maruti suzuki india ltd. - ventura securities ltdmaruti suzuki india ltd. (msil), a subsidiary of...

TRANSCRIPT

Maruti Suzuki India Ltd.

BUY

- 1 of 18 - Tuesday 1st October, 2013

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

ST

OC

K P

OIN

TE

R

Target Price `1,664 CMP `1,380 FY15 PE 12.4x

Index Details We initiate coverage on Maruti Suzuki India Ltd (MSIL) as a BUY with a Price Objective of `1,664. At the CMP of `1,380, the stock is trading at 15.3x and 12.4x its estimated earnings for FY14E & FY15E respectively, representing a potential upside of ~21% over a period of 18 months.

We are particularly enthused by the fact that MSIL over the last two years, despite challenging times like the Manesar plant lock out and intense competition across segments, has been able to maintain market share across all segments. We strongly believe that when the auto revival resumes MSIL would be best placed to benefit from this.

In the near term, we expect new models in the compact & hatchback (WagonR Stingray & Swift Sport) and SUV segment (XA Alpha) to drive sales growth. In addition, diesel engine capacity expansion and SPIL merger coupled with increasing localization initiatives (on the input side) will enhance scale of operations and improve operating margins. We forecast revenues and earnings to grow at a CAGR of 8.2% and 18.3% to `51,048 and `3,350.2 crore, respectively over FY14-15E.

Despite challenging times, MSIL is well placed to sustain

market share

Although MSIL (with its 1.1% growth to 4,37,056 units YTD in FY14) seems to

have bucked the prevailing recessionary trend in the PV segment, we have to

bear in mind that this growth was due to the low base effect (due to plant lock out

at Manesar) in the last fiscal. However, we could expect an improved

performance going forth as the monsoon has been satisfactory and elections are

around the corner. We expect the launch of new models, WagonR Stingray, Swift

Sport and SUV XA Alpha to drive sales.

Overall we expect volume to grow at a CAGR of 5% to 12,93,284 units over the

period FY13-15E. Sales are expected to grow at a CAGR of 8.2% to `51,048

crore while earnings are expected to ramp up to `3,350.2 crore (18.3% CAGR)

over the forecast period.

Sensex 19,517

Nifty 5,780

BSE 100 5,765

Industry Automobile

Scrip Details

Mkt Cap (` cr) 41,687

BVPS (`) 629.9

O/s Shares (Cr) 30.2

Av Vol (Lacs) 0.6

52 Week H/L 1773/1217

Div Yield (%) 0.6

FVPS (`) 5.0

Shareholding Pattern

Shareholders %

Promoters 56.2

DIIs 13.1

FIIs 22.0

Public 8.7

Total 100.0

Maruti Suzuki vs. Sensex

Key Financials (` in Cr)

Y/E Mar Net

Revenue EBITDA PAT EPS

EPS Growth (%)

RONW (%)

ROCE (%)

P/E (x)

EV/EBITDA (x)

2012 35,587.1 2,513.0 1,635.2 56.6 -28.6 10.8 21.6 24.4 16.7

2013 43,588.0 4,229.8 2,392.3 79.2 39.9 12.9 25.9 17.4 9.9

2014E 46,104.1 4,744.0 2,724.5 90.2 13.9 13.0 25.6 15.3 8.8

2015E 51,048.6 5,712.2 3,350.2 110.9 23.0 13.9 26.8 12.4 7.3

- 2 of 18 - Tuesday 1st October, 2013

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Increased localization and other measures to boost margins

The merger of diesel engine manufacturing facility Suzuki Powertrain India Ltd.

(SPIL) with itself, expansion of diesel engine capacity and thrust towards increased

localization should help boost margins besides lower exposure to the currency

fluctuations (through lowered imports). We expect margins to improve by 150 bps

to 11.2% by FY15E.

Further the new R&D centre at Rohtak, apart from being a valuable contributor to new technological advancement, should provide significant tax savings which should improve PAT margins. We expect PAT margins to improve to 6.6% by FY15E from the current 5.5% clocked in FY13.

Valuation

We initiate coverage on MSIL as a BUY with a Price Objective of `1,664 (target PE 15x) representing a potential upside of ~21% over a period of 18 months. At the CMP of `1,380, the stock is trading at 15.3x and 12.4x its estimated earnings for FY14E and FY15E respectively. Improved product mix along with increased localization and operational synergies of the SPIL merger should enable MSIL to boost revenue and profitability going forward. Accordingly we expect sales and earnings to grow at a CAGR of 8.2% & 18.3%, respectively to `51,048.6 crore & `3,350.2 crore by FY15.

- 3 of 18 - Tuesday 1st October, 2013

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Company Background

Maruti Suzuki India Ltd. (MSIL), a subsidiary of Suzuki Motor Corporation, Japan (with a 54.2% stake), is the largest passenger car (PV) company in India, accounting for 40% of the domestic passenger car market. MSIL derives ~64% of its domestic sales volume from the small car segment and has a dominant position in the segment with a market share of ~61%. The company operates from two facilities in India (Gurgaon and Manesar) and is in the process of expanding its manufacturing capacity to 1.8 mn units (1.26 mn units in FY13) by FY15. Currently, exports account for ~8% of its overall sales volume and MSIL is striving hard to expand its market in the non European countries (thereby reducing its dependency on the deteriorating European markets).

Key Investment Highlights

Despite challenging times, MSIL is well placed to sustain

market share

Given the tightening liquidity, heavy inflation, and economic slowdown, the Indian PV industry (sales volumes down 9.3%) is facing one of its most challenging times. The immediate future is also expected to continue to remain under stress as there seems to be no trigger to revive demand (barring for a good monsoon).

Although MSIL (with its 1.1% growth to 4,37,056 units YTD in FY14) seems to

have bucked the prevailing recessionary trend in the PV segment, we have to bear

in mind that this growth was due to the low base effect (due to plant lock out at

Manesar) in the last fiscal. However we could expect an improved performance

going forth as the monsoon has been satisfactory and elections are around the

corner. We expect the launch of new models, WagonR Stingray, Swift Sport and

SUV XA Alpha to drive sales.

PV Industry trend

-2

0

2

4

6

8

10

12

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

Sep

-07

Dec-0

7

Mar-

08

Ju

n-0

8

Sep

-08

Dec-0

8

Mar-

09

Ju

n-0

9

Sep

-09

Dec-0

9

Mar-

10

Ju

n-1

0

Sep

-10

Dec-1

0

Mar-

11

Ju

n-1

1

Sep

-11

Dec-1

1

Mar-

12

Ju

n-1

2

Sep

-12

Dec-1

2

Mar-

13

Ju

n-1

3

(%)

Nos.

PV Sales GDP (%) RHS

Inflation Rate (RHS) Interest Rate (RHS)

Source: MSIL, Ventura Research

- 4 of 18 - Tuesday 1st October, 2013

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Overall we expect volume to grow at a CAGR of 5% to 12,93,284 units over the period FY13-15E. Sales are expected to grow at a CAGR of 8.2% to ` 51,048 crore

while earnings are expected to ramp up to ` 3,350.2 crore (18.3% CAGR) over the forecast period.

Depreciating INR is bullish for MSIL’s exports Another positive factor which could drive growth is the fact that with the depreciation of the INR export markets are looking very rosy. With the mood in the domestic vehicle market being quite gloomy, we believe that the logical step to drive growth would be to increase exports which in recent times have seen a sharp deceleration. Besides improving the top line, the sharp fall in the currency value should also help improve profitability of MSIL’s exports.

Export Trend & % of Sales

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

Q1F

Y12

Q2F

Y12

Q3F

Y12

Q4F

Y12

Q1F

Y13

Q2F

Y13

Q3F

Y13

Q4F

Y13

Q1F

Y14

YT

DF

Y14

Nos.

Export Volume % of Sales (RHS)

Source: MSIL, Ventura Research

Sales Trend & PAT Margin

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

0

10000

20000

30000

40000

50000

60000

FY09 FY10 FY11 FY12 FY13 FY14E FY15E

Sales PAT Margins (RHS)

Source: MSIL, Ventura Research

- 5 of 18 - Tuesday 1st October, 2013

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Maintains market share in an otherwise crowded market One of the highlights of MSIL’s performance has been the fact that barring for the UV segment (where it has lost market share marginally), it has been able to maintain its dominant market share across segments and even improve it further. The segment wise performance of MSIL is enumerated below.

WagonR Stingray to propel compact segment market share further MSIL’s robust growth (of 11.9% to 1,63,274 units YTD in FY14) in the compact segment has enabled it to gain market share by a huge 900 bps to 76% in YTDFY14. Competitors have ceded market share to Alto 800 and Wagon R, which account for 44% and 30% share respectively of the overall compact segment.

We expect further gains in market share to come through the recently launched WagonR Stingray (August’13). The full-fledged effect of the same will be visible in H2FY14.

Competitive Price Range-Compact Volume Growth

0

1

2

3

4

5

6

7

8

Nan

o

Alt

o

A-S

tar

Wag

on

R

Esti

lo

Sp

ark

Eo

n

Nan

o-d

iesel

Pu

nto

Sti

ng

ray

` Lacs

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

Q1FY13 Q2FY13 Q3FY13 Q4FY13 Q1FY14 YTDFY14

Nos.

Compact Sales Y-o-Y (RHS)

Source: MSIL, Ventura Research Source: MSIL, Ventura Research

Market Share - Compact Segment

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Nano Spark Eon Alto 800 A Star Estilo Wagon R

Market Share (%)

FY13YTD FY14YTD

+9% Market Share Increased

-1%

+4%

-12%

Source: MSIL, Ventura Research

- 6 of 18 - Tuesday 1st October, 2013

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Swift Sport to drive growth in the Hatchback segment One of the most fiercely contested segments is the hatchback category where a flurry of models has been launched by new incumbents. Although, MSIL’s hatchback segment has reported a de-growth of ~4% to 90,969 units in YTDFY14, MSIL through the launch of model extensions and diesel variants has been able to ward of this competitive threat (with its Swift portfolio gaining an encouraging 500 bps to take its market share to 27%). We believe further gains in market share are possible post the launch of Swift Sport.

Competitive Price Range- Hatchback Volume Growth

0

1

2

3

4

5

6

7

8

9

San

tro

Ind

ica e

V2

Fig

o

Sail

U-V

a

Sw

ift

Liv

a

i20

Pu

nto

Po

lo

Rit

z

Bri

o

Beat

mic

ra

i10

Sw

ift S

po

rt

New

Beat

New

i10

i30

Fie

sta

Fo

rd B

max

Pan

da

Up

2W

D

Bri

o D

iesel

San

dero

`Lacs

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

Q1FY13 Q2FY13 Q3FY13 Q4FY13 Q1FY14 YTDFY14

Nos.

Hatchback Y-o-Y (RHS)

Source: MSIL, Ventura Research Source: MSIL, Ventura Research

Market Share - Hathback Segment

0%

5%

10%

15%

20%

25%

30%

San

tro

xin

g

Ind

ica e

V2

Fig

o

Sail

U-V

a

Liv

a

i20

Pu

nto

Po

lo

Sw

ift

Rit

z

Bri

o

Beat

i10

Mic

ra

Market Share (%)

FY13YTD FY14YTD

+4% Market Share Increased

+1%

-2% -1%

+1%-3%

0%0%

0%

+3%

0%

+1%

-4%

Source: MSIL, Ventura Research

- 7 of 18 - Tuesday 1st October, 2013

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

MUV segment demand to remain subdued This segment (consisting of Ertiga, Gypsy, Omni, & Eeco) has witnessed de-growth of 22.3% on YTD basis in FY14 to 61,947 units. Despite the fact that competitors have been launching new vehicles in the MUV segment, MSIL has been able to defend its market share at 39% in YTDFY14. The contributor to the volume growth was the satisfactory performance by Ertiga, which has sustained its market share at 15% in the MUV segment with a sale of 23,549 units YTD in FY14, whereas the nearest competitor Innova has shown significant decline in the market share by 300 bps to 14% over the same period.

Competitive Price Range- MUV Volume Growth

0

2

4

6

8

10

12

14

16

18

20

Bo

lero

Su

mo

Xylo

Tavera

Inn

ova

Ari

a

Om

ni

Eeco

Th

ar

ven

ture

Gyp

sy

En

joy

Ert

iga

H-1

Wag

on

Hexa S

pace

Ari

a A

T

Min

icat

Fia

t 500L

Lo

dg

y

Nis

san

No

te

`Lacs

-200%

0%

200%

400%

600%

800%

1000%

0

5000

10000

15000

20000

25000

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

Q1

FY1

4

YTD

FY1

4

Nos.

MUV YoY

Source: MSIL, Ventura Research Source: MSIL, Ventura Research

Market Share - MUV Segment

0%

5%

10%

15%

20%

25%

30%

Bo

lero

Xylo

Su

mo

Th

ar

Ari

a

Ven

ture

Ert

iga

Om

ni

Eeco

Gyp

sy

En

joy

Tavera

Inn

ova

Market Share (%)

FY14YTD FY13YTD

Marginal Market Share loss of 1%+3%

-3%

-3%-2%

+7%

-3%

+2%

0%0%

Source: MSIL, Ventura Research

- 8 of 18 - Tuesday 1st October, 2013

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

SUV foray – new growth opportunity MSIL is conspicuous by its absence in the fast growing SUV segment. Leveraging on its strong brand equity and the recent excitement around SUVs, MSIL is slated to launch a new model XA Alpha which would mark its entry into this segment. XA Alpha’s positioning “under 4 metres” (in line with the new excise norms), in our opinion, holds promise and should help spearhead growth.

Dzire to maintain growth trend in Midsized sedan category MSIL’s Midsized sedan segment (25% YTD growth in FY14) has so far managed to buck the overall slowdown. The growth has been primarily driven by the mounting demand for the Dzire model, which has helped it increase its market share to 46%. This is despite the fact that Honda’s new model Amaze has been a runaway success. Going forth, we expect this growth trend to be maintained.

Competitive Price Range-SUV UV industry Volume Trend

0

5

10

15

20

25

30

Dic

or

Sto

rme

Du

ste

r

Sco

rpio

XU

V5

00

Vit

ara

Re

xto

n

Eco

Sp

ort

Qu

an

to

XA

Alp

ha

Tra

x

Tra

ilB

laze

r

Tu

sco

n

Sa

nta

Fe

En

de

av

ou

r

Ru

sh

Vis

ta X

tre

me

XU

V5

00

Tig

ua

n 2

WD

Te

rra

no

XV

`Lacs

-20%

0%

20%

40%

60%

80%

100%

0

10000

20000

30000

40000

50000

60000

Ju

n-1

1

Au

g-1

1

Oct-

11

Dec-1

1

Feb

-12

Ap

r-12

Ju

n-1

2

Au

g-1

2

Oct-

12

Dec-1

2

Feb

-13

Ap

r-13

Ju

n-1

3

Au

g-1

3

UV YoY %

Nos

Source: MSIL, Ventura Research Source: MSIL, Ventura Research

Market Share – Sedan Segment

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Am

aze

Eti

os

Man

za+

Ind

igo

Su

nn

y

Lin

ea

Dzir

e

SX

4

Vern

a

Veri

to

Cit

y

Market Share (%)

FY13YTD FY14YTD

+4% Market Share Increased

+17%

-4%

-5%

-5%-4%

-1%

-1%

-1%

Source: MSIL, Ventura Research

- 9 of 18 - Tuesday 1st October, 2013

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

MSIL all set to take on impending competition

In a slowing market, new model launches from all the incumbents is expected to further intensify competition. While the loss of market share for the dominant player is obvious, we are not worried with regards to MSIL’s ability to hold its own. In the past MSIL has deftly demonstrated its ability to defend its market share through a combination of

launch of two new products aimed at pre-empting competition,

new model variants and product extensions have kept its brand portfolio fresh and reinvigorated

carefully chosen product pricing and positioning strategies

support of a country wide dealer network and customer service centres

Testimony to the above is its current performance where it has not only maintained

market share but even gained some in extremely competitive segments.

Competitive Price Rang- Sedan Volume Growth

0

5

10

15

20

25

Ve

rn

a

Ve

rit

o

Ind

igo

e

CS

Am

aze

Dzir

e

Ch

ev

lt S

ail

Etio

s

Ma

nza

Su

nn

y

Lin

ea

SX

4

To

yo

ta

V

ios

Fia

t V

iag

gio

Ac

co

rd

Cit

y

Civ

ic

Sylp

hy

Flu

en

ce

` Lacs

-60%

-40%

-20%

0%

20%

40%

60%

80%

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

Q1F

Y12

Q2F

Y12

Q3F

Y12

Q4F

Y12

Q1F

Y13

Q2F

Y13

Q3F

Y13

Q4F

Y13

Q1F

Y14

YT

DF

Y14

Nos.

Sedan-Midsize YoY

Source: MSIL, Ventura Research Source: MSIL, Ventura Research

Market Share YTDFY14 Market Share YTDFY13

Tata 6%

MSIL40%

Hyundai15%

Honda5%

M&M10%

Toyota5%

Others19%

Tata 11%

MSIL38%

Hyundai15%

Honda2%

M&M10%

Toyota7%

Others17%

Source: MSIL, Ventura Research Source: MSIL, Ventura Research

- 10 of 18 - Tuesday 1st October, 2013

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Upcoming launches in the PV segment

Company Segment Brand Launch Date Variant Price Range (INR)

TATA Compact Nano Facelift Sep-13 CNG 1.5-2.5L

TATA Compact Nano Facelift Sep-13 Diesel 2.5-3.5L

Maruti Compact WaganR Stingray Aug-13 Petrol 4-5L

Fiat Hatchback Grande Punto Evo End'13 Petrol/ Diesel 6 -7L

Maruti Hatchback Swift Sports CY13 Petrol/ Diesel 5-6L

Cheverolet Hatchback Beat Facelift Oct-13 Petrol/Diesel 3.5-5L

Hyundai Hatchback i10 Facelift Sep-13 Diesel 4-7L

Hyundai Hatchback i30 Oct-13 Petrol/Diesel 6.5-8L

Ford Hatchback Fiesta Oct-13 Petrol/Diesel 5-7L

Ford Hatchback Ford B max Nov-13 Petrol/Diesel 6-7L

Fiat Hatchback Fiat Panda Nov-13 Diesel 5.5- 7L

Volkswagon Hatchback Volkswagen Up 2WD Nov-13 Petrol/ Diesel 3.5- 5L

Honda Hatchback Brio Facelift May-14 Diesel 5- 6.5L

Ranault Hatchback Renault Sandero Jan-14 Both 5.5- 7.5L

Hyundai MUV H-1 Wagon Sep-13 Diesel 12-15L

Hyundai MUV Hexa Space Jan-14 Gasoline-GDI 7-9L

TATA MUV Aria AT Oct-13 15-19L

TATA MUV Minicat Feb-14 6.5-8L

Fiat MUV Fiat 500L Nov-13 Diesel 8- 10L

Nissan MUV Nissan Note Feb-14 Petrol 8-10L

Ranault MUV Renault Lodgy Nov-13 Petrol 7-9.5L

Maruti SUV XA Alpha CY14 Diesel 10L

Cheverolet SUV Trax Nov-13 Petrol/Diesel 7-10L

Cheverolet SUV TrailBlazer Jan-14 Diesel 17-20L

Hyundai SUV Tuscon Oct-13 Diesel 18-20L

Hyundai SUV Santa Fe Dec-13 Diesel 22-26L

Ford SUV Endeavour Facelift May-14 Diesel 17-22L

Toyota Kirloskar SUV Fortuner 2.5L Facelift Nov-13 Diesel 20-22L

Toyota Kirloskar SUV Rush Nov-13 Petrol/Diesel 8-10L

TATA SUV Vista D-90 Xtreme Dec-13 6-8L

M&M SUV XUV500-Compact Oct-13 Diesel 6-7.5L

Volkswagon SUV Tiguan 2WD Aug-13 Diesel 18- 25L

Nissan SUV Terrano XV Oct'13 Diesel 8.90L

Toyota Kirloskar. Sedan Toyota Vios Oct-13 Petrol/Diesel 7.5-10L

Fiat Sedan Fiat Viaggio Apr-14 Petrol 8-10L

Honda Sedan Accord Facelift Nov-13 Petrol 18- 23L

Honda Sedan Honda City Facelift Nov-13 Diesel 8.5-11L

Honda Sedan Honda New Civic Jan-14 Diesel 12.5-15L

Nissan . Sedan Nissan Sylphy Jan-14 Petrol 12-16L

Ranault Sedan Renault New Fluence Dec-13 Petrol 13-16L Source: MSIL, Ventura Research

- 11 of 18 - Tuesday 1st October, 2013

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Increased localization and other measures to boost margins

The merger of diesel engine manufacturing facility Suzuki Powertrain India Ltd.

(SPIL) with itself, expansion of diesel engine capacity, and thrust towards

increased localization should help boost margins besides lower exposure to the

currency fluctuations (through lowered imports). We expect margins to improve by

150 bps to 11.2% by FY15E.

Further the new R&D centre at Rohtak, apart from being a valuable contributor to new technological advancement, should provide significant tax savings which should improve PAT margins. We expect PAT margins to improve to 6.6% by FY15E from the current 5.5% clocked in FY13.

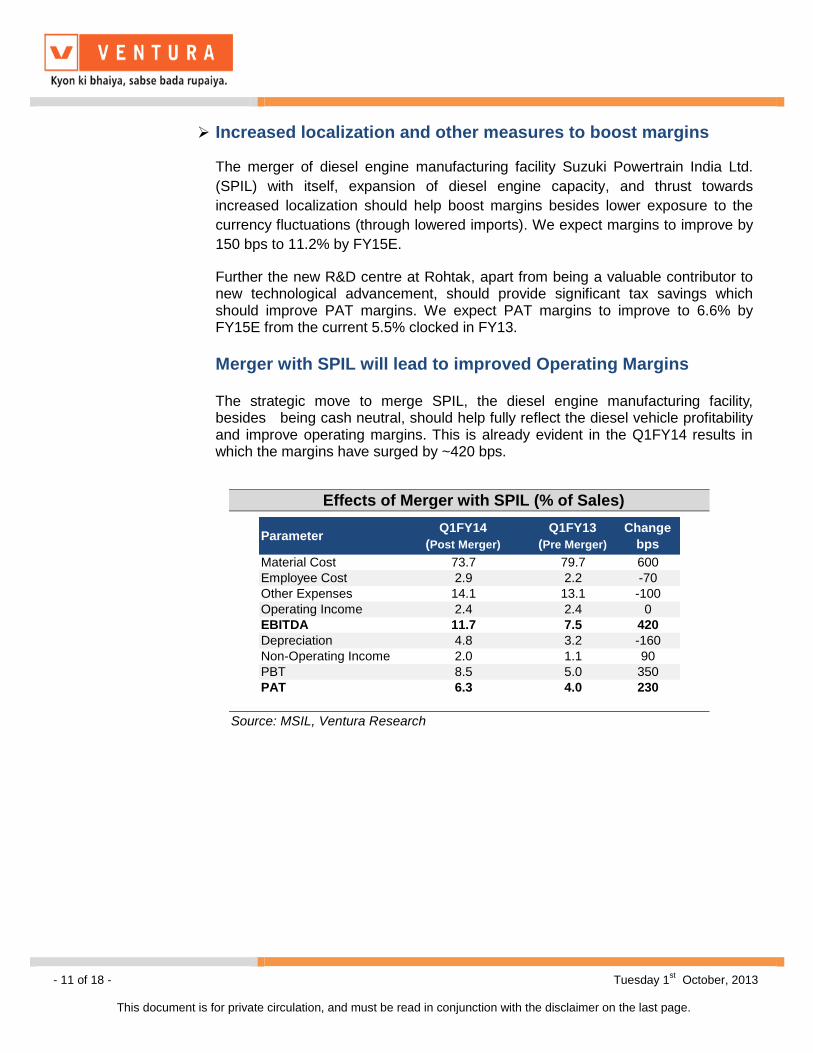

Merger with SPIL will lead to improved Operating Margins

The strategic move to merge SPIL, the diesel engine manufacturing facility, besides being cash neutral, should help fully reflect the diesel vehicle profitability and improve operating margins. This is already evident in the Q1FY14 results in which the margins have surged by ~420 bps.

Effects of Merger with SPIL (% of Sales)

ParameterQ1FY14

(Post Merger)

Q1FY13

(Pre Merger)

Change

bps

Material Cost 73.7 79.7 600

Employee Cost 2.9 2.2 -70

Other Expenses 14.1 13.1 -100

Operating Income 2.4 2.4 0

EBITDA 11.7 7.5 420

Depreciation 4.8 3.2 -160

Non-Operating Income 2.0 1.1 90

PBT 8.5 5.0 350

PAT 6.3 4.0 230

Source: MSIL, Ventura Research

- 12 of 18 - Tuesday 1st October, 2013

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

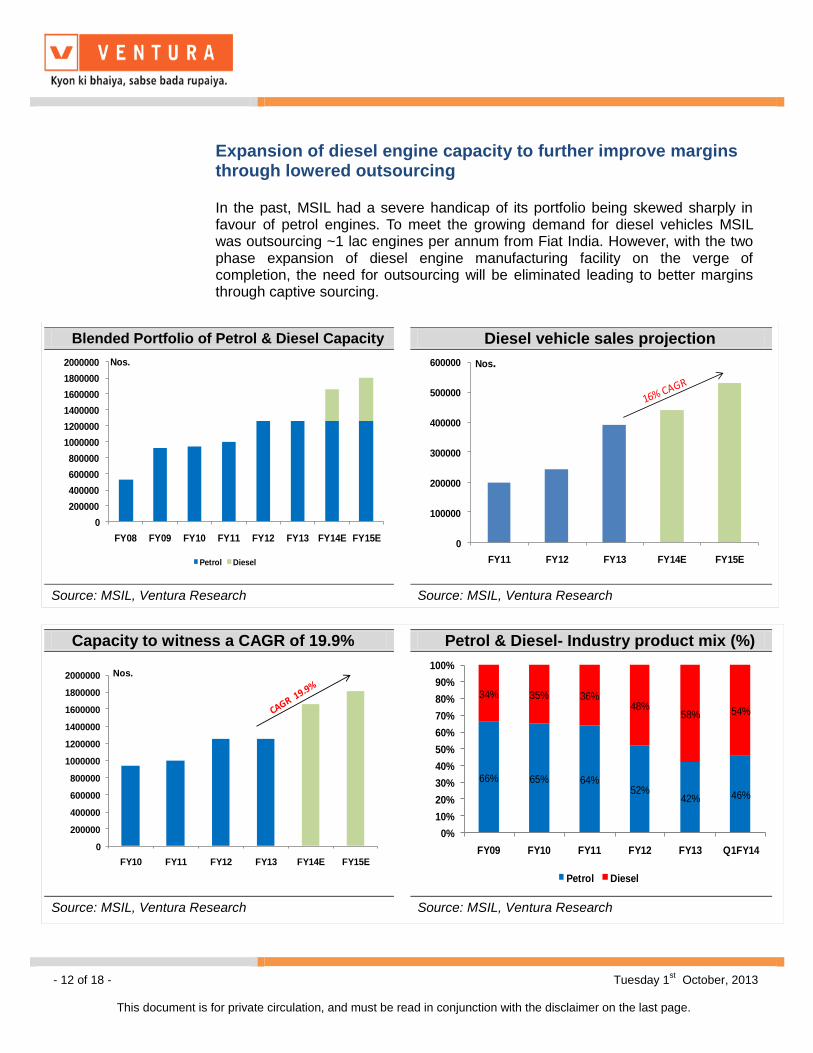

Expansion of diesel engine capacity to further improve margins through lowered outsourcing

In the past, MSIL had a severe handicap of its portfolio being skewed sharply in favour of petrol engines. To meet the growing demand for diesel vehicles MSIL was outsourcing ~1 lac engines per annum from Fiat India. However, with the two phase expansion of diesel engine manufacturing facility on the verge of completion, the need for outsourcing will be eliminated leading to better margins through captive sourcing.

Blended Portfolio of Petrol & Diesel Capacity Diesel vehicle sales projection

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

2000000

FY08 FY09 FY10 FY11 FY12 FY13 FY14E FY15E

Nos.

Petrol Diesel

0

100000

200000

300000

400000

500000

600000

FY11 FY12 FY13 FY14E FY15E

Nos.

Source: MSIL, Ventura Research Source: MSIL, Ventura Research

Capacity to witness a CAGR of 19.9% Petrol & Diesel- Industry product mix (%)

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

2000000

FY10 FY11 FY12 FY13 FY14E FY15E

Nos.

66% 65% 64%52%

42% 46%

34% 35% 36%48%

58% 54%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY09 FY10 FY11 FY12 FY13 Q1FY14

Petrol Diesel

Source: MSIL, Ventura Research Source: MSIL, Ventura Research

- 13 of 18 - Tuesday 1st October, 2013

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Increased localization to help improve cost efficiency and lower exposure to currency fluctuations

The recent plunge in the value of the rupee could easily disrupt any business, which is reliant on import of critical components. The proactive management had already initiated several measures to step up local sourcing and replace imports. We expect the imports to gradually be lowered by 8-10% over the next 2- 3 years from the current 19.5%. There is also the possibility that MSIL would lower its imports even further given the unprecedented sharp fall in the value of the INR.

Localization & Margins trend INR-JPY

26.0% 19.5%17.5%

15.5%

7.1%

9.7%10.4%

11.4%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

FY12 FY13 FY14E FY15E

% Localization EBIDTA (%) RHS

0.6

1.1

1.6

2.1

2.6

3.1

3.6

Feb

-05

Au

g-0

5

Feb

-06

Au

g-0

6

Feb

-07

Au

g-0

7

Feb

-08

Au

g-0

8

Feb

-09

Au

g-0

9

Feb

-10

Au

g-1

0

Feb

-11

Au

g-1

1

Feb

-12

Au

g-1

2

Feb

-13

Au

g-1

3

INR-JPY

Source: MSIL, Ventura Research Source: MSIL, Ventura Research

- 14 of 18 - Tuesday 1st October, 2013

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Focus on R&D – Move towards next generation technology

The Swift, Dzire and Ertiga models are largely a product of the company’s R&D initiative. And their good styling characteristics and next generation engines developed at the R&D centres has resulted in the runaway success of these models.

In order to keep abreast of technological & design advancements, MSIL is setting up a state of the art R&D centre at Rohtak. The centre is expected to be commissioned by FY16. Apart from contributing to the above, this centre along with MAT & deferred tax benefits is expected to help keep the effective tax rate ~22%.

Weighted Tax Benefit u/s 35(2AB) of Income Tax Act, 1961

173

416 372515 545 603

31%26%

24%

20%22% 22%

0%

5%

10%

15%

20%

25%

30%

35%

0

100

200

300

400

500

600

700

FY10 FY11 FY12 FY13 FY14E FY15E

`Crore

R&D Expenditure Tax Rate (RHS)

Source: MSIL, Ventura Research

- 15 of 18 - Tuesday 1st October, 2013

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Financial Performance

MSIL operating revenues in Q1FY14 witnessed de-growth of 5% YoY to `10,237 crore led by a fall in total volumes (which were down 10% YoY). Inspite of this, cheaper imports and increased local sourcing helped operating margins grow by 420 bps to 11.7%. Further merger of SPIL and the beneficial currency effect helped earnings grow by 49% bound to `.631.5 crore.

Quarterly Financial Performance (` in crore)

Particulars Q1FY14 Q1FY13 FY13 FY12

Income From Operations 10237.3 10778.2 43587.9 35587.1

Growth % -5.0 22.5

Total Expenditure 9071.2 9991.8 39402.1 33116.8

EBIDTA 1166.1 786.4 4185.8 2470.3

EBDITA Margin % 11.7 7.5 9.6 6.9

Depreciation 480.2 339.9 1861.2 1138.4

EBIT (EX OI) 685.9 446.5 2324.6 1331.9

Other Income 204.3 112.3 856.2 869.5

EBIT 890.2 558.8 3180.8 2201.4

EBIT Margin % 8.7 5.2 7.3 6.2

Interest 44.2 33.2 189.8 55.2

Exceptional items 0.0 0.0 0.0 0.0

PBT 846.0 525.6 2991.0 2146.2

PBT Margin % 8.3 4.9 6.9 6.0

Provision for Tax 214.5 101.8 598.9 511.0

PAT 631.5 423.8 2392.1 1635.2

PAT Margin (%) 6.2 3.9 5.5 4.6

Source: MSIL, Ventura Research

- 16 of 18 - Tuesday 1st October, 2013

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Financial Outlook

On the back of sustained volume growth led by new launches, we expect revenues to grow at a CAGR of 8.2% over the forecasted period of FY13-15 to `51,048 crore.

Operating profits are expected to post a CAGR of 16.2% over FY13-15 to `5,712.2 crore backed by the bump up in localization, resulting in lower input cost. Consequently, EBITDA margins are expected to grow by 150 bps to 11.2% in FY15E from the current 9.7% in FY13. In line with the improved profitability, earnings are expected to grow at a CAGR of 18.3% to `3,350.2 crore over the forecast period FY13-15.

Valuation We initiate coverage on MSIL as a BUY with a Price Objective of `1,664 (target PE 15x) representing a potential upside of ~21% over a period of 18 months. At the CMP of `1,380, the stock is trading at 15.3x and 12.4x its estimated earnings for FY14E and FY15E respectively. Improved product mix along with increased localization and operational synergies of the SPIL merger should enable MSIL to boost revenue and profitability going forward. Accordingly we expect sales and earnings to grow at a CAGR of 8.2% & 18.3%, respectively to `51,048.6 crore & `3,350.2 crore by FY15.

Revenue and Profitability Trend

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

0

10000

20000

30000

40000

50000

60000

FY10 FY11 FY12 FY13 FY14E FY15E

`Crore

Revenue EBITDA Margin RHS (%) PAT Margin RHS (%)

Source: MSIL, Ventura Research

- 17 of 18 - Tuesday 1st October, 2013

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

P/E

0

500

1,000

1,500

2,000

2,500

3,000

Jul-03 Jul-05 Jul-07 Jul-09 Jul-11 Jul-13

CMP 11X 14X 17X 20X 23X

Source: MSIL, Ventura Research

P/BV

0

500

1000

1500

2000

2500

3000

3500

Jul-03 Jul-05 Jul-07 Jul-09 Jul-11 Jul-13

CMP 2X 2.5X 3X 3.5X 4X

Source: MSIL, Ventura Research

EV/EBITDA

0

10000

20000

30000

40000

50000

60000

70000

80000

Jul-03 Jul-05 Jul-07 Jul-09 Jul-11 Jul-13

EV 5.5X 7X 8.5X 10X 11.5X

Source: MSIL, Ventura Research

- 18 of 18 - Tuesday 1st October, 2013

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Financials and Projections

Y/E March, Fig in ` Cr FY 2012 FY 2013 FY 2014e FY 2015e Y/E March, Fig in ` Cr FY 2012 FY 2013 FY 2014e FY 2015e

Profit & Loss Statement Per Share Data (Rs)

Net Sales 35587.1 43588.0 46104.1 51048.6 EPS 56.6 79.2 90.2 110.9

% Chg. -2.8 22.5 5.8 10.7 Cash EPS 96.0 140.8 158.7 188.1

Total Expenditure 33074.1 39358.2 41360.1 45336.4 DPS 7.5 8.0 8.0 8.0

% Chg. 0.3 19.0 5.1 9.6 Book Value 525.7 615.0 695.9 797.5

EBITDA 2513.0 4229.8 4744.0 5712.2 Capital, Liquidity, Returns Ratio

EBITDA Margin % 7.1 9.7 10.3 11.2 Debt / Equity (x) 0.0 0.0 0.0 0.0

Other Income 826.8 812.4 876.1 964.3 Current Ratio (x) 1.1 0.9 1.0 1.2

PBDIT 3339.8 5042.2 5620.1 6676.5 ROE (%) 10.8 12.9 13.0 13.9

Depreciation 1138.4 1861.2 2068.0 2332.9 ROCE (%) 21.6 25.9 25.6 26.8

Interest 55.2 189.8 59.1 48.4 Dividend Yield (%) 0.5 0.6 0.6 0.6

Exceptional items 0.0 0.0 0.0 0.0 Valuation Ratio (x)

PBT 2146.2 2991.2 3493.0 4295.1 P/E 24.4 17.4 15.3 12.4

Tax Provisions 511.0 598.9 768.5 944.9 P/BV 2.6 2.2 2.0 1.7

Reported PAT 1635.2 2392.3 2724.5 3350.2 EV/Sales 1.2 1.0 0.9 0.8

PAT Margin (%) 4.6 5.5 5.9 6.6 EV/EBIDTA 16.7 9.9 8.8 7.3

Raw Materials / Sales (%) 79.0 74.6 73.7 72.8 Efficiency Ratio (x)

Manpower cost / Sales (%) 2.4 2.5 2.5 2.5 Inventory (days) 18.4 19.0 19.0 19.0

Other opr Exp / Sales (%) 6.5 7.6 8.2 8.2 Debtors (days) 9.6 11.9 11.5 11.5

Tax Rate (%) 23.8 20.0 22.0 22.0 Creditors (days) 61.7 51.7 51.7 51.7

Balance Sheet Cash Flow statement

Share Capital 144.5 151.0 151.0 151.0 Profit After Tax 1635.2 2392.3 2724.5 3350.2

Reserves & Surplus 15042.9 18427.9 20871.5 23940.7 Depreciation 1138.4 1861.2 2068.0 2332.9

Minority Interest 0.0 0.0 0.0 0.0 Working Capital Changes 1185.1 878.1 -1028.9 -732.9

Total Loans 0.0 542.6 542.9 417.1 Others 136.2 126.2 827.6 993.3

Other Long Term Liability 264.9 329.5 348.5 385.9 Operating Cash Flow 4094.9 5257.8 4591.2 5943.6

Total Liabilities 15452.3 19451.0 21913.9 24894.8 Capital Expenditure -2510.3 -6066.3 -3600.0 -3000.0

Gross Block 14734.7 19800.7 24742.9 27742.9 Change in Investment -1040.7 -930.9 -750.0 -750.0

Less: Acc. Depreciation 7214.0 10001.5 12069.5 14402.4 Cash Flow from Investing -3551.0 -6997.2 -4350.0 -3750.0

Net Block 7520.7 9799.2 12673.4 13340.5 Proceeds from equity issue 0.0 6.5 0.0 0.0

Capital Work in Progress 941.9 1942.2 600.0 600.0 Inc/(Dec) in Debt -364.5 352.8 -58.8 -174.2

Investments & Lons 7514.4 9251.6 10001.6 10751.6 Dividend and DDT -251.8 -280.9 -280.9 -280.9

Net Current Assets -221.7 -1133.3 -952.4 611.4 Cash Flow from Financing -616.3 78.4 -339.7 -455.1

Deferred Tax Assets -303.0 -408.7 -408.7 -408.7 Net Change in Cash -72.4 -1661.0 -98.6 1738.5

Misc Expenses 0.0 0.0 0.0 0.0 Opening Cash Balance 2508.5 2436.1 775.0 676.4

Total Assets 15452.3 19451.0 21913.9 24894.8 Closing Cash Balance 2436.1 775.1 676.4 2414.9

Ventura Securities Limited Corporate Office: C-112/116, Bldg No. 1, Kailash Industrial Complex, Park Site, Vikhroli (W), Mumbai – 400079 This report is neither an offer nor a solicitation to purchase or sell securities. The information and views expressed herein are believed to be reliable, but no responsibility (or liability) is accepted for errors of fact or opinion. Writers and contributors may be trading in or have positions in the securities mentioned in their articles. Neither Ventura Securities Limited nor any of the contributors accepts any liability arising out of the above information/articles. Reproduction in whole or in part without written permission is prohibited. This report is for private circulation.