markets & the us election · pdf filemarkets & the us election october 2016 ......

TRANSCRIPT

Deutsche Bank

Markets & the US Election

October 2016

Tom Joyce CIB Capital Markets Strategist

Hailey Orr CIB Capital Markets Strategist

Francis Kelly Head of Government Affairs - Americas

Mariya Getsova CIB Capital Markets Strategist

Deutsche Bank

10/17/2016

1

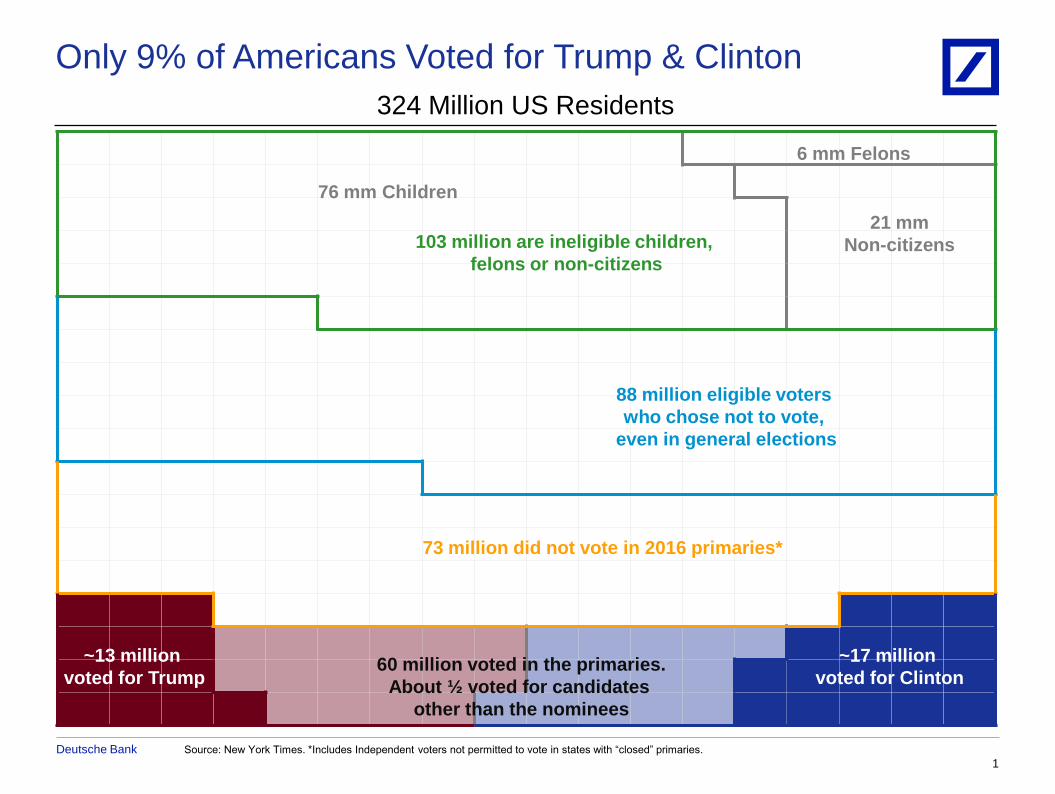

Source: New York Times. *Includes Independent voters not permitted to vote in states with “closed” primaries.

Only 9% of Americans Voted for Trump & Clinton

76 mm Children

21 mm

Non-citizens

6 mm Felons

324 Million US Residents

103 million are ineligible children,

felons or non-citizens

88 million eligible voters

who chose not to vote,

even in general elections

73 million did not vote in 2016 primaries*

60 million voted in the primaries.

About ½ voted for candidates

other than the nominees

~17 million

voted for Clinton

~13 million

voted for Trump

Deutsche Bank

2

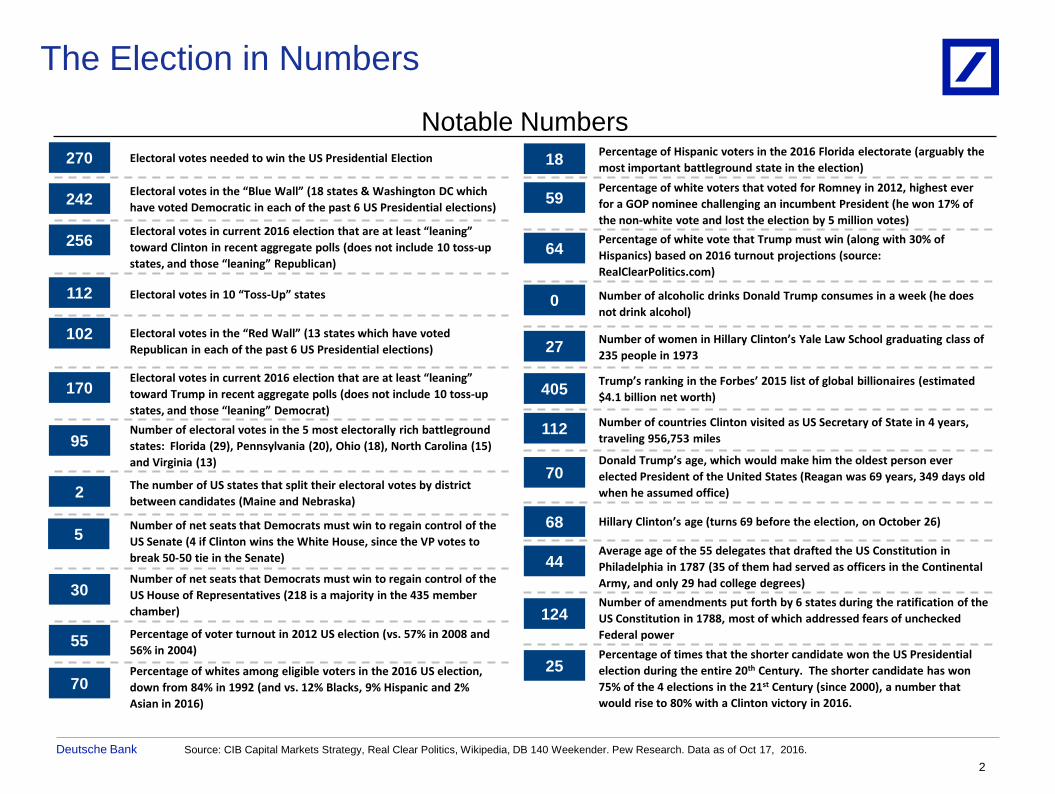

Percentage of Hispanic voters in the 2016 Florida electorate (arguably the

most important battleground state in the election)

Percentage of white voters that voted for Romney in 2012, highest ever

for a GOP nominee challenging an incumbent President (he won 17% of

the non-white vote and lost the election by 5 million votes)

Percentage of white vote that Trump must win (along with 30% of

Hispanics) based on 2016 turnout projections (source:

RealClearPolitics.com)

Number of alcoholic drinks Donald Trump consumes in a week (he does

not drink alcohol)

Number of women in Hillary Clinton’s Yale Law School graduating class of

235 people in 1973

Trump’s ranking in the Forbes’ 2015 list of global billionaires (estimated

$4.1 billion net worth)

Number of countries Clinton visited as US Secretary of State in 4 years,

traveling 956,753 miles

Donald Trump’s age, which would make him the oldest person ever

elected President of the United States (Reagan was 69 years, 349 days old

when he assumed office)

Hillary Clinton’s age (turns 69 before the election, on October 26)

Average age of the 55 delegates that drafted the US Constitution in

Philadelphia in 1787 (35 of them had served as officers in the Continental

Army, and only 29 had college degrees)

Number of amendments put forth by 6 states during the ratification of the

US Constitution in 1788, most of which addressed fears of unchecked

Federal power

Percentage of times that the shorter candidate won the US Presidential

election during the entire 20th Century. The shorter candidate has won

75% of the 4 elections in the 21st Century (since 2000), a number that

would rise to 80% with a Clinton victory in 2016.

Electoral votes needed to win the US Presidential Election

Electoral votes in the “Blue Wall” (18 states & Washington DC which

have voted Democratic in each of the past 6 US Presidential elections)

Electoral votes in current 2016 election that are at least “leaning”

toward Clinton in recent aggregate polls (does not include 10 toss-up

states, and those “leaning” Republican)

Electoral votes in 10 “Toss-Up” states

Electoral votes in the “Red Wall” (13 states which have voted

Republican in each of the past 6 US Presidential elections)

Electoral votes in current 2016 election that are at least “leaning”

toward Trump in recent aggregate polls (does not include 10 toss-up

states, and those “leaning” Democrat)

Number of electoral votes in the 5 most electorally rich battleground

states: Florida (29), Pennsylvania (20), Ohio (18), North Carolina (15)

and Virginia (13)

The number of US states that split their electoral votes by district

between candidates (Maine and Nebraska)

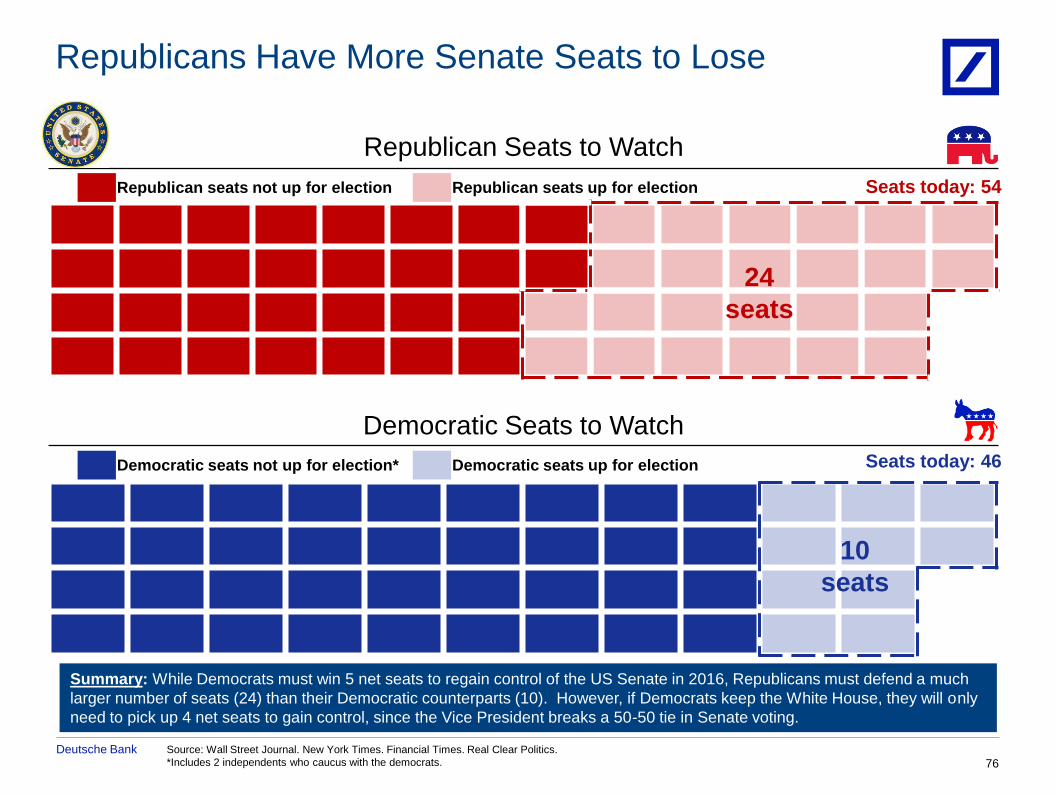

Number of net seats that Democrats must win to regain control of the

US Senate (4 if Clinton wins the White House, since the VP votes to

break 50-50 tie in the Senate)

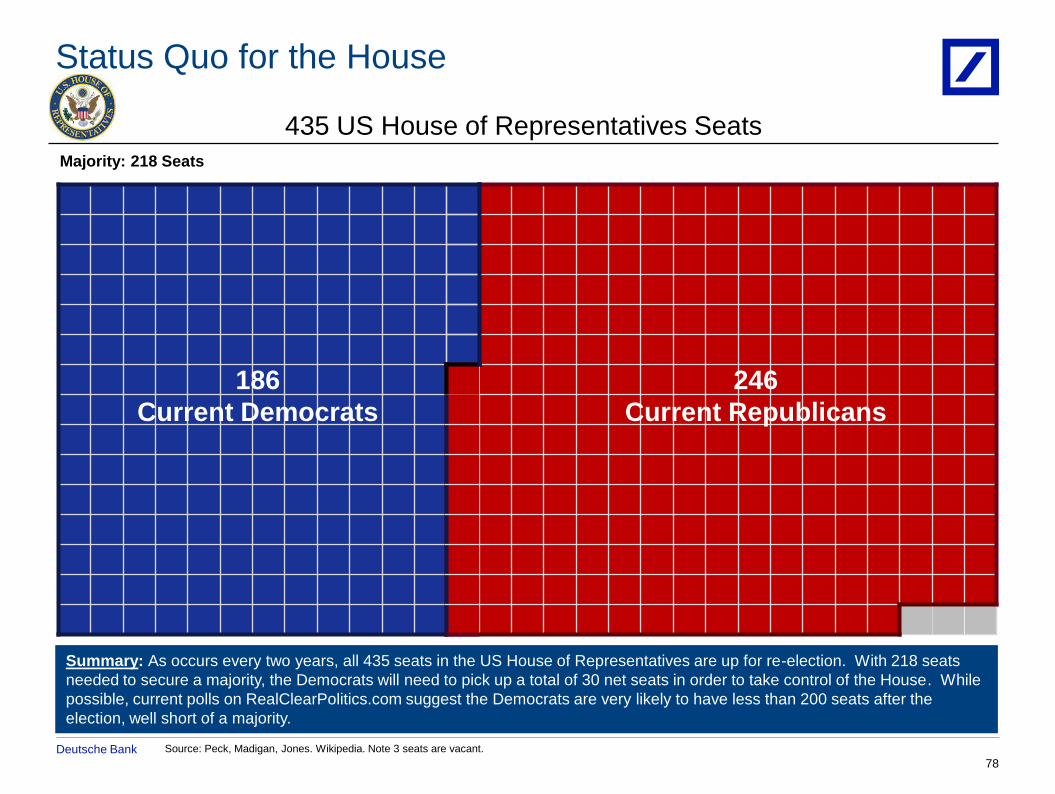

Number of net seats that Democrats must win to regain control of the

US House of Representatives (218 is a majority in the 435 member

chamber)

Percentage of voter turnout in 2012 US election (vs. 57% in 2008 and

56% in 2004)

Percentage of whites among eligible voters in the 2016 US election,

down from 84% in 1992 (and vs. 12% Blacks, 9% Hispanic and 2%

Asian in 2016)

270

242

256

102

170

2

5

70

18

59

64

0

27

405

112

70

68

Notable Numbers

30

95

55

44

124

25

The Election in Numbers

Source: CIB Capital Markets Strategy, Real Clear Politics, Wikipedia, DB 140 Weekender. Pew Research. Data as of Oct 17, 2016.

112

Deutsche Bank

I. Introduction

II. The Election

III. The Polls

IV. The Implications

Appendix:

A. GOP Leaders No Longer Supporting Trump

B. Summary of Republican and Democratic Party Platforms

C. The Senate and House Races

D. 50 Years of US Electoral College Maps

3

Markets & the US Election

Deutsche Bank

4

1. The Evolving Map

2. The Map Favors Democrats

3. Electoral College Math

4. The Path to 1600 Pennsylvania Ave

5. Large Battleground States

6. The New Vulnerables

7. The Third Rail

8. Shifting Demographics

9. The Importance of Turnout

10. A More Polarized Electorate

11. The Funding Advantage

12. The Ground Game

Markets & the US Election

II. The Election III. The Polls

13. This Election’s Big 3

14. Popular Vote Likely Close

15. Fading the Post Convention Bump

16. Temperament & Trust

17. Polling the Issues

18. Debates Can Matter

19. Higher Voter Engagement

20. The Gender Divide

21. Age Differences

22. Ethnicity & Race

23. Education & Income

24. The VP Impact

IV. The Implications

25. Transformational Change: Unlikely

26. Fiscal Stimulus: Yes, but Small

27. Growth: Numerous Channels

28. Volatility: The Uncertainty Principle

29. US Dollar: Modest Strengthening

30. At Risk Currencies: MXN & RMB

31. Fed Policy: Marginally More Hawkish

32. US Rates: Low Yields, Steeper Curve

33. US Credit: Extending the Cycle

34. US Equities: Sector Differentiation

35. Tax Reform: Still Difficult

36. Trade: Tide Shifting

Deutsche Bank

I. Introduction

Deutsche Bank

“I sought for the greatness and genius of America in her

commodious harbors and her ample rivers, and it was not

there…in her fertile fields and boundless forests, and it was not

there…in her rich mines and her vast world commerce, and it

was not there…in her democratic Congress and her matchless

Constitution, and it was not there. Not until I went into the

churches of America and heard her pulpits aflame with

righteousness did I understand the secret of her genius and

power. America is great because she is good, and if America

ever ceases to be good, she will cease to be great.”

-Alexis de Tocqueville, French political philosopher,

and author of “Democracy in America”

(1805 – 1859)

6

Deutsche Bank

10/17/2016

7

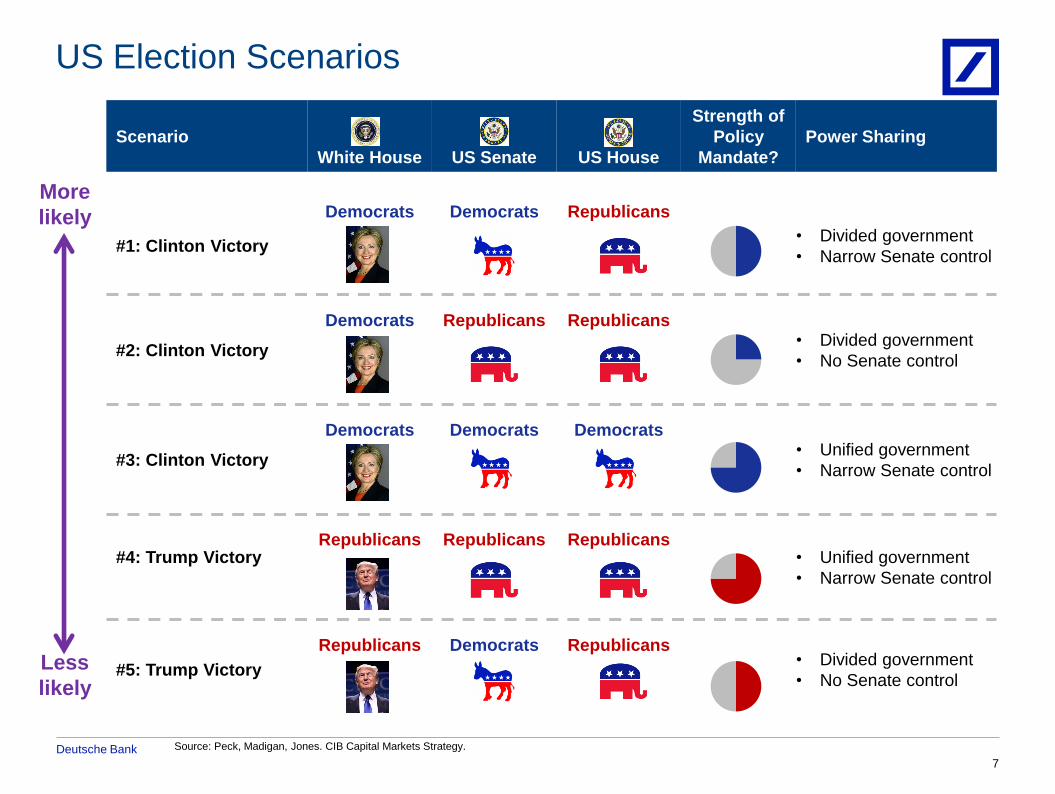

Source: Peck, Madigan, Jones. CIB Capital Markets Strategy.

US Election Scenarios

Scenario

White House US Senate US House

Strength of

Policy

Mandate?

Power Sharing

#1: Clinton Victory

Democrats Democrats Republicans

• Divided government

• Narrow Senate control

#2: Clinton Victory

Democrats Republicans Republicans

• Divided government

• No Senate control

#3: Clinton Victory

Democrats Democrats

Democrats

• Unified government

• Narrow Senate control

#4: Trump Victory

Republicans Republicans Republicans

• Unified government

• Narrow Senate control

#5: Trump Victory

Republicans Democrats Republicans • Divided government

• No Senate control

More

likely

Less

likely

Deutsche Bank 8

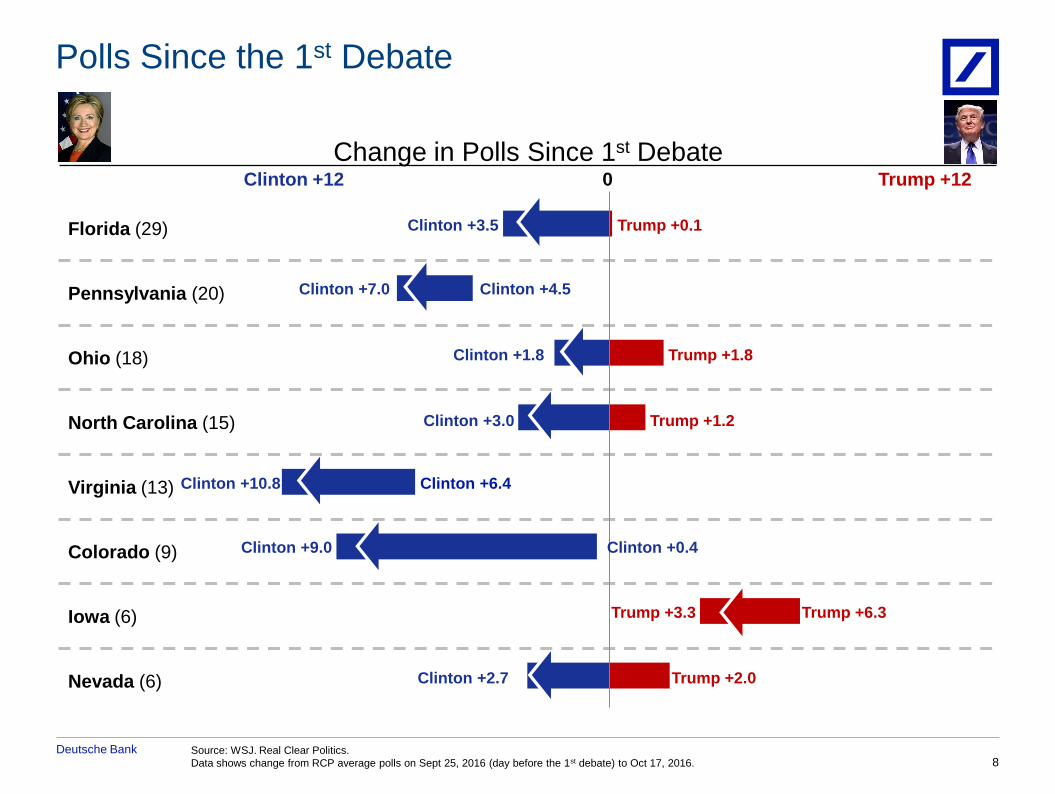

Source: WSJ. Real Clear Politics.

Data shows change from RCP average polls on Sept 25, 2016 (day before the 1st debate) to Oct 17, 2016.

Polls Since the 1st Debate

Change in Polls Since 1st Debate

Florida (29)

Pennsylvania (20)

Ohio (18)

North Carolina (15)

Virginia (13)

Colorado (9)

Iowa (6)

Nevada (6)

Clinton +12 0 Trump +12

Trump +0.1 Clinton +3.5

Clinton +4.5 Clinton +7.0

Trump +1.8 Clinton +1.8

Trump +1.2 Clinton +3.0

Clinton +6.4 Clinton +10.8

Clinton +0.4 Clinton +9.0

Trump +6.3 Trump +3.3

Trump +2.0 Clinton +2.7

Deutsche Bank Source: Real Clear Politics. Data as of Oct 17, 2016.

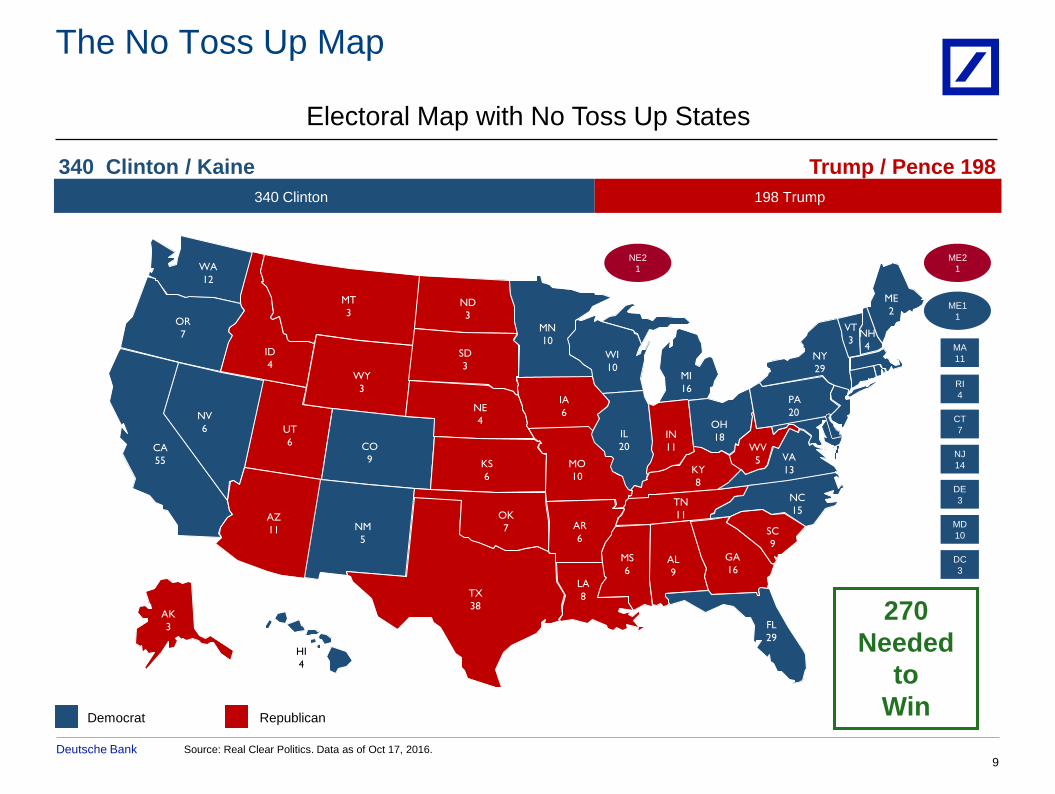

The No Toss Up Map

9

Recommendations and detected threats

OH

18 WV

5 VA

13

PA

20

NY

29

NC

15

SC

9

GA

16

TN

11

KY

8

IN

11

MI

16

WI

10

MN

10

IL

20

LA

8

OK

7

ID

4

NV

6

OR

7

WA

12

CA

55

NM

5

CO

9

WY

3

MT

3 ND

3

SD

3

IA

6

UT

6

FL

29

AR

6

MO

10

MS

6 AL

9

NE

4

KS

6

AK

3

HI

4

TX

38

ME

2

VT

3 NH

4

AZ

11

Republican Democrat

340 Clinton / Kaine Trump / Pence 198

340 Clinton 198 Trump

Electoral Map with No Toss Up States

270

Needed

to

Win

ME2

1

ME1

1

NE2

1

MA

11

RI

4

CT

7

NJ

14

DE

3

MD

10

DC

3

Deutsche Bank

10/17/2016

10

Source: Committee on Arrangements for the 2016 Republican National Convention. Democratic Platform Committee.

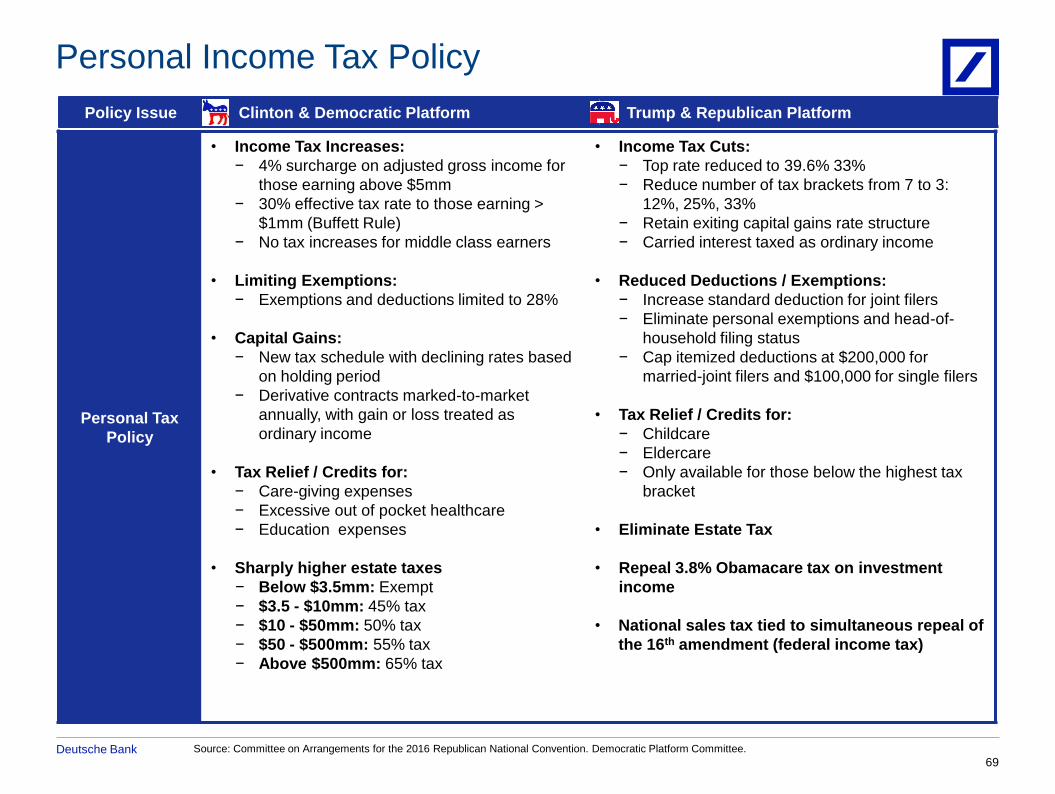

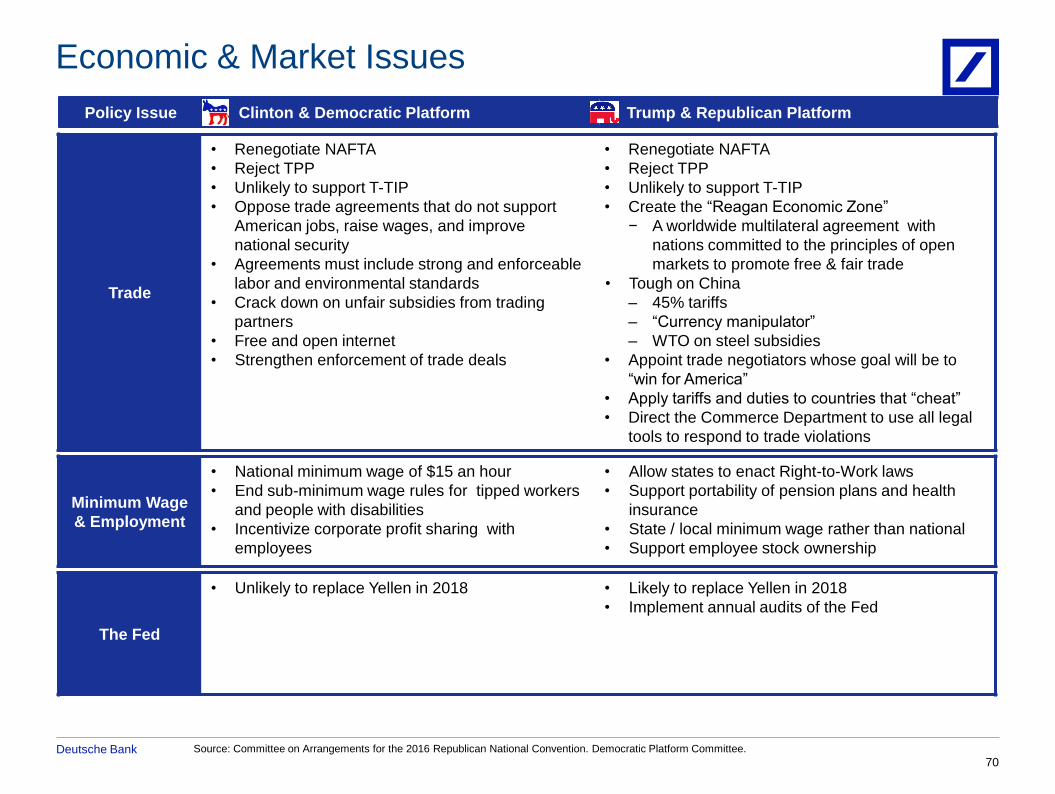

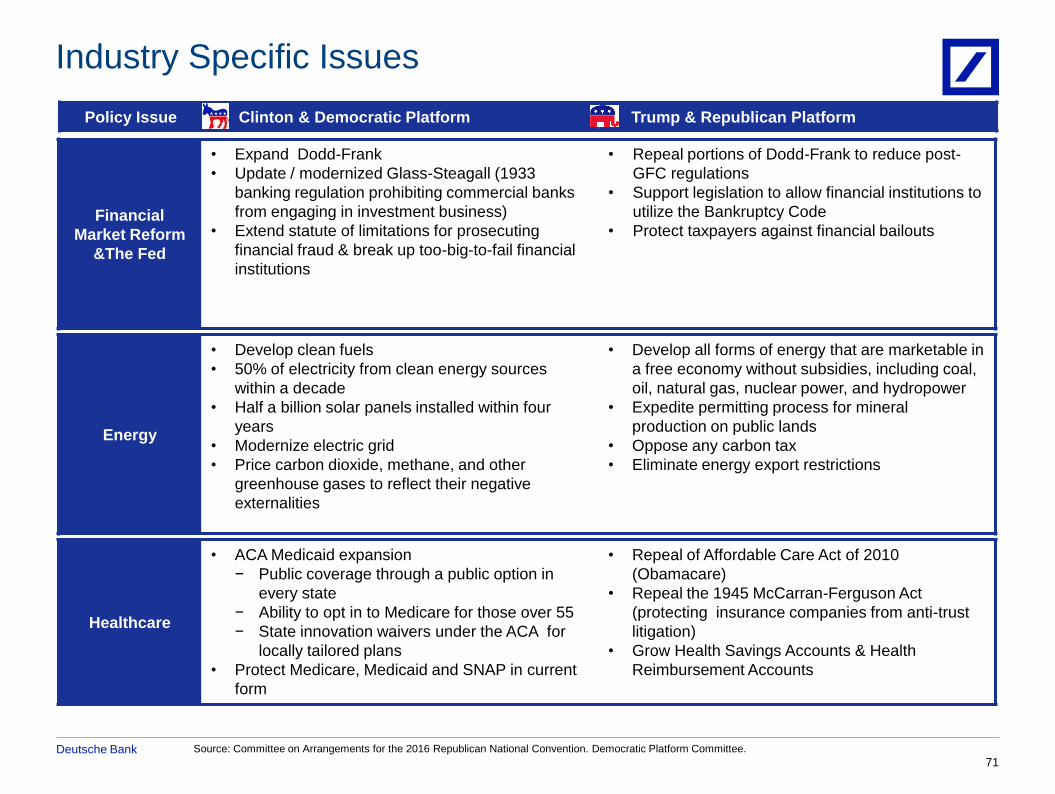

Policy Positions: The Economy

Clinton / Democrats Trump / Republicans

Trade & The Economy:

Fiscal stimulus

Renegotiate NAFTA

Reject TPP in current form

Tough on China (45% tariffs, “FX manipulator”, WTO on subsidies)

National minimum wage

The Fed:

Annual Fed audits

Likely replace Yellen in 2018

Industry Specific:

Repeal Affordable Care Act (Obamacare)

Repeal parts of Dodd-Frank

Modernize Glass-Steagall

“Risk fee” for large financials

Deregulate energy production & exports

Climate change initiatives

Deutsche Bank

10/17/2016

11

Source: Committee on Arrangements for the 2016 Republican National Convention. Democratic Platform Committee.

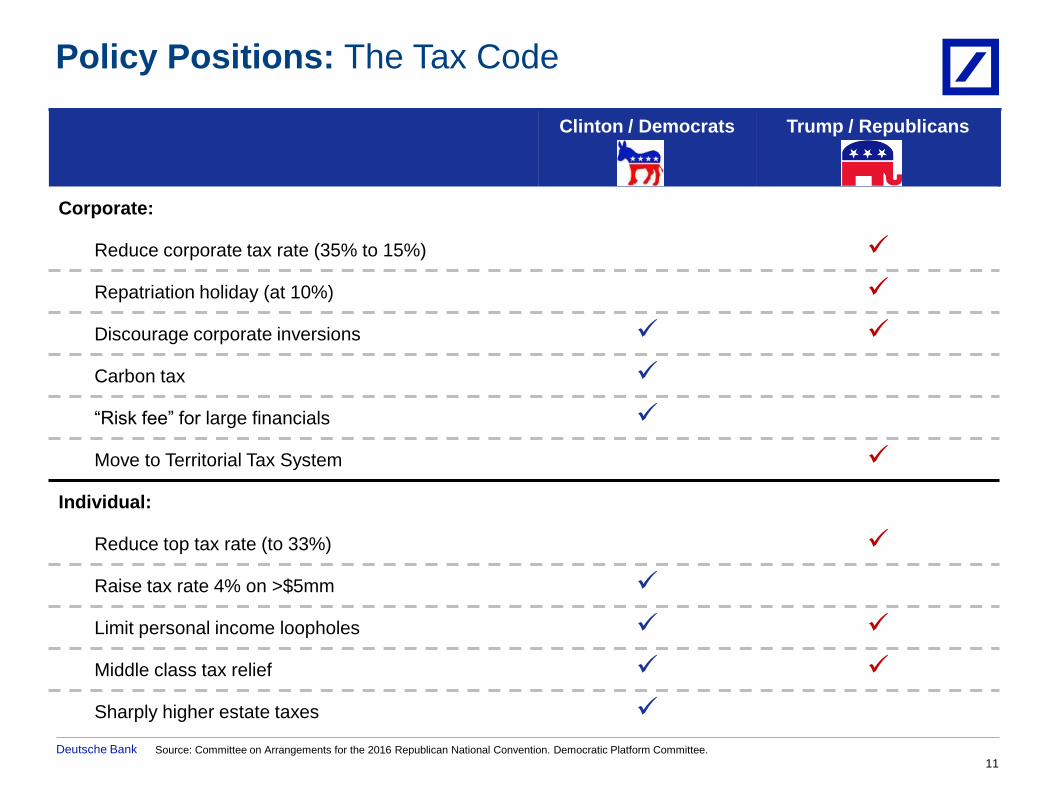

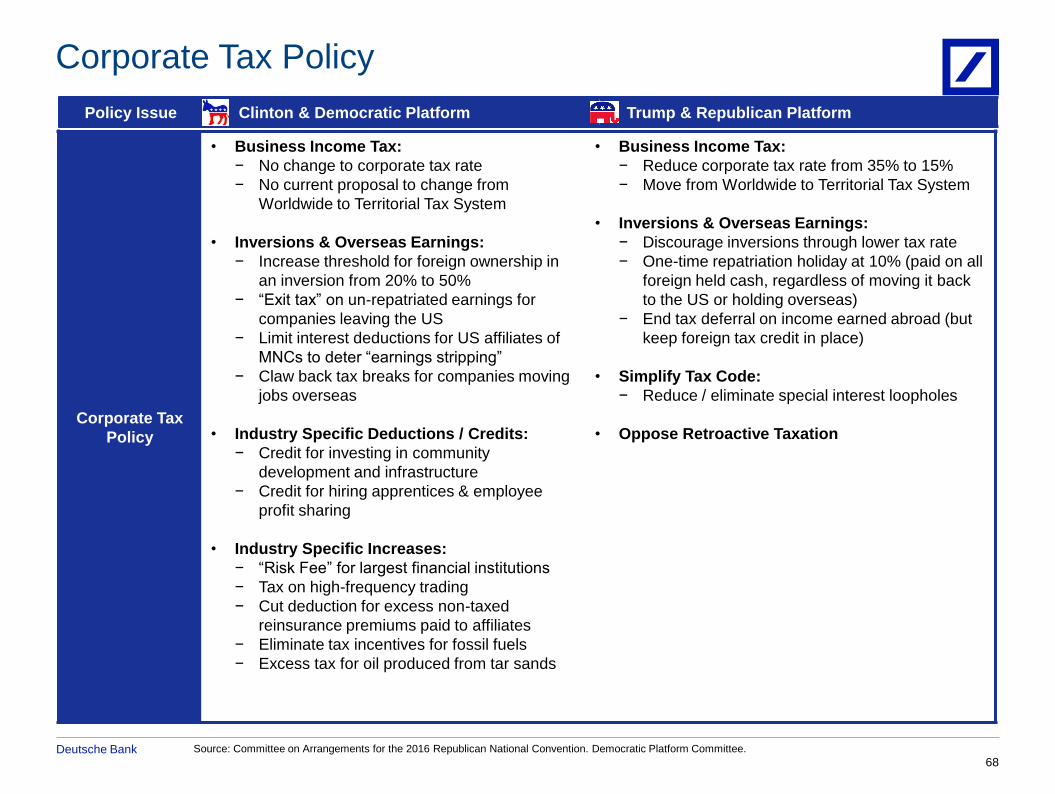

Policy Positions: The Tax Code

Clinton / Democrats Trump / Republicans

Corporate:

Reduce corporate tax rate (35% to 15%)

Repatriation holiday (at 10%)

Discourage corporate inversions

Carbon tax

“Risk fee” for large financials

Move to Territorial Tax System

Individual:

Reduce top tax rate (to 33%)

Raise tax rate 4% on >$5mm

Limit personal income loopholes

Middle class tax relief

Sharply higher estate taxes

Deutsche Bank

10/17/2016

12 Source: S&P Capital IQ, McGraw Hill Financial

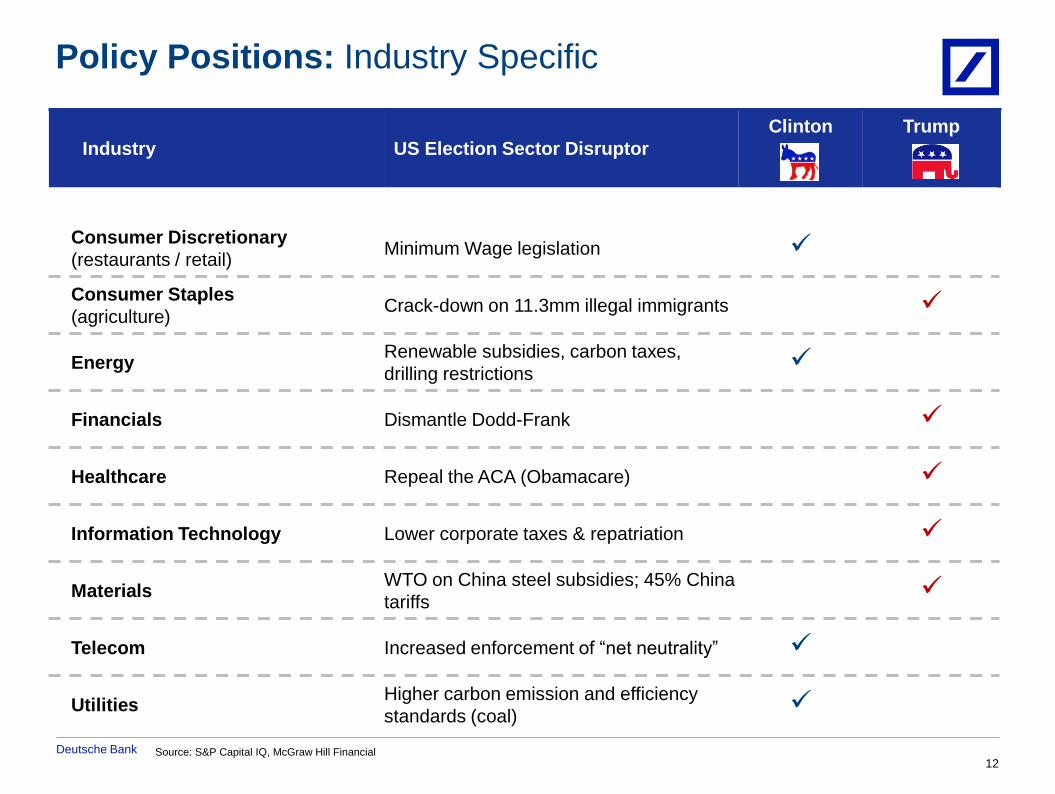

Policy Positions: Industry Specific

Industry

US Election Sector Disruptor

Clinton Trump

Consumer Discretionary

(restaurants / retail) Minimum Wage legislation

Consumer Staples

(agriculture) Crack-down on 11.3mm illegal immigrants

Energy Renewable subsidies, carbon taxes,

drilling restrictions

Financials Dismantle Dodd-Frank

Healthcare Repeal the ACA (Obamacare)

Information Technology Lower corporate taxes & repatriation

Materials WTO on China steel subsidies; 45% China

tariffs

Telecom Increased enforcement of “net neutrality”

Utilities Higher carbon emission and efficiency

standards (coal)

Deutsche Bank

10/17/2016

13

Source: DB Global Markets Research (Hsueh, Melentyev, Bianco, Konstam, Ruskin, Saravelos, Winkler).

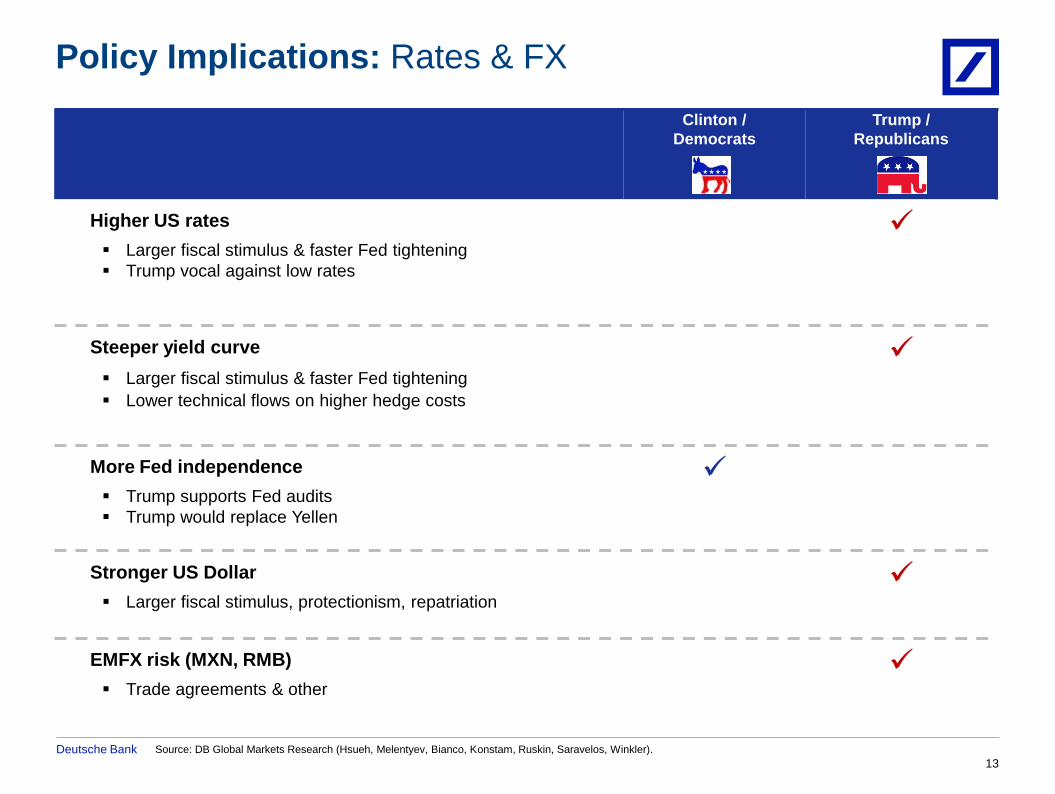

Policy Implications: Rates & FX

Clinton /

Democrats

Trump /

Republicans

Higher US rates

Larger fiscal stimulus & faster Fed tightening

Trump vocal against low rates

Steeper yield curve

Larger fiscal stimulus & faster Fed tightening

Lower technical flows on higher hedge costs

More Fed independence

Trump supports Fed audits

Trump would replace Yellen

Stronger US Dollar

Larger fiscal stimulus, protectionism, repatriation

EMFX risk (MXN, RMB)

Trade agreements & other

Deutsche Bank

10/17/2016

14

Source: DB Global Markets Research (Hsueh, Melentyev, Bianco, Konstam, Ruskin, Saravelos, Winkler).

Policy Implications: Oil, Credit & Equities

Clinton /

Democrats

Trump /

Republicans

Higher oil prices

Less oil market deregulation (i.e., less drilling)

Tighter credit spreads

Larger fiscal stimulus

Extends credit cycle length

Stronger corp balance sheets on repatriation

Higher credit issuance

Lower rates

Less funding needed if repatriation passed

Higher equity volatility

Unified Government more likely under Trump

Larger policy change & more uncertainty

Higher US equities

Global large caps

Smaller domestic

Deutsche Bank

10/17/2016

15

Source: Committee on Arrangements for the 2016 Republican National Convention. Democratic Platform Committee.

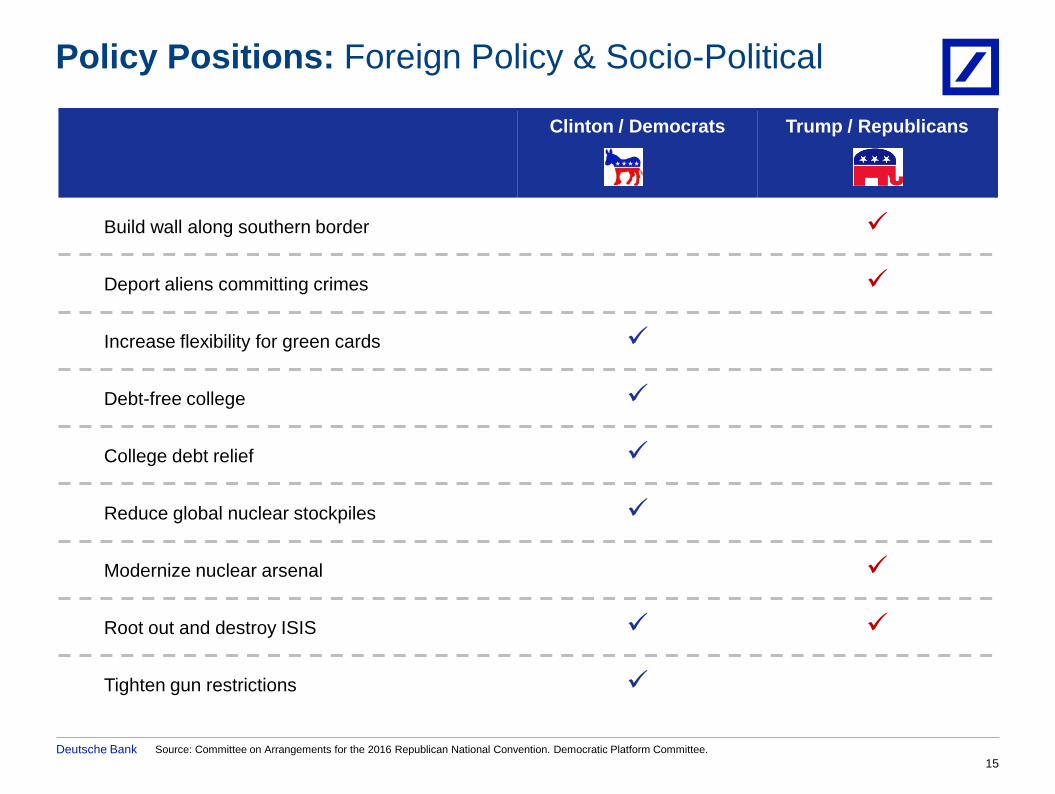

Policy Positions: Foreign Policy & Socio-Political

Clinton / Democrats Trump / Republicans

Build wall along southern border

Deport aliens committing crimes

Increase flexibility for green cards

Debt-free college

College debt relief

Reduce global nuclear stockpiles

Modernize nuclear arsenal

Root out and destroy ISIS

Tighten gun restrictions

Deutsche Bank

II. The Election

Deutsche Bank

“It has been frequently remarked, that it seems to have been

reserved to the people of this country to decide, by their conduct

and example, the important question, whether societies of men

are really capable or not, of establishing good government from

reflection and choice, or whether they are forever destined to

depend, for their political constitutions, on accident and force.”

-Alexander Hamilton, a Founding Father of the United States,

in Federalist Paper No. 1

(1755 - 1804)

17

Deutsche Bank

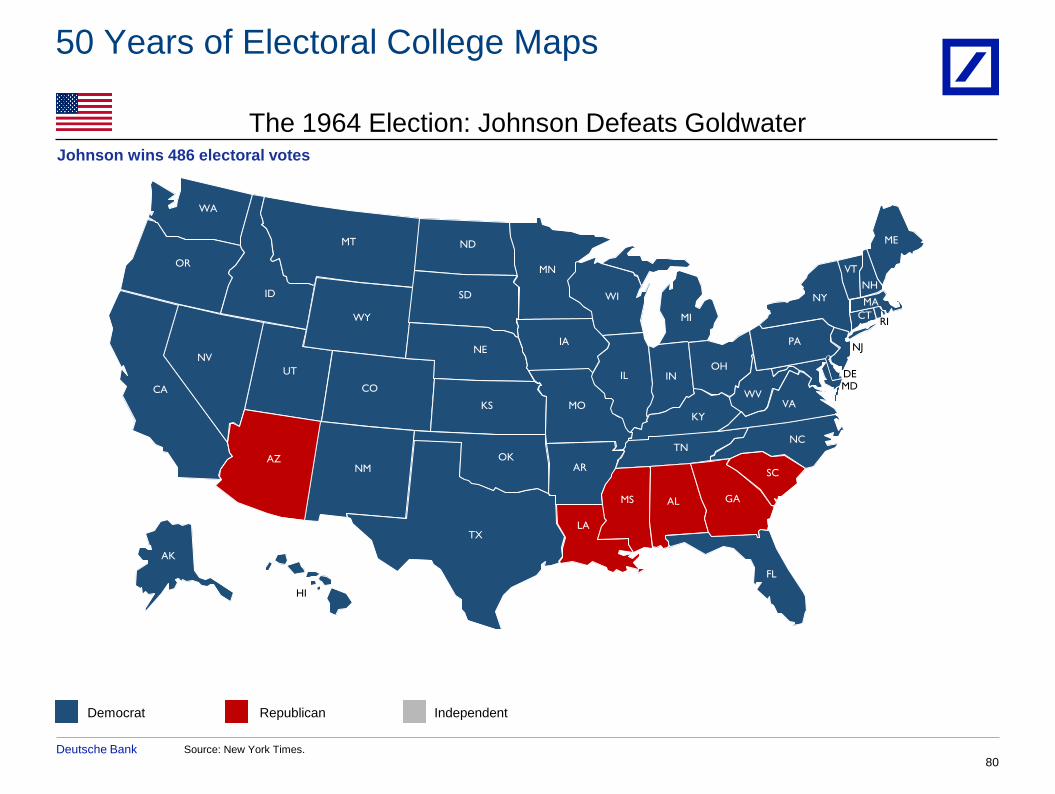

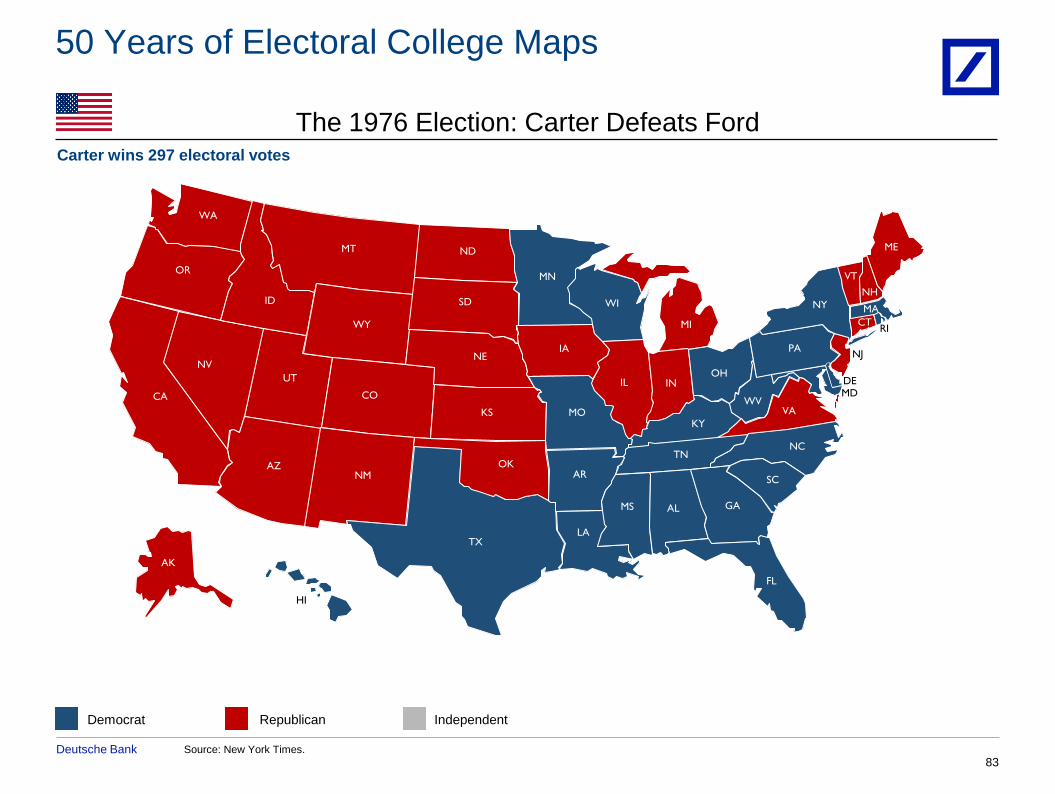

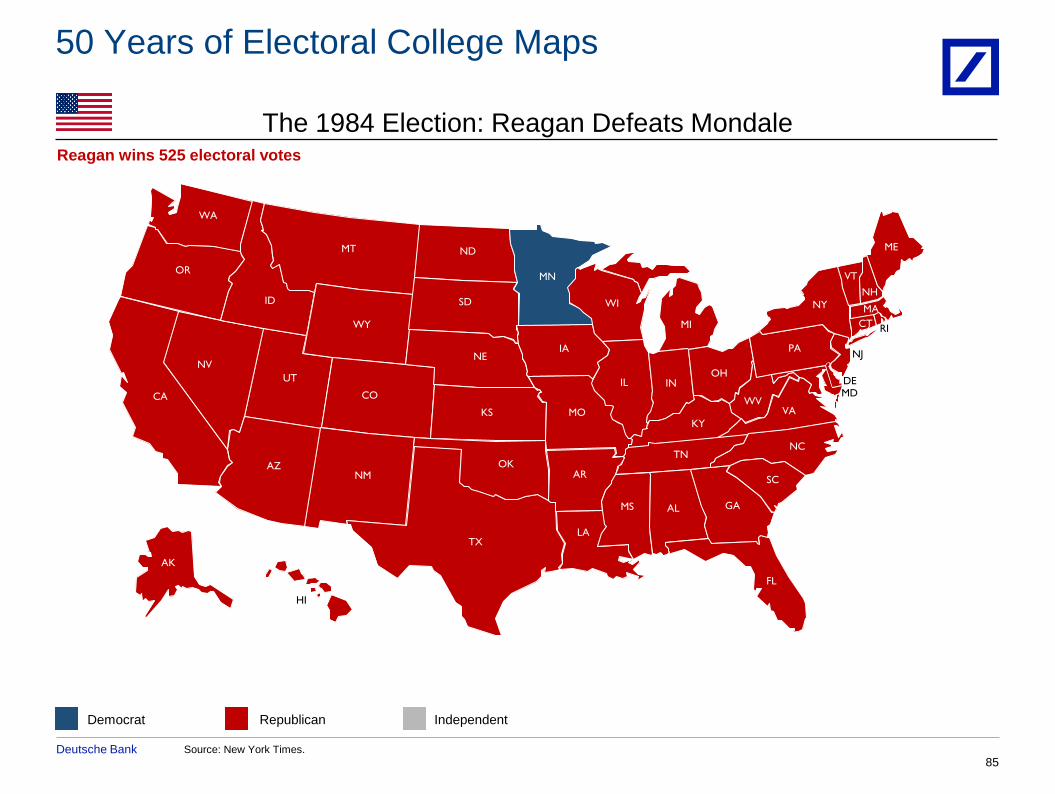

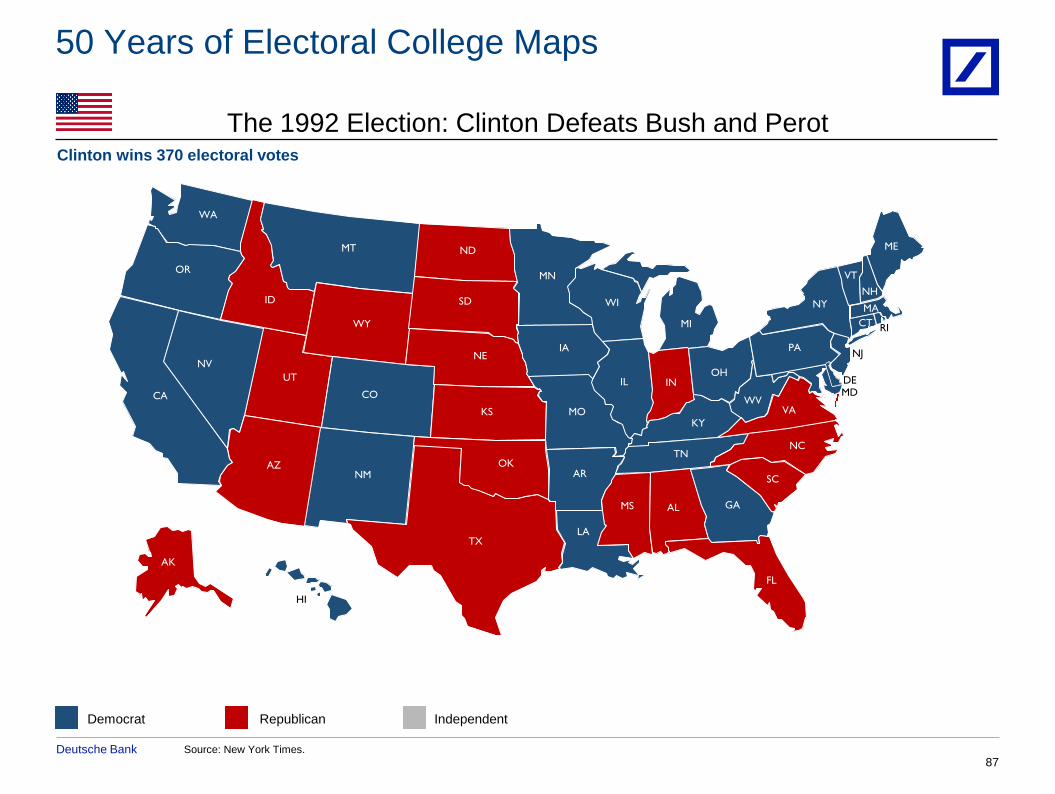

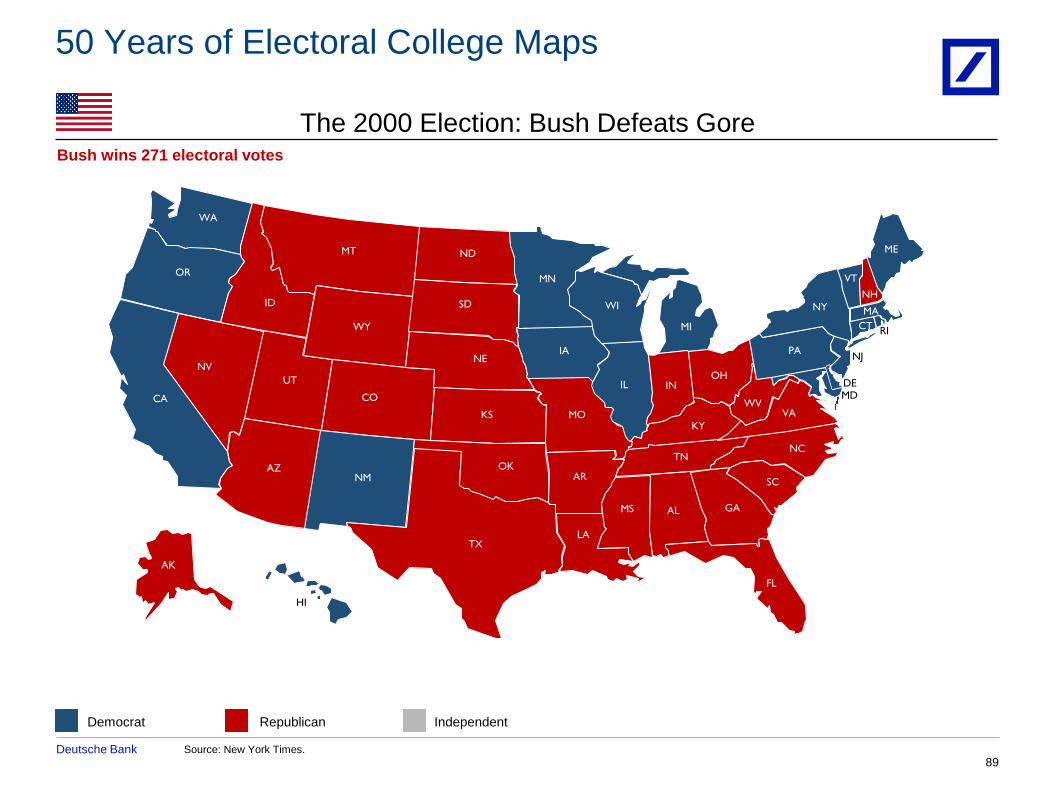

2000: Bush Defeats Gore

Source: New York Times. Peck, Madigan, and Jones.

18

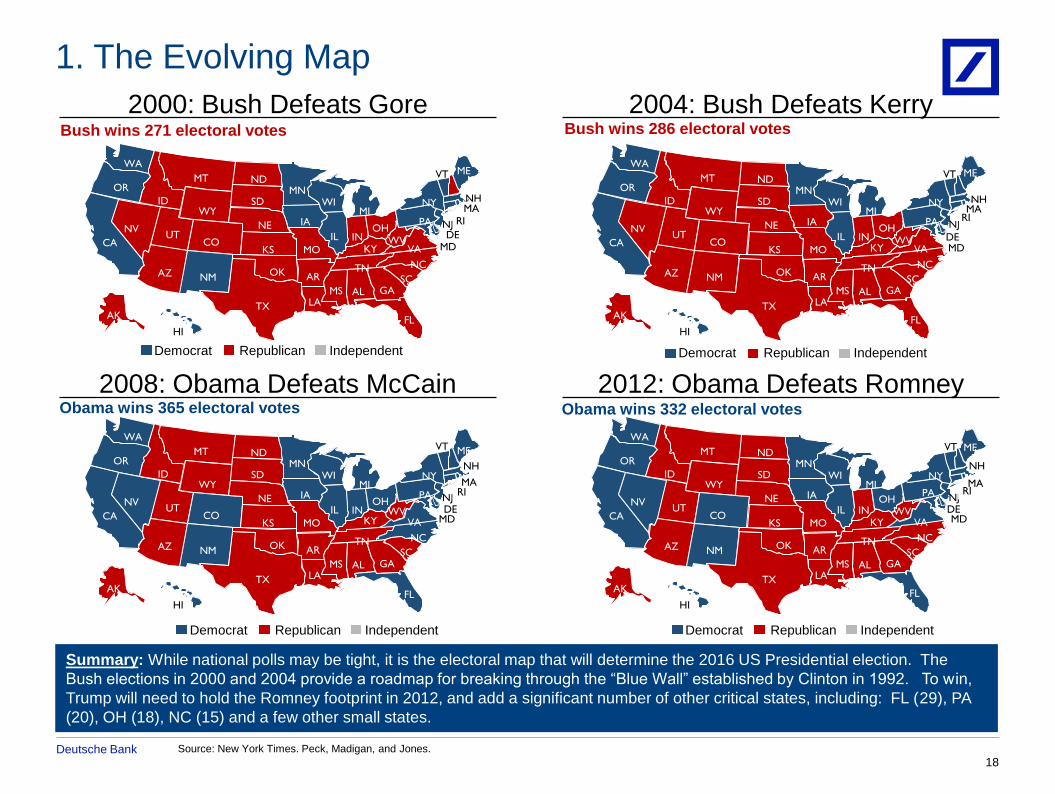

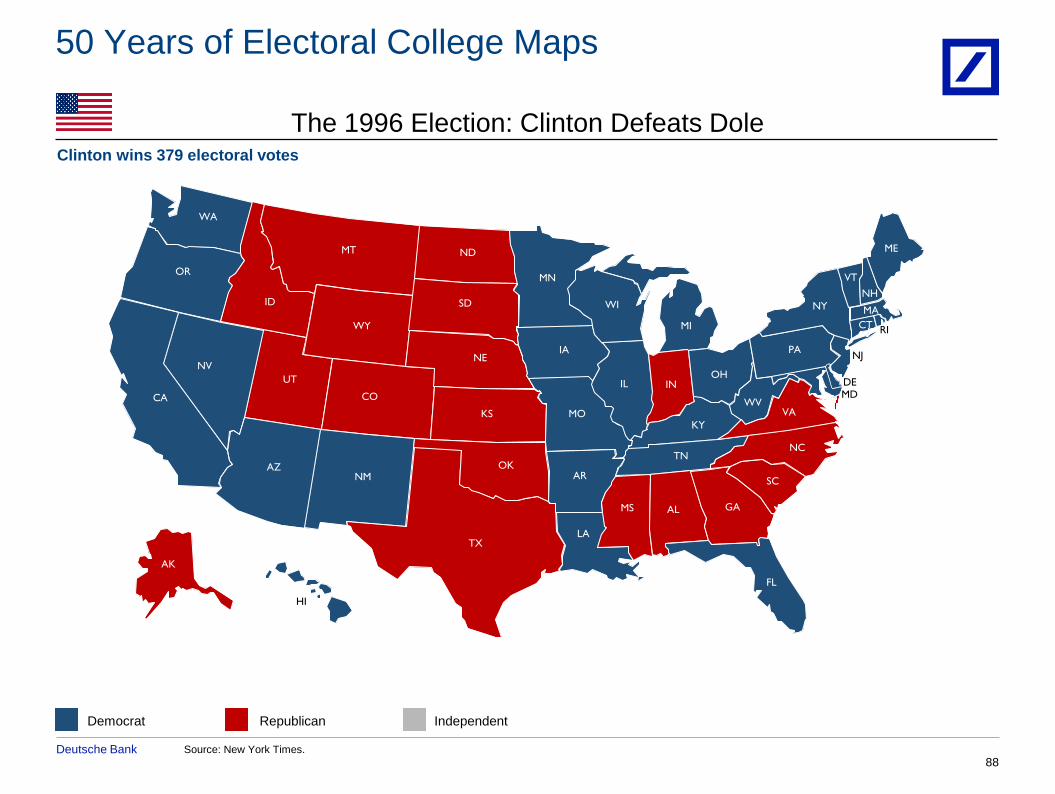

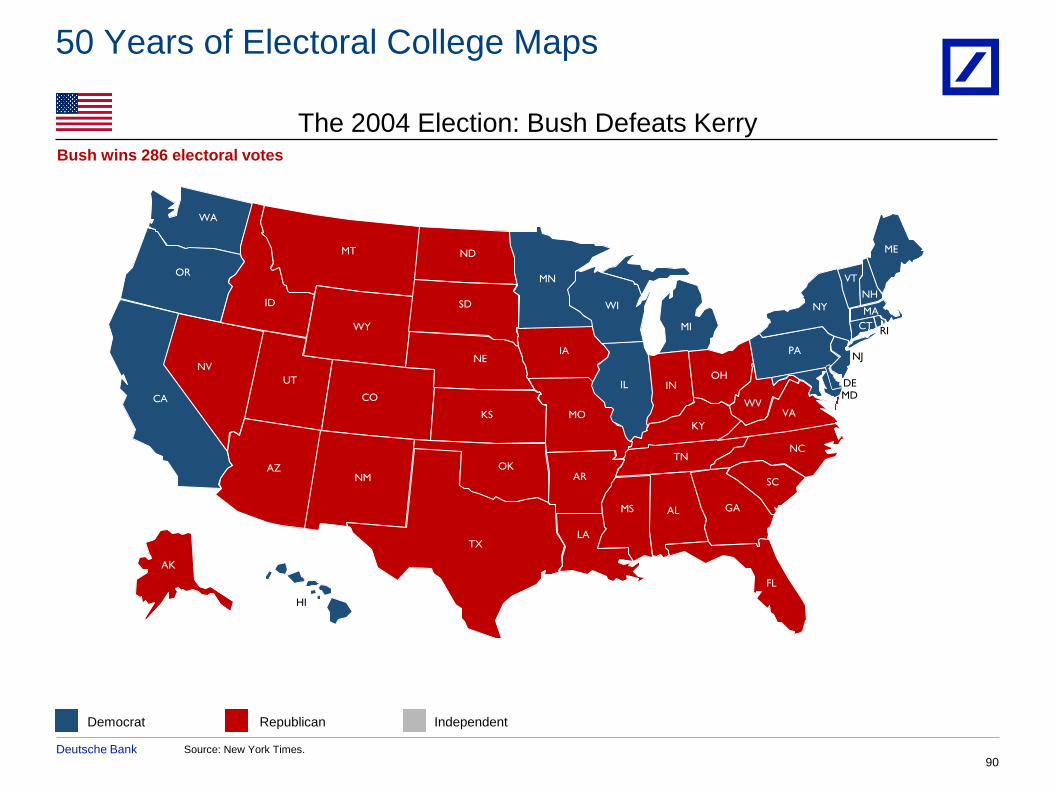

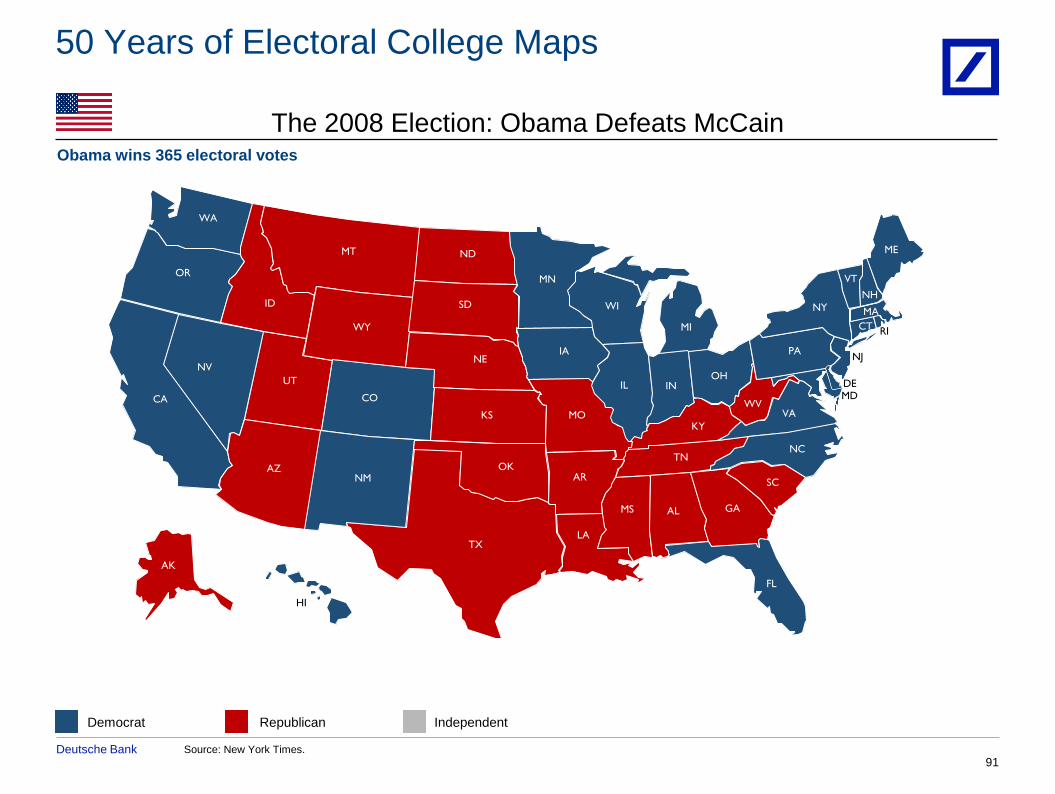

1. The Evolving Map

Summary: While national polls may be tight, it is the electoral map that will determine the 2016 US Presidential election. The

Bush elections in 2000 and 2004 provide a roadmap for breaking through the “Blue Wall” established by Clinton in 1992. To win,

Trump will need to hold the Romney footprint in 2012, and add a significant number of other critical states, including: FL (29), PA

(20), OH (18), NC (15) and a few other small states.

2004: Bush Defeats Kerry

2008: Obama Defeats McCain 2012: Obama Defeats Romney

RI

Recommendations

and detected

threats OH

WV VA

PA

NY

NC

SC GA

TN

KY IN

MI WI

MN

IL

LA

OK

ID

NV

OR

WA

CA

NM

CO

WY

MT ND

SD

IA

UT

FL

AR

MO

MS AL

NE

KS

NJ DE

MD

AK

HI

TX

ME VT

NH

C

T

AZ

MA

Independent Republican Democrat

Bush wins 271 electoral votes

RI

Recommendations

and detected

threats OH

WV VA

PA

NY

NC

SC GA

TN

KY IN

MI WI

MN

IL

LA

OK

ID

NV

OR

WA

CA

NM

CO

WY

MT ND

SD

IA

UT

FL

AR

MO

MS AL

NE

KS

NJ

DE MD

AK

HI

TX

ME VT

NH C

T

AZ

MA

Bush wins 286 electoral votes

RI

Recommendations

and detected

threats OH

WV VA

PA

NY

NC

SC GA

TN

KY IN

MI WI

MN

IL

LA

OK

ID

NV

OR

WA

CA

NM

CO

WY

MT ND

SD

IA

UT

FL

AR

MO

MS AL

NE

KS

NJ DE

MD

AK

HI

TX

ME VT

NH

C

T

AZ

MA

Obama wins 365 electoral votes

RI

Recommendations

and detected

threats OH

WV VA

PA

NY

NC

SC GA

TN

KY IN

MI WI

MN

IL

LA

OK

ID

NV

OR

WA

CA

NM

CO

WY

MT ND

SD

IA

UT

FL

AR

MO

MS AL

NE

KS

NJ DE MD

AK

HI

TX

ME VT

NH

C

T

AZ

MA

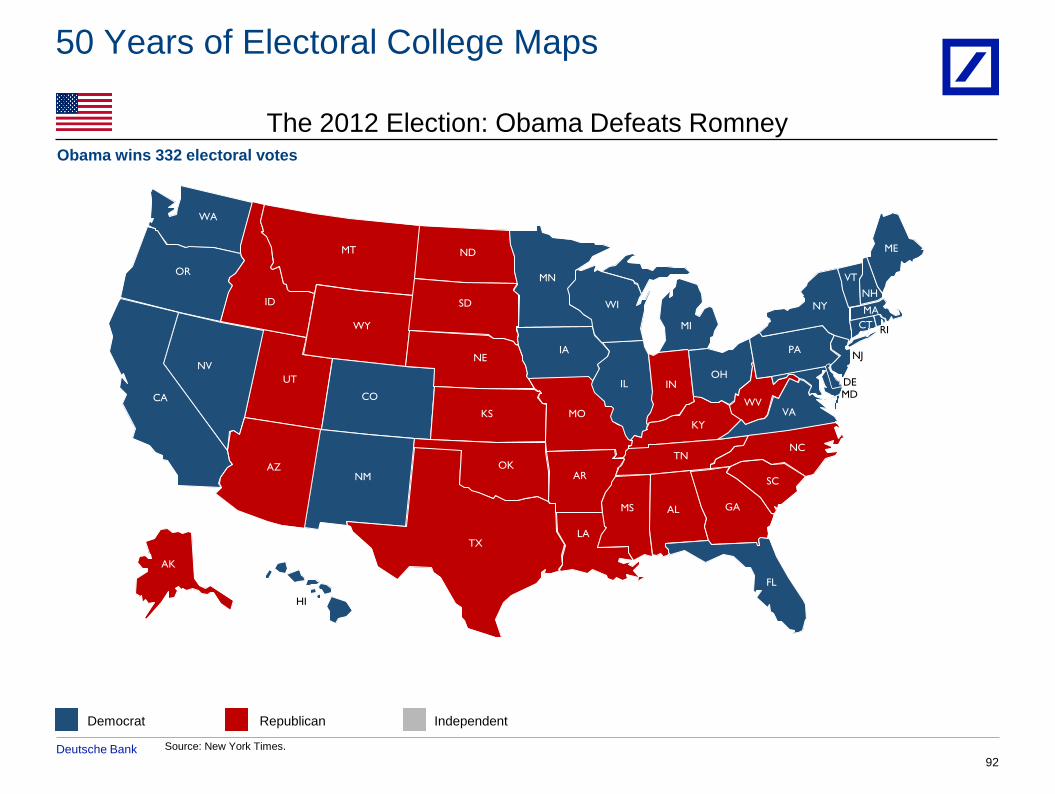

Obama wins 332 electoral votes

Independent Republican Democrat

Independent Republican Democrat Independent Republican Democrat

Deutsche Bank 19

Recommendations and detected

threats

OH

WV

VA

PA

NY

ME

NC

SC

GA

TN

KY

IN

MI

WI

MN

IL

LA TX

OK

ID

NV

OR

WA

CA

AZ

NM

CO

WY

MT ND

SD

IA

UT

FL

AR

MO

MS AL

NE

KS

VT

NH

MA

RI CT

NJ

DE

MD

AK

HI

DC

Source: Peck, Madigan & Jones. Data as of Oct 17, 2016.

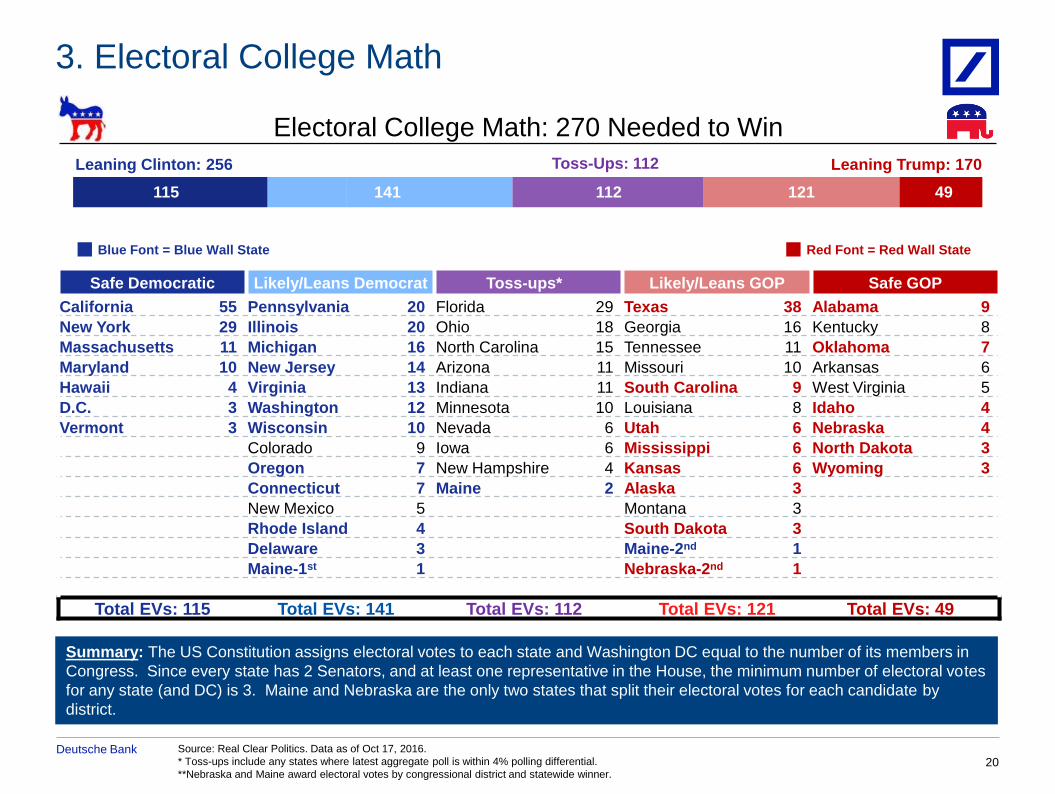

2. The Map Favors Democrats

Red and Blue Walls

Summary: The US electoral and demographic map favors Democrats. While Trump can absolutely win the election if voter

turnout and several key states go his way, he has fewer “paths to 270” given the historical strength of Democrats in a large block of

critical states.

• Blue Wall: 242 electoral votes

(18 states & DC have voted

Democratic in the past 6

elections)

• Leaning Dem in 2016: 256

electoral votes

• Toss-Up: 112 electoral votes

(10 competitive states)

• Red Wall: 102 electoral votes

(13 states voted GOP in past 6

elections)

• Leaning GOP in 2016: 170

electoral votes

Deutsche Bank Source: Real Clear Politics. Data as of Oct 17, 2016.

* Toss-ups include any states where latest aggregate poll is within 4% polling differential.

**Nebraska and Maine award electoral votes by congressional district and statewide winner.

20

Safe Democratic Likely/Leans Democrat Toss-ups* Likely/Leans GOP Safe GOP

California 55 Pennsylvania 20 Florida 29 Texas 38 Alabama 9

New York 29 Illinois 20 Ohio 18 Georgia 16 Kentucky 8

Massachusetts 11 Michigan 16 North Carolina 15 Tennessee 11 Oklahoma 7

Maryland 10 New Jersey 14 Arizona 11 Missouri 10 Arkansas 6

Hawaii 4 Virginia 13 Indiana 11 South Carolina 9 West Virginia 5

D.C. 3 Washington 12 Minnesota 10 Louisiana 8 Idaho 4

Vermont 3 Wisconsin 10 Nevada 6 Utah 6 Nebraska 4

Colorado 9 Iowa 6 Mississippi 6 North Dakota 3

Oregon 7 New Hampshire 4 Kansas 6 Wyoming 3

Connecticut 7 Maine 2 Alaska 3

New Mexico 5 Montana 3

Rhode Island 4 South Dakota 3

Delaware 3 Maine-2nd 1

Maine-1st 1 Nebraska-2nd 1

Total EVs: 115 Total EVs: 141 Total EVs: 112 Total EVs: 121 Total EVs: 49

3. Electoral College Math

Electoral College Math: 270 Needed to Win

Leaning Clinton: 256 Leaning Trump: 170

115 49 141 112 121

Summary: The US Constitution assigns electoral votes to each state and Washington DC equal to the number of its members in

Congress. Since every state has 2 Senators, and at least one representative in the House, the minimum number of electoral votes

for any state (and DC) is 3. Maine and Nebraska are the only two states that split their electoral votes for each candidate by

district.

Toss-Ups: 112

Red Font = Red Wall State Blue Font = Blue Wall State

Deutsche Bank

10/17/2016

21 Source: Peck, Madigan, Jones. Real Clear Politics. CIB Capital Markets Strategy. Data as of Oct 17, 2016.

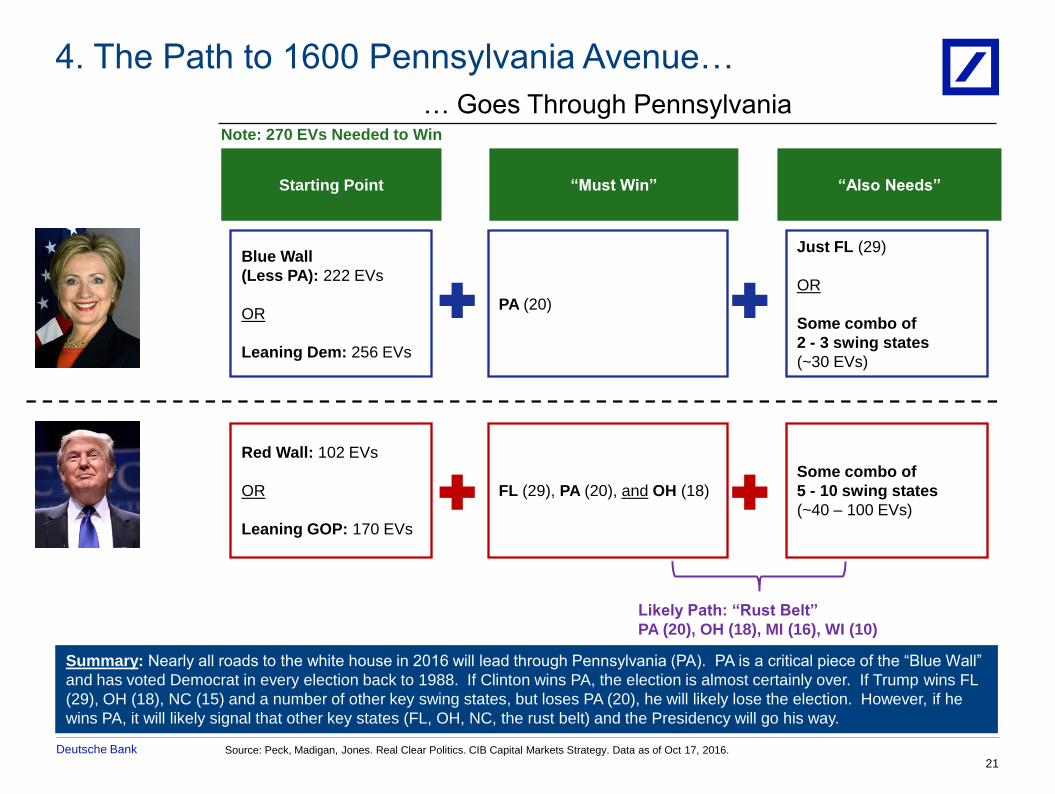

4. The Path to 1600 Pennsylvania Avenue…

Summary: Nearly all roads to the white house in 2016 will lead through Pennsylvania (PA). PA is a critical piece of the “Blue Wall”

and has voted Democrat in every election back to 1988. If Clinton wins PA, the election is almost certainly over. If Trump wins FL

(29), OH (18), NC (15) and a number of other key swing states, but loses PA (20), he will likely lose the election. However, if he

wins PA, it will likely signal that other key states (FL, OH, NC, the rust belt) and the Presidency will go his way.

Starting Point “Must Win” “Also Needs”

… Goes Through Pennsylvania

Blue Wall

(Less PA): 222 EVs

OR

Leaning Dem: 256 EVs

Red Wall: 102 EVs

OR

Leaning GOP: 170 EVs

PA (20)

FL (29), PA (20), and OH (18)

Just FL (29)

OR

Some combo of

2 - 3 swing states

(~30 EVs)

Some combo of

5 - 10 swing states

(~40 – 100 EVs)

Likely Path: “Rust Belt”

PA (20), OH (18), MI (16), WI (10)

Note: 270 EVs Needed to Win

Deutsche Bank

Feb-2016 Jun-2016

Mar-2016 Jul-2016

Feb-2016 Aug-2016

30%

40%

50%

Feb-2016 Jul-2016

30%

40%

50%

Mar-2016 Jul-2016

Clinton +7.0pts

Pennsylvania (20 EVs)

Source: Real Clear Politics. Data based on Real Clear Politics averages from most recent polls available. Wall Street Journal. Data as of Oct 17, 2016. *Number

of electoral votes. Start date in each box above based on varying data availability by state. 22

Clinton +10.8pts

Ohio (18 EVs) North Carolina (15 EVs) Virginia (13 EVs)

Florida (29 EVs*)

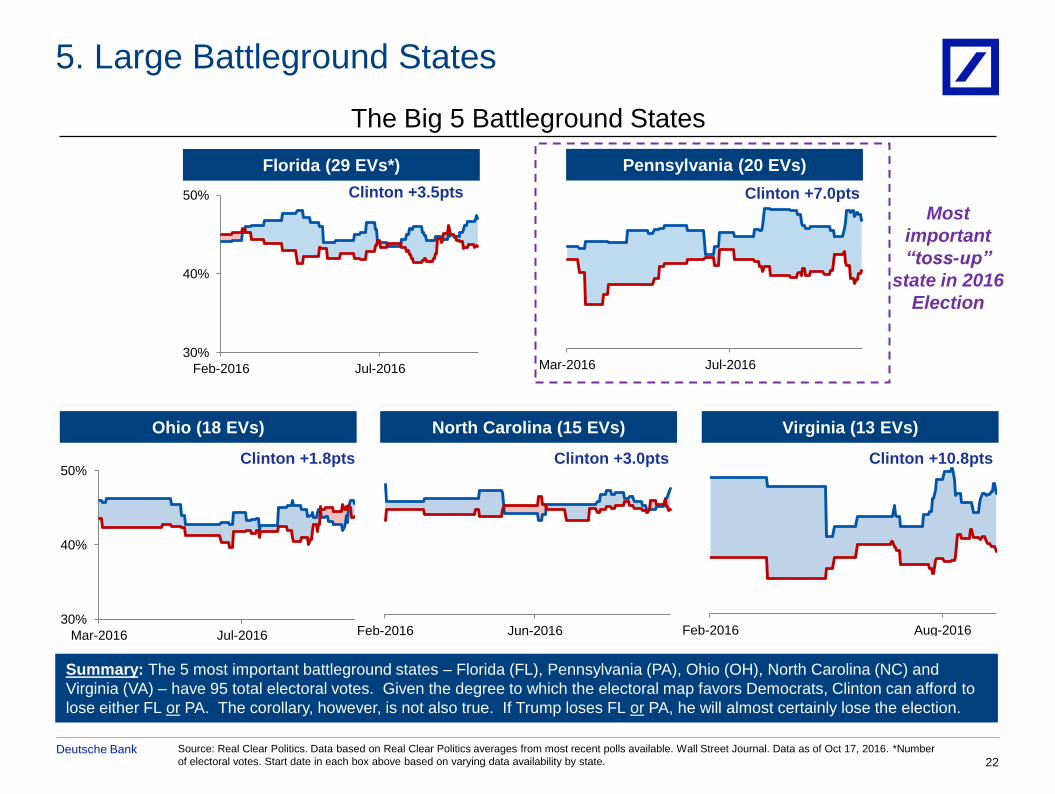

5. Large Battleground States

The Big 5 Battleground States

Clinton +1.8pts Clinton +3.0pts

Most

important

“toss-up”

state in 2016

Election

Clinton +3.5pts

Summary: The 5 most important battleground states – Florida (FL), Pennsylvania (PA), Ohio (OH), North Carolina (NC) and

Virginia (VA) – have 95 total electoral votes. Given the degree to which the electoral map favors Democrats, Clinton can afford to

lose either FL or PA. The corollary, however, is not also true. If Trump loses FL or PA, he will almost certainly lose the election.

Deutsche Bank

Feb-2016 Jun-2016

30%

40%

50%

Jun-2016 Aug-2016

30%

40%

50%

May-2016 Sep-2016

Clinton +2.7pts

10/17/2016

23

Source: Real Clear Politics. EV denotes # of electoral votes for each state. 270 electoral votes required to win. Data as of Oct 17, 2016.

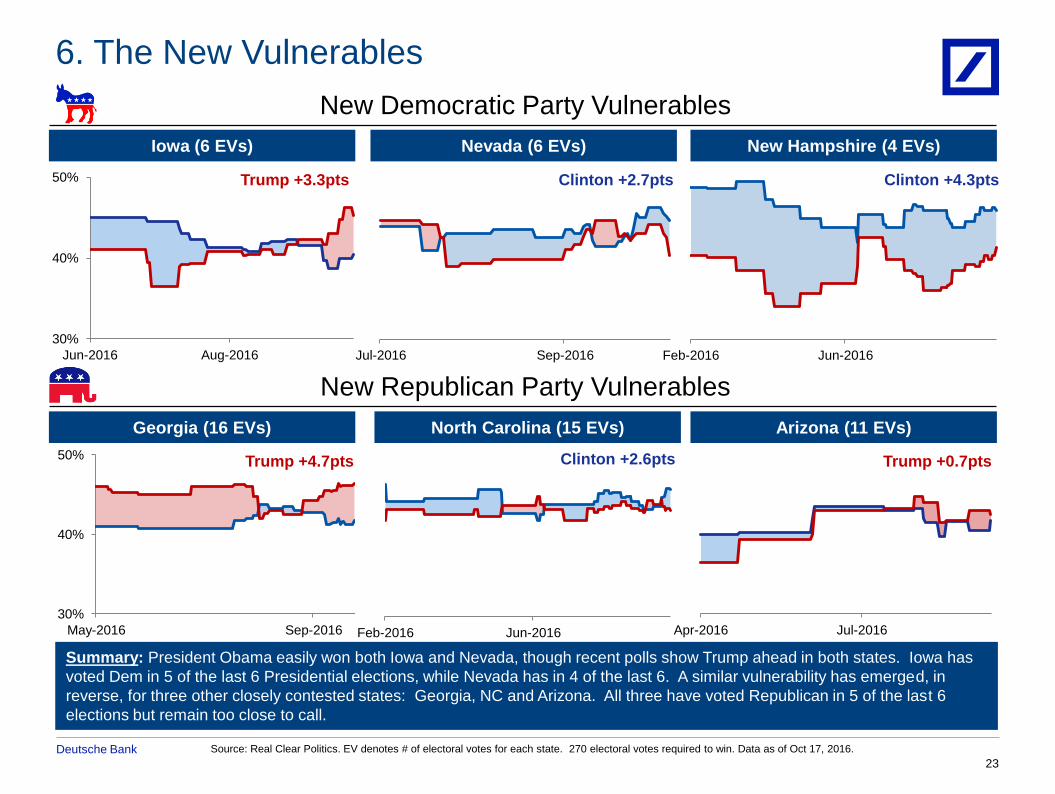

6. The New Vulnerables

New Democratic Party Vulnerables

Iowa (6 EVs) Nevada (6 EVs)

Trump +3.3pts Clinton +4.3pts

New Hampshire (4 EVs)

Georgia (16 EVs) Arizona (11 EVs) North Carolina (15 EVs)

Trump +4.7pts

New Republican Party Vulnerables

Summary: President Obama easily won both Iowa and Nevada, though recent polls show Trump ahead in both states. Iowa has

voted Dem in 5 of the last 6 Presidential elections, while Nevada has in 4 of the last 6. A similar vulnerability has emerged, in

reverse, for three other closely contested states: Georgia, NC and Arizona. All three have voted Republican in 5 of the last 6

elections but remain too close to call.

Trump +0.7pts Clinton +2.6pts

Apr-2016 Jul-2016

Jul-2016 Sep-2016 Feb-2016 Jun-2016

Deutsche Bank

Clinton Trump Johnson /

Stein

Florida (29) 46.0 42.5 5.8

Pennsylvania (20) 46.7 39.7 7.4

Ohio (18) 44.0 42.4 8.4

Georgia (16) 40.5 46.0 6.5

North Carolina (15) 45.0 42.1 9.3

Virginia (13) 45.0 36.3 8.8

Arizona (11) 41.0 42.0 10.0

Iowa (6) 38.0 41.7 10.0

Nevada (6) 43.2 41.8 7.4

New Hampshire (4) 43.3 39.7 8.3

10/17/2016

24

Source: Real Clear Politics. Seattle Times. Financial Times. Johnson/Stein shows compiled polling info for the two candidates.

Data as of Oct 17, 2016.

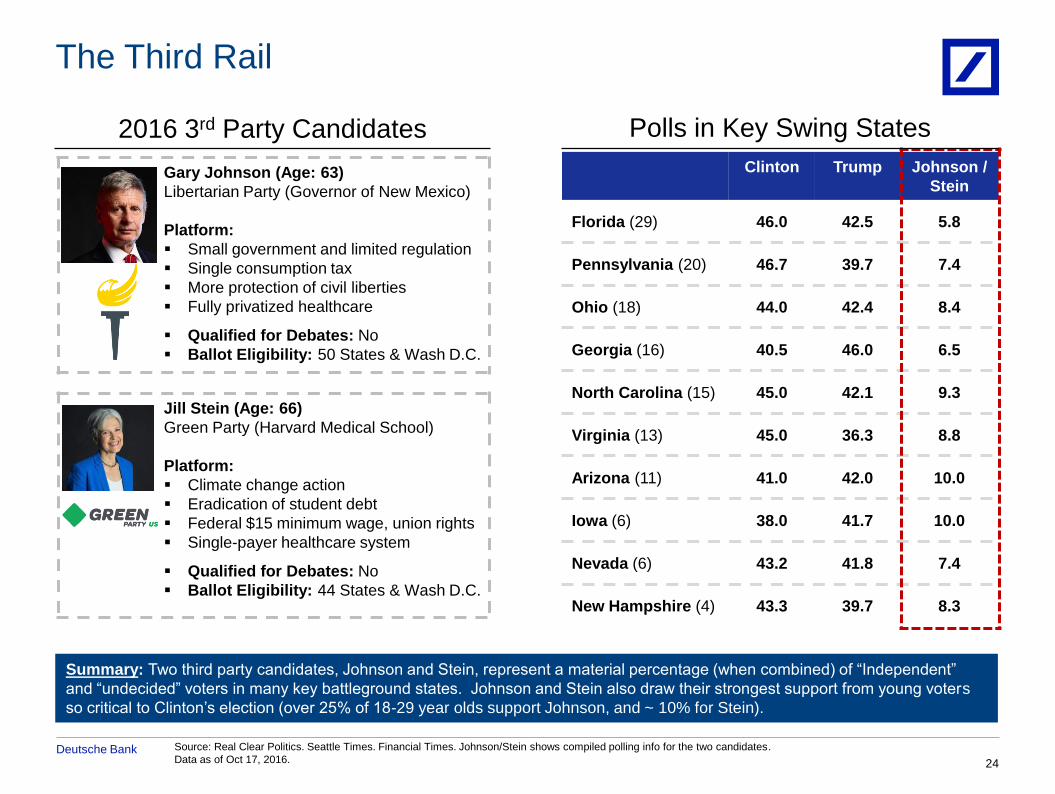

The Third Rail

2016 3rd Party Candidates Polls in Key Swing States

Gary Johnson (Age: 63)

Libertarian Party (Governor of New Mexico)

Platform:

Small government and limited regulation

Single consumption tax

More protection of civil liberties

Fully privatized healthcare

Qualified for Debates: No

Ballot Eligibility: 50 States & Wash D.C.

Jill Stein (Age: 66)

Green Party (Harvard Medical School)

Platform:

Climate change action

Eradication of student debt

Federal $15 minimum wage, union rights

Single-payer healthcare system

Qualified for Debates: No

Ballot Eligibility: 44 States & Wash D.C.

Summary: Two third party candidates, Johnson and Stein, represent a material percentage (when combined) of “Independent”

and “undecided” voters in many key battleground states. Johnson and Stein also draw their strongest support from young voters

so critical to Clinton’s election (over 25% of 18-29 year olds support Johnson, and ~ 10% for Stein).

Deutsche Bank

5 9

10

12

2

1

7

84%

70%

'92 '16

23

33

26

33

50%

33%

'92 '16

10/17/2016

25 Source: Peck, Madigan, Jones. Pew Research Center. Cook Political Report. Associated Press.

8. Shifting Demographics

Race & Ethnicity

Summary: Since 1992, the US electorate has become more educated, more ethnically diverse, and older. However, these

changes have impacted the two major parties differently. According to Pew Research, the Democratic Party is becoming less

white, less religious and better educated at a faster rate than the country. In contrast, Republican voter trends have been slower

than the national rate on these metrics, while aging at a comparatively more rapid pace.

Changing Demographic Profile of American Voters (1992 – 2016)

Education Age

White

Other Asian

Black

Hispanic

High

school

or less

Some

college

College

degree+

18-29

30-49

50-64

65+ 19 21

21

30

40

31

19% 16%

'92 '16

Deutsche Bank

Black

White

Hispanic

Asian

Female

Male

Silent/Greatest (>71)

Boomers (52-70)

Gen X (36-51)

Millennial (18-35)

10/17/2016

26

Source: Upshot estimates. Real Clear Politics, Peck, Madigan, and Jones. *Romney’s share of white working class vote, share Trump would need (estimate), share

Trump would need with 5 pts less support from Hispanic voters and college-educated whites.

9. The Importance of Turnout

2012 US Election Turnout

Estimated White Vote Needed for

Trump in Key Swing States

Summary: In 2012, Romney won 59% of the white vote (highest ever by a GOP candidate against an incumbent), and 17% of the

non-white vote in the 2012 election. To win, Trump will need the largest white male turnout in history, while Clinton will need strong

numbers from women, youth, Hispanics and African Americans.

55%

67%

64%

48%

47%

64%

60%

72%

69%

61%

46%

Total Eligible Voters:

By Ethnicity:

By Gender:

By Age:

State (EVs)

Romney’s

Share

Share Trump

Needs

Share with

5 pts less*

Florida (29) 64% 67% 72%

Pennsylvania (20) 56% 61% 64%

Ohio (18) 55% 58% 61%

Michigan (16) 53% 62% 65%

North Carolina (15) 70% 68% 71%

Virginia (13) 66% 72% 77%

Wisconsin (10) 50% 57% 60%

Minnesota (10) 49% 57% 61%

Colorado (9) 55% 63% 69%

Oregon (7) 47% 58% 62%

Iowa (6) 50% 56% 58%

Nevada (6) 58% 67% 72%

New Hampshire (4) 51% 56% 59%

Deutsche Bank

10/17/2016

27

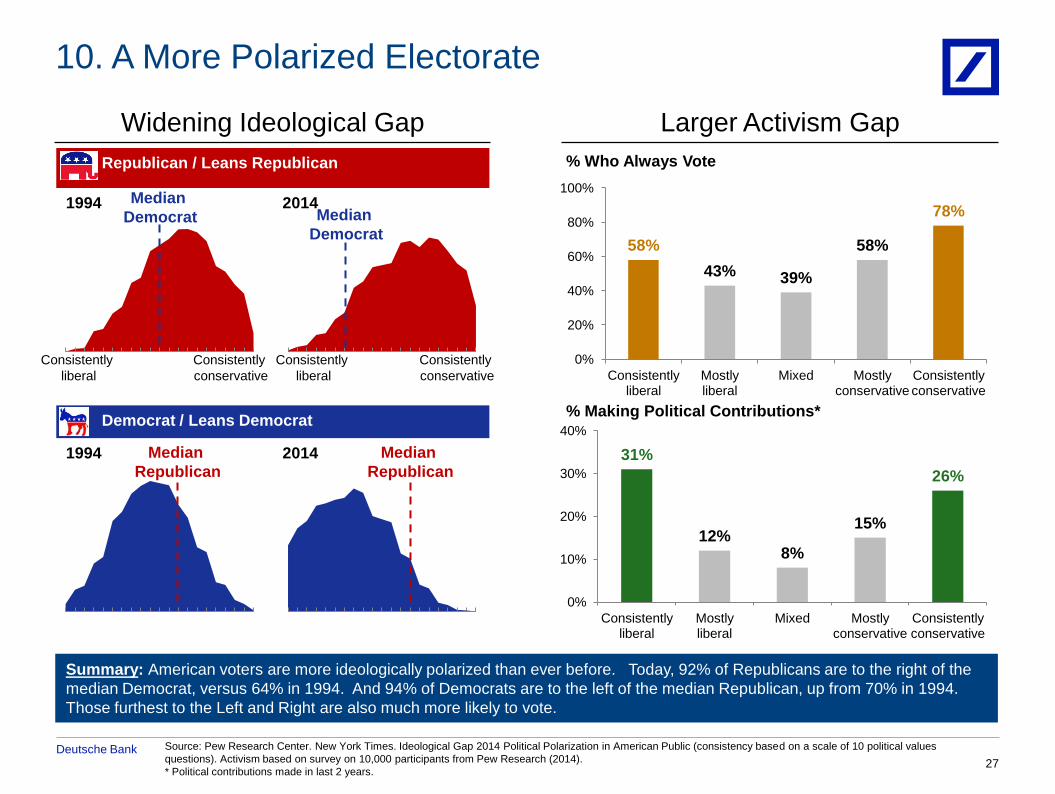

10. A More Polarized Electorate

Summary: American voters are more ideologically polarized than ever before. Today, 92% of Republicans are to the right of the

median Democrat, versus 64% in 1994. And 94% of Democrats are to the left of the median Republican, up from 70% in 1994.

Those furthest to the Left and Right are also much more likely to vote.

Source: Pew Research Center. New York Times. Ideological Gap 2014 Political Polarization in American Public (consistency based on a scale of 10 political values

questions). Activism based on survey on 10,000 participants from Pew Research (2014).

* Political contributions made in last 2 years.

Widening Ideological Gap Larger Activism Gap

% Who Always Vote

% Making Political Contributions*

58%

43% 39%

58%

78%

0%

20%

40%

60%

80%

100%

Consistently liberal

Mostly liberal

Mixed Mostly conservative

Consistently conservative

31%

12% 8%

15%

26%

0%

10%

20%

30%

40%

Consistently liberal

Mostly liberal

Mixed Mostly conservative

Consistently conservative

Republican / Leans Republican

1994 2014

Democrat / Leans Democrat

1994 2014

Median

Democrat

Consistently

liberal

Consistently

conservative

Median

Republican

Median

Democrat

Consistently

liberal

Consistently

conservative

Median

Republican

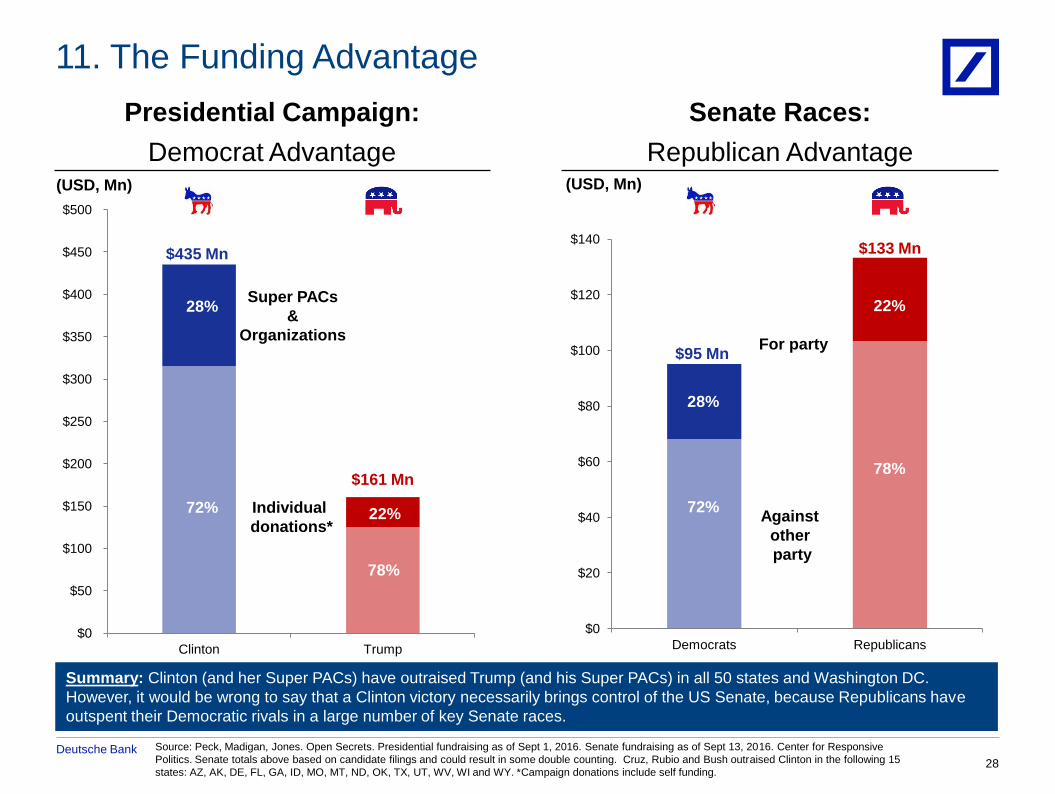

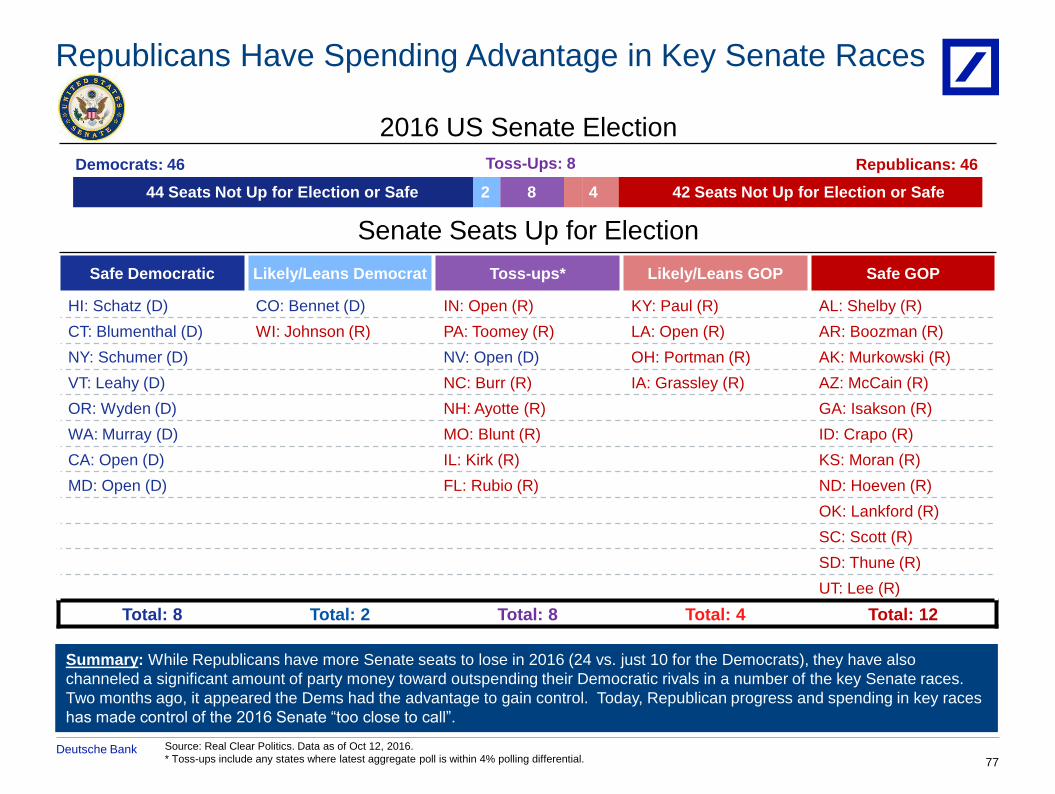

Deutsche Bank Source: Peck, Madigan, Jones. Open Secrets. Presidential fundraising as of Sept 1, 2016. Senate fundraising as of Sept 13, 2016. Center for Responsive

Politics. Senate totals above based on candidate filings and could result in some double counting. Cruz, Rubio and Bush outraised Clinton in the following 15

states: AZ, AK, DE, FL, GA, ID, MO, MT, ND, OK, TX, UT, WV, WI and WY. *Campaign donations include self funding.

10/17/2016

28

11. The Funding Advantage

Summary: Clinton (and her Super PACs) have outraised Trump (and his Super PACs) in all 50 states and Washington DC.

However, it would be wrong to say that a Clinton victory necessarily brings control of the US Senate, because Republicans have

outspent their Democratic rivals in a large number of key Senate races.

Presidential Campaign:

Democrat Advantage

Senate Races:

Republican Advantage

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

Clinton Trump

(USD, Mn)

$435 Mn

$161 Mn

Individual

donations*

Super PACs

&

Organizations

28%

72% 22%

78%

$0

$20

$40

$60

$80

$100

$120

$140

Democrats Republicans

(USD, Mn)

Against

other

party

For party $95 Mn

28%

72%

$133 Mn

22%

78%

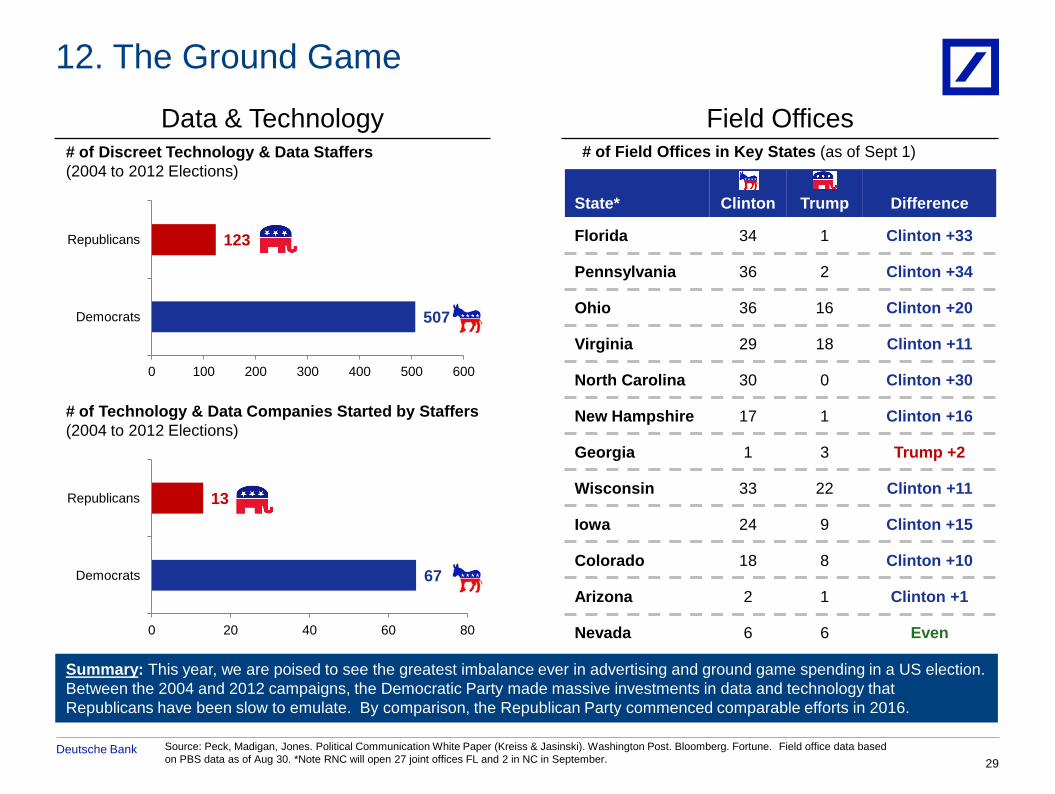

Deutsche Bank Source: Peck, Madigan, Jones. Political Communication White Paper (Kreiss & Jasinski). Washington Post. Bloomberg. Fortune. Field office data based

on PBS data as of Aug 30. *Note RNC will open 27 joint offices FL and 2 in NC in September.

10/17/2016

29

12. The Ground Game

Summary: This year, we are poised to see the greatest imbalance ever in advertising and ground game spending in a US election.

Between the 2004 and 2012 campaigns, the Democratic Party made massive investments in data and technology that

Republicans have been slow to emulate. By comparison, the Republican Party commenced comparable efforts in 2016.

Data & Technology Field Offices # of Discreet Technology & Data Staffers

(2004 to 2012 Elections)

# of Technology & Data Companies Started by Staffers

(2004 to 2012 Elections)

507

123

0 100 200 300 400 500 600

Democrats

Republicans

67

13

0 20 40 60 80

Democrats

Republicans

# of Field Offices in Key States (as of Sept 1)

State* Clinton Trump Difference

Florida 34 1 Clinton +33

Pennsylvania 36 2 Clinton +34

Ohio 36 16 Clinton +20

Virginia 29 18 Clinton +11

North Carolina 30 0 Clinton +30

New Hampshire 17 1 Clinton +16

Georgia 1 3 Trump +2

Wisconsin 33 22 Clinton +11

Iowa 24 9 Clinton +15

Colorado 18 8 Clinton +10

Arizona 2 1 Clinton +1

Nevada 6 6 Even

Deutsche Bank

III. The Polls

Deutsche Bank

“Madison’s experience at both the state and the federal level had convinced him

that ‘the people’ was not some benevolent, harmonious collective but rather a

smoldering and ever-shifting gathering of factions or interest groups committed to

provincial perspectives and vulnerable to demagogues with partisan agendas. The

question, then, was how to reconcile the creedal conviction about popular

sovereignty with the highly combustible, inherently swoonish character of

democracy. Perhaps the most succinct way to put the question was this: How

could a republic bottomed on the principle of popular sovereignty be structured in

such a way to manage the inevitable excesses of democracy and best serve the

long-term public interest?”

-Joseph Ellis, Pulitzer Prize Winning Author of

“The Quartet: Orchestrating the 2nd American Revolution, 1783-1789”

31

Deutsche Bank

10/17/2016

32

Source: Real Clear Politics Data as of Oct 17, 2016 (overall). Johnson and Stein shown on a combined basis. JMC analytics, based on survey of 781

registered voters. Survey conducted between September 7-8, 2016. YouGov, based on survey of 1091 likely voters. Survey conducted between August

30-September 2, 2016. CNN based on 1,006 Ohioans from Sept 7 - 12, 2016. Pew Research. David Rothschild, PredictWise.

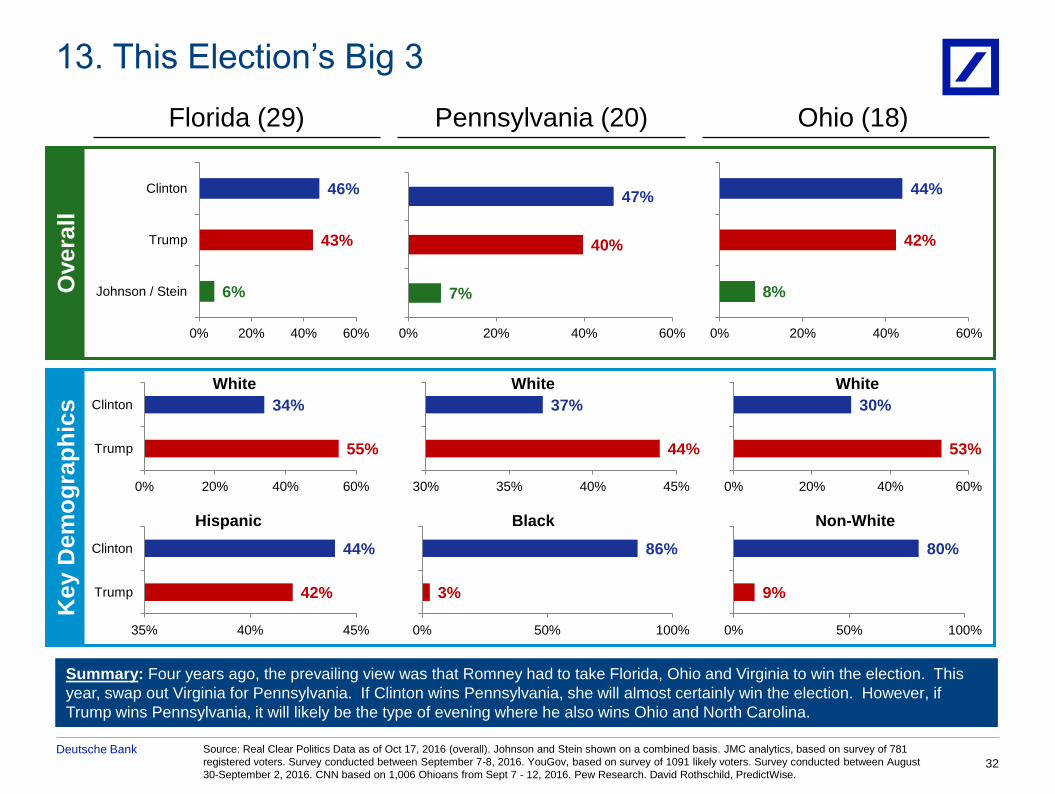

13. This Election’s Big 3

Summary: Four years ago, the prevailing view was that Romney had to take Florida, Ohio and Virginia to win the election. This

year, swap out Virginia for Pennsylvania. If Clinton wins Pennsylvania, she will almost certainly win the election. However, if

Trump wins Pennsylvania, it will likely be the type of evening where he also wins Ohio and North Carolina.

Florida (29) Pennsylvania (20) Ohio (18)

Overa

ll

Key D

em

og

rap

hic

s

34%

55%

0% 20% 40% 60%

Clinton

Trump

White

Hispanic

44%

42%

35% 40% 45%

Clinton

Trump

37%

44%

30% 35% 40% 45%

86%

3%

0% 50% 100%

White

Black

30%

53%

0% 20% 40% 60%

80%

9%

0% 50% 100%

White

Non-White

46%

43%

6%

0% 20% 40% 60%

Clinton

Trump

Johnson / Stein

47%

40%

7%

0% 20% 40% 60%

44%

42%

8%

0% 20% 40% 60%

Deutsche Bank

35%

37%

39%

41%

43%

45%

47%

49%

Jun-2016 Jul-2016 Aug-2016 Sep-2016

10/17/2016

33

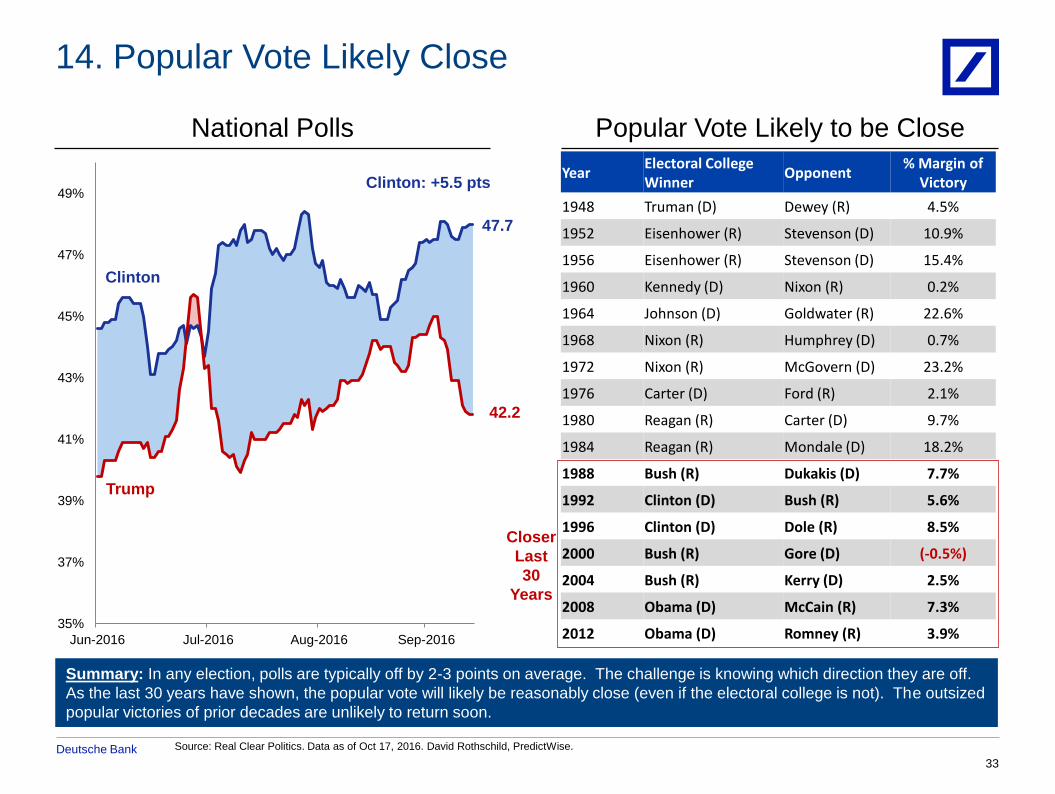

Source: Real Clear Politics. Data as of Oct 17, 2016. David Rothschild, PredictWise.

14. Popular Vote Likely Close

National Polls Popular Vote Likely to be Close

Year Electoral College Winner

Opponent % Margin of

Victory

1948 Truman (D) Dewey (R) 4.5%

1952 Eisenhower (R) Stevenson (D) 10.9%

1956 Eisenhower (R) Stevenson (D) 15.4%

1960 Kennedy (D) Nixon (R) 0.2%

1964 Johnson (D) Goldwater (R) 22.6%

1968 Nixon (R) Humphrey (D) 0.7%

1972 Nixon (R) McGovern (D) 23.2%

1976 Carter (D) Ford (R) 2.1%

1980 Reagan (R) Carter (D) 9.7%

1984 Reagan (R) Mondale (D) 18.2%

1988 Bush (R) Dukakis (D) 7.7%

1992 Clinton (D) Bush (R) 5.6%

1996 Clinton (D) Dole (R) 8.5%

2000 Bush (R) Gore (D) (-0.5%)

2004 Bush (R) Kerry (D) 2.5%

2008 Obama (D) McCain (R) 7.3%

2012 Obama (D) Romney (R) 3.9%

Clinton

Trump

Clinton: +5.5 pts

Summary: In any election, polls are typically off by 2-3 points on average. The challenge is knowing which direction they are off.

As the last 30 years have shown, the popular vote will likely be reasonably close (even if the electoral college is not). The outsized

popular victories of prior decades are unlikely to return soon.

Closer

Last

30

Years

47.7

42.2

Deutsche Bank

30%

35%

40%

45%

50%

55%

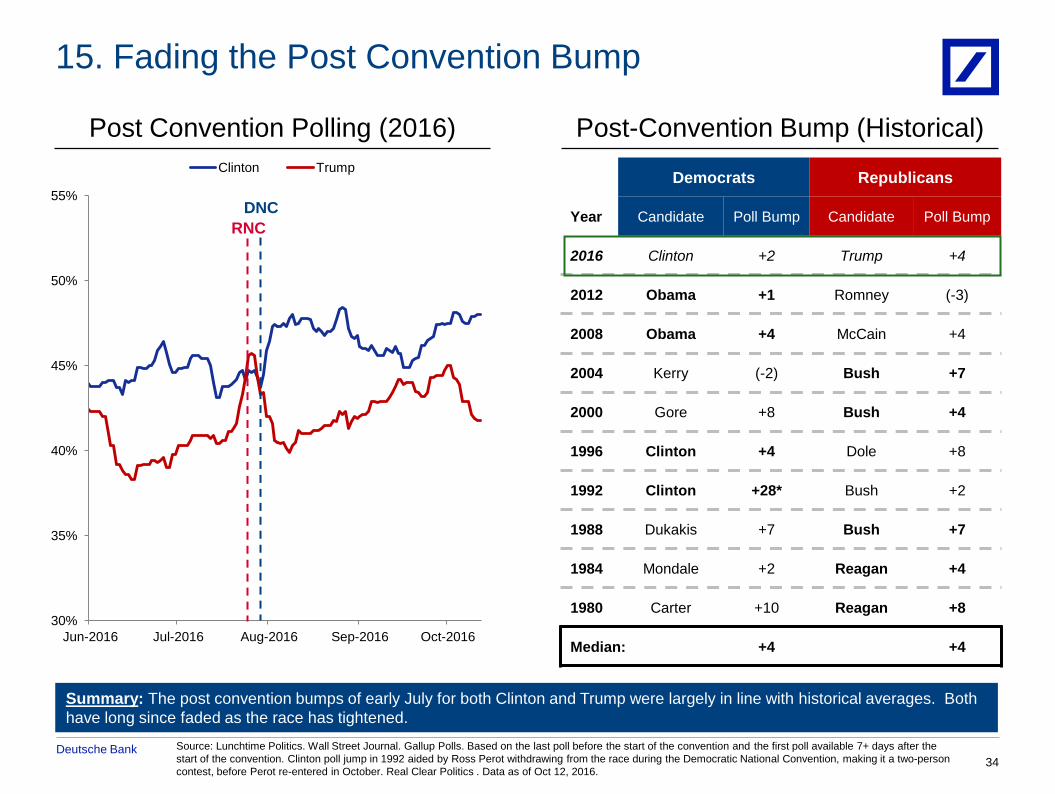

Jun-2016 Jul-2016 Aug-2016 Sep-2016 Oct-2016

Clinton Trump

Source: Lunchtime Politics. Wall Street Journal. Gallup Polls. Based on the last poll before the start of the convention and the first poll available 7+ days after the

start of the convention. Clinton poll jump in 1992 aided by Ross Perot withdrawing from the race during the Democratic National Convention, making it a two-person

contest, before Perot re-entered in October. Real Clear Politics . Data as of Oct 12, 2016. 34

Post Convention Polling (2016) Post-Convention Bump (Historical)

Democrats Republicans

Year Candidate Poll Bump Candidate Poll Bump

2016 Clinton +2 Trump +4

2012 Obama +1 Romney (-3)

2008 Obama +4 McCain +4

2004 Kerry (-2) Bush +7

2000 Gore +8 Bush +4

1996 Clinton +4 Dole +8

1992 Clinton +28* Bush +2

1988 Dukakis +7 Bush +7

1984 Mondale +2 Reagan +4

1980 Carter +10 Reagan +8

Median: +4 +4

RNC

15. Fading the Post Convention Bump

DNC

Summary: The post convention bumps of early July for both Clinton and Trump were largely in line with historical averages. Both

have long since faded as the race has tightened.

Deutsche Bank

10/17/2016

35

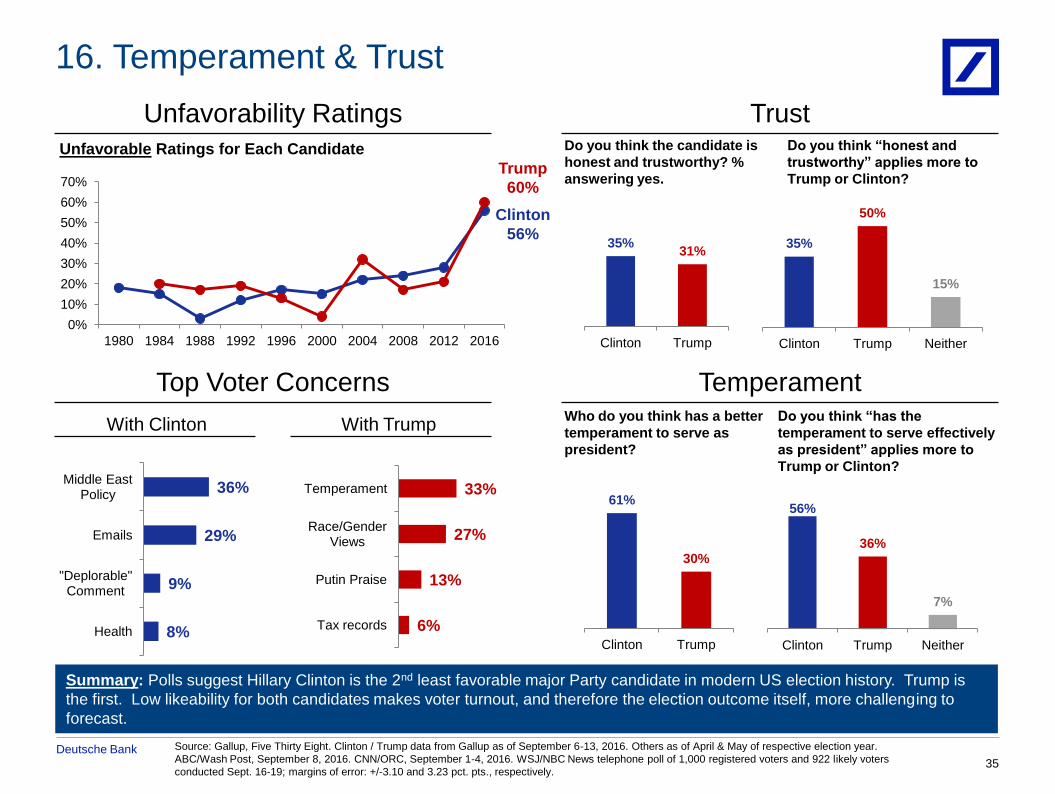

16. Temperament & Trust

Unfavorability Ratings Trust

Temperament

Summary: Polls suggest Hillary Clinton is the 2nd least favorable major Party candidate in modern US election history. Trump is

the first. Low likeability for both candidates makes voter turnout, and therefore the election outcome itself, more challenging to

forecast.

Source: Gallup, Five Thirty Eight. Clinton / Trump data from Gallup as of September 6-13, 2016. Others as of April & May of respective election year.

ABC/Wash Post, September 8, 2016. CNN/ORC, September 1-4, 2016. WSJ/NBC News telephone poll of 1,000 registered voters and 922 likely voters

conducted Sept. 16-19; margins of error: +/-3.10 and 3.23 pct. pts., respectively.

0%

10%

20%

30%

40%

50%

60%

70%

1980 1984 1988 1992 1996 2000 2004 2008 2012 2016

Clinton

56%

Trump

60%

35% 31%

Clinton Trump

35%

50%

15%

Clinton Trump Neither

Do you think the candidate is

honest and trustworthy? %

answering yes.

Do you think “honest and

trustworthy” applies more to

Trump or Clinton?

61%

30%

Clinton Trump

56%

36%

7%

Clinton Trump Neither

Who do you think has a better

temperament to serve as

president?

Do you think “has the

temperament to serve effectively

as president” applies more to

Trump or Clinton?

Unfavorable Ratings for Each Candidate

Top Voter Concerns

With Clinton With Trump

33%

27%

13%

6%

Temperament

Race/Gender Views

Putin Praise

Tax records

36%

29%

9%

8%

Middle East Policy

Emails

"Deplorable" Comment

Health

Deutsche Bank

10/17/2016

36

Source: Pew Research Center. Based on survey of 2,245 registered voters. Survey conducted between June 15-16, 2016.

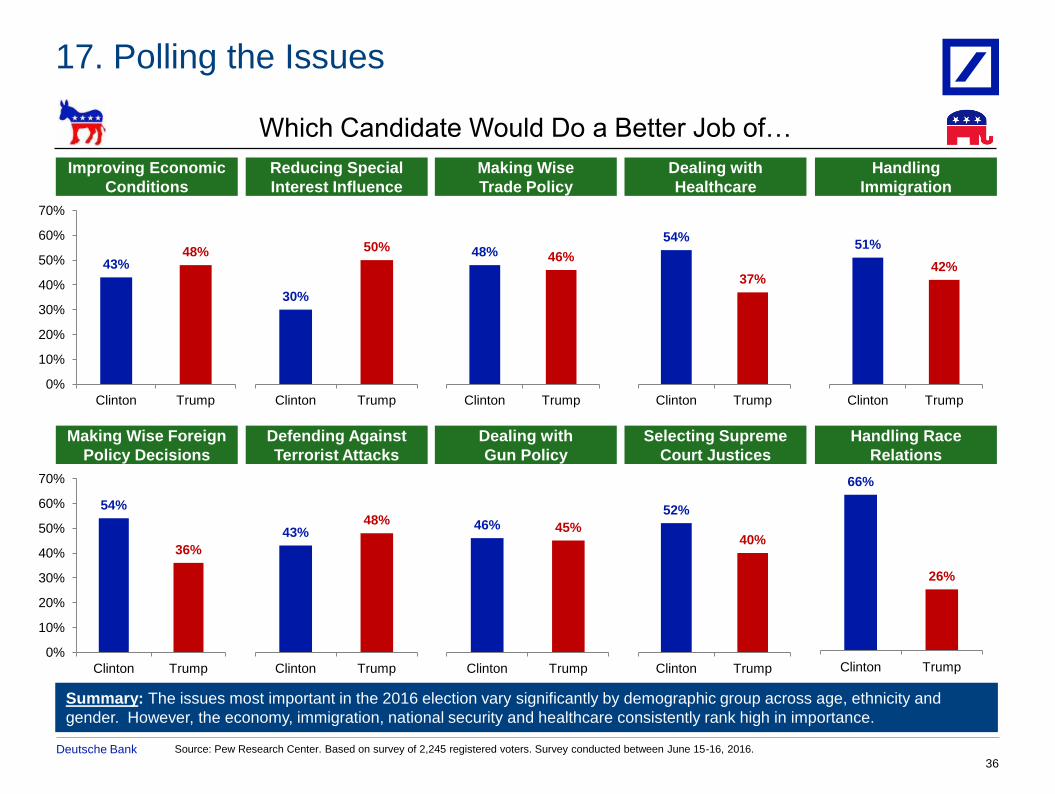

17. Polling the Issues

Summary: The issues most important in the 2016 election vary significantly by demographic group across age, ethnicity and

gender. However, the economy, immigration, national security and healthcare consistently rank high in importance.

Which Candidate Would Do a Better Job of…

Improving Economic

Conditions

Reducing Special

Interest Influence

Making Wise

Trade Policy

Dealing with

Healthcare

Handling

Immigration

Making Wise Foreign

Policy Decisions

Defending Against

Terrorist Attacks

Dealing with

Gun Policy

Selecting Supreme

Court Justices

Handling Race

Relations

43% 48%

0%

10%

20%

30%

40%

50%

60%

70%

Clinton Trump

30%

50%

Clinton Trump

48% 46%

Clinton Trump

54%

37%

Clinton Trump

51%

42%

Clinton Trump

54%

36%

0%

10%

20%

30%

40%

50%

60%

70%

Clinton Trump

43% 48%

Clinton Trump

46% 45%

Clinton Trump

52%

40%

Clinton Trump

66%

26%

Clinton Trump

Deutsche Bank

Year Poll Differential (Pre & Post Debate)

2008

McCain vs. Obama

2004

Bush vs. Kerry

2000

Gore vs. Bush

1996

Clinton vs. Dole

1992

Bush vs. Clinton

1988

Bush vs. Dukakis

1984

Reagan vs. Mondale

1980

Carter vs. Reagan

1976

Ford vs. Carter

10/17/2016

37

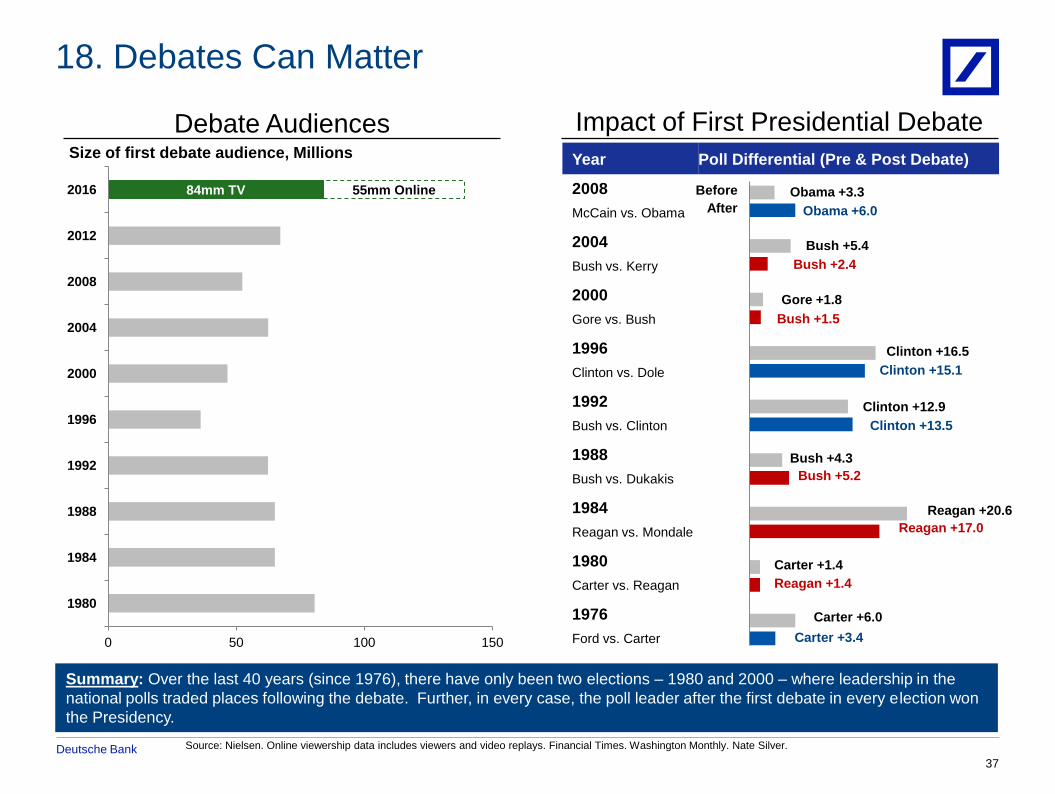

Source: Nielsen. Online viewership data includes viewers and video replays. Financial Times. Washington Monthly. Nate Silver.

18. Debates Can Matter

Impact of First Presidential Debate

Before

After

Obama +3.3

Obama +6.0

Bush +4.3

Bush +5.2

Bush +5.4

Bush +2.4

Gore +1.8

Bush +1.5

Clinton +16.5

Clinton +15.1

Clinton +12.9

Clinton +13.5

Reagan +20.6

Reagan +17.0

Carter +1.4

Reagan +1.4

Carter +6.0

Carter +3.4

Summary: Over the last 40 years (since 1976), there have only been two elections – 1980 and 2000 – where leadership in the

national polls traded places following the debate. Further, in every case, the poll leader after the first debate in every election won

the Presidency.

Debate Audiences

84mm TV 55mm Online

0 50 100 150

1980

1984

1988

1992

1996

2000

2004

2008

2012

2016

Size of first debate audience, Millions

Deutsche Bank

0%

20%

40%

60%

80%

100%

1992 1996 2000 2004 2008 2012 2016

0%

20%

40%

60%

80%

100%

1992 1996 2000 2004 2008 2012 2016

0%

20%

40%

60%

80%

100%

1992 1996 2000 2004 2008 2012 2016

00%

20%

40%

60%

80%

100%

2000 2004 2008 2012 2016

10/17/2016

38

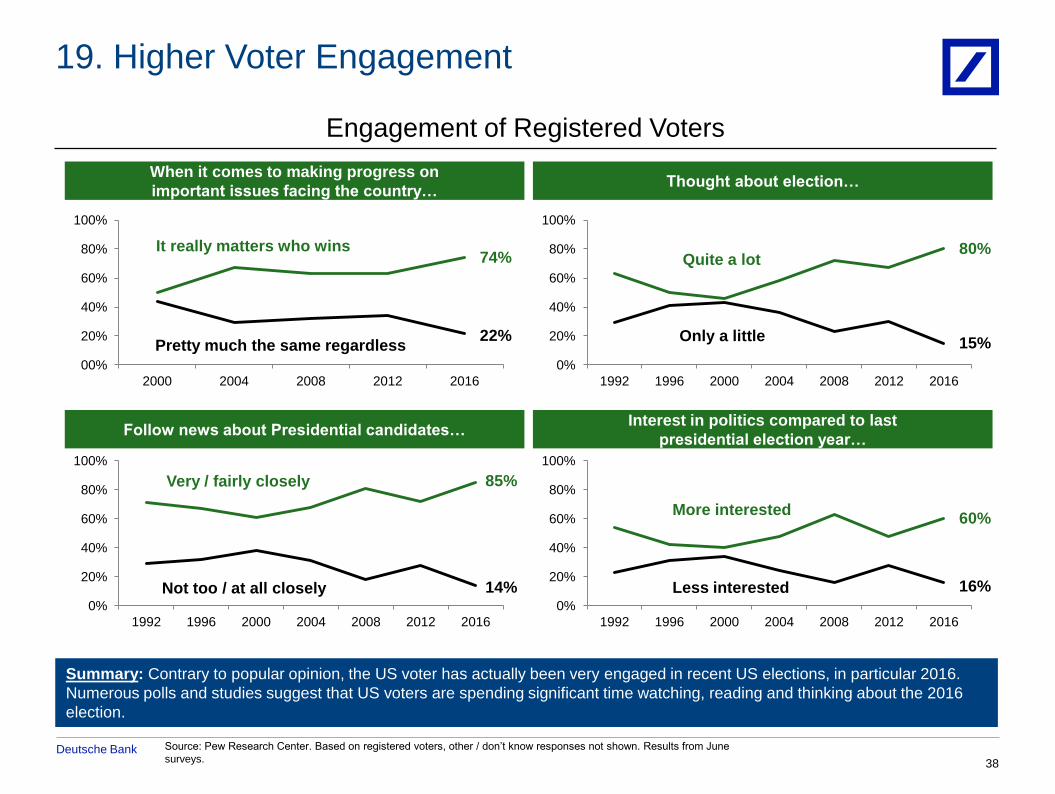

19. Higher Voter Engagement

Summary: Contrary to popular opinion, the US voter has actually been very engaged in recent US elections, in particular 2016.

Numerous polls and studies suggest that US voters are spending significant time watching, reading and thinking about the 2016

election.

Source: Pew Research Center. Based on registered voters, other / don’t know responses not shown. Results from June

surveys.

Engagement of Registered Voters

When it comes to making progress on

important issues facing the country… Thought about election…

Follow news about Presidential candidates… Interest in politics compared to last

presidential election year…

It really matters who wins

Pretty much the same regardless

74%

22%

Quite a lot

Only a little

80%

15%

Very / fairly closely

Not too / at all closely

85%

14%

More interested

Less interested

60%

16%

Deutsche Bank

10/17/2016

39

Source: NPR, Center for American Women in Politics. NBC / WSJ Polling. The USC Dornsife / LA Times Presidential Election

"Daybreak" Poll. Data based on a survey of over 2000 people. Data as of Oct 12, 2016.

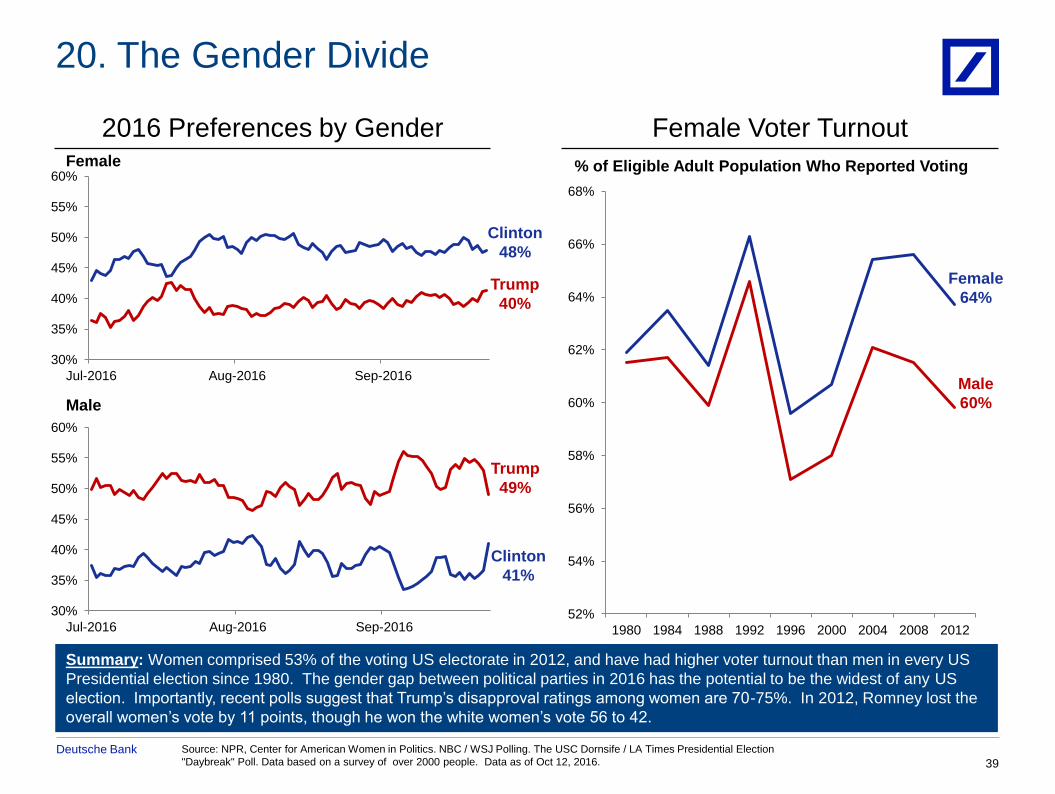

20. The Gender Divide

2016 Preferences by Gender Female Voter Turnout

52%

54%

56%

58%

60%

62%

64%

66%

68%

1980 1984 1988 1992 1996 2000 2004 2008 2012

Female

64%

Male

60%

% of Eligible Adult Population Who Reported Voting

Summary: Women comprised 53% of the voting US electorate in 2012, and have had higher voter turnout than men in every US

Presidential election since 1980. The gender gap between political parties in 2016 has the potential to be the widest of any US

election. Importantly, recent polls suggest that Trump’s disapproval ratings among women are 70-75%. In 2012, Romney lost the

overall women’s vote by 11 points, though he won the white women’s vote 56 to 42.

Female

Male

Clinton

48%

Trump

40%

Clinton

41%

Trump

49%

30%

35%

40%

45%

50%

55%

60%

Jul-2016 Aug-2016 Sep-2016

30%

35%

40%

45%

50%

55%

60%

Jul-2016 Aug-2016 Sep-2016

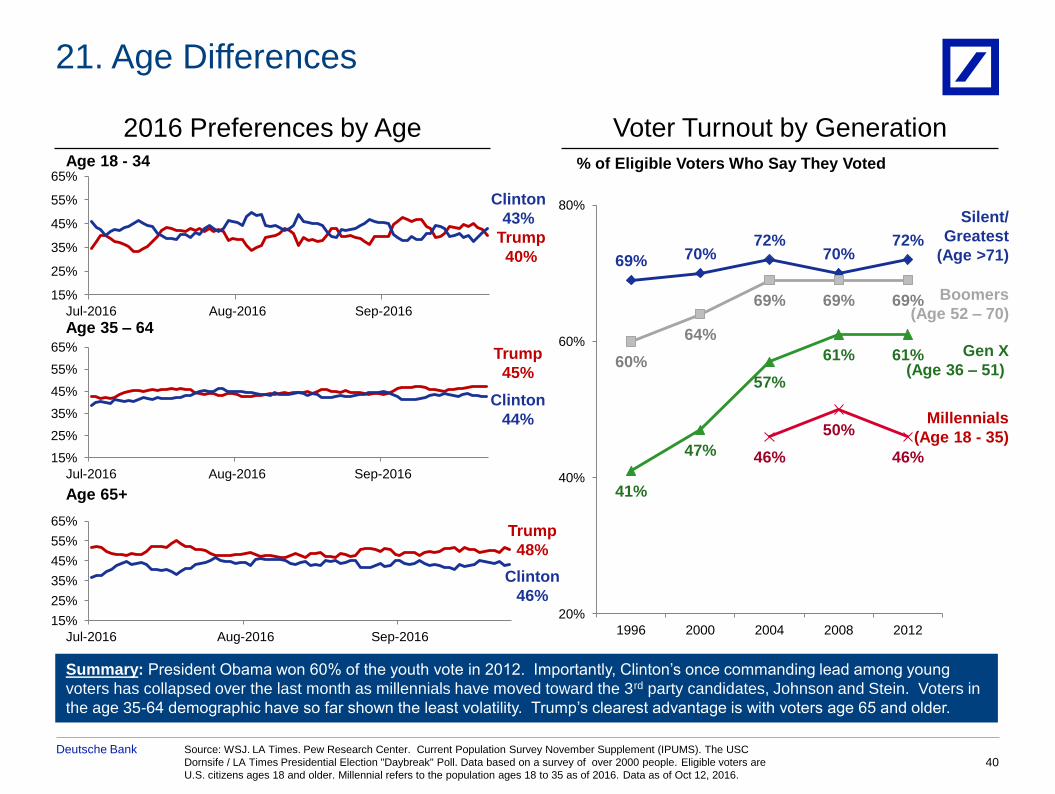

Deutsche Bank

Age 18 - 34

Age 35 – 64

Age 65+

69% 70% 72%

70% 72%

60%

64%

69% 69% 69%

41%

47%

57%

61% 61%

46%

50%

46%

20%

40%

60%

80%

1996 2000 2004 2008 2012

Voter Turnout by Generation

40

2016 Preferences by Age

21. Age Differences

Summary: President Obama won 60% of the youth vote in 2012. Importantly, Clinton’s once commanding lead among young

voters has collapsed over the last month as millennials have moved toward the 3rd party candidates, Johnson and Stein. Voters in

the age 35-64 demographic have so far shown the least volatility. Trump’s clearest advantage is with voters age 65 and older.

% of Eligible Voters Who Say They Voted

Source: WSJ. LA Times. Pew Research Center. Current Population Survey November Supplement (IPUMS). The USC

Dornsife / LA Times Presidential Election "Daybreak" Poll. Data based on a survey of over 2000 people. Eligible voters are

U.S. citizens ages 18 and older. Millennial refers to the population ages 18 to 35 as of 2016. Data as of Oct 12, 2016.

Clinton

43%

Trump

40%

Clinton

44%

Trump

45%

Clinton

46%

Trump

48%

Silent/

Greatest

(Age >71)

Boomers

(Age 52 – 70)

Gen X

(Age 36 – 51)

Millennials

(Age 18 - 35)

15%

25%

35%

45%

55%

65%

Jul-2016 Aug-2016 Sep-2016

15%

25%

35%

45%

55%

65%

Jul-2016 Aug-2016 Sep-2016

15%

25%

35%

45%

55%

65%

Jul-2016 Aug-2016 Sep-2016

Deutsche Bank

0%

25%

50%

75%

100%

Jul-2016 Sep-2016

White Black

Latino Other

Jul-2016 Sep-2016

Jul-2016 Sep-2016 0%

25%

50%

75%

100%

Jul-2016 Sep-2016

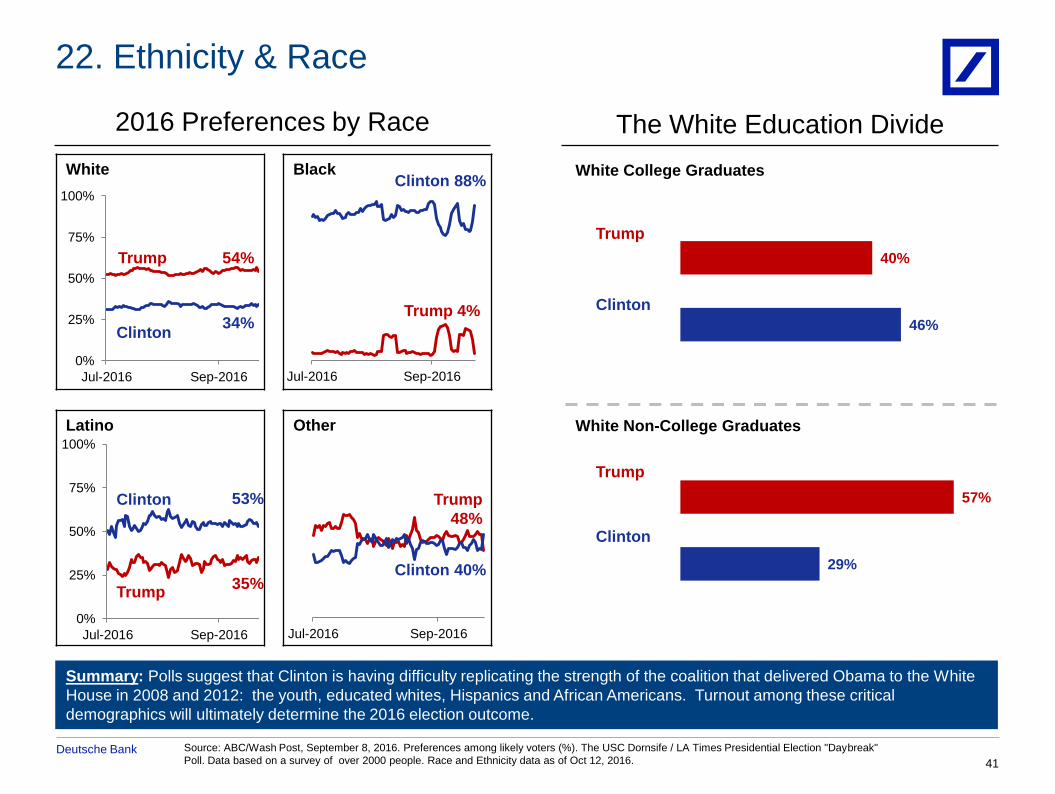

46%

40%

White College Graduates

White Non-College Graduates

29%

57%

10/17/2016

41

Source: ABC/Wash Post, September 8, 2016. Preferences among likely voters (%). The USC Dornsife / LA Times Presidential Election "Daybreak"

Poll. Data based on a survey of over 2000 people. Race and Ethnicity data as of Oct 12, 2016.

22. Ethnicity & Race

2016 Preferences by Race The White Education Divide

Summary: Polls suggest that Clinton is having difficulty replicating the strength of the coalition that delivered Obama to the White

House in 2008 and 2012: the youth, educated whites, Hispanics and African Americans. Turnout among these critical

demographics will ultimately determine the 2016 election outcome.

Trump

Trump

Clinton

Clinton

Trump

Clinton

54%

34%

Clinton 88%

Trump 4%

Trump

Clinton 53%

35%

Trump

48%

Clinton 40%

Deutsche Bank

25%

35%

45%

55%

65%

Jul-2016 Aug-2016 Sep-2016

25%

35%

45%

55%

65%

Jul-2016 Aug-2016 Sep-2016

25%

35%

45%

55%

65%

Jul-2016 Aug-2016 Sep-2016

20%

30%

40%

50%

60%

70%

Jul-2016 Aug-2016 Sep-2016

20%

30%

40%

50%

60%

70%

Jul-2016 Aug-2016 Sep-2016

20%

30%

40%

50%

60%

70%

Jul-2016 Aug-2016 Sep-2016

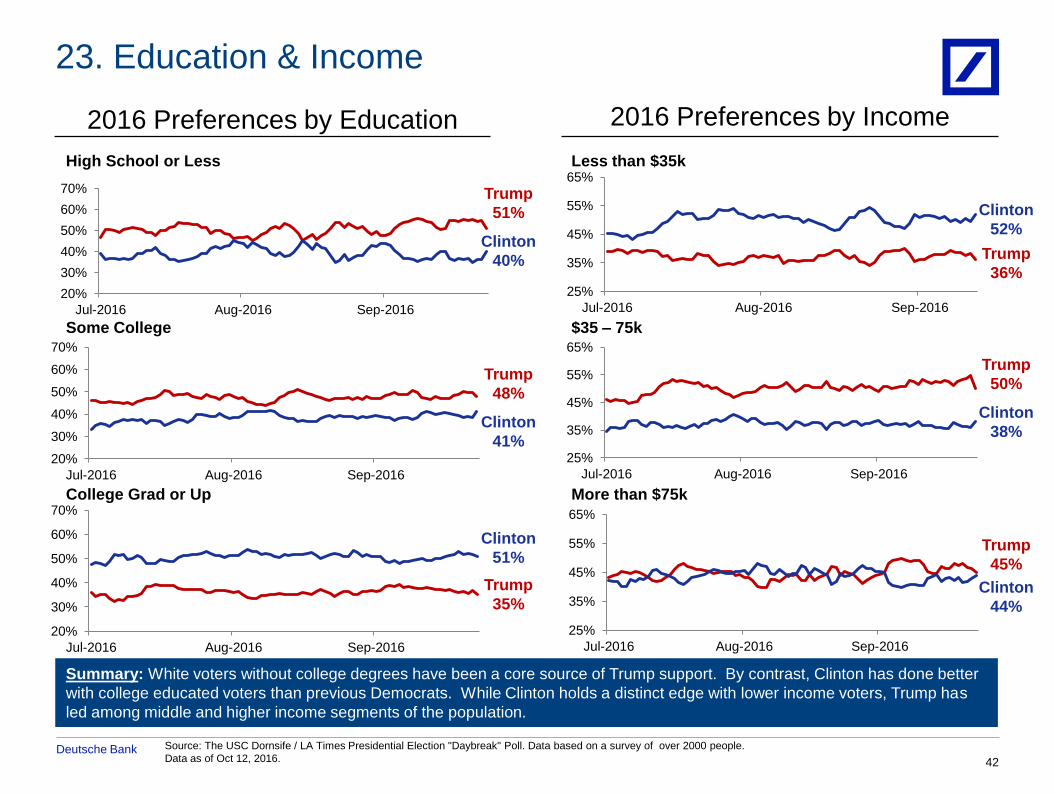

Less than $35k

$35 – 75k

More than $75k

High School or Less

Some College

College Grad or Up

42

2016 Preferences by Education 2016 Preferences by Income

23. Education & Income

Summary: White voters without college degrees have been a core source of Trump support. By contrast, Clinton has done better

with college educated voters than previous Democrats. While Clinton holds a distinct edge with lower income voters, Trump has

led among middle and higher income segments of the population.

Source: The USC Dornsife / LA Times Presidential Election "Daybreak" Poll. Data based on a survey of over 2000 people.

Data as of Oct 12, 2016.

Clinton

40%

Trump

51%

Clinton

51%

Trump

35%

Clinton

41%

Trump

48%

Clinton

44%

Trump

45%

Clinton

38%

Trump

50%

Clinton

52%

Trump

36%

Deutsche Bank

10/17/2016

43

Source: Washington Post, FiveThirtyEight, Real Clear Politics. State boost based on candidate performance in VP’s home state using relative voting

index (RVI) comparisons to prior and following elections (where available). Indiana polls are the average of 3 most recently available polls between

August 19 and October 13, 2016. Virginia data as of Oct 17, 2016.

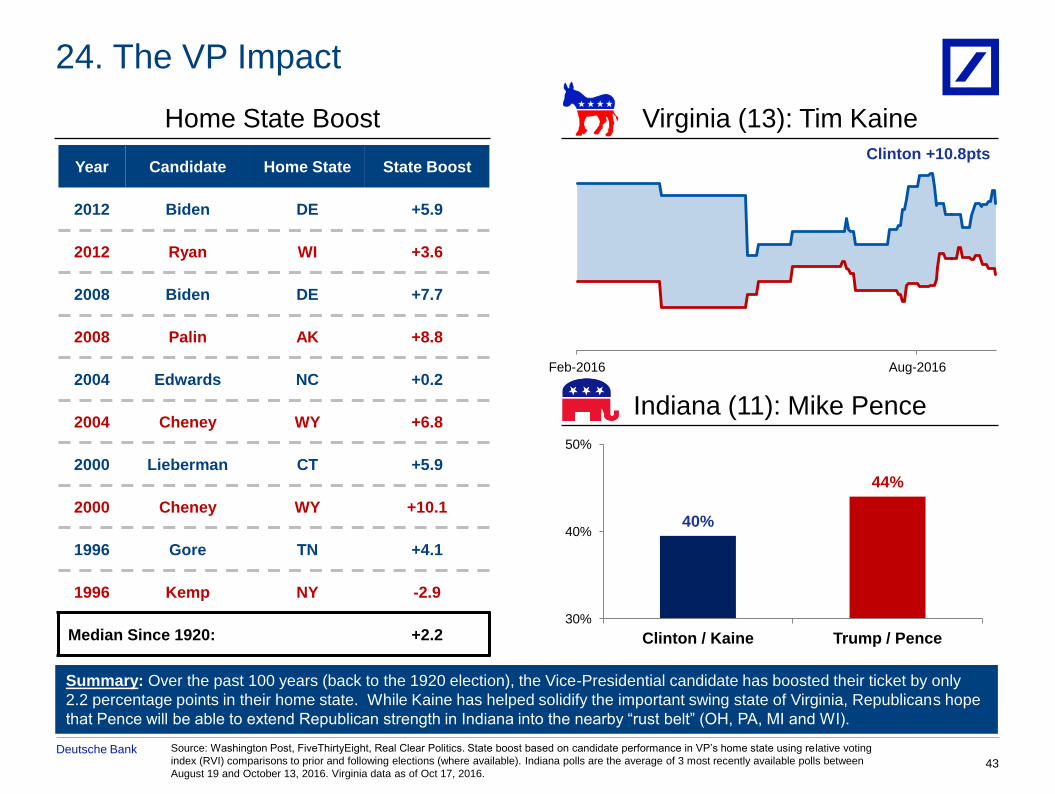

24. The VP Impact

Home State Boost

Indiana (11): Mike Pence

Virginia (13): Tim Kaine

Year Candidate Home State State Boost

2012 Biden DE +5.9

2012 Ryan WI +3.6

2008 Biden DE +7.7

2008 Palin AK +8.8

2004 Edwards NC +0.2

2004 Cheney WY +6.8

2000 Lieberman CT +5.9

2000 Cheney WY +10.1

1996 Gore TN +4.1

1996 Kemp NY -2.9

Median Since 1920: +2.2

Summary: Over the past 100 years (back to the 1920 election), the Vice-Presidential candidate has boosted their ticket by only

2.2 percentage points in their home state. While Kaine has helped solidify the important swing state of Virginia, Republicans hope

that Pence will be able to extend Republican strength in Indiana into the nearby “rust belt” (OH, PA, MI and WI).

Feb-2016 Aug-2016

Clinton +10.8pts

40%

44%

30%

40%

50%

Clinton / Kaine Trump / Pence

Deutsche Bank

IV. The Implications

Deutsche Bank

“If men were angels, no government would be necessary. If

angels were to govern men, neither external nor internal

controls would be necessary. In framing a government which is

to be administered by men over men, the greatest difficulty lies

in this: You must first enable the government to control the

governed; and in the next place oblige it to control itself. A

dependence on the people is no doubt the primary control on

government, but experience has taught mankind the necessity

of auxiliary precautions.”

-James Madison, 4th US President,

in Federalist Paper No. 51

(1751 - 1836)

45

Deutsche Bank

0

100

200

300

400

500

600

700

800

900

114th 113th 112th 111th 110th 109th 108th 107th 106th 105th 104th 103rd 102nd 101st 100th 99th 98th 97th 96th 95th 94th 93rd

Source: GovTrack. Congress.gov. Bills and Joint Resolutions Passed by Congress. DB Government Affairs (Frank Kelly). S&P. Peck, Madigan & Jones.

46

Legislation Passed by Each Congress

Congress

1973

Congress

2016

1970s Avg: 760

1980s Avg: 664

1990s Avg: 486

2000s Avg: 443

2010s Avg: 260

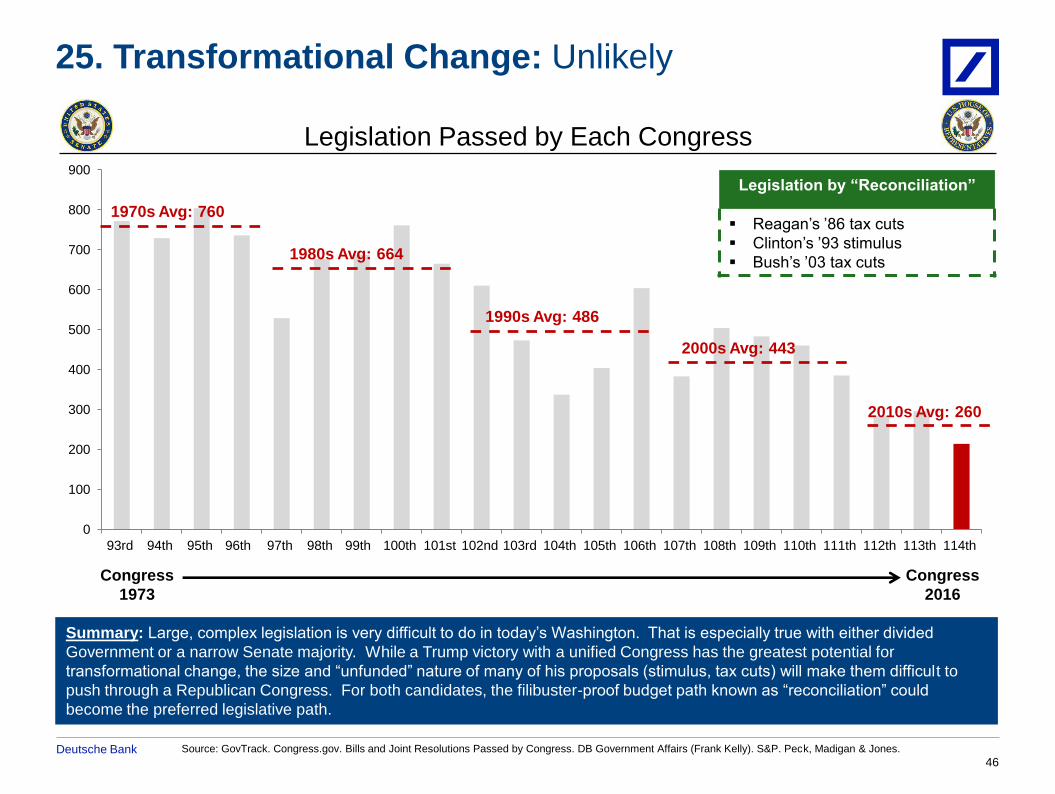

25. Transformational Change: Unlikely

Summary: Large, complex legislation is very difficult to do in today’s Washington. That is especially true with either divided

Government or a narrow Senate majority. While a Trump victory with a unified Congress has the greatest potential for

transformational change, the size and “unfunded” nature of many of his proposals (stimulus, tax cuts) will make them difficult to

push through a Republican Congress. For both candidates, the filibuster-proof budget path known as “reconciliation” could

become the preferred legislative path.

Legislation by “Reconciliation”

Reagan’s ’86 tax cuts

Clinton’s ’93 stimulus

Bush’s ’03 tax cuts

Deutsche Bank

10/17/2016

47

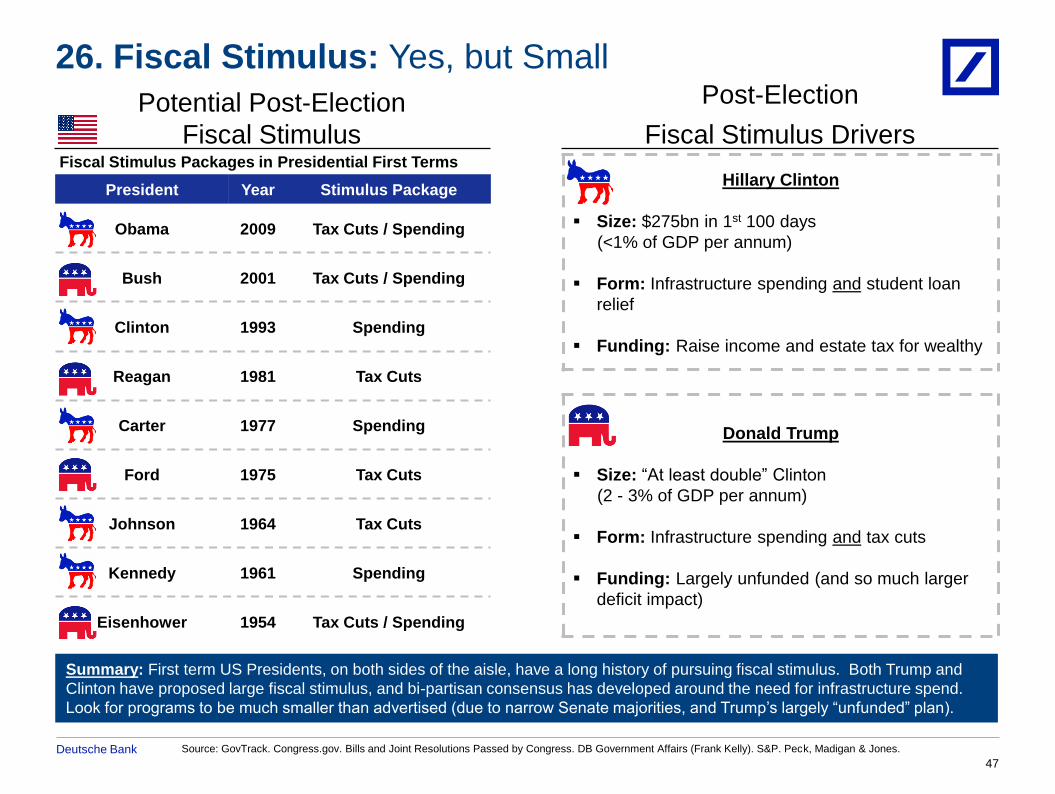

26. Fiscal Stimulus: Yes, but Small

Potential Post-Election

Fiscal Stimulus

Post-Election

Fiscal Stimulus Drivers

President Year Stimulus Package

Obama 2009 Tax Cuts / Spending

Bush 2001 Tax Cuts / Spending

Clinton 1993 Spending

Reagan 1981 Tax Cuts

Carter 1977 Spending

Ford 1975 Tax Cuts

Johnson 1964 Tax Cuts

Kennedy 1961 Spending

Eisenhower 1954 Tax Cuts / Spending

Fiscal Stimulus Packages in Presidential First Terms Hillary Clinton

Size: $275bn in 1st 100 days

(<1% of GDP per annum)

Form: Infrastructure spending and student loan

relief

Funding: Raise income and estate tax for wealthy

Donald Trump

Size: “At least double” Clinton

(2 - 3% of GDP per annum)

Form: Infrastructure spending and tax cuts

Funding: Largely unfunded (and so much larger

deficit impact)

Summary: First term US Presidents, on both sides of the aisle, have a long history of pursuing fiscal stimulus. Both Trump and

Clinton have proposed large fiscal stimulus, and bi-partisan consensus has developed around the need for infrastructure spend.

Look for programs to be much smaller than advertised (due to narrow Senate majorities, and Trump’s largely “unfunded” plan).

Source: GovTrack. Congress.gov. Bills and Joint Resolutions Passed by Congress. DB Government Affairs (Frank Kelly). S&P. Peck, Madigan & Jones.

Deutsche Bank

10/17/2016

48

Source: DB Asset Management (Larry Adam, CIO. Stefan Kreuzkamp). Recession time periods reflect 1929 – 20015. DB

Global Research (Hooper. Slok, Bianco. Spencer. Winkler). DB House View. GDP impact based on a summary of different

models.

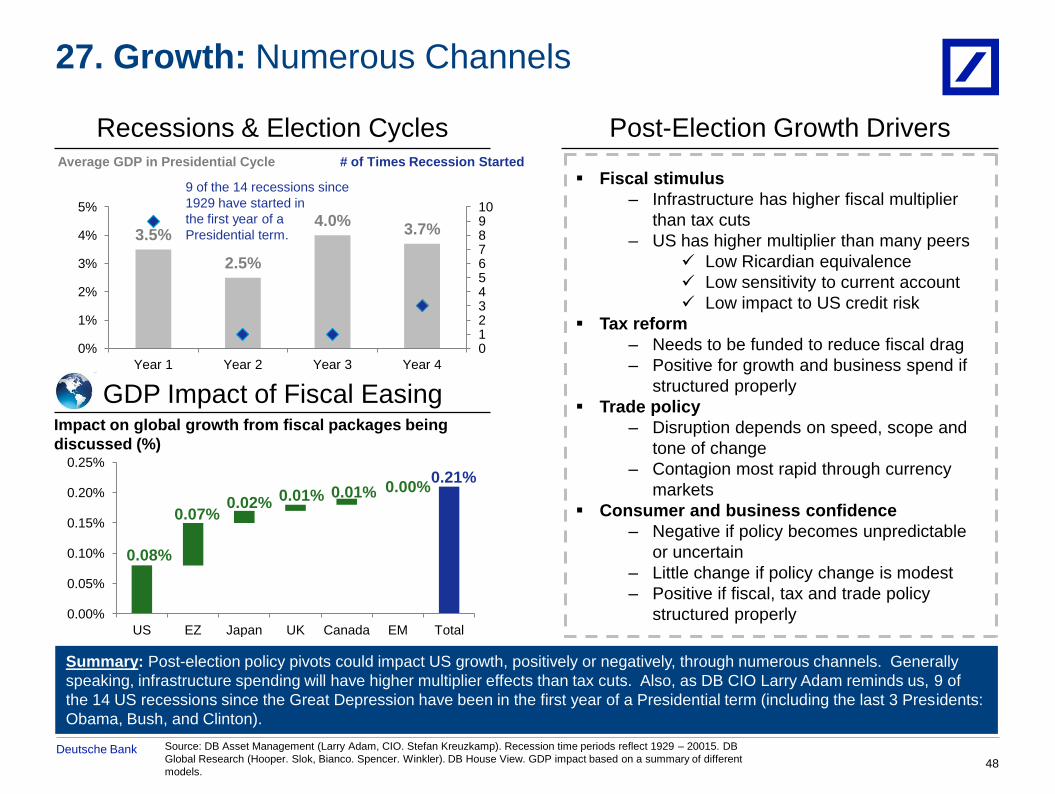

27. Growth: Numerous Channels

Recessions & Election Cycles Post-Election Growth Drivers

Summary: Post-election policy pivots could impact US growth, positively or negatively, through numerous channels. Generally

speaking, infrastructure spending will have higher multiplier effects than tax cuts. Also, as DB CIO Larry Adam reminds us, 9 of

the 14 US recessions since the Great Depression have been in the first year of a Presidential term (including the last 3 Presidents:

Obama, Bush, and Clinton).

Fiscal stimulus

– Infrastructure has higher fiscal multiplier

than tax cuts

– US has higher multiplier than many peers

Low Ricardian equivalence

Low sensitivity to current account

Low impact to US credit risk

Tax reform

– Needs to be funded to reduce fiscal drag

– Positive for growth and business spend if

structured properly

Trade policy

– Disruption depends on speed, scope and

tone of change

– Contagion most rapid through currency

markets

Consumer and business confidence

– Negative if policy becomes unpredictable

or uncertain

– Little change if policy change is modest

– Positive if fiscal, tax and trade policy

structured properly

GDP Impact of Fiscal Easing

0.00%

0.05%

0.10%

0.15%

0.20%

0.25%

US EZ Japan UK Canada EM Total

Impact on global growth from fiscal packages being

discussed (%)

0.08%

0.07% 0.02% 0.01% 0.01% 0.00%

0.21%

3.5%

2.5%

4.0% 3.7%

0 1 2 3 4 5 6 7 8 9 10

0%

1%

2%

3%

4%

5%

Year 1 Year 2 Year 3 Year 4

Average GDP in Presidential Cycle # of Times Recession Started

9 of the 14 recessions since

1929 have started in

the first year of a

Presidential term.

Deutsche Bank

-4%

-2%

0%

2%

4%

6%

8%

Jan

Fe

b

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

10/17/2016

49

Source: DB Asset Management (Larry Adams, CIO). DB Global Markets Research (Bianco). Bloomberg. Close Elections based on

average S&P performance in close election years (1952, 1960, 1968, 1976, 2004), one week rolling average with performance indexed

such that election day is 100. Open election data based on data from 1933 – 2015.

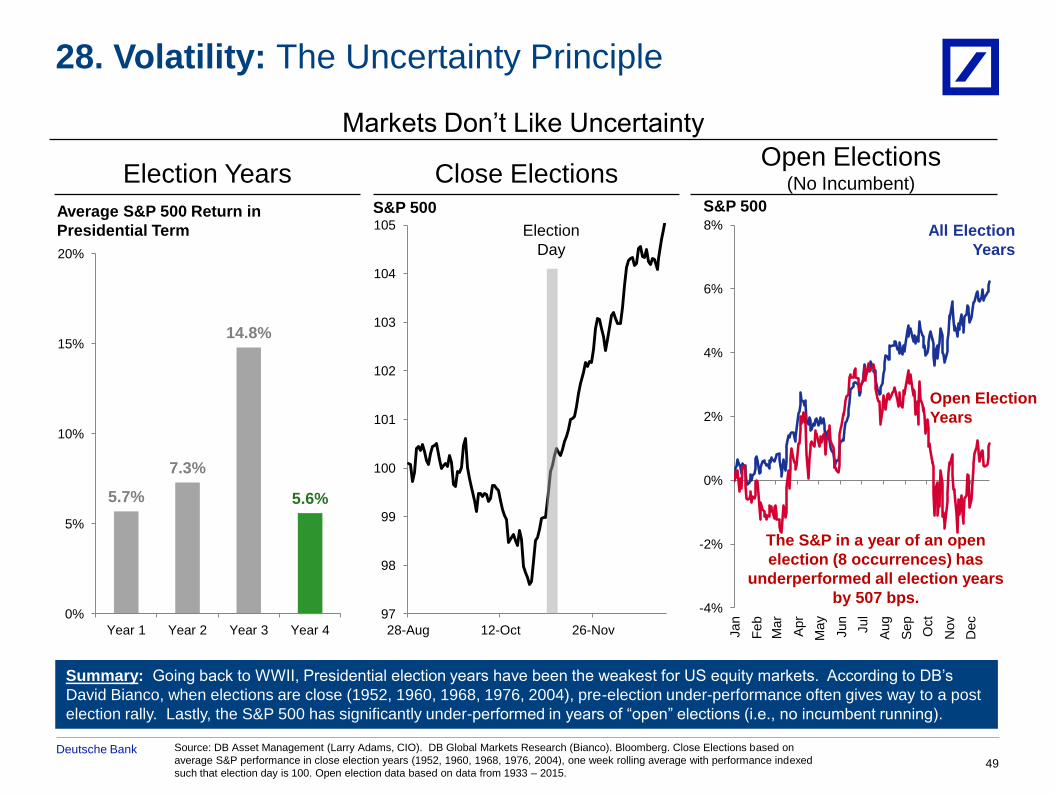

28. Volatility: The Uncertainty Principle

Summary: Going back to WWII, Presidential election years have been the weakest for US equity markets. According to DB’s

David Bianco, when elections are close (1952, 1960, 1968, 1976, 2004), pre-election under-performance often gives way to a post

election rally. Lastly, the S&P 500 has significantly under-performed in years of “open” elections (i.e., no incumbent running).

Election Years

Markets Don’t Like Uncertainty

Close Elections Open Elections

(No Incumbent)

5.7%

7.3%

14.8%

5.6%

0%

5%

10%

15%

20%

Year 1 Year 2 Year 3 Year 4

Average S&P 500 Return in

Presidential Term

97

98

99

100

101

102

103

104

105

28-Aug 12-Oct 26-Nov

Election

Day

S&P 500

The S&P in a year of an open

election (8 occurrences) has

underperformed all election years

by 507 bps.

All Election

Years

Open Election

Years

S&P 500

Deutsche Bank

10/17/2016

50

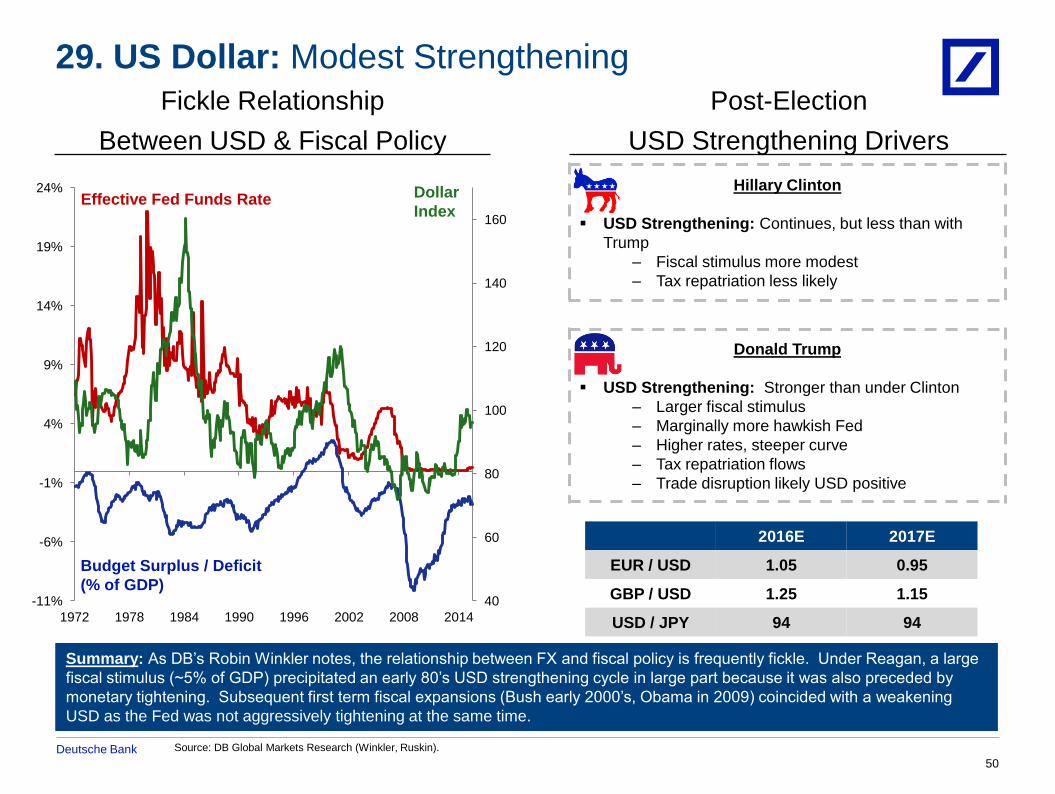

Source: DB Global Markets Research (Winkler, Ruskin).

29. US Dollar: Modest Strengthening

Fickle Relationship

Between USD & Fiscal Policy

2016E 2017E

EUR / USD 1.05 0.95

GBP / USD 1.25 1.15

USD / JPY 94 94

40

60

80

100

120

140

160

-11%

-6%

-1%

4%

9%

14%

19%

24%

1972 1978 1984 1990 1996 2002 2008 2014

Dollar

Index

Budget Surplus / Deficit

(% of GDP)

Effective Fed Funds Rate

Summary: As DB’s Robin Winkler notes, the relationship between FX and fiscal policy is frequently fickle. Under Reagan, a large

fiscal stimulus (~5% of GDP) precipitated an early 80’s USD strengthening cycle in large part because it was also preceded by

monetary tightening. Subsequent first term fiscal expansions (Bush early 2000’s, Obama in 2009) coincided with a weakening

USD as the Fed was not aggressively tightening at the same time.

Post-Election

USD Strengthening Drivers

Hillary Clinton

USD Strengthening: Continues, but less than with

Trump

– Fiscal stimulus more modest

– Tax repatriation less likely

Donald Trump

USD Strengthening: Stronger than under Clinton

– Larger fiscal stimulus

– Marginally more hawkish Fed

– Higher rates, steeper curve

– Tax repatriation flows

– Trade disruption likely USD positive

Deutsche Bank

12

13

14

15

16

17

18

19

20

2013 2014 2015 2016

10/17/2016

51

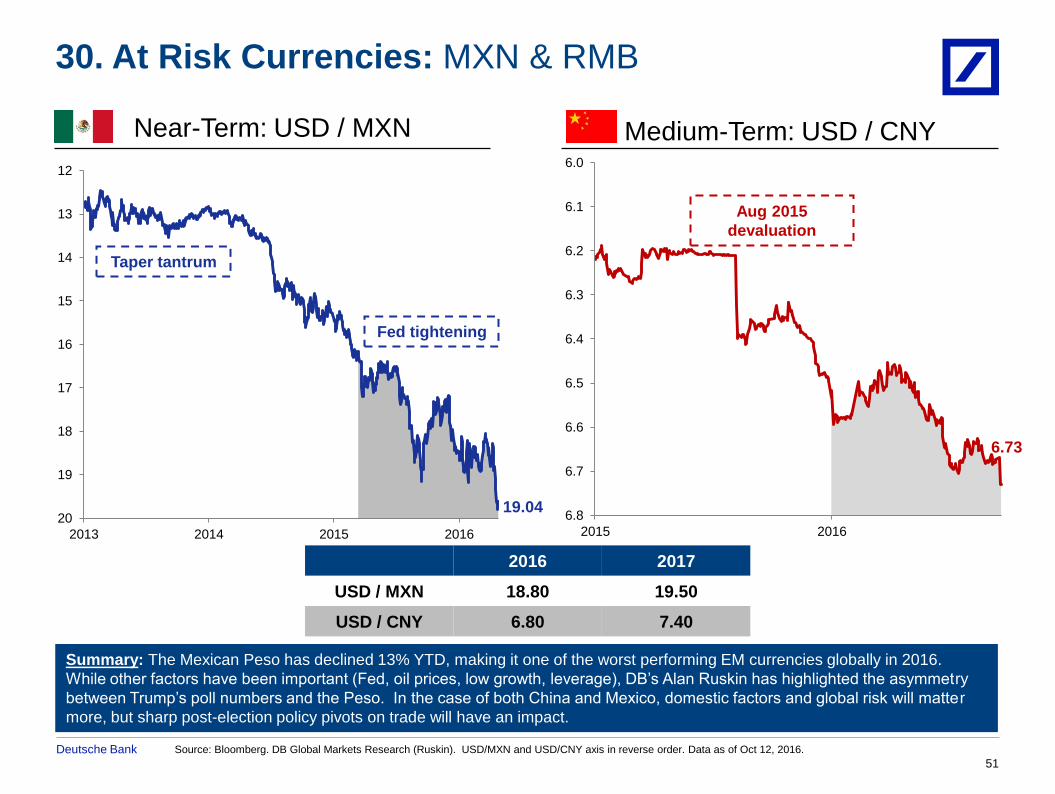

Source: Bloomberg. DB Global Markets Research (Ruskin). USD/MXN and USD/CNY axis in reverse order. Data as of Oct 12, 2016.

Near-Term: USD / MXN

2016 2017

USD / MXN 18.80 19.50

USD / CNY 6.80 7.40

Taper tantrum

Fed tightening

19.04

Aug 2015

devaluation

6.73

Medium-Term: USD / CNY

30. At Risk Currencies: MXN & RMB

Summary: The Mexican Peso has declined 13% YTD, making it one of the worst performing EM currencies globally in 2016.

While other factors have been important (Fed, oil prices, low growth, leverage), DB’s Alan Ruskin has highlighted the asymmetry

between Trump’s poll numbers and the Peso. In the case of both China and Mexico, domestic factors and global risk will matter

more, but sharp post-election policy pivots on trade will have an impact.

6.0

6.1

6.2

6.3

6.4

6.5

6.6

6.7

6.8

2015 2016

Deutsche Bank

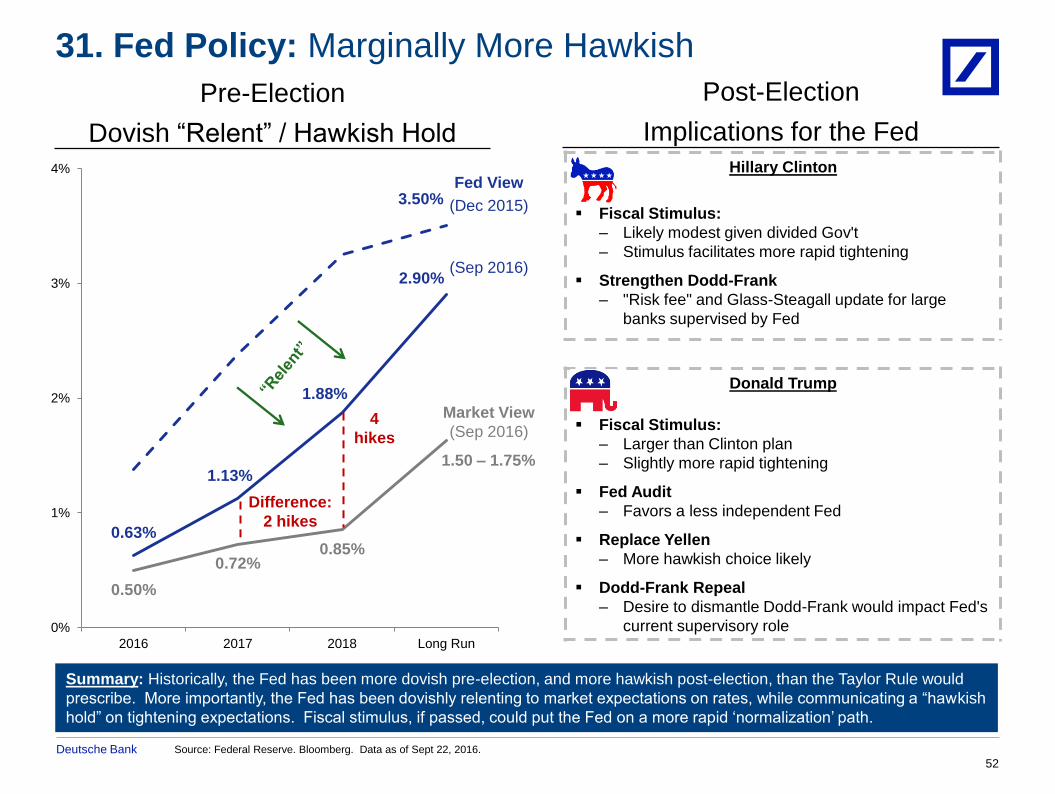

Hillary Clinton

Fiscal Stimulus:

– Likely modest given divided Gov't

– Stimulus facilitates more rapid tightening

Strengthen Dodd-Frank

– "Risk fee" and Glass-Steagall update for large

banks supervised by Fed

Donald Trump

Fiscal Stimulus:

– Larger than Clinton plan

– Slightly more rapid tightening

Fed Audit

– Favors a less independent Fed

Replace Yellen

– More hawkish choice likely

Dodd-Frank Repeal

– Desire to dismantle Dodd-Frank would impact Fed's

current supervisory role

10/17/2016

52

Source: Federal Reserve. Bloomberg. Data as of Sept 22, 2016.

31. Fed Policy: Marginally More Hawkish

Pre-Election

Dovish “Relent” / Hawkish Hold

Summary: Historically, the Fed has been more dovish pre-election, and more hawkish post-election, than the Taylor Rule would

prescribe. More importantly, the Fed has been dovishly relenting to market expectations on rates, while communicating a “hawkish

hold” on tightening expectations. Fiscal stimulus, if passed, could put the Fed on a more rapid ‘normalization’ path.

Post-Election

Implications for the Fed

3.50%

0.63%

1.13%

1.88%

2.90%

0.50%

0.72% 0.85%

0%

1%

2%

3%

4%

2016 2017 2018 Long Run

Market View

(Sep 2016)

(Dec 2015)

(Sep 2016)

Fed View

1.50 – 1.75%

Difference:

2 hikes

4

hikes

Deutsche Bank

10/17/2016

53

Source: DB Global Markets Research (Konstam. Winkler). Data as of September 15, 2016.

32. US Rates: Low Yields, Steeper Curve

Fiscal Stimulus & the Yield Curve

2016E 2017E

10Yr UST 1.75% 2.00%

Summary: Historically, the Fed matters more for US rates than elections. Having said that, if either Clinton or Trump managed to

push through a sizable fiscal stimulus (will be difficult), this would likely precipitate a hawkish re-pricing of Fed tightening

expectations, higher US rates, and a steeper yield curve. This, in turn, would be bullish for the Dollar.

Post-Election

US Rates Drivers

Fed Policy

– Matters more for US rates than elections

– Historically, more hawkish post election

– Trump would replace Yellen with more hawkish Chair

– Continued “financial repression” (excess monetary

easing) more likely under Clinton

Fiscal Stimulus

– Historically, curve steepening

– Form and size of stimulus matters (i.e., private sector

may “save” tax cuts)

– Productivity-enhancing if large and structured

properly

– Higher growth and terminal funds

– Accelerates Fed tightening

Tax Repatriation

– Could positively impact business spend and

productivity

Divided Government

– Historically, curve steepening

– Fiscal stimulus likely smaller -11%

-9%

-7%

-5%

-3%

-1%

1%

3%

1990 1994 1998 2002 2006 2010 2014

5s – 30s

Budget Surplus / Deficit

(% of GDP)

Deutsche Bank

10/17/2016

54

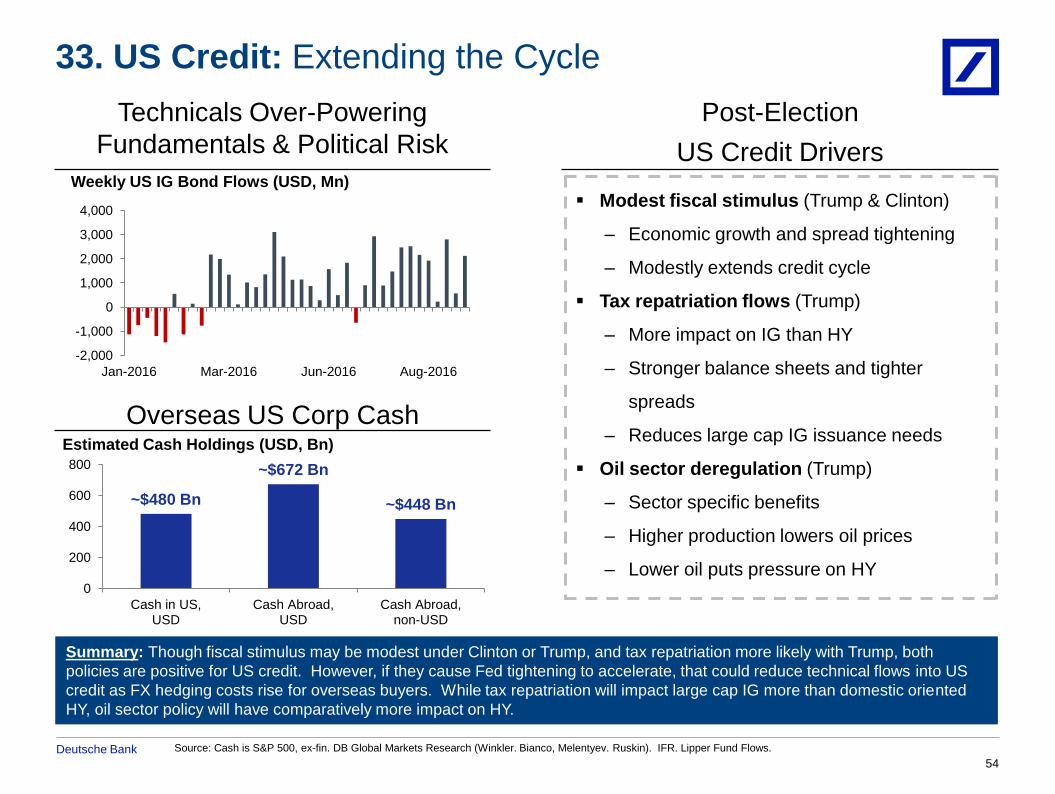

33. US Credit: Extending the Cycle

Technicals Over-Powering

Fundamentals & Political Risk

Post-Election

US Credit Drivers

Summary: Though fiscal stimulus may be modest under Clinton or Trump, and tax repatriation more likely with Trump, both

policies are positive for US credit. However, if they cause Fed tightening to accelerate, that could reduce technical flows into US

credit as FX hedging costs rise for overseas buyers. While tax repatriation will impact large cap IG more than domestic oriented

HY, oil sector policy will have comparatively more impact on HY.

Source: Cash is S&P 500, ex-fin. DB Global Markets Research (Winkler. Bianco, Melentyev. Ruskin). IFR. Lipper Fund Flows.

Modest fiscal stimulus (Trump & Clinton)

– Economic growth and spread tightening

– Modestly extends credit cycle

Tax repatriation flows (Trump)

– More impact on IG than HY

– Stronger balance sheets and tighter

spreads

– Reduces large cap IG issuance needs

Oil sector deregulation (Trump)

– Sector specific benefits

– Higher production lowers oil prices

– Lower oil puts pressure on HY

Overseas US Corp Cash

~$480 Bn

~$672 Bn

~$448 Bn

0

200

400

600

800

Cash in US, USD

Cash Abroad, USD

Cash Abroad, non-USD

Estimated Cash Holdings (USD, Bn)

Weekly US IG Bond Flows (USD, Mn)

-2,000

-1,000

0

1,000

2,000

3,000

4,000

Jan-2016 Mar-2016 Jun-2016 Aug-2016

Deutsche Bank

10/17/2016

55

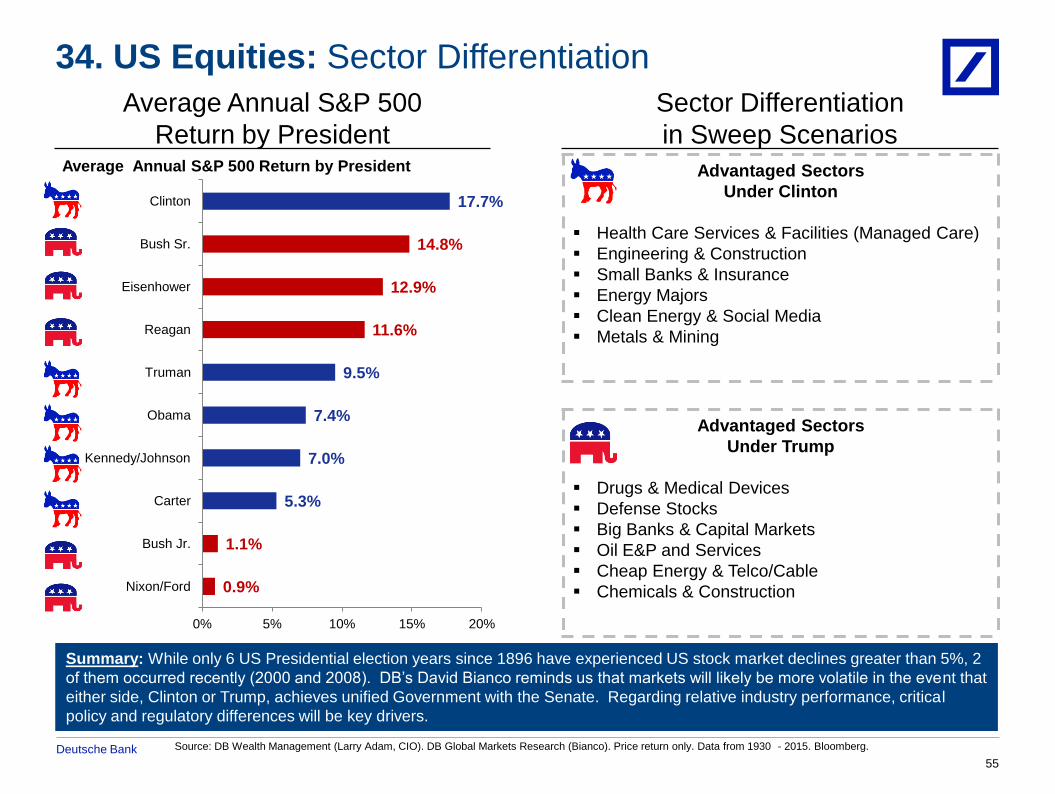

Source: DB Wealth Management (Larry Adam, CIO). DB Global Markets Research (Bianco). Price return only. Data from 1930 - 2015. Bloomberg.

34. US Equities: Sector Differentiation

Sector Differentiation

in Sweep Scenarios

Summary: While only 6 US Presidential election years since 1896 have experienced US stock market declines greater than 5%, 2

of them occurred recently (2000 and 2008). DB’s David Bianco reminds us that markets will likely be more volatile in the event that

either side, Clinton or Trump, achieves unified Government with the Senate. Regarding relative industry performance, critical

policy and regulatory differences will be key drivers.

Advantaged Sectors

Under Clinton

Health Care Services & Facilities (Managed Care)

Engineering & Construction

Small Banks & Insurance

Energy Majors

Clean Energy & Social Media

Metals & Mining

Advantaged Sectors

Under Trump

Drugs & Medical Devices

Defense Stocks

Big Banks & Capital Markets

Oil E&P and Services

Cheap Energy & Telco/Cable

Chemicals & Construction

Average Annual S&P 500

Return by President

17.7%

14.8%

12.9%

11.6%

9.5%

7.4%

7.0%

5.3%

1.1%

0.9%

0% 5% 10% 15% 20%

Clinton

Bush Sr.

Eisenhower

Reagan

Truman

Obama

Kennedy/Johnson

Carter

Bush Jr.

Nixon/Ford

Average Annual S&P 500 Return by President

Deutsche Bank

10/17/2016

56

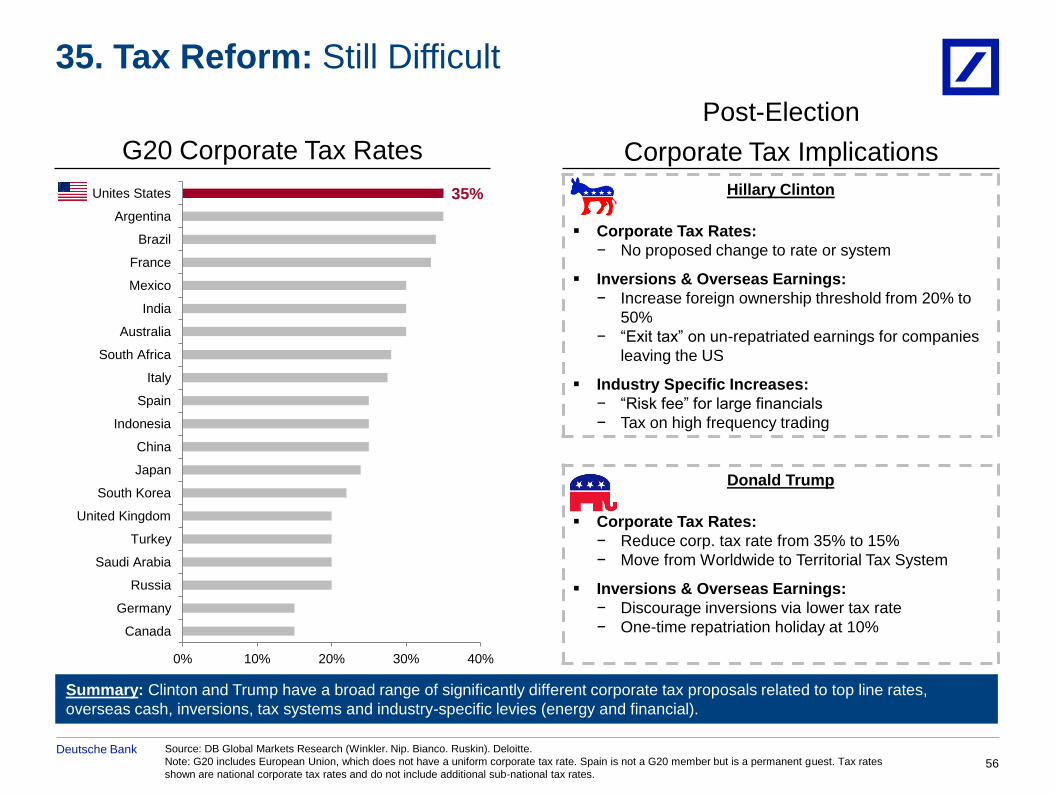

Source: DB Global Markets Research (Winkler. Nip. Bianco. Ruskin). Deloitte.

Note: G20 includes European Union, which does not have a uniform corporate tax rate. Spain is not a G20 member but is a permanent guest. Tax rates

shown are national corporate tax rates and do not include additional sub-national tax rates.

35. Tax Reform: Still Difficult

G20 Corporate Tax Rates

Summary: Clinton and Trump have a broad range of significantly different corporate tax proposals related to top line rates,

overseas cash, inversions, tax systems and industry-specific levies (energy and financial).

Post-Election

Corporate Tax Implications

Hillary Clinton

Corporate Tax Rates:

− No proposed change to rate or system

Inversions & Overseas Earnings:

− Increase foreign ownership threshold from 20% to

50%

− “Exit tax” on un-repatriated earnings for companies

leaving the US

Industry Specific Increases:

− “Risk fee” for large financials

− Tax on high frequency trading

Donald Trump

Corporate Tax Rates:

− Reduce corp. tax rate from 35% to 15%

− Move from Worldwide to Territorial Tax System

Inversions & Overseas Earnings:

− Discourage inversions via lower tax rate

− One-time repatriation holiday at 10%

35%

0% 10% 20% 30% 40%

Canada

Germany

Russia

Saudi Arabia

Turkey

United Kingdom

South Korea

Japan

China

Indonesia

Spain

Italy

South Africa

Australia

India

Mexico

France

Brazil

Argentina

Unites States

Deutsche Bank

Post-Election

Trade Implications

10/17/2016

57

Source: OECD. Pew Research. Financial Times. The World Trade Organization. The World Bank. Exports as % of GDP as of

2014. DB Global Markets Research (Hooper, Spencer, Slok).

36. Trade: Tide Shifting

Discriminatory Trade

Practices Rising Globally

US Trade Growth Since NAFTA

0%

10%

20%

30%

1960 1970 1980 1990 2000 2010

NAFTA

US Exports and Imports as % of GDP

Summary: At $380 bn in 2015, the US is the #1 FDI destination globally. Companies from proposed TPP and TTIP countries

account for 90% of inward US FDI. In the US, Congress has the ability to restrict the Trump or Clinton’s ambitions on a range of

social and economic issues (immigration, tax, spend). Notably, however, their protectionist trade pivots are an area where a new

President has more flexibility to unilaterally exercise power.

Hillary Clinton

Renegotiate NAFTA

Reject TPP

Unlikely to support TTIP

Strengthen enforcement of trade deals

Donald Trump

Renegotiate NAFTA

Reject TPP / Unlikely to support TTIP

Create the “Reagan Economic Zone”

“Tough on China”

− 45% tariffs

− WTO on steel subsidies

− Label as “currency manipulator”

28%

0

200

400

600

800

1000

1200

2008 2009 2010 2011 2012 2013 2014 2015 H1 2016

Number of discriminatory trade-related measures

Deutsche Bank

“Some men look at constitutions with sanctimonious reverence, and

deem them like the ark of the covenant, too sacred to be touched. They

ascribe to the preceding age a wisdom more than human, and suppose

what they did to be beyond amendment. I knew that age well; I belonged

to it and labored with it. It deserved well of its country… But I know also,

that laws and institutions must go hand in hand with the progress of the

human mind. As that becomes more developed, more enlightened, as

new discoveries are made, new truths discovered… institutions must

advance also, and keep pace with the times. We might as well require a

man to wear still the coat which fitted him as a boy as civilized society to

remain ever under the regime of their barbarous ancestors.”

- Thomas Jefferson, 3rd US President, toward the end of his life, in July 1816

Epilogue

Source: Joseph Ellis.

(1743 - 1826)

58

Deutsche Bank

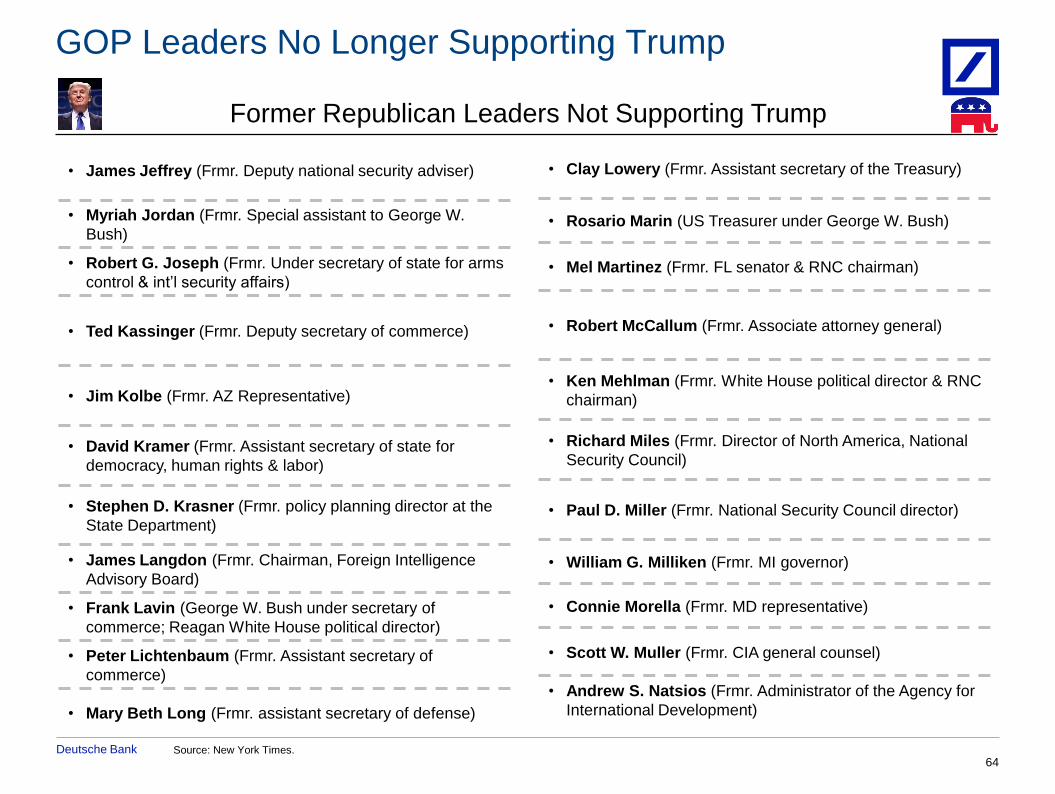

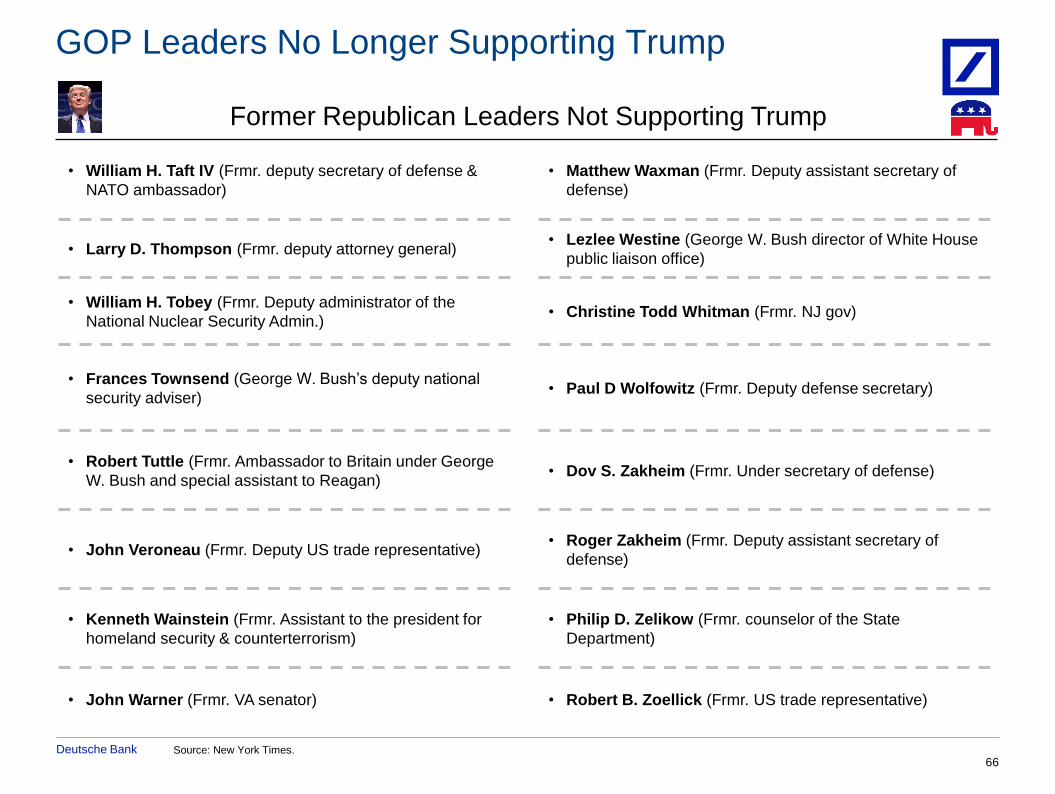

Appendix A: GOP Leaders No Longer Supporting Trump

Deutsche Bank Source: New York Times.

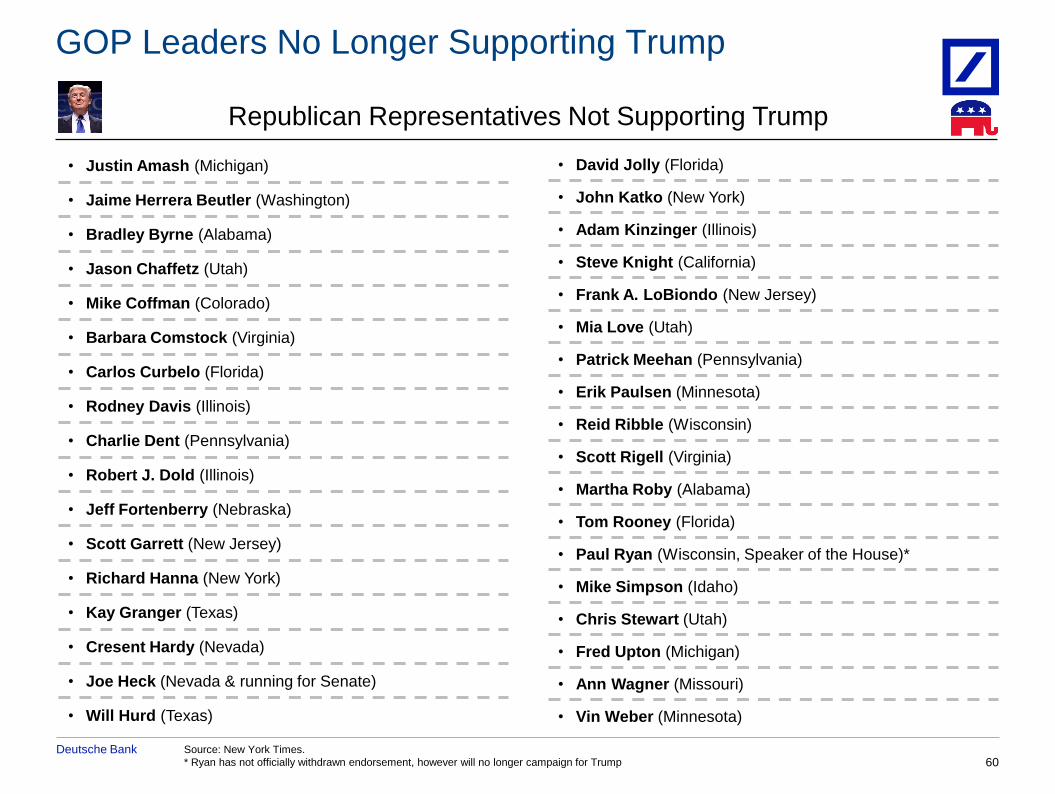

* Ryan has not officially withdrawn endorsement, however will no longer campaign for Trump 60

Republican Representatives Not Supporting Trump

• Justin Amash (Michigan)

• Jaime Herrera Beutler (Washington)

• Bradley Byrne (Alabama)

• Jason Chaffetz (Utah)

• Mike Coffman (Colorado)

• Barbara Comstock (Virginia)

• Carlos Curbelo (Florida)

• Rodney Davis (Illinois)

• Charlie Dent (Pennsylvania)

• Robert J. Dold (Illinois)

• Jeff Fortenberry (Nebraska)

• Scott Garrett (New Jersey)

• Richard Hanna (New York)

• Kay Granger (Texas)

• Cresent Hardy (Nevada)

• Joe Heck (Nevada & running for Senate)

• Will Hurd (Texas)

GOP Leaders No Longer Supporting Trump

• David Jolly (Florida)

• John Katko (New York)

• Adam Kinzinger (Illinois)

• Steve Knight (California)

• Frank A. LoBiondo (New Jersey)

• Mia Love (Utah)

• Patrick Meehan (Pennsylvania)

• Erik Paulsen (Minnesota)

• Reid Ribble (Wisconsin)

• Scott Rigell (Virginia)

• Martha Roby (Alabama)

• Tom Rooney (Florida)

• Paul Ryan (Wisconsin, Speaker of the House)*

• Mike Simpson (Idaho)

• Chris Stewart (Utah)

• Fred Upton (Michigan)

• Ann Wagner (Missouri)

• Vin Weber (Minnesota)

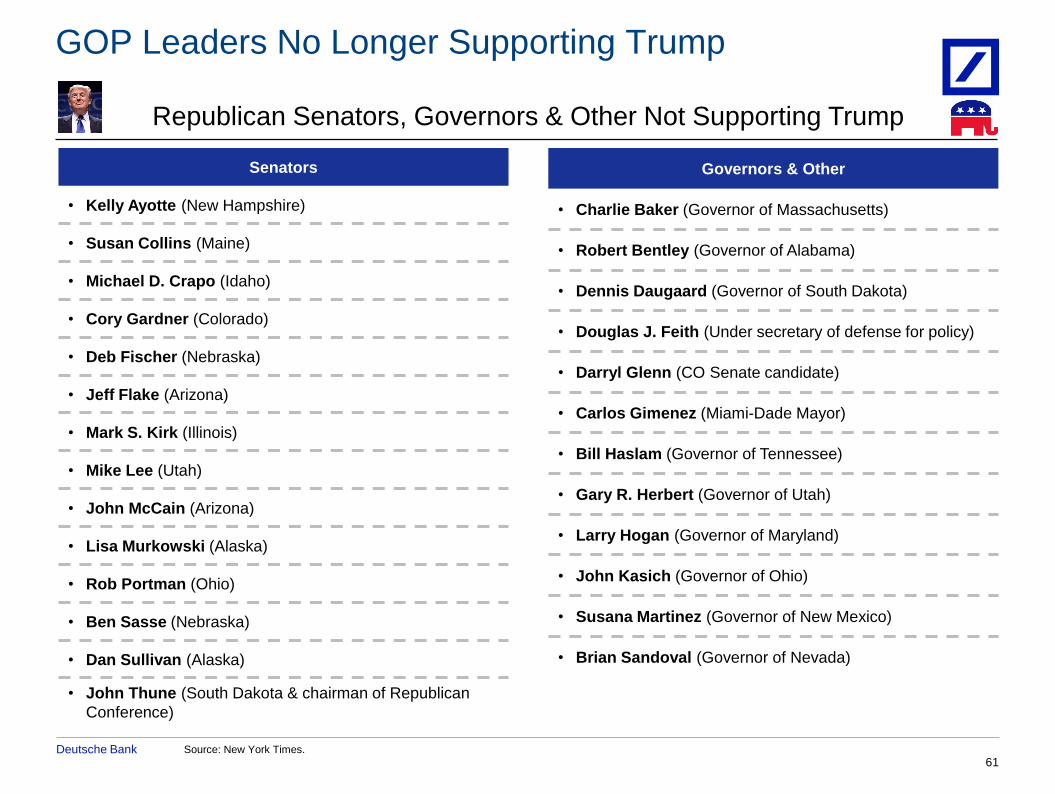

Deutsche Bank Source: New York Times.

GOP Leaders No Longer Supporting Trump

61

Republican Senators, Governors & Other Not Supporting Trump

Senators

• Kelly Ayotte (New Hampshire)

• Susan Collins (Maine)

• Michael D. Crapo (Idaho)

• Cory Gardner (Colorado)

• Deb Fischer (Nebraska)

• Jeff Flake (Arizona)

• Mark S. Kirk (Illinois)

• Mike Lee (Utah)

• John McCain (Arizona)

• Lisa Murkowski (Alaska)

• Rob Portman (Ohio)

• Ben Sasse (Nebraska)

• Dan Sullivan (Alaska)

• John Thune (South Dakota & chairman of Republican

Conference)

Governors & Other

• Charlie Baker (Governor of Massachusetts)

• Robert Bentley (Governor of Alabama)

• Dennis Daugaard (Governor of South Dakota)

• Douglas J. Feith (Under secretary of defense for policy)

• Darryl Glenn (CO Senate candidate)

• Carlos Gimenez (Miami-Dade Mayor)

• Bill Haslam (Governor of Tennessee)

• Gary R. Herbert (Governor of Utah)

• Larry Hogan (Governor of Maryland)

• John Kasich (Governor of Ohio)

• Susana Martinez (Governor of New Mexico)

• Brian Sandoval (Governor of Nevada)

Deutsche Bank 62

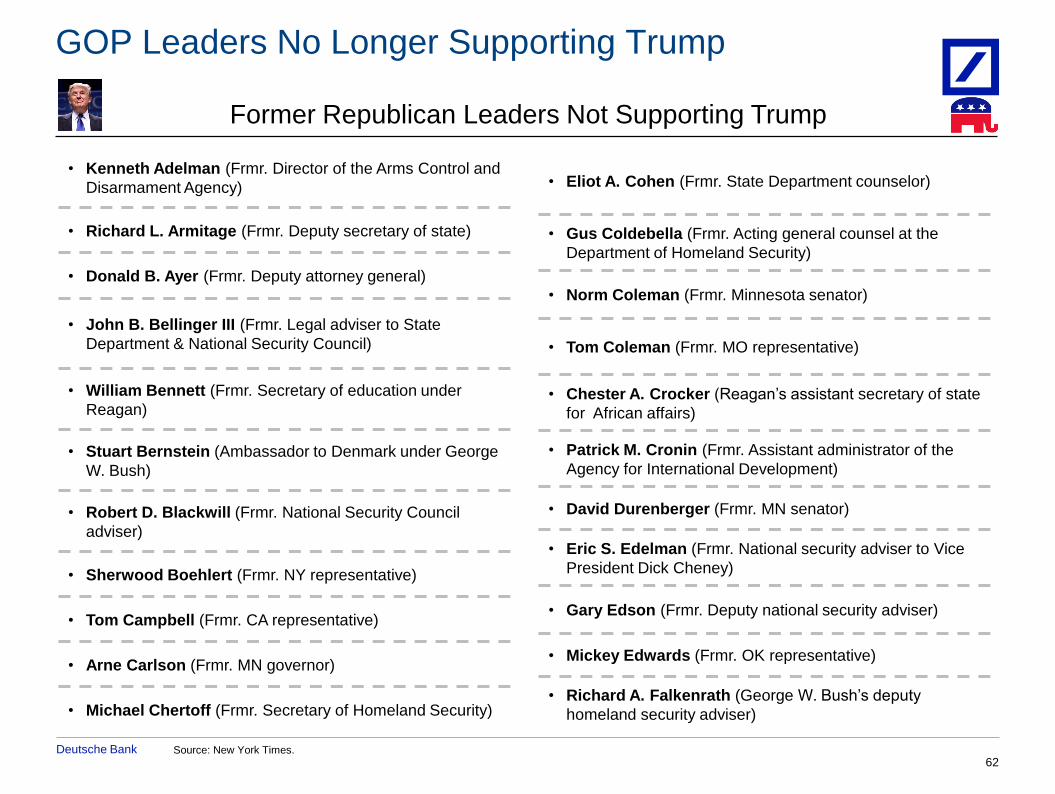

Former Republican Leaders Not Supporting Trump

• Kenneth Adelman (Frmr. Director of the Arms Control and

Disarmament Agency)

• Richard L. Armitage (Frmr. Deputy secretary of state)

• Donald B. Ayer (Frmr. Deputy attorney general)

• John B. Bellinger III (Frmr. Legal adviser to State

Department & National Security Council)

• William Bennett (Frmr. Secretary of education under

Reagan)

• Stuart Bernstein (Ambassador to Denmark under George

W. Bush)

• Robert D. Blackwill (Frmr. National Security Council

adviser)

• Sherwood Boehlert (Frmr. NY representative)

• Tom Campbell (Frmr. CA representative)

• Arne Carlson (Frmr. MN governor)

• Michael Chertoff (Frmr. Secretary of Homeland Security)

GOP Leaders No Longer Supporting Trump

Source: New York Times.

• Eliot A. Cohen (Frmr. State Department counselor)

• Gus Coldebella (Frmr. Acting general counsel at the

Department of Homeland Security)

• Norm Coleman (Frmr. Minnesota senator)

• Tom Coleman (Frmr. MO representative)

• Chester A. Crocker (Reagan’s assistant secretary of state

for African affairs)

• Patrick M. Cronin (Frmr. Assistant administrator of the

Agency for International Development)

• David Durenberger (Frmr. MN senator)

• Eric S. Edelman (Frmr. National security adviser to Vice

President Dick Cheney)

• Gary Edson (Frmr. Deputy national security adviser)

• Mickey Edwards (Frmr. OK representative)

• Richard A. Falkenrath (George W. Bush’s deputy

homeland security adviser)

Deutsche Bank 63