mcdonald’s corporation lu jiang section:mw 6:00 … 2013/ar final projects/ar final... ·...

TRANSCRIPT

Annual Report

McDonald’s Corporation

Lu Jiang

Section:MW 6:00-9:00pm

http://www.aboutmcdonalds.com/content/dam/AboutMcDonalds/Investors/Investor%202013/2012%20Annual%20Report%20Final.pdf

Introduction

• Chief executive officer: Don Thompson

• Location of home office: 2111 McDonald's Dr., Oak Brook,

IL 60523

• Ending date of latest fiscal year: December,31 2012

• Principal products: hamburgers, cheeseburgers, chicken,

french fries, breakfast items, soft drinks, milkshakes and

desserts

• Main geographic area of activity: United States, Europe, and

APMEA

Audit report

• Independent auditors: ERNST & YOUNG LLP

• The auditors state that the financial statement of McDonald’s corporation at December 31 2012 and 2011 and its cash flow in the recent three years are correspond to U.S. general accepted accounting principles. Moreover, company has a effective internal control over 2012’s financial report according to the COSO criteria.

Stock Market Information

• Stock price: $97.11 • Twelve month trading range of the company’s

stock:$83.31 - 103.70 (from yahoo finance) • Dividend per share:$2.87 • Date of the above information: Stock price: June 21,2013 twelve moth trading range: June 21, 2013 dividend per share: December 31,2012 • My opinion: I think it is better to hold the stock.

The price of the stock is fluctuating.

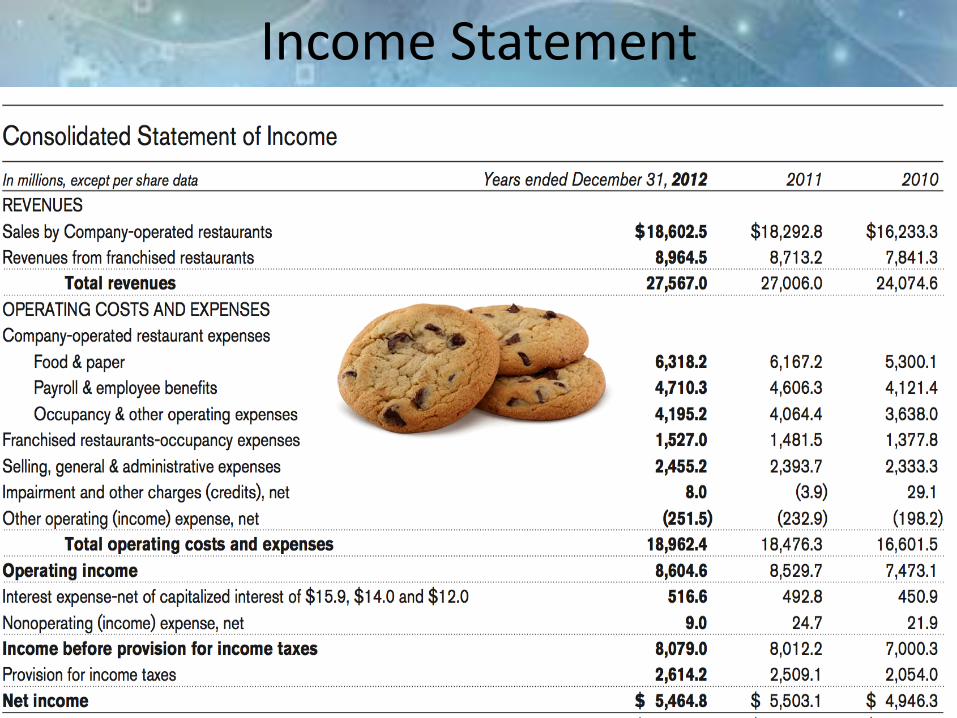

Income Statement

Income Statement In million 2012 2011

Gross profit 21248.8 20838.8

Income from operations 25111.8 24612.3

Net income 5464.8 5503.1

Income statement

• It is most like a multistep format

• The company has an increasing in the net income at the end of the year of 2011 but has a decrease at the end of the year of 2012. The company is in good operation because its operating income continues to increase through years.

B A L A N C E S H E E T

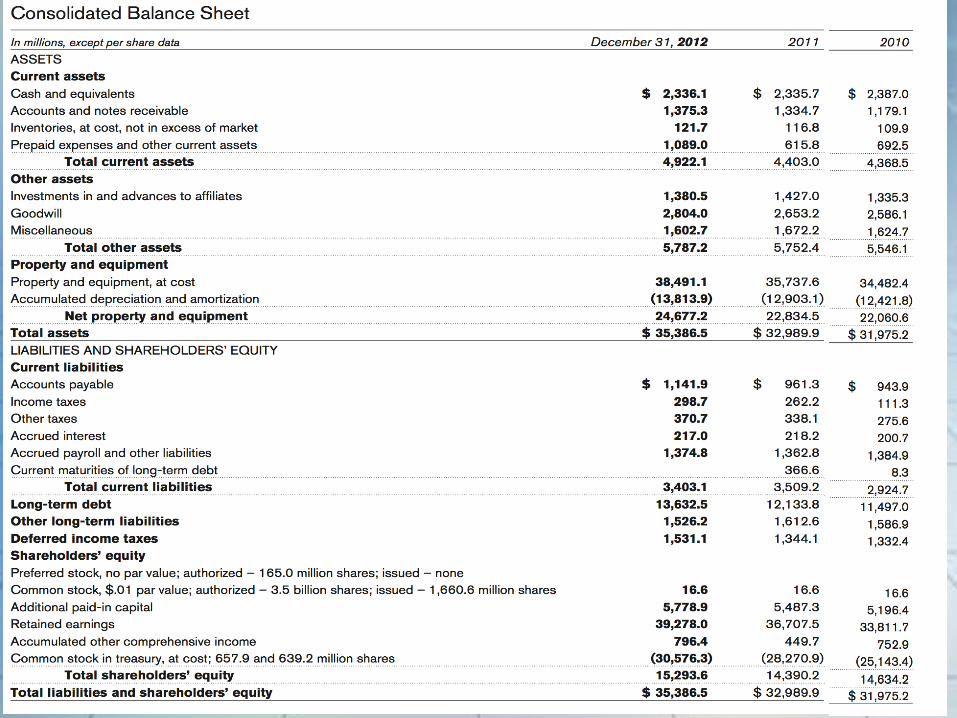

Balance sheet 2012 (in

millions)

Current Assets:

4922.1 Current Liabilities

3403.1

Other assets 5787.2 Long-term Liabilities

16689.8 (1)

Property and equipment

24677.2 Shareholders’ equity

15293.6

Total Assets 35386.6 Total Liabilities and shareholders equity

35386.6

Total assets = Total Liabilities+ shareholders equity

Calculation : (1) long-term liabilities=long-term debt +other long-term liabilities+ deferred income tax 16689.8=13632.5+1526.2+1531.1

Balance sheet 2011( in

millions)

Current Assets:

4403.0 Current Liabilities

3509.2

Other assets 5752.4 Long-term Liabilities

15090.5 (1)

Property and equipment

22834.5 Shareholders’ equity

14390.2

Total Assets 32989.9 Total Liabilities and shareholders equity

32989.9

Total assets = Total Liabilities+ shareholders equity

Calculation : (1) long-term liabilities=long-term debt +other long-term liabilities+ deferred income tax 15090.5=12133.8+1612.6+1344.1

Balance sheet

Company’s current assets and intangible assets continue to increase through years. It seems that the company has a lot of potential to create values in the future. Company’s property and equipment increases through years, and is the largest part of increasing in assets. This means the company tends to open more restaurants. Long term investments decrease a little in the year of 2012. In general, company’s total assets gradually increase through years. It accumulates a lot of things to generate value in the future. Company’s current liabilities gradually increase except current maturities of long term debt suddenly decrease to 0, which leads to the decreasing in the total current liabilities. This means company paid off a lot of its debt in 2012 and also it has less debt in 2012. Company’s long-term liabilities increase gradually through years to years. Company’s retained earnings increase mostly in year 2012 in shareholder’s equity.

Statement of cash flows

Cash Flows

In millions 2012 2011

Operating 7150.1 8341.6

Investing (2570.9) (2056.0)

financing (4533.0) (3728.7)

Statement of cash flows • Cash flow from operations increases in the past

• two years. • The company is growing through • investing activities because cash used • for investing activities increases in the • past two years. • In year 2012, the primary source of • financing for the company is long-term • financing issuances. • Overall, cash and equivalents decreases in the • year of 2012 but increases in the year of 2011.

Accounting policies Accounting policies:

(1)revenue recognition: consists sales by company-operated restaurants and fees from franchised restaurants operated by conventional franchisees. Sales are recognized on a cash basis.

(2)goodwill: represents the excess of cost over the net tangible assets and identifiable intangible assets of acquired restaurant businesses.

(3)Property and equipment: are stated at cost, with depreciation and amortization provided using the straight-line method

(4)long-lived assets: Long-lived assets are reviewed for impairment annually in the fourth quarter and whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable.

Topics in notes

Nature of business Consolidation Estimates in financial statements Revenue Recognition Foreign currency translation Advertising costs Share-based compensation Goodwill Long-lived assets Property and equipment Fair Value Measurements Certain Financial Assets and Liabilities Measured at Fair Value Non-financial assets and liabilities measured at fair value on a nonrecurring basis Certain financial assets and liabilities not measured at fair value Financial instruments and hedging activities

Financial Analysis

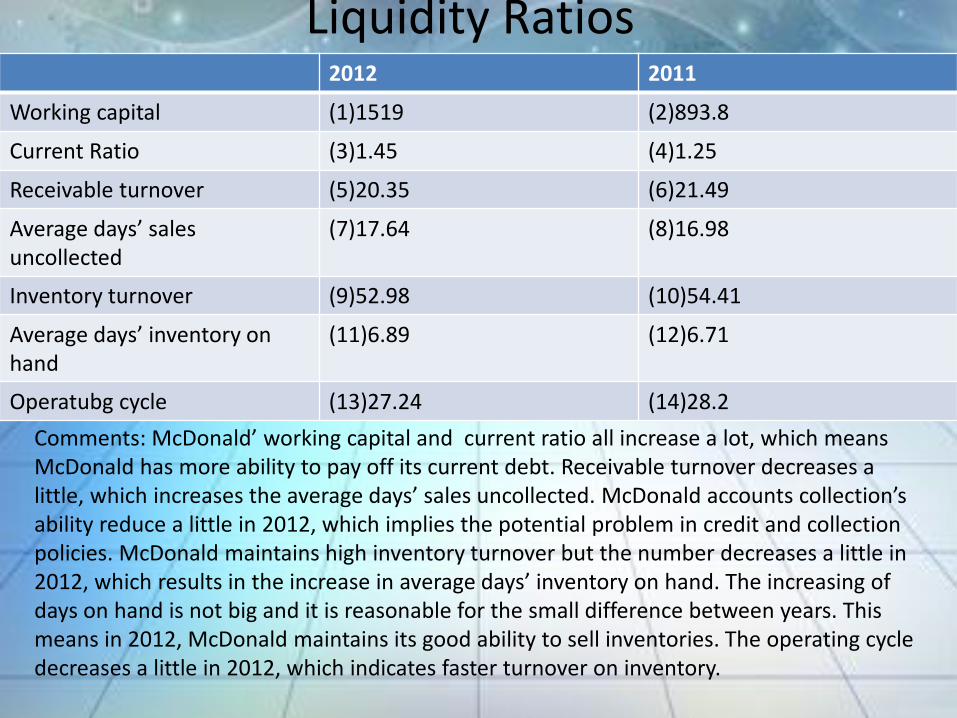

Liquidity Ratios 2012 2011

Working capital (1)1519 (2)893.8

Current Ratio (3)1.45 (4)1.25

Receivable turnover (5)20.35 (6)21.49

Average days’ sales uncollected

(7)17.64 (8)16.98

Inventory turnover (9)52.98 (10)54.41

Average days’ inventory on hand

(11)6.89 (12)6.71

Operatubg cycle (13)27.24 (14)28.2

Comments: McDonald’ working capital and current ratio all increase a lot, which means McDonald has more ability to pay off its current debt. Receivable turnover decreases a little, which increases the average days’ sales uncollected. McDonald accounts collection’s ability reduce a little in 2012, which implies the potential problem in credit and collection policies. McDonald maintains high inventory turnover but the number decreases a little in 2012, which results in the increase in average days’ inventory on hand. The increasing of days on hand is not big and it is reasonable for the small difference between years. This means in 2012, McDonald maintains its good ability to sell inventories. The operating cycle decreases a little in 2012, which indicates faster turnover on inventory.

Basic information: Current assets(2012)=4922.1 (2011)=4403 Current liabilities(2012)=3403.1 (2011)=3509.2 Sales(2012)=27567 (2011)=27006 Cost of good sold(2012)=6318.2 (2011)=6167.2 receivable=(2012)1375.3 average for 2012=(1375.3+1334.7)/2=1355 (2011)=1334.7 average for 2011=(1334.7+1179.1)/2=1256.9 (2010)=1179.1 Inventory(2012)=121.7 average for 2012=(121.7+116.8)/2=119.25 (2011)=116.8 average for 2011=(116.8+109.9)/2=113.35 (2010)=109.9

Calculation: (1) 4922.1-3403.1=1519 (2)4403-3509.2=893.8 (3)4922.1/3403.1=1.45 (4)4403/3509.2=1.25 (5)27567/1355=20.35 (6)27006/1256.9=21.49 (7) 365/20.35=17.94 (8)365/21.49=16.98 (9)6318.2/119.25=52.98 (10)6167.2/113.35=54.41 (11)365/52.98=6.89 (12)365/54.41=6.71 (13)20.35+6.89=27.24 (14)21.49+6.71=28.2

Profitability ratios 2012 2011

Profit margin (1)0.198 (2)0.204

Asset turnover (3)0.81 (4)0.83

Return on assets (5)0.16 (6)0.17

Return on equity (7)1.80 (8)1.88

Net income (2012)=5464.8 (2011)=5503.1 Total assets(2012)=35386.6 (2011)=32989.9 (2010)=31975.2 average for 2012=(35386.6+32989.9)/2=34188.25 average for 2011=(32989.9+31975.2)/2=32482.55 Revenue (2012)=27567 (2011)=27006 Shareholders’ equity(2012)=15293.6 (2011)=14390.2 Calculation: (1) 5464.8/27567=0.198 (2)5503.1/27006=0.204 (3) 27567/34188.25=0.81 (4)27006/32482.55=0.83 (5)0.198*0.81=0.16 (6)0.204*0.83=0.17 (7)27567/15293.6=1.80 (8)27006/14390.2=1.88

Comments on profitability ratios

• McDonald profit margin keeps constant through 2011 and 2012, which implies its stable efficient ability to use its resources. Its assets turnover ration is also constant and only decreases a little bit, and its assets increases a lot, which means McDonald maintains its ability to generate sales with increasing amount of assets. Moreover, return on assets keeps constant. McDonald keeps generate profit in the same ratio with increasing assets and this means that it has good operating in 2012. McDonald maintains its high return on equity ratio and this means it keeps its ability to generate cash internally.

Market strength ratios

2012 2011

Price/earnings per share (1)16.46 (2)19.74

Dividend yield (3)3.3% (4)2.5%

Price: December,31,2012 = 88.21 December,30,2011=100.33 Earning per share(2012)=5.36 (2011)=5.27 Dividends per share(2012)=2.87 (2011)=2.53 Calculation: (1)88.21/5.36=16.46 (2)100.33/5.27=19.04 (3)2.87/88.21=0.033 (4)2.53/100.33=0.025

Comments: McDonald maintain a normal P/E ratio and it decreases in 2012, which indicates a decreasing in the confidence in the company’s ability to maintain earnings growth, or indicates there was inflation in 2012. Dividend yield ratio increases in 2012, which means it become more attractive for investors.

Solvency ratio 2012 2011

Debt to equity (1)1.31 (2)1.29

Financing gap (3)38.73 (4)28.29

Statistics: Shareholders’ equity(2012)=15293.6 (2011)=14390.2 Total liabilities and SHE(2012)=35386.5 (2011)=32989.2 Total liabilities(2012)=35386.5-15293.6=20092.9 (2011)32989.2-14390.2=18599 Cost of good sold(2012)=6318.2 (2011)=6167.2 Accounts payable (2012)=1141.9 (2011)=961.3 DPO (2012)=1141.9/6318.2*365=65.97 (2011)=961.3/6167.2*365=56.89 Notes payable= Calculation: (1)20092.9/15293.6=1.31 (2)18599/14390.2=1.29 (3) 65.97-(20.35+6.89)=38.73 (4)56.89-(21.49+6.71) =28.69 Comments: Debt to equity ration of McDonald increase a little, and the numbers are all larger than 1, which means creditors are in control of the company. Financing gap maintains positive during 2011 and 2012, and even higher in 2012, which means that McDonald keeps a good ability of self-financing.

Industry Situatio & Company Plans • McDonald is the worlds’ biggest restaurant chain. The company serves to provide

people with delicious fast food and high-qualified service. McDonald maintains its good internal controls and gradually enlarge its size through years. Through its annual report, McDonald’s future goals are to take risk, maintains its priorities, and improve its products, services and customer experience. In its letter for shareholders, McDonald claims its potential opportunity to have more growth.

• On June 20, 2013, McDonald announced that it may soon begin franchising its restaurants of being family-owned and operated. Due to this plan, like what the company said in tits annual report, McDonald would like to improve its customer experience and service. Moreover, franchising its restaurants can also improve its products and services because the plan can motivate people, who will be franchised, to improve their own business.

• On June 7, 2013, The New York Times reports that McDonald tends to shift their target consumers from 18 to 30 year old people to younger generation. This means that McDonald may have more new products that are millennial favored. They may also provide more services for youth.

• Overall, McDonald targets to provide better service, products. It also tends to change its operation scheme and target consumers.

Citation: “McDonald's Considering Franchising Restaurants After 70 Years Of Being Family Owned And Operated”, The onion, June 20 2013 “Restaurant Chains Try to Woo a Younger Generation”, The New York Times, June 7, 2013

Executive Summary

• McDonald’s Corporation is a Centralized, International company. It keeps a tight grasp on operations, cost and quality. McDonald’s overseas investment relies heavily on franchising. It has a great potential to improve its business and gain more. However, McDonald needs to face the risk of its change in operation strategy.

Resources: McDonald’s 2012 Annual Report Final “McDonald's Considering Franchising Restaurants After 70 Years Of Being Family Owned A nd Operated”, The onion, June 20 2013 “Restaurant Chains Try to Woo a Younger Generation”, The New York Times, June 7, 2013