011 were

well above their level of 1 billion Euros in 2009 (see Figure 10). The increase in 2010 was

partly due to the difficult economic situation, which pushed many investors to sell their

businesses to willing buyers. The improved performances of the Ukrainian economy in 2010,

as well as the legislation changes in the financial industry also explain this increase. The fall

of IFDI in 2011 can be explained by the delay in concluding an association agreement with

the European Union (EU).

The EU countries that invest the most are Germany, Austria, the Netherlands, France and

Cyprus. The industrial companies are the one that catch the biggest mount of EU’s

23

"Global and Regional FDI Trends in 2010‖, Global Investment Trends Monitor, UNCTAD, 17 January 2011.

26

investments (34%). Financial institutions receive 32.4% of FDI. Then we can find the

companies engaged in real estate transactions, engineering, trade, vehicle repair, production

of household gods and personal goods.24

24

Worldwide News Ukraine: EU’s Direct Investments to Ukraine Grow 19.3 Percent Retrieved from:

http://wnu-ukraine.com/news/economy-business/?id=707

27

2. Main attractive sectors analysis for European investments in

Ukraine

2.1. Agribusiness

Agribusiness represents a comprehensive value chain that covers all aspects of agricultural

production (farming, seed, crop production, post-harvest handling and other agricultural

inputs), processing and distribution. World production, consumption and trade of agricultural

products are expected to increase sharply over the coming decade. Foreign agro-food

companies investing in emerging economies could play a significant role by improving

productivity while implementing the highest food safety and regulatory standards, allowing

access to developed markets such as the European Union.

Some emerging economies, such as Ukraine has a significant opportunity to strengthen its

important role in agribusiness thanks to global demand for food that is accelerating with the

worldwide population growth.“Today Ukraine is fully engaged in ensuring global food

security and meets the growing needs of humanity in food. Ukraine is ready to take an active,

enhanced and mutually beneficial cooperation”25

, said Mykola Prysyazhniyuk, Minister of

Agrarian Policy and Food of Ukraine in June 2013.

2.1.1. Ukraine’s agribusiness sector at a glance

Fertile land

Ukraine has over 40 million hectares of agricultural land; of which about 80 % (around 32

million hectares) is arable more than any other European country (see Figure 11 and Table 4).

The country is rich for black soil, which is one of the country's greatest resources. The

country is home to over 16 million hectares of ―chernozem‖ (black soil), a very fertile black-

colored soil with high content of humus and minerals that offers a high potential for

agricultural yields.26

25 Mykola Prysyazhniyuk, Minister of Agrarian Policy and Food of Ukraine. (13 June 2013) Panel discussion:

―Investment in the agricultural sector of Ukraine. Let’s feed the world together!‖ First Annual Business

conference ABC: Ukraine and partners. Retrieved from : http://www.ukraine-partners.org

26 OECD (2012), Competitiveness and Private Sector Development: Ukraine 2011: Sector Competitiveness

Strategy, OECD Publishing. ISBN 978-92-64-12878-1

28

Figure 11: Ukraine’s agriculture land structure

Source: The Ministry of Agrarian Policy and Food of Ukraine 2011

The table below demonstrates the comparison of the Ukrainian land to other countries on

total agricultural area with arable territories. According to the Food and Agriculture

Organization data, Ukraine has more arable land than some EU countries like France,

Germany, the United Kingdom or Poland.

Table 4: Agricultural land (millions ha)

Source: Food and Agriculture Organization (2011)

29

Climate

Climatic conditions are very favorable to the production of most agricultural products in

different areas of the country. The moderate climate gives agri producers strong competitive

advantages. Ukraine comprises three distinct climatic zones, which allows producers to vary

crop growth. The western regions are suited to crops that demand high humidity, specifically

vegetables and spring grains. The conditions in the central and north –eastern regions are

favorable for all kinds of grains. The southern regions are best-suited to winter crops as the

area is Ukraine’s warmest overall.

Cost-competitiveness

Ukraine’s average cost of production per ton of grain is lower than its competitors. Low

production costs, estimated 50% lower than of European producers like Germany, result from

low usage of input, low labor costs and a lack of proper equipment.

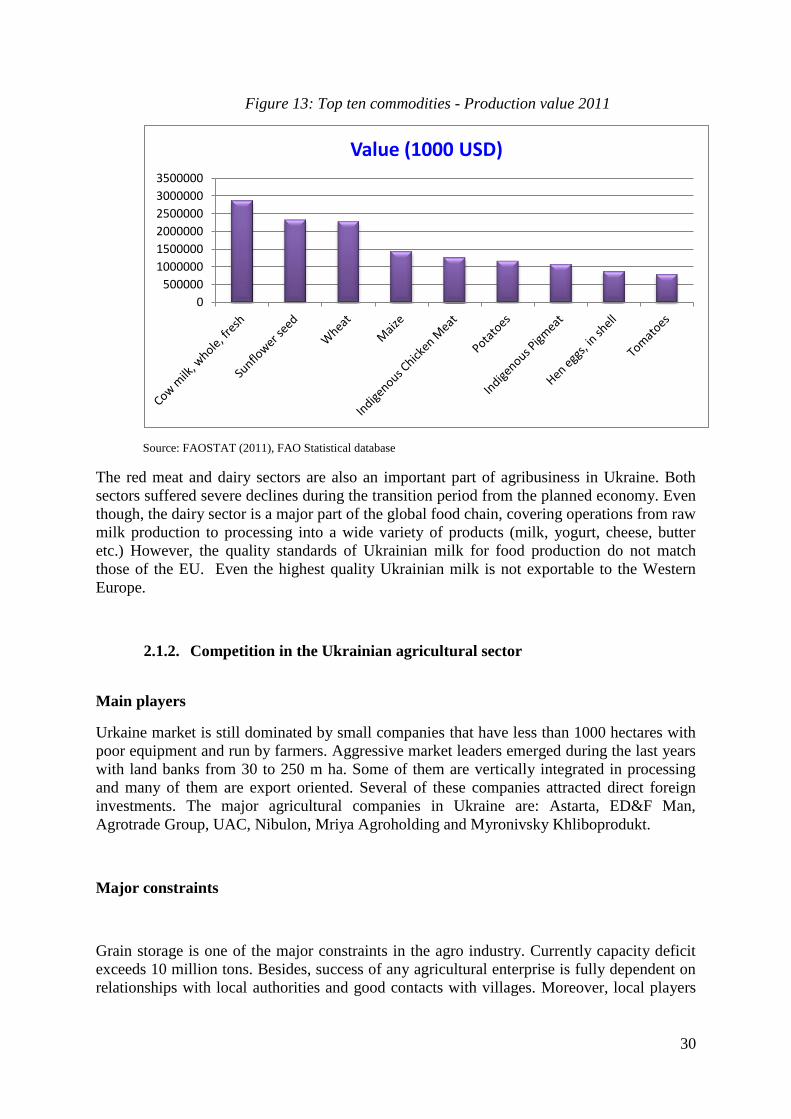

Ukraine’s production commodities

As it was mentioned before, excellent climate is very suitable for growing large-scale

production. Among production products there are: potatoes, cow and whole milk, sugar beet,

different grains, sunflower seeds, tomatoes, cabbages, soybeans.

Figure 12: Top ten commodities - Production quantity 2011

Source: FAOSTAT (2011), FAO Statistical database

Ukraine is already among the top five exporters of grain. In 2011 Maize was the most

cultivated grain, about 22,8 million tones harvested in 2011 (see Figure 12 above). Wheat is

the second largest grain produced with more than 22, 3 million tons harvested. Barley is the

third most important grain.

In 2011 Ukraine became the world’s largest producer and exporter of sunflower, globally

ahead of Argentina and Russia. In value terms, cow milk and sunflower seed are Ukraine’s

two most significant agricultural products (see Figure 13 below).

0

5000000

10000000

15000000

20000000

25000000

30000000

Quantity (t)

30

Figure 13: Top ten commodities - Production value 2011

Source: FAOSTAT (2011), FAO Statistical database

The red meat and dairy sectors are also an important part of agribusiness in Ukraine. Both

sectors suffered severe declines during the transition period from the planned economy. Even

though, the dairy sector is a major part of the global food chain, covering operations from raw

milk production to processing into a wide variety of products (milk, yogurt, cheese, butter

etc.) However, the quality standards of Ukrainian milk for food production do not match

those of the EU. Even the highest quality Ukrainian milk is not exportable to the Western

Europe.

2.1.2. Competition in the Ukrainian agricultural sector

Main players

Urkaine market is still dominated by small companies that have less than 1000 hectares with

poor equipment and run by farmers. Aggressive market leaders emerged during the last years

with land banks from 30 to 250 m ha. Some of them are vertically integrated in processing

and many of them are export oriented. Several of these companies attracted direct foreign

investments. The major agricultural companies in Ukraine are: Astarta, ED&F Man,

Agrotrade Group, UAC, Nibulon, Mriya Agroholding and Myronivsky Khliboprodukt.

Major constraints

Grain storage is one of the major constraints in the agro industry. Currently capacity deficit

exceeds 10 million tons. Besides, success of any agricultural enterprise is fully dependent on

relationships with local authorities and good contacts with villages. Moreover, local players

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

Value (1000 USD)

31

are traditionally short of development capital and the local firms are poorly equipped. At

least, westernized management and quality control are only implemented by few companies.

2.1.3. Investments opportunities for EU companies

European companies should first invest in the grain sub-sector. It includes wheat, rice, maize,

barley, oats, millet and other grains. Indeed, market trends for the grain sub-sector are driven

by an expected increase in global consumption. World wheat consumption is projected to rise

by around 1.1 % annually during the next decade to reach 746 million tons in 2020

(OECD/FAO, 2011).27

The growth of grain demand will come mainly from middle-eastern,

African and South-Asian countries due to increasing GDP per capita, rising feed

requirements for fast-growing livestock sectors and dynamic population growth. As

consequence, prices are expected to increase, making the grain sector potentially more

attractive for investment. By 2020, nominal wheat prices are expected to approach USD 240

per ton. Corn prices might reach USD 203/t in 2020.

Ukraine already accounts for about 10 % of global grain exports. It supplies grain to Asia,

North Africa, and the Middle East. In 2012, Ukraine ranked seventh in the world, exporting

almost 23 million tons of grain. According to 2012 state statistics, revenue from agricultural

exports reached an amount of $18 billion (25 percent of total export revenue). In the same

time the sector attracted $800 million of foreign direct investment. At the end of 2013 the

amount of FDI is even expected to reach $3 billion28

(see Table 5).

The growth has been reinforced by continuous financial support on behalf of international

financial organizations, including the European Bank for Reconstruction and Development,

Ukraine's largest investor, and the International Finance Corporation. The EBRD provided

nearly $180 million to Ukraine's agribusiness sector as of April 2013.29

27

OECD (2012), Competitiveness and Private Sector Development: Ukraine 2011: Sector Competitiveness

Strategy, OECD Publishing. ISBN 978-92-64-12878-1 28

SSCU (2012), State Statistics Service of Ukraine. Retrieved from : http:// www.ukrstat.gov.ua 29

Economic News and Events. (13 May 2013) European Bank for Reconstruction and Development. Retrieved

from: http://www.ebrd.com

32

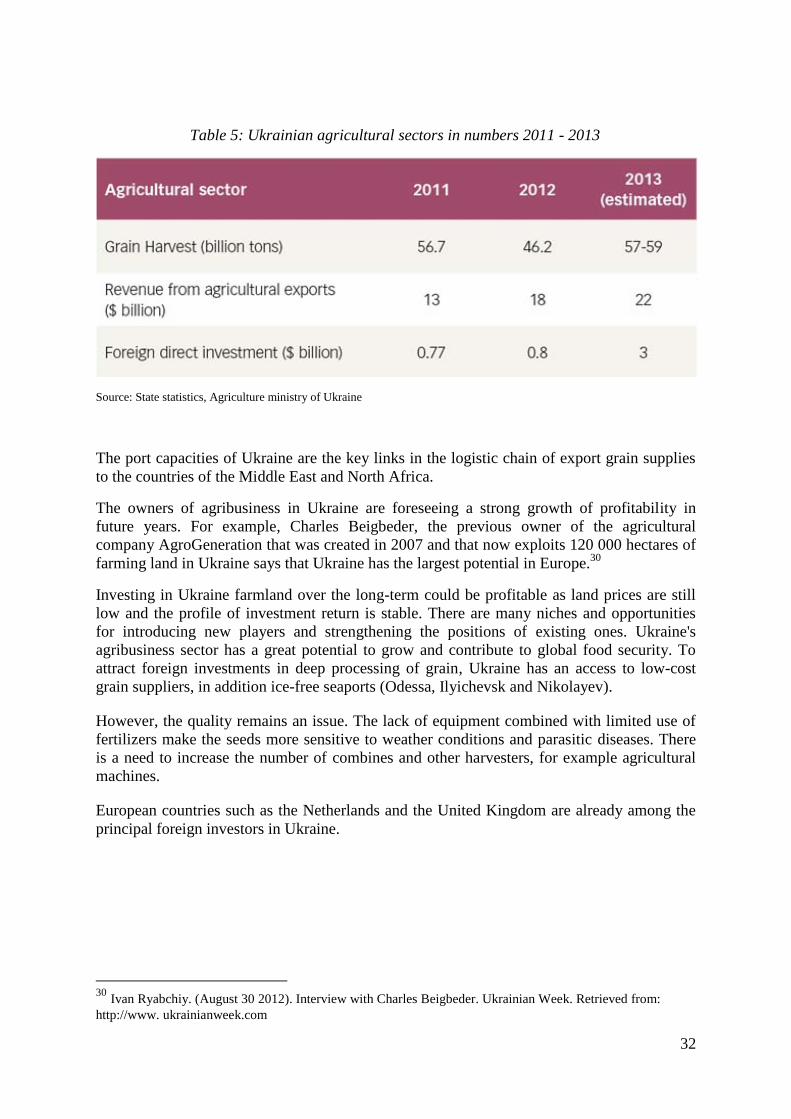

Table 5: Ukrainian agricultural sectors in numbers 2011 - 2013

Source: State statistics, Agriculture ministry of Ukraine

The port capacities of Ukraine are the key links in the logistic chain of export grain supplies

to the countries of the Middle East and North Africa.

The owners of agribusiness in Ukraine are foreseeing a strong growth of profitability in

future years. For example, Charles Beigbeder, the previous owner of the agricultural

company AgroGeneration that was created in 2007 and that now exploits 120 000 hectares of

farming land in Ukraine says that Ukraine has the largest potential in Europe.30

Investing in Ukraine farmland over the long-term could be profitable as land prices are still

low and the profile of investment return is stable. There are many niches and opportunities

for introducing new players and strengthening the positions of existing ones. Ukraine's

agribusiness sector has a great potential to grow and contribute to global food security. To

attract foreign investments in deep processing of grain, Ukraine has an access to low-cost

grain suppliers, in addition ice-free seaports (Odessa, Ilyichevsk and Nikolayev).

However, the quality remains an issue. The lack of equipment combined with limited use of

fertilizers make the seeds more sensitive to weather conditions and parasitic diseases. There

is a need to increase the number of combines and other harvesters, for example agricultural

machines.

European countries such as the Netherlands and the United Kingdom are already among the

principal foreign investors in Ukraine.

30

Ivan Ryabchiy. (August 30 2012). Interview with Charles Beigbeder. Ukrainian Week. Retrieved from:

http://www. ukrainianweek.com

33

2.2. Biomass-based energy production sector

2.2.1. Global trends

Renewable energy sources are playing an increasingly important role in meeting energy

needs across the world. They reduce dependence on fossil fuels and also help to protect the

environment by reducing greenhouse gas emissions, create new jobs and contribute to

economic development. In particular, heat and power production based on biomass was

identified as a pilot sub-sector. The OECD (2010) defines biomass as ―any organic material

of plant and animal origin, derived from agricultural and forestry production and resulting by-

products, and from industrial and urban wastes, used as feedstock for producing bio-energy

and other non-food applications‖.

It is estimated that the world demand for energy resources will more than triple before 2035

and China, India and the Middle East will count for 60% of this development.31

According to

the experts of International Energy Agency, the electricity and the biofuel based on biomass

will quadruple by 2035. Global bioenergy resources are more than enough to meet in the

same time the future demand for biofuel and for food.

2.2.2. Ukraine competitiveness in production of biomass-based energy

Ukraine’s abundant agricultural products and the rise in fossil energy prices are the two

elements that are likely to drive the future development of energy production based on

biomass.

Biomass resources are widely available in Ukraine. Biomass waste and residues are indeed

widely and conveniently available from the agriculture and forestry sectors. Straw, manure

and wood are especially promising as sources of heating. The economic potential of crop

wastes has been estimated by the National Academic of Sciences of Ukraine at 14 million

tonnes of coal equivalent per year. Therefore, the use of primary agricultural residue could

partly satisfy increasing heat consumption needs and replace traditional heat production

systems. In terms of regional distribution, all regions except the western part of the country

and the Crimean peninsula have high economic potential for development of energy

generation based on agricultural residues. This primarily correlates with production of wheat

and sunflowers, which are the primary sources of agricultural residues, however it is also

influenced by other factors, such as the quality of the soil and the region’s climate.

With natural gas prices expected to increase further as a result of the price reform in the

internal market, the use of natural gas for production of heat and power will become very

expensive. According to World Bank estimates, prices of natural gas might increase by more

than 400% from 2009 until 2017 in Ukraine.32

Global prices for other fossils fuels, such as oil

31

World Energy Outlook 2012. International Energy Agency (IEA). Retrieved from:

http://www.iea.org/aboutus/ 32

World Bank. Bank Recommends Phased Increase in Ukraine Gas Price. Retrieved from:

http://web.worldbank.org/WBSITE/EXTERNAL/COUNTRIES/ECAEXT/0,,contentMDK:20775037~pagePK:

146736~piPK:146830~theSitePK:258599,00.html

34

and coal are also expected to rise in the future. In contrast, renewable sources of energy, such

as hydropower, geothermal, wind and solar energy and biomass energy, are nearly limitless

2.2.3. European investments in biomass-based energy sector in Ukraine.

Ukraine has the highest biomass potential in Europe. It brings many opportunities for

investments in local bioenergy production and in the export of bioenergy crops.

Here are the possible FDI in the bio-energy projects in Ukraine:

Among the European countries investing in the biomass-based energy sector in Ukraine,

Germany is the most active one. In 2013 both countries have put their cooperation into a new

level with plans to promote the production of biofuels in Ukraine. This collaboration includes

creation of pilot bio-energy complexes. Germany is very interested to increase the production

of thermal energy and biogas from agricultural waste in Ukraine by providing technical

assistance for the development of bioenergy production in Ukraine.33

Such projects are

already widely spread in Germany where 5.7% of the electricity is already coming from the biomass in first half of 2012.34

Some European private companies producing alternative fuel already operate in Ukraine. For

example, Active energy group, a UK based company, operates in Ukraine since 2011 and is

currently one of the European leaders in providing of biomass to the European market. Active

Energy Ukraine has contracts for the purchase of wood, which it processes into chip fuel in

Ukraine and uses to replenish its supply to power facilities in Poland. Richard Spinks, the

chief executive at the Active Energy Group on the Ukrainian market: “The demand for wood

biomass is strong and expected to increase. We have the expertise and advantageous

geographic locations in Ukraine to procure, process and ship quickly and efficiently.”35

33

Ukrinform. Germany to help Ukraine produce biofuels. Retrieved from:

http://www.ukrinform.ua/eng/news/germany_to_help_ukraine_produce_biofuels_294845 34

CleanTechnica . Germany — 26% of Electricity from Renewable Energy in 1st Half of 2012. Retrieved from:

http://cleantechnica.com/2012/07/26/germany-26-of-electricity-from-renewable-energy-in-1st-half-of-2012/ 35

Christopher J. Miller. Interfax-Ukraine. (June 4 2013). Active Energy Group acquires biomass exporter

Nicofesco Holdings. KyivPost. Retrieved from: http://www.kyivpost.com

Acquisition of grain or cattle farms or forestry companies

Acquisition of a bolier manufacturer with focus on biomass technologies

Privatisation of dictrict heating companies and conversion of fossil-fuell untits to biomass-based units

35

2.3 The “National Projects” as practical tools of FDI attraction

Today Ukraine is facing the task to create a new operating platform for a constructive

dialogue between the government, businesses and potential investors on the local and

national levels. As a component of the Investment reform introduced by the Ukrainian

government in 2010, the ―National Projects‖ initiative represents an attractive tool to improve

the investment climate in Ukraine.

The ―National Projects‖ are the strategic projects of Ukraine focused on development of

priority economic and social sectors by means of attracting foreign direct investments in the

infrastructural projects. The President of Ukraine, Viktor Yanukovich, set up the agency

responsible for the National Projects which is called the State Agency for Investment and

Management of National Projects of Ukraine (Invest Ukraine). Its activity is based on a

priority investment funds over the government budget funds and partnership with the world's

best companies.36

The ―National Projects‖ are based on the principles:

Project management

Partnership with top-ranked companies

The main sources of financing of the ‖National Projects‖ are:

Private investments

International Financial Institutions

Loans and projects financing

As of October 2012, Ukraine has eleven ―National Projects‖. The list is the following:

1. ―LNG Terminal‖: sea terminal for liquefied natural gas

2. ―Air Express‖: construction of railway from Kyiv to ―Boryspil International Airport‖

3. ―Open World‖: introducing 4G technologies into educational management system

4. ―Clean City‖: update system of waste recycling complex

5. ―Affordable Housing‖: construction of affordable housing

6. ―Olympic Hope 2022‖: creation of sports and tourism infrastructure

7. ―New Life‖: presentation of maternity and childhood protection

8. ―Quality Water‖: ensuring Ukrainians with high quality potable water

9. ―Danube Corridor‖: development of transport connection in the Danube region

10. ―Energy of Nature‖: construction of solar hydropower station, production of

alternative fuel

11. ―FutureCity‖: formation of strategic plan and project system of the city

development.37

36

The National Projects. The Governmental Portal. Retrieved from: www.ukrproject.gov.ua

37 National Projects. Invest Ukraine 2012. Retrieved from : http://investukraine.com/investment-

opportunities/national-projects

36

Among the long-term projects, ―LNG Terminal‖ and ―Energy of Nature‖ are the two most

promising opportunities projects for European foreign direct investments. The table below

describes the two projects in brief.

Project name LNG Terminal Energy of Nature

Project summary Construction of a sea

terminal for liquefied natural

gas (LNG).

Develop a bioenergy industry

in Ukraine (wind energy,

biomass, solar energy, and

hydro energy).

Project timing Phase I: 2015

Phase II: 2016. Estimated 1.5 years.

Level of investment US$ 1.5-2 billion. 7 million Euros.

Payback period 8-9 years 5 years

The ―National projects‖ offer for investors from around the world unique opportunities to

open Ukraine as a country with extraordinary investment opportunities and comfortable

investment climate. These development projects have to become a driving force for the

development of the economy, and their implementation will be a part of the structural reform

of the economy.

They are implemented under the innovative technologies and practically form some new

industries. Each national project has long-term strategic goals.

37

3. Potential and risk of the European –Ukrainian collaboration

3.1. Possibility and goal of the EU-Ukraine Association Agreement

3.1.1. Background of the Association Agreement

Being the major participant of the Eastern Partnership, Ukraine considers The Eastern

Partnership as an instrument for collaboration with the EU, namely within the strategic

directions of cooperation such as negotiation on the EU-Ukraine Association Agreement,

which is to be the successor agreement to the Partnership and Co-operation Agreement. The

Association Agreement it is the first agreement based on political association between the EU

and any of the Eastern Partnership countries. The first negotiation on the new EU-Ukraine

Agreement including the aspect of Free Trade Agreement (FTA) began in 2007.38

The idea

to negotiate a FTA with Ukraine is actually a part of the EU’ policy to create a prosperous

European neighborhood environment via closer economic relations.

Soon after Ukraine gained a status of a World Trade Organization’s member in February

2008, the negotiation on the Association Agreement were raised up during the EU-Ukraine

summit in Paris. The mutual understanding of the text of the Association Agreement was

achieved between the leaders of the EU and the President Viktor Yanukovich on 19

December 2011. The initialing of the Association Agreement between Ukraine and the

European Union was launched according to the agreements achieved by their leaders during

the EU-Ukraine Summit in Brussels on 30 March 2012. The two parties initialed the

statements in the text of the Association on establishment of a Deep and Comprehensive Free

Trade Agreement.39

The Association Agreement constitutes a wide range of sector cooperation which is focused

on progressive reforms. It contains a brand new philosophy of the relations between the EU

and Ukraine since it contains new economic and political integration principles.

Negotiations on the Association Agreement have been built with a "modular" approach. In

particular, the transition negotiation process took place within the following individual

workgroups:

Foreign policy and security cooperation;

Field of justice, freedom and security;

Economic, sectoral issues and issues of human development;

FTA.

Basically, the draft of the Association Agreement is based on three pillars:

38

Delegation of the European Union to Ukraine. Association Agreement. The European Union and Ukraine

have initiated an Association Agreement as part of a joint effort to further strengthen the ties and bonds between

them. Retrieved from:http://eeas.europa.eu/delegations/ukraine/eu_ukraine/association_agreement/index_en.htm 39

EU-Ukraine Action Plan. Mission of Ukraine to the European Union. Documents / Ukraine-EU bilateral

documents / Main instruments. Retrieved from: http://ukraine-eu.mfa.gov.ua

38

1. Wide range of cooperation: rule of law, good governance, human rights, core reforms

on economic recovery, sector cooperation in energy, transport, environment

protection, education, equal rights, SME cooperation.

2. Mobility: liberalizing the visa regime for Ukrainian citizens for short term travel to

the European Union.

3. Trade related matters: Deep and Comprehensive Free Trade Area (DCFTA) is an

important integral element of the Association Agreement goes that far beyond WTO

regulations. DCFTA will create business opportunities between the EU and Ukraine.

The DCFTA is much larger than a typical free trade agreement. It considers not only the

lifting of tariff and non-tariff barriers but also, more importantly, Ukraine adopting EU legal

solutions and standards in this area. The key elements of the DCFTA are the following:

Market access for goods

Trade remedies

Technical barriers to trade

Sanitary and phytosanitary (SPS) measures

Customs and trade facilitation

Establishment, trade in services and electronic commerce

Trade and sustainable development

Mediation mechanism

Transparency

Public procurement

Intellectual property

Competition

Dispute settlement

3.1.2. Ukraine’s interests in the Association Agreement

In recent years, the share of the EU market has reached an average of 33% of the total exports

of Ukraine. Share of imports from the EU member countries averaged 35.6%. The EU market

differs significantly from others by its higher tariff protection especially on agricultural goods

and products. Under the agreements of the parties, liberalization will cover more than 97%

of tariff lines (or more than 95% of the volume of bilateral trade between the EU and

Ukraine). In this case, cancellation fees on importable EU goods will take place in the first

year of the agreement (on 99% of tariff lines).40

The establishment of a Free Trade regime with the EU member states would enhance the

export conditions of the Ukrainian products to the EU. Indeed, the EU market would become

open for Ukraine by removing or reducing import tariffs and quotas. It would also eliminate

non-tariff barriers by harmonizing laws, standards and regulations across all economic

40

Ihor Prasolov, Minister of Economic Development and Trade of Ukraine. Panel discussion report ―DCFTA

between Ukraine and the EU: prospects for business and investment‖. The First International Annual Business

Conference ―ABC Ukraine and Partners‖ on June 13-14, 2013. Retrieved from: http: www.ukraine-partners.org

39

sectors. It would therefore boost economic growth, increase trade, attract investments and

transform the Ukrainian economy to the European standard economy.

For Ukraine, the Association Agreement is the most effective tool for large-scale political and

economic reforms in the country. In fact, we can consider the Association Agreement as an

instrument to achieve the relevant criteria for EU membership. Ukraine as a European State

in accordance with the Treaties the EU has a full right to acquire the EU membership status,

if the both parties are ready. The relevant provisions supporting the European choice of

Ukraine are fixed in the draft of the Agreement.

The DCFTA included in the Association Agreement is based on the economic requirements

for EU membership. That makes this Free Trade Agreement different and highly important

for Ukraine which has future ambitious plans to access to the EU. Ukraine has to adapt its

current economy and legislation to the EU standards. Therefore, it is a kind of probation for

Ukraine: if, upon the conditions that all the DCFTA requirements are respected, the EU

would hardly refuse Ukraine in the membership.

3.1.3. European Union’s interests in the Association Agreement

Ukraine is the largest partner of the European Union within the Eastern Partnership initiative

but it represents only about 2% of trade for the EU so there is huge potential for growth. It

goes without saying that upon the signature of the DCFTA, the EU companies are expected to

obtain opportunities of investment in the Ukrainian business and enjoy the absence of custom

duties.

However, apart from the trade interest and the investment opportunities represented by the

Association Agreement, there is another less visible component which is the geopolitical

factor. Indeed, Ukraine borders with four EU’s member states: Poland, Romania, Hungary

and Slovakia. It is naturally for the EU to be concerned by creating a safe and strategically

reliable partnership on its East borders.

The EU authorities realized that Ukraine is a key intermediary in the transportation of energy

supplies to the EU. A strategically significant oil pipeline Odessa-Brody runs from Black Sea

to Brody, with Ukrainian-Polish border. The pipeline is transferring Caspian oil to the Central

Europe through the territory of Ukraine. The European Union is interested in reducing the

dependence on Russian oil and diversifying the suppliers as due to the unstable relations

between Russia and Ukraine. For example, in 2004 and 2010, Russia already blocked the

Caspian oil that was aimed to Poland through Ukraine.