market trends impacting and opportunities for the u.s. peach market

TRANSCRIPT

www.perishablesgroup.com

Market Trends Impacting and

Opportunities for the U.S. Peach

Market

Presented by Nielsen Perishables Group

February, 2012

www.perishablesgroup.com 2

Agenda

Discussion Overview

Economic/Industry Trends to Consider

Peach Purchase Dynamics

Thoughts on Peach varietal marketing

Summary

www.perishablesgroup.com 3

PG 2012…

Exclusive Retail

Programs and

Advisory Board

Alliances with

Information

Leaders

Collaboration

with Trade

Organizations

www.perishablesgroup.com 4

PG Overview

Data from 13,000 Supermarkets• 48 Markets, 100+ Retail Banners

Shopper Dynamics• Approx. 50,000 consumer interviews• Loyalty Card Data—30 million households

Consumer Demographics-Spectra demographic profiles

Advanced Analytics• Price Elasticity• Promotional impacts

www.perishablesgroup.com 5

Strategic Considerations

Economy improving but consumers are changed

Consumers 2012 are in pursuit of “value”

The soft fruit category is confused, largely undifferentiated

and dominated by commodity products

Do Peaches have a Red Delicious problem?

Retailers have no road map for success

How do you drive success at retail?

Success 2012 = Store specific marketing:

Consumer usage and

demographics

2012: Markets and consumers driven by uncertainty

Source: Yahoo Finance; DQNews; ChicagoFed.org; EIA.gov

FUEL COSTS

EQUITY MARKETS LABOR MARKETSHOME PRICES

INFLATION

www.perishablesgroup.com 7

“Median household income on downslide

$49,445

$50,599

$50,939

$52,823

$52,124

$51,739

$51,174

$51,353

$51,398

$52,005

$53,164

'10

'09

'08

'07

'06

'05

'04

'03

'02

'01

'00

Median household income in 2010 inflation adjusted dollars

Source: THE CINCINNATI ENQUIRER, The New York Times, Census Bureau & USA Today

-2.3%

-0.7%

-3.6%

1.3%

0.7%

1.1%

-0.3%

-0.1%

-1.2%

-2.2%

-0.2%

'10

'09

'08

'07

'06

'05

'04

'03

'02

'01

'00

% Change from Previous Year

www.perishablesgroup.com 8

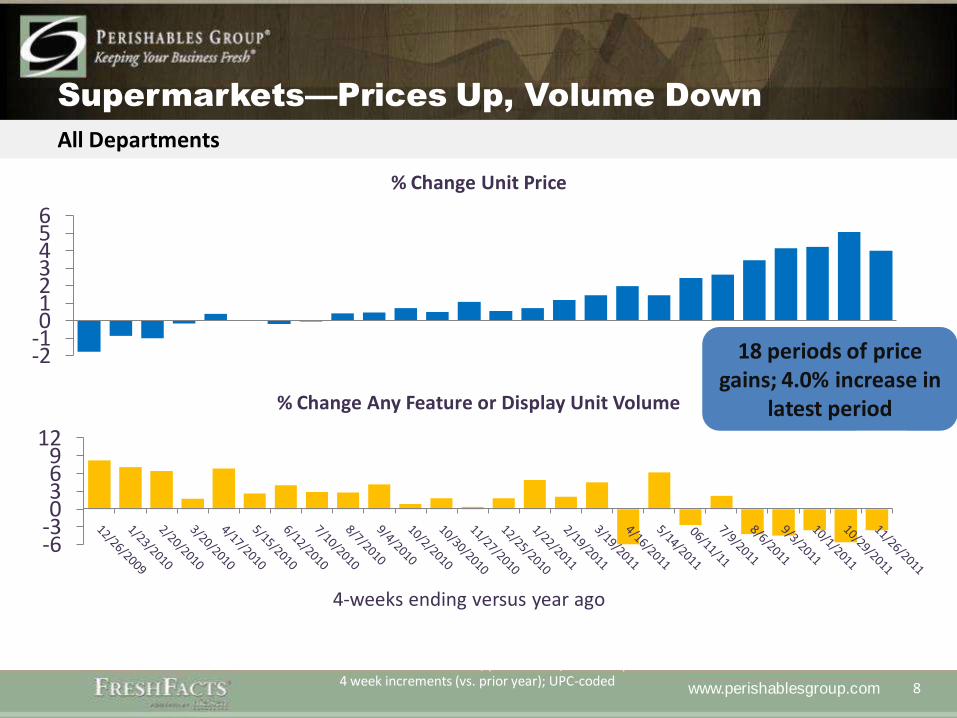

-2-10123456

% Change Unit Price

-6-30369

12

4-weeks ending versus year ago

% Change Any Feature or Display Unit Volume

Supermarkets—Prices Up, Volume Down

Source: Nielsen Scantrack, (U.S. FDM w/ Walmart) 4 week increments (vs. prior year); UPC-coded

All Departments

18 periods of price gains; 4.0% increase in

latest period

www.perishablesgroup.com 9

The new economic recovery….

U.S. Consumer is becoming more

polarized

www.perishablesgroup.com 10

The “Consumer Hourglass Theory”

A wide swath of American companies are convinced that the consumer market is bifurcating into high and low ends and eroding in the middle—the consumer hourglass is more pronounced now than ever.

“(Proctor and Gamble) The world's largest maker of consumer products is now betting that the squeeze on middle America will be long lasting. "It's required us to think differently about our product portfolio and how to please the high-end and lower-end markets," says Melanie Healey, group president of P&G's North America business. "That's frankly where a lot of the growth is happening.“

Wall Street Journal

September 12, 2011

Increasingly polarized consumers

Source: msnbc.com; CNN Money*Supplemental Nutrition Assistance Program (SNAP)

1 in 7 Americans rely on food stamps

1 in 2 Americans own stock, mutual fund, 401K or IRA

20% of Americans earn less than $20,000 a year

87% of Americans earning over $75,000 own stocks

www.perishablesgroup.com 12

-6%

-4%

-2%

0%

2%

4%

< $20K $20K -$29K

$30K -$39K

$40K -$49K

$50K -$69K

$70K -$99K

$100K +

Household Income

Shopping Trips Shopping Dollars

Polarized consumers

Source: Nielsen Homescan, 52 w/e 10/1/2011 versus 10/2/2010excludes gas-only or Rx-only trips

1 year trend

15% of USHHs

21% of USHHs

www.perishablesgroup.com 13

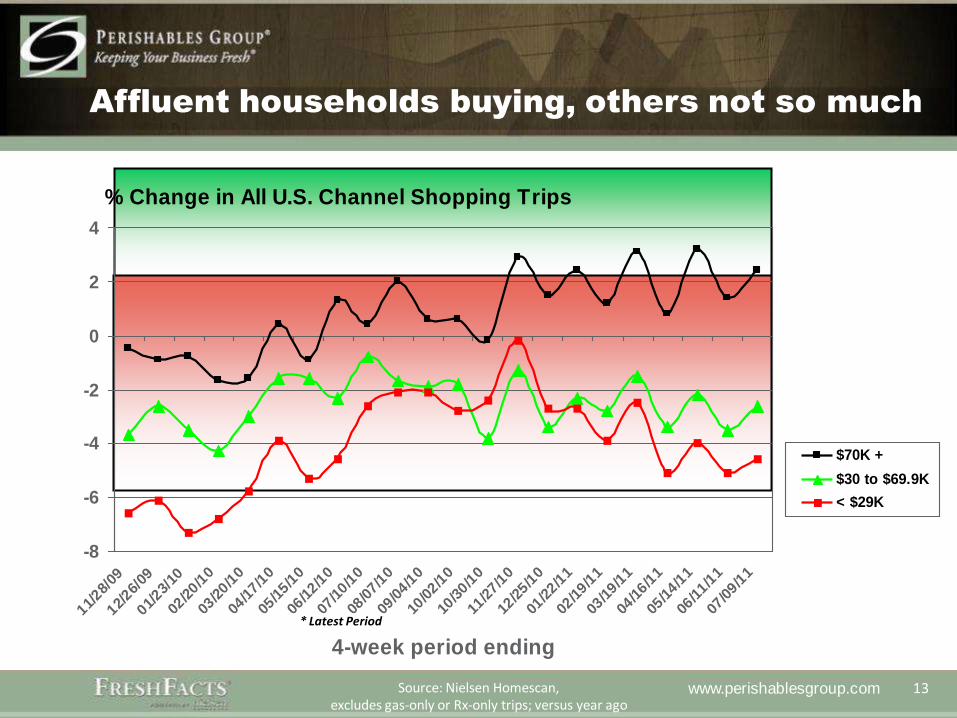

% Change in All U.S. Channel Shopping Trips

-8

-6

-4

-2

0

2

4

11/28/

09

12/26/

09

01/23/

10

02/20/1

0

03/20/1

0

04/17/1

0

05/15/1

0

06/12/1

0

07/10/1

0

08/07/1

0

09/04/1

0

10/02/1

0

10/30/1

0

11/27/1

0

12/25/1

0

01/22/1

1

02/19/1

1

03/19/1

1

04/16/1

1

05/14/1

1

06/11/1

1

07/09/1

1

4-week period ending

$70K +

$30 to $69.9K

< $29K

Affluent households buying, others not so much

* Latest Period

Source: Nielsen Homescan, excludes gas-only or Rx-only trips; versus year ago

www.perishablesgroup.com 14

It’s tough out there….even for college grads

www.perishablesgroup.com

15

WHAT DOES IT MEAN?

A Fresh Perspective on Category Development

www.perishablesgroup.com 16

Less Aggressive Deals, More Everyday Low Price

www.perishablesgroup.com 17

Focus Shifts from Shelf to Shopper

Circular ad

counts2

Source: 1) 2011 Global Retail CIO Survey from Aldata; 2) Perishables Group, Market Track Promotional Reporting; 3) Perishables Group FreshFacts® Powered by Nielsen

Volume sold on promo3

Promoted volume lift3

Promotional Retail Prices

Peaches

+5.3%

-13.2%

-30.2%

www.perishablesgroup.com 18

Consumer “Value” Intersects with Price

Price:“I want to save money”

Convenience:“I want something that will

save time”

Dietary Restrictions:“I need to lower my cholesterol.

What can I make that is more

healthy?”

Specialty:“Certain products are worth

the money”

Occasion:“I want to bring something

fancy/trendy to this party”

Indulgence:“I want to treat myself to

something special”

Health:“I don’t want my family to

be unhealthy”

Portion Control:“I don’t want to stuff myself”

Product Success Has Many Faces

www.perishablesgroup.com 19

CONVENIENCE

“I have so much to juggle right now. How can I cut down on

the time I spend in the kitchen?”

www.perishablesgroup.com 20

-3.4%

Consumers Visiting Retailers More

Frequently for Value-added Products

CONVENIENCE

+4.8% +0.8%

Trips per

Buyer

Value-Add Fruit Value-Add Veg Total Produce

Average

Retail Price+4.5% +14.6% +5.0%

Source: 1) Perishables Group FreshFacts® Powered by Nielsen, YTD 2) Perishables Group FreshFacts® Shopper Insights Powered by Spire, YTD

www.perishablesgroup.com 21

Wider Assortment Fueling Value-Added Growth

Source: Perishables Group FreshFacts® Powered by Nielsen, YTD

Average Retail Price: 4.9%

Dollars: 0.3%

Volume: 4.4% Bulk W

hole

Waterm

elon

Value-A

dd

Waterm

elon

Value-Added Produce Item Count

2006-2010: + 50%+ from 2006 to 2010

2011: 9.2% more value-add fruit items sold

11.2% more value-add vegetable items sold

Average Retail Price: $0.40/lbs

Average Retail Price: $1.17/lbs

Average Retail Price: 1.0%

Dollars: 108.0%

Volume: 105.8%

CONVENIENCE

www.perishablesgroup.com 22

TRIED AND TRUE INCREASINGLY

LOSES OUT TO VARIETY

“Since my go-to item is more expensive, maybe I should try

this new variety everyone is talking about?”

www.perishablesgroup.com 23

Newer Varieties Experienced Growth

Despite Higher Prices

TRIED AND TRUE

Volume Velocity: 10.1%

Dollar Velocity: 7.0%

Trips per Buyer 1.0%

Bulk N

avel

Oranges

3-pound

Clem

entines

Volume Velocity: 32.7%

Dollar Velocity: 32.6%

Trips per Buyer 2.0%

Average Retail Price: 3.4%

Regular Price: 1.2%

Promoted Price: 3.4%

Average Retail Price: 0.1%

Regular Price: 1.2%

Promo Price: 0.9%

www.perishablesgroup.com 24

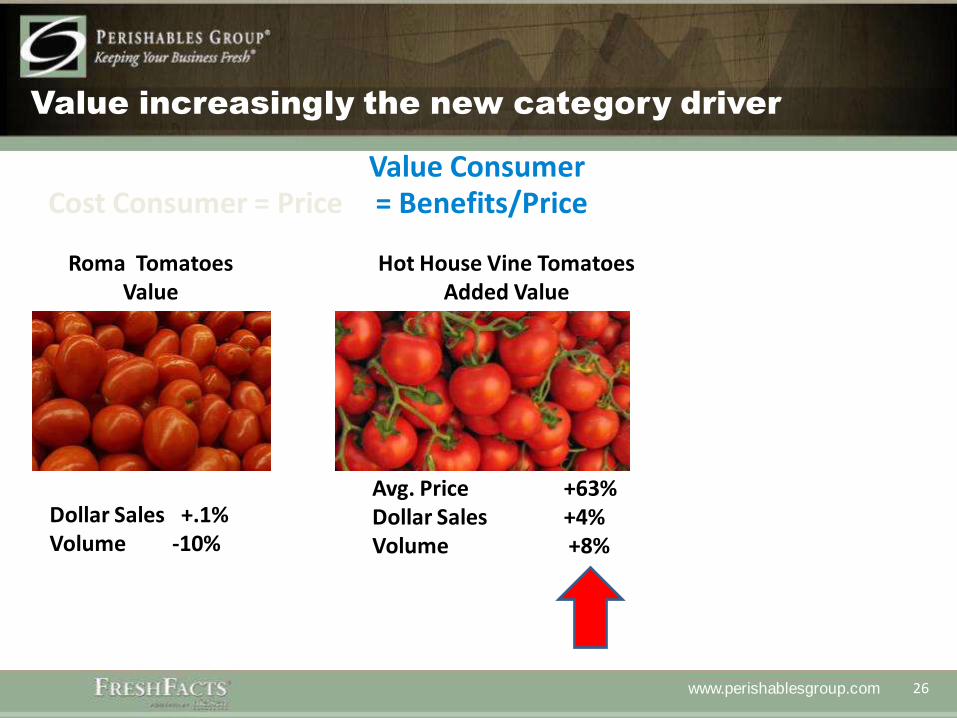

Cost Consumer = Price Value Consumer = Benefits/Price

Value increasingly the new category driver

Avg Price +121% higherDollar Sales 160%Unit Sales 203%

Dollar Sales 3%Unit Sales 1%

Remaining Yogurt Total Greek Yogurt

Dollar Sales6%

Unit Sales

Avg Price 83% higher Dollar Sales 9%Unit Sales 10%

Mainstream Chocolate Premium Chocolate

Dollar Sales -2%Pound Sales 1%

Avg Price 57% higher Dollar Sales 3%Pound Sales 5%

Pasta Excluding Health Healthy Pasta

Dollar Sales4%

Unit Sales -4%

Avg Price 18% higher Dollar Sales 8%Unit Sales 5%

Mainstream Coffee Premium Coffee Pod Coffee

Avg Price 40% higher Dollar Sales 115%Unit Sales 99%

Mid-Tier Toothpaste

Avg Price +268% higherDollar Sales 20%Unit Sales 20%

Dollar Sales-8%

Unit Sales -3%

Super Premium Toothpaste

Avg. Price +63% Dollar Sales +4%Volume +8%

Roma TomatoesValue

Hot House Vine TomatoesAdded Value

Snacking TomatoesPremium Value

Avg Price +126%Dollar Sales +10%Volume +5%

Dollar Sales +.1%Volume -10%

www.perishablesgroup.com 25

Cost Consumer = Price Value Consumer = Benefits/Price

Value increasingly the new category driver

Avg Price +121% higherDollar Sales 160%Unit Sales 203%

Dollar Sales 3%Unit Sales 1%

Remaining Yogurt Total Greek Yogurt

Dollar Sales6%

Unit Sales

Avg Price 83% higher Dollar Sales 9%Unit Sales 10%

Mainstream Chocolate Premium Chocolate

Dollar Sales -2%Pound Sales 1%

Avg Price 57% higher Dollar Sales 3%Pound Sales 5%

Pasta Excluding Health Healthy Pasta

Dollar Sales4%

Unit Sales -4%

Avg Price 18% higher Dollar Sales 8%Unit Sales 5%

Mainstream Coffee Premium Coffee Pod Coffee

Avg Price 40% higher Dollar Sales 115%Unit Sales 99%

Mid-Tier Toothpaste

Avg Price +268% higherDollar Sales 20%Unit Sales 20%

Dollar Sales-8%

Unit Sales -3%

Super Premium Toothpaste

Avg. Price +63% Dollar Sales +4%Volume +8%

Roma TomatoesPrice

Hot House Vine TomatoesAdded Value

Snacking TomatoesPremium Value

Avg Price +126%Dollar Sales +10%Volume +5%

Dollar Sales +.1%Volume -10%

www.perishablesgroup.com 26

Cost Consumer = PriceValue Consumer= Benefits/Price

Value increasingly the new category driver

Avg Price +121% higherDollar Sales 160%Unit Sales 203%

Dollar Sales 3%Unit Sales 1%

Remaining Yogurt Total Greek Yogurt

Dollar Sales6%

Unit Sales

Avg Price 83% higher Dollar Sales 9%Unit Sales 10%

Mainstream Chocolate Premium Chocolate

Dollar Sales -2%Pound Sales 1%

Avg Price 57% higher Dollar Sales 3%Pound Sales 5%

Pasta Excluding Health Healthy Pasta

Dollar Sales4%

Unit Sales -4%

Avg Price 18% higher Dollar Sales 8%Unit Sales 5%

Mainstream Coffee Premium Coffee Pod Coffee

Avg Price 40% higher Dollar Sales 115%Unit Sales 99%

Mid-Tier Toothpaste

Avg Price +268% higherDollar Sales 20%Unit Sales 20%

Dollar Sales-8%

Unit Sales -3%

Super Premium Toothpaste

Avg. Price +63% Dollar Sales +4%Volume +8%

Roma TomatoesValue

Hot House Vine TomatoesAdded Value

Snacking TomatoesPremium Value

Avg Price +126%Dollar Sales +10%Volume +5%

Dollar Sales +.1%Volume -10%

www.perishablesgroup.com 27

Cost Consumer = PriceValue Consumer= Benefits/Price

Value increasingly the new category driver

Avg Price +121% higherDollar Sales 160%Unit Sales 203%

Dollar Sales 3%Unit Sales 1%

Remaining Yogurt Total Greek Yogurt

Dollar Sales6%

Unit Sales

Avg Price 83% higher Dollar Sales 9%Unit Sales 10%

Mainstream Chocolate Premium Chocolate

Dollar Sales -2%Pound Sales 1%

Avg Price 57% higher Dollar Sales 3%Pound Sales 5%

Pasta Excluding Health Healthy Pasta

Dollar Sales4%

Unit Sales -4%

Avg Price 18% higher Dollar Sales 8%Unit Sales 5%

Mainstream Coffee Premium Coffee Pod Coffee

Avg Price 40% higher Dollar Sales 115%Unit Sales 99%

Mid-Tier Toothpaste

Avg Price +268% higherDollar Sales 20%Unit Sales 20%

Dollar Sales-8%

Unit Sales -3%

Super Premium Toothpaste

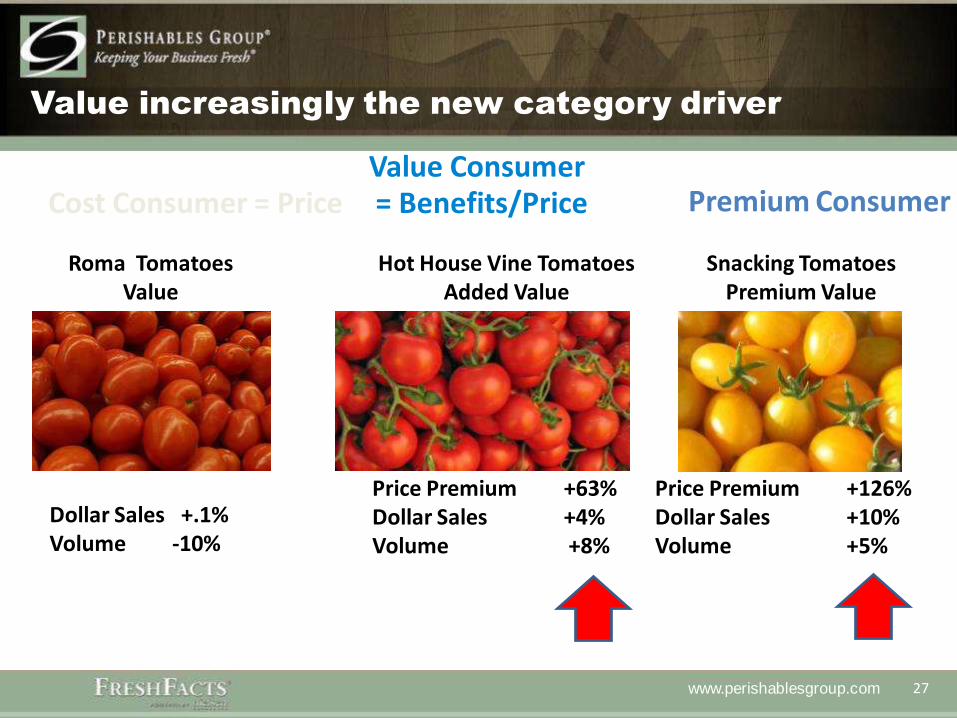

Price Premium +63% Dollar Sales +4%Volume +8%

Roma TomatoesValue

Hot House Vine TomatoesAdded Value

Snacking TomatoesPremium Value

Price Premium +126%Dollar Sales +10%Volume +5%

Dollar Sales +.1%Volume -10%

Premium Consumer

www.perishablesgroup.com 28

Cost Consumer = Price Value Consumer = Benefits/Price

Value increasingly the new category driver

Avg Price +121% higherDollar Sales 160%Unit Sales 203%

Dollar Sales 3%Unit Sales 1%

Remaining Yogurt Total Greek Yogurt

Dollar Sales6%

Unit Sales

Avg Price 83% higher Dollar Sales 9%Unit Sales 10%

Mainstream Chocolate Premium Chocolate

Dollar Sales -2%Pound Sales 1%

Avg Price 57% higher Dollar Sales 3%Pound Sales 5%

Pasta Excluding Health Healthy Pasta

Dollar Sales4%

Unit Sales -4%

Avg Price 18% higher Dollar Sales 8%Unit Sales 5%

Mainstream Coffee Premium Coffee Pod Coffee

Avg Price 40% higher Dollar Sales 115%Unit Sales 99%

Mid-Tier Toothpaste

Avg Price +268% higherDollar Sales 20%Unit Sales 20%

Dollar Sales-8%

Unit Sales -3%

Super Premium Toothpaste

Avg. Price +63% Dollar Sales +4%Volume +8%

Green PeppersValue

Hot House Vine TomatoesAdded Value

Snacking TomatoesPremium Value

Avg Price +126%Dollar Sales +10%Volume +5%

Dollar Sales +3%Volume +4%

www.perishablesgroup.com 29

Cost Consumer = Price Value Consumer = Benefits/Price

Value increasingly the new category driver

Avg Price +121% higherDollar Sales 160%Unit Sales 203%

Dollar Sales 3%Unit Sales 1%

Remaining Yogurt Total Greek Yogurt

Dollar Sales6%

Unit Sales

Avg Price 83% higher Dollar Sales 9%Unit Sales 10%

Mainstream Chocolate Premium Chocolate

Dollar Sales-2%

Pound Sales 1%

Avg Price 57% higher Dollar Sales 3%Pound Sales 5%

Pasta Excluding Health Healthy Pasta

Dollar Sales4%

Unit Sales -4%

Avg Price 18% higher Dollar Sales 8%Unit Sales 5%

Mainstream Coffee Premium Coffee Pod Coffee

Avg Price 40% higher Dollar Sales 115%Unit Sales 99%

Mid-Tier Toothpaste

Avg Price +268% higherDollar Sales 20%Unit Sales 20%

Dollar Sales-8%

Unit Sales -3%

Super Premium Toothpaste

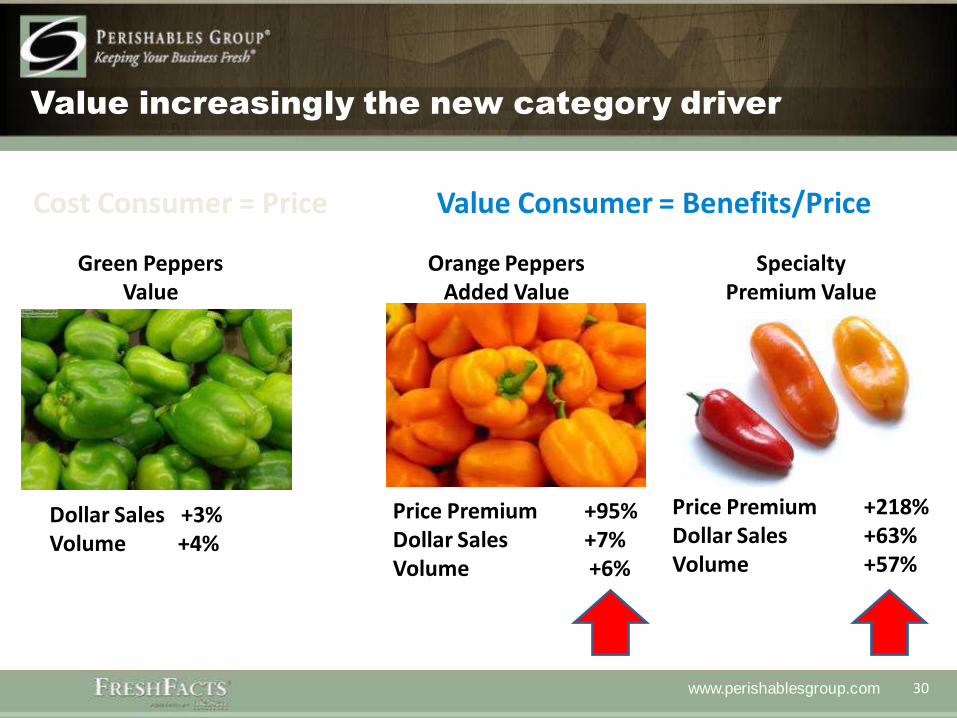

Price Premium +95% Dollar Sales +7%Volume +6%

Green PeppersValue

Orange PeppersAdded Value

Snacking TomatoesPremium Value

Avg Price +126%Dollar Sales +10%Volume +5%

Dollar Sales +3%Volume +4%

www.perishablesgroup.com 30

Cost Consumer = Price Value Consumer = Benefits/Price

Value increasingly the new category driver

Avg Price +121% higherDollar Sales 160%Unit Sales 203%

Dollar Sales 3%Unit Sales 1%

Remaining Yogurt Total Greek Yogurt

Dollar Sales6%

Unit Sales

Avg Price 83% higher Dollar Sales 9%Unit Sales 10%

Mainstream Chocolate Premium Chocolate

Dollar Sales -2%Pound Sales 1%

Avg Price 57% higher Dollar Sales 3%Pound Sales 5%

Pasta Excluding Health Healthy Pasta

Dollar Sales4%

Unit Sales -4%

Avg Price 18% higher Dollar Sales 8%Unit Sales 5%

Mainstream Coffee Premium Coffee Pod Coffee

Avg Price 40% higher Dollar Sales 115%Unit Sales 99%

Mid-Tier Toothpaste

Avg Price +268% higherDollar Sales 20%Unit Sales 20%

Dollar Sales-8%

Unit Sales -3%

Super Premium Toothpaste

Price Premium +95% Dollar Sales +7%Volume +6%

Green PeppersValue

Orange PeppersAdded Value

SpecialtyPremium Value

Price Premium +218%Dollar Sales +63%Volume +57%

Dollar Sales +3%Volume +4%

www.perishablesgroup.com 31

Cost Consumer = Price Value Consumer = Benefits/Price

Value increasingly the new category driver

Avg Price +121% higherDollar Sales 160%Unit Sales 203%

Dollar Sales 3%Unit Sales 1%

Remaining Yogurt Total Greek Yogurt

Dollar Sales6%

Unit Sales

Avg Price 83% higher Dollar Sales 9%Unit Sales 10%

Mainstream Chocolate Premium Chocolate

Dollar Sales -2%Pound Sales 1%

Avg Price 57% higher Dollar Sales 3%Pound Sales 5%

Pasta Excluding Health Healthy Pasta

Dollar Sales4%

Unit Sales -4%

Avg Price 18% higher Dollar Sales 8%Unit Sales 5%

Mainstream Coffee Premium Coffee Pod Coffee

Avg Price 40% higher Dollar Sales 115%Unit Sales 99%

Mid-Tier Toothpaste

Avg Price +268% higherDollar Sales 20%Unit Sales 20%

Dollar Sales-8%

Unit Sales -3%

Super Premium Toothpaste

Price Premium +1% Dollar Sales +13%Volume +9%

Yellow Peaches White Flesh PeachesAdded Value

Strawberry PeachPremium Value

Price Premium +84%Dollar Sales +15%Volume +25%

Dollar Sales +5%Volume -5%

www.perishablesgroup.com 32

Cost Consumer = Price Value Consumer = Benefits/Price

Value increasingly the new category driver

Avg Price +121% higherDollar Sales 160%Unit Sales 203%

Dollar Sales 3%Unit Sales 1%

Remaining Yogurt Total Greek Yogurt

Dollar Sales6%

Unit Sales

Avg Price 83% higher Dollar Sales 9%Unit Sales 10%

Mainstream Chocolate Premium Chocolate

Dollar Sales -2%Pound Sales 1%

Avg Price 57% higher Dollar Sales 3%Pound Sales 5%

Pasta Excluding Health Healthy Pasta

Dollar Sales4%

Unit Sales -4%

Avg Price 18% higher Dollar Sales 8%Unit Sales 5%

Mainstream Coffee Premium Coffee Pod Coffee

Avg Price 40% higher Dollar Sales 115%Unit Sales 99%

Mid-Tier Toothpaste

Avg Price +268% higherDollar Sales 20%Unit Sales 20%

Dollar Sales-8%

Unit Sales -3%

Super Premium Toothpaste

Price Premium +5% Dollar Sales +13%Volume +9%

Yellow Peaches White Flesh PeachesAdded Value

Strawberry PeachPremium Value

Price Premium +84%Dollar Sales +15%Volume +25%

Dollar Sales +5%Volume -5%

www.perishablesgroup.com 33

Cost Consumer = Price Value Consumer = Benefits/Price

Value increasingly the new category driver

Avg Price +121% higherDollar Sales 160%Unit Sales 203%

Dollar Sales 3%Unit Sales 1%

Remaining Yogurt Total Greek Yogurt

Dollar Sales6%

Unit Sales

Avg Price 83% higher Dollar Sales 9%Unit Sales 10%

Mainstream Chocolate Premium Chocolate

Dollar Sales -2%Pound Sales 1%

Avg Price 57% higher Dollar Sales 3%Pound Sales 5%

Pasta Excluding Health Healthy Pasta

Dollar Sales4%

Unit Sales -4%

Avg Price 18% higher Dollar Sales 8%Unit Sales 5%

Mainstream Coffee Premium Coffee Pod Coffee

Avg Price 40% higher Dollar Sales 115%Unit Sales 99%

Mid-Tier Toothpaste

Avg Price +268% higherDollar Sales 20%Unit Sales 20%

Dollar Sales-8%

Unit Sales -3%

Super Premium Toothpaste

Price Premium +5% Dollar Sales +13%Volume +9%

Yellow Peaches White Flesh PeachesAdded Value

Strawberry PeachPremium Value

Price Premium +84%Dollar Sales +15%Volume +25%

Dollar Sales +5%Volume -5%

www.perishablesgroup.com 34

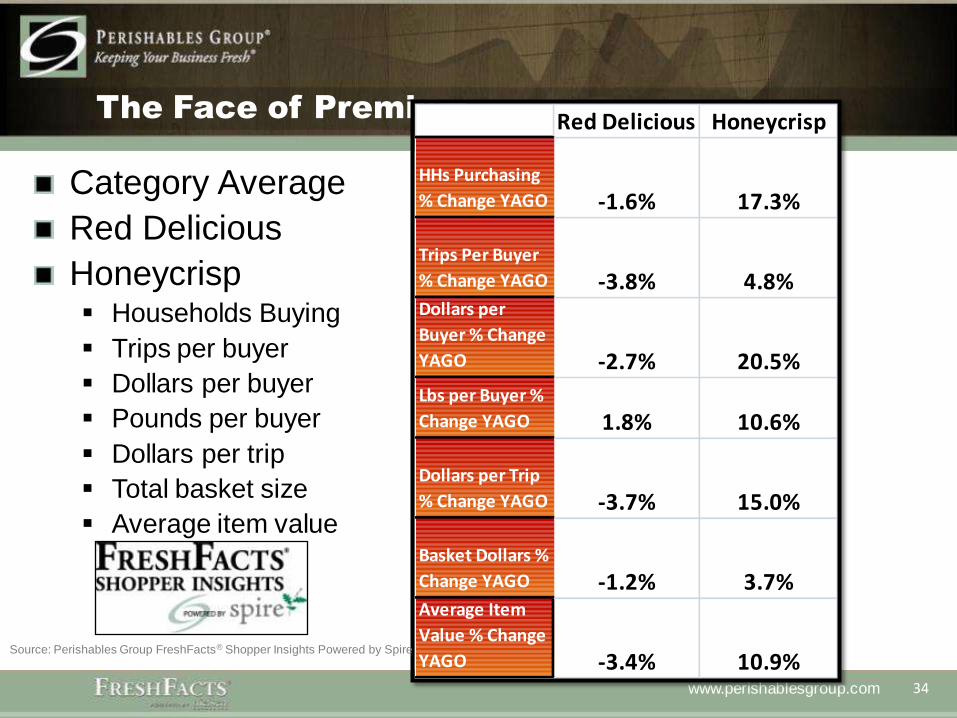

The Face of Premium…

Category Average $1.34

Red Delicious $1.31

Honeycrisp $1.99 Households Buying

Trips per buyer

Dollars per buyer

Pounds per buyer

Dollars per trip

Total basket size

Average item value

Red Delicious Honeycrisp

HHs Purchasing

% Change YAGO -1.6% 17.3%

Trips Per Buyer

% Change YAGO -3.8% 4.8%Dollars per

Buyer % Change

YAGO -2.7% 20.5%

Lbs per Buyer %

Change YAGO 1.8% 10.6%

Dollars per Trip

% Change YAGO -3.7% 15.0%

Basket Dollars %

Change YAGO -1.2% 3.7%Average Item

Value % Change

YAGO -3.4% 10.9%Source: Perishables Group FreshFacts® Shopper Insights Powered by Spire

www.perishablesgroup.com 35

Dollars per Transaction by Variety

$3.37

$3.00

$3.37$3.16

$2.82

$4.15

$2.95

$3.08$3.14 $3.07

$3.26 $3.10

$3.44

$3.10 $2.97

$5.12

$2.97$3.01

$3.41$3.30

Gala Red Delicious

Fuji Granny Smith

Golden Delicious

Honeycrisp McIntosh Braeburn Pink Lady Empire

FreshFacts Shopper Insights - Retailer CompositeAverage Apple Subcategories Dollars per Transaction

52 Weeks Ending Q2 2011

Prior Year Current Year

www.perishablesgroup.com 36

“Value” Often More Powerful Than Price…

Success is about understanding your consumer and

innovating to create value beyond price

Where Price Matters

Where Innovation Pays

TRIED AND TRUE

CONVENIENCEORGANIC

SUBSTITUTION

NEW FLAVORS

COMMODITY ITEMS

www.perishablesgroup.com 37

The New Fresh Landscape

2000 2012

Consumers follow price cues Consumers optimize value

Narrow category assortment Complex categories

Commodity focus by retailers Store specific focus

Limited consumer understanding Diversified consumers

Few opportunities for supply-side engagement Retailer-supplier partnership expectations

New Challenges for the Industry

www.perishablesgroup.com 38

The New Fresh Landscape

2000 2012

Consumers follow price cues Consumers optimize value

Narrow category assortment Complex categories

Commodity focus by retailers Store specific focus

Limited consumer understanding Diversified consumers

Few opportunities for supply-side engagement Retailer-supplier partnership expectations

New Challenges for the Industry

www.perishablesgroup.com 39

The New Fresh Landscape

2000 2012

Consumers follow price cues Consumers optimize value

Narrow category assortment Complex categories

Commodity focus by retailers Store specific focus

Limited consumer understanding Diversified consumers

Few opportunities for supply-side engagement Retailer-supplier partnership expectations

New Challenges for the Industry

www.perishablesgroup.com 40

The New Fresh Landscape

2000 2012

Consumers follow price cues Consumers optimize value

Narrow category assortment Complex categories

Commodity focus by retailers Store specific focus

Limited consumer understanding Diversified consumers

Few opportunities for supply-side engagement Retailer-supplier partnership expectations

New Challenges for the Industry

www.perishablesgroup.com 41

The New Fresh Landscape

2000 2012

Consumers follow price cues Consumers optimize value

Narrow category assortment Complex categories

Commodity focus by retailers Store specific focus

Limited consumer understanding Diversified consumers

Few opportunities for supply-side engagement Retailer-supplier partnership expectations

New Challenges for the Industry

www.perishablesgroup.com

42

UNDERSTANDING PEACH

PERFORMANCE AT RETAIL

www.perishablesgroup.com 43

Q3, 2011 Performance Total

Peach dollars increased due to price increases while

volume declined

Source: Perishables Group FreshFacts® Powered by Nielsen, Q3, 2011 vs. YAGO

Product Dollars %

Change vs

YAGO

Volume %

Change vs

YAGO

Average

Retail

Average Retail %

Change vs YAGO

Stone Fruits 5.6% -0.4% $1.53 6.0%

Peaches 6.2% -3.6% $1.45 10.2%

Nectarines 7.0% 3.9% $1.54 3.0%

Plums 1.5% 2.1% $1.64 -0.6%

www.perishablesgroup.com 44

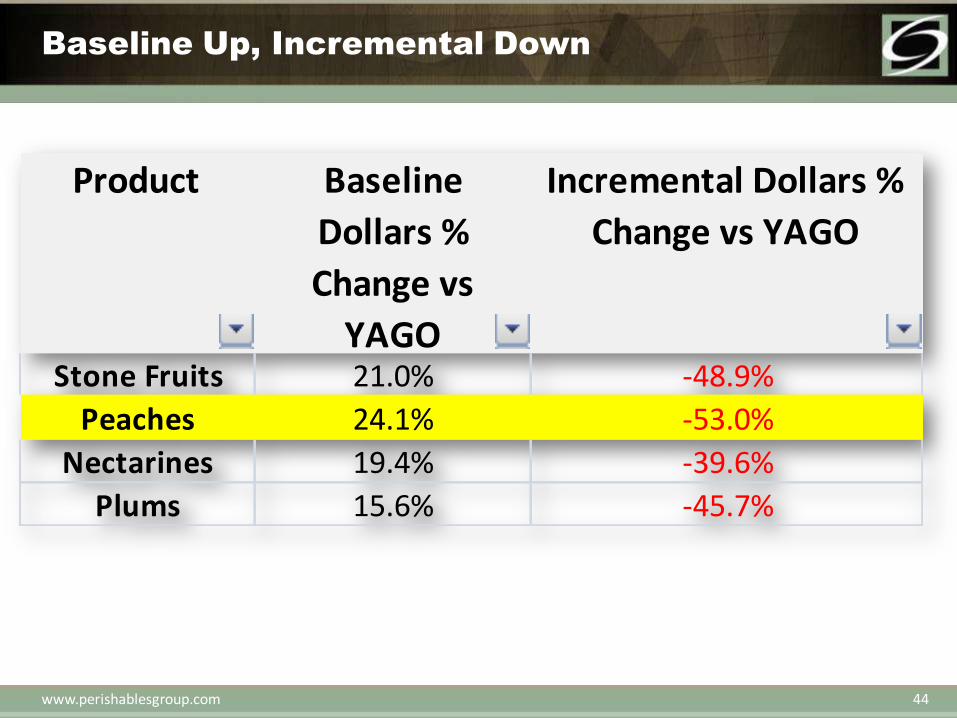

Baseline Up, Incremental Down

Product Baseline

Dollars %

Change vs

YAGO

Incremental Dollars %

Change vs YAGO

Stone Fruits 21.0% -48.9%

Peaches 24.1% -53.0%

Nectarines 19.4% -39.6%

Plums 15.6% -45.7%

www.perishablesgroup.com 45

Promotions Lose Impact

Product Dollars % on

Promotion

Dollars % on

Promotion YAGO

Dollars % Lift

on Promotion

Dollars % Lift

on Promotion

YAGO

Stone Fruits 37.7% 44.9% 41.2% 66.3%

Peaches 39.1% 47.1% 41.4% 69.2%

Nectarines 36.8% 44.1% 39.5% 59.5%

Plums 37.3% 41.9% 45.5% 74.0%

Very Similar Performance in Volume

www.perishablesgroup.com 46

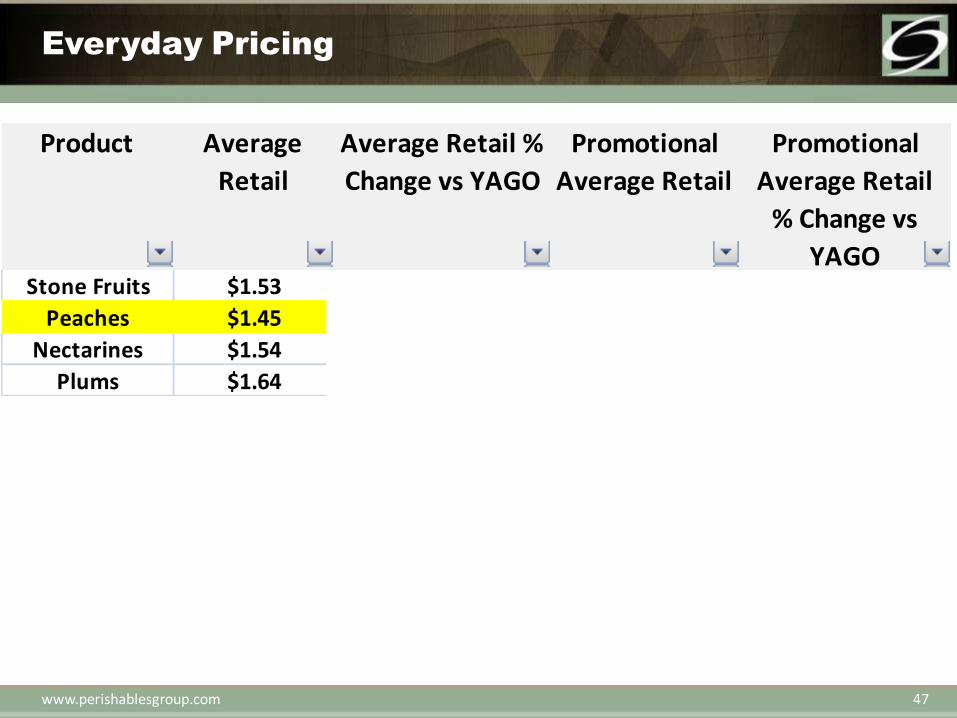

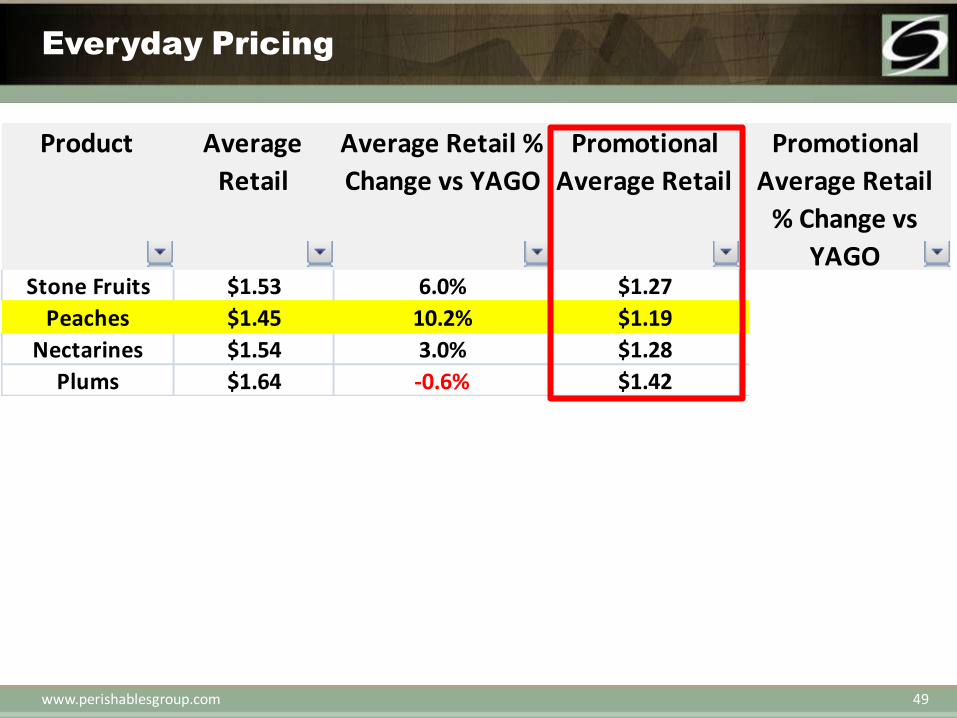

Everyday Pricing

Product Average

Retail

Average Retail %

Change vs YAGO

Promotional

Average Retail

Promotional

Average Retail

% Change vs

YAGOStone Fruits $1.53 6.0% $1.27 3.2%

Peaches $1.45 10.2% $1.19 5.3%

Nectarines $1.54 3.0% $1.28 2.0%

Plums $1.64 -0.6% $1.42 -1.5%

www.perishablesgroup.com 47

Everyday Pricing

Product Average

Retail

Average Retail %

Change vs YAGO

Promotional

Average Retail

Promotional

Average Retail

% Change vs

YAGOStone Fruits $1.53 6.0% $1.27 3.2%

Peaches $1.45 10.2% $1.19 5.3%

Nectarines $1.54 3.0% $1.28 2.0%

Plums $1.64 -0.6% $1.42 -1.5%

www.perishablesgroup.com 48

Everyday Pricing

Product Average

Retail

Average Retail %

Change vs YAGO

Promotional

Average Retail

Promotional

Average Retail

% Change vs

YAGOStone Fruits $1.53 6.0% $1.27 3.2%

Peaches $1.45 10.2% $1.19 5.3%

Nectarines $1.54 3.0% $1.28 2.0%

Plums $1.64 -0.6% $1.42 -1.5%

www.perishablesgroup.com 49

Everyday Pricing

Product Average

Retail

Average Retail %

Change vs YAGO

Promotional

Average Retail

Promotional

Average Retail

% Change vs

YAGOStone Fruits $1.53 6.0% $1.27 3.2%

Peaches $1.45 10.2% $1.19 5.3%

Nectarines $1.54 3.0% $1.28 2.0%

Plums $1.64 -0.6% $1.42 -1.5%

www.perishablesgroup.com 50

Everyday Pricing

Product Average

Retail

Average Retail %

Change vs YAGO

Promotional

Average Retail

Promotional

Average Retail

% Change vs

YAGOStone Fruits $1.53 6.0% $1.27 3.2%

Peaches $1.45 10.2% $1.19 5.3%

Nectarines $1.54 3.0% $1.28 2.0%

Plums $1.64 -0.6% $1.42 -1.5%

www.perishablesgroup.com 51

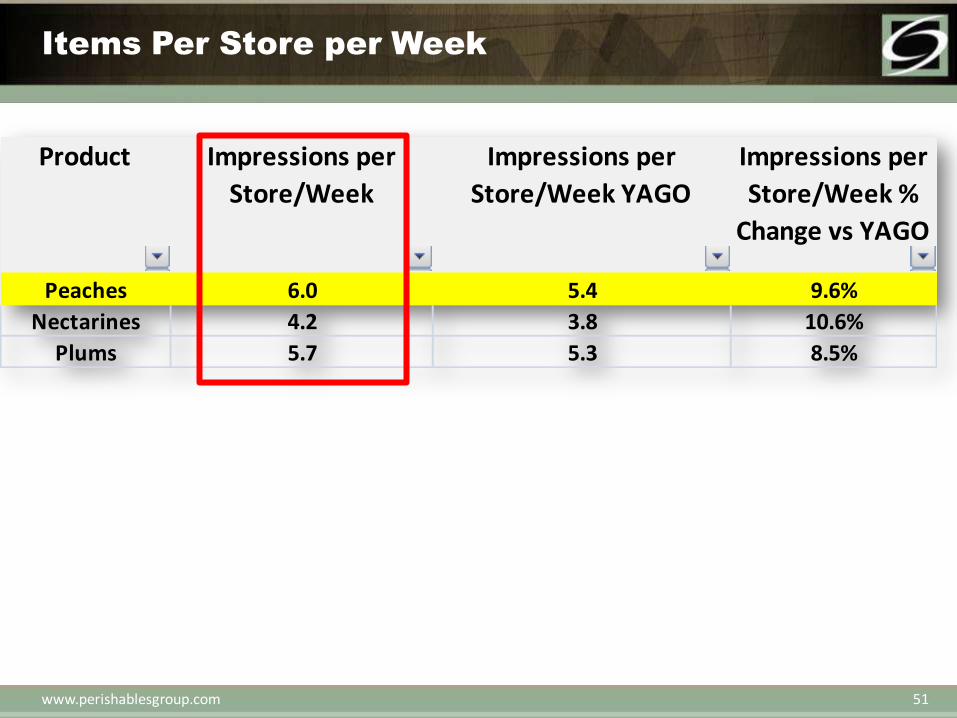

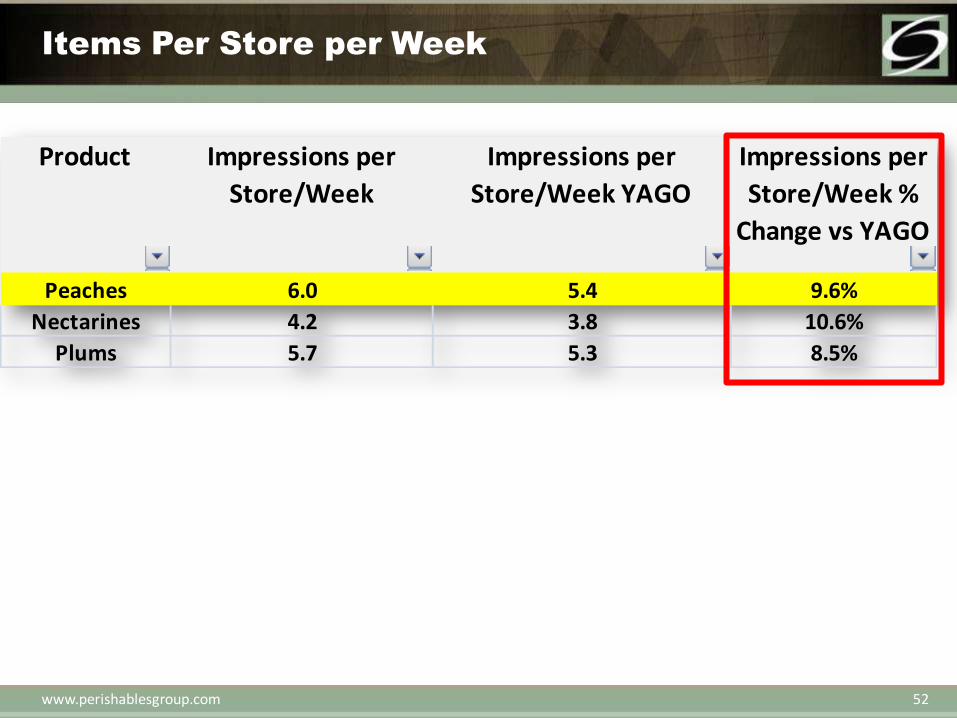

Items Per Store per Week

Product Impressions per

Store/Week

Impressions per

Store/Week YAGO

Impressions per

Store/Week %

Change vs YAGO

Peaches 6.0 5.4 9.6%

Nectarines 4.2 3.8 10.6%

Plums 5.7 5.3 8.5%

www.perishablesgroup.com 52

Items Per Store per Week

Product Impressions per

Store/Week

Impressions per

Store/Week YAGO

Impressions per

Store/Week %

Change vs YAGO

Peaches 6.0 5.4 9.6%

Nectarines 4.2 3.8 10.6%

Plums 5.7 5.3 8.5%

www.perishablesgroup.com 53

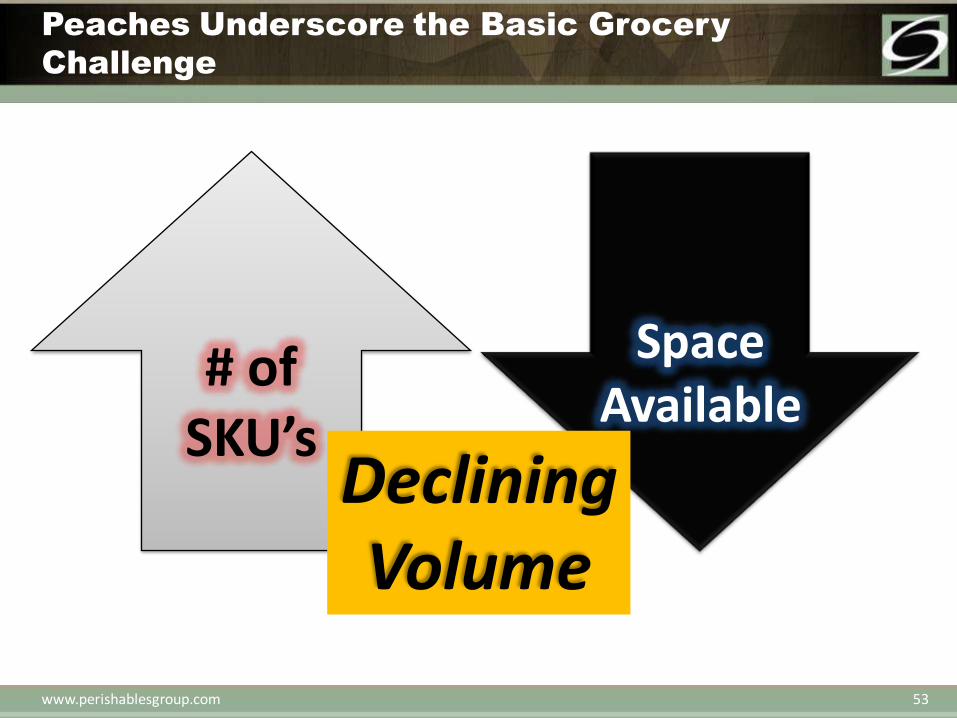

Peaches Underscore the Basic Grocery

Challenge

# of SKU’s

Space Available

Declining Volume

www.perishablesgroup.com 54

Consumer Purchase Dynamics

FreshFacts Powered by Spire, 2011

Product Household

Penetration

Trips per Buyer Multiple Item

Baskets

Peaches 36.1% 2.7 15.2%

Pears 28.8% 3.3 3.5%

Cherries 26.7% 2.1 1.0%

www.perishablesgroup.com 55

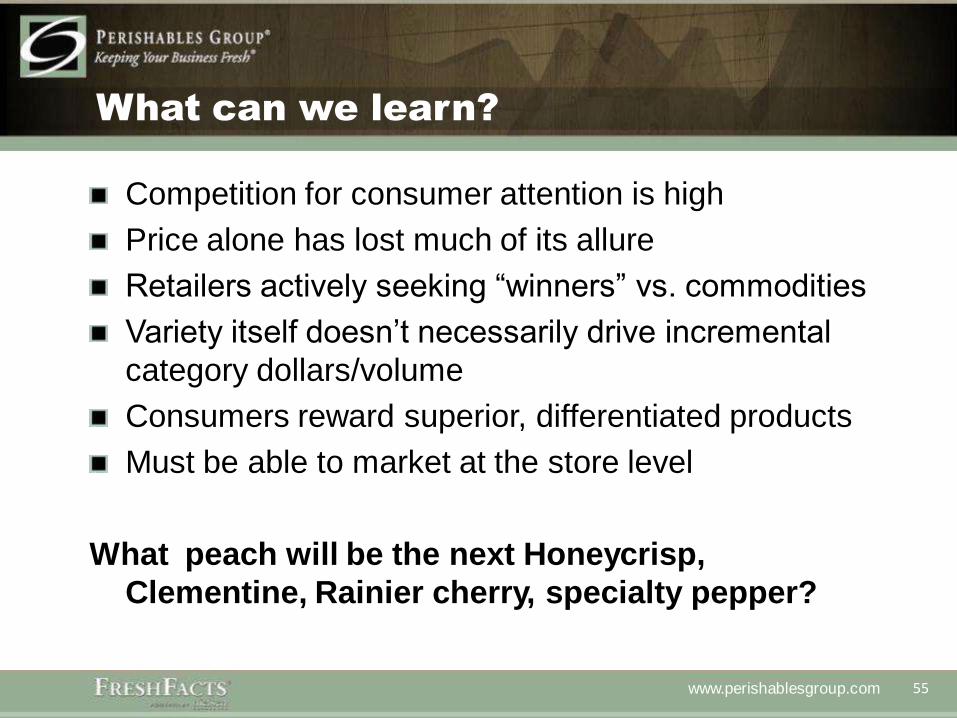

What can we learn?

Competition for consumer attention is high

Price alone has lost much of its allure

Retailers actively seeking “winners” vs. commodities

Variety itself doesn’t necessarily drive incremental

category dollars/volume

Consumers reward superior, differentiated products

Must be able to market at the store level

What peach will be the next Honeycrisp,

Clementine, Rainier cherry, specialty pepper?

www.perishablesgroup.com 56

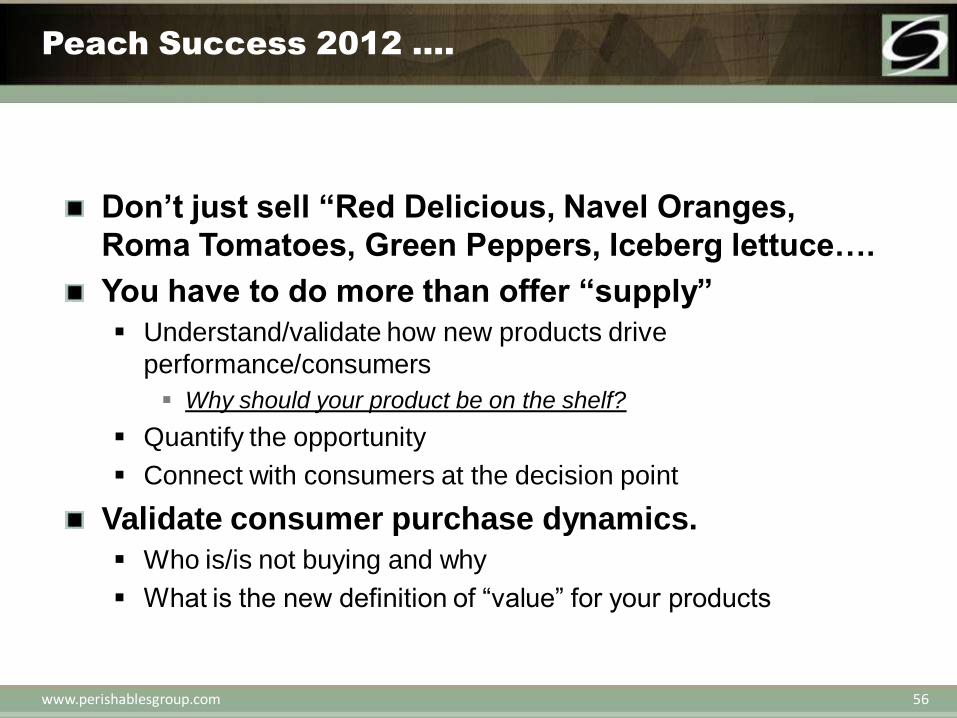

Peach Success 2012 ….

Don’t just sell “Red Delicious, Navel Oranges,

Roma Tomatoes, Green Peppers, Iceberg lettuce….

You have to do more than offer “supply”

Understand/validate how new products drive

performance/consumers

Why should your product be on the shelf?

Quantify the opportunity

Connect with consumers at the decision point

Validate consumer purchase dynamics.

Who is/is not buying and why

What is the new definition of “value” for your products

www.perishablesgroup.com 57

Thank you!

Contact Steve Lutz at Nielsen Perishables Group:

509.884.2616

www.perishablesgroup.com